GOLD:$1501.95 UP $19.30 (COMEX TO COMEX CLOSING)

Silver:$17.61 UP 33 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : $1500.20

silver: $17.56

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING 250/598

EXCHANGE: COMEX

CONTRACT: OCTOBER 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,482.000000000 USD

INTENT DATE: 10/01/2019 DELIVERY DATE: 10/03/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 H GOLDMAN 99

118 H MACQUARIE FUT 121

435 H SCOTIA CAPITAL 59

555 H BNP PARIBAS SEC 9

657 C MORGAN STANLEY 5

661 C JP MORGAN 495

661 H JP MORGAN 250

685 C RJ OBRIEN 1

686 C INTL FCSTONE 1

690 C ABN AMRO 20 8

700 C UBS 1

737 C ADVANTAGE 10 23

800 C MAREX SPEC 5 11

880 H CITIGROUP 69

905 C ADM 9

____________________________________________________________________________________________

TOTAL: 598 598

MONTH TO DATE: 8,095

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 598 NOTICE(S) FOR 59,800 OZ (1.8600 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 8095 NOTICES FOR 809,500 OZ (25.17 TONNES)

SILVER

FOR 0CT

63 NOTICE(S) FILED TODAY FOR 315,000 OZ/

total number of notices filed so far this month: 769 for 3,845,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

we are coming very close to a commercial failure!!

RUMOR just in, and that is all it is from a good source: China will soon declare Martial Law in Hong Kong, IF true, watch out!

https://finviz.com/futures_charts.ashx?t=GC

https://finviz.com/futures_charts.ashx?t=SI

Bitcoin: OPENING MORNING TRADE : $ 8232 DOWN $60

Bitcoin: FINAL EVENING TRADE: $ 8242 DOWN 42

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI FELL BY A FAIR SIZED 1022 CONTRACTS FROM 213,288 UP TO 212,266 DESPITE THE 30 CENT GAIN IN SILVER PRICING AT THE COMEX. AND WITH A SMALL EFP WE MUST HAVE HAD SOME BANKER SHORT COVERING.

TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:,

FOR OCT 0,; DEC 673 AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 673 CONTRACTS. WITH THE TRANSFER OF 673 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 673 EFP CONTRACTS TRANSLATES INTO 3.365 MILLION OZ ACCOMPANYING:

1.THE 30 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

6.255 MILLION OZ INITIALLY STANDING IN OCT

YESTERDAY, ANOTHER MAJOR ATTEMPT BY THE BANKERS TO COVER THEIR MASSIVE SHORTFALL AT THE SILVER COMEX AS ANOTHER RAID WAS INITIATED BUT IT FAILED MISERABLY. OUR OFFICIAL SECTOR//BANKERS AGAIN USED HUGE COPIOUS NON BACKED PAPER IN THEIR UNSUCCESSFUL ENDEAVOUR TO WHACK SILVER’S PRICE (30 CENT GAIN). THE TWO EXCHANGES HAD A LOSS OF 291 CONTRACTS SO WE MUST HAVE HAD SOME BANKER SHORT COVERING.

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

FOR THOSE OF YOU WHO ARE NEWCOMERS HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF OCTOBER FOR GOLD.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES, HERE IS THE BANKERS MODUS OPERANDI:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF OCT BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF OCT:

2399 CONTRACTS (FOR 2 TRADING DAYS TOTAL 2399 CONTRACTS) OR 11.995 MILLION OZ: (AVERAGE PER DAY: 1199 CONTRACTS OR 5.995 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 11.995 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 1684.09 MILLION OZ.

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ

FEB 2019 TOTALS: 147.4 MILLION OZ/

MARCH 2019 TOTAL EFP ISSUANCE: 207.835 MILLION OZ

APRIL 2019 TOTAL EFP ISSUANCE: 182.87 MILLION OZ.

MAY 2019: TOTAL EFP ISSUANCE: 136.55 MILLION OZ

JUNE 2019 , TOTAL EFP ISSUANCE: 265.38 MILLION OZ

JULY 2019 TOTAL EFP ISSUANCE: 175.74 MILLION OZ

AUG. 2019 TOTAL EFP ISSUANCE; 216.47 MILLION OZ

SEPT 2019 TOTAL EFP ISSUANCE 174.900 MILLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1022, DESPITE THE 30 CENT GAIN IN SILVER PRICING AT THE COMEX /YESTERDAY... THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 673 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 349 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 673 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1022 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 30 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $17.28 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY!!

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.081 BILLION OZ TO BE EXACT or 154% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED AT THE COMEX: 63 NOTICE(S) FOR 315,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.78.

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 6.255 MILLION OZ//

- THE RECORD WAS SET IN AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG 5458 CONTRACTS, TO 604,885 DESPITE THE $15.25 PRICING GAIN WITH RESPECT TO COMEX GOLD PRICING// YESTERDAY// /

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4784 CONTRACTS:

OCT 2019: 0 CONTRACTS, DEC> 4784 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 604,885,,. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A TINY SIZED LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 674 CONTRACTS: 5458 CONTRACTS DECREASED AT THE COMEX AND 4784 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 674 CONTRACTS OR 64,700 OZ OR 2.096 TONNES. YESTERDAY WE HAD A GAIN OF $15.25 IN GOLD TRADING….

AND WITH THAT STRONG GAIN IN PRICE, WE HAD A LOSS IN GOLD TONNAGE OF 2.096 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR WERE SUPPLYING INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON AS ANOTHER RAID WAS INITIATED AND FAILED. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE AS WELL AS UN SUCCESSFUL IN FLEECING GOLD LONGS FROM THE GOLD ARENA. THE BANKERS NO DOUBT COVERED SOME OF THE HUGE BANKER SHORT POSITIONS.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT : 15,166 CONTRACTS OR 1,516,600 oz OR 47.17 TONNES (2 TRADING DAY AND THUS AVERAGING: 7583 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 47.17 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 47.17/3550 x 100% TONNES =1.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 4454.80 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

FEB 2019 TOTAL EFP ISSUANCE: 344.36 TONNES

MARCH 2019 TOTAL EFP ISSUANCE: 497.16 TONNES

APRIL 2019 TOTAL ISSUANCE: 456.10 TONNES

MAY 2019 TOTAL ISSUANCE: 449.10 TONNES

JUNE 2019 TOTAL ISSUANCE: 642.22 TONNES

JULY 2019: TOTAL ISSUANCE: 591.56 TONNES

AUG. 2019 TOTAL ISSUANCE: 639.62 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX OF 5458 CONTRACTS DESPITE THE PRICING GAIN THAT GOLD UNDERTOOK YESTERDAY($15.25)) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4784 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE IN ACCOUNT THE 4784 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED GAIN OF 524 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4784 CONTRACTS MOVE TO LONDON AND 5458 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE LOSS IN TOTAL OI EQUATES TO 2.096 TONNES). ..AND THIS CONSIDERABLE DECREASE OF DEMAND OCCURRED DESPITE THE HUGE GAIN IN PRICE OF $15.25 WITH RESPECT TO YESTERDAY’S TRADING AT THE COMEX. WE MUST HAVE HAD SOME BANKER SHORT COVERING

THE COMEX IS NOW UNDER FULL ASSAULT WITH RESPECT TO GOLD AND SILVER.

we had: 598 notice(s) filed upon for 59800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP$19.30 TODAY//(COMEX-TO COMEX)

NO CHANGE IN GOLD INVENTORY AT THE GLD

INVENTORY RESTS AT 920.83 TONNES

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 33 CENTS TODAY:

A SMALL WITHDRAWAL OF 166,000 OZ TO PAY FOR FEES/INSURANCE

/INVENTORY RESTS AT 383.490 MILLION OZ.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

end

OUTLINE OF TOPICS TONIGHT

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A FAIR SIZED 1022 CONTRACTS from 213,288 DOWN TO 212,266 AND FURTHER FROM A NEW COMEX RECORD. THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

EFP ISSUANCE:

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

FOR OCT. 0; FOR DEC 673: AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 673 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 964 CONTRACTS TO THE 673 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 349 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 1.745 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 7.475 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY. 2.955 MILLION OZ STANDING IN FEBRUARY, 27.120 MILLION OZ FOR MARCH., 3.875 MILLION OZ FOR APRIL 18.765 MILLION OZ FOR MAY NOW 2.660 MILLION OZ FOR JUNE WITH JULY AT 22.605 MILLION OZ AUGUST AT 10.025 MILLION OZ// SEPT: 43.030 MILLION OZ//OCT: 6.225 MILLION OZ//

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 30 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY. WE ALSO HAD A STRONG SIZED 673 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

(report Harvey)

.

