GOLD:$1507.60 UP $8.60 (COMEX TO COMEX CLOSING)

Silver:$17.83 UP 3 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1515.60

silver: $17.97

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/3

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,498.400000000 USD

INTENT DATE: 09/19/2019 DELIVERY DATE: 09/23/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

737 C ADVANTAGE 2 2

905 C ADM 1

____________________________________________________________________________________________

TOTAL: 3 3

MONTH TO DATE: 1,741

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 3 NOTICE(S) FOR 300 OZ (0.00933 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1741 NOTICES FOR 174100 OZ (5.4152 TONNES)

SILVER

FOR SEPT

166 NOTICE(S) FILED TODAY FOR 830,000 OZ/

total number of notices filed so far this month: 8607 for 43,035,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 10153 DOWN 93

Bitcoin: FINAL EVENING TRADE: $ 10152 down 92

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A SMALL SIZED 320 CONTRACTS FROM 210,878 UP TO 211,198 DESPITE THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0, DEC: 465 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 465 CONTRACTS. WITH THE TRANSFER OF 465 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 465 EFP CONTRACTS TRANSLATES INTO 2.325 MILLION OZ ACCOMPANYING:

1.THE 4 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.180 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

WE AGAIN HAD ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY BUT TO NO AVAIL

AS THE TOTAL OPEN INTEREST IN BOTH EXCHANGES RISE ALBEIT BY A VERY SMALL AMOUNT.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

25,575 CONTRACTS (FOR 14 TRADING DAYS TOTAL 25,575 CONTRACTS) OR 127.87 MILLION OZ: (AVERAGE PER DAY: 1826 CONTRACTS OR 9.133 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 127.87 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 18.14% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1677.48 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 320, DESPITE THE 4 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 465 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 785 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 465 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 320 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 4 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $17.80 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.056 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 166 NOTICE(S) FOR 830,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.180 MILLION OZ//

2 THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

3 HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3637 CONTRACTS, TO 632,101 DESPITE THE $8.90 PRICING LOSS WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6488 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 6488 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 632,101,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,125 CONTRACTS: 3637 CONTRACTS INCREASED AT THE COMEX AND 6488 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 10,125 CONTRACTS OR 1,012,500 OZ OR 31.49 TONNES. YESTERDAY WE HAD A LOSS OF $8.90 IN GOLD TRADING….

AND DESPITE THAT LOSS IN PRICE, WE HAD A STRONG GAIN IN GOLD TONNAGE OF 31.49 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME WAS HUGE. THEY WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE LONGS AND AS YOU CAN SEE, THE TOTAL OPEN INTEREST IN BOTH EXCHANGES SKYROCKETED

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 98,588 CONTRACTS OR 9,858,800 oz OR 306.65 TONNES (14 TRADING DAY AND THUS AVERAGING: 7042 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAYS IN TONNES: 306.55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 306.55/3550 x 100% TONNES =8.63% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4458.25 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 3637 DESPITE THE PRICING LOSS THAT GOLD UNDERTOOK YESTERDAY($8.90)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6,488 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6488 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 10,125 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6488 CONTRACTS MOVE TO LONDON AND 3637 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 31.49 TONNES). ..AND THIS HUGE INCREASE OF DEMAND OCCURRED DESPITE THE LOSS IN PRICE OF $8.90 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.60 TODAY//(COMEX-TO COMEX)

INVENTORY RESTS AT 883.60 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 3 CENTS TODAY:

/INVENTORY RESTS AT 375.473 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 320 CONTRACTS from 210,878 UP TO 211,198 AND CLOSER TO A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 465: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 465 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 320 CONTRACTS TO THE 465 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIL SIZED GAIN OF 785 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.925 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: : 43.180 MILLION OZ//

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 4 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 465 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED UP 7.17 POINTS OR 0.24% //Hang Sang CLOSED DOWN 33.28 POINTS OR 0.13% /The Nikkei closed UP 34.64 POINTS OR 0.16%//Australia’s all ordinaires CLOSED UP .20%

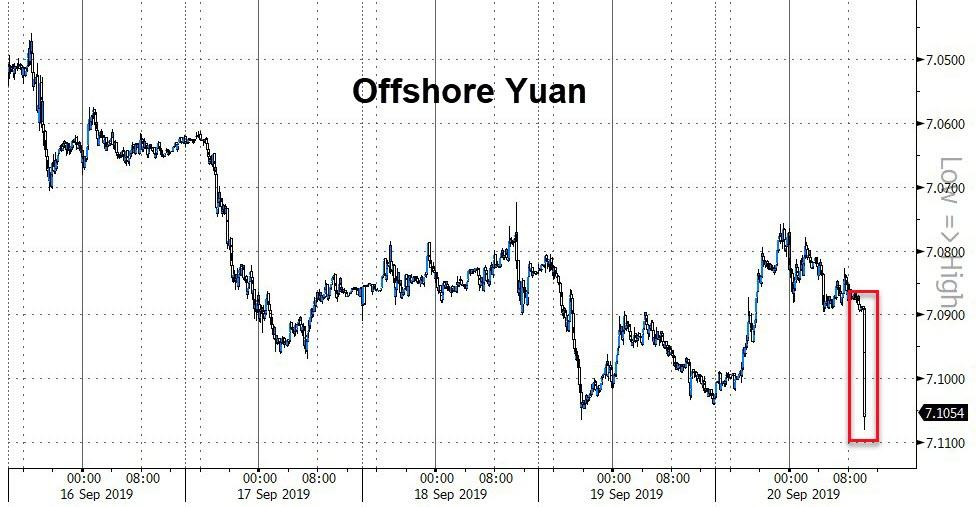

/Chinese yuan (ONSHORE) closed UP at 7.0878 /Oil UP TO 58.72 dollars per barrel for WTI and 64.68 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 7.0878 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0848 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

CHINA/USA

My goodness did that escalate fast. A Chinese trade delegation has cancelled its USA farm visit to Montana and agrictulre officials are returning to China sooner than expected. That sent odds of a trade deal reeling..

(zerohedge)

4/EUROPEAN AFFAIRS

UK

Our resident expert on UK affairs checks in and stats that the odds of a bad Brexit may be increasing due to the strengthening of liberal Democrats over Labour. This is one big mess but I am counting on Bo Jo to pull this out of the fire

(Mish Shedlock)

ii)GERMANY.

