GOLD:$1425.60 DOWN $3.90(COMEX TO COMEX CLOSING)

Silver:16.40 DOWN 14 CENTS (COMEX TO COMEX CLOSING)//

Closing access prices:

Gold : $1414.00

silver: $16.27

…

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 316/800

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,429.700000000 USD

INTENT DATE: 07/30/2019 DELIVERY DATE: 08/01/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 41

132 C SG AMERICAS 18

435 H SCOTIA CAPITAL 76

657 C MORGAN STANLEY 45

661 C JP MORGAN 303 316

685 C RJ OBRIEN 30

686 C INTL FCSTONE 254 15

690 C ABN AMRO 128

737 C ADVANTAGE 29 14

800 C MAREX SPEC 4

880 H CITIGROUP 260

905 C ADM 63 4

____________________________________________________________________________________________

TOTAL: 800 800

MONTH TO DATE: 800

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 800 NOTICE(S) FOR 80000 OZ (2.4883 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 800 NOTICES FOR 80,000 OZ (2.4883 TONNES)

SILVER

FOR AUGUST CONTACT MONTH: THE NUMBER OF NOTICES FILED

15 NOTICE(S) FILED TODAY FOR 75,000 OZ/

total number of notices filed so far this month: 15 for 75,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9985 UP 415

Bitcoin: FINAL EVENING TRADE: $ 10640 UP 823

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1979 CONTRACTS FROM 237,080 UP TO 239,059 WITH THE 8 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

0 FOR JULY. 0 FOR AUGUST, 652 FOR SEPT, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 652 CONTRACTS. WITH THE TRANSFER OF 652 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 652 EFP CONTRACTS TRANSLATES INTO 3.260 MILLION OZ ACCOMPANYING:

1.THE 8 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

5.3100 MILLION OZ INITIAL STANDING FOR AUGUST.

WE HAD ATTEMPTED COVERING OF SHORTS AT THE SILVER COMEX LAST NIGHT WITH ZERO SUCCESS..AND ZERO SPREADING ACCUMULATION.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

35,147 CONTRACTS (FOR 21 TRADING DAYS TOTAL 35,147 CONTRACTS) OR 175.74 MILLION OZ: (AVERAGE PER DAY: 1674 CONTRACTS OR 8.370 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 175.74 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 25.05% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1333.23 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1979, WITH THE 8 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 652 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 2631 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 652 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1979 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 8 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.54 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.196 BILLION OZ TO BE EXACT or 170% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 15 NOTICE(S) FOR 75,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ//AUGUST: 5.310 MILLION OZ//

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST FELL BY AN ATMOSPHERIC AND CRIMINALLY SIZED 8903 CONTRACTS, TO 563,298 DESPITE THE $9.00 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /THE SPREADING LIQUIDATION HAS NOW BEEN COMPLETED FOR GOLD AS WE ENTERED FIRST DAY NOTICE….AND WE SHOULD COMMENCE WITH ACCUMULATION OF SPREADERS IN SILVER ONCE THE AUGUST CONTRACT MONTH COMMENCES IN EARNEST.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9921 CONTRACTS: AUGUST 2019: 00 CONTRACTS, DEC> 9921 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 563,298,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1018 CONTRACTS: 8903 CONTRACTS DECREASED AT THE COMEX AND 9921 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 1,018 CONTRACTS OR 101,800 OZ OR 3.166 TONNES. YESTERDAY WE HAD A CONSIDERABLE GAIN OF $9.00 IN GOLD TRADING….AND WITH THAT STRONG GAIN IN PRICE, WE HAD A SMALL GAIN IN GOLD TONNAGE OF 6.329 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER. ALMOST ALL OF THE COMEX LOSS WAS DUE TO THE CLIMAX IN THE LIQUIDATION OF OUR SPREADERS.

WITH RESPECT TO SPREADING: WE HAVE WITNESSED THE MORPHING OF OUR SPREADERS OUT OF SILVER AND INTO GOLD AS THE JULY MONTH PROCEEDED TO ITS CONCLUSION ONCE WE ENTER INTO THE ACTIVE DELIVERY MONTH OF AUGUST. ONCE AUGUST BEGINS THE SPREADERS WILL RETURN TO SILVER WITH THE ACCUMULATION PHASE FIRST AND THEN LIQUIDATION DURING THE LAST WEEK OF AUGUST PRIOR TO FIRST DAY NOTICE OF THE SEPT CONTRACT MONTH.

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE COMEX SILVER DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE SILVER COMEX OPEN INTEREST WILL START TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO WILL THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF THE UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 190,187 CONTRACTS OR 19,018,700 oz OR 591.56 TONNES (21 TRADING DAY AND THUS AVERAGING: 9056 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY IN TONNES: 591.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 591.56/3550 x 100% TONNES =16.66% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3511.17 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 8903 DESPITE THE STRONG PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($9.00)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9921 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9921 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED GAIN OF 2035 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9921 CONTRACTS MOVE TO LONDON AND 8903 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 3.16 TONNES). ..AND THIS INCREASE OF DEMAND OCCURRED ACCOMPANYING THE GAIN IN PRICE OF $9.00 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE WILL NOW COMMENCE WITH SPREADING ACCUMULATION IN SILVER AS WE ENTER THE NON ACTIVE MONTH OF AUGUST.

we had: 800 notice(s) filed upon for 80,000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.90 TODAY//(COMEX-TO COMEX)

A NO CHANGES IN GOLD INVENTORY:

INVENTORY RESTS AT 824.89 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 356.715 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1979 CONTRACTS from 237,080 UP TO 239,059 AND NOW MUCH CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..THE SPREADERS WILL NOW COMMENCE THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER AS THEY HAVE STOPPED THEIR SPREADER- LIQUIDATION PHASE IN GOLD.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR JULY: 0 CONTRACTS FOR AUGUST: 0, FOR SEPT. 652 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 652 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1979 CONTRACTS TO THE 652 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 2631 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 5.239 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.885 MILLION OZ AND AUGUST AT 5.310 MILLION OZ SO FAR.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 8 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 652 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

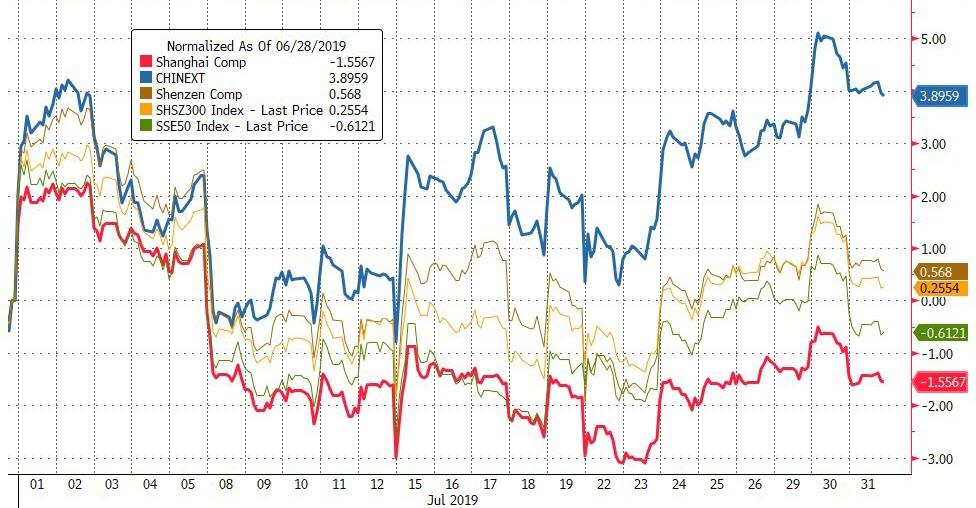

SHANGHAI CLOSED DOWN 19.83 POINTS OR 0.67% //Hang Sang CLOSED DOWN 368.75 POINTS OR 1.31% /The Nikkei closed DOWN 1876.78 POINTS OR 0.87%//Australia’s all ordinaires CLOSED DOWN .46%

/Chinese yuan (ONSHORE) closed DOWN at 6.8827 /Oil UP TO 58.39 dollars per barrel for WTI and 65.03 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8902 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3 c CHINA

i)This is dangerous! Mainland China gathers forces on the Hong Kong border

(zerohedge)

ii)The engine for global growth in China and when we see Chinese Mfg PMI in contraction and service PMI at 2019 lows, you know that the world is in trouble

iii)My goodness, that did not take long!! The USA China trade talks collapse after half a day of negotiations

4/EUROPEAN AFFAIRS

a)Bill Blain discusses two major issues before us:

- Brexit and the Irish backstop

- China/USA and its non trade deal

and it is these two factors which will cause the Fed to lower rates

(Bill Blain)

b) UBS is now set to charge its rich clients (deposits greater than 2 million Swiss francs) a negative interest rate of 3/4%

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)ted Butler reports on huge buying of silver futures and hints at a possible sovereign. I wonder who that could be?

