GOLD: $1325.50 DOWN $16.40 (COMEX TO COMEX CLOSING)

Silver: $14.66 DOWN 38 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1328.00

silver: $14.71

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/2

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,341.200000000 USD

INTENT DATE: 06/07/2019 DELIVERY DATE: 06/11/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

323 H HSBC 2

686 C INTL FCSTONE 1

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 2 2

MONTH TO DATE: 539

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 2 NOTICE(S) FOR 200 OZ (0.0064 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 539 NOTICES FOR 53900 OZ (1.6765 TONNES)

SILVER

FOR JUNE

1 NOTICE(S) FILED TODAY FOR 5,000 OZ/

total number of notices filed so far this month: 309 for 1545,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 7639 UP 52

Bitcoin: FINAL EVENING TRADE: $ 7907 UP 289

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A STRONG SIZED 2772 CONTRACTS FROM 219.051 UP TO 221,823 WITH THE GOOD 12 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR SILVER AND IT STOPPED FOR GOLD AS WELL. WE WILL WITNESS A RISE IN THE SPREADERS IN SILVER ONCE WE START TRADING IN JUNE… READY FOR THE FIRST DAY NOTICE JULY CONTRACT.) TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A VERY HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 FOR MAY, 0 FOR JUNE, 4032 FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 4302 CONTRACTS. WITH THE TRANSFER OF 4302 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4302 EFP CONTRACTS TRANSLATES INTO 20.16 MILLION OZ ACCOMPANYING:

1.THE 12 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

19,351 CONTRACTS (FOR 6 TRADING DAYS TOTAL 19,351 CONTRACTS) OR 96.755 MILLION OZ: (AVERAGE PER DAY: 3225 CONTRACTS OR 16.13 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 96.755 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.09% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 985.47 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2948 WITH THE GOOD 12 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A VERY LARGE SIZED EFP ISSUANCE OF 2719 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A VERY STRONG SIZED: 6804 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 4032 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2772 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 12 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.03 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 1 NOTICE(S) FOR 5,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.560 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE PROBABLY HAD STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY//

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A STRONG SIZED 8,375 CONTRACTS, TO 501,322 WITH THE GOOD $3.50 PRICE GAIN WITH RESPECT TO COMEX GOLD PRICING FRIDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADING FELLOWS HAVE ALREADY MORPHED INTO SILVER. THE GAIN IN OI GOLD CONTRACTS IS REAL AND NOT PUMPED UP BY SPREADING.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 13,862 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 13,862 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 501,322. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,237 CONTRACTS: 8375 CONTRACTS INCREASED AT THE COMEX AND 13,862 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 22,237 CONTRACTS OR 2,223,700 OZ OR 69.17 TONNES. YESTERDAY WE HAD A SMALLISH GAIN OF $3.50 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 69.17 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 80,146 CONTRACTS OR 8,014,600 OR 249.28 TONNES (6 TRADING DAYS AND THUS AVERAGING: 13,357 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 249.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 249.28/3550 x 100% TONNES =7.02% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,527.19 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 8375 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($3.50)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 13,862 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 13,862 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 22,237 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

13,862 CONTRACTS MOVE TO LONDON AND 8375 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 69.17 TONNES). ..AND THIS GAIN OF DEMAND OCCURRED WITH THE RISE IN PRICE OF ONLY $3.50 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 2 notice(s) filed upon for 200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $16.40 TODAY//

A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD.

INVENTORY RESTS AT 756.42 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 38 CENTS TODAY:

NO CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV

/INVENTORY RESTS AT 315.362 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUGE SIZED 2772 CONTRACTS from 219,051 UP TO 221,823 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 CONTRACTS FOR APRIL., 0 FOR MAY, FOR JUNE 0 CONTRACTS AND JULY: 4032 CONTRACTS AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4032 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2772 CONTRACTS TO THE 4032 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG GAIN OF 6804 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 34.02MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 1.570 MILLION OZ FOR JUNE.

RESULT: A LARGE SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 12 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A HUGE SIZED 4032 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN UP 24.23 POINTS OR .86% //Hang Sang CLOSED UP 613.36 POINTS OR 2.27% /The Nikkei closed UP 249.71 POINTS OR 1.21%//Australia’s all ordinaires CLOSED UP .91%

/Chinese yuan (ONSHORE) closed DOWN at 6.9320 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9320 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9535 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China

The Chinese are very clever people. They are dodging USA tariffs with fake “made in Viet Nam” tags

( zerohedge)

ii)China is indeed limiting its exports of rare earths as the trade war now accelerates\

(courtesy zerohedge)

4/EUROPEAN AFFAIRS

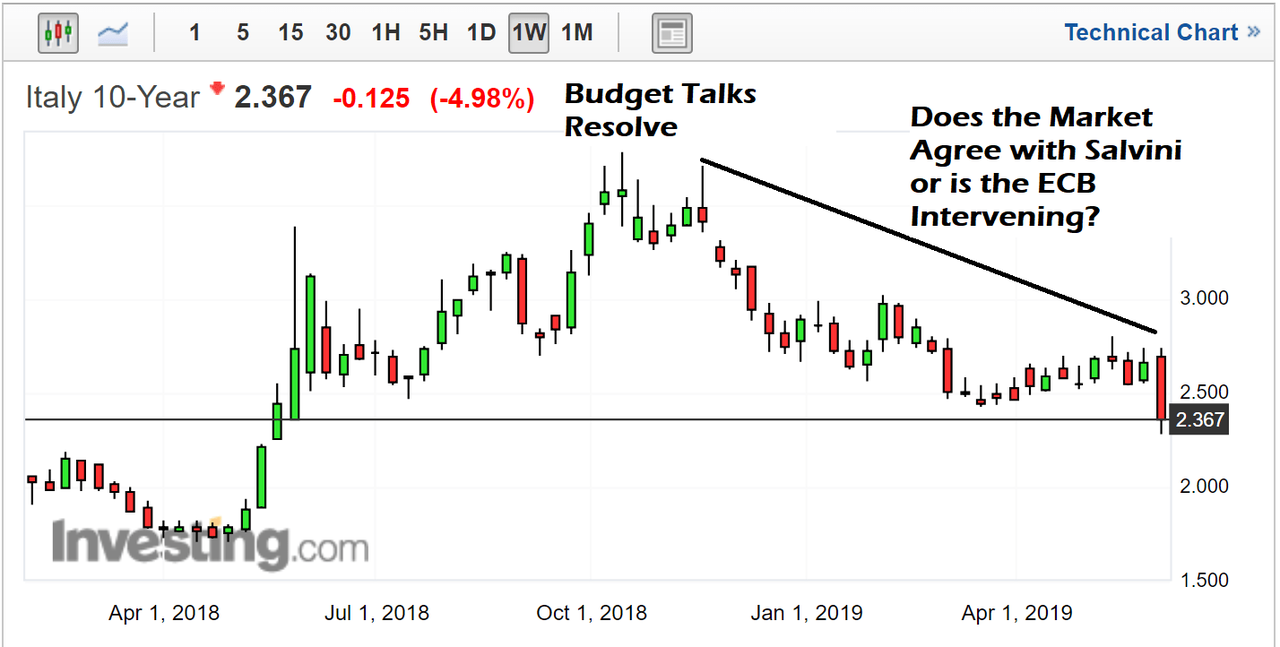

i) ITALY

An excellent commentary from tom Luongo as he highlights the Triumvirate of Conte, Tria and Mattarella who are backing Brussels trying to keep Italy in the EMU

