GOLD::$1523.85 UP $16.25 (COMEX TO COMEX CLOSING)

Silver:$18.63 UP 80 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1522.10

silver: $18.64

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

Ted Butler….

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,507.300000000 USD

INTENT DATE: 09/20/2019 DELIVERY DATE: 09/24/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

737 C ADVANTAGE 2 1

____________________________________________________________________________________________

TOTAL: 2 2

MONTH TO DATE: 1,743

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 2 NOTICE(S) FOR 200 OZ (0.00622 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1743 NOTICES FOR 174,300 OZ (5.4214 TONNES)

SILVER

FOR SEPT

36 NOTICE(S) FILED TODAY FOR 180,000 OZ/

total number of notices filed so far this month: 8643 for 43,215,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE : $ 9940 DOWN 87

Bitcoin: FINAL EVENING TRADE: $ 9802 DOWN 224

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A FAIR SIZED 765 CONTRACTS FROM 211,198 UP TO 211,963 WITH THE 3 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0,; DEC 1050 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1050 CONTRACTS. WITH THE TRANSFER OF 1050 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1050 EFP CONTRACTS TRANSLATES INTO 5.25 MILLION OZ ACCOMPANYING:

1.THE 3 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.300 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE

WE AGAIN HAD ATTEMPTED COVERING OF BANKER SHORTS AT THE SILVER COMEX YESTERDAY BUT TO NO AVAIL

AS THE TOTAL OPEN INTEREST IN BOTH EXCHANGES RISE BY A GOOD AMOUNT.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

26,625 CONTRACTS (FOR 15 TRADING DAYS TOTAL 26,625 CONTRACTS) OR 133.125 MILLION OZ: (AVERAGE PER DAY: 1775 CONTRACTS OR 8.875 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 133.125 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.01% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1682.73 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 667, WITH THE 3 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1050 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 1815 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1050 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 765 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH JUST A 3 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.83 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!! (also strange, the final oi numbers in silver is higher than the preliminary numbers//go figure)

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.059 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 36 NOTICE(S) FOR 180,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.300 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 2884 CONTRACTS, TO 634,985 ACCOMPANYING THE $8.60 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// FRIDAY// / THE TOTAL GOLD OPEN INTEREST IS CREEPING UP AND CLOSE TO THE RECORD OF 652,971 IN 2016.

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 9666 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 9666 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 634,985,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,550 CONTRACTS: 2884 CONTRACTS INCREASED AT THE COMEX AND 9666 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 12,550 CONTRACTS OR 1,255,000 OZ OR 39.03 TONNES. FRIDAY WE HAD A GAIN OF $8.60 IN GOLD TRADING….

AND WITH THAT STRONG GAIN IN PRICE, WE HAD A VERY STRONG GAIN IN GOLD TONNAGE OF 39.03 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME AND OPEN INTEREST ARE HUGE. THEY WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE LONGS AND AS YOU CAN SEE, THE TOTAL OPEN INTEREST IN BOTH EXCHANGES SKYROCKETED

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 108,254 CONTRACTS OR 10,825,400 oz OR 336.71 TONNES (15 TRADING DAY AND THUS AVERAGING: 7042 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAYS IN TONNES: 336.71 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 336.71/3550 x 100% TONNES =10.05% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4488.31 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 2884 WITH THE STRONG PRICING GAIN THAT GOLD UNDERTOOK FRIDAY($8.60)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9666 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9666 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG SIZED GAIN OF 12,550 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9666 CONTRACTS MOVE TO LONDON AND 2884 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 39.03 TONNES). ..AND THIS STRONG INCREASE OF DEMAND OCCURRED WITH THE GAIN IN PRICE OF $8.60 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 2 notice(s) filed upon for 200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $16.25 TODAY//(COMEX-TO COMEX)

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD..

A MONSTROUS PAPER DEPOSIT OF 10.55 TONNES OF NON EXISTENT GOLD.

INVENTORY RESTS AT 894.15 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 80 CENTS TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 375.473 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 765 CONTRACTS from 211,198 UP TO 211,963 AND CLOSER TO A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1050: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1050 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 765 CONTRACTS TO THE 1050 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 1815 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 9.075 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 43.300 MILLION OZ//

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 3 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1050 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED DOWN 27.37 POINTS OR 0.98% //Hang Sang CLOSED DOWN 213.27 POINTS OR 0.81% /The Nikkei closed UP 34.64 POINTS OR 0.16%//Australia’s all ordinaires CLOSED UP .32%

/Chinese yuan (ONSHORE) closed DOWN at 7.1262 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1262 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1197 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

SOUTH KOREA

This is a huge Bellwether on global growth: South Korea exports collapse 21%, it biggest drop in a decade

(zerohedge

3b) REPORT ON JAPAN

3C CHINA

i)China cancels the Montana and Nebraska trip saying that they did not want to interfere in USA politics. The negotiations are back on but there is no hope of a deal.

(zerohedge)

ii)The Chinese government taps on the shoulder of Chinese firms to rein in global purchases. They have now turned net seller for the first time in decades

(zerohedge)

4/EUROPEAN AFFAIRS

i)UK

the engine for Europe is Germany and we are continually reporting bad numbers. Today, it is the biggy, the PMI and the German mfg PMI plunges to a 7 year low

(zerohedge)

v)Bill Blain has an interesting read on the devastation in the aero space/holiday industry

(Bill Blain)

7. OIL ISSUES

Conflicting stories sent oil higher and then lower. First a Wall Street Journal report stated that it would take Saudi Arabia 8 moths to fix their hit on Aramco but that was refuted later and saying that they would be restored by the end of the month

(zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)The strange events that led to the removal of Nowak from the lBMA board. It is not immediate. It was 4 days after the fact

(Chris Powell/GATA)

ii)Chris Powell correctly states that gold/silver manipulation goes far beyond JPMorgan

(courtesy Silver Doctors/GATA)

iii)A terrific interview although short, Gold Money’s Alasdair Macleod reviews the evidence of strain in the entire ban

(Kingworldnews/Alasdair Macleod)

iv)The New Orleans conference will be extremely important for you to attend..as there is so much going on. The conference will explain everything in detail as to what is going on

(GATA/Chris Powell)

v)Martin Katusa tries to explain why negative rates are good for gold

(Martin Katusa)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

iii) Important USA Economic Stories

a)As promised, Trump did nothing wrong and this “whistle blower” story just blew up in all of the Dems faces

(courtesy Red State/Bonchie)

and thanks to Robert H for sending this to us.

b) zerohedge on the same subject as above

c)I guess when I say it nobody would listen, but when Goldman Sachs gives an ominous warning about the stock market chaos all should listen

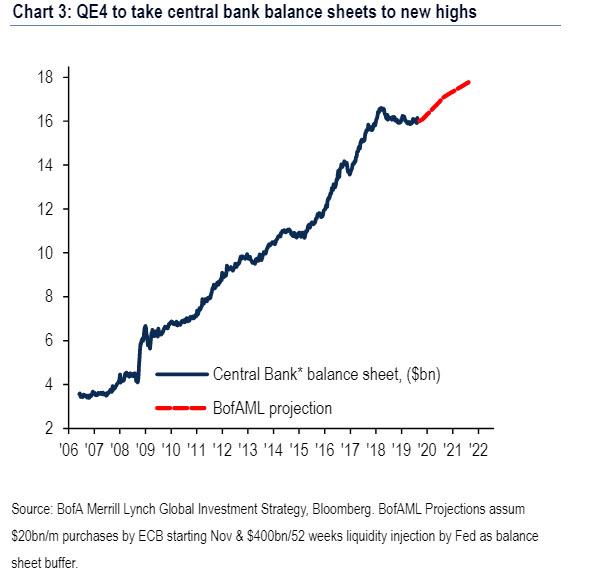

d)This one is a biggy!! Part 1 Simon Potter was the former head trader at the NY Fed and was surprisingly dumped by head honcho Williams (who has no experience whatsoever in the handling of the “plumbing system” at the New York Fed). Potter has now commented that the Fed has to buy initially at least another 400 billion dollars of POMO (QE4) to unclog the clot. The Fed’s balance sheet must rise by 750 billion dollars over two years and the excess reserves at the banking system must initially rise from 1.4 trillion dollars to 1.8 trillion dollars.