(Ted Butler/Kaiser/GATA)

ii)Hugo outlines a plan that the Mexican government can implement with a silver backed peso coin. This coin would not be inflationary but hoarded by the masses.

(courtesy Hugo Salinas Price/GATA)

iii)China’s foreign exchange agency (SAFE) finally gives details as to how they are diversifying away form the USA dollar

(South China Morning Post/GATA)

iv)Larry Lindsay blasts Trump with his call to devalue the dollar

(Lindsay/CNBC/GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

(ADP)

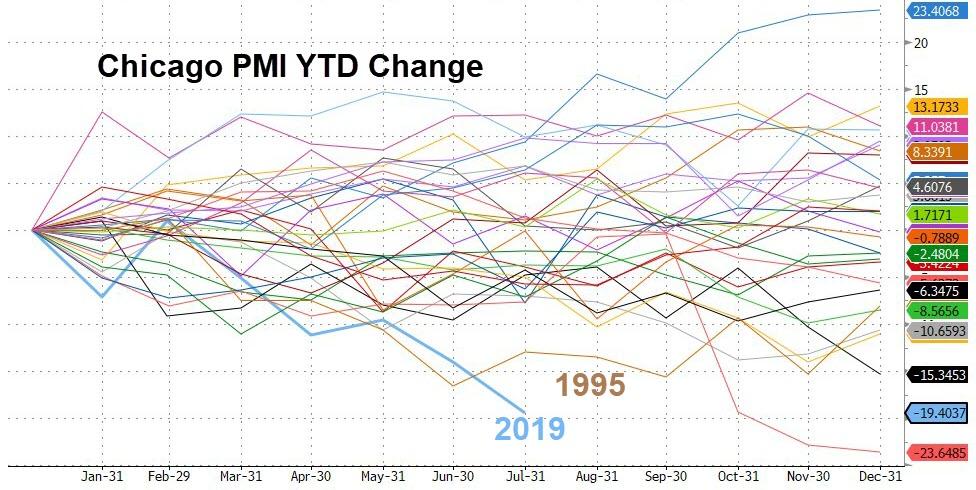

b)My goodness, this was a precipitous fall: The Chicago PMI contracts to the worst ever in over 30 years. While other regional areas fluctuate, the Chicago PMI continues to flounder,

(zerohedge)

iii) Important USA Economic Stories

Trump is silent after a huge number of coal miners bite the dust after declaring bankruptcy protection’

(zerohedge)

iv) Swamp commentaries)

a)A complete joke: a judge throws out a meritless DNC lawsuit against Trump, Russia Assange and just about everybody else..

(zerohedge)

b)Deep Staters in action:

c)It looks like Trump was right..there are texts between the FBi and MI 5 on the early role of the UK in Russiagate

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

1062 CONTRACTS X 5000 OZ PER CONTRACT = 5.310 MILLION OZ…WHICH IS HUGE. LET’S SEE IF WE WILL WITNESS MORE SILVER QUEUE JUMPING AS THE CROOKS TRY AND RETRIEVE FAST DEPLETING SILVER.

we had 1 dealer entry:

We had 1 kilobar entries

i) Into Brinks: 25,002.500 oz

total gold withdrawals; 32.15 oz

FOR THE AUGUST 2019 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 303 notices were issued from their client or customer account. The total of all issuance by all participants equates to 800 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 316 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account and 0 notices by the squid (Goldman Sachs)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2019. contract month, we take the total number of notices filed so far for the month (800) x 100 oz , to which we add the difference between the open interest for the front month of AUGUST. (8700 contract) minus the number of notices served upon today (800 x 100 oz per contract) equals 869,900 OZ OR 27.06 TONNES) the number of ounces standing in this active month of AUGUST

Thus the INITIAL standings for gold for the AUGUST/2019 contract month:

No of notices served (800 x 100 oz) + (8700)OI for the front month minus the number of notices served upon today (800 x 100 oz )which equals 870,000 oz standing OR 27.06 TONNES in this active delivery month of AUGUST.

.

SURPRISINGLY LITTLE TO NO GOLD HAS BEEN ENTERING THE COMEX VAULTS AND WE HAVE WITNESSED THIS FOR THE PAST YEAR!! WE HAVE ONLY 11.299 TONNES OF REGISTERED ( GOLD OFFERED FOR SALE) VS 27.06 TONNES OF GOLD STANDING// THEY SEEM TO BE USING CONSIDERABLE GOLD VAPOUR TO SETTLE UPON UNSUSPECTING LONGS. SINCE THERE IS HARDLY ANY GOLD AT THE COMEX WE WILL WITNESS CONSIDERABLE MORPHING OF CONTRACTS STANDING OVER TO LONDON.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 86,549 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 62,012 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 162,012 CONTRACTS EQUATES to 310 million OZ 44.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.18.% ((JULY 31/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.17% to NAV (JULY 31/2019 )

Note: Sprott silver trust back into NEGATIVE territory at -0.18%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.28 TRADING 13.82/DISCOUNT 3.21

END

And now the Gold inventory at the GLD/

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

JUNE 28/WITH GOLD UP $.90 TODAY: ANOTHER 2.05 TONNES OF PAPER GOLD REMOVED AND THIS GOLD WAS USED IN ATTACKING GOLD AT THE COMEX/INVENTORY RESTS AT 795.80 TONNES

JUNE 27/WITH GOLD DOWN $6.10: ANOTHER HUGE WITHDRAWAL OF 1.76 PAPER TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 797.61 TONNES

JUNE 26/WITH GOLD DOWN $3.00: WE HAD A HUGE WITHDRAWAL OF 2.37 TONNES FROM THE GLD/INVENTORY RESTS AT 799.61 TONNES

JUNE 25/WITH GOLD UP $1.30 (AND WAY UP BEFORE THE BANKERS WHACKED) WE WITNESSED ANOTHER 1.95 TONNES OF PAPER GOLD ADDED TO THE GLD INVENTORY//INVENTORY RESTS AT 801.98 TONNES

JUNE 24/WITH GOLD UP $18.00 A MONSTROUS PAPER DEPOSIT OF 34.93 TONNES/INVENTORY RESTS AT 799.03 TONNES

JUNE 21/WITH GOLD UP $ 2.90, NO CHANGE IN GOLD INVENTORY: INVENTORY RESTS AT: 764.10 TONNES

June 20/WITH GOLD UP $47.95, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 19 WITH GOLD DOWN $1.65: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONES

JUNE 18/JUNE 18/WITH GOLD UP $7.60: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 764.10 TONNES

JUNE 17/WITH GOLD DOWN $1.65 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 764.10 TONNES

JUNE 14/ WITH GOLD UP $1.05 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.40 TONNES OF PAPER GOLD INTO THE GLD///INVENTORY RESTS AT 764.10 TONNES

JUNE 13/WITH GOLD UP $6.60 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.52 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 759.70 TONNES

JUNE 12/WITH GOLD UP $7.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 756.18 TONNES

JUNE 11/WITH GOLD UP $1.65 CENTS TODAY: A TINY CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .24 TONNES AND THIS IS TO PAY FOR FEES/INVENTORY RESTS AT 756.18 TONNES

JUNE 10/WITH GOLD DOWN $16.40 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES/INVENTORY RESTS AT 756.42 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 31/2019/ Inventory rests tonight at 824.89 tonnes

*IN LAST 632 TRADING DAYS: 109.85 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 532 TRADING DAYS: A NET 55.83 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

JUNE 28/WITH SILVER UP 6 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.394 MILLION OZ//

JUNE 27/WITH SILVER DOWN 7 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.575 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.394 MILLION OZ//

JUNE 26/WITH SILVER UP 17 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 25/WITH SILVER DOWN 25 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ.

