GOLD: $1347.00 UP $7.60 (COMEX TO COMEX CLOSING)

Silver: $15.01 UP 18 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1346.85

silver: $15.01

TOMORROW IS THE BIG FOMC MEETING. DRAGHI PREEMPTED POWELL TODAY BY UNLEASHING POSSIBLE QE IN EUROPE

HERE ARE THE KEY PRICES OF GOLD AND SILVER TO WATCH FOR:

GOLD: $1350. THIS LEVEL IS IMPORTANT FOR THE BANKERS AND NO DOUBT HUGE DERIVATIVE TRADES WERE INITIATED HERE. THE BANKERS WILL DEFEND THEIR LIVES AT THIS LEVEL. GOLD HAS BEEN BEATEN BACK AT LEAST 6 TIMES ONCE GOLD PIERCED $1350.

SILVER: $15.06. MANY ARE COMMENTING ON $15.00 BUT THE REAL PRICE TO WATCH IS $15.06 AS THIS WAS THE PRICE THAT SILVER WAS BEATEN BACK DOWN INTO THE LOW 14 DOLLAR LEVEL. A PIERCING OF 15.06 WILL CREATE NIGHTMARE FOR OUR BANKERS.

STAY TUNED FOR TOMORROW..IT WILL BE A BIG DAY.

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 237/301

XCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,338.700000000 USD

INTENT DATE: 06/17/2019 DELIVERY DATE: 06/19/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2

661 C JP MORGAN 259 237

686 C INTL FCSTONE 9

690 C ABN AMRO 1

737 C ADVANTAGE 18 61

800 C MAREX SPEC 1

905 C ADM 14

____________________________________________________________________________________________

TOTAL: 301 301

MONTH TO DATE: 2,114

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 301 NOTICE(S) FOR 30100 OZ (0.9362 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2114 NOTICES FOR 211,400 OZ (6.5754 TONNES)

SILVER

FOR JUNE

3 NOTICE(S) FILED TODAY FOR 15,000 OZ/

total number of notices filed so far this month: 343 for 1765,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

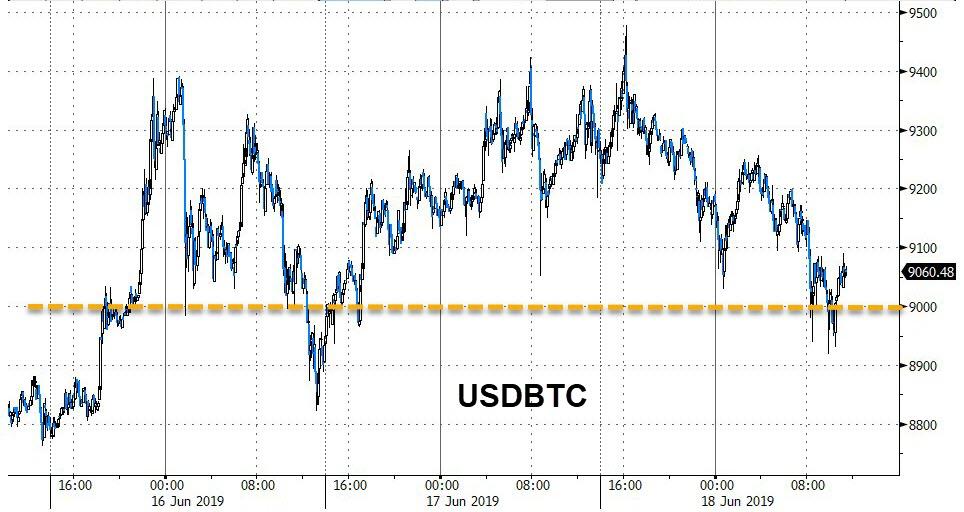

Bitcoin: OPENING MORNING TRADE : $ 9163 DOWN 143

Bitcoin: FINAL EVENING TRADE: $ 9101 DOWN 207

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A TINY SIZED 84 CONTRACTS FROM 232,913 UP TO 232,997 ACCOMPANYING THE 1 CENT GAIN IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR GOLD . HOWEVER WE ARE WITNESSING A RISE IN SPREADING ACCUMULATION BY THE BANKERS IN SILVER)..TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 406 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 406 CONTRACTS. WITH THE TRANSFER OF 406 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 406 EFP CONTRACTS TRANSLATES INTO 2.03 MILLION OZ ACCOMPANYING:

1.THE 1 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

1.560 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

32,529 CONTRACTS (FOR 12TRADING DAYS TOTAL 32,529 CONTRACTS) OR 162.65MILLION OZ: (AVERAGE PER DAY: 2710 CONTRACTS OR 13.56 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 162.65 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.23% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1033.40 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 84, WITH THE 1 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 406 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A FAIR SIZED: 490 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 406 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 84 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 1 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.83 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.082 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 3 NOTICE(S) FOR 15,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 1.560 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD SOME ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE SHARPLY WITH THE SMALLISH GAIN OF 1 CENT.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A SMALL SIZED 963 CONTRACTS, TO 523,341 DESPITE THE $1.65 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE ACCUMULATION PHASE OF THEIR OPERATION. THUS THE GAIN IN OI IS REAL AS INVESTORS ARE POURING INTO THE GOLD SECTOR

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5891 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 5891 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 523,341. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6854 CONTRACTS: 963 CONTRACTS INCREASED AT THE COMEX AND 5891 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 6854 CONTRACTS OR 685,400 OZ OR 21.31 TONNES. YESTERDAY WE HAD A TINY LOSS OF $1.65 IN GOLD TRADING.…AND WITH THAT SMALL LOSS IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 21.31 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 115,174 CONTRACTS OR 11,517,400 oz OR 358.24 TONNES (12 TRADING DAYS AND THUS AVERAGING: 9597 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 358.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 358.24/3550 x 100% TONNES =10.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,636.13 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED INCREASE IN OI AT THE COMEX OF 963 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK ON YESTERDAY($1.65)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5891 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5891 EFP CONTRACTS ISSUED, WE HAD AN STRONG SIZED GAIN OF 6854 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5891 CONTRACTS MOVE TO LONDON AND 963 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 21.31 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED DESPITE A LOSS IN PRICE OF $1.65 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 301 notice(s) filed upon for 30,100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $7.60 TODAY//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 764.10 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 18 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 319.070 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY SIZED 84 CONTRACTS from 232,913 UP TO 233,207 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 406 CONTRACTS FOR AUGUST: 0, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 406 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 84 CONTRACTS TO THE 406 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR GAIN OF 490 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 2.45MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 2.770 MILLION OZ FOR JUNE.

