GOLD:$1508.00 DOWN $9.80 (COMEX TO COMEX CLOSING)

Silver:$18.15 DOWN 60 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1507.00

silver: $18.16

You could tell that the bankers were dead set on whacking gold and silver. On onslaught started last night proceeded to knock gold down to 1503.00 and silver to 18.03..then the jobs report and that took the wind out of the sails of our crooked bankers. But rest assured it is Friday and a 1 pm est with London safely put to bed they raided again on stupid comments from Powell. Actually they were very bullish for gold and silver as it looks that he is set to lower rates in Sept. As I promised you, we will be zero bound in USA terms shortly.

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 8/13

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,515.400000000 USD

INTENT DATE: 09/05/2019 DELIVERY DATE: 09/09/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 2

661 H JP MORGAN 8

737 C ADVANTAGE 4 3

905 C ADM 9

____________________________________________________________________________________________

TOTAL: 13 13

MONTH TO DATE: 1,626

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 13 NOTICE(S) FOR 1300 OZ (0.0404 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1626 NOTICES FOR 162600 OZ (5.0575 TONNES)

SILVER

FOR SEPT

276 NOTICE(S) FILED TODAY FOR 1,380,000 OZ/

total number of notices filed so far this month: 6786 for 33,930,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10815 UP 246

Bitcoin: FINAL EVENING TRADE: $ 10,429 DOWN 203

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A HUGE SIZED 6304 CONTRACTS FROM 222,986 DOWN TO 216,682 WITH THE 68 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0, FOR DEC: 3637 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 3637 CONTRACTS. WITH THE TRANSFER OF 3637 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3637 EFP CONTRACTS TRANSLATES INTO 18.19 MILLION OZ ACCOMPANYING:

1.THE 68 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

38.020 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD NO DOUBT CONSIDERABLE COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY WITH THE HUGE RAID ORCHESTRATED BY THE CROOKED BANKERS. HOWEVER THE LOSS IN TOTAL OI WAS MUCH SMALLER THAN I HAD EXPECTED WITH A 68 CENT DRUBBING IN PRICE.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

11,593 CONTRACTS (FOR 4 TRADING DAYS TOTAL 11,593 CONTRACTS) OR 57.97 MILLION OZ: (AVERAGE PER DAY: 2898 CONTRACTS OR 14.490 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 57.97 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 8.28% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1607.68 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6304, WITH THE 68 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 3637 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A STRONG SIZED: 2667 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 3637 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 6304 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 68 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.75 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.083 BILLION OZ TO BE EXACT or 155% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 276 NOTICE(S) FOR 1,380,000, OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 38.020 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

IN GOLD, THE COMEX OPEN INTEREST FELL BY AN ATMOSPHERIC AND CRIMINALLY SIZED 25,323 CONTRACTS, TO 618,240 ACCOMPANYING THE HUGE $33.80 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 15,860 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 15,860 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 621,535,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALLER SIZE LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES THAN EXPECTED: 9463 CONTRACTS: OF WHICH 25,323 CONTRACTS DECREASED AT THE COMEX AND 15,860 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 9463 CONTRACTS OR 946,300 OZ OR 29.43 TONNES. YESTERDAY WE HAD A LOSS OF $33.80 IN GOLD TRADING....AND WITH THAT LOSS IN PRICE, WE HAD A SMALLER THAN EXPECTED LOSS IN GOLD TONNAGE OF 29.43 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS OVER 9 BILLION DOLLARS WORTH OF GOLD SHORTS WERE CALLED UPON TO WHACK OUR PRECIOUS METAL TO KINGDOM COME. FROM THE DATA THE BANKERS KNOCKED OUT THE OPEN INTEREST AT THE COMEX BUT MOST OF THESE GUYS LANDED IN EFP’S AS THEY MORPHED INTO LONDON BASED FORWARDS AND RECEIVED A FIAT SPECIAL FOR ENGAGING IN THIS CRIMINAL ACTIVITY.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 40,372 CONTRACTS OR 4,037,200 oz OR 126.82 TONNES (4 TRADING DAY AND THUS AVERAGING: 10,093 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY IN TONNES: 126.82 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 126.82/3550 x 100% TONNES =3.57% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4276.69 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 25,323 WITH THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($33.80)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15,860 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15,860 EFP CONTRACTS ISSUED, WE HAD A SMALLER THAN EXPECTED SIZED LOSS OF 9463 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

15,860 CONTRACTS MOVE TO LONDON AND 25,323 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 29.43 TONNES). ..AND THIS HUGE DECREASE OF DEMAND OCCURRED WITH THE LOSS IN PRICE OF $33.80 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 13 notice(s) filed upon for 1300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD..

WITH GOLD DOWN $9.80 TODAY//(COMEX-TO COMEX)

A BIG CHANGE IN GOLD INVENTORY AT THE GLD//

A PAPER WITHDRAWAL OF 6.15 TONNES (AND NO DOUBT THIS WAS USED IN THE RAID)

INVENTORY RESTS AT 889.75 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 60 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV:

A WITHDRAWAL OF 842,000 OZ OF PAPER SILVER

/INVENTORY RESTS AT 386.604 MILLION OZ.

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUGE SIZED 6093 CONTRACTS from 222,986 DOWN TO 216,682 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; DEC: 3637 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3637 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 6093 CONTRACTS TO THE 3637 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALLER SIZED THAN EXPECTED LOSS OF 2667 OPEN INTEREST CONTRACTS.THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 13.34 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ//SEPT 2019: 37.020 MILLION OZ

RESULT: A GIGANTIC SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 68 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 3637 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 13.74 POINTS OR 0.46% //Hang Sang CLOSED UP 175.23 POINTS OR 0.66% /The Nikkei closed UP 113.63 POINTS OR 0.54%//Australia’s all ordinaires CLOSED UP .48%

/Chinese yuan (ONSHORE) closed UP at 7.1155 /Oil UP TO 55.31 dollars per barrel for WTI and 59.31 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 7.1155 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.1113 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)China

The Chinese economy is suffering pretty bad due to the tariffs and the global slowdown. Now China cuts its banking Reserve Ratio in an attempt to stimulate their economy.

(zerohedge)

ii)With a major part of the pig market in China destroyed by the Pig Ebola, Chinese demand for donkey meat is now threatening to wipe out stocks of this meat in Kenya

iii)An excellent commentary from Brandon Smith and the fallacies about the China/USA trade war. he explains what the globalists are up to.