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED /The Nikkei closed DOWN 106.93 POINTS OR 0.49%//Australia’s all ordinaires CLOSED DOWN 1.46%

/Chinese yuan (ONSHORE) closed DOWN at 7.1483 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1483 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1536 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3A//NORTH KOREA/ SOUTH KOREA

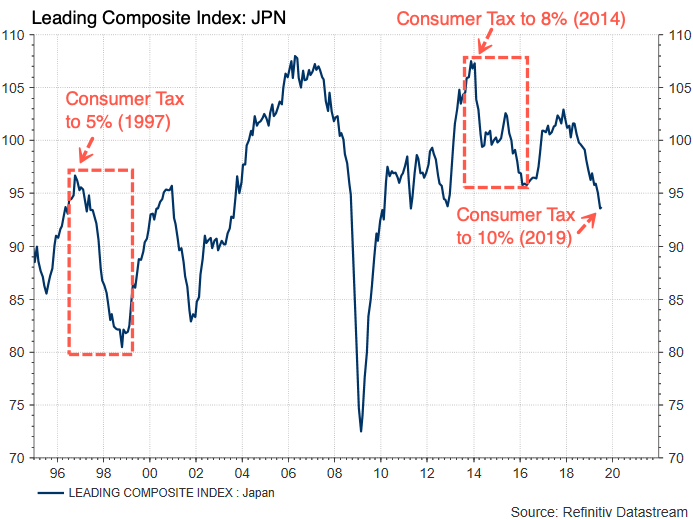

3b) REPORT ON JAPAN

This will no doubt tilt Japan into a big recession as they finally raised the sales tax to 10% form 8%

(zerohedge)

3C CHINA

4/EUROPEAN AFFAIRS

i)UK

More games from BoJo has he issues another ultimatum to the EU as Ireland bals at the new proposal of a hard line Irish backstop

(zerohedge)

iii)Europe/USA /Airbus

Europe will not be happy with this ruling. The WTO has ruled the subsidies given Airbus as illegal and now Trump can impose $7.5 billion dollars worth of tariffs on the EU

(zerohedge)

iv)And with the WTO decision, tariffs on $7.5 billion of EU imports starts onOct 18

(zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)China’s Golden week explains why gold fell on Monday. Yet in the past two days it has held up pretty good despite no China

(zerohedge)

ii)Ed Steer talks with Dr Dave Janda on the huge amount of gold standing in October

(Ed Steer/Dr Dave Janda)

10. important USA stories which will influence the price of gold/silver

MARKET TRADING//USA

a)Market trading/LAST NIGHT/USA

b)MARKET TRADING/USA/AFTERNOON

ii)Market data/USA

i)New York City ISM collapses

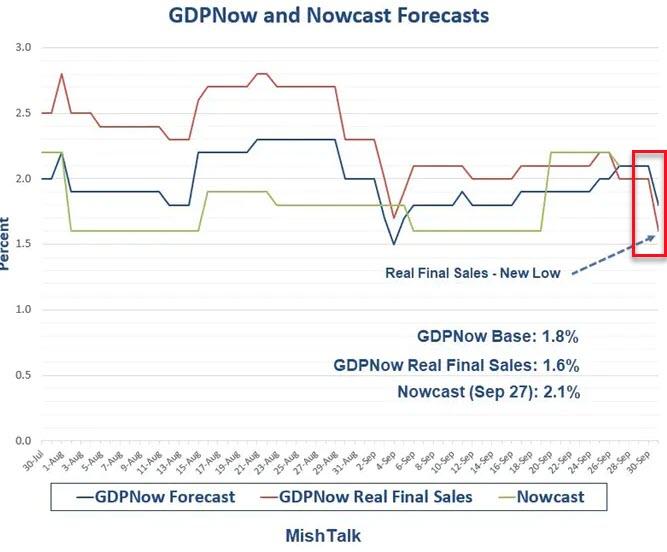

ii)Donald will not like this: GDP estimates have now fallen to 1.8% in 3rd quarter GDP due to the dismal ISM reports.(Mish Shedlock/Mishtalk)

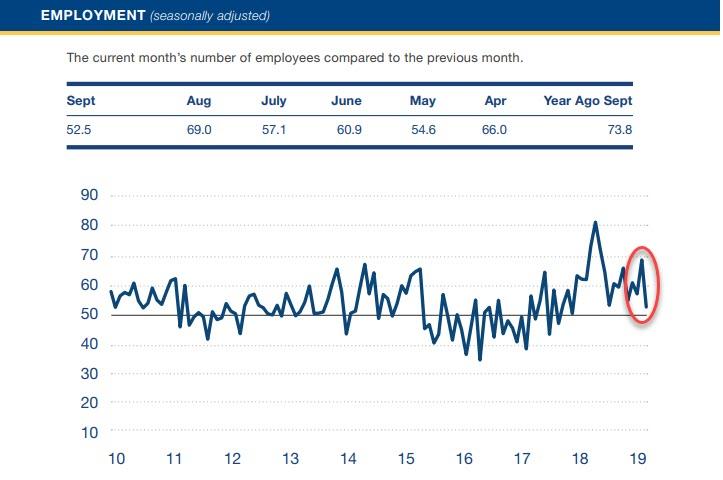

iii)the normally ebullient ADP report states that only 135,000 private sector jobs were created last month

iii) Important USA Economic Stories

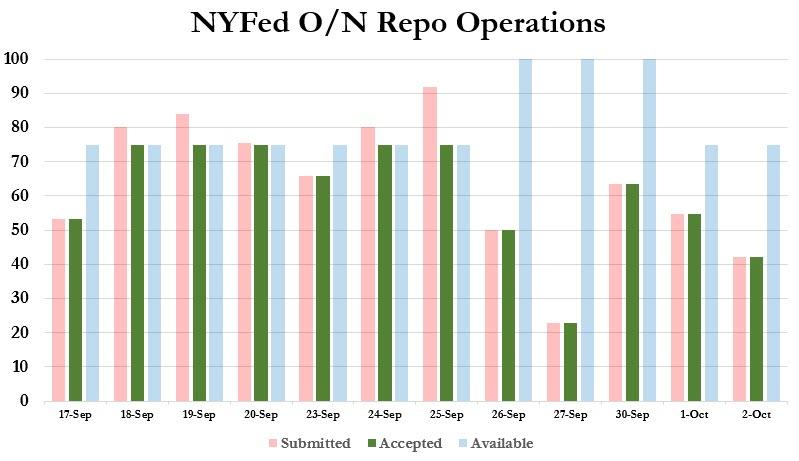

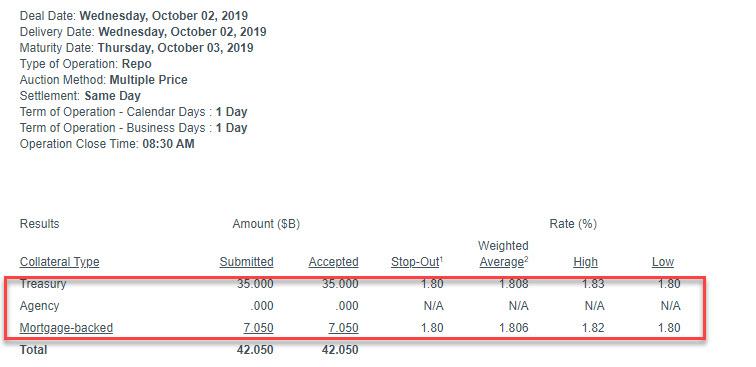

a)We still have an acute liquidity shortage as another $42 billion in repo update was recorded, This will last until Oct 10 and then we will see if the liquidity subsides or not. My guess is that Deutsche bank is in big trouble and no bank is willing to loan it money which explains the poor liquidity

(zerohedge)

b)Simon Black outlines the huge debt facing the USA and it is not getting any better

(simon Black/Sovereign Man)

c)Now this is going to get interesting..a new whistleblower says that Boeing focused in profit over safety with respect to the doomed 737 Max

d)If Trump wins the election next year, he will mostly likely ask Bullard to become chairman of the Fed

e)Here is the bank that is initially behind the Repo shock, JPMorgan.. But JPMorgan can also fronting for European banks especially Deutsche bank

iv) Swamp commentaries)

a)Fun and games with Deutsche bank’s financial “dirt” on Trump

(zerohedge)

b)Pompeo admits that he participated in a controversial call between Trump and Ukrainian President. Pompeo is angry that the Dems are bullying staff.

v) King report/Courtesy of Chris Powell of GATA which includes the major swamp stories.