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 1 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 406 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

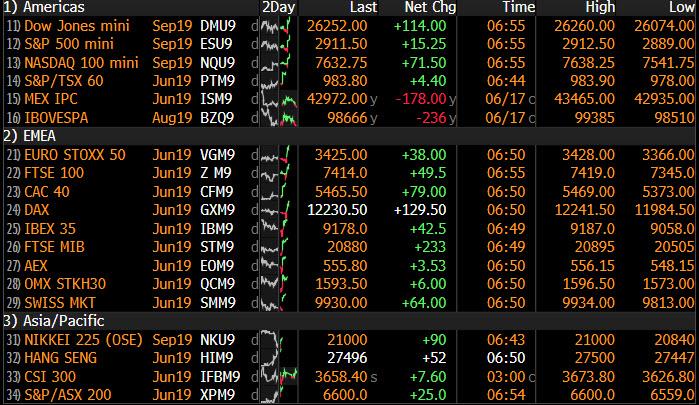

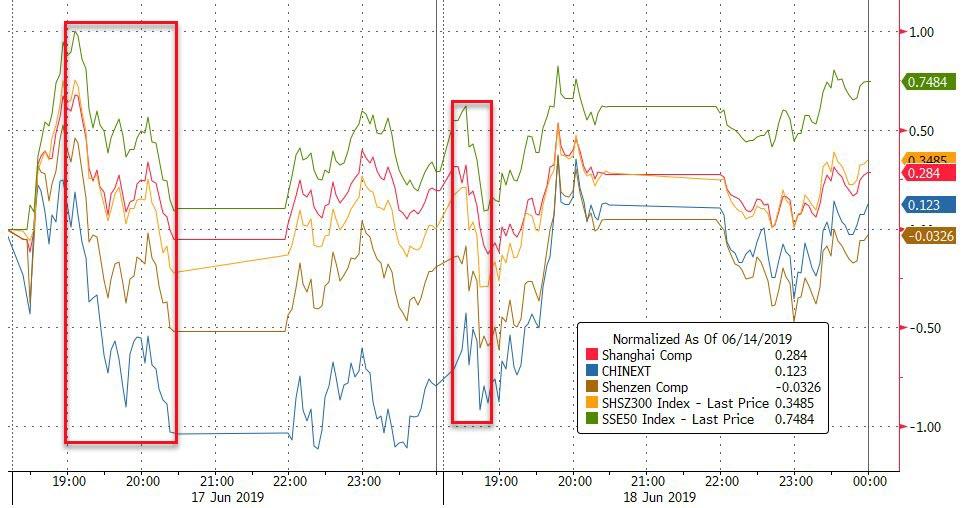

SHANGHAI CLOSED UP 2.54 POINTS OR 0.09% //Hang Sang CLOSED UP 271.61 POINTS OR 1.00% /The Nikkei closed DOWN 151.29 POINTS OR 0.72%//Australia’s all ordinaires CLOSED DOWN .58%

/Chinese yuan (ONSHORE) closed DOWN at 6.9267 /Oil DOWN TO 5189 dollars per barrel for WTI and 60.75 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.9267 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.9374 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/

China is set to roll out its new rare earth policy as soon as next week and it will be restrictive

(courtesy zerohedge)

Beijing slams Washington’s latest feeble attempt to set up a Trump -Xi meeting\\

( zerohedge)

4/EUROPEAN AFFAIRS

i)EUROPE/USA/AIRBUS/BOEING

I would say that Boeing is in a heap of trouble. On the first day of the big PARIS Air Show: the orders: Airbus 13 billion dollars worth of planes: Boeing zero

(zerohedge)

ii)ECB

Draghi clears the way for another round of stimulus which sends gold higher, the euro southbound. Yields all around the world collapse

(courtesy zerohedge)

iii)Fascinating, the greatest manipulator of the them all, the USA/President Trump accuses Draghi /EU of manipulating the euro.

(courtesy zero hedge)

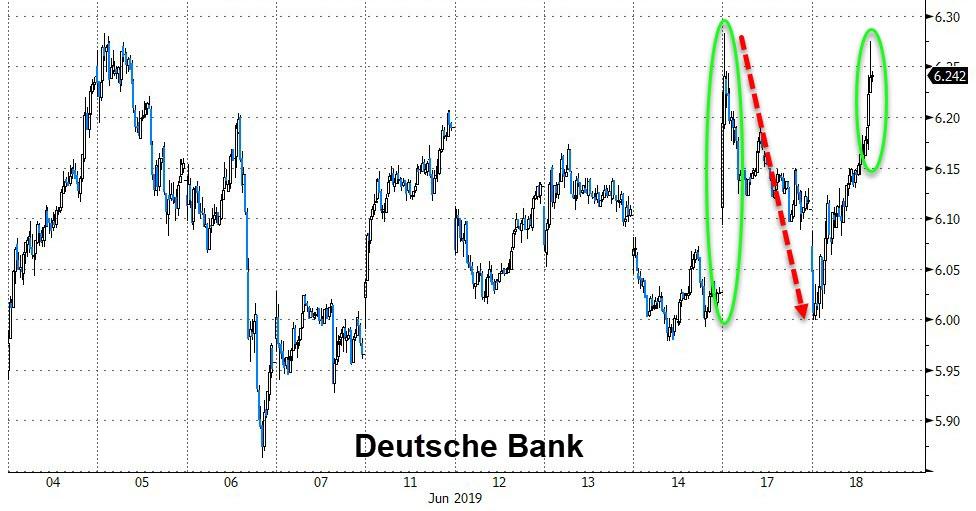

v)GERMANY/DEUTSCHE BANK

(courtesy zerohedge)

vi)The following is a critical important commentary that you must read. Many of you know full well that Deutsche bank is in serious trouble. They are the world’s largest derivative player and we have long suspected that their derivative book is way off side. You will also recall that Deutsche bank, unilaterally went to the judge in the gold and silver manipulation case to say that their are guilty of manipulating precious metals and if the court would go easy on them, they will provide copious emails and chat room discussions indicating that DB plus a plethora of other banks were guilty of collusion and manipulation..and they certainly provided the information to the court exactly like they said they would.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/USA

(zerohedge)

ii)Iran/uSA

The Jerusalem post reveals that the uSA is planning a tactical assault on Iran.

(JERUSALEM POST)

6. GLOBAL ISSUES

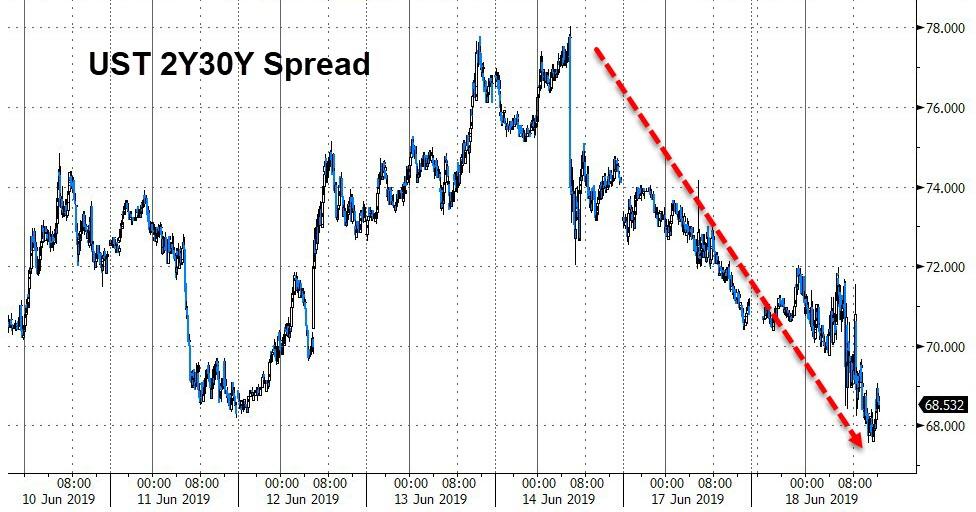

Unbelievable in a huge deflationary move, global yields are crashing all over the globe\

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

i)We have pointed out this story to you yesterday: China has cut its ownership of US Treasuries and they are now at a 2 yr low

( Bloomberg)

ii)Huge Swiss refiner Metalor will stop processing artisanal gold to reduce the risk of illegality

( Reuters /GATA)

iii)Bill Murphy comments how strange it is that our monetary metals is trading from violent to comatose

(LeMetropolecafe/.Bill Murphy/GATA)

