GOLD:$1796.90 UP $12.50 The quote is London spot price

Silver:$18.33// UP 8 CENTS London spot price

Closing access prices: London spot

i)Gold : $1796.40 LONDON SPOT 4:30 pm

ii)SILVER: $18.33//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUG GOLD: $1809.50 CLOSE 1.30 PM// SPREAD SPOT/FUTURE AUG /: $12.50

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $18.67…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 34 CENTS PER OZ

the gold market continues to be broken as future prices are much higher than spot prices. The comex is desperate to fix things but they have no available gold.

If one is to buy gold and or gold coins, the price is around $2600. usa per oz

and silver; $29.00 per oz//

LADIES AND GENTLEMEN: YOU ARE NOW WITNESSING FIRST HAND THE DIFFERENCE BETWEEN PAPER GOLD/SILVER AND THE REAL PHYSICAL STUFF!!

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

today RECEIVING: 181/658

issued: 536

EXCHANGE: COMEX

CONTRACT: JULY 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,788.500000000 USD

INTENT DATE: 07/06/2020 DELIVERY DATE: 07/08/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 5

072 H GOLDMAN 49

135 H RAND 1

152 C DORMAN TRADING 7

355 C CREDIT SUISSE 3

624 C BOFA SECURITIES 2

657 C MORGAN STANLEY 52

657 H MORGAN STANLEY 98

661 C JP MORGAN 536 181

686 C INTL FCSTONE 2

690 C ABN AMRO 17

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 37 67

800 C MAREX SPEC 80 136

878 C PHILLIP CAPITAL 5 7

905 C ADM 28

____________________________________________________________________________________________

TOTAL: 658 658

MONTH TO DATE: 5,631

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT: 658 NOTICE(S) FOR 65,800 OZ (2.0446 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 563100 NOTICES FOR 563,100 OZ (17.514 TONNES)

SILVER

FOR JULY

213 NOTICE(S) FILED TODAY FOR 1,065,000 OZ/

total number of notices filed so far this month: 13,253 for 66.265 MILLION oz

BITCOIN MORNING QUOTE $9259 DOWN 87

BITCOIN AFTERNOON QUOTE.: $9293 UP $293

GLD AND SLV INVENTORIES:

WITH GOLD UP $12.50 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL”?

NO CHANGE IN GOLD INVENTORY AT THE GLD:

GLD: 1,191.47 TONNES OF GOLD//

WITH SILVER UP 8 CENTS TODAY: AND WITH NO SILVER AROUND

NO CHANGE IN SILVER INVENTORY AT THE SLV:

RESTING SLV INVENTORY TONIGHT:

SLV: 503.871 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A STRONG SIZED 2115 CONTRACTS FROM 167,591 UP TO 169,706, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE STRONG SIZED GAIN IN OI OCCURRED WITH OUR 24 CENT GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A SMALL EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A SMALL DECREASE IN SILVER STANDING AT THE COMEX FOR JULY. WE HAD A NET GAIN IN OUR TWO EXCHANGES OF 2598 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: JULY: 0 AND SEP 483 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 483 CONTRACTS. WITH THE TRANSFER OF 483 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 483 EFP CONTRACTS TRANSLATES INTO 2.415 MILLION OZ ACCOMPANYING:

1.THE 24 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

82.205 MILLION OZ INITIALLY IN JULY.

MONDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 24 CENTS).. AND,OUR OFFICIAL SECTOR/BANKERS WERE NO DOUBT SUCCESSFUL IN THEIR ATTEMPT TO FLEECE SOME SILVER LONGS FROM THEIR POSITIONS. THE TINY GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A SMALL DECLINE IN STANDING OF SILVER OZ STANDING FOR JULY, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A STRONG NET GAIN OF 2598 CONTRACTS OR 12.999 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

JULY

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF JULY:

1677 CONTRACTS (FOR 4 TRADING DAY(S) TOTAL 1677 CONTRACTS) OR 8.385 MILLION OZ: (AVERAGE PER DAY: 419 CONTRACTS OR 2.096 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 8.385 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.19% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,145.80 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 8.385 MILLION OZ/

EXCHANGE FOR PHYSICAL ISSUANCE FOR THE PAST 60 DAYS IS A LOT LESS. NO DOUBT THAT THE COST TO CARRY THESE THINGS HAS EXPLODED AND AS SUCH CANNOT BE DONE AS FREQUENTLY AS BEFORE.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2115, WITH OUR 24 GAIN IN SILVER PRICING AT THE COMEX ///MONDAY… THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 483 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED A STRONG SIZED OI CONTRACTS ON THE TWO EXCHANGES: 2598 CONTRACTS (WITH OUR 24 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 483 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A STRONG SIZED INCREASE OF 2,115 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED DESPITE A 24 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $18.25 // MONDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.8380 BILLION OZ TO BE EXACT or 119% of annual global silver production (ex Russia & ex China).

