GOLD: $1338.40 UP $8.40 (COMEX TO COMEX CLOSING)

Silver: $14.92 UP 9 CENTS (COMEX TO COMEX CLOSING)//at its 200 day moving average

Closing access prices:

Gold : 1336.00

silver: $14.92

SORRY FOR YESTERDAY BUT MY INTERNET WAS OUT FOR 24 HOURS. IT WAS RESTORED THIS AFTERNOON AND I HAVE UPDATED ALL OF THE COMEX//GLD/SLV DATA FOR YOU

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 3/28

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,328.300000000 USD

INTENT DATE: 06/05/2019 DELIVERY DATE: 06/07/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 16

657 C MORGAN STANLEY 2

661 C JP MORGAN 1 3

686 C INTL FCSTONE 22 4

737 C ADVANTAGE 4 3

800 C MAREX SPEC 1

____________________________________________________________________________________________

TOTAL: 28 28

MONTH TO DATE: 528

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 28 NOTICE(S) FOR 2800 OZ (0.0087 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 528 NOTICES FOR 52800 OZ (1.642 TONNES)

SILVER

FOR JUNE

46 NOTICE(S) FILED TODAY FOR 230,000 OZ/

total number of notices filed so far this month: 308 for 1540,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 7690 DOWN 74

Bitcoin: FINAL EVENING TRADE: $ 7645 DOWN 200

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 651 CONTRACTS FROM 216,145 UP TO 215,494 DESPITE THE TINY 4 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY LARGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 3602 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3602 CONTRACTS. WITH THE TRANSFER OF 3602 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3602 EFP CONTRACTS TRANSLATES INTO 18.01 MILLION OZ ACCOMPANYING:

1.THE 4 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

12,600 CONTRACTS (FOR 4 TRADING DAYS TOTAL 12,600 CONTRACTS) OR 63.000 MILLION OZ: (AVERAGE PER DAY: 3150 CONTRACTS OR 15.75 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 63.00 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.00% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 951.71 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 651 DESPITE THE 4 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY HUGE SIZED EFP ISSUANCE OF 3602 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED AN STRONG SIZED: 2951 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3602 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 651 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A TINY 4 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.83 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 46 NOTICE(S) FOR 230,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.330 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE PROBABLY HAD GOOD ACTIVITY OF THE SPREADING ACCUMULATION IN SILVER TODAY//

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A VERY STRONG SIZED 8181 CONTRACTS, TO 489,676 WITH THE GOOD $6.00 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// YESTERDAY/THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADING FELLOWS WILL MORPH INTO SILVER ONCE JUNE GETS UNDERWAY. THE GAIN IN OI GOLD CONTRACTS IS REAL AND NOT PUMPED UP BY SPREADING.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 16,748 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 16,748 CONTRACTS, JUNE 2020 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 489,676. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 24,992 CONTRACTS: 8181 OI CONTRACTS INCREASED AT THE COMEX AND 16,748 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 24,929 CONTRACTS OR 2,492,900 OZ OR 77.53 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $6.00 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 77.53 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 58,719 CONTRACTS OR 5,871,900 OR 182,64 TONNES (4 TRADING DAYS AND THUS AVERAGING: 14,679 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAYS IN TONNES: 182,64 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 182.64/3550 x 100% TONNES =5.14% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2460.55 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 8181 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($6.00)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 16,748 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 16,748 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,929 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

16,748 CONTRACTS MOVE TO LONDON AND 8181 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 77.53 TONNES). ..AND THIS GAIN OF DEMAND OCCURRED WITH THE RISE IN PRICE OF $6.00 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 28 notice(s) filed upon for 2800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.40 TODAY//

NO CHANGES IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 757.59 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 9 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 312.038 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 651 CONTRACTS from 216,145 UP TO 215,494 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE STOPPED THEIR LIQUIDATION IN SILVER AND GOLD FOR NOW BUT WILL NOW MORPH INTO SILVER AS THE COMEX SILVER MONTH OF JUNE COMMENCES IN EARNEST..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 3602 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3602 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 299 CONTRACTS TO THE 3602 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG GAIN OF 2951 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 14.76MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A SDETRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.560 MILLION OZ FOR JUNE.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 4 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A HUGE SIZED 3602 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China

This will hurt Huawei as a monstrous 30% of all orders to key suppliers have been cancelled due to the USA product ban

( zerohedge)

4/EUROPEAN AFFAIRS

i) ECB

This will be good for gold: The ECB announces rates unchanged and then announced new TLTRO terms. The TLTRO is the exact same thing as QE

( zerohedge)

ii)The Europeans were not happy: they wanted more bang for their buck as the Euro jumps but stocks fall

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

Mexico/USA

After failing to reach a deal with the uSA, we now witness Mexican troops block migrants at Mexico’s southern border.

( zerohedge)

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

ii)Brought this to you yesterday but it is worth repeating: China is now looking beyond USA treasuries as they are no doubt trying to void USA hegemony

iii)A repeat of yesterday’s major story. Italy wants to incorporation a new alternative currency, the min bot which will be a forerunner of the new Lira. If implemented the entire European banking system implodes as I explained yesterday

iv)Interesting: Russian central bank will only sell roubles for dollars and not yuan. Pay close attention to this: Russia’s chief central banker Elvira Nabiullina is one smart cookie. I guess she thinks that China will implode their currency before the uSA does.( SCMP/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

I)Trump signals more Chinese tariffs

(zerohedge)

II)MARKET TRADING/EARLY THIS MORNING

Trump signals more Chinese tariffs

ii)Market data

a)USA exports and imports plunge. Thus the trade deficit shrinks but GDP is faltering

( zerohedge)

b)Mish Shedlock comments on the discrepancy on the two job reports and how the Bureau double or triple counts individuals. If you have 3 part time jobs the Bureau records this as 3 jobs

iii)USA ECONOMIC/GENERAL STORIES

a)As outlined above: Trump is threatening China with an additional 300 billion dollars worth of tariffs on their goods.

