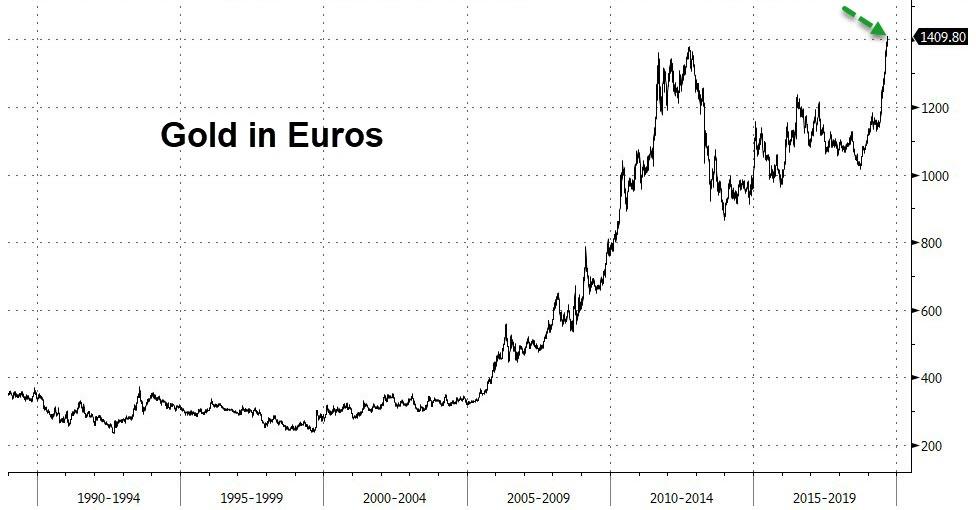

GOLD:$1500.00 UP $4.70 (COMEX TO COMEX CLOSING)

Silver:$18.10 UP 0 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1498.80

silver: $18.08

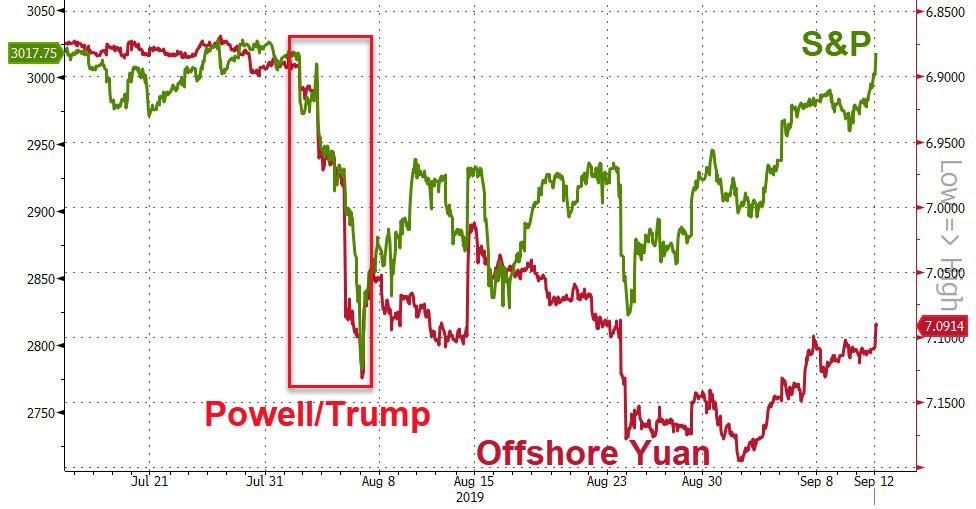

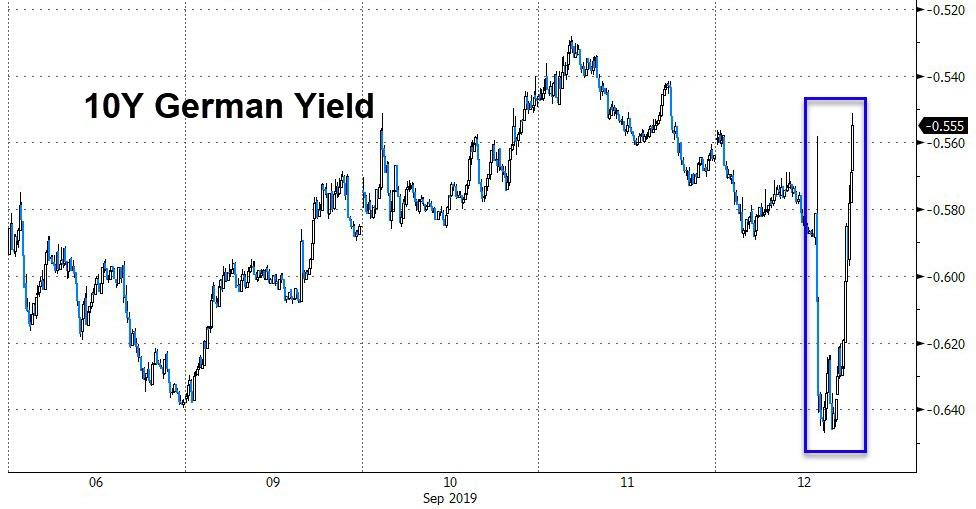

Today Draghi did not disappoint as he lowered interest rates by another 10 basis points but more important he is going to engage in more QE as Europe’s economy is moribund. In a classic confrontation, Draghi lied that he had 100% consent..he did not..only the southern club med boys were happy as the ECB will continue to buy their worthless sovereign bonds. The Northern boys like Germany, Holland and Finland were quite angry..we may have a Mutiny on the Bounty scenario. Christine Lagarde will take over in Oct and she is more dovish than Draghi. Draghi is thrilled to get out of this hell hole and leave it up to Lagarde to solve.

As per gold and silver today, the bankers have no doubt a very serious derivative problem here. It looks like $1500 gold and $18.20 silver is quite toxic to them.

your report for today…

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 2/4

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,494.400000000 USD

INTENT DATE: 09/11/2019 DELIVERY DATE: 09/13/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

661 C JP MORGAN 2

661 H JP MORGAN 1

737 C ADVANTAGE 4

____________________________________________________________________________________________

TOTAL: 4 4

MONTH TO DATE: 1,717

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 4 NOTICE(S) FOR 400 OZ (0.0124 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1717 NOTICES FOR 171,700 OZ (5.3405 TONNES)

SILVER

FOR SEPT

268 NOTICE(S) FILED TODAY FOR 1330,000 OZ/

total number of notices filed so far this month: 7871 for 39,355,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10146 DOWN 8

Bitcoin: FINAL EVENING TRADE: $ 10329 UP 171

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A TINY SIZED 257 CONTRACTS FROM 217,433 UP TO 217,690 WITH THE SMALL 1 CENT LOSS IN SILVER PRICING AT THE COMEX. (STRANGE: THE FINAL OI IN SILVER IS HIGHER THAN THE PRELIMINARY NUMBER BY 37 CONTRACTS)

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT: 0, FOR DEC: 1050 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1050 CONTRACTS. WITH THE TRANSFER OF 1050 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1050 EFP CONTRACTS TRANSLATES INTO 5.25 MILLION OZ ACCOMPANYING:

1.THE 1 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

41.495 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE AGAIN HAD SOME ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY AS THE 5TH CONSECUTIVE RAID ORCHESTRATED BY THE CROOKED BANKERS/OFFICIAL SECTOR ENDED IN FAILURE. IT IS BECOMING ALMOST IMPOSSIBLE FOR OUR BANKING/OFFICIAL SECTOR TO FLEECE OUR LONGS.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

18,033 CONTRACTS (FOR 8 TRADING DAYS TOTAL 18,033 CONTRACTS) OR 90.17 MILLION OZ: (AVERAGE PER DAY: 2254 CONTRACTS OR 11.27 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 90.17 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.88% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1639.78 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 257, WITH THE 1 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1050 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1270 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1050 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 220 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $18.10 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.087 BILLION OZ TO BE EXACT or 155% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 268 NOTICE(S) FOR 1,340,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 41.495 MILLION OZ//

