GOLD:$1551.60 UP $5.00 (COMEX TO COMEX CLOSING

Silver:$19.43 UP 28 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1553.00

silver: $19.59

Gold and silver had stellar performances again today with gold advancing by $5.0 and silver by 28 cents. As I stated yesterday: “I have been pointing out to you lately that the bankers are in serious trouble as they have a massive derivative shortage in both metals but a truly mammoth one in silver. Bankers get killed in derivatives with the speed to which our precious metal rises. Silver, in late June was trading around $14.75 so a gain of over 4.40 in 2 months fries our bankers. Deutsche bank with huge silver exposure will no doubt need the support of the Bundesbank to continue.”‘

Today I got quite excited to see gold and silver rise and especially into the close at the comex. The bankers are loathe to keep any new paper shorts longer than a few hours.

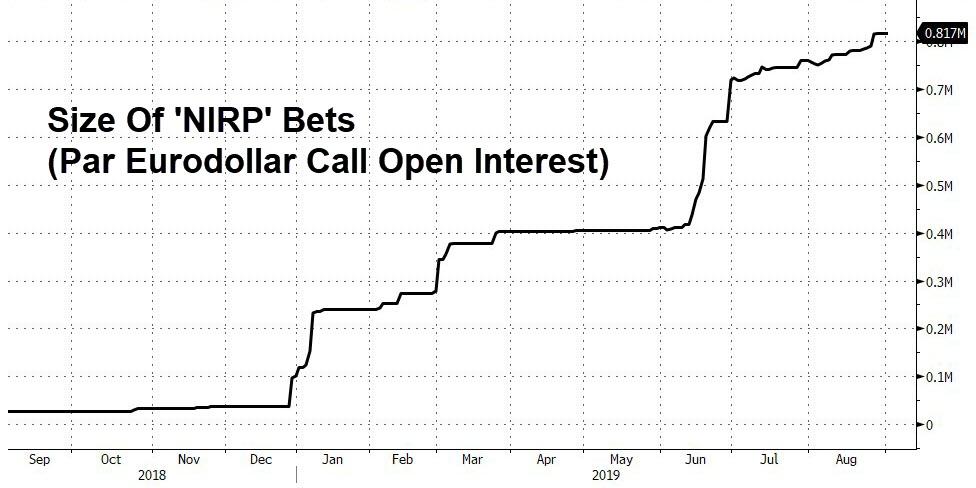

Yesterday I pointed out to you a very important paper from Alasdair MacLeod as we are now heading into zero bound interest rates. Jim Bianco comments today on the same topic and that is your must read for today.

we are getting very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 26/75

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,545.900000000 USD

INTENT DATE: 09/03/2019 DELIVERY DATE: 09/05/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 24

657 C MORGAN STANLEY 1

661 C JP MORGAN 4

661 H JP MORGAN 22

737 C ADVANTAGE 37 15

800 C MAREX SPEC 38

905 C ADM 9

____________________________________________________________________________________________

TOTAL: 75 75

MONTH TO DATE: 1,596

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 75 NOTICE(S) FOR 7500 OZ (0.2328 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1596 NOTICES FOR 159,600 OZ (4.9642 TONNES)

SILVER

FOR SEPT

651 NOTICE(S) FILED TODAY FOR 3,255,000 OZ/

total number of notices filed so far this month: 6132 for 30,660,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10,529 down 78

Bitcoin: FINAL EVENING TRADE: $ 10686 UP 64

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUGE AND CRIMINALLY SIZED 6901 CONTRACTS FROM 218,787 UP TO 225,688 WITH THE 83 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT: 0, AND ZERO; DEC: FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3322 CONTRACTS. WITH THE TRANSFER OF 3322 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3322 EFP CONTRACTS TRANSLATES INTO 16.61 MILLION OZ ACCOMPANYING:

1.THE 83 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

36.240 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD NEGLIGIBLE COVERING OF BANKER SHORTS AT THE SILVER COMEX ON YESTERDAY DESPITE THE FACT THAT THE BANKERS HAVE NOW COME TO REALIZE THAT THEY ARE IN SERIOUS TROUBLE. THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT.:

4592 CONTRACTS (FOR 2 TRADING DAYS TOTAL 4592 CONTRACTS) OR 22.96 MILLION OZ: (AVERAGE PER DAY: 1148 CONTRACTS OR 5.74 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 22.96 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 3.28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1572.67 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6,901, WITH THE 83 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD ANOTHER HUGE SIZED EFP ISSUANCE OF 3322 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC AND CRIMINALLY SIZED: 10,223 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3322 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 6,901 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 83 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $19.15 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.128 BILLION OZ TO BE EXACT or 161% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 651 NOTICE(S) FOR 3,255,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 36.240 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST ROSE BY AN OUT OF THIS WORLD: 24,886 CONTRACTS, TO 634,358 ACCOMPANYING THE $25.60 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING YESTERDAY// /

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 6946 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 11,621 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 634,358,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZE GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 36,507 CONTRACTS:,24,886 CONTRACTS INCREASED AT THE COMEX AND 11,621 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 36,507 CONTRACTS OR 3,650,700 OZ OR 113.55 TONNES. YESTERDAY WE HAD A GAIN OF $25.60 IN GOLD TRADING....AND WITH THAT GAIN IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 113.55 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON TRYING TO CONTAIN THE PRICE RISE. WE PROBABLY HAD SOME NEGLIGIBLE GOLD BANKER SHORT COVERING

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. : 18,567 CONTRACTS OR 1,856,700 oz OR 57.75 TONNES (2 TRADING DAY AND THUS AVERAGING: 9284 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY IN TONNES: 57.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 57.75/3550 x 100% TONNES =1.626% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4208.87 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 24,886 WITH THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($25.60)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,621 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,621 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 36,507 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES: (AND A NEW RECORD FOR A GAIN ON BOTH EXCHANGES)

11,621 CONTRACTS MOVE TO LONDON AND 24,886 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 113.55 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $25.60 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 75 notice(s) filed upon for 7500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.00 TODAY//(COMEX-TO COMEX)

A BIG CHANGE IN GOLD INVENTORY AT THE GLD; A HUGE PAPER DEPOSIT OF:11.73 TONNES

INVENTORY RESTS AT 890.04 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 28 CENTS TODAY:

VERY STRANGE!!

