GOLD:$1505.50 UP 1.50 (COMEX TO COMEX CLOSING)

Silver:$18.08 UP 14 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1501.00

silver: $18.01

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 1/6

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,503.100000000 USD

INTENT DATE: 09/16/2019 DELIVERY DATE: 09/18/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 2

661 C JP MORGAN 1

737 C ADVANTAGE 2 3

905 C ADM 4

____________________________________________________________________________________________

TOTAL: 6 6

MONTH TO DATE: 1,730

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 6 NOTICE(S) FOR 600 OZ (0.0186 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1730 NOTICES FOR 173000 OZ (5.3810 TONNES)

SILVER

FOR SEPT

147 NOTICE(S) FILED TODAY FOR 735,000 OZ/

total number of notices filed so far this month: 8344 for 41,720,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10,169 DOWN 85

Bitcoin: FINAL EVENING TRADE: $ 10251 UP 3

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A HUGE SIZED 1725 CONTRACTS FROM 216,366 DOWN TO 214,641 DESPITE THE HUGE 41 CENT GAIN IN SILVER PRICING AT THE COMEX. WE HAD CONSIDERABLE BANKER SHORT COVERING TODAY.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

SEPT , 0 FOR DEC. 1604, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1604 CONTRACTS. WITH THE TRANSFER OF 1604 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1604 EFP CONTRACTS TRANSLATES INTO 8.02 MILLION OZ ACCOMPANYING:

1.THE 41 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

42.560 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE AGAIN HAD HUGE COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY AS NO DOUBT OUR FRIENDS WERE SCARED OF THE GEOPOLITICAL LANDSCAPE THEY WERE FACING. THE 7 CONSECUTIVE THUMPING OF SILVER ENDED.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE ARE NOW WELL INTO THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

23,020 CONTRACTS (FOR 11 TRADING DAYS TOTAL 23,020 CONTRACTS) OR 115.10 MILLION OZ: (AVERAGE PER DAY: 2092 CONTRACTS OR 10.46 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 115.10 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 16.42% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1664.72 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1725 DESPITE THE 41 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1604 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 121 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1604 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1741 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 41 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.94 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.071 BILLION OZ TO BE EXACT or 153% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 147 NOTICE(S) FOR 735,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 42.560 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3377 CONTRACTS, TO 625,007 ACCOMPANYING THE $11.75 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7602 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 4483 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 625,218,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7860 CONTRACTS: 3377 CONTRACTS INCREASED AT THE COMEX AND 4483 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 7860 CONTRACTS OR 786,000OZ OR 24.44 TONNES. YESTERDAY WE HAD A GAIN OF $11.75 IN GOLD TRADING….

AND WITH THAT HUGE GAIN IN PRICE, WE HAD A GOOD GAIN IN GOLD TONNAGE OF 24.44 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TRYING TO CONTAIN THE PRICE RISE WITH NOT MUCH SUCCESS. AND WITH THAT GAIN IN PRICE, WE HAD A VERY STRONG GAIN IN GOLD TONNAGE OF 24.44 TONNES!!!!!!. OUR BANKER FRIENDS TRIED IN VAIN TO COVER THEIR SHORTS TODAY BUT TO NO AVAIL. AS IN SILVER THEY WERE FRIGHTENED BY THE GEOPOLITICAL LANDSCAPE BUT WERE BASICALLY HAPLESS IN THEIR ATTEMPT TO COVER THEIR HUGE SHORTFALL.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 76,407 CONTRACTS OR 7,640,700 oz OR 237.65 TONNES (11 TRADING DAY AND THUS AVERAGING: 6946 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAYS IN TONNES: 237.65 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 237.65/3550 x 100% TONNES =6.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4389.26 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 3377 DESPITE THE STRONG PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($11.75)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4483 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4483 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED GAIN OF 8071 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4483 CONTRACTS MOVE TO LONDON AND 3377 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 24.44 TONNES). ..AND THIS GOOD INCREASE OF DEMAND OCCURRED WITH THE STRONG GAIN IN PRICE OF $11.75 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 6 notice(s) filed upon for 600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $1.50 TODAY//(COMEX-TO COMEX)

NO CHANGES IN GOLD INVENTORY AT THE GLD//

INVENTORY RESTS AT 874.51 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 14 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 376.502 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 1725 CONTRACTS from 216,199 DOWN TO 214,641 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1604: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1604 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1725 CONTRACTS TO THE 1604 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL SIZED LOSS OF 121 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 0.605 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT 2019: 42.560 MILLION OZ//

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 41 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1604 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON. WE HAD CONSIDERABLE BANKER SHORT COVERING IN SILVER

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED DOWN 52.64 POINTS OR 1.74% //Hang Sang CLOSED DOWN 334.31 POINTS OR 1.23% /The Nikkei closed UP 13.03 POINTS OR 0.06%//Australia’s all ordinaires CLOSED UP .29%

/Chinese yuan (ONSHORE) closed DOWN at 7.0965 /Oil UP TO 61.77 dollars per barrel for WTI and 67.85 for Brent. Stocks in Europe OPENED RED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0965 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0913 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

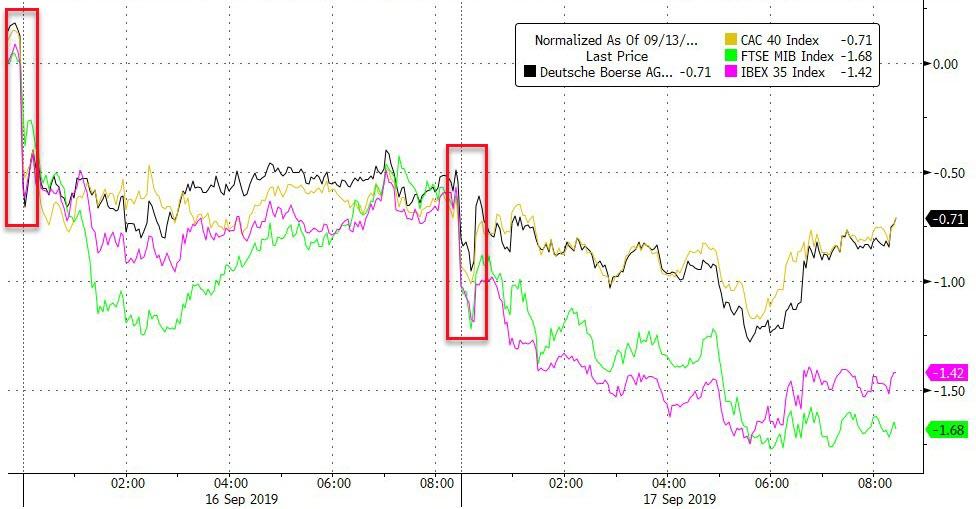

4/EUROPEAN AFFAIRS

Italy

Former Prime Minister Renzi has decided to leave his Democrat party and start a new party. He is a centrist but his party starting leaning far to the left. His new party will go back to his roots of being centrist. The Italian bonds tumbled on this news because of more instability

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

India/Pakistan

This does not look good: India’s Minister says Pakistan is about to lose Pakistani occupied Kashmir

(zeorhedge)

9. PHYSICAL MARKETS

i)China Gold, state owned operation of the Chinese government is now hunting for deals in gold equal to the $2 billion mark

(Bloomberg/GATA)

ii)Interesting: JPMorgan learned of spoofing as they inherited the assets including the huge short position of silver from Bear Stearns

(Bloomberg/GATA)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

The manufacturing data today was a little better than last month but not enough to overturn its recession label

(zerohedge)

iii) Important USA Economic Stories

a)We highlight to you the plight of the truckers. Mac Slavo gives us a good insight as to what happens if truckers stopped working all together: grocery stores would run out of food in 3 days

(Mac Slavo.SHFTPlan.com)

b)Michael Snyder weighs in on the hit of the Saudi oil facilities in Riyadh. The attack came from the North and West of Riyadh and due to the sophistication of the hits ,most likely it came from Iraq where Iranian Shiites are stationed. Documentation already exists that Iran has sent over to Iraq missiles capable of striking Riyadh.