Germany reaches a climate plan which is fiscally neutral. This disappoints the street greatly as they were counting on a huge German stimulus

(zerohedge)

iii)GERMANY/COMMERZBANK

Troubled German bank now plans to cut 4300 jobs and to sell its stake in Polish bank M Bank

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)Finally Lawrie Williams is beginning to state that GATA is correct in the manipulation of gold/silver by governments and banks

(GATA/Lawrie Williams/Chris Powell/GATA)

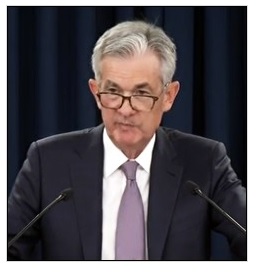

ii)Fed Chairman Powell fails to answer questions on whether Wall Street banks are just too big to manage and too big to fail due to their monstrous derivative positions

(courtesy Pam and Russ Martens/Wall Street on Parade)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

i)Global Macro Monitor analyze stuff pretty good. Here they outline 3 reasons for the lack of plumbing in the money markets.

i believe they are bang on.

(courtesy Global Macro Monitor)

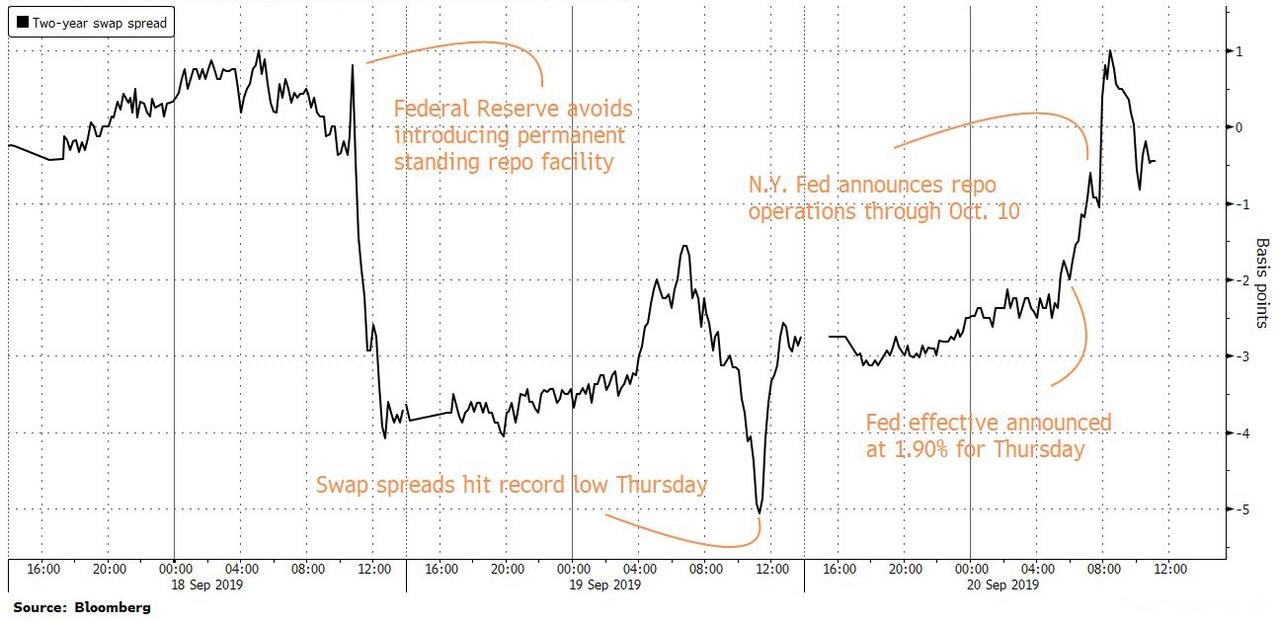

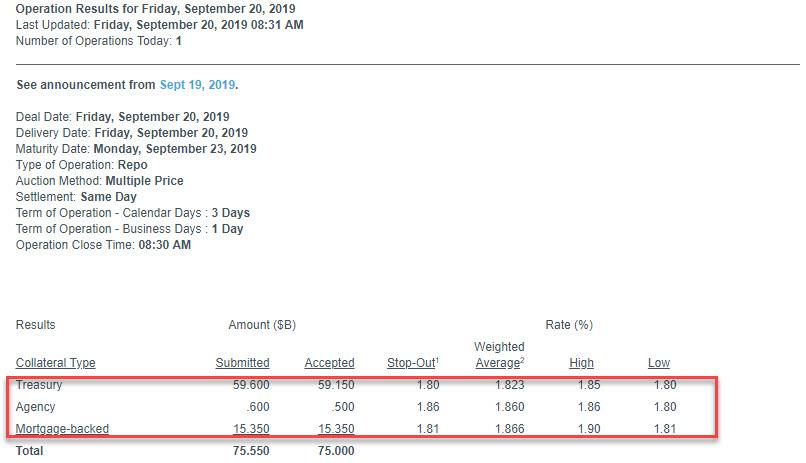

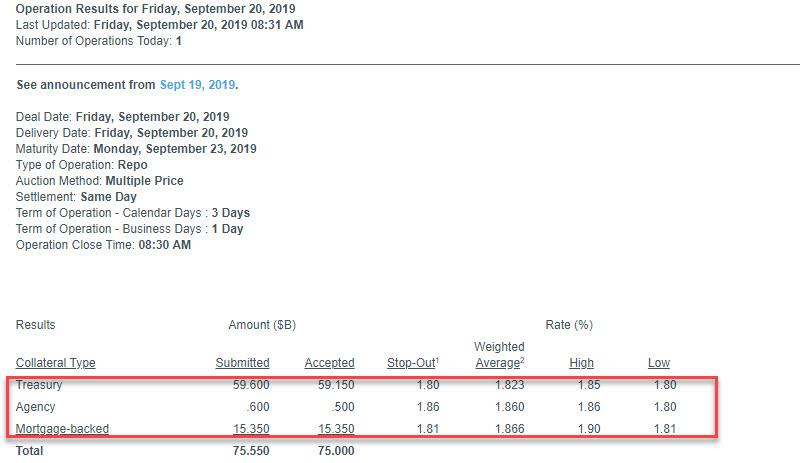

ii)The Fed Repo is oversubscribed for the 4th straight day but the funding drops to a touch over 75 billion. They still did not know what caused the plumbing to seize up but Goldman Sachs states that in very short order the Fed will engage in QE4 or POM0 which is identical in nature

