GOLD:$1503.25 DOWN $4.75 (COMEX TO COMEX CLOSING)

Silver:$18.09 DOWN 6 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1498.50

silver: $17.99

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 9/14

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,506.200000000 USD

INTENT DATE: 09/06/2019 DELIVERY DATE: 09/10/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 2

661 H JP MORGAN 9

737 C ADVANTAGE 3 3

905 C ADM 11

____________________________________________________________________________________________

TOTAL: 14 14

MONTH TO DATE: 1,640

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 14 NOTICE(S) FOR 1400 OZ (.0435 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1640 NOTICES FOR 164,000 OZ (5.1010 TONNES)

SILVER

FOR SEPT

203 NOTICE(S) FILED TODAY FOR 1,015,000 OZ/

total number of notices filed so far this month: 6989 for 34,945,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10,348 UP 67

Bitcoin: FINAL EVENING TRADE: $ 10288 DOWN 294

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 483 CONTRACTS FROM 216,682 DOWN TO 216,199 DESPITE THE MONSTROUS 60 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

SEPT, 0 FOR DEC : 2442, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 2442 CONTRACTS. WITH THE TRANSFER OF 2442 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2442 EFP CONTRACTS TRANSLATES INTO 12.21 MILLION OZ ACCOMPANYING:

1.THE 60 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

38.350 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD NO DOUBT SOME COVERING OF BANKER SHORTS AGAIN AT THE SILVER COMEX ON FRIDAY WITH THE HUGE RAID ORCHESTRATED BY THE CROOKED BANKERS AT 12:30 PM EST. HOWEVER IN CONTRAST TO THURSDAY, TOTAL OI INCREASED DRAMATICALLY DESPITE THE FURTHER DRUBBING IN PRICE OF OUR SILVER METAL WITH THE ABOVE AFOREMENTIONED RAID.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

14,035 CONTRACTS (FOR 5 TRADING DAYS TOTAL 14,035 CONTRACTS) OR 70.175 MILLION OZ: (AVERAGE PER DAY: 2809 CONTRACTS OR 14.045 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 70.175 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.03% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1619.89 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 483, DESPITE THE HUMDINGER 60 CENT LOSS IN SILVER PRICING AT THE COMEX /FRIDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 2442 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2284 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2442 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 483 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A HUGE 60 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.15 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.083 BILLION OZ TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 203 NOTICE(S) FOR 1,015,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 38.350 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL 1186 CONTRACTS, TO 617,054 DESPITE THE CONSIDERABLE SIZED $9.80 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// FRIDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7602 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 5296 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 617,054,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE, STRANGELY, DESPITE THE SECOND RAID IN A ROW, WE HAD A STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4110 CONTRACTS: OF WHICH 1186 CONTRACTS DECREASED AT THE COMEX AND 5,296 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4110 CONTRACTS OR 411,000 OZ OR 12.18 TONNES. FRIDAY, WE HAD A LOSS OF $9.80 IN GOLD TRADING....AND WITH THAT LOSS IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 12.18 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME WAS HUGE.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 45,668 CONTRACTS OR 4,566,800 oz OR 142.04 TONNES (5 TRADING DAY AND THUS AVERAGING: 9,134 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY IN TONNES: 142.04 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 142.04/3550 x 100% TONNES =4.00% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4293.16 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED DECREASE IN OI AT THE COMEX OF 1186 DESPITE THE CONSIDERABLE PRICING LOSS THAT GOLD UNDERTOOK FRIDAY($9.80)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5296 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5,296 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 4110 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5,296 CONTRACTS MOVE TO LONDON AND 1186 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 12.18 TONNES). ..AND THIS STRONG INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $9.80 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 14 notice(s) filed upon for 1,400 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.75 TODAY//(COMEX-TO COMEX)

NO CHANGES IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 889.75 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 6 CENTS TODAY:

WHAT FRAUDSTERS!!

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV;

A MAMMOTH WITHDRAWAL OF 5.425 MILLION PAPER OZ OF SILVER LEFT THE SLV

THIS NO DOUBT WAS USED IN THE RAID ON SILVER THESE PAST THREE DAYS.

/INVENTORY RESTS AT 381.179 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 483 CONTRACTS from 216,682 DOWN TO 216,199 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 2442: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2442 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 483 CONTRACTS TO THE 2442 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG GAIN OF 1959 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.795 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ//SEPT 2019: 38.350 MILLION OZ/

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 60 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// FRIDAY. WE ALSO HAD A STRONG SIZED 2442 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 25.14 POINTS OR 9.84% //Hang Sang CLOSED DOWN 9.36 POINTS OR 0.04% /The Nikkei closed UP 118.85 POINTS OR 0.56%//Australia’s all ordinaires CLOSED UP .11%

/Chinese yuan (ONSHORE) closed DOWN at 7.1259 /Oil UP TO 56/72 dollars per barrel for WTI and 61.81 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1259AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1211 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

i)Is China using Fentanyl as a “Chemical warfare: against the USA.?Tons of this deadly drug continues to enter into the uSA. China is refusing to stop it in the same manner as the opiods wars started at the end of the 18th Century.China lost and that is how HOng Kong became a British colony.

(zerohedge)

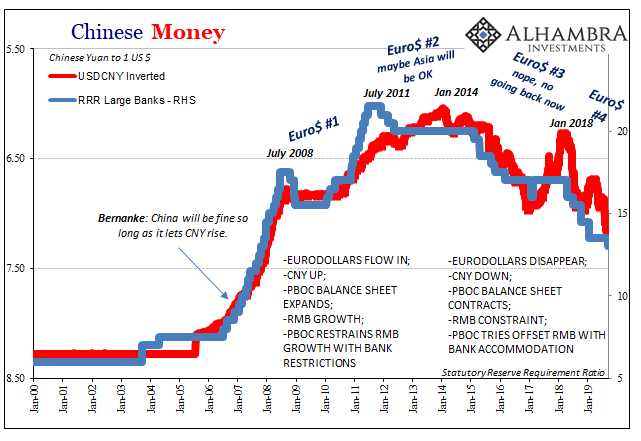

ii)Jeffrey Snider gives a detailed explanation for the RRR cuts by China. It is not for stimulus but because the banks are lacking dollars and the cuts are to free up some yuan to obtain badly needed dollars

iii)Protest continue for the 14th straight week despite Lam’s removal of the much hated extradition proposal.(zerohedge)

