GOLD:$1532.4 UP $8.65 (COMEX TO COMEX CLOSING)

Silver:$18.58 DOWN 5 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1531.60

silver: $18.61

Definition of Rico

RICO is typically used to indict mobsters – which makes its use against employees of the largest bank in America a very disquieting event. But even more disquieting is that two trial lawyers compared JPMorgan Chase to the Gambino crime family five long years ago and recommended in their 2016 book that the bank’s officers be prosecuted under the RICO statute.” … Pam Martens and Russ Martens

Ted Butler….

we are coming very close to a commercial failure!!

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 0/3

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,523.700000000 USD

INTENT DATE: 09/23/2019 DELIVERY DATE: 09/25/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 1

737 C ADVANTAGE 1 2

905 C ADM 2

____________________________________________________________________________________________

TOTAL: 3 3

MONTH TO DATE: 1,746

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 3 NOTICE(S) FOR 300 OZ (0.00611 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 1746 NOTICES FOR 174,600 OZ (5.4867 TONNES)

SILVER

FOR SEPT

19 NOTICE(S) FILED TODAY FOR 95,000 OZ/

total number of notices filed so far this month: 8662 for 43,310,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

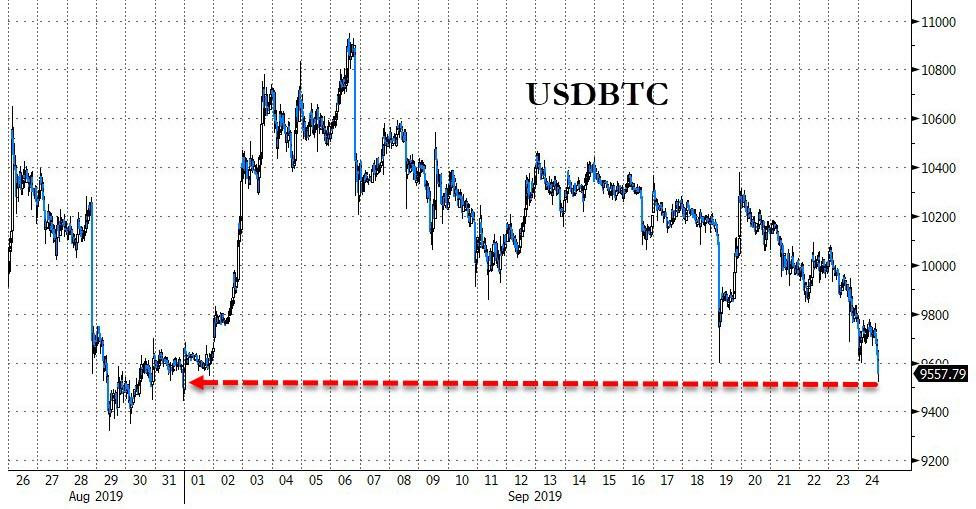

Bitcoin: OPENING MORNING TRADE : $ 9720 UP 15

Bitcoin: FINAL EVENING TRADE: $ 8714 DOWN 1776

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUGE SIZED 3652 CONTRACTS FROM 211,963 UP TO 215,615 WITH THE GIGANTIC 80 CENT GAIN IN SILVER PRICING AT THE COMEX.

TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR SEPT 0,; DEC 1562 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1562 CONTRACTS. WITH THE TRANSFER OF 1562 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1562 EFP CONTRACTS TRANSLATES INTO 7.91 MILLION OZ ACCOMPANYING:

1.THE 80 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.395 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

YESTERDAY, THERE WAS NOT EVEN A SLIVER OF AN ATTEMPT AT COVERING OUR BANKER SHORTS AT THE SILVER COMEX. OUR OFFICIAL SECTOR AGAIN USED COPIOUS NON BACKED PAPER IN AN ATTEMPT TO CONTAIN SILVER’S PRICE RISE BUT IS WAS TOO NO AVAIL.AS SILVER ADVANCED IN PRICE BY A HUGE 80 CENTS.

THE TOTAL OPEN INTEREST IN BOTH EXCHANGES RISE BY A HUGE AMOUNT.

THE LIQUIDATION OF COMEX OI OF SPREADERS HAVE STOPPED AND WE WILL NOW COMMENCE WITH THE ACCUMULATION PHASE OF SPREADERS GOLD OPEN INTEREST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

28,187 CONTRACTS (FOR 16 TRADING DAYS TOTAL 28,187 CONTRACTS) OR 140.935 MILLION OZ: (AVERAGE PER DAY: 1761 CONTRACTS OR 8.808 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 140.935 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 20.12% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1690.54 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3652, WITH THE 80 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE OF 1562 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED AN ATMOSPHERIC SIZED: 5214 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1562 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 3652 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 80 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $18.63 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.079 BILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 19 NOTICE(S) FOR 95,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.395 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF SEPT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF SEPT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

IN GOLD, THE COMEX OPEN INTEREST ROSE BY AN ATMOSPHERIC AND CRIMINALLY SIZED 12,407 CONTRACTS, TO 647,392 ACCOMPANYING THE $16.25 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

WE ARE NOW CLOSING IN OUR RECORD COMEX OPEN INTEREST OF 652,971 SET IN JULY 19 2016

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7602 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 8060 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 647,392,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 20,467 CONTRACTS: 12,407 CONTRACTS INCREASED AT THE COMEX AND 8060 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 20,467 CONTRACTS OR 2,046,700 OZ OR 63.66 TONNES. YESTERDAY WE HAD A GAIN OF $16.25 IN GOLD TRADING….

AND WITH THAT STRONG GAIN IN PRICE, WE HAD A HUMONGOUS GAIN IN GOLD TONNAGE OF 63.66 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS THE COMEX GOLD VOLUME AND OPEN INTEREST ARE HUGE. THEY WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE LONGS AND AS YOU CAN SEE, THE TOTAL OPEN INTEREST IN BOTH EXCHANGES SKYROCKETED

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 116,314 CONTRACTS OR 11,631,400 oz OR 361,78 TONNES (16 TRADING DAY AND THUS AVERAGING: 7269 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 361.78TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 361.78/3550 x 100% TONNES =10.19% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4513.88 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN ATMOSPHERIC AND CRIMINALLY SIZED INCREASE IN OI AT THE COMEX OF 12,407WITH THE HUGE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($16.25)) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8,060 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8060 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 20,467 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8060 CONTRACTS MOVE TO LONDON AND 12,407 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 63.66 TONNES). ..AND THIS HUMONGOUS INCREASE OF DEMAND OCCURRED WITH THE STRONG GAIN IN PRICE OF $16.25 WITH RESPECT TO FRIDAY’S TRADING AT THE COMEX.

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.65 TODAY//(COMEX-TO COMEX)

ANOTHER HUGE CHANGE IN GOLD INVENTORY AT THE GLD/

A PAPER GOLD DEPOSIT OF: 14.37 TONNES

WHAT A MASSIVE FRAUD!!

