GOLD:$1513.20 DOWN $7.35(COMEX TO COMEX CLOSING

Silver: $17.15 DOWN 9 CENTS (COMEX TO COMEX CLOSING)/

Closing access prices:

Gold : $1512.50

silver: $17.12

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 13/28

EXCHANGE: COMEX

CONTRACT: AUGUST 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,519.600000000 USD

INTENT DATE: 08/15/2019 DELIVERY DATE: 08/19/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 6

661 C JP MORGAN 13

686 C INTL FCSTONE 4 1

737 C ADVANTAGE 10 3

800 C MAREX SPEC 14

880 H CITIGROUP 5

____________________________________________________________________________________________

TOTAL: 28 28

MONTH TO DATE: 5,229

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 28 NOTICE(S) FOR 2800 OZ (0.08709 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 5229 NOTICES FOR 522,900 OZ (16.2643 TONNES)

SILVER

FOR AUGUST

47 NOTICE(S) FILED TODAY FOR 235,000 OZ/

total number of notices filed so far this month: 1993 for 9,965,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

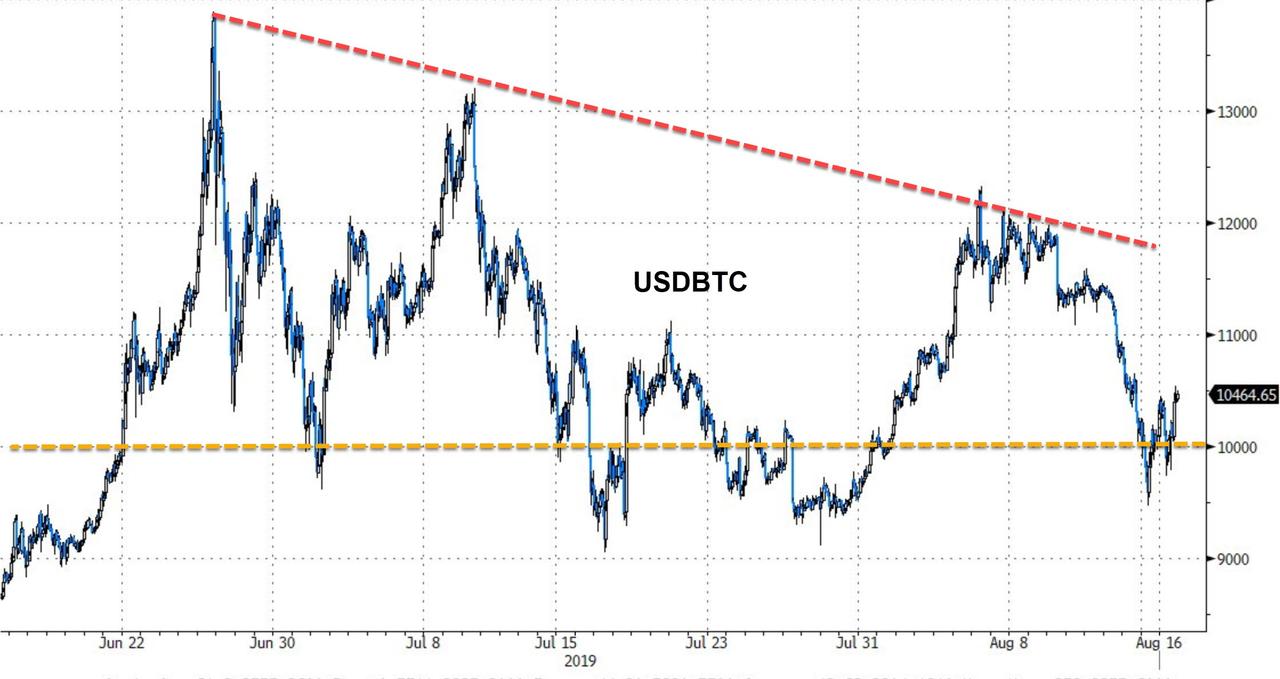

Bitcoin: OPENING MORNING TRADE : $ 10,070 down 226

Bitcoin: FINAL EVENING TRADE: $ 10400 UP 110

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A HUGE SIZED 4292 CONTRACTS FROM 233,095 DOWN TO 228,803… DESPITE THE TINY 2 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM THAT AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR AUGUST, 0 FOR SEPT 874, DEC, 200 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1074 CONTRACTS. WITH THE TRANSFER OF 1074 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1074 EFP CONTRACTS TRANSLATES INTO 5.37 MILLION OZ ACCOMPANYING:

1.THE 2 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

9.975 MILLION OZ INITIAL STANDING IN AUGUST.

WE HAD ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY WITH SOME SUCCESS..AND WE HAD NO APPRECIABLE SPREADING ACCUMULATION.

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

FOR NEWCOMERS, HERE IS THE MODUS OPERANDI OF THE CORRUPT BANKERS WITH RESPECT TO THEIR SPREAD/TRADING.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE VERY ACTIVE DELIVERY MONTH OF SEPTEMBER FOR SILVER.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST IS STARTING TO RISE IN THIS NON ACTIVE MONTH OF AUGUST BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF AUGUST:

23,404 CONTRACTS (FOR 12 TRADING DAYS TOTAL 23,404 CONTRACTS) OR 117.02 MILLION OZ: (AVERAGE PER DAY: 1950 CONTRACTS OR 9.7517 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 117.02 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 16.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1429.53 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3736, DESPITE THE TINY 2 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1074 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST AN ATMOSPHERIC SIZED: 3218 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1074 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 4292 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH JUST A 2 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $17.24 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!! THERE IS ONLY ONE ANSWER AS TO WHAT HAPPENED: MASSIVE BANKER SHORT COVERING..BANKERS HAVE CAPITULATED!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.146 BILLION OZ TO BE EXACT or 163% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 47 NOTICE(S) FOR 235,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 9.975 MILLION OZ

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 6979 CONTRACTS, TO 605,885 ACCOMPANYING THE $3.55 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY//THE SPREADING ACCUMULATION OPERATION HAS NOW COMMENCED ONLY FOR SILVER AND LITTLE WAS ACCOMPLISHED IN THAT ENDEAVOUR TODAY….. THE LIQUIDATION( AND ACCUMULATION) PHASE FOR COMEX OI GOLD HAS NOW STOPPED FOR THE AUGUST CONTRACT MONTH /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5939 CONTRACTS:

AUGUST 2019: 0 CONTRACTS, DEC> 5939 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 605885,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,918 CONTRACTS: 6979 CONTRACTS INCREASED AT THE COMEX AND 5939 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,918 CONTRACTS OR 1,291,800 OZ OR 40.41 TONNES. YESTERDAY WE HAD A GOOD GAIN OF $3.55 IN GOLD TRADING….AND WITH THAT GOOD GAIN IN PRICE, WE HAD A GIGANTIC GAIN IN GOLD TONNAGE OF 40.41 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TRYING TO CONTAIN THE PRICE RISE (HOWEVER IN SILVER, THE BANKERS WERE IN SHEAR FRIGHT AS THEY CONTINUED ON THEIR JOURNEY OF COVERING THEIR MASSIVE SILVER SHORTS)

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST : 138,195 CONTRACTS OR 13,819,500 oz OR 429.84 TONNES (12 TRADING DAY AND THUS AVERAGING: 11,516 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY IN TONNES: 429.84 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 429.84/3550 x 100% TONNES =12.10% OF GLOBAL ANNUAL PRODUCTION

(VOLUMES OF EFP’S ARE INCREASING IN GOLD)

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 3,940.53 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 6979 WITH THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($3.55)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5939 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5939 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 12,918 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5939 CONTRACTS MOVE TO LONDON AND 6979 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 40.14 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $3.55 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE HAVE NOW COMMENCED WITH SPREADING ACCUMULATION OF SILVER OI CONTRACTS IN THIS MONTH OF AUGUST BUT ZERO OCCURRED YESTERDAY.. ALL SPREADING ACTIVITY IN GOLD HAS STOPPED DURING THIS ACTIVE DELIVERY MONTH OF AUGUST.

we had: 28 notice(s) filed upon for 2800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN 7.35 TODAY//(COMEX-TO COMEX)

INVENTORY RESTS AT 844.29 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 9 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 380.154 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY AN ATMOSPHERIC AND CRIMINALLY SIZED 4292 CONTRACTS from 233,095 DOWN TO 228,803 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORDED HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET EXCEPT TODAY AS WE HAD A RISING PRICE..OUR SHORT DERIVATIVE BANKERS ARE NOW IN DEEP TROUBLE AS THEY ARE TERRIBLY OFFSIDE AND NEED ASSISTANCE FROM THE GOVERNMENT (FED) TO PROVIDE THE NECESSARY COLLATERAL TO CARRY THAT SHORT POSITION..THE SPREADERS HAVE COMMENCED THEIR ACCUMULATION OF OPEN INTEREST CONTRACTS IN SILVER FOR THE MONTH OF AUGUST, ALTHOUGH NEGLIGIBLE ACTIVITY YESTERDAY, AND THEY STOPPED ALL SPREADING ACTIVITY IN COMEX GOLD FOR THE MONTH OF AUGUST….