JUNE 24/WITH SILVER UP 11 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 21/WITH SILVER DOWN 22 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ//

JUNE 20/WITH SILVER UP 53 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.819 MILLION OZ/

JUNE 19/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ/

JUNE 18 WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 319.070 MILLION OZ

JUNE 17/WITH SILVER UP XXX CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ//

JUNE 14/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 12/WITH SILVER UP 4 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.413 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 316.775 MILLION OZ/

JUNE 11/WITH SILVER UP 10 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 315.652 MILLION OZ//

JUNE 10/WITH SILVER DOWN 38 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.652 MILLION OZ//

JULY 31/2019:

Inventory 356.715 MILLION OZ

ted Butler reports on huge buying of silver futures and hints at a possible sovereign. I wonder who that could be?

(Ted Butler/Kaiser/GATA)

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

With All Eyes On The Fed, US Futures Defy Global Gloom After Disappointing End To Trade Talks

The unexpectedly early end to the latest round of trade talks in Shanghai, indicating that any goodwill to restore US-China trade is now dead and buried, weighed on global stocks on Wednesday ahead of the highly anticipated Fed meeting, even as US equity futures levitated higher on the back of strong results and even stronger guidance from Apple (which is expected to surpass a $1 trillion market cap again today), with Treasury rates unchanged, the dollar holding firm and Britain’s pound subdued amid rising fears of no-deal Brexit.

Combative warnings from President Trump cast a shadow over the day’s other main event, as the Sino-U.S. trade talks concluded in Shanghai on Wednesday, with Beijing attributing the lack of progress to Washington’s flip-flopping.

“Trade talks have finished without an agreement,” said Justin Onuekwusi, fund manager at Legal & General Investment Management. “Of course, it doesn’t help that almost as a prelude to the conversation you get tweets that are quite antagonistic,” he said, referring to a tweet by Trump warning China against waiting out his current presidential term before finalizing a trade deal.

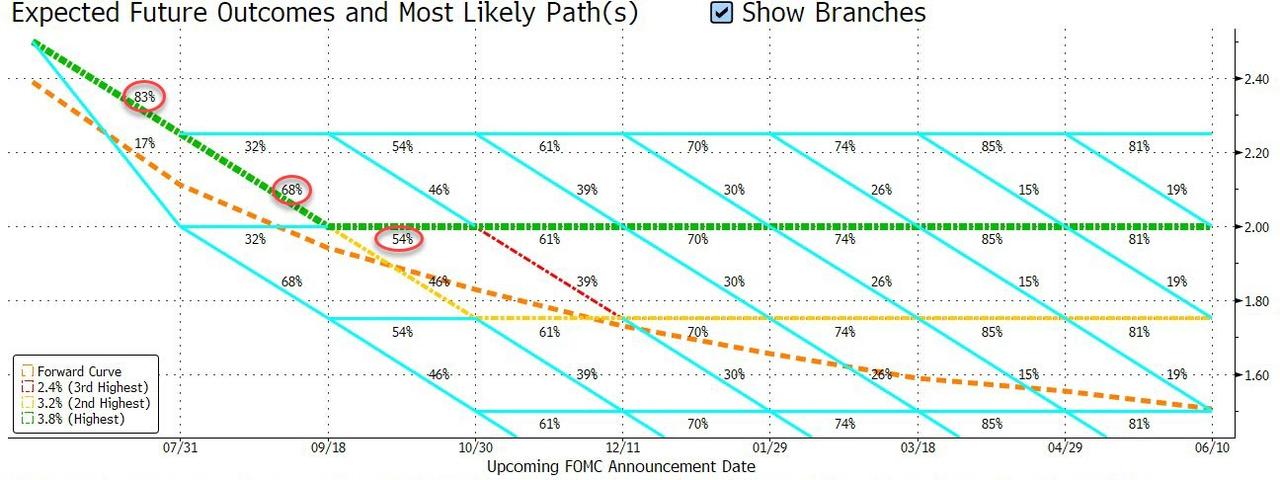

The fresh trade tensions come ahead a FOMC meeting which is expected to see interest rates reduced by 25 basis points in its first rate cut in more than a decade. Yet the focus is on whether this will be a “one and done”, or Powell will leave the door open for further easing to shore up the world’s largest economy in the face of slowing global growth and the fallout from trade conflicts.

A 25bps rate cut is certain as is another 25 basis point reduction by September – with the market pricing in a 20% chance of a 50bps rate cut today – but what will matter is whether this is seen as a recessionary cut (validated by a 50bps cut), or an “insurance”, or precautionary easing. How Powell frames today’s move will determine if stocks will rise or fall before the end of the day. Expectations for Fed easing helped lift the S&P 500 index 2.4% so far this month.

“Exactly what happens today is far from a foregone conclusion,” said Deutsche Bank’s Jim Reid. “Although the Fed have given no real encouragement to the notion of a 50 basis point (bps) cut it’s worth noting that the last time the Fed began a series of rate cuts, in September 2007, their opening move was a 50 bps cut, and a similar 50 bps cut happened when the Fed began cutting in January 2001.”

Trump on Tuesday reiterated his call for the Fed to make a large interest rate cut, saying he was disappointed in the U.S. central bank and that it had put him at a disadvantage by not acting sooner.

“The bond and equity markets have fully priced in a cut,” Paul Brain, head of fixed income at Newton Investment Management, said in a note. “On balance, there may be some that are disappointed by the size of the cut and the subsequent messaging, but once that is out of the way there will be a realization that rates are heading lower.”

Until the 2pm FOMC announcement, global stocks were biding their time, with the MSCI world index and Europe’s pan regional Stoxx 600 slipping 0.1%, the latter flirting with a fresh one-month low and decidedly underperforming the S&P500, as worries over trade wars and Brexit offset encouraging signals from the earnings season. The Stoxx Europe 600 index struggled for direction amid mixed company reports, with personal and household-goods shares among the biggest losers as L’Oreal dropped after posting disappointing sales figures. Construction companies led gains after upbeat results from Vinci. London’s FTSE fell 0.3% while Frankfurt stocks gained 0.2% and Paris was treading water.

In focus were banks, with strong results from French lender BNP Paribas and Switzerland’s Credit Suisse countering a poor report from British bank Lloyds. Also of note is the sharp rebound in German retail sales, which surged 3.5% M/M, smashing expectations of a modest 0.5% increase, and the biggest monthly increase since 2006.

Asian stocks ex-Japan fell to a six-week low with China mainland stocks down nearly 1% and Hong Kong tumbling 1.3% as China and the U.S. concluded their Shanghai trade talks without signaling any progress and disappointment among investors with corporate earnings. The MSCI Asia Pacific Index fell as much as 0.8% to the lowest level since June 19. Technology was the worst-performing group Wednesday, mainly dragged by Samsung Electronics as the company reported lower profit and said it faces uncertainty due to growing macroeconomic issues. Hong Kong market closed early Tuesday as a storm struck the city. Philippines’ PSEi Index fell 1.3%, led by basic materials companies. Elsewhere, India’s Sensex traded little changed.

Overnight, Chinese data showing factory activity shrank for the third month in a row in July added to the somber mood.