INVENTORY RESTS AT 908.52 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 5 CENTS TODAY:

A BIG CHANGE IN SILVER INVENTORY AT THE SLV//

A PAPER DEPOSIT OF 2.338 MILLION OZ/

/INVENTORY RESTS AT 377.811 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 3652 CONTRACTS from 211,963 UP TO 215,615 AND CLOSER TO FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR SEPT. 0; FOR DEC 1562: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1562 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3652 CONTRACTS TO THE 1562 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC AND CRIMINALLY SIZED GAIN OF 5214 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 26.07 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// AND FINALLY SEPT: 43.395 MILLION OZ//

RESULT: A GIGANTIC SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 80 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 1562 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 8.26 POINTS OR 0.28% //Hang Sang CLOSED UP 58.60 POINTS OR 0.22% /The Nikkei closed UP 19.75 POINTS OR 0.09%//Australia’s all ordinaires CLOSED DOWN .07%

/Chinese yuan (ONSHORE) closed DOWN at 7.1068 /Oil UP TO 58.13 dollars per barrel for WTI and 63.95 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1068 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 67.1043 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA

In a good will gesture China waives waivers for USA soybean purchases.

(Courtesy zerohedge)

4/EUROPEAN AFFAIRS

a)UK

In a landmark ruling, the uK Supreme Court ruled that Johnson’s suspension of Parliament is illegal. This may hurt his chances of a no deal Brexit. It looks like his only option is an election and let the citizens decide the makeup of Parliament and Brexit

(zerohedge)

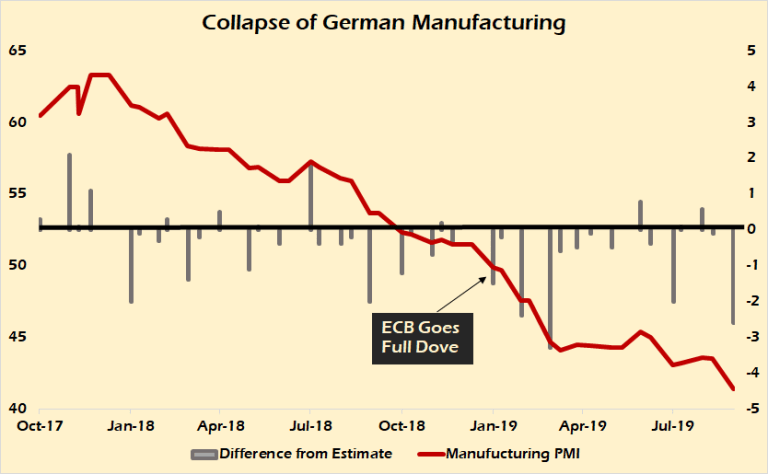

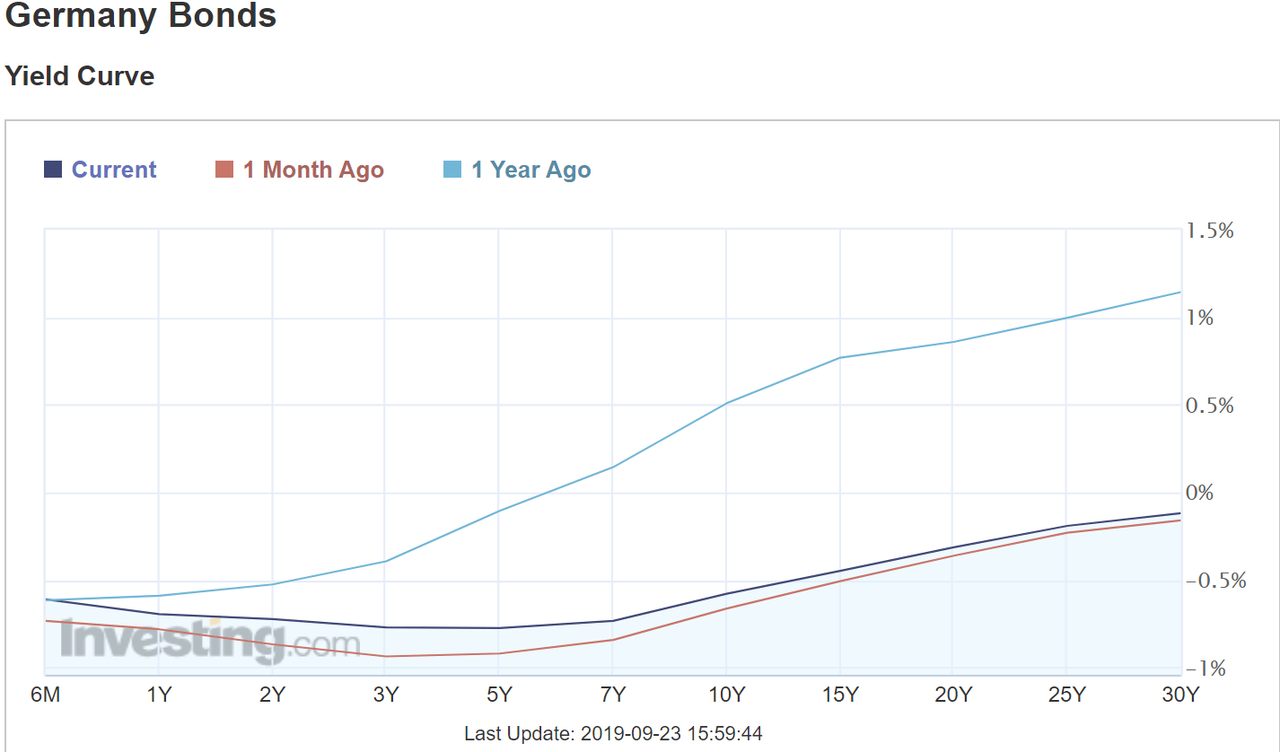

b(GERMANY

Extremely important..it is something that we have been pointing out to you for several months. Germany’s economy is faltering terribly. Its yield curve is starting to invert. And with Germany collapsing so is the Euro project

c))Mish Shedlock: an article in German translated shows how negative rates killed the German banks

(Mish Shedlock/Mishtalk)

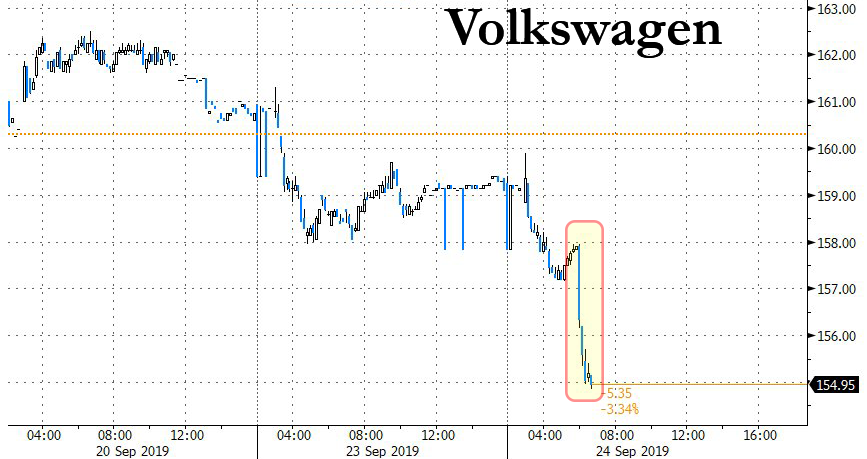

d)The CEO of Volkswagen has been charged with market manipulation in the emissions scandal as the shares of Volkswagen stumble

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

(Von Greyerz/Kingworldnews)

b)The UK has been importing a huge amount of physical gold as investors turn their paper Exchange for Physical into real physical

(Lawrie Williams)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

USA confidence tumbles to 2019 lows

(zerohedge)

iii) Important USA Economic Stories

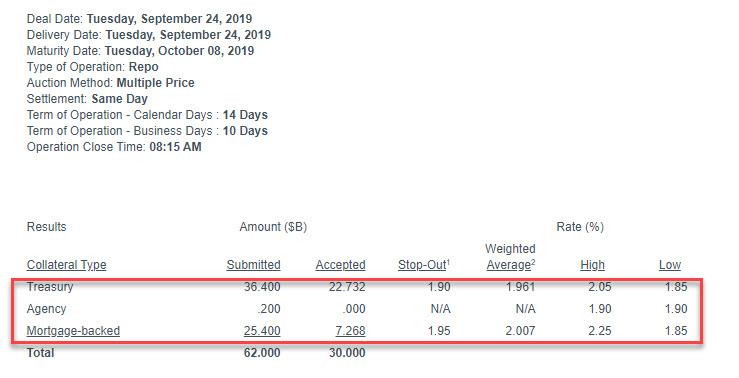

a)The first of the term repo auction has just been concluded as it is 2 x overscribed. It is the overnight repo auction that we are watching very closely and since we are close to the quarter end we may see a considerable jump in the QC repo rate.