LADIES AND GENTLEMEN: I HAVE WAITED A LONG TIME TO SEE THIS: OUR BANKER FRIENDS HAVE NOW COMPLETELY CAPITULATED AND THEY ARE DESPERATELY TRYING TO COVER THEIR MASSIVE SILVER SHORTFALL..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR AUGUST: 0, FOR SEPT. 874 ; FOR DEC. 200 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1074 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 4292 CONTRACTS TO THE 1074 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED LOSS OF 3218 OPEN INTEREST CONTRACTS.THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 16.09 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ ;AUGUST AT 9.740 MILLION OZ//

RESULT: A GIGANTIC SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE TINY 2 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 1074 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 8.03 POINTS OR 0.28% //Hang Sang CLOSED UP 239.76 POINTS OR 0.84% /The Nikkei closed UP 13.16 POINTS OR 0.06%//Australia’s all ordinaires CLOSED DOWN .07%

/Chinese yuan (ONSHORE) closed UP at 7.0406 /Oil UP TO 55/40 dollars per barrel for WTI and 59.09 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0406 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0469 TRADE TALKS STALL//YUAN LEVELS PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

We have been highlighting Japan’s problems for years. They now have the 10 year Japanese 10 yr bond yield greatly exceeding their target to .11. To get the yield up they have decided to cut their purchase of 5 and 10 yr bonds

(zerohedge)

3C CHINA

4/EUROPEAN AFFAIRS

Germany

Germany is very worried about its economy. It may go slightly into a deficit by going into debt. In the broad stream of things, this is small stuff

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Argentina

Everything is collapsing in Argentina: investment funds, the Peso, Argentinian bonds..the whole enchalada

(zero hedge)

9. PHYSICAL MARKETS

a)The Martens are truly correct: these 5 big banks with all of their derivatives hold the fate of the entire global financial system in their hands

(Pam and Russ Martens/Wall Street on Parade)