(courtesy Michael Snyder)

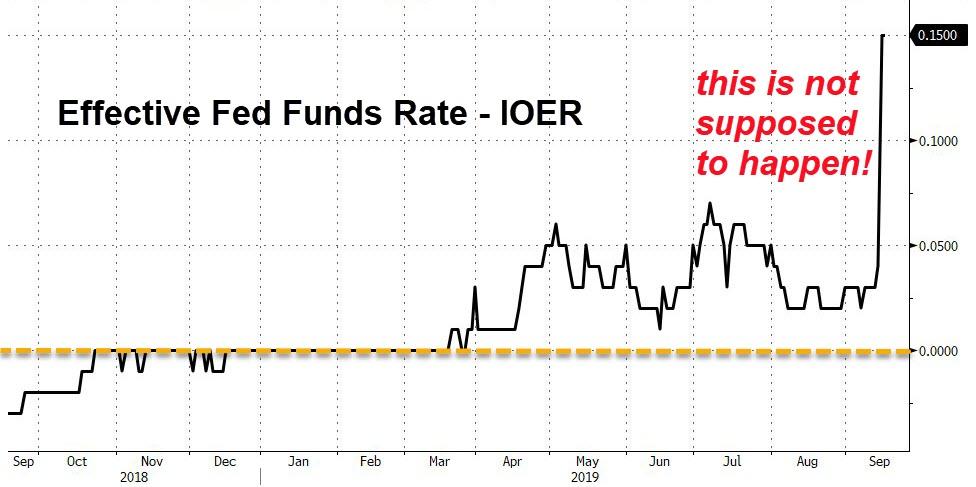

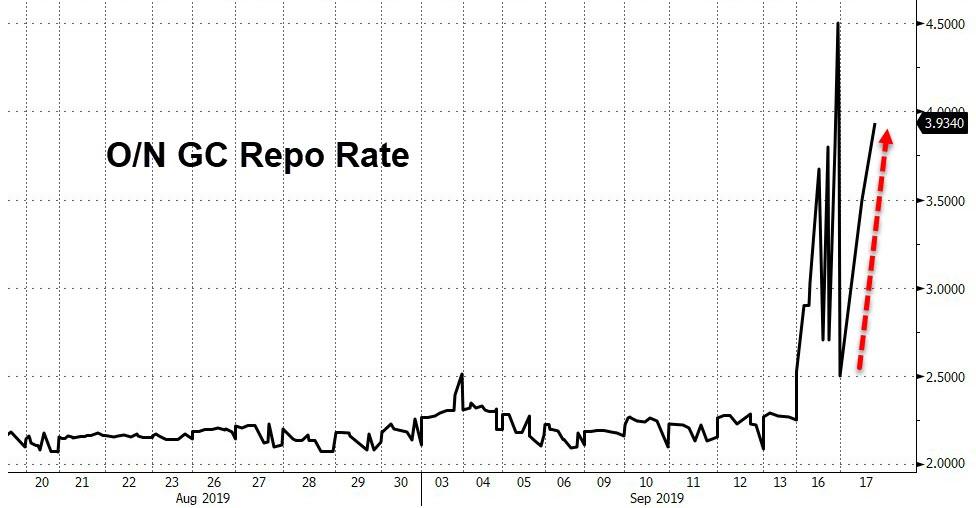

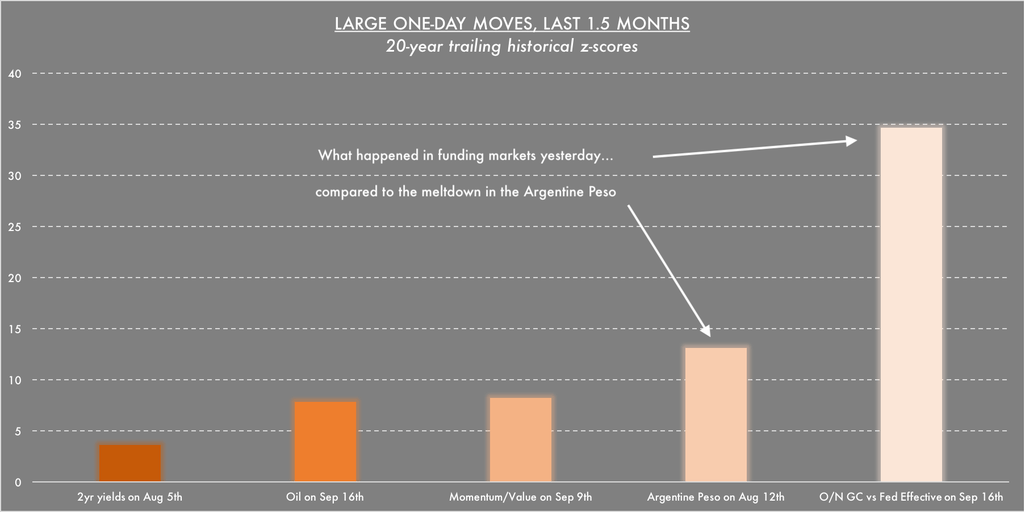

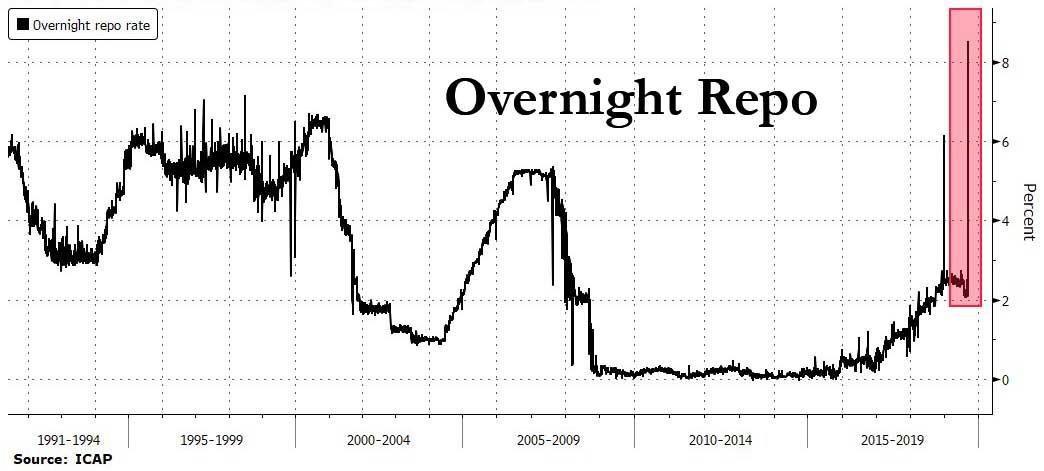

c)We pointed this out to you yesterday and the situation is getting worse. Now the rep market is freezing over due to lack of liquidity. The only way out of this s a huge QE

d)Whether it is due to lack of liquidity or the oil shock or whatever, the Fed has lost control of its rates again. The only way to bring them into equilibrium is more QE(zerohedge)