A BIG CHANGE IN SILVER INVENTORY AT THE SLV:

A WITHDRAWAL OF 708,000 OZ FROM THE SLV

/INVENTORY RESTS AT 387.446 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUGE SIZED 6,901 CONTRACTS from 218,787 UP TO 225,688 AND CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT 0 FOR DEC:. 3322 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3322 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 6913 CONTRACTS TO THE 3322 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 10,223 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 51.12 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ ;AUGUST AT 10.025 MILLION OZ//SEPT 2019: 36.240 MILLION OZ/

RESULT: A GIGANTIC SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 83 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 3322 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN UP 27.26 POINTS OR 0.93% //Hang Sang CLOSED UP 995.38 POINTS OR 3.90% /The Nikkei closed UP 23.98 POINTS OR 0.12%//Australia’s all ordinaires CLOSED DOWN .31%

/Chinese yuan (ONSHORE) closed UP at 7.1526 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 7.1526 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.1529 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

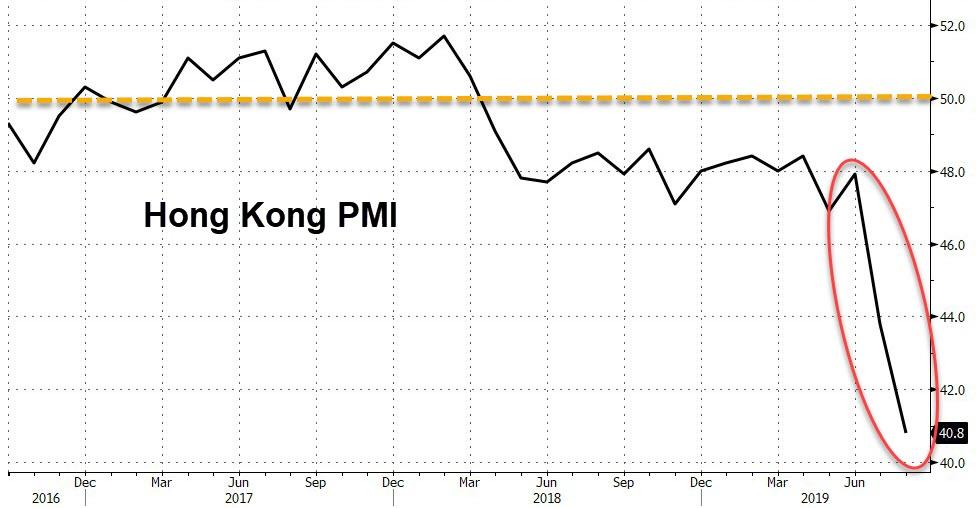

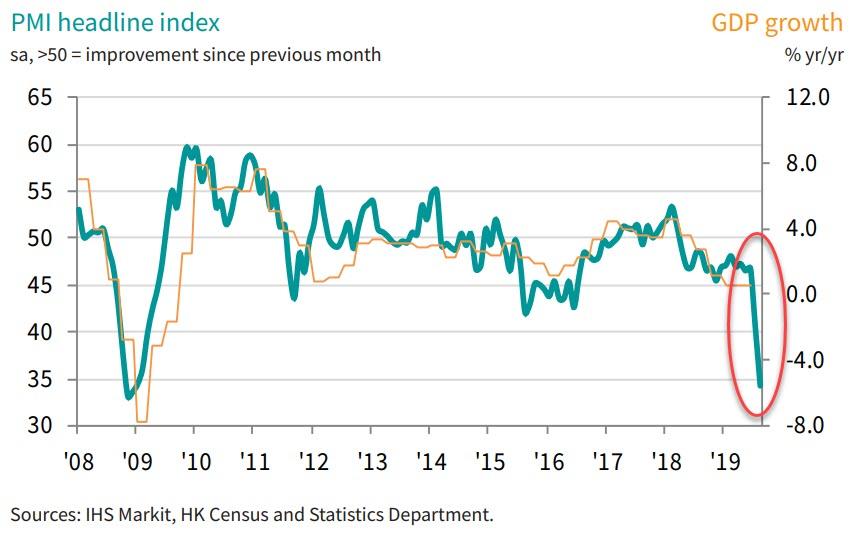

i)By goodness: Markit’s Hong Kong PMI collapsed to a massive contraction from 51.8 down to 40.8 due to the chaos in HK.

(zerohedge)

ii)Lam unexpectedly withdraws her hated extradition bill. However that is one only of the 5 demands. Also it is not Lam that is controlling the purse strings in Hong Kong but Mainland China. Let us see if protests stop

(zerohedge)

iii)In the words of Bill Blain:

“it is hard to put back the tear gas into the bottle”.. experts doubt the Lam’s big concession will pacify the pro democracy protest movement and thus expect more protests this weekend!

(zerohedge)

4/EUROPEAN AFFAIRS

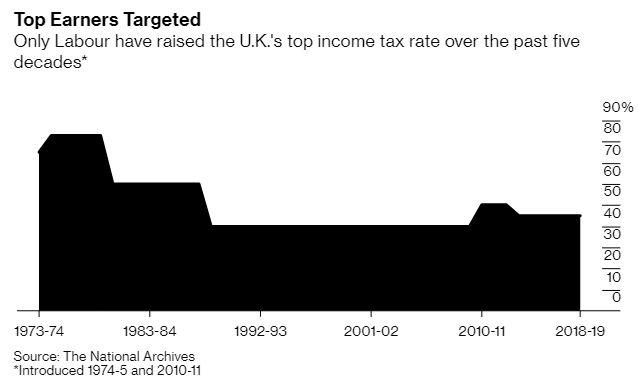

i)What a mess!! The pound surges as BoJo prepares for a snap election. However he needs the Liberals and he may not get their support as they may be decimated on anew election

(zerohedge)

ii)If Corbyn wins, the UK is preparing for a mass exodus of the richest taxpayer as well as Jewish people as he is anti- Semitic

7. OIL ISSUES

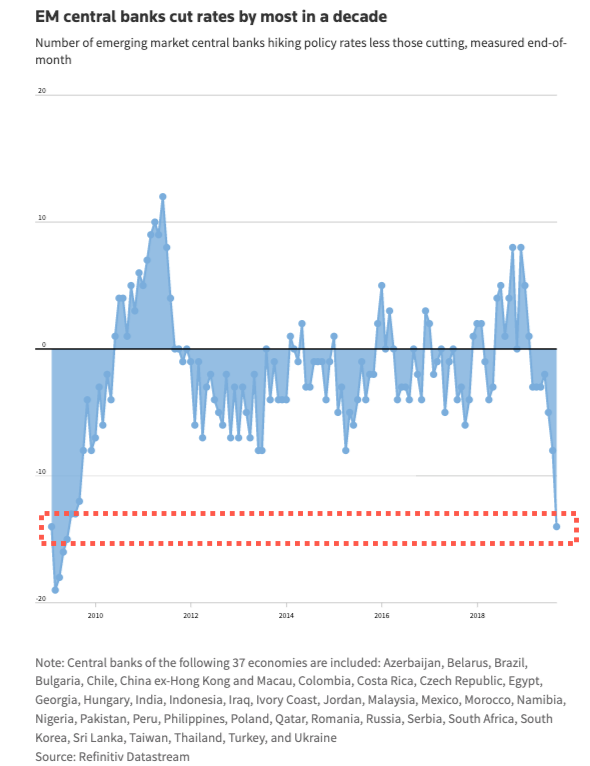

8 EMERGING MARKET ISSUES

The high USA dollar is again playing havoc to our emerging markets. The slowdown in trade growth has causes most of our emerging market central banks to cut rates and their cutting is the most since the financial crisis of 2008

(zerohedge)

9. PHYSICAL MARKETS

i)Is the USA heading for the zero bound in interest rates following Japan and Germany?

(London’s Financial Times/GATA)

ii)This is going to be interesting..long before the Communist party took over in China (1949), the Government in charge issued railroad bonds. These bonds have defaulted and the Chinese do not recognize their issuance. However Trump is studying the prospect of reviving century old claims on these Chinese bonds.

(Bloomberg)

iii)Von Greyerz is in my camp as to what value silver will eventually lead to. He even fathoms a 500 per oz price.

a good read..

