GOLD: $1345.15 DOWN $1,85 (COMEX TO COMEX CLOSING)

Silver: $14.98 DOWN 3 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1360.50

silver: $15.16

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 8/19

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,346.600000000 USD

INTENT DATE: 06/18/2019 DELIVERY DATE: 06/20/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

624 C BOFA SECURITIES 7

661 C JP MORGAN 8

737 C ADVANTAGE 19 4

____________________________________________________________________________________________

TOTAL: 19 19

MONTH TO DATE: 2,133

I wrote the following in yesterday’s commentary;

“TOMORROW IS THE BIG FOMC MEETING. DRAGHI PREEMPTED POWELL TODAY BY UNLEASHING POSSIBLE QE IN EUROPE

HERE ARE THE KEY PRICES OF GOLD AND SILVER TO WATCH FOR:

GOLD: $1350. THIS LEVEL IS IMPORTANT FOR THE BANKERS AND NO DOUBT HUGE DERIVATIVE TRADES WERE INITIATED HERE. THE BANKERS WILL DEFEND THEIR LIVES AT THIS LEVEL. GOLD HAS BEEN BEATEN BACK AT LEAST 6 TIMES ONCE GOLD PIERCED $1350. (check!/price surpassed)

SILVER: $15.06. MANY ARE COMMENTING ON $15.00 BUT THE REAL PRICE TO WATCH IS $15.06 AS THIS WAS THE PRICE THAT SILVER WAS BEATEN BACK DOWN INTO THE LOW 14 DOLLAR LEVEL. A PIERCING OF 15.06 WILL CREATE NIGHTMARE FOR OUR BANKERS. (check!!price surpassed)

STAY TUNED FOR TOMORROW..IT WILL BE A BIG DAY.”

it sure was!!!..

Now we watch for the banking derivatives on gold and silver to blow up!

your data…

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT: 19 NOTICE(S) FOR 1900 OZ (0.3701 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2133 NOTICES FOR 213,300 OZ (6.6345 TONNES)

SILVER

FOR JUNE

38 NOTICE(S) FILED TODAY FOR 190,000 OZ/

total number of notices filed so far this month: 391 for 1955,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9111 UP 28

Bitcoin: FINAL EVENING TRADE: $ 9116 UP 32

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A HUMONGOUS SIZED 6469 CONTRACTS FROM 232,997 UP TO 239,466 ACCOMPANYING THE 18 CENT RISE IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR GOLD . HOWEVER WE ARE WITNESSING A RISE IN SPREADING ACCUMULATION BY THE BANKERS IN SILVER)..TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 1300 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1300 CONTRACTS.

WITH THE TRANSFER OF 1330 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1300 EFP CONTRACTS TRANSLATES INTO 6.50 MILLION OZ ACCOMPANYING:

1.THE 18 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.960 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

33,829 CONTRACTS (FOR 13 TRADING DAYS TOTAL 33,829 CONTRACTS) OR 169.145 MILLION OZ: (AVERAGE PER DAY: 2602 CONTRACTS OR 13.01 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 169.145 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.16% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1039.90 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6469, WITH THE 18 CENT RISE IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1300 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED AN ATMOSPHERIC SIZED: 8128 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1300 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 6469 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 3 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $14.98 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.199 BILLION OZ TO BE EXACT or 171% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 38 NOTICE(S) FOR 190,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.960 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD VERY STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE SHARPLY WITH THE GOOD GAIN OF 18 CENTS.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A FAIR 2295 CONTRACTS, TO 525,636 WITH THE STRONG $7.60 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE ACCUMULATION PHASE OF THEIR OPERATION. THUS THE GAIN IN OI IS REAL AS INVESTORS ARE POURING INTO THE GOLD SECTOR

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7659 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 8495 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 525,636. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,790 CONTRACTS: 2295 CONTRACTS INCREASED AT THE COMEX AND 8495 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,790 CONTRACTS OR 1,079,000 OZ OR 33.56 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $7.60 IN GOLD TRADING….AND WITH THAT REASONABLE GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 33.56 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 117,778 CONTRACTS OR 11,777,800 oz OR 366.33 TONNES (13 TRADING DAYS AND THUS AVERAGING: 9059 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 366.33 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 366.33/3550 x 100% TONNES =10.31% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,617.81 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED INCREASE IN OI AT THE COMEX OF 2295 WITH THE PRICING GAIN THAT GOLD UNDERTOOK ON YESTERDAY($7.60)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8495 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8495 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED GAIN OF 10,790 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8495 CONTRACTS MOVE TO LONDON AND 2295 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 33.56 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED WITH A GOOD GAIN IN PRICE OF $7.60 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 19 notice(s) filed upon for 1,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.65 TODAY//

INVENTORY RESTS AT 764.10 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 3 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 319.07 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 6469 CONTRACTS from 232,997 UP TO 239,466 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 1300 CONTRACTS FOR AUGUST: 0, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1300 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 6469 CONTRACTS TO THE 1300 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC GAIN OF 7769 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 38.85MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 2.960 MILLION OZ FOR JUNE.

RESULT: A HUGE INCREASE IN SILVER OI AT THE COMEX WITH THE 18 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1300 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 27.65 POINTS OR 0.96% //Hang Sang CLOSED UP 703.37 POINTS OR 2.56% /The Nikkei closed UP 361.16 POINTS OR 1.72%//Australia’s all ordinaires CLOSED UP 1.21

/Chinese yuan (ONSHORE) closed UP at 6.9043 /Oil UP TO 3.83 dollars per barrel for WTI and 61.72 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.9243 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9068 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/APPLE/

This is not good for China as Apple now plans to shift up to 30% of production outside of China. The tariffs wars are certainly having their effect

( zerohedge)

4/EUROPEAN AFFAIRS

i)GERMANY/ECB/EUROPE

Jim Grant of Grant’s Interest Rate Observer notes the comments from the CEO of Germany’s 2nd largest bank: “In a few years we will notice that the ECB experiment was a historical mistake”

(Jim Grant)

ii)ITALY

Tensions are boiling with the MIn BOT issue

( Mish Shedlock/Mishtalk)

iii)EUROPE/USA/JAPAN

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)TURKEY/USA

The Turkish lira plummets as Trump and allies are ready to impose sanctions on a crippled Turkey economy. They are going to target the big Turkish companies with sanctions against doing business with the west.

this is deadly..