(zerohedge)

iv) Swamp commentaries)

a)Michael Snyder believes the dam may break on Thursday and the Democrats will stupidly try to impeach Trump

(Michael Snyder)

b)It looks like Trump actually withheld funds to Ukraine one week prior to the phone call. He wantss the u|kraine to rein in corruption

c)What an absolute farce!! Trump is set to release the Ukrainian transcript which took the thunder away from the Democrats. However Pelosi is still set to announce formal impeachment inquiry against Trump which they will lose for sure

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

we had 0 dealer entry:

We had 0 kilobar entries

total gold withdrawals; 100.000 oz

we had one adjustment from Delaware and this is a deemed settlement:

Out of Delaware: 1213.830 oz was removed from the dealer and this landed into the customer account of Delaware

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 41,290 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 135,857 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 135,857 CONTRACTS EQUATES to 679 million OZ 97.04% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.74% ((SEPT 24/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.89% to NAV (SEPT 24/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.74%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.53 TRADING 15.07/DISCOUNT 2.94

END

And now the Gold inventory at the GLD/

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 908.52 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

AUGUST 22.WITH GOLD DOWN $6.80 TODAY: TWO HUGE CHANGES IN GOLD INVENTORY AT THE GLD: I)A PAPER DEPOSIT OF 6.74 TONNES INTO THE GLD (LATE YESTERDAY EVENING) AND 2) A PAPER DEPOSIT OF 2.93 TONNES LATE THIS AFTERNOON./INVENTORY RESTS AT 854.84 TONNES

AUGUST 21/WITH GOLD DOWN $.30 TODAY:A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.76 TONNES INTO THE GLD INVENTORY/GOLD INVENTORY RESTS AT 845.17 TONNES

AUGUST 20//WITH GOLD UP $2.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/GOLD INVENTORY RESTS AT 843.41 TONNES

AUGUST 19/WITH GOLD DOWN $11.20//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .88 TONNES//INVENTORY RESTS AT 843.41 TONNES

AUGUST 16/WITH GOLD DOWN $7.35: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 844.29 TONNES

AUGUST 15/WITH GOLD UP $3.55 TODAY//WE HAVE A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: WE GOT BACK 7.63 TONNES OUT OF 11.11 TONNES LOST ON WEDNESDAY( A DEPOSIT OF 7.63 TONNES)/INVENTORY RESTS AT 844.29 TONNES

AUGUST 14/WITH GOLD UP $7.60 TODAY (AND DOWN $2.90 YESTERDAY) WE HAD A MONSTROUS WITHDRAWAL OF 11.11 TONNES OF GOLD FROM THE GLD/AND THIS WAS USED IN AN ABORTED RAID YESTERDAY: INVENTORY RESTS AT 836.66 TONNES

AUGUST 13.2019: WITH GOLD DOWN $2.60 TO DAY: A HUGE 7.92 PAPER GOLD TONNES WERE ADDED TO THE GLD/INVENTORY RESTS AT 747.77 TONNES

AUGUST 12.2019: WITH GOLD UP $7.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 839.85 TONNES

AUGUST 9/WITH GOLD DOWN $2.00//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REMAINS AT 839.85 TONNES OZ/

AUGUST 8: WITH GOLD DOWN $4.20: TWO TRANSACTIONS: A)A MONSTROUS PAPER DEPOSIT OF 8.50 TONNES WAS ADDED TO THE GLD/INVENTORY RESTS AT 845.42 TONNES b) A HUGE WITHDRAWAL OF 5.59 TONNES FROM THE GLD//INVENTORY RESTS AT 839.85 TONNES…ABSOLUTE FRAUD!

August 7/ WITH GOLD UP $31.00//A GOOD PAPER DEPOSIT OF 1.86 TONNES OF GOLD INTO THE GLD INVENTORY//INVENTORY RESTS AT 836.92 TONNES

AUGUST 6.2019: WITH GOLD UP $7.85 A STRONG DEPOSIT OF 4.50 TONNES OF PAPER GOLD INTO THE GLD LATE LAST NIGHT/INVENTORY RESTS AT 835.16 TONNES

AUGUST 5/2019//WITH GOLD UP $18.80/A STRONG DEPOSIT OF 2.94 TONNES OF PAPER GOLD INTO THE GLD/INVENTORY RESTS AT 830.76 TONNES.

AUGUST 2/2019: WITH GOLD UP $25.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.82 TONNES

AUGUST 1/2019: WITH GOLD DOWN $4.90 TODAY: TWO TRANSACTIONS: i) A PAPER WITHDRAWAL OF 1.47 TONNES (USED IN THE RAID THIS MORNING)/ and ii) A PAPER DEPOSIT OF 4.40 TONNES THIS AFTERNOON!/INVENTORY RISE TO 827.82 TONNES

JULY 31/WITH GOLD DOWN 3.90 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

JULY 30//WITH GOLD UP $9.00 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 824.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SEPT 24/2019/ Inventory rests tonight at 908.52 tonnes

*IN LAST 667 TRADING DAYS: 40.64 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 567- TRADING DAYS: A NET 126.01 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ//

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 22/WITH SILVER DOWN 11 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.696 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.850 MILLION OZ//

AUGUST 21/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 20.WITH SILVER UP 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 19/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 16/: WITH SILVER DOWN 9 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 380.154 MILLION OZ//

AUGUST 15/2019 WITH SILVER DOWN 2 CENTS: ANOTHER BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WHOPPING 3.977 MILLION OZ PAPER DEPOSIT/INVENTORY RESTS AT 380.154 MILLION OZ/

AUGUST 14/2019 WITH SILVER UP 27 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.538 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 376.177 MILLION OZ//

AUGUST 13/2019: WITH SILVER DOWN 9 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 6.082 MILLION OZ///INVENTORY NOW RESTS AT 371.637 MILLION OZ

AUGUST 12/2019: WITH SILVER UP 11 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 365.557 MILLION OZ.

