GOLD: $1414.00 UP $18.00 (COMEX TO COMEX CLOSING)

Silver: $15,40 UP 11 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1419.50

silver: $15.44

We have been witnessing gold and silver rise as I promised you it would once it pierced through $1350 gold/and $15.06 silver.

I would like to point out to you that the derivatives underwritten by the banks against gold and silver are now way offside and you can bet the farm that the banks are burning profusely inside their banking establishments. The crooks have leased and hypothecated just about every oz of gold and silver 500 x over and maybe in more. Ladies and Gentlemen: your end game is now being played out

YOUR DATA…

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/2

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT: 2 NOTICE(S) FOR 200 OZ (0.0063 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 2306 NOTICES FOR 230600 OZ (7.173 TONNES)

SILVER

FOR JUNE

102 NOTICE(S) FILED TODAY FOR 510,000 OZ/

total number of notices filed so far this month: 528 for 2,640,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10959 UP 56

Bitcoin: FINAL EVENING TRADE: $ 10,932 UP 26

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL A HUGE SIZED 7362 CONTRACTS FROM 236,657 DOWN TO 229,295 WITH THE 11 CENT GAIN IN SILVER PRICING AT THE COMEX. HOWEVER THE LOSS IN CONTRACTS WAS DUE TO THE LIQUIDATION OF THE SPREADERS (PLUS COMEX SHORT COVERING) AS WE NOW ARE EXACTLY ONE WEEK BEFORE FIRST DAY NOTICE IN THE JULY SILVER CONTRACT

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JUNE, 1595 FOR JULY. 0 FOR AUGUST, 0 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1595 CONTRACTS. WITH THE TRANSFER OF 1595 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1595 EFP CONTRACTS TRANSLATES INTO 7.97 MILLION OZ ACCOMPANYING:

1.THE 11 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.640 MILLION OZ STANDING FOR SILVER IN JUNE//

WE HAD SOME SHORT COVERING AT THE SILVER COMEX LAST NIGHT..AND MAJOR SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

41,187 CONTRACTS (FOR 16 TRADING DAYS TOTAL 41,187 CONTRACTS) OR 205.905 MILLION OZ: (AVERAGE PER DAY: 2574 CONTRACTS OR 12.87 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JUNE: 205.905 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 29.41% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1076.70 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7362, WITH THE 22 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY(.WITH THE LIQUIDATION OF THE SPREADERS BEING THE CHIEF CULPRIT IN THE DECLINE..) THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1595 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . OUR BANKERS WILL RESUME THEIR LIQUIDATION OF THE SPREAD TRADES FOR SILVER ONCE THE JUNE CONTRACT COMMENCES IN EARNEST….

TODAY WE LOST A GOOD SIZED: 5767 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1595 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 7362 OI COMEX CONTRACTS. AND ALL OF THIS SUPPOSED LACK OF DEMAND HAPPENED WITH A 11 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.29 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.147 BILLION OZ TO BE EXACT or 164% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 102 NOTICE(S) FOR 510,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.640 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

WITH RESPECT TO SPREADING: WE NO DOUBT HAD HUGE ACTIVITY OF SPREADING LIQUIDATION IN SILVER TODAY AS TOTAL OI COLLAPSED (IN TOTAL CONTRAST TO GOLD OI INCREASE)

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCHED TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SILVER OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NO INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF JUNE.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF JUNE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE OPEN INTEREST ROSE BY A SMALL 1217 CONTRACTS, TO 572,893 ACCOMPANYING THE $2.90 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS STOPPED, THESE SPREADERS HAVE ALREADY MORPHED INTO SILVER AND THEY ARE INTO THE LIQUIDATION PHASE OF THEIR OPERATION. THUS THE GAIN IN OI FOR GOLD IS REAL AS INVESTORS ARE MASSIVELY POURING INTO THE GOLD SECTOR . \TODAY IS THE 2ND DAY IN A ROW WHERE THERE IS A HUGE DIFFERENCE BETWEEN THE PRELIMINARY AND FINAL OI NUMBERS IN GOLD.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11,332 CONTRACTS:

APRIL 0 CONTRACTS,JUNE: 0 CONTRACTS, AUGUST 2019: 11,332 CONTRACTS, DEC> 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 572,893. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,549 CONTRACTS: 1,217 CONTRACTS INCREASED AT THE COMEX AND 11,332 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,549 CONTRACTS OR 1,254,900 OZ OR 39.03 TONNES. FRIDAY WE HAD A SMALL GAIN OF $2.90 IN GOLD TRADING.…AND WITH THAT SMALL GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 39.03 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 160,494 CONTRACTS OR 16,049,400 oz OR 499.20 TONNES (16 TRADING DAYS AND THUS AVERAGING: 10,030 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 499.20 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 499.20/3550 x 100% TONNES =14.06% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 2,750.67 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE..EXCHANGE FOR PHYSICALS RISING EXPONENTIALLY THIS MONTH. (ALREADY AT 500 TONNES)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLEDRIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED INCREASE IN OI AT THE COMEX OF 1217 WITH THE SMALL PRICING GAIN THAT GOLD UNDERTOOK ON FRIDAY($2.90)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,332 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,332 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 12,549 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,322 CONTRACTS MOVE TO LONDON AND 1,217 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 39.03 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED ACCOMPANYING THE SMALL GAIN IN PRICE OF $2.90 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX. WE HAD ZERO PRESENCE OF SPREADING ACCUMULATION IN GOLD ///TODAY/

we had: 2 notice(s) filed upon for 200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.90 ON FRIDAY AND $18.00 TODAY//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: (THIS OCCURRED LATE FRIDAY NIGHT)

A MASSIVE PAPER DEPOSIT OF 34.93 TONNES

INVENTORY RESTS AT 799.03 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 11 CENTS TODAY:

NO CHANGES WITH RESPECT TO SILVER INVENTORY AT THE SILVER SLV:

/INVENTORY RESTS AT 319.819 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUMONGOUS SIZED 7362 CONTRACTS from 236,657 DOWN TO 229,295 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AND STOPPED THE LIQUIDATION OF THE SPREADERS IN GOLD

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JUNE 0 CONTRACTS AND JULY: 1595 CONTRACTS FOR AUGUST: 0, FOR SEPT. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1595 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 7362 CONTRACTS TO THE 1595 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A HUGE LOSS OF 5767 OPEN INTEREST CONTRACTS WHICH NO DOUBT WAS CAUSED BY THE LIQUIDATION OF SPREADER COMEX CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 28.87 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY AND NOW 2.640 MILLION OZ FOR JUNE.

RESULT: A HUGE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 22 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 1595 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 6.17 POINTS OR 0.21% //Hang Sang CLOSED UP 39.29 POINTS OR 0.14% /The Nikkei closed UP 27.,35 POINTS OR 0.13%//Australia’s all ordinaires CLOSED UP .17%

/Chinese yuan (ONSHORE) closed DOWN at 6.8766 /Oil UP TO 57.84 dollars per barrel for WTI and 65.16 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8666 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8782 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TR

3A//NORTH KOREA/ SOUTH KOREA

b) REPORT ON JAPAN

3 China/Chinese affairs

i)China/USA

Nouriel Roubini outlines the 3 possible scenarios facing the USA and China in the trade conflict

a very important read..

(courtesy Nouriel Roubini)

Again important documents go astray after Fed Ex misses another delivery of a Huawei pkg.

( zerohedge)

4/EUROPEAN AFFAIRS

i)FRANCE

A good commentary by Gatestone’s Meotti on the divisiveness of France. On one side are the wealthy and the other, the poor. This was brought out by the Islamization of France.

a good read..

(courtesy Meotti/Gatestone)

ii)ECB

Are we about to witness a “Mutiny on the Bounty ” at the ECB?