(courtesy zerohedge)

6. GLOBAL ISSUES

CANADA

Strange: the Loonie spikes higher after Cdn core inflation soars to 10 yr highs. The view is that the North is emerging from its growth slowdown…I beg to differ..

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

i)Bill Murphy explains the significance of $1350 gold

( Bill Murphy/GATA/Reluctant Preppers)

ii)GOOD NEWS!! Robert Labourne our resident expert on BIS affairs reports a huge decline in gold activity via gold swaps. I guess the reason is the lack of gold.

( Robert Lambourne/GATA)

iv)Chris Marcus is interviewing me:

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

iii)USA ECONOMIC/GENERAL STORIES

a) Let us see if Michael Every is right as Powell might have to explain why he is cutting rates just like Draghi is scheduled to do.

( Michael Every/Rabobank)

b)Illinois farming is now in a mess as farmers have given up on planting corn

( Mac Slavo/SHFTPlan.com)

c)Interesting: 25% of Americans are now :”worse off” than they were before the great recession. Kind of kills the Trump narrative that the economy is booming

( Mac Slavo)

d).My goodness: they finally agree on something…a deal on Trump border funding

SWAMP STORIES

A democrat Congressman states that Mueller will testify. I extremely doubt it. It will be far worse for the democrats.

(zerohedge)

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 295.584 oz oz

FOR THE JUNE 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 19 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE /2019. contract month, we take the total number of notices filed so far for the month (2133) x 100 oz , to which we add the difference between the open interest for the front month of JUNE. (195 contract) minus the number of notices served upon today (19 x 100 oz per contract) equals 230,900 OZ OR 7.182 TONNES) the number of ounces standing in this active month of JUNE

Thus the INITIAL standings for gold for the JUNE/2019 contract month:

No of notices served (2133 x 100 oz) + (195)OI for the front month minus the number of notices served upon today (19 x 100 oz )which equals 230,900 oz standing OR 7.182 TONNES in this active delivery month of JUNE.

We GAINED 27 contracts or an additional 2700 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly.!!

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.08 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 7.182 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 304.040 million oz

The total number of notices filed today for the JUNE 2019. contract month is represented by 38 contract(s) FOR 190,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE, we take the total number of notices filed for the month so far at 391 x 5,000 oz = 1,955,000 oz to which we add the difference between the open interest for the front month of JUNE. (71) and the number of notices served upon today (38 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 391(notices served so far)x 5000 oz + OI for front month of JUNE( 71) -number of notices served upon today (38)x 5000 oz equals 2,120,000 oz of silver standing for the JN contract month.

WE LOST 93 CONTRACTS OR AN ADDITIONAL 465,000 OZ WILL STAND AT THE COMEX AS THESE GUYS MORPHED INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO ACCEPTING A FIAT BONUS. THIS IS THE FIRST TIME EVER THAT I CAN RECALL SEEING A MASSIVE CHANGE IN THE FRONT MONTH PRELIMINARY OI NUMBER TO THE FINAL NUMBER. IT MEANS THAT THE GUYS STANDING FOR METAL ON THIS SIDE OF THE POND JUST GAVE UP AND THEY WILL TRY THEIR LUCK OVER IN LONDON..

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 85,123 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 132,072 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 132,072 CONTRACTS EQUATES to 660 million OZ 94.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.77% (June 19/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.97% to NAV (june 19/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -1.77%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.43 TRADING 12.80/DISCOUNT 4.69

END

And now the Gold inventory at the GLD/

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

MAY 21/WITH GOLD DOWN $3.65 TODAY: A SURPRISE 2.00 TONNES WERE ADDED TO THE GLD GOLD INVENTORY//INVENTORY RESTS AT 738.17 TONNES

MAY 20/WITH GOLD UP $1.00 A HUGE 2.96 TONNE DEPOSIT INTO THE GLD//INVENTORY RESTS AT 736.17 TONNES

MAY 17/WITH GOLD DOWN $9.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 733.23 TONNES

MAY 16/WITH GOLD DOWN $11.50: A WITHDRAWAL OF 3.23 TONNES FROM THE GLD//INVENTORY RESTS AT 733.23 TONNES

MAY 15/WITH GOLD UP $1.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 736.46 TONNES

MAY 14//WITH GOLD DOWN $5.45 TODAY: STRANGE!! THE CROOKS DECIDED TO DEPOSIT A HUGE 3.23 TONNES INTO THE GLD INVENTORY//INVENTORY RESTS AT 736.46 TONNES

MAY 13/ WITH GOLD UP ANOTHER $15.40 TODAY: STRANGE! A MASSIVE WITHDRAWAL OF 6.41 TONNES OF GOLD (TO TAME GOLD’S RISE TODAY)/INVENTORY RESTS AT 733.23 TONNES

MAY 10 WITH GOLD UP $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 9//WITH GOLD UP $4.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 8/WITH GOLD DOWN $3.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 739.64 TONNES

MAY 7/ WITH GOLD UP $1.80: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 6/WITH GOLD UP $2.35: ANOTHER WITHDRAWAL OF 5.88 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 3/WITH GOLD UP $9.35 TODAY: A WITHDRAWAL OF 1.17 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 745.52

MAY 2/WITH GOLD DOWN $12.30 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

MAY 1/WITH GOLD DOWN $1.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 19/2019/ Inventory rests tonight at 764.10 tonnes