Seemingly oblivious to the global equity woes, US futures pointed to main indexes opening higher as General Electric delivered strong results. On Tuesday, major Wall Street stock averages ended slightly lower with the S&P 500 losing 0.26%, however, momentum reversed after the closing bell when Apple shares soared 4.2% as its Q3 earnings beat estimates and CEO Tim Cook cited “marked improvement in Greater China”.

In currency markets, the dollar index traded flat around 98.064 after pulling back from a two-month high of 98.206 touched on Tuesday. The dollar index was set for a monthly gain of 1.4%, its best since last October. The greenback was also steady against the yen and the euro, with the former undermined on Tuesday by the BOJ’s decision to refrain from expanding stimulus though it committed to doing so “without hesitation” if required. Most other currencies traded in narrow ranges before the Fed meeting.

Meanwhile the British pound hovered near a 28-month low hit the previous day on growing concerns about a disorderly Brexit. GBPUSD recovered from the drop seen in the past two sessions but was still set for a 4% decline this month, its worst showing since 2016. The Australian dollar climbed against all its major peers as headline inflation was higher than the estimate.

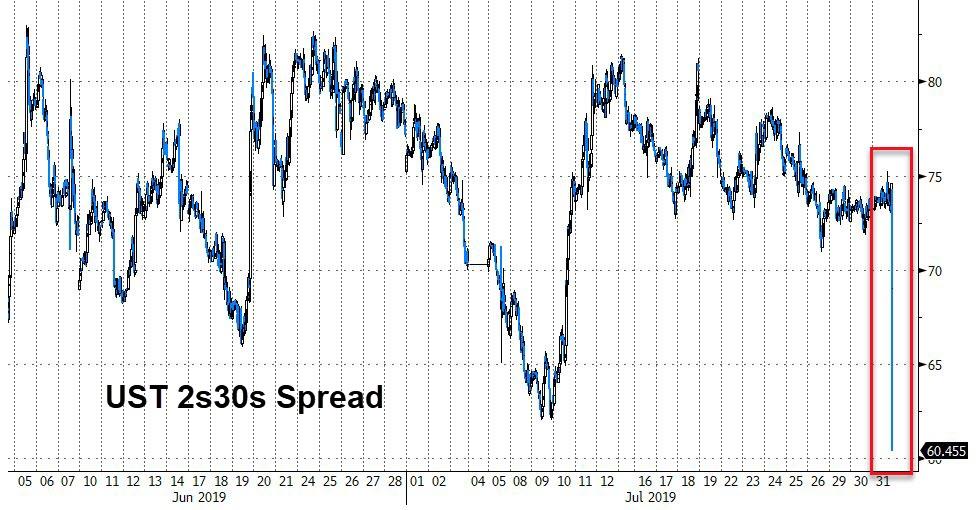

Treasuries were modestly higher, led by front-end ahead of the Fed’s expected rate cut. Volumes were light during Asia session and European morning with several additional key events ahead including July ADP employment change, quarterly refunding announcement and month-end. The 10-year yield was at 2.05% after a 3bps decline since July 25. The TSY curve had a small steepening bias, with yields richer by 1.2bp to 2bp across the curve with 10-year ~2.047%, lower by 1bp; Around the world, gilts underperformed, cheaper by 1.5bp vs. Treasuries, as sterling stabilizes following recent sell-off, while bunds keep pace.

In geopolitics, North Korea fired multiple projectiles early on Wednesday which was said to be 2 short-range ballistic missiles and a different type of weapon than previous launches, Following the launch, South Korea convened a national security meeting, while Japan Defense Ministry said no ballistic missiles reached Japan’s territory or exclusive economic zone and sees no immediate impact on Japan’s security from the North Korea launch.

In commodity markets, crude oil futures rose for the 5th straight day, buoyed by a bigger-than-expected drop in U.S. inventories. U.S. WTI crude gained 28 cents to $58.34 per barrel while Brent crude futures LCOc1 added 48 cents to $65.2. Three-month copper on the London Metal Exchange (LME) CMCU3 was almost unchanged at $5,950 a ton.

Expected data include mortgage applications. CME Group, Carlyle Group and Spotify are among companies reporting earnings.

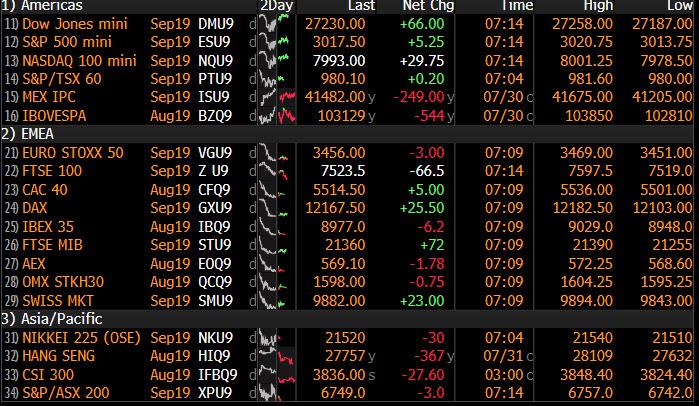

Market Snapshot

- S&P 500 futures up 0.2% to 3,019.50

- STOXX Europe 600 up 0.06% to 385.36

- MXAP down 0.6% to 158.48

- MXAPJ down 0.7% to 519.26

- Nikkei down 0.9% to 21,521.53

- Topix down 0.7% to 1,565.14

- Hang Seng Index down 1.3% to 27,777.75

- Shanghai Composite down 0.7% to 2,932.51

- Sensex up 0.06% to 37,418.69

- Australia S&P/ASX 200 down 0.5% to 6,812.56

- Kospi down 0.7% to 2,024.55

- German 10Y yield fell 0.7 bps to -0.406%

- Euro down 0.08% to $1.1146

- Brent Futures up 0.7% to $65.16/bbl

- Italian 10Y yield rose 8.7 bps to 1.308%

- Spanish 10Y yield fell 2.8 bps to 0.324%

- Brent Futures up 0.9% to $65.16/bbl

- Gold spot down 0.02% to $1,430.53

- U.S. Dollar Index up 0.06% to 98.11

Top Overnight News

- China and the U.S. concluded a new round of trade talks in Shanghai on Wednesday following a hiatus of almost three months, with little immediate evidence of progress being made toward ending their year-long dispute

- The talks come at a time when President Trump lashed out at China for what he said is its unwillingness to buy American agricultural products and said it continues to “rip off” the U.S.

- A tropical storm shut Hong Kong’s financial markets for the first time in almost two years, adding chaos to a city which has been wracked by protests for weeks

- German unemployment rose and demand for new workers dwindled, a sign that weakening economic momentum is starting to affect the labor market. Spanish economic growth slowed more than expected in the second quarter, adding another layer of gloom to an increasingly fragile situation in the euro region

- “We now have a fresh approach to negotiating a deal and are well prepared to leave the EU,” U.K. Brexit Secretary Stephen Barclay said on Twitter, adding that he was confident as two new Brexit committees “are now up and running”

- The White House is monitoring what a senior administration official called a congregation of Chinese forces on Hong Kong’s border

- North Korea fired multiple unidentified projectiles off its east coast early Wednesday, Yonhap reports, citing the South Korean Joint Chiefs of Staff

Asian equity markets followed suit to the negative performance seen across global peers amid trade concerns following US President Trump’s Twitter rant regarding China, while the looming FOMC decision, mixed Chinese PMI data and earnings deluge added to the cautious tone. ASX 200 (-0.5%) was dragged lower by losses in utilities and financials but with downside stemmed by strength in the energy sector after a rally in oil prices, while Nikkei 225 (-0.9%) suffered the ill-effects of a firmer currency with the best and worst performers in Tokyo driven by their quarterly results. KOSPI (-0.7%) weakened after North Korea conducted another launch which was said to be a new type of weapon and with earnings also in focus including index heavyweight Samsung Electronics which showed final Q2 oper. profit and revenue topped preliminary results but still suffered a 56% Y/Y drop in profits. Conversely, its main rival Apple saw a different fate with the US tech giant gaining around 4.5% after-hours due to a beat on both top and bottom lines and although it missed on iPhone sales its revenue forecast for next quarter surpassed Street estimates. Elsewhere, Hang Seng (-1.3%) and Shanghai Comp. (-0.7%) conformed to the wide risk averse tone after President Trump’s recent criticism on China and warning of a much tougher deal if China holds out until after the next US elections, with participants also digesting mixed Chinese PMI data in which the headline Manufacturing PMI beat expectations but remained below the 50 benchmark level and Non-Manufacturing PMI missed forecasts. Finally, 10yr JGBs traded relatively flat and were only marginally supported by the risk averse tone as well as the BoJ’s presence in the market for JPY 1.24tln of JGBs with 1yr-10yr maturities.

