GOLD: $1393.10 UP $47.95 (COMEX TO COMEX CLOSING)

Silver: $15.51 UP 53 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1391.80

silver: $15.46

Gold and silver broke out today as the bankers try desperately to cover their massive shortfall. Expect continued margin calls. However the big explosion in price will occur when our derivative banks blow up with nobody able to cover their trillions in losses. We have also witnessed massive volumes in Exchange for physical contracts. When buyers of these paper gold/silver turn them into real gold, the real fireworks commence. Tomorrow’s Comex OI in both silver and gold will be astronomical. I receive preliminary numbers late at night and if you interested, check in this spot at around 1 am and I will provide it for you…

____________________________________________________

OPEN INTEREST/PRELIMINARY: FOR FRIDAY

GOLD:

COMEX OPEN INTEREST ROSE BY A WHOPPING: 43,170 CONTRACTS

GOLD EXCHANGE FOR PHYSICAL ISSUANCE: 22,225 CONTRACTS

TOTAL: 65,395 CONTRACTS…SIMPLY MIND BOGGLING

IN SILVER:

TOTAL COMEX OI FELL BY 2164 CONTRACTS

SILVER EXCHANGE FOR PHYSICAL ISSUANCE: 4258 CONTRACTS

TOTAL OI GAIN: 2094 CONTRACTS.

____________________________________________________

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 36/85

EXCHANGE: COMEX

CONTRACT: JUNE 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,344.600000000 USD

INTENT DATE: 06/19/2019 DELIVERY DATE: 06/21/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

624 C BOFA SECURITIES 7

657 C MORGAN STANLEY 26

661 C JP MORGAN 36

686 C INTL FCSTONE 5

737 C ADVANTAGE 49 42

905 C ADM 5

____________________________________________________________________________________________

TOTAL: 85 85

MONTH TO DATE: 2,218

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 85 NOTICE(S) FOR 8500 OZ (0.2643 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2218 NOTICES FOR 221,800 OZ (6.8989 TONNES)

SILVER

FOR JUNE

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 391 for 1,955,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9220 DOWN $30

Bitcoin: FINAL EVENING TRADE: $ 9450 UP $200

end

XXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE A SMALL SIZED 39 CONTRACTS FROM 239,466 UP TO 239,505 ACCOMPANYING THE 3 CENT LOSS IN SILVER PRICING AT THE COMEX.( LIQUIDATION OF THE SPREADERS HAVE STOPPED FOR GOLD . HOWEVER WE ARE WITNESSING A RISE IN SPREADING ACCUMULATION BY THE BANKERS IN SILVER)..TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 1505 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1505 CONTRACTS.( WITH THE TRANSFER OF 1505 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1505 EFP CONTRACTS TRANSLATES INTO 7.525 MILLION OZ ACCOMPANYING:

1.THE 3 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.120 MILLION OZ STANDING FOR SILVER IN JUNE//

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

35,334 CONTRACTS (FOR 14 TRADING DAYS TOTAL 35,334 CONTRACTS) OR 176.67 MILLION OZ: (AVERAGE PER DAY: 2523 CONTRACTS OR 12.61 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 176. MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 25.23% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1047.42 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 39, DESPITE THE 3 CENT FALL IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1505 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE GAINED A STRONG SIZED: 1544 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1505 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 39 OI COMEX CONTRACTS. AND ALL OF THIS HUGE DEMAND HAPPENED WITH A 3 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.98 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.199 BILLION OZ TO BE EXACT or 171% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.120 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD VERY STRONG ACTIVITY OF SPREADING ACCUMULATION IN SILVER TODAY AS TOTAL OI ROSE SHARPLY DESPITE THE SMALLISH LOSS OF 3 CENTS.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS 13,315 CONTRACTS, TO 538,951 DESPITE THE $1.85 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED AND THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE ACCUMULATION PHASE OF THEIR OPERATION. THUS THE GAIN IN OI IS REAL AS INVESTORS ARE POURING INTO THE GOLD SECTOR

REMEMBER THAT THE GAIN IN GOLD AND SILVER OCCURED AFTER THE COMEX CLOSED AT 1:30. FOMC RESULTS WERE AT 2 PM

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9159 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 9159 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 538,951. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,466 CONTRACTS: 13,315 CONTRACTS INCREASED AT THE COMEX AND 9159 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 22,466 CONTRACTS OR 2,246,600 OZ OR 69.87 TONNES. YESTERDAY WE HAD A SMALL LOSS OF $1.85 IN GOLD TRADING.…AND WITH THAT SMALL LOSS IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 69.87 TONNES!!!!!! THE BANKERS WERE SUPPLYING COPIOUS SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 126,937 CONTRACTS OR 12,693,700 oz OR 394.82 TONNES (14 TRADING DAYS AND THUS AVERAGING: 9066 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAYS IN TONNES: 394.82 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 394.82/3550 x 100% TONNES =11.12% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,646.30 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 13,315 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK ON YESTERDAY($1.85)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9159 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9159 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC SIZED GAIN OF 22,466 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9159 CONTRACTS MOVE TO LONDON AND 13,315 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 69.87 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED WITH A LOSS IN PRICE OF $1.85 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 85 notice(s) filed upon for 8500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $47.95 TODAY//

NO CHANGE IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 764.10 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 53 CENTS TODAY:

A SMALL CHANGE WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV: A DEPOSIT OF 749,000 OZ

/INVENTORY RESTS AT 319.819 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 39 CONTRACTS from 239,466 UP TO 239,505 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE =0 CONTRACTS AND JULY: 1505 CONTRACTS FOR AUGUST: 0, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1505 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 39 CONTRACTS TO THE 1505 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A VERY STRONG GAIN OF 1544 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.772 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 2.120 MILLION OZ FOR JUNE.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 3 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1505 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 69.32 POINTS OR 2.38% //Hang Sang CLOSED UP 348.29 POINTS OR 1.24% /The Nikkei closed UP 128.99 POINTS OR 0.60%//Australia’s all ordinaires CLOSED UP .59%

/Chinese yuan (ONSHORE) closed UP at 6.8559 /Oil DOWN TO 52.12 dollars per barrel for WTI and 61.21 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 6.8559 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8618 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/HONG KONG/

