GOLD:$1495.30 UP $5.30 (COMEX TO COMEX CLOSING)

Silver:$18.10 DOWN 1 CENT (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1496.40

silver: $18.12

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 7/22

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,490.300000000 USD

INTENT DATE: 09/10/2019 DELIVERY DATE: 09/12/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 11

661 H JP MORGAN 7

686 C INTL FCSTONE 9

737 C ADVANTAGE 7 4

905 C ADM 6

____________________________________________________________________________________________

TOTAL: 22 22

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 22 NOTICE(S) FOR 2200 OZ (0.0604 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1713 NOTICES FOR 171,300 OZ (5.3282 TONNES)

SILVER

FOR SEPT

156 NOTICE(S) FILED TODAY FOR 780,000 OZ/

total number of notices filed so far this month: 7603 for 38,015,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

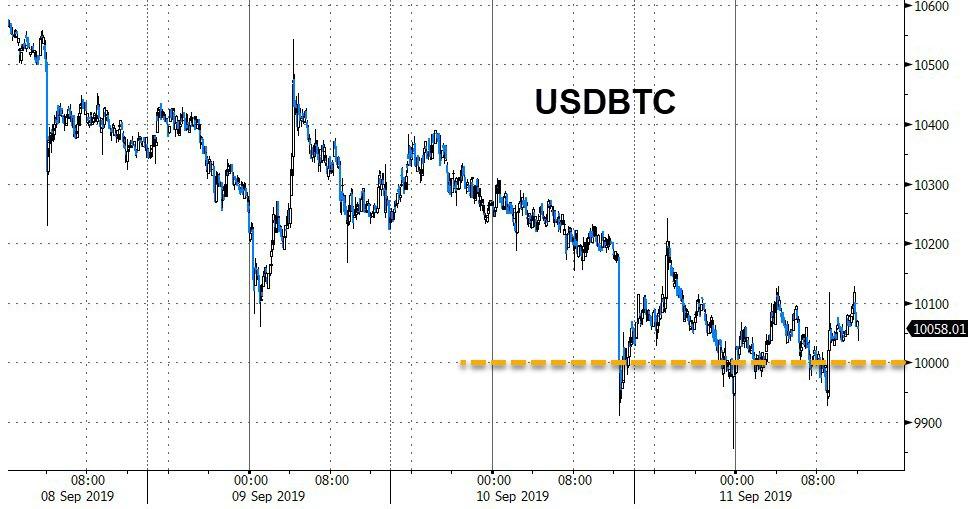

Bitcoin: OPENING MORNING TRADE : $ 10,088 DOWN 8

Bitcoin: FINAL EVENING TRADE: $ 10,086 DOWN 12

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A TINY SIZED 365 CONTRACTS FROM 217,798 DOWN TO 217,433 WITH THE 2 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0, FOR DEC: 1510 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1510 CONTRACTS. WITH THE TRANSFER OF 1510 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1510 EFP CONTRACTS TRANSLATES INTO 7.50 MILLION OZ ACCOMPANYING:

1.THE 2 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

40.225 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE AGAIN HAD SOME ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY WITH THE 4TH CONSECUTIVE RAID ORCHESTRATED BY THE CROOKED BANKERS/OFFICIAL SECTOR. HOWEVER IN TOTAL SYMPATHY WITH YESTERDAY, THE TOTAL OI INCREASED DESPITE THE ATTEMPTED DRUBBING IN PRICE OF OUR SILVER METAL. OUR GOOD FRIENDS ARE GETTING NOWHERE WITH THE RAIDS AS THE LONGS REFUSE TO BE FLEECED.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

16,972 CONTRACTS (FOR 7 TRADING DAYS TOTAL 16,972 CONTRACTS) OR 84.860 MILLION OZ: (AVERAGE PER DAY: 2388 CONTRACTS OR 11.94 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 84.860 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.11% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1634.53 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A TINT SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 365, WITH THE 2 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1510 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 818 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1510 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 365 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 2 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $18.11 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.081 BILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 156 NOTICE(S) FOR 780,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 40.225 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3042 CONTRACTS, TO 614,753 DESPITE THE HUGE WHACK GOLD TOOK YESTERDAY ( $11.25 FALL)// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3860 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 3860 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 614,753,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 818 CONTRACTS: 3042 CONTRACTS DECREASED AT THE COMEX AND 3860 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 818 CONTRACTS OR 81,800 OZ OR 2.544 TONNES. YESTERDAY WE HAD A LOSS OF $11.25 IN GOLD TRADING….AND WITH THAT LOSS IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 2.544 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON BUT LIKE SILVER IT WAS TO NO AVAIL. OUR BANKER FRIENDS/OFFICIAL SECTOR ARE GAINING NOTHING WITH THEIR CONTINUAL RAIDS.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 52,496 CONTRACTS OR 5,249,600 oz OR 163.28 TONNES (7 TRADING DAY AND THUS AVERAGING: 7499 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAYS IN TONNES: 163.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 163.28/3550 x 100% TONNES =4.59% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4314.89 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 3042 DESPITE THE HUGE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($11.25)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3860 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3860 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 818 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

3860 CONTRACTS MOVE TO LONDON AND 3042 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 2.544 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $11.25 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 22 notice(s) filed upon for 2200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.30 TODAY//(COMEX-TO COMEX)

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 882.42 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 379.401 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 365 CONTRACTS from 217,798 DOWN TO 217,433 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1510: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1510 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 365 CONTRACTS TO THE 1510 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD SIZED GAIN OF 1145 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 5.7250 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 40,225 MILLION OZ/

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 2 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1510 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 12.39 POINTS OR 0.41% //Hang Sang CLOSED UP 475.38 POINTS OR 1/78% /The Nikkei closed UP 205.66 POINTS OR 0.96%//Australia’s all ordinaires CLOSED UP .36%

/Chinese yuan (ONSHORE) closed DOWN at 7.1168 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1168 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1122 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

China’s auto sector is in disarray as it crashes for the 14th time in the last 15 months, this time by a huge 9.9%

(zerohedge)

4/EUROPEAN AFFAIRS

i)UK

Farage offers Johnson a non aggression pact in order to secure a Brexit

(zerohedge)

ii)Bill Blain comments on what really is bothering him this morning. He correctly states that tomorrow’s ECB meeting is critically important if they proceed with further QE