AUGUST 9/2019//WITH SILVER UP 2 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 2.245 MILLION OZ INTO THE SLV INVENTORY/INVENTORY ADVANCES 365.557 MILLION OZ

AUGUST 8/WITH SILVER DOWN 23 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT: 1.409 MILLION OZ INTO INVENTORY///INVENTORY RESTS AT 363.311 MILLION OZ//

AUGUST 7/WITH SILVER UP 74 CENTS: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 361.907 MILLION OZ/

AUGUST 6/ WITH SILVER UP 5 CENTS: TWO TRANSACTIONS: A HUGE PAPER DEPOSIT OF 2.34 MILLION OZ WAS DEPOSITED INTO THE SLV LATE LAST NIGHT: THEN A HUGE 2.994 MILLION OZ OF A PAPER DEPOSIT THIS AFTERNOON: INVENTORY RESTS AT 361.907 MILLION OZ

AUGUST 5.2019: WITH SILVER UP 12 CENTS A TINY 142,000 OZ WITHDRAWAL AND THAW AS TO PAY FOR FEES//INVENTORY RESTS AT 356.573 MILLION OZ..

AUGUST 2/2019: WITH SILVER UP 10 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 356.715 MILLION OZ/

AUGUST 1//WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 31/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

JULY 30/2019: WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 356.715 MILLION OZ//

SEPT 24/2019:

Inventory 377.811 MILLION OZ

LIBOR SCHEDULE AND GOFO RATES:

YOUR DATA…..

6 Month MM GOFO 2.14/ and libor 6 month duration 2.05

Indicative gold forward offer rate for a 6 month duration/calculation:

G0LD LENDING RATE: – .09

XXXXXXXX

12 Month MM GOFO

+ 2.05%

LIBOR FOR 12 MONTH DURATION: 2.04

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.01

end

end

PHYSICAL GOLD/SILVER STORIES

i) GOLDCORE BLOG/Mark O’Byrne

Gold At 2 Week High At $1,523/oz On Global Economy Concerns; Palladium At All Time Nominal High

Gold climbs as weak eurozone data underlines fears over global growth

Gold hits 2-week high on growth fears, palladium scales new peak

Global stocks sink on dismal economic data, mixed trade signals

European Central Bank Pressures EU Countries To Stimulate The European Economy

The Coming Currency War 2.0: Digital Money vs. the Dollar

Fed’s Williams: ‘We were prepared’ for the overnight funding jolt last week

Gold, Government Bonds Deliver `Portfolio Resilience’: BlackRock (video)

Gold Prices (LBMA – USD, GBP & EUR – AM/ PM Fix)

23-Sep-19 1519.50 1522.10, 1222.13 1225.90 & 1385.48 1385.11

20-Sep-19 1504.10 1501.90, 1199.07 1203.62 & 1361.06 1362.52

19-Sep-19 1498.40 1500.70, 1200.67 1201.76 & 1354.85 1357.08

18-Sep-19 1502.20 1503.50, 1206.27 1204.90 & 1360.39 1359.92

17-Sep-19 1499.30 1502.10, 1208.89 1207.24 & 1361.51 1360.45

16-Sep-19 1502.05 1497.20, 1207.35 1203.30 & 1357.25 1359.46

13-Sep-19 1506.30 1503.10, 1209.41 1208.19 & 1356.88 1358.35

12-Sep-19 1502.95 1515.20, 1219.94 1227.46 & 1362.88 1373.53

11-Sep-19 1493.65 1490.65, 1208.21 1209.07 & 1354.74 1355.90

10-Sep-19 1494.60 1498.25, 1211.52 1211.34 & 1353.51 1357.11

Click here to listen to the latest GoldCore Podcast

Receive our free Daily or Weekly Updates by signing up here and click here to subscribe to GoldCore’s You Tube Channel

ii) Important gold commentaries courtesy of GATA/Chris Powell

von Greyerz expects spectacular gains in gold and silver similar to the 2 million percent rise in Venezuela bolivars per oz of god due to the fact that central governments must print massive amounts of paper money to fund their governments.

(Von Greyerz/Kingworldnews)

iii) Other physical stories:

The UK has been importing a huge amount of physical gold as investors turn their paper Exchange for Physical into real physical

(Lawrie Williams)

LAWRIE WILLIAMS: Only 20% of latest Swiss gold exports going to Asia

Readers who have been following our coverage of Swiss gold exports will be aware that in ‘normal’ past trading months around 80% or more of Swiss gold exports have been destined for Asian markets – particularly to China, Hong Kong and India. However in the past couple of months this has not been the case, perhaps demonstrating something of a sea change in the markets. In both July and August by far the biggest recipient of Swiss re- refined gold has been the UK – a factor the ‘experts’ have put down to particularly strong demand from the gold ETFs, many of which have their gold vaulted in London,

Indeed in August, the Swiss refineries took imported more gold from Asia and the Middle East than it exported to what have, over the years, been the biggest recipients of Swiss gold exports. In the past month the biggest exporters of gold to Switzerland have been The United Arab Emirates (26.8 tonnes) and Thailand (16.5 tonnes) – both typically net gold importers. Meanwhile total Swiss gold exports to all Asian and Middle Eastern nations combined only amounted to 22.6 tonnes.

True, China – for the past few years the biggest importer of Swiss gold – has reportedly being restricting gold imports (although as the world’s biggest gold producer it can presumably meet domestic demand from its own sources). But the return of gold to Switzerland from traditional importers like the UAE and Thailand, suggests some liquidation and profit taking by local traders and consumers. The gold price has risen almost 20% so far this year giving a decent margin for profit taking, but also suggesting that the eastwards gold flows are not into quite such firm hands as suggested by many gold commentators. Conversely the big flows into the UK, if indeed these are due to gold ETF demand, suggest more of a geographical balance re-appearing for gold demand.

Obviously we will keep an analytical eye open on the future of Swiss gold exports. There appears that there may be a slight shortage of gold bullion availability in China currently – gold price premiums there are said to be at near record levels, and there are reports that China has been relaxing its strictures on gold imports. Thus perhaps we will see an uptick in Chinese imports from Switzerland in the months ahead. But if the gold price remains strong, and rises further, as some analysts are predicting, we could see heavy flows into the UK continuing thus affecting the short term supply/demand balance accordingly.

On the other hand, there is some evidence that central bank gold buying from the two biggest gold accumulators – Russia and China – may be diminishing slightly. There seems to be little strong evidence that global new mined gold supply is actually beginning to fall yet (peak gold) but is perhaps still marginally growing. Countries like Australia, Russia and Canada are seeing gold production increases offsetting declines elsewhere.

So the supply/demand balance is only changing subtly with factors like ETF demand offsetting other declining factors. This suggests that the gold (and silver) price path will remain heavily dependent on investor sentiment, which seems to be improving by the day as global equity market nervousness in the face of a likely global recession, and ever-present geopolitical uncertainties, lead to increasing safe haven demand. In our eyes the future for gold and silver prices still looks positive – pgms perhaps less so because of their industrial demand sensitivity and if there is a recession they will be affected adversely.

23 Sep 2019

-END-

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Futures, Global Stocks Jump On “Trade Hopes And Optimism”

It’s time for some trade optimism again to lift stocks again, just in case we haven’t had that every other day for the past year.

Rekindled U.S.-China trade hopes lifted share markets on Tuesday, while the pound spiked after the latest dramatic Brexit twist, when the UK’s top court ruled the government’s suspension of parliament had been unlawful.

And good thing algos had some positive trade news to trade on as one day after a disastrous German PMI print, there was more gloomy data from Germany to contend with too, including the worst German IFO Expectations print in a decade, and which would suggest a -6% GDP print is on deck.

That data, however, was ignored after Treasury Secretary Steven Mnuchin’s and Trade Representative Robert Lighthizer confirmed on Monday that they would meet Chinese Vice Premier Liu He in two weeks’ time, while a separate report that China had granted new tariff waivers for US soybean purchases indicated Beijing may be telegraphing some more goodwill ahead of the negotiations.