(Von Greyerz/KingworldNews)

iv)Craig Hemke is also dubious of the GLD gold being “real”

A study the strange UK gold import and export trends

(Craig Hemke/Sprott)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

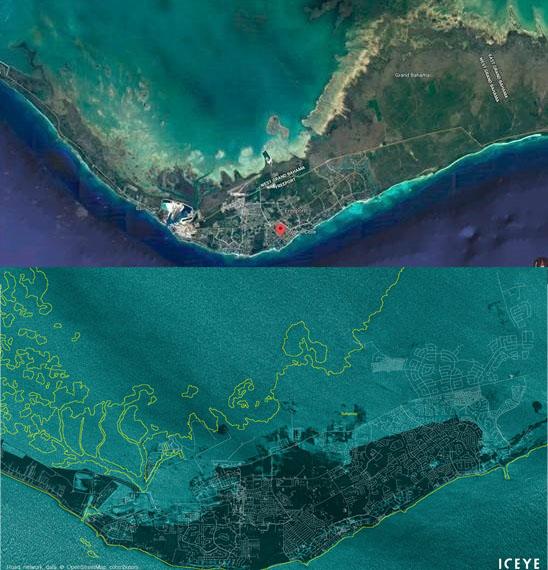

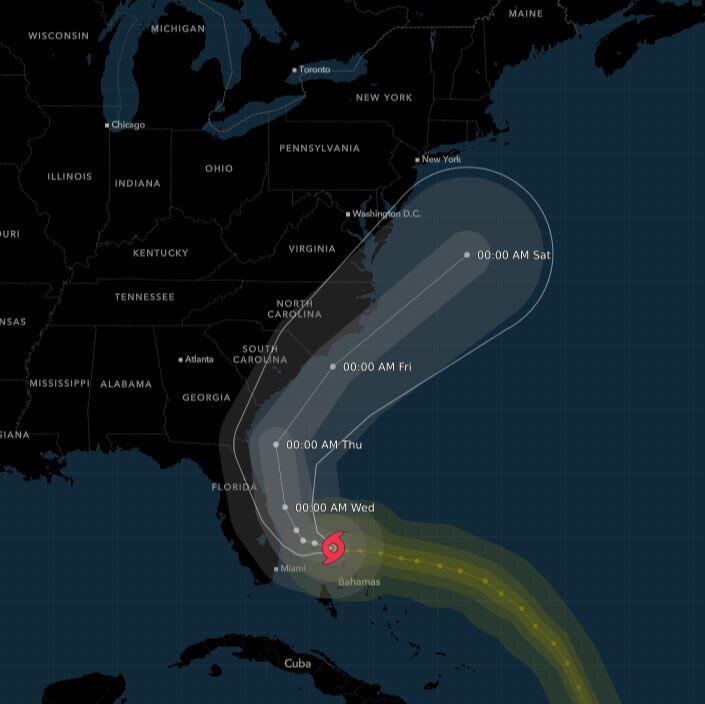

Dorian devastated Bahamas

(zerohedge)

iv) Swamp commentaries)

Seems that Omar is quite good at wrecking families: now her husband wants a divorce from her for dishonouring the family. Also Mynett is seeking a divorce from her husband who has having an affair with Omar

(zerohedge)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 1 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 8037.75 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 1487,047 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 208,663 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 208,663 CONTRACTS EQUATES to 1,043 million OZ 149.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.54% ((SEPT 4/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.95% to NAV (SEPT 4/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.54%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.96 TRADING 15.54/DISCOUNT 2.65

END

And now the Gold inventory at the GLD/

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 4/2019/ Inventory rests tonight at 890.04 tonnes

*IN LAST 656 TRADING DAYS: 45.34 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 556- TRADING DAYS: A NET 121.31 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 4/2019:

Inventory 387.446 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.05/ and libor 6 month duration 2.01

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .04

XXXXXXXX

12 Month MM GOFO

+ 1.92%

LIBOR FOR 12 MONTH DURATION: 1.94

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.02

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Gains 1.7% and Silver Surges 4.9% After Weak U.S. Data Compounds Global Recession Fears

* Gold gained 1.7% and silver surged 4.9% yesterday after weak U.S. manufacturing data reinforced fears of a U.S. and global recession

* The escalation in the U.S.-China trade war and the political shambles in the UK and Brexit further bolstered gold bullion’s safe-haven appeal

* U.S. manufacturing activity contracted for the first time in 3 years in yet another indication that we are in a recession or soon to enter one

* Silver surged 4.9% to near a 3 year high, breaching the $19/oz level

News and Commentary

Gold, silver surge after weak U.S. data compounds slowdown fears (Silver surges over 3%)

Gold rallies back to highest in over 6 years as ISM manufacturing marks lowest reading since 2016

Gold May Rise to $1,600, UBS WM’s Gordon Says (video)

One Of The Greats Says Despite Volatility Gold Bull Is Headed To $1,800

$1 billion decline in Venezuela’s gold reserves in first half of year

Wall Street bogged down by trade, growth concerns

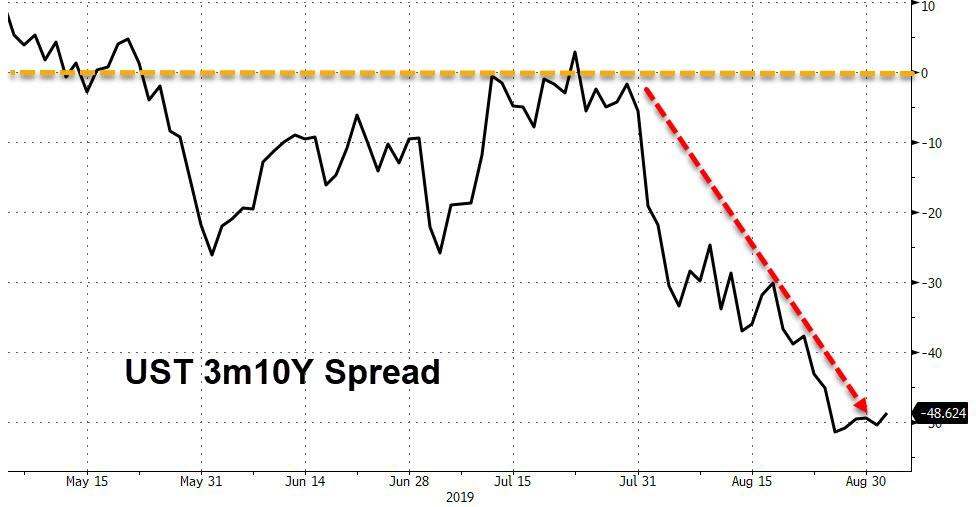

10-year Treasury yield falls to July 2016 low as ISM manufacturing index enters contraction

Switzerland Tried Negative Rates in the 1970s. It Got Very Ugly

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

03-Sep-19 1532.45 1537.85, 1278.06 1277.80 & 1400.35 1403.44

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

28-Aug-19 1541.75 1537.15, 1263.31 1258.77 & 1389.89 1387.43

27-Aug-19 1531.85 1532.95, 1250.91 1247.51 & 1378.97 1380.88

26-Aug-19 UK Bank Holiday

23-Aug-19 1495.50 1503.80, 1224.37 1228.91 & 1351.48 1357.63

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Is the USA heading for the zero bound in interest rates following Japan and Germany?

(London’s Financial Times)

Will U.S. follow Japan and Germany to rates below zero?