LET US BEGIN:

Let us head over to the comex:

THE BANKERS SUPPLIED THE NECESSARY AND INFINITE AMOUNT OF SHORT PAPER IN GOLD. THE BANKERS FAILED IN THEIR ATTEMPT AT CONTAINING GOLD’S PRICE AS IT ROSE BY A STRONG $15.25. JUDGING BY THE STRENGTH IN GAIN OF OUR TOTAL OI CONTRACTS, THEY WERE UNSUCCESSFUL IN THE ENDEAVOUR TO FLEECE ANY UNSUSPECTING LONGS WITH THEIR ATTEMPTED RAID YESTERDAY. GOLD HAD AN UPSIDE DAY REVERSAL IN PRICE AND THAT CAUSED SOME OF OUR BANKER FRIENDS TO SHED SOME OF THEIR BANKER SHORTS….

we had 0 dealer entry:

We had 1 kilobar entries

total gold withdrawals; nil oz

ADJUSTMENTS:

i) Out of International Delaware:

a phony entry:

96,450.000 oz of fake kilobars are adjusted out of the customer account and this arrives into the dealer account

(3,000 kilobars)

ii) a real entry: 5,900.810 oz was adjusted out of the customer and this landed into the dealer account

the problem is that no gold is going from dealer to the customer to signify a settlement.

i) Into Brinks: 1,212,331.760 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

TODAY’S ESTIMATED SILVER VOLUME: 69,075 CONTRACTS (we had considerable spreading activity..accumulation

CONFIRMED VOLUME FOR YESTERDAY: 88,553 CONTRACTS..

YESTERDAY’S CONFIRMED VOLUME OF 88,553 CONTRACTS EQUATES to 442 million OZ 63.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER..makes sense!!

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.87% ((OCT 2/2019)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.36% to NAV (OCT 2/2019 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ -1.87%

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 15.00 TRADING 14.55///DISCOUNT 3.02

END

And now the Gold inventory at the GLD/

OCT 2/WITH GOLD UP $19.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 920.83 TONNES

OCT 1/WITH GOLD UP $15.25 A HUGE PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD///INVENTORY REST AT 920.83 TONNES

SEPT 30/WITH GOLD DOWN $32.50: A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.06 TONNES FROM THE GLD /INVENTORY RESTS AT 922.88 TONNES

SEPT 27.WITH GOLD DOWN $8.20 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 924.94 TONNES

SEPT 26//WITH GOLD UP $2.70 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.94 TONNES

SEPT 25/WITH GOLD DOWN $26.90 A HUGE PAPER DEPOSIT OF: 16.42 TONNES//INVENTORY RESTS AT 924.94 TONNES

SEPT 24/WITH GOLD UP $8.65 TODAY: A MONSTROUS CHANGE IN GOLD INVENTORY AT THE GLD: AN OUT OF THIS WORLD DEPOSIT OF 14.37 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 894.15 TONNES

SEPT 23/WITH GOLD UP $16.25 ON THE DAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER ADDITION OF 10.65 TONNES//INVENTORY RESTS AT 894.15 TONNES

SEPT 20/WITH GOLD UP $8.60 ON THE DAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 883.06 TONNES

SEPT 19/WITH GOLD DOWN $8.90 TODAY: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 3.23 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 883.60 TONNES

SEPT 18/WITH GOLD UP $2.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 5.86 TONNES/INVENTORY RESTS AT 880.37 TONNES

SEPT 17/WITH GOLD UP $1.50: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 874.51 TONNES

SEPT 16/WITH GOLD UP $11.75 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER WITHDRAWAL OF 5.86 TONNES FROM THE GLD///INVENTORY RESTS AT 874.51 TONNES

SEPT 13/WITH GOLD DOWN $7.75 TODAY: A BIG PAPER WITHDRAWAL OF 2.05 TONNES FROM THE GLD/INVENTORY RESTS AT 880.37 TONNES

SEPT 12//WITH GOLD UP $4.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 11/WITH GOLD UP $5.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 10/WITH GOLD DOWN $11.75 TODAY: A HUGE 7.33 PAPER TONNES OF GOLD WAS WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 882.42 TONNES

SEPT 9/WITH GOLD DOWN $4.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 889.75 TONNES

SEPT 6//WITH GOLD DOWN $9.80: A BIG CHANGE IN GOLD INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 6.15 TONNES//INVENTORY RESTS AT 889.75 TONNES

SEPT 5/WITH GOLD DOWN $33.80 TODAY: A BIG ADDITION (DEPOSIT) OF 5.86 OF PAPER GOLD TONNES PROBABLY ADDED BEFORE THE RAID/EXPECT A HUGE PAPER WITHDRAWAL TOMORROW: INVENTORY RESTS AT 895.90 TONNES

SEPT 4/WITH GOLD UP $5.00 TODAY: A BIG CHANGE: A HUGE PAPER DEPOSIT OF: 11.73 TONNES/INVENTORY RESTS AT ….890.04 TONNES

SEPT 3/WITH GOLD UP $25.60 TODAY: STRANGE: A WITHDRAWAL OF 2.05 PAPER TONNES FROM THE GLD// /INVENTORY RESTS AT 878.31 TONNES

AUGUST 30 WITH GOLD DOWN $7.00: A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.05 TONNES/INVENTORY RESTS AT 880.36 TONNES

AUGUST 29/WITH GOLD DOWN $11.65: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.09 PAPER TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS AT 882.41 TONNES

AUGUST 28/WITH GOLD DOWN $2.15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 873.32 TONNES

AUGUST 27//WITH GOLD UP $14.50 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A PAPER DEPOSIT OF 13.49 TONNES INTO THE GLD///INVENTORY RESTS AT 873.32 TONNES

AUGUST 26/WITH GOLD UP 0.25 TODAY: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.99 TONNES/INVENTORY RESTS AT 859.83 TONNES

AUGUST 23/WITH GOLD UP $28.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 854.84 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

OCT 2/2019/ Inventory rests tonight at 920.83 tonnes

*IN LAST 673 TRADING DAYS: 28.33 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 573- TRADING DAYS: A NET 138.32 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

OCT 2/2019//WITH SILVER UP 33 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 166,000 OZ TO PAY FOR STORAGE FEES/INSURANCE//INVENTORY RESTS AT 383.490 MILLION OZ//

OCT 1.2019 //WITH SILVER UP 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 1.87 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 383.656 MILLION OZ//

SEPT 30/WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 27/WITH SILVER DOWN 34 CENTS TODAY/ NO CHANGE IN SILVER INVENTORY AT THE SLV//.INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 26/WITH SILVER DOWN 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 3.975 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 381.786 MILLION OZ/

SEPT 25.//WITH SILVER DOWN 58 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 24/WITH SILVER DOWN 5 CENTS TODAY: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.338 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 377.811 MILLION OZ//

SEPT 23.2019/WITH SILVER UP 80 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 20/ WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 375.473 MILLION OZ.