7. OIL ISSUES

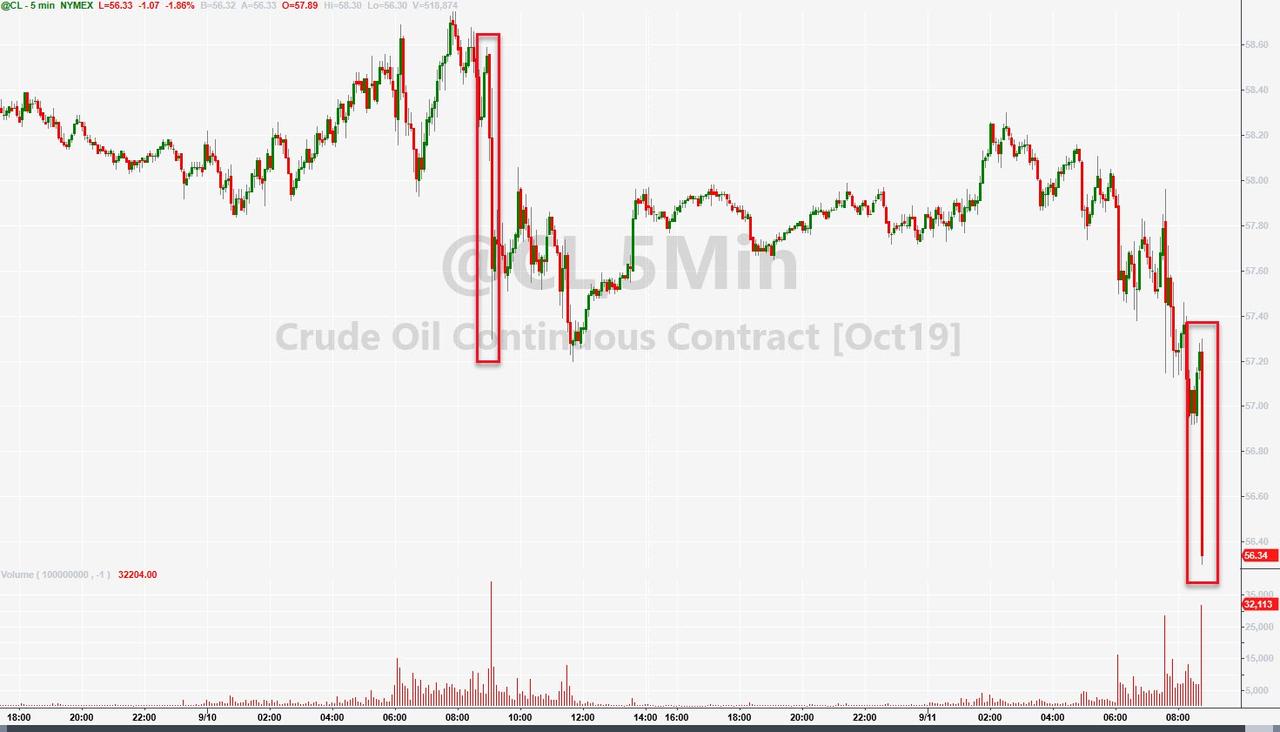

OIl prices plunge after we learn that Trump want to ease sanctions so as to get a face to face meeting with Rouhani.

Bolton was totally against easing sanctions.

(zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

Congressman Mooney still has no answers from Treasury or the CFTC as he asks about gold market rigging

This is his 3rd letter

For those of you who missed these letters, it is appended below

(GATA/Stefan Gleason/Mooney.GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

a)TRUMP is at it again: he is telling the Fed that they should cut rates to zero or less so that the uSA can refinance its debt and lengthen maturities. The fun begins tomorrow when the ECB lowers rates. Trump will pound the table why not the USA? He is providing an impetus for gold rising

(zerohedge)

iv) Swamp commentaries)

a)My goodness. The dept of Justice had a memo that exonerated Michael Flynn and they decided to hide it from him. Not only that but the memo was dated Jan 30 2017 and had the full knowledge of Comey. Thus Comey lied to the President stating that there is an ongoing investigation on Flynn even though he knew Flynn had nothing to do with the Russians

(Sara Carter)

b)Jim Jordan: The Inspector General is expected to conclude the FISA Warrants (all4 of them) were illegally obtained

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

THE BANKERS SUPPLIED THE NECESSARY AND INFINITE AMOUNT OF SHORT PAPER IN GOLD IN OUR 4TH CONSECUTIVE RAID YESTERDAY. THE BANKERS SUCCEEDED IN LOWERING GOLD’S PRICE BY A CONSIDERABLE $11.25. HOWEVER, JUDGING BY THE STRENGTH IN GAIN OF OUR TOTAL OI CONTRACTS, THEY WERE AGAIN UNSUCCESSFUL IN THE ENDEAVOUR TO FLEECE ANY UNSUSPECTING LONGS.

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

i) Into Brinks dealer: 1,007,029.735 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 41,359 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 124,266 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 124,266 CONTRACTS EQUATES to 621 million OZ 88.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.54% ((SEPT 11/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.41% to NAV (SEPT 11/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.54%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.16 TRADING 14.62/DISCOUNT 3.56

END

And now the Gold inventory at the GLD/

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

SEPT 11/2019/ Inventory rests tonight at 889.75 tonnes

*IN LAST 661 TRADING DAYS: 52.96 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 561- TRADING DAYS: A NET 113.69 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

end

Now the SLV Inventory/

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 11/2019:

Inventory 379.401 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.08/ and libor 6 month duration 2.03

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .05

XXXXXXXX

12 Month MM GOFO

+ 1.99%

LIBOR FOR 12 MONTH DURATION: 1.97

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.02

RATES NEGATIVE ALL THE WAY OUT TO ONE YEAR.

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Citigroup Say Gold May Top Record At $2,000 Per Ounce

◆ Gold will “trade stronger for longer” and Citigroup see gold possibly topping new nominal highs at $2,000 an ounce in the next year or two

◆ Citi is bullish on gold due to the prospect of the Fed cutting interest rates to zero, heightened geopolitical tensions and rising risks of a global recession (see News below)

◆ Strong demand from institutional investors and central bank diversification will provide support for gold prices

◆ Citigroup says recession risks and strong investor demand underpin their positive outlook for gold

NEWS and COMMENTARY

Citigroup Says Gold May Top Record – Bloomberg

Gold prices inch higher, all eyes on ECB meeting

Trump ousts NSA Adviser Bolton, says they ‘disagreed strongly’ on policy

Consumer Credit Card Debt Explodes In July Despite Rates At 18-Year Highs

Tech stock bubble continues – but wise investors should look for value elsewhere

“History doesn’t repeat itself, but it does rhyme” – Mauldin on Dalio

‘I’m even more bullish on silver than on gold’ – Ned Naylor-Leyland

Record-High Debt And Record-Low Yields May See Gold At $10,000 – Holmes

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

10-Sep-19 1494.60 1498.25, 1211.52 1211.34 & 1353.51 1357.11

09-Sep-19 1509.95 1509.20, 1223.81 1220.34 & 1368.62 1364.92

06-Sep-19 1504.95 1523.70, 1223.52 1237.09 & 1363.94 1378.49

05-Sep-19 1542.60 1529.10, 1257.06 1238.72 & 1397.44 1380.78

04-Sep-19 1538.80 1546.10, 1265.05 1269.97 & 1397.69 1403.86

03-Sep-19 1532.45 1537.85, 1278.06 1277.80 & 1400.35 1403.44

02-Sep-19 1523.35 1525.95, 1260.42 1265.01 & 1388.69 1391.51

30-Aug-19 1526.55 1528.40, 1253.14 1251.15 & 1382.75 1383.51

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Congressman Mooney still has no answers from Treasury or the CFTC as he asks about gold market rigging