(zerohedge)

ii b)Then early this afternoon: extremely important

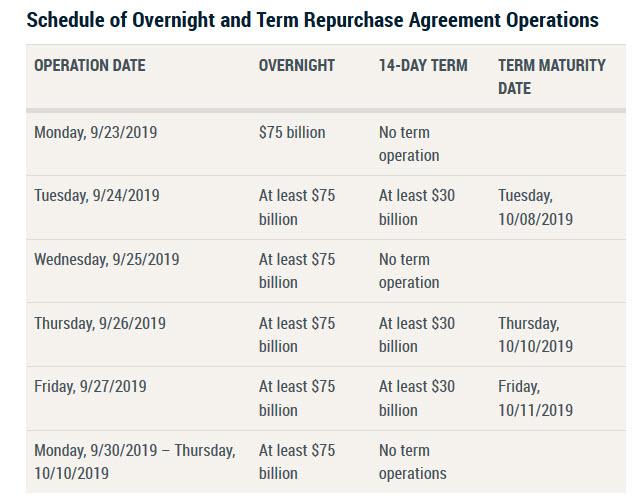

The Fed just announced a series of Repos next week each totalling $75 billion each plus a 14 day term Repo. The total amount of repos: 165 billion dollars. Obviously the plumbing has not been fixed, By late Oct or early Nov expect the Repos to be replaced by permanent POMO ( QE4)

zerohedge

iii)Here is the real story on the Fed dissents. Clearly Trump would like to fire Powell and bring on a Bullard Fed

(zerohedge)

iv)This is an accident waiting to happen. This company,We Work, is continually in the red and has no hope of turning a profit. It IPO has been stalled because of faulty valuation. It eventual bankruptcy will unleash a system risk to the economy

v)The mess in Illinois: now bankrupt cities are forced to cut services to fund pensions. Eventually they will have to cut their entire police force to pay these pensions. East St Louis has only two years of cash left

iv) Swamp commentaries)

As promised to you, this is a joke. The Democrats are going nuts on this. It seems that Trump wants more information from the Ukraine on the Joe Biden/Hunter Biden theft of billions of dollars from the Ukraine

(zerohedge)

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

THE BANKERS SUPPLIED THE NECESSARY AND INFINITE AMOUNT OF SHORT PAPER IN GOLD. THE BANKERS SUCCEEDED IN LOWERING GOLD’S PRICE BY A CONSIDERABLE LOSS OF $8.90. HOWEVER, JUDGING BY THE STRENGTH IN GAIN OF OUR TOTAL OI CONTRACTS, THEY WERE AGAIN UNSUCCESSFUL IN THE ENDEAVOUR TO FLEECE ANY UNSUSPECTING LONGS.

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; nil oz

We had one adjustment and for the first time in 3 months we had moving from the dealer to the customer:

From the Delaware vault:

702.03 oz was adjusted out of the dealer and this landed into the customer account and this is deemed a settlement.

i) Into the dealer CNT: 599,482.336 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 25,403 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 68,280 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 68,280 CONTRACTS EQUATES to 341 million OZ 48.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.06% ((SEPT 19/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.21% to NAV (SEPT 19/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -2.06%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.25 TRADING 14.77/DISCOUNT 3.15

END

And now the Gold inventory at the GLD/

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 20/2019/ Inventory rests tonight at 883.60 tonnes

*IN LAST 668 TRADING DAYS: 51.74 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 568- TRADING DAYS: A NET 114.87 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ//

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 20/2019:

Inventory 375.473 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.13/ and libor 6 month duration 2.08

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .05

XXXXXXXX

12 Month MM GOFO

+ 2.08%

LIBOR FOR 12 MONTH DURATION: 2.07

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = -.01

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

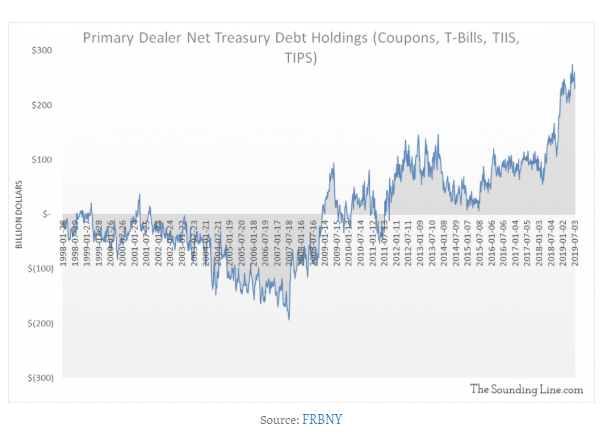

‘Plumbing of the U.S. Financial System’ Under Pressure; NY Fed Providing Massive Liquidity and Potentially Permanent Repo and QE

◆ The ‘plumbing of the U.S. financial system’ is under pressure as liquidity dries up forcing New York Federal Reserve to provide massive liquidity and potentially they may be forced to move to permanent repo operations and renewed quantitative easing or QE

◆ The New York Fed appears to be set to do another $75 billion overnight repo operation today. It follows massive liquidity injections of the same size yesterday and on Wednesday, and $53.2 billion on Tuesday.

◆ The Fed is preparing a ‘temporary’ liquidity injection for a fourth straight day and there are concerns that increased signs of severe stress in the funding markets in the U.S. may force the Fed to permanently increase their reserves by electronically creating dollars in order to buy more U.S. Treasurys

◆ The Fed is deploying this ‘remedy’ for the first time in a decade, since the last global financial crisis and there are signs that we may be on the verge of another financial crisis centered on the U.S. financial and monetary system

◆ Gold prices are marginally higher today and for the week and appear headed for their first weekly gain in four weeks, supported by concerns about the U.S. financial system, a softer dollar, the tinder box that is the Middle East and trade wars which are impacting global economic growth.