Submitted by cpowell on Tue, 2019-09-03 14:02. Section: Daily Dispatches

By Colby Smith

Financial Times, London

Tuesday, September 3, 2019

Some U.S. investors are girding themselves for the once-inconceivable prospect that the 10-year Treasury yield could be headed toward zero, as this year’s giant rally in bonds shows few signs of easing.

In a world awash with roughly $17 trillion of negative-yielding government debt — meaning buyers are guaranteed to get back less than they paid, via interest and principal, if they hold to maturity — America’s government bond market has long offered refuge to investors seeking higher returns.

…

German government bonds maturing in 10 years now yield minus 0.70%, while Japan’s 10-year debt yields minus 0.27%. In that context, the 1.5% yield on the 10-year Treasury looks attractive.

But roughly a month ago the 10-year note was yielding about 2%. The tight time frame of that 50 basis-point slide has caught investors by surprise, leading some to put the prospect of further heavy falls on their radars.

“We could see zero,” said Nick Maroutsos, the co-head of global bonds at Janus Henderson in Newport Beach, California, noting that any selloff in bonds so far, causing yields to rise, has been met with immediate buying. “The probability is increasing, particularly as we drop so rapidly.”

…

… For the remainder of the report:

https://www.ft.com/content/2bcac0e8-cb63-11e9-a1f4-3669401ba76f

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

This is going to be interesting..long before the Communist party took over in China (1949), the Government in charge issued railroad bonds. These bonds have defaulted and the Chinese do not recognize their issuance. However Trump is studying the prospect of reviving century old claims on these Chinese bonds.

(Bloomberg)

At least defaulted imperial Chinese railroad bonds don’t have negative rates

Submitted by cpowell on Tue, 2019-09-03 14:12. Section: Daily Dispatches

Trump’s New Trade War Tool Might Just Be Antique China Debt

By Tracy Alloway

Bloomberg News

Thursday, August 29, 2019

President Donald Trump’s next move in an increasingly fraught trade war with China could be one for the history books, literally. The Trump administration has been studying the unlikely prospect of reviving century-old claims on Chinese bonds sold before the founding of the communist People’s Republic.

The defaulted China bonds can be found in the attics and basements of thousands of Americans, or on EBay, where the certificates sell as collectibles for as little as a few hundred dollars each. The PRC, which succeeded the Republic of China after it replaced the imperial dynasty, has never recognized the debt, though that hasn’t stopped decades of attempts to collect payment on it.

…

Now, with Trump ratcheting up the trade rhetoric with China, holders of the antiquarian bonds are hoping he’ll press their case, even as other parts of the U.S. government are accusing people of fraudulently selling the same paper.

Perhaps the only thing more peculiar than the story of the Chinese debt and the bid to seek payment on it is the cast of characters drawn into its orbit. President Trump, U.S. Treasury Secretary Steven Mnuchin, and U.S. Commerce Secretary Wilbur Ross have met with bondholders and their representatives. Kirbyjon Caldwell, pastor of a Texas megachurch and spiritual adviser to George W. Bush, has been charged by the U.S securities regulator for selling the debt to elderly retirees. (Caldwell has pleaded innocent and maintains that the bonds are legitimate.) …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-08-29/trump-s-new-trade-war…

* * *

END

Von Greyerz is in my camp as to what value silver will eventually lead to. He even fathoms a 500 per oz price.

a good read..

(Von Greyerz/KingworldNews)

Von Greyerz tells KWN why silver will outpace gold

Submitted by cpowell on Tue, 2019-09-03 14:37. Section: Daily Dispatches

10:35a ET Tuesday, September 3, 2019

Dear Friend of GATA and Gold:

Swiss gold fund manager Egon von Greyerz today tells King World News why silver will outpace gold in their new bull market and that as the gold-to-silver ratio narrows to more normal levels and the manipulated paper silver market breaks, there won’t be any metal available — at least not at current prices. Von Greyerz’s comments are posted at KWN here:

https://kingworldnews.com/greyerz-says-the-price-of-silver-is-going-to-s…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke is also dubious of the GLD gold being “real”

A study the strange UK gold import and export trends

(Craig Hemke/Sprott)

Craig Hemke at Sprott Money: Curious U.K. gold import-export trends

Submitted by cpowell on Wed, 2019-09-04 01:42. Section: Daily Dispatches

9:40p ET Tuesday, September 3, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals report, writing tonight at Sprott Money, contemplates the trade data showing gold suddenly flowing back from Switzerland to London, and he wonders if it doesn’t presage the collapse of the fractional-reserve gold banking system and the market rigging it long has supported with derivatives.

Hemke’s analysis is headlined “Curious U.K. Gold Import-Export Trends” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/curious-uk-gold-import-export-trends-cr…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Venezuela central bank gold:

Venezuela Inventory gold June 30: 4.62 billion dollars at 1410.00 per oz = 3.3 million oz or 102.40 tonnes of which 34.13 tonnes is held at the Bank of England (and this gold is now doubt still leased out). That leaves 68.27 tonnes left in Caracas. It won’t be long until Venezuela is totally void of gold.

(Reuters/GATA)

$1 billion decline in Venezuela’s gold reserves in first half of year

Submitted by cpowell on Wed, 2019-09-04 02:36. Section: Daily Dispatches

Corina Pons and Mayela Armas

Reuters

Tuesday, September 3, 2019

CARACAS, Venezuela — Gold reserves held by Venezuela’s central bank fell by $1 billion in the first half of 2019, official data released this week showed, amid opposition accusations that the government is selling the precious metal abroad to raise revenue in the face of U.S. sanctions.

The value of the gold bars in central bank vaults fell to $4.62 billion, down 18.5% from $5.67 billion dollars at the end of 2018 — the lowest in 75 years, according to bank data

…

Opposition leaders have for months accused the government of President Nicolas Maduro of withdrawing gold to sell abroad as U.S. financial sanctions have crippled oil exports and blocked it from borrowing abroad.

The drop corresponds to a decline of 26.36 tons of gold from reserves, leaving the bank with about 102.40 tons. About one-third of that is held by the Bank of England.

Ruling Socialist Party officials accuse the Bank of England of refusing to repatriate the gold due to sanctions. The Bank of England has declined to comment, citing internal policy. …

… For the remainder of the report:

https://www.reuters.com/article/us-venezuela-gold/venezuela-gold-reserve…

* * *

END

iii) Other physical stories:

Nicholas B. proves our point that there is no gold at the comex

Follow his reasoning:

GARGANTUAN PAPER PRECIOUS METAL FRAUD NOW IN PLAIN SIGHT ON MANY FRONTS

An irate London motorist asked an Irish meter maid why she had issued a parking violation. She

replied “you cannot park at all on a single yellow line”. The motorist then asked as to the purpose of a

double yellow line. She replied “you cannot park at all at all on a double yellow line”. Harvey Organ

has been warning for a long time that there is virtually no precious metal at all in the COMEX

depositories. If we look at some recent data, I think we can upgrade this warning to “there is no

physical gold at all at all in the COMEX depositories”.

The CME issues daily updates on the status of gold and silver stored in its depositories. This data is not

archived, so one must not miss a single daily download if a complete record is desired. I read about

the filing of notices and the number of contracts standing for delivery and the number of contracts

stopped, but that data tends to be fragmented and disparate and moreover, based on the revelations

below, totally fictional. I then decided from 12 th July 2019 to analyze these CME daily reports to see

what the result would look like. Here is a summary of withdrawals from the CME USA depositories:

(this summary involves no less than 78 daily CME data files).