(courtesy Wolf Richter/.WolfStreet)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran/Saturday.

A very important commentary from Tom Luongo as to the real scoop behind the Iranian drone attack and the mine attack on those two tankers. It is well worth your time to read his thoughts.

(courtesy Tom Luongo)

ii)IRAN/USA

iii)Russia/Iran/USA Europe

iv)Iran/USA

Robert H email to me on the weekend:

a must read….

(courtesy Robert H)

v)Iran/USA

vi)TURKEY

vii)MIDDLE EAST/USA

viii)Despite Trump angry at protecting the shipping lanes despite zero compensation, he is still sending in more warships to the area. Pompeo signals that there will be a international coalition plus new sanctions against a crumbling economy inside Iran.

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

II)MARKET TRADING/USA

ii)Market data/USA

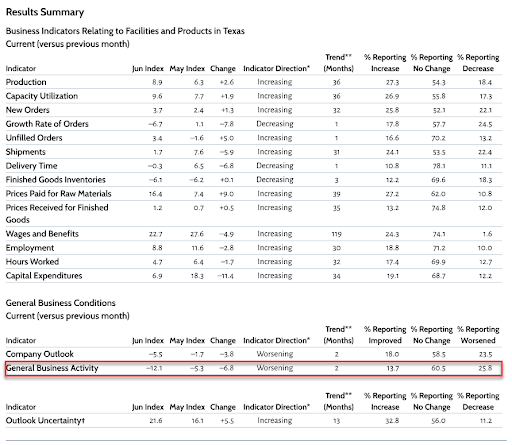

Although a soft entry data point, it certainly gives us a good idea as to what is going on th the USA economy. The Dallas Fed is generally the strongest of the Fed manufacturing reports. It tells us manufacturing strength in the Dallas Fort Worth area. It went from positive 5.3 to negative 12.1 in one month (very contractionary)

(zerohedge)

iii)USA ECONOMIC/GENERAL STORIES

a)Over 400 pilots have joined a class action lawsuit against Boeing accusing the company of an “unprecedented cover up”of “known design flaws” on their top selling Boeing 737 Max.

(courtesy zerohedge)

b)Trump is correct: why is the USA protecting the shipping lanes in the Gulf for zero compensation.

(zerohedge)

SWAMP STORIES

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 2031.684 oz

FOR THE JUNE 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE /2019. contract month, we take the total number of notices filed so far for the month (2306) x 100 oz , to which we add the difference between the open interest for the front month of JUNE. (163 contract) minus the number of notices served upon today (2 x 100 oz per contract) equals 246,700 OZ OR 7.6734 TONNES) the number of ounces standing in this active month of JUNE

Thus the INITIAL standings for gold for the JUNE/2019 contract month:

No of notices served (2306 x 100 oz) + (163)OI for the front month minus the number of notices served upon today (2 x 100 oz )which equals 246,700 oz standing OR 7.6734 TONNES in this active delivery month of JUNE.

We GAINED XX contracts or an additional 1400 oz will stand as these guys refused to morph into London based forwards as well as negating a fiat bonus. Somebody was in need of physical gold badly on this side of the pond.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 10.043 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 7.6734 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS.

total dealer silver: 86.515 million

total dealer + customer silver: 304.571 million oz

The total number of notices filed today for the JUNE 2019. contract month is represented by 102 contract(s) FOR 510,000 oz

To calculate the number of silver ounces that will stand for delivery in JUNE, we take the total number of notices filed for the month so far at 528 x 5,000 oz = 2,640,000 oz to which we add the difference between the open interest for the front month of JUNE. (102) and the number of notices served upon today (102 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE/2019 contract month: 528(notices served so far)x 5000 oz + OI for front month of JUNE( 102) number of notices served upon today (102)x 5000 oz equals 2,640,000 oz of silver standing for the JN contract month.

WE GAINED 1 CONTRACT OR AN ADDITIONAL 5,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND AS WELL THEY ALSO NEGATED A FIAT BONUS. IT SEEMS THAT SOMEBODY WAS BADLY IN NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 229,295 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 236,657 CONTRACTS..(we no doubt had considerable spreading activity as they are now starting to accumulate in silver)

YESTERDAY’S CONFIRMED VOLUME OF 236,657 CONTRACTS EQUATES to 1,118 million OZ 169%% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.95% June 24/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.35% to NAV (june 24/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -1.95%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 13.90 TRADING 13.31/DISCOUNT 4.25

END

And now the Gold inventory at the GLD/

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

june 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

june 7/WITH GOLD UP $3.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

jUNE 6/WITH GOLD UP $8.40 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 5 WITH GOLD UP $6.00 TODAY/STRANGE: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD/INVENTORY RESTS AT 757.59 TONNES

JUNE 4/WITH GOLD UP 0.85 TODAY: A MONSTROUS PAPER GAIN OF 16.44 TONNES/GLD INVENTORY RESTS AT 759.65 TONNES

JUNE 3/WITH GOLD UP $17.50 TODAY: ANOTHER BIG CHANGE, A DEPOSIT OF 2.35 TONNES OF GOLD INTO THE GLD//

MAY 31/WITH GOLD UP $17.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GLD INVENTORY RESTS AT 740.86 TONNES

MAY 30: WITH GOLD UP $6.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES/INVENTORY RESTS AT 740.86 TONNES

MAY 29/WITH GOLD UP $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 737.34 TONNES

MAY 28/WITH GOLD DOWN $6.50 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD> A WITHDRAWAL OF 1.47 TONNES/INVENTORY RESTS AT 737.34 TONNES

MAY 24/WITH GOLD DOWN $1.60 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 738.81 TONNES

MAY 23/WITH GOLD UP $11.10 TODAY: A STRANGE WITHDRAWAL OF .88 TONNES FORM THE GLD/INVENTORY RESTS AT 738,81 TONNES

MAY 22//WITH GOLD FLAT TODAY: WE HAD A GOOD 1.52 TONNES OF GOLD DEPOSIT INTO THE GLD/INVENTORY RESTS TONIGHT AT 739.69 TONNES

MAY 21/WITH GOLD DOWN $3.65 TODAY: A SURPRISE 2.00 TONNES WERE ADDED TO THE GLD GOLD INVENTORY//INVENTORY RESTS AT 738.17 TONNES

MAY 20/WITH GOLD UP $1.00 A HUGE 2.96 TONNE DEPOSIT INTO THE GLD//INVENTORY RESTS AT 736.17 TONNES

MAY 17/WITH GOLD DOWN $9.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 733.23 TONNES

MAY 16/WITH GOLD DOWN $11.50: A WITHDRAWAL OF 3.23 TONNES FROM THE GLD//INVENTORY RESTS AT 733.23 TONNES

MAY 15/WITH GOLD UP $1.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 736.46 TONNES

MAY 14//WITH GOLD DOWN $5.45 TODAY: STRANGE!! THE CROOKS DECIDED TO DEPOSIT A HUGE 3.23 TONNES INTO THE GLD INVENTORY//INVENTORY RESTS AT 736.46 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 24/2019/ Inventory rests tonight at 799.03 tonnes

*IN LAST 616 TRADING DAYS: 134.73 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 516 TRADING DAYS: A NET 30.90 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 6/WITH SILVER UP ANOTHER 9 CENTS TODAY: A FAIR SIZE DEPOSIT OF 630,087 OZ//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 5/WITH SILVER UP 4 CENTS TODAY: A HUGE PAPER DEPOSIT OF 2.396 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 314.434 MILLION OZ//

JUNE 4/WITH SILVER UP 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

JUNE 3/WITH SILVER UP 19 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.038 MILLION OZ//

MAY 31/WITH SILVER UP 6 CENTS TODAY: A DEPOSIT OF 422,000 OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 312.038 MILLION OZ/

May 30/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ///

MAY 29/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 28/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 24/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ/

MAY 23/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 22/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 311.616 MILLION OZ

MAY 21: WITH SILVER DOWN 3 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV; A WITHDRAWAL OF 750,000 OZ///INVENTORY RESTS AT 311.616 MILLION OZ//

MAY 20/WITH SILVER UP 6 CENTS:NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 312.366 MILLION OZ

MAY 17/WITH SILVER DOWN 13 CENTS TODAY: A BIG CHANGES IN SLV: A WITHDRAWAL OF 3.185 MILLION OZ FROM THE SLV INVENTORY VAULTS:/INVENTORY RESTS AT 312.366 MILLION OZ//

MAY 16/WITH SILVER DOWN 26 CENTS: NO CHANGES IN THE SLV INVENTORY//INVENTORY RESTS AT 315.551 MILLION OZ//

MAY 15/WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SLV INVENTORY: A WITHDRAWAL OF 1.031 MILLION OZ// THE SLV/INVENTORY RESTS AT 315.551 MILLION OZ.

