JULY 2//BANKERS AMBUSHED IN GOLD AS LONGS WAITING IN THE BUSHES TO OBTAIN CHEAP GOLD: GOLD UP$7.00 TO $1777.90//SILVER UP 4 CENTS TO $18.01//GOLD TONNAGE STANDING AT THE COMEX; 17.38 TONNES//SILVER OZ STANDING: 82.9 MILLION OZ//CORONAVIRUS UPDATE//USA COUNTERS THE CHINA NATIONAL SECURITY LAW WITH HUGE SANCTIONS ON POBC MEMBERS AND BANKS// MICHAEL EVERY.. A MUST READ…//ANOTHER ERROR FILED JOBS REPORT: TAKE IT WITH A GRAIN OF SALT//GHISLAINE MAXWELL ARRESTED//MORE SWAMP STORIES FOR YOU TONIGHT/////

GOLD:$1777.90 UP $7.00 The quote is London spot price

Silver:$18.01// UP 4 CENTS London spot price

Closing access prices: London spot

i)Gold : $1775.50 LONDON SPOT 4:30 pm

ii)SILVER: $17.95//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1789.50 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /: $11.60

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $18.23…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 30 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $29.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

TOMORROW WE WILL HAVE THE JOBS REPORT AND AS USUAL, THEY WHACK THE DAY BEFORE/

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 229/641

ISSUED 486

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,773.200000000 USD

INTENT DATE: 07/01/2020 DELIVERY DATE: 07/06/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 16

072 H GOLDMAN 63

099 H DB AG 47

135 H RAND 2

152 C DORMAN TRADING 8

159 C ED&F MAN CAP 1

355 C CREDIT SUISSE 3

357 C WEDBUSH 1

624 C BOFA SECURITIES 4 2

657 C MORGAN STANLEY 23

657 H MORGAN STANLEY 131

661 C JP MORGAN 486 229

686 C INTL FCSTONE 2

690 C ABN AMRO 28

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 25 35

800 C MAREX SPEC 75 76

878 C PHILLIP CAPITAL 4 6

905 C ADM 12

____________________________________________________________________________________________

TOTAL: 641 641

MONTH TO DATE: 4,441

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 641 NOTICE(S) FOR 64100 OZ (1.9937 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 4441 NOTICES FOR 444100 OZ (13.813 TONNES)

SILVER

FOR JULY

744 NOTICE(S) FILED TODAY FOR 3,720,000 OZ/

total number of notices filed so far this month: 13,012 for 65,060,000 MILLION oz

BITCOIN MORNING QUOTE $9192 DOWN 40

BITCOIN AFTERNOON QUOTE.: $9093 DOWN $192

GLD AND SLV INVENTORIES:

WITH GOLD UP $7 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES OF GOLD INTO THE GLD//

GLD:1,182.11 TONNES OF GOLD//

WITH SILVER UP 4 CENTS TODAY: AND WITH NO SILVER AROUND

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//

IN SILVER THE COMEX OI FELL BY A CONSIDERABLE SIZED 20066 CONTRACTS FROM 169,418 UP TO167,352, AND FURTHER FROM OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED LOSS IN OI OCCURRED DESPITE OUR STRONG 23 CENT LOSS IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE LOSS IN COMEX OI IS PRIMARILY DUE TO THE CONCLUSION OF OUR SPREADER LIQUIDATION (AS WE END JUNE)_, ALONG WITH SOME BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, SOME LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET LOSS IN OUR TWO EXCHANGES OF 1732 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 334 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 334 CONTRACTS. WITH THE TRANSFER OF 489 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 334 EFP CONTRACTS TRANSLATES INTO 1.67 MILLION OZ ACCOMPANYING:

1.THE 23 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

82.860 MILLION OZ INITIALLY IN JULY.

WEDNESDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL 23 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE NO DOUBT SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS. THE STRONG LOSS AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL DECLINE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) SOME LONG LIQUIDATION AS WE DID HAVE A STRONG NET LOSS OF 1732 CONTRACTS OR 8.660 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

823 CONTRACTS (FOR 2 TRADING DAY(S) TOTAL 823 CONTRACTS) OR 4.115 MILLION OZ: (AVERAGE PER DAY: 411 CONTRACTS OR 2.057 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 4.115 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 0.58% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,141.52 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 4.115 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2066, WITH OUR 23 LOSS LOSS IN SILVER PRICING AT THE COMEX ///WEDNESDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 334 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE LOST A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 1732 CONTRACTS (WITH OUR 23 CENT LOSS IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 334 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED DECREASE OF 2066 OI COMEX CONTRACTS. AND ALL OF THISDEMAND HAPPENED DESPITE A 23 CENT LOSS IN PRICE OF SILVER/AND A CLOSING PRICE OF $17.97 // WEDNESDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.8370 BILLION OZ TO BE EXACT or 119% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 744 NOTICE(S) FOR 3,720,000 MILLIONOZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 82.860 million oz

THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A CONSIDERABLE SIZED 6080 CONTRACTS TO 554,173 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CONSIDERABLE SIZED LOSS OF COMEX OI OCCURRED WITH OUR STRONG LOSS IN PRICE OF $12.90 /// COMEX GOLD TRADING// WEDNESDAY// WE HAD SOME BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH SOME LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR LOSS IN PRICE OF $12.90 .

WE HAD A VOLUME OF 6 4 -GC CONTRACTS//OPEN INTEREST 31

WE LOST A GOOD SIZED 5350 CONTRACTS (16.64 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2105 CONTRACTS:

CONTRACT .; AUG 2105 AND DEC: 0 ALL OTHER MONTHS ZERO//TOTAL: 2105. The NEW COMEX OI for the gold complex rests at 554,173. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5350 CONTRACTS: 7455 CONTRACTS DECREASED AT THE COMEXAND 2105 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 5350 CONTRACTS OR 16.64 TONNES. WEDNESDAY, WE HAD A LOSS OF $12.90 IN GOLD TRADING……