2 THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

3 HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP

ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 5459 CONTRACTS, TO 620,212 ACCOMPANYING THE $5.30 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7080 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 7080 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 620,212,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,539 CONTRACTS: 5459 CONTRACTS INCREASED AT THE COMEX AND 7080 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,539 CONTRACTS OR 1,253,900 OZ OR 39.00 TONNES. YESTERDAY WE HAD A SMALLISH GAIN OF $5.30 IN GOLD TRADING….AND WITH THAT GAIN IN PRICE, WE HAD A GIGANTIC GAIN IN GOLD TONNAGE OF 39.00 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TRYING TO CONTAIN THE PRICE RISE. AND WITH THAT GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 42.17 TONNES!!!!!!. THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON BUT LIKE SILVER IT WAS TO NO AVAIL. OUR BANKER FRIENDS/OFFICIAL SECTOR ARE GAINING NOTHING WITH THEIR CONTINUAL RAIDS. NO WONDER THE CROOKS ABANDONED THEIR RAIDING EFFORTS RATHER EARLY YESTERDAY MORNING.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 59,576 CONTRACTS OR 5,957,600 oz OR 185.31 TONNES (8 TRADING DAY AND THUS AVERAGING: 7447 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY IN TONNES: 185.31 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 185.31/3550 x 100% TONNES =5.22% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4336.91 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 5459 DESPITE THE SMALL PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($5.30)) //.WE ALSO HAD A HUGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7080 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7080 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG SIZED GAIN OF 12,539 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7080 CONTRACTS MOVE TO LONDON AND 5459 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 39.00 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE SMALLISH GAIN IN PRICE OF $5.30 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 4 notice(s) filed upon for 400 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $4.70 TODAY//(COMEX-TO COMEX)

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 882.42 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 0 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 379.401 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY SIZED 257 CONTRACTS from 217,433 UP TO 217,690 AND CLOSER TO A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1050: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1050 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 257 CONTRACTS TO THE 1050 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 1307 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 6.535 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ//

SEPT 2019: 41.495 MILLION OZ//

RESULT: A TINY SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 1 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1050 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 22.42 POINTS OR 0.75% //Hang Sang CLOSED DOWN 71.43 POINTS OR 0.26% /The Nikkei closed UP 161.85 POINTS OR 0.75%//Australia’s all ordinaires CLOSED UP .20%

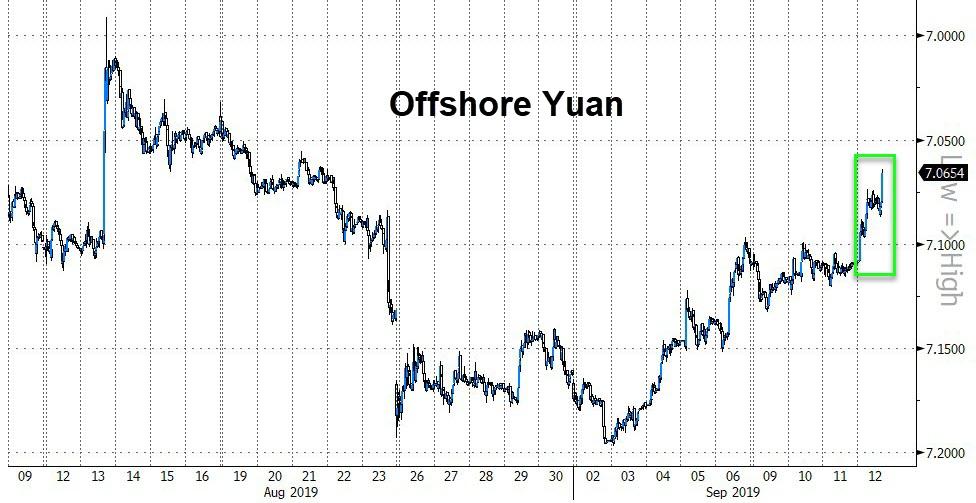

/Chinese yuan (ONSHORE) closed UP at 7.0852 /Oil DOWN TO 55.35 dollars per barrel for WTI and 60.02 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 7.0852 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0776 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

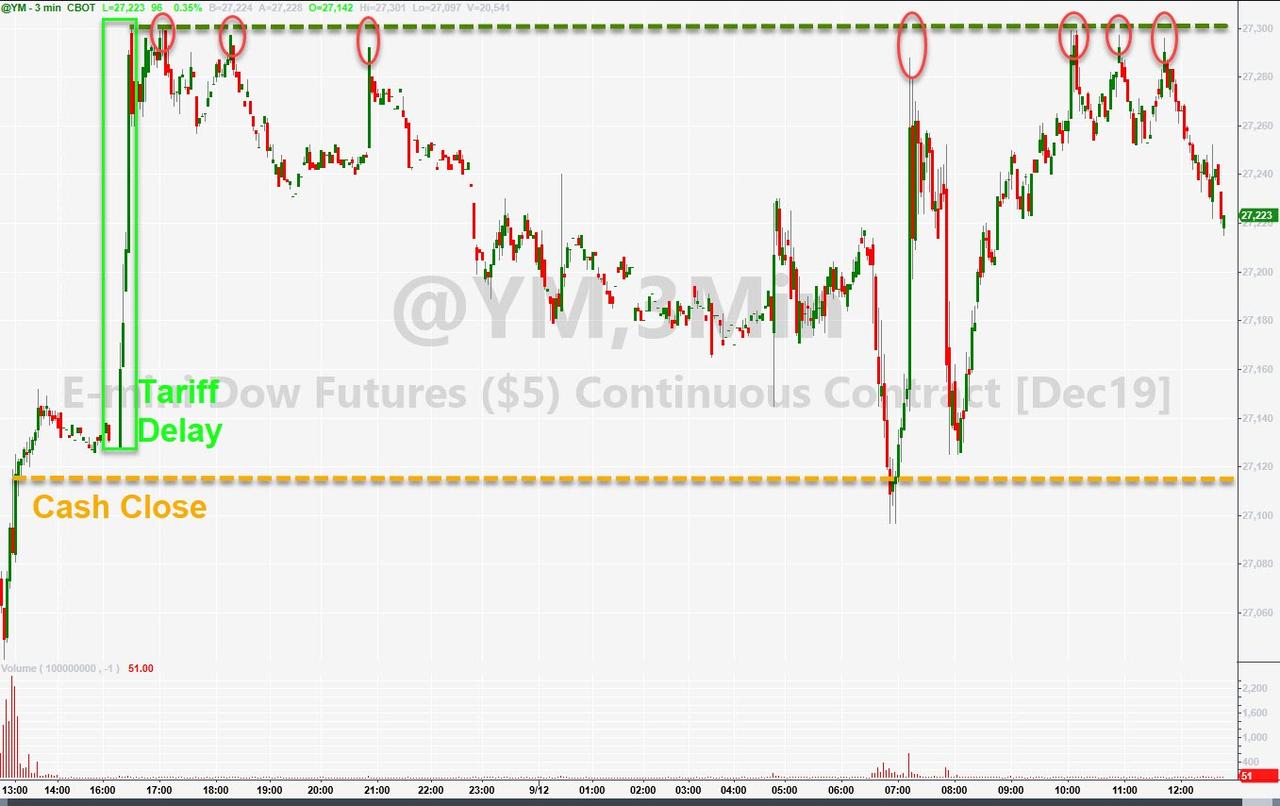

i)Last night: Trump delays increase in Chinese tariffs over just two weeks but that was enough to cause futures to surge

(zerohedge)

ii)CHINA/ARGENTINA/USA/During the night:

4/EUROPEAN AFFAIRS

i)ECB

This was not what the European banks wanted to hear: got expected 10 basis point cut in interest rates. They are to start open ended QE as well as easing TLTRO. He also introduces tiering to help the beleaguered banks.

(zerohedge)

ii)And the jawboning commences: Trump praises the ECB for “depreciating the Euro” as they slam the Fed for doing absolutely nothing

iii)looks like we have our good ol’ fashioned “Mutiny on the Bounty’ as European’s top central bankers dissented over new QE(zerohedge)

iv)ITALY

Rome asks for more time trying to tackle its huge debt at 135% of GDP. Brussels does not want to start a war with Italy as Conte is friendly to the European ways.