4/EUROPEAN AFFAIRS

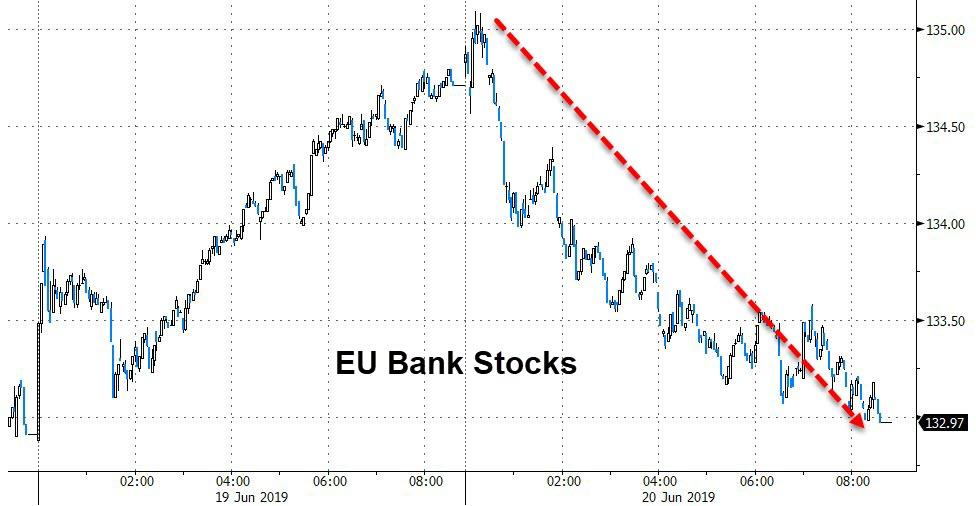

i)GERMANY/DEUTSCHE BANK

We now have the Fed investigating Deutsche bank for suspected money laundering especially with the Russian mob

( zerohedge)

iv)FRANCE/NATIXIS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)IRAN/ISRAEL/HEZBOLLAH

Israel holds the largest “Hezbollah War Exercise” as they fear an attack from the Iranians who hold some of the land in the south of Lebanon

( zerohedge)

ii)IRAN/USA

Iran shoots down a USA drone. Iran states that the drone was in Iranian airspace..the USA states that it was over the Strait of Hormuz.

Iran states that they are ready for war.

( zerohedge)

iii)Russia/USA/Iran

iv)TURKEY

v)SAUDI ARABIA/USA

6. GLOBAL ISSUES

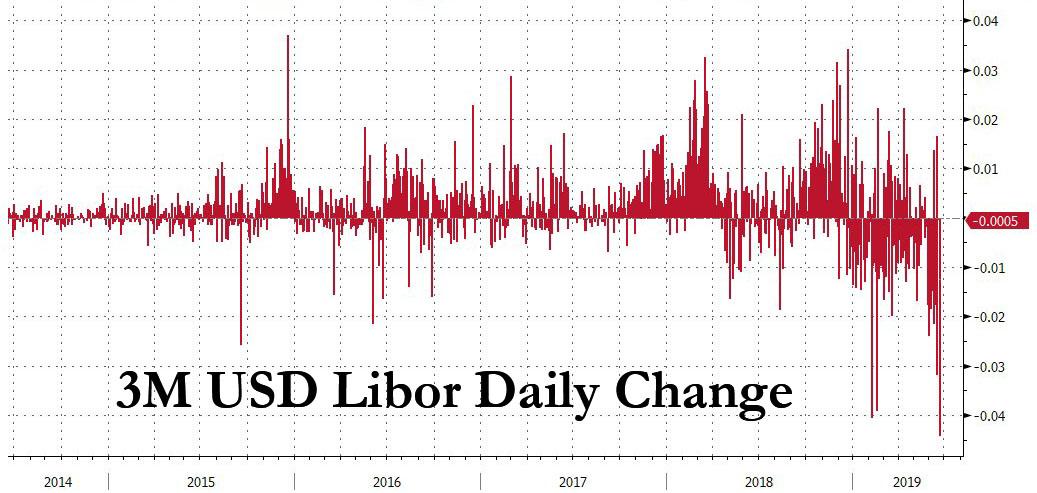

a)There is no greater sign that the world is deflating than this: libor tumbles the most since May 2009. This is why we are witnessing 10 yr yields from all countries collapse under this huge deflationary pressure as growth stymies

( zerohedge)

b)Simon Black gives up a very analysis on the demographics facing the globe. However the once country that is in severe trouble on that front is Japan.

(courtesy Simon Black/SovereignMan)

7. OIL ISSUES

The shooting down of the USA surveillance drone over international waters causes oil to spike the most in 5 months

(courtesy zerohedge)

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

(Bloomberg/GATA)

ii)A very important commentary from Ambrose Evans as he agrees with the above commentary that we are now entering a currency war as global demand dries up. Europe will be defenseless

( Ambrose Evans \Pritchard)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//

a)Market trading/LAST NIGHT/

II)MARKET TRADING

ii)Market data

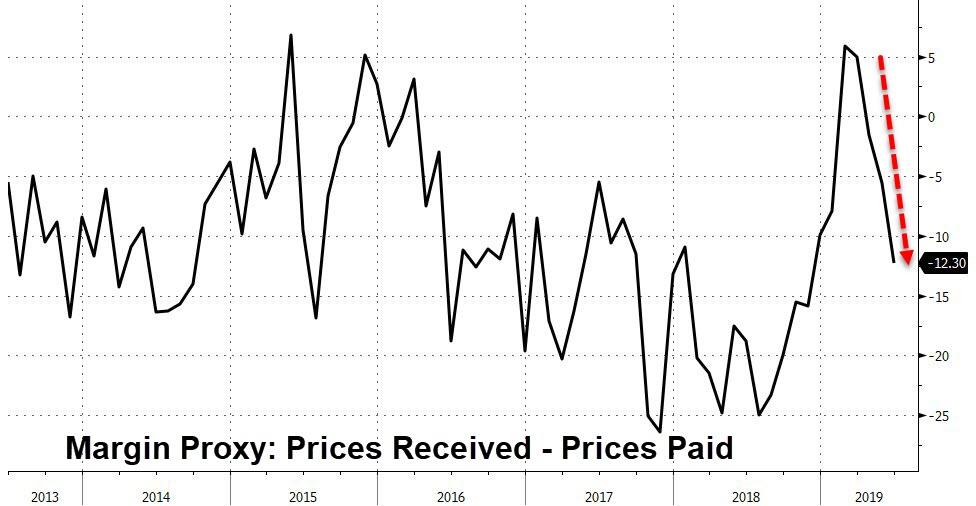

Philly Fed slumps in June as outgoing prices plunge putting massive pressures on margins

( zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)This is big!! we are now witnessing a complete collapse in the USA trucking industry

(courtesy Michael Snyder)

b)USA farmers are now calling for a 3rd farm bailout as the trade war intensifies

d)Goldman Sachs now capitulates: sees rate cuts in both Juoly and September(courtesy zerohedge)

e)A good commentary from Michael Every as he explains in detail what is going throughout the globe. As interest rates plummet to zero and below zero it will not help countries respective economies…the world is rapidly deflating…

f)Los Angeles area has been receiving a huge number of quakes in this last month.

