GOLD:$1517.80 DOWN $33.80 (COMEX TO COMEX CLOSING)

Silver:$18.75 DOWN 68 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1518.80

silver: $18.65

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 07/17

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,550.300000000 USD

INTENT DATE: 09/04/2019 DELIVERY DATE: 09/06/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 4

132 C SG AMERICAS 2

661 H JP MORGAN 7

737 C ADVANTAGE 15 4

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 17 17

MONTH TO DATE: 1,613

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 17 NOTICE(S) FOR 1700 OZ (0.0528 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1613 NOTICES FOR 161,300 OZ (5.0171 TONNES)

SILVER

FOR SEPT

378 NOTICE(S) FILED TODAY FOR 1,890,000 OZ/

total number of notices filed so far this month: 6510 for 32,550,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10,582 UP 15

Bitcoin: FINAL EVENING TRADE: $ 10510 DOWN 86

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A HUGE SIZED 2702 CONTRACTS FROM 225,688 DOWN TO 222,986 DESPITE THE STRONG 28 CENT GAIN IN SILVER PRICING AT THE COMEX. WE NO DOUBT HAVE SCARED OUR BANKERS AS WE HAD ATTEMPTED BANKER SHORT COVERING WITH LIMITED SUCCESS ON THEIR PART.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0, DEC:3364 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3364 CONTRACTS. WITH THE TRANSFER OF 3364 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3364 EFP CONTRACTS TRANSLATES INTO 16.82 MILLION OZ ACCOMPANYING:

1.THE 28 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

37.570 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY AS THE BANKERS HAVE NOW FINALLY COME TO REALIZE THAT THEY ARE IN SERIOUS TROUBLE. THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

7956 CONTRACTS (FOR 3 TRADING DAYS TOTAL 7956 CONTRACTS) OR 39.78 MILLION OZ: (AVERAGE PER DAY: 2652 CONTRACTS OR 13.26 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 39.78 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 5.68% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1589.49 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2702, DESPITE THE 28 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 3364 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A FAIR SIZED: 682 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3364 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2702 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 28 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.43 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.116 BILLION OZ TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 378 NOTICE(S) FOR 1,890,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

1.HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 37.570 MILLION OZ//

2 THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

3 HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. HOWEVER FINALLY THAT PRICE IS RISING. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST ROSE BY AN ATMOSPHERIC AND CRIMINALLY SIZED 9,205 CONTRACTS, TO 643,563 ACCOMPANYING THE $5.00 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY//

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5945 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 5945 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 643,563,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZE GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,150 CONTRACTS:,9205 CONTRACTS INCREASED AT THE COMEX AND 5,945 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 15,150 CONTRACTS OR 1,515,000 OZ OR 47.122 TONNES. YESTERDAY WE HAD A GAIN OF $5.00 IN GOLD TRADING....AND WITH THAT GAIN IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 47.122 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON TRYING TO CONTAIN THE PRICE RISE. WE PROBABLY HAD SOME NEGLIGIBLE GOLD BANKER SHORT COVERING BUT IT WAS SILVER THAT WITNESSED THE CONSIDERABLE ATTEMPTED BANKER SHORT COVERING.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 24,512 CONTRACTS OR 2,451,200 oz OR 76.24 TONNES (3 TRADING DAYS AND THUS AVERAGING: 8170 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAYS IN TONNES: 72.24 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 72.24/3550 x 100% TONNES =2.03% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4,227.36 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 9205 DESPITE THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($5.00)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5945 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5,945 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 15,150 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5945 CONTRACTS MOVE TO LONDON AND 9205 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 47.122 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE SMALLISH GAIN IN PRICE OF $5.00 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 17 notice(s) filed upon for 1700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD..

WITH GOLD DOWN $33.80 TODAY//(COMEX-TO COMEX)

A BIG CHANGE IN GOLD INVENTORY AT THE GLD; A HUGE PAPER DEPOSIT OF:5.86 TONNES//PROBABLY DONE JUST BEFORE THE RAID.

INVENTORY RESTS AT 895.90 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 68 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV:

/INVENTORY RESTS AT 387.446 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 2702 CONTRACTS from 225,688 DOWN TO 222,986 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0, FOR DEC: 3364 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3364 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2702 CONTRACTS TO THE 3364 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE STILL OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 975 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.310 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ//AUGUST AT 10.025 MILLION OZ//SEPT 2019: 37.570 MILLION OZ

RESULT: A HUGE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE VERY STRONG 28 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A HUGE SIZED 3364 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 28.45 POINTS OR 0.96% //Hang Sang CLOSED DOWN 7.70 POINTS OR 0.03% /The Nikkei closed UP 436.80 POINTS OR 2.12%//Australia’s all ordinaires CLOSED UP .97%

/Chinese yuan (ONSHORE) closed UP at 7.1448 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON// ONSHORE YUAN CLOSED UP // LAST AT 7.1448 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.1400 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

Japan/South Korea

My goodness the rift between South Korea and Japan intensifies. The South Koreans have not forgot about World War ii. Exports of Japanese beer falls by an unbelievable 97%

(zerohedge)

3C CHINA

i)China/USA

Seems that the Chinese media are ignoring Trump’s tweets

(zerohedge)

ii)HONG KONG

4/EUROPEAN AFFAIRS

i)Tom Luongo states what happened yesterday in Br. parliament perfectly

(courtesy Tom Luongo)

ii)Now Boris Johnson;s brother resigns as Junior Minister and by doing so gives his brother the “royal shaft”. England is now in a total mess.

(zerohedge)

iii)A terrific commentary from Mish Shedlock on the Brexit affair. He states that Boris Johnson’s moves were all planned and that he will get his no deal Brexit through because there will be no Queen’s consent.

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)A good interview of GATA board member Ed Steer

(Ed Steer/GATA/Goddard/HoweStreet.com)

ii)As I pointed out yesterday, are the rats fleeing a sinking ship:

Soc Generale flees the LBMA in their trading platform on gold and silver:

(courtesy Reuters/GATA)

iii)Rats fleeing a sinking ship?. Gold and silver rose immediately after this was announced.