4/EUROPEAN AFFAIRS

7. OIL ISSUES

8 EMERGING MARKET ISSUES

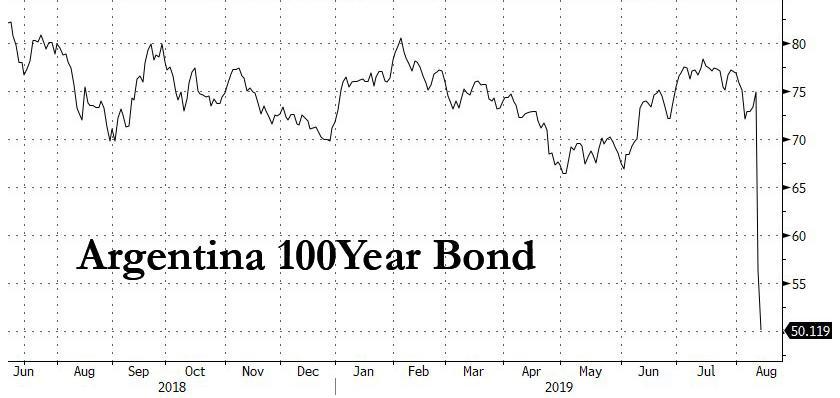

i)WHAT on earth was this guy smoking? Former Lehman hedge fund trader takes a one billion dollar loss betting on Argentinian bonds recovering. What a doorknob

(zerohedge)

ii)India

India’s auto sector has now come to a screeching halt as sales crash in August

(zerohedge)

9. PHYSICAL MARKETS

i)An excellent paper from Alasdair Macleod as he claims that in a downturn the USA dollar is more at risk than the yuan

(Alasdair Macleod)

the entire article is in the USA section of my commentary.

ii)BILL MURPHY interviewed by Chris Marcus

(courtesy Chris Marcus/GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

(zerohedge)

iii) Important USA Economic Stories

a must read…

(Alasdair MacLeod)

ii)Rabobank strategists are pretty good. Here is Phillip Mare//Senior uSA analyst at Rabobank

iv) Swamp commentaries)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

i) Into Brinks: 243,168.090 oz

ii) Into CNT 598,485.591 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 210,782 CONTRACTS //raid

CONFIRMED VOLUME FOR YESTERDAY: 202,135 CONTRACTS..//raid

YESTERDAY’S CONFIRMED VOLUME OF 202,135 CONTRACTS EQUATES to 1,0105 million OZ 144.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.46% ((SEPT 6/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.30% to NAV (SEPT 6/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -2.46%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.24 TRADING 14.77/DISCOUNT 3.10

END

And now the Gold inventory at the GLD/

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 6/2019/ Inventory rests tonight at 889.75 tonnes

*IN LAST 658 TRADING DAYS: 45.63 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 558- TRADING DAYS: A NET 121,02 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 6/2019:

Inventory 386.604 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.02/ and libor 6 month duration 1.99

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .03

XXXXXXXX

12 Month MM GOFO

+ 1.90%

LIBOR FOR 12 MONTH DURATION: 1.89

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = –.01

GOLD LEASE RATES NEGATIVE ALL THE WAY UP TO ONE YR

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold In Japan Reaches Highest Since 1980 – Surging Demand Results In Delays To Buy Gold

◆ Gold has reached its highest price in Japanese yen since 1980 at 165,045/oz (see charts below) as the yen depreciates amid “global economy jitters”

◆ A surge in demand in Japan is resulting in gold buyers needing to wait “2-3 hours to close deals” on gold bars according to Japan’s largest gold broker Tanaka Kikinzoku

◆ Gold is up 16% year to date in Japanese yen and near 40 year nominal highs due to concerns about the outlook for the yen, the Japanese and the global economy

◆ There is a “global hunt for the safe haven precious metal amid worries that the U.S.-China trade row could further depress the global economy” according to Reuters (see story below)

◆ Tokyo Commodity Exchange (TOCOM) gold futures have been surging since August and one commodity brokerage said Japanese speculators were taking profits at these levels

◆ Gold in dollars is down 1% and silver 0.4% this week after sharp falls yesterday; This follows gains earlier this week and strong gains over the summer which have made gold one of the best performing assets this year with gains of 18.4%

News and Commentary

Gold down 2.2% on China trade optimism, upbeat private-jobs data

Japan’s retail gold price clambers to highest since 1980 amid global economy jitters

Silver Rising in Value To $25/oz or $30/oz – Bloomberg Video

Fitch downgrades Hong Kong as city braces for more protests

China, HK stocks set for best week since June amid trade optimism

Former Zimbabwe president Robert Mugabe dead at 95

With tariffs eating into profits, some Asian companies are moving home

EU Bank Bosses Warn Of “Grave Consequences” If ECB Keeps Cutting Rates

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

05-Sep-19 1542.60 1529.10, 1257.06 1238.72 & 1397.44 1380.78

04-Sep-19 1538.80 1546.10, 1265.05 1269.97 & 1397.69 1403.86

03-Sep-19 1532.45 1537.85, 1278.06 1277.80 & 1400.35 1403.44

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

28-Aug-19 1541.75 1537.15, 1263.31 1258.77 & 1389.89 1387.43

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

An excellent paper from Alasdair Macleod as he claims that in a downturn the USA dollar is more at risk than the yuan

(Alasdair Macleod)

the entire article is in the USA section of my commentary.