\(zerohedge)

g) E cigarette company Juul is now under criminal investigation by the Feds as they are facing an FTC probe as well as an FDA

h)Peter Schiff delivers a terrific video//commentary as to what is going on. He correctly states that the Fed in 2011 gave us the illusion that they were going to unwind all of their new additions of bonds from the balance sheet. Once the illusion ends, we basically have QE to infinity as that is the only thing capable of holding up asset prices. This is why gold will continue on its northerly journeya must view..

(courtesy Peter Schiff/zerohedge)

iv) Swamp commentaries)

As promised, Trump did nothing wrong and this “whistle blower” story just blew up in all of the Dems faces

(courtesy Red State/Bonchie)and thanks to Robert H for sending this to us.

plus 4 other commentaries on the same subject

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

THE BANKERS SUPPLIED THE NECESSARY AND INFINITE AMOUNT OF SHORT PAPER IN GOLD. THE BANKERS FAILED IN THEIR ATTEMPT AT CONTAINING GOLD’S PRICE AS IT ROSE BY $8.60. , THE CROOKS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE LONGS FROM THEIR OI POSITIONS. THE OPEN INTEREST WILL RISE APPRECIABLY FOR TUESDAY’S READING AS GOLD /SILVER ROSE CONSIDERABLY IN THE ACCESS MARKET ON FRIDAY AFTERNOON.

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 482.265 oz oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 124,457 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 61,282 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 61282 CONTRACTS EQUATES to 306 million OZ 43.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.52% ((SEPT 23/2019)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.58% to NAV (SEPT 23/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -2.52%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.48 TRADING 15.03/DISCOUNT 2.88

END

And now the Gold inventory at the GLD/

SEPT 23/WITH GLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 24/2019/ Inventory rests tonight at 894.15 tonnes

*IN LAST 669 TRADING DAYS: 41.19 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 569- TRADING DAYS: A NET 125.42 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ//

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

SEPT 23/2019:

Inventory 375.473 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.12/ and libor 6 month duration 2.04

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .08

XXXXXXXX

12 Month MM GOFO

+ 2.05%

LIBOR FOR 12 MONTH DURATION: 2.06

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.01

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold Gains 0.8%, Silver 3.4% As Stocks Fall on Bad EU Data and Oil Gains On Middle East Concerns

NEWS and COMMENTARYGold gains on Middle East tensions; palladium hits record highGloomy European Data Hits Stocks as Bonds AdvanceOil gains more than 1% on Saudi supply doubts, Mideast tensionsIran warns it will ‘destroy aggressors’ after US troop announcementUK households’ financial worries hit five-year high: IHS MarkitGerman Industrial Recession Drags Economy Deeper Into Slump

Stocks Going Nowhere in an Interesting Way – Hussman

China’s Golden Corridor – Gold Reserves And Negative Yield

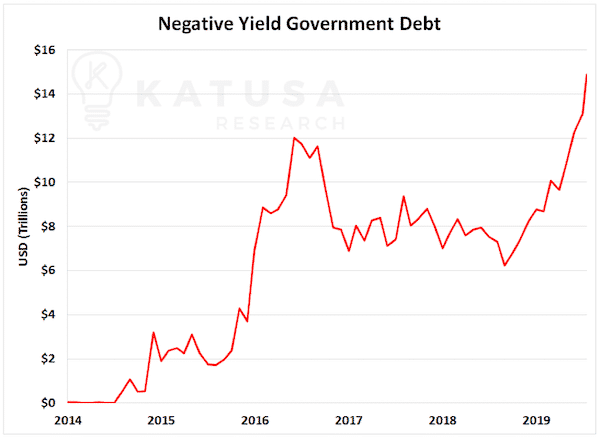

Repo Market’s Liquidity Crisis Has Been a Decade in the Making

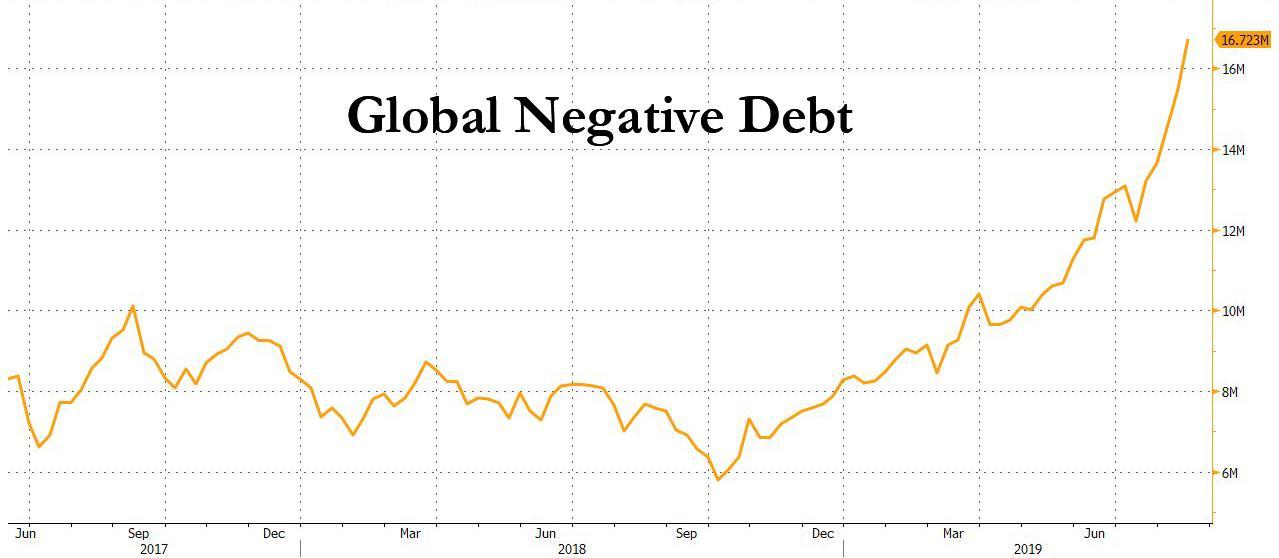

BIS Warns Of Financial Disaster Amid $17 Trillion In Negative-Yield Debt

Gold is “the most compelling form of potential hedge” – First Eagle

“We believe gold’s underlying long-term price stability, versatility, resilience, countercyclical relationship to stocks and duration make it the most compelling form of potential hedge.”

Thomas Kertsos of First Eagle

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

20-Sep-19 1504.10 1501.90, 1199.07 1203.62 & 1361.06 1362.52

19-Sep-19 1498.40 1500.70, 1200.67 1201.76 & 1354.85 1357.08

18-Sep-19 1502.20 1503.50, 1206.27 1204.90 & 1360.39 1359.92

17-Sep-19 1499.30 1502.10, 1208.89 1207.24 & 1361.51 1360.45

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

10-Sep-19 1494.60 1498.25, 1211.52 1211.34 & 1353.51 1357.11

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

The strange events that led to the removal of Nowak from the lBMA board. It is not immediate. It was 4 days after the fact

(Chris Powell/GATA)

Imagine what might happen if the FT asked more critical questions

Submitted by cpowell on Sat, 2019-09-21 15:41. Section: Daily Dispatches

11:53a ET Saturday, September 21, 2019

Dear Friend of GATA and Gold:

Why did the London Bullion Market Association drop JPMorganChase commodity trading desk chief Michael Nowak from its board of directors this week?