Top Asian News

- China, U.S. Trade Talks End Early in Shanghai

- Hong Kong Rioting Charges Signal Harsher Line Against Protesters

- Hintze’s CQS Strikes Deal With Asia Managers in Regional Push

Major European indices are mixed [Euro Stoxx 50 Unch], as this morning saw the early finish of US-China trade talks with initial reports indicating that the talks ended with no sign of a breakthrough after an earnings dominated morning for indices. Sectors are also mixed with no standout sector at present. In terms of this mornings earnings, L’Oreal (-3.8%) are under pressure after missing on sales growth in-spite of the Co’s CEO noting that H1 was the strongest in terms of like-for-like growth in decades; notably the Co. also announced a EUR 750mln share buyback. Sticking with the CAC 40 (+0.1%) this morning also saw earnings from Airbus (+0.8%) who beat on Q2 revenue and confirmed FY guidance; recently, the Co. also benefitting recently from WSJ reports indicating that internal risk analysis at Boeing (BA) showed the likelihood was high of further cockpit emergencies following the first crash. Elsewhere, of note for banking names Credit Suisse (+4.2%) are firmer after beating on Q2 net revenue and net income as are BNP Paribas (+3.5%) post earnings where the Co’s Q2 revenue beat on consensus.

Top European News

- Salvini Weighs Early 2020 Vote, Govt Breakup in Fall: Repubblica

- Polish Inflation Unexpectedly Surges to Highest Level Since 2012

- Next Surges as E-Commerce Sales Boost Fuels Guidance Upgrade

- DUP’s Foster Says Ireland Must ‘Get Real’ on Deal: Brexit Update

In FX, AUD, NZD – The Aussie stands as this morning’s G10 winner amid promising domestic inflation data which follows the RBA’s back-to-back rate cuts since June. CPI Y/Y rose to 1.6% (Prev. 1.3%) in Q2 but remains below the Central Bank’s 2-3% target. In terms of implications on monetary policy, the CB is likely to stand pat on rates for now in order to examine further effects of its recent rate cuts and the government’s tax cut package. AUD/USD trades closer to the top of the intraday range thus far, after testing 0.6900 to the upside. Elsewhere, the Kiwi is lacklustre after the ANZ business confidence further deteriorated alongside the activity outlook. NZD/USD hovers just above the 0.6600 mark having visited a current intra-day low of 0.6590.

- DXY, CNY – Relatively side-ways trade for the DXY (for now) heading into the FOMC’s latest policy decision (full preview available in the Research Suite) and with little impetus from the fallout of US-China talks in Shanghai. The initial reports/commentary on the meeting provided little substance. Although no breakthrough was reached (as expected), discussions are said to have been constructive and future talks between the nations will happen. DXY remains flat above 98.00 having earlier tested the figure to the downside. Meanwhile, the CNH also remains tentative and within a narrow range vs. the Buck after having visited its 50 DMA (6.8967) at the European open.

- GBP, EUR – Overall little changed thus far with the Pound capped amid fears of a Halloween no-deal crash and tomorrow’s BoE policy decision and QIR (full preview available in the Research Suite). GBP/USD continues to meander sub-1.2200, and as a reminder, the following support levels are still in play: 1.2110 (March 17 low), 1.2085 (Jan 17 low), 1.2000 (psychological) and 1.1841 (2016 flash crash low). Elsewhere The EUR remains flat within a 20-pip intraday range as mostly in-line inflation, growth and unemployment metrics failed to spur a reaction ahead of the FOMC’s policy decision. EUR/USD trades just below 1.1150 ahead of minor support levels at 1.1133/14/21/01, although large option expiries (1.3bln at 1.1145 and 1.2bln at 1.1100-05) may keep the pair contained heading into today’s NY cut.

- EM – Another day of gains for the Lira as traders anticipated the CBRT’s QIR to signal further normalisation in its domestic economy, in which it delivered. The Central Bank cut its 2019 year-end inflation forecast mid-point to 13.9% from 14.6% whilst its 2020 figure was maintained at 8.2%, adding that the economic outlook has brightened compared to the April release. USD/TRY breached its 200 DMA (5.5600) to the downside and took out a support level at 5.5500 to print a low of 5.5150 ahead of a Fib support at 5.4172.

In commodities, the oil complex has held onto most of its API-induced gains with WTI futures hovering just below USD 58.50/bbl and Brent north of USD 65/bbl. The report showed that crude inventories fell by 6.02mln barrels over the last week, a larger decline than the expected 2.60mln barrel drawdown. Traders today will be eyeing two events as catalysts: 1) The weekly EIA report for confirmation of the decline in stocks, 2) the FOMC’s policy decision for any Dollar or sentiment-induced action. Elsewhere, sources stated that Libya’s El-Sharara oilfield (300k BPD) has halted production amid a valve closure on a pipeline, although it is not clear how long the closures could last. Of note, WaPo reported that the Trump administration is set to announce that it will waiver five difference nuclear related sanctions on Iran, although it is currently unclear whether the waivers will be oil related. Looking at metals, gold and copper remain flat, as usually the case ahead of the FOMC’s decision.

US Event Calendar

- 8:15am: ADP Employment Change, est. 150,000, prior 102,000

- 8:30am: Employment Cost Index, est. 0.7%, prior 0.7%

- 9:45am: MNI Chicago PMI, est. 51, prior 49.7

- 2pm: FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

So today is the long-awaited Fed decision day, where markets are fully pricing in what is expected to be the first rate cut since December 2008. But exactly what happens today is far from a foregone conclusion, as the question still on investors’ minds is by how much the Fed will cut, and whether there’ll be any messages about the future path of rates going forward. The market currently fully prices a 25bp cut and implies an 16% chance of a larger 50bp cut. Although the Fed have given no real encouragement to the notion of a 50bps cut it’s worth noting that the last time the Fed began a series of rate cuts, in September 2007, their opening move was a 50bp cut, and a similar 50bp cut happened when the Fed began cutting in January 2001. Rates were higher back then though. The last time the Fed started an easing cycle with a 25bps cut was in September 1998, when they ultimately cut rates 3 times and successfully prolonged the expansion until the recession in 2001.

In their preview last Friday (link here ), our US economists predict a 25bp cut, but they say that “the key question is how Chair Powell and the Committee frame the narrative for further easing through year end.” With this in mind, investors will be paying close attention to Chair Powell’s press conference. Our economists write that they “do not expect the Committee to pre-commit to another cut in September”, but instead the amount of further easing is going to be data dependent. Will a market hungry for stimulus accept this?