(zerohedge)

v)Negative rates has totally destroyed savings for Germans. Remember when you have savings you have investment. This policy has hurt all European banks badly as they refuse to lend and no investment occurs as their economy continues to falter. Mish comments at the end of the commentary…

(Mish Shedlock/Mishtalk)

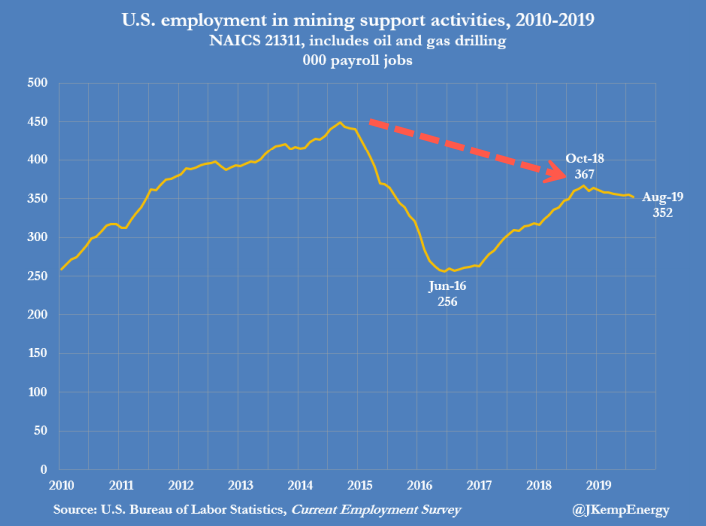

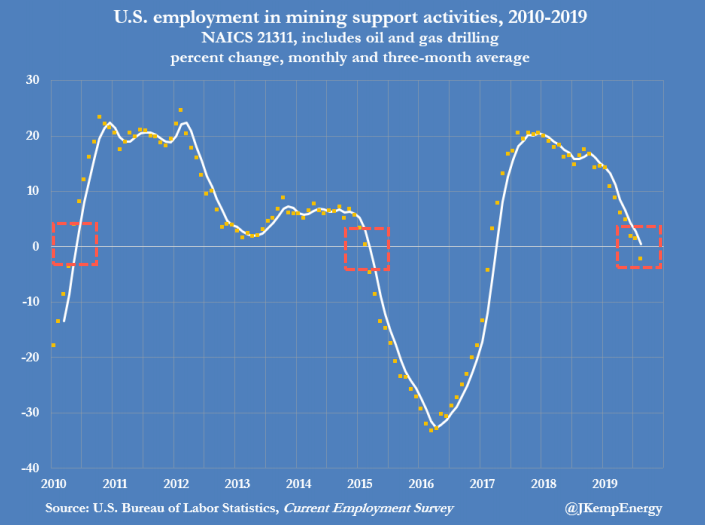

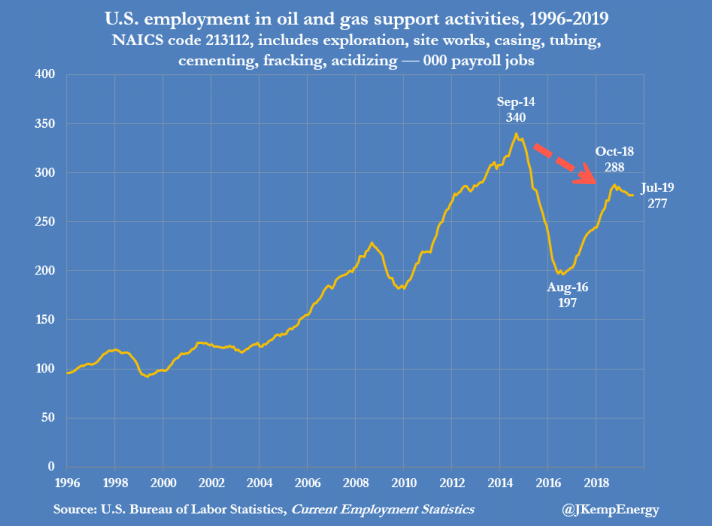

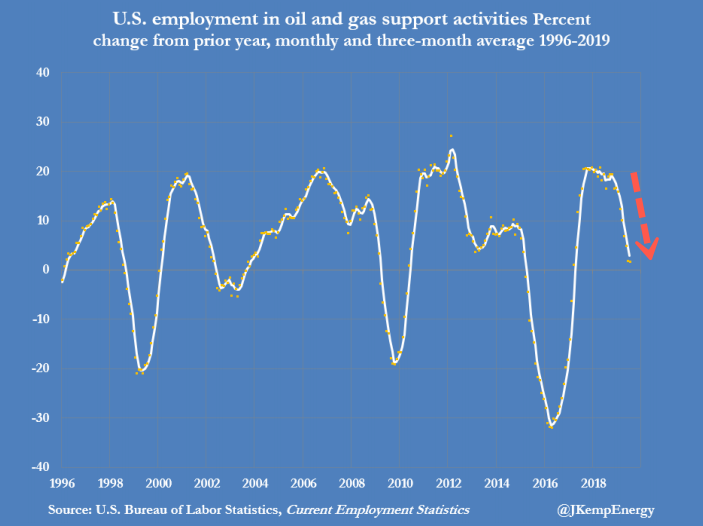

7. OIL ISSUES

We now witness employment in the shale oil and gas sector tumble..Here is the data on that:

(zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)We covered this yesterday but it is worth repeating. Trump urges zero or negative interest rates to tackle the huge USA debt. If this were to happen in the first 15 minutes at all USA rates go negative will cause gold to go infinite and all commodities will be backward..an impossible event.

(Reuters/GATA)

ii) Mario’s huge QE causes gold to rise

Gold trading/silver trading this morning

(zerohedge)

iii)A very important interview on negative interest rates with respect to gold. Chris Marcus interview Dave Kranzler

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

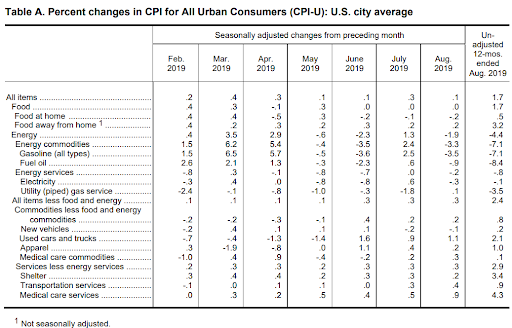

a)A mixed bag: core consumer prices surge although headline CPI rising less than expected. Now what will Powell do next week..will he lower rates and accommodate Trump or get him angry and stay pat.

(zerohedge)

b)Usually Sept. produces a positive income flow. However as he indicated to you yesterday, the USA for the first time will have a budgetary deficit greater than one trillion dollars and that number does not include deficits for auto loans and student loans

iii) Important USA Economic Stories

This Challenger report of jobs is extremely important. We are witnessing a record number of CEO’s leave their posts along with a growing corporate layoffs. This should tell you in spades what is really going on the jobs market,

(Mish Shedlock/Challenger Christmas/Gray//)

iv) Swamp commentaries)

a)Lindsay Graham’s goal is to declassify everything including all the FISA warrant applications. This should bury the democrats.

(Sara Carter)

b)Trump wins big as the Supreme Court overrules a California judge and grants asylum restrictions at the Southern border

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 707.300 oz

i)Into brinks: 598,520.229 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 102,946 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 96,960 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 96,960CONTRACTS EQUATES to 484 million OZ 69.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.77% ((SEPT 12/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.46% to NAV (SEPT 11/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.77%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.17 TRADING 14.65/DISCOUNT 3.43

END

And now the Gold inventory at the GLD/

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 12/2019/ Inventory rests tonight at 889.75 tonnes

*IN LAST 662 TRADING DAYS: 52.96 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 562- TRADING DAYS: A NET 113.69 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 11/2019:

Inventory 379.401 MILLION OZ

We covered this yesterday but it is worth repeating. Trump urges zero or negative interest rates to tackle the huge USA debt. If this were to happen in the first 15 minutes at all USA rates go negative will cause gold to go infinite and all commodities will be backward..an impossible event.

(Reuters/GATA)

iii) Other physical stories:

Gold and silver trading after Draghi unveils more easing

(zerohedge)

Gold Surges After Draghi Unveils Moar Easing

It seems open-ended ECB QE was just the thing that gold-buyers were waiting for as heavy volume sent gold futures soaring this morning…

Silver is not moving so much for now…

Negative Rates, Money Printing and Gold

“As well as being modified by its specific supply and demand conditions, Gold’s time preference is essentially for its moneyness, represented by its use as a medium of exchange and store of value. The moneyness aspect links it to its exchange value for all commodities, and it is this aspect of gold’s qualities that should warn us that a backwardation in gold, emanating from negative dollar interest rates, will herald a general backwardation in commodities as well.” – Alasdair Macleod, Negative Rates and Gold

The “perfect storm” is forming that will push gold to record highs in U.S. dollars. In 2008 a near-perfect storm hit the global financial system that drove the price of gold to record level in just about every currency including dollars. The only missing ingredient back then was negative interest rates. The same financial excesses that caused the previous financial crisis have reformed only now they are much larger in scale. Most of the western hemisphere has already implemented negative interest rates. Now Trump has opened that Pandora’s Box in the U.S.