*IN LAST 613 TRADING DAYS: 169.66 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 513 TRADING DAYS: A NET 4.03TONNES HAVE NOW BEEN REMOVED FROM THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 17/WITH SILVER UP 1 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

june 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

jUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

MAY 17/WITH SILVER DOWN 13 CENTS TODAY: A BIG CHANGES IN SLV: A WITHDRAWAL OF 3.185 MILLION OZ FROM THE SLV INVENTORY VAULTS:/INVENTORY RESTS AT 312.366 MILLION OZ//

MAY 16/WITH SILVER DOWN 26 CENTS: NO CHANGES IN THE SLV INVENTORY//INVENTORY RESTS AT 315.551 MILLION OZ//

MAY 15/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SLV INVENTORY: A WITHDRAWAL OF 1.031 MILLION OZ// THE SLV/INVENTORY RESTS AT 315.551 MILLION OZ.

MAY 14/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV. INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 13//WITH SILVE5 DOWN 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ…

MAY 10/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 9/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 8/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 7/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 6/WITH SILVER DOWN 3 CENTS WE HAD ANOTHER DEPOSIT OF 891,000 OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 3//WITH SILVER UP 34 CENTS TODAY: A DEPOSIT OF 843,000 OZ INTO THE SLV/TOTAL INVENTORY RESTS AT 315.691 MILLION OZ//

MAY 2/WITH SILVER DOWN ANOTHER 13 CENTS, MIRACUOUSLY THE AUTHORITIES ADD 2.869 MILLION OZ OF SILVER BACK INTO THE SLV/INVENTORY RESTS AT 314.848 MILLION OZ//

MAY 1/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ////

Gold Rises In All Currencies – Gains 1.6% To £1,079/oz In GBP, Near 7 Year High

GoldCore Note

Gold prices have risen in all currencies today and especially in British pounds with gold having risen 1.5% to £1,078/oz. Concerns regarding the weak UK economy and Brexit fears continue to weigh on sterling.

More loose monetary policies are making gold attractive again as are the elevated economic and geopolitical risks which are leading to safe haven demand.

Gold has gained more than 6%, since touching a 2019 low of $1,265.85 in early May, due to these risks.

Gold had seen its usual Monday sell off as futures market participants took profits and pushed prices lower again.

The U.S. central bank is expected to leave borrowing costs unchanged this time but possibly lay the groundwork for a rate cut later this year which will support gold.

Expectations of interest rate cuts in the U.S. have increased amid the deepening U.S.-China trade war and signs that the U.S. economy is slowing significantly.

LBMA Gold Prices (USD, GBP & EUR – AM/ PM Fix)

17-Jun-19 1333.20 1341.30, 1059.49 1065.13 & 1188.81 1193.09

14-Jun-19 1352.45 1351.25, 1069.79 1070.33 & 1200.03 1201.80

13-Jun-19 1335.80 1335.90, 1054.21 1052.69 & 1182.85 1184.81

12-Jun-19 1336.65 1332.35, 1049.27 1045.76 & 1179.99 1177.26

11-Jun-19 1322.65 1324.30, 1040.53 1041.30 & 1168.96 1170.42

10-Jun-19 1328.60 1328.60, 1046.94 1048.66 & 1175.41 1175.94

07-Jun-19 1334.30 1340.65, 1049.16 1052.14 & 1184.19 1184.60

06-Jun-19 1336.65 1335.50, 1053.15 1051.17 & 1189.62 1185.92

05-Jun-19 1337.75 1335.05, 1052.01 1049.22 & 1185.38 1184.99

04-Jun-19 1323.60 1324.25, 1045.51 1043.77 & 1177.47 1177.26

News and Commentary

Gold Rises as Dollar Weakens Ahead of U.S. Fed Meeting

China to Roll Out New Rare Earths Policy ‘as Soon as Possible’

ECB Will Provide More Stimulus if Inflation Doesn’t Pick Up: Draghi

Dollar Heads Towards Three-month Lows Before Fed Meeting; Draghi Eyed

Oil Prices Slip for Second Day on Global Growth Worries

Deutsche Bank To Launch €50 Billion “Bad Bank” Housing Billions In Toxic Derivatives

“We Will Fight Until The End”: Beijing Warns Washington Will Lose “Protracted” Trade War

Government Needs to Cut Spending Now – but It Will Not

Strange Gold and Silver Trading – From Violent to Comatose

Swiss Refiner Metalor to Stop Processing Artisanal Gold

end

Gold Surges To All Time Record Highs At $1,974/oz In Australian Dollars

19, June

GoldCore Note

Gold is lower in dollars today despite increasingly dovish signals from the Federal Reserve, ECB, Australian central bank and other central banks as economies slow.

Gold has surged higher in Australian dollars again this week and reached a new all time record high in the Aussie dollar yesterday at $1,974/oz. This is due to concerns about the Australian economy, the likelihood of interest rate cuts Down Under and the negative outlook for the Australian dollar.

Gold remains just off 14-month highs at $1,344.90 per ounce due to the likelihood that central banks will again loosen monetary policy because of the very uncertain geopolitical and economic outlook – particularly regarding global trade.

Stock markets globally remain near two- week highs today and have again been lulled into a false sense of security as speculators bet on a wave of central bank stimulus globally. There are increasing signs that there may be interest rate cuts as early as July in the slowing United States and the euro monetary zone.

Risk assets remain ‘irrationally exuberant’ partly due to President Mario Draghi’s significant ‘about turn’ on monetary policy easing. In one of the biggest policy reversals of his 8 year tenure, Draghi said the ECB would ease again if inflation fails to increase.

Central bankers desire for inflation is very bullish for gold. There has already been massive inflation seen in asset markets and particularly the price of stocks, bonds and of course property. The risk is that the ‘inflation genie may get out of the bottle’ and as economies slow, this creates the real risk of stagflation.