(Hobson/Reuters)

iv)Are the boys still engaging in spoofing despite their criminal guilty plea?? You can bet the farm that they are

(courtesy Chris Marcus/Arcadia Economics)

v)Just in case you missed Nicholas’ masterpiece from yesterday, I am repeating it:

(courtesy Nicholas Biezanek)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

Pure nonsense!/futures soar on news of a supposed resumption of trade talks in October

(zerohedge)

b)MARKET TRADING/USA/late morning

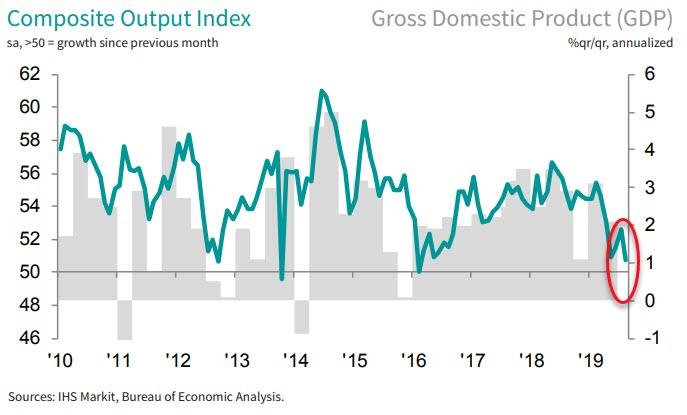

The ISM is a phony report and it showed a rebound while the identical survey Markit showed a huge downgrade. go figure!

ii)Market data/USA

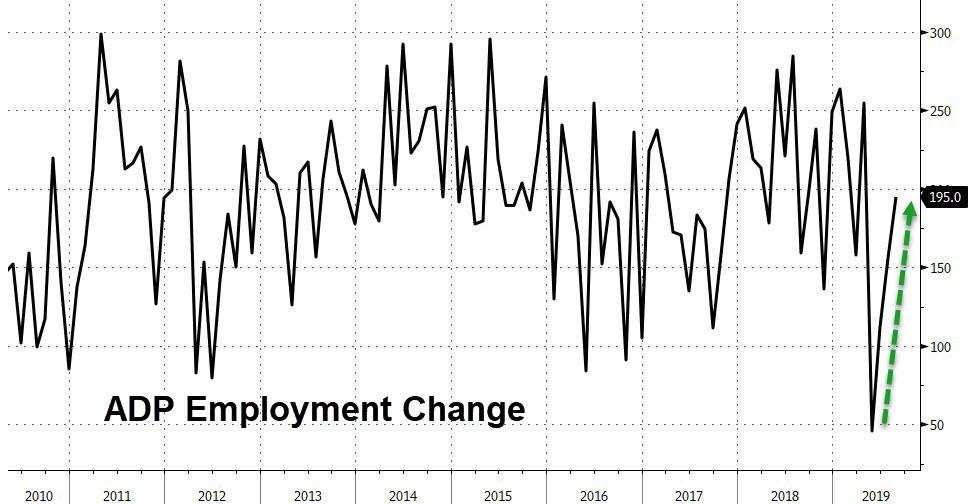

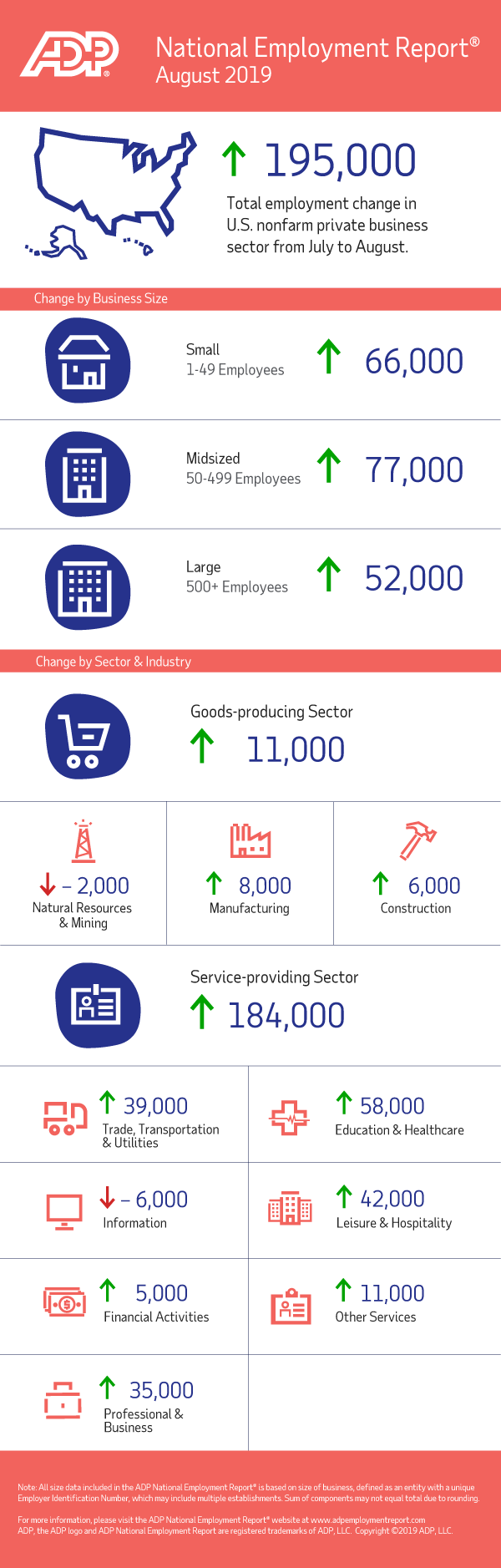

a)The phony ADP report which is always bullish surges in August showing a gain of 195,000 workers

(ADP/Zerohedge)

b)Again the ISM service report deviates from the Markit service..such crooks.

iii) Important USA Economic Stories

a)The Dems will not like this: Trump diverts $3.6 billion from the military budget to fund the border wall

(zerohedge)

b)Trump is angry at Barra for moving mega jobs over to China. Let us see what he will say today on this matter

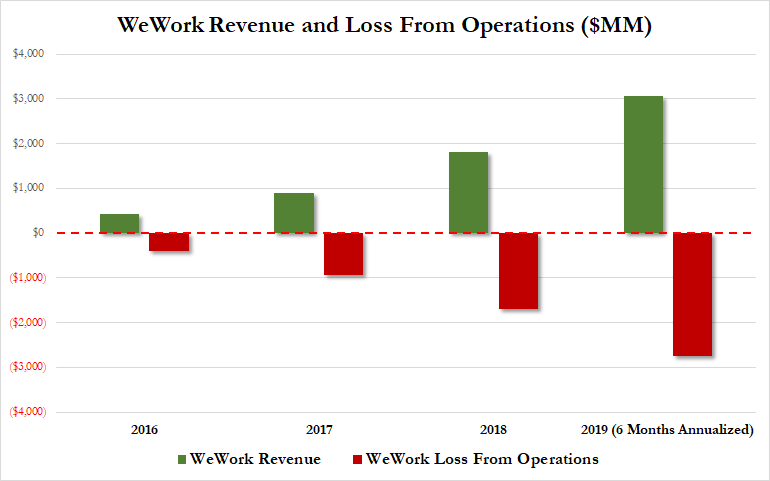

c)This is a disaster waiting to happen: The We work IPO is targeting a 20 to 30 billion dollar valuation a huge discount from the latest round(zerohedge)

iv) Swamp commentaries)

i)This should be interesting: Nunes files a civil lawsuit against Fusion stating that they were behind the smearing of his name with the purpose to obstruct justice and detail his investigation. I would love to be a fly on the wall during their discoveries

(Sara Carter)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 3 kilobar entries

total gold withdrawals; 1060.67 oz 33 kilobars

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 190,757 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 162,554 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 162,554 CONTRACTS EQUATES to 812 million OZ 116% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.09% ((SEPT 5/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.45% to NAV (SEPT 5/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -2.09%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.46 TRADING 15.01/DISCOUNT 3.00