4/EUROPEAN AFFAIRS

i)Our three resident experts on Brexit give their thoughts on how the Brexit will proceed. Put your money on No2 Mish

(Tom Luongo.Mish Shedlock/Michael Every)

II)Eric Reguly of the Globe and Mail Toronto gives his opinion of why the European banks are trembling over fears of more negative rates

iii)The Euro and bund yields rise with hints that Germany is going to undergo fiscal stimulus to get its moribund economy on track(zerohedge)

7. OIL ISSUES

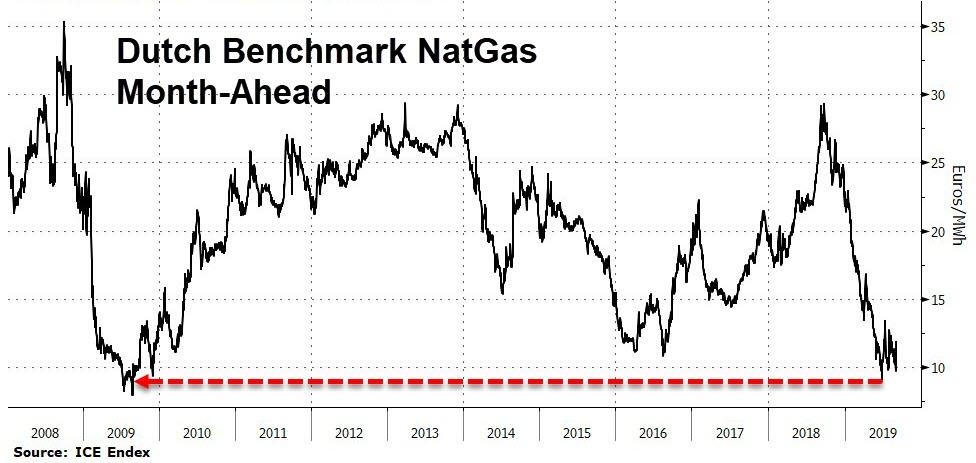

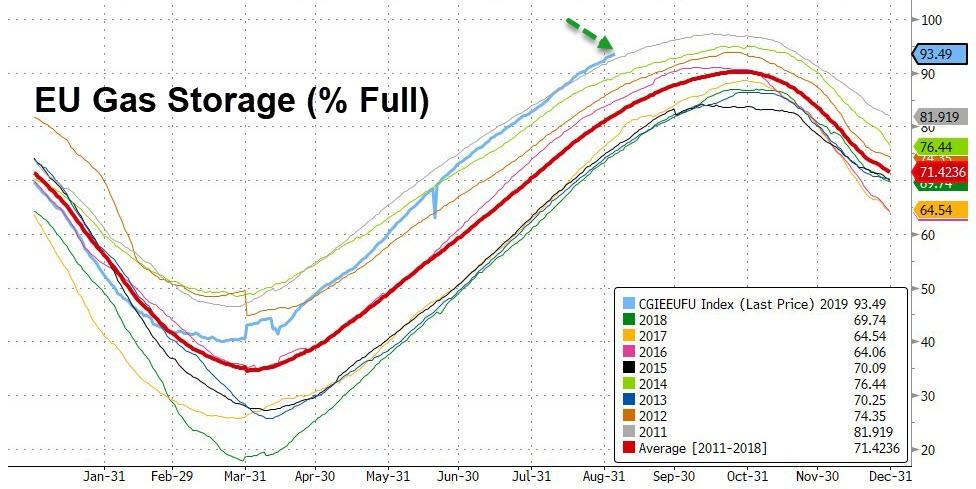

European gas prices plunge to a 10 yr low

Paraskova/OilPrice.com)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

I) Fed Clown (Chairman), Powell, says that even though they lost time in inflation, they will try and overshoot as time goes on

(London’s Financial times)

ii)A first: The UK’s Royal Mint plans its first stock exchange product using a gold ETF: the reason the huge demand for gold. Let’s have more paper gold

(Flood/London’s Financial Times)

iii)China officially reports an addition of 1000 tonnes of gold to its official reserves

(Bloomberg/GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

a)It sure looks like the consumer is not healthy at all

(zerohedge)

b)Will this be the spark that causes a rout in the bond market?: We have our first crashing angel and it is a biggy: Ford. with its 84 billion in debt. The total of debt which is just one step above junk totals 1 trillion, so you can imagine the trouble here.

iii) Important USA Economic Stories

i)For the 10th straight month, class 8 heavy duty truck orders fall. This itme the plunge is 79% in August

(zerohedge)

ii)This is going to be messy!! Purdue Pharma is now expected to file for bankruptcy amid no settlement negotiations

iv) Swamp commentaries)

Here is a good account of our good friend Robert Mueller helped the Saudis cover up their involvement in the 9/11 attacks. This has been brought out form a civil lawsuit

(zerohedge)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

TODAY’S NUMBER OF NOTICES FILED:

We, today, had 203 notice(s) filed for 1,015,000, OZ for the SEPT, 2019 COMEX contract for silver

we had 0 dealer entry:

We had 1 kilobar entries

and the entry is a phony!!//no gold is entering the comex

total gold withdrawals; nil oz

i) Into CNT: 601,318.900 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 66,135 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 228,892 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 228,892 CONTRACTS EQUATES to 1,145 million OZ 163.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.02% ((SEPT 9/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.46% to NAV (SEPT 6/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -2.02%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.14 TRADING 14.65/DISCOUNT 3.25

END

And now the Gold inventory at the GLD/

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 9/2019/ Inventory rests tonight at 889.75 tonnes

*IN LAST 659 TRADING DAYS: 45.63 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 559- TRADING DAYS: A NET 121,02 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 9/2019:

Inventory 381.179 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.03/ and libor 6 month duration 2.04

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: + .01

XXXXXXXX

12 Month MM GOFO

+ 1.94%

LIBOR FOR 12 MONTH DURATION: 1.95

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.01

gold lease ra

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Marginally Higher; China Buys 100 Tons of Gold For Its Reserves In 2019

◆ Gold eked out small gains of 0.4% to $1,512/oz after falling nearly 1% last week; Improved risk appetite are capping gains for now

