GOLD:$1520.75 UP $3.55(COMEX TO COMEX CLOSING

Silver: $17.24 DOWN 2 CENTS (COMEX TO COMEX CLOSING)/

Closing access prices:

Gold : $1523.50

silver: $17.27

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 342/749

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 749 NOTICE(S) FOR 74900 OZ (2.3297 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 5201 NOTICES FOR 520,100 OZ (16.177 TONNES)

SILVER

FOR AUGUST

138 NOTICE(S) FILED TODAY FOR 690,000 OZ/

total number of notices filed so far this month: 1946 for 9,730,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

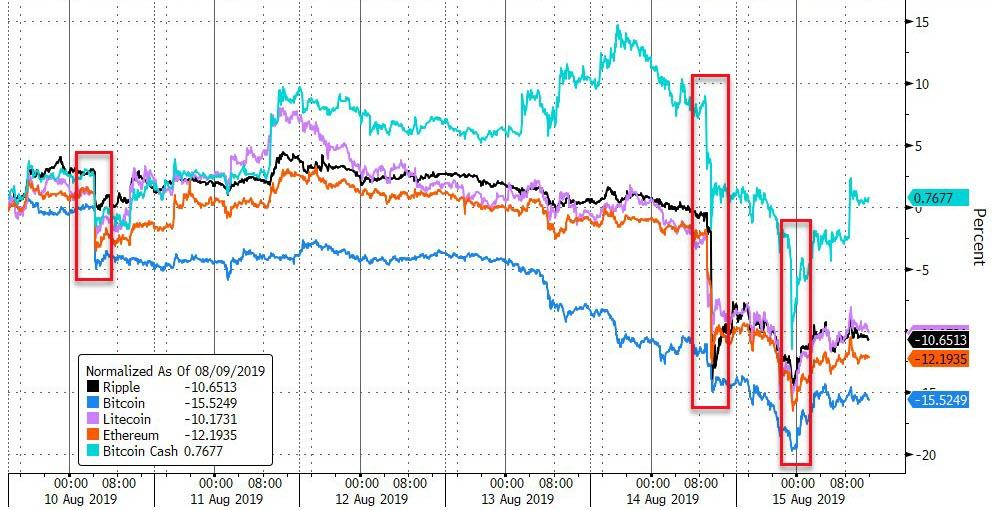

Bitcoin: OPENING MORNING TRADE : $ 9870 UP 109

Bitcoin: FINAL EVENING TRADE: $ 10,104 UP 47

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A SMALL SIZED 744 CONTRACTS FROM 233,839 DOWN TO 233,095… DESPITE THE STRONG 27 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR AUGUST, 0 FOR SEPT: 2700, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2700 CONTRACTS. WITH THE TRANSFER OF 2700 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2700 EFP CONTRACTS TRANSLATES INTO 13.50 MILLION OZ ACCOMPANYING:

1.THE 27 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

9.770 MILLION OZ INITIAL STANDING IN AUGUST.

WE HAD ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY WITH SOME SUCCESS..AND WE HAD LITTLE IF ANY SPREADING ACCUMULATION.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF AUGUST:

22,330 CONTRACTS (FOR 11 TRADING DAYS TOTAL 22,320 CONTRACTS) OR 111.600 MILLION OZ: (AVERAGE PER DAY: 2029 CONTRACTS OR 10.24 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 111.600 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 15.94% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1424.155 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 744, DESPITE THE 27 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 2700 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 1956 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2700 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 744 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 27 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.26 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.168 BILLION OZ TO BE EXACT or 167% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 138 NOTICE(S) FOR 690,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

AND NOW WE ARE WITHIN A WHISKER OF ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,169 BUT THIS TIME THE PRICE OF SILVER YESTERDAY WAS $17.18 AND HIGHER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 9.770 MILLION OZ

- CLOSE TO THE RECORD OPEN INTEREST IN SILVER 244,169 CONTRACTS (OR 1.228 BILLION OZ/, THE PREVIOUS RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4944 CONTRACTS, TO 598,906 ACCOMPANYING THE STRONG $13.60 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// //THE SPREADING ACCUMULATION OPERATION HAS NOW COMMENCED ONLY FOR SILVER AS LITTLE WAS ACCOMPLISHED IN THAT ENDEAVOUR TODAY….. THE LIQUIDATION( AND ACCUMULATION) PHASE FOR COMEX OI GOLD HAS NOW STOPPED FOR THE AUGUST CONTRACT MONTH

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7414 CONTRACTS:

AUGUST 2019: 0 CONTRACTS, DEC> 7414 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 598,906,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,358 CONTRACTS: 4944 CONTRACTS INCREASED AT THE COMEX AND 7414 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,358 CONTRACTS OR 1,235,800 OZ OR 38.44 TONNES. YESTERDAY WE HAD A STRONG GAIN OF $13.60 IN GOLD TRADING….AND WITH THAT GOOD GAIN IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 38.44 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER.THERE WAS NO APPRECIABLE SHORT COVERING IN THE GOLD COMEX ARENA AS MANY OF THE LONGS DEMANDING METAL JUST MORPHED INTO LONDON BASED FORWARDS.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 132,256 CONTRACTS OR 13,225,600 oz OR 411.37 TONNES (11 TRADING DAY AND THUS AVERAGING: 12,033 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY IN TONNES: 411.37 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 411.37/3550 x 100% TONNES =11.58% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3922.60 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 4944 WITH THE STRONG PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($13.60)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7414 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7414 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG SIZED GAIN OF 12,358 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7,414 CONTRACTS MOVE TO LONDON AND 4944 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 38,44 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $13.60 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAVE NOW COMMENCED WITH SPREADING ACCUMULATION OF SILVER OI CONTRACTS IN THIS MONTH OF AUGUST BUT ZERO OCCURRED YESTERDAY.. ALL SPREADING ACTIVITY IN GOLD HAS STOPPED DURING THIS ACTIVE DELIVERY MONTH OF AUGUST.

we had: 749 notice(s) filed upon for 74,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.55 TODAY//(COMEX-TO COMEX)

WE GOT BACK 7.63 PAPER TONNES OUT OF 11.11 LOST YESTERDAY

(A DEPOSIT OF 7.63 TONNES)

INVENTORY RESTS AT 844.29 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 2 CENTS TODAY:

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV

ANOTHER WHOPPING 3.977 MILLION OZ PAPER DEPOSIT INTO THE SLV

/INVENTORY RESTS AT 380.154 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 744 CONTRACTS from 233,839 DOWN TO 233,095 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORDED HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET EXCEPT TODAY AS WE HAD A RISING PRICE..OUR SHORT DERIVATIVE BANKERS ARE NOW IN DEEP TROUBLE AS THEY ARE TERRIBLY OFFSIDE AND NEED ASSISTANCE FROM THE GOVERNMENT (FED) TO PROVIDE THE NECESSARY COLLATERAL TO CARRY THAT SHORT POSITION…..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER FOR THE MONTH OF AUGUST, ALTHOUGH NEGLIGIBLE ACTIVITY YESTERDAY, AND THEY STOPPED ALL SPREADING ACTIVITY IN COMEX GOLD FOR THE MONTH OF AUGUST.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR AUGUST: 0, FOR SEPT. 2700 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2700 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 744 CONTRACTS TO THE 2700 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 1956 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.78 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ; AUGUST AT 9.770 MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 27 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 2700 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 6.88 POINTS OR 0.25% //Hang Sang CLOSED UP 193.18 POINTS OR 0.76% /The Nikkei closed DOWN 249.49 POINTS OR 1.21%//Australia’s all ordinaires CLOSED DOWN 2.80%

/Chinese yuan (ONSHORE) closed DOWN at 7.0399 /Oil UP TO 54.39 dollars per barrel for WTI and 58.30 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0399 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0555 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

a)This occurred prior to the Chinese comment that they hope that the USA will go half way in dealing with them.

Prior to that China rejects Trump’s tariff olive branch and they vow imminent retaliation against the Chinese. This still stands.

(zerohedge)

b)Hong Kong activist leaders calls for a run on Chinese banks and if that would happen it would destroy their banking system

(Watson/Summit News)