Chris Marcus of Arcadia Economics invited me onto this podcast to discuss the implications of Trump’s proposal and how it will affect the precious metals sector:

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

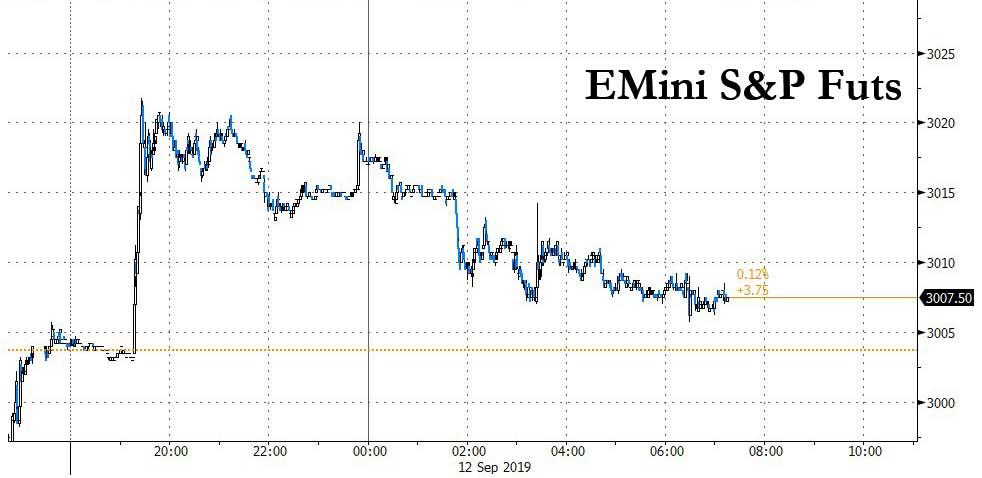

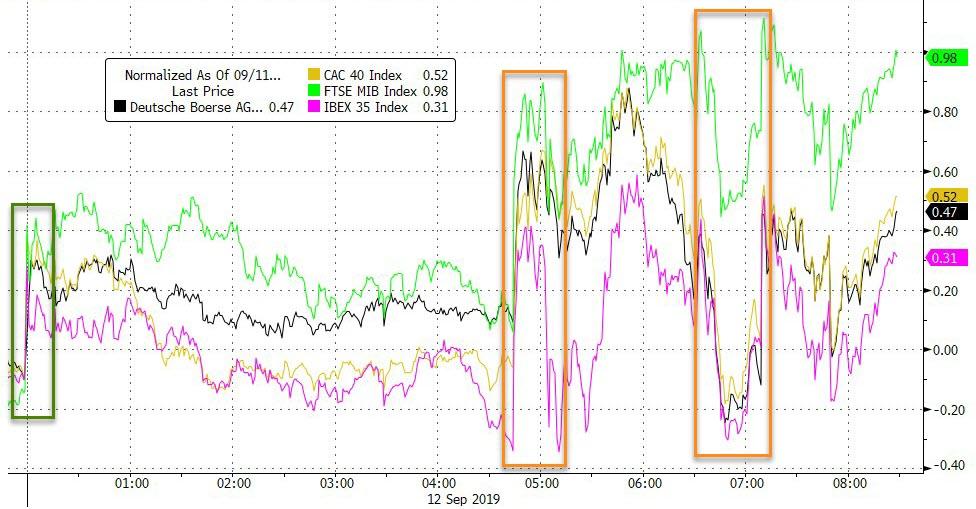

Rally Fizzles As Futures Fade Trade War De-Escalation, All Eyes On The ECB

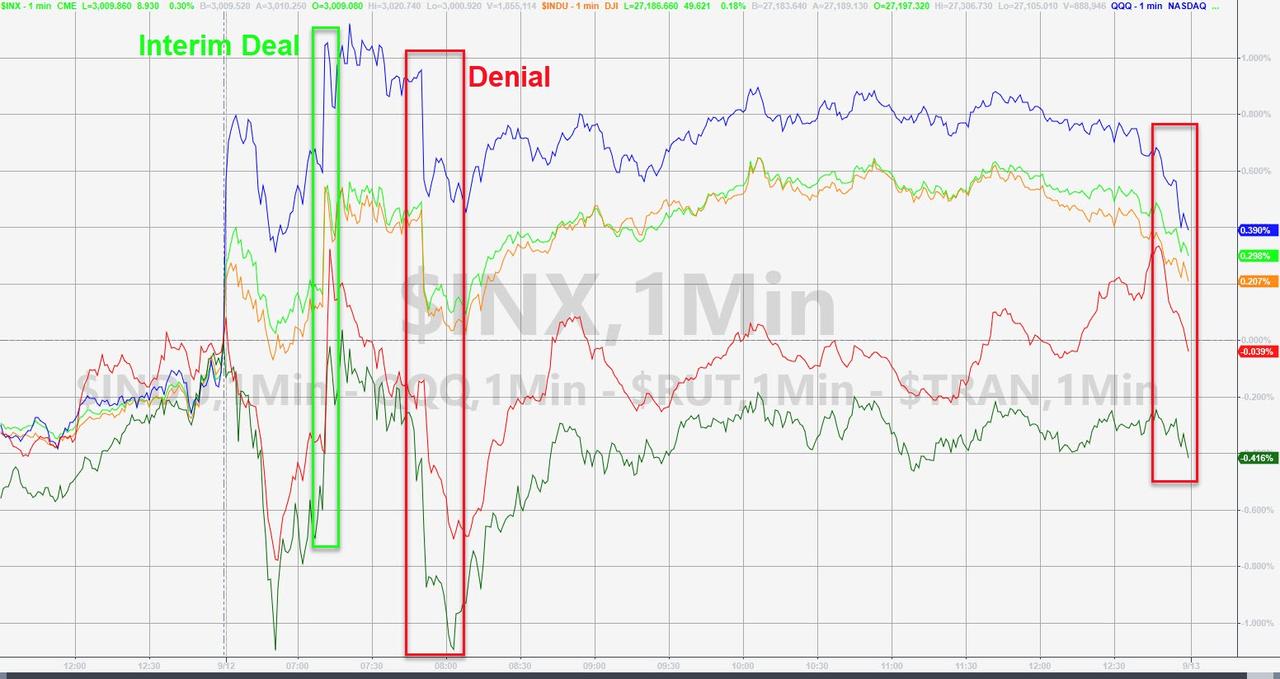

World stocks and US equity futures climbed to their highest in six weeks on Thursday, even if much of the gains fizzled in the overnight session, while the ECB was set to offer new stimulus measures and the United States and China made mutual concessions in their trade dispute.

Late on Wednesday, President Trump announced on twitter he would delay an increase in tariffs on Chinese goods by two weeks, after China exempted some U.S. drugs and other goods from tariffs, as a sign of “goodwill” toward China. The two moves buoyed stock markets from Asia to Europe and put pressure on safe assets like the Japanese yen.

In response to the Trump tweet, Global Times editor in chief Hu Xijin said that China “Welcome this decision. It should be seen as a goodwill gesture the US side made for creating good vibes for the trade talks scheduled in early October. Yesterday China announced to remove 16 categories of US products from tariff list. Hope reciprocity of goodwill can continue.”

Hu Xijin 胡锡进

✔@HuXijin_GT

Welcome this decision. It should be seen as a goodwill gesture the US side made for creating good vibes for the trade talks scheduled in early October. Yesterday China announced to remove 16 categories of US products from tariff list. Hope reciprocity of goodwill can continue. https://twitter.com/realDonaldTrump/status/1171925716503584773 …

Donald J. Trump

✔@realDonaldTrump

At the request of the Vice Premier of China, Liu He, and due to the fact that the People’s Republic of China will be celebrating their 70th Anniversary….

Meanwhile, China is considering whether to permit renewed imports of American farm goods including soybeans and pork, according to people familiar with the situation.

Still, some analysts said investors were getting too eager for good news on the U.S.-China trade war, and warned that the prospects of a quick resolution were still remote, they warned: “I don’t think we’re heading for a deal soon,” said Neil Wilson, chief market analyst at Markets.com. “The market is just buying on any kind of positive news – it seems hungry for anything. It’s setting itself up for a bit of disappointment.”

That may explain why after surging to just shy of all time high after the Trump tweet, futures have since faded much of the move.

The MSCI world equity index rose 0.1% to its highest since Aug. 1. It was on course for its seventh straight day of gains, its best winning streak in since early June.

Europe’s Euro STOXX 600 climbed to its highest in nearly seven weeks, but like US futures gave up most gains. Paris and London markets also relinquished early gains, though Frankfurt held onto a 0.2% advance. Wall Street futures gauges were up 0.1%.

Earlier in the session, Asian stocks rose for a second day, led by material producers and technology firms as trade tensions eased. Most markets in the region were up, with China leading gains. The Topix climbed 0.7% to a four-month high, as Daikin Industries and Daiichi Sankyo offered strong support. Japanese earnings revisions will likely bottom out next month, Citi equity strategist Tomochika Kitaoka wrote in a Sept. 12 note. The Shanghai Composite Index advanced 0.8%, with Kweichow Moutai and Ping An Insurance Group among major boosts. India’s Sensex fluctuated, as a rally in ICICI Bank countered declines in Reliance Industries and Tata Consultancy Services

With trade war apparently moving in the right direction, markets now focused on the ECB’s move, due at 745 ET, which also carries a risk of overly optimistic market expectations as major central banks worldwide have been loosening monetary policy, as inflation expectations are sliding and the powerhouse German economy is at risk of recession. Consequently, ECB President Mario Draghi has all but promised more support. But, as we discussed last night, the central bank’s exact moves are far from certain, and any decision that underwhelms markets could push up borrowing costs.

