GOLD:$1507.90 UP 2.40 (COMEX TO COMEX CLOSING)

Silver:$17.84 DOWN 24 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1501.00

silver: $18.01

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 1/3

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,505.100000000 USD

INTENT DATE: 09/17/2019 DELIVERY DATE: 09/19/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 1

737 C ADVANTAGE 3 2

____________________________________________________________________________________________

TOTAL: 3 3

MONTH TO DATE: 1,733

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 3 NOTICE(S) FOR 300 OZ (0.00933 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1733 NOTICES FOR 173300 OZ (5.3903 TONNES)

SILVER

FOR SEPT

94 NOTICE(S) FILED TODAY FOR 470,000 OZ/

total number of notices filed so far this month: 8438 for 42,190,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10170 DOWN 17

Bitcoin: FINAL EVENING TRADE: $ 10640 UP 823

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A HUGE SIZED 2127 CONTRACTS FROM 214,641 DOWN TO 212,514 DESPITE THE STRONG 14 CENT GAIN IN SILVER PRICING AT THE COMEX. WE AGAIN HAD CONSIDERABLE BANKER SHORT COVERING TODAY

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

SEPT, 0 FOR DEC: 1477, AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1477 CONTRACTS. WITH THE TRANSFER OF 1477 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1477 EFP CONTRACTS TRANSLATES INTO 7.385 MILLION OZ ACCOMPANYING:

1.THE 14 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE AGAIN HAD HUGE COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY AS NO DOUBT OUR FRIENDS WERE SCARED OF THE GEOPOLITICAL LANDSCAPE THEY WERE FACING.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

24,497 CONTRACTS (FOR 12 TRADING DAYS TOTAL 24,497 CONTRACTS) OR 122.48 MILLION OZ: (AVERAGE PER DAY: 2041 CONTRACTS OR 10.20 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 122.48 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.49% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1672.10 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2127, DESPITE THE STRONG 14 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1477 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 650 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1477 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 2127 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 14 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $18.08 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.063 BILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 94 NOTICE(S) FOR 470,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 5983 CONTRACTS, TO 630,990ACCOMPANYING THE $1.50 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5907 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 5907 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 630,990,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,890 CONTRACTS: 5983 CONTRACTS INCREASED AT THE COMEX AND 5907 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 11,890 CONTRACTS OR 1,189,000 OZ OR 36.98 TONNES. YESTERDAY WE HAD A SMALL GAIN OF $1.50 IN GOLD TRADING….

AND WITH THAT TINY GAIN IN PRICE, WE HAD A HUGE GAIN IN GOLD TONNAGE OF 36.98 TONNES!!!!!! THE BANKERS WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER TRYING TO CONTAIN THE PRICE RISE WITH SOME SUCCESS. AND WITH THAT SMALL GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 36.98 TONNES!!!!!!. OUR BANKER FRIENDS TODAY DID NOT EVEN TRY TO COVER THEIR SHORTFALL AS THEY PILED ON THE COPIOUS PAPER. THIS IS IN TOTAL CONTRAST TO SILVER WHERE THEY ARE FRIGHTENED BY THE LANDSCAPE AND THUS NIBBLING AWAY AT THEIR SHORTFALL.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 82,314 CONTRACTS OR 8,231,400 oz OR 256.03 TONNES (12 TRADING DAYS AND THUS AVERAGING: 6859 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 256.03 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 256.03/3550 x 100% TONNES =7.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4407.63 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED INCREASE IN OI AT THE COMEX OF 5983 DESPITE THE SMALL PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($1.50)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5907 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5907 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 11,890 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

5097 CONTRACTS MOVE TO LONDON AND 5983 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 36.98 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE TINY GAIN IN PRICE OF $1.50 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD..

WITH GOLD UP $2.40 TODAY//(COMEX-TO COMEX)

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES

(SOMETHING SCARED THESE GUYS)

INVENTORY RESTS AT 880.37 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 24 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV//

/INVENTORY RESTS AT 376.502 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A STRONG SIZED 2127 CONTRACTS from 214,641 DOWN TO 212,514 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1477: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1477 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2127 CONTRACTS TO THE 1477 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 650 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 2.735 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: SEPT 2019: 43.030 MILLION OZ//

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 14 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1477 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 7.54 POINTS OR 0.25% //Hang Sang CLOSED DOWN 36.12 POINTS OR 0.13% /The Nikkei closed DOWN 40.61 POINTS OR 0.18%//Australia’s all ordinaires CLOSED DOWN .15%

/Chinese yuan (ONSHORE) closed DOWN at 7.0885 /Oil UP TO 58.86 dollars per barrel for WTI and 64.34 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0885 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0831 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

4/EUROPEAN AFFAIRS

UK

Zero hedge outlines what comes next in this time line

(zerohedge)

7. OIL ISSUES

Oil continues to rise despite bigger than expected crude build. The geopolitical landscape is calling for increased oil prices

(zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)Bill Murphy interviewed by Phil Kennedy and the topic is how far will the rigging probe go?

(Bill Murphy/GATA/Kennedy)

ii)Thom Callandra on the metal price suppression

(Thom Callandra)

iii)Bill Murphy interviewed by Silver Doctors and Murphy suggests there are two factions in the USA government:

1 the lower level guys who are out to get the blood of JPMorgan

2 the upper echelon who knows of the official sector rigging and these guys are backing off

(courtesy Bill Murphy/Silver Doctors)

iv)Pam and Russ Martens now wonder if Jamie Dimon will finally lose his job over these racketeering charges? Will JPMorgan finally be punished for continual racketeering

an excellent commentary..

Russ and Pam Marten

(Wall Street on Parade)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/THIS MORNING/USA