AND WITH THAT LOSS IN PRICE, WE HAD A GOOD SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 16.64 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE SUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT FELL $12.90).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS SOMEWHAT SUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2001) ACCOMPANYING THE CONSIDERABLE SIZED LOSS IN COMEX OI (7455 OI): TOTAL LOSSIN THE TWO EXCHANGES: 5350 CONTRACTS. WE NO DOUBT HAD 1 )SOME BANKER SHORT COVERING, 2.)A STRONG INCREASED STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) SOME LONG LIQUIDATION; 4) CONSIDERABLE COMEX OI LOSS.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG LOSS IN GOLD PRICE TRADING//WEDNESDAY//$12.90.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX SGOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY : 6550 CONTRACTS OR 655,000 oz OR 20.37TONNES (2 TRADING DAY(S) AND THUS AVERAGING: 3275 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 20.37 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 20.37/3550 x 100% TONNES =0.574% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3047.96 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 20.37 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2066 CONTRACTS FROM 169,418 DOWN TO 167,352 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG LOSS IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) SOME BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 4) A SMALL DECREASE STANDING AT THE SILVER COMEX FOR JULY AND 5) SOME LONG LIQUIDATION

EFP ISSUANCE 334 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 334 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 334 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2066 CONTRACTS TO THE 334 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A LOSS OF 1732 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 8.662 MILLION OZ, OCCURRED WITH THE 23 CENT LOSS IN PRICE///

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEXWITH THE 23 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// WEDNESDAY. WE ALSO HAD A SMALL SIZED 334 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

SHANGHAI CLOSED UP 64.59 POINTS OR 2.13% //Hang Sang CLOSED UP 697.00 POINTS OR 2,85% /The Nikkei closed UP 24.23 POINTS OR 0.11%//Australia’s all ordinaires CLOSED UP 1.68%

/Chinese yuan (ONSHORE) closed DOWN at 7.0671 /Oil UP TO 40.12 dollars per barrel for WTI and 42.40 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED DOWN // LAST AT 7.0671 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 7.0715 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS /PANDEMIC : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A CONSIDERABLE 7455 CONTRACTS TO 554,173MOVING FURTHER FROM OUR RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND ALL OF THIS LARGE COMEX FALL OCCURRED WITH OUR LOSS OF $12.90 IN GOLD PRICING /WEDNESDAY’SCOMEX TRADING//). WE ALSO HAD A SMALL EFP ISSUANCE (2105 CONTRACTS),. THUS WE HAD 1) SOME BANKER SHORT COVERING AT THE COMEX AND 2) SOME LONG LIQUIDATION AND 3) ANOTHER HUMONGOUS STANDING AT THE GOLD COMEX//JULY DELIVERY MONTH (SEE BELOW) , … AS WE ENGINEERED A FAIR LOSS ON OUR TWO EXCHANGES OF 5350 CONTRACTSWITH GOLD’S CONSIDERABLE LOSS IN PRICE. NOTE THE FACT THAT THE EXCHANGE FOR PHYSICALS ARE SMALL.. SOME OF OUR MAJOR BANKERS ARE BANNED FROM USING THE SERIAL FORWARDS. IF THEY USE THIS VEHICLE IT MUST BE USED FOR PHYSICAL ONLY.

WE HAD 6 4 -GC VOLUME//open interest RISES TO 31

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS., THAT IS 2105 EFP CONTRACTS WERE ISSUED: AUG 2105AND 0 FOR DEC AND ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2105 CONTRACTS.

YOU WILL FIND THAT WHEN WE HAVE A PREMIUM IN THE FUTURES/SPOT, THEN THE NUMBER OF EXCHANGE FOR PHYSICALS DECLINE IN NUMBERS. THE COST IS JUST TOO MUCH FOR THEM TO ISSUE.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: 5350 TOTAL CONTRACTS IN THAT 2105 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST A CONSIDERABLE SIZED 7455 COMEX CONTRACTS. THE BANKERS PROVIDED ALL THE NECESSARY SHORT PAPER TO WHICH OUR LONGS DUTIFULLY ACCEPTED AS THEY GOBBLED UP A SMALL AMOUNT OF EXCHANGE FOR PHYSICALS WITH SOME BANKER SHORT COVERING, ACCOMPANYING OUR CONSIDERABLE COMEX OI LOSS, A HUGE GOLD TONNAGE STANDING FOR THE JULY DELIVERY (SEE CALCULATIONS BELOW)… AND SOME LONG LIQUIDATION……AND WITH ALL OF THE ABOVE WE HAD A STRONG LOSS IN COMEX PRICE OF 12.90 DOLLARS..

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $12,90). AND,THEY WERE SUCCESSFUL IN FLEECING SOME LONGS

AS THE TOTAL LOSS ON THE TWO EXCHANGES REGISTERED A FAIR 16.64 TONNES.

NET LOSS ON THE TWO EXCHANGES :: 5350 CONTRACTS OR 535,000 OZ OR 16.64 TONNES.

COMMODITY LAW SUGGESTS THAT COMMODITY FUTURES OPEN INTEREST SHOULD APPROXIMATE 3% OF TOTAL PRODUCTION. IN GOLD THE WORLD PRODUCES AROUND 3500 TONNES PER YEAR BUT ONLY 2200 TONNES ARE AVAILABLE FROM THE WEST (THUS EXCLUDING RUSSIA, CHINA ETC..WHO KEEP 100% OF THEIR PRODUCTION)

THUS IN GOLD WE HAVE THE FOLLOWING: 554,173 TOTAL OI CONTRACTS X 100 OZ PER CONTRACT = 55.41 MILLION OZ/32,150 OZ PER TONNE = 1723 TONNES

THE COMEX OPEN INTEREST REPRESENTS 1723/2200 OR 78.34% OF ANNUAL GLOBAL PRODUCTION OF GOLD.

Trading Volumes on the COMEX TODAY: 194,425 contracts//fair//most traders have moved to London

CONFIRMED COMEX VOL. FOR YESTERDAY: 289,353 contracts// volume good //most of our traders have left for London

Total monthly oz gold served (contracts) so far this month

4441 notices

444,100 OZ

13.813 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

xxx oz

We had 0 deposit into the dealer

total deposit: nil oz

DEALER WITHDRAWAL: 0

total dealer withdrawals: nil oz

we had 1 deposits into the customer account

i) Into JPMorgan: 160,755.000 oz 5,000 kilobars

total deposit: 160,755.000 oz

we had 0 gold withdrawals from the customer account:

total gold withdrawals; nil oz

We had 2 kilobar transactions +

ADJUSTMENTS: 0 //

customer to dealer:

Loomis: 12,924.300 (402 kilobars)

Manfra: 74,048.562 oz

both adjusted from the customer to dealer.