SWAMP STORIES

i)More shenanigans from the FBI as they totally ignored repeated warnings that the Manafort Black Ledger might be a fake

(courtesy zerohedge)

ii)the left is slamming Biden and his son????

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

FOR THE JUNE 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 85 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 36 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE /2019. contract month, we take the total number of notices filed so far for the month (2218) x 100 oz , to which we add the difference between the open interest for the front month of JUNE. (298 contract) minus the number of notices served upon today (85 x 100 oz per contract) equals 243,100 OZ OR 7.561 TONNES) the number of ounces standing in this active month of JUNE

Thus the INITIAL standings for gold for the JUNE/2019 contract month:

No of notices served (2218 x 100 oz) + (298)OI for the front month minus the number of notices served upon today (85 x 100 oz )which equals 243,100 oz standing OR 7.561 TONNES in this active delivery month of JUNE.

We GAINED 122 contracts or an additional 12,200 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly.!!

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.04 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 7.561 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 87.119 million

total dealer + customer silver: 304.692 million oz

The total number of notices filed today for the JUNE 2019. contract month is represented by 0 contract(s) FOR nil oz

To calculate the number of silver ounces that will stand for delivery in JUNE, we take the total number of notices filed for the month so far at 391 x 5,000 oz = 1,955,000 oz to which we add the difference between the open interest for the front month of JUNE. (33) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 391(notices served so far)x 5000 oz + OI for front month of JUNE( 33) -number of notices served upon today (0)x 5000 oz equals 2,120,000 oz of silver standing for the JN contract month.

WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 256,383 CONTRACTS (we had considerable spreading activity..accumulation/and short covering

CONFIRMED VOLUME FOR YESTERDAY: 111,181 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 111,181 CONTRACTS EQUATES to 555 million OZ 79.4% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.97% June 20/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.97% to NAV (june 20/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -1.97%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.69 TRADING 13.13/DISCOUNT 4.11

END

And now the Gold inventory at the GLD/

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WI6H GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

MAY 21/WITH GOLD DOWN $3.65 TODAY: A SURPRISE 2.00 TONNES WERE ADDED TO THE GLD GOLD INVENTORY//INVENTORY RESTS AT 738.17 TONNES

MAY 20/WITH GOLD UP $1.00 A HUGE 2.96 TONNE DEPOSIT INTO THE GLD//INVENTORY RESTS AT 736.17 TONNES

MAY 17/WITH GOLD DOWN $9.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 733.23 TONNES

MAY 16/WITH GOLD DOWN $11.50: A WITHDRAWAL OF 3.23 TONNES FROM THE GLD//INVENTORY RESTS AT 733.23 TONNES

MAY 15/WITH GOLD UP $1.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 736.46 TONNES

MAY 14//WITH GOLD DOWN $5.45 TODAY: STRANGE!! THE CROOKS DECIDED TO DEPOSIT A HUGE 3.23 TONNES INTO THE GLD INVENTORY//INVENTORY RESTS AT 736.46 TONNES

MAY 13/ WITH GOLD UP ANOTHER $15.40 TODAY: STRANGE! A MASSIVE WITHDRAWAL OF 6.41 TONNES OF GOLD (TO TAME GOLD’S RISE TODAY)/INVENTORY RESTS AT 733.23 TONNES

MAY 10 WITH GOLD UP $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 9//WITH GOLD UP $4.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 8/WITH GOLD DOWN $3.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 739.64 TONNES

MAY 7/ WITH GOLD UP $1.80: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 6/WITH GOLD UP $2.35: ANOTHER WITHDRAWAL OF 5.88 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 739.64 TONNES

MAY 3/WITH GOLD UP $9.35 TODAY: A WITHDRAWAL OF 1.17 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 745.52

MAY 2/WITH GOLD DOWN $12.30 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

MAY 1/WITH GOLD DOWN $1.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 746.69 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 20/2019/ Inventory rests tonight at 764.10 tonnes

*IN LAST 614 TRADING DAYS: 169.66 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 514 TRADING DAYS: A NET 4.03TONNES HAVE NOW BEEN REMOVED FROM THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 20/WITH SILVER UP 53 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 749,000 OZ/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 17/WITH SILVER UP 1 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

june 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

jUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

MAY 17/WITH SILVER DOWN 13 CENTS TODAY: A BIG CHANGES IN SLV: A WITHDRAWAL OF 3.185 MILLION OZ FROM THE SLV INVENTORY VAULTS:/INVENTORY RESTS AT 312.366 MILLION OZ//

MAY 16/WITH SILVER DOWN 26 CENTS: NO CHANGES IN THE SLV INVENTORY//INVENTORY RESTS AT 315.551 MILLION OZ//

MAY 15/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SLV INVENTORY: A WITHDRAWAL OF 1.031 MILLION OZ// THE SLV/INVENTORY RESTS AT 315.551 MILLION OZ.

MAY 14/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV. INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 13//WITH SILVE5 DOWN 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ…

MAY 10/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 9/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 8/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ///

MAY 7/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ//

MAY 6/WITH SILVER DOWN 3 CENTS WE HAD ANOTHER DEPOSIT OF 891,000 OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 316.582 MILLION OZ/

MAY 3//WITH SILVER UP 34 CENTS TODAY: A DEPOSIT OF 843,000 OZ INTO THE SLV/TOTAL INVENTORY RESTS AT 315.691 MILLION OZ//

MAY 2/WITH SILVER DOWN ANOTHER 13 CENTS, MIRACUOUSLY THE AUTHORITIES ADD 2.869 MILLION OZ OF SILVER BACK INTO THE SLV/INVENTORY RESTS AT 314.848 MILLION OZ//