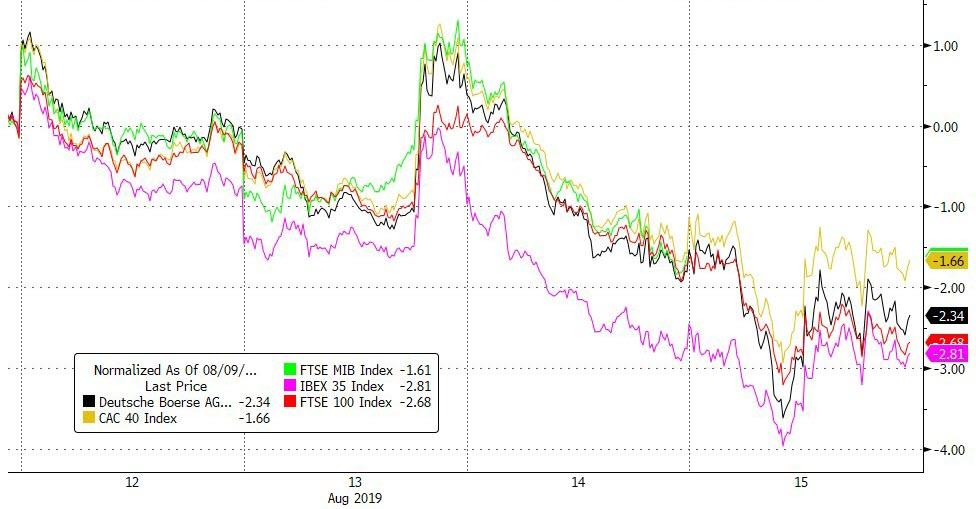

4/EUROPEAN AFFAIRS

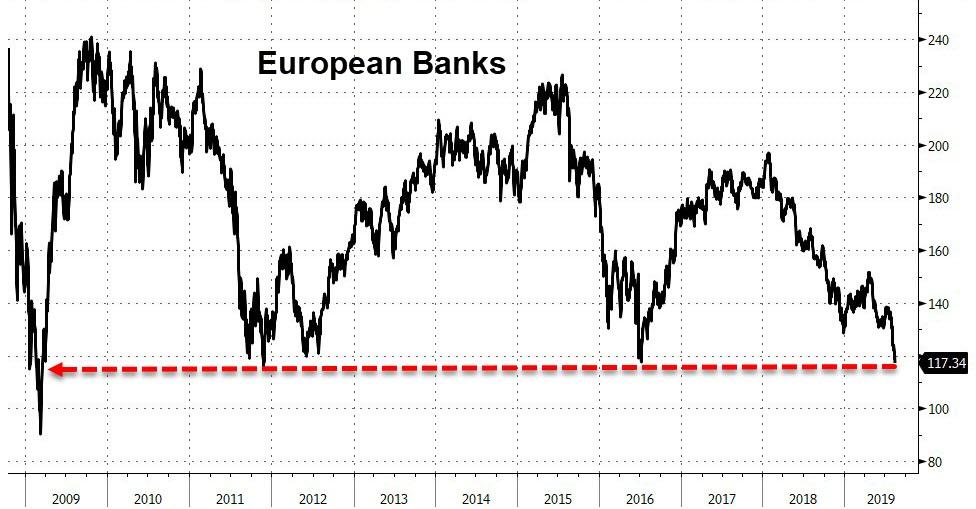

The big European banks did not like this: an ECB official says that new stimulus measures is coming in Sept and they “may overshoot”. The Euro stumbles and so does the banks.

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

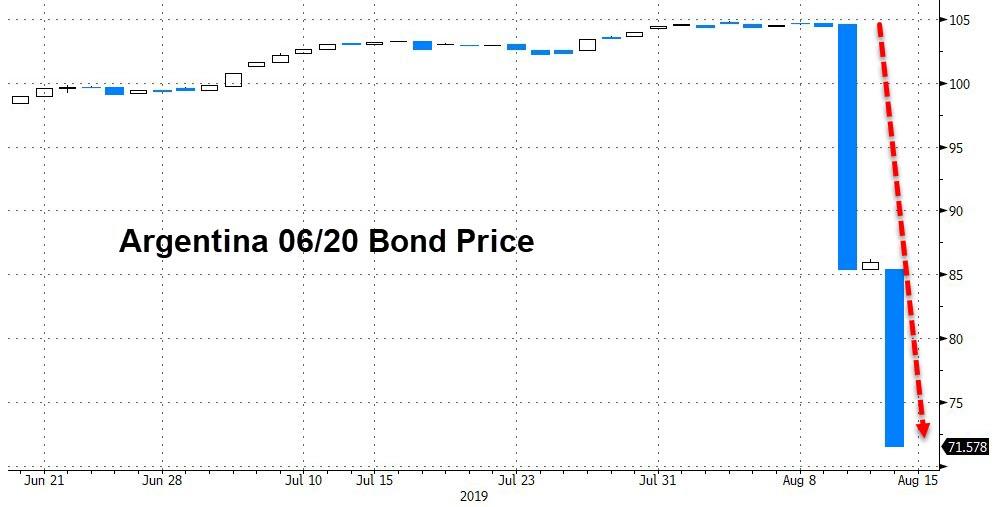

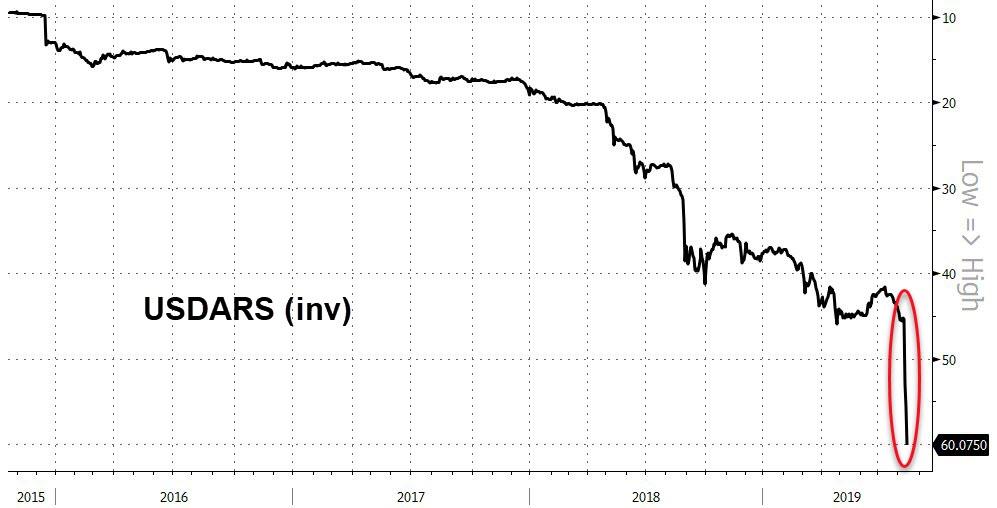

Argentina

Argentina basically collapses as its Peso is now over 60 pesos per dollar. The next big Argentina bond which is partly owned by Pimco has fallen badly and with a yield north of 50%, it will surely default

(zeorhedge)

9. PHYSICAL MARKETS

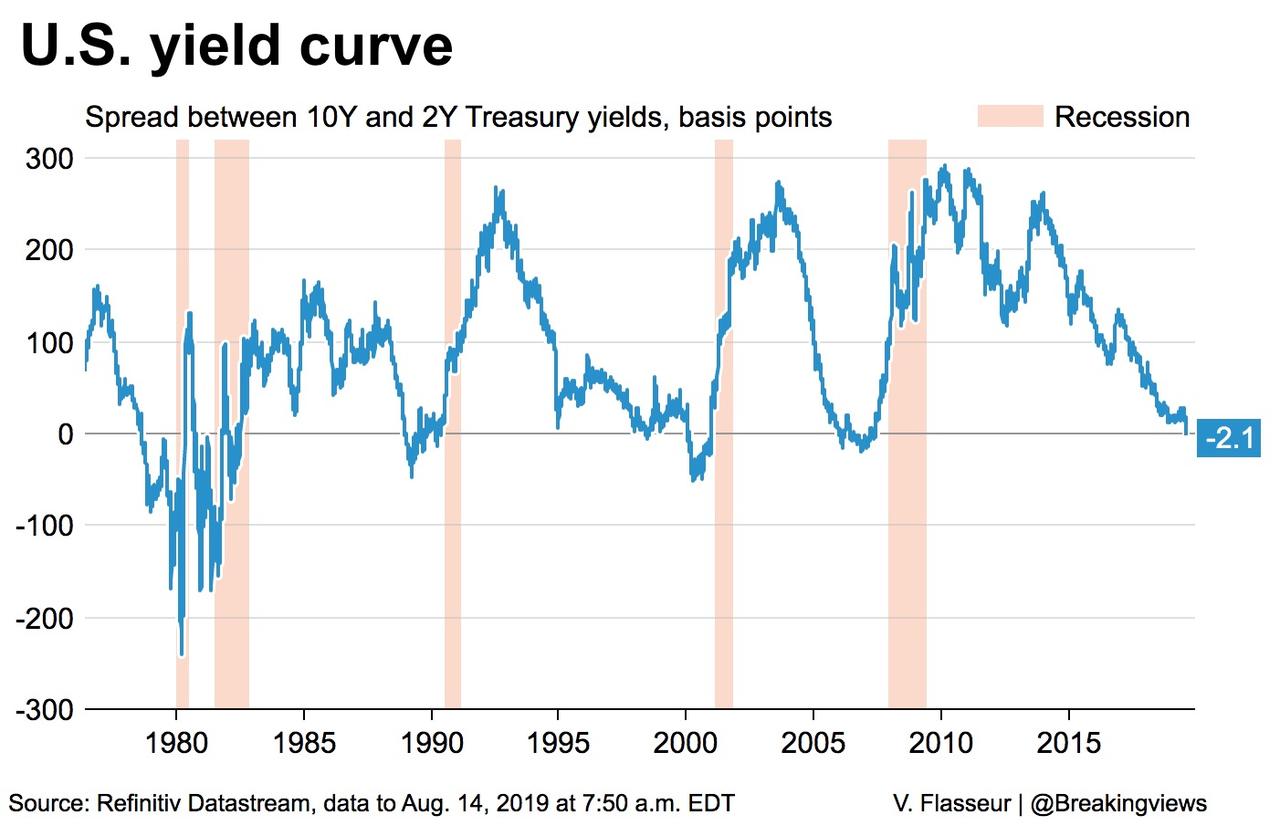

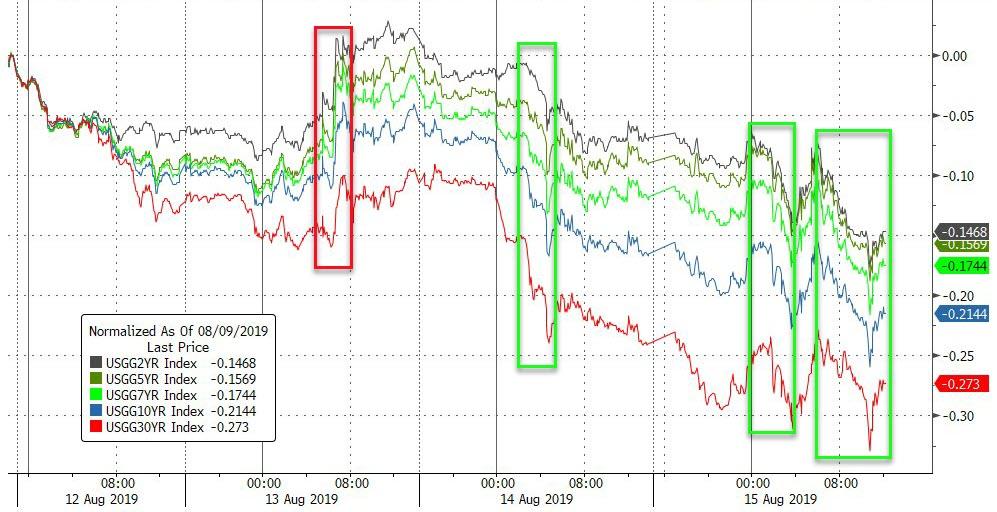

i)We brought this to your attention yesterday and it is worth repeating; the USA treasury bond curve inverts entirely for the first time since 2007