END

And now the Gold inventory at the GLD/

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 5/2019/ Inventory rests tonight at 895.90 tonnes

*IN LAST 657 TRADING DAYS: 39.48 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 557- TRADING DAYS: A NET 127,17 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 5/2019:

Inventory 387.446 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.05/ and libor 6 month duration 1.99

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .06

XXXXXXXX

12 Month MM GOFO

+ 1.92%

LIBOR FOR 12 MONTH DURATION: 1.90

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.02

GOLD lease rates negative all the way out to one yr/gold is very tight

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold To $3,000/oz By End Of 2020 As The Dollar Will Fall Sharply – Ron Paul

◆ Where Does Gold Go From Here? — Ron Paul’s “Cautious” Prediction

◆ “Gold is an ‘insurance policy’ as the dollar will continue go down in value as it is printed” and it will end in a monetary “calamity”

◆ “Gold is not money due to any man-made laws. Gold is money despite man-made laws, and is a product of the voluntary marketplace”

◆ Ron Paul has a “cautious” and “modest” prediction for gold and encourages people to own physical gold not as a speculation but for savings and insurance purpose

News and Commentary

Gold slips as China-U.S. trade talk hopes lift risk appetite

LME’s Gold, Silver Contracts in Doubt as Societe Generale Pulls Out

Boris Johnson fails in pushing through snap election after Brexit delay bill passes

Dow futures jump more than 300 points as China says US agrees to meet for trade talks

China and US agree to now meet in October for trade negotiation

China will crumble ‘WHEN I WIN’ trade war – Trump

Alan Greenspan says it’s ‘only a matter of time’ before negative rates spread to the US

The next global currency likely will have gold backing – Ed Steer Interview

John Williams of Shadowstats Interviewed by GoldSeek Radio

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

04-Sep-19 1538.80 1546.10, 1265.05 1269.97 & 1397.69 1403.86

03-Sep-19 1532.45 1537.85, 1278.06 1277.80 & 1400.35 1403.44

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

28-Aug-19 1541.75 1537.15, 1263.31 1258.77 & 1389.89 1387.43

27-Aug-19 1531.85 1532.95, 1250.91 1247.51 & 1378.97 1380.88

26-Aug-19 UK Bank Holiday

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

A good interview of GATA board member Ed Steer

(Ed Steer/GATA/Goddard/HoweStreet.com)

In Howe Street interview, GATA’s Ed Steer surveys gold and silver markets

Submitted by cpowell on Wed, 2019-09-04 14:37. Section: Daily Dispatches

10:37a ET Wednesday, September 4, 2019

Dear Friend of GATA and Gold:

GATA board member Ed Steer, publisher of Ed Steer’s Gold & Silver Digest (https://edsteergoldsilver.com/), was interviewed a few days ago by Jim Goddard for HoweStreet.com.

Among other things, Steer said:

— “Seasonality” means nothing in rigged markets like those of gold and silver.

…

— The next global currency likely will have gold backing.

— Zero interest rates are coming to the United States and will boost the price of all real assets.

— Bullion banks are hugely shorting the current rallies in gold and silver but physical demand is increasing.

The interview is 16 minutes long and begins at the 38:53 mark here:

https://www.howestreet.com/2019/08/31/this-week-in-money-198/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

As I pointed out yesterday, are the rats fleeing a sinking ship:

Soc Generale flees the LBMA in their trading platform on gold and silver:

(courtesy Reuters/GATA)

Bullion banks on the run?

Submitted by cpowell on Wed, 2019-09-04 20:09. Section: Daily Dispatches

Reuters Exclusive: LME’s Gold, Silver Contracts in Doubt as Societe Generale Pulls Out

By Peter Hobson and Pratima Desai

Reuters

Wednesday, September 4, 2019

LONDON — The London Metal Exchange’s gold and silver futures are being thrown into doubt with the imminent resignation of Societe Generale as a market maker threatening to deepen a decline in trading activity, three sources said.

SocGen, one of five lenders that partnered with the LME to launch the contracts in 2017, is expected to resign shortly as a market maker, taking the number of banks committed to offering tradeable prices to two — Goldman Sachs and Morgan Stanley, the sources said.

That has triggered a discussion over the contracts’ future.

“There’s still commitment,” said one of the sources. But if volumes remain low, they added, “we’ll have to sit down and decide what is the next stage — exit, restructuring, or something else.” …

… For the remainder of the report:

https://www.reuters.com/article/us-lme-precious-gold-exclusive/exclusive…

iii) Other physical stories:

Rats fleeing a sinking ship?. Gold and silver rose immediately after this was announced.

(Hobson/Reuters)

Exclusive: LME’s gold, silver contracts in doubt as Societe Generale pulls out

LONDON (Reuters) – The London Metal Exchange’s gold and silver futures are being thrown into doubt, with the imminent resignation of Societe Generale as a market maker threatening to deepen a decline in trading activity, three sources said.

SocGen, one of five lenders that partnered with the LME to launch the contracts in 2017, is expected to resign shortly as a market maker, taking the number of banks committed to offering tradeable prices to two — Goldman Sachs and Morgan Stanley, the sources said.

That has triggered a discussion over the contracts’ future.

“There’s still commitment,” said one of the sources. But if volumes remain low, they added, “we’ll have to sit down and decide what is the next stage — exit, restructuring, or something else.”

The LME bet that the contracts would benefit from tightening regulation pushing some of London’s $10 trillion-a-year gold market from over-the-counter (OTC) deals between banks and brokers to centrally cleared exchanges.

To drive activity, it took the unusual step of cutting a deal with partners to share revenue in return for commitments to trade.

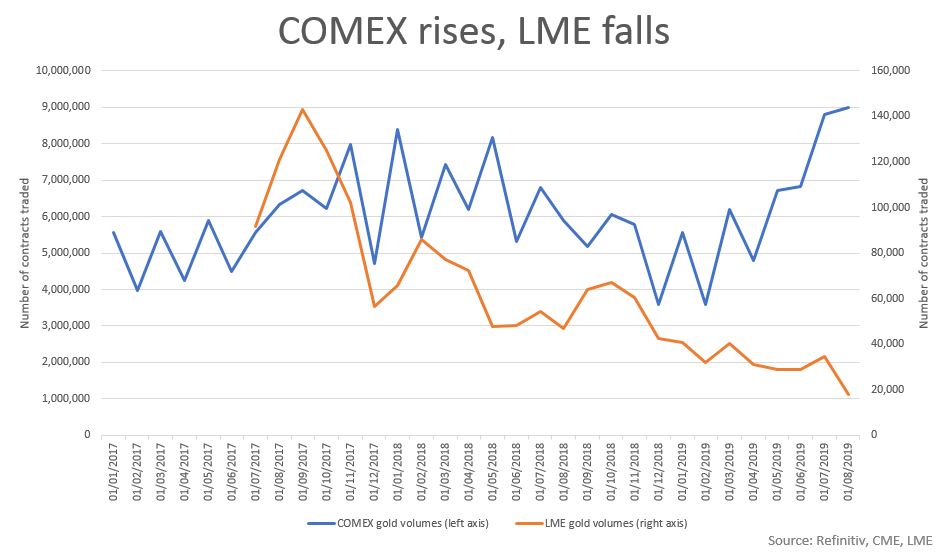

But even as a surge in gold prices this year pushes trading on CME Group’s New York COMEX market and the Shanghai Gold Exchange to record levels, turnover on the LME’s contracts, known as LMEprecious, has dropped.