Among the likely measures are a cut in the ECB’s record-low minus 0.4% deposit rate, a multi-tier deposit rate, and new guidance on rates that would tie any move to certain inflation conditions. A new round of bond buying, the bank’s most potent weapon, is also an option – but policymakers from Germany to France are sceptical about that move.

“We could see some disappointment here. The challenge is more about forward guidance and reassurance for the future,” said Christophe Barraud, chief economist at Market Securities in Paris. “It would be surprising if the ECB launches a big stimulus right now ahead of uncertainties such as hard Brexit and the trade war.”

“Whether the ECB cuts rates by 10 or 20 bps is neither here or there. The big question is whether they restart QE, and if they don’t, we will see a further sell-off in bonds, especially longer-dated ones.” said Chris Scicluna, head of economic research at Daiwa Capital Markets.

In rates, Euro zone government bonds were steady in early trade, after rising from record lows reached a week ago on doubts that the ECB would resume asset purchases.

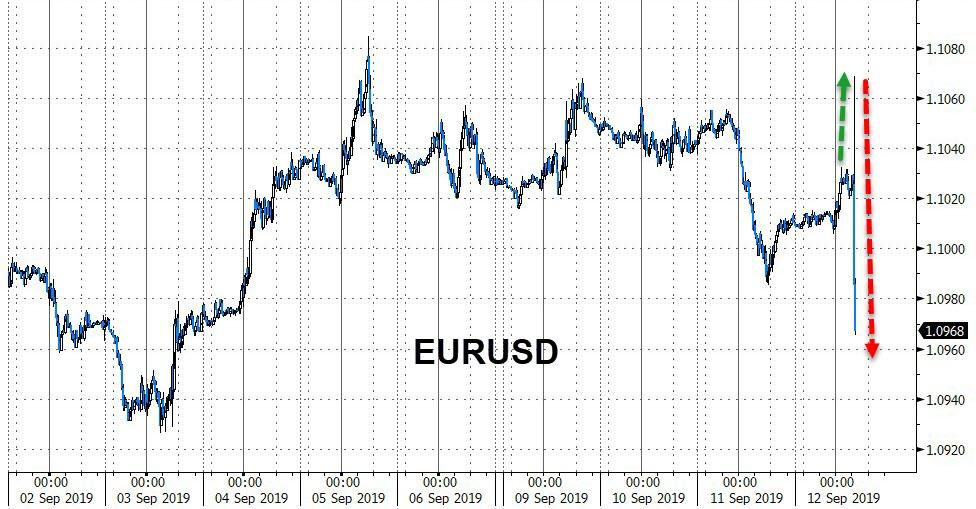

The optimism over trade and the looming ECB decision were felt in currency markets, too: the euro initially fell to a one-week low of $1.0983 overnight on expectations of ECB easing before steadying in morning trade, although it since spiked amid a wave of short covering. The euro has shed 3.5% since June. With risk-hungry investors emboldened, the Chinese yuan gained 0.4% against the dollar, touching a three-week high of 7.0855.

BMO’s FX strategist Stephen Gallo said he was surprised by the rebound, particularly in the yuan pushing beyond 7.10 to the dollar. “The bigger picture is one of a very tense geopolitical environment that is unlikely to be rectified quickly,” he said. The Japanese yen, a safe haven for nervous investors, fell to a six-week low against the dollar, and was last down 0.1% at 107.88.

In commodities, Brent crude futures fell as a meeting of the OPEC+ alliance yielded no discussion about increasing supply cuts. They focused instead on bringing Nigerian and Iraqi output down to their agreed quotas. Brent crude futures fell 69 cents, or 1.1%, to $60.12 a barrel, heading for a third session of losses.

Market Snapshot

- S&P 500 futures up 0.2% to 3,008.25

- STOXX Europe 600 up 0.02% to 389.78

- MXAP up 0.5% to 159.07

- MXAPJ up 0.5% to 513.33

- Nikkei up 0.8% to 21,759.61

- Topix up 0.7% to 1,595.10

- Hang Seng Index down 0.3% to 27,087.63

- Shanghai Composite up 0.8% to 3,031.24

- Sensex down 0.1% to 37,233.50

- Australia S&P/ASX 200 up 0.3% to 6,654.87

- Kospi up 0.8% to 2,049.20

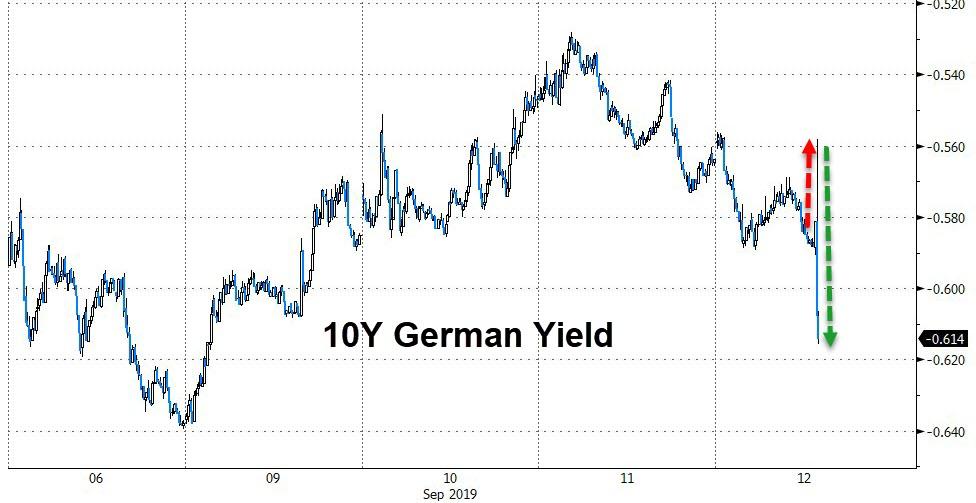

- German 10Y yield fell 1.5 bps to -0.579%

- Euro up 0.2% to $1.1028

- Italian 10Y yield fell 5.0 bps to 0.629%

- Spanish 10Y yield fell 3.2 bps to 0.223%

- Brent futures down 0.6% to $60.46/bbl

- Gold spot up 0.4% to $1,503.72

- U.S. Dollar Index down 0.1% to 98.51

Top Overnight News from Bloomberg

- Mario Draghi is embroiled in one of the most contentious policy meetings of his European Central Bank presidency as he prepares to ramp up monetary stimulus again despite skepticism from the euro area’s biggest economies

- The U.S. and China are taking small steps to ease trade tensions, as negotiators prepare for the resumption of face-to-face talks in coming weeks. On Wednesday, Trump said he was postponing the imposition of 5% extra tariffs on Chinese goods by two weeks; China is considering whether to permit renewed imports of American farm goods including soybeans and pork

- The full scale of the damage a no-deal Brexit could cause to the U.K. was revealed when Boris Johnson’s government published its worst-case scenario in a document it tried to keep secret. The five-page summary of no-deal planning, code-named Yellowhammer, was released late Wednesday

- The Hong Kong Exchanges & Clearing Ltd. plan to take over London Stock Exchange Group Plc is running into multiple obstacles less than 24 hours after the surprise bid was launched, with the U.K. bourse leaning toward rejecting the offer in its current form, according to people familiar

- As OPEC and its allies meet, the IEA said it faces a significant challenge in managing the market into 2020. Demand for the group’s crude in the first half of 2020 will be 1.4 million barrels a day below its August output as production surges from their competitors, including the U.S.

Asian equity markets were mostly higher as the region sustained the momentum from Wall St where US-China trade concessions fuelled the S&P 500 past the 3000 milestone and the DJIA back above 27k after China announced a tariff exemption list on imports from US, while US President Trump reciprocated by delaying the next round of tariffs on China to October 15th from October 1st. ASX 200 (+0.2%) and Nikkei 225 (+0.8%) were higher with support seen across the trade sensitive sectors in Australia although energy suffered amid recent losses in oil, while the Japanese benchmark was underpinned by a weaker currency and following better than expected Machine Orders data. Conversely, Hang Seng (-0.2%) and Shanghai Comp. (+0.8%) were mixed despite the encouraging trade developments as some suggested China’s olive branch could be to ease pressure from its weakening economy. The US delay of the tariff increase to 30% from 25% on USD 250bln of Chinese goods was also said to have left some dissatisfied in which Global Times noted comments that the postponement does not mean a big improvement as talks remain tough, while it was also suggested that the delay is far from enough and some called for a removal of the extra tariffs. Furthermore, the downside in Hong Kong was led by the blue-chip energy names and a slump in HKEX after its recent GBP 32bln proposal for LSE which could ultimately be rejected amid doubts regarding political risk and the deal structure. Finally, 10yr JGBs initially declined amid the improvement in trade relations and after similar pressure in USTs as yields rebounded, but later rebounded as support near 154.50 held and amid the BoJ presence for JPY 680bln of JGBs in the belly to super-long end.