Indeed we’re at a fascinating juncture in markets. It feels like the global macro risks are building for late summer/autumn (hard Brexit, US/China trade uncertainty, US/EU trade issues to come before year-end and global manufacturing effectively in recession) but all of us are reluctant to fight the central banks. Is this a trap? Indeed even our traditionally bullish Binky Chadha has some reservations about the risk/reward from this starting point. In his piece last week ( link ) he suggested that there have been 19 Fed easing cycles since the 1950s and this one fits almost exactly inline timing wise with the average slowdown in ISMs and LEIs through history. However, where it differs markedly is that only once (in 1995) has a rate cut occurred when the S&P 500 was around record highs. On average, the market has peaked 4 months before the cutting cycle started and was down a median -12% in between the two points. Also, he pointed out that 9 of the 19 rate cutting cycles failed to avert a recession. The recessions typically saw a -27% peak to trough drawdown in the S&P (mostly after the first cut) and on average bottomed 5 months after the Fed started cutting. Of the 10 that didn’t end in recessions, growth rebounded quickly – on average after 2-3 months – and although the S&P still fell around -7%, within 6 months of the first cut they had gained 12% from the lows and sat comfortably above pre-cut levels. So history would suggest quite a binary outcome from here and based on this alone one would have to say that the risk/reward doesn’t look particularly compelling especially as we’re at record highs. So don’t fight the Fed is a famous refrain but nearly 50% of the time they’ve been powerless to stop negative economic and market momentum in a growth slowdown.

Ahead of today’s FOMC decision, President Trump said yesterday that “I would like to see a large cut” in rates, maintaining his calls for easier monetary policy from the Fed. Separately, comments via Twitter from the President sent S&P futures lower before the US open, as he said that “China is doing very badly, worst year in 27 – was supposed to start buying our agricultural product now – no signs that they are doing so. This is the problem with China, they just don’t come through.” In response, The People’s Daily – the official paper of the Communist Party, said overnight that China has no motive to “rip off” the US and has never done so, and China won’t make concessions against its principles on trade. All this is occurring as the US and China have kick started a new round of trade talks in Shanghai. Watch this space for any headlines.

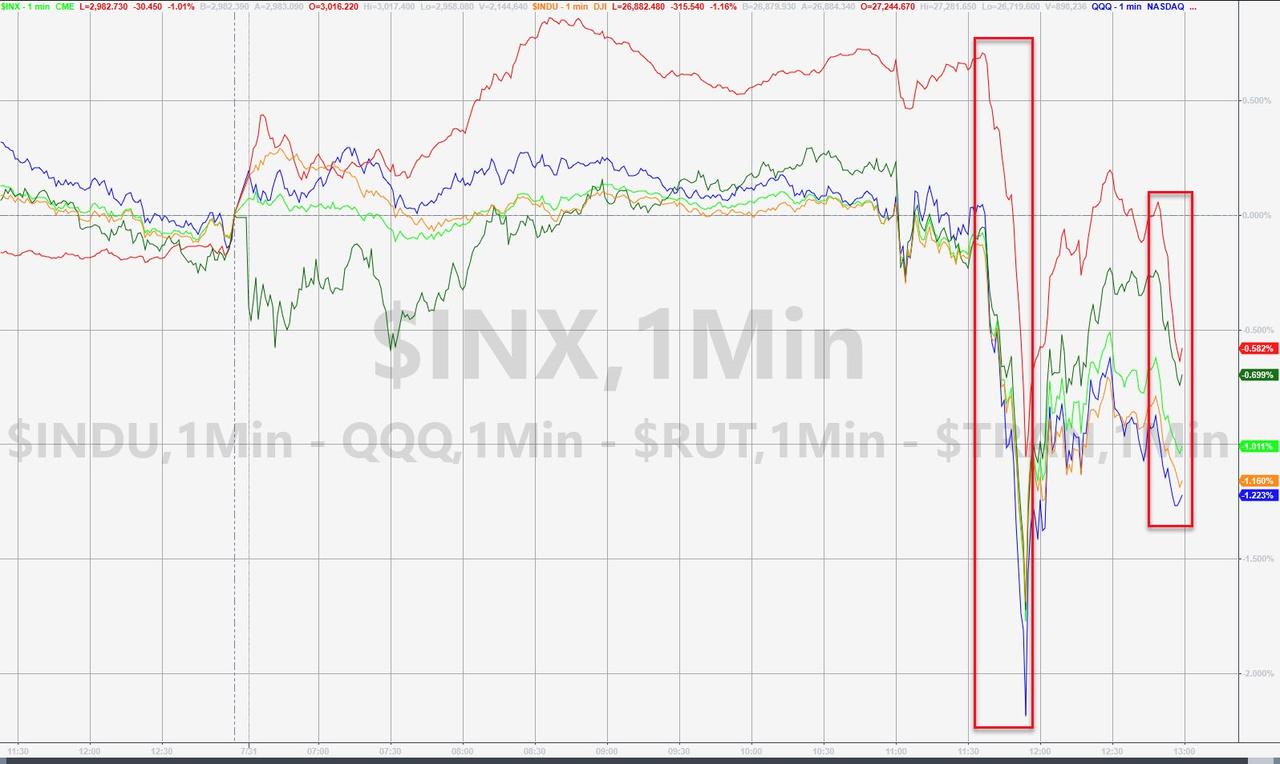

After this set back pre-market, US equities didn’t fall any further during the actual session but failed to get back to flat after trading in a relative narrow band through the day. The S&P 500 (-0.26%), NASDAQ (-0.24%), and DOW (-0.09%) all ended lower, though US bank stocks did gain +0.47% in contrast to their European cousins (more below). Fixed incomes moves were also muted, with 2- and 10-year treasury yields -1.4bps and -0.9bps lower, while HY credit spreads mirrored the moves in equities, widening +3.5bps. Earnings news was again mixed, with Under Armor (-12.28%) underperforming after signaling for a revenue decline from its core North American market. Procter and Gamble (+3.82%) and Merck (+0.96%) both gained after beating analyst expectations. After markets closed, Apple reported better-than-expected revenue and traded +4.42% overnight. Though iPhone sales and revenue disappointed, the company performed better via its mac, iPad and wearable business lines. Apple also reported gross margins at the top end of analyst estimates, illustrating that they continue to generate growth without lowering prices.

Meanwhile in Europe it was a gloomy day for equities, with the STOXX 600 falling -1.47%, its worst fall in 12 weeks and the index’s lowest close in a month. The continent’s indexes were lower across the board, with the DAX (-2.18% and worst day for 6 months), CAC 40 (-1.61%) and the FTSE MIB (-1.99%) all losing ground. Banks in particular suffered, with the STOXX Banks down –2.90%, bringing the index’s falls over the last two days to -3.77%, the biggest two-day fall since May. It’s not 100% clear to me why yesterday was such a bad day but weak Euro area data (see below), disappointing earnings, and perhaps worries about US/China trades talks may have weighed.

Bonds advanced for the most part, with ten-year bund yields matching their record low from earlier this month at -0.399% after falling -0.8bps yesterday. Spreads widened however, with Italian ten-year spreads over bunds up +2.1bps, while European HY spreads were up +6bps. Gilts rallied -1.9bps as fears of a hard Brexit continued to build.

The FTSE 100 outperformed again, only down -0.52%, although as before this was due to sterling’s continued slide, with the currency down -0.52% (trading largely unchanged this morning) against the dollar as it fell to fresh two-year low (only 0.89% off 34 year lows) as investor’s concerns over a no-deal Brexit outcome continued. The falls came as Prime Minister Johnson spoke to the Irish Taoiseach, Leo Varadkar, with a press release from Downing Street saying that “the Prime Minister made clear that the UK will be leaving the EU on October 31, no matter what”. He is also making it quite clear that he won’t sit down with EU leaders unless they agree to re-open the Withdrawal Agreement – something they have shown no appetite in doing. So unless someone blinks, or Parliament finds a way (including an election) to reverse course, then we are heading for a hard Brexit.