SocGen declined to comment. The French bank earlier this year announced it would exit over-the-counter (OTC) commodities trading as part of a push to improve profitability, but did not say it would close on-exchange business.

The LME said in a statement: “We are committed – with the support of our existing participants – to overcoming current challenges in order to achieve our original ambition.”

“We already have a new market participant program for clients, along with a number of initiatives in the pipeline to support broader participation in the LME precious contracts,” it added.

The other banks partnered with the LME — Goldman, Morgan Stanley, Natixis and ICBC Standard — either declined to comment or did not respond to a request for comment.

The World Gold Council, another backer of the LME’s contracts, said it “supports all efforts which promote a transparent gold market that meets the needs of market participants.”

Proprietary trader OSTC, also a partner, said it remained fully committed to the LMEprecious project.

Fewer than 18,000 LME gold contracts changed hands in August – the lowest monthly total on record and an eighth of the number traded in its heyday of September 2017.

(Graphic: LME gold trading activity vs price link: here)

Volumes on COMEX, by contrast, hit a monthly record of 9 million contracts, up from around 6.7 million in September 2017. Turnover of the most traded contract on the Shanghai gold exchange and in the London OTC market has also leaped.

ADVERTISEMENT

(Graphic: COMEX gold volumes vs LME gold volumes link: here).

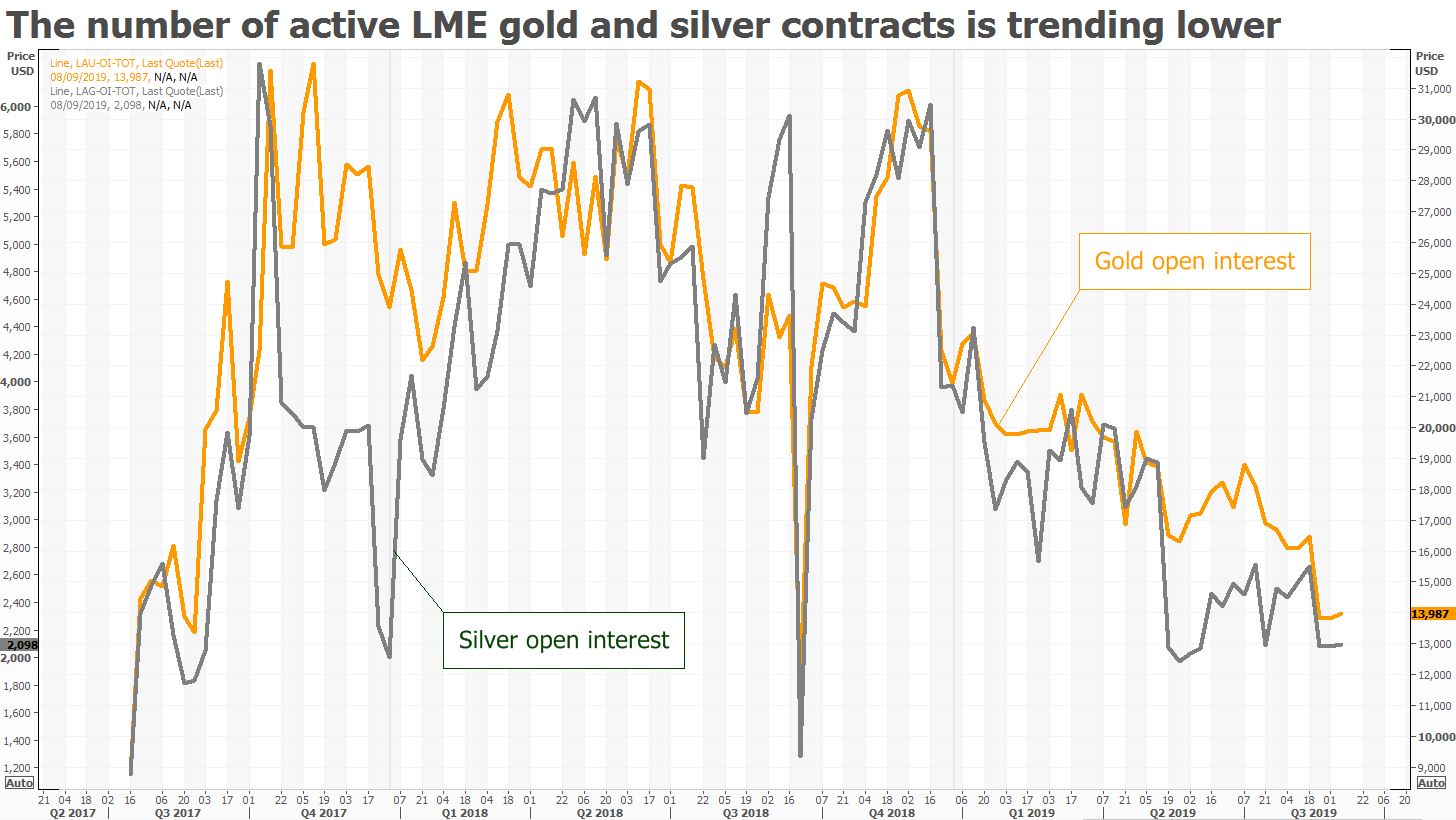

The number of open contracts in LME gold has meanwhile slumped to below 14,000 from a peak above 30,000 in 2017. In silver it is 2,098, a fraction of the near-7,000 achieved two years ago.

(Graphic: Open interest in LME gold and silver link: here).

London is the world’s biggest OTC gold trading hub, managing buy and sell orders from all over the world. But the biggest players, including JPMorgan and HSBC, have not joined LMEprecious.

At least one large newcomer is preparing to join, two sources said. They declined to say who this was, but said it should lift volumes.

Previous additions such as Commerzbank, ED&F Man and Marex Financial have however failed to provide significant boosts. Neither have incentives such as fee rebates and subscription fee waivers.

ADVERTISEMENT

The LME says traders can reduce their costs by using its contracts to put positions on the exchange.

Its partners may have saved by doing this, but the company they set up to invest in the LME’s contracts, EOS Precious Metals, has only lost money – almost $800,000 as of the end-2018, documents on Britain’s Companies House database show.

“Not enough is happening,” said a source at one of the banks backing LMEprecious. “If things go on as they are, at some point we’ll have to stop.”

