GOLD:$1492.00 DOWN $11.25 (COMEX TO COMEX CLOSING)

Silver:$18.11 UP 2 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1485.50

silver: $18.00

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 17/51

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,502.200000000 USD

INTENT DATE: 09/09/2019 DELIVERY DATE: 09/11/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

118 H MACQUARIE FUT 2

661 C JP MORGAN 25

661 H JP MORGAN 17

686 C INTL FCSTONE 38

737 C ADVANTAGE 3 7

905 C ADM 10

____________________________________________________________________________________________

TOTAL: 51 51

MONTH TO DATE: 1,691

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 51 NOTICE(S) FOR 5100 OZ (0.1586 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1691 NOTICES FOR 169100 OZ (5.2597 TONNES)

SILVER

FOR SEPT

458 NOTICE(S) FILED TODAY FOR 2,290,000 OZ/

total number of notices filed so far this month: 7447 for 37,235,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10230 DOWN 730

Bitcoin: FINAL EVENING TRADE: $ 9967 DOWN 330

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 1599 CONTRACTS FROM 216,199 UP TO 217,798 DESPITE THE 6 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

SEPT: 0FOR DEC: 1427, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1427 CONTRACTS. WITH THE TRANSFER OF 1427 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1427 EFP CONTRACTS TRANSLATES INTO 7.135 MILLION OZ ACCOMPANYING:

1.THE 6 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

39.535 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE HAD NO DOUBT SOME COVERING OF BANKER SHORTS AGAIN AT THE SILVER COMEX ON FRIDAY WITH THE HUGE RAID ORCHESTRATED BY THE CROOKED BANKERS AT 12:30 PM EST. HOWEVER IN CONTRAST TO THURSDAY, TOTAL OI INCREASED DRAMATICALLY DESPITE THE FURTHER DRUBBING IN PRICE OF OUR SILVER METAL WITH THE ABOVE AFOREMENTIONED RAID.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

15,462 CONTRACTS (FOR 6 TRADING DAYS TOTAL 15,462 CONTRACTS) OR 77.310 MILLION OZ: (AVERAGE PER DAY: 2577 CONTRACTS OR 14.045 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 77.310 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.03% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1627.03 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1599, DESPITE THE 6 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1427 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 3026 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1599 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1419 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 6 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.09 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.089 BILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 458 NOTICE(S) FOR 2,290,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 39.535 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1741 CONTRACTS, TO 617,795 DESPITE THE $4.75 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2968 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 2958 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 617,795,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3709 CONTRACTS: 741 CONTRACTS INCREASED AT THE COMEX AND 2968 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 3709 CONTRACTS OR 370,900 OZ OR 11.53 TONNES. YESTERDAY WE HAD A LOSS OF $4.75 IN GOLD TRADING….AND WITH THAT LOSS IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 11.53 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON TRYING TO CONTAIN GOLD’S PRICE AS WELL AS ATTEMPTING TO FLEECE SOME UNSUSPECTING LONGS.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 48,636 CONTRACTS OR 4,863,600 oz OR 151.27 TONNES (6 TRADING DAY AND THUS AVERAGING: 8106 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAYS IN TONNES: 151.27 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 151.27/3550 x 100% TONNES =4.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4302.89 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A SMALL SIZED INCREASE IN OI AT THE COMEX OF 741 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($4.75)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2968 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2968 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED GAIN OF 3709 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2968 CONTRACTS MOVE TO LONDON AND 741 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 11.53 TONNES). ..AND THIS GOOD INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $4.75 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 51 notice(s) filed upon for 5100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $11.25 TODAY//(COMEX-TO COMEX)

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD

A PAPER WITHDRAWAL OF 7.33 TONNES OF WHICH IS USED IN THE RAID YESTERDAY/TODAY

INVENTORY RESTS AT 882.42 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 2 CENTS TODAY: THE CROOKS ARE AT IT AGAIN!!

ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A “PAPER” WITHDRAWAL OF 1.778 MILLION OZ OF SILVER

FROM THE SLV/THIS WAS USED TO CONTAIN SILVER TODAY.

/INVENTORY RESTS AT 379.401 MILLION OZ.

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GOOD SIZED 1599 CONTRACTS from 216,199 UP TO 217,798 AND CLOSER TO A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1427: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1427 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1599 CONTRACTS TO THE 1427 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD SIZED GAIN OF 3026 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 15.13 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 39.535 MILLION OZ/

RESULT: A GIGANTIC SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 6 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A GOOD SIZED 1427 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 3.54 POINTS OR 0.12% //Hang Sang CLOSED UP 2.28 POINTS OR 0.01% /The Nikkei closed UP 73.68 POINTS OR 0.35%//Australia’s all ordinaires CLOSED DOWN .47%

/Chinese yuan (ONSHORE) closed UP at 7.1054 /Oil UP TO 58.21 dollars per barrel for WTI and 63.08 for Brent. Stocks in Europe OPENED RED EXCEPT GERMAN DAX// ONSHORE YUAN CLOSED UP // LAST AT 7.1054 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.1061 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

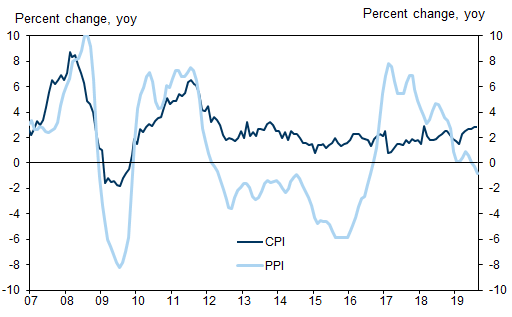

i)A good commentary explaining why the millenials are protesting big time in Hong Kong: the expensive cost of housing

(zerohedge)

ii)This does not bode well. China’s Xi just cannot believe what Trump is saying to him.

iii)Kyle Bass believes that Jack Ma, chairman of Alibaba will be either jailed or disappeared within one year as Xi does not like Ma’s strength in the financial community. If this were to come to pass, then that would end the Shanghai stock market ec.(Kyle Bass/zerohedge)

iv)China removes the 300 billion dollar Foreign Investment Limits for stock and bond markets..but nobody cares as already it was only 1/3 used

(zerohedge)

v)China vows to crush all pro democracy protesters in Hong Kong. They also warn the USA and other foreign nations against any influence in Hong Kong

4/EUROPEAN AFFAIRS

i)UK

As expected the UK parliament votes down an early election mainly because most of the remainers will lose their seat.