10. USA stories which will influence the price of gold/silver)

i)MARKET TRADING USA//

a)Market trading/LAST NIGHT/

b)MARKET TRADING/USA

ii)Market data/USA

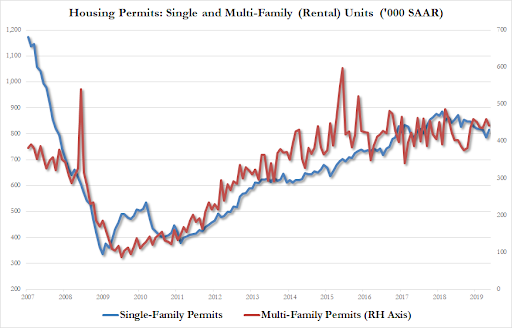

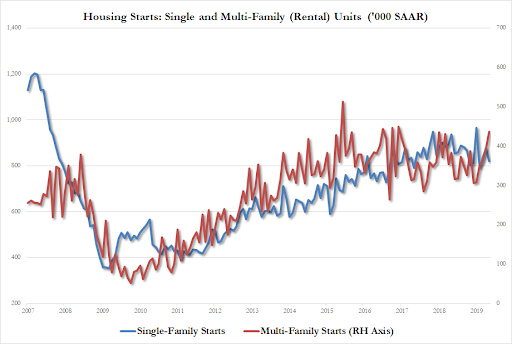

Even though rates are plunging everywhere, housing starts slid in May

( zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)The market will not like this: Trump is considering demoting Fed Chair Powell

( zerohedge)

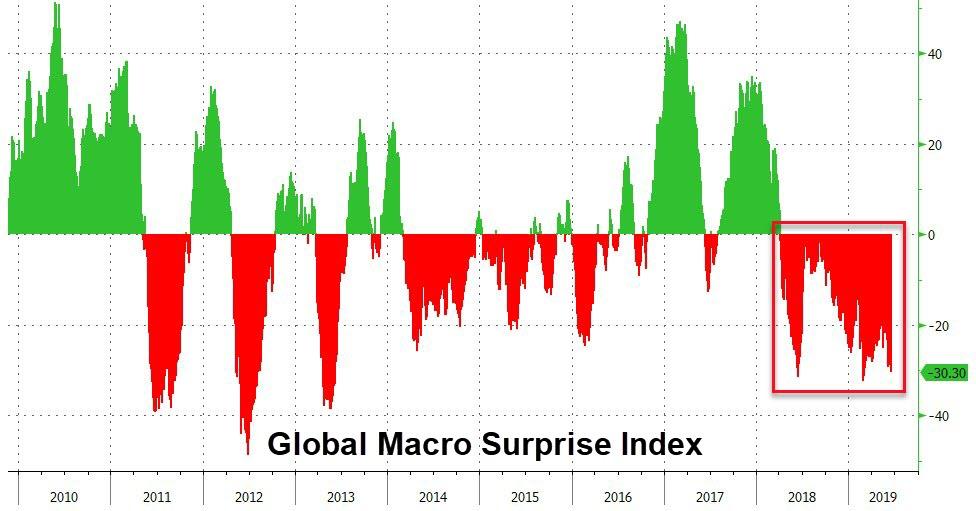

b)An excellent commentary from Michael Snyder as he reviews all of those bad economic numbers coming out during this month

( Michael Snyder)

SWAMP STORIES

i)Very sad!! after saying a year ago that his border town in Texas was not a war zone, the Mayor of a border town in the De; Rio district now is freaking out at the Republican for their inaction as illegals are overwhelming his city.

( zerohedge)

ii)New Clinton email review reveals multiple security incidents

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

this is a phony entry..they need paper gold elsewhere.

total gold withdrawals; nil oz

FOR THE JUNE 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 301 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 237 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE /2019. contract month, we take the total number of notices filed so far for the month (2114) x 100 oz , to which we add the difference between the open interest for the front month of JUNE. (469 contract) minus the number of notices served upon today (301 x 100 oz per contract) equals 228,400 OZ OR 7.104 TONNES) the number of ounces standing in this active month of JUNE

Thus the INITIAL standings for gold for the JUNE/2019 contract month:

No of notices served (2114 x 100 oz) + (469)OI for the front month minus the number of notices served upon today (301 x 100 oz )which equals 228,400 oz standing OR 7.104 TONNES in this active delivery month of JUNE.

We GAINED 2 contracts or an additional 200 oz will stand as these guys REFUSED TO morph into London based forwards as well as NEGATING a fiat bonus.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.08 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 7.104 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 303.593 million oz

The total number of notices filed today for the JUNE 2019. contract month is represented by 40 contract(s) FOR 40,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE, we take the total number of notices filed for the month so far at 353 x 5,000 oz = 1,765,000 oz to which we add the difference between the open interest for the front month of JUNE. (204) and the number of notices served upon today (3 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 353(notices served so far)x 5000 oz + OI for front month of JUNE( 204) -number of notices served upon today (3)x 5000 oz equals 2,770,000 oz of silver standing for the JN contract month.

WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 127,025 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 75,888 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 75888 CONTRACTS EQUATES to 379 million OZ 54.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.52% June 18/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -2.04% to NAV (june 18/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -1.52%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.20 TRADING 12.63/DISCOUNT 4.93

END

And now the Gold inventory at the GLD

JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

MAY 21/WITH GOLD DOWN $3.65 TODAY: A SURPRISE 2.00 TONNES WERE ADDED TO THE GLD GOLD INVENTORY//INVENTORY RESTS AT 738.17 TONNES

MAY 20/WITH GOLD UP $1.00 A HUGE 2.96 TONNE DEPOSIT INTO THE GLD//INVENTORY RESTS AT 736.17 TONNES

MAY 17/WITH GOLD DOWN $9.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 733.23 TONNES

MAY 16/WITH GOLD DOWN $11.50: A WITHDRAWAL OF 3.23 TONNES FROM THE GLD//INVENTORY RESTS AT 733.23 TONNES

MAY 15/WITH GOLD UP $1.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 736.46 TONNES

MAY 14//WITH GOLD DOWN $5.45 TODAY: STRANGE!! THE CROOKS DECIDED TO DEPOSIT A HUGE 3.23 TONNES INTO THE GLD INVENTORY//INVENTORY RESTS AT 736.46 TONNES

MAY 13/ WITH GOLD UP ANOTHER $15.40 TODAY: STRANGE! A MASSIVE WITHDRAWAL OF 6.41 TONNES OF GOLD (TO TAME GOLD’S RISE TODAY)/INVENTORY RESTS AT 733.23 TONNES

MAY 10 WITH GOLD UP $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 9//WITH GOLD UP $4.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 8/WITH GOLD DOWN $3.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 739.64 TONNES

MAY 7/ WITH GOLD UP $1.80: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 6/WITH GOLD UP $2.35: ANOTHER WITHDRAWAL OF 5.88 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 3/WITH GOLD UP $9.35 TODAY: A WITHDRAWAL OF 1.17 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 745.52

MAY 2/WITH GOLD DOWN $12.30 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

MAY 1/WITH GOLD DOWN $1.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 18/2019/ Inventory rests tonight at 764.10 tonnes

*IN LAST 612 TRADING DAYS: 169.66 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 512 TRADING DAYS: A NET 4.03TONNES HAVE NOW BEEN REMOVED FROM THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 18/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 17/WITH SILVER UP ONE CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.295 MILLION OZ///INVENTORY RESTS AT 319.070 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

june 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

jUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

MAY 17/WITH SILVER DOWN 13 CENTS TODAY: A BIG CHANGES IN SLV: A WITHDRAWAL OF 3.185 MILLION OZ FROM THE SLV INVENTORY VAULTS:/INVENTORY RESTS AT 312.366 MILLION OZ//

MAY 16/WITH SILVER DOWN 26 CENTS: NO CHANGES IN THE SLV INVENTORY//INVENTORY RESTS AT 315.551 MILLION OZ//

MAY 15/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SLV INVENTORY: A WITHDRAWAL OF 1.031 MILLION OZ// THE SLV/INVENTORY RESTS AT 315.551 MILLION OZ.