This is his 3rd letter

For those of you who missed these letters, it is appended below

(GATA/Stefan Gleason/Mooney.GATA)

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

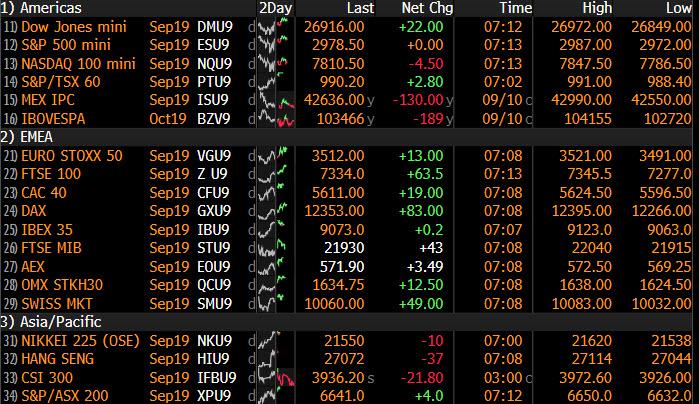

US Futures Drift, Global Markets Rally As China Takes Steps To Ease Trade War

S&P500 futures were perfectly unchanged in an oddly quiet session, failing to be inspired by a ramp in European and Asian stocks, after China announced exemptions from the 25% extra tariffs put in place last year in some product categories such as pharmaceuticals and lubricant oil, in a move that is being viewed as a good will concession by China to restart the trade negotiation on good terms in October. While this has lifted sentiment in Asia and Europe, combined with a technical rebound generally in equities…

… it failed to inspire a move in US futures, while US 10Y rates appear to have peaked at 1.74% overnight and with rate locks on a record $100 billion in investment grade issuance now in the rearview mirror, expect 10Y yields to resume their slide in the coming days.

Much of Europe’s gains came on the back of the tremendous momentum-to-value shift, which according to JPM’s Marko Kolanovic has “only occurred on two days in history“, with Europe’s Stoxx 600 Index benefiting from the strong rotation into cyclical sectors that had lagged behind this year, such as automaker and banking shares.

Leading the rally in equities was once again Japanese equities with Nikkei futures up 1.1% erasing the losses from the intermediate peak in July. The lift was broad based with Asian stocks gaining, led by financial firms and material producers, as investors assessed signs that China will move to lessen the trade war’s impact and awaited the European Central Bank’s policy decision on Thursday. Asian equities jumped in Japan and Hong Kong after the infamous twitter troll, Global Times editor Hu Xijin said in a Twitter post, that China will implement measures to ease the trade war’s impact on the world’s second-biggest economy. The moves planned by Beijing will benefit some companies from China and the U.S., Xijin said.

As a result, most markets in the region were up, with Japan and Singapore pacing gains. The Topix advanced 1.7% to a two-month high, as Japanese banks continued to rally following a rebound in U.S. Treasury yields. A weaker yen helped buoy shares of Japanese exporters. The Shanghai Composite Index dropped 0.4%, with Kweichow Moutai and Jiangsu Hengrui Medicine among the biggest drags. Haitong Securities led brokerages higher after China scrapped foreign investment limits in stock and bond markets. South Korean infrastructure shares outperformed after the departure of President Donald Trump’s national security adviser, spurring speculation the U.S. may show conciliatory gestures toward China and North Korea.

As Saxo Bank highlighted recently, economic surprises have become less and less negative with Citi’s Economic Surprise Index G10 turning almost positive. If we are right that central banks will deliver enough monetary stimulus, with ECB starting tomorrow, and macro data begin to surprise positively then the rally could continue.

Equities have rebounded sharply in September on hopes for fresh monetary stimulus from the ECB on Thursday (as long as there is bank tiering included in the package) and the Fed next week, while market-supportive measures by China helped lift sentiment.

“We are primed for a little bit of disappointment,” Investec’s Jeff Boswell told Bloomberg TV in Singapore. “On the QE front, whilst we’ve been expectant of something – certainly on the corporate bond-buying side that the market’s been expecting – it is unlikely to come tomorrow.”

In rates, treasury 10-year notes and similar German bunds drifted, after their yields earlier on Wednesday touched one-month highs. After hitting a session high of 1.74%, the 10Y Treasury dropped to session lows of 1.7057%, as rate locks on $100 billion of new investment grade issuance. Treasuries also halted a five-day decline as traders positioned before a pivotal eight-day period that includes meetings of the world’s three major central banks.

In FX, the yen fell for a third day after China announced measures to ease the negative impact of the trade war, reducing demand for haven assets. The pound rose, setting course for its third day of gains, as Prime Minister Boris Johnson was said to consider a fresh approach to the Irish border problem.

In commodities, oil futures climbed alongside gold.

The euro weakened, heading for its biggest drop in eight sessions.

Market Snapshot

- S&P 500 futures little changed at 2,978.25

- STOXX Europe 600 up 0.6% to 388.85

- MXAP up 0.9% to 158.09

- MXAPJ up 0.7% to 510.31

- Nikkei up 1% to 21,597.76

- Topix up 1.7% to 1,583.66

- Hang Seng Index up 1.8% to 27,159.06

- Shanghai Composite down 0.4% to 3,008.81

- Sensex up 0.4% to 37,294.35

- Australia S&P/ASX 200 up 0.4% to 6,638.04

- Kospi up 0.8% to 2,049.20

- Brent futures up 0.9% to $62.91/bbl

- Gold spot up 0.4% to $1,490.99

- U.S. Dollar Index up 0.2% to 98.52

- German 10Y yield rose 1.0 bps to -0.537%

- Euro down 0.2% to $1.1024

- Italian 10Y yield rose 7.6 bps to 0.679%

- Spanish 10Y yield rose 1.9 bps to 0.278%

Top Overnight News

- China announced a range of U.S. goods to be exempted from 25% extra tariffs put in place last year, as the government seeks to ease the impact from the trade war without lifting charges on major agricultural items like soybeans and pork.

- President Donald Trump said he fired his hawkish national security adviser, John Bolton, after disagreeing “strongly” with many of his positions, ending a tumultuous tenure marked by multiple setbacks in U.S. foreign policy.

- Hong Kong Exchanges and Clearing Ltd. made a surprise $36.6 billion bid for London Stock Exchange Group Plc.

- German Chancellor Angela Merkel said her government will work until the “last day” to ensure an orderly U.K. departure from the European Union but insisted Germany is ready for a no- deal Brexit.

- The European Central Bank is about to turn the screws again on financial institutions by diving even deeper into negative interest rates. For holders of German and French government bonds, this week’s European Central Bank meeting is coming just in the nick of time.