FOR THE NEW JULY DELIVERY MONTH/ THEY FILED AT THE COMEX: 213 NOTICE(S) FOR 1,065,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 IS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 82.205 million oz

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 2622 CONTRACTS TO 559,370 AND CLOSER TO OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE SMALL SIZED GAIN OF COMEX OI OCCURRED WITH OUR STRONG GAIN IN PRICE OF $6.50 /// COMEX GOLD TRADING// MONDAY// WE HAD HUGE BANKER SHORT COVERING, ANOTHER HUMONGOUS SIZED GOLD OZ STANDING AT THE COMEX FOR JULY, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE. THIS ALL HAPPENED WITH OUR GAIN IN PRICE OF $6.50 .

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 31

WE GAINED A GOOD SIZED 4686 CONTRACTS (14.57 TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 2064 CONTRACTS:

CONTRACT .; AUG 1864 AND OCT: 200 ALL OTHER MONTHS ZERO//TOTAL: 2064. The NEW COMEX OI for the gold complex rests at 559,370. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4686 CONTRACTS: 2622 CONTRACTS INCREASED AT THE COMEX AND 2064 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN OF 4686 CONTRACTS OR 16.36 TONNES. MONDAY, WE HAD A GAIN OF $6.50 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A GOOD SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 14.57 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $7.00).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL (SEE BELOW).

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2064) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (3197 OI): TOTAL GAIN IN THE TWO EXCHANGES: 5261 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)ANOTHER STRONG INCREASE IN GOLD STANDING AT THE GOLD COMEX FOR THE FRONT JULY MONTH, 3) ZERO LONG LIQUIDATION; 4) SMALL COMEX OI GAIN.. AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//MONDAY//$6.50.

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO GOLD

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN GOLD AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR SILVER..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR GOLD. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO GOLD AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JULY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF AUGUST FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF JULY. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN GOLD WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUGUST), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

JULY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 35.49 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 35.49/3550 x 100% TONNES =1.01% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3063.23 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 35.49 TONNES SO FAR..

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2115 CONTRACTS FROM 169,734 UP TO 169,706 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE STRONG GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) A SMALL DECREASE STANDING AT THE SILVER COMEX FOR JULY AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 483 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY: 0 CONTRACTS AND SEPT: 483 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 483 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2115 CONTRACTS TO THE 483 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2598 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 12.99 MILLION OZ, OCCURRED WITH THE 24 CENT GAIN IN PRICE///

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 24 CENT GAIN IN PRICING THAT SILVER UNDERTOOK IN PRICING// MONDAY. WE ALSO HAD A SMALL SIZED 483 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR THIS MONTH, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 12.46 POINTS OR 0.37% //Hang Sang CLOSED DOWN 363.50 POINTS OR 1.38% /The Nikkei closed DOWN 99.75 POINTS OR 0.44%//Australia’s all ordinaires CLOSED UP .01%

/Chinese yuan (ONSHORE) closed UP at 7.0257 /Oil UP TO 40.21 dollars per barrel for WTI and 42.83 for Brent. Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN CLOSED UP // LAST AT 7.0257 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0204 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED //CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

Gold Spikes Back Above $1800 After Bostic’s Downbeat Comments

Is ‘bad’ news, good news for precious metals?

Raphael Bostic diverged from Powell’s more optimistic outlook, warning this morning that he is seeing signs of a “levelling off” of the US economy’s recovery.

The Atlanta Fed chief told the Financial Times:

“There are a couple of things that we are seeing and some of them are troubling and might suggest that the trajectory of this recovery is going to be a bit bumpier than it might otherwise.”

Bostic added that he was “trying to figure out whether this levelling off is something that is a more sustained pattern, or just a pause.”

“Given that possibility, to start thinking about what the next relief package should look like.”

His comments appeared to line up with a renewed bid for gold, sending futures quickly back above $1800 as perhaps this means a renewed easing effort by The Fed (whose balance sheet has also leveled out in recent weeks)…

Gold futures hit $1809.70 as we publish – a new cycle high.