MAY 14/WITH SILVER UP 2 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV. INVENTORY RESTS AT 316.582 MILLION OZ/

Gold Hits New 6 Year High on Dovish Central Banks and Iran Risk

News and Commentary

Gold Hovers Near Six-year High as Dovish Central Banks, U.S.-Iran Tensions Fuel Demand

Gold Gains to Near Highest Since 2013 as Bulls ‘back in Control

The Gold ETF Continues to Set New Highs as Commodities Rebound and the Dollar Slumps

Iran Says It Will Confront Any U.S. Threat, Trump Eyes New Sanctions

World is Crazy and the Dollar is Lower. Gold is Above $1,400 for First Time in Years

“If You Don’t Own Gold, Get Some” – Stepek

Gold is Still the Hardiest of Hardy Annuals – Kinsella

Dollar Bear Market Called as Gundlach Sees Moment of Truth

Ron Paul: “it Was All a Lie. Qe Failed and is No Longer Just a “temporary” Measure” (Video)

Gold Stages Major Breakout, Breakout Retest Likely

LBMA Gold Prices (AM/ PM Fix – USD, GBP & EUR)

21-Jun-19 1388.35 1397.15, 1095.96 1101.93 & 1228.55 1233.12

20-Jun-19 1381.65 1379.50, 1086.25 1087.74 & 1222.90 1221.27

19-Jun-19 1342.40 1344.05, 1066.67 1066.64 & 1198.36 1199.43

18-Jun-19 1344.55 1341.35, 1073.22 1070.67 & 1201.89 1198.09

17-Jun-19 1333.20 1341.30, 1059.49 1065.13 & 1188.81 1193.09

14-Jun-19 1352.45 1351.25, 1069.79 1070.33 & 1200.03 1201.80

13-Jun-19 1335.80 1335.90, 1054.21 1052.69 & 1182.85 1184.81

12-Jun-19 1336.65 1332.35, 1049.27 1045.76 & 1179.99 1177.26

11-Jun-19 1322.65 1324.30, 1040.53 1041.30 & 1168.96 1170.42

10-Jun-19 1328.60 1328.60, 1046.94 1048.66 & 1175.41 1175.94

07-Jun-19 1334.30 1340.65, 1049.16 1052.14 & 1184.19 1184.60

And they scoff that gold doesn’t pay interest, though leasing it does

Submitted by cpowell on Sat, 2019-06-22 14:47. Section: Daily Dispatches

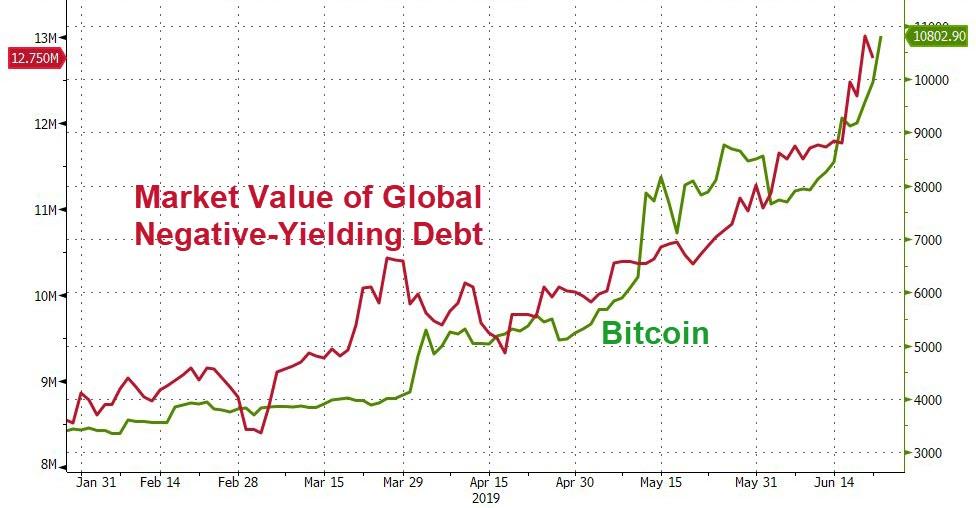

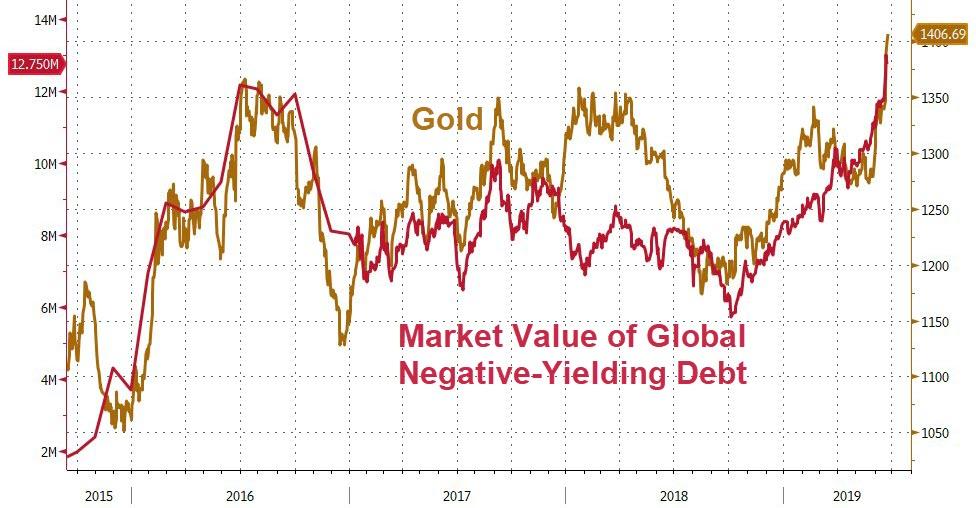

The World Now Has $13 Trillion of Debt With Below-Zero Yields

By Adam Haigh

Bloomberg News

Thursday, June 20, 2019

The universe of negative-yielding bonds grew about $1.2 trillion this week after dovish messages from central banks in Europe and the U.S., pushing the total past $13 trillion for the first time.

Joining the club of government debt with 10-year yields below zero this week were Austria, Sweden, and France. Japanese and German rates plumbed fresh all-time lows amid a global bond rally that even got Wall Street pondering life with Treasuries yields under 1%.

…

The message from the markets is that there are problems out there that central banks, not just the Fed, are now responding to,” Ed Hyman, Evercore ISI chairman, told Bloomberg TV.