I think that BoJO knows what he is doing. Follow Mish Shedlock’s view of how this thing will proceed

(zerohedge)

ii)Bill Blain explains what is worrying him today

(Bill Blain)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)Pam and Russ Martens on the truth of stock market gains

(Pam and Russ Martens/Wall Street on Parade)

ii)GATA chairman Bill Murphy describes gold’s assent despite the dollar’s rise.

(courtesy GATA)

iii)Ed Steer highlights the brazen raid on all four 4 precious metals last Friday.

(ed Steer)

iv)This is good. Mark Mobius is now bullish on gold

(Kitco)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

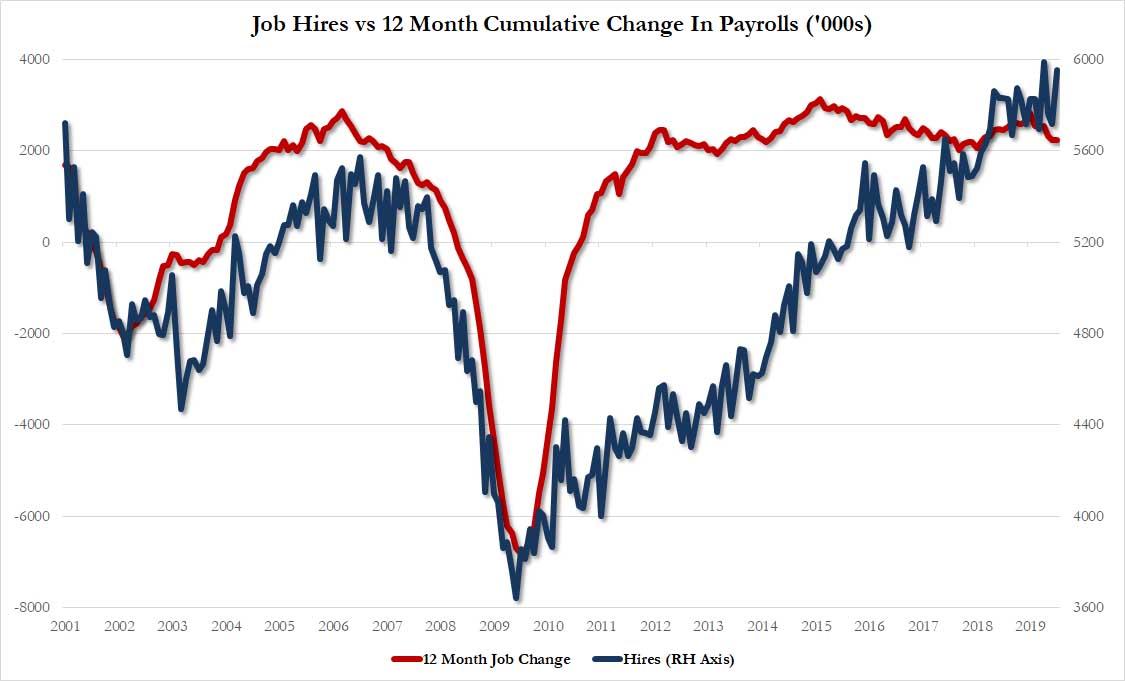

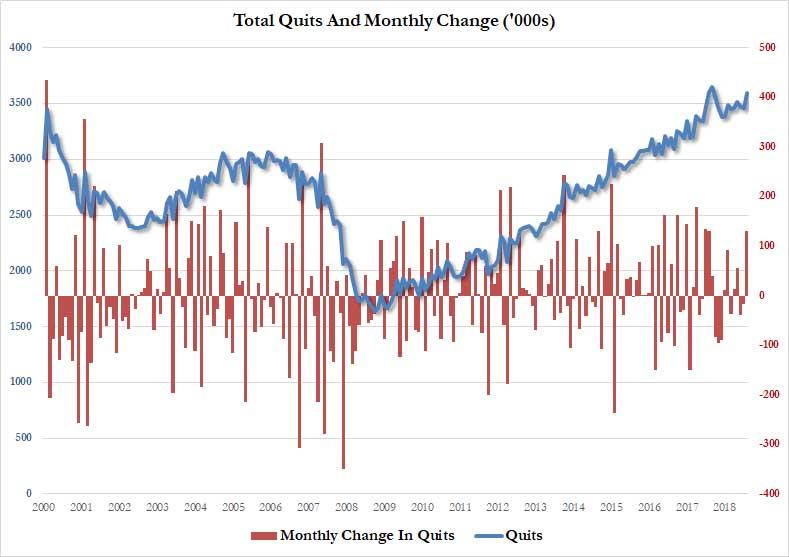

a)Another indicator that the uSA economy is faltering: job openings decline big time. Hires rise but also quits surge

(JOLTS/zerohedge)

b)As promised to you, the fiscal deficit for this year ending this month will be in excess of 1 trillion dollars. However if you add in the off balance sheet auto loans and student loans, you get your 1.2 trillion true deficit

iii) Important USA Economic Stories

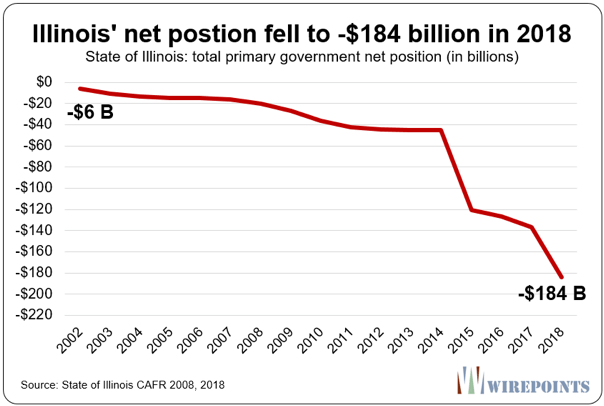

i)My goodness is Illinois bust!! They just recorded a huge 47 billion dollar loss due to understatement of pension liability