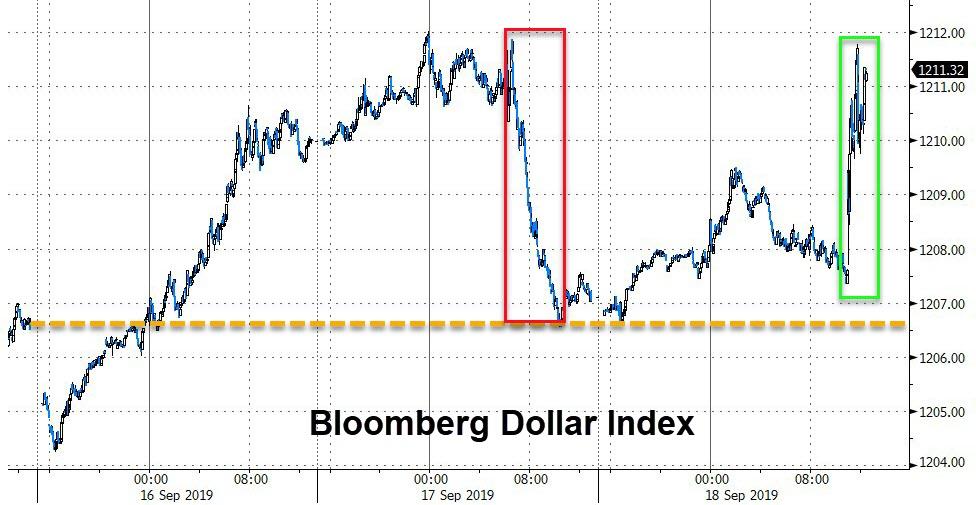

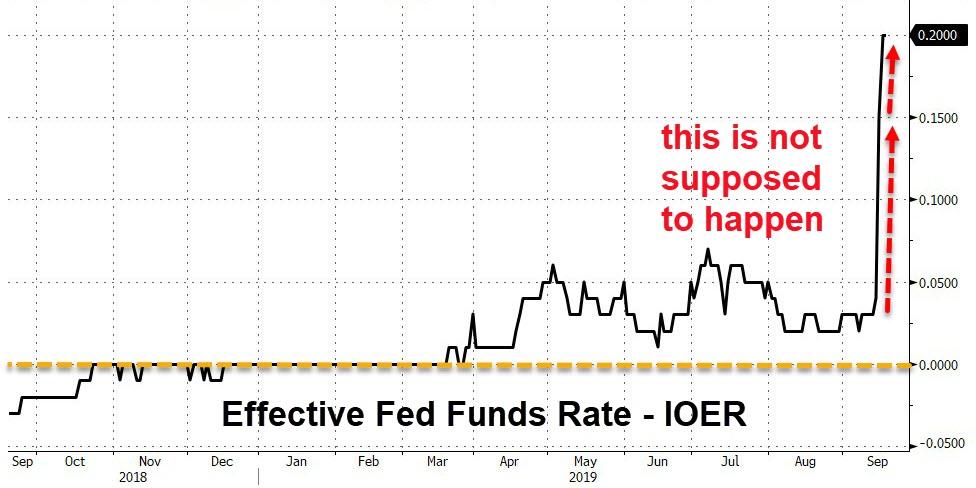

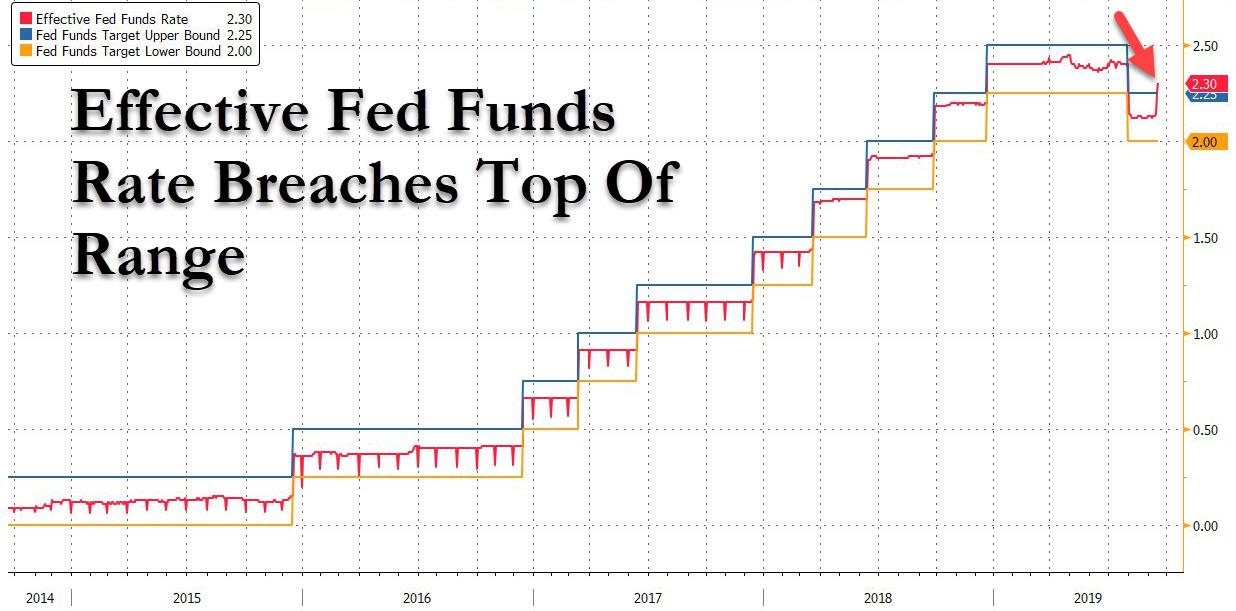

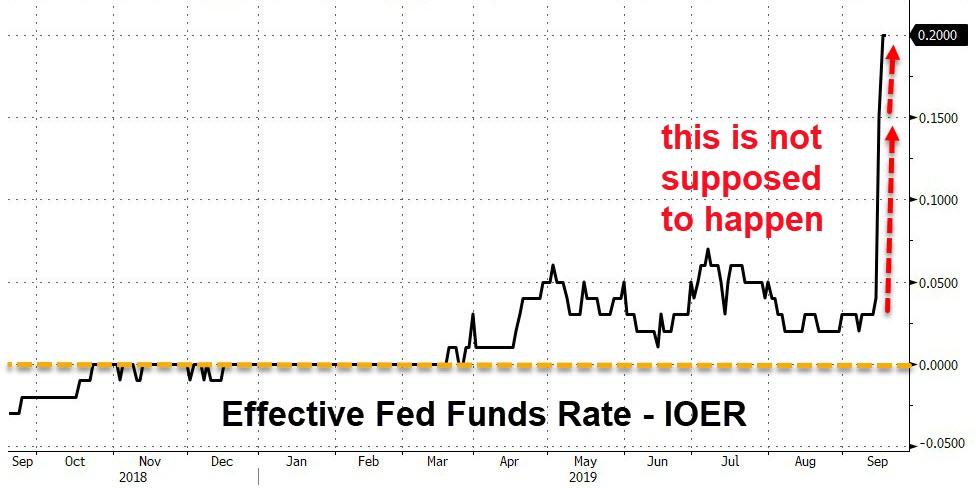

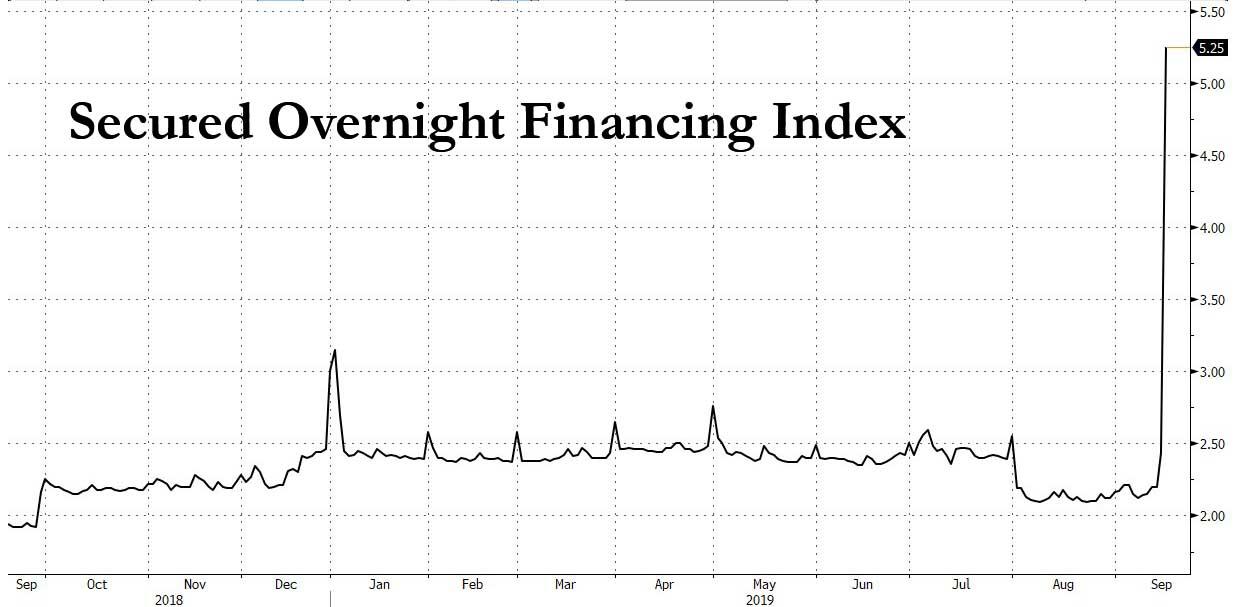

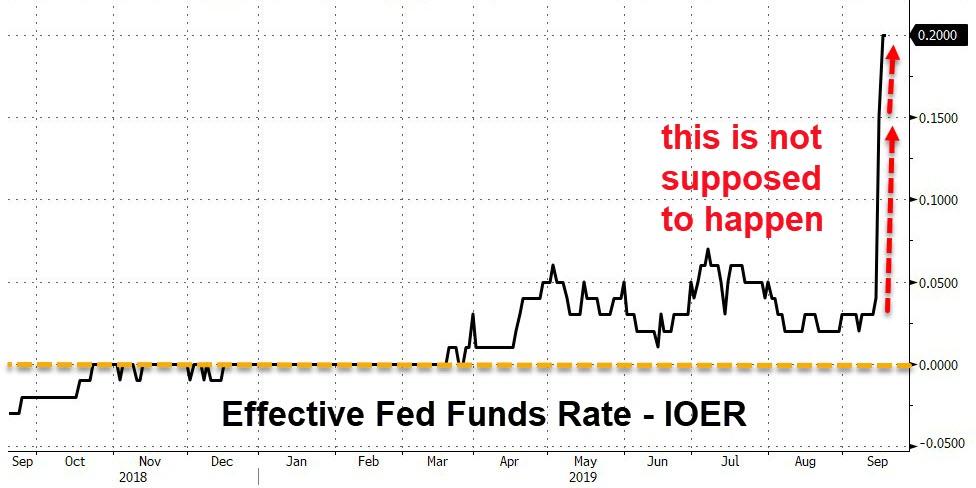

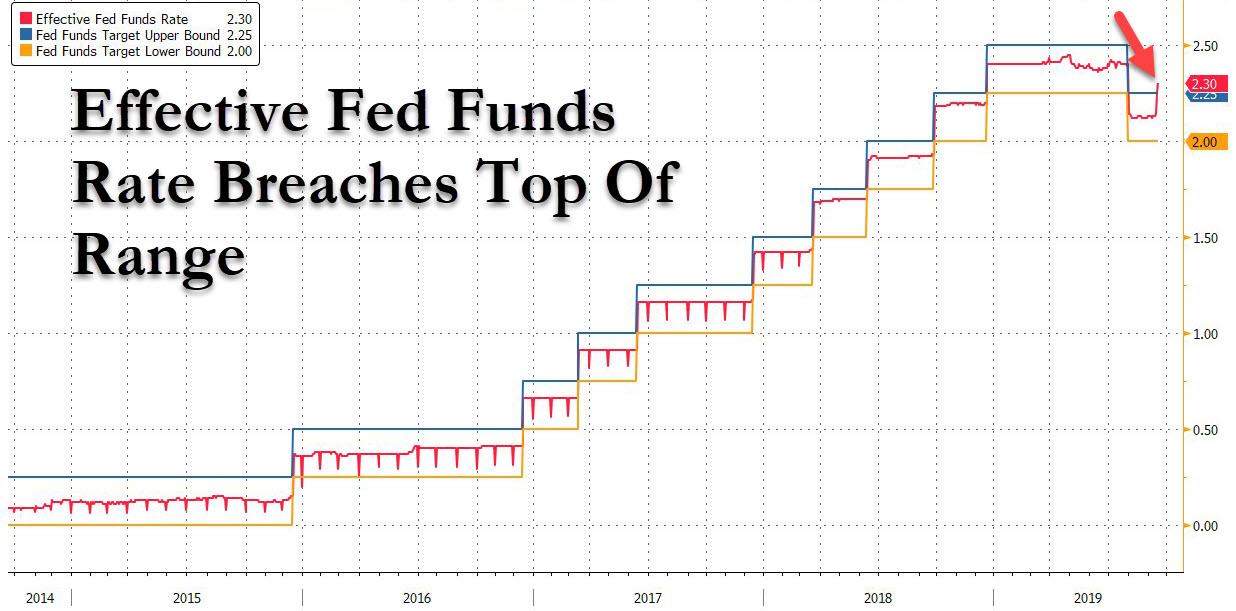

One of the big stories of the day: The Fed funds prints at 2.30% ,much higher than 2/25% ceiling due to the lack of liquidity in the market. And now the