Interestingly, there has been a noticeable increase in new clients from Australia in recent days and a pick up in demand for storage from existing clients. We have a smattering of Australian clients and take payment in Australian dollars. They own bullion coin and bar assets stored with us in Secure Storage in Zurich, Hong Kong and Singapore.

We believe the all time record high of gold in Aussie dollars yesterday (nominal high and not inflation adjusted) will be seen in other currencies in the coming months.

-END-

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Bill Murphy explains the significance of $1350 gold

(courtesy Bill Murphy/GATA/Reluctant Preppers)

Obviousness of gold smashes signifies desperation, GATA chairman says

Submitted by cpowell on Wed, 2019-06-19 02:59. Section: Daily Dispatches

11p ET Tuesday, June 18, 2019

Dear Friend of GATA and Gold:

Smashes of the gold price when it approaches $1,350 have become so obvious as to signal that the gold cartel is desperate to defeat demand for the monetary metal, GATA Chairman Bill Murphy tells Dunagin Kaiser of Reluctant Preppers today. Murphy also answers questions from the Reluctant Preppers audience. The interview is 27 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=1B5qCWEUEdQ&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

GOOD NEWS!! Robert Labourne our resident expert on BIS affairs reports a huge decline in gold activity via gold swaps. I guess the reason is the lack of gold.

(courtesy Robert Lambourne/GATA)

Robert Lambourne: BIS’ activity in gold market continues to diminish

Submitted by cpowell on Wed, 2019-06-19 03:14. Section: Daily Dispatches

By Robert Lambourne

Tuesday, June 18, 2019

The statement of account for May 2019 of the Bank for International Settlements, published this week, indicates that the bank is still trading gold swaps, which the bank uses to gain access to gold held by commercial banks. But the statement indicates that bank’s recent activity in the gold market is much reduced from its activity during the second half of 2018.

There is not enough information in the monthly reports to calculate the exact amount of swaps, but based on the information in the bank’s just-published statement of account, the bank’s gold swaps are estimated to be 78 tonnes as of May 31, compared to 88 tonnes at April 30, 177 tonnes at March 31, 303 tonnes at February 28, 247 tonnes at January 31, 2019, 275 tonnes at December 31, 2018, and 308 tonnes in November, 372 tonnes in October, 238 tonnes in September, and 370 tonnes in August 2018.

…

More background on the bank’s medium-term history of using gold swaps is available here:http://www.gata.org/node/18825

On February 3 this year GATA published comments from a former gold industry executive describing the activities of the BIS in gold swaps in earlier decades:

http://www.gata.org/node/18828

The former executive wrote: “Effectively this process created a supply of ‘paper gold’ — sometimes but not always marked to market — that had a depressing effect on the gold price.”

The BIS refuses to explain its activity in the gold market — its objectives and underlying parties in interest —

http://www.gata.org/node/17793

— and mainstream financial news organizations refuse to ask about it.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

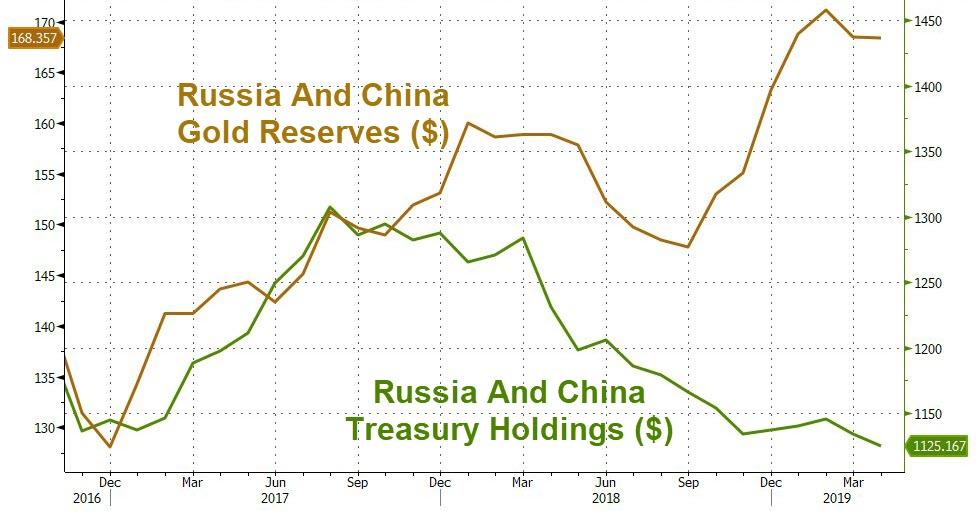

China stockpiles gold while letting U.S. bond holdings slide

Submitted by cpowell on Wed, 2019-06-19 03:28. Section: Daily Dispatches

By Yusho Cho

Nikkei Asian Review, Toyko

Wednesday, June 19, 2019

SHANGHAI — China reduced its holdings of U.S. government debt again in April even as Beijing’s gold reserves continued to grow, diversifying away from the dollar as ties with Washington fray.

The $7.5 billion dip on the month brought China’s total Treasury stockpile to $1.11 trillion, down $90 billion from the most recent peak in August 2017. This follows a roughly $10 billion decline in March.

…

The downtrend in recent months parallels the escalation of the trade war between Beijing and Washington, even as the latest data precedes the breakdown in talks last month that led to another round of tariffs. A shrinking current-account surplus has left China with less wherewithal to buy Treasurys, and Beijing appears to have decided that overextending itself to do so is unnecessary given the souring bilateral relationship.

But few other options are available for stashing large amounts of capital, and selling off U.S. government debt too quickly would risk further antagonizing Washington. Such a move also would drive up long-term yields, reducing the value of China’s remaining holdings.

Rather than dumping Treasurys as a way to gain leverage in trade negotiations, Beijing seems to be taking a subtler approach through trimming its holdings by $20 billion or less per month.