In Europe, another notable milestone was reached this week. Yields on Danish debt due to mature 20 years from now dropped to a record low, leaving the entire curve within an inch of turning negative. Some 40% of global bonds are now yielding less than 1%, according to data compiled by Bloomberg. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-06-21/the-world-now-has-13-…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

Michael Oliver has Kingworldnews commented correctly that gold started to rise before the dollar fell

(courtesy GATA/Kingworldnews)

Gold was rising even before dollar started falling, Michael Oliver tells KWN

Submitted by cpowell on Sat, 2019-06-22 15:27. Section: Daily Dispatches

11:25a ET Saturday, June 22, 2019

Dear Friend of GATA and Gold:

Interviewed at King World News, Michael Oliver of MSA Research says that gold has been rising in recent months without any weakness in the U.S. dollar, and now the dollar index is breaking down, which, he expects, will elevate gold and gold mining stocks even more. The interview is 14 minutes long and can be heard at KWN here:

https://kingworldnews.com/michael-oliver-6-22-2019/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

An excellent commentary today from Michael Kosares..well worth reading..

(mike Kosares/GATA)

Mike Kosares: This has been and is likely to remain gold’s century

Submitted by cpowell on Sat, 2019-06-22 16:55. Section: Daily Dispatches

12:55p ET Saturday, June 22, 2019

Dear Friend of GATA and Gold:

Investment-wise the 21st century so far has belonged to gold, USAGold’s Mike Kosares writes today, as the monetary metal has quietly outperformed equities, though equities have gotten most of the attention.

Kosares concludes: “The question becomes whether an investment that has performed so well in the past is likely to perform equally well in the future. Though nothing in the world of finance and economics is certain, we rest the bullish case for gold on the understanding that none of the economic and financial system problems that created a positive price environment for gold over the last nearly 19 years has been removed from consideration. In fact, a case could be made that they have only intensified — and dangerously so.”

Kosares’ commentary is headlined “Gold’s Century” and it’s posted at USAGold here:

https://www.usagold.com/cpmforum/golds-century/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

We now have another entity acknowledging the likelihood of gold price suppression

(Peak Prosperity/GATA)

Peak Prosperity acknowledges likelihood of gold price suppression

Submitted by cpowell on Sat, 2019-06-22 20:22. Section: Daily Dispatches

4:25p ET Saturday, June 22, 2019

Dear Friend of GATA and Gold:

With Adam Taggart’s essay about gold today, Peak Prosperity finally acknowledges “it’s highly likely that the price has been suppressed.” Who’s next — Pierre Lassonde? Mark Carney? The Financial Times? The Economist? Even the World Gold Council?

Better late than never, we may suppose, even if this evokes the observation by Mad magazine’s Alfred E. Neuman that some people are like blisters — they show up right after the work’s been done.

Taggart’s commentary is headlined “‘Somebody’ Finally Cares About Gold” and it’s posted at Peak Prosperity here:

https://www.peakprosperity.com/somebody-finally-cares-about-gold/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A new book which I am going to get explaining how Switzerland has handled itself in gold form the time of the Nazis to now

(courtesy Dominique Soguel dit Picard/GATA)

From Nazis to refineries: How Switzerland has handled the world’s gold

Submitted by cpowell on Mon, 2019-06-24 02:56. Section: Daily Dispatches

By Dominique Soguel-dit-Picard

Swiss Info, Bern, Switzerland

Sunday, June 23, 2019

A new book exposes the dark history of gold laundering in Switzerland and the modern challenge of cleaning up a lucrative industry. This is the story of the Alpine nation’s dominance over global gold trade.

Written by Swiss anti-corruption watchdog Mark Pieth, “Gold Laundering — The Dirty Secrets of the Gold Trade and How to Clean Up” — shines a light on the key players in the gold industry, the risks associated with large-scale versus artisanal mining, and the shortcomings of various international regulations and certification schemes.

How did we get here? In a discussion with swissinfo.ch, Pieth explained how Switzerland came to be at the heart of a highly profitable but opaque trade. These are some of the key historical moments in the Swiss gold story, according to him. …

… For the remainder of the report:

https://www.swissinfo.ch/eng/historical-book_from-nazis-to-refineries–h…

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 6.8766/ GETTING VERY DANGEROUSLY CLOSE TO 7:1

//OFFSHORE YUAN: 6.8782 /shanghai bourse CLOSED UP 6.17 POINTS OR 0.21%

HANG SANG CLOSED UP 39.29 POINTS OR 0.14%

2. Nikkei closed UP 27.35 POINTS OR 0.13%

3. Europe stocks OPENED ALL RED

USA dollar index DOWN TO 96.05/Euro RISES TO 1.1371

3b Japan 10 year bond yield: RISES TO. –.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.28/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.84 and Brent: 65.16

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.31%/Italian 10 yr bond yield UP to 2.12% /SPAIN 10 YR BOND YIELD DOWN TO 0.41%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.53: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 2.42

3k Gold at $1409.20 silver at: 14.38 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 15/100 in roubles/dollar) 62.89

3m oil into the 57 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.28 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9749 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1107 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now NEGATIVE territory with the 10 year FALLING to –0.31%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.03% early this morning. Thirty year rate at 2.53%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.7520..

S&P Futures Trade Near Record High As European Stocks, Dollar Stumble Ahead Of G20

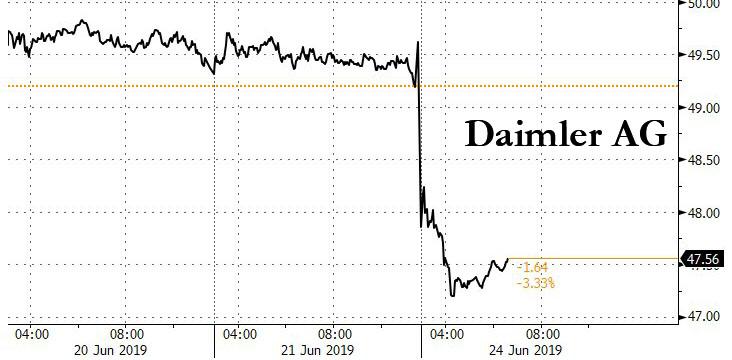

S&P futures levitated on Monday, rising to a high of 2,962 and just shy of a new record, alongside buoyant Asian stocks while European shares slumped as the Stoxx 600 Index reversed an earlier gain following the third profit warning from Daimler, and a slump in German business confidence; the dollar dropped to three-month lows as hopes waned for progress in China-U.S. trade talks at this week’s G20 meeting, while Trump was expected to announce even harsher sanctions against Iran today.

The European Stoxx 600 index fell 0.2%, reflecting losses in Paris and Milan. Stocks in London were little changed. Germany’s export-sensitive DAX fell 0.5% after a profit warning by Daimler caused its shares to drop nearly 5%.

Europe’s woes were compounded by the latest slump in German business confidence as trade tensions weighed on manufacturers. The June Ifo Business Confidence dropped to 97.4, its lowest level since late 2014, while an index of expectations also worsened, even though the news was largely priced in and the euro barely moved on the news and was up 0.2% at $1.1392 in early trading.

“It could get worse, maybe not much worse but a little,” said Ifo President Clemens Fuest in a Bloomberg Television interview. “It’s justified to at least postpone any tightening of monetary policy. But I don’t think further easing will help very much. Mario Draghi has rightly pointed out that governments need to use other instruments.”

Earlier in the session, gains in Asia saw the MSCI regional and global stocks gauges rise again towards last week’s six-week highs. Asian stocks advanced, led by health care and consumer discretionary firms, as investors awaited possible new sanctions against Iran and gauged the probability of a U.S.-China trade deal later this week. Markets were mixed in the region, with Australia climbing and Singapore retreating. Japan’s Topix reversed earlier losses to close 0.1% higher, with Sony and Daiichi Sankyo among the biggest boosts. The Shanghai Composite Index advanced 0.2% as U.S. and China trade teams prepared for a meeting between Donald Trump and Xi Jinping on the sidelines of the G-20 summit in Japan. The S&P BSE Sensex Index edged 0.2% lower, driven by Reliance Industries and Infosys, as India’s central bank deputy chief Viral Acharya asked to resign from his post

Investors are waiting to see if Presidents Donald Trump and Xi Jinping can de-escalate a trade war that is damaging the global economy and souring business confidence. The leaders will meet during a G20 summit in Japan which starts on Friday. Wall Street also looked in line for more gains after closing lower on Friday. S&P 500 e-minis pointed to a 0.2% rise at the open.