(Reuters/GATA)

ii)We also brought this to your attention: China is curbing gold imports for its citizens as it wants to stem the flow of cash leaving China

(Reuters)

iii)Murphy, Rule, Hemke and David Morgan discuss gold and silver

(GATA)

iv)An excellent podcast from Schiff

(Schiff)

v)Nicholas B on the fraudulent EFP issuance

(courtesy Nicholas B)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

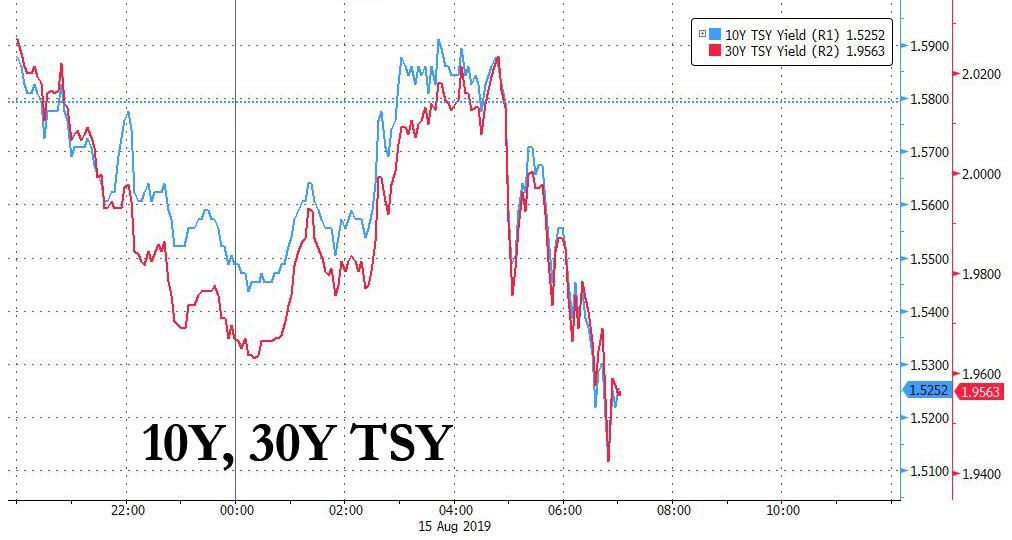

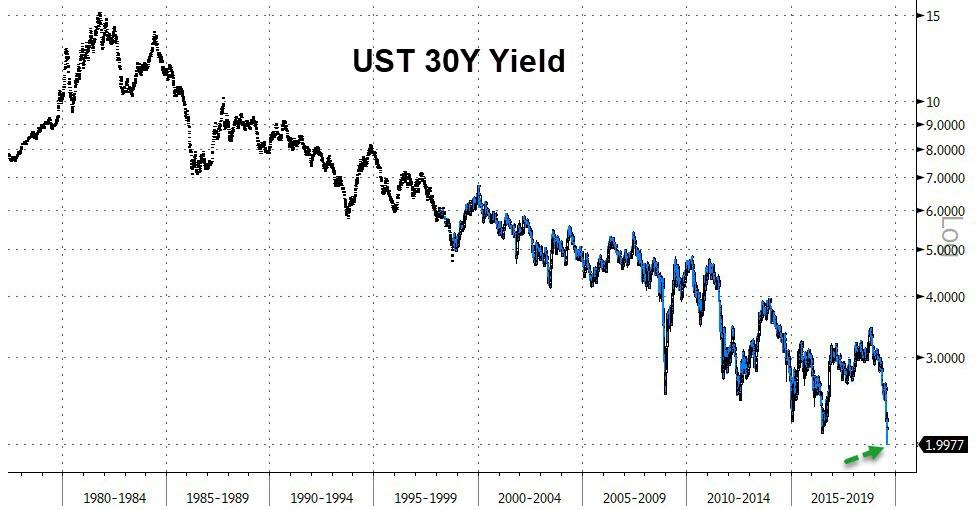

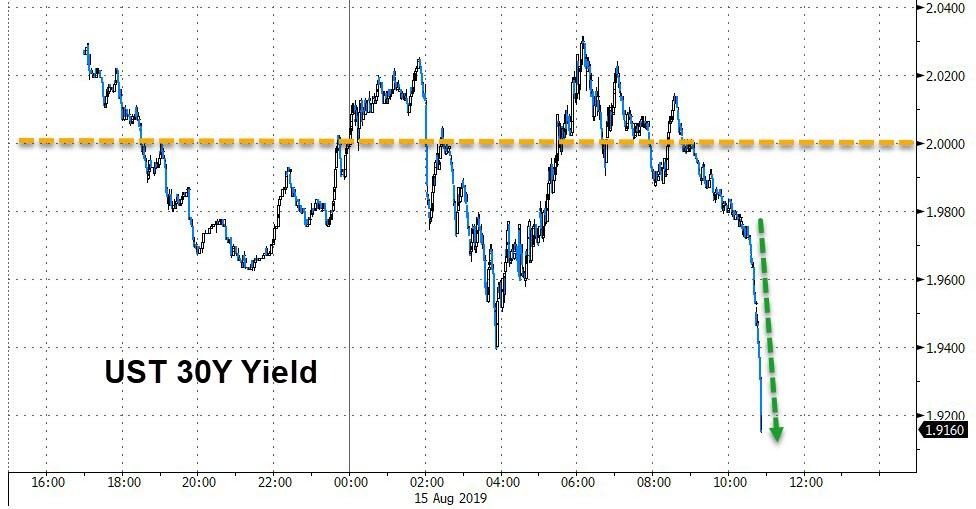

i)USA 30 yr bond yields tumbles to 1.98%..first time ever

(zerohedge)

b)MARKET TRADING/USA/MORNING

I)Absolute nonsense: futures suddenly explode higher on supposed Chinese conciliatory headline

These guys continue to talk and you need the newspaper to jolt futures.. the yuan hardly budged.

(zerohedge)

ii)That did not last long: Trump comments that China must do a deal on his terms and they will not do a deal half way. Dow reverses but the algos are trying to keep this thing into the green

ii)Market data/USA

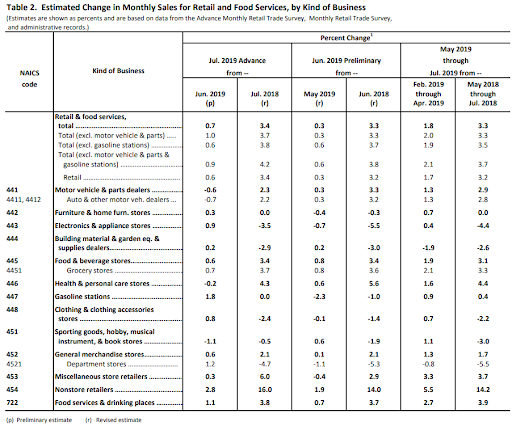

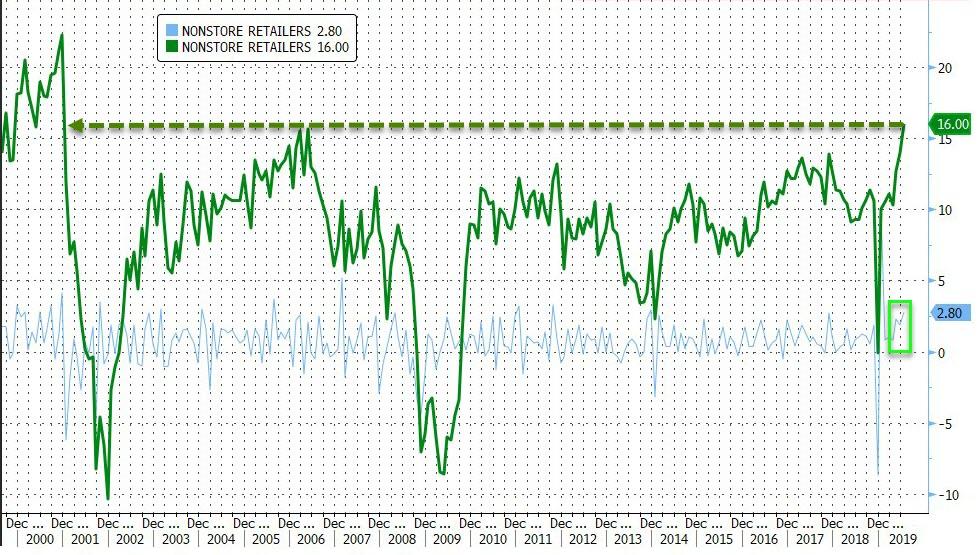

a)Retail sales surge in July but this was mainly due to Amazon’s |Prime Day

b)(zerohedge)

c)This is the far more important data points. Hard data USA manufacturing slumps back into contraction