(courtesy Tom Luongo)

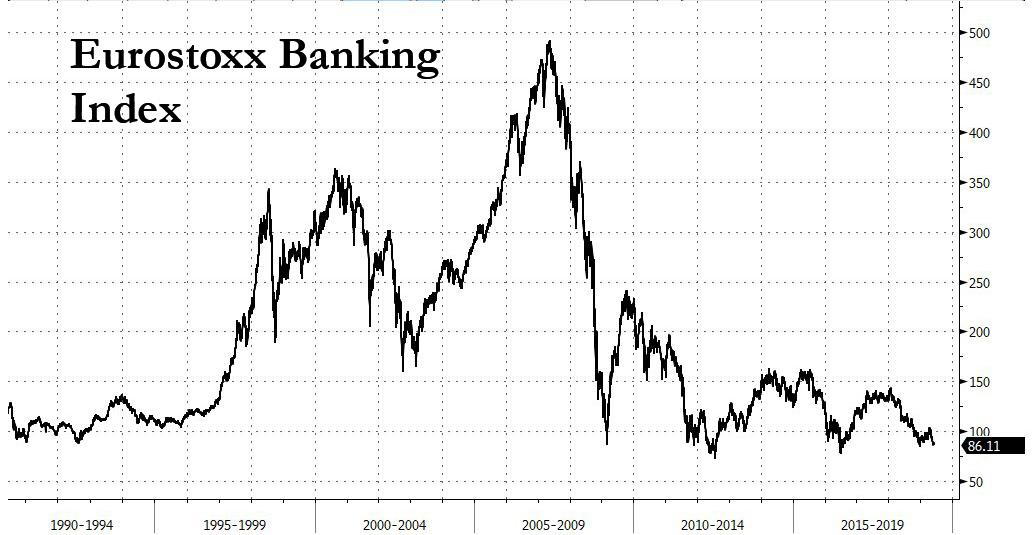

ii)The ECB sends another trial balloon through Reuters stating that it is willing to cut rates. It does not like to see its Euro exchange rate high as it is stifling growth in Germany et al. The problem of course, is that if the Euro is lowered so does the deposit rate which is already at record lows.

ii b)On the same subject as above: European markets are not reacting to Draghi’s hinting of lower rates(a must read/John Rubino)

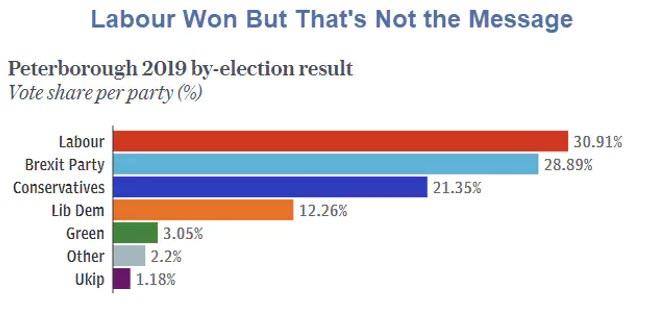

iii)Mish Shedlock explains to us the BREXIT situation and it is now up to Boris Johnson. It is his to lose(courtesy Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

Iran blasts Pompeo after the USA initiated more sanctions against Iranian petrochemical companies. Iran’s economy is now in complete shambles

( zerohedge)

( zerohedge)

6. GLOBAL ISSUES

Mexico/USA

a)Peso rises after the USA Mexico migration deal

(courtesy zerohedge)

b)Trump this morning states that another very important part of the Mexico deal is now finished. The New York Times and the Washington post thinks that the deal is a phony

(courtesy zerohedge)

7. OIL ISSUES

a)For those of you who think that the USA economy is still executing on all 4 cylinders led by shale production: guess again…the industry is nothing but a gusher of red ink…

(courtesy// Nick Cunningham)

b)Tom Luongo on the same subject as above

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

i)VENEZUELA/

(courtesy zerohedge)

9. PHYSICAL MARKETS

(Karen Yeung/SCMP/GATA)

ii)Looby’s message: The uSA may end its dollar dominance by doing stupid stuff

( Looby/GATA)

iii)Interesting: Ghana now overtakes South Africa in gold production

(courtesy Bloomberg/GATA)

iv)Putin calls for deep reform and a removal from the USA dollar(courtesy Agence France-Presse/GATA)

v)China announces an increase in reserves of 15.6 tonnes last month. China produces around 400 tonnes per year or 33.3 tonnes per month. No gold ever leaves China so they are continually hiding their gold stach.

(London’s Financial Times/GATA)

vi)Please support GATA as they are at the top trying to expose the crookedness of bankers

(Chris Powell)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

II)MARKET TRADING

ii)Market data

More indications that the uSA economy is faltering; job openings fall and layoffs pick up

(courtesy zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)Trump reaches a deal with Mexico. Let’s see if they will abide by the conditions of the agreement

( zerohedge)

b)Homelessness continues to rise in most major USA cities.

c)Peter Schiff believes very strongly that the Fed had no real intention for normalizing rates…it was a very big lie. He also states that the Fed is lying about the strong USA economy..hit is very weak. He extends the USA to lower rates from the already low 2.5% and probably bring the rates down to zero trying to avoid the deflation of assets.a good one..

( Peter Schiff)

SWAMP STORIES

a)Mark Meadows confirms on Friday night that the FBI knew within 60 days that the Russian probe was a phony

(courtesy zerohedge)

b)Trump just cannot win: after 1000’s of illegal immigrants have stormed into the USA, Trump threatened Mexico with tariffs. Mexico relented and Pelosi continues to slam Trump

what a farce!!

(courtesy zerohedge)

Let us head over to the comex:

i) Into Brinks: 32,215.302 oz

1002 kilobars

arrived from JPMorgan

Gold withdrawals;

i) We had 0 withdrawal: out of JPMorgan: nil oz

.

Gold To Reach 6 Year High Over $1,400 on Uncertain Outlook for Global Markets

Gold is finally gaining the traction needed to boost prices to a level not seen since 2013 as concern mounts over increased trade war tensions and the global growth outlook.

Bullion may touch $1,400 an ounce this year as investors hedge risk, according to Rhona O’Connell, head of market analysis for EMEA and Asia regions at INTL FCStone Inc.

Spot gold was at about $1,326 an ounce on Monday after jumping to a 13-month high of $1,348.31 on Friday on the back of a weaker than expected U.S. jobs report for May.

“All the dominant asset classes have a question mark over them at the moment, which is generally when gold comes into play,” O’Connell said by phone before this week’s Asia Pacific Precious Metals Conference in Singapore.

Gold is seeing a revival after a lackluster few months as investors weigh the prospects for slowing global growth and increasing expectations that the Federal Reserve will cut interest rates. Volatility in stocks following the escalating U.S. trade tensions with China and then with Mexico, has led to a surge in demand for havens, with 10-year Treasury yields near a 2017 low and Wall Street’s biggest banks warning of growing recession risks.

“There’s enough elements of risk in the outlook for world economies, there’s still a degree of geopolitical risk, currencies are looking volatile, and the fact that the market’s looking at a recession, the equity markets are obviously under threat,” according to London-based O’Connell.