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

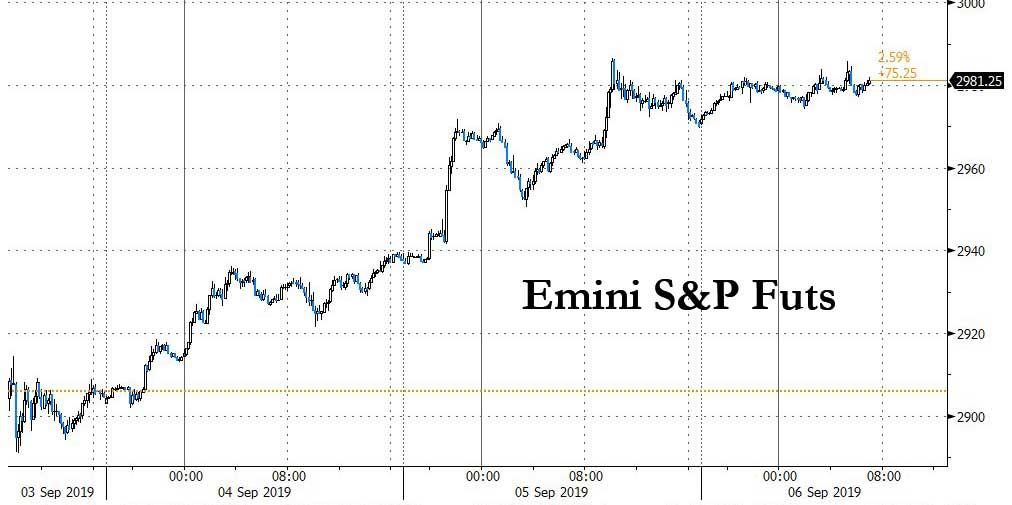

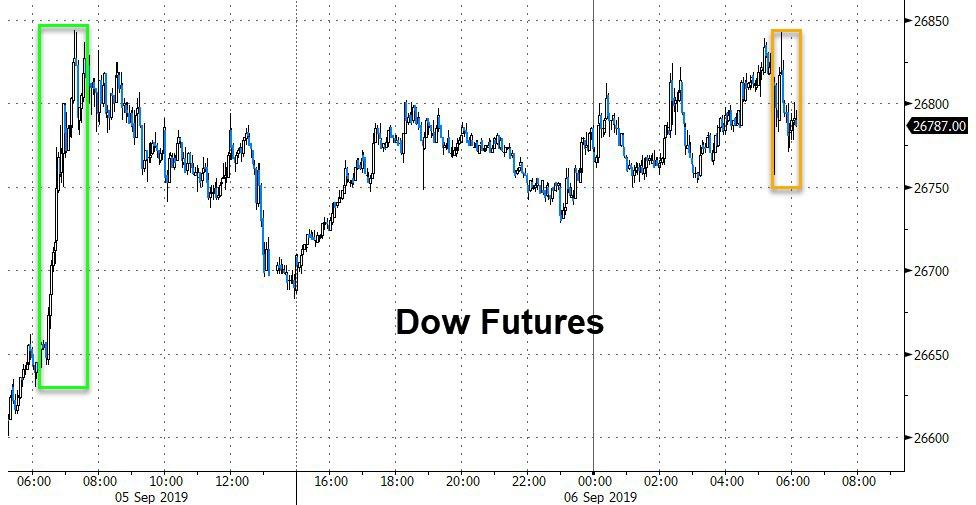

Futures Drift Higher Ahead Of Payrolls And Powell, Boosted By China Stimulus

US equity futures and global stocks were drifting rangebound ahead of today’s key payrolls data and Powell speech, when news of a targeted and broad RRR stimulus from China just after 5am ET helped cap a strong week for global markets while bond buyers and dollar dealers were patiently waiting for a major disappointment in today’s economic data after their first significant selloffs in months.

S&P 500 futures rose, pushing the broad US equity index to within 2% of its all-time high, although they have found some resistance just around 2,980, while Europe’s Stoxx 600 fluctuated, with automakers rising as energy shares fell on a drop in oil prices. Equities pared some gains after jumping briefly as China cut the amount of cash banks must hold as reserves, injecting liquidity into an economy facing headwinds to growth. The MSCI Asia Pacific Index headed for its biggest weekly advance since June.

After a roller-coaster week dominated by UK and Italian political drama, Washington and Beijing trade talk, global monetary stimulus and Argentina’s imposing capital controls, calm looked to have returned. Then Beijing cut in. Just as Chinese markets were closing, the country’s central bank said it was slashing the amount of cash that banks must hold as reserves for the third time this year and the first time since 2015 that Beijing announced a broad and targeted RRR cut. That released a total of 900 billion yuan ($126.35 billion) to shore up the slowing economy.

“It feels to me like the air is coming out of it a bit,” Societe Generale strategist Kit Juckes said, referring to the recent surge in volatility. “So we will see what we get from the payrolls.”

Light volumes and sluggish price action dominated the European morning’s wait ahead of payrolls and scheduled comments from Fed’s Powell. Europe’s pan-region Stoxx 600, London FTSE, Paris CAC 40 and DAX in Frankfurt were all higher, after rising to their highest in more than month on Thursday.

Asian equities followed Wall Street higher as trade war angst subsides; MSCI Asia-Pacific index ex Japan rose for a third day, adding 0.6% and giving it a 2.4% weekly gain, its best week since mid-June. The rise in Asian stocks was led by financial firms and energy producers, following a U.S. rally supported by strong jobs data. Almost all markets in the region were up, with India and Hong Kong among the top performers. The Topix advanced 0.2%, driven by automakers and electronics firms. Japanese households increased spending again in July despite poor weather, showing solid consumer confidence ahead of a sales-tax hike in October. The Shanghai Composite Index added 0.5%, with Ping An Insurance Group and CSC Financial among the biggest boosts. The gauge climbed for a fifth straight day to finish its best week since June. India’s Sensex rose 0.7%, buoyed by Reliance Industries and HDFC Bank. Automakers rallied as the government considered more measures including lower taxes to boost vehicle sales.

In rates, Treasuries fell, with 10-yr yield higher at 1.60% while JGB futures dipped. Euro zone bond yields steadied after their worst one-day selloff in more than a year. Bunds/USTs dipped after a choppy start, while peripheral spreads broadly tightened to core bonds. Italian short-end outperformed with 2y and 5y yields off 4.5bps, with Moody’s scheduled to review Italy later Friday. Long-end JGB yields rise ~7bps, digesting commentary from BOJ’s Kuroda who earlier in the session said yields on 20-, 30-year JGBs have “fallen a bit too far” noting that returns for life insurers and pension funds have fallen significantly, negatively impacting consumer sentiment.

In FX, the Yen was steady with the Bloomberg dollar index while the euro and pound saw weekly gains after the biggest drop for the dollar in a month. In Asia, the Aussie was 0.1% higher, while the CNY gained notably after the RRR Cut announcement.

In commodities, WTI crude steady near $56.37; while brent oil futures were little changed at $60.97 per barrel. Brent had climbed to a one-month peak of $62.40 per barrel on Thursday after data showed U.S. crude stockpiles decline and the news about U.S.-China trade talks. Gold retreated after reaching a 2019 high earlier in the week. Meanwhile, Hurricane Dorian threatens to hit cotton, tobacco, hemp and corn in the U.S. Southeast.

In other overnight news, Fitch downgraded Hong Kong’s rating to ‘AA’ from ‘AA+’ and kept the outlook negative due to protests related to the extradition bill. Fitch said in a statement that months of persistent conflict and violence are testing the perimeters and pliability of the “one country, two systems” framework that governs Hong Kong’s relationship with China.