(zerohedge)

end

iii) Important USA Economic Stories

(zerohedge)

iv) Swamp commentaries)

(zerohedge)

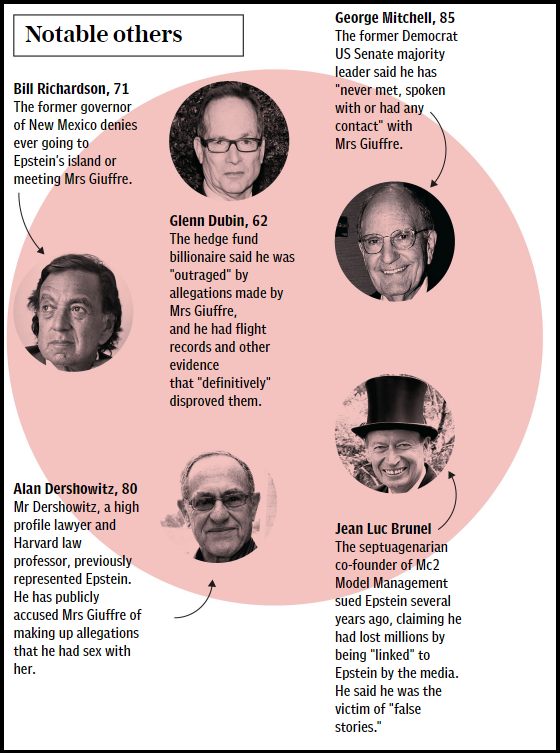

b)Where is Ghislaine?

c) Ghislaine Maxwell spotted in LA(zerohedge)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

i) Into CNT: 534,366.800 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 103,613 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 132,573 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 132,573 CONTRACTS EQUATES to 662 million OZ 94.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.70% ((AUGUST 15/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.20% to NAV (AUGUST 15/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -/70%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.09 TRADING 14.87/DISCOUNT 3.42

END

And now the Gold inventory at the GLD/

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO NGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 10//WITH GOLD UP $11.65 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER GOLD DEPOSIT OF 6.46 TONNES/INVENTORY RESTS AT 800.54 TONNES

JULY 9/WITH GOLD UP 70 CENTS, A HUGE PAPER WITHDRAWAL OF 2.89 TONNES WHICH WAS USED IN THE FUTILE RAID ON GOLD AND SILVER THIS MORNING//INVENTORY RESTS AT 794.08 TONNES

JULY 8/ WITH GOLD DOWN 35 CENTS A HUGE WITHDRAWAL OF 1.47 TONNES FROM THE GLD/INVENTORY FALLS TO 796.97 TONNES

JULY 5TH/WITH GOLD DOWN $19.50/NO CHANGES IN GOLD INVENTORY AT THE GLD//INV RESTS AT 798.44 TONNES

JULY 3// WITH GOLD UP $12.60 TODAY A SURPRISE WITHDRAWAL OF 1.76 TONNES FROM THE GLD//INVENTORY RESTS AT 798.44

JULY 2. WITH GOLD UP $18.90 A HUGE “PAPER” DEPOSIT OF 6.16 TONNES INTO THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 1: WITH GOLD DOWN $24.70 A HUGE “PAPER GOLD” WITHDRAWAL OF 1.76 TONNES FROM THE GLD/INVENTORY RESTS TONIGHT AT 794.04 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 15/2019/ Inventory rests tonight at 844.29 tonnes

*IN LAST 643 TRADING DAYS: 91.11 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 543- TRADING DAYS: A NET 75.43 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

JULY 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 9/WITH SILVER UP A SMALL 7 CENTS A GIGANTIC INVENTORY GAIN OF 4.026 MILLION OZ/ INVENTORY RESTS AT 332.518 MILLION OZ AND NOW IT SHOULD BE QUITE CLEAR THAT THE SLV ( AND GLD ARE FRAUDS)

JULY 8/WITH SILVER UP 7 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328,492 MILLION OZ

JULY 5/WITH SILVER DOWN 32 CENTS WE STRANGELY HAD A HUGE INVENTORY GAIN OF 2,234 MILLION OZ//INVENTORY RESTS AT 328.492 MILLION OZ

JULY 3 WITH SILVER UP 10 CENTS A HUGE INCREASE IN INVENTORY..INVENTORY RESTS AT 326.151 MILLION OZ

JULY 2/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 323.330 MILLION OZ//

JULY 1/ WITH SILVER DOWN 16 CENTS: A SURPRISING DEPOSIT OF 936,000 OZ INTO THE SLV/INVENTORY RESTS TONIGHT AT 323.330 MILLION OZ/

AUGUST 15/2019:

Inventory 380.154 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.16/ and libor 6 month duration 2.08

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .08

XXXXXXXX

12 Month MM GOFO

+ 1.93%

LIBOR FOR 12 MONTH DURATION: 2.03

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.10

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold At 2013 Highs Of $1,523/oz As Trump Calls The Fed “Clueless” and “Crazy” and Links Trade Wars to Hong Kong

* Gold prices consolidated today, after gold gained nearly 1% yesterday on safe-haven buying as stocks globally fell yesterday and today.

* The historic drop in long-term U.S. bond yields could portend a global recession which is impacting risk assets and seeing investors diversify into gold.

* China has curbed gold imports according to anonymous sources in western bullion banks as reported by Reuters (see below).

* Ordinarily, one would expect a pullback in gold after the recent rapid gains but these are far from ordinary times. Trump’s Presidency, trade wars, Brexit and other risks mean that gold could go higher before correcting lower.

* The wider economic, monetary and geopolitical backdrop will support safe haven assets and investors without an allocation to the precious metal should cost average into physical gold

Gold marks highest finish since 2013 as recession risk lifts the metal’s haven appeal

Gold rises as global recession fears lift safe-haven appeal

Exclusive: China curbs gold imports as trade war heats up

Dow tanks 800 points in worst day of 2019 after bond market sends recession warning

Stocks, oil tank on growing signs of global slowdown

Trump Calls the Fed “Clueless” and “Crazy”

U.S. 30-Year Yield Falls to Record Low and Curve Warns of Recession

Yield curve inversion shows Fed needs to cut rates: Trump adviser

Trump warns ‘good man’ Xi to treat Hong Kong humanely or risk trade deal

Trump Linking Trade to Hong Kong Risks Playing Into Xi’s Hands

Listen and Watch Jim Rogers Interview Here

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

14-Aug-19 1500.35 1513.25, 1241.69 1253.73 & 1341.61 1356.17

13-Aug-19 1527.20 1498.40, 1265.90 1240.38 & 1363.48 1338.67

12-Aug-19 1501.95 1504.70, 1244.82 1243.63 & 1343.64 1341.74

09-Aug-19 1503.50 1497.70, 1242.19 1240.99 & 1342.02 1338.05

08-Aug-19 1497.40 1495.75, 1230.26 1234.14 & 1335.08 1335.70

07-Aug-19 1487.65 1506.05, 1225.82 1239.33 & 1330.11 1341.44

06-Aug-19 1461.85 1465.25, 1199.59 1201.21 & 1304.85 1311.11

05-Aug-19 1457.45 1465.25, 1199.92 1203.85 & 1307.92 1310.23

02-Aug-19 1436.05 1441.75, 1184.17 1187.28 & 1294.02 1298.44

01-Aug-19 1406.40 1406.80, 1161.12 1161.74 & 1273.35 1273.29

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

We brought this to your attention yesterday and it is worth repeating; the USA treasury bond curve inverts entirely for the first time since 2007

(Reuters/GATA)

U.S. Treasury bond curve inverts for first time since 2007 in recession warning

Submitted by cpowell on Wed, 2019-08-14 13:40. Section: Daily Dispatches

From Reuters

Wednesday, August 14, 2019

LONDON — The U.S. Treasury bond yield curve inverted on Wednesday for the first time since 2007, in a sign of investor concern that the world’s biggest economy could be heading for recession.

The inversion — a situation where shorter-dated borrowing costs are higher than longer ones — saw U.S. 2-year note yields rise above the 10-year bond yield.

…

The curve inverted to as much as minus 1.7 basis points by 10″45 GMT.

Such an inversion, considered a classic recession signal, occurred last in June 2007 when the U.S. sub-prime mortgage crisis was gathering pace. The U.S. curve has inverted before every recession in the past 50 years, offering a false signal just once in that time. …

… For the remainder of the report:

https://www.reuters.com/article/us-us-bonds-curve/u-s-treasury-bond-curv…

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

We also brought this to your attention: China is curbing gold imports for its citizens as it wants to stem the flow of cash leaving China

(Reuters)

China curbs gold imports as trade war heats up, sources tell Reuters

Submitted by cpowell on Wed, 2019-08-14 18:35. Section: Daily Dispatches

From Reuters

Wednesday, August 14, 2019

China has severely restricted imports of gold since May, bullion industry sources with direct knowledge of the matter told Reuters, in a move that could be aimed at curbing outflows of dollars and bolstering its yuan currency as economic growth slows.