new replacement for Libor (Security Overnight Financing Index or SOFI) just skyrocketed a huge 2.87% to 5.25%

(zerohedge)

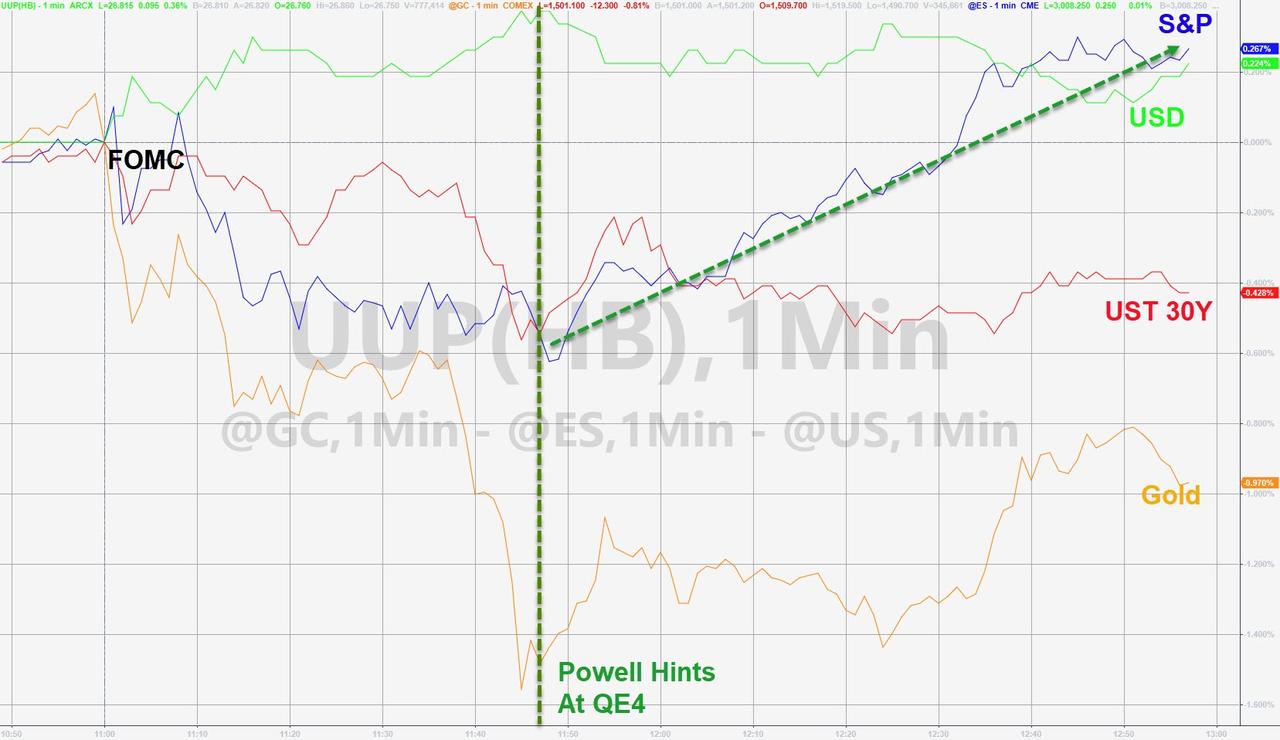

b)MARKET TRADING/USA/AFTERNOON/FOMC

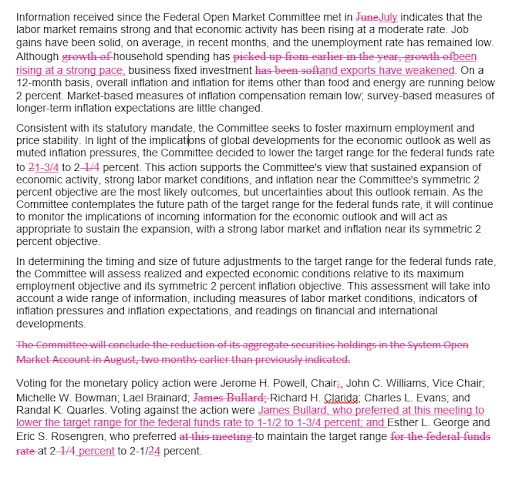

i)FOMC cuts rates, as well as failing to address the liquidity crisis. They did cut the IOER which is what they pay the banks on excess reserves by 30 basis points, hoping that will help the liquidity.