( zerohedge)

b)heavy duty truck orders collapse and we are now at 3 yr lows and a huge 70% in the May reading

( zerohedge)

c)My goodness: just take a look at Los Angeles: the homeless population now jumps in LA County to almost 59,000

(courtesy zerohedge)

d)This is a very good commentary from Brandon Smith. We have been highlighting his commentaries for the past few years. Today he outlines why the trade wars will turn out to be an economic world war iiii

SWAMP STORIES

a)It looks like the past is catching up to Biden as this will for sure mire with campaign in 2020

( zerohedge)

b)Looks like Elijah Cummings and his wife have a lot of explaining to do as records reveal charity money was transferred to the “for profit” company

Let us head over to the comex:

Gold withdrawals;

i) We had 0 withdrawal:

.

Global Collapse In Trust Is Driving A Secret Bull Market In Gold

by Dominic Frisby of Money Week

Every year, Incrementum AG – a Liechtenstein-based investment company – puts out its research note, In Gold We Trust.

At over 300 pages, it’s probably the most comprehensive gold analysis there is.

The 2019 edition came out just last week, and I thought this week I’d share some of the charts with you – those that really jumped out at me.

How much more distrusting have we become? Check out these charts

The main authors of In Gold We Trust – Ronald-Peter Stoeferle and Mark J Valek – are (as you might expect) hardcore goldbugs. Theirs is a world view with which many MoneyWeek readers will have a lot of sympathy. I know do.

There is too much debt in the world, especially government debt. Easy money, low rates, monetary manipulation, the balance sheets of central banks and all the rest of it have stored up a host of problems, and when the dam breaks it will be nasty. Gold is thus an essential diversifier in everybody’s portfolio.

One word, however, appeared more frequently than I have ever known it to. It’s a word with which bitcoin bugs will be only to familiar – “trust”. Bitcoin, of course, was designed to obviate the need for it – “in proof we trust”, runs the saying.

Incrementum observes that in the West, trust is disappearing. People no longer trust their governments. They do not trust their politicians. They do not trust their scientists, or their economists. Experts are biased. The media is biased. Even systems and processes are no longer trusted – whether it’s education, healthcare, even democracy itself.

The blue squares in the chart below chart declining levels of political trust in various countries around the world. Interestingly, Finland has seen the biggest falls.

It’s easy to explain why such trust should have evaporated, from lies about the Iraq war, to the authorities’ reaction to the financial crisis of 2008. Society, as a result, has become polarised in a way that we simply weren’t used in the nineties and early noughties.

It’s interesting that the UK actually saw a marginal rise in trust between 2007 and 2016, albeit from much lower levels. This probably reflects the difference in perception between the Brown and Cameron administrations. When the 2018-2019 data gets released, I think you’ll see UK trust in governments at an all-time low.

As far as Incrementum (and any like-minded gold or bitcoin bug) is concerned, this loss of trust in our institutions and in each other is leading up to the humdinger – a loss of trust in money itself. Indeed, that’s why bitcoin was designed in the first place.

At a global level, this is manifesting itself in mutual distrust among central banks. Some have repatriated gold held overseas, while others have been increasing their gold holdings in what is known as the de-dollarisation of the economy. Hungary has increased its gold holdings tenfold, for example. That’s extreme – but most nations are at it.

It’s no coincidence that the change in trend began in 2008. That’s when they bailed out the banks. What struck me, in particular, was, cumulatively, how much gold Russia has bought.

While the growth in China’s holdings, as I have written about before, is extraordinary.

So loss of trust was one big theme of this year’s report. And these central bank reserve charts go some way to demonstrating the scale aof that loss of trust.

Gold’s secret bull market

I just want to cover a couple more charts which caught my eye.

We tend to think of gold in US dollar terms, because that is the official price in which gold is measured. As a result, our perception is that gold peaked in 2011 at $1,920 per ounce and has been in a bear market ever since. Today it sits around $1,330.

But over the same period the US dollar has largely been in a bull market. It has been strengthening against most currencies.

On the other hand, I’ve often described gold as a hedge against your own government. And in the UK, for example, it has served that purpose well. Gold was £700/oz in early 2016, before the Brexit vote. Today it’s 50% higher, at roughly £1,050.

In this next chart we see the world price of gold – ie gold plotted against all major national currencies. You wouldn’t know it, but by this measure, gold has been in a bull market since 2013.

Gold has, in other words, been doing what it is supposed to do.

There are many great charts in the report, and I recommend you take a look. But I wanted to finish off with one final chart that caught my eye.

Commodity prices are incredibly low, believe it or not

A common theme of mine in recent years has been the extraordinary valuation ascribed to the digital economy, while the real economy has lagged. Whether it’s the valuations ascribed to FANG stocks or bitcoin, or the earnings of tech entrepreneurs, the digital economy has eclipsed the physical economy. The reason is scalability, as I outlined last week.

Real stuff is a burden. The physical economy is hard. Nowhere is this dichotomy more apparent than in the commodities markets. We think of the great commodities bull market of the 2000s, and then the subsequent bear market we are in today.

But oil is still above $50 a barrel, copper costs nearly $6,000 a tonne, and wheat is around $200 a bushel. Prices don’t feel that low.

However, if we look at commodity prices relative to stock prices, they are actually more depressed than they were at the turn of the century, before that great secular bull market. In fact they’re almost as low as they were in the late 1960s.

Here we see the ratio of the Goldman Sachs Commodities Index against the Dow Jones.

I don’t think it starts tomorrow. Probably not even this decade. But the stage is being set for a turnaround in commodities – and as such the real economy. And if all the inflation that has built up over the last decade manifests itself in commodity prices, then you really will need to own some gold.

For now, amid the recent stockmarket correction, gold has had a nice little rally over this past couple of weeks to around $1,330. It’s looking strong. But the big barrier remains that $1,360 area that has been resistance for some five years now. Will 2019 be the year it gets through? Let’s hope so.