…

The world’s second largest economy has cut shipments by some 300-500 tonnes compared with last year — worth $15-25 billion at current prices, the sources said, speaking on condition of anonymity because they are not authorized to speak to the media.

The restrictions come as an escalating trade confrontation with the United States has dragged China’s pace of growth to the slowest in nearly three decades and pressured the yuan to its lowest since 2008.

China is the world’s biggest importer of gold, sucking in around 1,500 tonnes of metal worth some $60 billion last year, according to its customs data — equivalent to a third of the world’s total supply. …

… For the remainder of the report:

https://www.reuters.com/article/us-china-gold-exclusive/exclusive-china-…

END

Murphy, Rule, Hemke and David Morgan discuss gold and silver

(GATA)

Murphy, Rule, Hemke, and Morgan interviewed by Phil Kennedy

Submitted by cpowell on Wed, 2019-08-14 19:39. Section: Daily Dispatches

3:39p ET Wednesday, August 14, 2019

Dear Friend of GATA and Gold:

Philip Kennedy of Kennedy Financial today puts together a panel discussion of GATA Chairman Bill Murphy, Rick Rule of Sprott Holdings U.S., Craig Hemke of the TF Metals Report, and Dave Morgan of Silver-Investor.com, and they all seem very encouraged about the prospects for gold and especially silver. The discussion is 46 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=x518eQVuStA&feature=youtu.be

end

An excellent podcast from Schiff

(Schiff)

Schiff: The World Will Drown In An Ocean Of Inflation; Gold Is Going Ballistic

The gold market took a one-two punch on Tuesday as Trump made some concessions in the trade war and inflation numbers came in a bit higher than expected. Peter Schiff talked about it in his latest podcast, saying gold traders still don’t understand the gold rally.

Stock markets surged as gold and silver dropped after US trade representatives said they would delay some of the additional tariffs recently announced by President Trump. The Dow closed 372 points higher (before collapsing back 800 points lower yesterday). Meanwhile, the price of gold dropped below $1,500 briefly before rallying back above that key number.

Gold actually began selling off before the trade war news when the Consumer Price Index number came in hotter than expected. Peter said he knew that would happen.

That is the way the lemmings trade, because according to the conventional wisdom, if inflation is higher, then the Fed will be less likely to cut rates. After all, they’re cutting rates because inflation is too low and if inflation comes in hotter, well, then there’s less of a reason for the Fed to cut rates. So paradoxically, higher inflation is seen as being bad for gold. And the reason I’m saying paradoxically is because gold is an inflation hedge. Normally, the more inflation the more you want to buy gold.”

Peter said investors are banking on the Fed fighting inflation, but they’re wrong.

There is no way the Fed is going to fight inflation. I don’t care how high it is … One of these days the traders have to realize that these numbers don’t matter. I mean, maybe they matter to the public who has to live with a rising cost of living. But they don’t matter to the Fed. The Fed is going to take rates back to zero no matter what these numbers are, because the economy is going into recession even as inflation rises.”

Peter said eventually traders will figure it out and start buying gold when they see inflation rising and the Fed sitting on the sidelines.

As far as the trade war announcement goes, Peter said it just shows that Trump was bluffing when he announced more tariffs. He said he thinks it makes the president look very weak.

This trade war is lost. The only question is when do we surrender and how do we admit defeat.Again, I don’t think we’re going to get any kind of deal.”

Meanwhile, the mainstream is starting to talk about a looming recession. They are also calling for the Fed to cut rates and go back to QE. Peter said they still don’t get it. They don’t understand that this time around is not going to be like QE1, QE2, and QE3 where everybody made money.

I understood from the beginning that the Fed’s plan could not succeed, that they could never normalize rates, that they would have to go back to zero, that they could never shrink their balance sheet, that they would have to call it off and do more QE, because I understood the problem back then, and I still understand the problem now, and I understand the consequences.”

Peter noted that New Zealand’s central bank recently cut its interest rate by 50 basis points, basically in an effort to preemptively keep inflation from dropping below its target level. He pointed out that nobody wants a strong currency.

Everybody is weakening their currency to create more inflation. Well, what’s going to happen? The world is going to drown in an ocean of inflation and gold is going ballistic.”

Peter said the fact that gold sold off on trade war news indicates traders don’t really get it.

The people who are selling gold don’t get it. Gold is not going up because of the tariffs. Gold is going up because of what the reserve bank in New Zealand did and because that’s what all the central banks are doing …

Every central bank has bought into this nonsense that we must have inflation and that interest rates need to be negative. Inflation needs to be high enough to have real negative rates all over the globe. That’s where we are heading. So, if that is the case, people have no place to hide except gold and that is why they’re buying.”

Peter said ultimately we are going to have a global currency crisis – a US dollar crisis – because it is at the epicenter of the global fiat monetary system.

end

iii) Other physical stories:

Just look at the potential liability of the banks with respect to Exchange for physicals:

an email from Nicholas to me:

(courtesy Nicholas)

Hi Harvey,

In the attached file I have started to record, from 12th July onwards, the summary of the daily report from the CME gold and silver depositories. Not one ounce of registered gold or silver has left the Comex between 12th July until yesterday and only 0.2 tonnes of eligible gold.

*More from Nicholas…

Too LenientHi Bill,

I listened to your round table discussion this morning.I believe that some of the participants were too pessimistic about the prospects of silver just because JP Morgan has 150 million troy ounces (primarily in the eligible category).

Assume these EFPs remain unredeemed claims. Then the profile of total potential claims looks like:

Regards

Nicholas

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

US Futures Slide, Yields Plunge After China Spurn Trump, Vows Retaliation

For the 4th day in a row the pattern of a stronger risk open following by a sharp drift lower in both asset prices and yields has re-emerged, much to the frustration of BTFDers.

Global stocks opened for trading on the right foot, with US equity futures initially rising despite 30Y yields falling to all time lows below 2.00% late on Thursday, after several late evening tweets by Trump seemed to indicate further conciliation between the US and China in the ongoing trade war while the PBOC finally fixed the yuan slightly stronger at 7.0268, vs 7.0312 one day before, if slightly weaker than expected 7.0236. However, it all ended with a bang, with S&P futures falling hard, and signaling another weak open for U.S. stocks, which fell 3% on Wednesday on rising recession fears …

… and European stocks slumping after China stepped up its trade-war rhetoric, vowing imminent retaliation against the US, and roiling markets that had been starting to calm. The result: US traders walking in to another sea of red.

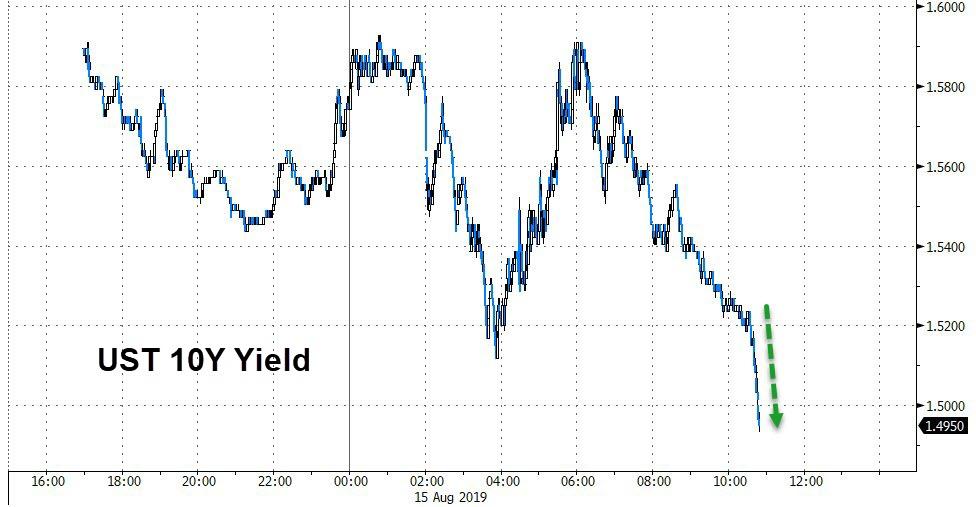

Treasuries and European bonds rallied, with the 10Y yield sliding further, and dropping as low as 1.51% while the 30Y dropped deeper into record territory, sliding as low as 1.95%, a new all time low.

“The only game in town is the central banks, hence the bond markets are rallying,” said Peter Schaffrik, global macro strategist at RBC Capital Markets. “We have regional bonfires in Hong Kong, Argentina, Japan against South Korea, and none of these are going away easily; each and every one is not necessarily strong enough to cause trouble.“

As widely discussed on Wednesday, recession fears grew on Wednesday after the 2s10s TSY spread inverted for the first time in 12 years, when the same yield curve inversion presaged the 2008 recession, and pretty much every other recession in the past 50 years.

“We have seen stocks trading very poorly as a result of the yield curve inversion, so that will be flashing some additional warning lights for the Fed that they have to do more,” said Andrea Iannelli, investment director at Fidelity International. “The only question is, can the Fed out-dove the market? At the very least they will have to match market expectations in the short term.”

So far the Fed is failing to out-dove the market, and the MSCI Asia Pacific Index declined, led by energy and health-care firms, after an inverted Treasury yield curve spurred worries over a possible recession. Country benchmarks were mixed, with Australia falling and Hong Kong advancing, while trading volume jumped across the region. Japan’s Topix retreated 1% to a seven-month low, as electronic firms and retail giants weighed on the gauge. The Shanghai Composite Index reversed earlier losses to close 0.3% higher, with Ping An Insurance and Foxconn Industrial Internet among the biggest boosts. China’s central bank added liquidity to the financial system amid prolonged trade tensions with the U.S.