MAY 1/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.979 MILLION OZ////

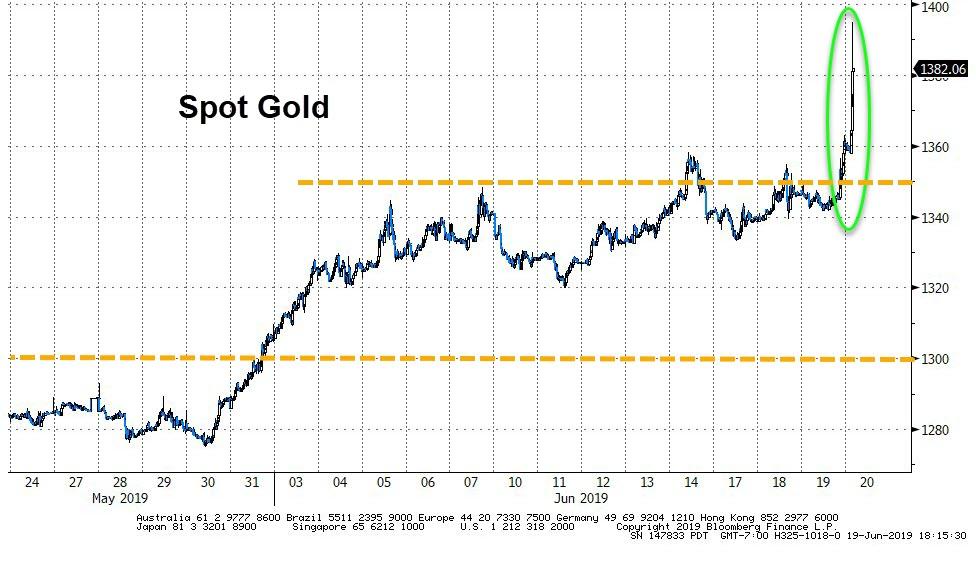

Gold Breaks Abov

end

GOLD TRADING LAST NIGHT

Gold Spikes To 6Y Highs As Dollar, Bond Yields Plunge

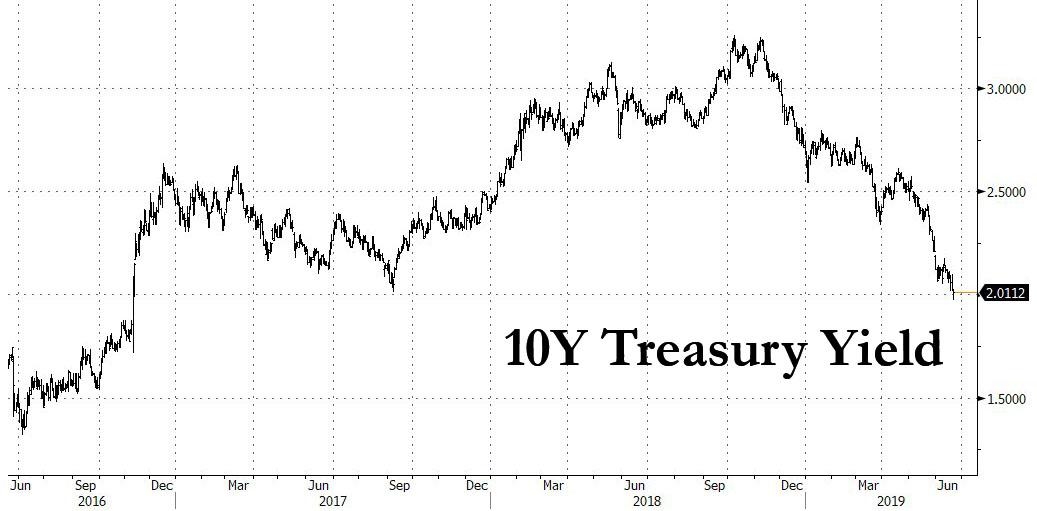

The 10Y US Treasury yield is now down 11bps from the FOMC Statement, plunging back below 2.00% for the first time since November 2016, erasing almost the entire move since President Trump was elected…

Citigroup sees 10-year Treasury yields falling to about 1.65% by year’s end as the Federal Reserve cuts interest rates up to three times to boost U.S. economy, senior technical strategist Shyam Devani tells Bloomberg.

“Yields have been falling across the curve, and this has been something you haven’t been able to fight,” Singapore-based Devani said by telephone.

“You’ve got a Fed that’s now changed its language and we’re on a path where there’s going to be rate cuts ahead — whether it’s two or three times, it’s hard to say — but there will be cuts”

“It’s a combination of things driving this including a slowing global growth environment, trade tensions and low inflation”

30Y is also extending its gains, with the yield dumping to 2.50%, erasing all of the post-Trump growth move…

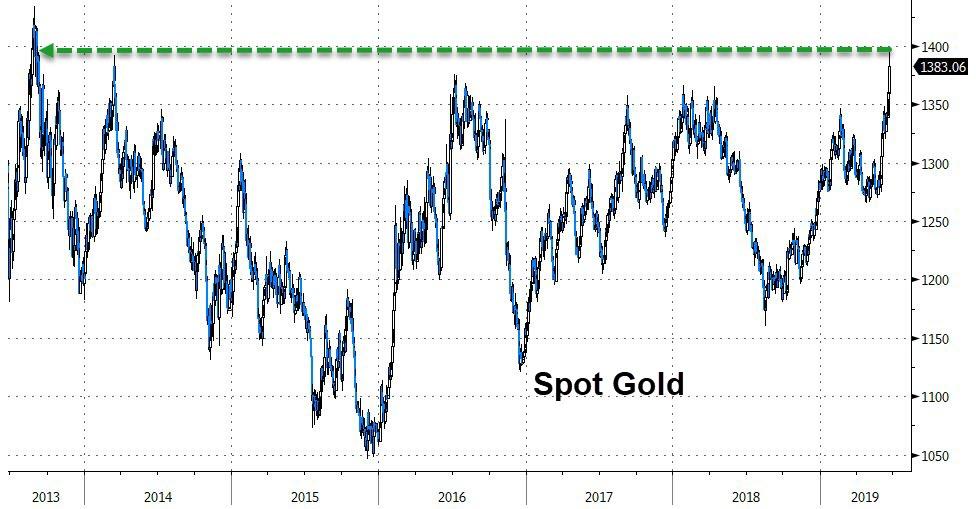

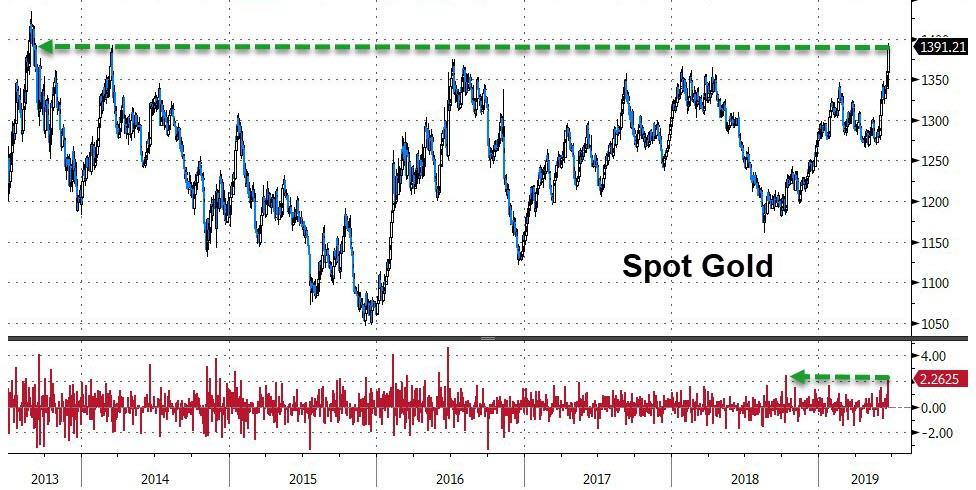

Gold has spiked up to almost $1400…

Its highest since September 2013

The Dollar is extending its losses…

And the jaws of death keep yawning wider…

Something’s gotta give (reminder, Friday is quad witch)!