China Vice Commerce Minister Wang Shouwen said China and US trade teams are having discussions, while he added that both sides should make compromises and hopes G20 sends a clear signal on fighting against trade protectionism. At the same time, China Assistant Foreign Minister Zhang Jun said the world economy faces increasing risks and the international community recognizes harm from protectionism, while he added that G20 should ensure unity and cooperation but also stated that China will safeguard its fundamental interests and will not allow anyone to interfere with its internal affairs no matter what forum.

“G20 is turning into a high-stakes poker game for risk, and if the sideline talks between Trump and Xi fail and trigger an escalation in tariffs, the odds of a full-blown global recession increase exponentially,” said Stephen Innes, managing partner at Vanguard Markets.

On Monday, Chinese Vice Commerce Minister Wang Shouwen said China and the United States should be willing to compromise in trade talks and not insist only on what each side wants. U.S. Vice President Mike Pence’s decision on Friday to call off a planned China speech was also considered a positive sign. Pence had upset China with a fierce speech in October that laid out a litany of complaints ranging from state surveillance to human-rights abuses.

Still, virtually all analysts doubt the two sides will come to any meaningful agreement. Tensions are reaching beyond tariffs, particularly after Washington blacklisted Huawei, the world’s biggest telecoms gear maker, effectively banning U.S. companies from doing business with it.

“Any high hopes ahead of the G20 meeting may be disappointed,” said Benjamin Schroeder, senior rates strategist at ING in Amsterdam. “In the end, uncertainty will persist and central banks could still be pushed closer to invoking their contingency plans.” (For Goldman’s preview of what to expect at the G-20, see this article).

Overnight, a Chinese newspaper said FedEx Corp was likely to be added to Beijing’s “unreliable entities list” following yet another delivery fiasco involving a Huawei shipment.

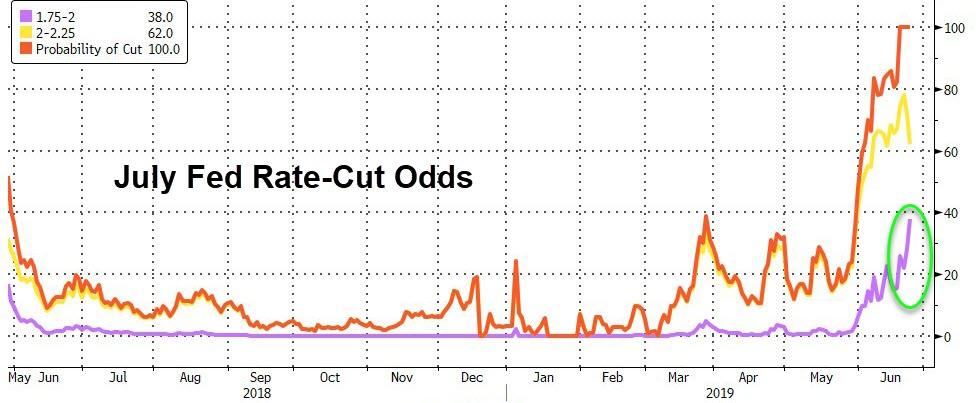

In FX, the dollar index slipped 0.1% lower to 96.11 after its biggest weekly drop in four months last week, when the Federal Reserve said that it may cut interest rates soon to bolster the U.S. economy. The dollar has led a broad selloff in major currencies as global central banks signaled a dovish outlook on monetary policy amid growing signs of a weak global economy. The dollar fetched 107.39 yen, having slipped as low as 107.045 on Friday, the lowest level since its flash crash on Jan. 3.

“The market is not expecting more Fed rate cuts than it had so far, but that the reasoning behind them is being interpreted in a different manner,” Commerzbank’s head of FX and commodity research, Ulrich Leuchtmann, wrote in a note to clients. “While for a long time the expected weakening of growth, fears of a recession and low inflation were used as reasons for rate cuts, another reason has now been added to the list: the Fed caving in to the White House.”

The euro rose to a three-month high of $1.1387 against the dollar, while the Aussie gained for a fifth day as central bank Governor Philip Lowe said there are limits to what further monetary easing can achieve. In developing markets, the Turkish lira strengthened as much as 2% after Turkey’s main opposition party won Istanbul’s re-run election for mayor, a blow to President Tayyip Erdogan.

In rates, European government bonds climbed alongside U.S. Treasuries, where 10- year yields fell 2bps to 2.03%, its first decline in two days.

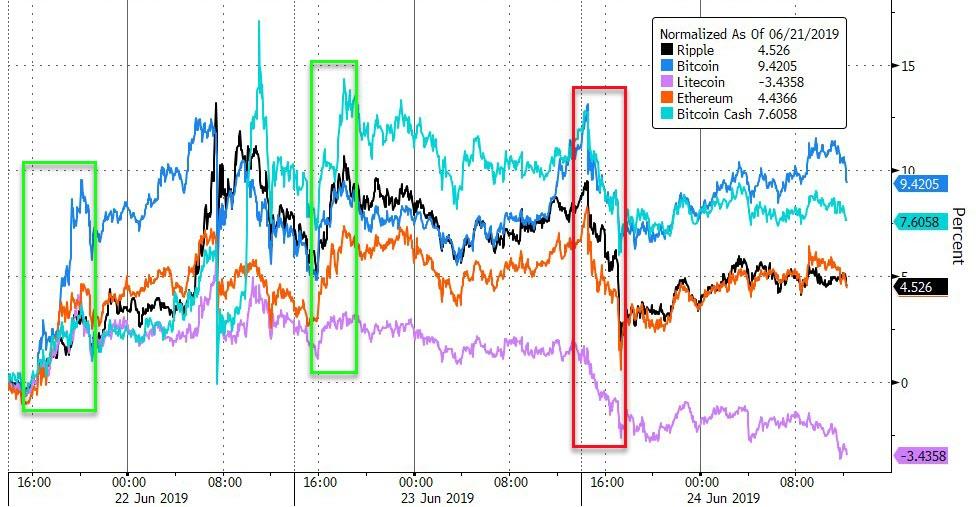

In cryptos, the resurgent Bitcoin pulled back from 18-month highs after jumping more than 10% over the weekend. Analysts said the gains came amid growing optimism over the adoption of cryptocurrencies after Facebook announced its Libra digital coin.

Meanwhile, gold resumed its rise amid economic woes, looming U.S. interest rate cuts and tensions between Tehran and Washington: the precious metal stood at $1,404.79 per ounce, not far from Friday’s six-year high of $1,410.78. The rising tensions between Iran and the United States, after Iran shot down an American drone, also pushed oil prices higher. U.S. Secretary of State Mike Pompeo said “significant” sanctions on Tehran would be announced.