(zerohedge)

ii)Trump furious as he slams the clown Powell as a terrible communicator. He says that he failed again

(zerohedge)

iii)Market reaction this afternoon.

the clown, Powell should take a bow;

ii)Market data/USA

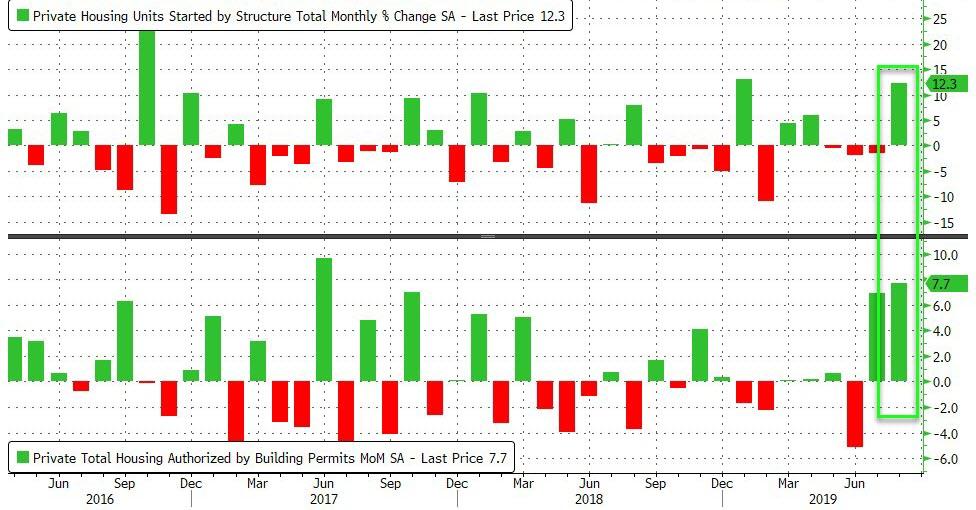

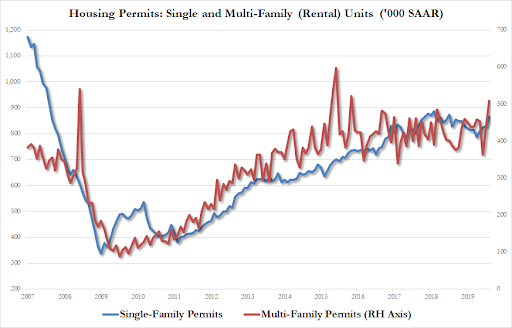

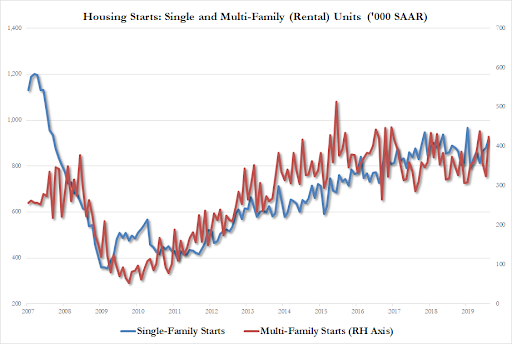

Low mortgage rates has finally spurred housing starts as well as permits

(zerohedge)

iii) Important USA Economic Stories

a)Last night, the liquidity shortage is getting worse!! The Fed is in a pickle. As we shall find out, they just did not know how to address this in their FOBC report

(zerohedge)

b) Trump brings on new advisor

(zerohedge)

iv) Swamp commentaries)

Mish blast the New York times for their obvious Kavanaugh smear piece.

(Mish Shedlock)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 73,390 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 92,020 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 92,020 CONTRACTS EQUATES to 460 million OZ 65.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.79% ((SEPT 18/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.03% to NAV (SEPT 18/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.79%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.03 TRADING 14.53/DISCOUNT 3.32

END

And now the Gold inventory at the GLD/

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 18/2019/ Inventory rests tonight at 880.37 tonnes

*IN LAST 666 TRADING DAYS: 55.01 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 566- TRADING DAYS: A NET 111.64 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 18/2019:

Inventory 376.502 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.13/ and libor 6 month duration 2.08

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .05

XXXXXXXX

12 Month MM GOFO

+ 2.07%

LIBOR FOR 12 MONTH DURATION: 2.08

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.01

gold lending rates negative out to the entire year.

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

JPMorgan’s Gold and Silver Desk Was a Criminal Enterprise – U.S. Justice Department

◆ JPMorgan’s head of precious metals trading and senior traders have been charged by the U.S. Department of Justice with rigging precious metal prices in a “massive, multiyear scheme”

◆ The DOJ’s indictment said the scheme generated millions of dollars in profits for JPMorgan Chase and caused millions in losses for counter-parties, prosecutors said

◆ JPM precious metals desk chief, Michael Nowak, who was indicted is a JPM managing director and London Bullion Market Association (LBMA) board member

◆ The U.S. DoJ has invoked RICO or Racketeer Influenced and Corrupt Organizations Act racketeering law in charging JP Morgan and racketeering is very rarely used in cases involving large banks

◆ JPM is accused of illegally monopolizing the silver futures market, engaging in “widespread spoofing, market manipulation and fraud” in the gold and silver market and defrauding investors

◆ JP Morgan may have accumulated the biggest stockpile of physical silver in history – See JP Morgan Cornering Silver Market?

NEWS and COMMENTARY

JPMorgan’s Metals Desk Was a Criminal Enterprise, U.S. Says

3 From JPMorgan Accused in Scheme to Game Precious Metals Market

Will Jamie Dimon finally lose his job over racketeering charges?

JP Morgan Racketeering Case Way More Than Gold & Silver Spoofing

How far will rigging probe go?Kennedy interviews GATA Chairman

Repo Market Chaos Signals Fed May Be Losing Control of Rates

Gold steady amid cautious mood, focus shifts to ‘losing control’ Fed

Gold notches second straight gain, adds to climb toward 1-week high

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

17-Sep-19 1499.30 1502.10, 1208.89 1207.24 & 1361.51 1360.45

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

10-Sep-19 1494.60 1498.25, 1211.52 1211.34 & 1353.51 1357.11

09-Sep-19 1509.95 1509.20, 1223.81 1220.34 & 1368.62 1364.92

06-Sep-19 1504.95 1523.70, 1223.52 1237.09 & 1363.94 1378.49

05-Sep-19 1542.60 1529.10, 1257.06 1238.72 & 1397.44 1380.78

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Bill Murphy interviewed by Phil Kennedy and the topic is how far will the rigging probe go?

(Bill Murphy/GATA/Kennedy)

In interview with Phil Kennedy, GATA chairman asks: How far will rigging probe go?

Submitted by cpowell on Tue, 2019-09-17 13:28. Section: Daily Dispatches

9:25a ET Tuesday, September 17, 2019

Dear Friend of GATA and Gold:

Interviewed last night by Phil Kennedy of Kennedy Financial, GATA Chairman Bill Murphy marveled at the publicity suddenly being given to gold and silver market rigging, on account of the latest indictments of traders for JPMorganChase. But Murphy added that the “spoofing” attributed to the JPM traders is the smaller part of the manipulation of the markets, the bigger part being surreptitious intervention by governments and central banks.

…

Kennedy and Murphy discussed how far the Justice Department’s investigation will go — to JPM’s former commodity desk chief, Blythe Masters? To the bank’s chief executive, Jamie Dimon? To the Federal Reserve, Treasury Department, and Bank for International Settlements? There is plenty of evidence that all of them were involved with metals market manipulation.

Kennedy and Murphy also discussed the possibility of more fraud lawsuits against JPMorganChase.

The interview is 26 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=a4fxLsSEEXU&feature=youtu.be

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Friday-Monday, November 1-4, 2019

https://neworleansconference.com/noic-promo/powellgata/

* * *

end

Thom Callandra on the metal price suppression

(Thom Callandra)

As monetary metals price suppression fails, you may want The Calandra Report

Submitted by cpowell on Tue, 2019-09-17 13:40. Section: Daily Dispatches

9:40a ET Tuesday, September 17, 2019

Dear Friend of GATA and Gold:

With infinite money and currency devaluation now being the policy of many central banks, the prospects for the monetary metals mining industry will be spectacular as central bank commodity price suppression policy fails from exposure by GATA and others.

So GATA supporters should consider a generous offer made by our old friend Thom Calandra, publisher of The Calandra Report, a financial letter with an emphasis on resource companies.

…

Thom will split with GATA the one-year subscription fee of $169 paid by GATA supporters who subscribe to The Calandra Report by September 21. That is, for each GATA supporter who subscribes, Thom will contribute $85 to GATA.

GATA supporters who subscribe by then will receive two bonuses as well.

— Thom’s frequent TCR Collateral missives, which include material from his notebook about financial people, companies, and commodities.

— A special recent issue of The Calandra Report that identifies what Thom believes are substantially undervalued gold, silver, and copper mining companies and a rising biomedical company with a promising new drug.

A note from Thom explains below.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

Hello Alpha-GATAs. I have supported GATA since the early 2000s. Over the years GATA Chairman Bill Murphy, GATA Secretary/Treasurer Chris Powell, and I have shared ideas, panel appearances, and even a drink or three.