MAY 14/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV. INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 13//WITH SILVE5 DOWN 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ…

MAY 10/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 9/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 8/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 7/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 6/WITH SILVER DOWN 3 CENTS WE HAD ANOTHER DEPOSIT OF 891,000 OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 3//WITH SILVER UP 34 CENTS TODAY: A DEPOSIT OF 843,000 OZ INTO THE SLV/TOTAL INVENTORY RESTS AT 315.691 MILLION OZ//

MAY 2/WITH SILVER DOWN ANOTHER 13 CENTS, MIRACUOUSLY THE AUTHORITIES ADD 2.869 MILLION OZ OF SILVER BACK INTO THE SLV/INVENTORY RESTS AT 314.848 MILLION OZ//

MAY 1/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ////

Gold Rises In All Currencies – Gains 1.6% To £1,079/oz In GBP, Near 7 Year High

(courtesy Goldcore)

18, June

Gold prices have risen in all currencies today and especially in British pounds with gold having risen 1.5% to £1,078/oz. Concerns regarding the weak UK economy and Brexit fears continue to weigh on sterling.

More loose monetary policies are making gold attractive again as are the elevated economic and geopolitical risks which are leading to safe haven demand.

Gold has gained more than 6%, since touching a 2019 low of $1,265.85 in early May, due to these risks.

Gold had seen its usual Monday sell off as futures market participants took profits and pushed prices lower again.

The U.S. central bank is expected to leave borrowing costs unchanged this time but possibly lay the groundwork for a rate cut later this year which will support gold.

Expectations of interest rate cuts in the U.S. have increased amid the deepening U.S.-China trade war and signs that the U.S. economy is slowing significantly…

-END-

end

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

END

We have pointed out this story to you yesterday: China has cut its ownership of US Treasuries and they are now at a 2 yr low

(courtesy Bloomberg)

China cuts U.S. Treasury holdings to 2-year low amid trade war

Submitted by cpowell on Tue, 2019-06-18 00:55. Section: Daily Dispatches

By Sarah McGregor and Katherine Greifeld

Bloomberg News

Monday, June 17, 2019

China cut its U.S. Treasury holdings to the lowest in almost two years as the months-long trade conflict dragged on between the worlds two largest economies.

The nation’s holdings of notes, bills, and bonds declined by $7.5 billion in April to $1.11 trillion, according to Treasury Department data released today in Washington.

The latest numbers were collected before tensions between Washington and Beijing escalated to a new level in May, when trade talks collapsed and President Donald Trump raised tariffs on $200 billion of Chinese goods and announced more increases to come. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-17/china-cuts-u-s-treasu…

END

Huge Swiss refiner Metalor will stop processing artisanal gold to reduce the risk of illegality

(courtesy Reuters /GATA)

Swiss refiner Metalor to stop processing artisanal gold

Submitted by cpowell on Tue, 2019-06-18 02:43. Section: Daily Dispatches

By Peter Hobson

Reuters

Monday, June 17, 2019

LONDON — Switzerland’s Metalor, one of the world’s biggest gold refineries, said today it would work only with gold from large industrial mines in order to reduce the risk of illegality in its supply chain.

Informal methods of gold production, known as “artisanal” or small-scale mining, have grown rapidly in recent years as demand for gold has boomed, pushing prices higher.

…

Artisanal mining provides a livelihood to millions of people, often in poorer countries in South America, Africa and Asia. But it often leaks chemicals into rocks, soil, and rivers, working conditions can be appalling, and the gold such mining yields is often smuggled or used to launder money.

Metalor said it would stop working with artisanal mines or collectors and aggregators — companies that collect and resell gold from artisanal mines — because of the difficulty of ascertaining the mines’ legality and the origin of the gold. …

… For the remainder of the report:

https://www.reuters.com/article/gold-asm-metalor/swiss-refiner-metalor-t…

* * *

end

Bill Murphy comments how strange it is that our monetary metals is trading from violent to comatose

(LeMetropolecafe/.Bill Murphy/GATA)

Bill Murphy: Isn’t it strange? Monetary metals trading goes from violent to comatose

Submitted by cpowell on Tue, 2019-06-18 02:48. Section: Daily Dispatches

From “Midas” commentary

By Bill Murphy

www.LeMetropoleCafe.com

Monday, June 17, 2019

What will go on in the gold/silver markets will depend on what the Gold Cartel has in mind and what they can get away with. Their designs are well advertised for the public to see — those who want to anyway.

The bull camp is best represented by the physical market and whether it is strong enough to assist speculative longs to hold their ground. …

What is remarkable and not discussed in gold/silver land is how both precious metals can trade in such violent fashion, as they did Friday, and then go comatose as they did today on the Comex, which is just what occurred following the initial flurries. It is just not normal. …

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

Pay Attention Why India is more focused on Silver than Gold

(courtesy Ted Butler)

Several recent articles have highlighted a surge of silver imports to India, prompting me to take a closer look. India has always been a big buyer of silver and gold, befitting the traditions and culture of the country with the world’s second largest population. The population of India, more than 1.3 billion citizens, is now only about 50 million less than that of China. Combined, both countries make up 35% of the total world population (7.7 billion) and have always been large buyers and holders of gold and silver. Together, India and China absorb close to 50% of total world gold and silver mine production.

One big difference between India and China is that the gold and silver buying in India is largely a grassroots phenomenon, emanating from the general population due to deep-rooted customs and traditions; where the buying from China is predominantly from official sources (similar to the gold buying by Russia). To me, this makes the gold and silver buying from India more “free market” and price-sensitive in nature because the more participants in any market, the freer the market is by definition. The many tens and even hundreds of millions of gold and silver buyers from India make the markets there the freest of all.

India has always played a vital role in gold and silver. I remember how my longtime friend and silver mentor, Izzy Friedman, more than 40 years ago, as he was deciding whether to make a major investment in silver in the mid-1970’s, actually flew to India to see for himself if the stories of great silver hoards about to flood the market should prices move higher (from $4 or $5) were true. Izzy saw plenty of silver, but none so closely held in large concentrated quantities to pose a market threat. I believe that’s still the case today.

Indian gold and silver buyers are quite price-sensitive and unlike the typical buyer in the West, Indians tend to buy more when prices are low and less when prices are high. Gold and silver flows into India are one-way affairs – what flows in stays there, never to leave the sub- continent. Gold prices are closer to the highest they have been over the past 5 or 6 years, while silver prices are closer to the lowest they have been over that period, resulting in the silver/gold price ratio widening out to the highest it has been in 25 years. I reviewed the import data from India over the past 15 years with that in mind. For silver, I relied on the Silver Institute’s World Survey and for gold, a straight Google search for Indian imports from 2004 to 2018.

Here’s what I found. The people of India, according to the import data, are buying more silver relative to gold than ever before. It’s not that gold imports are down sharply, it’s much more that silver imports are up sharply. I broke the data from the past 15 years into two segments – the 9 years from 2004 to 2012 and the six years from 2013 to 2018. As a reminder, by comparing the imports of gold and silver on a per ounce basis, all outside influences are neutralized, like currency and overall economic conditions. For instance, the great Indian demonetization of 2016, resulted in sharp declines in the imports of both gold and silver. That’s the objective beauty of making like-kind comparisons – it filters out peripheral issues.