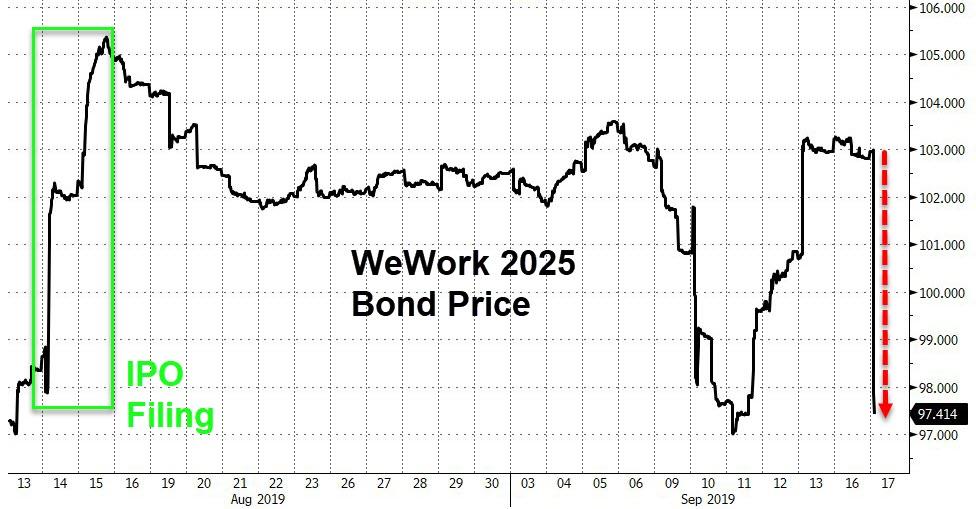

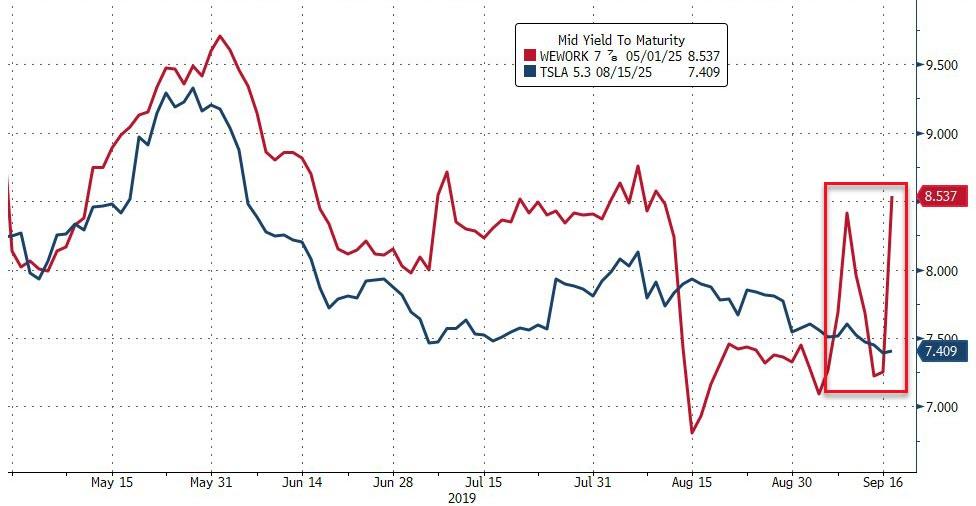

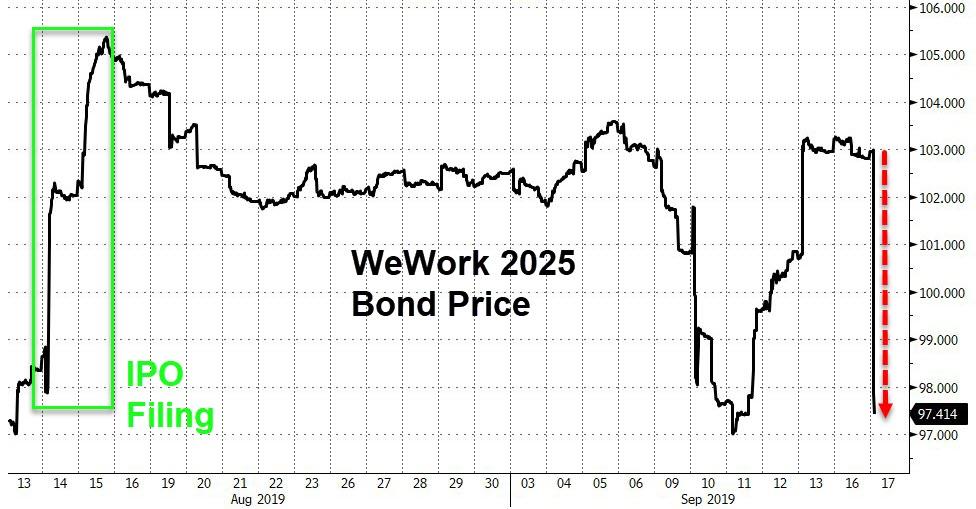

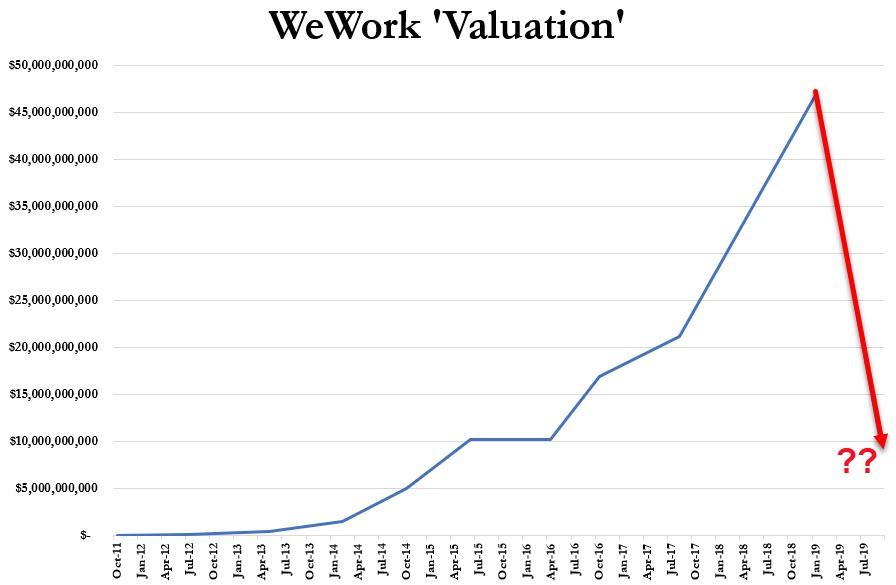

e)Another of our darling USA companies showing trouble. The ill fated We Work bonds are now crashing

f)Fed-Ex is a terrific bellwether for global growth. After the bell its shares tumbled after they slashed outlook..they blamed the trade war.(zerohedge)

iv) Swamp commentaries)

a)Trump is furious as the New York Times and demands the resignation of all of those involved in the latest Kavanaugh smear story/Russian Witch Hunt Hoax