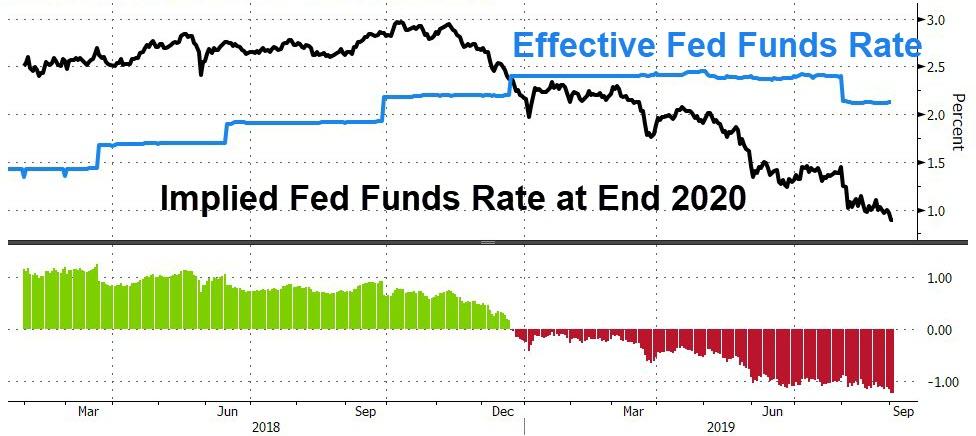

With a barrage of news in the rearview mirror, the closely watched U.S. non-farm payrolls report due at 830 am is expected to show 160,000 jobs were added in August and the unemployment rate was unchanged at 3.7% (see our full preview here). Surveys on Thursday had suggested the U.S. may be in better shape than investors have been fearing. Services activity accelerated in August and private employers increased hiring more than expected. Despite the reassuring signs, bond markets still expect the Federal Reserve to cut U.S interest rates this month and a total of 55 basis points of cuts by the end of the year.

In terms to what the market wants from today’s payroll, DB’s Jim Reid notes that it’s hard to know where the ‘risk-friendly’ number lies. With all the concerns about the economy in recent weeks, we’re probably still in a period where good is good for risk, even if it will price out the more extreme central bank action. This week we’ve already seen markets respond negatively to a weak ISM manufacturing and then positively to strong ISM non-manufacturing yesterday. So it appears that we’re treating data on its merit again. DB economists expect a below consensus NFP print of 140k, partly reflecting a one-tenth increase in average weekly hours. DB also notes that headline and private payrolls have missed the consensus forecast in four of the last five August numbers with the median miss being 38k. For wages, they expect average hourly earnings to have increased +0.3% mom, which is in-line with the market although the risk is that the annual rate rounds down to +3.0% yoy. The unemployment rate is expected to hold steady at 3.7%.

“The strong U.S. data are the main part of the latest turn in markets as they are key factors impacting equities and U.S. yields, therefore determining how long this ‘risk on’ phase will last,” said Junichi Ishikawa, senior FX strategist at IG Securities in Tokyo. The August payrolls report “will get more attention than usual as it could further fuel the risk-on phase, which in turn would boost the dollar,” Ishikawa said.

Also on deck today, Powell is slated to speak on the economic outlook at an event in Zurich at 12:30pm ET. “While this has been some positive economic data, it makes it a little more difficult for the Fed to cut rates,” Kristina Hooper, chief global market strategist at Invesco, told Bloomberg TV. “I suspect what we will hear from Powell is a very tepid commentary on the Fed’s ability to provide monetary policy accommodation.”

A reminder that the Fed’s media blackout period kicks in at the weekend so it’s a last opportunity for the Fed and Powell to get a message across, if they want to. Consensus expects Powell’s comments to largely mirror his Jackson Hole speech which was broadly dovish in acknowledging the argument for future policy accommodation but not pre-committing to any specific policy actions.

Top Overnight News

- Boris Johnson’s opponents are seeking ways to outmaneuver him on Brexit. Their latest idea is to hold a U.K. election in late October

- The Bank of England will start topping up its 10 billion-pound ($12 billion) corporate-bond holdings next week, providing a test of its ability to support credit markets just weeks before a potential no-deal Brexit.

- German industrial production unexpectedly declined further in July as trade tensions and waning business confidence continued to weigh on global demand.

- Mario Draghi is expected to go big in a final stimulus push as European Central Bank president, overriding protests from among his ranks that tools such as bond purchases aren’t yet needed.

- The EU still doesn’t know whether Boris Johnson is bluffing when he says he wants to leave the bloc with a deal, according to officials close to the Brexit negotiations

- Mario Draghi is expected to go big in a final stimulus push as European Central Bank president, overriding protests from among his ranks that tools such as bond purchases aren’t yet needed.

- After August’s historic drop, it was starting to seem like Treasury yields could only fall. And then came Thursday, when an enormous surge reminded bulls the world’s biggest bond market isn’t a one-way street

- Fitch Ratings downgraded Hong Kong as an issuer of long-term, foreign currency debt for the first time since 1995, saying that recent political turmoil raises doubts about its governance

- Oil is heading for the biggest weekly advance since mid-July as American crude stockpiles shrunk more than forecast, while U.S.-China trade talks look set to continue in Washington next month

Market Snapshot

- S&P 500 futures up 0.2% to 2,978.50

- STOXX Europe 600 down 0.04% to 385.78

- MXAP up 0.5% to 156.04

- MXAPJ up 0.6% to 506.49

- Nikkei up 0.5% to 21,199.57

- Topix up 0.2% to 1,537.10

- Hang Seng Index up 0.7% to 26,690.76

- Shanghai Composite up 0.5% to 2,999.60

- Sensex up 0.8% to 36,937.75

- Australia S&P/ASX 200 up 0.5% to 6,647.33

- Kospi up 0.2% to 2,009.13

- Brent Futures down 0.03% to $60.93/bbl

- Gold spot down 0.7% to $1,507.92

- U.S. Dollar Index down 0.02% to 98.39

- German 10Y yield fell 0.2 bps to -0.596%

- Euro up 0.06% to $1.1042

- Brent Futures down 0.03% to $60.93/bbl

- Italian 10Y yield rose 13.2 bps to 0.604%

- Spanish 10Y yield fell 3.2 bps to 0.203%

Asian equity markets traded higher after sustaining the momentum from Wall St. where all major indices rallied and the S&P 500 notched a 1-month high amid US-China trade hopes, while better than expected ISM Non-Manufacturing and ADP jobs data ahead of today’s NFP report added to the optimism. ASX 200 (+0.5%) and Nikkei 225 (+0.5%) were higher with the gains in Australia led by tech following similar outperformance of the trade-sensitive sector stateside and with the JPY-risk dynamic at play in Tokyo. Hang Seng (+0.7%) and Shanghai Comp. (+0.5%) conformed to the global optimism although gains in the region were somewhat capped ahead of the key US jobs data and after a mostly inactive PBoC this week resulted to a net weekly liquidity drain of CNY 100bln. Finally, 10yr JGBs were lower following the extended its slide below 155.00 after-hours yesterday as the heightened risk appetite triggered declines across global bonds. However, downside has since been stemmed on selling fatigue and with the BoJ present in the market for over JPY 1.2tln of JGBs heavily concentrated on 1yr-10yr maturities, while BoJ Governor Kuroda also reiterated that lowering rates further into negative territory is always an option and noted both 20yr and 30yr yields have declined a bit too far.