◆ Gold may go lower in the short term and support is at $1,500 and $1,450 per ounce but strong global safe haven demand from investors, family offices and central banks including China and Russia (see News below) should lead to further gains

◆ China has raised it gold holdings for ninth straight month, with the PBOC buying another 5.9 tons in August and adding nearly 100 tons of gold to its reserves since it resumed declaring purchases in December

◆ Russia’s massive gold stash is now worth more than $100 billion and the value of Russia’s gold reserves climbed 42% in the past year

News and Commentary

Gold inches higher, but improved risk appetite caps gains

Gold fell 0.7% on Friday and fell 0.9% last week

Gold Investments Hit Record High As Family Offices Seek Safe Haven

China Has Added Nearly 100 Tons of Gold to Its Reserves

Russia’s Massive Gold Stash Is Now Worth More Than $100 Billion

Global stocks gain on hopes of central bank stimulus

China will not tolerate attempts to separate Hong Kong from China

China’s exports to US fell 16% in August as Trump escalates trade war

More Americans will die after U.S. abruptly ends Afghan talks, Taliban say

UK’s Royal Mint plans first stock exchange product with gold ETF

‘Gold is the way to go’ as interest rates fall, says Mark Mobius

Gold At $10,000 Isn’t Crazy – Frank Holmes

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

06-Sep-19 1504.95 1523.70, 1223.52 1237.09 & 1363.94 1378.49

05-Sep-19 1542.60 1529.10, 1257.06 1238.72 & 1397.44 1380.78

04-Sep-19 1538.80 1546.10, 1265.05 1269.97 & 1397.69 1403.86

03-Sep-19 1532.45 1537.85, 1278.06 1277.80 & 1400.35 1403.44

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Fed Clown (Chairman), Powell, says that even though they lost time in inflation, they will try and overshoot as time goes on

(London’s Financial times)

(Flood/London’s Financial Times)

iii) Other physical stories:

Russia and China understand fully what is going on and they ave massively accumulating gold instead of dollar assets.

(zerohedge)

Russia, China Continue “Massive Substitution” Of Dollar Assets By Gold

“I think it’s clear to everyone now” exclaimed Russian President Vladimir Putin, (and French President Macron recently said so publicly), “that the leading role of the West is ending. I cannot imagine an effective international organization without [Russia], India and China.”

And while most politicians are all talk, in the case of both Russia and China, their actions speak louder than their words.

China‘s foreign exchange reserves jumped to $3.1072 trillion despite the falling yuan and escalating trade war with the US, while raising its gold holdings by nearly 2.89 million troy ounces (99 tons) in nine months. That’s nearly five percent more since the end of last year.

Source: Bloomberg

As Bloomberg reports, that buying spree likely to persist in the coming years, according to Australia & New Zealand Banking Group Ltd.

Trade war restrictions, in the case of China, or sanctions, as with Russia, give “an incentive for these central banks to diversify,” John Sharma, an economist at National Australia Bank Ltd., said in an email.

“Also, with increasing political and economic uncertainty prevailing, gold provides an ideal hedge, and will therefore be sought after by central banks globally.”

But China is not alone. Figures released by the Central Bank of Russia (CBR) on Friday show Russia’s gold bullion holdings have reached $109.5 billion as the nation continues to shift its growing international reserves away from the US dollar.

As Bloomberg reports, Russia’s central bank has been the largest buyer of gold in the past few years…

Source: Bloomberg

“Russia prefers to cushion its macroeconomic stability through politically neutral tools,” said Vladimir Miklashevsky, a strategist at Danske Bank A/S in Helsinki.

“There is a massive substitution of U.S. dollar assets by gold – a strategy which has earned billions of dollars for the Bank of Russia just within several months.”

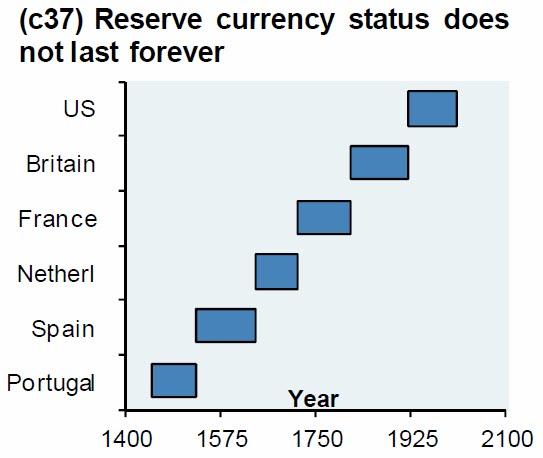

In fact, globally, the trend is clear…

Source: Bloomberg

Remember, nothing lasts forever…

(courtesy //zerohedge/Chris Powell)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Global Stocks Rise On Central Bank Stimulus Hopes

When it comes to overnight stock market levitation, there are two catalysts: hopes of an “imminent” trade deal (this has been the case for the past year) and hopes for central bank easing (this has been the case for the past decade). Overnight, it was the latter that pushed US equity futures by another 7 points, sending the Emini just shy of 3,000, trading at 2,987 last, and Global stock markets broadly higher.

European markets opened higher after data showed a surprise rise in German exports and on expectations of stimulus by the ECB later this week, including even lower rates and a restart of asset purchases. The pan-European STOXX 600 index was fractionally higher just after 7:00 EDT, while the MSCI All Country World Index was up 0.05%.

Germany’s trade-sensitive DAX index rose 0.2% after data showed seasonally adjusted exports rose 0.7% in July. A Reuters poll of economists had pointed to a drop of 0.5%. The report was a much needed green shoot for an economy that is currently in a technical recession and amid gloomy data from major economies since Friday, which heightened expectations of stimulus from central banks

The strong German trade data came after the US reported that August jobs slowed more than expected, while data over the weekend from China showed the country’s exports unexpectedly shrank as shipments to the U.S. slowed.

“If all the currently proposed tariffs are implemented, we foresee that growth in the first half of next year will slow toward the brink of a recession,” said UBS chief investment officer, Mark Haefele, emphasizing a report we discussed last week.

Of course the worse the data, the better for stocks, and the prospect of central-bank support kept risk sentiment alive and well. MSCI’s broadest index of Asia-Pacific shares outside Japan rose 0.2% and E-mini futures for the S&P 500 index rose 0.3%.