(zerohedge/Mark Glennon )

iv) Swamp commentaries)

a)This has to be a big joke: The Dems are now probing whether Trump and Guiliani pressured the Ukraine to hurt the Biden campaign even though the Bidens stole billions from the Ukraine

(zerohedge)

b)Another big joke the FBI was given huge evidence of a Clinton linked Libyra scheme, They ignored that and instead launched the phony Trump Russia mess

c)What took Trump so long? Bolton is finally fired and now the swamp is rid of one war mongerer

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 2123.385 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 114,807 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 143,898 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 143,878 CONTRACTS EQUATES to 719 million OZ 102% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.53% ((SEPT 10/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.15% to NAV (SEPT 6/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.53%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.05 TRADING 14.56/DISCOUNT 3.27

END

And now the Gold inventory at the GLD/

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 10/2019/ Inventory rests tonight at 889.75 tonnes

*IN LAST 660 TRADING DAYS: 52.96 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 560- TRADING DAYS: A NET 113.69 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 10/2019:

Inventory 379.401 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.05/ and libor 6 month duration 2.04

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .01

XXXXXXXX

12 Month MM GOFO

+ 1.95%

LIBOR FOR 12 MONTH DURATION: 1.95

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.00

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

‘Protect Oneself’ From A ‘Paradigm Shift’ Akin to the 1930s With Gold Diversification – Ray Dalio

Diversify Well To Protect Oneself Against The Coming ‘Paradigm Shift’

by Ray Dalio, Bridgewater Associates

The most important forces that now exist are:

1) The End of the Long-Term Debt Cycle (When Central Banks Are No Longer Effective)

+

2) The Large Wealth Gap and Political Polarity

+

3) A Rising World Power Challenging an Existing World Power

=

The Bond Blow-Off, Rising Gold Prices, and the Late 1930s Analogue

In other words now

1) central banks have limited ability to stimulate,

2) there is large wealth and political polarity and

3) there is a conflict between China as a rising power and the US as an existing world power.

If/when there is an economic downturn, that will produce serious problems in ways that are analogous to the ways that the confluence of those three influences produced serious problems in the late 1930s.

Before I get into the meat of what I hope to convey, I will repeat my simple timeless and universal template for understanding and anticipating what is happening in the economy and markets.

My Template

There are four important influences that drive economies and markets:

- Productivity

- The short-term debt/business cycle

- The long-term debt cycle

- Politics (within countries and between countries).

There are three equilibriums:

- Debt growth is in line with the income growth required to service the debt,

- The economy’s operating rate is neither too high (because that will produce unacceptable inflation and inefficiencies) nor too low (because economically depressed levels of activity will produce unacceptable pain and political changes), and

- The projected returns of cash are below the projected returns of bonds, which are below the projected returns of equities and the projected returns of other “risky assets.”

And there are two levers that the government has to try to bring things into equilibrium:

- Monetary policy

- Fiscal policy

The equilibriums move around in relation to each other to produce changes in each like a perpetual motion machine, simultaneously trying to find their equilibrium level. When there are big deviations from one or more of the equilibriums, the forces and policy levers react in ways that one can pretty much expect in order to move them toward their equilibriums.

For example, when growth and inflation fall to lower than the desired equilibrium levels, central banks will ease monetary policies which lowers the short-term interest rate relative to expected bond returns, expected returns on equities, and expected inflation. Expected bond returns, equity returns, and inflation themselves change in response to changes in expected conditions (e.g. if expected growth is falling, bond yields will fall and stock prices will fall).

These price changes happen until debt and spending growth pick up to shift growth and inflation back toward inflation. And of course all this affects politics (because political changes will happen if the equilibriums get too far out of line), which affects fiscal and monetary policy. More simply and most importantly said, the central bank has the stimulant which can be injected or withdrawn and cause these things to change most quickly.

Fiscal policy, which changes taxes and spending in politically motivated ways, can also be changed to be more stimulative or less stimulative in response to what is needed but that happens in lagging and highly inefficient ways.

For a simpler explanation of this template see my 30-minute animated video “How the Economic Machine Works” and for a more comprehensive explanation see my book Understanding the Principles of Big Debt Crises, which is available free as a PDF here or in print on Amazon. Also, to learn more about our extensive debt cycle research, please visit our debt crises research library on Bridgewater.com.

Looking at What Is Happening Now in the Context of That Template

Regarding the above template and where we are now, in my opinion, the most important things that are happening (which last happened in the late 1930s) are

a) we are approaching the ends of both the short-term and long-term debt cycles in the world’s three major reserve currencies, while

b) the debt and non-debt obligations (e.g. healthcare and pensions) that are coming at us are larger than the incomes that are required to fund them,

c) large wealth and political gaps are producing political conflicts within countries that are characterized by larger and more extreme levels of internal conflicts between the rich and the poor and between capitalists and socialists,

d) external politics is driven by the rising of an emerging power (China) to challenge the existing world power (the US), which is leading to a more extreme external conflict and will eventually lead to a change in the world order, and [Ian Bremmer calls this the return of a bi-polar world but with significant differences in the goals of the powers—JM]

e) the excess expected returns of bonds is compressing relative to the returns on the cash rates central banks are providing.

As for monetary policy and fiscal policy responses, it seems to me that we are classically in the late stages of the long-term debt cycle when central banks’ power to ease in order to reverse an economic downturn is coming to an end because:

- Monetary Policy 1 (i.e. the ability to lower interest rates) doesn’t work effectively because interest rates get so low that lowering them enough to stimulate growth doesn’t work well,

- Monetary Policy 2 (i.e. printing money and buying financial assets) doesn’t work well because that doesn’t produce adequate credit in the real economy (as distinct from credit growth to leverage up investment assets), so there is “pushing on a string.” That creates the need for…

- Monetary Policy 3 (large budget deficits and monetizing of them) which is problematic especially in this highly politicized and undisciplined environment.

More specifically, central bank policies will push short-term and long-term real and nominal interest rates very low and print money to buy financial assets because they will need to set short-term interest rates as low as possible due to the large debt and other obligations (e.g. pensions and healthcare obligations) that are coming due and because of weakness in the economy and low inflation.