- President Donald Trump said he fired his hawkish national security adviser, John Bolton, after disagreeing “strongly” with many of his positions, ending a tumultuous tenure marked by multiple setbacks in U.S. foreign policy

- Pound volatility is at emerging-market levels and U.K. assets are set for a substantial repricing once the Brexit outcome becomes known, according to Bank of England Governor Mark Carney

- A cross-party group is seeking a way out of the Brexit “nightmare” by working together to find a deal that can secure a majority in Parliament, suggesting a Northern Ireland- only backstop may be one answer

Asian equity markets eventually traded mostly higher as the region shrugged-off the indecision from Wall St, which had been subdued by the continued global bond rout and tentativeness ahead of this week’s ECB. ASX 200 (+0.3%) and Nikkei 225 (+1.0%) were higher but with gains in Australia capped as the outperformance in mining names was counterbalanced by weakness in tech, while Tokyo exporters continued to reap the benefits of recent currency weakness and after source reports suggested BoJ policymakers could be open to additional easing measures. Advances were also seen across the Apple supply chain in Japan and Taiwan following the tech giant’s launch event where it announced a new streaming service and health app, as well as new iWatch, iPhone and iPad models. Hang Seng (+1.7%) and Shanghai Comp. (-0.4%) were mixed after a tepid PBoC liquidity effort in which the mainland failed to take impetus from China’s fresh efforts to further open its financial markets by dropping QFII and RQFII quota limits. Sources noted China is ready to sweeten a deal by buying US goods, however, the report added that a purchase agreement is no certainty and would be in exchange for a delay on tariffs as well as an easing of restrictions on Huawei. China’s Global Times Editor also later suggested China will introduce important measures to ease the impact from the trade war which would benefit some companies from both China and the US which briefly fuelled appetite for risk. Finally, 10yr JGBs were lower amid a continuation of the global bond rout which was partly attributed to this week’s supply and heavy corporate issuances, with weaker results across all metrics in today’s 5yr JGB auction adding to the pressure.

Top Asian News

- Duterte Will Ignore South China Sea Ruling for China Oil Deal

- BOJ’s Dilemma Spurs Speculation on Reverse ‘Operation Twist’

- Hong Kong Stocks Climb to Six-Week High as Developers Jump

- Asia Apple Suppliers Rise as MS Sees IPhone Price Driving Demand

Major European bourses are broadly in the green [Eurostoxx 50 +0.5%], following on from a similar APAC lead as sentiment is supported by China releasing a tariff exemption list for the US, effective from September 17th. Items on the list will not be subject to additional tariffs imposed by China on US goods as countermeasures to trade action taken by the US, however, the list does not include corn, soybean or pork. Spain’s IBEX (U/C) is the underperformer thus far amid disappointing earnings from heavyweight Inditex (-2.9%) whilst broad-based gains are seen across the region. Sectors are mixed with defensive sectors lagging, although the energy sector also feels some headwind from yesterday’s price decline in the oil complex. Turning to individual movers, LSE (+5.6%) shares spiked higher amid reports that Hong Kong Exchanges and Clearing have proposed a combination with LSE, terms of proposed deal would imply an enterprise value of GBP 31.6bln, and the transaction implies a value of GBP 83.61 for each LSE share. LSE said its board will consider the proposal. On the flip side, Suez (-1.3%) and Kone (-1.9%) opened lower amid downgrades, although the former saw some upside amid reports that the Co. won an approx. EUR 1bln treatment contract for the Dongying China chemical plant, contract is for 50 years.

Top European News

- Merkel Answers IMF, Saying Lack of Money Not Germany’s Problem

- British Airways Scraps Flights as Impact of Pilot Strike Lingers

- Nordea’s Wholesale Banking Unit in Need of ‘Thorough Review’

- Foreign Binge on European Bonds Is Ending Just in Time for ECB

In FX, the Euro is not quite the biggest G10 loser or underperformer, but the single currency has been a notable mover after topping out above 1.1050 against the Dollar and failing to close above key resistance just below yet again (1.1049 represents a 38.2% retracement of the decline from 1.1249 to 1.0926 ytd low). Eur/Gbp selling into the early 9 am fix may also have impacted, as the cross retests recent sub-0.8925 lows, but Eur/Usd is holding around the 10 DMA and bids said to be sitting just below (at 1.1022 and 1.1020 respectively) with one eye on Thursday’s ECB meeting and some form of easing/stimulus as German institutes continue to downgrade GDP estimates, while the other keeps tabs on higher global bond yields/spreads.

- JPY/CHF – More safe-haven unwinding has nudged the Yen and Franc down to circa 107.85 and 0.9940 vs the Buck, and Usd/Jpy has breached a Fib, exporter offers plus a cloud top formation in the process, at 107.49, 107.50 and 107.71, with some fundamental/macro impetus stemming from another upturn in US Treasury yields and more curve steepening against the backdrop of positive-looking US-China trade headlines (such as Chinese tariff exemptions and buying US goods as a sweetener for upcoming talks).

- GBP/AUD/NZD/CAD – All narrowly mixed vs the Greenback, with Cable forming multiple/lower peaks ahead of 1.2400 and reported stops at 1.2385+ and the Aussie fading into 0.6900 and the 100 DMA at 0.6907 following another downbeat sentiment survey overnight (Westpac consumer confidence turned negative). However, the Pound has not seen much angst in wake of an official ruling in Scotland against UK PM Johnson’s Parliament prorogation, while Aud/Usd is still outpacing Nzd/Usd as the latter remains heavy on the 0.6400 handle and the Kiwi struggles to stay above 1.0700 in cross terms ahead of NZ manufacturing PMI tomorrow and Westpac’s Q3 consumer survey on Friday. Elsewhere, the Loonie is maintaining its post-Canadian jobs momentum, but finding 1.3150 a tough hurdle to overcome convincingly.

- NOK/SEK – Even though crude prices remain on a roll and the Norges Bank is still on course to take another step towards policy normalisation before the Riksbank (albeit not likely next week given yesterday’s soft inflation data), Eur/Nok is hovering around 9.8850 within a 9.9010-9.8765 range in contrast to Eur/Sek nearer the base of 10.6990-6595 parameters in wake of latest Riksbank comments reaffirming tightening guidance and dismissing weaker than expected Swedish CPI/CPIF metrics.

- EM – The Rand’s bull run has been derailed around 14.6100 vs the Dollar and a deterioration in SA business confidence has hardly helped as Usd/Zar rebounds to 14.7000+, even though Moody’s indicated low risk of a ratings downgrade this year.