The front month of JULY registered a total of 1788 oi contracts FOR a LOSS of 232 contracts. We had 484 notices served on WEDNESDAY so we GAINED a whopping 252 contracts or an additional 25,200 oz will stand for delivery as they refused to morph into London based forwards.

Next comes August another strong delivery month and here the OI FELL by A STRONG 10,765 contracts DOWN to 382,574 contracts.

Sept saw another addition of 20 contracts to stand at 56. Oct lost 229 contracts up to 35,934.

We had 744 notices filed today for 74,400 oz

FOR THE JULY 2020 CONTRACT MONTH)Today, 0 notice(s) were issued from JPMorgan dealer account and 486 notices were issued from their client or customer account. The total of all issuance by all participants equates to 641 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 229 notice(s) was (were) stopped/ Received) by j.P.Morgan//customer account and 79 notices by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2020. contract month, we take the total number of notices filed so far for the month (4441) x 100 oz , to which we add the difference between the open interest for the front month of JULY (1788 CONTRACTS ) minus the number of notices served upon today (641 x 100 oz per contract) equals 558800 OZ OR 17.381 TONNES) the number of ounces standing in this active month of JUNE

thus the INITIAL standings for gold for the JULY/2020 contract month:

No of notices filed so far (4441 x 100 oz + (1788 OI) for the front month minus the number of notices served upon today (641) x 100 oz which equals 558,800 oz standing OR 17.381 TONNES in this active delivery month. This is a HUGE record amount for gold standing for a JULY delivery month (a non active delivery month).

We are now witnessing an increase in queue jumping on a daily basis. Sooner or later they will be running out of metal to supply our longs.

NEW PLEDGED GOLD: BRINKS

144,088.952 oz NOW PLEDGED JAN 21.2020/HSBC 5.4807 TONNES

312,441.780 oz PLEDGED JUNE 24// 2020 JPMORGAN: 10.036 TONNES

42,548.308.00 PLEDGED APRIL 3/2020: SCOTIA: 1.3234 tonnes

19,290.600 oz Pledged May 8/2020 INT DELAWARE: .600 TONNES

657,424.187 oz pledged June 12/2020 Brinks/july 2 20.448 tonnes

total pledged gold: 1,175,793.827 oz 36.572 tonnes

SURPRISINGLY WE HAVE BEEN WITNESSING NO REAL PHYSICAL GOLD ENTERING THE COMEX VAULTS FOR THE PAST YEAR!! ..ONLY PHONY KILOBAR ENTRIES…. WE HAVE 363.52 TONNES OF REGISTERED GOLD WHICH CAN SETTLE UPON LONGS ie. 17.381 tonnes

CALCULATION OF REGISTERED GOLD THAT CAN BE SETTLED UPON:

total registered or dealer 12,863,015.270 oz or 400.093 tonnes

which includes the following:

a) pledged gold held at HSBC which cannot settled upon 144,088.952 oz x ( 4.4817 TONNES)//

b) pledged gold held at JPMorgan (SOME DELETED JUNE 24 2020) which cannot be settled upon: 312,441.780 oz (or 9.718 tonnes)

total pledged gold:

c) pledged gold at Scotia: 1.3234 tonnes or 42,548.308 oz which cannot be settled (1.3234 tonnes)

d) pledged gold at Manfra: DELETED MAY 26.2020

e) pledged gold at int.Del. 19,290.600 oz which cannot be settled: (.600 tonnes)

f) pledged gold at Brinks: 21,026.754 oz which cannot be settled June 5 (.65402 tonnes)

g) pledged gold at Brinks: 657,424.187 oz added which cannot be settled: 20.448 tonnes

total weight of pledged: 1,175,793.827 oz or 36.572 tonnes

thus:

registered gold that can be used to settle upon: 11,687,222.0 (363.52 tonnes)

total eligible gold: 19,582,269.640 oz (609.09 tonnes)

total registered, pledged and eligible (customer) gold; 32,445,284.910 oz 1009.18 tonnes (INCLUDES 4 GC GOLD)

total 4 GC gold: 126.34 tonnes

total gold net of 4 GC: 882.84 tonnes

end

I have compiled data with respect to registered (or dealer) gold taken on first day notice for each of the past 24 months

The data begins on first day notice for the May month taken on the last day of April 2018. and it continues to present day. Thus 24 data entry points.

I then took, how many deliveries were recorded by the CME for each and every month. I also included for reference the price of gold on first day notice.

The first graph is a logarithmic graph and the second graph, linear.

You can see the huge explosion of registered gold at the comex along with deliveries. Gold owners are very clear people. They would know full well that

the gold at the comex is unallocated and that they would not be stupid enough to keep their gold at the comex especially in the registered category once deliveries are asked upon. If physical gold was present it would be have removed from the comex… It shows there is no gold at the comex. They are just trading in sticky paper.

THE GOLD COMEX SEEMS TO BE UNDER SEVERE ASSAULT FOR PHYSICAL

END

JULY 2/2020

And now for the wild silver comex results

we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2066 CONTRACTS FROM 169,418 DOWN TO 167,352 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,384 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG LOSS IN OI SILVER COMEX WAS DUE TO; 1) CONSIDERABLE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE AMOUNT OF SILVER OZ STANDING AT THE COMEX FOR THE JULY CONTRACT MONTH , 4) SOME LONG LIQUIDATION

WE STILL HAVE A HUMONGOUS AMOUNT OF SILVER STANDING AT THE COMEX FOR JULY.