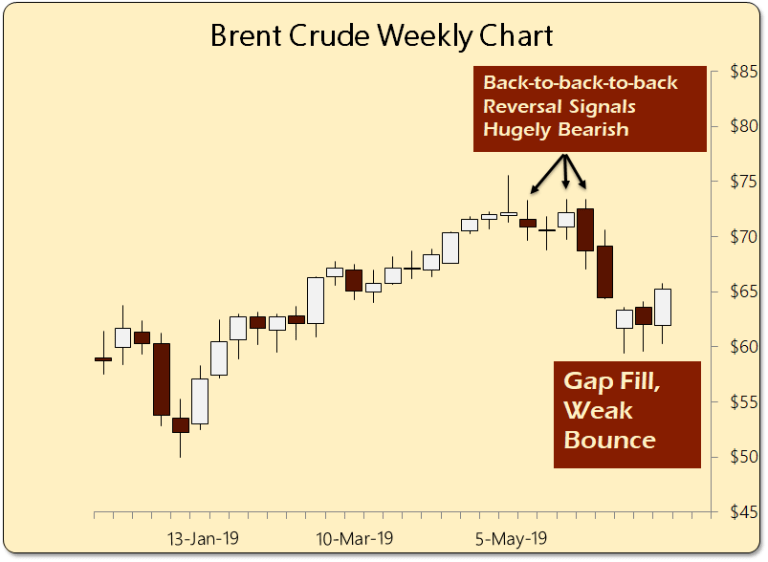

Brent crude futures rose 0.4% to $65.42 per barrel, near Friday’s three-week high of $65.76. U.S. crude futures were up 0.9% at $57.91, standing at its highest in over three weeks

Over the weekend, President Trump said that they are moving ahead with additional sanctions on Iran aimed at preventing it from getting a nuclear weapon and that military action is still on the table, while other reports also noted the White House is pressing for additional options including in cyberspace and other additional clandestine plans to counter Iranian aggression in the Persian Gulf. Subsequently, Iranian Navy Commander says the downing of the US Spy drone was a “firm response” and can be repeated, according to Tasmin News. Russian Deputy Foreign Minister says Russia and allies will counteract US sanctions on Iran. Additionally, Russia’s Deputy Foreign Minister stated that the US is deliberately increasing tensions with Iran.

Today’s expected data include Chicago Fed National Activity Index and Dallas Fed Manufacturing Outlook. No major company is scheduled to report earnings

Market Snapshot

- S&P 500 futures up 0.2% to 2,957.25

- STOXX Europe 600 down 0.2% to 384.00

- MXAP up 0.3% to 159.71

- MXAPJ up 0.2% to 525.93

- Nikkei up 0.1% to 21,285.99

- Topix up 0.1% to 1,547.74

- Hang Seng Index up 0.1% to 28,513.00

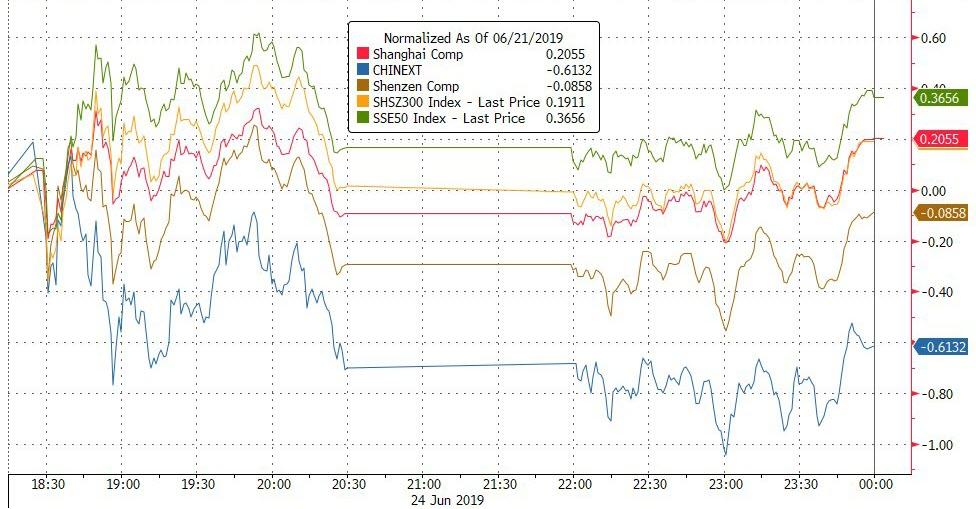

- Shanghai Composite up 0.2% to 3,008.15

- Sensex down 0.2% to 39,127.17

- Australia S&P/ASX 200 up 0.2% to 6,665.44

- Kospi up 0.03% to 2,126.33

- German 10Y yield fell 1.0 bps to -0.295%

- Euro up 0.2% to $1.1392

- Italian 10Y yield rose 0.4 bps to 1.786%

- Spanish 10Y yield fell 2.2 bps to 0.416%

- Brent futures up 0.5% to $65.52/bbl

- Gold spot up 0.3% to $1,404.21

- U.S. Dollar Index down 0.2% to 96.07

Top Overnight News from Bloomberg

- In the first signs of negotiations since talks broke down in May, U.S. and Chinese trade teams are discussing next steps after Presidents Donald Trump and Xi Jinping agreed to meet on the sidelines of the upcoming Group of 20 summit in Japan, a senior trade official said in Beijing

- Turkish opposition candidate Ekrem Imamoglu won the redo of the Istanbul mayor’s race by a landslide on Sunday, in a stinging indictment of President Recep Tayyip Erdogan’s economic policies and his refusal to accept an earlier defeat

- Turkish President Recep Tayyip Erdogan, weakened by an opposition party’s landslide victory in Istanbul’s repeat election, scrambled to reassert his standing as the country’s most dominant politician in half a century by refocusing attention on a crucial trip to Asia

- Australian central bank chief Philip Lowe threw his support behind those casting doubt on how effective a new round of monetary policy easing by major economies would be in supporting global growth

- President Trump is threatening Iran with additional sanctions as soon as Monday, but there’s not much left for the U.S. to target because most of the Islamic Republic’s economy is already crippled under the weight of financial restrictions. Oil gains on the threat of new sanctions against Iran

- Viral Acharya, deputy governor of the Reserve Bank of India, resigned six months before his term ends, Business Standard reported, citing him

- Boris Johnson faces mounting pressure to submit to public scrutiny, after his rival in the race to be U.K. prime minister tried to turn questions about the front-runner’s character to his advantage

- President Trump denied that he’d threatened to demote Federal Reserve Chairman Jerome Powell but said he’d “be able to do that if I wanted”

- President Trump sent North Korean leader Kim Jong Un a personal letter, and the U.S. is ready to restart talks with Pyongyang “at a moment’s notice,” Secretary of State Michael Pompeo said

- New Zealand plans to introduce a bank deposit protection regime to bring it into line with other developed nations and increase public confidence in its lenders

- A slump in German business confidence deepened in June as trade tensions weighed on manufacturers. U.S.-led protectionist threats have clouded the growth outlook in Europe’s largest economy for months, contributing to a manufacturing slump

- The Reserve Bank of India will lose one of its most outspoken officials, further raising questions about the independence of the central bank six months after the governor resigned under a cloud. Deputy Governor Viral Acharya has asked to leave the central bank not later than July 23, 2019, citing “unavoidable personal circumstances”

Asian equity markets began the week somewhat choppy with participants tentative ahead of the Trump-Xi meeting at the G20 this week and following the mild pullback last Friday on Wall St where all majors ended slightly lower on the day, but still notched gains of more than 2% for the week. ASX 200 (+0.2%) was initially led lower by underperformance in Consumer Staples and as comments from RBA Governor Lowe appeared to question the impact easing could have on the economy, while a non-committal tone was seen in the Nikkei 225 (+0.1%) amid a mixed currency. Hang Seng (+0.2%) and Shanghai Comp. (+0.1%) were indecisive after the PBoC refrained from open market operations and as global markets await the latest developments in the trade war saga including the Trump-Xi showdown this week, while the US recently added 5 Chinese entities to its blacklist barring them from buying US parts without government approval. Finally, 10yr JGBs were subdued with after recent similar moves in T-notes and as yields bounced back from multi-year lows, while demand was also dampened after stocks in Tokyo pared opening weakness and amid the absence of the BoJ in the market.