“The comments (from Mnuchin on China trade talks) gave a little bit of boost to sentiment, but markets are still not that optimistic, either,” said Masahiro Ichikawa, senior strategist at Sumitomo Mitsui DS Asset Management. “It seems there have been a lot going on behind the scenes,” he said, referring to U.S. President Donald Trump’s questioning a decision by his top trade negotiators to ask Chinese officials to delay a planned trip to U.S. farming regions. That cancellation was seen by markets as a sign of trouble in the U.S.-China talks and sent stock prices tumbling on Friday.

As a result, U.S. index futures advanced with European stocks while Asian shares rose modestly as investors weighed renewed hopes for a trade deal – a catalyst for higher prices since the summer of 2018 – against increasingly recessionary economic data from around the globe. “A perceived lull in U.S.-China trade tensions has eased market fears about an economic downturn,” BlackRock strategists wrote in a note.

Not everyone was euphoric however: “All eyes are on early October, although there’s not a lot of expectation that anything material is going to come out from it,” John Lau, head of Asian equities at SEI Investments Co., said of the trade talks in an interview with Bloomberg Television. “If we get some kind of deal, any kind of deal, that would actually move markets.”

The European Stoxx 600 index rose 0.3%, with the eurozone banking index up 0.6% after it had slumped 2.8% in the previous session. European auto stocks stumbled following news that Volkswagen’s CEO and Chairman were charged with market manipulation over the emissions scandal, sending the company’s stock sliding and hitting the broader auto sector.

Earlier in the session, Asian stocks inched higher, led by energy producers while MSCI’s Asia index rose 0.1%, led by 0.6% gains in mainland Chinese shares after the vice head of China’s state planner said Beijing will step up efforts to stabilize growth. Markets in the region were mixed, with Japan and Singapore leading gains and Indonesia retreating. The Topix climbed 0.4% to its highest since April, with retail giants among the biggest boosts, after a three-day weekend. The Shanghai Composite Index added 0.3%, driven by Kweichow Moutai and Foxconn Industrial Internet. China has an abundant toolkit of monetary policy instruments, the Chinese central bank said in a statement. India’s Sensex fluctuated following its biggest two-day rally in 10 years, as Reliance Industries advanced and HDFC Bank declined.

Also overnight, Japan’s Foreign Minister Motegi said trade deal negotiations with US finished and that he doesn’t see much delay from goal of signing deal by end of the month, while a Foreign Ministry spokesman also said there is still have time to agree to a trade deal with US by end of the month. However, earlier reports suggested a deal may be delayed due to a disagreement regarding the auto tariffs and that an agreement will not be ready to sign when Japanese PM Abe meets US President Trump on Wednesday as it is still undergoing legal checks with the sides to sign separate documents confirming a final agreement.

Currency moves were mostly range bound with the exception of the pound: traders had waited for a Supreme Court ruling on UK Prime Minister’s Boris Johnson five-week suspension of parliament — a move known as prorogation in Westminster speak — and when it came it was dramatic and blunt. The move was “unlawful”. Sterling initially climbed as high $1.2487 on the view it would help prevent the UK being bundled toward a ‘no-deal’ Brexit at the end of October. But it quickly ran out of momentum and retreated to $1.2460, up a modest 0.2% on the day.

“I wasn’t surprised to see the currency hop higher but I also wasn’t surprised to see cable (pound vs the dollar) run out of steam ahead of $1.25,” said TD Securities’ European head of currency strategy Ned Rumpeltin.

Johnson is now likely to head to his Conservative party’s annual conference at the weekend and rally his troops in preparation for a likely national election which will be a bitter fight over Brexit.

“He is going to have to rally his base and he is going to do that around hard Brexit,” Rumpeltin said. “That will be a moment of clarity for the FX market. It will look at the polling and the Conservatives are leading in the polls.”

In geopolitical news, President Trump said we’re getting along well with North Korea and maybe we will be able to make a deal or maybe not. South Korea spy agency said US-North Korea working level talks will take place in 2-3 weeks and a summit is possible by year-end, while it added North Korea’s leader Kim could attend Korea-ASEAN summit in Busan in November. Trump also said he will discuss Iran in his UN speech today, while he added the US have a lot of pressure on Iran and that he is not looking for a mediator on Iran – Trump is scheduled to speak at 10:15ET. In response, Iran President Rouhani said our message to the world is peace and stability, although there were earlier comments from a senior official that Iran will never yield to the US and the US should lift sanctions if it wants to reduce tensions.

Among the main commodities, oil prices dipped on expectations of subdued demand although uncertainty remained about whether Saudi Arabia would be able to fully restore output after recent attacks on its oil facilities. Brent crude futures fell 40 cents to $64.37 a barrel by 0624 GMT. West Texas Intermediate futures were down 33 cents to $58.31.

“The demand side of the equation is back in focus,” said Michael McCarthy, senior market analyst at CMC Markets in Sydney, pointing to sluggish manufacturing numbers in leading economies in Europe as well as Japan.

Boosting risk sentiment, on Monday, St. Louis Fed President James Bullard who now is clearly gunning for Powell’s chairman seat by coming up with increasingly dovish proposals, said the central bank may need to ease monetary policy further to offset downside risks from trade conflicts and too-low inflation. Not all policy makers are on the same page, though. People’s Bank of China Governor Yi Gang said the country isn’t in a rush to add massive monetary stimulus, while Francois Villeroy de Galhau admitted he opposed the ECB’s decision to restart quantitative easing.

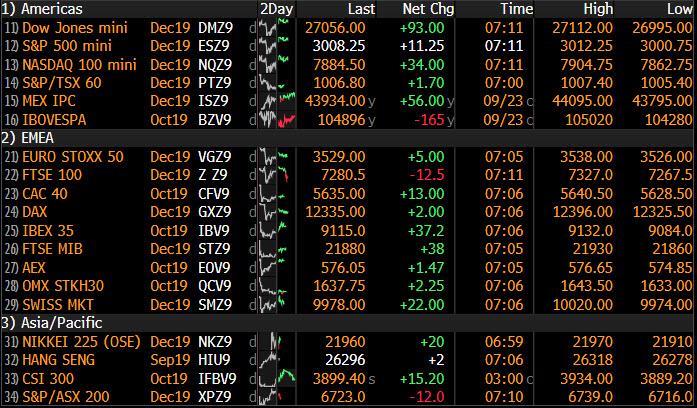

Market Snapshot

- S&P 500 futures up 0.2% to 3,003.75

- STOXX Europe 600 up 0.2% to 390.44

- MXAP up 0.07% to 159.32

- MXAPJ up 0.06% to 509.14

- Nikkei up 0.09% to 22,098.84

- Topix up 0.4% to 1,622.94

- Hang Seng Index up 0.2% to 26,281.00

- Shanghai Composite up 0.3% to 2,985.34

- Sensex down 0.1% to 39,043.39

- Australia S&P/ASX 200 down 0.01% to 6,748.87

- Kospi up 0.5% to 2,101.04

- German 10Y yield rose 0.5 bps to -0.576%

- Euro unchanged at $1.0993

- Italian 10Y yield fell 9.0 bps to 0.492%

- Spanish 10Y yield fell 1.8 bps to 0.131%

- Brent futures down 0.9% to $64.20/bbl

- Gold spot down 0.1% to $1,520.39

- U.S. Dollar Index little changed to 98.64

Top Overnight News from Bloomberg

- The U.K.’s top judges dealt an unprecedented legal rebuke to Prime Minister Boris Johnson, branding his controversial decision to suspend Parliament unlawful and giving lawmakers another chance to frustrate his plans for Brexit