SEPT 19/WITH SILVER DOWN 4 CENTS TODAY; A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 1.029 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 375.473 MILLION OZ/

SEPT 18/WITH SILVER DOWN 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 17/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 376.502 MILLION OZ//

SEPT 16/WITH SILVER UP 41 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A PAPER WITHDRAWAL OF 2.899 MILLION OZ OF SILVER LEAVES THE SLV///INVENTORY RESTS AT 376.502 MILLION OZ/

SEPT 13/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 12/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 11/WITH SILVER DOWN ONE CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 10/WITH SILVER UP 2 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 1.778 MILLION PAPER OZ OF SILVER///INVENTORY RESTS AT 379.401 MILLION OZ//

SEPT 9/WITH SILVER DOWN 6 CENTS TODAY: A MAMMOTH CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 5.425 MILLION PAPER OZ/INVENTORY RESTS AT 381.179 MILLION OZ../

SEPT 6/WITH SILVER DOWN ANOTHER 60 CENTS TODAY: A RATHER TIMID CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 842,000 PAPER OZ FROM THE SLV///INVENTORY RESTS AT 386.604 MILLION OZ//

SEPT 5/WITH SILVER WHACKED 68 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 4/WITH SILVER UP 28 CENTS TODAY:STRANGE!! A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 708,000 OZ FROM SLV’S INVENTORY:/INVENTORY RESTS AT 387.446 MILLION OZ//

SEPT 3/WITH SILVER UP 83 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 388.154 TONNES

AUGUST 29/WITH SILVER DOWN 13 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 2.714 MILLION OZ INTO THE SLV INVENTORY//INVENTORY RESTS AT 388.154 MILLION OZ/

AUGUST 28/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ/

AUGUST 27/WITH SILVER UP 52 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 26/WITH SILVER UP 23 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 1.59 MILLION OZ INTO SLV INVENTORY///INVENTORY RESTS AT 385.440 MILLION OZ//

AUGUST 23/WITH SILVER UP 37 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 383.850 MILLION OZ//

OCT 2/2019:

Inventory 383.490 MILLION OZ

(Ed Steer/Dr Dave Janda)

iii) Other physical stories:

A superb commentary from Nicholas Biezanek on the Comex fraud

(courtesy Nicholas Biezanek)

EVIDENCE of the COMEX PAPER FRAUD

Nicholas Biezanek

Whilst the obscenely clandestine EFP contract type (refer below) is clearly the principal mechanism that prevents the COMEX paper fraud from imploding, all transactions recording physical precious metal movements on the COMEX are promulgated in a format that does not link to related warehouse inventory movements. I therefore decided to download the daily COMEX reports and compile a consolidated profile of COMEX movements depicted purely in hard figures. Unfortunately this analysis of the July- Sept. 2019 quarter only started on 12th July. (These daily reports are not archived and are available only until the subsequent report is posted; in other words this succinct profile is one that the COMEX certainly does not facilitate.)

|

Registered Gold Tonnes |

Eligible Gold Tonnes |

Registered Silver Troy ozs. 000,000 |

Eligible Silver Troy ozs. 000,000 |

|

|

As at 11th July 2019 |

10.04 |

229.37 |

91.99 |

214.65 |

|

Inflow. |

0.83 |

15.37 |

5.98 |

22.48 |

|

Withdrawals |

NIL |

(0.92) |

NIL |

(20.91) |

|

Transfers (net) |

21.64 |

(21.64) |

(21.26) |

21.26 |

|

Closing at 30th Sept. |

32.51 |

222.18 |

76.71 |

237.48 |

There are also about 24 tonnes (as at 30th Sept. 2019) of kilo bars warehoused in Hong Kong. Since these are eligible stocks only, they are presumably not available to satisfy demand notices re futures contracts. Silver is an industrial metal, with many uses, so it is hardly surprising that some metal is withdrawn from the eligible category at the COMEX. August was a designated delivery month for gold and September was a designated delivery month for silver, and since the period in the table above covers the full transaction history of both these months, one might have expected just a microscopic movement on the withdrawal line above- but not even a flicker of a pulse. Moreover in this period of 80 days, less than one tonne of gold was withdrawn from the eligible category of inventory and hence the conclusion seems reasonable that the COMEX , for all intents and purposes, is effectively closed for any meaningful delivery of physical gold from either the registered or eligible category. Hence the importance of the EFP farce, discussed below.

Open Interest: As at 30th September 2019, the recorded open interest on the COMEX was stated at 1,958 tonnes of gold and 1.068 billion troy ounces of silver. As per contract law, any delivery notice can only be settled from the registered category of inventory at the COMEX, so any computation of the cover provided by the registered inventories in respect of this obscenely elevated open interest is allocating to the corrupt COMEX a dignity that it simply does not deserve, in light of the proof above that no deliveries are ever executed from either the COMEX registered inventory of either gold or silver.

Exchange for physical (EFP) transfers in the 21 months from 1st January 2018:

EFP contracts from 1st January 2018 to date, (in existence before 2018 but not monitored by Harvey Organ) total 11,971 tonnes of gold and 4,572 billion troy ounces of silver. Both these amounts are many multiples of global annual mine supply. The only certainty is that no physical metal has ever exchanged hands, but otherwise you must draw your own conclusions because of a conspiracy of silence surrounding these contracts that generate such truly gargantuan volumes. Harvey Organ posts daily a postulation of Andrew Maguire that all these obligations arising from EFP transfers are recorded as serial forward contract obligations of less than 14 days and perpetually rolled over to deceive the London Regulators which constitutes a massive criminal conspiracy to defraud. Indeed the amounts involved portend a potential catastrophic impairment to UK Bank liquidity/solvency so perhaps the maniacal suppression of precious metal is easy to comprehend. The legal doctrine of common purpose renders these UK Regulators as guilty parties in respect of this massive conspiracy .Whilst the Regulators on both sides of the Atlantic currently adopt the relatively short term expediency of simply ignoring any questions on this EFP issue, eventually any unsustainable prolonged concentration of magma inevitably seeks release directly proportionate to the intensity of its former suppression.

LBMA : The LBMA has recently managed to purge its directorate of an alleged JPM criminal, but otherwise nothing much changes at all. The holdings of precious metals as at 30th June 2019 were released at noon on 1st October and the aggregate holdings only ever vary by microscopic amounts each month. There are 7,608 tonnes of gold in loco London vaults of which 4,959 tonnes is attributed to the BOE and the residual 2,649 tonnes includes the gold allegedly held by GLD and many other ETF funds. There are 1.143 billion ounces of silver, which includes the amounts allegedly held by SLV. Since the loco London vault holdings are so metronomically constant, it is a safe assumption that the obligations imposed on the LBMA by EFP transfers from the COMEX are not discharged by delivery of any physical metal at all. Good news for holders of allocated precious metal at the LBMA is that, with a UK General Election looming, both main political parties are proposing marginal increases in the caring allowance afforded to minders of congenital idiots, and COMEX allocated account holders certainly pass the stringent qualifying criteria for lunacy with consummate ease.

ETFs: Nick Barisheff, CEO of the Bullion Management Group, recently stated that many ETFs only hold a fraction of the physical precious metal required to comply with their charters, and he cited many enabling loopholes in the rules of these opaque constructs.Egon von Greyerz also recently expounded upon this same theme. Since fractional reserving is now an established (criminal) practice prevalent throughout most custodial type enterprises, this claim intuitively seems to be more than extremely probable. ETF shareholdings can increase substantially in a matter of hours and the absurd assumption is made that somehow the requisite holding of the underlying precious metal is immediately and automatically rebalanced upwards. ETFs are clearly mechanisms whereby demand for physical precious metal is channeled into constructs that are primarily paper based and extraction of any physical precious metal from these custodians is a privilege accorded only to upper echelon insiders. Otherwise you lose.