Silver is also spiking…

As Ron Paul recently wrote, with lending facilities providing to the Federal Reserve the ability to give money directly to businesses and governments, the Fed is now just one step away from implementing Ben Bernanke’s infamous suggestion that, if all else fails, the Fed can drop money from a helicopter. These interventions will not save the economy. Instead, they will make the inevitable crash more painful.

The next crash can bring about the end of the fiat monetary system. The question is not if the current monetary system ends, but when. The only way Congress can avoid the Fed causing another great depression is to begin transitioning to a free-market monetary system by auditing, then ending, the Fed.

end

J.Johnson//gold and silver report:

https://www.jsmineset.com/2020/07/07/the-derailing-train-of-debt-vs-currencies-vs-precious-metals/

The Derailing Train of Debt, vs Currencies, vs Precious Metals

Posted July 7th, 2020 at 9:01 AM (CST) by J. Johnson & filed under General Editorial.

Great and wonderful Tuesday Morning Folks,

Precious Metals are rarely allowed a follow thru day after a nice and positive move up is made like yesterday, with Gold now at $1,784.20, down $9.20 after hitting a low of $1,781.20 with the high so far today at $1,797.60. Silver is leading us lower, as usual, with the trade at $18.31 down 27.2 cents after hitting the London low of $18.235 with the high up at $18.68. The US Dollar finally did get overseas support with its value now at 96.90, up 21.9 points after hitting a high of 97.105 with the low at 96.555. Of course, all this happened already, before 5 am pst, the Comex open, the London close, and after Sven the trader, claims “Markets are basically just a liquidity meth lab”…with no earnings growth during the last few years, “it is folly to pretend markets are about anything else but the Fed”. One thing for certain, meth labs and currencies do blow up, as witnessed in our next few paragraphs.

In Venezuela, Gold value is now priced at 17,819.70 Bolivar taking back 26.96 overnight with Silver at 182.871 showing a drop of 2.247 Bolivar. In Argentina, the Peso has Gold valued at 126,242.61 showing a gain of 134.27 with Silver down 12.22 A-Peso’s with the price at 1,295.51. Gold’s price in Turkey now sits at 12,251.21 Lira, showing a reduction of 19.81 with Silver losing 1.559 T-Lira with the last trade at 125.725.

Here are some charts to ponder upon, Gold’s price under the Venezuela’s Bolivar rallied 502,617.91% in 3 years’ time. It’s unfortunate this same site removed the other currencies vs. Gold’s past multiyear rally, because they were substantially huger, much huger, in fact ginormous! Pardon my Trump-ette. Argentina’s Peso only shows a 115.52% gain since last year, here is a chart between the Argentine Peso and US Dollar where the currency values are many % points higher past that 1 year period. Btw, the Argentine Peso is our highest printed blow up currency to date. Turkey’s Lira has also fallen against the US Dollar which also means Gold price rise was substantial as well. This is why we believe the prices of precious metals, under our dollar, just may meet, or exceed, these past facts as everything unwinds.

July Silver Delivery Demands now stand at 3,401 fully paid for 5,000-ounce contracts and with a price range between $18.26 and $18.22 with the last buy at the high, proving a drop of 132 in the demand count since yesterday’s posts and with a Volume of 78 already up on the board. Yesterday’s activity happened between $18.64 and $18.21 with the last buy at $18.53 with the close lower at $18.504. The fear is rising and so is the Open Interest in Silver as another 2,117 more shorts had to be added yesterday or today the price would be higher with the total count now at 169,735 Overnighters going against the physicals.

July Gold’s Delivery Demands now totals 861 fully paid for 100-ounce contracts proving a drop of 409 receipts either getting filled here at the Comex or EFP’d over to London, with this mornings trading range between $1,789.30 and $1,784.90 with the last buy at the low and with a Volume of 178 already up on the board. The fear is also showing up behind the price in Gold as well, as the Open Interest gained another 3,079 more short contracts in order to supply liquidity, bringing the early morning total to 559,945 Overnighters.

To add more reasons to the fear trading in the markets, the U.S. Mint is upping its coin production, after shortages of stamped coins have been reported in the U.S., and after purchases dropped off until the CCP19 bio got out. The second half of 2020, the Mint estimates an increase production to 1.2 billion coins in June and 1.35 billion coins per month for the rest of the year– which would add up to a projected total of 14.2 billion coins produced in 2020. This helps point out the idea that people are leaving the crime ridden investment arenas where the regulatory bodies are equally as guilty as the perpetrators, and as things start to heat up in the failed debt markets, which leads right to Currency Devaluations, which leads right to Precious Metals Rising, like they did in our emerging markets currency watch.