In commodities, WTI and Brent futures are holding onto most of its intra-day gains/consolidation following yesterday’s decline which was induced by the EIA cutting its 2019 and 2020 global oil demand forecasts by 100k BPD and 30k BPD, whilst downside was exacerbated after US President Trump fired the White House National Security Advisor/known policy-hawk Bolton. Prices have rebounded and remain on an upward trajectory thus far with WTI futures around the 58.00/bbl mark whilst its Brent counterpart trades just under 63.00/bbl (at time of writing). This morning also saw the release of the OPEC Monthly Oil Report in which its 2019 global oil demand growth forecast was revised lower by 80k BPD, in-fitting with the EIA STEO, next up IEA will release its report tomorrow at 0900BST. Ahead of tomorrow’s JMMC meeting, the Iraqi Oil Minister noted that the producers will have a discussion on whether or not there is the need for a deeper production cut with OPEC+, although this was rebuffed by the Russian Energy Minister who also expressed concern regarding global economy. Novak added that the slowing global demand for oil will also be discussed at the meeting tomorrow. Elsewhere, gold prices remain capped below the 1500/oz ahead of this week’s key risk events including US CPI and the ECB rate decision, whilst copper prices are little changed with little by way of immediate catalyst. Finally, Dalian iron ore prices rose for a third session amid a decline in shipments coupled with hopes of further Chinese stimulus.

US Event Calendar

- 8:30am: PPI Final Demand MoM, est. 0.0%, prior 0.2%; PPI Final Demand YoY, est. 1.7%, prior 1.7%

- 8:30am: PPI Ex Food and Energy MoM, est. 0.2%, prior -0.1%; PPI Ex Food and Energy YoY, est. 2.15%, prior 2.1%

- 10am: Wholesale Inventories MoM, est. 0.2%, prior 0.2%; Wholesale Trade Sales MoM, est. 0.5%, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

Yesterday was the annual day in the diary when I wake up determined to take no notice of the new Apple product launch event and go to bed with a note in my diary to be the first in the online queue a few days later. It looks like I’ll be ordering a new phone due to the enhanced camera and a new watch due to the new fitness tracking improvements. I do believe they saw me coming.

To help me count down the hours until Friday’s pre-ordering, we have the small matter of tomorrow’s ECB meeting to look forward to. As we approach this main event, the relentless sell-off in global bond markets continues to show little sign of abating just yet. In fairness it took until the final couple of hours of the European session yesterday for yields to move notably higher on both sides of the Atlantic but the move carried on well into the US close with 10y UST yields finishing +9.1 bps at 1.735% – c.6bps occurred after Europe went home. That takes the 5-session move to 27.7bps, the steepest selloff since November 2016. The 2s10s curve didn’t do a lot though, holding steady at +5.1bps. Earlier 10y Bunds closed up +3.6bps. That now means that yields have closed higher in 4 out of the last 5 sessions with the move since the September 3rd intraday low now up to +19.5bps. The moves yesterday also meant 30y Bunds (+4.5bps) closed back in positive territory at 0.042% for the first time since August 2nd. Meanwhile BTPs sold off +7.8bps and Gilts +4.8bps.

There wasn’t actually a huge amount to report with regards to yields with the main talking point coming late in the European session with yet another pre-ECB MNI article, this time suggesting that we could see the ECB delay QE “possible contingent on further economic deterioration”. The headlines got the market excited but a closer read suggested that the base case from the main source in the article was that QE was still likely to be announced.

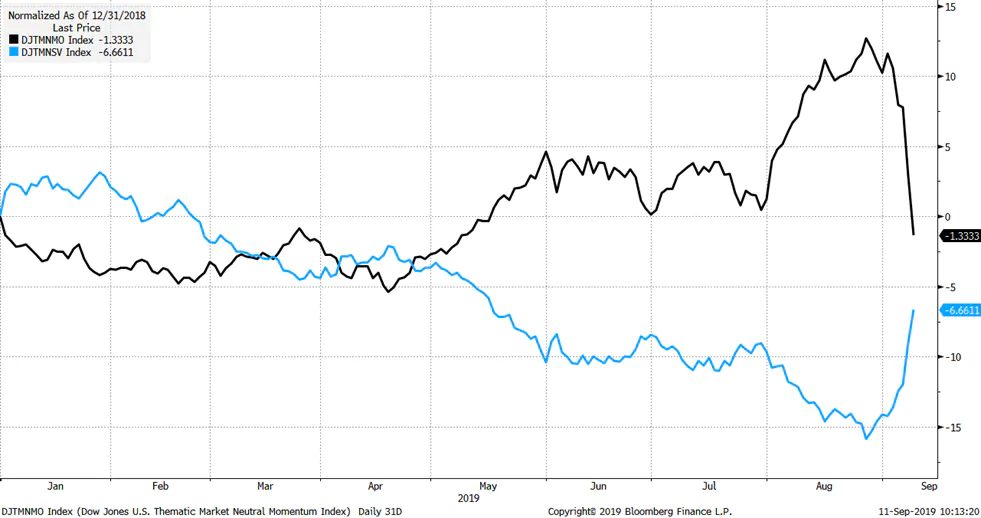

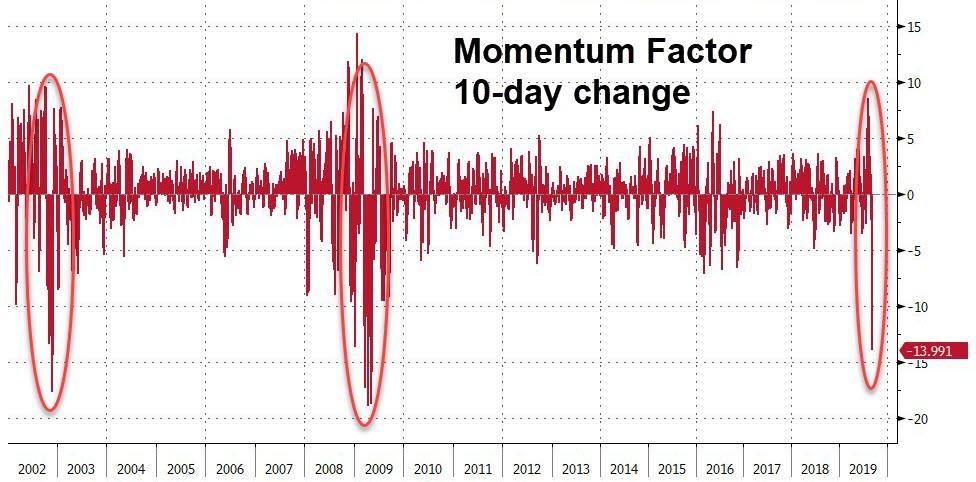

Equity markets have had an interesting couple of days where there’s been a big unwind in some popular trades. Several recent trends have reversed sharply, including momentum, growth versus value, and large versus small caps. Rising yields and steeper curves certainly contributed to the moves, but positioning had become stretched in recent months, as Binky highlighted in his report last week (link here ). To put the recent moves in context, the Bloomberg momentum index fell -1.26% to take its two-day loss to -2.51%, the worst since July 2008. Growth stocks have underperformed value by -4.09% over the last two days, the biggest shift since December 2016. Meanwhile, over the last seven sessions, growth stocks have underperformed -6.65%, the most since August 2009. Small caps have also underperformed versus large caps by 1.73% this week, the most in six weeks.