The steepening U.S. yield curve shows bond traders have concluded that the case for the Fed to cut rates is only strengthening. Last week, Chairman Jerome Powell signaled an openness to loosening, pledging to keep a close watch on the fallout from disputes between the U.S. and its largest partners.

“We are in the late end of the cycle, the Fed’s move is likely a cut, maybe it happens a little later than some are hoping for, but inevitably most likely, it will happen,” said Bart Melek, the global head of commodity strategy at TD Securities in Toronto, who’s also attending the conference.

He sees bullion hitting $1,400, but not until early 2020.

“As volatility increases and the risk of a correction in equity market increases, we’re going to start seeing more significant flows of capital into the gold markets,” said Melek, who sees prices in a range of $1,320 to $1,375 in the second half, and a 2020 fourth-quarter average of $1,425.

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

07-Jun-19 1334.30 1340.65, 1049.16 1052.14 & 1184.19 1184.60

06-Jun-19 1336.65 1335.50, 1053.15 1051.17 & 1189.62 1185.92

05-Jun-19 1337.75 1335.05, 1052.01 1049.22 & 1185.38 1184.99

04-Jun-19 1323.60 1324.25, 1045.51 1043.77 & 1177.47 1177.26

03-Jun-19 1313.95 1317.10, 1039.47 1042.35 & 1175.99 1175.38

30-May-19 1276.45 1280.95, 1010.44 1015.92 & 1146.25 1151.70

29-May-19 1283.50 1281.65, 1016.02 1013.27 & 1151.04 1150.67

28-May-19 1283.90 1278.30, 1012.87 1008.20 & 1146.91 1142.29

27-May-19 UK Holiday

News and Commentary

Gold Market Stretches Gains to 8th Session After Weak Jobs Growth

China’s Gold Reserves Grow for 6th Straight Month

Trump Is ‘perfectly Happy’ to Hit China With New Tariffs if Xi Meeting Doesn’t Go Well: Mnuchin

Oil Just Had Its Worst Run Since 2008

Global Trade Heading for Worst Year Since Financial Crisis – ING

“Global Trade Conflicts Should See Gold Continue to Outperform” – Goldcore

China Is Buying More and More Gold as the Trade War Drags On

Gold Looks Headed Toward Six-Year High as Global Markets Outlook Dims

Putting America First May End Dollar Dominance

Gold Giants Battling to Lure Back Investors Who Fled Industry

Gold Production In South Africa Continues to Fall – Now 2nd Largest Producer in Africa After Ghana

Look now who is talking about manipulation!! Mnuchin is accusing China of manipulating its currency because of the tariffs. However he says nothing of the uSA manipulating its stock market and the precious metals

(Karen Yeung/SCMP/GATA)

Manipulation is when you stop manipulating, treasury secretary says

Submitted by cpowell on Sat, 2019-06-08 15:09. Section: Daily Dispatches

China Is Letting Value of Yuan Slide to Offset Trade War Tariffs, US Treasury Secretary Steven Mnuchin Says

By Karen Yeung

South China Morning Post, Hong Kong

Saturday, June 8, 2019

U.S. Treasury Secretary Steven Mnuchin today accused China of allowing the value of its currency to slide in a bid to offset the impact of Washington’s trade tariffs on the cost of its goods to American consumers.

“It’s not coincidental in my mind that the currency has moved from approximately 6.30” yuan to the U.S. dollar “to 6.90,” the official said on the sidelines of the G20 finance leaders’ meeting in Japan.

…

* * *Help keep GATA goingGATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:http://www.gata.orgTo contribute to GATA, please visit:http://www.gata.org/node/16

end

Putin calls for deep reform and a removal from the USA dollar

(courtesy Agence France-Presse/GATA)

Putin says role of dollar should be reconsidered in world trade

Submitted by cpowell on Sat, 2019-06-08 15:28. Section: Daily Dispatches

From Agence France-Presse

via The Business Times, Singapore

Friday, June 7, 2019

https://www.businesstimes.com.sg/government-economy/putin-says-role-of-d…

ST. PETERSBURG, Russia — Russian leader Vladimir Putin on Friday renewed calls to revisit the role of the U.S. dollar in global trade and accused Washington of seeking to dominate the world.

Speaking at an economic forum alongside Chinese President Xi Jinping, the Russian president called for deep reform, claiming that trust in the dollar had been on the decline.

… Changes in the global economy “call for the adaptation of international financial organisations, rethinking the role of the dollar, which … has turned into an instrument of pressure by the country of issue on the rest of the world,” Mr. Putin said.

The Kremlin chief, whose country has chafed under numerous rounds of U.S. sanctions, has repeatedly slammed the global financial system established by Washington in the aftermath of World War II.

In a speech at a plenary session, Mr. Putin accused Washington of seeking to “extend its jurisdiction to the whole world.”

“But this model not only contradicts the logic of normal international communication. The main thing is, it does not serve the interests of the future.”

* * *

end

Looby’s message: The uSA may end its dollar dominance by doing stupid stuff

(courtesy Looby/GATA)

John Looby: Putting America first may end dollar dominance

Submitted by cpowell on Sun, 2019-06-09 03:14. Section: Daily Dispatches

By John Looby

The Sunday Times, London

Sunday, June 9, 2019

https://www.thetimes.co.uk/edition/ireland/putting-america-first-may-end…

For three-quarters of a century, the hegemony of the dollar and its role as the global reserve currency has been secure. Even the break with gold, and the effective collapse of Bretton Woods in 1971, served only to strengthen rather than weaken its position. Crucially, the dominance of the dollar was cemented by the big oil-exporting states — led by Saudi Arabia — asking for payment exclusively in US dollars.

More recently, China has played a central role. Thirty years ago, Sino-US trade was essentially irrelevant. Since then, the trade relationship has exploded, with the US consuming vastly more than the value of its output, and China doing the mirror opposite. By choosing to direct the vast bulk of its dollars into US treasuries, China is now the biggest private creditor of the US federal government, and arguably the single biggest supporter of the dollar.

Although the US economy today is roughly the same size as the EU — accounting for just over a fifth of global GDP — the dollar still accounts for almost three-quarters of global foreign exchange reserves, and almost 90% of global foreign exchange transactions.

In his insightful 2010 book, “Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System,” economic historian Barry Eichengreen concludes the likelihood of continuing dollar dominance remains high. Yet his reasoning has a caveat: “Serious economic and financial mismanagement by the United States is the one thing that could precipitate flight from the dollar. And serious mismanagement is not something that can be ruled out. We may yet suffer a dollar crash, but only if we bring it upon ourselves.”

Grappling with the likelihood of such US self-harm, the post-war path of the UK and its troubled currency is instructive.

In 1945, the UK had an extensive empire, formidable armed forces and a globally significant currency. It was also a nuclear power, a permanent member of the UN security council and a serious presence across Asia, Africa and the Middle East. Notwithstanding its relative decline, disproportionate power and prosperity continued to beckon.

But the reckless risk of the Suez Crisis in 1956 — where the threat to sterling from the Oval Office proved decisive — effectively ended the UK’s autonomy. Never again would it be free to act without the imprimatur of the White House. The overestimation of its power had proven calamitous.

By 1976 the UK economy was widely and accurately known as “the sick man of Europe”. Mired in industrial strife and with sterling crashing again, the Callaghan government had little choice but to seek a humiliating IMF bailout in the form of a huge dollar loan. The telling image of the chancellor of the exchequer Denis Healy at Heathrow airport, forced to abandon a trip to Hong Kong and return to the treasury to apply for the loan, captured vividly the loss of power and prestige.