The LME is owned by Hong Kong Exchanges and Clearing Ltd.

end

Just in case you missed Nicholas’ masterpiece from yesterday, I am repeating it:

(courtesy Nicholas Biezanek)

GARGANTUAN PAPER PRECIOUS METAL FRAUD

NOW IN PLAIN SIGHT ON MANY FRONTS

Nicholas Biezanek

An irate London motorist asked an Irish meter maid why she had issued a parking violation. She replied “you cannot park at allon a single yellow line”. The motorist then asked as to the purpose of a double yellow line. She replied “you cannot park at all at all on a double yellow line”. Harvey Organ has been warning for a long time that there is virtually no precious metal at allin the COMEX depositories. If we look at some recent data, I think we can upgrade this warning to “there is no physical goldat allin the COMEX depositories”.

The CME issues daily updates on the status of gold and silver stored in its depositories. This data is not archived, so one must not miss a single daily download if a complete record is desired. I read about the filing of notices and the number of contracts standing for delivery and the number of contracts stopped, but that data tends to be fragmented and disparate and moreover, based on the revelations below, totally fictional. I then decided from 12thJuly 2019 to analyze these CME daily reports to see what the result would look like. Here is a summary of withdrawals from the CME USA depositories: (this summary involves no less than 78 daily CME data files).

-

12thJuly to 31 stJuly 2019

1stAugust to 31stAug 2019

Registered Gold

NIL

NIL

Registered Silver

NIL

NIL

Eligible Gold

0.09 tonnes

0.241 tonnes

Eligible Silver

2,357,813 troy ounces

8,736,111 troy ounces

August 2019 was a designated active delivery month for gold and yet there was NO delivery whatsoever of any physical gold from the registered categories at the COMEX (the only category, per contract law, from which trading commitments can be executed).This is hardly surprising considering that the registered inventory in both gold and silver is no more (less in the case of silver) than 1% of the open interest (details are provided below) What more evidence is needed that these depositories are taking more than unsustainable strain? The one and only COMEX ‘delivery’ game in play, therefore, is comprised of transactions styled as ‘EFP’s (refer below), and no one has any even remote visibility as to what is involved in these gargantuan yet totally opaque transfers. Indeed one could possibly assume that the CME releases these daily reports hoping that the reader will assume that withdrawals of gold/silver do occur in the registered category, but just not today. All it takes, however, is the daily discipline to download and save these reports to ascertain the true picture. David Jensen recently stated that only 0.04% of gold contracts in NY were settled by physical delivery; it would now seem (no, not ‘seem’ ,rather it is proven) that NIL is the new norm, irrespective of any fine words about the delivery side of the COMEX in daily action.

No wonder that every single CME report contains this disclaimer:

|

The information in this report is taken from sources believed to be reliable; however, |

|

the Commodity Exchange, Inc. disclaims all liability whatsoever with regard to its accuracy or completeness. |

|

This report is produced for information purposes only. ( Author’s comment-what makes the weekly COT report immune from such dire ‘health warnings’?) (There was no movement at all in this period relating to the JP Morgan combined silver inventory of 153.7 million ounces. This inventory is the subject of much commentary, but, in the grand scheme of things, is a bit less than three months global mine supply (excluding Russia and China) and so is not that material-have a look at the total silver EFP volumes below to contextualize the figures ) |

Let us now review what little LBMA data is disseminated (90 days in arrears). Here is the profile of month end loco London vault holdings as up to date as possible. The December 2017/January 2018 profile is included since Harvey Organ has recorded the particulars of all reported EFP transfers from 1stJanuary 2018 onwards – tens of thousands of tonnes of these EFPs and virtually no meaningful impact on this profile:

There are several ETF funds in addition to GLD/SLV which warehouse their gold in loco London, so the net residual gold at the LBMA is quite a bit less than the figure computed above, but what would be the point of meticulous further microscopic analysis of historic data that is virtually useless in these days of real time utilization of information. Anyway, it is always assumed that just because shares are purchased in an ETF, then it follows that a commensurate increase in that ETF’s holding of physical gold/silver, as mandated in its prospectus, will automatically and instantaneously follow. That is a totally unwarranted assumption . At least the CME data enables an analysis of the full picture of August 2019 withdrawals by 2ndSeptember, or just one day later because of Labour Day. Also the UK’s own gold reserves are only 310 tonnes, so it would be a bit naïve to believe that the total gold in the BOE vaults (segregated in the above table) has not been impaired by BIS swap transactions (which the BIS freely acknowledges it instigates- from where else would the BIS source its ammunition?)

It is manifestly obvious that the core holdings of precious metal at the LBMA are permanently constrained within very restricted parameters, and hence the only physical gold/silver metal that leaves these loco London vaults is virtually equivalent to any inflows. The claims of the LBMA to stratospheric trading volumes merely relate to propaganda associated with the churning of undeliverable paper contracts in a zero sum game. But anyway this dribbling of delayed historic information is no more than disinformation in the absence of any details at all in respect of the true totality of all claims on this LBMA vaulted physical gold/silver; the only certainty is that such claims are many multiples of the available metal.This is not surprising given that the ongoing alleged viability of the entire global financial system is now predicated on the inexorable crescendo of criminal fractional reserving practices, uber rehypothecation and the Ponzi scheme embodied in the unbridled proliferation of sovereign debt.

The COMEX, on a daily basis now, serially engineers Exchange for Physical (EFP) transfers over to the LBMA, so that the open interest does not go stratospheric .Let us, however, first refresh our minds in respect of the open interest farce:

-

Open Interest (o/i) at 31st August 2019

Gold(Tonnes)

Silver (000,000 ozs)

Total o/i

1,925

1,121

Registered Inv.

24

9

o/i Cover

1.225%

0.779%

Eligible inv.

236

230

Total Comex Inv.

259

239

o/i Cover

13.464%

21.288%

Since 1stJanuary 2018 (but certainly in existence prior to this date) the volume of EFP transfers until 31stAugust 2019 is as follows (data from Harvey Organ):

-

Gold (Tonnes)

Silver (000,000 ozs)

1st Jan 2018 to 31st Dec 2018 7,310

2,847

To 31st August 2019 4,151

1,550

Total for 20 months 11,461

4,397

20 months EFPs/Global Annual Mine Production About 4.5 years

About 6 years

The criminals have now abusively over utilized these EFPs on a daily basis to such an extent that it is manifestly obvious today that the term ‘physical’ has been high jacked in the false and misleading nomenclature attributable to this manipulative charade. These EFP volumes are of such magnitude that the only certainty is that absolutely no physical metal is involved. Annual global mine supply (ex Russia/ China) is about 200 tonnes per month in the case of gold and about 55 (could be 60) million ounces of silver per month.

My personal interpretation of the LBMA market is as follows:

Unallocated accounts: this is a transaction whereby a fiat ‘loan’ is made to an LBMA principal, and the transaction can be redeemed by accepting a fiat settlement only, priced on the current manipulated paper price of gold/silver ,but certainly no physical metal is involved at all.