As for yesterday, the S&P 500, DOW and NASDAQ ended +0.03%, +0.28% and -0.04% respectively after a late rally but with tech names in particular struggling (-0.49%) again. Prior to this the STOXX 600 limped to a +0.10% gain thanks to a small bounce into the close although banks did rally another +1.83% owing to the rates move. This means that after bottoming out of August 15th, the rally off the intraday lows for European banks has been an impressive +14.52%. US banks are also up +11.89% over the same period. Elsewhere, in credit HY spreads were -8.7bps tighter in the US but +3.3bps wider in Europe. The talking point though has been primary and most notably for US IG where another 13 deals were announced yesterday. Amazingly we’ve seen deals from 80 borrowers since the Labour Day holiday.

Overnight in Asia markets are largely trading higher with the Nikkei (+0.88%), Hang Seng (+1.35%) and Kospi (+0.73%) all up. Chinese markets are trading lower after recovering from larger early losses – the Shanghai comp is trading flat while the CSI (-0.32%) and Shenzhen Comp (-0.25%) are trading down. 10y JGB yields are up +3.4bps this morning to -0.202% while US treasury yields are heading slightly lower across the curve after the recent run – 2y (-1.2bps), 5y (-1.3bps), 10y (-1.2bps) and 30y (-1.4bps). Elsewhere, futures on the S&P 500 are up +0.1% this morning while WTI is up +0.87% as a report from the American Petroleum Institute indicated that the US crude inventories fell by 7.23 mn barrels last week.

Sticking with Asia, China’s Global Times editor Hu Xijin said in a twitter post overnight that China will implement measures to ease the impact of the trade war while adding that the measures will benefit some companies from China and the US. Elsewhere South Korea’s trade minister said that the country will file a complaint today with the WTO against Japan’s export curbs on key materials used by the country’s chip and display makers.

Back to yesterday and in Germany Finance Minister Scholz confirmed that the budget proposed for next year (and up to 2023) is balanced. However Scholz also said that “it’s central that we’re in a position, with financial fundamentals we have, to respond with many, many billions, if indeed an economic crisis erupts”. It’s worth pointing out that the budget will likely not be passed until late November with the major political debate to take place around the ‘climate cabinet’ on the 20th of September. So there is still some chance that the budget adds new tax/spending measures to address the climate question.

As for the data, in the US the August NFIB small business optimism reading slid 1.6pts to 103.1 and a little worse than expectations for 103.5. For context though this index is still holding in relatively well compared to other surveys. Later on the JOLTS job data for July showed that job opening fell slightly for the second consecutive month, potentially signaling softer labour demand and reaching a five month low. Meanwhile, the report showed that hiring increased 0.1pp to 4.3%, which tends to be a strong leading indicator for wage inflation.

Here in the UK there was some decent wages data with basic earnings growth of +3.8% yoy (vs. +3.7% expected). The unemployment rate also edged down one-tenth to 3.8% after expectations were for no change. It’s worth noting that headline wages are now back in line with pre-crisis levels albeit boosted by historic revisions to the June data. Another puzzler for the BoE to square with the weaker demand data. Staying with the UK, Governor Carney sounded slightly hawkish yesterday, saying specifically that he doesn’t view negative rates as a tool in the UK. This backs up comments from Vlieghe on Monday.

To the day ahead now, which is another quiet one for data with little of note this morning while in the US the highlight is the August PPI report. Later on we’ll also get the final July wholesale inventories and trade sales prints. Away from that we get the Poland rate decision and OPEC monthly oil market report.

3A/ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED DOWN 12.39 POINTS OR 0.41% //Hang Sang CLOSED UP 475.38 POINTS OR 1/78% /The Nikkei closed UP 205.66 POINTS OR 0.96%//Australia’s all ordinaires CLOSED UP .36%

/Chinese yuan (ONSHORE) closed DOWN at 7.1168 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1168 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1122 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

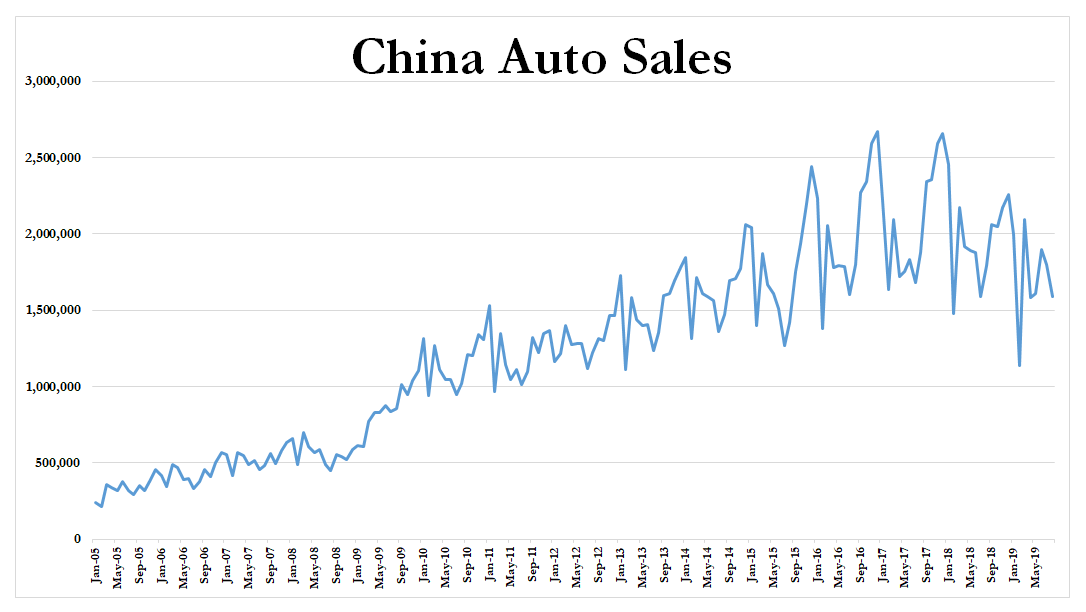

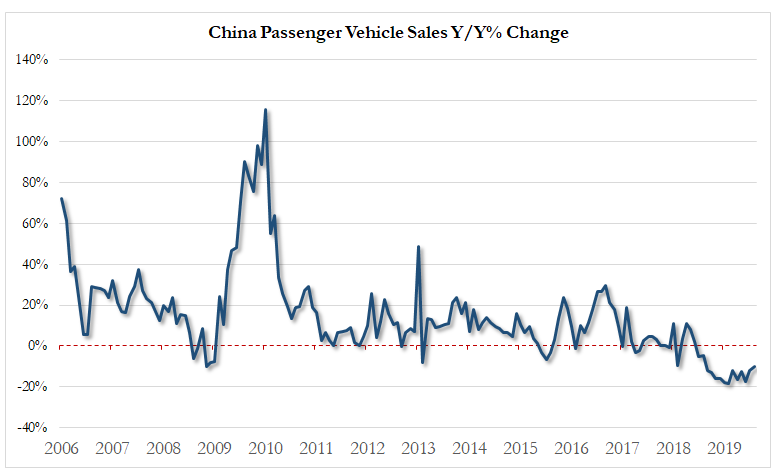

China’s auto sector is in disarray as it crashes for the 14th time in the last 15 months, this time by a huge 9.9%

(zerohedge)

Chinese Auto Sales Crash For The 14th Time In 15 Months, Falling 9.9%

Chinese auto sales continue to plunge deeper into recession, with the country’s China Passenger Car Association releasing preliminary data for August that in no way indicates that the trend could be slowing.