Top Asian News

- Axiata, Telenor Call Off Talks on Forming Asian Mobile Giant

- Bali Beaches, Thai Temples Go Quiet as Chinese Stay at Home

- Bank Bonds Gain in India as Mergers Set to Boost Credit Profiles

- Hong Kong ‘Will Be Done’ If China Deploys Troops, Jimmy Lai Says

Major European bourses are flat [Eurostoxx 50 +0.1%] after the region saw a tentative open ahead of today’s key risk events (US Jobs data, Fed Chair Powell to speak on economic outlook and monetary policy). Bourses experienced some short-lived upside upon the PBoC’s announcement of its 50bps RRR cut effective Sep 16th. Further RRR cuts will be implemented on some banks in two phases of 50bps each on October 15th and November 15th. The PBoC estimates a release of CNY 900bln in liquidity. Sectors are mixed with marginal outperformance in consumer discretionary names whilst utilities lag. Looking at individual movers Telenor (-4.3%) are subdued after the Co. and Axiata agreed to end discussions regarding a non-cash combination of their telecom infrastructures. Meanwhile Sodexo (-3.7%) is just below on the Stoxx 600 on the back of a broker move. On the flip side, Thyssenkrupp (+2.2%) share continues its ascent amid constructive comments from Kone (+2.0%) regarding the former’s elevator unit, with indicative bids for this unit to be submitted by Wednesday.

Top European News

- Markets Are Expecting Too Much From the ECB, Constancio Says

- Aviva Chairman to Lead U.K. Finance Lobby’s Advisory Council

In FX, pre-NFP caution and consolidation has curtailed the Dollar’s recovery, with the index churning within a tight 98.309-463 range just shy of Thursday’s post-ADP and non-manufacturing ISM high (98.538). In terms of Friday’s fundamental drivers, the data spotlight falls on US jobs ahead of Fed chair Powell ahead of the September FOMC and pre-policy meeting purdah, but from a technical perspective the DXY is delicately placed between 10 and 20 DMAs at 98.480 and 98.210 respectively.

- NZD/AUD/CAD – In keeping with this week’s evolving and improving risk tone, supplemented by 50-100 BP PBoC RRR cuts, high beta and more sensitive to overall sentiment G10 currencies have forged further gains, with Nzd/Usd managing to clamber back above 0.6400 and overtaking Aud/Usd in the process as the cross fades after several 1.0700+ forays. However, the Aussie has formed a firmer footing vs its US counterpart and nibbled through buy-stops between 0.6830-35 alongside a more pronounced bounce in the Yuan (Usd/Cnh eyeing 7.1100 compared to highs not far from 7.2000 recently). Meanwhile, Usd/Cad has slipped back to test 1.3200 after comments from BoC’s Schembri basically underscored Wednesday’s rates appropriate for now guidance, albeit adding more emphasis on weak commodity prices and not ruling out NIRP in extreme circumstances. Next up for the Loonie, Canadian labour data alongside US NFP, and then IVEY PMI after this week’s sub-50 Markit manufacturing print.

- EUR – The single currency is holding rock steady against the Greenback between 1.1030-50 and may not venture much further ahead of the aforementioned US labour report, or after given hefty option expiry interest at 1.1045-55 (1.8 bn) and Fib resistance near the middle of that band (1.1049).

- JPY/GBP/CHF – All on the back foot, with the Yen pivoting 107.00 and wary of decent expiries between the big figure and 107.05 (1.7 bn), but cushioned by bids reportedly layered from 107.10 to 107.20 ahead of corporate supply at 107.50. Elsewhere, Sterling has been more volatile amidst the ongoing UK political and Brexit uncertainty, with Cable waning ahead of 1.2350 and losing grip of the 1.2300 handle again before gleaning some traction on the High Court’s ruling that PM Johnson’s Parliament suspension is not unlawful. Conversely, the Franc is underperforming around 0.9900 and under 1.0900 vs the Euro after reiterations from SNB head Jordan that sub-zero Swiss interest rates are still required, and in advance of another scheduled appearance by the chief alongside his US peer.

- EM – Try aside, regional currencies are revelling in the stronger appetite for risk, and the Rub is now exception even though the CBR is widely expected to lower rates by 25 bp shortly.

In commodities, WTI and Brent crude futures are lower on the day thus far, as is usually the case on US jobs report day, with participants also awaiting Fed Chair Powell’s speech on economic outlook and monetary policy. WTI futures reside under the 55.50/bbl mark after it failed to convincingly breach its 100 DMA to the upside yesterday whilst today breaching both its 50 and 200 DMAs to the downside (both at 56.15/bbl). Meanwhile, Brent futures trade below 60.00/bbl at time of writing. In terms of weekly performance, both energy benchmarks were swayed by the flip-flop in risk sentiment over the week, WTI futures fluctuated in-between its 50 WMA (57.63/bbl) and 200 WMA (53.25/bbl), whilst its Brent counterpart printed a weekly range of 57.26-60.90/bbl for now. Elsewhere, gold prices remain on the backfoot despite a weaker Buck as the recent bout of risk appetite (driven by US/China trade hopes and better-than-forecast ISM N-manufacturing) took the yellow metal closer to the 1500/oz mark (vs. weekly high at 1557/oz). Meanwhile, as it stands, copper is poised to end the week on a more positive note as prices remain above the 2.60/lb level (vs. sub-2.50/lb low). Finally, nickel ore prices saw a correction of around 3.0% amid supply glut concerns followings its recent rally with downside attributed to Indonesia stated that nickel miners can apply for new export quotas for the rest of the year in addition to their already approved quotas.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 160,000, prior 164,000

- Unemployment Rate, est. 3.7%, prior 3.7%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

- Average Hourly Earnings YoY, est. 3.0%, prior 3.2%

- Average Weekly Hours All Employees, est. 34.4, prior 34.3

- Labor Force Participation Rate, prior 63.0%

- Underemployment Rate, prior 7.0%

- 12:30pm: Powell Speaks in Zurich on Economic Outlook

DB’s Jim Reid concludes the overnight wrap

15 years ago today, I met my current long-term partner after breaking up with my previous partner of 9 years – my first relationship. Having never been with anyone else, I didn’t really know what to expect. Was it love at first sight? I wouldn’t say so but love has subsequently blossomed. I’ve no idea if they’ve ever wanted to divorce me but probably best I don’t know. There have been rows, tensions and disagreements but over the years a great mutual respect has developed. Yes, on September 6th 2004 I joined DB and to a great bunch of people in research. The previous week, I’d climbed Kilimanjaro at the end of my gardening leave, so the last 15 years have been pretty straightforward relative to that.