EFP transfers from COMEX TO LBMA: even if the terms of the underlying agreements are ‘ad hoc’ and not standardized (who knows?), the liability for delivery is assumed by an LBMA principal, who cannot possibly deliver ,so the counter party exacts ‘special/onerous’ terms as incentivization for not demanding physical delivery. Please refer to Harvey Organ re the ‘conspiracy to defraud’ embodied in the (non) reporting to the regulator by the banks in respect of these liabilities styled as “serial forward contract obligations under 14 days “

Allocated accounts: this is a transaction whereby a congenital idiot labours under the delusion that his fully funded and numbered .995 finesse gold bars are available for delivery on demand, whereas these bars have long ago been re-refined to .9999 finesse and shipped eastwards (aka re-hypothecation-‘‘you lose , you get nothing ,good day sir “.) GATA and others have referred to numerous examples of such “failures to deliver”.

It was inevitable that the meagre physical inventory at the COMEX would become (indeed has long ago become) totally inadequate to satisfy demand for physical delivery but any crisis of failure to deliver has been temporarily suppressed by the creation of all these EFP transfers. The form of these EFP contracts is unknown as is the identity and intentions of the counterparties. The EFP volumes recorded above embody an orgy of excess that has completely shredded any pretext of ultimate deliverability and yet the regulators refuse to even acknowledge that any query merits the dignity of an acknowledgement, let alone a response. When does all this insanity reach a denouement? Perhaps the success hitherto in suppressing the gold price became a catalyst for the hubris of consigning positive interest rates to the dustbin of history and the euphoric philosophy that the limitless proliferation of sovereign debt need no longer be constrained in the absence of any associated interest burden. China and Russia have accumulated possibly as much as 30,000 tonnes of physical gold each (unless you have personally audited the extensive network of vaults under the Kremlin and microscopically performed the calculus relating to Chinese gold importation and domestic production over the years, any contra opinion you may hold is as weighty as a dandelion blowing in the wind). The end game is easy to forecast and the headline price of gold will not be set for ever by the frantic supply of gargantuan volumes of undeliverable naked short and fraudulent paper promises. Whilst the BOE governor (a Canadian from a country that has disposed of all its gold reserves) recently, at Jackson Hole, made suggestions about creating a hermetic cyber seal to encapsulate fiat digital ‘air’ to create an alternative to the fiat US$ as a reserve currency, the new One Belt One Roadtrading bloc (eventually encompassing more than two thirds of the global population) will indeed re instate an alternative, and it could not be more obvious that it will incorporate a gold standard. The pure unadulterated insanity of Western Modern Monetary Theory (MMT) is a wonderful encapsulation of the immortal words of Tacitus; “those whom the Gods wish to destroy they first make mad”.

Post script: GATA has been in existence for at least two decades, and I have been a member for about 15 years. Initially the seminal work of Frank Veneroso heavily influenced GATA’s early writings, and Veneroso estimated that the manipulation of the physical gold price via swaps/loans/leases etc. would ‘hit a brick wall’ between 2011 and 2013 as physical metal supply dried up. Obviously the manipulators managed to engineer even more suppressive techniques than were factored into computations back in the ‘eighties’. Limitless, naked short, undeliverable, fraudulent paper gold promises aided by incessant MSM propaganda and infinite CB fiat resources and CME/LBMA accommodation and regulatory complicity proved to be a bit more overwhelming and formidable than initial forecasts. August 2019 has witnessed the decimation of some serious and well established chart resistance levels in respect of the precious metals; GATA has been predicting for about a decade such price action (aka a commercial signal failure) that eventually will culminate in a price ‘moon shot’ as the physical market assumes its rightful hegemony . Some commentators outside GATA have even estimated that the fractional reserving of paper promises to available physical gold/silver could even be in a ratio of up to 500/1.

end

Are the boys still engaging in spoofing despite their criminal guilty plea?? You can bet the farm that they are

(courtesy Chris Marcus/Arcadia Economics)

Arcadia Economics

Was The August 13th Gold And Silver Plunge A JP Morgan “Spoof”?

September 4, 2019

There have been more recent arrests by the Department of Justice in their precious metals investigation. And when you consider the timeline, it’s interesting to wonder whether JP Morgan or other banks are actually continuing to “spoof” and manipulate the price of gold and silver. Even while they’re simultaneously being investigated and having their employees arrested!

Christian Trunz was working as an executive director at J.P. Morgan up until August 20th when he “pleaded guilty to criminal charges of manipulating the precious metals markets for nine years”.

The CNBC article by Dawn Giel also mentioned that like the other 2 traders who have already pleaded guilty to “spoofing the market” (one is a former JP Morgan employee, and the other worked for Scotia Capital and Bear Stearns – which was taken over by JP Morgan), he “admitted learning the illegal trading tactics from senior traders at the bank and to using those tactics with the knowledge and consent of supervisors.”

All three of the articles about the arrests mention that it was a widespread practice at the traders’ firms, and that it was done with the knowledge of their supervisors. So this wasn’t just some rogue junior traders. This was being condoned from a higher level. And given that Trunz was actually still working at JP Morgan when he was arrested, was he, his colleagues, his supervisors, or his peers at some of these other banks responsible for what happened to the silver and gold prices only a week earlier on August 13?

When the price of both metals spiked downward, at the exact same time, on no known news or fundamentals that I, or any of the other silver experts that I regularly interview on my show have been able to identify.

(chart courtesy of kitco.com)

(chart courtesy of kitco.com)

Now if you’re wondering what “spoofing” actually means, the article mentions that “in his guilty plea, Trunz admitted that from approximately July 2007 and August 2016 he placed thousands of orders that he did not intent to execute for gold, silver, platinum and palladium futures contracts.”

In one of the other cases, “Corey Flaum (the former Scotia Bank and Bear Stearns trader) during his guilty plea admitted that from approximately June 2007 and July 2016 he placed thousands of orders to manipulate the prices of gold, silver, platinum and palladium futures contracts according to the Justice Department.”

So they were placing trades they didn’t intend on executing in order to manipulate the price. Which former CFTC commissioner Bart Chilton, who oversaw the agency’s investigation into silver manipulation, also elaborated further on in the interview I did with him earlier this year.

Chris Marcus: You mentioned spoofing. And I’m curious, because my understanding of how some of the manipulation has occurred is that if silver is trading $20.05, there are a lot of stop orders placed around the $20 handle. And often, if the price can get pushed a little bit, then you get a lot of those high frequency algorithms kicking in, and you see a drop, with many feeling that the people nudging the price a little, are the same ones buying it back lower.

Does that sound like a reasonably accurate portrayal to put it in perspective for folks? Or would you phrase it differently?

Bart Chilton: Well, it’s a good portrayal. Actually, it’s a very good portrayal.

But it’s actually also a reflection of what I was just speaking about. How trading has changed. Even back in 2008, 2009, 2010, and maybe a little bit of 2011, even when a lot of these silver trades, and some gold trades were pretty suspect, when you were looking at them, you didn’t have high frequency traders in these markets like you do today.

The difference in your description is that today, when a market moves because of a spoof, it could move a lot more.

So while I don’t have access to the trading records that the CFTC and the DOJ have (although if you’d like to send them or your local Congressional representatives this article by all means go ahead), what happened on August 13th sure seems to match what Bart and the guilty pleas describe.