By Dominic Frisby via Money Week

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

05-Jun-19 1337.75 1335.05, 1052.01 1049.22 & 1185.38 1184.99

04-Jun-19 1323.60 1324.25, 1045.51 1043.77 & 1177.47 1177.26

03-Jun-19 1313.95 1317.10, 1039.47 1042.35 & 1175.99 1175.38

30-May-19 1276.45 1280.95, 1010.44 1015.92 & 1146.25 1151.70

29-May-19 1283.50 1281.65, 1016.02 1013.27 & 1151.04 1150.67

28-May-19 1283.90 1278.30, 1012.87 1008.20 & 1146.91 1142.29

27-May-19 Closed for UK Holiday

24-May-19 1281.50 1282.50, 1011.36 1011.89 & 1145.92 1145.40

23-May-19 1275.95 1283.65, 1009.79 1015.37 & 1146.19 1152.46

News and Commentary

Gold Settles at a 3 1/2-month High After ADP Report Reveals Very Weak Hiring

Gold Rises to 15-wk High as Trade-conflicts, Rate Cut Hopes Fuel Demand

Wall St. Climbs as Weak Private Jobs Data Boost Rate Cut Hopes

Fed Says Contacts Worry About Trade War; Economy Growing Modestly

Gold at 3-month High Amid Rate-cut Expectations

Gold Price Is Poised To Leap Upwards: Bloomberg’s McGlone (Radio)

The Global Collapse in Trust Has Driven a Secret Bull Market in Gold

Mish: Gold Gains As Faith In Central Banks Is About To Be Tested Again

The Fed Dusts Off “Whatever It Takes”

Italy Revives ‘alternative Currency’ Proposal

German Bundesbank Comes Clean on Euro Default Risks After Italy’s ‘Parallel Currency’ Decree

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

India’s gold imports jumped a huge 49%

(courtesy Reuters)

India’s gold imports in May jumped 49% on festive demand

Submitted by cpowell on Wed, 2019-06-05 01:03. Section: Daily Dispatches

By Aftab Ahmed and Rajendra Jadhav

Reuters

Tuesday, June 4, 2019

India’s gold imports in May jumped 49 percent from a year earlier to 116 tonnes as a correction in local prices during a key festival boosted retail demand, a government source said today.

China looks beyond U.S. Treasuries for dollar investments

Submitted by cpowell on Wed, 2019-06-05 01:09. Section: Daily Dispatches

By Abhinav Ramnarayan, Virginia Furness

Reuters

Tuesday, June 4, 2019

LONDON — China may be expanding its investments beyond U.S. Treasuries into debt issued by top-rated European and other government agencies, allowing it to keep its money in dollar assets while picking up some extra yield, bankers with knowledge of the matter say.

For the remainder of the report:

Prominent among these are the European Investment Bank, a development bank backed by European Union countries, KfW, a German government-guaranteed institution, and AIIB, a Beijing-based pan-Asian development bank that issued its first ever bond last month. …

… For the remainder of the report:

https://www.reuters.com/article/china-treasuries/china-looks-beyond-u-s-…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

Italy revives ‘alternative currency’ proposal

Submitted by cpowell on Wed, 2019-06-05 12:59. Section: Daily Dispatches

By Davide Ghiglione and Valentina Romei

Financial Times, London

Wednesday, June 5, 2019

Debate is growing in Italy about the suggestion that a new domestic currency could be introduced by the government to pay its debts — and the possibility that Rome’s Eurosceptic coalition might use it to facilitate the nation’s departure from the euro.

Prominent members of deputy prime minister Matteo Salvini’s ruling League party have floated the proposal — which was endorsed by a vote in the Italian parliament last week. But how would it work, and how likely is it to happen?

…

The Italian government should issue debt in small denominations that can change hands as a medium of exchange — that, at least, is the view of key advisers to Mr Salvini.Claudio Borghi, one of the League’s most influential economic advisers, has championed the idea, as has Alberto Bagnai, president of the finance committee in Rome’s Senate. Mr Borghi, who has been strongly critical of Italy’s membership of the single currency, is president of the budget committee in the lower house of Italy’s parliament.

The proposal involves creating a new type of Treasury bill — dubbed mini-bills of Treasury (mini-BOTs) — which could be used by the government to pay the arrears it owes to commercial businesses, and by citizens to pay their taxes, Mr Borghi has suggested.

Thus it would have the scope to grow into what would in effect be a parallel domestic currency, separate from Italy’s official currency, the euro. …

… For the remainder of the report:

https://www.ft.com/content/aca3c80a-86ac-11e9-97ea-05ac2431f453

end

Interesting: Russian central bank will only sell roubles for dollars and not yuan. Pay close attention to this: Russia’s chief central banker Elvira Nabiullina is one smart cookie. I guess she thinks that China will implode their currency before the uSA does.

(courtesy SCMP/GATA)

Despite Russia’s ties to China, Russian banks will sell rubles only for dollars, not yuan

Submitted by cpowell on Wed, 2019-06-05 15:40. Section: Daily Dispatches

China, Russia Urged to Continue Efforts to Defang U.S.-dollar Sanctions Weapon

By Laura Zhou

South China Morning Post, Hong Kong

Wednesday, June 5, 2019

China and Russia should avoid using U.S. dollars in financial translations to minimise Washington’s ability to bully other countries into following its rules with the threat of sanctions, according to a top adviser to Russian President Vladimir Putin.

The two nations have been keen to cut their dependence on the U.S. dollar for some time, and continue to talk about establishing a new system for direct yuan-rouble settlements despite multiple delays.

…

The U.S. is the most powerful economy in the world. If we want to avoid dollar hegemony, the first thing we need to do is to avoid using dollars, because the foundation of the U.S. economy is based on the dollar reserves owned by other countries and this has given it the ability and confidence to press other countries to play by its rules,” said economist Sergey Glaziev. …

The dependence of the Russian economy on the U.S. dollar was illustrated by three failed attempts this week during the St. Petersburg International Economic Forum to exchange Chinese yuan for Russian roubles. Three major Russian banks refused to process the transaction, saying they would sell roubles only for U.S. dollars. …

… For the remainder of the report:

https://www.scmp.com/economy/global-economy/article/3013246/china-russia…

LAWRIE WILLIAMS: UPDATE: GLD turnaround very positive for gold

Gold showed signs of weakness through most of April and May and no less than 35 tonnes of gold were liquidated out of GLD, the world’s largest gold ETF, between April 1st and the Memorial Day holiday on May 27th. But as so often seems to be the case, the U.S. holiday seemed to trigger a turning point and, since then, GLD has added around 20 tonnes of gold to its holdings (although there was a withdrawal yesterday when the gold price turned down a few dollars – we think temporarily). And the GLD increase has coincided with a very sharp uptick in the gold price which is currently approaching $1,340 spot as I write, after a brief stutter – a big increase from a low point of around $1,275 only a week ago.