Overstock Founder Dumps His Stake for Gold, Silver and Crypto Assets

Serious inroads into manipulation but still unfinished business

Fed chairman fails to answer whether Wall Street banks are too big to manage

Repo Rates And Gold: Something Big Is Happening

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

19-Sep-19 1498.40 1500.70, 1200.67 1201.76 & 1354.85 1357.08

18-Sep-19 1502.20 1503.50, 1206.27 1204.90 & 1360.39 1359.92

17-Sep-19 1499.30 1502.10, 1208.89 1207.24 & 1361.51 1360.45

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

10-Sep-19 1494.60 1498.25, 1211.52 1211.34 & 1353.51 1357.11

09-Sep-19 1509.95 1509.20, 1223.81 1220.34 & 1368.62 1364.92

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

Finally Lawrie Williams is beginning to state that GATA is correct in the manipulation of gold/silver by governments and banks

(GATA/Lawrie Williams/Chris Powell/GATA)

Lawrie Williams at Sharps Pixley: Maybe GATA isn’t so nuts after all

Submitted by cpowell on Thu, 2019-09-19 15:48. Section: Daily Dispatches

11:45a ET Thursday, September 19, 2019

Dear Friend of GATA and Gold:

GATA has never gotten treatment as approving from London bullion dealer Sharps Pixley and its market analyst, Lawrie Williams, as it did with Williams’ commentary Monday.

Williams quoted at length from your secretary/treasurer as if our tinfoil hats have transformed themselves into combat helmets for a new charge against the tyranny and corruption of central banking.

Or else Williams now is wearing a tinfoil hat too.

Williams’ commentary is headlined “JPMorgan Gold and Silver Spoofing Defined as ‘Racketeering’ by U.S. Prosecutors” and it’s posted at Sharps Pixley here:

https://www.sharpspixley.com/articles/lawrie-williams-jp-morgan-gold-and…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

LAWRIE WILLIAMS: JP Morgan gold and silver spoofing defined as ‘racketeering’ by U.S. Prosecutors

Probably yesterday’s biggest precious metals story was not only the indictment of JP Morgan’s precious metals trading desk on ‘spoofing’ in the markets, but the extremely serious nature of the charges being brought against the U.S.’s biggest bank. For years there have been arguments and counter arguments against whether there has been price manipulation in the precious metals markets by the big banks. This latest prosecution suggests strongly that there is as ‘spoofing’ is a key weapon in the manipulators’ arsenal and JP Morgan is no small regional bank but perhaps the U.S.’s biggest which appears to have made millions, if not billions, of dollars from these alleged activities.

‘Spoofing’ is the practice of making huge buy and sell orders on the futures markets, thus substantially influencing prices, but then cancelling the orders before they are executed. Prosecutors seem to be suggesting that such manipulative activities were inherited from the practices of Bear Stearns, which was taken over by JP Morgan back in 2008, and have been going on ever since – probably at an enhanced level – but without mentioning the names of the banks concerned. However it is two JP Morgan traders and their department head who have been indicted.

According to a Bloomberg report, the JPMorgan investigation grew out of a multibank U.S. crackdown on manipulation of commodities markets using techniques including spoofing. The Justice Department had already brought criminal charges against 16 people, including traders who worked for Deutsche Bank and UBS. Seven pleaded guilty, one was convicted at trial and another was acquitted. The latest indictments may thus be only the ‘tip of the iceberg’ in terms of large scale manipulations of all kinds of markets.

In the words of Chris Powell of GATA (The Gold Anti-Trust Action Committee) precious metals price manipulation goes much further and that the commercial banks, which are the prime movers in forms of market manipulation, are working in conjunction with many of the world’s central banks keen to protect their domestic currencies from the safe haven attraction of gold in particular.

According to Powell, this means firstly that “metals and minerals are underpriced, along with most commodities, because of the price suppression engineered by central banks to defend their currencies and government bonds. Central banks and governments in the developed world don’t want gold, silver, other metals, and other commodities to compete with their currencies as stores of value. (As the recent acquisition of gold by Russia, China, and other governments suggests, gold price suppression has been figured out in some quarters at last and certain countries are turning to gold to regain financial sovereignty.)

Second, it means that there is a vast and uncoverable short position in the monetary metals and other strategic commodities. Thus they have great potential for price appreciation.

Third, it means that Western central banks are not likely to surrender this short position without a fight or another negotiated international currency revaluation.

Fourth, since governments can create infinite money, it means that if you are trading against secret trading by the government, you are likely to lose.

Fifth, it means that if commodity prices ever regain free markets, commodity producers should be prepared for stiffer royalty requirements and windfall profits taxes.

And sixth, it means that people in the mining and commodities businesses may have an obligation to their investors and clients to inform them of the opposition of major governments to free markets and higher commodity prices. It means we all may have an obligation to clamor for governments to tell us the truth about their surreptitious interventions in the markets. For this price suppression works only through deception.

Because it depends entirely on government for its mining claims, royalty requirements, and enforcement of environmental regulations, the mining industry is the industry most vulnerable to government. Any government can shut down any mining company on any pretext at any time.”

Powell said back in 2008 “There are no markets anymore, just interventions” applying the manipulations to all markets, not just those of precious metals. This has been borne out by a number of prosecutions against traders in key global financial markets, often accompanied by guilty pleas from the individuals indicted.

What is perhaps unprecedented in the latest indictments is the language used by the prosecutors in describing JP Morgan’s precious metals desk as a ‘criminal enterprise operating inside the bank’ and the individuals indicted as partaking in a ‘conspiracy to conduct the affairs of an enterprise involved in interstate or foreign commerce through a pattern of racketeering activity.’ For several years now, Ted Butler, who is a close follower of precious metals markets with an emphasis on silver, has described JP Morgan’s market activities as ‘criminal’ in the true sense of the word – it now seems that U.S. prosecutors are taking a similar position, thus vindicating Ted’s ongoing campaign. Indeed Ted’s frequent accusations of JP Morgan’s criminality were made without the bank denying this accusation at any time.

But the JP Morgan employees and past employee, who are the subjects of the indictments, should probably be seen as the mere implementers of an ongoing policy to which even more senior bank employees will have turned a blind eye. It is hugely unlikely that a part of the business which was continually making enormous profits for the bank would not have raised eyebrows and received tacit approval. However top management is probably sufficiently insulated from the activities of the more junior staff members (the sacrificial lambs) to avoid prosecution, although the stigma will remain. One assumes too that those who have been indicted will be well rewarded for taking the fall!

Of course JP Morgan is most probably not the only major bank which has indulged in this kind of activity in the name of mega profits. Whether the Department of Justice will broaden, or extend, its enquiry into such activity elsewhere, or will see the JP Morgan case as a warning for others to cease and desist from such activities, is uncertain at this point. Similar activity by the big money may well continue, although perhaps will be even more surreptitious in nature.