12 th July to 31 st July 2019 1 st August to 31 st Aug 2019

Registered Gold NIL NIL

Registered Silver NIL NIL

Eligible Gold 0.09 tonnes 0.241 tonnes

Eligible Silver 2,357,813 troy ounces 8,736,111 troy ounces

August 2019 was a designated active delivery month for gold and yet there was NO

delivery whatsoever of any physical gold from the registered categories at the

COMEX (the only category, per contract law, from which trading commitments can

be executed).This is hardly surprising considering that the registered inventory in

both gold and silver is no more (less in the case of silver) than 1% of the open

interest (details are provided below) What more evidence is needed that these

depositories are taking more than unsustainable strain? The one and only COMEX

‘delivery’ game in play, therefore, is comprised of transactions styled as ‘EFP’s (refer

below), and no one has any even remote visibility as to what is involved in these

gargantuan yet totally opaque transfers. Indeed one could possibly assume that the

CME releases these daily reports hoping that the reader will assume that

withdrawals of gold/silver do occur in the registered category, but just not today. All

it takes, however, is the daily discipline to download and save these reports to

ascertain the true picture. David Jensen recently stated that only 0.04% of gold

contracts in NY were settled by physical delivery; it would now seem (no, not ‘seem’

,rather it is proven) that NIL is the new norm, irrespective of any fine words about

the delivery side of the COMEX in daily action.

No wonder that every single CME report contains this disclaimer:

The information in this report is taken from sources believed to be reliable; however,

the Commodity Exchange, Inc. disclaims all liability whatsoever with regard to its accuracy or completeness.

This report is produced for information purposes only. (Author’s comment-what makes the weekly COT

report immune from such dire ‘health warnings’?)

(There was no movement at all in this period relating to the JP Morgan combined silver inventory of 153.7 million ounces.

This inventory is the subject of much commentary, but, in the grand scheme of things, is a bit less than three months

global mine supply (excluding Russia and China) and so is not that material-have a look at the total silver EFP volumes

below to contextualize the figures )

Let us now review what little LBMA data is disseminated (90 days in arrears). Here is the profile of

month end loco London vault holdings as up to date as possible. The December 2017/January 2018

profile is included since Harvey Organ has recorded the particulars of all reported EFP transfers from

1 st January 2018 onwards –tens of thousands of tonnes of these EFPs and virtually no meaningful

impact on this profile:

LBMA Profiles Dec 2017 June 2018 April 2019 May 2019

total Loco London 7827 7828 7680 7627

Less BOE (5321) (5318) (5019) (4990)

Less GLD (848) (824) (747) (741)

Residual: 1658 1686 1885 1916

Total Loc Silver. 1106 1109 1160 1152

less SLV 323 311 312 312

Residual: 783 798 848 840

There are several ETF funds in addition to GLD/SLV which warehouse their gold in loco London, so the

net residual gold at the LBMA is quite a bit less than the figure computed above, but what would be

the point of meticulous further microscopic analysis of historic data that is virtually useless in these

days of real time utilization of information. Anyway, it is always assumed that just because shares are

purchased in an ETF, then it follows that a commensurate increase in that ETF’s holding of physical

gold/silver, as mandated in its prospectus, will automatically and instantaneously follow. That is a

totally unwarranted assumption . At least the CME data enables an analysis of the full picture of

August 2019 withdrawals by 2 nd September, or just one day later because of Labour Day. Also the UK’s

own gold reserves are only 310 tonnes, so it would be a bit naïve to believe that the total gold in the

BOE vaults (segregated in the above table) has not been impaired by BIS swap transactions (which the

BIS freely acknowledges it instigates- from where else would the BIS source its ammunition?)

It is manifestly obvious that the core holdings of precious metal at the LBMA are permanently

constrained within very restricted parameters, and hence the only physical gold/silver metal that

leaves these loco London vaults is virtually equivalent to any inflows. The claims of the LBMA to

stratospheric trading volumes merely relate to propaganda associated with the churning of

undeliverable paper contracts in a zero sum game. But anyway this dribbling of delayed historic

information is no more than disinformation in the absence of any details at all in respect of the true

totality of all claims on this LBMA vaulted physical gold/silver; the only certainty is that such claims

are many multiples of the available metal.This is not surprising given that the ongoing alleged

viability of the entire global financial system is now predicated on the inexorable crescendo of

criminal fractional reserving practices, uber rehypothecation and the Ponzi scheme embodied in the

unbridled proliferation of sovereign debt.

The COMEX, on a daily basis now, serially engineers Exchange for Physical (EFP) transfers over to the

LBMA, so that the open interest does not go stratospheric .Let us, however, first refresh our minds in

respect of the open interest farce:

Open Interest (o/i) at 31st August 2019

Gold(Tonnes) Silver (000,000 ozs)

Total o/i 1,925 1,121

Registered Inv. 24 9

o/i Cover 1.225% 0.779%

Eligible inv. 236 230

Total Comex Inv. 259 239

o/i Cover 13.464% 21.288%

Since 1 st January 2018 (but certainly in

existence prior to this date) the volume

of EFP transfers until 31 st August 2019 is

as follows (data from Harvey Organ):

Gold (Tonnes) Silver (000,000 ozs)

1 st Jan 2018 to 31 st Dec 2018 7,310 2,847

To 31 st August 2019 4,151 1,550

Total for 20 months 11,461 4,397

20 months EFPs/Global Annual Mine Production About 4.5 years About 6 years

The criminals have now abusively over utilized these EFPs on a daily basis to such an extent that it is

manifestly obvious today that the term ‘physical’ has been high jacked in the false and misleading

nomenclature attributable to this manipulative charade. These EFP volumes are of such magnitude

that the only certainty is that absolutely no physical metal is involved. Annual global mine supply (ex

Russia/ China) is about 200 tonnes per month in the case of gold and about 55 (could be 60) million

ounces of silver per month.

My personal interpretation of the LBMA market is as follows:

Unallocated accounts: this is a transaction whereby a fiat ‘loan’ is made to an LBMA principal, and the

transaction can be redeemed by accepting a fiat settlement only, priced on the current manipulated paper price

of gold/silver ,but certainly no physical metal is involved at all.

EFP transfers from COMEX TO LBMA: even if the terms of the underlying agreements are ‘ad hoc’ and not

standardized (who knows?), the liability for delivery is assumed by an LBMA principal, who cannot possibly

deliver ,so the counter party exacts ‘special/onerous’ terms as incentivization for not demanding physical

delivery. Please refer to Harvey Organ re the ‘conspiracy to defraud’ embodied in the (non) reporting to the

regulator by the banks in respect of these liabilities styled as “serial forward contract obligations under 14 days “

Allocated accounts: this is a transaction whereby a congenital idiot labours under the delusion that his fully

funded and numbered .995 finesse gold bars are available for delivery on demand, whereas these bars have

long ago been re-refined to .9999 finesse and shipped eastwards (aka re-hypothecation-‘‘you lose , you get

nothing ,good day sir “.) GATA and others have referred to numerous examples of such “failures to deliver”.