b)A good interview between Egon Von Greyerz..and Max Keiser..two smart cookies

(courtesy Egon Von Greyerz)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

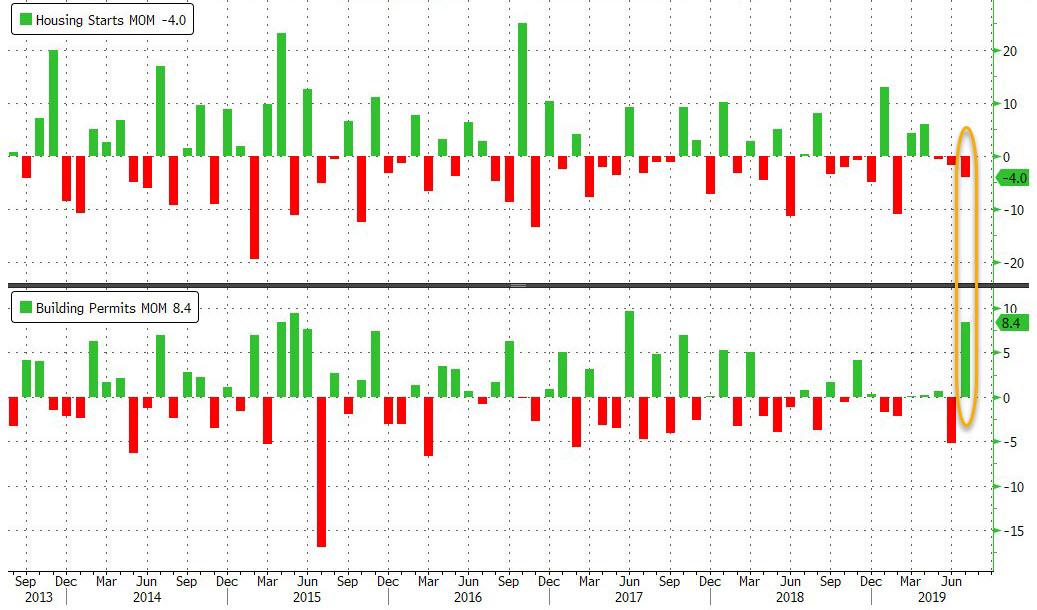

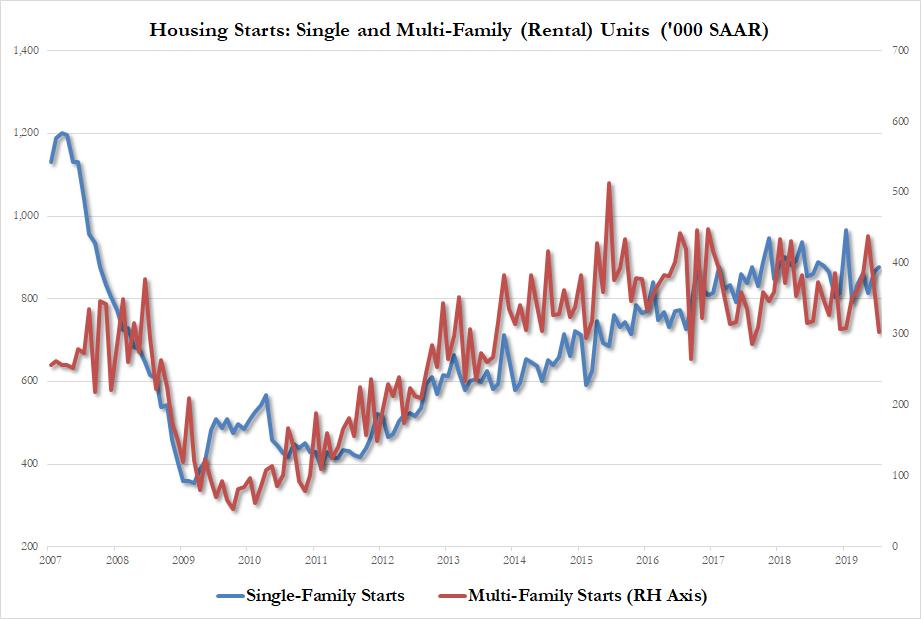

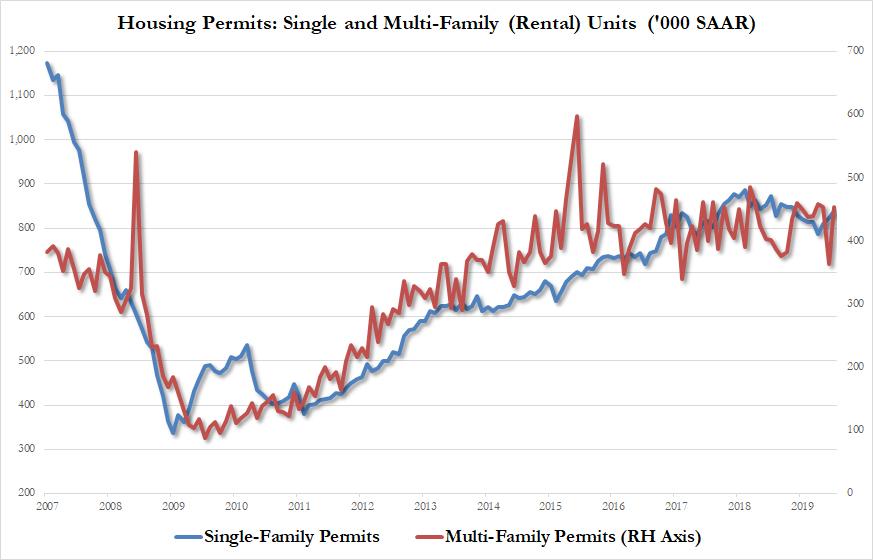

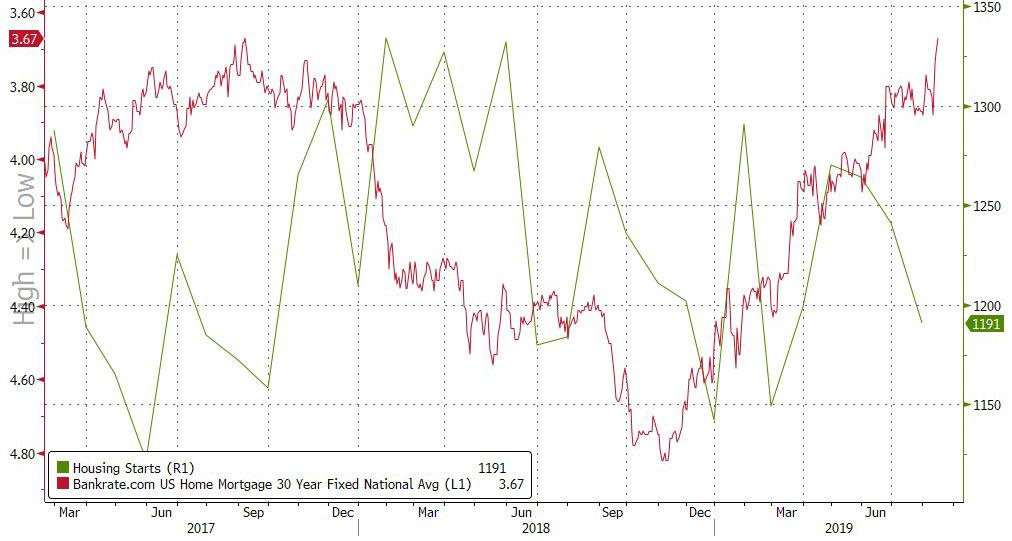

a)Despite low interest rates, housing starts continue to plunge. We are now witnessing a rental unit crash as well

(zerohedge)

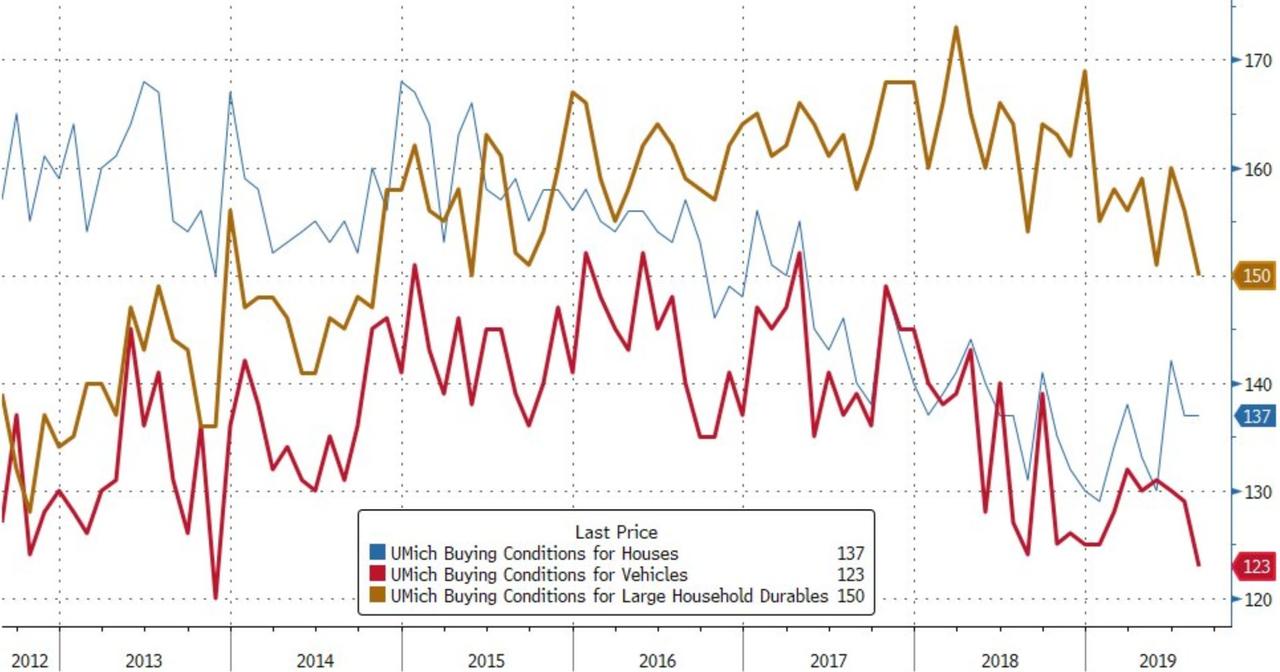

b)Consumer confidence crashes!!

iii) Important USA Economic Stories

(Michael Snyder)

b)Peter Schiff again warns on the “Great Recession:” which will jeopardize Trump’s re election efforts and put the entire globe in turmoil

(Mac Slavo.SHFTPlan.com.

c)My goodness!! this is very telling..Powell just issued a gag order against his Fed Presidents for speaking at any time re the economy. So much for transparency..must be very bad

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 3 kilobar entries

total gold withdrawals; 225.05 oz oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 44,482 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 112,718 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 112,718 CONTRACTS EQUATES to 564 million OZ 80.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -0.32% ((AUGUST 15/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.04% to NAV (AUGUST 15/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -/32%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 14.98 TRADING 14.49/DISCOUNT 3.24

END

And now the Gold inventory at the GLD/

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 29/WITH GOLD UP $1.00: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 6.75 TONNES INTO THE GLD INVENTORY///INVENTORY RISES TO 824.89 TONNES

JULY 26/WITH GOLD UP $4.50: A HUGE INVENTORY WITHDRAWAL OF 4.09 TONNES OF PAPER GOLD LEAVES THE GLD/INVENTORY RESTS AT 818.14 TONNES

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH GOLD DOWN $1.00: A MASSIVE DEPOSIT OF 11.44 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 814.62

JULY 18/WITH GOLD UP $5.55 TODAY: A BIG PAPER DEPOSIT OF 3.81 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 803.18 TONNES

JULY 17/WITH GOLD UP $11.35 TODAY: A BIG WITHDRAWAL OF 1.17 TONNES FROM THE GLD//INVENTORY RESTS AT 799.37 TONNES

JULY 16: WITH GOLD DOWN $2.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 15: WITH GOLD UP $1.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 12/WITH GOLD UP $5.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

JULY 11.WITH GOLD DOWN $5.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.54 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 16/2019/ Inventory rests tonight at 844.29 tonnes

*IN LAST 644 TRADING DAYS: 91.11 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 544- TRADING DAYS: A NET 75.43 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 29/2019: WITH SILVER UP 4 CENTS TODAY: A SMALL WITHDRAWAL OF 468000 OZ FROM THE SLV/INVENTORY LOWERS TO 356.715 MILLION OZ//

JULY 26.2019: WITH SILVER DOWN 2 CENTS TODAY: A HUGE 1.03 MILLION OZ OF PAPER SILVER LEAVES THE SLV/INVENTORY LOWERS TO 357.183 MILLION OZ//

JULY 25.2019: WITH SILVER DOWN 19 CENTS: ANOTHER PAPER WITHDRAWAL OF 1.17 MILLION OZ/INVENTORY REST AT 358.213 MILLION OZ

JULY 24…A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A GAIN OF 1.685 MILLION OZ/INVENTORY RESTS AT 359.383 MILLION OZ

JULY 23/2019: WITH SILVER UP 5 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.221 MILLION PAPER OZ ADDED INTO THE GLD INVENTORY//INVENTORY RESTS AT 357.698 MILLION OZ////

JULY 22.2019/WITH SILVER UP 21 CENTS TODAY: A MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 8.939 MILLION OZ ADDED TO THE SLV INVENTORY/INVENTORY RESTS AT 355.919 MILLION OZ//

JULY 19/WITH SILVER FLAT TODAY: ANOTHER MONSTROUS PAPER DEPOSIT OF 3.276 MILLION OZ ENTERS THE SLV//WHAT A MASSIVE FRAUD//INVENTORY RESTS AT 346.980 MILLION OZ

JULY 18/WITH SILVER UP 24 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.668 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 343.704 MILLION OZ//

JULY 17: WITH SILVER UP ANOTHER 29 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 8.518 MILLION OZ/INTO THE SLV INVENTORY///INVENTORY RESTS AT 341.036 MILLION OZ//

JULY 16: WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY: 15 WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 332.518 MILLION OZ

JULY 12/WITH SILVER UP 10 CENTS: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 332.518 MILLION OZ//