EFP ISSUANCE 334 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 334 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 334 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2066 CONTRACTS TO THE 334 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A CONSIDERABLE LOSS OF 1732 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 8.660 MILLION OZ OCCURRED WITH THE 23 CENT LOSS IN PRICE///

RESULT: A STRONG SIZED DECREASE IN SILVER OI AT THE COMEXWITH THE 23 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// WEDNESDAY. WE ALSO HAD A SMALL SIZED 334 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL

JULY 2/2020

JULY SILVER COMEX CONTRACT MONTH

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

301,895.740 oz

CNT

Scotia

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

600,063.800 oz

CNT

No of oz served today (contracts)

744

CONTRACT(S)

(3720,000 OZ)

No of oz to be served (notices)

3560 contracts

17,800,000 oz)

Total monthly oz silver served (contracts)

13012 contracts

65,060,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

We had 0 deposit into the dealer:

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

i)we had 1 deposits into the customer account

into JPMorgan: 0

ii) Into CNT: 600,063.800 oz

*** JPMorgan for most of 2017, 2018 and onward, has adding to its inventory almost every single day.

JPMorgan now has 160.744 million oz of total silver inventory or 49.69% of all official comex silver. (160.819 million/323.598 million

total customer deposits today: 600,063.800 oz

we had 1 withdrawals:

i) Out of CNT: 986.03 oz

total withdrawals; 986.03 oz

We had 1 adjustments

Customer account to Dealer:

i) CNT 781,536.09

total dealer silver: 126.259 million

total dealer + customer silver: 323.598 million oz

The front month of July has an open interest of 4304 contracts, as we lost 905 contracts. We had 810 notices served on WEDNESDAY, so we LOST 95 contracts or an additional 475,000 oz will NOT stand in this active delivery month of July as they received a London based forward and a fiat bonus for their effort..

The next month after July is the non active month of August and here sees its open interest ROSE by 53 contracts UP to 745

The big September contract month sees a LOSS of 1426 contracts DOWN to 131,297.

The total number of notices filed today for the JULY 2020. contract month is represented by 744 contract(s) FOR 3.720 MILLION, oz

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 13,012 x 5,000 oz = 65,060,000 oz to which we add the difference between the open interest for the front month of JULY.(4304) and the number of notices served upon today 744 x (5000 oz) equals the number of ounces standing.

Thus the INITIAL standings for silver for the JULY/2019 contract month: 13,012 (notices served so far) x 5000 oz + OI for front month of JULY (4304)- number of notices served upon today (744) x 5000 oz of silver standing for the JULY contract month.equals 82,860,000 oz. (A WHOPPER )

WE LOST 95 CONTRACTS OR 475,000 OZ WILL NOT STAND ON DAY 2. HOWEVER IF HISTORY SERVES US WELL, WE WILL WITNESS SHORTLY QUEUE JUMPING AS THE BANKS(BULLION DEALERS) TRY TO SQUANDER AS MUCH SILVER AS THEY GAIN ON THIS SIDE OF THE POND.

FOR YESTERDAY: 92,870.,CONFIRMED VOLUME//volume very good/

YESTERDAY’S CONFIRMED VOLUME OF 92,870 CONTRACTS EQUATES to 464 million OZ 66.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER..

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO- 0.04% ((JULY 2/2020)

2. Sprott gold fund (PHYS): premium to NAV RISES TO +0.03% to NAV: (JULY 2/2020 )

Note: Sprott silver trust back into NEGATIVE territory at +%-/Sprott physical gold trust is back into NEGATIVE/ 0.04%

(courtesy Sprott/GATA

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 16.84 TRADING 16.80///NEGATIVE 0.25

END

And now the Gold inventory at the GLD/

JULY 2/WITH GOLD UP $7.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.21 TONNES INTO THE GLD////INVENTORY RESTS AT 1182.11 TONNES

JULY 1/WITH GOLD DOWN $12.90//NO CHANGES IN GOLD INVENTORY AT THE GLD: /INVENTORY RESTS AT 1178.90 TONNES

JUNE 30//WITH GOLD UP $16.50 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1178.90 TONNES

JUNE 29/WITH GOLD UP $2.90 TODAY: A HUGE DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1178.90 TONNES

JUNE 26/WITH GOLD UP $5.03 TODAY: VERY STRANGE: A PAPER WITHDRAWAL OF 1.46 TONNES//INVENTORY RESTS AT 1175.39 TONNES

JUNE 25//WITH GOLD DOWN $3.30 TODAY//ANOTHER STRONG PAPER DEPOSIT OF 7.6 TONNES///INVENTORY RESTS AT 1176.85 TONNES

JUNE 24/WITH GOLD DOWN $1.50 TODAY; A STRONG 3.21 TONNES ADDED TO THE GLD//INVENTORY RESTS AT 1169.25 TONNES

JUNE 23/WITH GOLD UP $25.50 TODAY/ANOTHER CRIMINAL PAPER DEPOSIT OF 6.73 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1166.04 TONNES

JUNE 22/WITH GOLD UP $14.00 A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 23.09 TONNES//INVENTORY RESTS AT 1159.31 TONNES

JUNE 19/WITH GOLD UP$16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//; INVENTORY RESTS AT 1136.22 TONNES

JUNE 18//WITH GOLD DOWN $2.75 TODAY: NO CHANGES IN GOLD INVENTORY: INVENTORY RESTS AT 1136.22 TONNES

JUNE 17/WITH GOLD DOWN $1.05: NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY RESTS AT 1136.22 TONNES

JUNE 16//WITH GOLD UP $6.70 TODAY: NO CHANGES IN GOLD INVENTORY: /INVENTORY RESTS AT 1136.22 TONNES

JUNE 15/WITH GOLD DOWN ANOTHER $8.80 TODAY, NO CHANGES IN GOLD INVENTORY/INVENTORY RESTS AT 1136.22 TONNES

JUNE 12//WITH GOLD DOWN $1.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 1.17 TONNES AT THE GLD//INVENTORY RESTS AT 1136.22 TONNES

JUNE 11//WITH GOLD UP $16.80 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A DEPOSIT OF 6.55 TONNES AT THE GLD//INVENTORY RESTS AT 1135.05 TONNES

JUNE 10/WITH GOLD DOWN $.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 4.02 TONNES AT THE GLD/INVENTORY RESTS AT 1129.50 TONNES

JUNE 9//WITH GOLD UP $16.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.63 TONNES OF GOLD AT THE GLD//INVENTORY RESTS AT 1125.48 TONNES

JUNE 8//WITH GOLD UP $18.70 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 4.10 TONNES AT THE GLD//INVENTORY RESTS AT 1128.11 TONNES

JUNE 5//WITH GOLD DOWN $40.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY: A PAPER WITHDRAWAL OF 1.16 TONNES OUT OF THE GLD//INVENTORY RESTS AT 1132.21 TONNES

JUNE 4//WITH GOLD UP $20.60: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD…A DEPOSIT OF 4.09 TONNES INTO THE GLD//INVENTORY RESTS AT 1133.37 TONNES