Top Asian News

- Turkey Can Go Big on Rate Cut Without Erdogan’s Iconoclast Nudge

- Yahoo Japan to Pay $3.7 Billion to Take Over Maezawa’s Zozo

- Iron Ore Glory Days Seen Numbered as China Demand Rolls Over

A mixed session for European equities thus far [Eurostoxx 50 +0.2%] after the trade-fuelled gains seen at the open somewhat dissipated ahead of the much-anticipated ECB meeting and US CPI data amid the risk that the Central Bank may disappoint. Sectors are mixed with energy the laggard amid price action in the complex. Turning to individual stocks, AB InBev (+3.8%) shares were bolstered to the top of the Stoxx 600 amid renewed efforts to explore an IPO of its Budweiser Brewing unit on the Hong Kong Stock Exchange. Meanwhile, sources stated that LSE (Unch) is poised to reject the GBP 32bln merger offer from the Hong Kong Exchange due to concerns over political risks and deal structure. On the flip side, Whitbread (-2.7%), Lloyds (-2.0) and Accor (-3.3%) are all lower on the back of broker moves. In terms of commentary from banks, BAML sees 5% upside in European stocks over the coming 6-months due to positive EZ PMI momentum. The bank targets Stoxx 600 at 395 points for year end (~389 at time of writing).

Top European News

- France’s Bouygues Sells 13% Stake in Alstom for $1.2 Billion

- TeamViewer IPO Gives Germany Its First Tech Champion in Decades

- U.K. Earnings Would Still Rise in a No-Deal Brexit, Citi Says

- Trainline Surges After U.K. Ticket Sales Prompt Guidance Rise

In FX, the EUR has reclaimed 1.1000+ status vs the Greenback and survived another test of technical support ahead of 0.8900 against the Pound having crossed the 100 DMA, but the Euro’s fate will ultimately depend to a large extent on how much policy easing the ECB delivers later, or what President Draghi says to address any disappointment/overexuberance in the post-meeting news conference and Q&A. Indeed, given the wide spread of options signalled by the Bank in July and clearly divergent leanings from the GC since, expectations are far more polarised than usual – see our full preview on the Research Suite. In the run up to 12.45BST and 13.30BST, a spread of hefty option expiries should keep Eur/Usd occupied and contained, with 1.1 bn at 1.0970-80, 1.5 bn at 1.1000 and 1.8 bn between 1.1040-55 vs the 1.1006-32 range so far.

- NZD/AUD/CHF – The Antipodean Dollars are just outperforming the Franc at the head of the G10 ranks, as US-China trade relations continue to thaw via President Trump responding to Beijing’s goodwill gesture by delaying planned tariff hikes on Chinese goods for 14 days from October 1 to 15. However, the recently lagging Kiwi has benefited most this time, with Nzd/Usd regaining a firmer foothold above 0.6400, while the Aussie continues to face heavy resistance and cross-winds ahead of 0.6900 and over 1.0700 in Aud/Nzd. Meanwhile, Usd/Chf has retreated towards 0.9900 again, shrugging off softer Swiss producer/import prices, but aided by a broad Buck fade (DXY slipping back to pivot 98.500 compared to a 98.746 peak yesterday) and the aforementioned still defensive Eur (cross meandering from 1.0945 to 1.0915).

- CAD/JPY/GBP – All on a softer footing, as the Loonie hands back more gains having failed to sustain its rally beyond 1.3150 and a further downturn in crude prices also weighs on sentiment ahead of US CPI, initial claims and more Canadian housing data. Usd/Cad has subsequently extended to almost 1.3200, in line with Usd/Jpy rising through 108.00 before waning around the 100 DMA (108.15), but holding above decent expiry interest at 107.50-60 (1.6 bn). Elsewhere, Sterling has faded some distance from recent peaks and short of 1.2350 amidst less than positive reports from the EU on the subject of a Brexit breakthrough, as the UK has still not provided a real alternative to the Irish border backstop. Cable is currently just above the 55 DMA (1.2311) circa 1.2325.

- EM – Broad gains across the region in part due to the constructive US-China trade developments and the Dollar’s loss of momentum noted above, but with the Yuan also heeding another steady PBoC reference rate overnight, while the Lira has regained some composure into the CBRT after markedly underperforming of late amidst aggressive easing forecasts – again a more detailed primer is available via the Ransquawk website.

In commodities, WTI and Brent futures have been dipping in recent trade after a sideways overnight session, with the JMMC meeting in Abu Dhabi underway. Commentary from oil ministers has largely surrounded the need to bring compliance to 100% for all members. Sources also noted that the oil producers are holding discussions over whether to enhance compliance with oil cuts, which could result in an effective output reduction of around 400k bpd; although, this may be less than participants envisaged. Furthermore, the new-appointed Saudi Energy Minister stated that the Kingdom will continue to over-comply, whilst noting that Saudi October production will be 9.89mln BPD, up from the August level of 9.63mln BPD, which could have added pressure in the oil complex. WTI and Brent futures currently reside below 55.50/bbl and 60.50/bbl ahead of the ECB Monetary Policy decision. Elsewhere, gold prices have reclaimed the 1500/oz to the upside amid a weaker USD and nervousness that the ECB could disappoint. It’s also worth keeping in mind that President Trump delaying the China tariffs does not ultimately change the landscape in regard to sticking points, with China noting that talks remain tough and there will be no compromises on IP if it stalls China’s growth. Copper, on the other hand, has extended gains above the 2.60/lb level ahead of its 100 DMA at 2.66/lb amid continued hope that Chinese stimulus will buoy the demand side of the equation.

US Event Calendar

- 8:30am: US CPI MoM, est. 0.1%, prior 0.3%; CPI YoY, est. 1.8%, prior 1.8%

- 8:30am: US CPI Ex Food and Energy YoY, est. 2.3%, prior 2.2%; CPI Core Index SA, est. 264.1, prior 263.6

- 8:30am: Real Avg Hourly Earning YoY, prior 1.3%

- 8:30am: Initial Jobless Claims, est. 215,000, prior 217,000; Continuing Claims, est. 1.68m, prior 1.66m

- 9:45am: Bloomberg Consumer Comfort, prior 63.4

- 2pm: Monthly Budget Statement, est. $197.5b deficit, prior $119.7b deficit

DB’s Jim Reid concludes the overnight wrap

At the end of August, I pretty much finished this year’s annual Long Term Asset Return Study and am just administering the final touches to it ahead of a launch in the next 10 days. To celebrate the maiden voyage, I will be presenting the findings of the report at DB’s London HQ on Wednesday, September 25th at 8.30am (teas and coffees) for a 9am presentation. The report is entitled “The History and Future of Debt” and I specifically look at the record high levels of global debt and assess the likely future path using historical experience of how the level of indebtedness has ebbed and flowed through time. To register for the event please click here .

It won’t be a surprise to anyone that QE features heavily in the report both in historical terms and my belief that QE will eventually turn into helicopter money in the years ahead and that central bank holdings of government bonds will only grow and grow. With the crucial ECB meeting today, the main talking point in the near term is whether additional QE – that looked so nailed on a month ago – actually gets downplayed in the overall easing package or even postponed.

Before we preview the ECB in full, it’s worth highlighting the following overnight tweet from Mr Trump that shows some small signs of progress in the trade war. He tweeted that “at the request of the Vice Premier of China, Liu He, and due to the fact that the People’s Republic of China will be celebrating their 70th Anniversary….on October 1st, we have agreed, as a gesture of goodwill, to move the increased Tariffs on 250 Billion Dollars worth of goods (25% to 30%), from October 1st to October 15th”. Hu Xijin, of the Communist Party-controlled Global Times newspaper tweeted that he saw Mr. Trump’s decision as creating “good vibes” for the early-October talks. In addition, Bloomberg is reporting this morning that the Chinese government is considering whether to permit renewed imports of US farm goods including soybeans and pork, in a show of reciprocation of goodwill ahead of the upcoming face-to-face trade talks. In terms of markets reaction, the onshore Chinese yuan is up +0.41% this morning to 7.0872 alongside most Asian FX.