Top Asian News

- India Poised to Lose Outspoken Central Banker as Acharya Resigns

- Pakistan to Get $3b in Deposits, Investments From Qatar

- China Is Going Bananas for Bananas as Purchases Surge to Record

- Nostrum Oil & Gas Studies Options Including Sale of Company

A choppy day for European equities thus far [Eurostoxx 50 -0.4%] following on from a similar Asia-Pac session as markets await the Trump-Xi showdown later this week. Major bourses are mostly in the red, losses for the DAX (-0.5%) stem from declining auto names after Daimler (-4.7%) issued its third profit warning in 12 months, citing losses caused by the diesel emission scandal; hence, Volkswagen (-1.2%) and BMW (-1.2%) have fallen in sympathy. Sectors are also lower with consumer discretionary names pressured by Daimler’s profit warning. In terms of individual movers, Leonardo (+2.4%) shares spiked higher at the open amid speculation that the Co. is considering bidding for Maxar Technologies’ space robotics business, which sources state could be valued over USD 1bln. Meanwhile, Carrefour (+1.6%) shares are underpinned after it reached an agreement to sell 80% of its Chinese operations with the transaction representing an enterprise value of EUR 1.4bln. Finally, Morphosys (+7.2%) shares are bolstered amid news that a treatments primary endpoint was met.

Top European News

- German Business Confidence Takes Another Dive as Economy Wobbles

- Italy Wins Temporary Reprieve in Bid to Stop EU Punishment

- Hunt Says Johnson Dodges Scrutiny as Race for U.K. PM Heats Up

- Santander Pays Allianz $1.1b to Terminate Spanish Venture

In FX, the USD has fallen further following last week’s dovish Fed policy meeting and Friday’s relatively weak PMIs, with the DXY faltering after a fleeting attempt to pare losses and probe above 96.200. The 96.000 handle looks under threat and could be relinquished amidst strength elsewhere, with Gold edging back over Usd 1400/oz and Eur/Usd eyeing 1.1400. Note also, the pressure could build as the week unfolds with at least one currency rebalancing model flagging a strong sell signal for the end of June, Q2 and H1, not to mention the G20 where US President Trump is due to meet his Chinese counterpart Xi for extensive trade talks.

- NZD/AUD – Perhaps surprisingly given ongoing global trade and geopolitical uncertainty, the Antipodean Dollars are outperforming major peers, or rather deriving most momentum from their US rival’s demise. The Kiwi is pivoting 0.6600 and Aussie 0.6950 ahead of this week’s RBNZ meeting on Wednesday with rates widely tipped to remain unchanged before another cut in August, while comments from RBA’s Lowe may have dampened some dovish expectations as he questioned the effectiveness of easing to support the economy in the context of moves by other Central Banks aimed at sustaining growth and reaching inflation targets.

- CAD/EUR – The next best G10 currencies, as the Loonie consolidates recovery gains through 1.3200 after its post-Canadian retail sales wobble, with some support from firmer crude prices, and the Euro draws encouragement from the latest German Ifo survey that was not as weak as forecast overall. Moreover, the institute maintained its 2019 GDP estimate and played down the prospect of a recession even though the economy is in the doldrums, or heading that way. However, Eur/Usd has tested the 50 DMA (1.1390) after clearing 200 DMA and WMAs, but falling just short barriers at the next big figure where the top end of 2 bn option expiries lie (from 1.1390 coincidentally).

- CHF/GBP/JPY – All narrowly mixed vs the Buck as the Franc stalls ahead of 0.9750 and Pound meets resistance above 1.2750 in the form of a 38.2% retracement of the fall from 1.3185 to 1.2506 at 1.2766. Meanwhile, the Yen has retreated a bit further from 107.00 and into a 107.29-48 band with technical support seen a fraction under (107.27 Fib) and decent expiry interest a whisker above (1.3 bn at the 107.50 strike).

- EM – The Lira has rebounded further from recent lows and in large part on the back of a resounding result at the 2nd Istanbul election that will not be contested this time. Indeed, President Erdogan congratulated the victor after the landslide saw Imamoglu defeat ex-PM Yildirim by whopping 800k votes. Usd/Try is hovering towards the bottom of a 5.7085-8200, with additional support for the Lira from an improvement in Turkish manufacturing sentiment.

In commodities, WTI and Brent futures have retreated from highs in recent trade as the upside momentum seen in the complex somewhat wanes ahead of this week’s US-Sino meeting. Over the weekend, US President Trump announced the intention of further tariffs on Iran to stem the country’s nuclear developments, although Russia’s Deputy Foreign Minister noted that the US is deliberately raising tensions with Iran and stated that Moscow and allies will counteract US sanctions on Tehran. WTI futures hover around USD 58/bbl (having hit an intraday high of USD 58.20/bbl) whilst its Brent counterpart trades just below the USD 65.50/bbl mark and closer to the bottom of today’s range. Elsewhere, gold prices hover around 6yr highs amid dovish central banks and rising tensions in the Middle East. Meanwhile, copper prices declined back below the USD 2.7/lb level as the red metal side-lines strikes at Chile’s Chuquicamata copper mine and takes the cue from the subdued risk tone heading into the G20 summit. Finally, Chinese Rebar steel traded near eight-year highs as demand picks up while output curbs have been extended in an attempt to reduce air pollution.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0, prior -0.4

- 10:30am: Dallas Fed Manf. Activity, est. -2, prior -5.3

DB’s Jim Reid concludes the overnight wrap

Welcome to the last week of June and ever longer nights here in the northern hemisphere. Many months ago I got time off for good behaviour and booked in to play a 2 day golf tournament over this past weekend. It had a cut at the halfway stage to qualify for Sunday’s final round. However our recent weekends have been busier than anticipated and we desperately needed time to buy two sofas for the new house. After high level negotiations we agreed that if I missed the cut we’d go sofa shopping Sunday morning. If there was a greater motivation to play well then this was it. All Saturday all I could think of when I stood over the ball was that if I made a mistake then I’d have to spend hours the next day comparing different levels of cushion comforts and fabrics. Alas that pressure proved too much and Sunday was spent with scatter cushions and not scattering it around the golf course as I did on Saturday. I wonder if Rory and Tiger are under the same pressure to make the cut at the Open.

I hope there are some nice sofas in Osaka next weekend as the main event this week will be the much anticipated G-20 summit on Friday and Saturday with the Trump/Xi meeting on the sidelines of the utmost importance. It’ll also be interesting to see what global leaders make of trade tensions and the recent growth slowdown, and whether the US will sign up to the accord. Back to US/China tensions, today’s multiple times rearranged speech from VP Pence – expected to be critical of China – has again been postponed as progress seems to be being made between the two sides. So there will be hope that positivity can continue to extend after they meet. If it doesn’t the problem is that the tariffs on the last $300bn of Chinese exports into the US will be very close to being ready to be imposed. So a bit binary but the fact that they are meeting means that we’re in a better place that we were this time last week. Staying with global politics, the US/Iran relationship darkened further last week and over the weekend the US national security adviser suggested fresh sanctions could come as early as today. So another one to watch especially as it appeared that Mr Trump pulled back from planned military strikes last week. He did appear a little conciliatory over the weekend and suggested he is ready for talks. WTI crude oil price is trading up +0.66% this morning.

Just on that upcoming meeting between Trump and Xi, China’s Vice Commerce Minster Wang Shouwen said overnight that “Compromise will be on both sides. It will be a two-way street,” while adding that China’s principles for the trade talks remain the same, including “mutual respect, treating each other as equals, win-win outcomes, working together and respecting the rules of the World Trade Organization.” To highlight that talks will not be easy, the Trump administration has put five more Chinese tech entities on a trade blacklist. The accompanying statement from the US Commerce Department said the new entities listed were part of China’s efforts to develop supercomputers. It said they raised national security concerns because the computers were being developed for military uses or in cooperation with the Chinese military. Companies added to the backlist included AMD’s Chinese joint-venture with partner Higon – THATIC, Sugon, Chengdu Haiguang Integrated Circuit and Chengdu Haiguang Microelectronics Technology.