For the 9 years 2004 to 2012, the silver/gold price ratio averaged 56 to 1 and India imported an average of 26.5 million ounces of gold and 85 million ounces of silver each year – or 3.2 times more ounces of silver than gold. Over the next 6 years 2013 to 2018, the silver/gold price ratio widened out to 73 to 1, with silver getting progressively cheaper relative to gold (except in 2016). Over the most recent six years, gold imports fell slightly to an average annual 25.2 million oz, while silver imports surged to 188 million oz annually, up 120% over the yearly average of the prior 9 years. Where imports of silver compared to gold in ounces were 3.2 times from 2004 to 2012, they jumped to 7.5 times from 2013 to 2018.

In the most recent full year of import data, 2018, India imported 24.4 million ounces of gold, the second lowest amount in 9 years, while silver imports were 224 million ounces, the second highest total in 15 years. The amount of silver ounces imported to India last year was more than 9 times the amount of gold imported, the highest level ever. The average silver/gold price ratio for 2018 was 82 to 1, the cheapest silver had been to gold in 15 years, so it’s not surprising that Indian buyers reacted as they did. Of course, while full year data is not available for 2019, the silver/gold price ratio has averaged 86 to 1 year to date, with very recent readings of 90 to 1.

Considering that the silver/gold price ratio has continued to widen out since 2018, exceeding 90 to 1, making silver even cheaper compared to gold, there is every reason to expect that India’s imports of silver have continued to grow, both on an absolute and relative basis compared to gold. What this means, aside from confirming the price-sensitivity (and good sense) of the Indian buyer, is that prices do have consequences. It’s often said that the cure for low prices is low prices because low prices discourage production and encourage demand. The record of India’s silver imports would seem to be clear confirmation of that.

The main price consequence of the surge in silver imports to India is as a direct result of the COMEX price suppression and manipulation of the price. The collective investment reaction in the US and West to the low price of silver (or any investment asset) is not to buy – that’s our investment culture, for better or worse. The collective reaction in India is markedly different and in a very real sense is the ultimate confirmation that silver prices have been manipulated; as what else could prove more conclusively that silver prices were artificially suppressed than the surge in demand from India?

In fact, had there been no surge in demand from India, that would be proof silver wasn’t manipulated in price. What else could possibly explain the surge in silver demand from tens of millions of Indian buyers if not that they felt prices were depressed – not just on an absolute basis, but relative to gold as well? I’m not suggesting that the many millions of Indian buyers are at all aware of the COMEX price manipulation; they just know that silver is unusually cheap and undervalued relative to gold.

So here we have compelling new proof that silver prices have been manipulated – not that more proof was needed. By depressing the price of silver, JPMorgan may have succeeded in discouraging western investment demand and cornering the physical market for its own accumulation, but has also inadvertently stimulated Indian demand. As a result, a brand new Catch-22 has emerged in silver. As and when JPMorgan decides to let silver prices fly to the upside, it is reasonable to assume that Indian demand would fall off, but as that demand falls off, the higher prices will jumpstart western demand. If the right hand doesn’t get you, then the left hand will. Should JPM choose to prolong the silver price suppression, the imports to India should continue to surge and with the concurrent decline in world silver mine production, a physical crunch becomes inevitable. Prices do have consequences. – Ted Butler

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9267/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9374 /shanghai bourse CLOSED UP 2.54 POINTS OR 0.09%

HANG SANG CLOSED UP 271,61 POINTS OR 1.00%

2. Nikkei closed DOWN 151.79 POINTS OR 0.72%

3. Europe stocks OPENED GREEN/

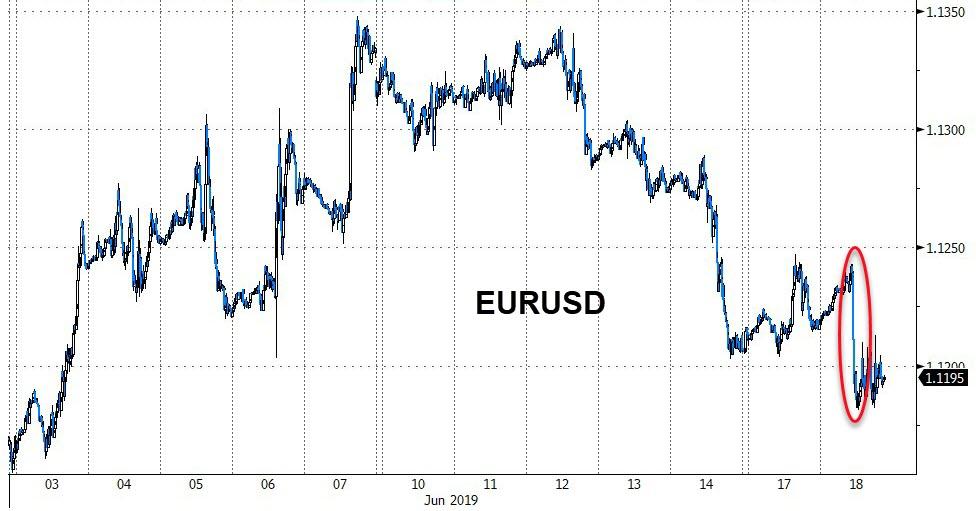

USA dollar index UP TO 97.69/Euro FALLS TO 1.1191

3b Japan 10 year bond yield: FALLS TO. –.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.24/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.89 and Brent: 60.75

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

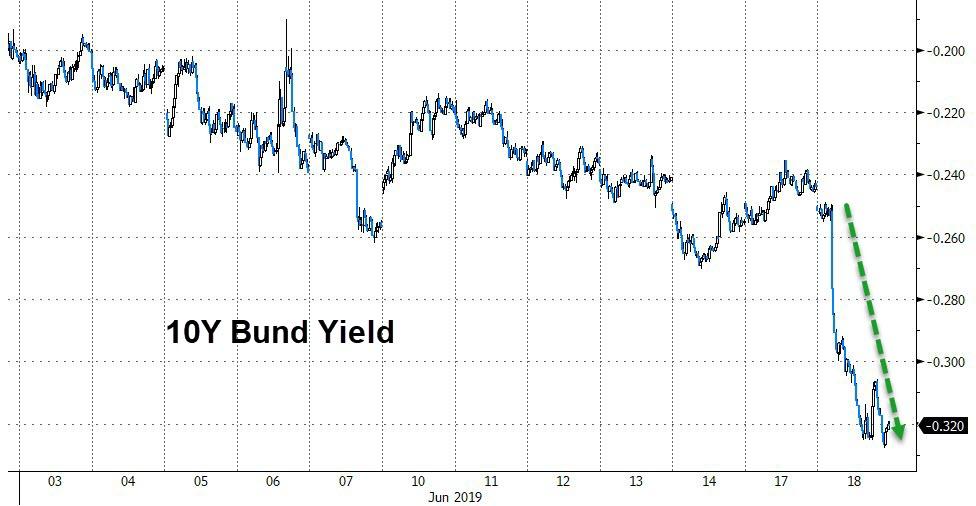

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.32%/Italian 10 yr bond yield DOWN to 2.12% /SPAIN 10 YR BOND YIELD DOWN TO 0.42%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.44: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 2.52

3k Gold at $1350.70 silver at: 14.97 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 6/100 in roubles/dollar) 64.25

3m oil into the 51 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.34 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9993 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1182 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.32%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.02% early this morning. Thirty year rate at 2.52%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8358..