Additionally, the guilty pleas mention that the specific instances they were confessing to occurred between 2007-2016. Which is really the time when this started becoming more blatant. Hopefully the CFTC or DOJ will comment soon. Because exactly what they describe as the violation that the traders are getting arrested for appears to be continuing to occur. As they’re getting arrested!

Each article also mentions that the defendants “are also cooperating with federal prosecutors in ongoing probes of major banks.” And that “the Justice Department is conducting multiple criminal investigations into big banks with the cooperation of traders who have pleaded guilty to spoofing-related crimes.”

Which JP Morgan has even mentioned in the legal section of one of their financial disclosures: “Various authorities, including the Department of Justice’s Criminal Division, are conducting investigations relating to trading practices in the precious metals markets and related conduct. The Firm is responding to and cooperating with these investigations.”

It will be interesting to see how the case unfolds, because at the same time the manipulation is becoming more public knowledge, the market is also rallying. Which means that many of these same banks who have been short the market are currently losing money on their positions. At the same time some of them are being investigated (Scotia appears to be on the verge of exiting the market). And the central banks are getting ready to start QE again.

As always, if you have any questions about this article you can email me here. And to stay updated on the case, just subscribe to future Arcadia updates in the box below.

Chris Marcus

September 4, 2019

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Global Stocks, US Futures Surge As China, US Set To Restart Trade Talks

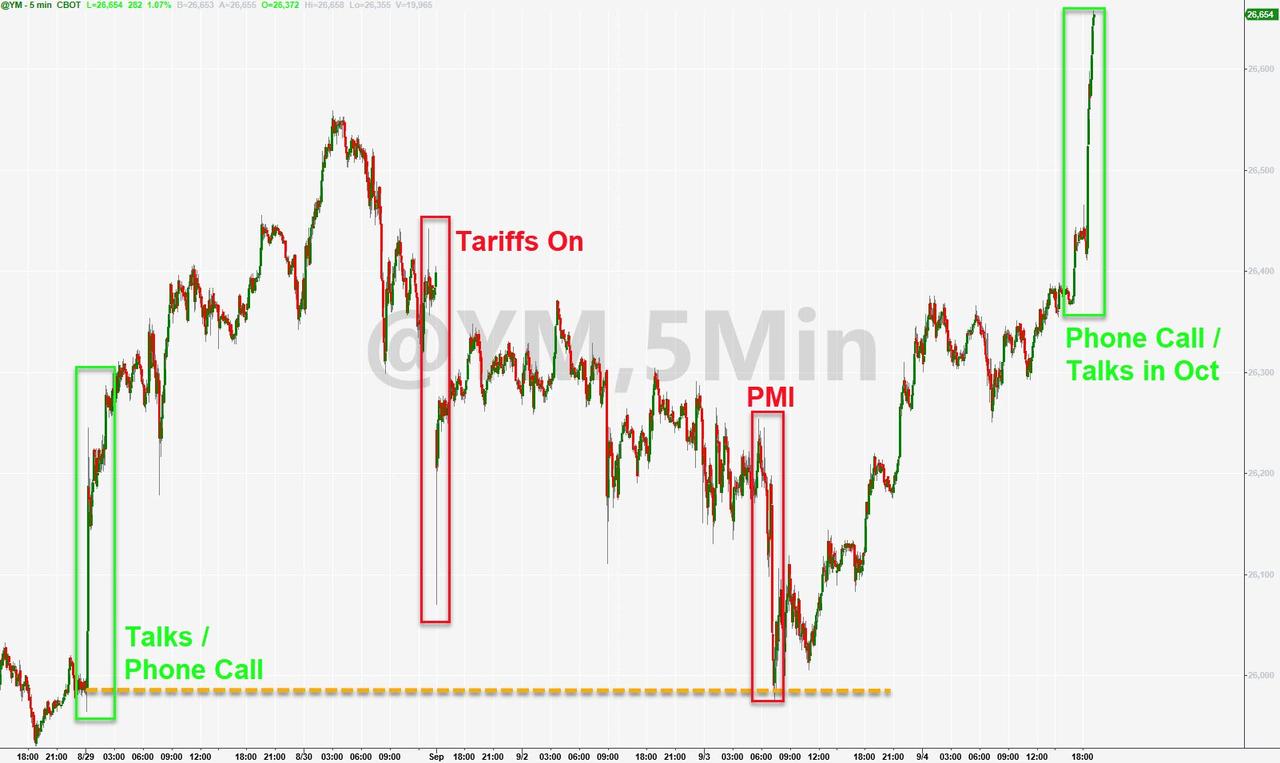

In a world where every single trading day’s mood is set by the latest trade war news, headlines, rumors and innunedo, it should come as no surprise that following news that the US and China are set to agreed to restart high-level trade talks in early October in Washington, that global stocks and US equity futures will be another sea of green, with the S&P jumping 26 point and now just 2% below its all time highs.

The latest round of talks, which was announced just 4 days after even higher tariffs were slapped on US and Chinese goods, was agreed to in a phone call between Chinese Vice Premier Liu He and USTR Robert Lighthizer and U.S. Treasury Secretary Steven Mnuchin, China’s commerce ministry said in a statement on its website. China’s central bank governor Yi Gang was also on the call.

“Both sides agreed that they should work together and take practical actions to create good conditions for consultations,” the ministry said. “Lead negotiators from both sides had a really good phone call this morning,” ministry spokesman Gao Feng said in a weekly briefing. “We’ll strive to achieve substantial progress during the 13th Sino-U.S. high-level negotiations in early October.”

The glimmer of hope in the global trade war – officials from the U.S. and China had been struggling to agree on new talks – added to a broad risk-on mood that took hold Wednesday, when British lawmakers moved to block an imminent no-deal Brexit and Hong Kong’s leader sought to quell unrest in Asia’s key financial hub. Focus will now shift to remarks from Fed Chair Jerome Powell and the latest U.S. jobs report, both due Friday, amid expectations for further monetary easing.

While it is virtually certain that nothing tangible will emerge from this latest attempt at de-escalation, which is meant to calm the popular mood around China’s October 1 National Day holiday, it was predictably sufficient to boost algo trading optimism and sent stocks sharply higher around the globe.

Indeed, news of the early October talks lifted most Asian share markets on Thursday, raising hopes these can de-escalate the U.S.-China trade war before it inflicts further damage on the global economy. Asian stocks climbed, led by technology firms and material producers. Almost all markets in the region were up, with Japan leading gains. The Topix jumped 1.8% for its biggest gain since July 19, as electronics firms and machinery makers advanced. The Shanghai Composite Index rose 1%, buoyed by large insurers and banks, while Hong Kong’s Hang Seng Index closed little changed following a 3.9% rally on Wednesday. China’s cabinet signaled further monetary easing to counter economic headwinds. India’s Sensex dropped 0.1% as investors assessed waning economic growth

European stocks followed Asia’s lead, pushing higher on renewed trade optimism as China and the U.S. are set resume talks next month. The Stoxx Euro

pe 600 Index rose for a second day, led by technology, autos and industrials, with every major national benchmark except the U.K.’s FTSE 100 in the green and carmakers setting the pace. Traders ignored the latest batch of dismal German economic data, which saw German industrial orders fell more than expected in July on weak demand from abroad, suggesting that struggling manufacturers could tip Europe’s biggest economy into a recession in the third quarter. Orders for “Made in Germany” goods were down 2.7% from the previous month in July, driven by a big drop in bookings from non-euro zone countries. Consensus had expected a -1.5% drop. The June reading was revised up to an increase of 2.7 from a previously reported 2.5% increase.