Asian markets have started the week generally on a slightly firmer footing with the Nikkei (+0.19%), Hang Seng (+0.23%) and Kospi (+0.08%) all up while the Shanghai Comp (-0.09%) is down. Elsewhere futures on the S&P 500 are trading +0.32%. Elsewhere, in mayoral re-elections in Istanbul, opposition candidate Ekrem Imamoglu won 54% of the vote, with the ruling AK Party’s candidate, former Prime Minister Binali Yildirim capturing 45% (per Bloomberg). The report further added that Turkish President Erdogan, who had called for re-election post Imamoglu’s previous win, accepted the outcome of the rerun but has hinted the new mayor could run into legal problems. He suggested Imamoglu might be tried for allegedly insulting a provincial governor, and a prison sentence could lead to his ouster. The Turkish lira is trading up +0.79% this morning. Staying in Europe, the FT has reported overnight (citing sources) that the European Commission won’t formally trigger its excessive deficit procedure for Italy during a meeting tomorrow. The report also added that the Italian PM Giuseppe Conte is determined to follow EU budget rules to avoid an infringement procedure. This seems to be trying to buy both sides some time to come to an agreement.

In other news, the US President Trump continued with his attack on the Fed Chair Powell by saying in a NBC’s interview, conducted Friday and broadcast on Sunday, that “I’m not happy with his actions. No, I don’t think he’s done a good job.” He also denied that he’d threatened to demote Federal Reserve Chairman Jerome Powell but said he’d “be able to do that if I wanted.”

Moving on, in terms of key data this week, the highlights in the US this week include Durable Goods (Wednesday), final Q1 GDP revisions (Thursday) and PCE inflation (Friday). We’ll also get plenty of survey data. Fed Chair Powell will speak (Tuesday) and part two of the Fed’s stress tests results will be released (Thursday) after all passed in round one late on Friday. In US politics, on Wednesday twenty contenders for the Democratic presidential nomination are due to debate over two nights. This includes Senator Elizabeth Warren and front runner Joe Biden. In Europe today’s IFO in Germany is going to be important and given that 5yr5yr Euro inflation swaps hit record lows last week prior to Sintra, June’s CPI reports in Europe (Thursday and Friday) will be of note. The full day by day week ahead is published at the end.

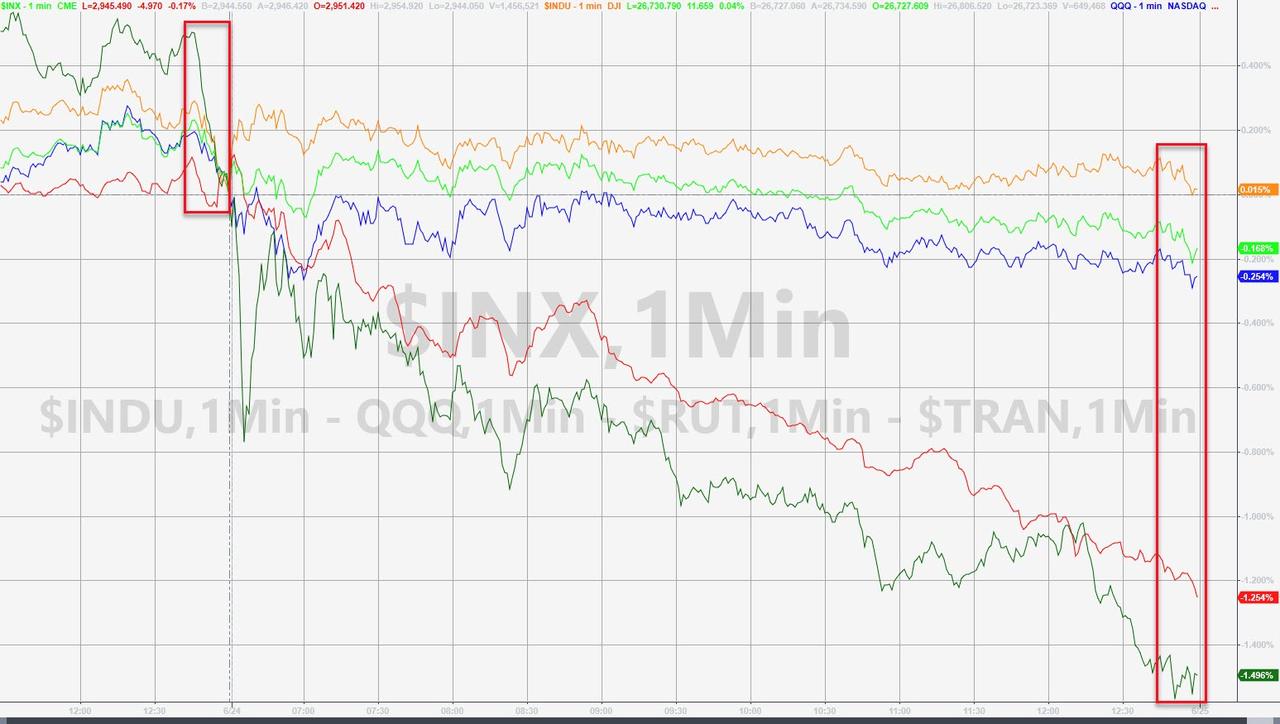

After a busy week of macro news, Friday turned out to be relatively calm. For the most part, market moves were minor retracements of the week’s earlier action, with equities giving back a part of their gains, rates rising slightly after their big rally, and credit spreads widening a touch. The most noteworthy data on Friday, the flash PMIs in Germany, France, and the US, was mixed, with European readings doing better than expected but the US’s falling to a post-crisis low. The S&P 500 ended the week +2.20% (-0.13% Friday) and touched a new all-time high closing level on Thursday, while the NASDAQ and DOW made similar moves, up +3.01% and +2.41% (-0.24% and -0.13% Friday) respectively. In Europe, the STOXX index ended +1.57% (-0.36%) and Italian equities outperformed, with the FTSE MIB up +3.77% (+0.13% Friday). High yields credit spreads ended the week -16bps and -35bps tighter in the US and Europe (+1bps and -1bps Friday).

The moves in currencies continued their trends from earlier in the week, with the dollar dropping -1.40% (-0.44% Friday) and the euro gaining +1.43% (+0.66%). Oil also continued to rally, with WTI staging its strongest week since 2016 as US-Iran tensions heated up. That rally was worth +9.81% (+1.78%) for WTI, and a relatively more modest +5.40% (+1.41% Friday) for Brent. Gold advanced +4.28% (+0.77% Friday) to its highest level in five years. Energy-linked stocks performed well, with the S&P energy sector up +5.16% (+0.82% Friday), and the higher prices also sparked a move higher in inflation breakevens. Five year-five year inflation swap rates rose by +17.0bps and +6.3bps (+0.04bps and -0.8bps Friday) in the euro area and US, respectively after the central bank moves of last week. Those moves in inflation expectations added some nuance to the moves in bonds, where rises in breakevens were offset by falling real yields. Ultimately, the 10-year treasury ended -2.3bps lower (+2.9bps Friday) at 2.057% while bund yields were -3.0bps lower (+3.3bps Friday) at -0.285%. Treasuries had dipped below the 2% mark earlier in the week and bunds brushed a new all-time low. US 2s10s steepened +4.5bps (+3bps on Friday) on the week but traded in an 11.5bps range. For us the fact that the Fed went more dovish and the curve steepened was a sign that the market trusts them for now.

3A/ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 6.17 POINTS OR 0.21% //Hang Sang CLOSED UP 39.29 POINTS OR 0.14% /The Nikkei closed UP 27.,35 POINTS OR 0.13%//Australia’s all ordinaires CLOSED UP .17%