Probably not because Nowak was indicted by the U.S Justice Department, accused of racketeering with other Morgan traders in part of the longstanding manipulation of the monetary metals markets. For the indictment was announced Monday and the LBMA did not drop Nowak until Friday.

…

More likely the LBMA dropped Nowak because a major financial news organization, the Financial Times, asked the LBMA about Nowak on Friday.

How did the FT’s query come about?

It came about by fortunate happenstance arising from the work of Bullion Star gold researcher Ronan Manly.

Here’s the chronology of events.

The indictment was announced Monday:

http://www.gata.org/node/19445

In a post on Bullion Star on Tuesday that was quickly distributed by GATA, Manly disclosed Nowak’s position with the LBMA:

http://www.gata.org/node/19453

Meanwhile the Financial Times was researching a story about investors moving their gold from politically turbulent Hong Kong to Singapore. In the course of that research a reporter for the FT contacted Bullion Star proprietor Torny Persson, since Bullion Star operates a metals vault in Singapore.

The FT’s inquiry about metals vaulting prompted Persson to suggest to Manly that he send the FT reporter his report on Nowak’s position with the LBMA. Manly did so and the FT reporter on the Singapore story forwarded it to another FT reporter.

On Thursday the second FT reporter contacted Manly, and on Friday morning the newspaper published a story saying the LBMA was having “discussions” with JPMorganChase about Nowak. A photocopy of part of that story is here:

http://www.gata.org/files/FT-LBMA-Nowak-Story1-09-20-2019.jpeg

Four and a half hours later that story was removed from the FT’s internet site and replaced with a story reporting Nowak’s removal from the LBMA board:

http://www.gata.org/node/19466

Both FT stories described Nowak’s indictment as an “embarrassment” for the LBMA. But of course it would have been no embarrassment at all if Bullion Star’s Manly had not made an issue of it and prodded the FT to report it, since few people would have known about Nowak’s connection to the LBMA otherwise.

Such is the power of the press. It can trigger conscience, insofar as conscience is, as H.L. Mencken wrote, “the inner voice that warns us someone may be looking.”

Except for Manly, Bullion Star, and the inquiry from FT, Nowak might have remained on the LBMA board despite his indictment, the LBMA being barely less a criminal organization than JPMorganChase.

The point here is to imagine what might happen if the Financial Times, other news organizations, and those who purport to be market analysts started putting a few critical questions to governments, central banks, and investment houses about their surreptitious activity in the monetary metals markets.

What if, for example, such news organizations and analysts pressed the U.S. Treasury Department, Federal Reserve, and Commodity Futures Trading Commission for answers to the questions long posed to them by GATA and U.S. Rep. Alex X. Mooney but ignored? That is, which markets is the U.S. government secretly trading in and what is the purpose of that trading? Does the CFTC have jurisdiction over manipulative trading by the government or brokers working for the government, or is such manipulative trading legal, authorized by the Gold Reserve Act of 1934?

What if those news organizations and analysts made a big deal of the refusals to answer?

What if news organizations and analysts pressed the Bank for International Settlements to answer GATA’s questions about the bank’s surreptitious trading in gold and gold derivatives and made a big deal about the bank’s refusal to answer?

In that case the institutions being questioned might suffer actionable embarrassment just as the LBMA did this week.

But of course there can be no embarrassment when nobody is watching.

That is why, powerful as governments and central banks are with their ability to create and dispose infinite money, their greatest advantage long has been something else: the cowardice or corruption of mainstream financial news organizations and market analysts.

For as Mark Twain wrote, the human race “in its poverty has unquestionably one really effective weapon — laughter. Power, money, persuasion, supplication, persecution — these can lift at a colossal humbug, push it a little, weaken it a little, century by century. But only laughter can blow it to rags and atoms at a blast. Against the assault of laughter nothing can stand.”

The pious fraud of modern central banking will stand until news organizations stop being pious frauds themselves. Then the world will change.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

END

Chris Powell correctly states that gold/silver manipulation goes far beyond JPMorgan

(courtesy Silver Doctors/GATA)

Gold manipulation goes far beyond JPM, GATA secretary tells Silver Doctors

Submitted by cpowell on Sat, 2019-09-21 19:08. Section: Daily Dispatches

3:07p ET Saturday, September 21, 2019

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed this week for Silver Doctors and SD Bullion by James Anderson, discussing the new indictments of JPMorganChase monetary metals traders and the far bigger market manipulations behind the ones attributed to the investment bank. The interview can be heard at SDBullion.com here:

https://sdbullion.com/blog/jp-morgan-gold-rigging-a-fraction-of-the-stor…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A terrific interview although short, Gold Money’s Alasdair Macleod reviews the evidence of strain in the entire ban

king system

(Kingworldnews/Alasdair Macleod)

iii) Other physical stories:

Martin Katusa tries to explain why negative rates are good for gold

(Martin Katusa)

China’s Golden Corridor – Gold Reserves And Negative Yield

Authored by Marin Katusa via InternationalMan.com,

Earlier this year, gold prices hit all-time highs in most major currencies.

The British Pound… the Canadian Dollar… the Australian Dollar… the Indian Rupee… the Japanese Yen… the Chinese Yuan… the South African Rand… and more.

It also broke above $1,500 in dollar terms. The highest it’s been in 6 years.

This shouldn’t come as a total surprise…a trade war between global economic powers, global debt spiraling out of control…

Iran and North Korea building up weapons…

The world is in uncharted waters.

Are the chickens going to come home to roost?

Today I’ll share a few of the major key themes that every investor needs to be aware of right now.

The Chinese Yuan is in Freefall

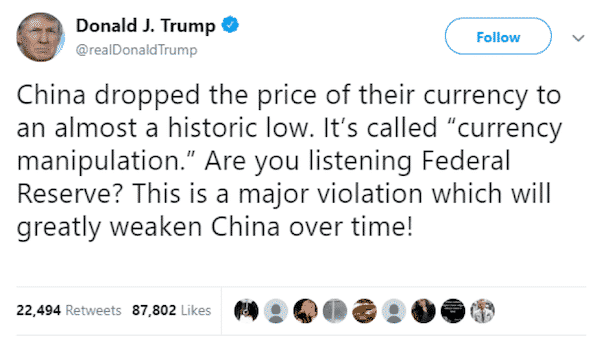

Given the recent onslaught of tweets from Donald Trump, you’d think the Chinese Yuan had just started falling.

In reality though, the Yuan has been depreciating since 2014.

This trend was further magnified when the Chinese government let the Yuan fall below its symbolic threshold of 7 Yuan per U.S. dollar.

When this happened, the #POTUS tweeting machine went out in full force, labeling China a currency manipulator.

Below is a chart which shows the historical exchange rate between the Yuan and the U.S. dollar.

Currency devaluation aside, it makes a lot of sense to own assets which hold their value.

Physical assets like gold, art and vintage wine all make for excellent hedges against currency devaluation.

But it’s tough for major institutions or governments to buy enough art or wine to truly protect themselves. This leaves gold as the number one acquisition.

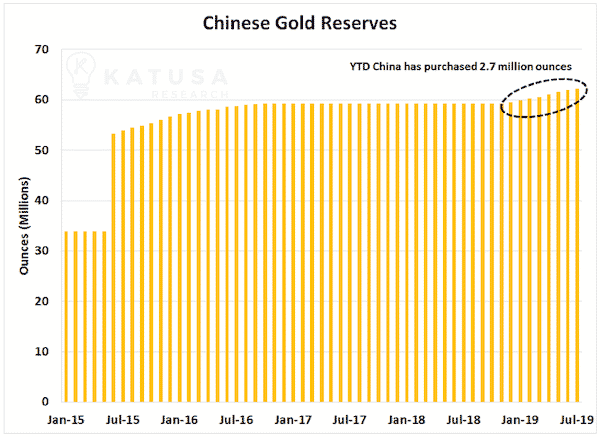

It should come as no surprise that central banks have been very active in buying gold.