Asian stocks advanced, heading for a fourth day of gains, as China cut reserve ratios for banks and the country’s weak trade data fueled speculation for further easing. Most markets in the region were up, with Japan and China leading gains. Technology and industrial firms were among top performers. The Topix climbed 0.9% to a five-week high, led by electronics makers and pharmaceutical companies. Despite a downward revision to second-quarter growth, Japan’s economy is estimated to remain strong enough for an upcoming sales-tax hike. The Shanghai Composite Index closed 0.8% higher for a sixth day, with PetroChina and 360 Security Technology among the biggest boosts. India’s Sensex added 0.4%, driven by Housing Development Finance and Larsen & Toubro, as investors awaited more government stimulus

As a reminder, on Friday, China’s central bank cut reserve requirements for a seventh time since early 2018 to free funds for lending, while Fed Chairman Jerome Powell said the Fed would continue to “act as appropriate” to sustain U.S. economic expansion.

And while the European Central Bank is expected to cut rates this week, Euro-area bonds fell as investors showed less conviction that the Central Bank’s policy meeting Thursday will result in bold steps for more monetary stimulus. Longer-dated euro zone government bond yields ticked higher, with most yields up 3 to 4 basis points in early trade, while US 10Y yields rebounded from Friday’s plunge, trading around 1.60% last.

“There has been a tremendous rally in bonds and the central banks are the key determinant of what’s going to happen with the rates market,” Frances Hudson, global thematic strategist for multi-asset investing at Aberdeen Standard Investments, told Bloomberg TV. “With equities there is still an element of self-determination.”

Chinese sovereign bonds fell after the central bank disappointed investors by not rolling over maturing medium-term loans. The People’s Bank of China drained a net 56.5 billion yuan via monetary policy tools on Monday, selling 120 billion yuan of seven-day reverse repos, while 176.5 billion yuan of medium-term lending facility matured, Bloomberg reported. Paradoxically, that move came just one business day after the PBOC eased financial conditions, when it announced on Friday it was cutting the amount of cash banks must hold in reserve to the lowest since 2007, injecting liquidity into a domestic economy facing a slowdown and headwinds from the trade war with the U.S. “It seems like the PBOC is continuing its balancing act,” said Tommy Xie, economist at OCBC Banking Corp. in Singapore. “The inaction in MLF today to some extent offsets the impact of the RRR cut.”

Separately, data released on Sunday showed that exports decreased 1% in dollar terms from a year earlier in August as the trade war with the US is grinding China’s mercantilist apparatus to a crawl.

In currencies, the euro fell to a five-day low but recovered ground by 0820 GMT to trade 0.1% higher at $1.1036 as the dollar traded near a two-week low as the focus turned to whether the Federal Reserve will cut interest rates again this month. Aussie and kiwi both edged higher as Asian risk assets were boosted by some follow-through buying from China’s decision Friday to cut banks’ reserve ratios. The pound shrugged off earlier losses to rise to the highest level since July after the U.K. economy grew surprisingly fast in July, and after the latest defection from Prime Minister Boris Johnson’s Conservative party which will soothe fears Britain was facing a pre-Brexit recession.

In commodities, oil rose on expectations that Saudi Arabia, the world’s largest oil exporter, will continue to support output cuts by OPEC and other producers to prop up prices under new Energy Minister Prince Abdulaziz bin Salman.

Market Snapshot

- S&P 500 futures up 0.2% to 2,986.00

- STOXX Europe 600 down 0.06% to 386.91

- MXAP up 0.4% to 156.83

- MXAPJ up 0.3% to 507.72

- Nikkei up 0.6% to 21,318.42

- Topix up 0.9% to 1,551.11

- Hang Seng Index down 0.04% to 26,681.40

- Shanghai Composite up 0.8% to 3,024.74

- Sensex up 0.4% to 37,122.70

- Australia S&P/ASX 200 up 0.01% to 6,647.96

- Kospi up 0.5% to 2,019.55

- German 10Y yield rose 3.8 bps to -0.6%

- Euro up 0.06% to $1.1036

- Brent Futures up 0.4% to $61.78/bbl

- Italian 10Y yield fell 6.8 bps to 0.537%

- Spanish 10Y yield rose 3.0 bps to 0.203%

- Brent futures up 0.7% to $61.96/bbl

- Gold spot up 0.2% to $1,509.12

- U.S. Dollar Index little changed to 98.39

Top Overnight Headlines from Bloomberg

- Boris Johnson is refusing to back down and pushing on with his hardline Brexit strategy despite the risk of being taken to court. Johnson is in Dublin on Monday for talks with his Irish counterpart Leo Varadkar, who demanded “realistic, legally binding and workable” arrangements for the Irish border if an agreement is to be reached

- European Central Bank President Mario Draghi will test the composure of global policy makers this week as he unleashes a barrage of stimulus to shore up economic growth

- Apple Inc. and manufacturing partner Foxconn violated a Chinese labor rule by using too many temporary staff in the world’s largest iPhone factory, the companies confirmed following a report that also alleged harsh working conditions

- The contraction in China’s trade in August underscored what economists were already saying about the government’s stimulus efforts: they’re not yet enough to put a floor under the slowing economy

- Oil extended gains after Saudi Arabia ousted its long-time energy minister before an OPEC+ committee that monitors compliance with output cuts meets this week in Abu Dhabi

Asian equity markets traded mostly positively but with gains relatively mild as the region digested the latest developments from the world’s 2 largest economies including the PBoC RRR cut announcement, mostly weaker than expected Chinese trade data and US NFP. ASX 200 (U/C) was choppy as upside in tech was counterbalanced by continued weakness in gold miners and after soft Chinese trade data which showed a surprise drop in Exports, while Nikkei 225 (+0.5%) remained afloat after Final GDP figures for Q2 printed inline with estimates. Hang Seng (Unch.) and Shanghai Comp. (+0.8%) were mixed as the mainland reacted to the PBoC’s 50bps RRR cut and further targeted 100bps reduction for qualified banks which is expected to release CNY 900bln of liquidity, although advances were limited by the weak trade figures and with Hong Kong dampened after further violent protests over the weekend. Finally, 10yr JGBs were higher despite the mostly positive risk tone and reclaimed the 155.00 level, although prices later stalled amid mixed results in the enhanced liquidity auction for 2yr-20yr JGBs.