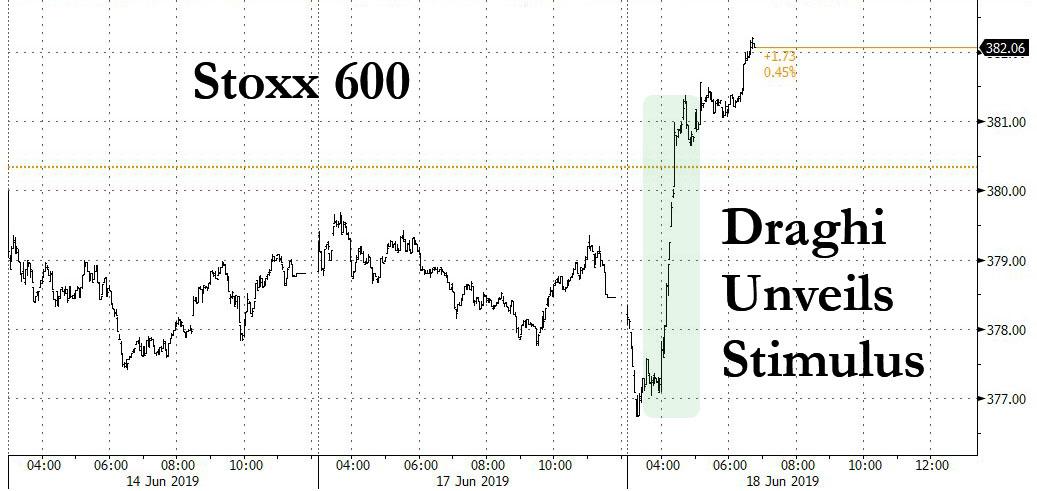

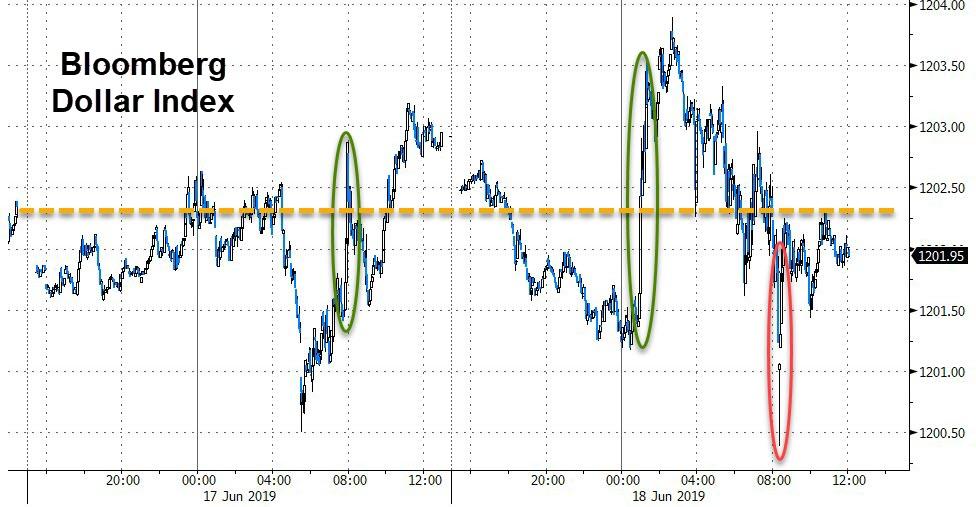

Draghi Unleashes Global Chaos With Preview Of More Stimulus, Prompts Angry Response From Trump

It was shaping up as a slow, boring session with everyone waiting “patiently” for the Fed tomorrow, until right after the European open, when two years after Mario Draghi first laid out the blueprints for the ECB’s rate normalization with a speech about the Eurozone’s “strengthening and broadening recovery” at the ECB’s Sintra forum in 2017, the ECB president finally threw in the towel and said that if the outlook doesn’t improve and inflation doesn’t strengthen, “additional stimulus will be required” adding that the ECB can amend its forward guidance, that rate cuts remain “part of our tools” and asset purchases are also an option. In short, full dovish capitulation by the ECB chief, which in a market addicted to monetary stimulus, was just what the bulls needed to hear.

The news sent global stocks surging…

… the Stoxx 600 rebounding from a loss to a gain of over 1%…

… S&P futures up 14 points, and back over 2,900…

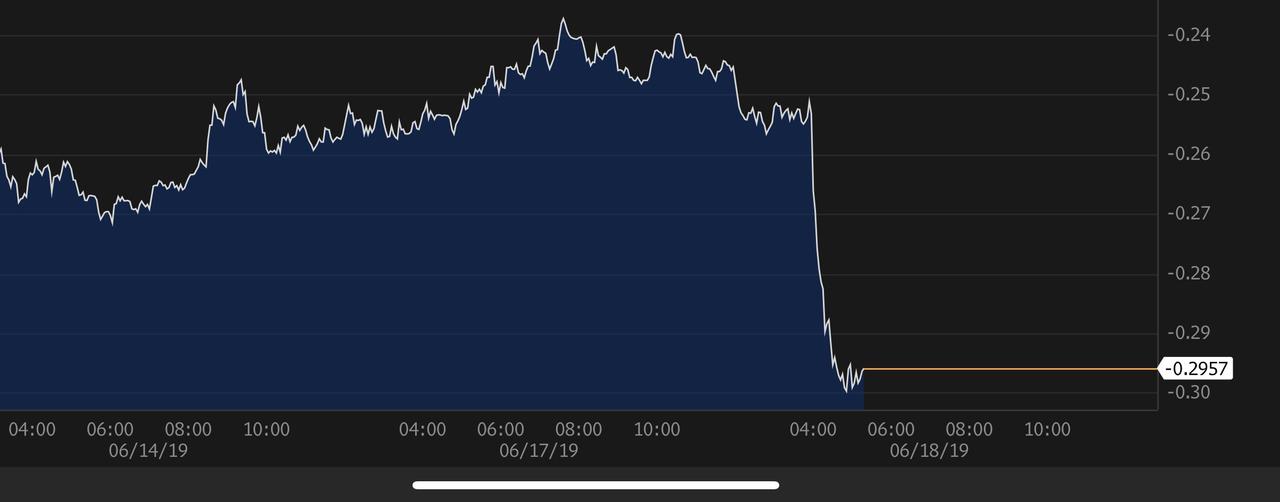

… the German 10Y Bund yield tumbling to an all time record low below -0.30%...

Amusingly, Draghi’s somewhat striking admission of defeat, prompted an immediate response from none other than the US president, who tweeted “Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others”…

Donald J. Trump

✔@realDonaldTrump

Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others.

… then immediately followed by “European Markets rose on comments (unfair to U.S.) made today by Mario D!”

Donald J. Trump

✔@realDonaldTrump

European Markets rose on comments (unfair to U.S.) made today by Mario D!

This in turn served to push the Euro slightly higher, recovering some of its losses, as Trump’s warning was interpreted as a threat of more Eurozone tariffs, or alternatively, more pressure on the Fed to cut rates…

… as the final race to the bottom emerges, and looks as follows:

- ECB unveils more easing

- Trump threatens ECB, responds with Eurozone tariffs

- ECB unveils even more easing

So with all these fireworks taking place in just a few short hours, what else happened?

Well, earlier, Japan’s Topix slipped, even as most Asian gauges rose. With European sovereign bonds soaring, led by Italy and Greece, while the Swedish and Austrian 10Y yield dropped below 0% for the first time, as fuel was added to the fire by a report that investor confidence in Germany’s economic outlook worsened dramatically in June…

… US 10Y Yields plunged to new lows, and just 3.2bps away from a 1-handle!