The more sanitised version of the Obama doctrine is: “Don’t do stupid stuff.” Generally seen as a pithy insight guiding his approach to foreign policy, it arguably summarises the broad approach of post-war US policy in many areas. For decades, as the architect and chief beneficiary of the post-1945 global order, America has adroitly defended and extended the reach and the power of the rules-based multilateral system.

The end of US dominance was never likely to be smooth. But compared with his post-war predecessors, the current occupant of the White House has a radically different view of the power and interests of the US. The evidence is accumulating that the benign rationality of US engagement with the rest of the world has inverted.

The possibility that this may undermine the dominance of the dollar is now real and growing. The salutary experience of the UK highlights the cost of myopic and reckless decisions. China, for example, can direct its dollars wherever it chooses. While buying treasuries has been its historic choice, future choices may well be different.

More generally, a new era may be dawning where policymakers and investors across the globe are losing a long-standing constant, while the US faces the loss of a valuable privilege chasing a delusional fantasy to put “America First”. Like sterling before it, there is nothing inevitable or immortal about the dominance of the dollar.

It’s time for investors to review their exposure to dollar-denominated assets. Complacent inertia could prove very costly.

—–

John Looby is a senior portfolio manager at KBI Global Investors. The views expressed are his own.

…

end

Interesting: Ghana now overtakes South Africa in gold production

(courtesy Bloomberg/GATA)

The African nation built on gold, loses its production crown to a rival

Submitted by cpowell on Sun, 2019-06-09 14:42. Section: Daily Dispatches

By Felix Njini

Bloomberg News

Sunday, June 9, 2019

The country that led global gold production for a century and extracted about half the bullion ever mined is now Africa’s second-largest gold producer. Output is shrinking as operators capitulate to stubbornly high costs, regular strikes and the geological challenges of tapping the world’s deepest mines.

Meanwhile, Ghana, a country whose gold mining industry dates back to the 19th century, is benefiting from lower-cost mines, friendlier policies and new development projects.

..South African industry stalwarts AngloGold Ashanti Ltd. and Gold Fields Ltd. are shifting their focus to other countries — including Ghana — where deposits are cheaper and easier to mine. The largest remaining gold miner in South Africa, Sibanye Gold Ltd., is cutting thousands of jobs and diversifying into platinum group-metals as it struggles to contain costs.

The difficulties facing South African gold mines mean output is contracting even though it’s got the world’s second-largest reserves of the metal, according to estimates from the U.S. Geological Survey. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-09/nation-built-on-gold-…

end

Please support GATA as they are at the top trying to expose the crookedness of bankers

(Chris Powell)

If GATA is doing the right thing, please consider helping us

Submitted by cpowell on Sun, 2019-06-09 16:05. Section: Daily Dispatches

12:11p ET Sunday, June 9, 2019

Dear Friend of GATA and Gold:

For years GATA’s officers have marveled among themselves that central banking’s gold price suppression policy couldn’t get more obvious, and each time we have been proven wrong. But in a way that may be an indicator of a certain amount of success for the organization.

For with its research, documentation, interpretation, aggregation of relevant news, complaint, and clamor, GATA does seem to have made it harder for central banks to cover their tracks in the gold market. More analysts are either acknowledging that the gold market isn’t free or are ceasing their silly denials of surreptitious market manipulation undertaken or underwritten by governments.

The futures markets, to which central banks retreated with gold price suppression policy when outright and public dishoarding of gold reserves began to fail in the 1960s and 1970s, are showing more signs of strain and producing more crazy anomalies.

Government officials themselves increasingly talk in public about gold’s potential to compete with or even supplant the U.S. dollar in the world financial system, the more so as the United States is weaponizing the dollar and, it seems, threatening to expel nearly everybody from the dollar system, as if the system then would be of any use even to the United States itself.

The rising gold prices of the last few weeks give hope that markets are starting to understand what has been going on for so long. GATA is not the rooster of fable who thought his crowing made the sun rise, but if we have revealed or publicized information that has increased this understanding around the world, maybe we fairly can claim to have hastened the day of deliverance from the totalitarianism and imperialism represented by gold market rigging — hastened the transition to limited and accountable government, fair dealing among nations, free markets, and democracy.

Of course others are far better suited to this work and more obliged to take it on — the monetary metals mining industry itself, its trade organizations like the World Gold Council, and most of all mainstream financial news organizations. When they do their duty GATA will be glad to withdraw. We never meant this work to become a career. Indeed, if it becomes a career, it will have been a failure, and there are many other walls against which one’s head well may pound, if not many that are higher, thicker, and more sinister.

So with your help we aim to press on indefinitely. Our officers lately have been doing many more interviews than usual and some of them have been quite successful in building interest in our issue. Our e-mail dispatch list recent surpassed 8,000 addresses, indicating that our reach is growing, even as we already knew that only a small fraction of the people on that list have contributed to us financially.

So if you have not already made a donation, please consider making one now. To support its work GATA should be trying to raise money constantly, but we’re a small organization and not terribly adept at it. Further, of course, the monetary metals sector has been demoralized for years.

Being up against nearly all the money and power in the world, GATA can’t promise victory, just to keep trying. But Isaiah prophesizes that strength will come to those who do the right thing, and history shows that the bad guys lose when they go too far. So if we are doing the right thing, we’ve got a chance, because the bad guys have gone way too far here.

Since GATA is a tax-exempt 501-c-3 civil rights and educational organization under the U.S. Internal Revenue Code, donations are federally tax-deductible in the United States. To donate, please visit our internet site here:

Even a contribution of $1 will be a dollar more than GATA has received or is ever likely to receive from Newmont Mining and Barrick Gold. Their indifference will make your generosity even more appreciated.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

… end

China announces an increase in reserves of 15.6 tonnes last month. China produces around 400 tonnes per year or 33.3 tonnes per month. No gold ever leaves China so they are continually hiding their gold stach.

(London’s Financial Times/GATA)

China announces gold reserve increase for sixth straight month

Submitted by cpowell on Mon, 2019-06-10 01:46. Section: Daily Dispatches

China Gold Reserves Climb for Sixth Month in May

By Alice Woodhouse

Financial Times, London

Monday, June 10, 2019

https://www.ft.com/content/ca50aa10-8b18-11e9-a1c1-51bf8f989972?desktop=…

China increased its gold purchases for the sixth month running in May, taking its total reserves to 1,916 tonnes, while the country’s foreign exchange holdings defied expectations for a fall.

The People’s Bank of China bought 15.6 tonnes of the precious metal last month, according to the central bank.

…

The country has accumulated 74 tonnes of the precious metal since the end of November, when it initially began ramping up purchases, according to Refinitiv data. The value of its reserves has risen to $79.8 billion as US-China trade tensions have rumbled on.

end

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

|

|

|||

THEY ARE LOSING BADLY, SO THEY CHEAT — Bill Holter

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9320/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9535 /shanghai bourse CLOSED UP 24.23 POINTS OR .86%

HANG SANG CLOSED UP 613.36 POINTS OR 2.27%

2. Nikkei closed UP 249.71 POINTS OR 1.21%

3. Europe stocks OPENED ALL GREEN/

USA dollar index UP TO 96.84/Euro FALLS TO 1.1310

3b Japan 10 year bond yield: FALLS TO. –.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.62/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.11 and Brent: 63.40

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.23%/Italian 10 yr bond yield DOWN to 2.41% /SPAIN 10 YR BOND YIELD DOWN TO 0.61%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.64: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.85

3k Gold at $1335.00silver at: 14.91 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 6/100 in roubles/dollar) 64.73

3m oil into the 54 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.62 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9909 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1199 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.23%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.14% early this morning. Thirty year rate at 2.62%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8004..