After initially trading higher, Europe’s Stoxx 600 slumped as much as 0.5%, erasing earlier gains, after China’s surprise warning it would have to take countermeasures after the latest trade war salvo. The Chinese comments sent London and Frankfurt lost over 1%.

Meanwhile, in rates German 30-year yields dipped below minus 0.2% for the first time. Ten-year yields touched a record low of minus 0.67% with Sept. bund futures rising +25 ticks to 178.56; France 10y -1bp to -0.38%; Italy 10y +1bps to 1.51% Also notable: Europe’s 50Y swap rate turned negative for the first time ever.

Meanwhile, across the Atlantic, and as noted above, Treasuries outperformed bunds, while core bonds lead gains over semi-core peers and curves flatten. Italian bonds are steady with futures volumes running at less than half the 10-day average. Gilts rose amid haven buying even as U.K. retail sales for July beat the median estimate.

What sent the U.S. curve over the brink into inversion was German data on Wednesday that showed the economy had contracted in the quarter to June. That came on the heels of dire Chinese data for July. The British yield curve also inverted. The German curve is at its flattest since 2008.

The growth panic comes amid economic stress in Argentina and some other emerging markets, fears of Chinese military intervention in Hong Kong and trade tensions that show no sign of abating.

“Hoping for the best on the policy front but positioning for the worst on the economic backdrop seems to be the flavor of the day,” said Stephen Innes, a managing partner at Valour Markets. “The Fed, now out of necessity alone, will need to adjust policy much more profoundly than they expected.”

In FX, the dollar index .DXY was down at 97.862, with the euro – which has now emerged a carry funding and safe haven currency just like the yen – up at $1.1155; and speaking of the yen, it was flat at 105.8 to the dollar having earlier traded at 106.74. The currency has gained against the dollar for eight of the past 10 sessions. Excluding a mini-crash episode in January, it recently hit 17-month highs. The pound traded near the day’s high as U.K. retail sales data for July unexpectedly rose; Australia’s dollar bounced back from Wednesday’s sell-off after employment beat forecasts and damped bets on a central bank rate cut next month

In commodities, oil prices plunged with Brent crude LCOc1 losing another 2% to $58.4 a barrel, after shedding 3% overnight. Safe-haven gold was up 0.3% at $1,520 per ounce XAU=, just off recent six-year highs.

Market Snapshot

- S&P 500 futures up 0.8% to 2,863.25

- STOXX Europe 600 up 0.07% to 366.41

- MXAP down 0.9% to 149.84

- MXAPJ down 0.5% to 483.27

- Nikkei down 1.2% to 20,405.65

- Topix down 1% to 1,483.85

- Hang Seng Index up 0.8% to 25,495.46

- Shanghai Composite up 0.3% to 2,815.80

- Sensex up 1% to 37,311.53

- Australia S&P/ASX 200 down 2.9% to 6,408.09

- Kospi up 0.7% to 1,938.37

- German 10Y yield fell 0.5 bps to -0.655%

- Euro up 0.06% to $1.1146

- Italian 10Y yield fell 10.9 bps to 1.156%

- Spanish 10Y yield rose 0.4 bps to 0.147%

- Brent futures down 1.5% to $58.60/bbl

- Gold spot up 0.2% to $1,519.56

- U.S. Dollar Index little changed at 97.94

Top Overnight News from Bloomberg

- China called planned U.S. tariffs on an additional $300 billion in Chinese goods a violation of accords reached by Presidents Donald Trump and Xi Jinping, signaling its intention to impose retaliatory measures

- The recession alarm bell ringing in U.S. government bond markets sent investors rushing once more to haven assets, pushing the world’s stockpile of negative-yielding bonds to another record

- The inverted yield curve looks set to be a global phenomenon, with major Asian debt markets primed to mirror the moves in Treasuries as fears grow that the world economy is teetering on the brink of a recession

- Germany Inc.’s outlook for the rest of the year is filled with gloom, suggesting a recession could be in the cards. Companies from Europe’s largest economy lead the list of profit warnings issued in the region during the latest earnings season

Asian equity markets conformed to the rout seen on Wall St. where all major indices fell around 3% and the DJIA slumped 800 points in its worst performance YTD after recent weak data from China and Germany, with recession fears also stoked after the US 2s/10s curve inverted for the first time since 2007. ASX 200 (-2.9%) and Nikkei 225 (-1.2%) were lower in which the energy sector led the declines in both indices after similar underperformance stateside following a near-5% drop in crude prices and with Australia mulling over a slew of earnings releases, although gold stocks have bucked the trend as the stock sell-off spurred safe-haven appeal. Hang Seng (+0.7%) and Shanghai Comp. (+0.3%) were heavily pressured at the open but with downside later stemmed after continued PBoC liquidity efforts in which it injected CNY 30bln through reverse repos and CNY 400bln through 1yr MLF, while reports that Hong Kong Airport resumed normal operations and with strength in China Unicom post-earnings helped soften the blow for Hong Kong which briefly turned positive. However, the recovery in the Hang Seng was short-lived due to the broad risk averse tone and with losses in index heavyweight Tencent following mixed earnings and a cautious outlook. Finally, 10yr JGBs printed fresh highs as the global recession fears spurred a safe-haven bid, which saw the 10yr, 20yr and 30yr JGB yields at their lowest in more than 3 years. This coincided with the US 2s/10s yields winding in and out of inversion and the US 30yr yield dropping below 2% for the first time on record, while mild support was also seen following stronger results at the 5yr JGB auction.

Top Asian News

- Hong Kong and China Stocks Rise in Shadow of Global Growth Fears

- China Border Agents Probe Hong Kong Travelers’ Personal Devices

- Chinese Champion Huawei Under Fire for Calling Taiwan a Country

Major European indices were initially firmer at the open but following negative updates on the US-China trade front, a further bout of risk off swept through markets [Euro Stoxx 50 -1.5%], on reports that China’s Finance Ministry say China will have to take countermeasures on US moves and their actions violate the consensus achieved at the Osaka G20 meeting. No notable over/under performers amongst indices which are all firmly in negative territory following the aforementioned US-China update, but as a reminder Italy’s equity markets are closed due to Assumption Day. Sectors are posting a slightly mixed performance but have also dropped firmly into negative territory, Energy names are lagging as oil prices remain under pressure with the added factor of Iran’s Grace 1 tanker reportedly to be released today; though the US Department of Justice are trying to seize the tanker. Also factoring on the complex is underperformance from Vestas Wind Systems (-3.5%), who represent 3.5% of the Stoxx 600 Oil & Gas index, after missing on Q2 metrics and narrowing revenue guidance. Elsewhere, RBS (-10.0%) are at the bottom of the Stoxx 600 weighed on by a downgrade at HSBC; note, the Co. are trading ex-dividend today. Returning to earnings, and at the other end of the Stoxx spectrum, are both GVC (+2.3%) and Carlsberg (+3.5%) after stating that FY outlook is ahead of expectations and confirming FY guidance with organic beer volume higher by 1.4% YY respectively.

Top European News

- Vestas Profit Misses Forecasts as Wind Turbine Revenue Falls

- German Profit Warnings Signal Trade Woes May Trigger Recession

- U.K. Retail Sales Unexpectedly Rise Amid Online Promotions

In FX, the upbeat jobs data has helped the Aussie withstand another bout of risk aversion prompted by an official blast from China on the trade front and reiteration that Beijing will retaliate with countermeasures against the additional Usd300 bn tariffs that contravene the G20 truce agreement. Aud/Usd is holding firmly above 0.6750, albeit off 0.6790 overnight highs spurred by a significant beat in the payroll count vs expectations, and mainly due to full time workers. Similarly, Sterling got an unexpected lift from UK retail sales data confounding consensus for some payback after previous excesses, but Cable continues to meet resistance around 1.2100.

- JPY – The Yen is back to roughly flat vs the Dollar and most other currency counterparts after a sudden slide in early EU trade that is still baffling market participants and pundits given no clear catalyst for the move. For the record, factors ranging from in incorrect order to official intervention have been touted, and clearly the speed of the sell-off did trigger stops and chart-based transactions, while a more macro or fundamental motive could have been a back-up in US Treasury yields and curve dis-inversion. However, risk aversion has resurfaced amidst the latest Chinese sabre-rattling and Usd/Jpy is back below 106.00 from circa 106.80 at one stage.

- NOK – The Norwegian Crown has also been volatile within 10.0470-9.9720 parameters against the Euro, as the Norges Bank removed specific reference to next month when maintaining guidance for further policy normalisation this year due to heightened external risks and uncertainty. Nevertheless, it remains on track for more divergence in terms of benchmark rates compared to G10 and many if not all other global Central Bank peers, bar the Riksbank.

- EUR/CAD/CHF/NZD – All relatively rangebound vs the Greenback even though overall sentiment has taken another turn for the worse after tentative signs of stability. The single currency is stuck between 1.1155-35, the Loonie is pivoting 1.3300, while the Franc has tracked its safe-haven Yen peer to a degree from around 0.9755 to 0.9725, and the Kiwi is straddling 0.6450, albeit largely on the downside towards 0.6425.

- EM – Amidst widespread deviation for global/general and more specific or unique reasons, perhaps the rebound in Usd/Cnh from circa 7.0305 lows to 7.0630 is telling/ominous after 7.0268 Usd/Cny fix. Note also, Hong Kong has slashed its 2019 GDP projection to exacerbate global growth concerns, though the Government has injected Hkd 19.1bn via economic measures to try and ward off recession.