It was inevitable that the meagre physical inventory at the COMEX would become (indeed has long

ago become) totally inadequate to satisfy demand for physical delivery but any crisis of failure to

deliver has been temporarily suppressed by the creation of all these EFP transfers. The form of these

EFP contracts is unknown as is the identity and intentions of the counterparties. The EFP volumes

recorded above embody an orgy of excess that has completely shredded any pretext of ultimate

deliverability and yet the regulators refuse to even acknowledge that any query merits the dignity of

an acknowledgement, let alone a response. When does all this insanity reach a denouement? Perhaps

the success hitherto in suppressing the gold price became a catalyst for the hubris of consigning

positive interest rates to the dustbin of history and the euphoric philosophy that the limitless

proliferation of sovereign debt need no longer be constrained in the absence of any associated

interest burden. China and Russia have accumulated possibly as much as 30,000 tonnes of physical

gold each (unless you have personally audited the extensive network of vaults under the Kremlin and

microscopically performed the calculus relating to Chinese gold importation and domestic production

over the years, any contra opinion you may hold is as weighty as a dandelion blowing in the wind).

The end game is easy to forecast and the headline price of gold will not be set for ever by the frantic

supply of gargantuan volumes of undeliverable naked short and fraudulent paper promises. Whilst

the BOE governor (a Canadian from a country that has disposed of all its gold reserves) recently, at

Jackson Hole, made suggestions about creating a hermetic cyber seal to encapsulate fiat digital ‘air’ to

create an alternative to the fiat US$ as a reserve currency, the new One Belt One Road trading bloc

(eventually encompassing more than two thirds of the global population) will indeed re instate an

alternative, and it could not be more obvious that it will incorporate a gold standard. The pure

unadulterated insanity of Western Modern Monetary Theory (MMT) is a wonderful encapsulation of

the immortal words of Tacitus; “those whom the Gods wish to destroy they first make mad”.

Post script: GATA has been in existence for at least two decades, and I have been a member for about

15 years. Initially the seminal work of Frank Veneroso heavily influenced GATA’s early writings, and

Veneroso estimated that the manipulation of the physical gold price via swaps/loans/leases etc.

would ‘hit a brick wall’ between 2011 and 2013 as physical metal supply dried up. Obviously the

manipulators managed to engineer even more suppressive techniques than were factored into

computations back in the ‘eighties’. Limitless, naked short, undeliverable, fraudulent paper gold

promises aided by incessant MSM propaganda and infinite CB fiat resources and CME/LBMA

accommodation and regulatory complicity proved to be a bit more overwhelming and formidable

than initial forecasts. August 2019 has witnessed the decimation of some serious and well established

chart resistance levels in respect of the precious metals; GATA has been predicting for about a decade

such price action (aka a commercial signal failure) that eventually will culminate in a price ‘moon shot’

as the physical market assumes its rightful hegemony . Some commentators outside GATA have even

estimated that the fractional reserving of paper promises to available physical gold/silver could even

be in a ratio of up to 500/1.

end

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Global Markets Soar As Tensions Ease From Hong Kong To Italy And London

Just one day after stocks tumbled on concerns of an imminent economic recession when the US Manufacturing ISM tumbled below 50 for the first time in 3 years, all fears appeared to evaporate this morning as U.S. stock-index futures surged, erasing almost all of yesterday’s losses, boosted by hopes of a return to calm in Hong Kong combined with political developments in Italy and the U.K. S&P futures surged as much as 1% after news that Hong Kong’s chief executive plans to formally withdraw the extradition bill that had sparked widespread protests.

Stocks got a further boost out of the latest development in Italy, where the FTSE MIB Index was the best performer among local European markets, up 1.7%, after Giuseppe Conte cleared the last hurdle to become prime minister, when he got backing from supporters of the Five Star Movement in an online vote. Finally, the no-deal Brexit storm appears to be passing as lawmakers in the U.K. supported moves to block Prime Minister Boris Johnson from taking the nation out of the European Union without a deal.

As a result, global stocks rose 0.4%, as Europe rallied 1.1% and after a positive session in Asia following a report showing that growth in China’s service sector accelerated despite broader economic headwinds.

Asian equity markets eventually traded mostly higher as the headwinds from Wall Street, where the S&P 500 and DJIA snapped a 3-day win streak due to ongoing trade uncertainty and weak ISM Manufacturing, was eventually counterbalanced as data from the region provided some encouragement.

ASX 200 (-0.3%) and Nikkei 225 (+0.1%) were mixed with broad weakness seen across Australia’s sectors as participants digested GDP figures which showed growth slowed to its weakest since the GFC as expected and with a cut at next month’s RBA meeting seen as a coin flip.

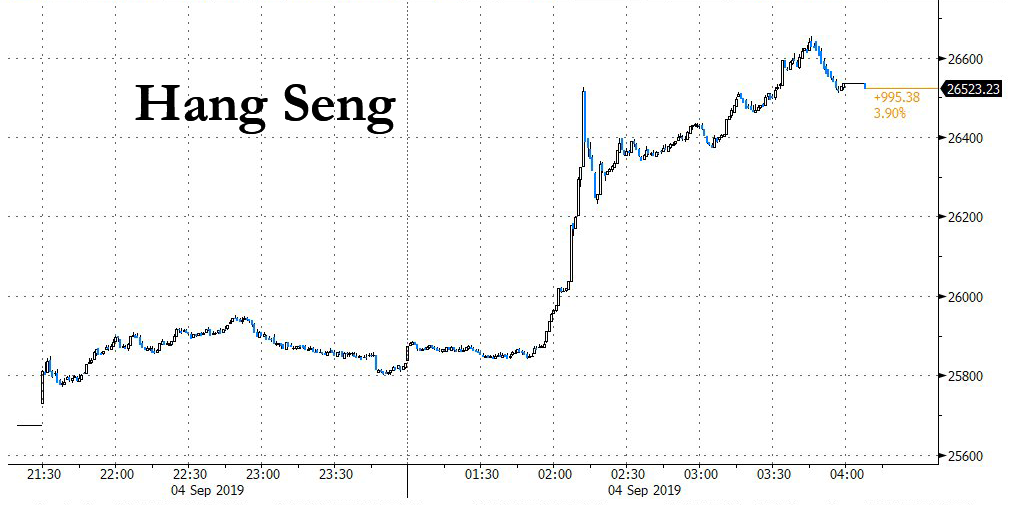

In terms of sectors, the top-weighted financial industry was among the laggards, although gold miners bucked the trend on recent strength in the precious metal. The Japanese benchmark was indecisive but pared opening losses as it found mild support from favourable currency moves, while Hang Seng (+3.9%) and Shanghai Comp. (+0.9%) were positive after Chinese Caixin Services PMI topped estimates to print a 3-month high with Hong Kong the outperformer after HK CEO Carrie Lam unexpectedly withdrew legislation that would’ve allowed extraditions to China.

The MSCI Hong Kong Index surged 5.4%, its biggest gain since October 2011. Real estate firms led the gains, with Wharf Real Estate Investment Co., New World Development Co. and Sun Hung Kai Properties Ltd. all up more than 9%. The Hong Kong dollar strengthened as much as 0.08%. The Hang Seng Index closed 3.9% higher.

However, gains in the mainland were restricted amid a continued PBoC liquidity drain and ongoing trade uncertainty after President Trump reiterated China will get a tougher deal if he wins the 2020 elections and was said to be angered by China’s tariff retaliation that he wanted to double the tariffs but resorted to a 5% hike after consultations. The Shanghai Composite Index added 0.9%, supported by large financial firms. Finally, 10yr JGBs were lacklustre amid the indecision in Japan and a lack of BoJ presence in the market, which saw prices retrace some of the recent gains.