- German businesses gave mixed signals on economy on Tuesday, a day after a report showed manufacturing stuck in an ever deeper slump; the Ifo institute’s key business sentiment gauge rose slightly more than expected in September, recording its first gain in six months; however, all of the increase was due to the view of the current situation, and a measure of expectations continued to plunge, reaching the lowest level in a decade

- The Chinese government has given new waivers to several domestic state and private companies to buy U.S. soybeans without being subject to retaliatory tariffs, according to people familiar with the situation

- Japan and the U.S. have finished talks on a trade deal with no indication yet on how the two sides responded to Trump’s threat to slap tariffs on the $50 billion in cars and parts shipped by Japan to the U.S. annually

- Anheuser-Busch InBev NV has pulled off the year’s second-biggest IPO the second time around, raising about $5 billion in listing its Asian unit in Hong Kong two months after scrapping the original share sale

- The U.K. government has ordered an investigation into the role of Thomas Cook Group Plc’s management in the collapse of the 178-year-old tour operator

Asian equity markets traded indecisively following a similar close on Wall St where the major indices spent the day steadily recouping the opening losses brought on by weak Eurozone PMI data. ASX 200 (U/C) was choppy as outperformance in gold stocks and resilience in financials were counterbalanced by losses across the broader market, while Nikkei 225 (+0.1%) remained afloat on return from the extended weekend but with gains capped by a choppy currency and as officials scrambled to finalize a US-Japan trade deal amid uncertainty regarding auto tariffs. Elsewhere, Hang Seng (+0.2%) and Shanghai Comp. (+0.3%) traded positively after continued PBoC liquidity efforts and as the central bank suggested there was still ample monetary policy tools, although advances were initially limited by the trade-related overhang as participants mulled over the recent ebbs and flows of the US-China trade saga ahead of next month’s high level talks. Finally, 10yr JGBs gained on return from the holiday closure amid the recent temperamental US-China trade headlines and indecisive risk tone in the region, while the BoJ were also present in the market today for JPY 810bln of JGBs in the belly to the short-end.

Top Asian News

- PBOC’s Yi Says China Is ‘Not in a Rush’ to Ease Policy Massively

- Global Investors Rethink India Stocks on Historic Tax Boost

- Xiaomi Unveils First 5G Phone for China in Challenge to Huawei

- The Danger When China’s Bull Market Owes So Much to So Few

Major European Bourses (Eurostoxx 50 +0.2%) are modestly firmer, albeit off highs, in tentative trade, following a mixed AsiaPac session. The FTSE 100 is the underperformer, under pressure from sterling strength after the UK Supreme Court ruled UK PM Johnson’s decision to prorogue parliament unlawful and, as such, prorogation voided. While stocks are mostly higher, the more defensive Utilities (+1.0%), Health Care (+0.9%) and Consumer Staples (+0.5%) sectors outperform, indicative of continued apprehension in wake of yesterday’s weak EZ PMI data, although the more risk sensitive IT and Financial are also higher. Materials (-0.5%) and Energy (-0.4%) are the laggards, with the latter pressure by lower crude prices. In terms of individual movers; Aviva (+0.8%) is higher on reports the Co. is looking to sell its Singapore and Vietnam businesses in a deal which could be valued at USD 2.5bln. Ryanair (+2.7%) is up, as the airline sector continues to gain in wake of Thomas Cook’s collapse and with the news that the co.’s cabin crew have voted in favour (approx. 80%) for a four-year Collective Labour Agreement. K+S (-4.3%) is lower after being downgraded at SocGen after the co. cut guidance yesterday, while Royal Mail (-2.8%) is under pressure after a downgrade at Liberum Capital. Finally, Volkswagen (-2.6%) sunk on the news thatGerman Prosecutors had indicted CEO Diess, Chairman Poetsch and the former CEO relating to the Diesel emissions scandal.

Top European News

- German Manufacturing Drags Business Expectations to Decade Low

- Scout24 Is Said to Kick Off Sale Process for Auto-Trading Unit

- Danske’s Ex-CEO in Estonia Has Gone Missing; Police Start Hunt

- HSBC Wins EU Court Fight Over $37M Fine for Euribor Rigging

In FX, GBP was firmer after the UK Supreme Court dealt a blow to UK PM Johnson after it ruled the decision as a court matter before announcing that the suspension was unlawful. With prorogation defeated, UK MPs will return to their seats and the parliamentary session will continue as Speaker John Bercow expectedly stated that the HoC should reconvene immediately. GBP/USD touched an intraday high of 1.2487 ahead of its 21 WMA at 1.2490, although the pair then returned to pre-announced levels of around 1.2450 amid unclarity regarding the next steps alongside some profit taking. It is worth nothing that, with parliament back in session, an anti-no deal majority could continue to frustrate government efforts to find a deal with the EU/try to force a no deal. Meanwhile, the Euro had relatively uninspiring day thus far as EUR/USD remains within a tight 1.0984-97 parameter with little impetus derived from the Ifo measures which mostly topped estimates (ex-expectations), although the institute noted that the outlook for the coming months has deteriorated and the domestic economy is likely to shrink in Q3 and stagnate in Q4, a similar comment mate by IHS yesterday. In terms of option expiries, EUR/USD sees 1.3bln at strike 1.10 and 1.1bln at strike 1.1025-30 for today’s NY cut.

- AUD – Governor Lowe has aided the AUD to gain a 0.68+ status after noting that fundamental factors underpinning the longer-term outlook for the Australian economy remain strong and economy has reached a gentle turning point, a comment made at the last speech which signals that the Central Bank could stand pat on at the next meeting on October 1st. The Governor reiterated that the Board is prepared to ease monetary policy further if needed to support sustainable growth in the economy, make further progress towards full employment, and achieve the inflation target over time whilst inflation is expected to pick up, but to remain below the midpoint of the target range for some time to come. AUD/USD immediately spiked higher from 0.6784 to 0.6805 ahead of resistance at 0.6810 before consolidating around the 0.6800 mark.

- SEK – The Swedish Crown currently stands as the G10 laggard amid slightly more dovish comments from Riksbank’s Governor Ingves who noted that rates are likely to increase at a “very slow” rate over the period ahead (vs. prior “should be possible to slowly raise rates”) whilst also acknowledging low interest rates and weaker sentiment abroad. First Deputy Governor Jansson added further to the dovish fire by highlighting low Swedish inflation numbers and worrying inflation expectations, whilst adding that he sees no appreciable upside for Swedish prices. EUR/SEK, in wake of the governor’s comments, bounced further from its 100 DMA (10.66) to an intraday high of 10.71 (ahead of resistance at 10.73) before retreating below the 10.70 mark.