In commodities, Brent and WTI prices are firmly in negative territory, post the US-China updates, and have dipped below the USD 59.00/bbl and USD 55.00/bbl levels respectively which had been somewhat of a base for the benchmarks overnight after yesterdays significant downside for the complex, which saw Brent settle lower by around 3% on the day. On the supply/geopolitical front reports indicate that it is likely Iranian tanker Grace 1 will be permitted to leave Gibraltar as Chief Minister Picardo will not renew the vessels detention order which expires on Saturday; after which a court is to decide on the next steps. However, reports indicate that the US Department of Justice has applied to seize the tanker, which casts some doubt over the likelihood of the vessels near-term release. As a reminder prior to the vessel’s seizure reports indicated that it had loaded a 2mln/bbl cargo in Iranian waters around mid-April. Elsewhere, tomorrow sees the delayed release of OPEC’s monthly oil market report, focus will be on whether it takes a similar stance to the IEA and EIA reports in cutting 2019 world oil demand growth forecast. Turning to metals, where spot gold (+0.4%) remains above the USD 1500/oz mark as the market has settled somewhat from yesterday’s significant risk-off moves, but didn’t benefit much from the aforementioned trade headlines; the data slate ahead includes a number of notable US data points, which may spark further bouts of global growth worry if the prints are weak. Separately, copper prices are similarly little changed in-line with the largely tentative market sentiment thus far.

US event calendar

- 8:30am: U.S. Initial Jobless Claims, Aug. 10, est. 212k, prior 209k

- 8:30am: U.S. Retail Sales Advance MoM, July, est. 0.3%, prior 0.4%

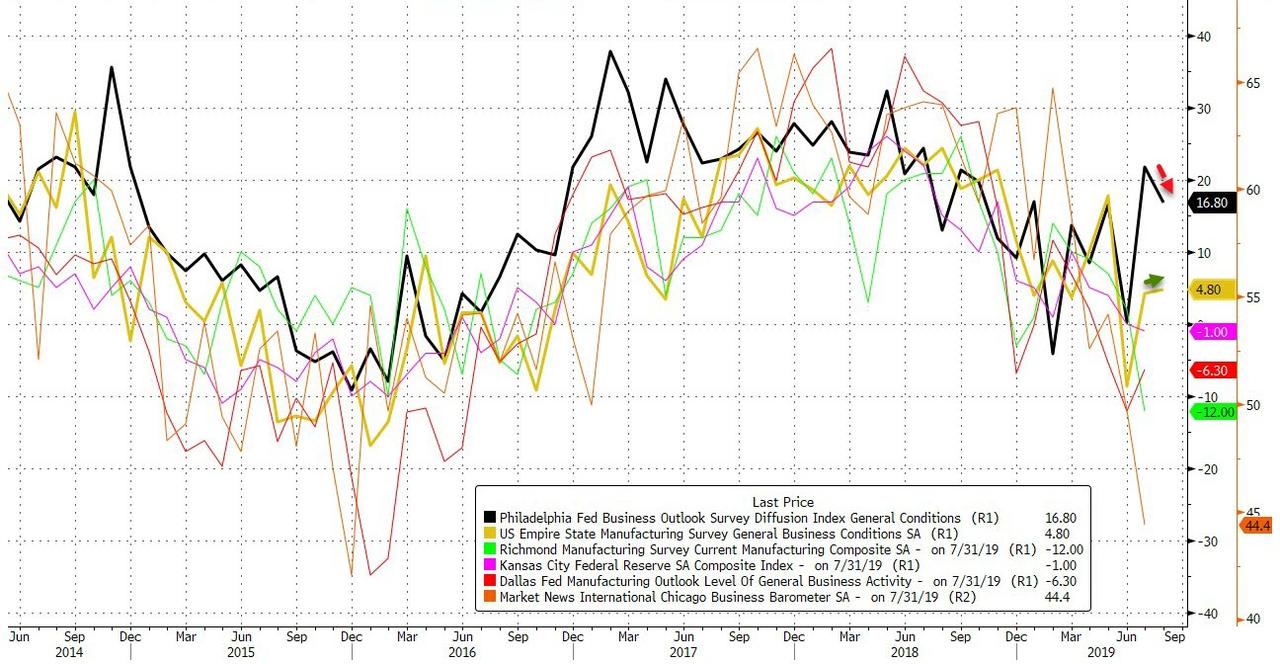

- 8:30am: U.S. Empire Manufacturing, Aug., est. 2.0, prior 4.3

- 8:30am: U.S. Philadelphia Fed Business Outl, Aug., est. 9.5, prior 21.8

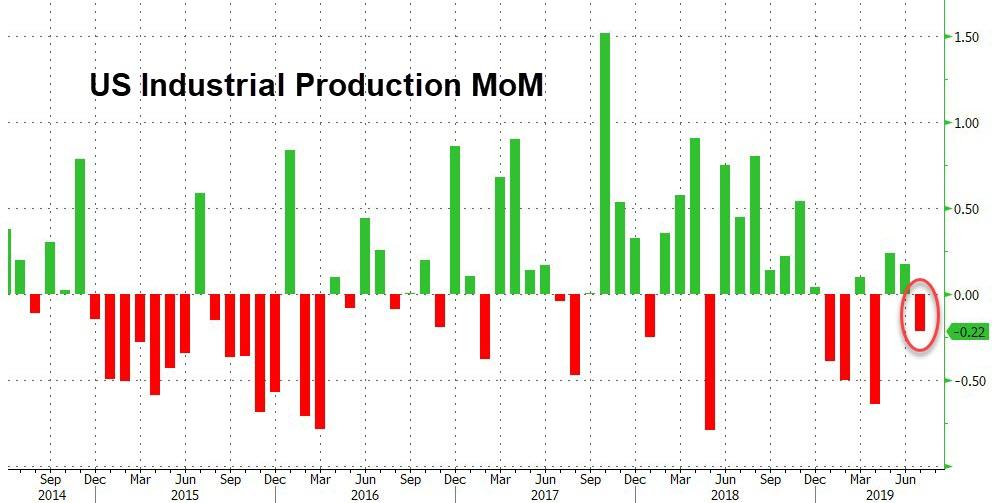

- 9:15am: U.S. Industrial Production MoM, July, est. 0.1%, prior 0.0%

- 4pm: U.S. Net Foreign Security Purchases, June, no est., prior $3.5b

DB’s Craig Nicol concludes the overnight wrap

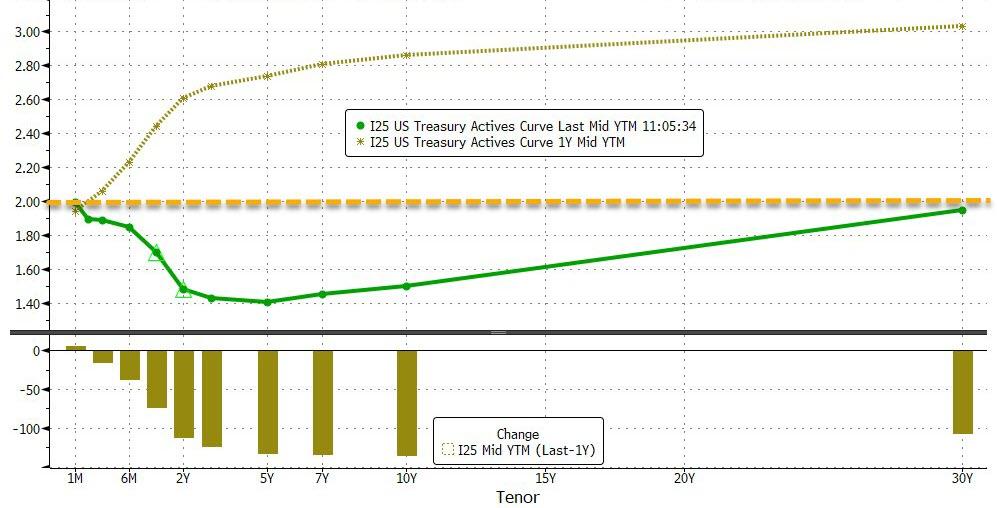

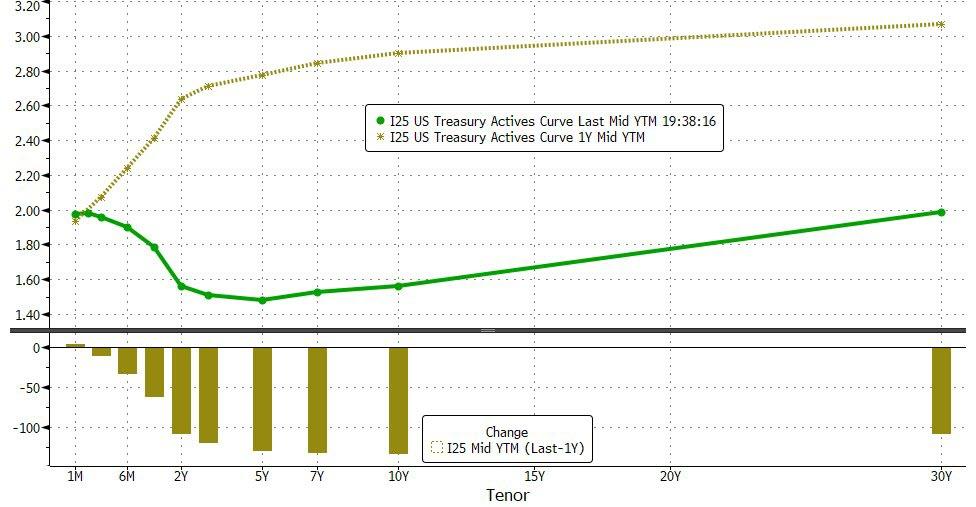

A mere 4,453 days had passed since the last time the US 2s10s curve was negative. That was until yesterday morning when the curve struck a low of -1.9bps. It ebbed and flowed around 0 for most of the day after that before closing the US session at +0.1bps. Still, the symbolic nature of the curve inverting is not to be underestimated. In fairness all of the other frequent measures of the yield curve have already inverted, namely the 3m10s (-37.8bps), 3s5s (-2.8bps), 2s5s (-8.0bps), and 18m3m-3m (-58.0bps). However, as we’ve discussed on many occasions, the 2s10s curve has the greatest power as a recession indicator in our view.