Equity markets are also heading higher on the news with the Nikkei (+0.89%), Shanghai Comp (+0.20%) and CSI 300 (+0.40%) all up. The Hang Seng is down -0.12%, weighed down by a slide in the city’s exchange thanks to the surprise $36.6bn takeover bid yesterday from Hong Kong Exchanges & Clearing Ltd for the London Stock Exchange Group Plc, a bold move that would upend the UK bourse’s combination with Refinitiv. South Korean markets are closed for a holiday. Elsewhere, futures on the S&P 500 are up +0.49% while yields have moved up by c. 2bps across the US treasury curve. As for overnight data releases, Japan’s August PPI came in one-tenth lower than consensus at -0.3% mom and July core machine orders stood at +0.3% yoy (vs. -3.7% yoy expected).

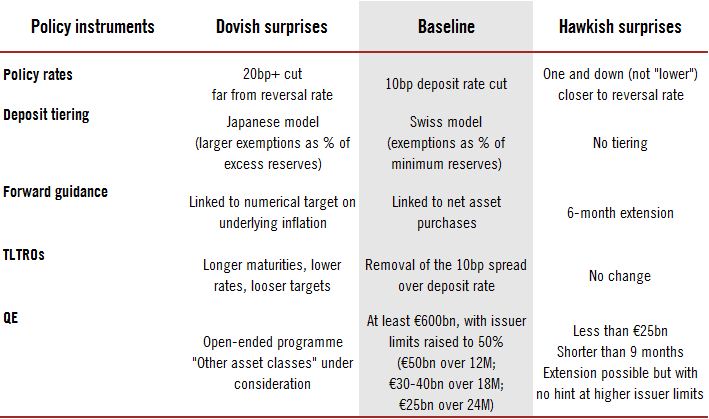

Back to the ECB preview now and the package today will likely include the first cut in the deposit rate since 2016 at what will be President Draghi’s penultimate meeting in charge. At time of writing, the market is split between seeing a 62.9% likelihood of a 10bp move lower, and a smaller 37.1% likelihood of a larger, 20bp cut. In their preview last Friday (link here ), our European economists wrote that they expect the ECB to announce a broad policy easing package, but they think the likelihood of QE being a part of that package have declined, as a result of opposition to new QE from some Governing Council members, along with the risk that further QE which flattens the yield curve would be counterproductive for banks. Their view is that there’ll be a 10bp deposit facility rate cut, upgraded forward guidance, and tiering, which would be more positive for banks.

In terms of the specifics, they expect the 10bp deposit rate cut will be followed by another 10bps in December, after Draghi has left office, and think the “or lower” easing bias will be maintained. On tiering, they think that the ECB will keep the mechanism simple, although this may come at the expense of a dynamic solution (one that adjusts continuously to the volume of excess liquidity). And on forward guidance, they think that the more likely option will be using guidance to strengthen the symmetry of the inflation target. The highest level of uncertainty relates to QE. After Draghi’s dovish Sintra speech, QE became part of baseline expectations. However, our economists are concerned about the inconsistency between QE – big QE at least – and tiering if the latter signals an emergent sensitivity to banking, especially given the fact that some ECB officials have spoken out against new QE over the last few weeks. Even the hawks haven’t really pushed back against rate cut expectations. Our economists adjusted their view on QE last week to anticipate a moderately more pro-banking outcome. That is, a steeper curve which results from no QE or QE targeted at the short end or QE targeted at private assets only. Less QE rather than more, which might be the compromise between hawks and doves, fits with the argument.

So this could be the meeting where the ECB implicitly acknowledges that the reversal rate across the whole curve is near to being breeched or has already been. It’s not a coincident that the Euro Bank Stoxx index hit 7 year lows on August 15th, the first day 10yr Bunds ever closed below -0.7%. In fact, over the last 30 years of data (7,715 days) the banks index has only closed lower than the August 15th level on 8 days, 4 during the 2012 Euro sovereign crisis and 4 in 1987. Not even the GFC/Lehman default period saw lower closes. The +12.99% rally since the recent trough has coincided with the yield sell-off, which has been largely associated with lower expectations for QE. Given how important the banking sector is to the European economy are we at a stage where no public-sector QE would actually be more positive for European growth and markets than some? An open question to you all.

Looking at markets now, it was another eventful day in fixed income yesterday with 10yr Treasuries swinging between gains and losses before ultimately selling off for the sixth consecutive session, up +1.0bps. The picture in Europe was more mixed, as 10yr bund yields ended -1.7bps, having been +1.9bps at their intraday high, while BTPs also fell -5.1bps and gilts closed flat. 30yr bund yields ended the session -2.0bps to almost close in negative territory once again, while in credit, US HY spreads rose +1.3bps to end their run of five successive moves tighter, and Euro HY also moved +1.1bps as they widened for a fourth consecutive session. IG supply still runs at high levels, which is causing some indigestion there.

It was a more consistent story in equity markets where advances were seen across the board. The S&P 500 (+0.71%), Nasdaq (+1.06%) and the Dow Jones (+0.85%) all closed higher with Apple leading the way (+3.18%) after the release of its new iPhone 11. Investor sentiment was boosted by the news we highlighted from the Asia session yesterday that China would be exempting a new list of products from import tariffs for 12 months from September 17. It comes ahead of a planned meeting next month where Chinese Vice Premier Liu He will be travelling to Washington. Trade-related stocks performed strongly, with the Philadelphia semi-conduct index up +1.46%. Yesterday’s strong credit data from China helped sentiment as well, as new yuan loans and aggregate financing both rose more than expected. In Europe, the STOXX 600 rose +0.85% to reach its highest level in 6 weeks, although the STOXX Banks index (discussed at length above) snapped a run of 5 consecutive gains to be down -0.21%.

Elsewhere oil fell further yesterday, with WTI -2.44%, after news reports that President Trump had looked at easing Iranian sanctions in order to agree a meeting with Iranian President Rouhani. Former National Security Advisor Bolton had taken a hawkish stance on Iran, and his resignation had already sent oil prices lower as markets reacted to the increased chances of diplomacy with Iran. Less risk of supply disruptions translates to a lower risk premium for the commodity. However, WTI prices are back up +0.90% this morning on the news of delay in tariff implementation mentioned above.

Earlier, President Trump had also tweeted about the Fed again, saying they “should get our interest rates down to ZERO, or less, and we should then start to refinance our debt.”

There was an interesting development yesterday in the Brexit saga, as the Court of Session in Scotland ruled yesterday that the prorogation of Parliament was ‘unlawful’, in another in a series of defeats for Prime Minister Johnson. All eyes will now be on the UK Supreme Court, which is set to hear the case on Tuesday. Meanwhile, a spokesman for the Conservatives ruled out a pact with the Brexit Party in an upcoming general election, which could have potentially monopolised the pro-Brexit vote under a single banner. Sterling fell -0.17%, coming a touch off its six-week high against the dollar.

It was a quite day for data with August US PPI the highlight. It rose to 1.8% (vs. 1.7% expected), while the PPI ex-food and energy rose to 2.3% (vs. 2.2% expected). Roll on CPI today.

Looking to the day ahead, the ECB decision and Draghi’s press conference is the main highlight, while the CBT are also meeting. Our CEEMEA team are expecting a 275bps rate cut, in line with expectations, which follows the 425bps cut at the July meeting, but they see the balance of risks tilting towards a larger-than-expected cut (potentially up to 400bps). They also updated their view on TRY, shifting to a more negative view (link here ) . In terms of data releases, we have Euro Area industrial production data for July, the final August CPI readings for France and Germany and Q2 unemployment from Italy. Meanwhile from the US, we’ve got August’s CPI readings and weekly initial jobless claims. Lastly on the political scene, we have another Democratic primary debate tonight, with the top 10 candidates vying for the nomination all on the same stage for the first time.

3A/ASIAN AFFAIRS

I)THURSDAY MORNING/ WEDNESDAY NIGHT:

SHANGHAI CLOSED UP 22.42 POINTS OR 0.75% //Hang Sang CLOSED DOWN 71.43 POINTS OR 0.26% /The Nikkei closed UP 161.85 POINTS OR 0.75%//Australia’s all ordinaires CLOSED UP .20%

/Chinese yuan (ONSHORE) closed UP at 7.0852 /Oil DOWN TO 55.35 dollars per barrel for WTI and 60.02 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED UP // LAST AT 7.0852 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0776 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

Last night: Trump delays increase in Chinese tariffs over just two weeks but that was enough to cause futures to surge

(zerohedge)

Trump Delays Increase In China Tariffs Until October 15; Futures Surge

Just hours after China, as a gesture of goodwill, waived tariffs on 16 types of US goods in a clear attempt to get on Trump’s good side and “sweeten” trade talks, a move which clearly was not lost on the US president, moments ago Trump said he was delaying a 5% increase in tariffs on Chinese goods by two weeks, supposedly out of respect for the celebration of the 70th anniversary of the revolution that brought the communist government to power.