Especially China’s…

The Chinese Central Bank is Buying TONS of Gold

And I mean that literally.

Just so far this year, the Chinese have acquired 2.7 million ounces (92.5 tons) of gold. Using a spot price of $1,500, that’s $4 billion worth of bullion.

Below is a chart showing Chinese Gold Reserves.

As a country focused on exporting more than it imports, it’s no surprise China wants to keep its currency value low. I could see the Chinese accumulating more gold over the coming months if their currency continues to weaken due to the trade war.

The U.S.-China trade war has not only impacted the American and Chinese economies, but the entire pattern for global trade as well.

Leading global economic indicators like national Purchasing Manufacturing Indexes have only recently begun to nosedive. And this could easily be just the tip of the iceberg.

To make matters worse, it’s getting harder and harder to find somewhere safe to park cash.

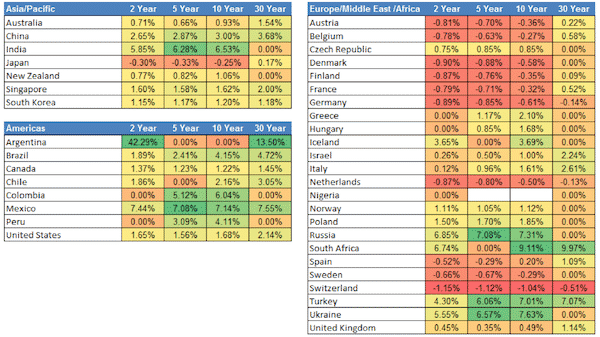

In times of chaos, government bonds are usually a standard go-to investment.

However, times are changing.

Right now, many government bonds actually have a negative yield.

You read that right – if you invest $100 into negative yield or a government bond in almost any European nation, you’re going to get back less than $100 in 10 years’ time.

How crazy is that?

Below is a table which shows the current yields on government bonds in nations around the world. The darker the red, the more negative the yield.

I don’t see this changing anytime soon either.

I believe there’s more devaluation to come.

Below is a chart which shows the soaring amount of negative yield government debt. It has recently surpassed $15 trillion.

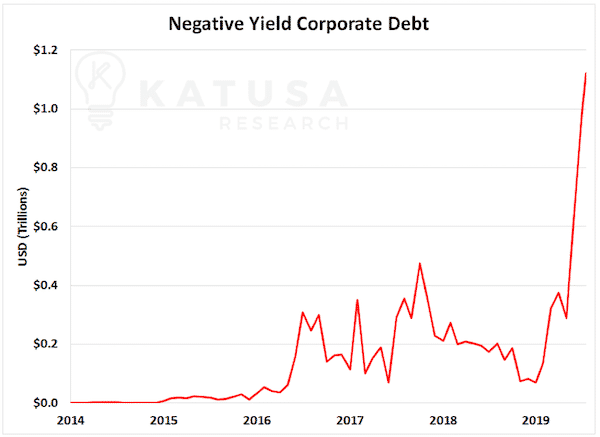

More alarming is the amount of corporate debt that has also hit negative yield. Currently there is over $1.2 trillion in negative yield corporate debt.

Just a few years ago there was virtually none. Below is a chart showing this dramatic increase.

Unquestionably there is blood in the streets of the bond market. Investors have no choice but to look for other places as stores of value.

That’s when investors look to the famous “pet rock” and “barbarous relic” for some wealth protection.

After all, it’s that or slowly lighting your money on fire buying bonds in countries with negative interest rates.

With bond yields the least attractive they’ve been in years, investors and central banks are turning to gold.

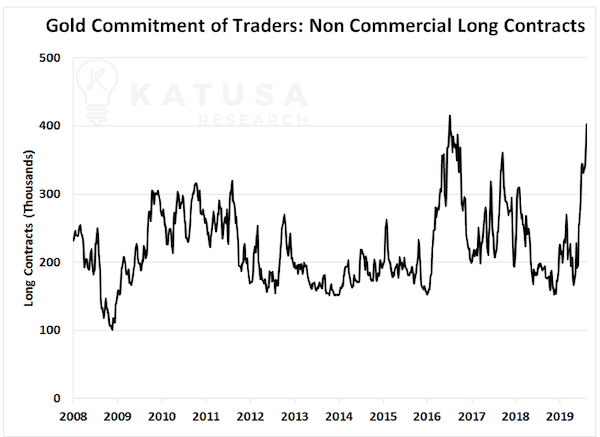

And with the recent surge in the Commitment of Traders long positioning and the price of gold smashing through $1,500… many pundits are saying “THIS IS IT!”

The technical chartists are all coming out with their best head and shoulders, bull flag, sliding wedge and upside-down watermelon patterns that determine the next leg up in gold.

To be honest, I couldn’t care less what the talking heads say their target price is.

From a fundamental perspective gold is very strong right now.

With nearly two decades of experience managing a fund focused on the commodity sector… I know that being positioned in the best gold developers and gold producers offers tremendous leverage to rising gold prices.

My subscribers and I are up over 100% on one of my strongest conviction investments so far this year.

Many of our other positions are up over 50% so far this year. Our portfolio is incredibly well positioned to profit from the global market chaos.

The unrest in China, the trade war and the rise of negative yield debt aren’t likely to be cleanly resolved anytime soon.

And in the meantime, many will flock to the safest haven they know – gold.

* * *

Negative interest rates are spreading like wildfire around the world. Investors have no choice but to look for other places as stores of value. That’s why many smart investors are running towards gold. It’s also why the big buyers, like China and Russia, are accumulating as much gold as possible. Here’s the bottom line… Negative interest rates and the devaluation of currencies will hurt a lot of people, particularly savers and retirees. But they will also give rocket fuel to the coming bull market in precious metals. That’s precisely why legendary speculator Doug Casey and resource expert Marin Katusa just released an urgent video on this topic. Doug and Marin breakdown exactly what is coming, and what you can do about it. Click here to watch it now.

LAWRIE WILLIAMS: Russia continues gold purchases but volume down yoy

Russia adds 12.44 tonnes of gold to its official reserves. Russia produces around 210 tonnes of gold per year or 17.5 tonnes. No gold ever leaves Russia so no official gold was bought from outside.

The Russian central bank has announced the purchase of another 400,000 ounces (12.44 tonnes) of gold in August for its gold reserves. This brings its total holding to around 2,230 tonnes keeping it in fifth place among national holders of gold, and closing in on France and Italy – currently in 4th and 3rd places in terms of reserves as reported to the IMF, with respective holdings of around 2,436 and 2,452 tonnes. Of course many believe that China is actually higher than all these in terms of gold held as against the 1,936.5 tonnes it reports to the IMF as it has a track record of holding additional gold in accounts it claims are not reportable to the IMF. Be that as it may, if Russia keeps up gold purchases at the current rate it could surpass the French and Italian holdings within the next 18 months.

However there is some evidence that Russia may be cutting back its annual rate of gold purchasing, although it remains in first place in terms of annual central bank gold reserve increases. For the past three years it has accumulated 200 tonnes of gold each year, or more, but this year seems to be heading for purchases of perhaps 180 tonnes or less. So far this year Russia has added around 118 tonnes of gold to its reserves and, at the current rate, it looks like it may add a further 50 tonnes by the year end bringing this year’s total to perhaps 170 tonnes. Last year the nation added some 275 tonnes to its gold reserves, so this year’s likely accumulations represent a big cut. Although it should be noted that last year’s gold accumulation coincided with a particularly big drop in U.S. dollar related securities.