In fact, Jim must have had a dull day on holiday as he kept on emailing us about the 2s10s inversion. In the end he asked us to put this para in this morning to reflect his view. “Although other measures of the US yield curve have progressively inverted over the last few quarters, for me yesterday’s 2s10s inversion is the one that worries me most. In my opinion, it has the best track record for predicting an upcoming recession over more cycles than any of the others. Indeed, every inversion since 1956 has seen a recession follow. Although the median length of time to a recession is 17 months, credit spreads have pretty much exclusively widened from the point of inversion onwards (see p7 of Yield Curve 101 here ). Of those 2 of the 9 recessions since the 1950s took more than 2 years to materialise after the first inversion though. The first in the mid-1960s (took nearly 4 years) was due to a Fed policy error where the Fed didn’t raise rates as expected (they actually cut) with inflation rising. The curve re-steepened and only inverted again as the Fed reversed course and hiked a few quarters later. The recession soon followed the subsequent inversion. The second, following the May 1998 inversion, took 34 months until a recession arose but the inversion was relatively brief and occurred just prior to the Russian/LTCM crisis where the Fed rapidly cut 75bps thus re-steepening the curve. The Fed then raised rates again from 1999 and the curve re-inverted in early 2000, around a year before the actual recession. So, the conclusion is that the Fed has successfully acted before to delay the inversion turning into a recession but only on 2/9 occasions. Given that the market already prices in 65bps of cuts before year end it feels like they might need to out-pace that to make it 3 out of 10 where they’ve delayed the recession. I should say that our analysis uses closing prices, and we actually closed at 0.1bps last night so I have to be a bit careful here. But having spent most of my career suggesting that this was the most reliable indicator that the US cycle is entering its last act, I have to become far more negative now it looks likely to be triggered, especially given the history of credit spreads immediately after. As an aside, I don’t think this time is different because of term premium being much lower and global QE etc. as we think the causality is through animal spirits. In an inverted yield curve environment, this gets increasingly drained and thus impacts financial and economic activity. So I really don’t care why the curve inverts, just that it does. Anyway, see our “Yield Curve 101” link above for more and I’ll go back to steeper and steeper mountains in the Alps (no flat bits here) and hand you back to Craig and Quinn.”

That move for the curve included a 12.5bps rally for 10y Treasuries which saw them break below 1.60% to close at 1.580%, although this morning they’ve pushed on further to 1.549%. That puts them just 18.9bps above the 2016 lows now. In addition to that, the 10y real yield turned negative yesterday for the first time since October 2016. As for 30y yields, they have dipped below 2% for the first time ever overnight, currently trading at 1.966%, while 2y yields are trading at 1.557% which compares to a closing level on Tuesday of 1.669%. It’s quite amazing to think that 30y yields are also now below the effective Fed Funds rate. It was a similar story in Europe too yesterday, where 10y Bunds dropped -4.1bps and to a new low of -0.654%. Spain and Portugal are now within 14bps and 16bps of being negative at the 10y, while that Austrian 100y bond is now trading at a cash price of over 200. That corresponds to a yield of 0.689%. Not to be outdone also, the 2s10s Gilt curve also briefly turned negative yesterday.

While the 2s10s curve turning negative no doubt compounded the risk-off yesterday, the reality is that sentiment was already hit hard by that weak China data and then later by confirmation that Germany’s economy contracted in Q2 (more on that below). The trade rhetoric didn’t help at the margin too with commerce secretary Wilbur Ross telling CNBC that there is no date set for US-China trade talks while later on White House trade advisor Peter Navarro said in an interview with Fox that the US “can’t meet China halfway” and that “seven structural issues” still remain. Interestingly one of those was a reference to “hacking,” which hasn’t been a clear part of the trade talks so far and is likely to present an additional hurdle to a deal. Nevertheless, President Trump later tweeted overnight that “Good things were stated on the call with China the other day.” He also said that the tariff postponement to December “actually helps China more than us, but will be reciprocated.

Unsurprisingly, equity markets had a day to forget. The S&P 500, DOW and NASDAQ tumbled -2.93%, -3.05% and -3.02%, respectively, with the move for the S&P 500 the second worst since December. Sector wise, energy and financials fell the most with the S&P 500 banks index actually tumbling -4.29% for the biggest daily loss since 4 December. That index has now fallen on 8 of the last 11 days and is back to trading at the lowest since March. The moves were incredibly broad-based, with 99.4% of S&P 500 companies trading lower, which was the worst ratio since February 2018. Other risk assets also struggled mightily yesterday too. In Europe the STOXX 600 closed down -1.68%. EM equities shed -2.88% and currencies retreated, highlighted by the South African rand (-1.83%), the Brazilian real (-2.10%), and the Argentine peso (-7.36%). In commodities oil fell -3.27%, while gold gained +0.99% to reach $1,516, its highest level since 2013. Meanwhile HY credit spreads in the US and Europe were +24bps and +3bps wider, respectively. On that, yesterday we published a short note which makes six observations about recent price action in the US IG and HY credit market. See the link here for the full report.

Overnight, markets are mostly trading lower in Asia too, however the good news at least is that most bourses have pared back heavier declines at the open. As we go to print the Nikkei (-1.29%), Shanghai Comp (-0.62%) and Hang Seng (-0.17%) are all in the red along with the ASX (-2.61%) following the latest employment data in Australia. Meanwhile, S&P 500 futures are up +0.19% as we type. In rates, with the US 2s10s curve hovering near where it closed last night, bond markets have rallied through much of Asia too with 10y JGBs in particular now down to -0.247% and approaching the 2016 low of -0.295%.

Meanwhile, and in some non-curve related news, with 11 weeks to go until the UK’s scheduled departure from the EU on October 31st, Labour leader Jeremy Corbyn has written to other MPs who oppose a no-deal Brexit, calling on them to support a “strictly time-limited temporary government” led by Corbyn as Prime Minister, with the purpose of getting an Article 50 extension and calling a general election. However, with a number of MPs in other parties, including the anti-Brexit Liberal Democrats, opposing Corbyn as PM, this may prove a difficult vision to actually realise. Corbyn’s letter also said that he would call a no-confidence vote “at the earliest opportunity when we can be confident of success.” The House of Commons won’t be sitting again until September 3rd though, so there’ll be at least a couple of weeks before any moves like this could take place.

In other news, the data highlight was the negative GDP print in Germany, which showed the economy contracted -0.1% qoq as expected, which certainly did not help sentiment. Our economists have lowered their full-year 2019 German growth forecasts to 0.3% from 0.7%, see their full note here . Elsewhere, French CPI was confirmed at 1.3% yoy and -0.2% mom, though UK CPI came in higher than expected at 2.1% yoy versus expected 1.9%. The UK’s core CPI metric printed at 1.9%, 0.1pp stronger than expected.

On the Fedspeak front, the only notable comments from St. Louis President Bullard, who said that “macroeconomic outcomes are quite good for the US.” He talked about the ongoing Fed policy review, saying that the key question is how to avoid getting “stuck at an inflation rate that’s lower than your inflation target.” He included negative interest rates as a potential tool, which may have contributed to the marked selloff in bank stocks, though other Fed officials have downplayed the likelihood of that tool. Next week is the Fed’s annual Jackson Hole conference, where it is possible that Powell and other senior officials could speak. We are likely to get the schedule of speeches this evening.

Looking at the day ahead, this morning the only data out in Europe is the July retail sales report in the UK. However it’s busy for data in the US this afternoon. We’ll get August manufacturing surveys from the NY and Philly Fed, while preliminary Q2 nonfarm productivity and unit labour costs data is due. Perhaps the most significant will be the July retail sales report however where the core and control groups readings are expected to show +0.4% mom and +0.5% mom, respectively. We’ll also get the latest jobless claims reading, July industrial and manufacturing production, August NAHB housing market index print and June business inventories. Central bank policy meetings are also due in Norway and Mexico, and in the evening, likely around 7:30pm, we should get the programme for the Fed’s Jackson Hole conference next week, which could see Powell speak.

3A/ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 6.88 POINTS OR 0.25% //Hang Sang CLOSED UP 193.18 POINTS OR 0.76% /The Nikkei closed DOWN 249.49 POINTS OR 1.21%//Australia’s all ordinaires CLOSED DOWN 2.80%

/Chinese yuan (ONSHORE) closed DOWN at 7.0399 /Oil UP TO 54.39 dollars per barrel for WTI and 58.30 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0399 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0555 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

This occurred prior to the Chinese comment that they hope that the USA will go half way in dealing with them.

Prior to that China rejects Trump’s tariff olive branch and they vow imminent retaliation against the Chinese. This still stands.

(zerohedge)