This is no coincidence as both the GLD deposits and the rising gold price signify a major change in sentiment about the prospects for gold from some of the big money funds. Ray Dalio’s Bridgewater, reputed to be the world’s biggest hedge fund with around $150 billion under management, has been leading the clarion call for gold. Dalio is said to be a gold believer and is reported as recently having his fund increase its gold exposure in the light of what he sees as an escalating trade war between the U.S. and China which he regards as potentially moving out of control. In a recent blog post he noted “History shows that countries in conflict have seen that such conflicts can easily slip beyond their control and become terrible wars that all parties, including the leaders who got their countries into them, deeply regretted, so the parties in the negotiations should be careful that that doesn’t happen. Right now we are seeing brinksmanship negotiations, so it is a risky time.”

While that may be a contentious assessment of the current trade negotiations, many feel that Dalio has a strong point here and President Trump’s ‘shoot from the hip’ approach to weaponise U.S.-assumed financial clout certainly has huge dangers – not least for segments of the U.S.’s own economy. National leaders, who have ‘face’ to protect – particularly China – may not cave in to bullying tactics of this type as easily as Trump’s business rivals may have done in the past. Equity markets in the U.S. and globally are looking nervous and there are fears around of a full-on global recession.

Where Dalio is seen to go, others follow, so it is not too surprising that GLD seems to be seeing gold inflows. The big question is how far can this apparent change in sentiment boost the gold price before it is seen as having risen too far too fast with a correction coming back in?

But meanwhile there are other elements boosting the gold price – not least a falling U.S. dollar index which usually coincides with a rising gold price. Geopolitical tensions seem to be ever-present, there are ongoing tariff, counter-tariff and economic sanction impositions, the U.S. Fed is now seen as more likely to cut interest rates rather than raise them, equity market nervousness, central bank gold buying, etc. All these would seem to be in favour of an increasing role for gold globally. Thus the target for a $1,400 plus gold price in the second half of the year would seem to be comfortably in play again. Indeed even higher price levels may come about should some of the current global tensions remain unresolved or escalate further.

06 Jun 2019

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9101/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9288 /shanghai bourse CLOSED DOWN 33.62 POINTS OR 1.17%

HANG SANG CLOSED UP 69,80 POINTS OR 0.26%

2. Nikkei closed UP 2.06 POINTS OR 0.01%

3. Europe stocks OPENED RED/

USA dollar index FALLS TO 97.13/Euro RISES TO 1.1256

3b Japan 10 year bond yield: FALLS TO. –.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.31/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.64 and Brent: 60.91

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.22%/Italian 10 yr bond yield DOWN to 2.52% /SPAIN 10 YR BOND YIELD DOWN TO 0.62%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.75: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.92

3k Gold at $1337.10silver at: 14.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 22/100 in roubles/dollar) 65.11

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.25 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9917 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1166 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.10% early this morning. Thirty year rate at 2.59%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7691..

Rally Fizzles As Trade Tensions Mount But Central Banks Say “Buy, Buy, Buy”

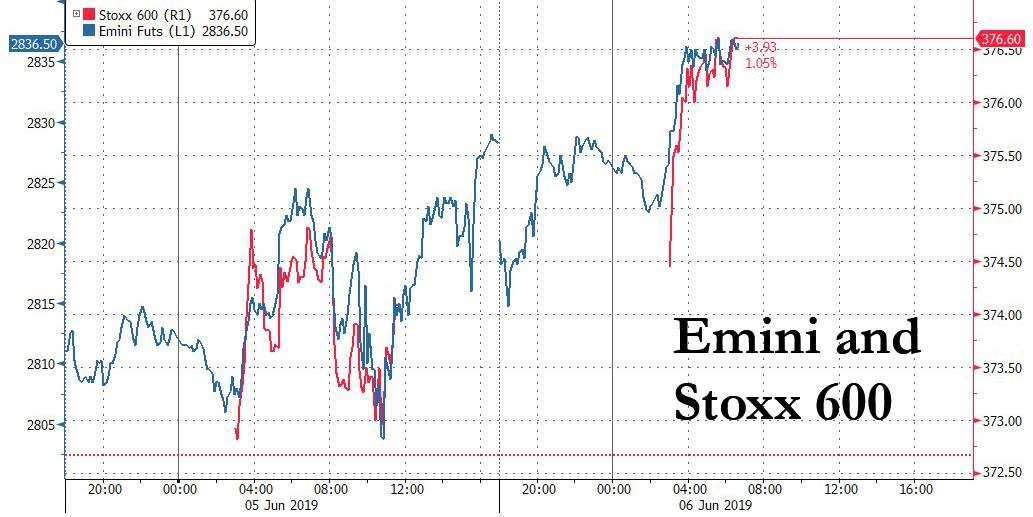

US equity futures and European market advanced on Thursday, ignoring the latest slump in Chinese stocks, as the hope of easier monetary policy continued to help fuel a rebound in stocks. The euphoria of recent days was gone, however, as German bond yields plumbed new record lows on Thursday and U.S. treasury yields resumed their fall as renewed trade tensions re-emerged overnight.

Sentiment soured on a lack of progress in talks between U.S. and Mexican officials and after President Trump issued a fresh threat to hit China with tariffs on “at least” another $300 billion worth of Chinese goods. The latest escalation followed a mixed bag of economic data that sparked fresh recession fears, but was also offset by expectations that central banks will ride to the rescue.

As a result, the MSCI index of Asia-Pacific shares ex-Japan and the Nikkei eased a touch, the pan-European STOXX 600 rose 0.6%, with Germany’s DAX up 0.5% while France’s CAC gained 0.7%. US equity futures were up 8 points, tracking European gains.

Early in the session, Chinese stocks fell despite the PBOC’s 500 billion yuan cash injection via a 500 billion MLF, to offset a maturing 463 billion yuan loans. This however was seen as insufficient by the market, and the Shanghai Composite dropped 0.5% and Shenzhen Comp loses 1.2%.

European stocks shrugged off losses in Chinese equities to rise for a fourth straight day, pushing the Stoxx 50 up 0.7%, however gains in Europe were driven by defensive sectors such as utilities, real estate and consumer staples rather than riskier sectors. Much focus was also on the auto sector after Italy’s Fiat Chrysler Automobiles MV abandoned its $35 billion offer for Renault SA, the latter seeing its shares tumble as much as 8%, and depressing automakers which were among the laggards.

“We are still caught in this whirlwind of conflicting economic and corporate stories… we are getting mixed political signals, and quite mixed economic news,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments. “We have not seen people move away from safe haven assets.”