JULY 11/NO CHANGE IN SILVER INVENTORY

AUGUST 16/2019:

Inventory 380.154 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.04/ and libor 6 month duration 2.01

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .03

XXXXXXXX

12 Month MM GOFO

+ 1.88%

LIBOR FOR 12 MONTH DURATION:1.93

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.05

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Deutsche Falls To New Record Low Showing ‘Lehman Shock’ Contagion Risk

* Deutsche bank’s new record low at €5.80 underscores German and European banking contagion risk

* FTSE 100 opens slightly higher after trading delay of 90 minutes on trading trading services ‘issue’

* GE falls the most in 11 years after Madoff whistleblower calls it a ‘bigger fraud than Enron’

* Gold prices are marginally lower today but are currently set for another higher weekly close as safe-haven buying continues

* The wider economic, monetary and geopolitical backdrop will support safe haven assets and investors without an allocation to the precious metal should cost average into physical gold

News and Commentary

Gold heads for 3rd weekly gain on trade, growth concerns

Gold to Rise to $1,650 by 2Q 2020: UOB Private Bank

Deutsche Bank’s New Record Low Underscores European Banking’s Decline

German banks are in a much worse position than the rest of Europe – Citi

FTSE 100 opens after trading delay of 90 minutes on trading trading services ‘issue’

GE falls the most in 11 years after Madoff whistleblower calls it a ‘bigger fraud than Enron’

10-year Treasury yield falls to three-year low below 1.5%, 30-year rate declines to record low

Market plunge sheds harsh light on big banks and their derivatives counterparties

Nomura: Yesterday Was A Complete Rout, Raising Odds Of September “Lehman Shock”

“The End Of The World As We Know It” – China Going Nuclear Means There’s No Turning Back Now

Gold has been acting as a safe-haven – Ira Epstein

Listen and Watch Jim Rogers Interview Here

Gold Prices via LBMA (AM/ PM Fix – USD, GBP & EUR)

14-Aug-19 1500.35 1513.25, 1241.69 1253.73 & 1341.61 1356.17

13-Aug-19 1527.20 1498.40, 1265.90 1240.38 & 1363.48 1338.67

12-Aug-19 1501.95 1504.70, 1244.82 1243.63 & 1343.64 1341.74

09-Aug-19 1503.50 1497.70, 1242.19 1240.99 & 1342.02 1338.05

08-Aug-19 1497.40 1495.75, 1230.26 1234.14 & 1335.08 1335.70

07-Aug-19 1487.65 1506.05, 1225.82 1239.33 & 1330.11 1341.44

06-Aug-19 1461.85 1465.25, 1199.59 1201.21 & 1304.85 1311.11

05-Aug-19 1457.45 1465.25, 1199.92 1203.85 & 1307.92 1310.23

02-Aug-19 1436.05 1441.75, 1184.17 1187.28 & 1294.02 1298.44

01-Aug-19 1406.40 1406.80, 1161.12 1161.74 & 1273.35 1273.29

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

The Martens are truly correct: these 5 big banks with all of their derivatives hold the fate of the entire global financial system in their hands

(Pam and Russ Martens/Wall Street on Parade)

iii) Other physical stories:

A good interview between Egon Von Greyerz..and Max Keiser..two smart cookies

(courtesy Egon Von Greyerz)

EGON VON GREYERZ ON THE KEISER REPORT – “CENTRAL BANKS IN PANIC MODE”

August 16, 2019 by Egon von Greyerz

In this interview Max and Egon discuss the enormous pressures in the financial system and the coming stampede into gold. Also:

- The final phase of the currency race to zero has just started

- Massive energy in gold, built up over the last 6 years

- Gold will break its all time high of $ 1920, without effort

- Gold hit new all-time highs in many currencies. Now on its way to at least $10,000 or even $50,000

- Central banks panicking over global banking system

- Negative rates – Government bonds, world’s most risky investment

- At some point, investors will dump overvalued bonds, resulting in hyperinflation and implosion of bond market

- Dow Jones stock index, will face a vicious fall very soon and in years to come

THE INTERVIEW STARTS AT 12 MINS 40 SECONDS:

Egon von Greyerz

Founder and Managing Partner

Matterhorn Asset Management

Zurich, Switzerland

Phone: +41 44 213 62 45

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

US Futures Surge, Global Markets Rise Amid Lull In Bad News

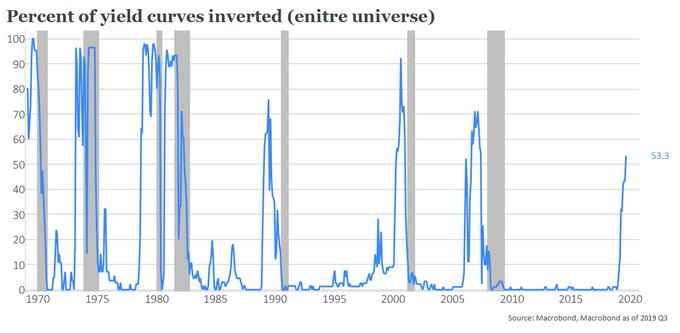

In a quiet end to an extremely tumultuous week (pending one or more shocking Trump tweets) there were no overnight trade war tape bombs from China, no additional curve inversions even as more than half of the world’s yield curves are now inverted…

Jeffrey Kleintop

✔@JeffreyKleintop

Percentage of yield curves inverted around the world now over 50%

… and so US equity futures surged and European stocks and most Asian shares posted modest gains on Friday, while Treasuries pared some of their recent blistering advance, taking advantage of the rare moment of quiet, as expectations grew of further stimulus by central banks, offsetting worries about slowing economic growth which intensified this week as the the US 2s10s yield curve inverted for the first time since 2007.

S&P 500 futures pushed above prior day’s highs amid renewed trade optimism after U.S. President Donald Trump said a call is planned very soon with Chinese leader Xi Jinping.

MSCI’s All Country World Index was up 0.2% on the day, although it was set for its third straight losing week, down 2.2%.

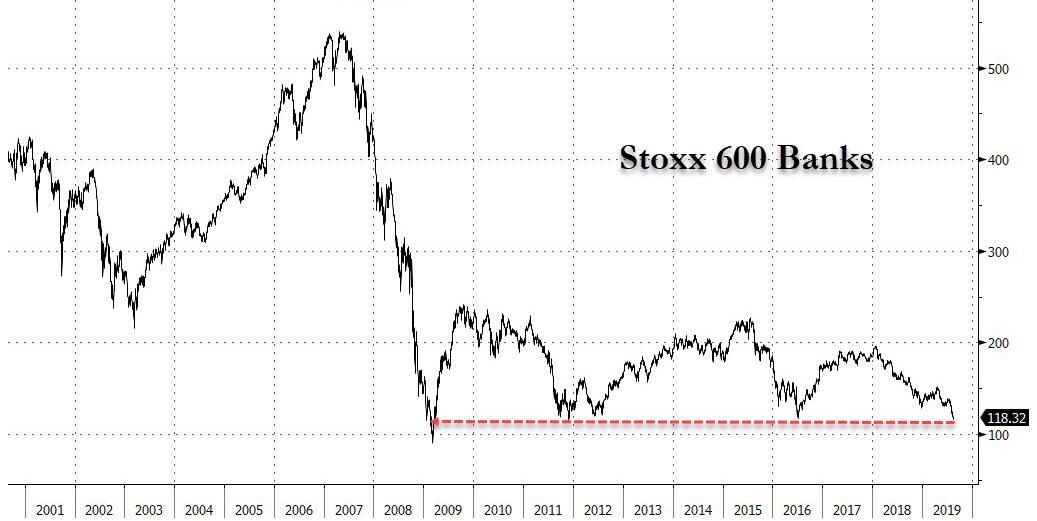

European shares rebounded from six-month lows, with the European Stoxx 600 index over 1% higher, drifting in low-volume trade in a morning devoid of fresh news flow or data. The Stoxx 600 Banks Index was one of Europe’s best-performing sectors today, gaining 1.1%, in contrast with other cyclical industries like autos and chemicals that lagged behind the broader market. Commerzbank was the biggest gainer in the index as the negative yield sentiment took a step back. The catalyst: the 10y Bund yield was slightly up Friday by 1bps as the benchmark’s bond is heading for the fifth weak of falling yields; somehow this was enough to launch a relief rally in Europe’s banks which have tumbled to near record low levels. Italian banks also among the top performers after the country’s market was closed for a holiday Thursday. The banks were also catching up on comments from ECB’s Olli Rehn about a potential “impactful and significant” stimulus package.