Their hope will be that doing so will drive the expected returns of cash below the expected returns of bonds, but that won’t work well because:

a) these rates are too close to their floors,

b) there is a weakening in growth and inflation expectations which is also lowering the expected returns of equities,

c) real rates need to go very low because of the large debt and other obligations coming due, and

d) the purchases of financial assets by central banks stays in the hands of investors rather than trickles down to most of the economy (which worsens the wealth gap and the populist political responses).

This has happened at a time when investors have become increasingly leveraged long due to the low interest rates and their increased liquidity. As a result we see the market driving down short-term rates while central banks are also turning more toward long-term interest rate and yield curve controls, just as they did from the late 1930s through most of the 1940s.

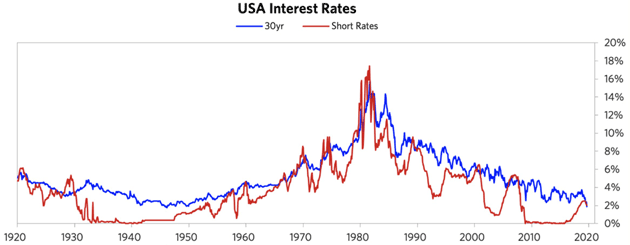

To put this interest rate situation in perspective, see the long-term debt/interest rate wave in the following chart. As shown below, there was a big inflationary blow-off that drove interest rates into a blow-off in 1980–82. During that period, Paul Volcker raised real and nominal interest rates to what were called the highest levels “since the birth of Jesus Christ,” which caused the reversal.

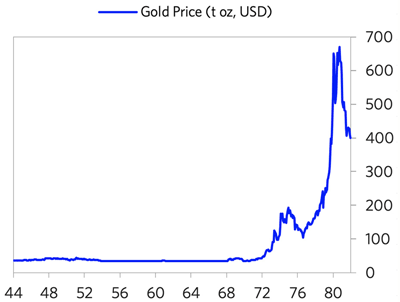

During the period leading into the 1980–82 peak, we saw the blow-off in gold. The below chart shows the gold price from 1944 (near the end of the war and the beginning of the Bretton Woods monetary system) into the 1980–82 period (the end of the inflationary blow-off). Note that the bull move in gold began in 1971, when the Bretton Woods monetary system that linked the dollar to gold broke down and was replaced by the current fiat monetary system. The de-linking of the dollar from gold set off that big move. During the resulting inflationary/gold blow-off, there was the big bear move in bonds that reversed with the extremely tight monetary policies of 1979–82.

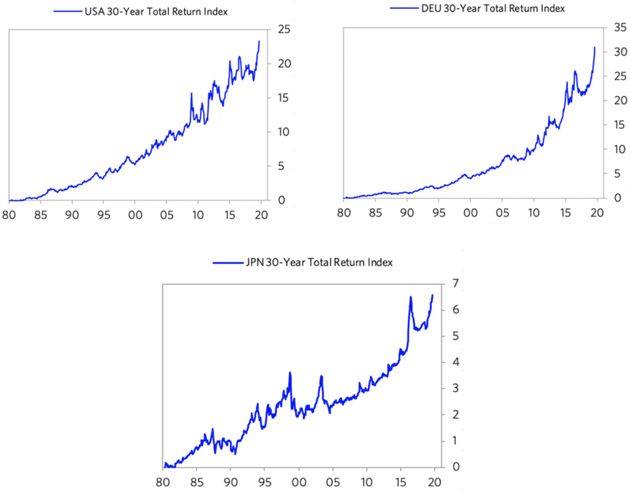

Since then, we have had a mirror-like symmetrical reversal (a dis/deflationary blow-off). Look at the current inflation rates at the current cyclical peaks (i.e. not much inflation despite the world economy and financial markets being near a peak and despite all the central banks’ money printing) and imagine what they will be at the next cyclical lows. That is because there are strong deflationary forces at work as productive capacity has increased greatly. These forces are creating the need for extremely loose monetary policies that are forcing central banks to drive interest rates to such low levels and will lead to enormous deficits that are monetized, which is creating the blow-off in bonds that is the reciprocal of the 1980–82 blow-off in gold. The charts below show the 30-year T-bond returns from that 1980–82 period until now, which highlight the blow-off in bonds.

To understand the current period, I recommend that you understand the workings of the 1935–45 period closely, which is the last time similar forces were at work to produce a similar dynamic.

Please understand that I’m not saying that the past is prologue in an identical way. What I am saying that the basic cause/effect relationships are analogous:

a) approaching the ends of the short-term and long-term debt cycles, while

b) the internal politics is driven by large wealth and political gaps, which are producing large internal conflicts between the rich and the poor and between capitalists and socialists, and

c) the external political conflict that is driven by the rising of an emerging power to challenge the existing world power, leading to significant external conflict that eventually leads to a change in the world order.

As a result, there is a lot to be learned by understanding the mechanics of what happened then (and in other analogous times before then) in order to understand the mechanics of what is happening now.

It is also worth understanding how paradigm shifts work and how to diversify well to protect oneself against them.

by Ray Dalio, Bridgewater Associates, August 28, 2019 via Linkedin

RELATED CONTENT

Bitcoin “Is A Bubble” but Gold Is Money Says World’s Biggest Hedge Fund Manager

Dalio Warns Of Dollar Crisis – “History Is Doomed To Repeat Itself”

NEWS and COMMENTARY

Gold pulls back, suffer a 3-session skid

Gold edges up on rate cut bets, firmer equities limit upside

Top U.S. regulator warns over corporate debt, market risks

JPMorgan’s new “Volfefe” index tracks the impact of Trump’s tweets on markets

Three Big Issues Likely To Lead To Rising Gold Prices – Dalio on Linkedin

Ed Steer’s Gold & Silver Digest

Are Stock Markets Really Setting New Highs?

Can Mario Draghi save the eurozone all over again?