Top Asian News

- Chinese Food Producers Have World’s Richest Valuations

- Chinese Automobile Sales Decline for 14th Time in 15 Months

- Nissan CEO Saikawa Says Ready to Resign Once Successor Is Found

- Towngas China Surges Most in a Decade as Citi Predicts Takeover

Major European indices are mixed this morning but overall little changed [Euro Stoxx 50 +0.1%], as markets struggle for clear direction amidst a relatively quiet schedule and no further updates to the US-China trade situation. Unsurprisingly, sectors are painting a similar picture this morning though the energy sector outperforms amidst strength in the broader complex. In terms of individual movers, ProSiebensat (+5.5%) lead the Stoxx 600 after being upgraded to buy at UBS and the Co. stating they are to remain focused on their free-to-air business. At the other end of the spectrum are ThyssenKrupp (-2.3%) after the Co’s CEO states he would prefer a minority stake sale in their elevator division which has the potential to be valued at over EUR 15bln. Elsewhere, Lloyds (-0.4%) are slightly subdued after suspending their GBP 1.75bln share buyback scheme due to a substantial inflow of PPI claims, as such the Co. need to make an incremental charge of GBP 1.2-1.8bln on top of their prior Q3 provisions.

Top European News

- Italy Prepares to Tap Debt Market Just as Europe Demand Stutters

- Ireland’s Bonds Seen Increasingly Risky as Brexit Nears Endgame

- Thyssenkrupp CEO Said to Prefer Minority Sale for Elevators

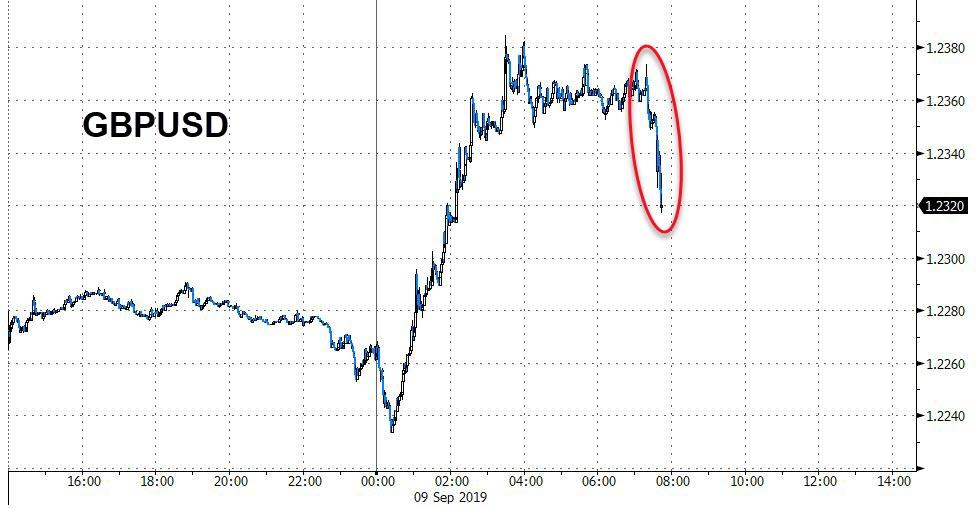

In FX, Pound Sterling survived and bout of selling pressure that pushed Cable down through 1.2250 and Eur/Gbp up above 0.9000, but was already recouping and reversing gains before a raft of UK releases that beat expectations across the board. This raised eyebrows and speculation about some being privy to the numbers or nature of the data beforehand, but others also pointed to the fact that the bill ensuring another Brexit extension rather than now deal is due to receive Royal Assent later today and reports that PM Johnson may have conceded that he may have to accept another 3 months if he fails to strike an accord with the EU before October 31. Meanwhile, opening remarks from his meeting with Irish PM Varadkar were largely upbeat and confident on the subject of resolving the Irish border backstop, including alternatives to the current WA proposal as he claimed there are many prospective options, but not for public consumption. In response and/or follow-through from the aforementioned encouraging data, Cable cleared 1.2300 more convincingly on its way over the 55 DMA (1.2328) and above last Friday’s post-NFP high (1.2338) to circa 1.2360, while Eur/Gbp reversed through the big figure and 0.8950, eyeing 0.8900 next.

- AUD/NZD/NOK/CAD – The Antipodean Dollars have extended recovery gains vs their US counterpart in wake of the latest PBoC RRR cuts, a sub-forecast rise in US payrolls and despite Chinese trade data revealing an unexpected decline in exports. Aud/Usd has now advanced towards 0.6870 and Nzd/Usd is approaching 0.6450 as the Aud/Nzd cross pivots 1.0650. Elsewhere, strong Norwegian GDP for the month of July and firm oil prices are underpinning the Nok as it rebounds through 9.9000 vs a steady Eur overall, while the Cad is inching closer to resistance ahead of 1.3150 against its US rival on the back of Canada’s labour report and a bumper jump in the jobs tally.

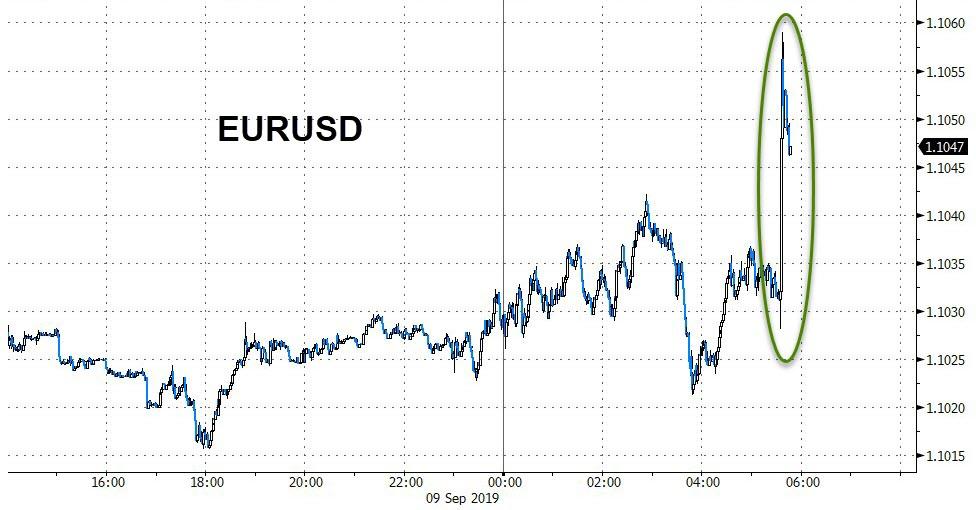

- EUR/JPY – Both narrowly mixed vs the Greenback around 1.1025 and 107.00 respectively, and well flanked by heavy option expiry interest as 1.8 bn rolls off at 1.1000 and 1 bn at 1.1050 in Eur/Usd, while 1.5 bn, 1.3 bn and 1.3 bn are layered in Usd/Jpy from 106.50-60, through 106.85-95 to 107.25-30. Note also, the Euro and Yen are not deriving much from the Buck indirectly as the DXY trades within a tight 98.512-309 band.