17 Sep 2019

Fed Chairman Powell fails to answer questions on whether Wall Street banks are just too big to manage and too big to fail due to their monstrous derivative positions

(courtesy Pam and Russ Martens/Wall Street on Parade)

Pam and Russ Martens: Fed chairman fails to answer whether Wall Street banks are too big to manage

Submitted by cpowell on Fri, 2019-09-20 00:57. Section: Daily Dispatches

8:56p ET Thursday, September 19, 2019

Dear Friend of GATA and Gold:

Systemic risk abounds with the big banks on Wall Street, Pam and Russ Martens write today at Wall Street on Parade, but no journalist at Federal Reserve Chairman Jerome Powell’s press conference this week bothered to ask about it, and only one reporter came even close.

Powell, the Martenses write, “pretends that 2008 never happened. Lending came to a frightening halt in 2008 because no one could predict with any clarity which Wall Street bank would fail next as a result of its own high leverage or its exposure to a highly levered borrower like Lehman Brothers.”

…

Of course GATA long has complained about the critical questions the mainstream financial news organizations won’t put to governments and central banks about their surreptitious interventions in the markets.

The Martenses’ commentary is headlined “At Press Conference, Fed Chair Powell Refuses to Answer Whether Wall Street Banks Are Too Big to Manage” and it’s posted at Wall Street on Parade here:

https://wallstreetonparade.com/2019/09/at-press-conference-fed-chair-pow…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Press Conference, Fed Chair Powell Refuses to Answer Whether Wall Street Banks Are Too Big to Manage

By Pam Martens and Russ Martens: September 19, 2019 ~

Following a lack of liquidity on Wall Street, which necessitated the Federal Reserve having to provide $53 billion on Tuesday and another $75 billion on Wednesday to normalize overnight lending in the repo market, the Chairman of the Fed, Jerome (Jay) Powell held his press conference at 2:30 p.m. yesterday. The press gathering followed both a one-quarter point cut in the Fed Funds rate by the Fed yesterday as well as the first intervention by the Fed in the overnight lending market since the financial crash. (The Fed had to intervene again this morning, making another $75 billion in repo loans available.)

The week’s unsettling events should have provided the basis for reporters to fire questions at the Fed Chair along the following lines: (1) Did the overnight repo lending rate jump to an historical high of 10 percent on Tuesday because some of the largest Wall Street banks backed away from lending? (2) With six mega banks on Wall Street holding 90 percent of the risky $272 trillion U.S. derivatives market and also a disproportionate share of Federally-insured deposits, could the U.S. see another 2008 type of crash on Wall Street? (3) Are these six banks too interconnected with each other, meaning that if one of them gets into trouble as Citigroup did in 2008, could it spill over to every other mega Wall Street bank?

While every major business news outlet was represented at the press conference, not one of the above questions was asked. One reporter, however, came close.

Hannah Lang, a reporter with American Banker, asked Powell about reports out yesterday that Bank of America was being investigated by the Consumer Financial Protection Bureau for opening unauthorized accounts. She asked if the Fed was also investigating this and said that given the pending order against Wells Fargo for the same kind of behavior, if Powell was concerned that these banks are too big to manage.

Powell said he saw the news about Bank of America but he had no further information to share. He said that the Wells Fargo situation was quite harmful to the customers and damaged the firm’s reputation. As for whether these mega banks are too big to manage, Powell simply ignored that portion of the question entirely.

If Lang had wanted to add critical ammunition to her question, she might have posed it this way: “Chairman Powell, for the first time in U.S. history, two of the largest banks on Wall Street are admitted felons. Citigroup admitted to one criminal felony count in 2015 for its role in rigging foreign currency markets. JPMorgan Chase, the largest bank in the U.S. and on Wall Street, has admitted to three criminal felony counts in the last five years: two counts for its role in Bernie Madoff’s Ponzi scheme and one count for its involvement in rigging foreign currency markets. On Monday, JPMorgan Chase was back in the news again with the Department of Justice charging three of its gold and silver traders with racketeering – a criminal charge typically used against organized crime. And, today, Bank of America is under investigation for opening the same kind of unauthorized customer accounts that happened at Wells Fargo. Mr. Chairman, are these banks too big to manage and too corrupt to be allowed to exist?”

If one considers the trillions of dollars in derivatives that these banks are on the hook for, they have once again become highly leveraged and dangerous. Chairman Powell responded to a question from Nancy Marshall-Genzer of Marketplace about debt in the system like this:

“The level of debt relative to GDP in the business sector is at a high level. However, so is the size of the business sector. So, actually, the business sector itself is not materially higher leveraged than it was. None the less, there are a lot of highly levered companies. And that’s the kind of thing that happens during a long cycle when there aren’t downturns. We’re now into our eleventh year, you do get that kind of phenomenon in a long cycle. That’s something we’re monitoring and I think our view still is that’s a real issue but what it really represents is a potential amplifier of a macro-economic downturn. It does not have the makings of anything that would undermine the workings of the financial system, for example, or could itself create a shock that would turn the economy down…”

That answer effectively pretends that 2008 never happened. Lending came to a frightening halt in 2008 because no one could predict with any clarity which Wall Street bank would fail next as a result of its own high leverage or its exposure to a highly levered borrower like Lehman Brothers, for example.

Chairman Powell, who spent most of the press conference answering questions from a written script in a folder on the podium, did let this one nugget slip out about highly levered businesses. Powell said “The Financial Stability Board is actually conducting a project right now to identify where these loans are held all around the world. So, it’s a subject of a lot of study and work and we’re trying to keep on top of it.”