LAWRIE WILLIAMS: Can gold’s breakout be sustained?

Well yesterday’s price action in precious metals turned out to be something of a bull’s dream. The whole complex moved substantially higher, and though palladium and rhodium may have seemed the key players with some substantial dollar price increases, gold surged through what many analysts have seen as the key $1,365 level. Silver meanwhile, perhaps the most out of favour of the precious metals, showed a very substantial gain in percentage terms of nearly 4% in US dollar terms so far this week. With the gold:silver ratio still languishing at over 90 silver’s potential, should the gold price continue upwards, may just be beginning to show itself. But then silver can be the most erratic metal in the precious metals complex and can thus be the most dangerous to invest in, although potential percentage gains are the highest for those who like a price gamble.

We have noted here before that there would seem to be a number of economic and political factors predicating that gold has a strong short term future – and where gold goes the other precious metals tend to follow. But the triggers which created the latest surge were statements from the heads of the U.S. Fed, and of the European Central Bank both suggesting that the next move in interest rates on both sides of the Atlantic are likely to be downwards. While this was hardly unexpected, the twin official confirmations of this likelihood was sufficient to move the markets quite substantially. Add to that a tweet from the U.S. President taken as suggesting that the next stage in his Make America Great Again policies, following on from his tariff and sanctions impositions, could well be a currency war, and the markets were well and truly affected. A likely loosening of interest rate policy by the Fed and the possibility of a forced down U.S. dollar boosted both equities and precious metals. It remains to be seen how the all-important U.S. markets in particular take things when they open today. Asian and European equities have been rising, as has the gold price after an initial dip, but will this be sustained in the cool light of the American day!

There may well be a downwards reaction once the U.S. markets open, but we feel this will probably be shortlived and gold, and the other precious metals will, after a period of consolidation continue their upwards movement throughout the northern hemisphere summer months, albeit with the occasional setback.. If this is indeed the case then the consensus gold price forecasts for the second half of the year will likely be overtaken – perhaps in the next few weeks even. We certainly wouldn’t be surprised to see many bank and other analysts increasing their forecasts for the gold price in the second half of the year to $1,500 or above. But the powers that be may well try and put a stop to what might be seen as an excessive condemnation of the strength of the U.S. dollar and force prices back. But if President Trump is serious about weakening the dollar in the light of key competitive nations weakening their own currencies to gain a trade advantage, then the upwards momentum for gold – in U.S. dollar terms, which is the way the world sees it – may prove to be unstoppable making even a $1,500 price forecast for the second half of the year well within reach! We shall see what transpires. The next few days may be critical.

20 Jun 2019

end

For those that missed my interview with Chris Marcus, here it is again:

(courtesy Chris Marcus/Harvey Organ)

MEX Running Out of Silver? – with Harvey Organ

Anyone who studies the silver market for any period of time quickly realizes that things are far from normal.

For years silver investors have been stunned by the amount of paper silver contracts that are dumped on the market and keep the price low. While at the same time, other counter-parties are taking as much physical metal out of the market as they can. Which as you can well imagine has created quite a supply and demand imbalance.

So how does it all play out? And are we nearing the point where someone shows up for their silver and there’s a failure to deliver?

Fortunately Harvey Organ joined me on the show to explain what he’s seeing on the COMEX, and what investors should know before it’s too late to respond.

To find out more, click to listen to the interview now!

Chris Marcus

June 13, 2019

-END-

GATA STORIES WITH RESPECT TO GOLD/PRECIOUS METALS.

Trump very early realized what Draghi was going to do..cut interest rates to ward off deflationary effects. This of course would lower the Euro and make it more difficult for the uSA to compete. Trump thus signals a move from a trade war towards a currency war.

(Bloomberg/GATA)

Trump moves from trade war toward currency war

Submitted by cpowell on Wed, 2019-06-19 13:03. Section: Daily Dispatches

By Shawn Donnan, Rich Miller, and Katherine Greifeld

Bloomberg News

Wednesday, June 19, 2019

President Donald Trump has already given the global economy trade wars. Now there are signs he may be gearing up for a currency war too.

With a series of tweets on Tuesday aimed at the European Central Bank and an announcement by Mario Draghi, its president, that he was prepared to cut interest rates further below zero in response to Europe’s slowing growth, Trump made a rare American presidential intervention into another economy’s monetary policy.

…

“Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others,” he tweeted. Later, he added: “German DAX way up due to stimulus remarks from Mario Draghi. Very unfair to the United States!” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-19/trump-adds-currency-w…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

A very important commentary from Ambrose Evans as he agrees with the above commentary that we are now entering a currency war as global demand dries up. Europe will be defenseless

(courtesy Ambrose Evans \Pritchard)

Ambrose Evans-Pritchard: Currency war is next phase of global conflict and Europe, the chief parasite, is defenseless

Submitted by cpowell on Thu, 2019-06-20 01:51. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Wednesday, June 19, 2019

https://www.telegraph.co.uk/business/2019/06/19/currency-war-next-phase-…

Europe has been warned. Any use of monetary levers to hold down the euro exchange rate will be deemed a provocation by the Trump administration.

Further cuts in interest rates to minus 0.5 percent or beyond will be scrutinized for currency manipulation. A revival of quantitative easing will be considered a devaluation policy in disguise, as indeed it is, since the money leaks out into global securities and depresses the euro.

…

The Bank for International Settlements says E300 billion of Europe’s QE funding reached London alone between 2014 and 2017.

If the ECB copies the Swiss National Bank and starts to amass foreign assets directly to cap currency strength Europe will face certain retaliation.

Whether the Swiss can get away with their policy for much longer is an open question. The SNB has foreign holdings of $760 billion — near 120 percent of GDP — and owns slices of Apple, Microsoft, Amazon, Facebook, and Exxon.

As the global economy falters we are entering the next phase of currency warfare. There is going to be an ugly fight for scarce global demand.

What is striking about Donald Trump’s tweets against the ECB this week is how quick he was to see the significance of Mario Draghi’s policy pirouette in Sintra — already dubbed “whatever it takes II” by bond markets — and how quickly he pounced:

* * *

Mario Draghi just announced more stimulus could come, which immediately dropped the euro against the dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others.

— Donald J. Trump (@realDonaldTrump) June 18, 2019

* * *

This has the imprint of his trade guru Peter Navarro.

The dollar is of course overvalued. The Federal Reserve’s broad dollar index reached a 17-year high in early June. The manufacturing trade deficit has ballooned to $900bn.