Meanwhile in rates, a buy on dips mentality continues to dictate price action in bond markets, with most European sovereign yields steady to 4bps lower across the curves. The 10-yr BTP/bund spread was 1bp wider at 271bps, as the yield on Germany’s 10-year government bond fell to new all-time lows ahead of the EBC’s June meeting.

At the same time, the two-year Treasury yields struck their lowest since December 2017, while futures have priced in around 70bps of easing by December. the 10Y Treasury remains firm with 10-year yield off 3bps at 2.10%; Aussie curve steepens for fourth day on 3-year strength. JGB futures retrace about half of Wednesday’s rally. Dalian iron falls 2.4%; WTI crude near $51.80

European yields are likely to slide even more after the ECB tries to boost the eurozone economy and may even set the stage for more action later this year as an escalating global trade war saps growth and unravels the benefits of years of ECB stimulus. In a long-flagged move, the ECB is likely to unveil the TLTRO, offering to pay banks if they borrow cash from the central bank and pass it on to households and firms.

In currency markets, the safe-haven yen was rose, nudging the dollar down 0.2% to 108.21. The dollar lingered against a basket of currencies to trade at 97.234, having bounced from a seven-week low overnight. The euro traded at $1.1240 after briefly stretching as high as $1.1306 on Wednesday. “We expect the ECB to turn more dovish and push the euro lower,” said CBA FX analyst Joseph Capurso. “We expect the ECB to change their forward guidance on interest rates and to trim their macroeconomic projections and modify their forward interest rate guidance because of low inflation and heightened uncertainty about global trade.”

Meanwhile Mexico’s peso plunged as much as 1.3% under a double whammy from trade woes and ratings agency Fitch downgrading the country’s credit rating to BBB, while Moody’s changed its outlook to negative from stable. All of this saw the dollar jump 0.7% against a beleaguered Mexican peso.

In commodity markets, the non-stop chatter of rate cuts helped lift gold to 15-week highs and the precious metal was last trading at $1,332.71 per ounce. Oil prices flatlined after diving overnight when the Energy Information Administration (EIA) reported the largest build in crude oil and oil product inventories since 1990. WTI was at $51.94 a barrel after having hit its lowest since January, while Brent crude futures stood at $60.91.

Expected data include trade balance and jobless claims. J.M. Smucker, Saputo, and Beyond Meat are among companies reporting earnings

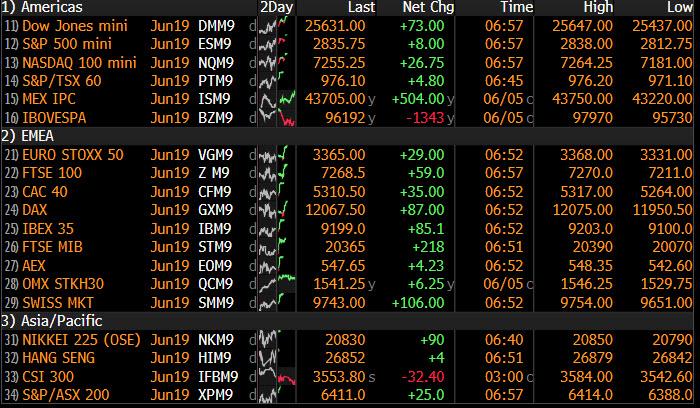

Market Snapshot

- S&P 500 futures up 0.3% to 2,836.00

- STOXX Europe 600 up 0.6% to 376.21

- MXAP down 0.2% to 153.58

- MXAPJ down 0.1% to 501.50

- Nikkei down 0.01% to 20,774.04

- Topix down 0.3% to 1,524.91

- Hang Seng Index up 0.3% to 26,965.28

- Shanghai Composite down 1.2% to 2,827.80

- Sensex down 1.1% to 39,628.42

- Australia S&P/ASX 200 up 0.4% to 6,383.00

- Kospi up 0.1% to 2,069.11

- German 10Y yield rose 0.3 bps to -0.223%

- Euro up 0.2% to $1.1239

- Italian 10Y yield fell 4.5 bps to 2.1%

- Spanish 10Y yield fell 1.9 bps to 0.61%

- Brent futures up 0.6% to $60.99/bbl

- Gold spot up 0.5% to $1,336.71

- U.S. Dollar Index down 0.1% to 97.23

Top Overnight News from Bloomberg

- President Trump said “not nearly enough” progress was made in talks with Mexico to mitigate the flow of undocumented migrants and illegal drugs, raising the likelihood the U.S. will follow through with tariffs

- U.S. and Mexican negotiators are set to resume talks Thursday with time running short to avert Trump’s threat to impose tariffs next week. The U.S. president, who’s traveling overseas, said that “not nearly enough” progress was made during a 90- minute meeting between Mexico’s foreign minister and top American officials

- Trump also reiterated that the U.S. is prepared to place tariffs on another $300 billion of Chinese imports and asserted Beijing “wants to make a deal badly”

- China unveiled a stimulus plan to help spur demand for automobiles and electronics as the escalating tensions with the U.S. threaten to hurt the economy. Measures announced by the National Development and Reform Commission on Thursday include banning local governments from placing any new curbs on car purchases or limits on usage of new energy vehicles

- The contest to succeed Theresa May as U.K. prime minister quickly shifted into high gear as rival candidates battled over the rights and wrongs of forcing through a no-deal Brexit. Ex-Brexit Secretary Dominic Raab riled moderates suggesting he could suspend Parliament to deliver Brexit

- The three top players in Italy’s bickering populist coalition have come together to defy European Union budget rules as the bloc’s executive arm started disciplinary proceedings against Rome

- India’s central bank cut its benchmark interest rate for a third time this year and paved the way for more policy easing to support an economy growing at the slowest pace since 2014

- U.S. Treasury Secretary Steven Mnuchin aims to talk about including a currency clause in a bilateral trade deal when he meets Japanese Finance Minister Taro Aso on the sidelines of the G-20 conference in Japan this weekend, Asahi reports

- U.S. economy broadly expanded in recent weeks and the business outlook remained “solidly positive,” according to a Fed’s Beige book

- Tory leadership hopeful Michael Gove says he’s open to a further Brexit extension — but Dominic Raab rules one out