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

09-Sep-19 1509.95 1509.20, 1223.81 1220.34 &1368.62 1364.92

06-Sep-19 1504.95 1523.70, 1223.52 1237.09 & 1363.94 1378.49

05-Sep-19 1542.60 1529.10, 1257.06 1238.72 & 1397.44 1380.78

04-Sep-19 1538.80 1546.10, 1265.05 1269.97 & 1397.69 1403.86

03-Sep-19 1532.45 1537.85, 1278.06 1277.80 & 1400.35 1403.44

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

29-Aug-19 1536.65 1540.20, 1260.51 1262.96 & 1387.29 1392.03

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Pam and Russ Martens on the truth of stock market gains

(Pam and Russ Martens/Wall Street on Parade)

(courtesy GATA)

iii) Other physical stories:

This is good. Mark Mobius is now bullish on gold

(Kitco)

|

|

Mark Mobius, founder of Mobius Capital Partners LLP

|

Friday, in an interview with CNBC, Mobius reiterated his bullish outlook on gold and said that all investors should have at least 10% of their portfolio in physical gold.

“Physical gold is the way to go, in my view, because of the incredible increase in money supply,” said Mobius, in the interview. “All the central banks are trying to get interest rates down, they are pumping money into the system. Then, you have all of the cryptocurrencies coming in, so nobody really knows how much currency is out there.”

Last month, Mobius told Bloomberg TV that investors should buy gold at any level because the price is going “up, up, up.”

His latest comments to CNBC come as gold prices hold critical support above $1,500 an ounce. December gold futures last traded at $1,510.60 an ounce, down 0.36% on the day. The yellow metal is down from last month’s six-year high.

Mobius added that the recent strength in the U.S. dollar could be the spark that ignites a global currency war. Although off its recent highs, the U.S. Dollar Index continues to hold near a two-year high, trading over 98 points.

Mobius said the dollar could start to slide as the Trump administration voices its support for a weak U.S. dollar in an attempt to boost U.S. exports.

“They are certainly going to try to weaken the dollar against other currencies and of course, it’s a race to the bottom. Because, as soon as they do that, other currencies will also weaken,” said Mobius. “People are going to finally realize that you got to have gold, because all the currencies will be losing value.”

Because of its role as a stable global currency, Mobius said that central banks will continue to increase their holdings in the yellow metal. He added that China will continue to be a big gold buyer in the current environment.

Over the weekend, the People’s Bank of China reported that it increased its gold reserves by 6 tonnes in August. The Chinese central bank has purchased nearly 100 tonnes of gold since December.

“China is the biggest producer of gold to begin with. And then of course, they’ve been buying gold, so nobody really knows how much they have in the vaults,” said Mobius.

But it is more than just China buying. Data from the World Gold Council (WGC) shows that central banks have a ravenous demand for the yellow metal.

In the first half of the year, central banks bought 374.1 tonnes of gold — “the largest net H1 increase in global gold reserves in our 19-year quarterly data series,” the WGC said in a report published last month.

“Central banks, like other investors, sought safety in gold as they looked to protect themselves in the face of many looming risks,” the analysts said.

The WGC has also said that they don’t expect central bank gold buying to end anytime soon as global uncertainty and the threat of a global recession continues to loom on the horizon.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

US Futures Drift Higher On Chinese Invitation To Bagholders, Trade And Central Bank Optimism

There wasn’t the usual trade talk optimism overnight, nor central bank trial balloons that record low interest rates will be dragged even deeper into negative territory.

Instead, what helped send European equity markets and US equity futures back in the green after an overnight slump that pushed the Emini from 2,985 to 2,965, was news that China removed one more hurdle for foreign investment into its capital markets almost 20 years after it first allowed access, when Beijing scrapped quotas for approved foreign institutional investors in domestic bond and equity markets. This means that all those WeWork bagholders who may have lost a majority of their investments, can now go ahead and lose the other half by investing in China, where the auditors have a habit of “community adjusting” everything.

In any case, the news helped send the Emini back in the green from overnight session lows just after the European open..

… with global markets back to unchanged.

Meanwhile, what we said about no central bank trial balloons, well we were kidding, because just after 7am, Reuters leaked that the BOJ “may be open to debate additional easing”, because apparently the existing easing has worked so well. According to the report, the BOJ is considering taking rates further into negative territory if it decides to ease, but other options – such as tiering – also remain on the table, Reuters reports, citing unidentified people familiar. The BOJ’s decision on whether and when to ease is expected to be a close call; conclusion may not be final until the last minute which will be just after the Fed’s own rate cut announcement. Ultimately, the BOJ’s thinking is driven by the bank’s growing less confident about early pickup in global growth

Actually, it turns out that we were also kidding about the lack of trade optimism: according to Bloomberg, China’s Premier Li said that US and China should find a solution to the ongoing trade dispute, adding that he hopes (there’s that word again) that trade talks make progress.In response there was an immediate “risk on” move as European equity indices spiked higher as a result of these headlines with the DAX Sep’ 19 futures spiking higher to 12,265 from 12,235, while the crude complex and USD/JPY also saw positive ticks. That said, the sharp move higher in US equities was less pronounced and quickly faded.

The Stoxx Europe 600 Index dropped a second day, led by financial services and health-care shares, although it rebounded following the China Li and BOJ more easing news. The pound fluctuated as embattled British Prime Minister Boris Johnson insisted he won’t ask for another Brexit delay, while U.K. wage and unemployment data beat estimates. Most euro-zone sovereign bonds nudged lower as European Central Bank officials prepare to meet.

Earlier in the session, Asian stocks fluctuated, with energy producers advancing and health-care firms retreating. Markets in the region were mixed as investors assessed the global growth outlook and China-U.S. trade negotiations with South Korea up and Thailand down. The Topix climbed 0.4%, as Japanese banks contributed most to gains following a rebound in long-term U.S. Treasury yields, which in turn pushed JGB yields modestly higher as well. The Shanghai Composite Index edged down 0.1%, snapping a six-day rising streak, after China’s PPI fell further into contraction, threatening to add deflationary pressure to the global economy (See below) with Kweichow Moutai and Ping An Insurance Group among the biggest drags. The big news out of China, as noted above, is that global funds no longer need approvals to purchase quotas to buy Chinese stocks and bonds, the State Administration of Foreign Exchange said in a statement on Tuesday. It removed the $300 billion overall cap on overseas purchases of the assets, about two-thirds of which remain unused.