Instead, it has been a “historically prolonged slump” for the world’s largest car market, according to Bloomberg.

The CPCA reported on Monday that sales of sedans, SUVs, minivans and multipurpose vehicles in August fell 9.9% to 1.59 million units.

It has been the industry’s largest downturn in three decades and automakers are still facing headwinds as trade tensions with the U.S. continue. China has tried to roll out several stimulus measures to help the industry, including loosening car purchase restrictions, but they have done little to encourage consumption thus far.

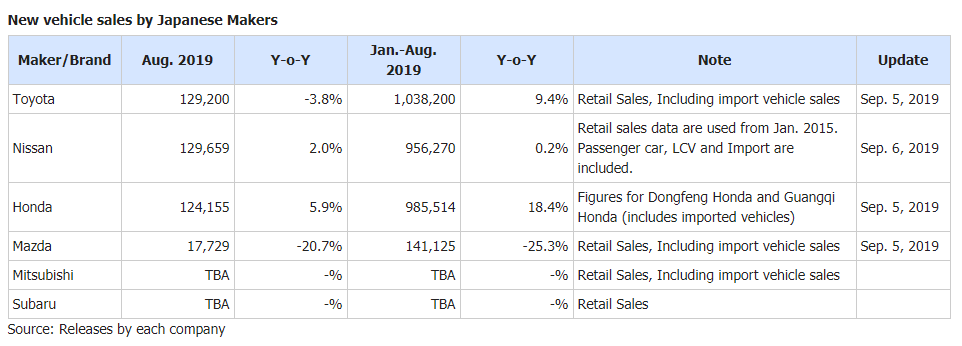

Preliminary data from MarkLines on Japanese automakers selling in China shows Nissan and Honda posting 2.0% and 5.9% gains, respectively, while Toyota sales fell 3.8% and Mazda sales suffered the largest blow, down 20.7%. We will revisit this data toward the middle of the month, when it is updated to include additional manufacturers from around the globe.

Top Chinese SUV maker Great Wall Motor Co. saw its first half profit lower by an astounding 59% and SAIC Motor Corp., China’s biggest automaker, also cut its sales forecast recently and predicted its first annual sales decline in at least 14 years. Geely Automobile Holdings Ltd. saw sales fall 19% in August.

Finalized data from July shows that Japanese sales led the charge, posting an 11.2% gain, while Chinese brands, American brands and French brands all fell by double digits.

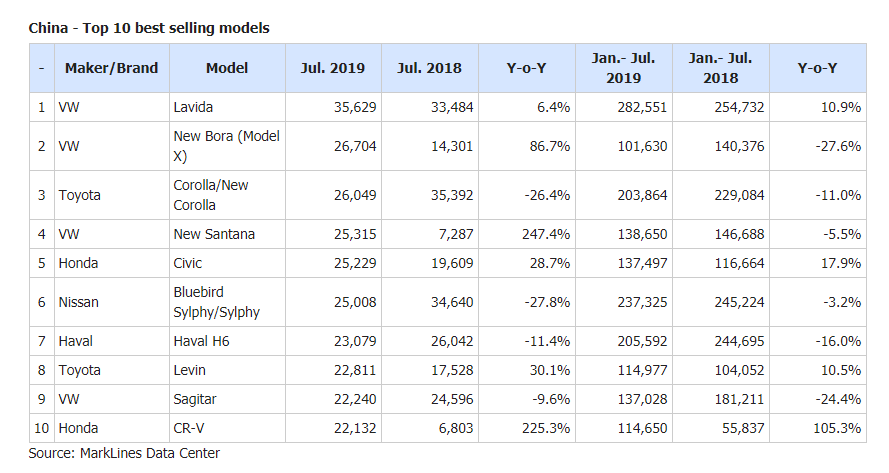

For July, three of the top 4 best selling models in China were manufactured by VW, who made up 5 of the 10 best selling models in the country. Toyota, Haval, Honda and Nissan also edged their way into the top 10 list of models sold.

Exports from China in July also fell significantly:

Overall vehicle exports in July totaled 81,000 units, reflecting a 15.5% m/m decrease and a 14% y/y decline. Passenger car exports totaled 60,000 units, reflecting a 12.5% m/m decrease and a 12.9% y/y decline. Commercial vehicle exports totaled 21,000 units, reflecting a 23.1% m/m decrease and a 17% y/y decline.

And while China continues its struggles, other large markets, like India, are also tumbling. India posted a 41% sales drop for automobiles in August, the largest such drop on record. U.S. automakers eeked out a slight rebound in sales, but were helped along by the Labor Day weekend partially falling in August.

We will update this post as more data from August becomes available.

4/EUROPEAN AFFAIRS

Farage offers Johnson a non aggression pact in order to secure a Brexit

(zerohedge)

Farage Reaches Out To Johnson About Possible Election “Non Aggression Pact”

With the conservative party in chaos due to its botched handling of Brexit, many – including Brexit Party leader Nigel Farage – suspect that, if an election is held in the not-too-distant future, Boris Johnson and his fellow Tories won’t come out on top. Farage has long maintained that if the UK remains a member of the EU after Oct. 31, something that looks increasingly likely, then many of those who voted ‘Leave’ during the Brexit referendum will defect from the conservatives to the Brexit Party.

And with Prime Minister Boris Johnson having already lost his majority thanks to expulsions and defections, Farage has offered his one-time ally an election pact, according to Reuters, in order to give him a chance to win a majority. Otherwise, he suspects Johnson’s conservatives will “take a real kicking” in the upcoming vote.

Brexit Party leader Nigel Farage offered Prime Minister Boris Johnson an election pact on Wednesday but warned that unless there was a clean-break Brexit, the Conservatives would take a “real kicking” in any election and could not win a majority.

Johnson, who has lost his working majority in the House of Commons, wants to hold an election but parliament has ordered him to ask the EU to delay Brexit until 2020 unless he can strike a transition deal at an EU summit on Oct. 17-18.

Even though Johnson’s pleas for another general election have been rebuffed so far, Farage said it’s clear that there will be an election soon. But when that vote is held, Labour and the Conservatives will find that traditional party loyalties have shifted thanks to the Brexit impasse.

“If we go beyond the 31st of October and we are still a member of the European Union – which looks increasingly likely – then a lot of votes will shift from the Conservative Party to the Brexit Party,” Farage told reporters.

“The Conservatives will take a real kicking from Nov. 1 onwards,” he said. “I very much hope that Boris Johnson will simply look at the numbers. If we stand against them, they cannot win a majority.”