After one of the biggest bond routs yesterday for years in some cases, it’s amusing to reflect that when I started at DB, 10yr yields in the US, Germany and the UK were all comfortably above 4%. Will I see such yields in my career again? Anyway, today’s payrolls report comes at a fascinating time given yesterday’s move. 10y and 2y Treasury yields rose +9.8bps (a further +1bps this morning) and +10.2bps (a further +0.5bps) – both the sharpest sell-offs since January 4. Europe saw similar moves. In fact, 30y Bunds (+14.2bps) had their sharpest sell-off in 4 years and even briefly turned positive again having touched a low of -0.311% as recently as August 16. In the end, 10y Bunds rose +8.1bps and back to the gravity-defying heights of -0.594% while BTPs were up +13.5bps. The bond moves helped US and European Banks to rally +2.46% and +3.35%, respectively.

Firmer data and the positive trade war news we mentioned yesterday appeared to cause the mini-shockwave through the bond market. As we’ve also been highlighting this week, it’s been a bumper few days for US IG supply with $74bn of issuance so far since Monday already eclipsing the previous weekly record of $66bn in September 2013. There was also some attention paid to a WSJ article from chief economic correspondent Nick Timiraos, who has developed a reputation for being well connected to the Fed. The article said that “the idea of an aggressive half-point cut to battle the slowdown hasn’t gained much support inside the central bank,”. This helped spark a sell-off in fed funds futures with implied odds of 12% for the larger 50bps cut this month, down from 30% on Wednesday. Through year-end, there are now 60bps of cuts priced, down -7.5bps yesterday.

In terms to what the market wants from today’s payroll, it’s hard to know where the ‘risk-friendly’ number lies. With all the concerns about the economy in recent weeks, we’re probably still in a period where good is good for risk, even if it will price out the more extreme central bank action. This week we’ve already seen markets respond negatively to a weak ISM manufacturing and then positively to strong ISM non-manufacturing yesterday. So it appears that we’re treating data on its merit again. The consensus expects a 160k reading, which is broadly in line with last month’s 164k reading. Our economists are, however, below consensus at 140k, partly reflecting a one-tenth increase in average weekly hours. Our colleagues also make the point that headline and private payrolls have missed the consensus forecast in four of the last five August numbers with the median miss being 38k. For wages, they expect average hourly earnings to have increased +0.3% mom, which is in-line with the market although the risk is that the annual rate rounds down to +3.0% yoy. The unemployment rate is expected to hold steady at 3.7%.

If the data fails to provide much direction, then there’s always Fed Chair Powell speaking at 5.30pm BST/12.30pm EST in Zurich at a SNB event. A reminder that the media blackout period kicks in at the weekend so it’s a last opportunity for the Fed and Powell to get a message across, if they want to. Our colleagues expect Powell’s comments to largely mirror his Jackson Hole speech which was broadly dovish in acknowledging the argument for future policy accommodation but not pre-committing to any specific policy actions.

Risk assets go into these two big events on the back of a decent two-day rally with a +1.30% return for the S&P 500 yesterday putting it back to within 1.65% of the all-time highs. That’s also now six positive days out of the last eight. The DOW (+1.41%) and NASDAQ (+1.75%) also had strong days while in credit US HY spreads finished -13bps tighter. The incrementally positive news about trade including the announcement from Chinese Vice Premier Liu He (from the Asian session yesterday) about agreeing to a visit in early October was a driver, as was the data.

The headline news though was the better-than-expected ISM non-manufacturing where the August reading bounced +2.7pts to 56.4 (vs. 54.0 expected). New orders (60.3 vs. 54.1) were a big driver; however, it didn’t go unnoticed that the employment component slid over 3pts to 53.1 and to the lowest level since December 2017. That was somewhat countered by a strong ADP reading where the August print of 195k bettered expectations for 148k even though revisions subtracted -14k from July’s figure. An interesting divergence also opened between the ISM manufacturing employment index and manufacturing hiring in ADP. Historically these two series have been fairly well correlated.

Asian markets are following Wall Street’s lead this morning with the Nikkei (+0.60%), Hang Seng (+0.64%), Shanghai Comp (+0.16%) and Kospi (+0.17%) all up. Futures on the S&P 500 are +0.22% higher while spot gold prices are down -0.30% to 1514.50/ troy ounce. 10y JGB yields have tracked up +2.1bps this morning to -0.253%. As for overnight data releases, Japan’s July household spending came in line with consensus at +0.8% yoy, marking the 8th straight increase and the longest streak on record in comparable data dating back to 2000, as consumer spending remains elevated ahead of the planned October sales tax hike. Real labour cash earnings surprised on the downside though with the reading at -0.9% yoy (vs. -0.7% yoy expected).

In other overnight news, Fitch have downgraded Hong Kong’s rating to ‘AA’ from ‘AA+’ and kept the outlook negative due to protests related to the extradition bill. Fitch said in a statement that months of persistent conflict and violence are testing the perimeters and pliability of the “one country, two systems” framework that governs Hong Kong’s relationship with China.

In terms of Brexit developments yesterday, there were none really. All eyes will be on Monday when Mr Johnson will try to get an election vote through and all depends on whether the Labour and/or SNP party support it. Overnight, Bloomberg and other news outlets have reported that Labour’s Corbyn is in talks with the SNP’s leadership over pushing for a delay with their preference being October 29th and thus trying to force Mr Johnson to go to Brussels, against his will, to ask for an extension. I’m sure they’ll be lots of rumours in the weekend papers.

As for the rest of the US data yesterday, jobless claims remained low at 217k and are still yet to show any signs of meaningful deterioration. The services PMI was revised down 0.2pts to 50.7 while nonfarm productivity and unit labour costs were revised up one-tenth and two-tenths, respectively, to 2.3% and 2.6% for Q2. Elsewhere, factory orders were reported as rising a slightly better-than-expected +1.4% mom in July while core capital goods orders were revised down two-tenths to +0.2% mom.