- Denmark’s nationalists had their worst drubbing ever in Wednesday’s election with Mette Frederiksen set to become next prime minister

- The three top players in Italy’s bickering populist coalition came together Wednesday to defy European Union budget rules as the bloc’s executive arm started disciplinary proceedings against Rome

Asian equity markets traded somewhat mixed with the region cautious after hopes of an agreement to avert Trump tariffs on Mexico have so far failed to materialize, although officials will continue discussions on Thursday. Nonetheless, ASX 200 (+0.4%) and Nikkei 225 (U/C) remained afloat as Australia continued to ride the wave of the lower rate environment and amid broad gains across the sectors aside from mining names, while the Japanese benchmark was also higher but with gains capped amid an indecisive currency, as well as weakness in automakers including Nissan and Mitsubishi Motors after Fiat abruptly withdrew its merger proposal for Renault. Hang Seng (+0.3%) and Shanghai Comp. (-1.2%) were mixed ahead of their extended weekend with initial weakness seen as Chinese press continued to point the blame on the US for the breakdown of negotiations and with Chinese agencies said to be collecting opinions on further countermeasures against the US. However, some of the losses were later pared after the PBoC announced CNY 500bln in 1-year MLFs and reiterated to keep liquidity in the banking system ample. Finally, 10yr JGBs pulled back to below the 153.50 level amid mild gains in Japanese stocks and as yields recovered from multi-year lows, while the enhanced liquidity auction for longer-dated JGBs also showed slightly weaker demand.

Top Asian News

- China Unveils Stimulus to Help Sales of Cars, Electronics

- Taiwan Central Bank Surprises With Comments on Currency Market

- India Cuts Rate to 9-Year Low and Signals More Easing Ahead

- Black Market in $2b of Meat Severed by Pig Fever Battle

European equities are higher across the board [Eurostoxx 50 +0.8%] as sentiment somewhat diverges from the mixed handover in Asia ahead of the ECB monetary policy decision. Sectors are mostly higher, although European Telecom names underperform with the likes of Vodafone (-3.0%) weighing on the sector as they are ex-dividend. Notable movers include Renault (-7.3%) after Fiat Chrysler (Unch) withdrew its merger offer after the French state, Renault’s largest shareholder, requested discussions be put off to a later date; albeit the French Budget Minister did note that future merger talks between the company may happen. The news of the break-up in talks saw most European autos open lower, although Renault competitor Peugeot (+2.0%) spiked to the top of the CAC. Elsewhere, the FTSE reshuffle is due to take place on June 24th, with confirmation that easyJet (+0.5%) and Hikma Pharmaceuticals (Unch) will be demoted, whilst JD sports (-0.4%) and Aveva (+1.1%) will be added to the blue-chip index. Furthermore, in Italy, the FTSE MIB will see Nexi (+1.1%) replace Banca Generali (+0.1%).

Top European News

- German Factory Orders Unexpectedly Gain in Sign of Resilience

- Russian Rate Cut Is Possible Next Week, Nabiullina Says

- Rolls-Royce Transfers $5.8b of Pension Assets to L&G

- Hillhouse Said to Near Deal to Acquire Scotch Brand Loch Lomond

In FX, the Dollar is off recovery highs, but the index is consolidating above the 97.000 axis after rebounding from sub-96.500 at one stage on Wednesday when Fed rate cut fever rose on the back of dovish leaning speeches from Brainard and Evans (latter changing tune somewhat from the previous day), hot on the heels of a dismal ADP survey (albeit partly corrective perhaps). Subsequent comments from Kaplan advocating the current wait-and-see policy and a solid looking services ISM helped the Greenback regain composure and the latest Beige Book also maintained a relatively upbeat tone. Hence, the DXY is holding within a 97.344-198 range ahead of more potentially pivotal US data and Fed commentary.

- JPY/NZD/AUD/EUR – Usd/Jpy looks pretty tethered to the 108.00 level after another rally on improved risk sentiment and a resultant rebound in US Treasury yields fizzled out ahead of 108.50. However, the headline pair may now be hostage to option-related flows given a mass of mega expiries ranging from 108.00 to 109.00 and totalling 10.5 bn. Meanwhile, the Antipodean Dollars are both firmer vs their US counterpart, albeit not breaking fresh ground after recent RBA and RBNZ policy actions and guidance, with Aud/Usd and Nzd/Usd meandering between 0.6983-64 and 0.6633-18 respective parameters. Note, little net reaction to Aussie trade data overnight as a sub-forecast surplus was partly compensated by an encouraging rebound in exports. Elsewhere, the single currency is also fairly contained vs the Buck and generally eyeing the upcoming ECB policy meeting and press conference to see how dovish or not President Draghi is and anticipating details of TLTRO3 – see our Research Suite for a full preview. Eur/Usd is currently hovering around 1.1230 and also close to decent option expiry interest lying at 1.1220-30 in 2 bn and 1.1200-10 in 1.5 bn.

- NOK/SEK – The Scandi Crowns have both bounced off worst levels to retest technical and psychological resistance vs the Euro around 9.7850 and 10.6000 respectively, with the former propped by an uptick in Norway’s 2019 mainland GDP forecast from the Stats office which also sees the Norges Bank hiking this month in line with official guidance.

- CAD/GBP/CHF – All relatively flat vs the Usd, but the Loonie could derive some independent impetus from Canadian trade later and deviate from 1.3400-30 bounds, while Cable hovers just below 1.2700 and the Franc near 0.9950.