I’d like you to join The Calandra Report community. It’s been going since 2011, and since 1998 for MarketWatch.com, which I co-founded.

Here’s a small biography:

https://thomcalandra.com/about-thom-calandra/

Here’s a subscription offer exclusively for GATA supporters, like the offer we made last year.

You get the twice-weekly private reports for one year for $169 — along with our TCR Collateral letters — and GATA will receive fully half of that amount: $85.

For your review Chris has posted here —

http://gata.org/files/CalandraReport-08-04-2019.pdf

— a recent edition of TCR, which covers the weeklong resources symposium just concluded in Vancouver.

To accept this offer and help GATA, please go here:

https://www.paypal.com/cgi-bin/webscr?cmd=_s-xclick&hosted_button_id=588…

And please feel free to e-mail me with testimonials, ideas, and names: thom@thomcalandra.com

Thank you from northern California!

— Thom Calandra

end

Bill Murphy interviewed by Silver Doctors and Murphy suggests there are two factions in the USA government:

1 the lower level guys who are out to get the blood of JPMorgan

2 the upper echelon who knows of the official sector rigging and these guys are backing off

(courtesy Bill Murphy/Silver Doctors)

Indictments for rigging suggest two factions in U.S. govt., GATA chairman says

Submitted by cpowell on Wed, 2019-09-18 00:04. Section: Daily Dispatches

8:04p ET Tuesday, September 17, 2019

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy, interviewed today by Paul Eberhart of Silver Doctors, speculated that the increasing indictments of JPMorganChase personnel for gold market rigging suggest that there are two factions in the U.S. government, one superintending the rigging and one fighting it.

…

Murphy added that JPMorganChase CEO Jamie Dimon must have known about the market manipulation undertaken by the bank’s traders.

Murphy also said he believes that silver has become more sensitive than gold for those trying to suppress the monetary metals.

And why, Murphy wondered, is the Justice Department doing work that the Commodity Futures Trading Commission should be doing?

The interview is 25 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=hnT8h_67asM

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Pam and Russ Martens now wonder if Jamie Dimon will finally lose his job over these racketeering charges? Will JPMorgan finally be punished for continual racketeering

an excellent commentary..

Russ and Pam Marten

(Wall Street on Parade)

Pam and Russ Martens: Will Jamie Dimon finally lose his job over racketeering charges?

Submitted by cpowell on Wed, 2019-09-18 01:54. Section: Daily Dispatches

9:54p ET Tuesday, September 17, 2019

Dear Friend of GATA and Gold:

Pam and Russ Martens of Wall Street on Parade today take note of the latest indictments at JPMorganChase & Co. and itemize the corruption and criminality of the investment bank under the chairmanship and chief executiveship of Jamie Dimon.

…

The Martenses conclude: “If you’re a regular citizen on probation and you seriously break the law, you are highly likely to go back to jail. In the case of JPMorganChase, it has been a serial recidivist and yet its deferred prosecution agreements have not been rescinded by the U.S. Department of Justice. According to the latest indictments, the activity occurred up to August 2016, when the bank was already on probation for criminal felony charges.”

The commentary is headlined “Will Jamie Dimon Finally Lose His Job Over Racketeering Charges?” and it’s posted at Wall Street on Parade here:

https://wallstreetonparade.com/2019/09/will-jamie-dimon-finally-lose-his…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

iii) Other physical stories:

What a joke: regulators at the CFTC are expanding their already massive precious metals manipulation to other firms and other markets

(zerohedge)

Regulators Expand Already Massive Precious Metals Manipulation Probe To Other Markets

Just two days after the DOJ took the unprecedented step of designating the JPMorgan precious metals trading desk as a “criminal enterprise” using unusually aggressive language which reminded legal experts of indictments utilizing the RICO Act, and which hopefully ended years of precious metal manipulation by the group formerly headed by Blythe Masters, CNBC now reports that the probe is set to spread significantly as Federal prosecutors and regulators “are expanding their already aggressive investigations of fraudulent precious metals trades at J.P. Morgan Chase to other U.S. markets and financial firms.”

The inquiry into market manipulation of all kinds comes amid a spike in criminal prosecutions and civil actions in the past year involving so-called “spoofing” in the precious metals markets, which we now find had been taking place with reckless abandon for years at JPMorgan and virtually all other major banks.

The prosecutors broadened their investigation thanks to information received from traders questioned for spoofing-related charges, and as in most RICO cases, the information obtained from those traders has led to criminal charges against other individuals.

In short: what we for many years said was blatant manipulation of precious metals was precisely that, and now the participants in said manipulating cabal are being treated as a mafia syndicate by the DOJ.

The widening inquiry is being led by the Justice Department and the U.S. Commodity Futures Trading Commission as they continue their pursuit of individuals and firms for manipulating U.S. markets.

The crackdown may result in one of the biggest conviction rings for the DOJ since the financial crisis, with CNBC adding that the scope of the investigations has grown to the point where the criminal fraud division of the Justice Department expects to add personnel to the existing team to assist with the investigations and prosecutions of cases.

According to CNBC source, prosecutors now have an easier time identifying suspected spoofing due to advancements in the way the Department collects and analyzes trade data internally. Of course, they could have merely come to this site any time between 2009 and 2018 and observed the countless cases of blatant intraday gold and silver manipulation/spoofing which we pointed out, week after week.

CNBC further adds that prosecutors are using information about suspected spoofing to collect additional evidence against a trader and, if warranted, question that trader about their own conduct and that of others. So far, the increased focus on spoofing has resulted in federal prosecutors bringing a total of 13 spoofing cases against 19 defendants in the past five years. Of those, eight have pleaded guilty, while seven are fighting the charges and awaiting trial.

Following the indictment of three J.P. Morgan precious metals traders on Monday, Assistant Attorney General Brian Benczkowski said that the Justice Department is not finished with its probes.

“Our investigation is ongoing, and we’re going to follow the facts wherever they lead whether it is across desks here or at any other bank or upwards into the financial institution,” Benczkowski said.

At the same time, CFTC, the commodity regulator, has also been enhancing its own data analytic capabilities to detect spoofing and other suspicious activity in the markets, which makes sense considering that in 2013 the same CFTC found absolutely no evidence of manipulation in the silver market.

Oops.

“Our goal is to build a really comprehensive data analytical capability — a complete set of data with the expertise to analyze all of it in each specific market so that we have a comprehensive ability to identify suspicious activity in any form it takes in any market it occurs in,” said the Director of the CFTC’s Enforcement Division James McDonald in an interview with CNBC.

McDonald used that knowledge when he moved to revamp the CFTC’s cooperation program. That effort has worked in tandem with the agency’s investment and development in data analytics.

“You can identify the person who executed the trade, but is there a supervisor or someone higher up the chain who may also have culpability?” McDonald said, explaining how to leverage data analysis with personal interviews of traders.

“It can be hard to go up the chain without having someone to tell you what is happening on the inside,” McDonald said.

We can only hope that this time the CFTC actually takes its job seriously, although at this point it is no longer lowly commercial traders who are manipulating gold but central bankers and the BIS itself, something we first reported years ago. We doubt regulators will go after central bankers with the same zeal they have been pursuing the small fish.

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Frazzled Traders Fade Futures, Buy Bonds Ahead Of Repo Injection, Fed Decision

Soaring, then tumbling oil prices; soaring, then sliding repo rates; unprecedented factor volatility as crowded positions exploded – it sure has been quite a week headed into today’s Fed decision which quickly lost the top spot as the most market-moving event of the week amid a barrage of six sigma, exogenous shocks.

While everyone’s attention slowly turned to see how much the Fed would cut today, how Powell would justify easing even as the US economy is once again rebounding, and how the US central bank would respond to the unprecedented liquidity shortage in the repo market, traders were still on edge over this week’s record move in crude even as oil prices cooled further Wednesday after Saudi Arabia said full oil production would be restored by month’s end as it had already revived 41% of capacity. As a result, Brent futures dipped 0.28% to $64.34 a barrel, having conceded about 65% of its gains made after the weekend attack on Saudi Arabia’s oil facilities.

Saudi Energy Minister Prince Abdulaziz bin Salman on Tuesday sought to reassure markets, saying the kingdom would restore its lost oil production by month-end having recovered supplies to customers to the levels they were prior to weekend attacks. “I would think a spike in oil prices will likely prove to be short-term given that the global economy isn’t doing too well,” said Akira Takei, bond fund manager at Asset Management One.