JUNE 3//WITH GOLD DOWN $26.15//A SMALL CHANGE IN GOLD INVENTORY//A DEPOSIT OF 0.78 TONNES OF GLD INTO THE GLD//INVENTORY RESTS AT 1129.28 TONNES

JUNE 2//WITH GOLD DOWN $11.20 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1128.40 TONNES

JUNE 1//WITH GOLD UP $1.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES OF GOLD//GLD INVENTORY RESTS TONIGHT AT 1123.14 TONNES

MAY 29/WITH GOLD UP $19.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD///GLD INVENTORY RESTS THIS WEEKEND AT 1119.05 TONNES

MAY 28//WITH GOLD UP $4.00 TODAY/NO CHANGES IN GOLD INVENTORY TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

MAY 27/WITH GOLD UP $.10 TODAY: A STRONG 2.34 TONNES OF GOLD ADDED TO THE GLD//INVENTORY RESTS AT 1119.05 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Inventory rests tonight at

JULY 2/ GLD INVENTORY 1182.11 tonnes*

LAST; 852 TRADING DAYS: +238.21 NET TONNES HAVE BEEN ADDED THE GLD

LAST 752 TRADING DAYS://+416.39 TONNES HAVE NOW BEEN ADDED INTO THE GLD INVENTORY.

end

Now the SLV Inventory/

JULY 2/WITH SILVER UP 4 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 4.01 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 502.008 MILLION OZ

JULY 1/WITH SILVER DOWN 23 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.403 MILLION OZ//INVENTORY RESTS AT 498.007 MILLION OZ/

JUNE 30/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 29/WITH SILVER DOWN ONE CENT TODAY: A TWO CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 466,000 OZ TO PAY FOR STORAGE FEES AND INSURANCE//// AND A LARGE DEPOSIT OF 1.212 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 492.604 MILLION OZ//

JUNE 26/WITH SILVER UP 6 CENTS TODAY: ANOTHER HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ RESTS AT 491.858 MILLION OZ//

JUNE 25/WITH SILVER UP 12 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 931,000 OZ INTO THE SLV////INVENTORY RESTS AT 491.858 MILLION OZ//

JUNE 24///WITH SILVER DOWN 31 CENTS// NO CHANGE IN SILVER INVENTORY//INVENTORY RESTS AT 490.927 MILLION OZ

JUNE 23//WITH SILVER UP 16 CENTS TODAY: A MONSTROUS CHANGE IN INVENTORY: A PAPER DEPOSIT OF 4.473 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 490.927 MILLION OZ//

JUNE 22/WITH SILVER UP 15 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/: INVENTORY/INVENTORY RESTS AT 486/454 MILLION OZ//

JUNE 19//WITH SILVER UP 22 CENTS TODAY: STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 839,000 OZ FROM THE SLV////INVENTORY RESTS AT 486,454 MILLION OZ..

JUNE 18/WITH SILVER DOWN 16 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 932,000 OZ INTO THE SLV////INVENTORY RESTS AT 487.293 MILLION OZ

JUNE 17/WITH SILVER UP 8 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.261 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.361 MILLION OZ

JUNE 16//WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.118 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 483.100 MILLION OZ//

JUNE 15/WITH SILVER DOWN 14 CENTS NO CHANGES IN SILVER INVENTORY: //INVENTORY RESTS AT 481.982 MILLION OZ///

JUNE 12/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: TWO DEPOSITS OF 7.269 MILLION OZ AND 1.802 MILLION OZ ADDED TO THE SLV///INVENTORY RESTS THIS WEEKEND AT 481.982 MILLION OZ//

JUNE 11//WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY: ///INVENTORY RESTS AT 472.89 MILLION OZ//

JUNE 10/WITH SILVER UP 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 472.849 MILLION OZ//

JUNE 9/WITH SILVER DOWN 6 CENTS TODAY//A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.605 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 422.849 MILLION OZ//

JUNE 8/WITH SILVER UP 36 CENTS TODAY: TWO HUGE WITHDRAWALS OF 932,000 MILLION OZ AND 1.491 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 470.240 MILLION OZ//

JUNE 5/WITH SILVER DOWN 46 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A PAPER WITHDRAWAL OF 648,000 OZ FROM THE SLV////INVENTORY RESTS AT 472.663 MILLION OZ

JUNE 4//WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV.//INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 3//WITH SILVER DOWN 23 CENTS TODAY//NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVENTORY RESTS AT 473.315 MILLION OZ//

JUNE 2//WITH SILVER DOWN 31 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUMONGOUS 6.686 MILLION OZ ADDED TO THE SLV////INVENTORY RESTS TONIGHT AT 473.315 MILLION OZ//

JUNE 1//WITH SILVER UP 38 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.56 MILLION OZ INTO THE SLV////INVENTORY RESTS TONIGHT AT 466.629 MILLION OZ//

MAY 29//WITH SILVER UP 52 CENTS TODAY: A MASSIVE DEPOSIT OF 2.796 MILLION OZ INTO THE SLV//INVENTORY RESTS THIS WEEKEND AT 463.273 MILLION OZ//

MAY 28//WITH SILVER UP 9 CENTS TODAY: A MASSIVE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.660 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 460.477 MILLION OZ//

MAY 27/WITH SILVER UP 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 455.817 MILLION OZ//

JULY 2.2020:

SLV INVENTORY RESTS TONIGHT AT

502.008 MILLION OZ.

END

LIBOR SCHEDULE AND GOFO RATES// GOLD LEASE RATES

YOUR DATA…..

6 Month MM GOFO 4.00/ and libor 6 month duration 0.38

Indicative gold forward offer rate for a 6 month duration/calculation:

GOLD LENDING RATE: -3.62%

NEGATIVE GOLD LEASING RATES INCREASING BY A HUGE AMOUNT//GOLD SCARCITY AND CENTRAL BANKS CALLING IN ALL OF THEIR GOLD LEASES

ii) Important gold commentaries courtesy of GATA/Chris Powell

what went wrong is beautifully explained in this interview..i.e. infinite money was created to the benefit of the elite over Main street.

Jan Nieuwenhuijs/GATA

Jan Nieuwenhuijs: What went wrong in 1971 is explained

Submitted by cpowell on Wed, 2020-07-01 14:26. Section: Daily Dispatches

10:25a ET Wednesday, July 1, 2020

Dear Friend of GATA and Gold:

Voima Gold researcher Jan Nieuwenhuijs this week posts an excellent interview with a couple of amateur Austrian School economists who maintain an internet site built on the premise that the world started going haywire upon President Richard Nixon’s disconnection of the U.S. dollar from gold in 1971.