Some of this capital is going into gold. China’s gold reserves have grown for six straight months since December, the first time the country increased its holdings of the precious metal in more than two years. Russia has made similar moves, slashing its dollar-denominated assets while purchasing gold as essentially a borderless currency. …

… For the remainder of the report:

https://asia.nikkei.com/Economy/Trade-war/China-stockpiles-gold-while-le…

* * *

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.9043/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.9068 /shanghai bourse CLOSED UP 27.65 POINTS OR 0.96%

HANG SANG CLOSED UP 703.37 POINTS OR 2.56%

2. Nikkei closed UP 361.16 POINTS OR 1.72%

3. Europe stocks OPENED ALL MIXED/

USA dollar index UP TO 97.55/Euro RISES TO 1.1206

3b Japan 10 year bond yield: FALLS TO. –.14/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.68/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.83 and Brent: 61.72

3f Gold DOWN/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.29%/Italian 10 yr bond yield DOWN to 2.10% /SPAIN 10 YR BOND YIELD UP TO 0.41%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.39: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.48

3k Gold at $1342.85 silver at: 14.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 5/100 in roubles/dollar) 64.00

3m oil into the 53 dollar handle for WTI and 61 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.40 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9973 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1175 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.29%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.08% early this morning. Thirty year rate at 2.56%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.8648..

Global Markets Drift Amid Concerns The Fed May Disappoint

After yesterday’s torrid, euphoric surge on the back of Draghi’s dovish deluge and Trump’s announcement of a G-20 meeting with Xi, world stocks were rather muted, holding near two-week highs on Wednesday, and in the case of the S&P500 just shy of all time highs as investors bet on a worldwide wave of central bank stimulus…

… amid growing expectations that the United States and the euro zone may deliver interest rate cuts as early as July.

Which of course has put Powell in a very difficult position: with Trump demanding by the day, if not hour, that the Fed cur rates, just how does the Fed Chair pull it off without looking political when since the March FOMC meeting: i) stock prices are higher; ii) the unemployment rate fell to a 50-year low; iii) growth forecasts have improved; iv) the tariffs on Mexico that prompted the latest calls for rate cuts have been taken off the table. We’ll find out in just over 6 hours.

Meanwhile, Draghi already capitulated “pre-emptively” on Tuesday, frontrunning the Fed, when in one of the biggest policy reversals of his eight-year tenure, Draghi flagged more easing if inflation failed to pick up, firing up markets and resulting in one of the biggest one-day moves in global stocks of 2019.

But, as Reuters notes, some caution seeped in after the previous day’s frenzy. German and U.S. bond yields, which hit record lows and two-year lows respectively after Draghi’s comments, inched higher to trade just off those levels.

European shares slipped off six-week highs in early trading (although they have since rebounded) and Wall Street futures indicated a slightly weaker opening on Wednesday. Most of the concern is down to the U.S. Federal Reserve’s meeting, the decision of which is due at 1800 GMT. It is widely expected to follow the lead of the European Central Bank and open the door to future rate cuts.

“It should be really clear to absolutely everyone that this is a monetary policy turning point … Those rate cut expectations have now shifted much closer,” said Ulrich Leuchtmann, head of currency and emerging markets research at Commerzbank, quoted by Reuters. “Of course the other question is: What is the Fed doing? If the Fed takes the fundamental risk of political pressure seriously, they cannot do anything today,” he said, noting that Trump’s strident calls for lower interest rates posed a dilemma for the Fed.

Meanwhile, futures are almost fully priced for a quarter-point easing in July and imply more than 60 basis points of cuts by Christmas. As for Europe, markets have almost fully priced a cut in September, though some analysts, such as those at Germany’s Commerzbank, now say rates will be cut in July, rather than in the last quarter of the year as they had predicted earlier.

The risk is that for all the clamor for easing creates risks that policymakers will disappoint.

“Market expectations for a dovish shift are nearly universal, the only question seems to be the degree,” said Blake Gwinn, head of front-end rates at NatWest Markets, referring to the Fed. “Markets will be looking for validation of this pricing. We think this represents a fairly high bar for the Fed to deliver a dovish surprise.”

It wasn’t just central banks though: Bullish market sentiment was reinforced by news that Trump will meet Chinese leader Xi Jinping at the G20 summit this month, even though many doubt the two men can reach a breakthrough on ending their trade dispute.

MSCI’s global equity index rose 0.4%, adding to Tuesday’s 1% gain, as Asian shares excluding Japan followed the lead of their European and U.S. counterparts to jump almost 2% — their biggest one-day rally since January as investors bet on a possible easing of U.S.-China trade tensions. Technology shares led the rally after President Donald Trump said he would meet Chinese counterpart Xi Jinping at the G-20 summit next week. All markets in the region were up, with Hong Kong and Taiwan leading gains, while Australian stocks hit an 11-year high. The Topix gauge climbed 1.7%, as Keyence and SoftBank provided the biggest boosts. Construction stocks rose after a magnitude 6.7 earthquake struck off the northwest coast of Japan.

Over in China, the Shanghai Composite Index closed 1% higher, as brokerage shares jumped on a media report that China encouraged banks to boost liquidity support for securities firms. The S&P BSE Sensex Index fluctuated, with Kotak Mahindra Bank rising and Mahindra & Mahindra declining. India’s second-biggest life insurer said it was time to take money out of the nation’s equities.

In rates, the yield on 10-year Treasuries pared some of the drop from a day earlier, after reaching the lowest level since September 2017 at 2.016%, a world away from the 3.25% top touched in November last year. The yield rose slightly from those lows but is down some 60 bps since January, while that of Japan’s benchmark sank to the lowest since August 2016 at -0.145%. German yields were close to the minus 0.33% record low hit on Tuesday, while Japanese yields

The fallout in currencies has been significantly less, mostly because it is hard for one to gain when all the major central banks are under pressure to ease. The euro did pull back after Draghi’s comments, but at $1.118 it touched only a two-week low. The dollar eased slightly on the yen to 108.3, but was flat versus a basket of currencies. The yuan touched three-week highs versus the dollar on the trade news. The pound gained for a second day.