Still, heightened geopolitical tensions underpinned oil as well as some safe-haven assets such as U.S. bonds. A U.S. official told Reuters on Tuesday the United States believes the attacks originated in southwestern Iran, an assessment that could further increase the rivalry between Tehran and Riyadh. Adding to uncertainties in the Middle East were exit polls from Israel’s election, which showed the race too close to call suggesting Prime Minister Benjamin Netanyahu’s fight for political survival could drag on.

At the same time, now that the record barrage of investment grade issuance is finally over, as are hedging rate locks, bonds rallied globally while stocks struggled for traction ahead of Wednesday’s Fed decision, as the dollar rose.

In equities, European stocks traded without direction, with the Stocks 600 index swinging from a loss to a modest gain, led by utilities and oil companies.

A similar drift was observed earlier, when Asian stocks traded little changed as investors awaited the Fed’s decision. Shares rose in China, but declined in Japan and Australia. The Topix dropped for the first time in nine days, ending its longest winning streak in almost two years. Electric appliance makers slid, with Sony Corp. being the biggest drag on the benchmark. Elsewhere, China’s Shanghai Composite Index gained as much as 0.6%, boosted by consumer stocks including Kweichow Moutai Co Ltd. and Foshan Haitian Flavouring & Food Company Ltd. India’s Sensex gained as much as 0.6% as market fears of higher oil prices were assuaged on signs Saudi Arabia is restoring production. The U.S. central bank is broadly expected to cut rates by 25 basis points Wednesday.

S&P 500 Index nudged lower, once again hugging the 3,000 line as Fedex shares plunged in pre-market trading after the company slashed its profit outlook, blaming a global economy weakened by trade tensions.

Looking at today’s main event, in which Fed officials are widely expected to cut their benchmark rate by a quarter-point, some investors such as DoubleLine Capital’s Jeffrey Gundlach are saying the central bank may also boost its balance sheet launching what we dubbed “QE Lite” to stabilize the volatile repo market. Traders also are keeping an eye on whether a potential oil shortage weighs on the global economy, and on preparations by the U.S. and China for top officials to meet on trade in October.

“Markets are currently almost pricing in three more rate cuts by the end of next year, including one by the end of this year, but the chances are that the Fed’s stance will be more hawkish than markets and we could see a rise in bond yields in the near term,” said Masahiko Loo, portfolio manager at Alliance Bernstein.

“Markets want to hear that the Fed is there if needed, the Fed is a backstop,” Alec Young, managing director for global markets research at FTSE Russell, told Bloomberg TV. “There is concern, obviously, from trade, manufacturing, and we’re seeing that bleed into some job-growth weakness, and these are all the big questions that Chairman Powell is going to be getting.”

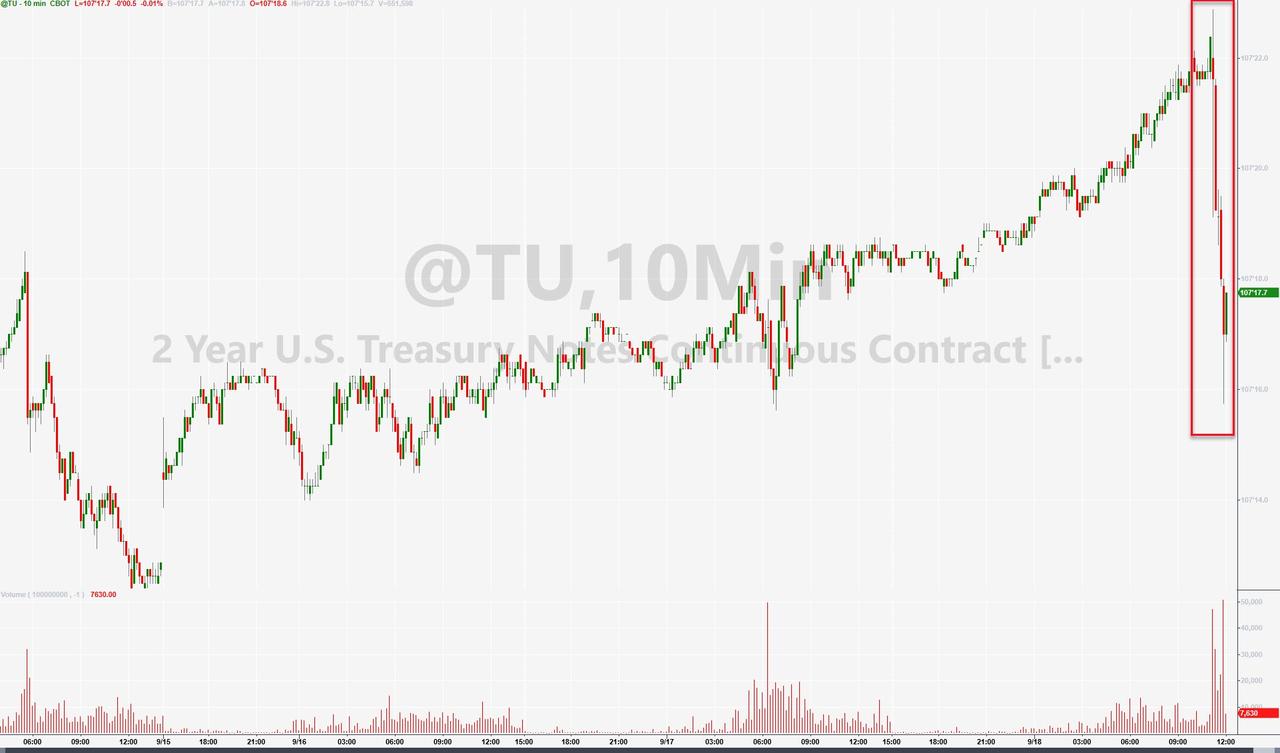

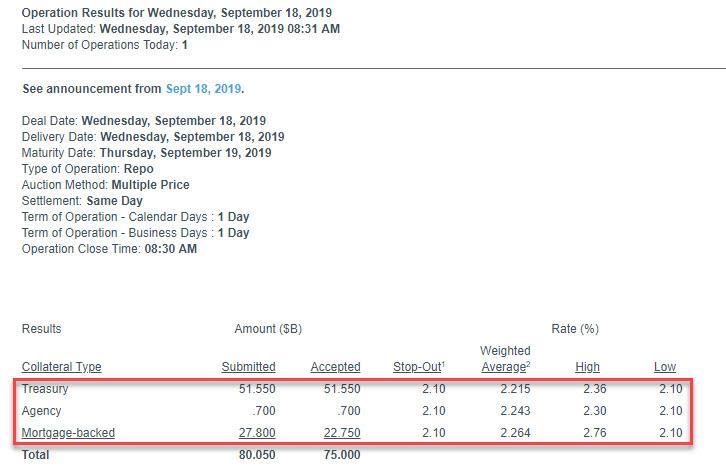

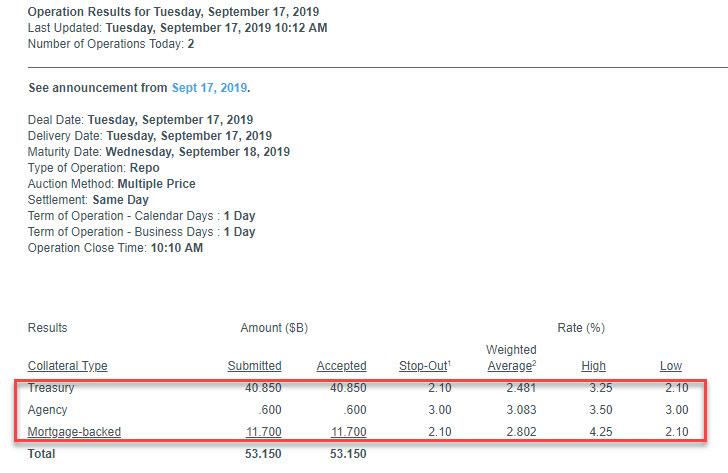

Further complicating the Fed’s discussions, short-term U.S. interest rates shot up this week, with overnight repo rates rising to 7%, due largely to seasonal factors such as huge payments for taxes and bond supply. That prompted the New York Fed to conduct its first repo operation in more than a decade to inject funds to stressed money markets.