The interview suggests that the closing of the “gold window” not only began the age of infinite money but also caused economic inequality to explode by inflating financial asset values without increasing wages.

Nieuwenhuijs’ interview is headlined “What Went Wrong in 1971” and it’s posted at Voima Gold here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

The story on how Kingold jewelry secures a 2.8 billion dollars in loans with gilded copper

(SCMP/GATA)

China’s Kingold Jewelry secures $2.8 billion in loans with gilded copper bars

Submitted by cpowell on Wed, 2020-07-01 15:37. Section: Daily Dispatches

What’s the big deal here? Being at least copper, those bars are more real than the paper gold that has flooded the world.

* * *

Kingold Jewelry Secures $2.8 billion in Loans with Gilded Copper Bars

By Peggy Sito

South China Morning Post, Hong Kong

Tuesday, June 30, 3030

Kingold Jewelry, a Nasdaq-listed jeweller and producer of household ornaments, has been accused of large-scale fraud in the second major scandal in three months involving a Chinese company listed in the United States.

The Wuhan-based company is alleged to have used fake gold bars as collateral to fraudulently obtain 20 billion yuan (US$2.8 billion) in loans, in a case that risks fuelling a recent drive by American politicians to expel Chinese companies from Wall Street.

Shares of the Nasdaq-listed gold processor plunged by almost a quarter after the allegations emerged Monday morning on the website of Caixin, a mainland Chinese financial news outlet.

Kingold strongly denies any wrongdoing and is being investigated by the “authorities,” according to Caixin. The company could not be reached for comment by the Post.

Kingold, one of China’s largest gold jewellery manufacturers, allegedly used 83 tonnes of gold bars as loan collateral, which later turned out to be gilded copper. Caixin described it as one of the largest gold loan fraud cases China has ever seen. …

Revenu Quebec has just concluded a secret agreement with the Montreal firm Metaux Kitco, accused of multi-million-dollar tax evasion in the gold sector.

Revenu Quebec argued that Kitco owed it at least C$284 million for claiming and obtaining tax refunds to which the company was not entitled. According to publicly available information, the taxman ultimately receive only $50 million of this amount.

According to the government agency, Kitco produced false invoices to carry out “artificial transactions” making it possible to transform pure gold (zero-rated) into scrap gold (taxable), then again into pure gold (zero-rated).

Kitco’s business partners include security firms GardaWorld and G4S, as well as the Royal Canadian Mint, a federal Crown corporation, to which Kitco entrusts the refining of its scrap gold. Nothing indicates that these entities participated in the scheme denounced by the tax authorities.

Revenu Quebec requested that a confidentiality clause be added to the agreement to prevent its disclosure. In a document filed in court, however, it was stated that the agency is entitled to C$49.9 million as “full and final payment” for its claim of C$284 million.

Revenue Canada, for its part, will receive $ 31.7 million. The total of C$81.7 million represents the amount that the tax authorities had withheld from tax-refund claims submitted by Kitco.

The agreement will allow Kitco to get out of the judicial restructuring process in which the company was placed in 2011 in reaction to the notices of assessment filed by Revenu Quebec. The Superior Court is to ratify the agreement next month.

Revenu Quebec refused to answer questions from the Journal yesterday, except to indicate that “the Court of Quebec remains seized of criminal files” concerning Metaux Kitco and its founding president, Bart Kitner. According to spokesperson Geneviève Laurier, procedures must resume on May 24.

However, a document filed in court stipulates that the agreement concluded with the taxman “settles” all disputes with Kitco, including “criminal offenses.”

The taxman demanded fines totaling more than $454 million from Kitco and Mr. Kitner as well as a prison sentence for the latter.

Since 2011 the amount of gold held by Kitco has decreased by 20 percent. Despite everything the company still has 77,000 ounces of this precious metal for a market value of C$127 million, accounting firm Richter told the court.

end

Generally technical analysis does not work in manipulated markets. However if you use long term charts, there is value in it.

Today, Von Greyerz shows gold breaking out and silver is about to:

(Egon Von Greyerz/GATA)

At KWN, Von Greyerz’s charts indicate breakouts for gold and silver

Submitted by cpowell on Thu, 2020-07-02 01:56. Section: Daily Dispatches

9:55p ET Wednesday, July 1, 2020

Dear Friend of GATA and Gold:

While GATA has little use for technical analysis of markets as manipulated as those for gold and silver, from time to time you may be entitled to some cheering up after all the news we bring you about the bad guys. So thanks to King World News, enjoy the chart work done tonight by Swiss gold fund manager Egon von Greyerz. It’s headlined “Gold and Silver Are Close to Major Breakouts That Will Send Prices Soaring” and it’s posted here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

iii) Other physical stories:

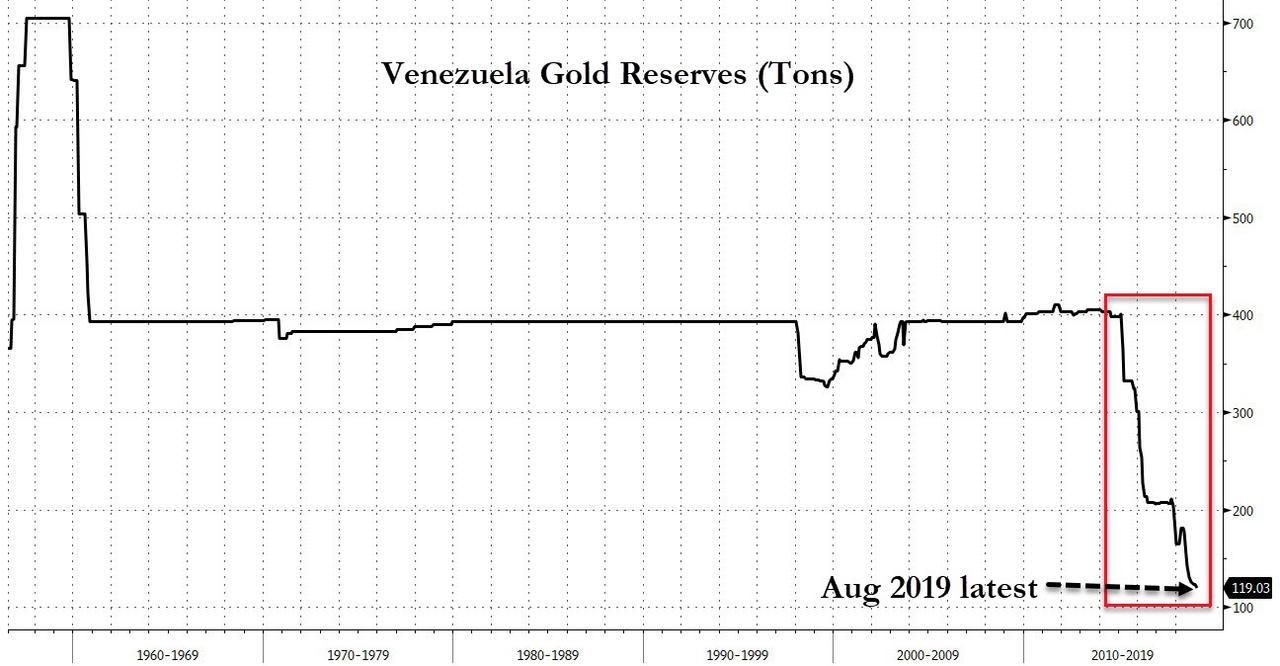

Former bus driver, Maduro receives news that the British Court refuses to release Venezuela one billion dollars worth of gold.

(zerohedge)

British Court Refuses To Release Venezuelan Gold To Maduro

18 months ago, the ‘virtue-signaling’ Bank of England stuck a knife between the ribs of Venezuela’s embattled socialist leader, Nicolas Maduro, a former bus driver and anointed successor of Hugo Chavez who managed to cling to power last year despite a Western-backed coup attempt led by opposition leader Juan Guaido, whose government was officially recognized by dozens of foreign governments.

But when the Venezuelan military refused to break with Maduro, choosing instead to back him over Guaido, Guaido gradually faded into irrelevance. He’s still there, and still claiming to be the legitimate ruler of Venezuela, but instead of looking like a credible alternative to Maduro, he’s sounding more like a deranged street preacher proclaiming that he is the one true messiah.

Despite the fact that Venezuela’s leadership is no longer in doubt, a lawsuit brought by the Venezuelan central bank against the British government seeking the release of the Venezuelan gold sitting in the BoE’s vaults ended on Thursday with a decision against the Maduro government,as it was denied access to $1 billion of venezuelan gold in the BoE vaults. Instead, the court ruled that it could only release the gold to the legitimate government of Venezuela. Since Britain recognizes Guaido as Venezuela’s legitimate ruler, the British government has legal standing to treat the Maduro government like an illegitimate regime, allowing the gov’t to essentially freeze and seize government assets at will.

Mr Justice Teare, a commercial court judge sitting in the high court, ruled on Thursday the Maduro-supporting bank was not entitled to make the request. “Her Majesty’s government does recognise Guaidó in the capacity of the constitutional interim president of Venezuela and, it must follow, does not recognise Maduro as the constitutional interim president of Venezuela,” he said.

“Whatever the basis for the recognition, Her Majesty’s government has unequivocally recognised Guaidó as president of Venezuela. It necessarily follows that Her Majesty’s government no longer recognises Maduro as president of Venezuela … There is no room for recognition of Mr Guaidó as de jure president and of Maduro as de facto president.”

Sarosh Zaiwalla, senior partner at Zaiwalla & Co, representing the Banco Central de Venezuela, said his clients would appeal and challenged the court judgement for “entirely ignoring the reality of the situation on the ground”.

He said the ruling would delay money being sent to help the people of Venezuela. “Maduro’s government is in complete control of Venezuela and its administrative institutions, and only it can ensure the distribution of the humanitarian relief and medical supplies needed to combat the coronavirus pandemic.”

He added that none of the member of a rival, Guaidó-appointed BcV board that sought to keep the gold in the UK, have “been resident in Venezuela for some years now”.

Though the Venezuelans plan to appeal, we suspect they won’t have very much luck. That’s of course terrible news for the Maduro government, which is officially broke with its oil output at record lows and its currency essentially worthless, the government has no money to finance anti-COVID-19 programs. And the international community, aside from Maduro’s benefactors in Russia and China, has been pretty unforgiving. Back in May, we pointed out that Venezuela’s gold vaults are probably empty, or close to it, after the government was forced to make some payments to the Iranians in gold.

The central bank’s solicitor argued that the decision was illegal under international law as an illegal intervention in the affairs of Venezuela. The decision also puts the kibosh on a Venezuelan plan whereby proceeds from the gold could be handed to the UN allowing it to intermediate the purchases of critical COVID-19 supplies for Venezuela.

Ultimately, we imagine Hugo Chavez, who took strides to repatriate most of Venezuela’s gold held in the vaults of foreign central banks, is rolling over in his grave. And Maduro is learning once again that gold doesn’t have any owners – only spenders. He who controls the vault, controls the gold.

end

Due to the criminal conviction of trader Edmonds, the USA prosecution is seeking to halt the civil lawsuit. I was misinformed: all discoveries in a civil suit are public and because of that, the prosecution gives the defendants the right to plead the 5th if their testimony incriminates them

(courtesy zerohedge/Chris Powell)

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

A sign of JP Morgan Chase Bank is seen in front of their headquarters tower in New York.

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

A federal judge tells traders that they can combine cases (with the other 6 banks) as they accused JPMorgan of rigging the precious metals market

(courtesy CNBC)

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Spencer Platt | Getty Images

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

Justice Department stalls another class action in gold market rigging, this one against JPM

Submitted by cpowell on Tue, 2019-03-05 14:40. Section: Daily Dispatches

9:47a ET Tuesday, March 5, 2019

Dear Friend of GATA and Gold:

Proceedings in the federal class-action anti-trust lawsuit against JPMorganChase charging the investment bank with manipulating the gold and silver futures markets —

— have been suspended for three months at the request of the U.S. Justice Department, just as the department has arranged suspension of proceedings in the class-action anti-trust lawsuit against Deutsche Bank charging similar market manipulation.

…

In both cases the Justice Department has told U.S. District Court for the Southern District of New York that proceedings would jeopardize its criminal investigation into market rigging, which has been admitted by a former JPMorganChase trader, John Edmonds, who awaits sentencing.