- CHF – The G10 laggard as the Franc retreats from its post-NFP peaks towards 0.9900 again and Eur/Chf climbs towards the top of a 1.0930-1.0890 range amidst firmer risk sentiment overall and expectations that the SNB will respond to likely stimulus from the ECB this week and Fed next week at its September Quarterly Policy review.

- EM – The Lira continues to underperform or hand back recovery gains following more dovish prompting from Turkish President Erdogan ahead of this month’s CBRT policy convene where forecasts range from 225-275 bp worth of easing after the significantly bigger than anticipated -425 bp in July. Usd/Try is back above 5.7300 in contrast to Usd/Zar that is now under 14.7500 irrespective of more warnings from the ratings agencies about aid for SA’s power company Eskom and S&P advising caution when restructuring the firm’s bonds.

In Commodities, Brent and WTI prices are firmer this morning, with both WTI and Brent having successfully surpassed the USD 57.00/bbl and USD 62.00/bbl marks at best thus far. Nothing too fresh in the way of fundamental news flow this morning, but weekend reports showed that Saudi Energy Minister Al Falih has been replaced by Prince Abdulaziz; PVM indicate that no changed is to be expected in the current strategy of OPEC and if anything this may strengthen their resolve to balance markets. Other energy minister comments from Secretary General Barkindo that the JMMC could debate potential new production targets, meeting is scheduled for September 12th. The complex may have derived some support this morning from renewed geopolitical tensions via Iran, who have told the IAEA that they intend to produce enriched uranium with advanced centrifuges and as such would breach the nuclear deals imposed ban. Although, gold has failed to generate too much in the way of support from these comments with the yellow metal little changed on the day and still holding above the USD 1500/oz mark going into a critical week for markets courtesy of the ECB on Thursday. Separately, China’s Iron imports increased 6% YY to their highest since January 2018, which ING note is due to increasing shipments from Australia and amidst a recovery in Brazilian exports.

US Event Calendar

- 3pm: Consumer Credit, est. $16.0b, prior $14.6b

DB’s Jim Reid concludes the overnight wrap

I hope you had a good weekend. We had a joint 4th birthday and house warming party and after having 50 plus toddlers creating havoc I think it might be easier to just get the builders back in and start again with the refurb rather than tidy up. This weekend might go down as the one where Maisie lost all sense of reality though as every parent brought her a present. She now has a room full of gifts ahead of her actual birthday next week. Also given we invited 50 kids I’m worried that we’ll get invited back to around 50 4th birthday parties over the next year. There goes my weekly game of golf… and my savings!!

If last week was back to school with a bang with Brexit and a bond market sell-off the highlights, this coming week has plenty more potential ‘boom’ moments. The ECB on Thursday will be hard to top but today’s trip to Dublin from UK PM Johnson and the subsequent election vote later in Parliament (highly likely to be defeated) will be fascinating and in data terms the highlights are US CPI (Thursday) and Friday’s US retail sales and UoM consumer confidence which last month fell to the lowest since October 2016.

With regards to the ECB, this will be President Draghi’s penultimate press conference before his term comes to an end. Our economists expect the ECB to cut interest rates by 10bps at Thursday’s policy meeting. They also anticipate a new system of reserve tiering, where some subset of reserves are exempted from the cost of negative interest rates, plus an enhanced version of forward guidance.While a shift to a symmetric inflation target or to a price level target would almost certainly be too radical for them to consider without a deeper policy review, they are likely to commit to some form of “lower for longer” rate guidance. There are also risks that they cut by more than 10bps, given the apparent lack of pushback by hawkish members of the Governing Council against a rate cut. There was more public pushback over the last few weeks against asset purchases, so that may be harder to agree on. Our economists nevertheless think a €30 billion per month purchase program is possible, though they could also see a more generous form of TLTROs if the ECB wants to focus on credit easing instead of measures that may flatten the curve. Their full preview is available here .

Staying with our economists views, on Friday, Matt Luzzetti and the US econ team updated their economic forecasts to reflect the latest trade news (full note here ). Though they had included a trade war escalation in their forecasts, the current conflict has exceeded their expectations and they now expect growth to slow more sharply. They forecast Q4/Q4 GDP growth of 1.9% and 1.8% for this year and next, down from 2.0% and 2.2%. As a result, they expect unemployment to rise a bit to 4.3% next year which will translate to below-target inflation for the next several quarters. To combat this, they add another 50bps of Fed rate cuts to their expectations; they now see 100bps of cuts over the next several months, including cuts at the September, October, December, and January meetings. The most interesting comment in the piece is that they believe trade developments have neared a tipping point. Their baseline expects that data and risk assets will weaken enough over the coming months to pull the US administration back from further escalations. If not though they think a mild recession is possible and taking the Fed Funds rate to zero.

Turning to Brexit, events are expected to continue to journey into the unknown this week. A vote in the House of Commons to hold an election will likely get defeated today with the opposition parties trying to force Mr Johnson into asking the EU for an extension. The weekend papers were full of talk about the government working out whether they could sidestep the law with the Sunday Times reporting that the PM wants to even use the Supreme Court as an option. There was also talk of a PM resignation as one option being considered and even talk of the PM actively disobeying the law and perhaps facing a potential prison sentence if he does. As for the polls, after a torrid time in Westminster for the PM last week and over the weekend with another cabinet and party resignation, the Conservation Party have generally maintained their lead (between 3 and 14pts lead over 6 polls) but one poll suggested that if Brexit didn’t happen by October 31st then the lead would reverse and Labour would take a 2 point lead. This highlights why the opposition are gambling on denying an election this side of that date. The polls also show that hard tactics in Westminster are not necessarily damaging the governments support. However, the collateral damage to the party is significant so it’s high stakes for everyone.