These imbalances have been made worse by Mr. Trump’s own policies. His tax cuts at the top of the cycle have pushed the budget deficit to 4 percent of GDP. They forced the Fed to jam on the brakes last year.

This “loose fiscal/tight money” regime is the textbook formula for a strong currency. But the White House is not going to admit this. It is going to blame foreigners, and foreigners are not innocent either.

The eurozone is chief global parasite. It has been sucking demand out of the global economy with current account surpluses of E300 billion to E400 billion. China is a saint by comparison. This “free rider” behavior is the result of the euro structure and the austerity bias of the Stability Pact and German ideology amplified through currency union.

The rest of the world pays the price for euroland’s half-built experiment and its failure to stimulate — that is to say its failure to create a joint treasury with shared debt issuance that would make an investment revival possible in the depressed half of Europe.

Mr. Navarro has special twist on this: The warped mechanism of monetary union allows Germany to keep the implicit Deutsche Mark “grossly undervalued” and to lock in a beggar-thy-neighbor trade advantage over southern Europe. Hence Germany’s chronic current account surplus of 8.5 percent of GDP.

Mr. Trump’s White House has had enough of this and the battleground is over the currency. Democrats are singing from the same hymn sheet. Presidential candidate Elizabeth Warren has launched a campaign of “economic patriotism” with active currency management.

The Economic Policy Institute in Washington proposes buying the bonds of any country engaged in currency manipulation to neutralize the effect. The U.S. Treasury is in charge of currency policy and can effectively order the Fed to support U.S. foreign policy objectives.

It reminds me of the Reagan Doctrine during the Cold War: playing Moscow at its own game by sponsoring guerrilla insurgencies (Nicaragua, Afghanistan, etc). It bled the Soviet Union dry.

This is the new world order that Mario Draghi faces as he tries to stop the eurozone from sliding into a deflationary quagmire. The ECB’s market measure of inflation expectations — 5-year/5-year swaps — have collapsed with all the nefast consequences this has for nominal GDP growth and Italy’s debt trajectory.

Yields on 10-year Bunds have crashed to minus 0.30 percent. The bond markets are signalling an ice age. Clearly the decision to shut down the E2.6 trillion QE program in January and declare mission accomplished — when Euroland was already in an industrial recession — was a policy blunder. It was forced upon Mr. Draghi by hawks.

He is now taking revenge on the ECB’s governing council with a fait accompli. Unless the eurozone starts to recover “additional stimulus will be required,” and for good measure: “If the crisis has shown anything, it is that we will use all the flexibility within our mandate to fulfil our mandate,” he said in Sintra.

This pledge was made without first securing the consent of the Teutonic bloc. Angela Merkel’s Christian Democrats called it “an alarming signal for the ECB’s integrity.” This time Mr. Draghi may have overreached in every sense.

The ECB can of course buy corporate bonds and bank debt (a shield for Italy). It can do some stealth monetization of public debt. But plain-vanilla QE at this stage is tinkering. Little more stimulus can be extracted by pulling down the long end of the yield curve. The curve is near inversion already.

“It is ceremonial. The ECB is powerless. It is scrounging about trying to create a sense of action, but none of this has any effect,” says Ashoka Mody, a former bailout chief in Europe for the IMF and author of “Eurotragedy: a Drama in Nine Acts.”

The deflationary cancer is now so deeply lodged in the eurozone that it would take helicopter money or People’s QE — monetary financing of public works — to fight off any future global slump. Such action would violate the Lisbon Treaty and would test to destruction Germany’s political acquiescence in the euro project.

In truth QE in Europe has always worked chiefly through devaluation. The euro’s trade-weighted index fell 14 percent a year after Mr. Draghi first signalled in 2014 that bond purchases were coming. That was powerful stimulus. When the euro climbed back up the eurozone economy stalled.

It takes permanent suppression of the exchange rate to keep euroland going. As the Japanese have discovered, it is very hard for an economy with near zero inflation and a structural trade surplus to stop its exchange rate from rising unless it resorts to overt currency warfare. That is exactly what Mr. Trump is not going to allow.

Every avenue of monetary stimulus is cut off in the eurozone. Only fiscal stimulus a l’outrance — 2 or 3 percent of GDP — will be enough to weather a serious crisis. That too is blocked.

“The ECB has masked the fragility over the last seven years and nobody knows when the hour of truth will come,” said Jean Pisani-Ferry, economic adviser to France’s Emmanuel Macron and a fellow at the Bruegel think tank.

“There is no common deposit scheme for banks. Cross-border investments are retreating. The vicious circle between banks and states could come return any moment,” he said.

Mario Draghi’s rhetorical coup in July 2012 worked only because he secured a partial approval from Germany for the ECB to act as lender-of-last resort for Italy’s debt (under strict conditions). That immediately halted an artificial crisis. The situation today is entirely different. The threat is a deflationary slump. The ECB has no answer to this.

Markets thought they heard a replay of “whatever it takes” in Mr. Draghi’s speech and hit the buy button. But economists heard another note in Sintra: a plaintive appeal for EMU fiscal union before it is too late.

The exhausted monetary warrior was telling us that the ECB cannot alone save the European project a second time.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

end

* * *

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8559/

//OFFSHORE YUAN: 6.8618 /shanghai bourse CLOSED UP 69.32 POINTS OR 2.38%

HANG SANG CLOSED UP 348.29 POINTS OR 1.240%

2. Nikkei closed UP 129.99 POINTS OR 0.60%

3. Europe stocks OPENED ALL GREEN EXCEPT SPAIN/

USA dollar index DOWN TO 96.69/Euro RISES TO 1.1298

3b Japan 10 year bond yield: FALLS TO. –.17/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.68/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 55.30 and Brent: 63.41

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.31%/Italian 10 yr bond yield DOWN to 2.03% /SPAIN 10 YR BOND YIELD DOWN TO 0.37%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.34: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.40

3k Gold at $1381.00 silver at: 15.35 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 45/100 in roubles/dollar) 63.28

3m oil into the 55 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.81 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9864 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1146 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 yearFALLING to –0.31%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.01% early this morning. Thirty year rate at 2.53%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7438..

“Powell Throws In The Towel”: Gold, Global Stocks Soar, S&P At All Time High As Yields Tumble

Risk assets, safe havens? it doesn’t matter: just buy it all as central banks enter the last stretch of the race to the (credibility) bottom.

The global dovish tsunami – still in its jawboning phase – which was started by Mario Draghi on Tuesday and escalated on Wednesday when Fed chair Powell finally threw in the towel and effectively said he would cut rates in July, has resulted in a global scramble for bothrisk assets and safe havens, with global equity markets a sea of green…

… and S&P500 futures at all time high, indicating a record S&P print when the cash market opens…

… even as the 10Y Treasury yield plunged overnight, dropping below 2% for the first time since November 2016 and reaching as low as 1.97% before rebounding.