According to court filings, the White Plains, New York, law firm representing the plaintiffs against JPMorganChase, Lowey Dannenberg, concurred in the government’s request to suspend proceedings. The stay is to continue for three months and may be extended.

The Justice Department’s motion, granted by the court on February 26 —

— said “the government is not seeking an open-ended stay that could indefinitely postpone this matter and thus jeopardize the parties’ interests in a timely resolution.” The motion added, “Any developments in the criminal case during the period the consolidated action is stayed may reduce or completely resolve the need to litigate certain issues in the consolidated action.”

Much of the Justice Department’s motion is redacted to conceal from the public evidence still under investigation. Edmonds has said he and other traders manipulated the gold and silver markets for years with the knowledge of their supervisors at JPMorganChase. In its motion to conceal that evidence, also granted by the court on February 26, the Justice Department said disclosure “could lead to destruction of evidence, flight from prosecution, and otherwise interfere with the government’s ability to conduct its investigation”:

Monetary metals investors may be skeptical of the Justice Department’s stalling the Deutsche Bank and JPMorganChase cases, since the department and the U.S. Commodity Futures Trading Commission do not seem ever to have responded conscientiously to complaints of gold and silver market rigging until the class actions commenced.

How much time will the court give the Justice Department to delay getting to the bottom of the issue? The court might hasten matters if enough monetary metals mining companies protested the harm done to them and their shareholders by market rigging, but of course most monetary metals mining companies don’t mind at all.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

* * *

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/7 AM EST

i) Chinese yuan vs USA dollar/CLOSED / LAST AT: 7.0671/ GETTING VERY DANGEROUSLY PAST 7:1

//OFFSHORE YUAN: 7.0715 /shanghai bourse CLOSED UP 64.59 POINTS OR 2.13%

HANG SANG CLOSED UP 697.00 POINTS OR 2.85%

2. Nikkei closed UP 24.23 POINTS OR 0.11%

3. Europe stocks OPENED ALL GREEN/

USA dollar index DOWN TO 96.91/Euro FALLS TO 1.1287

3b Japan 10 year bond yield: FALLS TO. +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.42/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//CARRY TRADERS GETTING KILLED

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 40.12 and Brent: 42.40

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO -.41%/Italian 10 yr bond yield DOWN to 1.24% /SPAIN 10 YR BOND YIELD DOWN TO 0.46%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.65: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.18

3k Gold at $1765.60 silver at: 17.88 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 40/100 in roubles/dollar) 70.39

3m oil into the 40 dollar handle for WTI and 42 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.42 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9431 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0646 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3r the 10 Year German bund now NEGATIVE territory with the 10 year RISING to –0.41%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 0.68% early this morning. Thirty year rate at 1.43%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.8552..

Futures Surge On Even More “Optimism” Ahead Of Payrolls

After sliding to 2,983.5 in early Sunday trading on fears of a second wave of covid infections, futures have completely forgotten what they were concerned about at the start of the week, and have since levitated in largely linear fashion some 150 points higher, rising to 3,130.75 overnight, on even more hope and optimism, this time for a reassuring job report coupled with yesterday’s hopes for positive vaccine developments. The dollar slipped and 10Y yields rose.

At 7:20 a.m. ET, Dow e-minis were up 275 points, or just over 1%, S&P 500 e-minis were up 25 points to 3,128, and Nasdaq 100 e-minis were up 52 points to 10320. Travel-related stocks were among the biggest gainers in premarket trade, with cruise line operators Carnival, Royal Caribbean Cruises and Norwegian Cruise Line Holdings rising between 3% and 4%, while economically-sensitive stocks including Morgan Stanley, Goldman Sachs, Citigroup, JPMorgan Chase and Bank of America up between 1% and 3%. Tesla was up another $100 overnight, rising to a new record high above 1,200.

Indeed, as Reuters writes this morning, “optimism about a post-pandemic rebound in business activity, aggressive U.S. stimulus and hopes of a COVID-19 vaccine” have fueled a Wall Street rally since April, with the tech-heavy Nasdaq notching up its sixth record closing high since early June on Wednesday.

After the latest ISM data showed U.S. manufacturing unexpectedly hit its highest level in June in more than a year, the Labor Department’s jobs report due later in the day is expected to show record job growth last month, signaling that a COVID-19-driven recession was probably over, at least until its returns next month when government stimulus checks run out. Meanwhile, with several states scaling back or pausing reopenings to tackle a recent surge in coronavirus infections, analysts have warned of another selloff in financial markets if the damage to Corporate America mounts.

Third-quarter earnings for S&P 500 companies are now expected to tumble 25%, compared with a forecast of a 2.7% drop on April 1, according to Refinitiv. In the second quarter, earnings are forecast to have plunged 43%.

Europe’s Stoxx 600 Index extended its initial gains on advances in banks and automakers with the Eurostoxx 50 rallying as much as 1.9% to fresh highs for the week; IBEX outperforms, gaining over 2.5%. Europe’s Stoxx 600 Travel & Leisure index rose as much as 3.6%, the most since June 16, led by airlines and gaming stocks. IAG was up as much as 7.4% and EasyJet advances 6.6%; the U.K. is planning to lift quarantine rules for 75 countries, according to a report in the Telegraph. Gaming stocks including GVC (+3.1%) and Flutter (+2.9%) also higher after brushing off a U.K. House of Lords report calling for the introduction of new rules to reduce gambling-related harm.

Asian stocks also gained, led by communications and energy, after ending flat in the last session. Hong Kong shares outperformed after traders returned from a holiday, despite the recent tensions over China’s new national security law over the city. The Shanghai Composite turned positive for the year to date, with Zhangjiagang Freetrade Science & Technology Group and Xinjiang Tianye posting the biggest advances.Stocks in Australia, China, Japan and South Korea also rose. The Topix gained 0.3%, with Retail Partners and GungHo Online rising the most. Trading volume for MSCI Asia Pacific Index members was 62% above the monthly average for this time of the day.

“The rally for equities could survive even if the U.S. jobs data disappoint, after the Fed’s signal of sustained low rates,” said Stephen Gallo, a foreign-exchange strategist at the Bank of Montreal. “Bad numbers could extend that outlook for cheap money.” Translation: a good jobs number will be good, a bad jobs number will be better.