In commodities, WTI (+0.1%) and Brent (+0.5%) futures are higher on the day, but with gains capped as the benchmarks hold onto most of yesterday’s supply-sparked losses following the barrage of bearish numbers including record high US production and a mammoth surprise build in stockpiles. WTI tested resistance around the USD 52.00/bbl broke the level in a short-lived move, whilst its Brent counterpart briefly breached the USD 61.00/bbl to the upside. In terms of implications ahead of the OPEC gathering, concerns about the rise in US inventories were flagged by oil producers at the JMMC meeting, and this was reinforced by OPEC and allies yesterday in which OPEC Secretary General Barkindo noted that they will take the current “economic bearishness” into account when they meet in the coming weeks. In terms of the meeting date, Russian Energy Minister Novak noted that he is discussing postponing the OPEC+ gathering to July 2nd/4th, ahead of a meeting with his Saudi counterpart on June 10th. Elsewhere, gold (+0.5%) extends on recent gains and remains near three-month highs as trade tensions show no signs of abating as US-Mexico talks failed to conclude with an agreement; albeit dialogue is expected to resume today. Meanwhile, copper declined to a two-year low amid the bleak demand outlook whilst Dalian iron ore futures were pressured by anticipation of increased supply.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 10.9%

- 8:30am: Trade Balance, est. $50.7b deficit, prior $50.0b deficit

- 8:30am: Nonfarm Productivity, est. 3.5%, prior 3.6%; Unit Labor Costs, est. -0.9%, prior -0.9%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 215,000; Continuing Claims, est. 1.66m, prior 1.66m

- 9:45am: Bloomberg Consumer Comfort, prior 60.8

- 12pm: Household Change in Net Worth, prior $3.73t deficit

DB’s Jim Reid concludes the overnight wrap

Morning from Berlin where I held a CEO dinner at our big DB Access German conference last night. Basically the theme of my dinner speech was that Germany had done wonderfully well from globalisation and was now in need of a revised business model to deal with what is a potentially vastly different world order going forward due to de-globalisation, the competitive threat of China, the tech revolution and Europe’s problems. Interestingly there wasn’t a huge push back from major business leaders in Germany. I flew to Berlin after opening our 23rd annual Leverage Finance conference back in London. I started my speech by asking the audience five question to gauge the mood and I thought I’d share the results for interest from a room that had several hundred investors.

- Where will European Crossover trade by YE 2019? (290 at the time). A) Sub 250 – 5%. B) 250-275 – 11%. C) 275-300 – 23%. D) 300-325 – 30%. E) 325-350 21%. F) Over 350 – 9%.

- For predicting the next US recession would you trust a US Economist or the Yield Curve more? A) Definitely a US Economist – 3%. B) More a US Economist but I would worry if the YC started to signal a recession and Economists didn’t – 12%. C) The Yield curve is usually a good indicator but I acknowledge that this time might be different as most US economists think – 50%. D) Definitely the Yield Curve – 34%.

- When will the next US recession occur? A) 2019 – 4%. B) 2020 – 27%. C) 2021 – 43%. D) 2022 – 20%. E) To infinity and beyond – 6%.

- Will President Trump get re-elected in 2020? A) YES – 74%. B) NO – 26%.

- Will a 10yr Italian BTP pay back par AND in Euros? A) YES – 67% B) NO – 33%.

The answers I found most interesting were those for the yield curve and Italy. Indeed the yield curve remains a favourite of investors as a predictive tool for the business cycle. Probably much more than economists trust in it. As for Italy, I did the same poll last year and the number expecting Italy to pay back its debt in full dropped from 79% to 67%. So it’s quite remarkable that in a two trillion Euro plus market, one thirds of investors expect there to be a haircut of some kind within a decade.

Anyway more on Italy later but plenty to get through this morning following a fairly action packed last 24 hours. Before we recap and comment on events there’s the not-so-small case of an ECB meeting to look ahead to today. Our economists expect today’s meeting to be more about signals than actions and beyond a 20bp discount on TLTRO3, think the focus will be on forward guidance, not tiering. We’ll also get new staff forecasts which should show some downgrades. Our colleagues ultimately expect the ECB to focus on preserving the easy policy stance by ensuring the market believes it has credible options to ease the stance further if necessary and protect the transmission mechanism from impairment. See their full summary here .

Back to markets where, one day after the biggest gain for US equities in months and a big sell-off in rates, we’re back to a slightly more measured tone for risk and another big repricing lower at the front end of the Treasury curve after a volatile day in rates. Indeed the MOVE index increased +3.16% again and stretched new 29-month highs. Two-year yields rallied -4.1 bps (down a further -3.4bps this morning) but they retraced off their early morning lows of -11.5bps. The initial catalyst for the sharp move was the worst ADP employment change reading (27k vs. 185k expected) since 2010 or more specifically since the recovery took hold which had the market once again debating rate cuts. However, a better than expected ISM non-manufacturing (56.9 vs. 55.4 expected) and one that included a much stronger 58.1 employment component reading slammed the breaks on the rally and helped yields rise again.

That being said, the July FOMC meeting is now priced in for 21bps of cuts, with 88bps of cuts priced in for the next 12 months. The market is still priced for a very dovish shift in policy. Friday’s jobs report is looking ever-more pivotal for the Fed and for markets. Despite the firming market expectations for rate cuts, the 2s10s curve actually bull steepened to 27.7bps (over 30bps intra-day and 28.8bps this morning) and to the steepest since November last year with 10y yields down a more modest -0.9bps (down a further -2.5bps this morning though). In three days the curve has actually steepened more than +8bps and it continues to defy inversion unlike most of the other common yield curve measures in the US. As we’ve mentioned numerous times this remains our favoured yield curve measure for predicting recession. Meanwhile the end result of all that for equities was a +0.82% and +0.64% move for the S&P 500 and NASDAQ respectively, while the USD was a touch stronger at +0.28% and US HY spreads narrowed -2bps. A decent move lower for WTI oil (-3.25%) post the latest inventories data, which showed another big build in US crude stockpiles, helped ensure that energy was the only industry sector in the red.

Of course we also had our daily dose of trade headlines yesterday. White House trade advisor Navarro said on CNN that Mexico still has time to stop US tariffs going into effect so long as the country addresses steps necessary to take asylum seekers and also heighten security at the border. Interestingly, he declared that the newly announced measures will be “good for the markets.” The tariffs are planned to take effect in four days, barring a change in policy from the White House. Meanwhile, President Trump has said overnight that “not nearly enough” progress was made in talks with Mexico which are set to continue today. He further added that “If no agreement is reached, Tariffs at the 5% level will begin on Monday, with monthly increases as per schedule,” while saying, “The higher the Tariffs go, the higher the number of companies that will move back to the USA!” The Mexican Peso flipped between gains and losses yesterday, ultimately ending -0.16% weaker and is down a further -0.92% this morning.

This morning in Asia markets are trading mixed as sentiment has been dampened by the US and Mexico failing to reach a deal yesterday. Chinese equity markets – the CSI (-0.20%), Shanghai Comp (-0.46%) and Shenzhen Comp (-1.16%) are all down while the Hang Seng (+0.22%) and Nikkei (+0.19%) are up. Futures on the S&P 500 are trading fattish (-0.04%). Markets in South Korea are closed for a holiday. In other overnight news, the PBOC added CNY 500bn to the financial system, its second-largest cash injection on record, likely in a move to ease liquidity concerns after a surprise takeover of a local lender last month.