The best way to keep on top of it is to look at what’s on and off the balance sheets at the mega Wall Street banks.

end

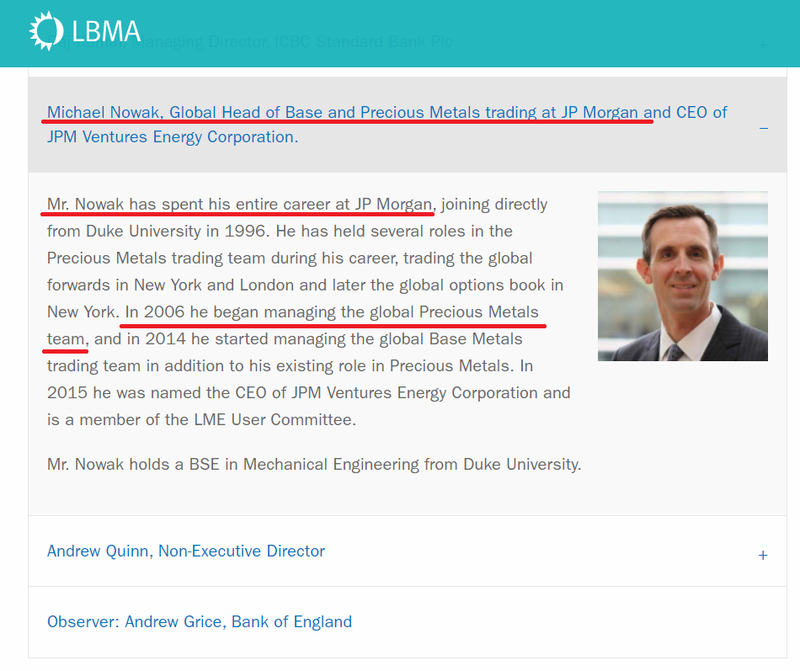

Late today:

GATA) LBMA removes JPMorgan board member after indictment

Submitted by cpowell on 03:55PM ET Friday, September 20, 2019. Section: Daily Dispatches

By Henry Sanderson

Financial Times, London

Friday, September 20, 2019

https://www.ft.com/content/22250f48-db9a-11e9-8f9b- 77216ebe1f17

The London Bullion Market Association has removed Michael Nowak, JPMorgan’s head of precious metals trading, from its board after he was indicted by the U.S. Department of Justice for a “massive, multi-year scheme” to manipulate the precious metals markets.

“In light of the ongoing investigation by the Department of Justice, the LBMA, under the terms of its Articles of Association, has removed Mr. Nowak from its board,” the LBMA said.

The indictment is an embarrassment for the LBMA, which represents London’s precious metals market and launched a code of conduct for its members in 2017.

Mr. Nowak’s name was no longer listed on the LBMA’s website as of today.

JPMorgan, along with HSBC, dominates gold trading in London and is one of the most powerful members of the LBMA.

Mr. Nowak was charged Monday along with two colleagues, Gregg Smith and Christopher Jordan, on federal racketeering charges normally used to take down organized crime syndicates.

The indictment alleged that the three traders engaged in “widespread spoofing, market manipulation, and fraud.”

They placed orders they intended to cancel before execution in an effort to “create liquidity and drive prices toward orders they wanted to execute on the opposite side of the market,” it alleged.

Mr. Nowak and Mr. Smith are on leave from JPMorgan, according to a person familiar with the matter, while Mr. Jordan has left the bank.

The Justice Department is also looking at other commodities and other banks, according to a person familiar with the matter.

JPMorgan is also one of the biggest traders of base metals such as aluminium.

A spokesman for JPMorgan declined to comment.

***

end

Gold-Rigging Scandal Hits The LBMA: JPMorgan’s Gold Manipulator Nowak Kicked Off LBMA Board

Submitted by Ronan Manly, BullionStar.com

Just when you think it couldn’t get any more embarrassing for JP Morgan’s precious metals business and its embattled head, Michael Nowak, it just did today as the powerful London Bullion Market Association (LBMA) moved to oust Nowak, who has become too toxic, from the LBMA’s board of directors.

According to the Financial Times:

“The London Bullion Market Association has removed Michael Nowak, JPMorgan’s head of precious metals trading, from its board after he was indicted by the US Department of Justice for a “massive, multiyear scheme” to manipulate the precious metals markets.

“In light of the ongoing investigation by the Department of Justice, the LBMA, under the terms of its Articles of Association, has removed Mr Nowak from its board,” the LBMA said.

The DoJ indictment is an embarrassment for the LBMA, which represents London’s precious metals market, and launched a code of conduct for its members in 2017.

Mr Nowak’s name was no longer listed on the LBMA’s website as of Friday.”

Toxic Board Member – Widespread Spoofing

As background, JP Morgan managing director and head of precious metals trading Nowak become too toxic to retain his seat on the LBMA Board from at least last Monday, when DoJ charged and unsealed an indictment against Nowak, JP Morgan precious metals trader Gregg Smith, and former JP Morgan precious metals trader Christopher Jordan for:

“alleged participation in a racketeering conspiracy and other federal crimes in connection with the manipulation of the markets for precious metals futures contracts, which spanned over eight years and involved thousands of unlawful trading sequences.”

In the words of the DoJ indictment, the three and and their co-conspirators allegedly engaged in:

“a massive, multiyear scheme to manipulate the market for precious metals futures contracts and defraud market participants”

“widespread spoofing, market manipulation and fraud while working on the precious metals desk” at JP Morgan “through the placement of orders they intended to cancel before execution (Deceptive Orders) in an effort to create liquidity and drive prices toward orders they wanted to execute on the opposite side of the market.

In thousands of sequences, the defendants and their co-conspirators allegedly placed Deceptive Orders for gold, silver, platinum and palladium futures contracts traded on the New York Mercantile Exchange Inc. (NYMEX) and Commodity Exchange Inc. (COMEX), which are commodities exchanges operated by CME Group Inc.”

In its charges, the DoJ used the severe Racketeer Influenced and Corrupt Organizations Act (RICO Act), charging each of Nowak, Jordan and Smith with one count of conspiracy under the RICO Act.

The background and details to the DoJ charges were explained in a BullionStar article on Tuesday titled “LBMA Board Member & JP Morgan Managing Director Charged with Rigging Precious Metals“, which also broken the news that Nowak was a board member of the powerful London Bullion Market Association (LBMA), an Association which is dominated by bullion banks such as JP Morgan, and an Association which is in the self-proclaimed words of the LBMA is the “the world’s authority on precious metals”.

Promoting a Fair, Effective and Transparent market

All through this week, Nowak’s continued role as a board member of the LBMA seemed strange in light of the DoJ charges, and stranger still that the LBMA claims that its Global Precious Metals Code that the Code:

“promotes a fair effective and transparent market. It provides market participants with Principles and Guidance to uphold high standards of business conduct. All of this creates confidence in the market for all participants”

More specifically, the LBMA’s Global Precious Metals Code states that:

“Market Participants should not engage in trading strategies or quote prices with the intent of hindering market functioning or compromising market integrity.”

“Such strategies also include collusive and/or manipulative practices, including but not limited to those in which a trader enters a bid or offer with the intent to cancel before execution (sometimes referred to as “spoofing”, “flashing” or “layering”) and other practices that create a false sense of market price, depth or liquidity.”