A technical glitch delayed the start of trading of the UK’s benchmark FTSE 100 and midcap stock indexes for almost two hours. It was the longest outage at one of the world’s top stock markets in eight years.

Earlier in the session, Asian shares were mostly higher, with Chinese stocks climbing and Korean shares dipping.

Treasuries drifted lower over Asia session and into early European session, paring some Thursday’s rally. Yields were up 0.5bp to 3.2bp across the curve in a bear steepening move with 2s10s wider by ~1bp and 5s30s by ~2bp; 10-year yields ~1.54% are cheaper by 1.5bp but remain towards richer end of 1.473% to 1.733% weekly range. In Europe, Bunds outperformed Treasuries, while gilts underperformed as money markets trim pricing on Bank of England easing; Chancellor Sajid Javid holds Brexit talks in Berlin later Friday.

To be sure, the bulk of the action this week was in the bond market, where with no trade war settlement in sight, investors hedged against a global slowdown by buying bonds. Yields on 30-year debt dropped to a record low 1.916% on Thursday, leaving them down 27 basis points for the week, the sharpest decline since mid-2012.

That means investors are willing to lend the government money for three decades for less than either the overnight rate or Libor. Which also means that all those who pegged their ARM mortgages to the 30Y instead of Libor are now winning.

Some analysts say the current bond market is a different beast than past markets and might not be sending a true recession signal: “The bond market may have got it wrong this time, but we would not dismiss the latest recession signals on grounds of distortions,” said Simon MacAdam, global economist at Capital Economics. “Rather, it is of some comfort for the world economy that unlike all previous U.S. yield curve inversions, the Fed has already begun loosening monetary policy this time.”

And so with the bond market screaming a recession is coming, the futures market is bracing for action from the Fed and the Fed Funds market now sees a one in three chance the Federal Reserve will cut rates by 50 basis points at its September meeting, and see rates reaching just 1% by the end of next year.

On Thursday, the ECB’s Olli Rehn flagged the need for even stronger easing in September. Markets currently anticipate a cut in the ECB’s deposit rate of at least 10 basis points and a resumption of bond buying, sending German 10-year bund yields to a record low of ‑0.71%.

“The underlying concern and drivers such as a recession and the expectation for an aggressive policy response, fueled by Rehn’s comments yesterday, has given the bond market another boost at already elevated levels,” said Commerzbank rates strategist Rainer Guntermann.

Meanwhile, Mexico overnight joined the global easing tide and became the latest country to surprise with a rate cut, the first in five years. Canada – whose yield curve inverted by the most in nearly two decades – is likely next to cut.

In other overnight news, President Trump said Fed Chair Powell should be cutting rates because other countries are lowering rates and we want to remain even. Meanwhile, Fed’s Kashkari (Non-Voter, Dove) said the Fed will debate what to do on rates and that he is leaning towards further rate reduction, while he added that Fed officials are committed to ignoring politics and focusing on jobs. Kashkari also noted that he sees some cautious signs as well as some signs of optimism and that it is definitely a nervous time.

Additionally, Trump said he doesn’t think China will retaliate to an increase in tariffs and understands the September meeting between negotiators is still on, while he added that he has a call scheduled with Chinese President Xi and will be speaking to him soon. Trump also stated that US consumers may have to pay something at some point to cover the cost of tariffs on Chinese goods, that China very much wants to make a deal and he thinks the trade war will be fairly short.

In FX, the talk of ECB easing knocked the euro lower for a fourth day back to a two-week low of $1.1075 and away from a top of $1.1230 early in the week. It was last down 0.3% at $1.1078, helping lift the dollar index to 98.283 and off the week’s low of 97.033. Australia’s dollar rose for a second day as U.S. President Donald Trump said he had a phone call coming soon with China’s Xi Jinping, boosting optimism trade tensions between the two nations will ease. The pound headed for its first weekly gain against the euro for three months, as opposition lawmakers sought to find a way to stop a no-deal Brexit, while Chancellor of the Exchequer Sajid Javid will become the first senior member of Boris Johnson’s government to hold Brexit talks with EU leaders when he flies to Berlin today to speak to German finance minister Olaf Scholz.

In commodities, gold fell 0.7% to $1,512.7, just off a six-year peak. Oil prices surged. Brent crude futures added 2% to $59.48 a barrel, while U.S. crude rose 2% to $55.60 a barrel.

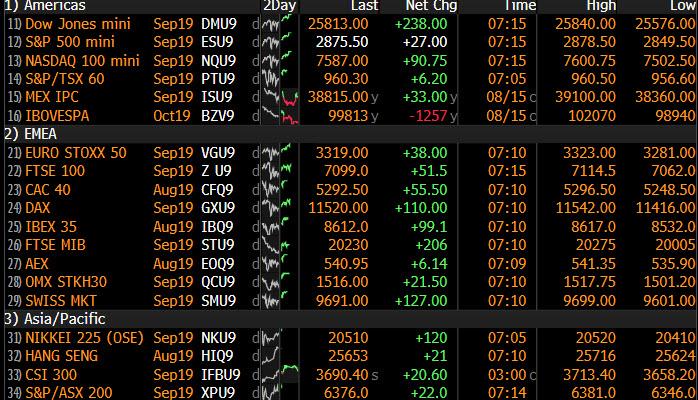

Market Snapshot

- S&P 500 futures up 0.9% to 2,872.75

- STOXX Europe 600 up 0.8% to 367.96

- MXAP up 0.3% to 150.51

- MXAPJ up 0.4% to 486.38

- Nikkei up 0.06% to 20,418.81

- Topix up 0.1% to 1,485.29

- Hang Seng Index up 0.9% to 25,734.22

- Shanghai Composite up 0.3% to 2,823.82

- Sensex up 0.3% to 37,409.18

- Australia S&P/ASX 200 down 0.04% to 6,405.53

- Kospi down 0.6% to 1,927.17

- German 10Y yield rose 0.6 bps to -0.707%

- Euro down 0.2% to $1.1086

- Italian 10Y yield fell 17.1 bps to 0.985%

- Spanish 10Y yield unchanged at 0.034%

- Brent futures up 1.5% to $59.09/bbl

- Gold spot down 0.7% to $1,512.71

- U.S. Dollar Index up 0.1% to 98.26

Top Overnight News

- The European Central Bank is throwing every tool it has at the sluggish euro-zone economy. Starting in September, it’ll make a generous funding offer to lenders in the region, returning to an approach it’s used twice before in the past five years. It’s also considering tweaking its interest-rate policy to limit the punitive side effect of its stimulus.

- Japanese investors bought a record amount of U.S. agency bonds in June, data from Department of Treasury showed Thursday. Purchases worth $14.3b were the highest in data going back to 1977

- Labour Party leader Jeremy Corbyn’s appeal to other U.K. parties that he should become a caretaker prime minister to stop a no- deal Brexit looks to have already fallen flat, as even some in his own party apparently accepted an alternative plan was needed

- Japan’s 10-year bond yield slipped to its lowest since July 2016, intensifying scrutiny over the central bank’s yield- curve control policy amid a global debt rally. New Zealand’s benchmark rate also fell to a new record low

- The U.S. is gravely disappointed with the U.K. after a Gibraltar court allowed the release of an Iranian tanker suspected of hauling oil to Syria, and threatened sanctions against ports, banks and anyone else who does business with the ship or its crew, two administration officials said

- “I’m leaning towards the camp of yes, we need to give more stimulus to the economy, more support, we need to continue the expansion and not allow a recession to hit us,” Minneapolis Fed President Neel Kashkari told Minnesota Public Radio

- North Korea fired two unidentified projectiles on Friday into waters off its east coast between the Korean Peninsula and Japan, South Korea’s defense ministry said

Asian equity markets struggled for firm direction following the mixed lead from Wall St where most major indices eventually composed themselves after the recent sell-off but with price action tumultuous on continued US-China trade uncertainty. ASX 200 (Unch.) was subdued as upside in healthcare and financials counterbalanced weakness in commodities and telecoms, with a heavy slate of earnings adding to the mix. Nikkei 225 (Unch.) was restricted by an uneventful currency, while KOSPI (-0.6%) underperformed as it caught up to the recent rout on return from holiday and amid a deterioration in inter-Korean relations after North Korea fired 2 more projectiles and stated it has no intention to talk with South Korea again. Hang Seng (+0.9%) and Shanghai Comp. (+0.3%) were initially choppy amid conflicting rhetoric from both sides of the trade spat. In addition, policymakers later contributed to the outperformance in the mainland after the PBoC’s continued liquidity efforts resulted to a net weekly injection of CNY 300bln and with the NDRC announcing to roll out a plan to boost disposable incomes. Finally, 10yr JGBs initially edged higher to test the 155.00 level to the upside as 10yr yields fell to -0.25% which was the lowest since 2016, although prices then reversed in the aftermath of the BoJ’s Rinban operation in which it reduced purchases of 5yr-10yr bonds for the first time since December as speculated, to stem the decline in yields.