(zerohedge)

b)The Kavanaugh smear seems to unravel as the original accuser’s witness now doubts the story in its entirety

(zerohedge)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; 96.453 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 82,310 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 112,213 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 112,213 CONTRACTS EQUATES to 561 million OZ 80.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.57% ((SEPT 17/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -1.02% to NAV (SEPT 17/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.57%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.16 TRADING 14.67/DISCOUNT 3.21

END

And now the Gold inventory at the GLD/

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 17/2019/ Inventory rests tonight at 874.51 tonnes

*IN LAST 665 TRADING DAYS: 60.87 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 565- TRADING DAYS: A NET 105.78 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 17/2019:

Inventory 376.502 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.11/ and libor 6 month duration 2.08

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .03

XXXXXXXX

12 Month MM GOFO

+ 2.08%

LIBOR FOR 12 MONTH DURATION: 2.07

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.01

gold lending rates negative all the way to one year

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Central Bank Gold Buying Is “Sustainable and Indeed May Accelerate”

◆ Why central banks including China and Russia will keep buying gold due to concerns about the outlook for currencies, including the dollar and the euro, Mark O’Byrne, Research Director of GoldCore told Marketwatch

◆ While the gold tonnage demand from central banks in recent months has been significant and near records, gold remains a tiny fraction of most central banks’ massive foreign-exchange reserves,” O’Byrne says, adding that the trend is “sustainable and indeed may accelerate”

◆ “Price is not the determining factor in central bank buying—rather, [the banks] are more likely being guided to secure an allocation of a percentage of their overall foreign-exchange reserves in gold bullion,” says O’Byrne. The central bank diversification and hedging are likely to support gold at these levels and could be a driver of higher prices in the coming months, he says

◆ “The risk of the trade war descending into a currency war may also be feeding central bank diversification into gold”

Read the full article on Barron’s and Marketwatch

NEWS and COMMENTARY

Gold prices hold steady ahead of Fed verdict

Gold settles at a more than a 1-week high as historic oil outage rattles investor nerves

$1,500 is the new floor for gold prices, says Kinross CEO

Gold & silver rally as investors seek safe havens amid global uncertainty

Expectations suddenly are rising that the Fed might not cut interest rates this week

Trump says he’s in no rush to respond to the attacks on Saudi oil facilities

Trump says U.S. reaches trade deals with Japan, no vote needed

China Gold are looking for “acquisition opportunities quite aggressively”

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

10-Sep-19 1494.60 1498.25, 1211.52 1211.34 & 1353.51 1357.11

09-Sep-19 1509.95 1509.20, 1223.81 1220.34 & 1368.62 1364.92

06-Sep-19 1504.95 1523.70, 1223.52 1237.09 & 1363.94 1378.49

05-Sep-19 1542.60 1529.10, 1257.06 1238.72 & 1397.44 1380.78

04-Sep-19 1538.80 1546.10, 1265.05 1269.97 & 1397.69 1403.86

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

China Gold, state owned operation of the Chinese government is now hunting for deals in gold equal to the $2 billion mark

(Bloomberg/GATA)

China Gold is hunting for deals of as much as $2 billion

Submitted by cpowell on Mon, 2019-09-16 23:08. Section: Daily Dispatches

By Vinicy Chan

Bloomberg News

Monday, September 16, 2019

China Gold International Resources Corp., the overseas arm of state-owned China National Gold Group, is on the hunt for acquisitions to replenish its pipeline as deal-making in the sector heats up thanks to a jump in the metal’s price.

“We need more pipeline, especially in gold production,” Jerry Xie, executive vice president, said in an interview today on the sidelines of the Denver Gold Forum. “We’re looking for acquisition opportunities quite aggressively. We’re doing this on behalf of our parent company, not just for ourselves.”

…

The miner, listed both in Canada and Hong Kong, is targeting companies with assets in operational stages that have ramp-up plans. The company is comfortable making purchases with a price at roughly $1 billion to $2 billion, Xie said.

The company is open to studying potential acquisitions of single-asset companies with mines near production, he said. It is also interested in possible asset sales that may come from Barrick Gold Corp. and Newmont Goldcorp Corp., which both have plans to divest after recent mega-mergers. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-09-16/china-gold-is-hunting…

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

END

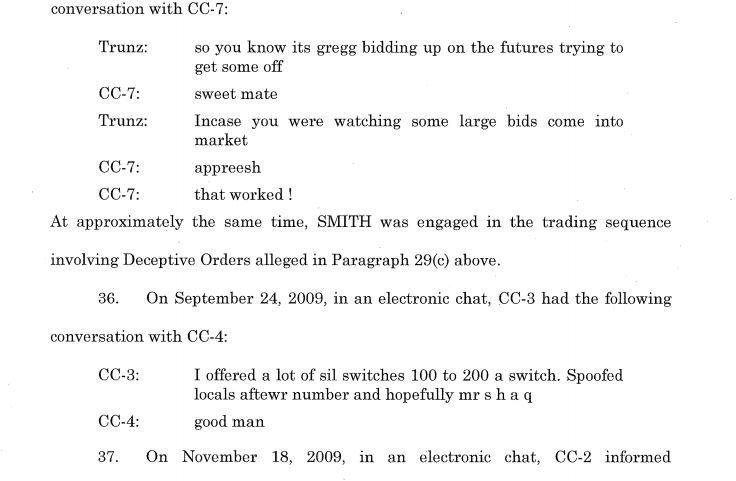

Interesting: JPMorgan learned of spoofing as they inherited the assets including the huge short position of silver from Bear Stearns

(Bloomberg/GATA)

JPMorgan inherited ‘spoof’ method from Bear Stearns and refined it, indictment says

Submitted by cpowell on Mon, 2019-09-16 23:25. Section: Documentation

A powerful vindication of silver market analyst and whistleblower Ted Butler, who long has said the racket began with JPMorganChase’s acquisition of Bear Stearns.

* * *

By Tom Schoenberg and David Voreacos

Bloomberg News

Monday, September 16, 2019

When JPMorgan Chase & Co. took over Bear Stearns more than a decade ago, it got two traders with a new trick.

Their strategy: Use multiple fake orders to manipulate the prices of precious metals futures. The maneuver, adopted by the traders’ new colleagues at JPMorgan, became part of a spoofing and rigging campaign so expansive that federal authorities have now likened it to a criminal enterprise operating inside the U.S.’ biggest bank.

In a criminal indictment unsealed today —

https://www.justice.gov/opa/press-release/file/1202466/download

— U.S. prosecutors accused three JPMorgan traders of rigging futures trades in precious metals for nearly a decade, making millions of dollars for the bank at the expense of counterparties that included the bank’s own clients.

…

The charges were the latest turn in a years-long investigation that has previously yielded guilty pleas from traders at several banks, including two from JPMorgan. Prosecutors said more than a dozen JPMorgan employees ultimately helped make manipulative “spoof” trades for the bank, in part by using the strategy their new colleagues brought in May 2008.

That pair, Gregg Smith and Christiaan Trunz, showed their new JPMorgan colleagues “a new style of layering multiple deceptive orders at different prices in rapid succession,” prosecutors wrote. The strategy made their market spoofing more difficult to execute and detect, prosecutors wrote in the indictment of Smith and two others. Trunz pleaded guilty last month and is cooperating with authorities.