On Tuesday, we therefore wondered:

“how does the LBMA explain that one of its Board of Directors has been charged in US Federal Courts of these very practices, using the RICO Act, an act that was created to take down mafia mobsters?”

while also asking:

“Will the LBMA remove Nowak from its Board of Directors? Will the LBMA reprimand or expel JP Morgan from its membership list?

LBMA in discussions with JP Morgan

As the week progressed and the world’s financial media continued to cover the story, there was still no word out of the LBMA as to how it would react, if at all to the Michael Nowak story. This then promoted the Financial Times on Friday morning to ask the LBMA what it intended to do about the indictment of Nowak, one of its board members, to which the LBMA responded that it was merely in ‘discussions’ with JP Morgan.

According to the FT’s early story:

The London Bullion Market Association is in “discussions” with JP Morgan after its board member was indicted by the US Department of Justice for a “massive, multiyear scheme” to manipulate the precious metals markets.

The LBMA said that it had not made any decision to remove Michael Nowak, JP Morgan’s head of precious metals, from its board. “We are still in discussions with JP Morgan,” Aelred Connelly, a spokesmas for the LBMA, said.

The DoJ indictment is an embarrassment for the LBMA, which represents London’s precious metals market, and launched a code of conduct for its members in 2017. JP Morgan, along with HSBC, dominates gold trading in London, and is one of the most powerful members of the LBMA.

“People are shocked that an LBMA board member is at the centre of the DoJs case, and in disbelief that Nowak is still, according to the LBMA website, listed as a LBMA board member,” Ronan Manly, a precious metals analyst at BullionStar in Singapore, said.

“The LBMA board sits above the entire LBMA governance structure, so even though the DoJ case is allegation at this stage, it taints the LBMA.”

Nowak’s Bio removed from LBMA website

What exactly went down in the ‘discussions’ between LBMA and JP Morgan today is not clear, but within a few hours after the Financial Times’ initial story, the LBMA released a statement to the FT saying that:

“In light of the ongoing investigation by the Department of Justice, the LBMA, under the terms of its Articles of Association, has removed Mr Nowak from its board.”

At the same time the LBMA quietly removed Michael Nowak’s bio from its board of directors page. The previous version of the LBMA Board members page, including Nowak, can be seen here. The new updated version where all references to Nowak have been removed, can be seen here.

Now that the LBMA has made its move, can the London Metal Exchange (LME) be far behind? For the same Michael Nowak, who is head of both base metals and precious metals trading at JP Morgan, is also on the LME ‘User Committee’ as can be seen on the LME website here, and in case the page changes, a Wayback Machine archive from today can be seen here.

Conclusion

All that remains for now is for Michael Nowak’s defense lawyer, David Meister of law firm Skadden, Arps, Slate, Meagher & Flom, the same Meister who was former Director of Enforcement for the CFTC from November 2010 to October 2013 under then chairman Gary Gensler, to show how he is going to get Nowak off the hook on this one.

While he’s at it, Meister needs to also explain how there is not a conflict of interest in representing Nowak, when the CFTC closed down an investigation into the manipulation of the silver markets in October 2013, an investigation that had been running since September 2018, saying that there was:

“not a viable basis to bring an enforcement action with respect to any firm or its employees related to our investigation of silver markets.“

And finally, does David Meister sleep soundly at night representing an alleged criminal enterprise of market manipulation at Jp Morgan, knowing that in July 2013, Meister stated in another CFTC enforcement case that:

“While forms of algorithmic trading are of course lawful, using a computer program that is written to spoof the market is illegal and will not be tolerated. We will use the Dodd Frank anti-disruptive practices provision against schemes like this one to protect market participants and promote market integrity, particularly in the growing world of electronic trading platforms.”

iii) Other physical stories:

Always listen to Egon Von Greyerz

(courtesy Good as Gold/Australia/Von Greyerz)

EGON VON GREYERZ INTERVIEWED BY AS GOOD AS GOLD AUSTRALIA: GOLD TO REACH $10,000 – PROPERTY PRICES TO COLLAPSE

September 20, 2019 by Egon von Greyerz

In this interview, Brian & Darryl Panes from As Good As Gold Australia speak with Egon von Greyerz who confirms the world is running on empty.

Governments and Central Banks are panicking, having used up all their arsenal – massive money printing and hyperinflation lies ahead.

Gold at US$10,000 per ounce is just a starting point. Property values to lose 95% of their value relative to Gold. Preservation of wealth is vital, as we enter a period of extreme volatility with interest rates surging after a 5,000 year historical low.

Also:

- Gold now starting the next leg of a massive bull market.

- Gold going from west to east – West to run out of Gold.

- Australia’s property market, is massive bubble.

- Worldwide banking crisis in the making.

- People have no savings, all destroyed by governments.

- Central banks across the globe committed to money printing.

- Bond market is biggest bubble ever, will trigger the biggest collapse the world has ever seen.

- USD is the sickest of all currencies, only supported by debt and military.

- Debt needs to implode so world can grow soundly again.

- Gold severely suppressed, will explode to very high levels.

- COMEX failure, will result in a run on physical metals.

- Don’t sell any gold or silver for a very long time.

Egon von Greyerz is a Keynote speaker at the “Gold and Alternative Investment Conference” in Sydney, Australia on October 24-26. 2019.

EGON VON GREYERZ INTERVIEWED BY AS GOOD AS GOLD AUSTRALIA: GOLD TO REACH $10,000 – PROPERTY PRICES TO COLLAPSE

Egon von Greyerz

Founder and Managing Partner

Matterhorn Asset Management

Zurich, Switzerland

Phone: +41 44 213 62 45

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Futures Frozen With $8.3 Billion Expiring At S&P 3,000 On Quad-Witching Friday