Conclusion: Whilst in Nigeria for nine years I had to teach myself the art of revaluing a bond portfolio held at fair value (most other Nigerian companies were valuing their bonds on the’ hold to maturity’ basis).The Nigerian yield curve, whilst relatively flat, could fluctuate widely in the 12% to 24% range, so the (unrealized) consequences of this quarterly revaluation exercise were often very material. So I believe that I have a good grasp of the fundamentals of valuation in respect of bonds. I must confess, however, that I just cannot get my mind around this new child of MMT, being negative interest rates. A few years ago there was massive concern about the PIIGS and the viability of their bond obligations, but now some members of the PIIGS also enjoy negative yields on a portion of their shorter dated debt. One of the wisdoms of Sophocles was that the only true knowledge is knowledge of one’s own ignorance, so I am not ashamed of the fact that I cannot get my unreconstructed mind around this negative interest rate conundrum. Maybe, however, the sheer incomprehensibility of this insanity does not lie in the wiring in my neural network, but elsewhere.

Then I also query the vogue mantra that crypto currencies are the new ‘tulip bulbs’, but this time, (provided the global power grids hold up), their value will be eternal. I googled “how many crypto currencies are there?’ Here is the very first response: ‘The number of crypto currencies available over the internet as of 19th August 2018 is over 1600 and growing. A new crypto currency can be created at any time’. I believe my intractable scepticism is more than well founded in refusing to genuflect to this fiat ‘digital air’. Applying block chain technology to reign in the addiction of criminal banks to the practices of rehypothecation (theft) and fractional reserving would be a most welcome development, but that is a completely different matter.

So whilst MMT gains traction in the West, the Chinese and Russians have accumulated upwards of 30,000 tonnes of gold each, and the Persian Empire (Iran) has an affinity for gold dating back to at least 600 BC and the Ottoman Empire (Turkey) is a great believer in physical gold (and then there is India), the only certainty is that physical gold will regain (is currently regaining) its hegemony as the only true currency as the NEW SILK ROAD trading bloc emerges. Undeliverable, fraudulent naked short paper gold promises will be consigned to the dustbin of history and historians will ponder how the West could have been so manipulated and deceived in its devotion to paper.

end

Chris Marcus interviews Dave Kranzler and the top is the repo failure

(courtesy Chris Marcus/Dave Kranzler/IRD)

An Unavoidable Global Debt Implosion

“[Whatever] the repo failure involved, it is likely to prove a watershed moment, causing US bankers to more widely consider their exposure to counterparty risk and risky loans, particularly leveraged loans and their collateralised form in CLOs. a new banking crisis is not only in the making, for which the repo problem serves as an early warning, but it could escalate quite rapidly.” Alasdair Macleod, “The Ghost of Failed Bank Returns”

The delinquency and default rate on consumer and corporate debt is rising. This creates funding gaps and cash flow shortfalls at banks. In a fractional banking system, banks only have to put up $1 of reserve for every $9 of money loaned. When the value of the loans declines because of non-performance, it requires capital – cash liquidity – to make up the shortfall in debt service payments received by the banks. In simple terms, the banks are staring at a systemic “margin call.”

To be sure, the current repo funding shortfall may subside. But it will not fix the underlying causes (Deutsche Bank, CLO Trusts, subprime debt, consumer debt, derivatives), which are likely leading up to another round of what happened in 2008 – only worse this time.

Chris Marcus of Arcadia Economics invited me to discuss my thoughts on the meaning behind the sudden need for the Fed to inject $10’s of billions into the overnight bank lending system:

You can learn more about Investment Research Dynamics newsletters by following these links (note: a miniumum subscription period beyond the 1st month is not required): Short Seller’s Journal subscription information – Mining Stock Journal subscription information

***

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

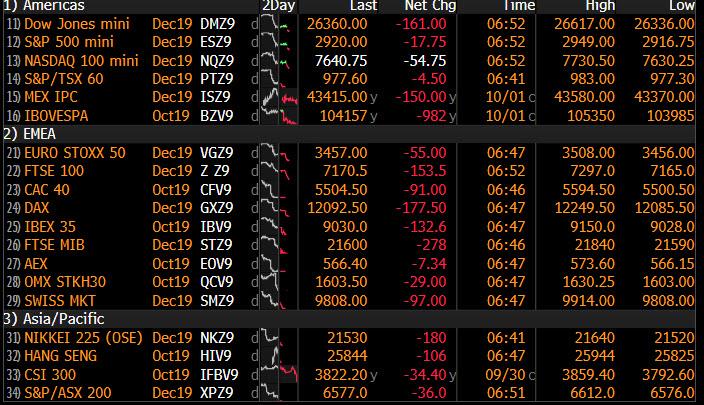

Global Stocks Tumble, Futures Slide To One Month Low As Recession Fears Rise

Global markets slumped, S&P futures dropped and European bourses tumbled as the MSCI world index dipped 0.3% to its lowest since Sept. 5, after shedding 0.83% in the previous session, after the US manufacturing ISM tumbled to more than a decade low, sparking worries a recession may now be unavoidable as the fallout from the U.S.-China trade war spreads to the U.S. economy, whose slowdown would remove the last remaining bright spot in the global economy just as Europe is falling back into recession.

S&P index futures retreated with Asian shares as miserable manufacturing data from the world’s largest economy continued to reverberate around markets. The dollar advanced. The S&P Emini dropped to 2,920, the lowest level since September 4; one day earlier the S&P 500 lost 1.23% to hit four-week lows after a disastrous ISM print.

Markets had been expecting the index to rise back above the 50.0 mark denoting growth: “Historically, equity returns are worst when the ISM manufacturing drops from levels below the 50 threshold,” Patrik Lang, head of equity research at Julius Baer. “Uncertainty around the US-China trade war is obviously the main reason for the weakness, with companies exposed to global trade increasingly putting off investment decisions.”

European shares opened lower, with London stocks lagging the most on fresh Brexit drama. The pan-European STOXX 600 index was down almost 1 percent.

European stocks tumbled, the Stoxx 600 sliding more than 1%, with all sectors in the red led by miners, construction and chemical producers, falling 1.4% or more. The gauge slid for a second day after reaching a one-year high on Monday. The Basic Resources Index (SXPP) dropped for a third day, losing as much as 1.8%, as sentiment continues to sour following the string of poor data released on Tuesday: diversified miners all fell with BHP Group -1.7%, Anglo American -1.7%, Rio Tinto -2%, and Glencore -1.4%. The FTSE 100 was among the worst performers after PM Johnson issued a hard Brexit ultimatum to the EU and prepared to announce his final Brexit offer. Bunds drifted lower, peripheral spreads trade around the tightest levels of the week as curves continue to bear steepen.

Adding to investor anxieties, European companies are set for their worst quarterly earnings in three years as revenue drops for the first time since early 2018, according to the latest Refinitiv data.

“Our base case is that trade tensions will remain elevated, and we expect global growth to slow in 2020 to its slowest pace since the global financial crisis,” said Mark Haefele, chief investment officer at UBS Global Wealth. “We don’t rule out a worsening of the trade situation over the next six to 12 months.”

Earlier in the session, Asian stocks also dropped, with the MSCI ex-Japan Asia-Pac index dropping 0.8%, led by material and technology firms, as investors pared exposure to risk assets following dismal U.S. factory data and violent protests in Hong Kong. All major markets in the region were down, with Singapore and Indonesia leading declines, Australian shares falling 1.5% and South Korean shares shedding 1.95%. China markets are closed for a one-week holiday. Japan’s Nikkei slid 0.5% and the Topix dropped 0.4%, dragged by electronics makers including Keyence and Sony. Automakers also fell after weak U.S. auto sales in September.

While markets in China and India were closed for holidays, Hong Kong’s Hang Seng Index declined 0.2%, as Tencent Holdings and HSBC Holdings weighed. The index fell as much as 1.2% in early trade. On Tuesday, Hong Kong police shot a teenage protester, the first to be hit by live ammunition in almost four months of unrest in the Chinese-ruled city. Protesters and police battled across the city in some of the most serious clashes since widespread unrest began in June.