The strategy was adopted by Michael Nowak, who was JPMorgan’s global head of precious metals trading when he was put on leave last month. …

The Commodity Futures Trading Commission also filed a lawsuit against Nowak and Smith today and settled a suit against Trunz. …

JPMorgan bought Bear Stearns in a marriage arranged by the U.S. Federal Reserve during the height of the financial crisis in 2008.

Already, people inside JPMorgan were using deceptive trading methods, prosecutors said. Their new colleagues brought new ones. In May, the same month the deal was completed, Smith executed the deceptive-layering technique, the indictment said. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-09-16/precious-metals-trade…

JP Morgan Blames Bear Stearns For ‘Criminal Enterprise’ At Precious Metals Trading Desk

Now that prosecutors have blamed what they have described as a criminal organization operating inside JP Morgan, it appears the largest bank in the US by assets is resorting to an old strategy for sloughing off accusations of corporate fraud: Blaming it all on an acquisition.

According to Bloomberg, two traders who joined JPM’s precious metals trading desk after the takeover of Bear Stearns helped introduce the illegal manipulation strategy known as ‘spoofing’ to their peers on the desk, including the bank’s now-former head of the bank’s precious metals trading desk, Michael Nowak, who was one of three employees charged with participating in an organized fraud yesterday. Though prosecutors allege that some of the desk’s employees were already engaged in ‘deceptive practices’.

The two men who purportedly brought ‘spoofing’ to JP Morgan are Gregg Smith, one of the men arrested yesterday, and Christiaan Trunz, who joined the desk after JPM’s government-backed takeover of Bear Stearns. Trunz was famously quoted in yesterday’s indictment, including one exchange where he was telling a co-conspirator about fake orders being put out by Smith.

Prosecutors said that ultimately 12 JPM employees used the strategy during the years between 2008 and 2016 that are the primary focus of the investigation.

That pair, Gregg Smith and Christiaan Trunz, showed their new JPMorgan colleagues “a new style of layering multiple deceptive orders at different prices in rapid succession,” prosecutors said. The strategy made their market spoofing more difficult to execute and detect, prosecutors wrote in the indictment of Smith and two others. Trunz pleaded guilty last month and is cooperating with authorities.

The strategy was adopted by Michael Nowak, who was JPMorgan’s global head of precious metals trading when he was put on leave last month. Federal prosecutors charged Nowak, Smith and a third man, Christopher Jordan, of “conspiracy to conduct the affairs of an enterprise involved in interstate or foreign commerce through a pattern of racketeering activity” – language that sounds more like RICO charges.

On Monday, Jordan and Nowak appeared handcuffed in federal court in Newark, New Jersey, where US Magistrate Judge Michael Hammer released them on $250,000 bond. They could face up to 30 years in prison on the most serious charges. Meanwhile, Jordan was released to the custody of his parents pending being released this week to a residential alcohol treatment program (“Chris Jordan is innocent of these heavy-handed charges, and we intend to defend him vigorously,” his attorneys said. Nowak was ordered to receive mental health testing and treatment. The men were forbidden to have any contact with any other current or former employees of the JPM precious metals trading desk.

Earlier, Trunz, a former Georgetown lacrosse player, and the other former JPMorgan trader who admitted guilt said the manipulation was routine and sanctioned by higher ups on the desk.

“While at JPMorgan I was instructed by supervisors and more senior traders to trade in a certain fashion, namely to place orders that I intended to cancel before execution,” former trader John Edmonds said at a October 2018 hearing, after admitting to commodities fraud and conspiracy. Edmonds entered into a cooperation agreement with the CFTC in July.

Trunz told a federal judge in Manhattan last month that spoofing trades of precious metals was rampant at the bank and that he learned the technique from other traders at Bear Stearns and JPMorgan. Trunz, who entered his guilty plea on Aug. 20, said he manipulated futures markets for gold, silver, platinum and palladium from offices in New York, London and Singapore from 2007 to 2016.

Of course, the traders who are facing trial have reason to be optimistic. Prosecutors have failed to convict traders in the last two big securities fraud trials.

end

GATA) Ronan Manly: Indicted JPM metals desk chief is LBMA board member

Submitted by cpowell on 01:05PM ET Tuesday, September 17, 2019. Section: Daily Dispatches

9:05a ET Tuesday, September 17, 2019

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly reports today that JPMorganChase, more of whose metals traders were indicted yesterday in the United States on charges of manipulating the metals markets, is a member of the London Bullion Market Association and that one of those traders, Michael Nowak, chief of the bank’s precious metals desk, is a member of the LBMA’s Board of Directors.

Manly adds that the LBMA’s code of conduct explicitly prohibits market manipulation. Manly doesn’t say if the LBMA code provides any particular penalties for violation, but it’s a fair guess that they include being winked and nodded at.

Manly’s report is headlined “LBMA Board Member & JP Morgan Managing Director Charged with Rigging Precious Metals” and it’s posted at Bullion Star here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

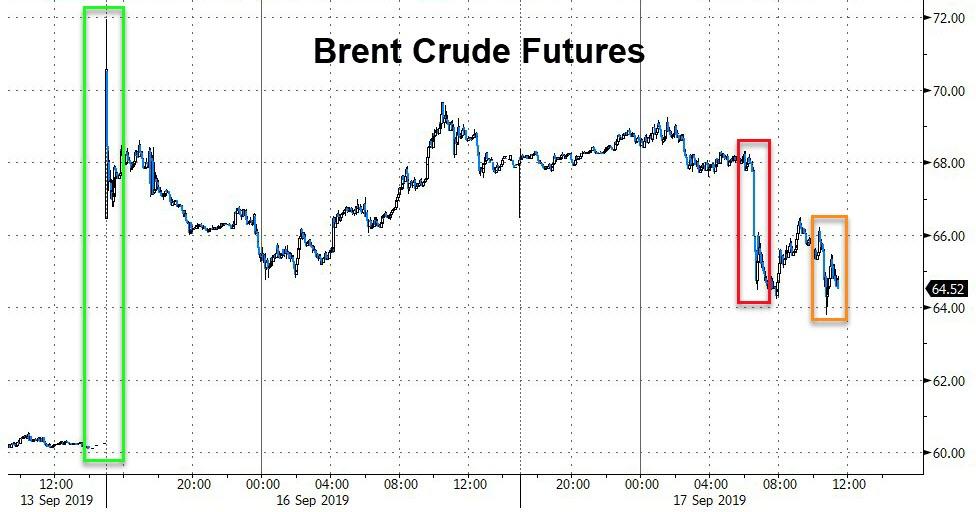

Markets Slide As Traders Put Oil Crunch On Backburner, Turn To Fed

Global stocks and US equity futures dipped, with the E-mini back under 3,000 again, as attention turned to the Fed (and the slight possibility Powell may disappoint investors again)…

… while Brent shed some of its massive gains on Tuesday as the United States de-escalated concerns of an imminent war with Iran and also flagged the possible release of crude reserves.

Investors, desperate for more love from money printers, were unsure what to do ahead of tomorrow’ interest rate cut from the Fed, which is fully priced in by the market even if tiny doubt appears to have crept in with 5% odds of “no change” which would crash the markets, as well as the next round of U.S.-China trade talks on Thursday.

MSCI’s All-Country World Index was down 0.1% on the day.

European shares opened lower, with energy stocks giving up gains as crude prices eased. Europe’s broad STOXX 600 index dropped 0.2%, led by declines in banks and automakers shares, even though Germany showed clear green shoots, and signs of sentiment rebound after the ZEW Economic Sentiment surged to -22.5 from -44.1, smashing the Expected print of -37.0.