Farage said the Brexit Party had reached out to the Conservative Party about a possible non-aggression pact during the next election, but that the Brexit Party had not yet received a clear response. After emerging as the biggest gainer in May’s European Parliament elections, Farage warned that his party would likely win seats in the Midlands, south Wales and northern England, stealing votes from both Labour and the Conservatives, during another vote.

Asked what he thinks will happen during the coming weeks, Farage said he expects the EU will make some last-minute concessions to Johnson before Oct. 31, and that Johnson would try and push the deal through parliament.

“There is going to be give from Brussels – there is going to be some sort of change to the Withdrawal Agreement on the backstop but I suspect absolutely nothing else,” he said.

“My sense is that he (Johnson) comes back to the House of Commons and tries to get that through,” he said.

But if the past is any guide, Johnson likely won’t succeed. At that point, with Parliament demanding another delay, an election will likely become inevitable.

Blain: What Really, Really Worries Me Is That Markets Are Losing Faith In Central Banks

Blain’s morning porridge, submitted by Bill Blain of Shard Capital

“It is not enough to serve our enemies with legal papers…”

Many of my readers think I’m some sort of uber-bear, repeatedly predicting some inevitable and unavoidable market Armageddon is imminent and just moments away. While Scotsmen are seldom mistaken for a sunny day, I’m actually a fairly cheerful soul. Even while foretelling the dire and bloody end of the financial world I always caveat it with no matter how bad the next downturn might be – the sun will come up the following morning. However, and but again (dark clouds blank the sun) I do think we should be aware of just how tenuous all this market euphoria in Bonds and Stocks still is.

This morning we wake up to lots of stuff that could move markets:

It’s no surprise We Work’s IPO now looks in serious trouble. Largest stockholder, Softbank, asked the firm to postpone the IPO. Its junk bonds are crashing because without the IPO, We Work loses access to an agreed $6 bln bank credit-line finance. While the Junk debt price tumbles, it’s unlikely the firm launch a new bond to cover the shortfall in its curious lose more money to make less business strategy. Investors are turning away. We Work is now caught in the classic liquidity death spiral. There are few ways to successful escape such a terminal stall. Their CEO, Adam Neumann, has made himself one of the most disliked and divisive figures in Tech world, and could find himself at the receiving end of unpalatable demands he surrenders control, gives up his controlling stock – which could uncover a host of interesting surprises on how he’s milked it.

Meanwhile, the latest White House whammy, John Bolton’s departure as NSA, leaves Trump surrounded by a coterie of empty yes-men. It might lead to less aggressive USA foreign policy, but the image of a Roman Emperor surrounded by horses he’s elevated into Senators sticks in the mind. I guess we better figure out what Mike Pompeo is thinking to figure out what Trump will tweet next.

And, I’m delighted to see the UK’s Labour Party is adopting a fairness policy towards Brexit. Deputy Leader of the Party Tom Watson has decided it’s only electorally equitable if they split themselves as divisively as the Conservatives by announcing Labour policy is now to have a new Remain referendum before a general election, and Labour’s stance is “unequivocally” to remain. Not quite how labour policy was described to me yesterday, but it’s marvellous stuff. We now have even less idea what Labour policy might be – which puts them in same league as Boris.

As the UK tumbles towards political civil war with both parties divided, can no one else perceive the horrible danger ahead of us? Is anyone else trying to figure out just how terrible a UK government controlled by “nice” “sensible” “caring and understanding” Liberals might be??? Imagine patronising 300 School Head Teachers telling us what to do… It’s just too frightening to contemplate… (PLEASE MAKE IT STOP!)

However, all these above are just the starters…

What really, really worries me this morning is the very real possibility markets are losing their faith in Central banks.

What if Central Banks were to ‘fess-up and admit ZIRP and QE has been utter bunkum, hasn’t worked and we need to do something else? What if such an outbreak of honesty triggers a Taper Tantrum of monstrous proportions? It would kill the bond market – just a time when investors are still putting in money to bonds out of stocks in search of yield and because they believe most corporates will weather the looming global recession!

Such a confidence collapse might be about to happen.

The last 10-years of distorted markets and addiction to Central Banks has been the consequence of unwise monetary experimentation, (aided and abetted by some extraordinarily stupid political decisions, like austerity, stupid regulation and bureaucratic behaviour – read my book: The Fifth Horseman for the whole picture).

Collectively, they’ve got the financial markets into their current mess. Bond yields are a massive bubble. Stocks are overvalued. We’re due a reset. Personally, I want to put more money into alternatives – real assets decorrelated from the distortions in financial assets. As a private PA investor, I’m struggling to find such funds to invest in! (IDEAS PLEASE?)

My current worry is Central Bankers are increasingly trapped. If they don’t keep interest rates artificially low rates, then both the bond and stocks bubbles will burst. Even if they sustain the illusion, but keep on cutting, its effectiveness is weakening. The bubbles may burst anyway. It will result in that most of amusing of financial moment… discovering who has been swimming without any swimwear.

Stocks should be in trouble because the global economy is going to slow. Bonds should be in trouble because low rates are not justified by inflation expectations (which are rising) or by deflationary threats – which are real, but not powerful enough to justify NIRP in a real world. Something has to give.

There are two forces at play.

- The first is political: In the US, the president is trying to boost his re-election chances by screaming it’s the fault of the Central Bank for not juicing the economy more by slashing rates. In more sensible places, politicians are realising monetary policies don’t drive growth, so they want to juice economies with Fiscal policy – borrow more money to spend into growth.

- The second force is overcoming the orthodoxy – which holds fiscal policy is dangerous because it hikes debt to levels where investors lose confidence in the economy. It’s a fair point that’s been proven many times.

All of which makes me look at the recent headlines in Europe; the number of ECB members openly disagreeing with Draghi’s calls to further ease, or German politicians arguing against a fiscal boost for the ailing German economy. These sound very negative and orthodox. But are we looking at a under the radar Central Banking coup in Europe?

According to a number of well briefed papers and articles, the ECB may not give us the easing and bond buying bonanza the markets have been promised. Even French members of the ECB committee are saying “Non!”. We’ve got senior economists like Jurgen Stark, former ECB Chief Economguesser saying “With a second asset-purchase programme the ECB will continue to disturb markets and prices do not reflect the risks anymore.” Or how about Olli Rehn’s recent gem: “if you don’t do anything, then you don’t have any side effects, but you don’t have any impact on the economy either!” Or the French Finance Minister, Bruno Le Maire: “We are at the end of the efficiency of monetary policy. The risks we are now facing are not related to financial stability, but how to fuel growth. The response is not only in hands of the ECB.”

Is it deliberate? If the ECB can’t keep buying.. then maybe its time for Plan B? These comments above all play into the hands of new ECB head, Christine Legarde, whose job will be to politically herd the felines of the ECB and European governments into a Fiscal Union to boost German and European fiscal spending.

Tomorrow’s ECB meeting is going to be critical. Don’t miss it!

The ECB decision is coming — here’s what to expect

Sept 11, 2019 10:26 a.m. ET

ECB rate cut expected to be announced Thursday