Adding to tensions in Asia, North Korea carried out at least one more projectile launch on Wednesday, a day after it announced it will hold working-level talks with the United States at the weekend. Japanese Cabinet Minister Suga said the launch did not directly impact Japan but one North Korean ballistic missile landed inside the Exclusive Economic Zone (EEZ) and one outside. Japanese PM Abe condemned the North Korea launches and added that it violates UN resolutions. Further, Japanese PM Abe will hold a meeting of the National Security Council to decide how to respond to the projectile firings. In terms of details, South Korean Defence Ministry said the missiles launched by North Korea have a range of circa 1300km and was likely launched at a higher apogee to decrease range and could have been fired from a submarine. Japan has not yet determined whether North Korea’s missiles were Submarine-launched ballistic missile and notes it may have been one missile which split into two. The White House said it is aware of the launch and is monitoring the situation.

In rates, yesterday’s early hours Rates selloff is all but a distant memory now, as a disastrous US ISM print has again kicked-off another “global growth scare” that is rallying Bonds / havens, as Nomura’s Charlie McElligott writes. Eurozone bond yields inched up after another speech from outgoing ECB chief Mario Draghi calling for fiscal stimulus to boost the region’s sluggish economy.

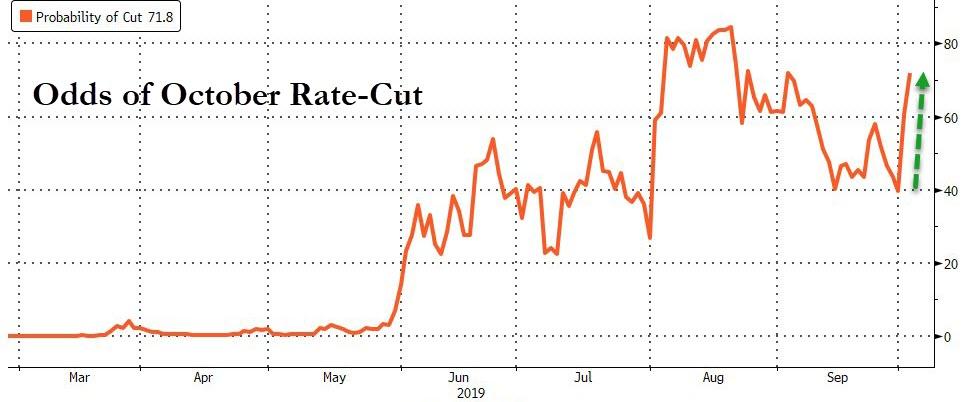

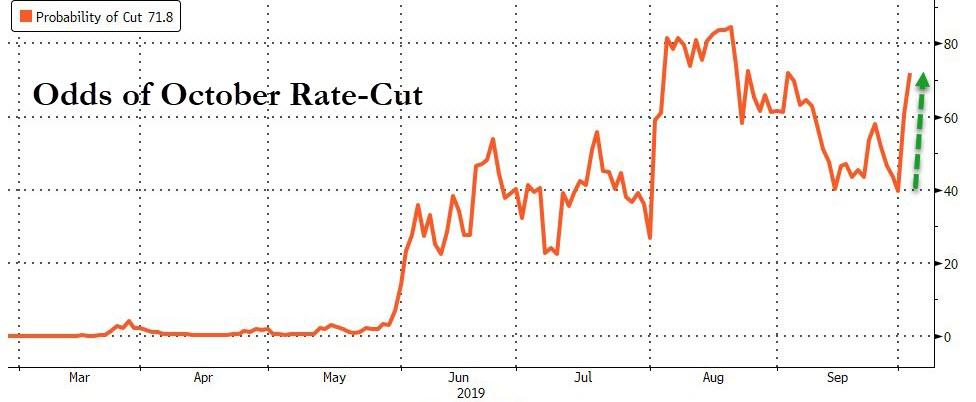

The recent poor data lifted the Fed funds rate futures price sharply, with the November contract now pricing in about an 80% chance the U.S. Federal Reserve will cut interest rates on Oct. 30, compared to just over 50% before the data. Even so, the dollar rebounded to fresh two years highs after sliding in Tuesday’s session. The index that measures the greenback against a basket of peers was up 0.16%.

Elsewhere in FX, the yen rose to 107.7 from Tuesday’s low of 108.47. The euro fell 0.15% to $1.0915 EUR while the Australian dollar traded at $0.6693, having hit a 10-1/2-year low of $0.6672 the previous day after the Reserve Bank of Australia cut interest rates and expressed concern about job growth.

In commodities, gold rose to $1,479.13 per ounce from a two-month low of $1,459.50 hit on Tuesday on the back of a robust U.S. dollar. The weak U.S. data pushed oil prices to near one-month lows, although a surprise drop in U.S. crude inventories helped them to rebound. Brent crude futures rose 0.2% to $59.01 a barrel, after hitting a four-week low of $58.41 on Tuesday, while West Texas Intermediate crude gained 0.69% to $53.99 per barrel after hitting a one-month low of $53.05.

Expected data include mortgage applications and ADP employment change. Acuity Brands, Lamb Weston, Lennar, and Paychex are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.4% to 2,926.50

- STOXX Europe 600 down 1% to 383.94

- MXAP down 0.6% to 155.99

- MXAPJ down 0.8% to 497.74

- Nikkei down 0.5% to 21,778.61

- Topix down 0.4% to 1,596.29

- Hang Seng Index down 0.2% to 26,042.69

- Shanghai Composite down 0.9% to 2,905.19

- Sensex down 0.9% to 38,305.41

- Australia S&P/ASX 200 down 1.5% to 6,639.94

- Kospi down 2% to 2,031.91

- German 10Y yield rose 2.5 bps to -0.539%

- Euro down 0.2% to $1.0914

- Italian 10Y yield rose 3.4 bps to 0.518%

- Spanish 10Y yield rose 1.5 bps to 0.167%

- Brent futures down 0.3% to $58.73/bbl

- Gold spot up 0.1% to $1,480.55

- U.S. Dollar Index up 0.2% to 99.32

Top Overnight News from Bloomberg

- Boris Johnson is poised to issue an ultimatum to the European Union on Wednesday: negotiate Brexit on his terms within the next nine days, or face a no-deal divorce. A key EU player has already rejected the prime minister’s plan

- The ECB began its official transition to a new benchmark short-term interest rate Wednesday, as global regulators move away from tainted Libor gauges. The new rate, known as ESTR, which reflects overnight borrowing costs of banks in the monetary bloc, fixed at -0.549% for Oct. 1, the central bank said on its website

- Germany’s five leading research institutes slashed their forecasts for economic growth, as manufacturers in Europe’s biggest economy struggle with waning global demand and lingering trade disputes. GDP will expand by 1.1% in 2020, they predicted, down from 1.8% forecast in April

- Japan’s struggling government bond market shows just how vulnerable it can be to the whim of the central bank. JGBs generated the smallest return among all 46 sovereign debt markets tracked by Bloomberg in the third quarter, gaining less than 0.6% amid a global bond rally. They lost 1.1% in September

- North Korea fired what appeared to be a ballistic missile designed for submarines, testing President Donald Trump’s tolerance for weapons tests just hours after agreeing to restart stalled nuclear talks with the U.S.

- European Union governments have discussed giving the U.K. a major concession on Brexit by possibly time-limiting the contentious backstop mechanism for the Irish border, two people familiar with the matter said. A time limit would only be on offer if the U.K. accepted a backstop which would keep Northern Ireland in a customs union with the bloc

- Brazilian President Jair Bolsonaro’s proposal to overhaul Brazil’s pension system and rein in public debt passed a first of two votes on the senate floor late on Tuesday.