Russia has been running down its holdings of U.S. dollar-related Treasuries as a protection against a possible U.S.-instigated asset freeze as part of the latter’s ongoing and escalating, sanctions programme. The build-up in gold reserves is presumably an integral part of this process. In terms of gross value the Russian gold accumulations also look to have been a smart value move given the advance in the gold price so far this year to in excess of $1,500 an ounce, around a 25% increase over the past 12 months.

Russia also seems to be increasing its annual gold output as the world’s third largest producer of the yellow metal with an annual ouput estimated at 300 tonnes or more. It may even have aims of surpassing both the world’s No.1 (China) and No.2 (Australia) in terms of annual gold output over the next few years, given China’s gold production appears to be in a downwards phase largely due to stricter environmental controls being applied to the country’s mining operations. However, Australia’s gold output, although only a few tonnes in excess of Russian production, is also rising – it has also recently recorded a new record annual figure (see: Australian gold output hits new record) so there is something of a race to the top in progress, while China may not give up its No.1 producer crown without a fight. All three nations are likely to end up with 2019 annual gold production figures of between 300 and 400 tonnes, but retain their respective producer positions for the current year at least.

22 Sep 2019

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

US Futures, Global Markets Slide As Europe Careens Into A Recession

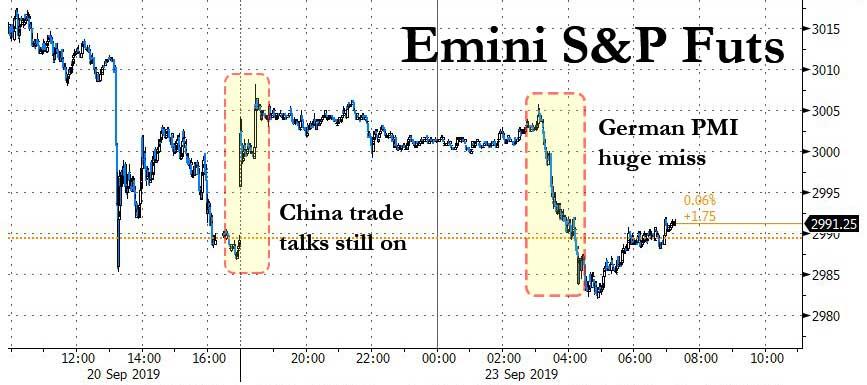

The overnight trading session has been a tale of two halves, with the start of the session marked by sharply higher futures, following this weekend’s news that China’s canceled trip to Montana and Nebraska was made at the request of the US, and not as traders first assumed, by a negative turn in the lower-level discussions held in Washington last week. However, the early optimism quickly crashed after Germany reported the latest PMI data, which missed across the board, printing at 7 year lows, and was – in the words of Phil Smith, Principal Economist at IHS Markit, “simply awful.” (And it’s not just Germany: French PMIs were ugly too, missing across the board).

The result was an instant shift in risk sentiment, as not only is the German manufacturing recession getting worse, but the Services PMI also dropped, dragging the composite below 50 for the first time in seven years…

… slamming US equity futures, which hit session lows shortly after the German print…

… sending most global markets promptly into the red.

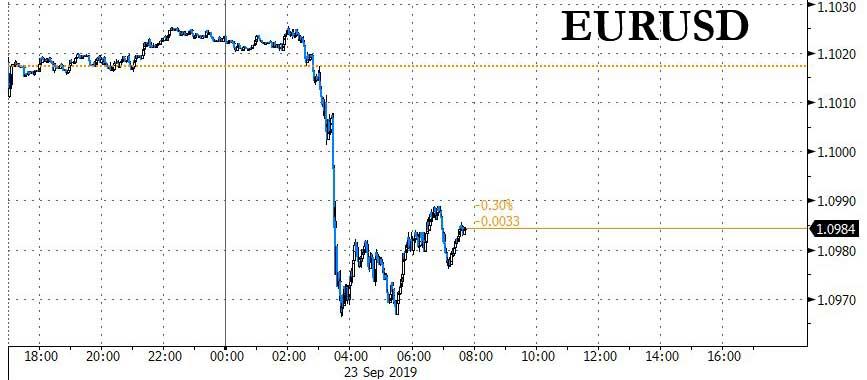

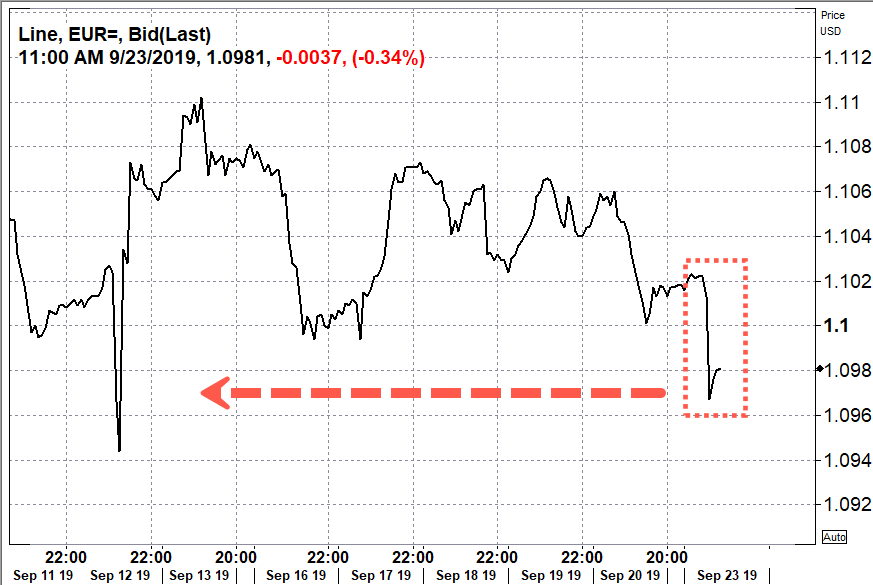

… and slamming the EURUSD back under 1.10

The Stoxx Europe 600 Index extended losses and European bonds rallied. Monday’s abrupt sentiment reversal followed the worst session for US equity indexes in about two weeks on Friday – ending a three-week run of gains – after a Chinese agriculture delegation canceled a visit to Montana, dampening optimism about the trade talks. Stock markets had been buoyed earlier in the week by the Federal Reserve’s decision to cut interest rates for the second time in 2019, joining other central banks around the world in easing monetary policy.

The gloomy European data was a stark reminder to investors of the fragility of the global economy. While markets remain on edge ahead of next month’s planned high-level trade talks between the U.S. and China, they’re also fixated on any action or messaging from the world’s major central banks that could support growth. A slew of policy makers will speak this week.

“Global growth risks are rising,” Beverley Morris, director of rates and inflation at QIC Ltd. in Brisbane, told Bloomberg TV. “It’s certainly not panic stations at this stage, but certainly in terms of our portfolio actions, we are being more cautious.”