Also overnight, China reported that its headline CPI inflation was flat at 2.8% year-on-year in August, just above consensus expectations and close to the 3% policy target; in month-on-month terms, headline CPI inflation moderated to +2.9% in August from +3.5% in July. A bigger problem was the second consecutive print of negative year-over-year PPI inflation, which moderated further to -0.8% yoy in August, on both a high base (PPI up 3.6% mom s.a. ann in August 2018) and a sequential decline of 2.8% mom s.a. ann in August. Inflation in the ferrous metals sector slowed the most, followed by petroleum industry, suggesting corporate profits will be further depressed in coming months.

In emerging markets, a four-day rally in equities stalled and the risk premium on sovereign debt rose as investors marked time before the resumption of trade talks between China and the U.S. as well as central-bank meetings in coming days. Developing-nation stocks climbed almost 4% in the previous four days after China and the U.S. announced face-to-face negotiations aimed at ending the tariff war would be held in Washington next month. China, meantime, removed one more hurdle for foreign investment into its capital markets almost 20 years after it first allowed access, when it said Tuesday that global funds no longer need approvals to purchase quotas to buy Chinese stocks and bonds.

With the European Central Bank announcing its policy decision in Thursday and the Federal Reserve next up, investors are hoping on increased monetary stimulus to prop up markets. A gauge of emerging-market currencies gained for a fifth day, the longest streak since June, with South Africa’s rand leading the advance.

“Markets were oversold, rebounded and without any genuinely positive catalysts are faltering again,” said Julian Rimmer, a trader at Investec Bank in London. “Funds were clearly bearishly positioned over the summer with the salami slicing of global growth expectations, low volumes and the worldwide hunt for yield. Some of that negativity has diminished slightly so we had some short-covering and a bit more risk-on, but fundamentally nothing has changed and all those concerns are still apparent.”

In rates, European bond markets inched lower while the region’s stocks declined for a second day ahead of Thursday’s ECB policy announcement. Bear steepening resumed in the German curve although the long-end claws back some initial weakness to trade back at 0%. Peripheral spreads widened to core, with the long-end of the Spanish curve underperforming. Gilts drifted lower after robust domestic employment and wages data, but as ever, Brexit keeps any hawkish repricing in check.

The recent pullback in the bond rally “is a correction to an outsized move in yields during August, not a turn in the trend,” Kit Juckes, chief global FX strategist at Societe Generale SA, wrote in his daily note. “Last Friday’s U.S. labor market data show, clearly enough for me, that the U.S. economy is slowing slowly but steadily as the global trade slowdown infects it.”

In geopolitical news, North Korea launched 2 projectiles; a Japanese Defence Ministry official later commented that the latest North Korea missiles pose no immediate threat to Japan’s national security. Pakistani Foreign Minister has told UN Human Rights council that India’s “illegal Kashmir military occupation” raises spectre of “genocide”. Additionally, Pakistan’s Qureshi says that he sees ‘no possibility of a bilateral engagement with India’.

In FX, the Bloomberg Dollar Spot Index halted a five-day slide Tuesday as the yield on 10-year U.S. Treasuries fell 2bps, its first decline in five days. The only G-10 currency to climb against the dollar was the Swiss franc but moves were limited; meanwhile, the largest losses were seen by the Swedish krona, as the currency weakened by almost 1% to the dollar and the euro after Swedish inflation unexpectedly slowed to its lowest in three years, in more bad news for the Riksbank which is keen to increase interest rates. Finally, the Norwegian krone tumbled alongside its Swedish peer after similarly disappointing inflation reading.

Elsewhere, oil extended gains to the highest level in almost six weeks as Saudi Arabia’s new energy minister signaled his commitment to production cuts ahead of an OPEC+ meeting later this week. Gold headed for its fourth day of declines, sinking to around $1,495 an ounce. Sweden’s krona tumbled after the country’s inflation unexpectedly slowed.

Expected data include NFIB Small Business Optimism. HD Supply and Zscaler are reporting earnings

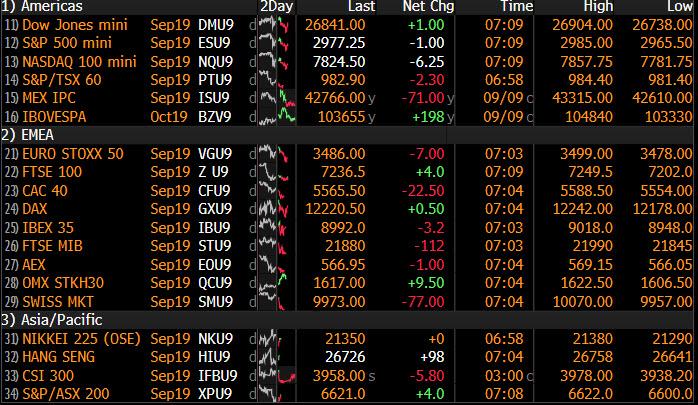

Market Snapshot

- S&P 500 futures down 0.1% to 2,973.75

- STOXX Europe 600 down 0.5% to 383.96

- MXAP down 0.01% to 156.79

- MXAPJ down 0.2% to 507.06

- Nikkei up 0.4% to 21,392.10

- Topix up 0.4% to 1,557.99

- Hang Seng Index up 0.01% to 26,683.68

- Shanghai Composite down 0.1% to 3,021.20

- Sensex up 0.4% to 37,145.45

- Australia S&P/ASX 200 down 0.5% to 6,614.06

- Kospi up 0.6% to 2,032.08

- Brent futures up 0.2% to $62.74/bbl

- Gold spot down 0.2% to $1,496.06

- U.S. Dollar Index up 0.1% to 98.41

- German 10Y yield rose 0.6 bps to -0.579%

- Euro down 0.05% to $1.1043

- Italian 10Y yield rose 6.6 bps to 0.603%

- Spanish 10Y yield rose 1.5 bps to 0.233%

Top Overnight News from Bloomberg

- After Parliament blocked his Brexit strategy, and then refused to give him the election he wanted, U.K. Prime Minister Boris Johnson is promising to work for a deal with the EU. Monday night saw him suffer his sixth consecutive defeat in a vote in the House of Commons, after his attempt to get approval for a snap poll was rejected for a second time