Of course, Draghi isn’t even the main event. Traders were far more focused on what the Federal Reserve announces on Wednesday to see whether Chairman Jerome Powell and his colleagues will validate widespread expectations for interest-rate cuts. The ECB’s announcement may just have changed the calculus.

In currencies, the Bloomberg Dollar Spot Index erased declines as the euro first fell below $1.12, then rebounded above it. Money markets are pricing in a 10bps cut by December from the European Central Bank after President Mario Draghi emphasized the need for stimulus. The kiwi dollar led gains in the Group-of-10 currencies, while the yen was boosted from demand versus the Aussie after RBA’s latest minutes showed more easing is likely

In commodities, oil dropped, with OPEC nations still unable to agree on a date for their next meeting, adding to uncertainty over whether production cuts would be extended.

Expected data include housing starts and building permits. Adobe is among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.5% to 2,911.00

- STOXX Europe 600 up 0.6% to 380.85

- MXAP up 0.3% to 154.95

- MXAPJ up 0.6% to 507.49

- Nikkei down 0.7% to 20,972.71

- Topix down 0.7% to 1,528.67

- Hang Seng Index up 1% to 27,498.77

- Shanghai Composite up 0.09% to 2,890.16

- Sensex up 0.4% to 39,102.96

- Australia S&P/ASX 200 up 0.6% to 6,570.00

- Kospi up 0.4% to 2,098.71

- German 10Y yield fell 5.0 bps to -0.294%

- Euro down 0.2% to $1.1191

- Italian 10Y yield fell 4.8 bps to 1.933%

- Spanish 10Y yield fell 6.8 bps to 0.458%

- Brent futures down 0.7% to $60.54/bbl

- Gold spot up 0.4% to $1,345.06

- U.S. Dollar Index up 0.1% to 97.68

Top Headline News from Bloomberg

- ECB’s Draghi said if the outlook doesn’t improve, and inflation doesn’t strengthen, “additional stimulus will be required.” He noted that the ECB can amend its forward guidance, that rate cuts remain “part of our tools” and asset purchases are also an option. He was speaking at the ECB’s annual forum in Sintra, Portugal

- Bond investors are preparing for another wave of QE from the ECB by returning to some of their favorite post-crisis trades. First up: buy the debt of nations such as France that have greater scope for purchases by the ECB. Next, bet on a drop in longer-maturity yields relative to near-term rates. Then go for higher-returning bonds, like Spain and Italy

- Investor confidence in Germany’s economic outlook worsened dramatically in June after the Bundesbank predicted the economy will shrink this quarter. An index measuring prospects for the next six months fell to -21.1 in June, a far worse reading than the -5.6 economists expected

- President Donald Trump’s top trade envoy Robert Lighthizer will be in the congressional hot seat for two days this week, giving lawmakers the chance to grill him about the prospects for a deal with China, as well as various punitive measures threatened by his boss

- Hong Kong leader Carrie Lam personally apologized for backing a bill that would allow extraditions to China for the first time, her latest move to try and defuse protests that have rocked the city

- Australia’s central bank is likely to lower interest rates again to drive increased hiring and boost households’ confidence that inflation will return to target. RBA says further rate cut ‘more likely than not’ in period ahead

- China cut its U.S. Treasury holdings to the lowest in almost two years as the months-long trade conflict dragged on between the world’s two largest economies. The nation’s holdings of notes, bills and bonds declined by $7.5 billion in April to $1.11 trillion, according to Treasury Department data released on Monday

- Rory Stewart, the rank outsider in the contest to become Britain’s next leader, is suddenly winning support and giving his bigger-name rivals a reason to worry. Officials working for three better-known contenders privately said they believed Stewart could deliver a major upset in the Conservative Party leadership votes this week

- The U.K. economy will probably flatline in the second quarter and the Bank of England won’t raise interest rates until well into next year, according to a Bloomberg survey

Asian equity markets mostly saw cautious gains ahead of this week’s key risk events and following the marginal gains in the US where trade was otherwise uneventful aside from the strength in tech and telecoms. ASX 200 (+0.6%) and Nikkei 225 (-0.7%) were mixed with Australia led higher by tech and commodity related sectors, in which government plans to introduce a AUD 158bln income tax cut package, as well as anticipation for further RBA policy easing, added to the optimism. Tokyo sentiment was hampered by a firmer currency. Hang Seng (+1.0%) outperformed as business returned to normal following the recent protests and the Shanghai Comp. (+0.1%) was indecisive despite continued PBoC liquidity efforts, as trade uncertainty lingered after economic regulators refused to rule out using rare earths in the trade dispute and the Global Times Editor suggested the potential for a protracted trade war. Finally, 10yr JGBs initially traded steady amid the indecisiveness in the region but were later supported as sentiment in Japan further deteriorated and after the 5yr auction results showed a decline in yields and higher accepted prices from the prior month.

Top Asian News

- China Cuts Treasury Holdings to Two-Year Low Amid Trade War

- China’s Trade War Has Investors Flocking to Consumer Stocks

- Metro Pacific Said Preparing to Start $2 Billion Hospital Sale

European equities are higher across the board [Eurostoxx 50 +1.2%] as the region was bolstered by a dovish Draghi. The DAX (+1.2%) is now back above the 12k level after having visited a pre-Draghi low of 11,986, albeit gains are somewhat limited by a subdued IT sector, meanwhile, the FTSE 100 lags as the index fails to benefit from Draghi’s speech. In terms of sectors, financial names underperform amid the prolongation of negative rates. Defensive sectors are outperforming with healthcare and utilities the standout outperformers. Movers to the downside today include chipmakers following a profit warning from Siltronic (-13.0%) , citing US-China trade issues. The downbeat market outlook spilled onto STMicroelectronics (-2.0%), ASML (-1.2%) and Infineon (-5.7%), albeit the latter is more influenced by the launch of a capital increase to fund the Cypress Semiconductor acquisition. Finally, Lufthansa shares rest near the foot of the Stoxx 600 following three separate broker downgrades.

Top European News

- Canary Wharf Group Is Said in Talks to Buy CapCo’s Earls Court

- Tieto to Buy Evry for $1.5 Billion in Nordic Software Tie- Up

- German Highway Toll Ruled Illegal and Discriminatory by EU Court

- Weidmann Waits as Merkel’s Candidate for Juncker Job Falters

In currencies, The EUR currency has slumped to the bottom of the G10 pile and even below the Aussie that was hit overnight by RBA minutes flagging further easing on the basis that benign inflation and wage trends are likely to persist for even longer. In similar vein, ECB President Draghi used the stage at Sintra to deliver a much more dovish/downbeat assessment of price developments and all but signalled another tweak to official guidance at the next policy meeting, if not further stimulus. In short, he acknowledged the recent pronounced drop in inflation expectations and said the GC will look at measures to counter the severity of risks to price severity in coming weeks, and if the situation fails to improve more stimulus will be needed. Eur/Usd has reversed from circa 1.1240 to just over 1.1180 and through 2.1 bn option expiries between 1.1195-1.1205 that may yet influence direction into the NY cut, while Eur/Gbp has pulled back sharply from around 0.8975 to 0.8925. Back down under, Aud/Usd is hovering off 0.6832 lows and Aud/Nzd has reversed towards 1.0500 as the Kiwi keeps tabs on the 0.6500 handle vs its US counterpart ahead of the latest GDT auction and NZ Q1 current account data.