Major European bourses are also higher across the board, with the Stoxx 50 +0.8%, and all industry groups in the Stoxx Europe 600 index advanced, almost erasing the gauge’s August decline as risk appetite was initially spurred by the news that Hong Kong Chief Executive Carrie Lam will formally withdraw the extradition bill, which is responsible for the ongoing protests in the region. UK’s FTSE 100 (+0.3%) marginally lags its peers amid unfavorable Sterling action to exporters after the UK Parliament approved a motion to seize control of Parliamentary time in an attempt to block a no-deal Brexit, sending . Meanwhile, Italy’s FTSE MIB (+1.5%) is led by constructive developments in Italian politics, after the 5SM’s online vote of grassroot members showed a backing for the formation of a 5SM/PD coalition, thus eliminating the risk of political limbo. Luxury-goods makers that depend on Hong Kong sales including Richemont and Swatch climbed along with stocks in Italy, where a new political coalition took shape that may be more conciliatory toward the European Union.

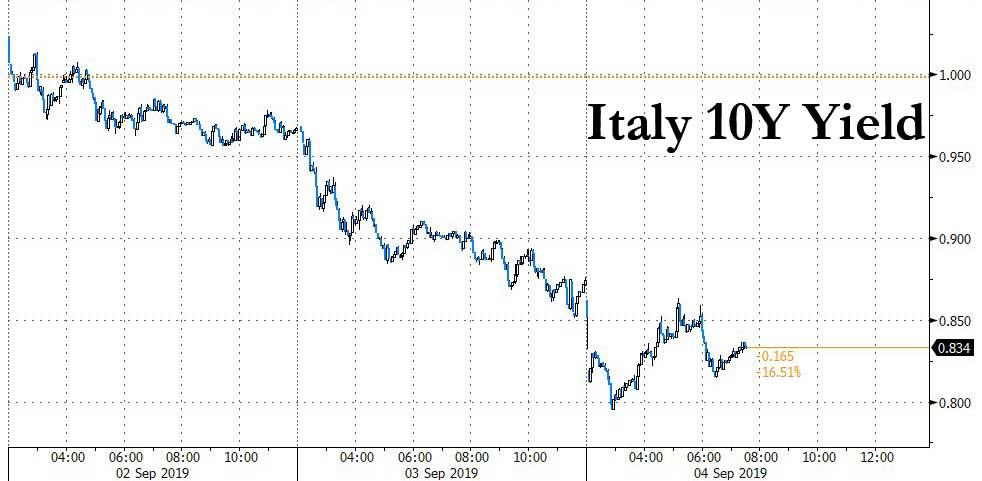

Italian bonds rose after members of the “anti-establishment” 5-Star Movement backed a proposed coalition with the establishment, center-left Democratic Party on Tuesday, opening the way for a new government to take office in the coming days. As a result 10-year Italian government bond yields hit 0.803%, a new record low, while Italian banks, another proxy for political risk in the country, rallied 2%.

“The next hurdle for the government will be the confidence vote in Parliament. But at the moment risks appear limited,” said Giuseppe Sersale, fund manager at Anthilia Capital.

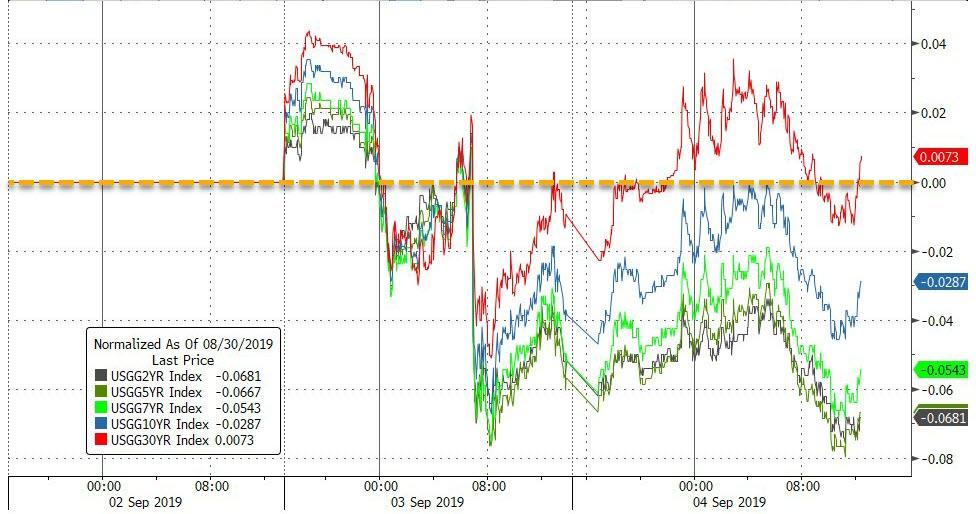

Yields on the safe-haven 10-year German Bund rose to 0.676% after falling to a fresh record low on Tuesday, while the yield on the 10-year U.S. Treasury rose to 1.489% after hitting its lowest since July 2016 in the previous session in light of the weak ISM U.S. factories reading.

Political concerns and expectations of further easing measures by central banks have been squeezing bond yields globally but the return of risk appetite on Wednesday on the back of political developments in Europe and upbeat economic data from China triggered a rebound.

In FX, China’s yuan rose the most in a week as the dollar slid on weak data and the central bank set its daily fix at a level stronger than market watchers expected for an 11th day. The People’s Bank of China set the yuan’s daily reference rate at 7.0878 per dollar, stronger than the average forecast of 7.1023 by 20 traders and analysts surveyed by Bloomberg. The yuan rose as much as 0.2% against the greenback, which fell after a disappointing U.S. manufacturing report reignited concern about global economic growth. The yuan will continue to trade between 7.1 and 7.2 as long as trade tensions between China and the U.S. don’t escalate further, according to Gao Qi, a currency strategist at Scotiabank in Singapore.

The Bloomberg Dollar Spot Index slipped for a second day, while the pound rises for a second day amid broad dollar weakness after Prime Minister Boris Johnson began moved to trigger a snap general election to resolve the Brexit standoff. Traders were also awaiting a speech by Bank of England Governor Mark Carney and the August inflation report.

In commodities, oil prices recovered some ground, helped by the positive China data and having touched their lowest in close to a month during the previous session on fears over the weakening global economy. Brent crude was up 22 cents at $58.48 a barrel, while WTI futures gained 31 cents at $54.25 at barrel.

On today’s calendar, trade balance, mortgage applications are due. Scheduled earnings include Palo Alto Networks, Slack.