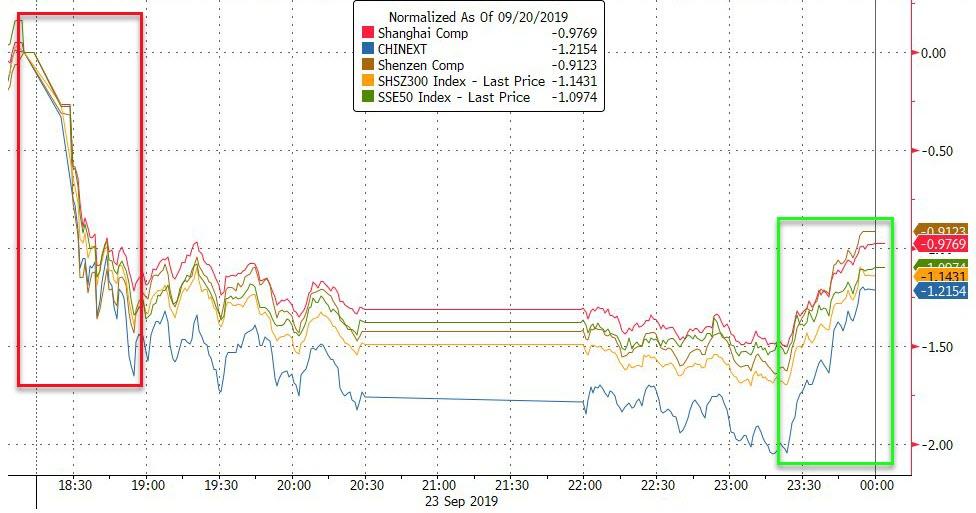

Asian stocks edged lower, led by technology firms, as investors gauged South Korea’s export slump as well as the twists and turns of China-U.S. trade talks, with Tokyo shut for a holiday. Markets in the region were mixed, with India jumping and China retreating. The Shanghai Composite Index dropped 1%, dragged by large banks and insurers. China’s cancellation of a planned visit to farms in the American heartland was done at the request of the U.S., people familiar with the matter said. Equities in India continued a surge, with the Sensex surging as much as 3.8%, set for its biggest two-day rally in 10 years, amid optimism that the government’s $20 billion company tax cut will revive growth. HDFC Bank and ICICI Bank were among the biggest boosts. The Kospi closed little changed, as South Korean exports headed for a 10th monthly slide amid flagging chip sales

In FX, the Bloomberg Dollar index climbed then pared gains as the U.S. and China continued to engage in discussions to overcome trade differences. The euro fell sharply and global bonds rallied after German manufacturing suffered its worst downturn since the financial crisis. Sterling slipped as U.K. Prime Minister Boris Johnson cautioned against the chances of a Brexit breakthrough when he meets with key European leaders in New York. The onshore yuan fell amid caution in the run-up to next week’s national holidays. The Korean won sank as exports continued to deteriorate.

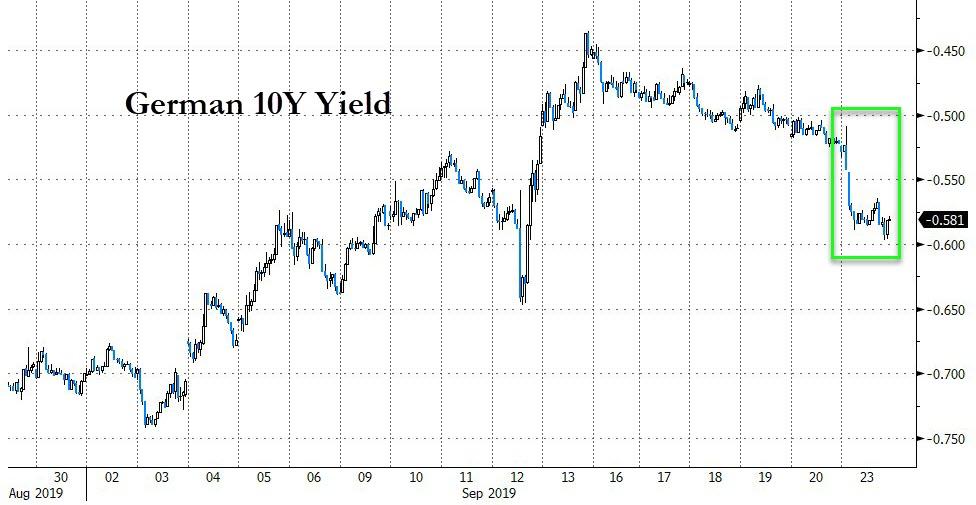

In rates, U.S. Treasuries advanced for a sixth day with the 10-year yield sliding to its lowest since Sept. 12, dropping to 1.68%.

Oil fluctuated following a report that full repairs to Saudi facilities hit by a drone attack may take many months. Brent fell below $64 a barrel on Monday, reversing an earlier gain, pressured by the prospect of a faster-than-expected full restart of Saudi Arabian oil output and by fresh signs of European economic weakness. It was up earlier in the session, supported by scepticism over how fast output would come back.

“Oil prices are tracking European markets lower this morning, understandably knocked by the woeful manufacturing data from the bloc and the implications for global growth and demand,” said Craig Erlam, analyst at OANDA. Brent has still gained about 18% this year, helped by a supply-limiting pact led by the Organization of the Petroleum Exporting Countries, although concern about slowing economic growth has limited the advance.

Expected economic releases include PMIs. Cantel Medical is reporting earnings. Also on the radar is a speech by Federal Reserve Bank of New York President John Williams at the 2019 U.S. Treasury Market Conference at 9:50 a.m. ET.

Market Snapshot

- S&P 500 futures down 0.2% to 2,983.00

- MXAP down 0.06% to 159.29

- MXAPJ down 0.3% to 509.64

- Nikkei up 0.2% to 22,079.09

- Topix up 0.04% to 1,616.23

- Hang Seng Index down 0.8% to 26,222.40

- Shanghai Composite down 1% to 2,977.08

- Sensex up 3.1% to 39,197.38

- Australia S&P/ASX 200 up 0.3% to 6,749.72

- Kospi up 0.01% to 2,091.70

- STOXX Europe 600 down 1% to 388.85

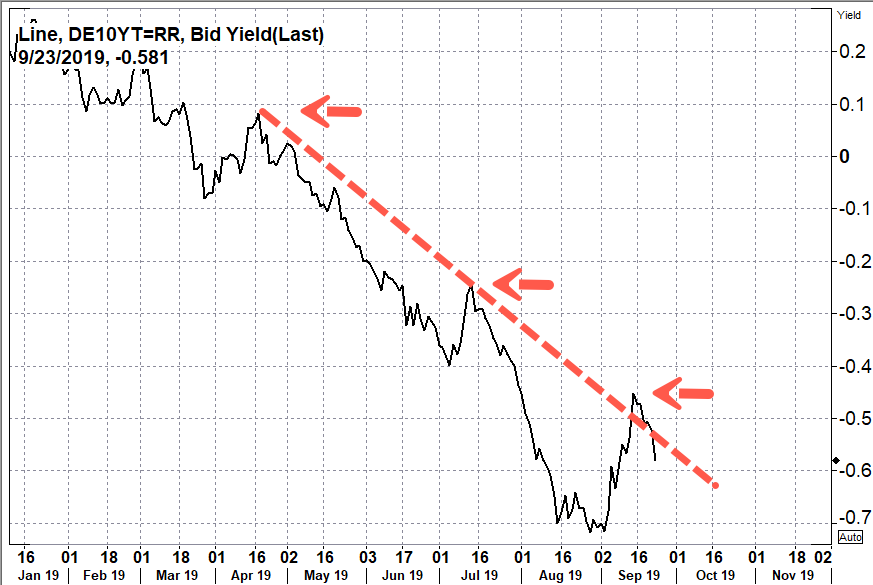

- German 10Y yield fell 5.9 bps to -0.58%

- Euro down 0.3% to $1.0980

- Italian 10Y yield rose 3.7 bps to 0.582%

- Spanish 10Y yield fell 7.3 bps to 0.163%

- Brent futures up 0.4% to $64.51/bbl

- Gold spot up 0.2% to $1,519.44

- U.S. Dollar Index up 0.2% to 98.74

Top Headline News from Bloomberg

- Germany’s private sector is suffering its worst downturn in almost seven years as a manufacturing slump deepens, raising pressure on the government to add fiscal stimulus; a Purchasing Manager’s Index fell to 49.1 in September from 51.7 a month earlier, according to IHS Markit; the reading was worse than economists predicted and the lowest since October 2012