Earlier in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan was down 0.66%. Chinese shares fell 1.07%, while Hong Kong shares slumped 1.18% after China’s central bank disappointed investors when it refrained from lowering a key interest rate.

US stocks futures were flat to slightly lower, indicating subdued open on Wall Street later, with the S&P set to open below 3,000 once again.

All eyes were on oil however, which gave back only a bit of Monday’s record surge: Brent crude oil fell 0.1% to $68.96 per barrel on Tuesday. On Monday, it surged as much as 14.6% for its biggest one-day percentage gain since at least 1988. In the US, West Texas Intermediate futures were down 0.87% to $62.25 per barrel following a 14.7% surge on Monday, the biggest one-day gain since December 2008.

Saudi Aramco now faces weeks or months before the majority of output is restored at the giant Abqaiq processing plant after the attack, adding a fresh headwind for the global economy. The developments in the Middle East are testing sentiment after a bullish start to the month for global equities and other riskier assets. Meanwhile, Iran won’t negotiate with the U.S. on any level, anywhere, the Islamic Republic’s supreme leader said.

“The key thing to think about is do we have an oil shock or a short-term disruption?” said Virginie Maisonneuve, chief investment officer at Eastspring Investments, in a Bloomberg TV interview. “You’re seeing this wait-and-see attitude, and that’s why the markets are quite nervous.”

Meanwhile, president Trump authorized the release of emergency crude stockpiles if needed, which could ease some upward pressure on crude futures. Trump said on Monday it looked like Iran was behind the attacks but stressed that he did not want to go to war, striking a slightly less bellicose tone than his initial reaction.

“Although Saudi Arabia’s spare capacity and U.S. Strategic Petroleum Reserves could plug some of the lost output, where oil trades in the near term will be influenced by how long it takes for Saudi production to fully recover,” said Lukman Otunuga, research analyst at FXTM. “It is this concern over negative supply shocks amid geopolitical tensions which should keep oil prices buoyed in the short term.”

Middle-eastern events overshadowed investor concerns about the simmering trade war. American and Chinese working-level trade negotiators are set to resume talks in the next week, before a meeting of top officials in October. Meanwhile, President Donald Trump said the U.S. and Japan have reached an initial trade accord over tariffs.

In other news, late on Monday Trump said that the United States has reached initial trade agreements with Japan, but traders are also focused on the U.S.-Sino trade war. “In the next week, positive developments on Brexit and/or Iran have the potential to move markets higher from here. It shows why staying strategically invested in equities is important,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “But with scope for central banks to disappoint and global growth continuing to slow, we see little reason to change our tactically more cautious stance.”

Deputy-level talks between the United States and China are scheduled to start in Washington on Thursday, paving the way for high-level talks next month aimed at resolving a bitter trade row that has dragged on for more than a year.

In rates, the recent blowout in interest rates continued to fade, as the yield on benchmark 10-year Treasury notes fell slightly to 1.8292%, while the surge in overnight repo rates eased. Euro zone government debt yields edged lower as geopolitical uncertainty stemming from the attack on Saudi underpinned a cautious tone in bond markets.

In currencies, the dollar gained versus all of G-10 peers as the Fed kicks-off its two-day monetary policy meeting and tensions in the Middle East fail to dictate market sentiment. Investors are focusing on reasons to fade any greenback weakness – ECB easing, a no-deal Brexit, dovish RBA minutes – and the Bloomberg Dollar Spot Index is up 0.1% and approaching a two week high, after forming a bullish outside day on Monday. Elsewhere, the pound slipped 0.2% to 1.2403, down a second day as PM Boris Johnson’s lawyers were set to defend his Brexit strategy in the U.K.’s highest court. The Euro was down 0.1% below 1.10, to 1.0992 as option-related bids above 1.1000 failed to absorb leveraged pressure. On the other side of the world, the Australian dollar led losses in G-10 with AUD/USD down 0.5% to 0.6831, lowest since Sept. 6. The Reserve Bank of Australia said wages growth appears to have stalled and the job market is set to moderate in its September minutes. AUD/USD was also sold by macro and leveraged funds due to the decline in Chinese stocks, according to Asia-based FX traders.

Elsewhere, Gold moves sideways, holding on to recent gains that saw the precious metal jump back above USD 1500/oz; though it has struggled to stay above this mark. Separately, the Indian Government may be considering a full exit from Hindustan Copper as according to reports.

Economic data include industrial production for August. FedEx is due to publish earnings

Market Snapshot

- S&P 500 futures down 0.1% to 2,997.25

- STOXX Europe 600 down 0.1% to 389.01

- MXAP down 0.4% to 159.03

- MXAPJ down 0.7% to 510.32

- Nikkei up 0.06% to 22,001.32

- Topix up 0.3% to 1,614.58

- Hang Seng Index down 1.2% to 26,790.24

- Shanghai Composite down 1.7% to 2,978.12

- Sensex down 1.4% to 36,604.95

- Australia S&P/ASX 200 up 0.3% to 6,695.25

- Kospi up 0.01% to 2,062.33

- German 10Y yield fell 0.6 bps to -0.486%

- Euro up 0.2% to $1.1021

- Brent Futures up 0.3% to $69.21/bbl

- Italian 10Y yield fell 3.7 bps to 0.504%

- Spanish 10Y yield fell 0.3 bps to 0.254%

- Brent Futures down 0.5% to $68.65/bbl

- Gold spot up 0.1% to $1,497.72

- U.S. Dollar Index down 0.03% to 98.58

Top Overnight News from Bloomberg

- One of the key U.S. borrowing markets saw a massive surge Monday, a sign the Federal Reserve is having trouble controlling short-term interest rates.

- American and Chinese senior trade negotiators are expected to resume negotiations in the next week and a half, with much work remaining to reach a comprehensive deal, U.S. Chamber of Commerce Chief Executive Officer Thomas Donohue said.

- Swiss National Bank chief Thomas Jordan is out of the hot seat for now — perhaps until Brexit hits.

- Gulf dollar bonds went into the weekend as investor darlings and came out as risky assets. Money managers poured into the Gulf region in the weeks running up to Saturday’s unprecedented attack on Saudi Arabia’s key oil facilities.