- The U.K. economy continued to create jobs over the summer and wages jumped, despite the escalating turmoil over Brexit. The jobless rate fell to the lowest since the 1970s but jitters weighing on the wider economy were appearing. Employment growth was weaker than forecast; vacancies slipped to the lowest since 2017

- Mario Draghi needs to go out with a bang if he’s to renew a surge in bond prices that sent yields to unprecedented lows. Markets have factored in the ECB slashing interest rates and restarting QE, so it will take a multi-faceted stimulus package in his penultimate meeting Thursday to impress investors

- Germany’s worship of fiscal discipline is being challenged by a looming recession and tantalizingly cheap credit — and a silent revolution is under way at the finance ministry to shed its economic dogma

- Executives of WeWork and its largest investor, SoftBank, are discussing whether to shelve plans for an initial public offering of the money-losing co-working company, said people with knowledge of the talks

- China removed one more hurdle for foreign investment into its capital markets almost 20 years after it first allowed access

Asian equity markets traded mixed as they followed suit to the indecisive tone seen on Wall St amid a sell-off in treasuries and as the region also digested ambiguous inflation figures from China. ASX 200 (-0.5%) was negative with gold miners frontrunning the declines in Australia after the precious metal slipped below the psychological key USD 1500/oz level but with further losses in the index stemmed by strength in the energy sector following the recent rally in oil prices, while Nikkei 225 (+0.4%) was kept afloat by favourable currency moves. Elsewhere, Hang Seng (Unch.) and Shanghai Comp. (-0.1%) gave back initial gains despite the liquidity efforts by the PBoC and firmer than expected Chinese inflation data, as the figures were largely influenced by a 10% increase in food prices amid the swine fever epidemic and also showed PPI at its sharpest contraction in 3 years. Finally, 10yr JGBs were lower following the bear-steepening seen in US and broad declines across global bonds, while the absence of the BoJ from the market today also added to the lacklustre demand.

Top Asian News

- North Korea Tests More Weapons After Floating Fresh U.S. Talks

- Hong Kong Leaders Grow More Frustrated by Leaderless Protesters

- Hong Kong Dollar Peg Questions Seen Fading One Way or Another

- Chinese Exporters Cut Currency Hedges in Sign of Yuan Pessimism

European equities are modestly softer [Eurostoxx 50 -0.3%] following on from a mixed Asia-Pac session as participants remain on standby ahead of Thursday’s ECB monetary policy decision. Sectors are mixed with underperformance in the IT sector, whilst energy names outperform as the oil complex holds onto its recent gains and banking names remain supported by yesterday’s surge in yields (RBS +4.4%, UBS +3.4%, Barclays +4.5%). In terms of stocks on the move, EDF (-7.5%) share fell from the open after the Co. noted deviations in technical standards governing the manufacture of nuclear-reactor components. On the flip side, Subsea 7 (+2.7%) shares opened higher after the Co. announced its current COO as the new CEO effective January 1st 2020, additionally the Co. were awarded an offshore contract in Saudi Arabia. Finally, JD Sports (+3%) shares are supported post earnings after H1 sales rose 47% Y/Y and the Co. forecasts FY results to be at the mid-point of their previously guided range.

Top European News

- EDF Flags Issues in Reactor Parts in Blow to Nuclear Industry

- Spanish Banks Risk Setback in Fight Over Unfair Mortgage Claims

- Germany Doesn’t Need to Splurge to Address Slowdown, Scholz Says

- Sweden Inflation Slows to 3-Year Low in Blow to Riksbank

In FX, the major underperformers in wake of softer than forecast Swedish and Norwegian inflation data that calls into question hawkish guidance from the Riksbank and Norges Bank. Eur/Sek has rebounded from sub-10.7000 levels through 10.7500 and breached several technical resistance points in the process, including 10 and 21 DMAs plus a Fib retracement, while Eur/Nok is back above 9.9000 from almost 9.8500 and also taking on board the latest Norges Bank regional network survey showing that contacts envisage slightly slower growth in the coming 6 months.

- USD – The Dollar is mixed to marginally firmer awaiting this week’s top-tier US data for more input ahead of the September FOMC after last Friday’s rather inconclusive BLS report and broadly upbeat comments from Fed chair Powell, on balance. However, the DXY remains rangebound between 98.260-463 and well within near term chart support and resistance not to mention recent highs and lows for the index.

- CHF/NZD/AUD – The Franc has pared some losses vs the Greenback and single currency as risk appetite wanes/falters and selling abates into key technical psychological markers, like 0.9950 in Usd/Chf and 1.1000 in Eur/Chf. Meanwhile, the Aussie and Kiwi have lost some momentum, with Aud/Usd drifting back towards 0.6850 in wake of a downturn in NAB business sentiment and dip in conditions overnight, and Nzd/Usd fading ahead of 0.6450 as Aud/Nzd meanders between 1.0645-85.

- GBP/CAD/JPY/EUR – Sterling staged another attempt to hunt out stops around 1.2385 vs the Buck and briefly crossed the 100 DMA against the Euro (0.8930), but failed to sustain momentum again amidst the ongoing UK political and Brexit paralysis. However, the ensuing Pound pull-back was arrested by more encouraging data as earnings beat consensus on a headline basis and the jobless rate eased to 3.8% from 3.9%. Note also, 2 bn option expiries in Cable at the 1.2300 strike have provided a buffer. Elsewhere, trade has been considerably more rangebound with the Loonie straddling 1.3175, Yen holding within 107.19-49 parameters and Euro stuck in a 1.1037-59 band awaiting Thursday’s ECB policy pronouncements for more direction.

- EM – Contrasting fortunes again for the Rand and Lira, as Usd/Zar continues its deep reversal from 15.0000+ towards 14.6900 regardless of more SA ratings warnings from Moody’s, but Usd/Try elevated above 5.7500 in the run up to this week’s CBRT rate verdict and heeding even more dovish calls (-500 bp touted in a Turkish paper) alongside the persistent threat of US sanctions.