Global Stocks Race HIgher On Trade Deal, Rate Cut Hopes As Yuan Tumbles, UK Economy Implodes

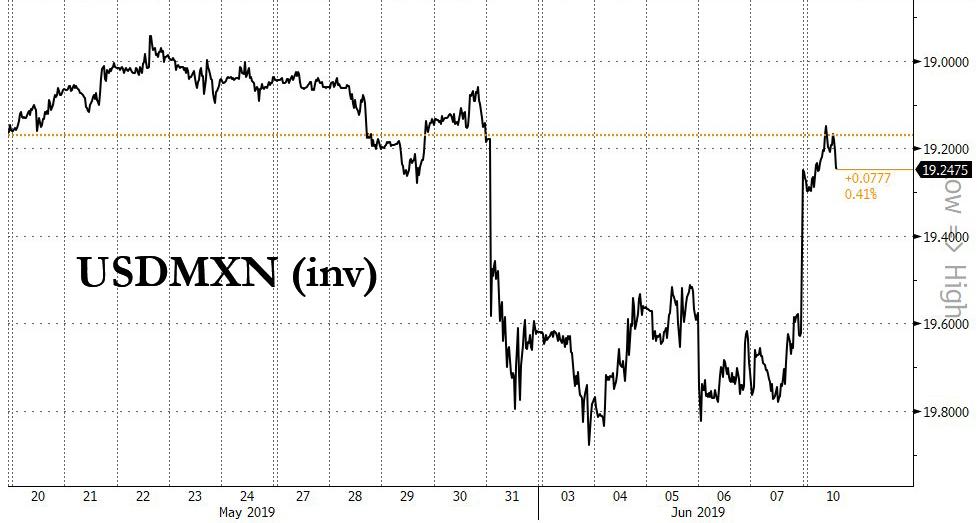

June’s euphoric rebound from the May slump continued on Monday, as European shares followed Asian stocks higher on Monday after the United States ended plans to impose tariffs on Mexico (at least until the proposal is voted down by Mexico’s legislative body) and as investors anticipated lower U.S. interest rates when the Federal Reserve meets next week on the back of poor jobs data.

The biggest overnight mover was the Mexican peso which soared more than 2% on Monday, its biggest gain in over a year, as investors bought the currency in a relief rally after fretting for the past week that opening up another trade conflict, while still battling with China, could push the United States and other major economies into recession.

Futures on the S&P 500, Dow Jones Industrial Average and Nasdaq 100 all climbed, as one would expect, but much of the overnight rally fizzled as the real threat to the global economy – the trade war with China – showed no signs of relenting.

All Asian markets advanced on Monday in celebration another trade war front had been averted for now, led by Hong Kong and Japan. Hong Kong’s Hang Seng Index closed 2.3% higher, extending its gains into the third day, while China’s Shanghai Composite Index jumped 0.9%. Japan’s Topix Index gained 1.3% to a three-week high and the Nikkei rose 1.2%, with Nippon View Hotel Co. and Denki Kogyo Co. contributing most of the index’s gains. India’s S&P BSE Sensex Index rose 0.2%.

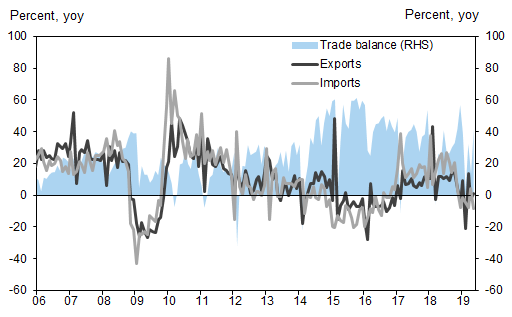

Investors also focused on Chinese trade data reported overnight, which showed imports in May tumbled 8.5% from a year earlier, a much worse than expected outcome that signaled weak domestic consumption. Exports, however, unexpectedly rose 1.1% last month, though this was once again due to front-loading of shipments by firms to avoid higher U.S. tariffs. The frontloading may continue in June, according to Goldman, due to the concerns of possible tariff for the $300bn of China exports to US (late June or early July at the earliest if implemented), which could support exports momentum in the near term. However, with the fading of this effect, exports momentum may turn notably weaker, especially amid moderate global economic growth, which would call for easier domestic policy to maintain growth stability.

Further commenting on the report, Goldman said that growth of imports for major commodities went down broadly. In value terms, crude oil imports slowed to +5.5% yoy in May (vs. +15.5% yoy in April); steel products imports continued to decline by 22.5% yoy in May (vs. -12.7% yoy in April); iron ore imports increased +24.0% yoy in May (vs. +23.1% yoy in April). In volume terms, crude oil imports decelerated to +3.0% yoy in May (vs. +10.8% yoy in April); steel products imports resumed the contraction by 13.1% yoy in May (vs. -3.8% yoy in April); iron ore imports decreased by 11.0% yoy in May (vs. -2.6% yoy in April), all indicating an economy that has hidden a sudden and profound air pocket.

China’s trade also happens to be the core issue depressing global sentiment today: “Mexico is not China and investors will want to see some clear signs of improvement in U.S.-China relations before increasing exposure to risk assets. Before then the market is left focusing on poor Chinese import figures for May…..as speculation builds over whether the PBOC [the People’s Bank of China] allows yuan to trade through 7 per dollar,” said Chris Turner head of FX strategy at ING Bank.

Over the weekend, we learned that China will implement export controls on sensitive sectors to prevent and resolve national security risks, while there were also reports that Chinese authorities reportedly warned several tech companies not to reduce exposure to China more than what was necessary due to trade restrictions or there would be consequences.

European shares followed Asian stocks higher on Monday on the “No Mexican Tariffs” relief rally, and as investors anticipated lower U.S. interest rates when the Federal Reserve meets next week on the back of poor jobs data. The European auto sector was boosted by signs that Fiat Chrysler Automobiles NV and Renault SA were looking for ways to revive their collapsed merger plan and secure the approval of Nissan Motor Co. Fiat Chrysler jumped 3%, while Renault’s shares were up 1%. In London, Thomas Cook’s shares rose 20% after a report that Hong Kong-listed Fosun Tourism was in talks to buy its tour operating business as the British group faces breakup after issuing three profit warnings in the past year.