- CAD/CHF/GBP – All weaker vs the Greenback and partly in sympathy with the Euro and Aussie, but the Loonie also had more negative Chinese-Canadian headlines to digest as Beijing suspended pork imports pending closer inspection of the product. Meanwhile, the Franc slipped through parity, but strengthened in Eur/Chf cross terms to 1.1175 at one stage and will do doubt arouse SNB attention given that the ECB seems to be on the brink of easing further (-10 bp now priced in for December). Elsewhere, Cable is now eyeing 1.2500 and very early January lows after breaching key support at 1.2560, with the next leg of the Tory leadership race looming before UK CPI, retail sales and the BoE unfolds tomorrow and Thursday.

- JPY/NOK/SEK – The major outperformers, as the Yen regains a safe-haven bid to retest support ahead of 108.00, while the Scandi Crowns benefit from single currency weakness and ECB-Norges Bank/Riksbank policy divergence given a widely expected hike from the former on Thursday. Moreover, the Sek derived some traction from a cautiously upbeat Riksbank business survey and significantly improved 2019 budget surplus forecasts from the SNDO. Eur/Nok around 9.7780 vs 9.8170 at one stage and Eur/Sek holding within a 10.6484-6147 range.

- EM – Although the Buck has rebounded firmly, if not quite uniformly as noted above (back over 97.500), the Lira has maintained recovery momentum with the aid of some rare constructive comments on the US-Turkey front and reports that talks about the S-400 deal will be held at NATO next week. Usd/Try trading near the base of a 5.8225-8777 band.

In commodities, WTI and Brent futures are lower on the day with the former just above the USD 51.50/bbl level whilst the latter hovers around the USD 60.50/bbl mark. News-flow for the complex was largely surrounding OPEC this morning, with WSJ noting that Saudi intends to push for tighter compliance to OPEC production curbs. Sources also stated that the renewed pact would see the under-complying countries reducing crude supply by 300-400k BPD. In terms of a date, IFX reported that Moscow has reportedly agreed to consider an OPEC+ meeting on July 12th, postponed from the scheduled June 25/26. Looking ahead, traders will be keeping an eye on tonight API inventory release with the street looking for a draw of around 1.75mln barrels. Elsewhere, gold is hovering near intraday highs amid a bout of demand for the safe haven asset. Meanwhile, copper prices are supported despite the underlying risk off tone in the market as Glencore has shut down its Mufulira copper smelter at its Mopani copper mine in Zambia whilst Chile’s Codelco said the Chuquicamata copper mine maintained output capacity at 50% due to the 4th full day of a union strike.

US Event Calendar

- 8:30am: Housing Starts, est. 1.24m, prior 1.24m; MoM, est. 0.4%, prior 5.7%

- 8:30am: Building Permits, est. 1.29m, prior 1.3m; MoM, est. 0.23%, prior 0.6%

DB’s Jim Reid concludes the overnight wrap

I’m still in NY and last night I FaceTimed home to find there had been a big furniture delivery. No, not for our new house, but for my daughter’s new dolls house. I bought what I thought was a very good value but nice one only to find that the real money has to be spent furnishing it. It comes completely undecorated and bare. I had a bit of a shock when I saw how much all the trappings to go inside cost. So yesterday a four poster bed, a dining table and various kitchen appliances arrived. Then we spent most of the rest of the conversation debating whether we should also buy dolls house wallpaper! There is part of me that wondered whether I imagined this conversation in some kind of surreal jet lag haze but alas it was only too real.

It was a bit of a sleepy first day of the new week for markets yesterday with fairly minimal news flow to trade off. The good news, however, is that we’ve got a full day of the ECB Forum in Sintra ahead of us and today’s agenda includes an introductory speech from Draghi this morning, comments from various ECB officials including Guindos, Praet, Lane and Coeure, and then a policy panel featuring Draghi, the BoE’s Carney and former Fed Vice Chair Fischer this afternoon. It remains to be seen what will come of the Forum; however, as we mentioned yesterday, we have seen markets move sharply in previous years following comments that emerged from Sintra and with there being plenty of chatter about potentially more stimulus coming from the ECB, it’s worth watching it closely. In his opening remarks last night, Draghi declined to discuss policy or the current outlook, instead keeping his comments focused on the conference and on introducing Olivier Blanchard, who used his keynote address to argue for greater use of fiscal policy in the next downturn; an unusual topic for a central banking conference!

Ahead of the conference yesterday, comments from the ECB’s Coeure attracted a bit of attention following an interview with the FT. Coeure highlighted the dilemma the ECB faces with market pricing, saying that the ECB should neither ignore it nor blindly follow it. Most notably, Coeure said the costs associated with easing policy should not deter the ECB from acting – while also going on to mention rate cuts and the impact of NIRP on banks. In addition to those potential tools, he cited QE and forward guidance as other options. Coeure acknowledged the existing limits on bond-buying, but emphasized that the limits were chosen by the ECB, not by the ECJ or some other outside force, thus hinting that they could be modified. In a similar vein to Blanchard last night, he hinted at the frustration at the lack of fiscal policy from those that could potentially do it. This lack of action might force the ECB to do more in the future, which in turn would magnify the potential lower for longer problem.

With the exception of BTPs – which rallied -4.8bps on minimal news – bond markets were slightly weaker yesterday with 10y Bunds up +1.2bps in yield to the lofty heights off -0.247%. Similarly, Treasuries were +1.4bps higher although they did see a slight rally on the back of a shockingly weak empire manufacturing reading – the biggest monthly decline ever in fact. We’ll have more on that below. That being said, equity markets didn’t appear too fussed with the NASDAQ leading the charge following a +0.62% bounce. FANGS led the way with the NYSE FANG index up +1.75%, though the Philly semiconductor index retreated -0.64%, as cyclical sectors more broadly underperformed. Banks retreated -1.00% and the DOW transports index fell -1.03%. Elsewhere, the S&P 500 (+0.09%) and the STOXX 600 (-0.09%) were both little changed. HY credit spreads were -2bps tighter in the US, while the dollar traded flat. EM currencies were flat as well, while EM equities fell -0.36%.

This morning in Asia markets have mostly followed the lead from Wall Street; however, the exception is the Nikkei, which is down -0.70% after BoJ Governor Kuroda said that the “risks to the global economy are tilted to the downside”. A reminder that the BoJ meeting is this Thursday. Elsewhere the Hang Seng (+0.73%), Kospi (+0.38%) and Shanghai Comp (+0.08%) are all up. In other news, Chinese holding of US Treasuries are continuing to decline with the US Treasury Department data released yesterday highlighting that China’s holdings of US notes, bills and bonds declined by $7.5bn in April to $1.1tn, the lowest since June 2017.

Staying with Asia, yesterday news also broke that President Xi will travel to North Korea on June 20-21, the first time a Chinese leader has made the trip in 14 years. It is possible that North Korea talks are another arena of the US-China confrontation, so developments there could reverberate back onto the tariff war. Separately, Chinese tech giant Huawei said that the new Western sanctions will cost them around $30bn this year and next, as they anticipate 40-60mn fewer smartphone sales this year. While many countries have not joined the US in sanctioning the company, the threat and uncertainty surrounding the firm is enough for many major wireless providers to opt not to carry Huawei’s newest phone model. This was the first time that the company quantified the impact of the US’s sanctions, and the new information was worse than expected.

Also on the trade front, it’s worth keeping an eye on any headlines that could potentially emerge from US Trade Representative Lighthizer’s testimony before Congress today. While the aim of the testimony is to campaign to get Congress to approve the US-Mexico-Canada trade agreement, there’s a reasonable chance that US-China trade issues also get brought up. So that should be worth a watch.