Here’s a good thread of closing thoughts that can only be answered in time; Is it possible the Ginormous Precious Metals Deliveries inside our July demand count, is the US mint itself? Is this proof their normal supply chain got disrupted because of a lab-designed-bio that shut down a world for 60 days? Demand is Demand, and the US Mint is required to meet the physical demands, and here we are.

Nothing can stop this derailing train of debt vs. currencies vs. precious metals. Yet those that hold the physicals, have a much better chance of retaining their purchasing power, while the world observes how much has to be printed in order to pay off a debt, that has been piled high to a level of uncollectable.

Stay positive no matter what, it’s food for the soul in times like these. Have a smile on your face and a prayer for all, and as always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

end

This is going to hurt production: Cadelco is the largest copper mine in the world. It also produces some molybdenum, silver and gold.

(Bloomberg)

Thousands of Copper Workers Have Fallen Ill in Chile (CORONAVIRUS)

Mines have been attempting to keep their workers safe without forgoing too much output by postponing non- essential activities such as maintenance and construction work. Fewer workers on site mean less risk of infection.

But cases keep rising, and unions and local politicians are calling for tighter restrictions. With Chilean supply risk growing at a time of recovering Chinese demand, the price of copper is back to near where it started the year.

Codelco’s hardest hit mines are El Teniente and Chuquicamata, with 872 and 571 cases, respectively, as of July 1, according to the union.

The state behemoth has halted development projects at El Teniente, its largest mine, adding to other curtailments and shift-pattern changes. At Chuquicamata, Codelco suspended smelting and sharply reduced refining. BHP Group announced plans last week to scale back its Cerro Colorado mine.

While Chile managed to maintain output at high levels in May, the first clear view into how it fared in June comes on Tuesday, with monthly export data…