“At the request of the Vice Premier of China, Liu He, and due to the fact that the People’s Republic of China will be celebrating their 70th Anniversary on October 1st, we have agreed, as a gesture of good will, to move the increased Tariffs on 250 Billion Dollars worth of goods (25% to 30%), from October 1st to October 15th,” Trump tweeted at7;17pm.

Donald J. Trump

✔@realDonaldTrump

At the request of the Vice Premier of China, Liu He, and due to the fact that the People’s Republic of China will be celebrating their 70th Anniversary….

Donald J. Trump

✔@realDonaldTrump

….on October 1st, we have agreed, as a gesture of good will, to move the increased Tariffs on 250 Billion Dollars worth of goods (25% to 30%), from October 1st to October 15th.

While Trump claimed that the move was out of respect for the Chinese National Day holiday, it is far more likely an in kind response to China’s announcement that a range of U.S. goods would be exempted from 25% extra tariffs put in place last year.

The delay comes into place just 11 days after a new round of tariffs kicked into place, and followed an escalation of the U.S.-China trade war in August when Trump announced an increase in the tariffs on $250 billion in Chinese goods to 30% from 25% starting Oct. 1.

The nations are scheduled to hold two rounds of face-to-face negotiations in Washington in coming weeks with the first this month and the second in early October with a visit from He.

The news sent S&P Emini futures surging by 0.6%, or up 17 points, to 3,020, just 7 points away from the July 26 all time high, and the Dow up over 140 points…

… sending the Dow back to where it was when Trump suffered his tariff tantrum at the end of July…

… with the Nasdaq…

… and the Yuan also sharply higher.

Source: Bloomberg

In the process roundtripping back to where the yuan was before China announced its retaliation to the latest round of US sanctions.

Source: Bloomberg

But yuan remains dramatically decoupled from US stocks.

Source: Bloomberg

At this rate, the S&P will be at its all time highs by the open tomorrow, which means that next Thursday the Fed will cut rates by 25 bps with the US stock market at fresh all time highs…. unless of course, the Fed sees today’s de-escalation as a key transition in the trade war and decides to delay rate cuts. Which, however, it won’t as otherwise – with the ECB set to cut tomorrow and restart QE – Trump will show up at the Marriner Eccles building with a flamethrower and burn the whole place down.

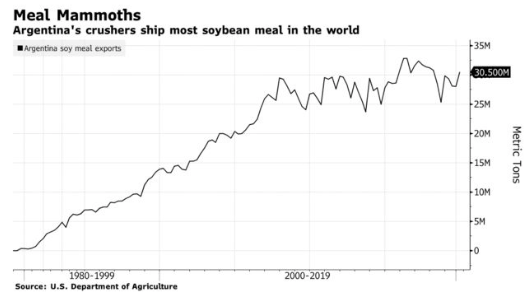

Huge Blow To US Farmers: China Heads To Argentina For Soy Meal In Landmark Deal

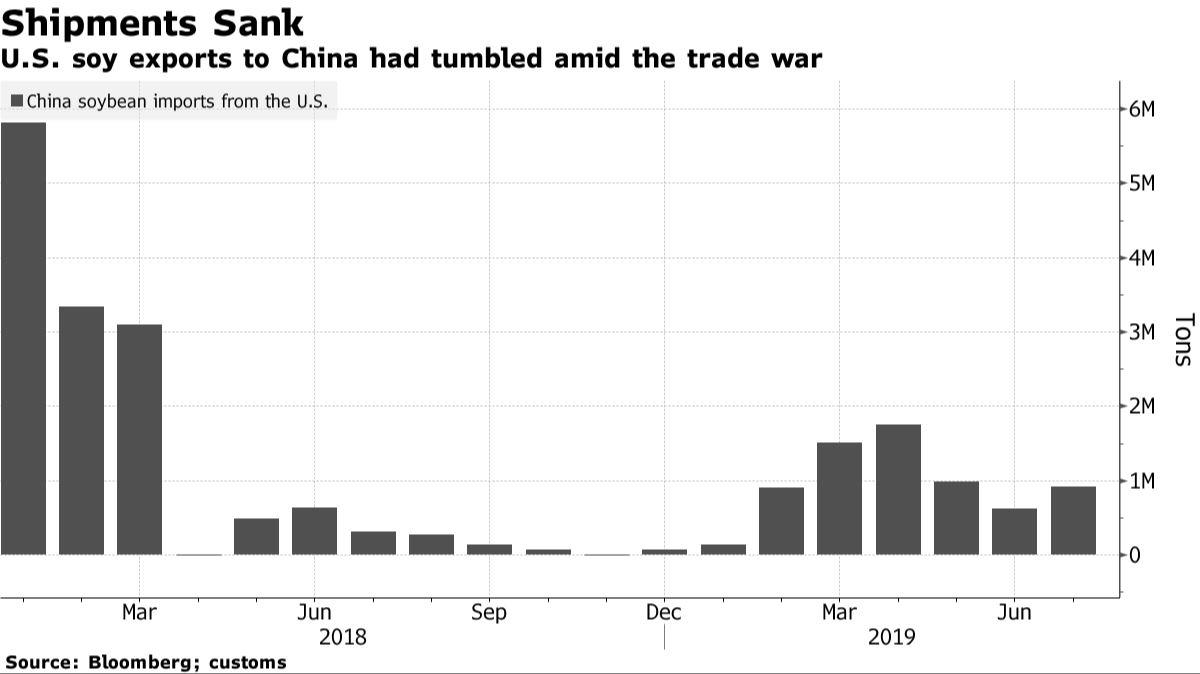

News for US farmers gets worse by the week. From collapsing farm incomes to plunging crop exports to China, the trade war has likely ushered in the next farm crisis, set to explode across the Central and Midwest US next year.

A new report from Reuters outlines how China has ditched US farmers for Argentina. An agreement between both countries is expected to be signed on Wednesday in Buenos Aires, describes how Argentina, the world’s biggest exporter of the animal feed, will allow China to import soy meal for the first time.

Last month Chinese officials examined several Argentine soy meal companies ahead of the signing ceremony on Wednesday.

Argentina’s Agriculture Ministry said in a statement on Tuesday that after two decades of discussions, the Asian giant will begin imports of soy meal in the near term.

The deciding factor for the landmark deal was the US-China trade war, which strengthened Argentina’s hand after China halted all US agriculture product imports this summer, prompting China to source more agriculture products from South America.

“This is a historic agreement,” Gustavo Idigoras, president of Argentina’s CIARA-CEC chamber of grains exporting companies told Reuters, though he added the deal still required a two-step process of plant authorizations and then registrations that could take several more months.

Idigoras said, “shipments aren’t expected to start immediately,” but could start in the near term. China still has some bureaucratic bottlenecks before cargoes can set sail, he added.

In a separate report last month, China is preparing a bid that would allow it to dredge Argentina’s Parana River, the country’s only river that acts as a waterway for bulk vessels that transport soybean and corn from the Pampas farm belt to the South Atlantic.

An increased waterway would allow China to create a grain superhighway in Argentina that would effectively be able to replace US farmers.

Argentina, already the top exporter of processed soy, is expected to export 26 million tons of soy meal this year worldwide, and 8.5 million tons of raw beans.

“It is excellent and timely news. Argentina needs to add more value to its exports to China and the world,” said Luis Zubizarreta, president of Argentina’s ACSOJA soy industry organization that represents farmers.

Allowing China to buy from Argentine farmers would tremendously boost exports next year. China has come at the right time, considering profit margins have been falling, and idle capacity has increased to more than 50%.

China has been busy in South America. They’ve been building massive infrastructure projects across Argentina, from hydroelectric plants to railways.

Business-friendly President Mauricio Macri has said the new partnership with China would boost the country’s agricultural sector and create enormous opportunities for farmers.

While boom times are here for Argentine farmers, a bust cycle is imminent for US farmers who are on the brink of collapse after being shut out of China thanks to President Trump’s trade policies.

Beijing Considers Re-Authorizing Imports Of US Agricultural Products In Latest ‘Goodwill’ Gesture

Last night, we reported that President Trump had decided to delay a 5% increase in tariffs on Chinese goods by two weeks, supposedly out of respect for Beijing and its celebration of 70 years of Communist Party rule on Oct. 1. Trump’s decision came less than a day after China waived 25% tariffs on 16 types of US goods to try and “sweeten” the deal ahead of trade talks next month.

Now, in the latest tit-for-tat deescalation of trade tensions, Bloomberg reports that Beijing is considering whether to permit imports of American agricultural products including soybeans and pork, a move that would further alleviate trade tensions while bolstering support for Trump in the midwestern farm states that comprise a sizable chunk of his base. Foodstuffs and farm products were notably not included in the 16 goods exempted from tariffs earlier this week. According to the Ministry of Commerce, Chinese companies have started asking about prices for US soybeans and pork, a sign that they could restart imports in the near future.