- China’s cancellation of a planned visit to farms in America was done at the request of the U.S., people familiar with the matter said, indicating it wasn’t caused by a negative turn in the lower- level discussions held in Washington last week; trade groups from the two nations held “constructive” talks during Sept. 19-20, China’s Ministry of Commerce said Saturday

- Thomas Cook Group Plc collapsed under a pile of debt after talks with creditors failed, forcing the British government to charter planes to bring home more than 150,000 of the storied travel provider’s stranded customers; trading in Thomas Cook’s stock was suspended in London and its euro bonds plunged 72%

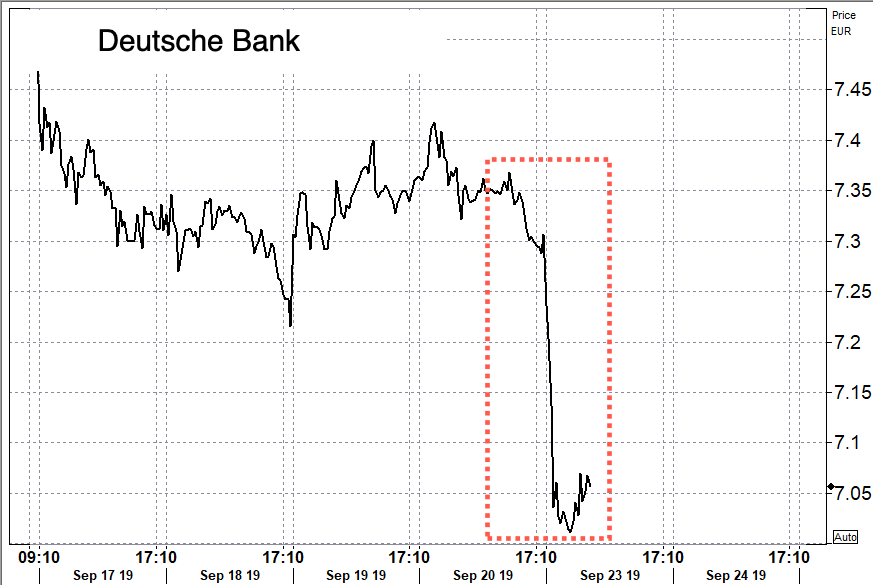

- Deutsche Bank AG completed a deal with BNP Paribas SA to transfer its prime brokerage business to the French bank as part of the German lender’s biggest overhaul in recent history

- U.K.’s Johnson will start a week of intense diplomacy on Monday, as he tries to push for a Brexit deal on the sidelines of the United Nations General Assembly in New York

Asian equity markets were mixed following the negative close last Friday on Wall St. amid temperamental US-China trade headlines, while the absence of Japanese markets also contributed to the lacklustre tone. ASX 200 (+0.3%) was positive with the index led higher by the commodity related stocks after gold advanced above the USD 1500/oz level and with oil underpinned by reports it could take 8 months for Saudi output to return to normal, while India’s NIFTY (+2.9%) outperformed again after the recent corporate tax cut announcement. Conversely, weakness in Hang Seng (-0.8%) and Shanghai Comp. (-0.8%) dampened sentiment in the region with underperformance in the mainland as ongoing trade uncertainty overshadowed the liquidity efforts by the PBoC. This followed conflicting reports in which US President Trump stated Chinese agricultural purchases will not be enough and reiterated that he does not need a deal before the 2020 election although it was also reported the US granted temporary tariff exemptions on over 400 types of Chinese products, while China’s delegation cancelled its US farm visit but this was later attributed to concerns it could turn into a media circus or may be misconceived as meddling and was not due to a breakdown in trade talks

Top Asian News

- Bond Traders in India Caught Out by Surprise Fiscal Flip Flop

- Israel Arabs Back Bid by Netanyahu’s Rival to Unseat Premier

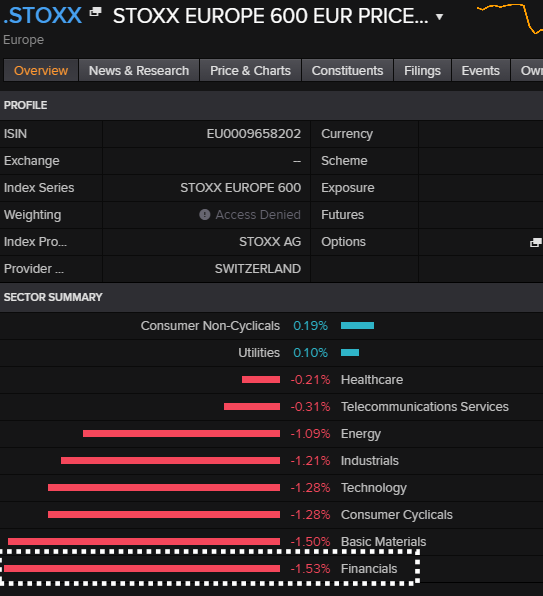

Major European bourses are lower (Euro Stoxx 50 -1.0%), after disappointing PMI data stoked further concerns about the slowdown in Eurozone growth. The DAX (-1.2%) is the notable underperformer, slipping briefly below last week’s low and recent support at 12300, after German manufacturing PMI data pointed to the sector falling further into contractionary territory. Amid the risk off sentiment, utilities (+0.1%), consumer staples (+0.2%) and health care (unch.) sectors are supported, while materials (-1.6%), financials (-1.7%) and tech (-1.4%) are softer. Bucking the general risk tone are European airlines, including TUI (+7.5%), Ryanair (+1.1%) and easyJet (+3.5%), who are higher after rival Thomas Cook ceased trading activities and filed for bankruptcy. In terms of individual movers; William Hill (-4.0%) reversed early gains, despite premarket news that the Co. is looking for US broadcaster deals in an attempt to promote its brand. Elsewhere, K+S (-5.7%) sunk after being downgraded at Pareto Securities. Ocado (+0.2%) managed to reverse losses on triggered by news that the Co’s Chairman stated they “will go to any length” to protect their intellectual property, amid a court battle with a co-founder. Finally, ABN AMRO (-3.5%) is under pressure after being downgraded at Santander.

Top European News

- Germany May See No Growth This Year as Manufacturing Slumps

- Euro- Area Economy Comes Close to Stalling as Factories Suffer

- Vonovia Becomes Sweden’s Biggest Landlord With $1.3 Billion Deal

- Has Poland’s Government Become a Threat to Business?

In FX, further concerns about the European economy have weighed on the Euro in early trade as the latest flash PMIs out of the region deteriorated significantly vs. expectations. Germany’s release took EUR/USD below the 1.100 level with IHS noting that on its current trajectory, Germany may not see any growth before year-end, whilst VDMA added further pessimism to the German economic outlook. Further, the EZ release did little to immediately sway asset classes as participants anticipated a softer pan-release, but IHS highlighted that Q3 EZ GDP growth looks set to rise just 0.1%. Analysts at CapEco highlighted concerns regarding manufacturing contagion on the services sector whilst noting that a continuation in the employment component could lead to further easing in wages. Thus, the analysts believe that “there is little reason to think that GDP growth will pick up as the ECB and the consensus forecasts assume”. EUR/USD took out Friday’s low and a Fib level around 1.0995-97 to print a base at 1.0967 ahead of support at 1.0966 and 1.0950 (YTD low at 1.0924). Next up, participants will be eyeing ECB President Draghi’s final testimony to the European Parliament at 1400BST. Meanwhile, the Buck has derived support in light of a weaker Single Currency as DXY extends its gains above 98.50 to a high of 98.84 and ahead of the psychological 99.00 and resistance at 99.10. On the docket State-side, traders will be on the lookout for a few Fed speaks including Williams (voter, neutral) at the US Treasury Market Conference at 1450BST, Bullard (voter, dove, dissenter) on monetary policy at 1800BST and Daly (non-voter, neutral) on supporting US economy in urban & rural communities.