Top Asian News

- BOJ Steps in With Cut to Bond Purchases as Yields Keep Sliding

- Thailand Plans $10 Billion Economic Boost to Hit 3% Growth

- Modi’s Kashmir Move Faces UN Test After Top Court Skips Pleas

European equities are higher across the board [Eurostoxx 50 +1.1%] following on from a mixed Asia-Pac session, with Europe continuing to feel tailwind from ECB’s Rehn, who yesterday hinted to a preference for a bazooka of Central Bank stimulus (in the form of rate cuts and APP) whilst stating its better to overshoot with stimulus than undershoot. UK’s FTSE 100 (+0.4%) fails to benefit from the prospect of EU stimulus and also encountered technical problems which delayed the bourse’s open by just over 90 minutes. Sectors are all in positive territory, whilst some early outperformance was seen in the IT sectors in light of NVIDIA’s (+5.3% pre-market) earnings which beat on both top and bottom lines and supported the likes of fellow chip names [AMS (+3.2%), Infineon (+2.2% and STMicroelectronics (+1.2%)]. Meanwhile, the EU banks saw a sudden sharp decline, although the current yield environment is not attractive, some are citing a technical break below 80 in the Euro Stoxx Bank Index (SX7E). In terms of individual movers, Bayer (+2.3%) rose on the back of an upgrade at BAML, whilst Ryanair (-2.6%) shares were impacted by a double downgrade.

Top European News

- In Brave New World, U.K. Markets Don’t See Any BOE Hike, Forever

In FX, Sterling looks set to end the week on top of the G10 table after a run of firmer or better than expected UK data (average earnings, CPI and retail sales) and latest moves to block a no deal Brexit. Cable has reclaimed 1.2100+ status and inched above yesterday’s high (1.2150) even though the Dollar is also generally bid after Thursday’s strong US data/survey releases, while Eur/Gbp has reversed sharply from ytd highs of 0.9325 through Fib support at 0.9160 and 0.9150 amidst all round Euro weakness on the back of dovish ECB rhetoric and perhaps with some fix flow in the mix as well, as the cross probes 0.9125.

- EUR – As noted, the single currency remains under pressure following yesterday’s aggressive policy pronouncements from ECB’s Rehn who is advocating conventional easing and substantial bond buying to be unveiled in September on the premise that too much is better than not enough in terms of stimulus. Hence, Eur/Usd is hovering just above the next sub-1.1100 target area or bidding zone between 1.1080-70 and at this stage expiry option interest at the big figure does not seem likely to factor (especially as there is less than 1 bn rolling off).

- DXY – The index is inching closer to nearest chart resistance above 98.000 in wake of the aforementioned bullish US macro updates, at 98.301 vs 98.371, with the Greenback also gleaning momentum at the expense of other majors in contrast to EM currencies that are clawing back losses amidst an improved risk environment overall.

- JPY/CHF/NZD – All on the back foot, with the Yen unable to breach 106.00 vs the Buck or threaten decent expiries below (1.1 bn from 105.80-70) and subsequently slipping to circa 106.50 as supply at 106.30 dried up, but holding in ahead of support via a Fib at 106.68 for now. Safe-haven unwinding is also weighing on the Franc that is hovering around 0.9800 and even lagging against the independently weak Euro, albeit still above 1.0900 and pivoting 1.0850. Elsewhere, the Kiwi has not derived any comfort from the upturn in risk sentiment after more deep RNBZ rate cut calls overnight (UBS looking for the OCR to hit 0.5% by February next yesr) and a sub-50 NZ manufacturing PMI, with Nzd/Usd closer to the base of 0.6450-25 parameters.

- CAD/NOK – A decent rebound in crude prices has helped the Loonie pare some losses relative to its US counterpart within a 1.3325-1.3290 band, while 1.2 bn expiries at 1.3340 are also providing support ahead of 1.3350, and Eur/Nok has reversed from 10.0320 towards 9.9600 with the aid of oil’s recovery and ECB/Norges Bank policy divergence after the latter kept a 25 bp hike on the agenda for this year, albeit not necessarily next month as previously inferred.

- EM – Regional currencies have extended their recoveries vs the Dollar as noted earlier, and irrespective of factors that would appear bearish or negative, like an unexpected 25 bp ease from Banxico and much weaker than forecast Turkish IP. However, Usd/Mxn and Usd/Try are both mid-range circa 19.5750 and 5.5500 respectively with the Peso and Lira getting traction from the wider pick-up in risk appetite.

In commodities, a positive session thus far for WTI and Brent futures as the benchmarks recover from yesterday’s losses with upside supported by constructive trade comments from US President Trump, who stated that a call is scheduled with his Chinese counterpart and the September meeting between the negotiators is still on. WTI reclaimed the 55/bbl handle during Asia-Pac hours whilst Brent prices moved north of 59/bbl in early EU trade; and both remain north of these marks. Looking ahead on the docket, OPEC are due to release its delayed Monthly Oil Market report with focus on any revisions to its global oil demand outlook following 2019 downgrades by both the EIA and IEA (to 1.1mln BPD and 1.0mln BPD respectively). Currently OPEC estimates that oil demand will grow by 1.4mln BPD in both 2019 and 2020. On a weekly basis, both benchmarks are poised to post mild gains, albeit this is very much subject to macro-newsflow heading into the final settlement of the week. Elsewhere, gold prices are retreating closer to the 1500/oz level as the Dollar index continues to gain ground above 98.000, whilst profit taking and an unwind in haven positions are contributing to the downside. Meanwhile, copper prices are little changed intraday and remain below the 2.60/lb level as a rise in Chinese refined copper output counterbalances some of the optimism from Trump’s latest China comments. Finally, Dalian iron ore futures are relatively flat as demand woes were neutralised by supply concerns after Brazil’s Vale halted operations at its Viga concentration plant, thus impacting some 330k tonnes of iron ore per month.

US Event Calendar

- 8:30am: Housing Starts, est. 1.26m, prior 1.25m; Housing Starts MoM, est. 0.24%, prior -0.9%

- 8:30am: Building Permits, est. 1.27m, prior 1.22m; Building Permits MoM, est. 3.08%, prior -6.1%

- 10am: U. of Mich. Sentiment, est. 97, prior 98.4; Current Conditions, prior 110.7; Expectations, prior 90.5

DB’s Craig Nicol concludes the overnight wrap

After running to stand still recently, yesterday felt almost like a rare day of calm for risk assets although we still had the usual intraday swings to deal with. Indeed, it wasn’t like there wasn’t much newsflow to digest. We had more trade headlines, strong US data, and ECB stimulus talk. By the end of play, the S&P 500 limped to a +0.25% gain while the DOW and NASDAQ ended +0.39% and -0.09%, respectively. Volumes were still above average and the VIX remained elevated around 21.18; however, it did feel a bit calmer certainly relative to recent days. That being said, Treasuries continued to rally with 2y, 10y and 30y yields ending -7.8bps, -5.1bps and -4.5bps lower, respectively. They did actually weaken a bit into the close as prior to that we saw 10y yields fall below 1.50% intraday. The moves also meant that the 2s10s slope ended slightly steeper at +2.3bps. So we’re still waiting for the first official negative print on a closing basis in this cycle. Cash HY credit spreads finished +3bps and +4bps wider in the US and Europe, respectively. US IG spreads also widened slightly, though they were impacted by the sharp move in GE’s benchmark 2035 bonds, which widened +45bps after reports circulated, accusing the company of “accounting fraud.” The company’s shares fell -11.30% for their worst day since April 2008.

Just on the trade headlines, they focused on China’s state council tariff committee saying that China “has no choice but to take necessary measures to retaliate” and that the US had violated the Xi-Trump consensus with the latest tariff announcement. The statement didn’t suggest what the countermeasures might be; however, Zhou Xiaoming – a former Ministry of Commerce official – suggested that the retaliation may not be limited to tariffs. President Trump also said that an agreement with China has to be on “our terms” while he also indicated that he has a call with Xi “very soon” and that “they would like to do something”.