Market Snapshot

- S&P 500 futures up 0.9% to 2,932.25

- STOXX Europe 600 up 1.1% to 383.83

- MXAP up 0.9% to 153.57

- MXAPJ up 1.6% to 497.54

- Nikkei up 0.1% to 20,649.14

- Topix down 0.3% to 1,506.81

- Hang Seng Index up 3.9% to 26,523.23

- Shanghai Composite up 0.9% to 2,957.41

- Sensex up 0.4% to 36,718.48

- Australia S&P/ASX 200 down 0.3% to 6,553.01

- Kospi up 1.2% to 1,988.53

- German 10Y yield rose 2.4 bps to -0.682%

- Euro up 0.2% to $1.0991

- Brent Futures up 0.5% to $58.56/bbl

- Italian 10Y yield fell 9.1 bps to 0.535%

- Spanish 10Y yield rose 1.7 bps to 0.126%

- Brent Futures up 0.5% to $58.56/bbl

- Gold spot down 0.6% to $1,537.47

- U.S. Dollar Index down 0.2% to 98.82

Top Overnight News from Bloomberg

- U.K. Prime Minister Johnson began moves to trigger a snap election after suffering a defeat for his Brexit strategy. Members of the House of Commons voted 328 to 301 to take a first step toward forcing the prime minister to delay Brexit by three months

- Economic situation with U.S. manufacturing contracting amounts to a “global shock” that warrants an aggressive step by the Fed at its meeting in two weeks, St. Louis Fed President James Bullard says

- Boston Fed President Eric Rosengren said the U.S. economy remains “relatively strong” despite clearly heightened risks, leaving him unconvinced the central bank needs to cut interest rates this month

- ECB policy maker Francois Villeroy de Galhau signaled skepticism over the need for renewed asset purchases while leaving open the question of whether he’d still back a stimulus package that includes them.

- President Donald Trump sought to prod China into doing a trade deal before the U.S. presidential election in November 2020, or face even more difficult negotiations during his potential second term

- French Finance Minster Bruno Le Mairemet with U.S. authorities in Washington as part of a plan to offer Iran a $15 billion economic lifeline and rescue the Iran nuclear accord

- Economists are downgrading their forecasts for economic growth in China to below a level seen as necessary for the Communist Party to meet its own goals in time for its centenary in 2021

- China softened toward Hong Kong’s protesters, saying peaceful demonstrations were allowed under the law, even as it ruled out a fundamental demand for direct democracy

Asian equity markets eventually traded mostly higher as the headwinds from Wall St, where the S&P 500 and DJIA snapped a 3-day win streak due to ongoing trade uncertainty and weak ISM Manufacturing, was eventually counterbalanced as data from the region provided some encouragement. ASX 200 (-0.3%) and Nikkei 225 (+0.1%) were mixed with broad weakness seen across Australia’s sectors as participants digested GDP figures which showed growth slowed to its weakest since the GFC as expected and with a cut at next month’s RBA meeting seen as a coin flip. In terms of sectors, the top-weighted financial industry was among the laggards, although gold miners bucked the trend on recent strength in the precious metal. The Japanese benchmark was indecisive but pared opening losses as it found mild support from favourable currency moves, while Hang Seng (+3.9%) and Shanghai Comp. (+0.9%) were positive after Chinese Caixin Services PMI topped estimates to print a 3-month high with Hong Kong the outperformer after HK Chief Exeutive Carrie Lam withdrew the controversial Extradition Bill. However, gains in the mainland were restricted amid a continued PBoC liquidity drain and ongoing trade uncertainty after President Trump reiterated China will get a tougher deal if he wins the 2020 elections and was said to be angered by China’s tariff retaliation that he wanted to double the tariffs but resorted to a 5% hike after consultations. Finally, 10yr JGBs were lacklustre amid the indecision in Japan and a lack of BoJ presence in the market, which saw prices retrace some of the recent gains.

Top Asian News

- Traders Fixate on Trump’s Twitter Everywhere, Except in China

- China Foreign Ministry Doesn’t Comment on H.K. Bill Withdrawal

- Anil Ambani’s Reliance Naval Facing Cash Crunch Amid Debt Revamp

- Miners Offer Some Tactical Opportunities in Late Cycle, DB Says

Major European bourses are higher across the board [Eurostoxx 50 +0.8%] as risk appetite was initially spurred amid source reports (later confirmed) that Hong Kong Chief Executive Carrie Lam is to formally withdraw the extradition bill today, which is responsible for the ongoing protests in the region. UK’s FTSE 100 (+0.3%) marginally lags its peers amid unfavourable Sterling action to exporters after the UK Parliament approved a motion to seize control of Parliamentary time in an attempt to block a no-deal Brexit. Meanwhile, Italy’s FTSE MIB (+1.5%) is led by constructive developments in Italian politics, after the 5SM’s online vote of grassroot members showed a backing for the formation of a 5SM/PD coalition, thus eliminating the risk of political limbo. Sectors are in a sea of green with substantial outperformance in consumer discretionary names as luxury stocks soar on optimistic Hong Kong news. Kering (+3.7%), Richemont (+3.5%), Swatch (+3.2%) all reside near the top of the Stoxx 600. In terms of individual movers, Thales (+6.4%) shares spiked higher at the open after posting an improvement in earnings, meanwhile Mediaset (+2.1%) shareholders approved the merger of its Italian and Spanish units to compete with the likes of Netflix. On the flip side, Barratt Developments (-1.4%) shares fell post-earnings, whilst Deutsche Telekom (-0.1%) is subdued amid reports that Illinois has joined the lawsuit aimed at blocked a merger between T-Mobile (of which Deutsche Telekom owns 63% of) and Sprint.

Top European News

- Germany Cabinet Aims to Reduce Glyphosate Usage in Coming Years

- U.K. on Course for Recession as Services Growth Stagnates

- U.K.’s Super-Rich Prepare to Flee From Corbyn Rule, Not Brexit

- European Car-Parts Makers Rise as JPMorgan Sees Year-End Rally

In FX, the Pound remains at the top of the G10 ranks after MPs voted in favour of a no Brexit deal blocking motion last night, with Cable breaching technical resistance in the form of the 21 DMA at 1.2144 and Eur/Gbp extending its reversal through 0.9100 and pivoting 0.9050. However, Sterling lost some momentum after the UK services PMI completed a set of misses vs consensus and IHS/Markit conjects that the slowdown in the sector combined with more pronounced contraction in manufacturing and construction indicates that GDP is likely to slip 0.1% q/q in Q3. If confirmed this would mean a technical recession and Cable is waning just ahead of 1.2200 having eclipsed Monday’s 1.2175 high and Fib resistance around the same level, or 1.2176 to be precise.

- AUD/NZD/EUR/SEK – The next best majors and all benefiting from further Greenback weakness post yesterday’s sub-50 US manufacturing ISM (DXY down to 98.571) on top of a broad upturn in risk sentiment on the aforementioned positive Brexit developments, Italy’s 5-Star approving its tie-up with the PD party and Hong Kong’s CE Lam withdrawing the extradition bill. Aud/Usd just pulled up shy of the 0.6800 mark with the added impetus of China’s Caixin services/composite PMIs surpassing expectations and not too ruffled by Aussie GDP data confirming forecasts for a slowdown in growth to GFC levels. Nzd/Usd continues to lag around 0.6350 as the Aud/Nzd cross holds above 1.0650, but Eur/Usd is back on the 1.1000 handle following a run of firmer than expected Eurozone services PMIs and ahead of more ECB speakers. Nevertheless, the Swedish Krona is outperforming on the back of an even stronger services PMI print and not perturbed by Nordea revising its Riksbank rate outlook from unchanged through 2020 to a 25 bp ease in December this year on the eve of this month’s policy meeting, with Eur/Sek straddling 10.7500.

- CAD/CHF – Also firmer vs the Greenback, but a bit more contained as the Loonie faces resistance around 1.3300 in the run up to Canadian trade data and the BoC, while the Franc is ever wary that too much appreciation will not be tolerated and is fading into 0.9840 with Eur/Chf meandering between 1.0825-60.