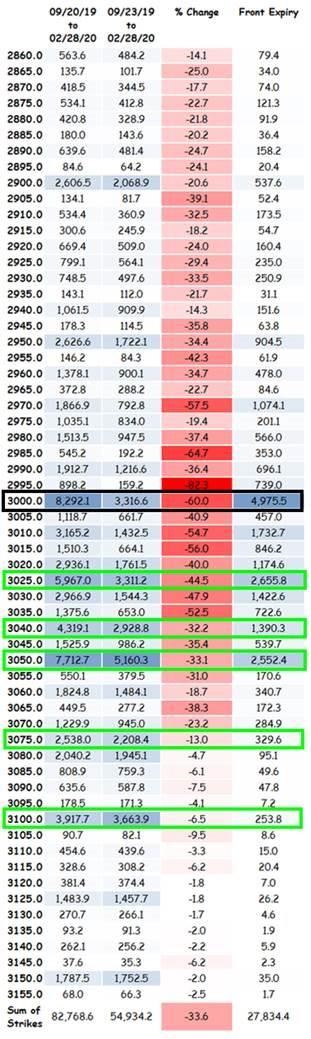

One week after Friday the 13th, a far more important for the market Friday has arrived: quad-witching day, when once every quarter we get the simultaneous expiration of contracts for index futures, index options, stock options, and single stock futures, and when increased volatility and an explosion in volumes usually follow. As such, these days are entirely at the mercy of dealer and trader positioning, and as Charlie McElligott pointed out yesterday, as of this moment the S&P is “shackled” by a “Long Gamma” death-grip, with some $8.3BN in expiration at the 3,000 strike, which will ensure that the S&P gravitates around 3,000 for most of the day.

Sure enough, overnight markets were largely uneventful, with European and Asian stocks climbing modestly on Friday as a busy week of central bank meetings drew to a close, while US equity futures traded up a modest 5 points to 3,013 with focus now likely to shift back to the trade war. Treasuries initially edged higher for a fifth day as dollar droped, but the entire move has since reversed.

Despite the “gamma gravity” pin, FOMC volatility, USD repo market stress and mixed macro numbers, US equities are managing to hold the line close less than 1% from a record high, while Europe’s Stoxx Europe 600 Index rose as much as 0.3%, poised for its highest close since May 2018, led higher by the more defensive and bond yield-sensitive telecom, healthcare and utilities sectors: Novartis was +1.3% after sales of its Cosentyx rose 1.7%. Oil stocks, including Total, Shell also climbed, with Brent heading for biggest weekly increase since January as traders wait to see whether Saudi Arabia can fulfill promises to swiftly repair a critical processing facility attacked last weekend

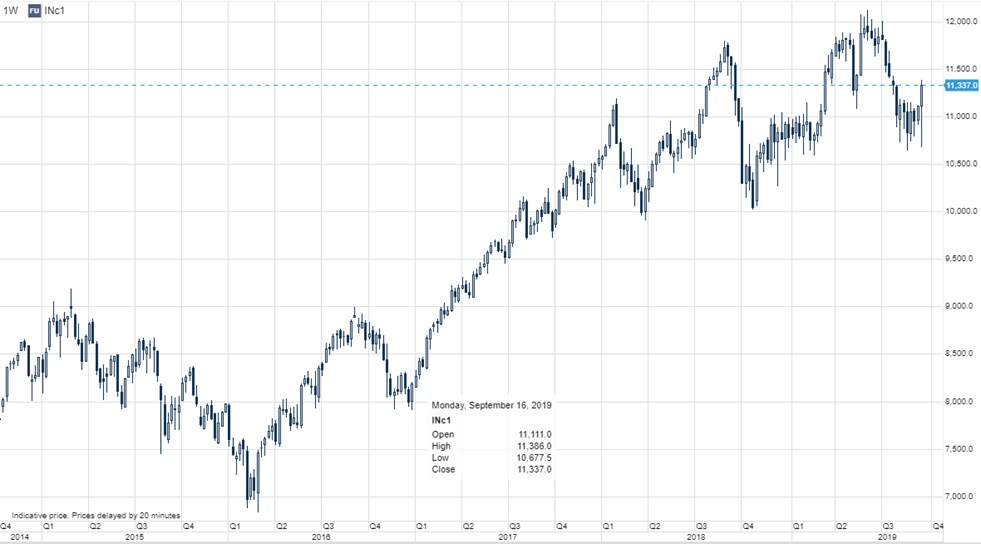

Earlier in the session, Asian stocks climbed after a four-day losing streak, as health care and technology firms led gains in a week packed with monetary policy decisions. Most of the major markets in the region were up, with India’s stock benchmark poised for its biggest jump in a decade after the government unexpectedly slashed the corporate tax rate to boost economic growth. As Saxo Bank notes, “India is a train wreck with credit worsening and consumer confidence measured by new car registrations plummeting. However, today news broke that the Indian government is stimulating the economy through cutting the corporate taxes for new domestic companies. The Nifty 50 Index was up 4% breaking above the recent trading range but in the greater picture (see chart) the technical picture looks ugly. As long as the global economy is slowing down and the USD remains strong India is an equity market investors should underweight.”

The Topix pared earlier gains and closed little changed as advances in health care stocks were offset by declines in utilities and industrial shares. The Shanghai Composite Index edged 0.2% higher, with Jiangsu Hengrui Medicine and Kweichow Moutai among the biggest boosts.

China’s move higher was despite trader disappointment in the latest PBOC easing as analysts called for stronger monetary stimulus from Beijing after China’s new gauge of borrowing costs – the Loan Prime Rate – was only slightly lowered Friday, from 4.25% to 4.20% for the 1 year rate, and kept unchanged at 4.85% for the 5 year rate which is likely to be used for mortgages, despite expectations for a modest cut. The boost to economic activity is expected to be slight. The rate is for banks’ best customers and total reductions so far, of 11 bps, are less than half of the Fed’s quarter-point rate cut on Thursday, reflecting Chinese policymakers’ concerns that much-cheaper credit could lead to unproductive investment and property bubbles.

“Since the new rate is relatively untested, the PBOC (People’s Bank of China) appears to be taking a measured approach at first,” Julian Evans-Pritchard, senior China Economist at Capital Economics, said in a note. “However, with economic activity likely to come under further pressure in the coming quarters and monetary easing so far failing to generate much of a pick-up in credit growth, we think the PBOC will need to start engineering larger declines before long.”

The move was far smaller than easings by the U.S. Federal Reserve and the European Central Bank over the past week, suggesting Chinese policymakers remain reluctant to join a global stimulus wave due to worries about mounting debt. Still, analysts say Beijing’s restraint is being put to the test, as worsening economic data in August has raised fears that third-quarter growth could slip below 6%, breaching the lower end of the government’s 2019 target. With higher U.S. tariffs looming, many China watchers believe more forceful measures will be needed soon to avoid a sharper slowdown.