In Europe the only data of note was the volatile factory orders series in Germany, where orders were reported as falling -2.7% mom in July (vs. -1.4% expected). That didn’t stop the STOXX 600 from climbing +0.72%.

Onto the day ahead, where the obvious focus is the US employment report this afternoon. Prior to that we’ll get July industrial production and Q2 labour costs data in Germany this morning along with the July trade balance in France. Not long afternoon we’ll get the final Q2 GDP revisions for the Euro Area where the last estimate pegged growth at +0.2% qoq. The other potentially important event for markets is Powell’s speech tonight in Zurich.

3A/ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 13.74 POINTS OR 0.46% //Hang Sang CLOSED UP 175.23 POINTS OR 0.66% /The Nikkei closed UP 113.63 POINTS OR 0.54%//Australia’s all ordinaires CLOSED UP .48%

/Chinese yuan (ONSHORE) closed UP at 7.1155 /Oil UP TO 55.31 dollars per barrel for WTI and 59.31 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 7.1155 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.1113 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

China

The Chinese economy is suffering pretty bad due to the tariffs and the global slowdown. Now China cuts its banking Reserve Ratio in an attempt to stimulate their economy.

(zerohedge)

China Cuts Required Reserve Ratio Releasing $126BN In Liquidity; Yuan Surges

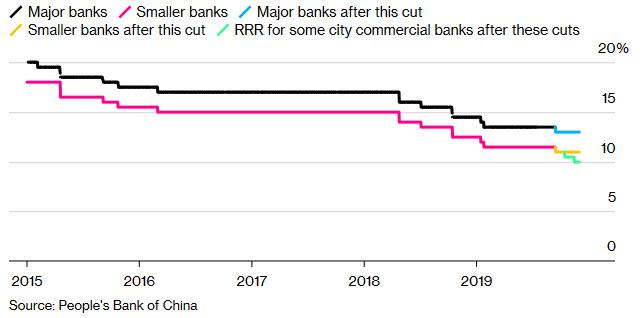

As had been widely previewed in China’s official financial press in recent days, on Friday the PBOC announced it would cut the required reserve ratio (RRR) for all banks by 0.5% effective Sept. 16 (and by 1% for some city commercial banks, to take effect in two steps on Oct. 15 and Nov. 15), releasing 900 billion yuan ($126 billion) of liquidity, helping to offset the tightening impact of upcoming tax payments.

While today’s rate cut – which was expected following the State Council meeting and ahead of the Oct.1 National Day Chinese holiday – was more than the previous cuts in January and May, which released 800 billion yuan and 280 billion yuan, respectively, the PBOC stated that “China won’t adopt flood-like monetary stimulus” and that they will continue “prudent” monetary policy to “keep liquidity at (a) reasonably ample level” and will “strengthen the counter-cyclical adjustment” which is basically gibberish for it will do whatever it sees appropriate.

With the Chinese economy slowing drastically in recent months, with various economic indicators at multi-decade lows, the RRR cut was aimed at supporting demand by funneling credit to small firms and echoes the earlier cuts this year. Indeed, as Bloomberg notes, China’s economy softened substantially in August after poor results in July, and will likely deteriorate further in the remainder of the year. Trade tension between China and the U.S. expanded onto the financial front recently after China allowed the currency to decline below 7 a dollar, prompting the U.S. to name it a currency manipulator.

Anticipating cries of foul play from Trump’s twitter account which is just minutes away from unleashing hell at the Fed for not doing what China is doing, the cut “doesn’t reflect an aggressive easing,” said Commerzbank economist Zhou Hao. “In fact, China has recently massively tightened property financing. Hence this is still a re-balancing – to lower the funding costs for the manufacturing sector but tighten liquidity in the property sector due to asset bubble concerns.”

The widely anticipated news of further Chinese easing helped boost US equity futures, with the Emini S&P 500 future spiking to session highs of 2,986 after the announcement, although it has since faded much of the gains.

The offshore yuan gained 0.35% to 7.1128 a dollar as of 6:30 p.m. in Beijing.

Amusingly, the PBOC pulled a page from the Fed’s “mid-cycle adjustment” playbook and emphasized that the policy change wasn’t a massive step up in easing. “The cut is not flooding the economy with stimulus and the stance of prudent policy has not changed,” it said in a separate statement. The RRR cut will offset the tax season in mid-September, and the overall liquidity in the banking system will stay basically stable, according to the PBOC.

“The cuts don’t mean significant easing in monetary policy,” said Standard Chartered economist Ding Shuang. “Rather it is something they must do, a sort of marginal easing, in order to prevent tightening in monetary policy.”

Whether the impact of the RRR cut is limited or not, it will certainly antagonize Trump, especially since PBOC officials indicated recently they are wary of larger-scale easing measures, and have so far refrained from following the U.S. Federal Reserve in cutting benchmark interest rates.

Meanwhile, even though the rate cut should – in theory – be currency negative, in today’s upside down world, the offshore yuan surged from around 7.14 to just stronger than 7.11 against the dollar.

And now we await Trump’s angry response, slamming the Fed for failing to keep up with every other central bank.