- EM – The Lira is staging another recovery with strength attributed to media reports that the US is said to make a new offer to Turkey regarding F-35s and Patriots system after the two Presidents’ phone call over the weekend. USD/TRY fell from an intraday high of 5.7208 to a current low of 5.6782 ahead of its 55 and 50 DMAs at 5.6779 and 5.6705 respectively. Later, Turkish President Erdogan will make a speech at the UNGA before meeting with his French counterpart Macron and UK PM Johnson and UN Secretary General Guterres

In commodities, WTI and Brent prices are weaker this morning on a rather tentative session thus far on a lack of specific newsflow for the complex, but notably ahead of the UNGA where US President Trump has stated he is to discuss Iran in his speech. He has also added that the US has lots of pressure on Iran, which does follow from the instigation of sanctions on the Iranian Bank by the US; as such, focus today will be on the remarks from Trump and if there is any reference to further sanctions or the prospect of more forceful action. In terms of scheduling proceedings at the UN are to formally begin at around 13:00BST with President Trump scheduled to arrive at the UN headquarters around 14:30BST. Elsewhere, focus turns to tonight’s API release where expectations are form a 0.6mln/bbl draw; though, ING note that the result may surprise market expectations due to the number of storm related refinery disruptions that have occurred recently. In terms of metals, Gold is little changed hovering around the USD 1520/oz mark within a tight USD 1.0/oz range for the session; ahead of risk factors including the UNGA and a number of Central Bank speakers. Separately, copper prices are overall little changed, retaining their non-committal tone from the Asia-Pac session; though the metal does remain comfortably above the USD 2.62/lb mark.

US Event Calendar

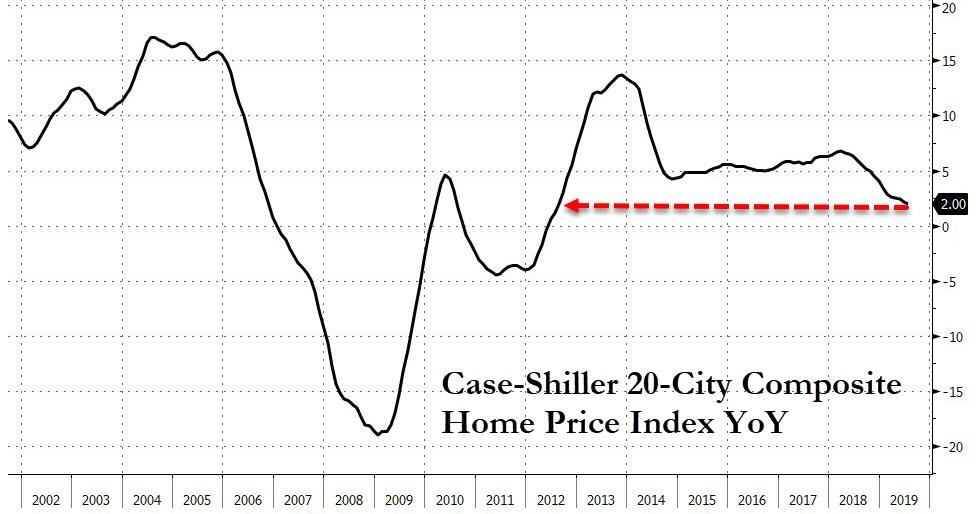

- 9am: FHFA House Price Index MoM, est. 0.25%, prior 0.2%

- 9am: S&P CoreLogic CS 20-City MoM SA, est. 0.1%, prior 0.04%; CoreLogic CS 20-City YoY NSA, est. 2.1%, prior 2.13%

- 10am: Richmond Fed Manufact. Index, est. 1, prior 1

- 10am: Conf. Board Consumer Confidence, est. 133, prior 135.1

DB’s Jim Reid concludes the overnight wrap

Fiscal policy and money printing will inevitably need to be far more joined up in the future and yesterday’s European PMIs pushed us a very small way towards this realisation. The real problem came from the worrying declines in the services sectors in Germany and France, which had previously been the beacon of hope in the recent PMIs. Germany saw the services reading fall 2.3pts to 52.5 (vs. 54.3 expected). That is a nine-month low while there was no sign of improvement in the manufacturing sector, where the reading slumped another 2.1pts to 41.4 (vs. 44.0 expected) and to the lowest in the best part of ten years. That put the composite at 49.1 – the first sub-50 reading for Germany in this cycle and the lowest reading in 83 months, while it’s also worth flagging that the new orders prints were also very worrying including manufacturing new orders at 37.9 being the weakest outside of the peak of the GFC.

As for France, the services reading fell 1.8pts to 51.6 and the manufacturing 0.8pts to 50.3, while for the Eurozone as a whole the manufacturing reading slumped 1.4pts to 45.6 and the services 1.5pts to 52.0. Those are the lowest in 83 months and 8 months respectively. As a result, the composite Eurozone reading is now at 50.4 (vs. 52.0 expected) and the lowest in 75 months. So these services readings are clearly a very concerning sign for Europe and the end result is a barely positive run rate of growth in the Eurozone right now. Let’s see what today’s IFO brings.

Unsurprisingly, bond yields fell as soon as the data was released. By the close of play 10y Bunds finished -5.8bps lower at -0.583%, OATs -6.9bps lower and BTPs -9.3bps lower. Treasuries also rallied post the Euro PMIs but got an added kicker after the US services PMI printed at a weaker than expected 50.9 (vs. 51.4 expected) before reversing the day’s rally late to close unchanged and at the higher end of a 10bps intra-day range. In fairness the services PMI was a 0.2pt improvement from September but disappointed the market at the margin. On top of that, the fact that the employment component declined into contractionary territory at 49.1 (and to the lowest in 10 years) raised a few concerned eyebrows. In fact the two-month decline for services employment is the largest since the crisis. As for the manufacturing PMI, it rose 0.7pts to 51.0 (vs. 50.4 expected) – so a modest bounce but clearly still at low absolute levels.

The moves in equity markets, at least in the US, were more muted. The S&P 500 finished down -0.01% by the closing bell last night with the NASDAQ -0.06%. European equities suffered on the poor data releases however, with the STOXX 600 (-0.80%), DAX (-1.01%) and CAC (-1.06%) all closing lower. European banks led the declines, down -2.76% on the economic weakness and bond rally. Elsewhere, Gold (+0.35%) got a slight lift from the modest risk-off while Oil was +0.95%.

Meanwhile after the US close yesterday, Treasury Secretary Mnuchin said that Chinese Vice Premier Liu He would be visiting for talks next week. Mnuchin also said that “The good news” is that the Chinese have started buying U.S. agriculture products again; “it’s a sign of good gesture,”. He also added that US farmers are important in the China trade negotiations with intellectual property “the most important issue.” The visit can be seen as a slightly positive signal as the Vice Premier was originally scheduled to visit Washington the following week. Also, as we go to print Bloomberg has reported that the Chinese government has given new waivers to several domestic state and private companies to buy US soybeans without being subject to retaliatory tariffs. For now this is likely to increase hopes that trade progress is being made.

Talking of trade, the US and Japan have finished talks on an initial trade deal with Japanese Foreign Minister Toshimitsu Motegi saying after the talks that he would explain more about the tariffs in two days’ time after a meeting of Trump and Japanese Prime Minister Shinzo Abe at the sidelines of the UNGA. He also said that he didn’t think that auto tariffs would be a cause for concern.

This morning in Asia markets are largely heading higher with the Nikkei (+0.14%), Hang Seng (+0.32%), Shanghai Comp (+0.77%) and Kospi (+0.19%) all up. Elsewhere, futures on the S&P 500 are up +0.24% while the 10y UST yield is down -2.1bps. In terms of overnight data releases, Japan’s preliminary September PMIs came out on the softer side with manufacturing standing at 48.9 (vs. 49.3 last month), marking 7 months of contraction this year, while services stood at 52.8 (vs. 53.3 last month) bringing the composite PMI to 51.5 (vs. 51.9 last month).