Overnight most Asian markets are trading higher, with the Nikkei (+0.09%), Shanghai Comp (+0.69%) and the Hang Seng (+0.74%) all advancing. However, the Kospi (-0.70%), which is trading again after yesterday’s Liberation Day bank holiday, has fallen back as news has come through overnight from South Korea that North Korea fired two projectiles, the latest in a series of tests that North Korea has launched in recent weeks. Meanwhile in Japan, 10y JGB yields fell to -0.257% in trading earlier for the first time since 2016, although at time of writing have risen to -0.241%. We’ve also heard overnight that the BoJ reduced their purchases of 5- to 10-year bonds by 30bn yen, the first reduction in their purchases of that maturity since December.

Sticking with Asia, we also heard yesterday that Hong Kong revised down their growth forecasts for this year, down to 0-1%, having been 2-3% previously, while also announcing stimulus measures. This morning, we’ll get Hong Kong’s final Q2 GDP print, which follows the advance estimate last month that showed GDP contracting by -0.3% qoq in Q2, with a yoy growth rate of +0.6%. Looking ahead, S&P 500 futures are currently up +0.58%.

In terms of that US data yesterday that we mentioned at the top, front and centre was the July retail sales report, which was undoubtedly strong with above-market prints for the core (+0.9% mom vs. +0.5% expected) and control group (+1.0% mom vs. +0.4% expected) components. There was a small downward revision to the prior month; however, this was still the fifth straight monthly increase in retail sales, which underscores the solidity of consumer activity at the moment. In addition to that, both the August empire manufacturing (4.8 vs. 2.0 expected) and Philly Fed (16.8 vs. 9.5 expected) surveys surprised to the upside while jobless claims ticked up slightly to 220k but still remain historically low.

The flip side for risk was the upward revision to unit labor costs to +2.4% qoq, which points to some modest upside risk to core CPI over the next year. The other slightly negative print was misses for July industrial production (-0.2% mom vs +0.1% expected), and manufacturing production (-0.4% mom vs. -0.3% expected) albeit slightly offset by upward revisions to the prior. All in all, the general takeaway from the slew of data was that this might make it harder for the Fed to surprise with a more aggressive cut next month (50bps as opposed to 25bps) given the solid consumer data, resilient business sentiment especially in the face of the trade war escalation, and a firming of pricing pressure in the labour market. It’s worth noting that GDP trackers ticked higher yesterday, with the Atlanta Fed estimate now at 2.2% for the third quarter, up +0.3pp from its previous level.

Meanwhile, the ECB stimulus talk concerned comments from policymaker Rehn who said that ECB easing should include an “significant and impactful” stimulus package at its September meeting, in an interview with the WSJ. He went on to say that “when you’re working with financial markets, it’s often better to overshoot than undershoot.” That left the market pricing higher odds of a big QE announcement for the September ECB meeting. Bonds rallied across the continent, with 10y yields in Germany, France, and Italy dropping -6.2bps, -6.6bps, and -17.6bps. The euro weakened as much as -0.42% in response and ultimately closed -0.29% lower versus the dollar, though the pass-through to equities was not overly strong, as the STOXX 600 still closed -0.29% lower.

Across the pond, Fedspeak didn’t really move markets, though we did get confirmation that Chair Powell will speak at 3pm London time next Friday to kick off the Jackson Hole conference. The text of his speech will likely be released at the same time. There were also unsubstantiated reports that Powell is cracking down on Fed staff communicating with market participants and/or the media, though it’s hard to believe that they would change their communications policy without publicizing it. Separately, St. Louis Fed President Bullard spoke and sounded, at the margin, dovish. He said that the market’s inflation expectations were “not high enough to meet our target so that is something I will definitely take into account if it is sustained going forward”. Minneapolis Fed President Kashkari also said yesterday that “I’m leaning towards the camp of yes, we need to give more stimulus to the economy”.

In other news, the only other data worth flagging yesterday was in the UK where the July retail sales data was by and large surprisingly positive, with the core measure rising +0.2% mom versus expectations for a -0.2% mom decline. That took the year-on-year reading to +2.9% versus the expected +2.3%. As for other central banks, the global march toward more accommodation continued as the Norges Bank gave a surprisingly dovish statement, sending the krone -0.39% weaker versus the dollar. Mexico’s central bank also surprisingly cut interest rates by 25bps.

Finally to the day ahead, which is quiet for data this morning with only the June trade balance for the Euro Area due. Over in the US this afternoon, we’ll get July housing starts and building permits data before the preliminary University of Michigan consumer sentiment survey is released. It’s worth keeping an eye on the household inflation expectations component of this survey, which remains low despite a pickup last month and has been flagged as a concern by Fed officials. The only other release worth flagging is OPEC’s monthly oil market report.

3A/ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 8.03 POINTS OR 0.28% //Hang Sang CLOSED UP 239.76 POINTS OR 0.84% /The Nikkei closed UP 13.16 POINTS OR 0.06%//Australia’s all ordinaires CLOSED DOWN .07%

/Chinese yuan (ONSHORE) closed UP at 7.0406 /Oil UP TO 55/40 dollars per barrel for WTI and 59.09 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0406 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0469 TRADE TALKS STALL//YUAN LEVELS PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

We have been highlighting Japan’s problems for years. They now have the 10 year Japanese 10 yr bond yield greatly exceeding their target to .11. To get the yield up they have decided to cut their purchase of 5 and 10 yr bonds

(zerohedge)

BOJ Cuts Purchases Of 5-10 Year Bonds For The First Time Since December

One of the more jarring, if underreported shifts in the world of central bank finance over the past three years, was the dramatic decline in the BOJ’s annual purchases of JGBs, which has shrank drastically from its 2015 peak, and was back to levels first seen just after the start of Japan’s QQE.

And yet despite this obvious tapering in the BOJ’s QE, the yield on 10Y JGBs has not increased; on the contrary, courtesy of the paralyzed Japanese bond market, where barely anyone is left to trade with the BOJ now owning more than half of all government bonds, price formation has been made virtually impossible, and furthermore, as a result of the recent sharp drop in global yields, the benchmark 10Y JGB has seen its yield slide from 0% at the start of the year to -0.15% in recent months, and most recently take a sharp move lower as it plunged to the lowest on record at -0.25% as of today.

This plunge in JGB yields to a level below the JGB’s lower bound on its Yield Curve Control corridor which extends to -0.20%, prompted some to comically expect the BOJ to start selling bonds…

zerohedge@zerohedgeJAPAN 10-YEAR LEAD BOND FUTURES RISE TO RECORD HIGH OF 154.97

Is BOJ going to sell some to keep rate in corridor

… while other, more serious, traders expected the BOJ to announce a sharp cut in the amount of JGB bonds in the 5-10 year bucket it would repurchase at today’s rinban, or POMO, operation.

As Mitsubishi UFJ’s Katsutoshi Inadome noted, today marks the first buying operation in the 5-10 year zone since Japan’s benchmark 10-year yield fell below the bottom of the BOJ’s targeted range on Aug. 6, and with the yield since falling further and touching minus 0.25% on Thursday, if the BOJ didn’t announce or do anything when yields are looking set to decline further, it would be an issue – and a message – from the point of maintaining the yield curve control, namely that the BOJ no longer cares if yields go straight down.

The alternative was simple: reduce the amount of bonds the BOJ buys back, with some speculating that the BOJ could reduce purchases of 5-10 year zone by as much as 50BN yen – which would be the largest cut in this zone since the introduction of the yield curve control policy in September 2016 – while sending a very strong signal to the market against falling yields.

In the end the BOJ picked a middle option: it did indeed cut the amount of bonds in the 5-10 year bucket it would purchase, but the amount was less than the most aggressive expectations, dropping by 30BN yen, from 480BN yen to 450BN. This was the first cut in the core maturity zone since December 14.

However, while the Bank of Japan did as widely expected in response to the aggressive bull-flattening in JGBs, this move will hardly end the rally as the market tests Kuroda’s tolerance for yields underneath the target range, according to Bloomberg’s Tommi Utoslahti, who also writes that “today’s decision to trim 5-to-10 year bond purchases by 30b yen suggests BOJ’s yield-curve control settings remain unchanged — whereas leaving the operation sizes unchanged could have been seen as a de facto widening of the targeted range.”