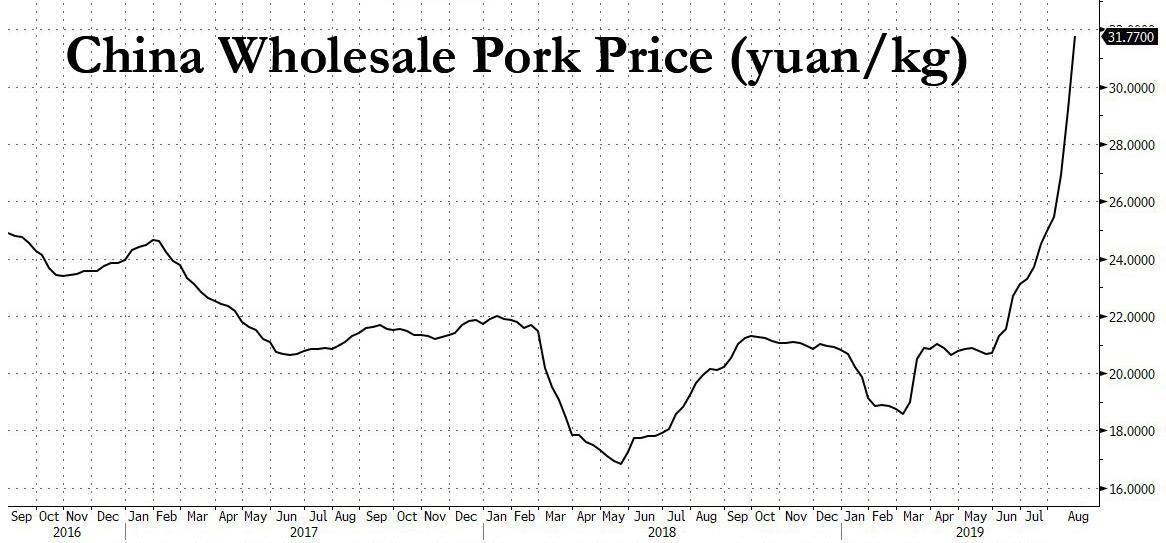

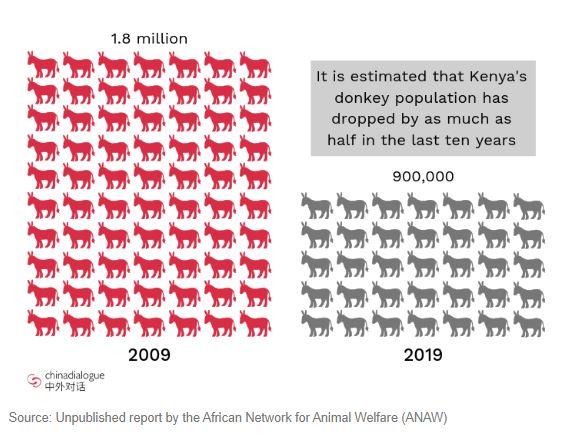

Chinese Demand Threatens To Wipe Out Kenyan Donkey Stocks As ‘Pig Ebola’ Outbreak Worsens

As African swine flu – better known as ‘pig ebola’ – continues to ravage Chinese pig farms, triggering a massive surge in pork prices, we’ve written about how consumers’ search for alternatives to the dietary staple has turned duck farmers into millionaires overnight.

But duck isn’t the only protein alternative that Chinese consumers are buying up in droves as pork prices have climbed nearly 70% over the past year, to near-unprecedented levels.

As China Dialogue, a China-based English-language publication, reports, surging demand for Donkey meat and skin in China is rapidly depleting donkey stocks in Kenya. If demand continues to climb, animal rights activists warn, the Kenyan Donkey could soon disappear from the East African country.

Over the past five years, four new donkey abbattoirs have opened up in Kenya to help meet rising demand in China. This, of course, predates the ‘pig ebola’ outbreak, as the Communist Party and state-backed agribusiness has struggled to source food for China’s 1.4 billion consumers even under normal conditions.

Though most US consumers would probably cringe at the thought of eating donkey, their meat is considered a delicacy in China. Their skins are also processed into a traditional remedy called ejiao that’s used to treat everything from anemia to dizziness. Ejiao has also grown in popularity alongside China’s growing prosperity.

According to a report by the African Network for Animal Welfare, the slaughterhouses are operating at less than half of their capacity, as demand from China has already depleted the donkey population from around 1.8 million animals in 2009 to roughly half that level – about 900,000 – today.

Some activists have warned that Chinese demand is making the Kenyan donkey trade ‘unsustainable’. Like other forms of livestock, donkeys are slow to reproduce, with gestation periods of 11-14 months.

The rising demand has also caused the price of donkey meat to soar. Today, one donkey can fetch a price of between 15,000 to 25,000 Kenyan shillings ($145-$242), up from 6,000 to 8,000 shillings ($58 to $78) four years ago. Males typically cost more.

This could create serious problems for the local economy. Many Kenyans rely on donkeys for transportation, particularly in the northern part of the country, where donkeys pull carts that carry water, firewood and other supplies. Higher donkey prices mean these staples are increasingly out of reach for the average merchant or farmer.

The Kenyan government is facing criticism for not exercising more oversight of the abbattoirs. Some believe the government could have implemented breeding programs to ensure that donkey stocks would keep up with rising demand. Others believe it’s too late for any remedy short of calling for a total ban on the trade in donkey meat and ejiao (though it’s unlikely Beijing would let that happen).

As the the swine flu outbreak worsens, news reports earlier this week claimed that Beijing is on the verge of releasing some of its emergency pork reserves as the number of pig casualties from the swine flu crosses 100 million, equivalent to one-third of China’s pig population.

That doesn’t bode well for the donkeys.

The Ugly Truth About The Trade War

Authored by Brandon Smith via Alt-Market.com,

This past week was an interesting exercise in false expectations and assumptions. Once again, trade war theatrics were used to stall a stock market plunge as insinuations of a possible “deal” were made by Donald Trump, followed by China’s claim that maybe, just maybe, they would not immediately issue a new round of tariffs right now, but possibly tomorrow, or in a month…

Then, all hell broke loose again when only a few days later both sides jumped into a new round of tariffs leaving markets confused and algo trading computers bewildered, so much so that sometimes they even buy on bad news thinking it’s good news. This is the problem with the Pavlovian response mechanism – You train a dog to salivate at the sound of a bell because he thinks he’s going to get a treat, but then what if you change the bell, or the treat, or the entire dynamic of the process? The dog’s whole world is turned upside down and he curls up in a ball in the corner of the room to make the mental anguish stop.

This is exactly the kind of reaction the globalists are looking for, hence the stop/start insanity of trade discussions, not to mention the dove/hawk behavior of the Federal Reserve. Everything people once thought predictable is being deliberately discombobulated.

Ultimately the circus and the confusion are only products of peoples biases. They want to believe they will get a treat if they act a certain way when certain indicators signal. They want to believe the trade war can be won, or at least that Trump is trying to win. They want to believe that the Fed will save them with a surge of QE. They want to believe that the instability will be smoothed away by the hands of the political and banking elites. But what if the elites have no intention of doing this? What if they WANT an economic crisis?

In terms of the trade war, there are some facts that do not support some of the assumptions out there on either side of the debate.These facts run contrary to the mainstream narrative, as well some narratives within the alternative media. On the conservative side I ‘m seeing a kind of artificial patriotic fervor; an organized attempt using memes and propaganda to convince conservatives that the trade war requires mindless fealty to the anti-China message.

First, to be clear, I think China is a despicable communist regime with a record of human rights abuses, but that’s what makes it a rather perfect distraction for Americans on the political right. I’m reminded of the war fever against Iraq after 9/11, and how so many conservatives bought into the very thin claim of Iraqi involvement and the lies about WMDs. We don’t like dictators, and we don’t like China, but conservatives are being duped into thinking the trade war against China is an ideological crusade that will lead to a better America, or a better world.This is not what the trade war is intended to do.

Let’s start with the assumptions (as well as lies and disinformation) surrounding the trade war and then look at the evidence that debunks them…

Fallacy #1: China Is Dependent On The US Consumer