In commodities, the rate-cut buzz kept gold just off 14-month highs at $1,345.16 per ounce. Brent crude futures however slipped 0.6% to $61.75 a barrel, pressured by economic growth worries.

Expected data include mortgage applications. Oracle and Steelcase are reporting earnings

Market Snapshot

- S&P 500 futures little changed at 2,924.50

- STOXX Europe 600 little changed at 384.68

- MXAP up 1.8% to 157.98

- MXAPJ up 1.8% to 518.37

- Nikkei up 1.7% to 21,333.87

- Topix up 1.7% to 1,555.27

- Hang Seng Index up 2.6% to 28,202.14

- Shanghai Composite up 1% to 2,917.80

- Sensex up 0.1% to 39,086.68

- Australia S&P/ASX 200 up 1.2% to 6,648.13

- Kospi up 1.2% to 2,124.78

- German 10Y yield rose 2.2 bps to -0.298%

- Euro up 0.09% to $1.1204

- Italian 10Y yield fell 18.0 bps to 1.753%

- Spanish 10Y yield rose 4.2 bps to 0.435%

- Brent futures down 0.5% to $61.82/bbl

- Gold spot down 0.3% to $1,342.61

- U.S. Dollar Index little changed at 97.60

Top Headline News from Bloomberg

- Facing pressure from Wall Street and President Trump, Fed Chairman Powell and his colleagues may be running out of patience

- President Trump said he had a “very good” phone conversation with Chinese counterpart Xi. The two will hold an extended meeting at the G-20 summit on June 28-29, Trump said on Twitter

- Boris Johnson extended his lead over his rivals in the race to become Britain’s next prime minister and looked poised to pick up more votes as the hardest Brexiteer in the contest was eliminated

- Trump administration is weighing three sanctions packages to punish Turkey for its purchases of the Russian S-400 missile-defense system, according to people familiar

- Japan’s exports fell for a sixth month as U.S.-China trade tensions add to concerns about global demand and economic growth

- President Trump asked White House lawyers earlier this year to explore his options forremoving Jerome Powell as Fed chairman, according to people familiar

- Trump officially announced his campaign for re-election, delivering a speech thick with grievance in which he warned of a dark future for America if his opponents win in 2020

- An OPEC committee sees global oil inventories contracting by almost 500,000 barrels a day if the group continues restraining supply in the second half of the year, a delegate said

- China is stepping up efforts to avert a funding squeeze among the nation’s banks and securities companies after a rare government seizure of a small lender triggered concerns about a vital part of the nation’s financial plumbing.

- Wednesday’s Federal Reserve rate decision carries more wild cards than most. While market participants don’t expect a rate cut this time around, they do see lower rates this year

- The Trump administration is weighing three sanctions packages to punish Turkey over its purchases of the Russian S-400 missile- defense system, according to people familiar with the matter. The most severe package under discussion between officials would all but cripple the already troubled Turkish economy

Asian equity markets rallied across the board as the region followed suit from the heightened global risk appetite due to a double dosage of optimism from ECB President Draghi’s hints of potential easing and after US President Trump confirmed a meeting with his Chinese counterpart at the G20. ASX 200 (+1.2%) and Nikkei 225 (+1.8%) were higher with Australia led by energy names after a surge in oil prices and with outperformance also seen in the trade sensitive industries such as tech, materials and miners, while the Japanese benchmark gapped above the 21K level fuelled by favourable currency flows and strength in commodity-related sectors. Hang Seng (+2.5%) and Shanghai Comp. (+1.0%) were buoyed after US President Trump announced the resumption of US-China trade talks and that he will be conducting an extended meeting with Chinese President Xi at the G20 following “a very good” telephone conversation between the 2 leaders, while the PBoC were also supportive with the announcement of liquidity injections through reverse repos and its medium-term lending facility. Finally, 10yr JGBs were higher after the dovish comments from ECB’s Draghi added to the declining global yields narrative which saw a drop in 10yr JGB yields to their lowest since August 2016, while the BoJ also kick starts its 2-day policy meeting where they are expected to maintain current policy settings and reaffirm guidance of keeping rates at very low interest rate levels for an extended period of time at least through around Spring 2020.

Top Asian News

- Agung Jumps as Jakarta Issues Permit for Reclamation Projects

- Nomura Jumps on $1.4b Buyback, Governance Tweaks

- Boutique Firm Led by Ex-UBS Banker Said to Bid for Abraaj Funds

- KKR Is Said to Near Partial Exit From $2b Helicopter Firm

European equities are tentative [Eurostoxx 50 Unch] as the region gears up for the FOMC rate decision later today (Full preview available in the Research Suite). Sectors are mixed, underperformance is seen in defensive stocks with healthcare, utilities and consumer staples all lower. In terms of movers, STMicroelectronics (+3.2%) and Infineon (+2.7%) shares gained following a broker move at Morgan Stanley and Bernstein respectively. On the flip side, Steinhoff (-6.5%) opened at the foot of the Stoxx 600 after the Co.’s delayed 2018 results posted losses, whilst Belgian retailer Colruyt (-12.2%) plunged on disappointing earnings.