Back to yesterday and mixed US data wasn’t the only big story in markets. In Europe, we got confirmation from the EU that they are taking the first steps of disciplinary action over Italy’s swelling debt issues. The risks around this issue were certainly rising, however our economists had thought that escalation was going to be more gradual, with an EDP more likely in Q4 after the draft 2020 budget. They have an updated note here . It certainly makes today’s ECB meeting more interesting, especially with regards to the TLTRO eligible collateral base and whether or not to increase it, as our colleagues noted yesterday. In any case the next thing to watch is to see if the EFC decide whether or not to back the EU’s decision, with a two-week or so timeframe to do so.

Thereafter the Commission has to prepare a report for ECOFIN, possibly for their 9 July planned meeting, so this is likely to rumble on for a while yet with the ultimate focus still being the draft 2020 budget in September. Italian assets underperformed yesterday with the FTSE MIB falling -0.36% (versus a +0.29% gain for the STOXX 600) and Italian Banks down -1.70%. Nevertheless, BTPs actually ended up rallying -4.6bps, reversing an intraday rise of +11.4bps, possibly boosted by Commissioner Moscovici’s conciliatory comment in an interview that “we are not talking about fines” and “we want to lead to a common future.” Bund yields fell -2.0bps to another fresh record low but taking the BTP-bund spread to 270bps, right near the middle of its recent range.

It wasn’t just Italy facing the wrath of the EU with Spain also getting a warning from the Commission that it faces a “significant risk of deviation from its 2019 and 2020 fiscal goal”. The details didn’t offer much new however with the Commission having also previously flagged concerns at the time of the failed budget negotiations in Spain at the end of 2018. It’s worth noting that Spain is also coming out of an EDP which therefore offers a bit more flexibility over the next few years with a headline deficit for example of likely closer to 2% of GDP in 2019 (versus 2.5% in 2018). One to watch however. It’s worth noting that the IBEX closed +0.36% yesterday however Spanish yields were still -3.4bps lower.

We also had some commentary from Fed officials again yesterday, with Governor Brainard and regional presidents Kaplan and Evans all speaking (all are voting members of the FOMC this year), plus the beige book of economic conditions. Brainard, viewed as near the center of the committee’s thinking, toed the same line as Clarida and Powell yesterday, saying that trade is a downside risk and that the Fed is prepared to adjust policy to sustain growth if needed. She also emphasised that she will be watching payrolls data closely, though she won’t read too much into any single months’ print. Separately, Dallas President Kaplan said that he would rather “be patient here” since it “its early to make a judgment” on whether a cut will be warranted. Chicago President Evans leaned more dovish, as he usually does, saying that low inflation “by itself could be a reason for a little more accommodation,” even before thinking about trade risks. Finally the beige book suggested that the economy continues to grow modestly but positively, though there were some signs of slowing activity and elevated uncertainty.

As for the remaining data yesterday, in the US the services PMI in May was unrevised at 50.9, leaving the composite also at 50.9. In Europe the services PMI for the Euro Area was confirmed at 52.9 and up 0.4pts versus the flash. That was partly as a result of a 0.4pt upward revision for Germany while Italy (50.0 vs. 49.8 expected) surprised on the upside. Italy’s composite (49.9 vs. 49.3 expected) remained in contraction for the sixth time in the last eight months however.

Before we recap the day ahead, Nick from my team published a new slide pack yesterday which provides a comprehensive overview of the supply and demand dynamics within the EUR non-financial HY market. We explore trends in issuance, redemptions, coupons and fund flows as well as taking a look at rating transitions between HY and IG. Click on the link here to read more.

To the day ahead now, where datawise this morning we have April factory orders and the final Q1 GDP revisions for the Euro Area. That data comes just before the aforementioned ECB meeting before we get Q1 nonfarm productivity and unit labour cost revisions, claims and the April trade balance data all in the US. We’re also due to hear from the BoJ’s Kuroda this morning, the BoE’s Carney and then the Fed’s Kaplan and Williams this afternoon. President Trump is also expected to meet with French President Macron while Chinese President Xi Jinping delivers the keynote address at an international economic forum in Russia.

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED DOWN 33.62 POINTS OR 1.11% //Hang Sang CLOSED UP 69.80 POINTS OR 0.26% /The Nikkei closed UP 2.06 POINTS OR 0.01%//Australia’s all ordinaires CLOSED UP .35%

/Chinese yuan (ONSHORE) closed DOWN at 6.9101 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED UP // LAST AT 6.9101 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9288 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China

This will hurt Huawei as a monstrous 30% of all orders to key suppliers have been cancelled due to the USA product ban

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

i) ECB

This will be good for gold: The ECB announces rates unchanged and then announced new TLTRO terms. The TLTRO is the exact same thing as QE

(courtesy zerohedge)

ECB Extends Forward Guidance, Will Keep Rates Unchanged Until First Half Of 2020, Announces TLTRO Terms

With the ECB scrambling to offset the accelerating European contraction, moments ago Mario Draghi announced that the three main rates would remain unchanged (as expected) at least through the first half of 2020, extending the “patient” forward guidance period, from “the end of 2019” previously.

The Governing Council now expects the key ECB interest rates to remain at their present levels at least through the first half of 2020, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

And while the ECB also noted that it would continue reinvesting principal bond maturities, “for as long as necessary to maintain favorable liquidity conditions and an ample degree of monetary accommodation” as expected, the notable other change in today’s statement was the ECB’s disclosure of the terms of the TLTRO, which “will be set at a level that is 10 basis points above the average rate applied in the Eurosystem’s main refinancing operations over the life of the respective TLTRO.” For those banks whose eligible net lending exceeds a benchmark, “the rate applied in TLTRO III will be lower and can be as low as the average interest rate on the deposit facility prevailing over the life of the operation plus 10 basis points.”

While in line with expectations, the TLTRO rate was seen as slightly less favorable than expected by the market.

Full announcement:

At today’s meeting, which was held in Vilnius, the Governing Council of the European Central Bank (ECB) took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council now expects the key ECB interest rates to remain at their present levels at least through the first half of 2020, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

(2) The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.