“The misery in manufacturing continues. The decline in new orders significantly increases the risk of a recession for the German economy,” VP Bank analyst Thomas Gitzel said. “The danger is great that negative growth will also be recorded in the third quarter,” Gitzel added, eyeing the possibility of a technical recession after German GDP contracted by -0.1% in Q2, with Q3 GDP now widely expected to shrink as well.

Bond yields rose across most curves, with 10-yr bund and UST yields rising 3bps and 5bps, respectively. European yields curves steepened across the board as investors take heed of the doubters in the European Central Bank over a fresh package of quantitative easing.China’s government bonds advanced as sentiment got a boost from Beijing’s call for monetary easing and inclusion in a major global index. The yield on 10-year sovereign bonds fell 3 basis points to 3.02%, the lowest since Aug. 15. China’s cabinet has called for the “timely” use of tools such as reserve-ratio cuts to support the economy. Adding to the optimism, JPMorgan said it will include some onshore bonds into its benchmark emerging-market indexes, a move that would spur capital inflows. Meanwhile, traders are bracing for a PBOC cut in the RRR: “China is starting a new round of easing,” said Ming Ming, head of fixed-income research at Citic, adding the 10-year government yield could fall toward 2.8%. “The central bank will likely reduce broad RRR and also ease in a targeted manner to support smaller companies. We also can’t rule out a cut to interest rates.”

In FX, the pound added to Wednesday’s big gains following Parliament’s move to block both a no-deal exit from the European Union and an early British election. The dollar fell for a third day, sliding 0.1% lower, while the euro edged higher despite disappointing factory data in Germany. The SEK lead G-10 gains after the country’s central bank defied expectations it would turn more dovish, sticking with its plan to withdraw stimulus from the biggest Nordic economy.

Elsewhere, West Texas oil fluctuated. Florida orange groves seemingly escaped major damage from Hurricane Dorian, but concern is now turning to soy, corn and cotton fields as well as livestock in Georgia and the Carolinas as the storm churns northward.

Today, US investors will look forward to several big data points, including Challenger job cuts, jobless claims and services

Market Snapshot

- S&P 500 futures up 0.8% to 2,962.25

- STOXX Europe 600 up 0.5% to 385.24

- MXAP up 1.1% to 155.32

- MXAPJ up 0.8% to 502.11

- Nikkei up 2.1% to 21,085.94

- Topix up 1.8% to 1,534.46

- Hang Seng Index down 0.03% to 26,515.53

- Shanghai Composite up 1% to 2,985.87

- Sensex down 0.4% to 36,593.44

- Australia S&P/ASX 200 up 0.9% to 6,613.17

- Kospi up 0.8% to 2,004.75

- German 10Y yield rose 2.7 bps to -0.647%

- Euro down 0.02% to $1.1033

- Brent Futures up 0.2% to $60.83/bbl

- Italian 10Y yield fell 6.3 bps to 0.472%

- Spanish 10Y yield rose 4.8 bps to 0.197%

- Gold spot down 0.7% to $1,541.85

- U.S. Dollar Index down 0.08% to 98.37

Top Overnight News from Bloomberg

- Boris Johnson was humiliated by Parliament for a second day running, with his do-or-die Brexit strategy derailed and even his plan for a general election rejected. But having bet everything on getting Britain out of the European Union by Oct. 31, he can’t back down.

- China and the U.S. announced that face- to-face negotiations aimed at ending their tariff war will be held in Washington in the coming weeks, amid skepticism on both sides that any substantive progress can be made.

- Hong Kong leader Carrie Lam said her decision to scrap extradition legislation was only the “first step” to addressing the city’s unrest, but resisted protesters’ calls to immediately meet the rest of their demand

- Mario Draghi’s bid to reactivate bond purchases in a final salvo of stimulus is being threatened by the biggest pushback on policy ever seen during his eight-year reign as European Central Bank president.

- German factory orders fell in July, aggravating an industrial slump that has pushed Europe’s largest economy to the brink of recession. Demand fell 2.7% from June, when it rose at the same pace, as orders from outside the euro region plunged

Asian equity markets traded higher across the board as the region took impetus from the upside in global peers after dovish Fed rhetoric and positive developments in Hong Kong in which the extradition bill was fully withdrawn, while US-China trade hopes exacerbated the gains after the sides agreed to hold talks in Washington early next month. ASX 200 (+0.9%) and Nikkei 225 (+2.1%) were boosted by the trade developments and with the energy sector frontrunning the gains in Australia due to the recent advances in oil prices, while exporter names in Tokyo benefitted from a weaker currency. Hang Seng (U/C) and Shanghai Comp. (+1.0%) conformed to the heightened risk appetite after the phone call between China’s Vice Premier Liu He with US Treasury Secretary Mnuchin and USTR Lighthizer in which the sides also agreed on trade consultations mid-September ahead of next month’s talks and will take action to create good conditions for the consultations. Furthermore, expectations of PBoC easing after China’s Cabinet announced it will implement RRR reductions ‘in time’ have added to the optimism, although the advances in Hong Kong were restricted considering its benchmark had already surged just shy of 1000 points or a near-4% gain yesterday due to the extradition bill withdrawal. Finally, 10yr JGBs briefly slipped below the 155.00 level amid pressure across global bond futures triggered by the US-China trade talk announcement, although prices later nursed some of the losses after a mostly firmer than previous 30yr JGB auction.

Top Asian News

- Thailand’s Death Toll From Tropical Storms, Floods Rises to 16

- Singapore’s CXA Says Seeking $50 Million in New Funding Round

- China Strongly Opposes Escalation of Trade War, Gao Says

- Indonesia Allows Miners to Add Export Quotas; Nickel Tumbles

A positive session thus far for most of the major European bourses [Eurostoxx 50 +0.8%] as the region follows suit from a mostly positive Asia-Pac session as trade optimism bolstered sentiment after China’s Mofcom announced a US/China meeting in Washington next month, although an explicit date has not been reported. UK’s FTSE 100 (-0.7%) is the laggard and has slipped further due to a strengthening GBP after UK PM Johnson received a double whammy with UK Parliament voting to pass the bill to delay Brexit and defeated the PM’s bid for snap elections. Sectors are mixed with the IT sector the clear outperformer as chip names rally on US-China optimism; meanwhile defensive sectors are in the red amid the risk appetite. In terms of individual movers, Equinor (+7.9%) shares spiked higher after the Co. began a USD 5bln share buyback programme which is to be completed at the end of 2020. Elsewhere, Safran (+6.1%) and Melrose (+6.3%) rose on the back of earnings. On the flip side, William Hill (-1.7%) shares opened lower following on from the resignation of its CEO.

Top European News