In commodities, WTI and Brent futures are holding onto most of its recent gains with the two benchmarks around 58.00/bbl and 63/bbl respectively at the time of writing. News-flow for the complex has been light, although reports stated that Russia’s Energy Minister Novak will be meeting with newly appointed Saudi Energy Minister Abdulaziz in Jeddah later today to discuss the energy market alongside strengthening Saudi-Russia cooperation ahead of Thursday’s JMMC meeting. Meanwhile, Nigeria’s Finance Ministry notes of strong indications of an oil glut next year, and thus lowered its benchmark forecast to 55/bbl from 60/bbl. This evening will also see the release of EIA’s Short-Term Energy Outlook with focus on global demand growth forecasts. Looking further ahead, participants will also be eyeing the weekly API crude inventory data with markets expecting a headline drawdown of 2.5mln barrels. Elsewhere, gold prices are largely unchanged below the 1500/oz mark amid the undecisive risk tone in the market ahead of this week’s key events. Meanwhile, copper prices have seen a more pronounced downside compared to yesterday with the red-metal flirting with 2.60/lb to the downside at the time of writing. Finally, Dalian iron ore prices advanced as much as 4% amid expectations that China will ratify further economic stimulus that would boost steel demand.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 103.5, prior 104.7

- 10am: JOLTS Job Openings, est. 7,331, prior 7,348

DB’s Jim Reid concludes the overnight wrap

Every year in early September the financial world takes in a new breed of graduates and to you all I say welcome and good luck in your career. If you’d have started as a newbe last Thursday then the whole of your career would have been in a big bond bear market. You’d be excused for wondering if bonds ever actually rally. Indeed yesterday saw another fixed income sell-off, as reports on the German fiscal stance and positive comments on the US-China trade war supported investor sentiment. 10yr Bund yields rose +5.3bps, reaching their highest level in nearly a month at -0.59%, while 30y bunds rose +7.8bps but after spending much of the day in positive territory closed at -0.003%. Nearly but not quite. Lending to the German government out to 2049 will still involve a small haircut. For context the long run return on US equities has been around 9% p.a. over the last couple of hundred years and by my calculations that would mean you would earn 13 times your original investment over an average 30 year period through history. Even at the lower long run return for German equities of c.8% you would earn over 10 times your original investment over the same period. I’m not wildly excited about current equity valuations but this is food for thought for all you new graduates as you invest for your retirement. It’s too late for us but you can save yourselves.

The bond sell-off was global with 10y Treasuries up +7.7bps, BTPs up +6.7bps, and Gilts +8.5bps. Yield curves also steepened, with US 2s10s up +3.2bps to 4.9bps and to its highest level in three weeks. In credit, spreads widened in Europe, with Euro IG spreads +2.0bps and at a 7-week high, while Euro HY spreads were flat. In the US it was a different story as IG and HY spreads tightened further, down -1.3bps and -9bps respectively. Safe havens sold off across the board however, with gold down -0.53%, while the Swis Franc was the worst performing G10 currency, down -0.48% against the dollar, followed by the Japanese Yen (-0.32%).

The sell-off came as Reuters reported that Germany is considering creating a “shadow budget”, which would allow the government to get round the country’s fiscal rules. This would be done by setting up independent bodies, which could take advantage of the country’s low borrowing costs and invest in “infrastructure and climate protection”, but this spending would not count under the debt brake. Meanwhile, the euro strengthened after a letter obtained by Bloomberg News showed Bettina Hagedorn, a deputy finance minister, wrote that the government could change its plans to run balanced budgets if the economic situation required. The reports come ahead of this morning’s debate on the 2020 budget, which will be taking place in the Bundestag. These stories have become more frequent in recent weeks and whilst the market always gets more excited by the headlines than is justified by hard evidence of any change in policy, it’s fair to conclude that market pressure and chatter on this story is building.

Other drivers behind the bond sell-off included data which showed German exports unexpectedly rising by +0.7% (vs. -0.5% expected) in July, while imports fell by -1.5% (vs. -0.3% expected), sending the current account balance for July up to 22.1bn (vs. 16.4bn expected). So good news on exports even if declining imports might be demand led. Meanwhile comments from Secretary Mnuchin further helped things, as he said “we’ve made a lot of progress” in the trade talks, ahead of the planned meeting between China and the US in Washington next month. Ahead of Thursday’s much-anticipated ECB meeting, these positive developments seem to have marginally reduced the implied odds that markets have given to a larger 20bps reduction in the deposit rate, which now stand at 44%, having been at 61% just a week ago.

In equity markets, US stock indices were mixed with relatively high divergence between sectors. The S&P 500 ended just about flat (-0.01%) while the DOW gained +0.14%. Relatively more of the DOW is made up of bank stocks, which performed well (+3.15%) amid the higher yields. Tech lagged, with the NASDAQ down -0.19%. In Europe, the picture was similarly mixed, with the STOXX 600 losing -0.28%. Much of the fall came from UK stocks, with the FTSE 100 -0.72% as it reacted to sterling’s appreciation, but the CAC 40 (-0.27%) also declined, while the DAX and the FTSE MIB only made modest gains. European banks mirrored their American cousins’ positive performance, with the STOXX Banks up +2.72% on rising yields, while energy stocks also saw gains as Brent Crude rose +1.85% to reach a one-month high.

Overnight in Asia, markets are trading mixed with the Nikkei (+0.36%) and Kospi (+0.37%) both up while the Hang Seng (+0.08%) is trading flattish and the Shanghai Comp (-0.36%) is trading down. In Fx, all G10 currencies are slightly weaker against the greenback this morning with the exception of the New Zealand dollar (+0.19%). The onshore Chinese yuan is trading up c. 0.1% at 7.1164. Sovereign bond yields have ticked up in Asia this morning following the global sell-off with 10y JGB yields up +2.9bps at -0.234%. Elsewhere, futures on the S&P 500 are trading flattish (-0.06%) while WTI crude oil is up +0.45% after Saudi Arabia’s new energy minister signaled his commitment to production cuts ahead of an OPEC+ meeting on Thursday in Abu Dhabi to discuss their production pact. In terms of overnight data releases, China’s August CPI and PPI both came in one tenth higher than consensus at +2.8% yoy and -0.8% yoy, respectively.