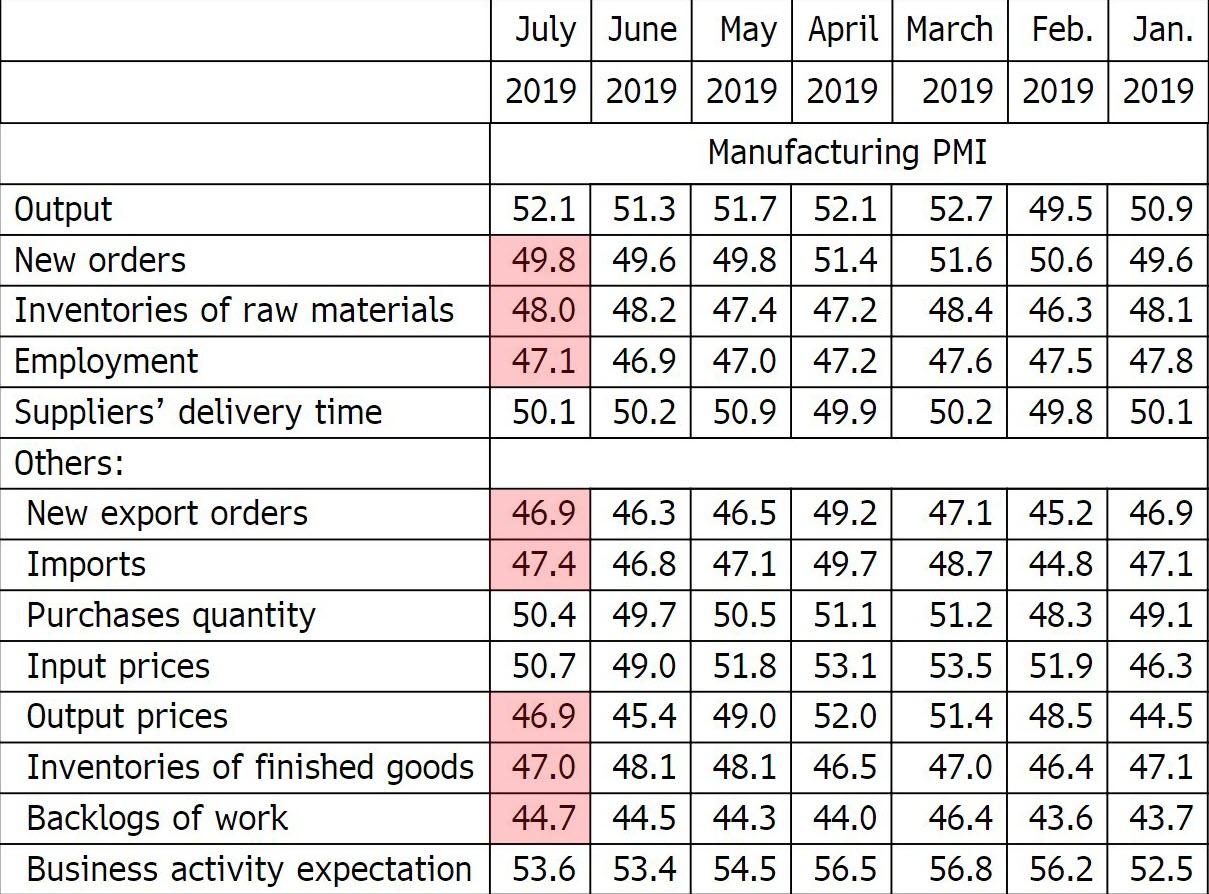

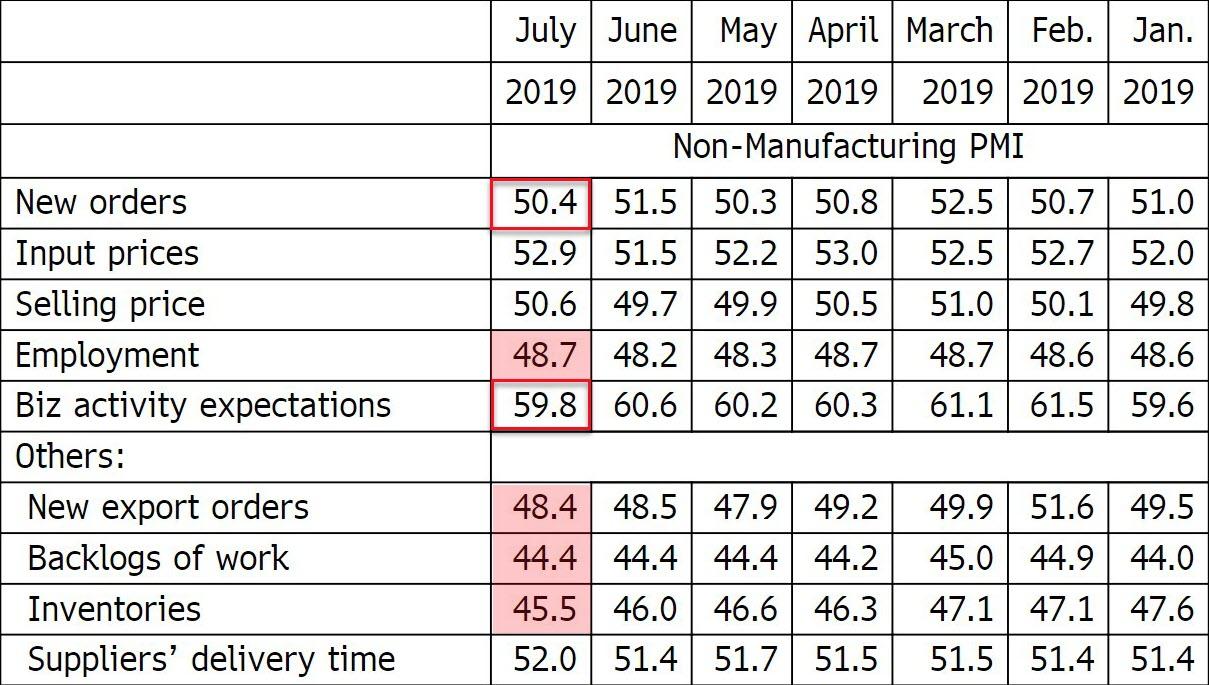

Overnight in Asia we have seen China’s July PMIs with manufacturing printing at 49.7 (vs. 49.6 expected), marking it the third consecutive month in contractionary territory. There was improvement in conditions for large enterprises (at 50.7 vs 49.9 last month) while small (at 48.2 vs 48.3 last month) and medium (at 48.7 vs. 49.1 last month) enterprises continued to deteriorate. The new export orders component rose to 46.9 (vs. 46.3 last month) but continues to remain well below 50. The services PMI came in at 53.7 (vs. 54.0 expected) bringing the composite PMI to 53.1 (vs. 53.0 last month). After the official PMIs, the focus is likely to turn to China’s Caixin manufacturing PMI tomorrow which focuses more on private sector/SME and is expected to print at 49.5. Meanwhile, China’s political leadership has announced its priorities for 2H 2019 by pledging to tackle ongoing tensions over trade “effectively” while offering incremental additions to stimulus policies.

Staying with Asia, Hong Kong’s Chief Executive Carrie Lam said yesterday that there is “no room for optimism for the second quarter and the entire year,” on GDP growth given the US-China trade war and other “uncertainties,” while pledging to “spare no efforts” to deal with anti-government protests that risk harming the city’s growth. Hong Kong’s GDP data is due today at 4:30 pm (Hong Kong time). Elsewhere, this morning North Korea fired two short-range ballistic missiles off its east coast, conducting its second such test in a week ahead of US Secretary of State Michael Pompeo’s visit to Asia. South Korean Defense Minister Jeong Kyeong-doo said in remarks after the launch that “If they threaten us and provoke us, North Korea’s regime and the North Korean military is with no doubt defined as our ‘enemy.’” This suggests that such actions could cause Seoul to reconsider its decision to downgrade the threat level of its neighbour.

This morning in Asia markets are following Wall Street’s lead with the Nikkei (-0.74%), Hang Seng (-1.11%), Shanghai Comp (-0.53%) and Kospi (-0.15%) all down. Elsewhere, futures on the S&P 500 are up +0.23% while WTI crude oil prices are up +0.67% on a report from the American Petroleum Institute that US crude inventories dropped by 6.02 million barrels last week.