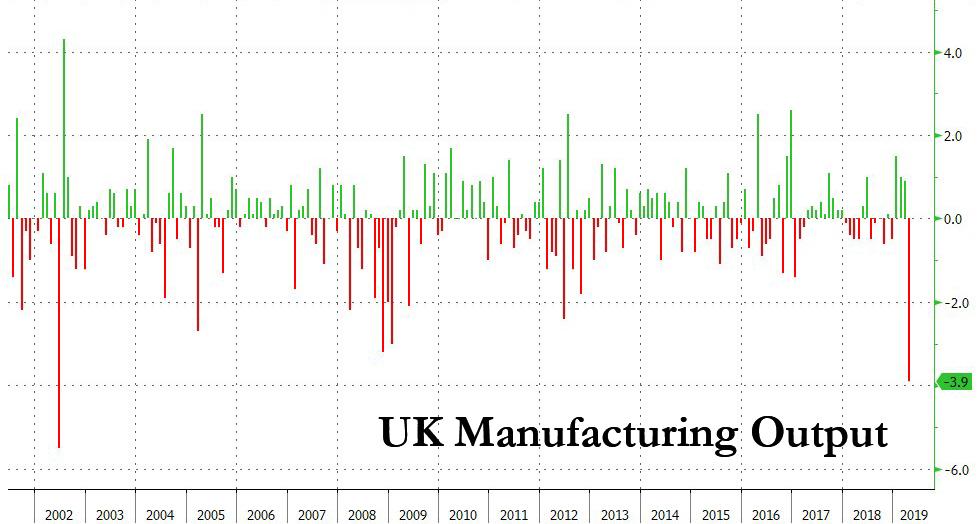

And speaking of the UK, the country was the center, or rather centre, of an “economic shock” today as a twofer of dismal economic data hit: U.K. Manufacturing output tumbled -3.9%, far below the -1.0% expected, the biggest drop in almost 17 years in April, or since June 2002, as the boost from Brexit stockpiling evaporated and car producers went ahead with planned shutdowns.

At the same time, GDP data “was a bit of a shocker even factoring in domestic politics,” according to Neil Jones, head of hedge-fund currency sales at Mizuho. The pound slumped as much as 0.4% to $1.2685 as GDP comes in at -0.4% m/m versus estimated -0.1%.

“The GDP estimate was downbeat anyway and we came in even lower”: said Jones, noting that the Pound was likely to slide further as “weekend politics does not look encouraging, this morning data is very downbeat and we’re in a market with only a small short at best”

In the United States, expectations the Fed will cut rates boosted stocks on Friday, with the buying continuing on Monday, after a weak jobs report from the U.S. Labor Department. Fed funds rate futures prices, down on Monday after the Mexico deal, are still pricing in more than two 25-basis point rate cuts by the end of this year, with one almost fully priced in by July. The Federal Reserve’s next policy meeting is set for next week, on June 18-19.

Still, not everyone was rushing to buy stocks just inches away from all time highs: “We remain a bit skeptical about the rally since last week, which is again due to expectations for easier monetary policy and easing trade tensions,” said Goldman strategist Christian Mueller-Glissmann. “Equity valuations remain high and global growth is still weak, which suggests draw-down risk remains elevated. As a result, we are reluctant to buy the dip.”

In rates, European government bond yields remained close to all-time lows. Core bond yields in the bloc were still at all-time lows, despite the two basis point move higher in the German bund in early trade to -0.24%, as expectations of easier monetary policy fuel bond buying. US Treasurys were near session highs, rising to 2.1414% after dipping below 2.06% after Friday’s payrolls report.

In FX, the dollar gained versus all G10 peers as Treasuries dropped; antipodeans came under pressure amid a drop in China’s imports, while the yen also felt the heat from the possibility of further BOJ monetary stimulus. The euro briefly fell below $1.13, sliding 0.3%, as leveraged names unwound short-term dollar shorts, even if near a 2-1/2-month high of $1.1347 touched on Friday. Meanwhile in China, the onshore yuan fell to its weakest level since November as trading resumed after a holiday, following comments from China’s central bank governor in which he hinted there was no line in the sand for the currency. Monday’s decline followed the offshore yuan’s tumble to its weakest level since November on Friday, as People’s Bank of China Governor Yi Gang signaled that he was not wedded to defending the nation’s currency at a particular level. Financial markets in China and Hong Kong were closed Friday

In commodities, oil prices rose on Monday after Saudi Arabia said producer club OPEC and Russia should restrict supplies to current levels, with front-month Brent crude futures at $63.61, 0.5%, above Friday’s close. Gold slipped almost 1%, having hit a 14-month high of $1,348.1 per ounce on Friday, near a major resistance around $1,350.

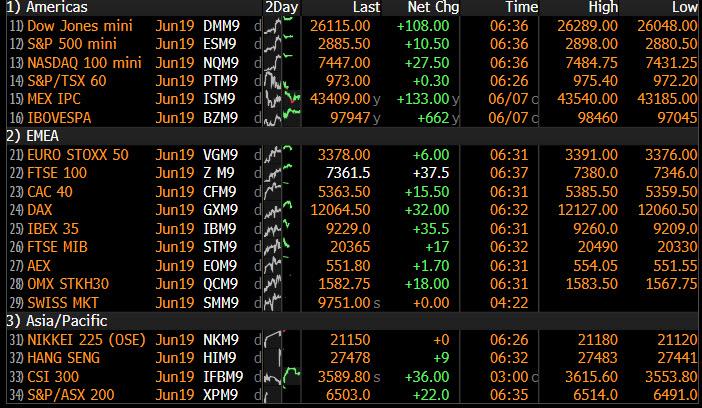

Market Snapshot

- S&P 500 futures up 0.3% to 2,883.50

- STOXX Europe 600 up 0.2% to 378.26

- MXAP up 0.9% to 155.69

- MXAPJ up 1% to 508.27

- Nikkei up 1.2% to 21,134.42

- Topix up 1.3% to 1,552.94

- Hang Seng Index up 2.3% to 27,578.64

- Shanghai Composite up 0.9% to 2,852.13

- Sensex up 0.06% to 39,640.72

- Australia S&P/ASX 200 up 1% to 6,443.89

- Kospi up 1.3% to 2,099.49

- German 10Y yield rose 2.3 bps to -0.234%

- Brent Futures up 0.2% to $63.39/bbl

- Italian 10Y yield fell 12.7 bps to 1.991%

- Spanish 10Y yield rose 4.2 bps to 0.595%

- Brent futures down 0.2% to $63.19/bbl

- Gold spot down 0.9% to $1,328.61

- U.S. Dollar Index up 0.3% to 96.87

Top Headline News from Bloomberg

- President Trump pushed Mexico — and his own party — to the brink when he threatened massive new tariffs over illegal immigration. And he now has a cross-border deal to show for it

- China’s export growth unexpectedly rebounded in May and imports dropped, as the trade standoff with the U.S. intensifies and both countries show no signs of deescalating tensions

- Bank of Japan can deliver more big monetary stimulus if necessary, but needs to take care with its side effects on the financial system, Governor Haruhiko Kuroda said

- U.K. manufacturing output fell the most in almost 17 years in April as the boost from Brexit stockpiling evaporated and car producers went ahead with planned shutdowns. The 3.9% decline, the most since June 2002, saw the economy as a whole shrink for a second straight month. Vehicle production plunged by a quarter

- Hong Kong’s leader pledged to press ahead with Beijing- backed legislation easing extraditions to China despite one of the city’s largest protests since the former British colony’s return more than two decades ago

- Fears are mounting at the European Central Bank that investors are losing faith in the inflation outlook, in a self-reinforcing spiral that could force the institution to dig deeper into its stimulus toolkit. Staff at the euro area’s national central banks are worried that inflation expectations are becoming “deanchored,” according to officials familiar with the matter

- The Bank of Japan can deliver more big monetary stimulus if necessary, but needs to take care with its side effects on the financial system, Governor Haruhiko Kuroda said