In other overnight news,the PBoC Governor Yi Gang said in a press briefing, with Finance Minister Liu Kun and National Bureau of Statistics head Ning Jizhe, that China must avoid massive stimulus, keep debt levels sustainable and maintain a prudent monetary policy stance while reiterating the central bank’s policy stance. The statement comes as concerns over China’s growth slowdown are mounting.

Back to yesterday, where ironically, both Draghi and Lagarde spoke post the weak PMIs although neither of their comments were particularly market moving. Draghi mostly repeated his ECB message, including suggesting that EU fiscal rules should be revisited, while Lagarde was asked on the limits of central bank policy but didn’t mention anything particularly ground-breaking. Over at the Fed, we heard from St Louis Fed President Bullard, who was alone in voting for a larger 50bp rate cut at last week’s meeting. He said that “instead of creeping down slowly I would prefer to get to where we need to be”, and voiced support for a further 25bp cut this year. Elsewhere, Williams spoke on the recent repo turmoil and said that it is “important that we examine these recent dynamics and their implications for the liquidity needs in relation to the overall amount of reserves held at the Fed”. Former NY Fed President Dudley also said he thinks the Fed will “strongly consider” a standing repo facility.

As for Brexit, sterling fell –0.39% as chief EU negotiator Michel Barnier made negative comments on a possible deal being reached, describing the UK’s current proposals on the backstop as “unacceptable.” Meanwhile the Labour Party conference rejected calls for the party to back remaining in the EU in a second referendum, instead supporting Jeremy Corbyn’s policy of a wait-and-see approach which translates as 1) get a better deal, 2) put it to a referendum, and then 3) decide whether to back the new Labour deal or remain. It’ll be interesting to see whether their position is a big political gamble or smart sitting on the fence. Given the European election results, I would have more thought the former. At their conference they also pledged to commit the UK to a 32-hour four day week within the decade. If successful I haven’t yet decided which day the EMR will cease to be published.

Looking at the day ahead, data out in Europe this morning includes September confidence indicators in France, the Sept IFO survey in Germany and August public finances and public sector net borrowing numbers in the UK. This afternoon in the US the highlight will likely be the September consumer confidence report, while the September Richmond Fed survey, July S&P CoreLogic house price data and July FHFA house price index are also to be released. Expect there to also be focus on comments from the ECB’s Villeroy and Guindos, while here in the UK the Supreme Court will be ruling this morning on PM Johnson’s suspension of Parliament.

3A/ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 8.26 POINTS OR 0.28% //Hang Sang CLOSED UP 58.60 POINTS OR 0.22% /The Nikkei closed UP 19.75 POINTS OR 0.09%//Australia’s all ordinaires CLOSED DOWN .07%

/Chinese yuan (ONSHORE) closed DOWN at 7.1068 /Oil UP TO 58.13 dollars per barrel for WTI and 63.95 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1068 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 67.1043 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

In a good will gesture China waives waivers for USA soybean purchases.

(Courtesy zerohedge)

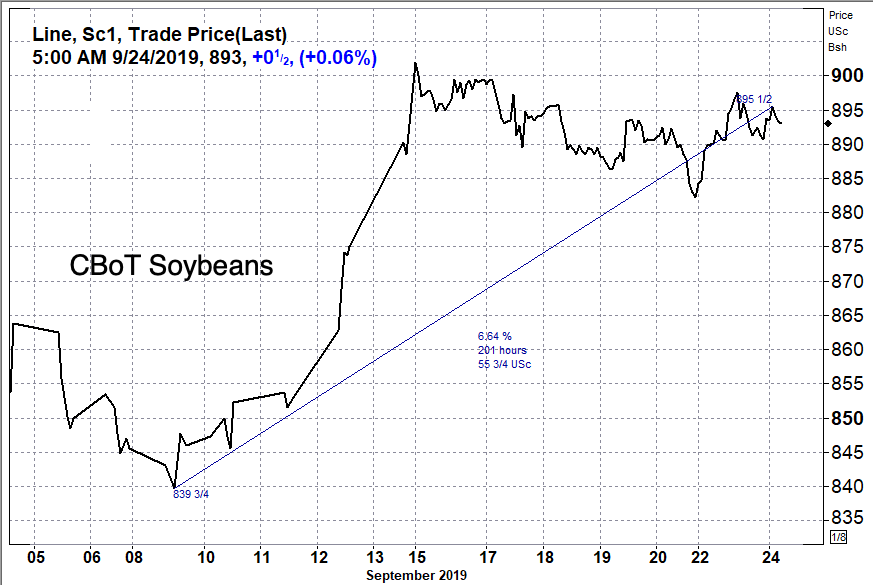

China Grants New Tariff Waivers For US Soybean Purchases

Chicago Board of Trade soybean futures have been rising for the past 14 days, a total of +6.64%, on reports, China is granting new waivers to several domestic state and private companies to purchase U.S. soybeans without being subject to tariffs, according to Bloomberg. The companies received waivers for between 2 million to 3 million tons, sources told Bloomberg. Collectively, these firms bought 20 cargoes, or about 1.2 million ton of the soybeans from the U.S. Pacific Northwest on Monday.

It depends on the news source to the exact quantity, Reuters is reporting that Chinese importers only bought 10 cargoes, or about 600,000 tons, expected to be shipped from Pacific Northwest export terminals from Oct. to Dec.

Bloomberg said state-owned buyers Cofco and Sinograin, as well as five other crushers, were awarded waivers this month to purchase U.S. soybeans.

Sources said the waivers were granted after a meeting last week with working officials; purchases of agriculture products like soybeans are seen as kind gestures ahead of a trade meeting between U.S. and China next month.

As shown below, soybeans have enjoyed a wave of buying over the past two weeks on expectations of a similar gesture of goodwill by China and positive trade war news flow.

A trade deal appeared distant late last week after Chinese officials canceled a visit to the Central and Midwest states, but confirmed Monday that the cancellation was non-trade related.

Monday’s 10 to 20 cargoes, or 600,000 to 1.2 million tons of soybeans will leave Pacific Northwest terminals in the coming months. These are some of the most significant soybean purchases since Beijing raised import tariffs by 25% on U.S. soybeans last summer in retaliation for duties on other Chinese goods.

Yet while China is repurchasing U.S. soybeans, Argentina’s Agriculture minister confirmed Monday that China has “approved the first seven crushing plants in Argentina to begin exporting soymeal to the world’s biggest consumer of the livestock feed,” reported Reuters.

Last month, we reported how China wants to build a grains ‘superhighway‘ in the South American country by dredging the Parana River, it will allow large bulk vessels to transport soybeans from the Pampas farm belt to the South Atlantic to the Pacific, and ultimately to China.

While the Trump administration celebrates China’s latest agriculture purchases – keep in mind that China wants to become fully independent from the U.S., in terms of agriculture sourcing, which is why it’s hedging itself with Argentina.

4/EUROPEAN AFFAIRS

UK

In a landmark ruling, the uK Supreme Court ruled that Johnson’s suspension of Parliament is illegal. This may hurt his chances of a no deal Brexit. It looks like his only option is an election and let the citizens decide the makeup of Parliament and Brexit

(zerohedge)

In Landmark Ruling, Top UK Court Says Johnson’s Suspension Of Parliament Illegal