In terms of data yesterday, the Conference Board’s consumer confidence came in well-above expectations at 135.7 in July (vs. 125.0 expected), the highest level in 8 months. The present situation reading also rose to 170.9 while the expectations measure rose to 112.2. Also encouragingly, the prior month’s readings on each of those metrics were revised several points higher. The closely-watched labour differential, which is a good leading indicator for the labour market, rebounded +5.2pts after last month’s sharp drop, approaching again its highest level of the expansion. Separately, the core PCE inflation figure for June came in at 1.6%, consistent with DB econ’s forecast but 0.1pp below consensus. Our economists also noted that, as a function of revisions, the trend over the last few months has weakened while 2017-2018 looks even stronger. This gives further ammunition to the FOMC’s doves at today’s meeting.

In Europe however, ahead of today’s Q2 GDP and July inflation release for the Eurozone, the releases only added to concerns over the economic slowdown. French GDP in Q2 grew by a smaller-than-anticipated 0.2% qoq (vs. 0.3% expected), while the Swedish economy actually contracted by -0.1% (vs. 0.3% growth expected). The European Commission’s economic sentiment indicator for the Eurozone fell to 102.7 in July, down from 103.3 in June and its lowest level since March 2016, and the sectoral breakdowns didn’t offer much hope either, as the industrial confidence reading fell to -7.4, its lowest since July 2013, and services confidence fell to 10.6, its lowest since September 2016. And to finish off the gloomy picture, Germany’s GfK consumer confidence reading fell to 9.7, the lowest figure in over two years, while German HICP inflation fell to 1.1% in July, the lowest since November 2016. The ECB and market tends to focus on the HICP, which is used for German inflation-linked bonds, though it has different weights from CPI (which surprised to the upside at 1.7%).

Turning to the day ahead, the outcome of the much-anticipated FOMC meeting is obviously the highlight for investors. It’s also a very big day for data releases, with the highlights being the advance reading of Eurozone GDP in Q2, along with the June unemployment rate and July CPI. In addition, there are German retail sales for June and the unemployment change for July, Italian Q2 GDP and unemployment for June, French CPI inflation for July, Canadian GDP for May, and from the US the MNI Chicago PMI for July. In terms of earnings, the main releases tomorrow include General Electric, Airbus and Lloyds Banking Group, and we have the second night of Democratic primary debates.

end

3A/ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 19.83 POINTS OR 0.67% //Hang Sang CLOSED DOWN 368.75 POINTS OR 1.31% /The Nikkei closed DOWN 1876.78 POINTS OR 0.87%//Australia’s all ordinaires CLOSED DOWN .46%

/Chinese yuan (ONSHORE) closed DOWN at 6.8827 /Oil UP TO 58.39 dollars per barrel for WTI and 65.03 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 6.8827 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8902 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

This is dangerous! Mainland China gathers forces on the Hong Kong border

(zerohedge)

Crackdown Coming? China Gathers Forces On Hong Kong Border Amid Unrest

Massive anti-Beijing protests which have gripped Hong Kong over the past month, and have become increasingly violent as both an overwhelmed local police force and counter-protesters have hit back with force, are threatening to escalate on a larger geopolitical scale after the White House weighed in this week.

With China fast losing patience, there are new reports of a significant build-up of Chinese security forces on Hong Kong’s border, as Bloomberg reports:

The White House is monitoring what a senior administration official called a congregation of Chinese forces on Hong Kong’s border.

From nearly the start of the protests which began over a proposed extradition bill (which would see Hong Kong citizens under legal accusation potentially extradited to the mainland) interpreted as major Chinese overreach inside historically semi-autonomous Hong Kong, officials in Beijing have suggested an “external plot” afoot, more recently alleging the hidden hand of the United States.

The latest charge made Tuesday by mainland government officials is that the still escalating Hong Kong unrest is the “creation of the US” — something which the admin official speaking under anonymity to Bloomberg firmly denied.

On Monday Secretary of State Mike Pompeo said during a press interview that “protest is appropriate” and that “we hope the Chinese will do the right thing” regarding respecting Hong Kong’s historic “one country, two systems” status. This was enough to elicit a quick response alleging US meddling out of Beijing on Tuesday.

“It’s clear that Mr. Pompeo has put himself in the wrong position and still regards himself as the head of the CIA,” Chinese Foreign Ministry spokeswoman Hua Chunying said at a news briefing. “He might think that violent activities in Hong Kong are reasonable because after all, this is the creation of the U.S.”

China’s position has been to recently declare the protests going “far beyond” what’s legal and “peaceful” amid clashes with police.

Last week Chinese military leaders hinted that People’s Liberation Army troops could be used to quell the protests following widespread reports of vandal attacks on the central government’s liaison office in Hong Kong, according to The New York Times. Ministry of National Defense, Senior Col. Wu Qian, said at the time, “That absolutely cannot be tolerated.”

For now, few details are known concerning the reported “build-up” of Chinese forces on the border, which could consist of military forces, as Bloomberg added to its report:

The nature of the Chinese buildup wasn’t clear; the official said that units of the Chinese military or armed police had gathered at the border with Hong Kong. The official briefed reporters on condition he not be identified.

The timing of the back and forth unsubstantiated allegations is interesting especially in light of President Trump seeking to reinvigorate stalled trade deal negotiations with China, currently being conducted in Shanghai following the ceasefire to the trade war.

China Manufacturing PMI Stuck In Contraction As Services Hit 2019 Lows

Despite record credit injections and endless easing, China’s economic survey data goes from bad to worse.

- While China Manufacturing PMI managed a de minimus gain from 49.4 to 49.7, it remains in contractionary territory for the 7th month in the last 9.

- China Services PMI continued to slide, back to its lowest since 2018.

Confirming global weakness seen in Japanese and European PMIs.

In a seemingly desperate reach, Bloomberg notes that the stronger result (49.4 to 49.7) signaled some optimism is emerging in the Chinese economy in spite of lingering uncertainty over trade talks and domestic demand.

PMI data improves as “the government’s tax cuts have helped improve growth slightly,” Yao Shaohua, economist at ABCI Securities Co. in Hong Kong

Under the hood things are less rosy with Manufacturing New Orders and Employment both contracting…

And Non-Manufacturing Employment is contracting…

We are less enthusiastic as July has more working days than June, which could also have helped lift production.

US-China Trade Talks Collapse After Half A Day Of Negotiations

That didn’t take long.

After roughly half-a-day of negotiations, the US trade delegation has broken off talks with its Chinese counterpart and is already on its way back to Washington, a sign that no new progress was made, and that trade talks between the US and China remain at an impasse.

According to Bloomberg, US delegates including Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer wrapped up talks with Vice Premier Liu He and their other Chinese counterparts on Wednesday afternoon at the Xijiao State Guest Hotel in Shanghai, according to a pool report.

As the talks ended, China’s Ministry of Foreign Trade issues a response to President Trump, who has been warning the Chinese not to keep stalling on the talks.

In response to a question about Trump’s tweets, Chinese Foreign Ministry spokeswoman Hua Chunying said that although she was not aware of the latest developments during the talks, it was clear it was the US that continued to “flip flop.”

“I believe it doesn’t make any sense for the US to exercise its campaign of maximum pressure at this time. It’s pointless to tell others to take medication when you’re the one who is sick,” Hua said.

The People’s Daily, mouthpiece of the Communist Party, also responded to Trump on Wednesday with a commentary saying that China has no motive to “rip off” the U.S. and has never done so, and China won’t make concessions against its principles on trade.

This week’s meetings, the first in-person trade talks since a G20 truce last month, amounted to a working dinner on Tuesday at Shanghai’s historic riverfront Fairmont Peace Hotel and a half-day of negotiations on Wednesday, Reuters reports. Neither team commented publicly.

Liu He bid farewell to his US counterparts as their motorcade pulled away from the Guest Hotel following a group photo. The talks concluded at around 1:45 pm local time – roughly 30 minutes before they were scheduled to begin.