- Saudi Aramco is growing less optimistic there will be a rapid recovery in oil production from the weekend’s attack and now faces weeks or months before the bulk of output is restored at its Abqaiq processing plant

- Oil’s record-breaking advance paused as the market awaits clarity on how long it’ll take Saudi Arabia to restore output

- President Donald Trump said his administration has reached an initial trade accord with Japan and he intends to enter into the agreement in coming weeks

- Chinese working-level trade officials are scheduled to travel to the U.S. this week to prepare for a meeting of top negotiators in October, the Ministry of Commerce said

- Boris Johnson will see his decision to suspend Parliament under scrutiny in the first of three days of hearings at the U.K.’s Supreme Court

- In minutes of its Sept. 3 meeting, Reserve Bank of Australia said “the upward trend in wages growth appeared to have stalled” and forward-looking indicators suggested employment growth would moderate

- Argentina’s central bank modified capital control rule to allow sovereign bond payments to be made abroad

- Trump said he “probably” won’t travel to Pyongyang for the next round of nuclear talks with Kim Jong Un, but would be willing to visit the North Korean capital in the future

Asian equity markets were mixed/lower following a subdued lead from Wall St where the S&P 500 slipped back below the 3k milestone and the DJIA snapped an 8-day win streak after attacks on Saudi’s oil facilities, while participants continue to await the looming billow of central bank policy updates. ASX 200 (+0.3%) and Nikkei 225 (+0.1%) were lacklustre in which weakness in Australia’s mining and materials sectors overshadowed the continued rise in energy stocks as oil prices took a breather from the prior day’s record surge, while the Japanese benchmark lacked conviction amid a choppy currency and with SoftBank among the worst performers due to a delay of the WeWork IPO which the Co. and its affiliates hold about a 29% stake in. Hang Seng (-1.2%) and Shanghai Comp. (-1.7%) were the laggards after the PBoC refrained from open market operations and although it announced to lend CNY 200bln through its Medium-term Lending Facility, this was below the CNY 265bln maturing today and the rate was maintained at 3.3% to the disappointment of the increased speculations for a cut. Finally, 10yr JGBs initially gained to reclaim the 154.00 level amid safe-haven flows and with the BoJ also present in the market for JPY 760bln of JGBs in the belly to the shorter-end of the curve, although prices later reversed gains in conformity with the indecision seen across Japanese asset classes.

Top Asian News

- Singapore Woos Banks in Battle of Asia’s Biggest Forex Hubs

- South Korea Latest Asian Nation Hit by African Swine Fever

- Jokowi Orders Crackdown on Arsonists: SE Asia Haze Update

- China Stocks Fall, Yuan Weakens as Central Bank Holds Loan Rate

Major European indices are tentative following a mixed lead from the Asia Pacific Session, as the market awaits an update on the damages from the Saudis at 18.00 BST re. the weekend’s attacks, and ahead of tomorrow’s FOMC meeting, with major bourses little changed overall this morning. Energy sector (+1.1%) continues to outperform, as crude prices cling on to the recent outsized gains, which continues to weigh on airline names including EasyJet (-1.3%) and RyanAir (-2.5%). Meanwhile, some strength in the more defensive utilities (+0.6%), health care (+0.9%) and consumer staples (+0.8%) sectors is suggestive of a fragile risk tone, although the risk sensitive tech sector (+0.3%) is also in the green. Leading the laggards are Financials (-1.2%), with this week’s fall in yields and pronounced curve flattening failing to provide any support. In terms of stock specifics; Zalando (-9.1%) is the notable underperformer, after the Co. announced the placement of over 13mln new shares. Total (+1.7%) is deriving support not only from higher crude prices but also the news of a 30% output increase in one of its South Korean ethylene plants. AB InBev (+0.7%) is supported by news that the co. is looking to raise USD 4.8bln (according to a company statement) in the IPO of its AsiaPac unit in Hong Kong; although this is below the pre-market reports that they were seeking around USD 7bln. Finally, ThyssenKrupp (-0.8%) failed to garner support from reports that Advent International and Cinven & Abu Dhabi Investment Authority had teamed up to place a bid on the co.’s elevator unit, which could put them in competition with the likes of Kone (-0.3%).

Top European News

- Boris Johnson’s Brexit Plan Goes to Court With EU Talks in Chaos

- Balkan Leader Boosts Re-Election Bid With 500 Euro Wage Pledge

- Sweden Unemployment Reaches 4-Year High in New Blow to Riksbank

- EON Wins Conditional EU Approval to Take Over Innogy

In FX, SEK/AUD marked G10 underperformers and both undermined by Central Bank releases to varying degrees, while worrying data from Sweden has also undermined the Crown as unemployment jumped in August and total employment declined. Eur/Sek has rallied from around 10.6240 to 10.7150+ in wake of minutes from the Riksbank revealing deeper divisions on the repo rate path with Janssen unsure whether it is appropriate to maintain guidance for a hike around the turn of the year. Meanwhile, Aud/Usd has retreated further from recent peaks towards 0.6830 as the RBA remains ready to ease again to support growth and keep inflation on course to reach target, adding that it is reasonable to expect the OCR to be low for a lengthy period of time.

- NZD/GBP/CHF – The Kiwi is also on the back foot and hovering around 0.6325 vs its US counterpart after a dip in Westpac’s Q3 consumer survey overnight, but holding up a bit better in Aud/Nzd cross terms within a 1.0827-1.0790 range ahead of NZ Q2 current account data and the latest GDT auction. Meanwhile, Sterling is struggling to survive a stringent test of 1.2400 and support just below at 1.2385 following a fruitless journey to Luxembourg by UK PM Johnson and pending the Supreme Court judgement on his suspension of parliament, and the Franc is trying to contain losses circa 0.9950/1.0950 against the Buck and Euro respectively in the run up to the Fed and SNB tomorrow and Thursday.

- JPY/CAD – The Yen has lost a degree of its Saudi safe-haven premium, with Usd/Jpy firmer above the 108.00 level amidst reports that the US and Japan have agreed tentative trade deal terms, while the Loonie is unwinding some oil-inspired gains ahead of Canadian manufacturing sales, as Usd/Cad pivots 1.3250 compared to lows of just a few pips off 1.3200 at one stage yesterday.

- EUR – The single currency has made a better fist of overcoming downside pressure at a big figure/psychological marker than the Pound, albeit with some assistance from a much more pronounced improvement in German ZEW economic sentiment than anticipated. Indeed, Eur/Usd has reclaimed 1.1000+ status after another probe below to 1.0990 (close to the 1.0985 pre-ECB base) even though the Dollar is firmer in general with the DXY comfortably back above 98.500 within a 98.573-749 band ahead of US ip data and the aforementioned Fed on Wednesday. However, decent option expiries layered between 1.1025-30 and 1.1040-50 (1 bn each time) may cap further Euro recovery gains vs the Greenback.

- RBA Minutes (Sept 3rd) reiterated the board would consider further policy easing if needed to support growth and inflation targets, while it is reasonable to expect extended period of low rates to achieve employment and inflation targets. Furthermore, minutes noted the Australian economy could sustain lower rates of unemployment and that there are further signs of a turnaround in the housing sector, although the turnover is still low and outlook for consumption growth is a key uncertainty.

In commodities, the crude complex consolidated on Tuesday morning, and holds on to the lion’s share of yesterday’s outsized gains which came on the combination of an uptick in geopolitical risk premia and supply shock after an attack left a significant portion of Saudi oil production offline. Brent Nov’ 19 futures, although well off yesterday’s extreme near USD 72/bbl highs, has lost the USD 68.0/bbl handle, while WTI Oct’ 19 futures range places it around the USD 62.0/bbl mark. The market now awaits an official update from the Saudis at 18.00/18:15 BST regarding the extent of the damage to the country’s oil producing infrastructure; mixed reports thus far, some suggested about 40% of the disrupted output has been restored and the remaining production could be back online as soon as month-end, but others were less optimistic and anticipate a return to full output could take months. In terms of commentary, US Energy Secretary Perry, when asked about tapping the US SPR, said that he is confident the markets are well supplied, and that the US will take a wait and see approach when it comes to its potential use. Russian Energy Minister Novak said there is still no information regarding the weekend’s Saudi Oil attacks and that the price spike following the attacks reflects uncertainty and risk. Meanwhile, as the dust settles in wake of the attack, evidence of supply disruptions continue to emerge; Saudi Aramco have reportedly delayed some oil loading grades by a number of days following and have asked some customers to accept different oil grades. Moreover, Indian State refiners are reportedly mulling switching crude oil grades to avoid supply disruptions from Saudi Aramco. Elsewhere, Gold moves sideways, holding on to recent gains that saw the precious metal jump back above USD 1500/oz; though it has struggled to stay above this mark. Separately, the Indian Government may be considering a full exit from Hindustan Copper as according to reports.