At the same time, Japan’s 10Y JGB futures hit a new all time high overnight after the central bank telegraphed that it is considering rate flexibility during Kuroda’s press conference following the latest BOJ decision.

Finally, the ultimate safe asset, gold, has surged 1.5% overnight, and has finally broken out above multi-year support as we noted last night.

The rest of the world joined the party, with Europe’s Stoxx 600 Index boosted by gains in technology shares and carmakers. Just like in the US, European stocks and bonds rally simultaneously in the aftermath of the Fed’s dovish tilt yesterday. Euro Stoxx 50 +0.9% to highest since May 6, led by technology, autos and industrials. In rates, Euro-area yields were steady to 4bps lower across the 2-yr through 10-yr tenors, with 10-yr BTPs outperforming bunds by 6bps.

Earlier in the session, Asian stocks also climbed, heading for their best week since January. The MSCI Asia Pacific Index rose for a third day, with communications and finance among the best-performing sectors. Most markets in the region were up, as China and Hong Kong led gains. Chinese stocks rallied the most in Asia with a surge in large caps as risk appetite picked up around the world. Investors adjusted positions before FTSE Russell is set to add A shares to its global indexes for the first time. The Shanghai Composite Index closed 2.4% higher, with Kweichow Moutai and large financial firms offering the biggest boosts, after Chinese President Xi Jinping began a state visit to North Korea. A rally pushed the price of gold surged to the highest level in more than five years, sending shares of gold miners across Asia higher. The Topix gauge advanced 0.3%, driven by SoftBank and Nintendo.

In the latest central bank news:

- Norges Bank, busy building a reputation as one of the world’s most hawkish central banks , unanimously delivered on the promised 25bps June hike, with the Key Rate now at 1.25%, as expected.” Governor Olsen highlighted that the “assessment of the outlook and balance of risks suggests that the policy rate will most likely be increased further in the course of 2019”, with policy forecasts signalling faster rate rises in the coming years. In-fitting with some of the calls, the rate path was left unchanged from the March release.

- The Bank of Japan kept monetary policy unchanged Thursday,

- Indonesia’s central bank signaled it’s ready to cut interest rates.

- The Philippines central bank kept its key rate unchanged.

- RBA Governor Lowe said the possibility of lower rates remain on the table and that it is not unrealistic to expect a further reduction in the Cash Rate. RBA Governor Lowe also commented that recent data suggests we are not making any inroads into the economy’s spare capacity and it is unrealistic to think one 25bps cut can alter the growth path, while he also suggested that it is important to recognize monetary policy is not the only option and that he is very hopeful we will not need to cut as far as some central banks in Europe. (Newswires)

- The Bank of England kept rates unchanged but warned that the risk of a no-deal Brexit is rising, sending cable sliding.

In FX, the Bloomberg USD index tumbled -0.5%, its biggest drop since March 20, as a fresh round of leveraged and real money selling after the London open kept the greenback under pressure. Norway’s krone rallied as Norges Bank signaled its rate hike Thursday may be followed by a similar move later this year, while sterling rose above $1.27 before the Bank of England policy decision.

In the biggest geopolitical news of the day, the Iranian Revolutionary Guard shot down a US drone according to reports citing the state news agency, although the US military later stated that no US aircraft had operated in Iranian airspace. Iran’s Revolutionary Guard Corp Top Commander Salami says the the downing of the US drone sent a clear message to Washington, according to State TV.

In commodities, both Brent ($63.26) and WTI ($55.21) rally as Mideast tensions ratchet up, with gold jumping to the highest level in more than 5 years.

Market Snapshot

- S&P 500 futures up 0.8% to 2,957.50

- STOXX Europe 600 up 0.7% to 387.36

- MXAP up 1.2% to 159.89

- MXAPJ up 1.3% to 525.59

- Nikkei up 0.6% to 21,462.86

- Topix up 0.3% to 1,559.90

- Hang Seng Index up 1.2% to 28,550.43

- Shanghai Composite up 2.4% to 2,987.12

- Sensex up 0.7% to 39,388.97

- Australia S&P/ASX 200 up 0.6% to 6,687.41

- Kospi up 0.3% to 2,131.29

- German 10Y yield fell 1.8 bps to -0.306%

- Euro up 0.6% to $1.1290

- Italian 10Y yield fell 0.6 bps to 1.747%

- Spanish 10Y yield fell 2.9 bps to 0.374%

- Brent futures up 2.6% to $63.46/bbl

- Gold spot up 1.5% to $1,380.15

- U.S. Dollar Index down 0.4% to 96.73

Top Overnight news

- Fed Chairman Jerome Powell made clear that uncertainty — primarily about the president’s trade battles — was a major factor behind the central bank’s policy shift, along with weak inflation

- President Trump told confidants he believes he has the authority to replace Jerome Powell as Fed chairman, according to people familiar with the matter. Powell said he intends to serve his full four-year term

- Bank of Japan kept monetary policy unchanged, just hours after the Fed became the latest central bank to signal a willingness to cut interest rates in the face of rising threats to economic growth

- Australia’s central bank chief Philip Lowe reiterated it was “not unrealistic” to expect a further rate cut

- New Zealand’s economic growth held at a five- year low, leaving the door open for the central bank to cut rates again. GDP rose 2.5% from a year earlier, matching the revised pace for the fourth quarter of 2018

- Norway’s central bank is set to raise rates again as a boom in oil wealth spending and investments put the economy at odds with a global economic cooling

- U.K. Conservative members of Parliament will choose the final shortlist of two candidates to succeed Theresa May as prime minister Thursday, a day after the favorite Boris Johnson stretched his lead to 89 votes; U.K. Chancellor Philip Hammond will urge the Tory leadership contenders to consider holding a general election or second referendum in order to break the Brexit impasse, rather than an economically damaging no-deal exit

- Norges Bank is busy building a reputation as one of the world’s most hawkish central banks as it delivers its third interest- rate hike since September and signals there’s more to come

- U.K. Conservative members of Parliament will choose the final shortlist of two candidates to succeed Theresa May as prime minister, a day after the favorite, Boris Johnson, stretched his lead to 89 votes. Tory MPs are due to vote twice Thursday, each time eliminating one candidate

- The Bank of England must decide whether to temper warnings of future interest-rate hikes as investors and other major central banks prepare for more policy easing. While the Monetary Policy Committee is expected to keep the key rate unchanged on Thursday, Citigroup predicts some votes for an immediate increase

- Iran said it shot down a U.S. spy drone in its airspace, escalating already fierce tensions in the Persian Gulf. The reported drone downing followed a missile strike by Yemeni rebels overnight on Saudi Arabia

Asian equity markets traded mostly positive as the region digested the dovish FOMC. ASX 200 (+0.6%) was led higher by gold names after the precious metal surged to its highest since 2013 but with upside in the broader market capped by weakness in other miners including Rio Tinto after it lowered its iron ore production outlook and with Caltex heavily pressured on disappointing guidance. Nikkei 225 (+0.6%) was also supported in the aftermath of the FOMC although a firmer currency and unsurprising BoJ announcement limited the advances, while Hang Seng (+1.2%) and Shanghai Comp. (+2.4%) outperformed on optimism ahead of the US-China trade talks and as financials surged after continued liquidity efforts by the PBoC. Finally, 10yr JGBs were higher as they tracked the upside in T-notes amid a decline in global yields with the US 10yr yield below 2.00% for the first time since November 2016 and with the 30yr yield also at similar multi-year lows.