- Boris Johnson, the front- runner to succeed Theresa May as U.K. prime minister, promised to take Britain out of the EU in October with or without a deal as he hardened his rhetoric on Brexit and unveiled a tax-cut plan as the other leading candidates prepared to start their campaigns on Monday

- U.S. Treasury Secretary Steven Mnuchin said he had a “constructive” talk on trade with PBOC Governor Yi Gang. Mnuchin said “if they want to come back to the table and have a real agreement we will negotiate”

- China extended its gold- buying spree as the trade war with the U.S. damps growth expectations and boosts demand for a portfolio diversifier

- Hong Kong’s leader pledged to press ahead with Beijing-backed legislation easing extraditions to China despite one of Hong Kong’s largest protests since the former British colony’s return more than two decades ago

Asian equity markets began the week higher with sentiment underpinned after US and Mexico reached an agreement to avert tariffs which were set to kick in today, while the region also took impetus from the last Friday’s gains on Wall St. where disappointing Non-Farm Payrolls data spurred Fed rate cut hopes. Nikkei 225 (+1.2%) was lifted by favourable currency flows and following an upward revision to Q1 GDP, with automakers also underpinned by the tariff-related relief as well as news Fiat and Renault Chairmen discussed reviving their merger plan. Elsewhere, Australia remains closed for holiday, while Hang Seng (+2.2%) and Shanghai Comp. (+0.9%) were positive but with initial weakness seen in the mainland following a net liquidity drain by the PBoC and mixed Chinese Trade data in which Trade Balance and Exports topped estimates although a contraction in Imports highlighted subdued domestic demand. Finally, 10yr JGBs were initially pressured on safe-haven outflows but then staged an aggressive comeback as the declining yield narrative persisted and with the BoJ also in the market for JPY 775bln of JGBs.

Top Asian News

- Chinese Imports Drop as Growing Tensions With U.S. Cloud Trade

- Kuroda Says BOJ Has Enough Ammunition, Wary of Side Effects

- China Trust Shares Plunge as $1.7 Billion Products Face Default

- Hong Kong Stocks Lead Catch-Up Rally Amid Policy Easing Signals

European equities are marginally higher [Stoxx 600 +0.2%] following on from a positive Asia-Pac handover, with sentiment underpinned by the US-Mexico trade agreement, albeit with the positive momentum fading as Washington’s trade spat with China remains a grey cloud over the market. UK’s FTSE 100 (+0.5%) marginally outperforms its peers as exporters in the index benefit from a weaker domestic currency, whilst German, Swiss, Austrian and Norwegian cash markets are closed due to Whit Monday. Sectors largely reflect a “risk-on” mood as defensive sectors such as Utilities, Healthcare and Consumer Staples lag their peers. In terms of individual movers, BAE Systems (+1.2%) shares are supported in light of a mammoth merger between US listed Raytheon (RTN) and United Technologies (UTX), which some say point to renewed demand in the sector; the merger of equals will result in the new Co. having a annual revenue of around USD 74bln. Elsewhere, Fiat Chrysler (+2.2%) shares spiked higher amid reports of potential renewed talks with Renault (+2.1%), with the former also potentially buoyed by the US-Mexico trade agreement as it is one of 8 automakers with plants in the South American country. Finally, Thomas Cook (+14.5%) shares were bolstered by acquisition chatter as Forsun (18% shareholder) is reportedly planning a potential offer for Co’s tour arm which generates sales of GBP 7.4bln.

Top European News

- Russia U-Turn on Wealth Fund May Cause Dutch Disease, S&P Warns

- Some ECB Officials Fear Markets Losing Faith in Inflation Goal

- Ocado Invests in Indoor Farming in Step Beyond Grocery Tech

- Italy’s Conte Sets Warning to Populists on Talks With Brussels

In FX, the USD has extended its recovery from Friday’s lows, albeit in part due to renewed weakness in rival currencies and despite outperformance in certain EMs on fundamental and technical factors. The DXY just topped out a fraction below 97.000 having declined to sub-96.500 in wake of a weak BLS report that raised already lofty market expectations for Fed easing, with the focus now switching to upcoming CPI data to add more justification for the FOMC to deliver a cut.

- GBP – Not the biggest G10 loser, but Sterling has been one of the weakest majors in early EU trade on the back of monthly GDP for April showing a faster than forecast contraction in the UK economy as ip, manufacturing and construction output all slumped more than anticipated. The ONS assigned much of the blame to planned shutdowns and Brexit uncertainty that led to a record decline in car production, while transport equipment tanked the most since 1974. Cable duly retreated through 1.2700 in response and Eur/Gbp breached 0.8900 to post 5 month+ peaks.

- NZD/AUD – The main victims of a slump in Chinese imports, but somewhat perversely it is the Kiwi that is feeling the brunt of the data that exacerbates US-China trade tensions rather than the Aussie and perhaps due to Australia’s national holiday. Nzd/Usd is hovering just above 0.6600 vs Aud/Usd holding around last Friday’s low and several key technical support levels either side of 0.6950, like 10 and 21 DMA convergence circa 0.6955 and a Fib at 0.6945, while the Aud/Nzd cross is hugging the upper end of a 1.0525-00 range.

- JPY/CHF/EUR – The US-Mexican trade accord has seen the Yen and Franc lose safe-haven appeal and retreat vs the Buck to 108.50+ and 0.9900+ respectively, but Usd/Jpy faces some upside hurdles in the form of 1.1 bn option expiries at the 109.00 strike and then trend-line resistance at 109.15, while Usd/Chf and Eur/Chf (latter pivoting 1.1200) will be conscious that Thursday’s SNB quarterly policy review is looming. Elsewhere, Eur/Usd is testing 1.1300 and bids below the big figure after a brief and minor breach of Fib/30 DMA support at 1.1293 amidst more bleak Italian data that was only partly attributed to calendar distortions due to a national holiday, per ISTAT. Note also, decent expiry interest at 1.1300 in 1.1 bn.

- CAD – The Loonie remains relatively bid after Canada’s healthy jobs release in contrast to the US and with some extra encouragement via contagion from the aforementioned US-Mexican agreement that bodes well for USMCA prospects. Usd/Cad off lows but still well under 1.3300 in a 1.3278-25 band and near multi-month lows ahead of Canadian housing starts and building permits.

- EM – As noted above, several regional currencies outpacing the Dollar and none more so than the Peso in relief that Mexico will avoid US tariffs – Usd/Mxn sub-19.2000 and down through 19.1400 at one stage. Meanwhile, the Rand and Lira are also doing well, albeit in corrective moves after hefty losses of late on a steep deceleration in SA GDP/SARB mandate uncertainty, and ongoing US-Turkey strains, as attention turns to the upcoming CBRT policy meeting. Usd/Zar has reversed from 15.0000+ to around 14.8500 and Usd/Try down towards 5.8000, but conversely Usd/Cnh remains close to recent 6.9600+ peaks on the drop in Chinese imports.