US Event Calendar

- 9:15am: Industrial Production MoM, est. 0.2%, prior -0.2%; Manufacturing (SIC) Production, est. 0.2%, prior -0.4%

- 10am: NAHB Housing Market Index, est. 66, prior 66

- 4pm: Net Long-term TIC Flows, prior $99.1b

- 4pm: Total Net TIC Flows, prior $1.7b

DB’s Jim Reid concludes the overnight wrap

Yesterday was one of the most unexciting, exciting days for markets for a long time. After the huge initial moves in the Asian session for oil, things settled down into a relatively tight range in most markets through most of the Asian, European and US sessions. WTI closed up +12.82% at $61.88, which was the biggest one day move higher since February 2009, with the move taking WTI back up to its highest level since May. Similarly, Brent closed up +14.61% at $69.02, breaking higher towards the session close. The moves weren’t just confined to crude though with Gasoline also rallying +11.45%, while natural gas rose +2.79%. Overnight WTI (-1.41%) and Brent (-1.10%) are both erasing a small amount of yesterday’s gains.

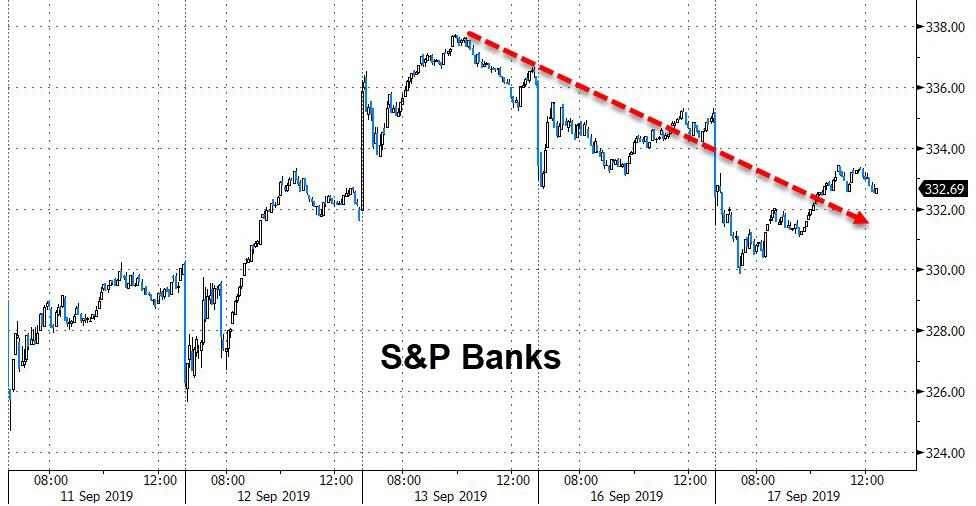

It was no great surprise then that markets elsewhere were dictated by the oil moves with the broad-based move being a moderate risk-off (with the weak China data also a factor). In equity markets the magnitude of the moves were actually fairly minor outside of energy. The S&P 500 closed down -0.31% with a +3.29% rally for the energy sector helping to buffer the slide. The likes of Apache (+16.89%), Hess (+11.18%) and Marathon (+11.57%) were the big winners at a stock level with the move for Apache the biggest since 2008. The DOW (-0.52%) and NASDAQ (-0.28%) also closed lower along with the STOXX 600 (-0.58%), although again the STOXX Oil and Gas index was up +2.13%. Arguably one of the areas of markets most sensitive to oil is US HY credit where spreads at a broad index level finished +0.5bps wider, with energy spreads rallying -24bps to help offset the risk off. It was a similar trend in CDS where there were big moves tighter for the likes of higher beta Chesapeake and Whiting in particular. One credit which did struggle though was A-rated Saudi Aramco where the spread on the 2049s traded about +7.5bps wider.

The risk-off tone also helped fuel a bid for Gold (+0.67%) and Silver (+2.33%) while in FX the oil-sensitive Norwegian Krone (+0.27%) and Canadian Dollar (+0.33%) also benefited. As for rates, most DM markets did their best to reverse a small amount of last week’s selloff but were fairly stable after the initial move. In the end 10y Treasuries ended -4.9bps (down a further -2.1bps this morning) lower at 1.847% having touched as low as 1.810% intraday, while the 2s10s curve fell -0.9bps to 8.3bps (7.9bps this morning). In Europe Bunds rallied -3.3bps and BTPs -3.8bps.

Overnight we have some fresh trade headlines to throw into the mix with China’s Ministry of Commerce saying in a statement that Chinese working-level trade officials are scheduled to travel to the US this week to prepare for a meeting of top negotiators in October. The statement added that Liao Min, deputy director of the Office of the Central Commission for Financial and Economic Affairs and vice finance minister, will lead a delegation to visit the US tomorrow for trade consultations. Separately, USTR Rober Lighthizer spoke with the US Chamber of Commerceyesterday post which the group’s CEO Thomas Donohue said that “there’s much more work” to be done on a trade deal with China while adding that Lighthizer indicated that there’s some movement on China buying US farm products and other issues but it’s “an extraordinary challenge” to get a complete deal. Donohue also said that Lighthizer said there are staff-level meetings between Chinese and U.S. negotiators on Friday, with senior negotiators to meet in the ensuing week or week and a half.

Continuing with trade, President Trump said late yesterday that his administration has reached an initial trade accord with Japan over tariffs and that he intends to enter into the agreement in the coming weeks. USTR Robert Lighthizer has said earlier that the limited trade deal will cover agriculture, industrial tariffs and digital trade. Trump didn’t provide details about what was in the initial deal and didn’t mention whether the limited deal will end his threat to slap tariffs on Japanese auto imports as part of the trade deal.

Asian markets are trading mixed this morning on all the above headlines with the Nikkei (-0.02%) trading largely flat while the Topix (+0.25%) is up as Japanese markets re-opened post a holiday. The Hang Seng (-1.01%), Shanghai Comp (-1.02%), CSI (-0.94%) and Shenzhen Comp (-1.38%) are all down while the kospi (+0.11%) is up. The onshore Chinese yuan is trading weak, down -0.30% to 7.0886, alongside most Asian EM Fx. The Hang Seng seems to be dragged down by the prospect of US sanctions as the city’s prominent local activist Joshua Wong is set to address US lawmakers today who are considering changes to special trade privileges for the financial hub. Ahead of the address, Hong Kong leader Carrie Lam said that “I uphold this principle of accountability, but at the moment it is all for us to see that Hong Kong is undergoing a very difficult situation, and sanctions or punishment are not going to help lift Hong Kong out of this very difficult situation.” Elsewhere, futures on the S&P 500 are trading flattish (-0.06%).

In other overnight news, Bloomberg reported that Former Italian Prime Minister Matteo Renzi is leaving the Democratic Party to found his own movement but pledged continued support for Prime Minister Giuseppe Conte. The report also added that Renzi could announce his move as early as today while Italian news agency ANSA reported that in a telephone call to Conte last night, Renzi assured the premier that his move won’t threaten the newly formed administration.