Top Asian News

- Japan Bond Futures Climb to Record as Kuroda Signals Flexibility

- Philippine Central Bank Holds Key Rate After Inflation Quickens

- Bank Indonesia Cuts Reserve Ratio for Lenders to Boost Liquidity

- Malaysia Leader Says ‘No Proof’ Russia to Blame for MH17 Downing

European equities are higher across the board [Eurostoxx 50 +0.8%] as the region carries the FOMC-spark gains from Wall Street and Asia overnight. UK’s FTSE 100 (+0.5%) marginally lags its peers as the index is pressured by a firmer Sterling ahead of the BoE Monetary Policy Meeting. Sectors are also broadly in green, albeit financial names lag amid the post-FOMC yield decline. In terms of individual movers, Dixons Carphone (-13%) sunk to the bottom of the Stoxx 600 after the Co. cut guidance. Meanwhile, Fresenius Medical Care (+2.1%) is supported by a positive Barclays broker move. Finally, more bad news for Deutsche Bank (-1.1%) after NYT reported of a criminal probe over alleged money laundering.

Top European News

- BOJ Stands Pat as Fed and ECB Signal Possible Rate Cuts Ahead

- Polish Judges’ Retirement-Age Cut Is Illegal, EU Court Aide Says

- Guindos Says ECB Is Prepared to Act If Situation Deteriorates

- Norges Bank Stuns Markets With ‘Sole Hawk in Town’ Performance

In FX, the Dollar is down across the board as the FOMC matched market expectations by shifting further towards a rate cut, while Fed chair Powell delivered an extra dovish snippet in the press conference by revealing that even those not plotting an ease are more prone towards loosening monetary policy if needed. The has now index lost grip of the 97.000 handle and extended losses towards 96.500, with chart support just below (ie the 96.459 post-NFP low) under threat ahead of weekly claims, Philly Fed and the LEI.

- NOK/NZD/CHF – The G10 outperformers, with the Norwegian Crown benefiting from a hawkish Norges Bank hike on top of the aforementioned Greenback weakness, and also further divergence vs the ECB as the revised rate path pencils in 2 more 25 bp tightening moves (next in September 2019 and 3rd before Summer next year). Usd/Nok and Eur/Nok down to circa 8.5500 and 9.6630 respectively in response. Meanwhile, the Kiwi and Franc drew additional impetus from data in the form of NZ Q1 y/y GDP and Swiss trade, as Nzd/Usd rebounds firmly towards 0.6600 and Usd/Chf retreats sharply through 0.9900, with 0.9850 in sight.

- EUR/AUD/CAD/GBP – The next best majors in terms of gains relative to the Buck, as the single currency tests 1.1300 and unwinds more post-Draghi declines, while the Aussie pivots 0.6900 even though RBA Governor Lowe underscores room for further OCR cuts and the CBA believes back-to-back easing is in the offing with another ¼ point reduction in July. Elsewhere, the Loonie has built on Wednesday’s strong headline Canadian CPI platform to probe 1.3200 offers and psychological resistance and the Pound has reclaimed 1.2700+ status ahead of the BoE amidst market expectations or perceptions that the outturn might be hawkish on balance – see the headline feed or Research Suite for a more detailed preview. Note, not much reaction in Cable to UK retail sales that were weak and came with back data downgrades as the ONS flagged bad weather impacting clothes and footwear in mitigation.

- EM – Broad rallies or rebounds at the Dollar’s expense, but the Lira also gleaning impetus to breach 5.7500 via an improvement in Turkish consumer sentiment, while the Rand is testing 14.2000 in anticipation of SA President Ramaphosa’s SOTU address and the Ruble is getting an oil-related boost and rallied to 63.2400 at one stage.

In commodities, WTI and Brent futures extended on gains in early European trade as the upside seen amid the dovish FOMC was exacerbated by reports that Iran shot down a US spy drone over the Strait of Hormuz, as tensions in the region escalates. WTI futures rose to levels just shy of USD 56.00/bbl whilst its Brent counterpart ran out of steam ahead of USD 64/bbl. Both benchmarks have since come off highs but hold onto a bulk of its gains, amid light news flow in the complex. Elsewhere, gold remains closer to the 1400/oz after having experienced a post-FOMC flash spike, with some attributing the move to a breakout from a five year range. Meanwhile, copper is back above the USD 2.70/lb amid a weaker Dollar and upbeat risk sentiment around the market. Finally, Dalian iron ore hit fresh record highs after Rio Tinto yesterday lowered its Pilbara shipment guidance, suggesting that supply could remain tight despite Vale resuming operations at its Brucutu Mine.

US Event Calendar

- 8:30am: Current Account Balance, est. $124.3b deficit, prior $134.4b deficit

- 8:30am: Initial Jobless Claims, est. 220,000, prior 222,000, Continuing Claims, est. 1.68m, prior 1.7m

- 8:30am: Philadelphia Fed Business Outlook, est. 10.4, prior 16.6

- 9:45am: Bloomberg Consumer Comfort, prior 61.6

- 10am: Leading Index, est. 0.1%, prior 0.2%

DB’s Jim Reid concludes the overnight wrap

By the time you read this I’ll have just taken off on the last flight out of NY back home. The biggest thing waiting for me on my arrival will be knowing whether my 3.75yr old daughter Maisie managed to be persuaded to sleep without her dummy for the first time ever last night. The dentist last week insisted it went ASAP. As such the reason we bought the dolls house furniture earlier in the week was a bribe. When she’s ready to give the dummy to the dummy fairy, said fairy will give her the furniture. Every night this week my wife has asked her if she’s ready to leave her dummy out for the fairy and every night she’s sobbed that she’s not ready. However last night she reluctantly agreed after seeing some of the furniture. My wife said it had to last through the night for the fairy to do the swap. I’ll wait to see what happens.