Top European News

- Airline Shares Fall as HSBC Sees More Profit Warnings Ahead

- Piraeus Tests Risk-Hungry Market With CCC Rated Greek Bank Debt

- U.K. Inflation Returns to BOE Target on Air Fares, Car Prices

- German Property Stocks Fall on Fears of Rent Regulation Ahead

In FX, relatively tight lines are being drawn ahead of the FOMC in G10 land, as is often the case, but the Greenback has clawed back some losses against EMs after Tuesday’s euphoria over the US and China reopening lines of communication on the trade front. However, the index is braced for the Fed within a confined 97.683-553 range, and seemingly reluctant to breach chart/psychological resistance or support around 97.639 (61.8% Fib retracement of pull-back from 98.373 ytd peak to recent 96.451 low) and 97.500 respectively in the run up – see the Ransquawk Research Suite for a full preview.

- GBP/CHF – Bucking the overall muted trend, Cable has continued its recovery towards 1.2600 after broadly in line with forecast UK CPI and PPI data and ahead of the BoE tomorrow, while Eur/Gbp has also retraced further to test 0.8900 compared to circa 0.8975 before ECB President Draghi’s apparent dovish Sintra revelations. Similarly, the Franc is consolidating back above parity and over 1.1200 vs the single currency as markets tread more cautiously in wake of yesterday’s risk-on session.

- EUR/JPY/CAD/AUD/NZD – All narrowly mixed vs the Buck, as noted above, with the Euro licking wounds inflicted by latest dovish ECB vibes and back on the 1.1200 handle where extremely heavy option expiry interest is anchored (5.2 bn 10 pips either side of the big figure). The Yen is also wary of BoJ guidance skewed towards ongoing or even more stimulus, and bound by hefty expiries as 2.95 bn rolls off at the 108.00 strike and 1.3 bn between 108.30-40 vs the 108.25-61 range so far. Elsewhere, the Loonie awaits Canadian CPI data and is holding above 1.3400 with decent expiries from 1.3350-70 (1.2 bn) in close proximity, while the Aussie and Kiwi are both maintaining their recovery momentum over 0.6850 and 0.6500 respectively ahead of RBA Governor Lowe and NZ Q1 GDP, with the former not unduly ruffled by the latest in a growing list of calls for more rate cuts.

- EM – The Lira is back on the rack and underperforming amidst the general retracement noted above, and the renewed threat of US sanctions against Turkey has lifted Usd/Try off recent lows to 5.9150+ at one stage. Elsewhere, the Rand has unwound some of its Eskom-related outsize gains despite firmer the forecast SA CPI, with Usd/Zar rebounding through 14.5000.

In commodities, WTI and Brent futures are marginally lower on the day as yesterday’s upbeat sentiment in the complex somewhat wanes ahead of today’s DoE release. Last night’s API numbers showed a slightly narrower-than-forecast draw in crude stocks (-0.81mln vs. Exp. -1.1mln) . Traders will be keeping an eye on the more widely followed DoE numbers for any short term direction (crude stocks expected to draw by 1.077mln barrels), ahead of tonight’s FOMC meeting. On the OPEC front, the oil producers have decided to hold the OPEC meeting on July 1st and the OPEC+ meeting on the 2nd following weeks of indecisiveness. Elsewhere, gold is unwinding some of its risk premium amid President Trump and his Chinese counterpart showed willingness to reignite US-Sino trade talks at the G20, albeit the yellow metal is certain to be swayed by tonight’s Fed meeting and presser. Meanwhile, copper is little changed but holds onto most of its trade-driven gains. Finally, Dalian iron ore futures spiked higher by almost 6% as the base metal followed the broad rally across assets.

US Event Calendar

- 7am: MBA Mortgage Applications -3.4%, prior 26.8%

- 2pm: FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

Wherever you’re reading this, get comfortable as this is a long one today after probably the biggest day of the year for market moving news. We’ll start by recycling the famous quote, “When the facts change, I change my mind. What do you do?”.