Turning to Asia, over the weekend we got China’s August trade data with the trade balance reportedly standing at $34.8bn (vs. $44.3bn expected) primarily due to exports declining unexpectedly(-1.0% yoy vs. +2.2% yoy expected) while imports fell -5.6% yoy (vs. -6.4% yoy expected). In terms of trade with the US, exports stood at $37.3bn (-16.0% yoy) while imports stood at $10.4bn (-22.2% yoy) bringing the trade balance to $26.7bn (-13.2% yoy). Meanwhile, in Japan, this morning the final Q2 annualized GDP growth rate came in line with expectations and 0.5pp lower than the initial read at +1.3% qoq.

Although China’s trade data was soft, Friday’s RRR cut by the PBoC has helped equity markets to post modest gains this morning with the Shanghai Comp (+0.36%) and CSI 300 (+0.27%) both up. The Kospi (+0.45%) and Nikkei (+0.67%) have also risen while the Hang Seng (-0.08%) is struggling for traction a little. Meanwhile, futures on the S&P 500 are up +0.20% and WTI oil prices are up +1.11% following the news that Saudi Arabia has replaced its long-time energy minister before an OPEC+ committee meeting this week in Abu Dhabi.

As for markets on Friday, the two big risk events passed without really rocking the boat. The August jobs report showed a slightly weaker-than-expected headline number at 130,000, plus downward revisions of 20,000 to the previous two months. However, wage growth was stronger than expected at +0.4% mom and +3.2% yoy. So a bit of a wash, though yields did fall several basis points from their earlier highs. Separately, Fed Chair Powell spoke in Switzerland, the last official communication before the Fed’s media blackout period before their September 18 meeting. He said the latest payrolls report is consistent with a good economic outlook, but highlighted “significant risks.” That basically confirmed expectations for a 25bps cut later this month.

The S&P 500 ended the week +1.79% higher (+0.09% Friday), while the DOW posted a similar gain of +1.49% (+0.25% Friday). The NASDAQ gained +1.76% on the week, but lagged on Friday (-0.17%) as large-cap tech firms were hit by new reports of antitrust investigations. The NYFANG index ended +2.19% on the week (-0.72% Friday). European equities outperformed, with STOXX 600 and DAX up +2.02% and +2.11% (+0.32% and +0.54% Friday) respectively. Bank stocks were helped by higher rates, with indexes of European and US bank shares up +3.93% and +1.74% (+0.01% and -0.42% Friday).

The move in yields wasn’t eye-watering outside of a big move on Thursday, but it was still the biggest weekly selloff in eight weeks for the major benchmarks. Bunds, treasuries, and gilts ended +6.2bps, +6.4bps, and +2.7bps (-4.4bps, +0.02bps, and -9.4bps Friday) respectively. Front-end US rates increased less, with the 2-year yield up +3.6bps (+1.4bps Friday), taking the 2y10y yield curve back into positive territory after last month’s brief inversion. It ended +2.8bps steeper at 1.4bps (-1.5bps Friday). The dollar weakened -0.91% (-0.41% Friday), while EMs outperformed, with an index of EM currencies gaining +1.36% (+0.21% Friday). Credit yields were tighter in the US, with HY cash spreads -12bps narrower (-5bps Friday), though they widened in Europe by +9bps (+6bps Friday). US IG spreads traded flat, despite the largest week of issuance on record. Staying with credit on Friday Craig published a piece on US HY where he highlights the quite amazing statistic that is 2019 YTD is the only year where by HY has returned at least 10% but BBs have outperformed CCCs, both in total and excess return terms. The note touches on some of the reasons why and looks at whether the CCC/BB is a reliable leading indicator.

3A/ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 25.14 POINTS OR 9.84% //Hang Sang CLOSED DOWN 9.36 POINTS OR 0.04% /The Nikkei closed UP 118.85 POINTS OR 0.56%//Australia’s all ordinaires CLOSED UP .11%

/Chinese yuan (ONSHORE) closed DOWN at 7.1259 /Oil UP TO 56/72 dollars per barrel for WTI and 61.81 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1259AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1211 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

Is China using Fentanyl as a “Chemical warfare: against the USA.?Tons of this deadly drug continues to enter into the uSA. China is refusing to stop it in the same manner as the opiods wars started at the end of the 18th Century.China lost and that is how HOng Kong became a British colony.

(zerohedge)

China Is Using Fentanyl As “Chemical Warfare” Against US, Experts Say

After President Trump’s recent disappointment at China’s lack of progress in stalling fentanyl exports to the US, increasingly outspoken anti-China activist Kyle Bass is highlighting the potential return of ‘Opium Wars’ as an intentional attack on Americans.

“The Opium Wars, beginning in the late 18th century, took China from the world’s largest economy to less than half afterwards. China is using [the same] asymmetric chemical warfare against the United States.

We lost 2,977 lives (net of the 19 hijackers who don’t matter) in the Sept 11th attacks. We now lose 50,000 people per year to opioid overdoses. That’s almost 7 deaths per hour every day every year. China is responsible for 90% of fentanyl coming into our country.

Chinese killing of US citizens through fentanyl exports is the functional equivalent of more than 10 Sept 11th attacks each year. When will our entire government realize that china’s communist party is our mortal enemy? When will we disengage with the murderous regime?“

And, as The Epoch Times’ Bowen Xiao details, behind the deadly opioid epidemic ravaging communities across the United States lies a carefully planned strategy by a hostile foreign power that experts describe as a “form of chemical warfare.”

It involves the production and trafficking of fentanyl, a synthetic opioid that caused the deaths of more than 32,000 Americans in 2018 alone, and fentanyl-related substances.

China is the “largest source” of illicit fentanyl in the United States, a November 2018 report by the U.S.-China Economic and Security Review Commission stated. That same commission said that since its 2017 report, they found no “substantive curtailment” of fentanyl flows from China to the United States. They also noted that in “large part, these flows persist due to weak regulations governing pharmaceutical and chemical production in China.”

President Donald Trump has continued to increase his crackdown on fentanyl—he recently ordered all U.S. carriers to “search for and refuse” international mail deliveries of the synthetic opioid pain reliever. Trump specifically named FedEx, Amazon, UPS, and the U.S. Postal Service (USPS).