Indeed, despite the shrinkage in stated BOJ purchases – amid what has already been a secular decline in BOJ bond purchases despite the ongoing QE – the market barely reacted, and the USDJPY is unchanged, while JGB futures remain close to 155.02 record high, and as Bloomberg notes, “will likely extend gains unless the BOJ provides more detailed insight into its thinking.”

Meanwhile, JGB bulls will have little incentive to not test the BOJ or cede control in their push to revisit the all time record low 10Y yield of -0.30%.

3 C CHINA

4/EUROPEAN AFFAIRS

Germany

Germany is very worried about its economy. It may go slightly into a deficit by going into debt. In the broad stream of things, this is small stuff

(zerohedge)

Stocks, Bund Yields Spike On Another Spiegel Report Germany Ready To Run Budget Deficit

One week after the Spiegel floated a media trial balloon, attempting to spark a change in Germany’s approach toward deficit spending, reporting that the government was proposing a €500 MM debt deal to fund climate protection, news which was promptly denied by the government, Spiegel has done it again, reporting moments ago that Angela Merkel and Finance Minister Olaf Scholz are ready to run a budget deficit… if Europe’s largest economy goes into recession.

According to the report, the shortfall in tax revenue from economic slump could be offset by new debt, Spiegel – which desperately wants to get the government and public on the side of deficit spending – reports, citing the usual anonymous “sources” in the chancellery and the finance ministry. As a reminder, under the German constitution, net federal debt can increase by only 0.35% of output if there is GDP growth, but since the rules can be relaxed during recession, it is not clear how the Spiegel report is actually news.

None of this was a consideration to algos, which saw “Germany” and “deficit spending” and sent the Emini surging…

… and the 10Y bund yield spiking to session highs.

Again, as a reminder, last Thursday, the Spiegel reported that a senior government official stated that Germany considering issuance of new debt to finance climate plans, implying a revisit to its current balanced federal budget and the “black zero” principle, (i.e. the principle that avoids creating new debt for more climate protection measure), essentially a “debt brake.” That report was promptly rejected by the government.

And now we await for the usual government channels to deny that the Spiegel report represents any change to current German fiscal policy.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.Global Issues

Bill Blain comments that 4 stocks could start a market crash. I will add a 5th:

1. HSBC

2.GE

3 Boeing

4. New IPO We work

and 5th (Harvey) Deutsche bank

(courtesy Bill; Blain/Shard Capital)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

Argentina

Everything is collapsing in Argentina: investment funds, the Peso, Argentinian bonds..the whole enchalada

(zero hedge)

Forget The Yield Curve, It’s Argentina’s Collapse That Highlights The Market’s Biggest Problem

Distracted by Hong Kong social unrest and focused on yield curve inversions and negative yields worldwide, it is not surprising the ‘average joe’ investor is missing the real forest fire for the trees.

With almost $17 trillion in global debt now yielding below zero… (Harvey: $17 trillion out of a total $52 trillion)

and more than half of the world’s sovereign yield curves inverted...

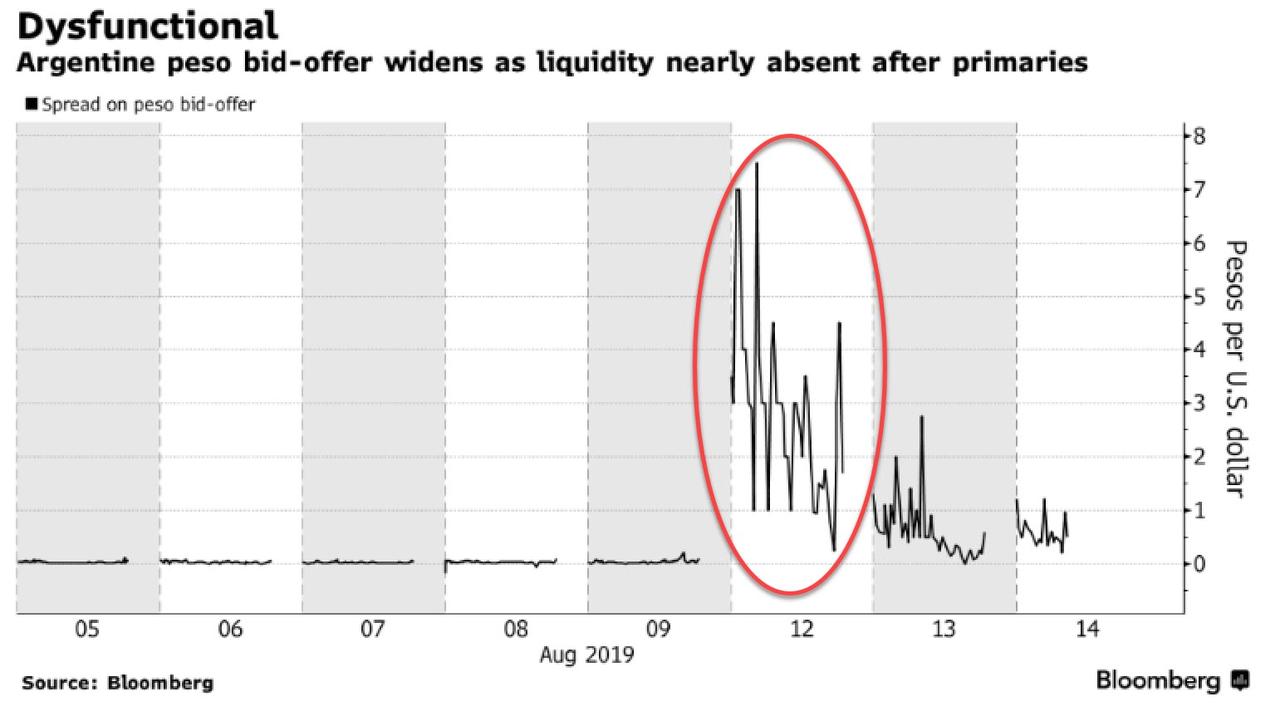

It is easy to be worried about the state of the global economy (and theoretically therefore the state of global financial markets), but, as Bloomberg’s Cormac Mullen notes, the biggest alarm bell for investors this week wasn’t the inverted U.S. yield curve; the market dislocation in Argentina was a clear signal to get out of illiquid securities soon or face exaggerated losses at the next significant meltdown.

President Mauricio Macri’s stunning rout in primary elections led to fears of another sovereign default. Argentina’s stock market plunged nearly 40%, the peso slid 15% and bonds slumped in a 4-sigma event — statistical speak for just 0.006% likely to happen.

The point isn’t to highlight the potential risk should a populist end up in the Casa Rosada, it’s to flag what can happen when event risks meet illiquid markets.

Just look at the reaction the Argentine currency. The gap between bid and offer prices surged to over 7 pesos per dollar on Monday.

The nation’s central bank and Treasury accounted for about a third of spot-market volume. Even with the currency down over 20% since last Friday it seems traders have yet to unload the bulk of their holdings

Argentina is a poster child for the way investors were drawn to once-inconceivable assets by the hunt for yield. And in a world where algorithms and machine trading are replacing brokers and market makers, the inability to exit all but the most liquid positions smoothly has become an ever bigger risk – a liquidity breakdown was the biggest fear for quant investors in a JPMorgan survey in May.

It’s not only exotic assets at risk of a breakdown in liquidity – a spike in ultra-long Treasury futures triggered a circuit-breaker in thin trading Wednesday. The yen experienced a flash crash during Tokyo’s New Year holidays.

Warnings have grown louder in recent months about the risks fund managers are running by investing in difficult-to-trade assets — what’s happening in Argentina is a reminder to heed them.

All of which confirms our recent discussion on the looming liquidity crisis:

First it was the shocking junk bond fiasco at Third Avenue which led to a premature end for the asset manager, then the three largest UK property funds suddenly froze over $12 billion in assets in the aftermath of the Brexit vote; two years later the Swiss multi-billion fund manager GAM blocked redemptions, followed by iconic UK investor Neil Woodford also suddenly gating investors despite representations of solid returns and liquid assets, and most recently the ill-named, Nataxis-owned H20 Asset Management decided to freeze redemptions.

By this point, a pattern had emerged, one which Bank of England Governor Mark Carney described best when he said last month that investment funds that promise to allow customers to withdraw their money on a daily basis are “built on a lie.”

And now, the chief investment officer of Europe’s biggest independent asset manager agrees with him, because while for much of 2019 the biggest risk bogeymen were corporate credit, leveraged loans, and trillions in negative yielding debt, gradually consensus is emerging that investment funds themselves may be the basis for the next liquidity crisis.