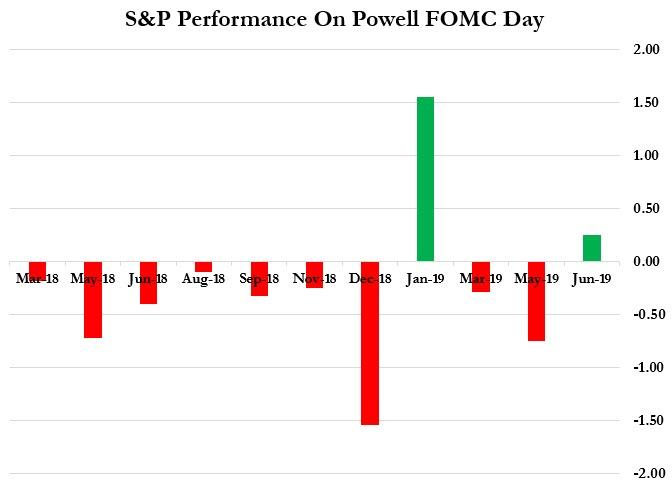

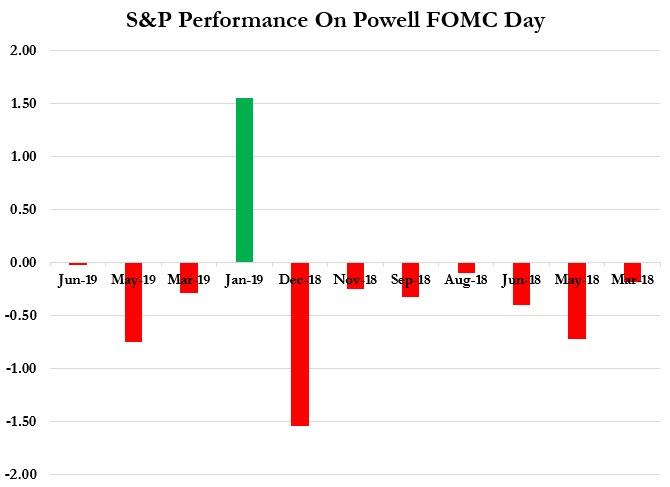

After yesterday’s huge day in financial markets it no longer feels appropriate to be tactically underweight credit. To recap, we decided to move to this position in May as the trade escalation left us feeling that weak markets or poor economic data were needed to push the US and China into meaningful talks. To be fair we did initially see weak markets and slipping economic data but then came a huge change in market pricing of central bank activity, first in terms of the Fed and then the ECB, culminating in Draghi’s extremely dovish signal yesterday. If that wasn’t enough, our weekend sources in Washington which we detailed on Monday were proved correct as Mr Trump tweeted just after the US open that he will meet with China’s President Xi at next week’s G-20. So the balance of risks (and there still are a lot of risks) have become more balanced and more supportive of the carry trade of which credit is a key one. So the path of least resistance now seems tighter for credit, with European credit likely to be additionally propped up by expectations that CSPP is a step closer after yesterday (see this note from last week for more on how to assess the probabilities of this). The risks to the view is that the events of the last month are already leading to a global slowdown that central banks can’t do much about and/or that the Trump/Xi G20 talks end up going nowhere and we get the final round of tariffs applied very soon after and then further escalations. The next hurdle is today’s FOMC which is another much anticipated moment. The market and Mr Trump have put a lot of pressure on the Fed. It’s hard to imagine that they’ll disappoint given all that’s going on but we should note that under Mr Powell, nine out of ten FOMC meeting days have seen equities down. We’ll preview in full below.

Before we go through the details of Mr Draghi and Mr Trump’s significant comments, respectively, it’s worth starting with markets where we can now list new all-time yield lows for 10y bonds. Germany, Denmark, Netherlands, Austria, Finland, Sweden, France, Belgium, Slovakia, Ireland, Slovenia, Latvia, Spain, Portugal, Cyprus and Croatia all experienced this yesterday. Indeed it wouldn’t be a surprise if we missed one or two. Bunds rallied -7.6bps to close at the eye wateringly low level of -0.322%, OATs hit an intraday low of -0.004% – the first time they have been below 0% – while yields in Sweden and Austria closed at -0.027% and -0.052%, both below 0% for the first time too. BTPs also rallied -18.5bps which is the biggest one-day move since October. If you want a scary example of just how extreme the rates move was, then Austria’s 100y bond rose 5.5pts yesterday, taking it to a cash price of 156.9. That means it has jumped nearly 40pts YTD already, equivalent to a -61.2bp fall in yield so far in 2019. The coupon on that bond is 2.1% and the yield is now just 1.14%. Oh, and it has a duration of 51.8! You’d be hard to pressed to find many fixed income assets which have delivered a bigger return YTD. Yesterday’s moves were even more remarkable since they were driven by collapsing real yields as inflation expectations perked up. The European five year-five year inflation swap rate popped up 8.9bps to 1.23%, which is still extremely low by historical standards but was the biggest rise since March 2012.

The move for European rates reverberated throughout the US too. Indeed 10y Treasuries rallied -3.5bps (though they were down -7.9bps before the Trump tweet) and are now down to 2.060%, the lowest level since September 2017. They have held that level overnight also. The 2s10s curve also dipped to 19.15bps (-2.8bps on the day). The amount of negative yielding debt in the world now is around $12.5tn and the most ever. Oh, and the Bund curve is now negative out to 18 years. The other side of the coin for markets was a big rally for risk. The STOXX 600 (+1.67%) had its best day since January. The DAX, CAC and FTSE MIB also all closed up more than 2% while in the US the S&P 500, NASDAQ and DOW ended +0.97%, +1.39% and +1.35%, respectively. Despite the yield move, banks rose +1.54% in Europe (possibly on hints of tiering alongside rate cuts) and +1.79% in the US. EM equities also finished +2.44%, their best session since January, while HY credit spreads were -10bps and -6bps tighter in Europe and the US, respectively. Oil also rallied +3.79%, helped by the improved risk sentiment but also by news that the OPEC+ group will meet to discuss a possible extension to their supply cuts. Finally the euro finished down -0.21% – a fairly modest move all things considered, though -0.43% from its pre-Draghi level.

Overnight in Asia markets are following Wall Street’s lead with the Nikkei (+1.71%), Hang Seng (+2.37%), Shanghai Comp (+1.50%) and Kospi (+1.11%) all posting decent gains. In rates, yields on 10y JGBs are down -2.1bps to -0.158%, thereby hitting the lowest yield since July 2016 and testing the limits of the BoJ’s target range. In other news, here in the UK, the Times reported overnight that the Labour Party leader Jeremy Corbyn will today back a move to change the party’s Brexit policy and support a second referendum in all circumstances. This supposedly follows rising internal pressure from his own MPs. Meanwhile, as we go into the print, Bloomberg is reporting that the Trump administration is weighing three sanctions packages to punish Turkey over its purchases of the Russian S-400 missile-defense system. The Turkish lira is trading down -0.71% on the news.

Back to Draghi, where the most significant statement was “in the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required”. He added “in the coming weeks, the Governing Council will deliberate how our instruments can be adapted commensurate to the severity of the risk to price stability” and that “further cuts in policy interest rates” remain part of the ECB’s toolkit. The plural “cuts” didn’t go unnoticed, and nor did the reference to “how” instruments can be changed, rather than “if.” Draghi went on to say that the “APP still has considerable headroom,” possibly signaling a relaxation in the 33% country limit on purchases. Peter Praet, former ECB Chief Economist whose term ended 3 weeks ago, also added to Draghi’s comments by saying that the ECB will look at tiering if a rate cut moves onto the agenda. There’s little doubt that this counts as a u-turn compared to the June meeting, as evidenced by markets yesterday. The ECB has joined the Fed and the question is how much easing is there to come. Markets are now pricing in around 9bps of cuts by the September meeting, plus another 5bps between September and December. So fully pricing at least one 10bps cut before the year is out. We should also note that overnight, anonymously sourced articles (per Bloomberg) said both that rates will the primary tool before restarting QE and that the options are still being considered.