The New York Federal Reserve said late Tuesday it would conduct a repurchase agreement operation early on Wednesday “in order to help maintain the federal funds rate within the target range of” 2.00% to 2.25%. Jeffrey Gundlach, chief executive of DoubleLine Capital, said on Tuesday that the repo market squeeze makes it more likely that the Federal Reserve will resume expansion of its balance sheet “pretty soon.”

In FX, the dollar gained against all peers, paring most of Tuesday’s losses, as money markets remained on edge and traders awaited Wednesday’s Federal Reserve policy decision. The pound retreated from the almost two- month high reached Tuesday; the currency was hit by inflation data and increasing pessimism of the Brexit deal being reached before the Oct. 31 deadline. The Norwegian krone was at the center of attention in the G-10, given that it risks volatility around its central bank decision on Thursday. Sterling traded at $1.2483, down 0.1% so far on the day, having hit a two-month high of $1.2528 as investors reversed their bets against the currency on fear of a no-deal Brexit at the end of next month.

Gold was mostly flat at $1,502.10, while the 10-year U.S. Treasuries yield fell to 1.799%, compared with Friday’s 1-1/2-month high of 1.908% ahead of the Fed’s policy announcement on Wednesday.

Expected data include mortgage applications and housing starts. General Mills will report earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 3,003.25

- STOXX Europe 600 up 0.08% to 389.66

- MXAP down 0.1% to 158.87

- MXAPJ up 0.06% to 511.04

- Nikkei down 0.2% to 21,960.71

- Topix down 0.5% to 1,606.62

- Hang Seng Index down 0.1% to 26,754.12

- Shanghai Composite up 0.3% to 2,985.66

- Sensex up 0.3% to 36,576.19

- Australia S&P/ASX 200 down 0.2% to 6,681.59

- Kospi up 0.4% to 2,070.73

- German 10Y yield fell 2.2 bps to -0.496%

- Euro down 0.2% to $1.1053

- Italian 10Y yield rose 7.7 bps to 0.581%

- Spanish 10Y yield fell 1.9 bps to 0.267%

- Brent futures down 1% to $63.91/bbl

- Gold spot little changed at $1,501.66

- U.S. Dollar Index up 0.2% to 98.41

Top Overnight Headlines from Bloomberg

- The Fed bought $53.2 billion of U.S. securities on Tuesday to quell a liquidity squeeze, and said it would conduct another overnight repo operation of up to $75 billion Wednesday morning; the moves had markets reeling and underscored just how deep the structural problems in U.S. money markets have become

- Under pressure from Wall Street and President Donald Trump, the Fed is widely expected to reduce interest rates, but its sharply divided policy panel may be reluctant to forecast further cuts

- Saudi Arabia reassured anxious customers that crude exports will keep flowing as normal and its industry can recover quickly from the worst attack in its history; the kingdom restored about half of pre-attack capacity at the crucial Abqaiq facility

- European Commission President Jean-Claude Juncker said the risk of a no-deal Brexit on Oct. 31 is now “palpable,” sparking a drop in the pound; he said the main sticking point continued to be the so-called backstop to avoid a hard Irish border and demanded that the U.K. provide its proposals for an alternative in written form as soon as possible

- Benjamin Netanyahu’s gamble to hold elections for a second time this year backfired after a stunning deadlock left Israel rudderless and convulsed by a new wave of political turmoil

Asian equity markets traded tentatively following the cautious gains on Wall St amid positioning heading into a flurry of central bank activity including the FOMC decision where the Fed are expected to deliver a consecutive 25bps cut. ASX 200 (-0.2%) and Nikkei 225 (-0.2%) were indecisive ahead of the looming risk events and with Australia subdued by losses in the energy sector after an aggressive pullback in oil prices due to reports Saudi oil output will return to normal levels quicker than initially anticipated, while the Japanese benchmark remained at the whim of a choppy currency amid somewhat inconclusive data which showed Exports contracted for a 9th consecutive month albeit at a narrower than expected decline. Hang Seng (-0.1%) and Shanghai Comp. (+0.3%) conformed to the holding pattern seen across regional and global counterparts after the PBoC opted for a net neutral position in its liquidity operations and after President Trump reverted back to a blasé approach on US-China trade in which he suggested a deal could come soon, possibly before the 2020 election or after. Finally, 10yr JGBs initially continued to oscillate around the 154.00 level as the BoJ kick-started its 2-day policy meeting, although prices eventually gained traction after tripping stops through this week’s resistance levels and largely ignored the mostly weaker 20yr JGB auction results.

Top Asian News

- An Army of Japanese Salarymen Is Rocking Global Currency Markets

- Vietnam Becomes a Victim of Its Own Success in Trade War

- Profiting From Trade War, China Fund Jumps 54% in First Year

- London Trading More Rupee Than India Shows What Modi Needs to Do

- Thai Court Rejects Petition Seeking to Disqualify Prime Minister

Major European bourses are flat (Euro Stoxx 50 +0.1%), following on from a tentative AsiaPac session, amid cautious trade ahead of this evening’s FOMC meeting. IBEX 35 (+0.2%) was mildly softer after the open, although has since turned around, amid more political uncertainty, after the King stated there was no candidate for a parliament investiture vote; meaning Spaniards will return to the polls in November for the fourth time in four years. In terms of sector performance; Energy (+0.4%) has managed to shrug off yesterday’s fall in oil prices, while Telecoms (u/c), Consumer Discretionary (-0.4%), Consumer Staples (-0.2%) and Industrials (-0.1%) are the laggards. Luxury names, including Richemont (-4.1%) and Swatch Group (-2.6%), are under pressure after UBS downgraded the sector, with downside in Moncler (-4.5%) exacerbated by cautious comments from the co.’s CEO, who expressed concern about the situation in Hong Kong. In the lead are utilities (+0.4%), with gains in EDF (+3.7%) helping to prop up the sector (the Co. reported weld issues in six reactor units relating to 16 steam generators but does not believe they pose a significant adverse effect now), while materials (+0.2%) and Tech (+0.4%) are also higher. In terms of other notable individual movers; Kingfisher (-2.4%) is lower after sales disappointed (GBP 6.0bln vs. Exp. GBP 6.02bln and like-for-like sales down 1.8%). Elsewhere, Wirecard (+3.1%) took a leg higher on the news that the co. has signed a strategic co-operation agreement with Japan’s Softbank. Finally, Beiersdorf (-1.0%) is under pressure after being downgraded at Goldman Sachs.

Top European News

- U.K. Inflation Rate Falls to Lowest Since 2016 on Games, Clothes

- Comcast’s Sky Moves Beyond BT’s Network in U.K. with Fiber Deal

- Cobham’s $5 Billion Sale to Advent Sparks U.K. Security Probe

- EDF Rises on Belief That Reactor Weld Issues Don’t Need Fixing

In FX, the DXY seems to have established a firm base above 98.000 and Fib support just above the big figure, partly due to weakness in the Greenback’s G10 counterparts, but also on the back of recent firmer than forecast US data/surveys, increased demand for short term Usd funds and a marked change in Fed rate expectations going into September’s policy meeting (odds between another 25bp hike and no change much closer to even from around 90% for +1/4 point only a few days ago). The index is currently just shy of 98.500 and considerably closer to nearest resistance (98.744 yesterday) than the aforementioned downside chart retracement level (98.034).

- GBP/NZD/AUD – The major underperformers, with Cable already retreating after another 1.2500+ sortie and failure to sustain gains above the 100 DMA (1.2501) amidst relatively negative Brexit remarks from EU’s Barnier and Juncker, but then extending its pull-back through 1.2450 at one stage in wake of significantly softer than expected UK CPI on the eve of retail sales and the BoE rate convene. Meanwhile, the Kiwi is back under pressure alongside the Aussie after overnight releases showing a decline in Westpac’s LEI and mixed NZ Q2 current account metrics, with Nzd/Usd under 0.6350 again and Aud/Usd sub-0.6850. Note, Aud/Nzd is still pivoting 1.0800 following this week’s dovish RBA minutes and eyeing NZ Q2 GDP later today, while Aud/Usd appears capped by decent upside option expiry interest at 0.6860-65 (1 bn) and 0.6895-0.6900 (2.6 bn).