- North Korea fired what appeared to be a submarine-based ballistic missile off its eastern coast Wednesday in an escalation that came just hours after saying it would resume stalled U.S. nuclear talks

- The European Central Bank begins its official transition to a new benchmark short-term interest rate Wednesday, as global regulators move away from tainted Libor gauges

- Ukrainian President Volodymyr Zelenskiy said he never met or talked by phone with Donald Trump’s personal lawyer Rudy Giuliani, whose contacts in Ukraine are part of an impeachment inquiry in Washington

Asian equity markets took the cue from the negative lead on Wall Street where the major indices declined on the first day of Q4 after US ISM Manufacturing PMI contracted to its worst level since June 2009. Losses in ASX 200 (-1.5%) accelerated after NAB shares tumble 3% amid an additional AUD 1.2bln charge relating to increased provisions for customer-related remediation, whereas upside in the Nikkei 225 (-0.5%) was limited by the unfavourable currency flow, whilst Toyota shares slumped due to poor North American vehicle sales and Sony remained near the bottom of the index after cutting streaming prices ahead of Google’s Stadia launch. Elsewhere, the Hang Seng (-0.2%) climbed off lows after returning from a long weekend, albeit oil giants remained pressured after Norway’s Sovereign Wealth Fund received the green light to sell USD 6bln worth of oil and gas stocks, meanwhile upside in the index was capped by the ongoing situation in Hong Kong as protestors vowed to step up action after a police officer shot a teenager yesterday. Meanwhile, South Korea’s KOSPI (-2.0%) was pressured after North Korea fired short-ranged projectiles towards the East Sea. As a reminder, Mainland China and Indian markets were closed today due to public holidays.

Top Asian News

- U.K. Protests Slows Down Mainland Visitor National Day Arrivals

- Israel Plans to Boost Supply in Landmark Gas Deal With Egypt

- Bears Retreat From Turkey Stocks as Real Returns Draw Buyers

- SoftBank Debtholders Hope For More Caution After WeWork Woes

Major European Bourses (Euro Stoxx 50 -1.3%) are firmly lower, amid a lack of fresh bearish fundamentals, as the region more takes its cue from a negative AsiaPac lead; sentiment was downbeat overnight following Wall Street underperformance after bad US ISM Manufacturing data, the latest missile test launch out of North Korea and ongoing tensions in Hong Kong. Looking ahead, at 15.00 BST the WTO is expected to announce its decision on the US’ right to retaliate to against the EU over their Airbus (-0.8%) subsidies, a potential source of impetus. Prior reports have suggested the ruling will allow the US to impose tariffs on roughly USD 8bln of EU imports on a wide range of products. Sectors are also firmly in the red; Materials (-2.1%), Industrials (-1.7%) and Energy (-2.0%) (despite slightly higher crude prices) are leading the sectors lower while Consumer Staples (-0.9%), Telecoms (-0.8%) and Utilities (-1.0%) hold up comparatively better. In terms of individual movers; Flutter Entertainment (+18.4%) shot higher on the news of the co.’s merger with Stars Group, pulling other betting names higher such as William Hill (+4.3%) higher in tandem. Nestle (-0.2%) shares are being supported by the Co.’s sale of its Skin Health unit. Tesco (+0.6%) managed to reverse early losses and now trades higher, after the co. released decent earnings premarket, but its CEO resigned. Pernod Ricard (+0.7%) is higher after being upgraded at Jefferies. Luxury names including LVMH (-2.0%) and Richemont (-2.1%) underperformed the market, with bad retail data out of Hong Kong (the largest decline on record) weighing.

Top European News

- ECB Begins Transition of Benchmark Short-Term Interest Rate

- German Fiscal Stimulus Already Creeping In, Whatever Merkel Says

- Lenders Selling Loan Exposures to Thomas Cook at 90% Discount

- Metro Bank Founder Hill to Leave Board Early as Stock Slides

In FX, the Dollar has clawed back some losses following yesterday’s abrupt U-turn from new 2019 highs in the DXY with the index bouncing firmly ahead of 99.000 towards 99.420, as attention switches to NFP via ADP and hopefully better news from the services side of the US economy after the more pronounced ISM manufacturing activity slowdown. However, the Greenback is also benefiting from renewed weakness in rival currencies and general risk aversion awaiting the WTO ruling on the extent that the US can counter EU subsidies for Airbus and repercussions in Brussels after UK PM Johnson delivers his latest/last Brexit proposal.

- CHF/GBP – The clear G10 underperformers, with the Franc deflated on weak Swiss CPI grounds, further SNB guidance from Maechler expounding the virtues of NIRP allied to direct FX intervention and the KOF cutting growth and inflation estimates, while the Pound has been hit by a dire UK construction PMI and the ongoing political/Irish border wrangling. Consequently, Usd/Chf is back up near parity and Cable has recoiled from 1.2300+ towards Tuesday’s low only a few pips away from the big figure below, with the focus turning to Johnson’s appearance at the Tory Party conference from noon.

- NZD/AUD – The Aussie and Kiwi are also unwinding/reversing post-US ISM manufacturing gains, as Aud/Usd returns to ytd lows circa 0.6670 and Nzd/Usd retests bids protecting 0.6200 alongside YUAN depreciation in holiday-thinned trade.

- EUR/CAD – Holding up a bit better than most major counterparts, but some way off best levels vs the Buck as the single currency failed to sustain momentum through 1.0950 and Loonie could not breach 1.3200 amidst confirmation of more German GDP forecast downgrades and a downturn in crude prices.

- JPY – Bucking the broad, if not overall trend, safe-haven demand/positioning has kept the Yen elevated between 107.90-55 against the Dollar, and from a chart perspective the 100 DMA in Usd/Jpy (now around 107.76) remains pivotal.

- EM – Rand in the spotlight ahead of ANC judgment on the latest SA growth plan and following the SARB’s semi-annual MPR, with some technical support coming from a pull-back from 1 month peaks in Usd/Zar around 15.4000 to almost 15.3000 at one stage.

- Goldman Sachs economists say the RBA’s internal economic model suggests the Central Bank will need to release a USD 200bln QE programme to achieve its unemployment and inflation targets. (AFR)

In commodities, the crude complex is mixed, giving away the majority of overnight gains, where the complex bounced from post US ISM Manufacturing data lows helped by a bullish headline API print, as risk sentiment took a turn for the worse at the European open. WTI and Brent currently sit just below the USD 54.00/bbl and USD 59.00/bbl levels respectively. To the downside technicians will be eyeing the USD 53.00/bbl handle in WTI; yesterday’s low and the late August/early September base. After yesterday’s choppy session, which saw Gold price swings of north of USD 40/oz, the precious metal is lacklustre and seemingly awaiting further macro drivers in the form of today’s ADP employment report, ISM Non-manufacturing tomorrow and NFP on Friday. In fitting with fragile risk sentiment, Copper remains under pressure as global growth concerns linger, albeit the red metal is off yesterday’s post ISM Manufacturing data lows.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -10.1%

- 8am: Fed’s Barkin Speaks at a Conference on the Rural Economy

- 8:15am: ADP Employment Change, est. 140,000, prior 195,000

- 9am: Fed’s Harker Speaks at Community Banking Conference

- 10:50am: New York Fed’s Williams Speaks in San Diego

DB’s Jim Reid concludes the overnight wrap

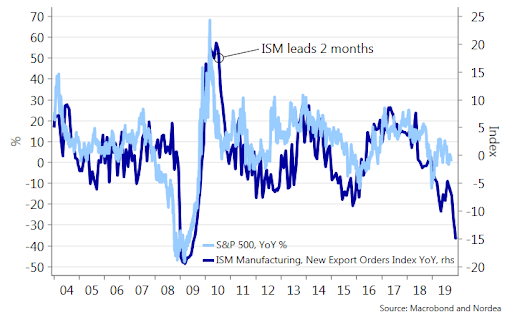

The warning signs that we got from the Chicago PMI data on Monday turned out to be correct with yesterday’s shocking ISM manufacturing print being the talk of the town in markets. Indeed the headline was the decade-low September print of 47.8, a 1.3pt decline from August and also well below expectations for a 50.0 reading. In fact it was below even the lowest economist’s forecast on Bloomberg. The details were arguably even more concerning though. New orders (47.3 vs. 47.2 previously), employment (46.3 vs. 47.4) and production (47.3 vs. 49.5) all either remained soft or deteriorated further.Only 3 of the 18 industries in the survey reported growth, the lowest figure since 2009. In addition, the leading indicator new exports component slumped to 41.0. The last time it was lower was during the depths of the GFC in March 2009, and if we look at the full 380 months’ of history, this index has only been lower than it is right now on 6 occasions.