Jeff Nyquist, an author and researcher of Chinese and Russian strategy, said China is using fentanyl as a “very effective tool.”

“You could call it a form of chemical warfare,” Nyquist told The Epoch Times.

“It opens up a number of opportunities for the penetration of the country, both in terms of laundering money and in terms of blackmail against those who participate in the trade and become corrupt like law enforcement, intelligence, and government officials.”

China also uses the money generated by the importing of fentanyl to effectively “influence political parties,” according to Nyquist.

“It opens doors for Chinese influence operations, Chinese People’s Liberation Army, and intelligence services, so that they can get control of certain parts of the U.S.,” he said.

In August, Trump called out Chinese leader Xi Jinping, accusing him of not doing enough to stop the flow of fentanyl, which enters the United States mostly via international mail.

Liu Yuejin, vice commissioner of the China National Narcotics Control Commission, disputed Trump’s criticism, telling reporters on Sept. 3 that they had started going after illicit fentanyl production, according to state-controlled media. China also denies that most of the illicit fentanyl entering the United States originates in China.

“President Xi said this would stop—it didn’t,” Trump said on Twitter on Aug. 23.

Overdose deaths from synthetic opioids such as fentanyl surged from around 29,000 in 2017 to more than 32,000 in 2018, according to data from the Centers for Disease Control and Prevention (CDC).

Not all opioid-related deaths in the United States can be blamed on China’s fentanyl export policies, as some come from prescription overdoses, according to Dr. Robert J. Bunker, an adjunct research professor at the U.S. Army War College Strategic Studies Institute.

But Bunker told The Epoch Times that China is still “greatly contributing” to America’s opioid epidemic. Bunker described how Beijing is using the trafficking of dangerous drugs to achieve its greater Communist Party goals.

“Contributing to a major health crisis in the U.S., while simultaneously profiting from it would in my mind give long-term CCP plans to establish an authoritarian Chinese global system as a challenge to Western liberal democracy,” he said via email.

“[It’s] a win-win situation for the regime,” he continued. “In fact producing and sending fentanyl to the U.S., which could be considered a low-risk policy of ‘drug warfare,’ is very much in line with the means and methods advocated in the 1999 work ‘Unrestricted Warfare.’”

The book mentioned by Bunker is authored by two of China’s air force colonels, Qiao Liang, and Wang Xiangsui, and published by the People’s Liberation Army.

Local police, fire department, and deputy sheriffs help a man who is overdosing in the Drexel neighborhood of Dayton, Ohio, on Aug. 3, 2017. It’s unclear what he overdosed on. (Benjamin Chasteen/The Epoch Times)

Recent cases of fentanyl-related overdose and deaths are linked to “illegally made fentanyl,” the CDC has said. Fentanyl has been approved for treating severe pain for conditions such as late-stage cancer. Fentanyl is 50 times more potent than heroin and 100 times more potent than morphine. It is prescribed by doctors through transdermal patches or lozenges.

A USPS spokesman told The Epoch Times they are “aggressively working” to add in provisions from the STOP Act. The Synthetics Trafficking and Overdose Prevention legislation, signed in 2018 by Trump, aims to curb the flow of opioids sent through the mail while increasing coordination between USPS and the U.S. Customs and Border Protection (CBP).

USPS has notified China’s postal operations that if any of their shipments don’t contain Advance Electronic Data (AED), they “may be returned at any time,” the spokesman said via email. CBP is also notifying air and ocean carriers to confirm that 100 percent of their postal shipment containers have AED before loading them onto their conveyance.

Recent Seizures

In August, law enforcement seized 30 kilograms (around 66 pounds) of fentanyl,among other narcotics as part of a major arrest operation over the course of three days.As a result, officers arrested 35 suspects for “conspiracy to distribute and possess with intent to distribute large amounts of heroin, fentanyl, cocaine, and cocaine base.”

G. Zachary Terwilliger, U.S. Attorney for the Eastern District of Virginia, said in a statement that the amount of fentanyl seized was enough to “kill over 14 million people.” One of the suspects in Virginia had ordered the fentanyl from a vendor in Shanghai and was receiving it at his residence through USPS, according to the indictment.

“The last thing we want is for the U.S. Postal Service to become the nation’s largest drug dealer, and there are people way above my pay grade working on that, but absolutely, it’s about putting pressure on the Chinese,”Terwilliger said.

CBP Enforcement Statistics reveal that fiscal year seizures of illicit fentanyl spiked from about one kilogram (2.2 pounds) in 2013 to nearly 1,000 kilograms (2,200 pounds) in 2018. The number of law enforcement fentanyl seizures in the United States also vaulted from about 1,000 in 2013 to more than 59,000 in 2017.

Also, in August, the Mexican navy found 52,000 pounds of fentanyl powder in a container from a Danish ship that was coming from Shanghai. The navy intercepted the unloaded 40-foot container on Aug. 24, at the Port of Cardenas.

“There is clear evidence that fentanyl or fentanyl precursors, chemicals used to make fentanyl is coming from China,” Dr. Andrew Kolodny, co-director of Opioid Policy Research at the Heller School for Social Policy and Management, told The Epoch Times.

A fatal dose of fentanyl displayed next to a penny. (DEA)

Two commonly used fentanyl precursors are chemicals called NPP and 4-ANPP. In early 2017, journalist Ben Westhoff started researching the chemicals, finding many advertisements for them all over the internet from different companies. He later determined a majority of those companies were under a Chinese chemical company called Yuancheng, according to an excerpt from his upcoming book “Fentanyl, Inc.: How Rogue Chemists Are Creating the Deadliest Wave of the Opioid Epidemic,” an excerpt of which was published in The Atlantic.

Fentanyl Analogs

One of the concerns related to the production of illicit opioids is the creation of fentanyl analogs, products that are similar to fentanyl and also simple to make.

“You can very easily manipulate the molecule and create a new fentanyl-like product that hasn’t been banned, that’s not technically illegal,” Kolodny told The Epoch Times.

“Some of the manufacturers, the folks creating the drugs, are aware of that.”

“We saw this with other synthetic drugs that are abused in the U.S., when law enforcement make the drug illegal or when they ban the molecule,” he said. “In some cases, fentanyl analogs are even stronger than fentanyl. There’s an analog called carfentanil, which is even more potent than fentanyl.”