- JPY/CAD/CHF/EUR – Also weaker against their US peer, albeit on a sliding scale as the Yen contains losses over the 108.00 mark with the aid of a narrower than anticipated Japanese trade gap and with expiries also in close proximity (1.1 bn at 108.25-40 and then 1 bn at 108.75 if Tuesday’s multi-week peak and 108.50 are breached) ahead of the FOMC and BoJ tomorrow. Meanwhile, the Loonie has regained some poise and traction having held just above 1.3300 yesterday to meander around 1.3250 awaiting some independent impetus from Canadian CPI in advance of the Fed. Elsewhere, the Franc remains anchored near 0.9950, but has weakened vs the Euro to 1.1000 into the SNB on Thursday even though the single currency has lost momentum against the Buck following another approach towards 1.1100. Indeed, Eur/Usd has pulled back below 1.1050 amidst downbeat commentary from ECB’s de Guindos and the headline pair may gravitate further given more downside option expiry interest compared to upside (1.6 bn at the 1.1000 strike and 1 bn between 1.1020-30 vs 1.7 bn from 1.1100 to 1.1115).

- EM – The Rand is also awaiting the Fed before turning attention to tomorrow’s SARB meet, and Usd/Zar has largely taken in stride slightly firmer than forecast SA CPI ahead of retail sales within a 14.7080-6325 band, though mostly trading near the base.

In commodities, the crude complex is largely in consolidation mode ahead of key risk events (FOMC) amid a lack of fresh catalysts and following yesterday’s declines, triggered by news that Saudi oil output will return to normal levels faster than originally assumed; Energy Minister Abdulaziz said oil supply is fully back online and resumed as before after more than half the oil output was resumed in the past few days and that it will keep full oil supply to its customers this month. Losses were later exacerbated by a surprise build in API inventories. Brent Nov’19 futures sit just above the USD 64/bbl handle, just above yesterday’s USD 63.50/bbl lows, with WTI similarly lacklustre just above the USD 59.0/bbl mark. In terms of geopolitical developments, the pace appears to have slowed somewhat; the Trump administration is reportedly considering a range of options to retaliate against Iran including cyberattack or physical strike on Iran’s oil facilities or Revolutionary Guards assets, meanwhile, the Saudis continue to point the finger at Iran, who have doubled down in denial. Looking ahead, IEA Birol will conduct a press conference today at 14.00BST alongside a press conference from the Saudis who are expected to show evidence of Iran’s involvement and that Iranian weapons were used in Aramco attacks. Separately, lacklustre trade in the metals complex reflects cautious sentiment, with gold holding on to the USD 1500/oz level for now and copper a touch lower.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 2.0%

- 8:30am: Housing Starts, est. 1.25m, prior 1.19m; Housing Starts MoM, est. 4.95%, prior -4.0%

- 8:30am: Building Permits, est. 1.3m, prior 1.34m; Building Permits MoM, est. -1.29%, prior 8.4%

DB’s Jim Reid concludes the overnight wrap

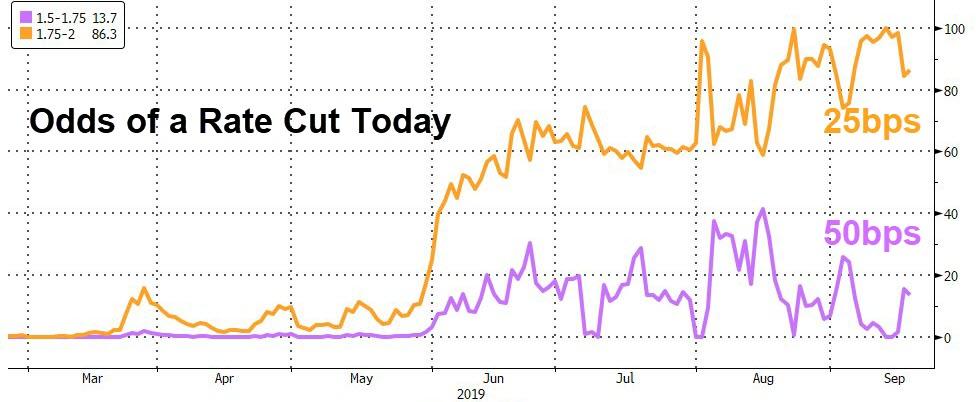

I write this from Paris this morning but there’s only one place to start and that’s in Washington ahead of the Fed meeting this evening. Not long ago this FOMC was perhaps gearing up to be closer to a 50/50 call between a 25bp or 50bp cut however the latter looks a lot less likely now with markets only pricing in about a 15% chance of that happening. That fits with the view of our US economists who also expect a 25bp cut which mirrors the consensus.

The bigger focus will be on what the Fed signals about the expected policy trajectory in the coming months. Our US economists note that a continued dovish bias should be evident in the statement language, Summary of Economic Projections and Chair Powell’s press conference. The latter in particular should echo the narrative that, while the baseline outlook for the economy remains favorable, officials are attuned to significant risks emanating from softer global growth and elevated trade uncertainty. As in July, Powell should stop short of detailing the likelihood and timing of any future actions, but the signal should be that the bar is set relatively low for further rate reductions with the Committee intent to “act as appropriate to sustain the expansion”.

Our colleagues do not expect the September rate cut to be the last of this cycle though. With accumulating evidence that the economy is slowing amid greater sensitivity to the trade turmoil, they recently adjusted their call to reflect a further cumulative 75bps of rate cuts after this meeting, specifically at the October, December and January get togethers. All eyes on 7pm BST/2pm EST.

In an ideal world the Fed was probably hoping that markets would go into today in a relative state of calm however the mini sell-off across bond markets over the last couple of weeks and the biggest daily climb for oil in over a decade put an end to that. You can also add panic in the US funding market to that list after the overnight repo rate touched as high as 10% intraday yesterday and one of the highest levels on record. Notwithstanding a technical delay, the NY Fed did move to calm the market by conducting an overnight repo operation – the first in a decade – for $53bn which helped to push the rate back down however another operation is planned for today for up to $75bn.

There appeared to be various schools of thought on what caused the explosion in overnight funding rates with bulging treasury supply, a mismatch of cash liquidity tax payments, regulatory constraints, bloated dealer sheets, banking seasonals and investors selling bonds back to dealers all cited as possible reasons. We remained confused about the real cause!! Whatever created the tensions it’s not gone unnoticed that we’ve had two huge moves in different asset classes this week, in addition to the rates’ selloff of the prior two weeks.

Just on oil, WTI and Brent both sold-off around 6% yesterday – and thus gave up about half of Monday’s gains – after Reuters reported that Saudi Arabia is supposedly close to restarting 70% of the lost oil production following the weekend attack. The same story also suggested that output would be fully back online in the next couple of weeks, citing a “top Saudi source”. The Kingdom later confirmed that they will ensure this month’s supply by drawing on reserves. Aramco’s CEO also confirmed that the Abaqiq facility should be back to pre-attack levels of output by the end of September. Gasoline (-7.73%) and Heating Oil (-9.42%) also fell in tow however the end result for equities was fairly muted. Indeed the S&P 500 ended +0.26% while the DOW and NASDAQ ended +0.13% and +0.40% respectively. This was after the STOXX 600 had closed -0.05%. After the US bell, trade bellwether FedEx cut its 2020 profit outlook on a weaker global economy and trade tensions. The shares were down as much as 10% in after-hours trading potentially wiping out gains for the year.

Meanwhile US HY credit spreads finished little changed with energy spreads 4bps wider. As for bonds, 10y Treasuries finished -4.5bps lower with the 2s10s curve flattening 1bp to +7.2bps, while Bunds finished little changed. It was BTPs (+7.9bps) which stood out the most in Europe though following (an albeit expected) confirmation of the news we discussed yesterday morning that former PM Renzi was leaving the PD to form his own party, further complicating the political stability picture in Italy.

This morning in Asia, with the exception of Japan where the Nikkei (-0.13%) is a touch lower, most bourses are flat to slightly higher ahead of the Fed. That’s the case for the Hang Seng (+0.03%), Shanghai Comp (+0.39%) and Kospi (+0.44%). The yen is slightly weaker, following weak trade export data in Japan this morning (albeit not as weak as expected), and the news yesterday that South Korea had removed Japan from its list of most trusted trading partners.