We updated our simple equity versus PMI model last night following the latest slug of data and unsurprisingly the equity markets in Europe and the US now appear overvalued on this metric. This is most severe in Germany (20%), Italy (16%) and the Eurozone (14%) as a whole. The S&P 500 is 6% overvalued relative to the latest ISM however interestingly it’s the reverse in Asia where the Nikkei and Shanghai Comp are actually 8% and 13% cheap respectively. For Europe it’s worth noting that current equity market pricing imply PMIs around 50 while the S&P 500 implies an ISM of 50.4. So pricing bad news but not this bad. Although this analysis is based on the historical relationship between PMIs/ISMs and equities it’s fair to say that rarely has there been such a long standing and wide gap between manufacturing and services. So there is still hope if services buck the historical trend and hold up but there have been cracks of late. So all eyes on tomorrow’s services readings.

What is hard to argue with is that the global manufacturing sector is now very much in a recession. This now makes an already important Fed meeting later this month even more of a crucial risk event. With that in mind it’s worth noting that there are only 20bps of cuts priced in for this month’s meeting, albeit up from 14.5bps on Monday. Markets do seem to be having a somewhat hard time pricing in a more dovish Fed, though the pricing could also reflect expectations for another IOER adjustment. Our US economists do expect a cut this month.

By the end of the session yesterday, the S&P 500 was down -1.23%, off -1.75% from its pre-ISM highs. The NASDAQ (-1.13%) and DOW (-1.28%) were down similar amounts. In Europe the STOXX 600 (-1.31%) turned in its worst performance in six weeks. The domestic PMI revisions hardly made for any more comfortable reading on the continent (more on those below).

Meanwhile the trend in rates prior to the ISM was for yields to move higher following the big sell-off in JGBs just over 24 hours ago. That quickly reversed once the data was out with 2y and 10y Treasuries closing down -7.8bps and -2.9bps respectively, and -13.4bps and -12.0bps off the intraday highs. President Trump tweeted shortly after the data came out and called the Fed “pathetic” and that “they don’t have a clue” however that didn’t move the dial in markets. The curve steepened +5.5bps to 8.9bps last night and sits at 10.4bps this morning while in Europe Bunds retraced a +6.1bps selloff to end the session just +0.7bps higher. Elsewhere, the end result in credit was for US HY spreads to widen +8bps while the risk off helped Gold (+0.55%) and safe haven currencies like the Yen (+0.36%) and Swiss Franc (+0.55%).

Separate from the macro news, stock markets were also jolted yesterday by the announcement by Charles Schwab Corp (-9.74%) that they will eliminate online trading commissions for stocks, ETFs, and options. The prominent brokerage is locked in a price war with its main competitors as more and more assets shift toward lower-fee and passive investment strategies. E*Trade Financial (-16.43%) and TD Ameritrade (-25.83%) both saw steep selloffs in response.

This morning in Asia equity markets have followed the US lower, with the Nikkei (-0.65%) and the Hang Seng (-0.54%) both losing ground. South Korea’s KOSPI (-1.35%) was one of the worst performers, which came as the country’s military said that it detected a North Korean missile launch that flew 450km. It comes just hours after North Korean state media said that they would start further denuclearization talks with the US this weekend. Meanwhile 10yr JGBs are down -1.9bps at time of writing, 10yr USTs back up +2.5bps, with S&P futures up +0.20%.

Onto Brexit where there’s been a lot of developments over the last 12 hours with more likely today. A Bloomberg story as London went home caused a bit of a stir yesterday, which suggested that the EU is considering accepting a time limit on the Irish backstop, though it did later emphasise that the deliberations have only been between EU capitals, not with the UK. An EU spokesperson later said that the EU are not considering this, while an Irish government spokesman said it hadn’t been discussed.

Mr. Johnson will give a key speech today at the Conservative Party conference where more Brexit news will follow. It’s expected firm Brexit proposals will be sent to the EU soon after the conference ends – possibly within 24 hours. So a potentially big couple of days ahead. The overnight reporting suggested that he will offer a plan which will include “two borders for four years;” with a time-limited backstop for Northern Ireland that is separate from the UK. If so and as mentioned above, it is unlikely that the EU will agree to such a plan, which would require customs checks between Northern Ireland and the Republic of Ireland. The Irish finance minister has already been quoted as saying that if this is the plan then “that in itself is bad faith”. So today could be the beginning of the end for any hopes of a deal ahead of the EU council meeting in two weeks.

Back to the data yesterday, where the PMIs in Europe where little changed at the final revision. Indeed the Eurozone reading was nudged up 0.1pts to 45.7 with Germany revised up 0.3pts to 41.7 but France revised down 0.2pts to 50.1. The countries outside of Germany and France were within the margin of error of what was implied by the flash PMIs while the US reading was revised up 0.1pts to 51.1 and contrasting with the more widely followed ISM equivalent. Overall we counted a total of 35 manufacturing PMIs/ISMs around the globe yesterday and 18 were below 50 with the unweighted average being 48.9. Award for the highest reading went to Greece! And the lowest South Africa.

Away from the data and on to the policy front, where there was a slew of speeches from Fed and ECB officials yesterday, but almost no new substantive information. In the US, Vice Chair Clarida and Governor Bowman both spoke but avoided talking about the economy or rates. Chicago President Evans reiterated his recent (surprising) hawkish shift by repeating that he expects policy to be on hold “for some time.”

As for the ECB, outgoing President Draghi spoke again about the need for fiscal support and cited an argument we used in our long term study that fiscal is much more powerful when monetary policy is close to the effective lower bound (see pages 47-51 of the note here ). Meanwhile Bundesbank President Weidmann pushed back against the Draghi’s recent call for unanimity. Last week, Draghi had said in testimony that “the form in which dissent is made known is very important (…) in order not to undermine the effectiveness of our decisions.” Weidmann yesterday criticised that argument, albeit without singling Draghi out by name, saying that “intensive discussions” regarding policy, including QE, are “absolutely necessary.” Incoming President Lagarde will have her hands full when she inherits the Presidency next month.

To the day ahead now which is a very quiet one for data releases with the only print due this morning being the September construction PMI in the UK, while in the US the September ADP employment change is due. The consensus for the latter is for a 140k print, following a 195k reading in August. Away from the data we’ve got scheduled comments from the Fed’s Barkin, Harker and Williams this afternoon.

3A/ASIAN AFFAIRS

I)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED //Hang Sang CLOSED /The Nikkei closed DOWN 106.93 POINTS OR 0.49%//Australia’s all ordinaires CLOSED DOWN 1.46%

/Chinese yuan (ONSHORE) closed DOWN at 7.1483 /Oil UP TO 57.21 dollars per barrel for WTI and 64.13 for Brent. Stocks in Europe OPENED MIXED// ONSHORE YUAN CLOSED DOWN // LAST AT 7.1483 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.1536 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

This will no doubt tilt Japan into a big recession as they finally raised the sales tax to 10% form 8%

(zerohedge)

Japan Hikes National Sales Tax Despite Recession Fears

Japan has increased its national sales tax to 10% from 8% on Tuesday, a significant policy change that could tilt the world’s third-largest economy into recession by depressing consumer sentiment, reported Market Watch.

The last two times policymakers increased the sales tax, 2-point rise to 5% in 1997 and another to 8% in 2014, an economic contraction shortly followed.

Prime Minister Shinzo Abe twice delayed the tax hike in recent years.

Abe has indicated the tax is now unavoidable given the demographic challenges in the aging country. He said the tax would help pay down the enormous national debt, and position the country towards more financial responsibility in balancing the budget by 2025. But taxing the consumer as the economy is deteriorating could be a recipe for economic disaster in 2020.