- GBP, CAD – Weaker on the day, albeit more on the back of a firmer USD with Brexit-watchers still on the lookout for the Supreme Court’s decision on PM Johnson’s parliament prorogation. If ruled against (as legal experts expect), then the PM could be forced to recall MPs back to parliament. Cable remains marginally softer below the 1.2450 level (vs. high of 1.2490) after finding a base at 1.2424, which marks the lowest since 17th September (although that day saw a low of 1.2393). The Loonie also takes a spot as a G10 laggard, but mostly pressured by a retreat in oil prices as the post-PMI sentiment seeped into the energy complex. USD/CAD hovers around the 1.3300 handle (vs. low of 1.3257) with resistance seen to the upside at 1.3305 (200 DMA), 1.3346 and the psychological 1.3350 levels.

- CHF, JPY – Marginally firmer amid a weakening EUR and flights to safety post-EZ PMI with USD/JPY back below the 107.50 level to a low of 107.30 ahead of support at 107.10, whilst EUR/CHF trades flat on the day but fell from an intra-day high of 1.0930 (50 DMA) to a base just above 1.0850 (with support and YTD low at 1.0809). Attention remains on the 1.08 level amid the recent rise in SNB total sights deposits with TD noting that the data suggests the SNB may be defending the level.

- AUD, NZD – The antipodeans remain above water with the Kiwi outperforming its Tasman-peer ahead of this week’s RBNZ Monetary Policy Decision amid consensus for an unchanged Cash Rate at 1.00%, following its unexpected rate cut at its prior meeting, whilst the Shadow Board also recommends no change in policy. The currencies seem to have also derived some support from the US-China trade saga with Chinese state media noting that talks are constructive, and that the cancelled China visit to US farms was not a sign of deteriorating talks. NZD/USD hovers near intra-day highs (0.6277) after finding a base at 0.6250 whilst its Aussie counterpart remains above 0.6750, albeit off highs (0.6780).

In commodities, oil prices continued to come off its earlier highs, as focus shifted from the prospect of a more protracted disruption to Saudi Aramco supply than expected (which helped prices over the weekend) to concern over global growth, after more abysmal Eurozone PMI data triggered a bout of selling in the complex. Downside was exacerbated soon thereafter on source reports that Saudi Arabia’s Khuraris and Abqaiaq facilities are to fully restore oil production early next week (form current production levels of around 4.3mln BPD), contrary to WSJ reports over the weekend that repairs could take up to 8 months. WTI Nov’ 19 futures slumped through last week’s lows around the USD 58/bbl handle, before finding a base at USD 57.40/bbl, while Brent Nov’ 19 fell below the USD 64/bbl handle, although last week’s USD 63.06 low is still some way off. Gold prices are higher, despite opening on the back foot (on weekend reports that Chinese agriculture officials didn’t end their US trip early due to trade talk difficulties) and a firmer buck, with negative risk sentiment exacerbated by the aforementioned Eurozone PMIs helping to lift the precious metal; spot gold continues to climb from its recent USD 1500/oz base. On the flip side, global demand concerns are keeping copper prices under pressure.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0, prior -0.4

- 9:45am: Markit US Manufacturing PMI, est. 50.4, prior 50.3

- 9:45am: Markit US Services PMI, est. 51.5, prior 50.7;

- 9:45am: Markit US Composite PMI, prior 50.7

DB’s Jim Reid concludes the overnight wrap

As astronomical autumn arrives today in the Northern hemisphere its apt that I got my wellies out yesterday for the first time in a few months after a fair bit of rain. Winter is coming. Also on ordering groceries online last night I got a bit of a shock as they have now started to sell mince pies in time for Xmas. Only 92 days left and just under 8 million seconds. It’ll be here before you know it.

After the central bank frenzy of the last 10 days, the next few days should be somewhat lighter for news flow for markets. Data highlights include the preliminary global September PMIs (today), the German IFO (tomorrow), and the US Conference Board’s consumer confidence reading (tomorrow) and UoM equivalent (Friday) with the spread between the two of notable interest as it has been a lead indicator of the cycle in the past (see below). From central banks, we have ECB President Draghi’s final “Monetary Dialogue” before the European Parliament’s Economic and Monetary Affairs Committee (today), along with a number of other key speakers, especially from the Fed. Finally, we should hear the outcome of the UK Supreme Court Case on the prorogation of Parliament, while world leaders will be gathering at the UN General Assembly.

In a little more detail now, the key data highlight this week will be the preliminary September PMIs today (Japan tomorrow due to a holiday) with the big question continuing to be how and when the divergence between manufacturing and services will end. As an example the Euro manufacturing PMI has been in contractionary territory since February, while the services PMI has shown consistent growth over that period. The consensus expectation is for this divergence to narrow modestly, with the manufacturing Euro PMI rising three-tenths to 47.3, with the services PMI falling two-tenths to 53.3. The German manufacturing PMI will be of particular interest, which last month was at 43.5, and has been below 50 for the entire year so far.

Speaking of Germany, another key highlight will be the Ifo business climate survey tomorrow. In August, the indicator fell to 94.3, its lowest level since November 2012, while the expectations reading fell to 91.3, the lowest since June 2009. Nevertheless, the consensus expectation is for a rebound in both this month, with the business climate indicator expected to rise to 94.6.

With respect to US economic data, Tuesday’s consumer confidence report (132.0 forecast vs. 135.1 previously) and Friday’s University of Michigan consumer sentiment survey (92.0 final vs. 92.0 preliminary) will provide further information on the consumer outlook. As our economists have pointed out, as of August, the spread between the level of the two surveys was at an all-time high, which as their recent research has highlighted, may be sending a concerning signal even though on the surface the levels of both series remain elevated (see ” Yield curve inversion signals recession…(consumer) surveys say? ” ).

Another one to also watch out for is the third estimate of Q2 US GDP, although expectations are for the annualised rate to remain unchanged from the second estimate, at +2.0%. Meanwhile on Friday we’ll also see personal income and personal spending data for August, along with the preliminary durable goods orders reading.

There are a number of central bank speakers this week kicking off today with ECB President Draghi appearing before the European Parliament’s Economic and Monetary Affairs Committee, in his last “Monetary Dialogue” before his eight-year term ends on 31 October Other speakers this week include Bank of Japan Governor Kuroda and Federal Reserve Vice-Chairs Quarles and Clarida, while the Bank of Mexico will be making its latest policy decision. Within the Fed Bullard (voter/dove – wanted 50bps last week) and Daly (nonvoter/dove) will also be making appearances later on today, and Chicago’s Evans (voter/dove) will follow on Wednesday.

Turning to politics, the UK Supreme Court is expected to rule on the case over the prorogation of Parliament early this week according to the Supreme Court President. An update on timing is likely today. It’s also the Labour Party Conference, which is taking place currently until Wednesday, ahead of the Conservative Party Conference the subsequent week. The Labour Party are still fighting over a coherent Brexit strategy which further complicates potential scenarios going forward as it doesn’t seem to be working for them in recent opinion polls. Labour party leader Corbyn said that his party is pledging to hold a second referendum on Brexit if it’s elected to government, pitting ‘Remain’ against a “credible” deal he negotiates with the EU but without saying which side he’d campaign for. Elsewhere in politics, the annual General Debate of the UN General Assembly begins on Tuesday, with a number of world leaders expected to appear.