Commodities are mixed as the energy complex continues to consolidate following its recent sell-off, with the benchmarks somewhat underpinned by the risk appetite around the market after US President Trump called off tariffs on Mexico which were due to be imposed today. WTI and Brent futures currently hover just above USD 54.00/bbl (ahead of its 200 DMA at 52.60) and USD 63.00/bbl respectively. Turning to OPEC, Saudi’s Energy Minister echoed some comments from the back-end of last week in which he stated that Russian is the only country still undecided on an OPEC+ deal extension, and subsequently, Russia’s Finance Minister noted that Brent prices could potentially fall to USD 40/bbl if the deal is not extended. Elsewhere, amid the possible ramifications of the US-Sino trade war on the global economy, Barclays revised its 2019 oil demand forecast lower by 300K BPD to 1.3mln BPD (in-line with IEA’s 2019 forecast of 1.3mln BPD and marginally higher compared to OPEC’s forecast of around 1.21mln). In terms of precious metals, a firmer risk tone and a stronger Greenback have shaved off some gains in gold (-1.0%) and silver (-1.5%), whilst copper (+0.7%) prices benefit from the risk appetite after Washington struck a deal with Mexico. Finally, iron ore futures are marginally firmer as a firmer Buck caps gains in the base metal, despite China’s iron ore imports rebounding from an 18-month-low last month, against the backdrop of tight supply amidst the recent production disruptions including Vale’s shipment cuts and China’s smog alerts.

US Event Calendar

- 10am: JOLTS Job Openings, est. 7,496, prior 7,488

DB’s Jim Reid concludes the overnight wrap

I hope you all had a good weekend. I’ve woken up with paint still splattered on me after a Sunday of arts and crafts and also smelling of fairy liquid. My brother bought the kids an industrial sized, battery operated bubble machine and given it’s size it required a big glug of washing up liquid. A very messy afternoon which ended with Maisie in agony and hysterics as fairy liquid ended up being rubbed into her eyes. I was in the doghouse for letting it happen on my watch !!

Markets are blowing small celebratory bubbles this morning as late on Friday the US announced a deal with Mexico to ensure that tariffs don’t get imposed today as planned. However there was some subsequent confusion as Mr Trump tweeted that Mexico has agreed to buy “large” amounts of agricultural products from the US as part of the deal. This didn’t seem to be anywhere in the accord released and sources close to the negotiations suggested on Bloomberg that there weren’t any additional side deals planned. So a bit puzzling but there will be relief that the tariffs have been avoided and perhaps some might believe it shows Trump’s propensity to strike deals after brinkmanship. As such there may be those thinking that a similar thing might happen with the China trade situation. That might eventually be true but it’s not clear this is imminent and as such high uncertainly will continue. As a result of the deal, the Mexican peso is up +2.04% this morning, the highest single day gain since July 2018.

Most other markets in Asia have started the week on a firmer footing taking as a result of the news. The Nikkei (+1.09%), Hang Seng (+2.00%), CSI (+1.43%), Shanghai Comp (+0.98%) and Kospi (+0.86%) are all up. China’s onshore yuan is trading down -0.35% at 6.9338, the weakest level of the year, with all the G-10 currencies also trading softer against the dollar. Elsewhere, futures on the S&P 500 are up +0.23% and the yield on 10y USTs is up +3.5bps while that on 2y USTs is up +4bps bringing the 2s10s spread down to +22.7bps. Gold prices are -0.85% this morning while WTI crude prices are up +0.56%.

This morning in China, we’ve seen trade data for May with the balance standing at $41.65bn (vs. $22.30bn expected) as exports jumped more than expected (at +1.1% yoy vs. -3.9% yoy) while imports saw a sharp slide (at -8.5% yoy vs. -3.5% yoy expected). In terms of trade with the US, exports declined -4.2% yoy (vs. -13.1% yoy last month) while the decline in imports was sharper at -26.8% yoy (vs. -25.8% yoy last month). Meanwhile, China’s May foreign reserves surprised on the upside at $3.101tn (vs. $3.090tn expected and $3.095tn last month). Our China strategists suggest this could either be due to lumpy coupon payments on their holdings or early signs that the Chinese are diversifying away from dollar holdings. You only mark to market when you sell so reserves could go up on this sort of event. We’ll wait for the latest Treasury holdings data to see.In terms of other data releases, Japan’s final Q1 GDP came in one tenth above the preliminary read at +0.6% qoq.

Moving on to this week, China data will take centre stage. After the trade data released earlier we have May CPI and PPI data tomorrow and then the full May activity indicators on Friday. At some stage during the week we should also get the May credit data, which is expected to show an increase in aggregate financing versus the month prior.

As we go into Fed blackout period, in the US the main highlights are May PPI tomorrow, CPI on Wednesday, the May retail sales report on Friday alongside the industrial production print and the preliminary University of Michigan consumer sentiment survey for June. In Europe we’re due to get final May CPI revisions over the week including data for Spain on Wednesday, Germany on Thursday and France and Italy on Friday. The April industrial production print for the Euro Area is also due on Thursday. In the UK we get the April GDP and industrial production data today and April/May employment data on Tuesday.

As for last week, global equity markets performed well, with the S&P 500 snapping a streak of four consecutive weekly losses to advance +4.41% (+1.06% on Friday), its best week since November. Other indexes performed similarly well, with the NASDAQ and DOW gaining +3.88% and +4.71% (1.66% and +1.02% Friday) respectively. There were two key drivers for the strength: increased confidence that the Fed will ease policy this year and firmer expectations that tariffs on Mexico would be avoided before today’s deadline. This was clearly what happened late on Friday night.

May’s nonfarm payrolls report showed that the US economy added only 75,000 jobs last month, minus another -75,000 in net revisions to the prior months. Average hourly earnings were also a touch softer than expected at +0.2% mom and 3.1% yoy. Futures markets moved to completely price in a Fed rate cut at the July meeting, plus an additional 62 basis points of cuts over the subsequent year. Bond yields fell sharply, with 10-year yields down -4.4bps on the week (-3.6bps Friday), but yet again the bigger moves were in the front-end, where 2-year yields fell -7.5bps (-3.1bps Friday).

European equities lagged the US, as the ECB’s meeting proved disappointing last Thursday. President Draghi barely changed the economic outlook or the balance of risks and was reluctant to signal further easing. The market reaction was negative, with equities falling, especially bank shares, the euro strengthening, and bond yields falling. Ultimately, the STOXXX 600 ended +2.28% (+0.93% Friday), though an index of bank stocks ended -0.29% on the week (-0.10% Friday). Bond yields fell across the continent, with bunds down -5.5ps (-1.8bps Friday) to -0.257% and a fresh all-time low. OATs also reached a record low of 0.085% after falling -12.5bps (-3.0 Friday), while BTPs outperformed, falling -31.2ps (-13.0bps Friday) even as the EU stepped up their fight over Italy’s debt. The mix of central bank easing expectations and soft data provided the impetus for the rally, but Italy was also boosted by positive rhetoric from the leaders of its two governing parties, Di Maio of the Five Star Movement and Salvini of the Northern League. They issued a joint statement on Thursday night that said “the government must move forward” on implementing “a constructive dialog with Europe,” helping to alleviate some of the concerns around a potential confrontation with Brussels.

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN UP 24.23 POINTS OR .86% //Hang Sang CLOSED UP 613.36 POINTS OR 2.27% /The Nikkei closed UP 249.71 POINTS OR 1.21%//Australia’s all ordinaires CLOSED UP .91%

/Chinese yuan (ONSHORE) closed DOWN at 6.9320 /Oil DOWN TO 52.49 dollars per barrel for WTI and 60.38 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9320 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9535 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a NORTH KOREA/SOUTH KOREA

3 b JAPAN AFFAIRS

3 C CHINA/CHINESE AFFAIRS

China

The Chinese are very clever people. They are dodging USA tariffs with fake “made in Viet Nam” tags

(courtesy zerohedge)