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

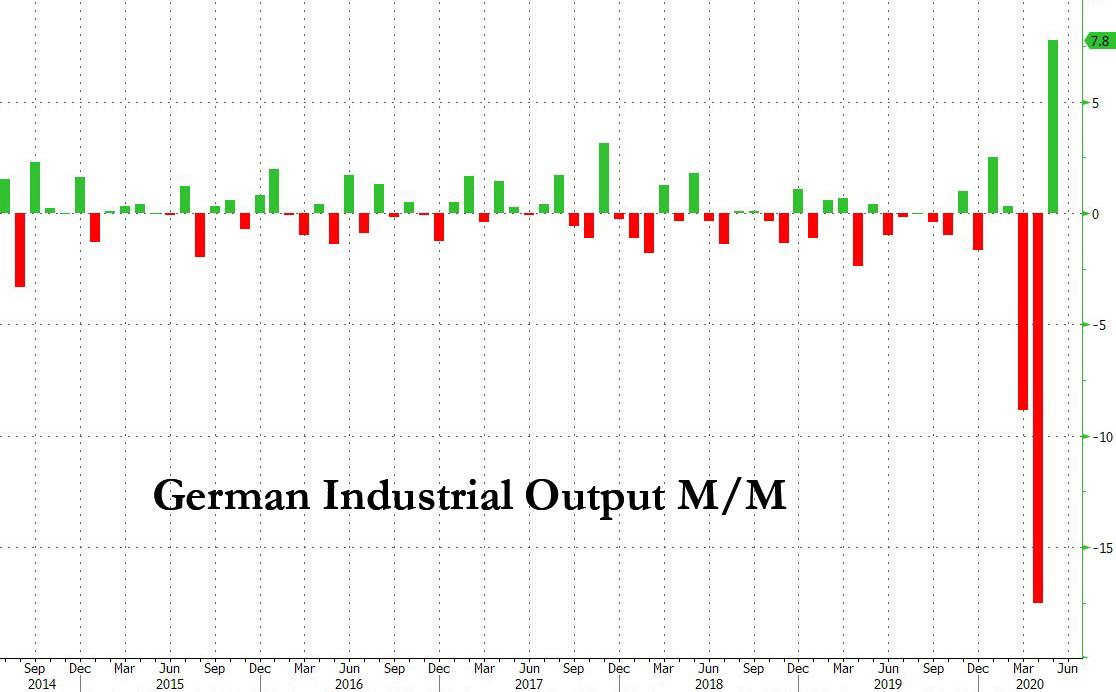

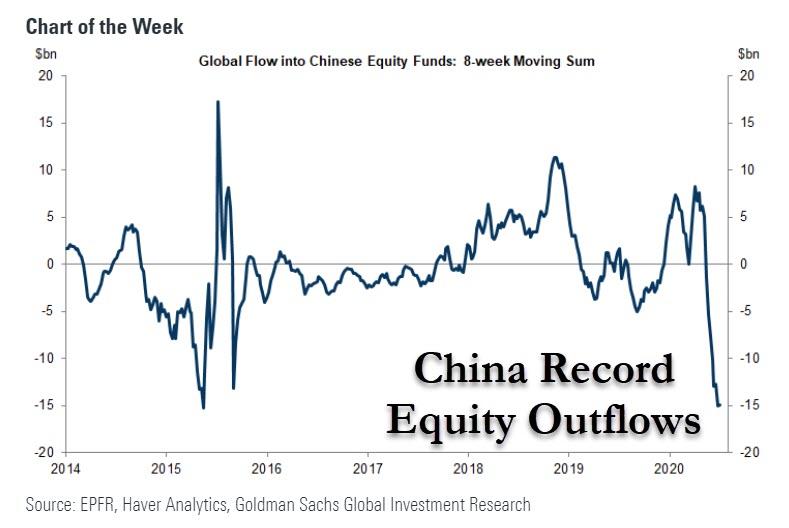

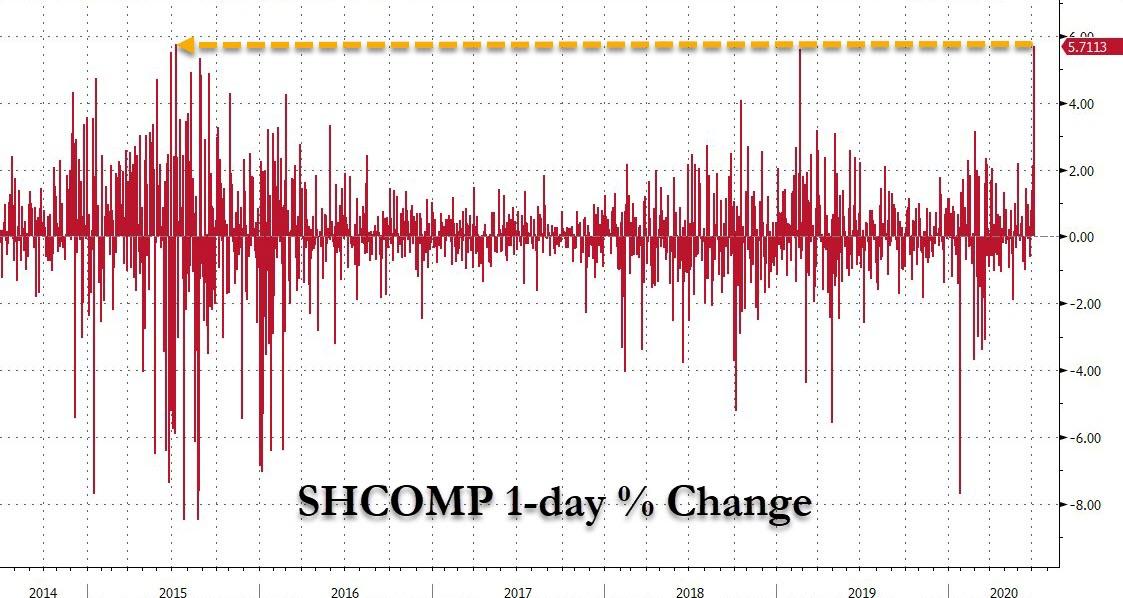

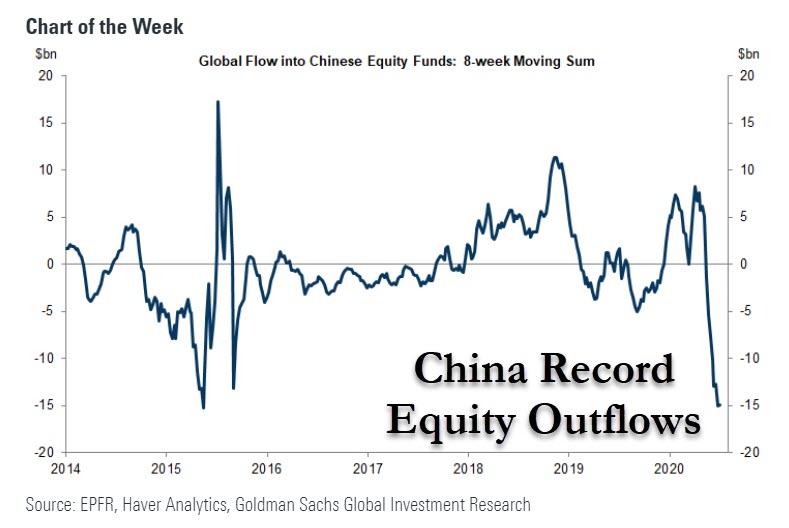

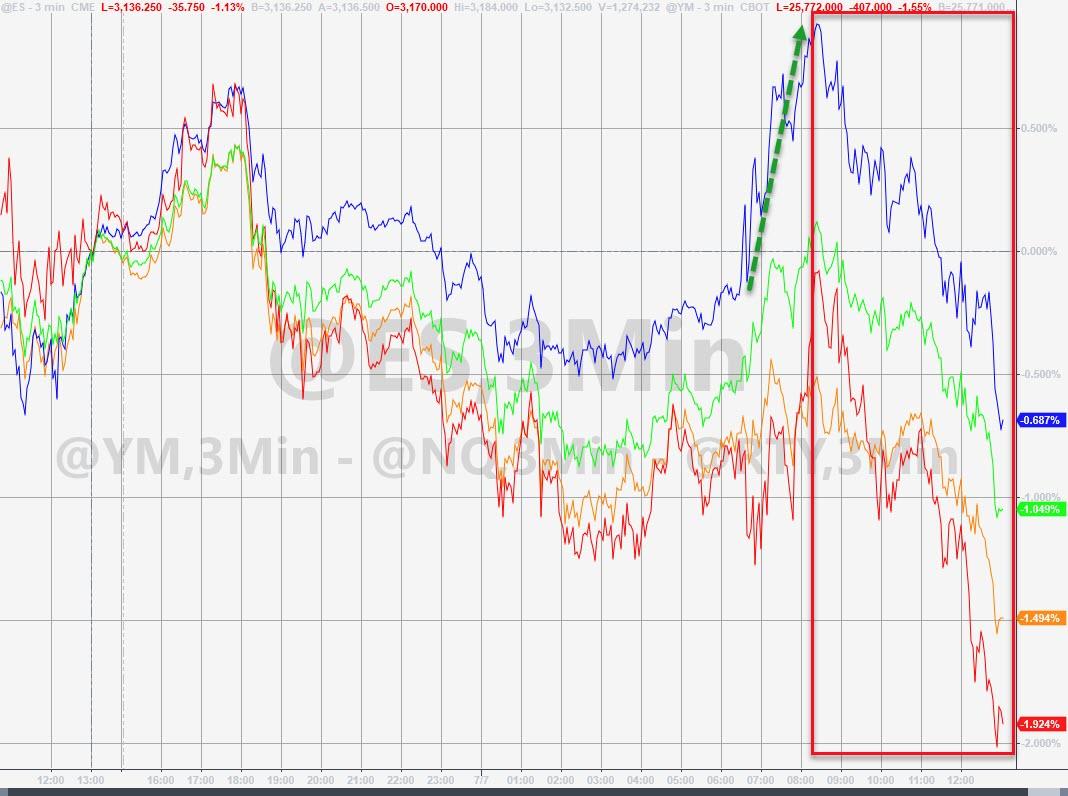

Futures Fall As Europe Slides, Chinese Media Talks Back Rally

One day after a torrid ramp in Chinese stocks sent US futures surging and the Nasdaq hit a fresh all time high, on Tuesday Emini index futures slipped following the benchmark S&P 500 and Nasdaq’s five-day rally, as European stocks slumped after officials warned the economy will take longer to recover and Germany reported weaker-than-expected industrial data, the rally in China fizzled after officials talked back their previous urges to buy stocks, and investors weighed the risks to the economy from tens of thousands of new coronavirus cases nationwide.

On Monday, Miami became the latest U.S. coronavirus hot spot to roll back its reopening while Texas registered an all-time high in the number of people hospitalized at any one moment with COVID-19 for the eight straight day. Travel-related stocks fell in premarket trading. United Airlines Holdings and American Airlines were down 3% and 2.8%, respectively. Royal Caribbean Group and Norwegian Cruise Line Holdings also dropped about 3% each, even as they announced a joint task force to help develop safety standards for restarting their businesses.

The latest virus news dented bullish sentiment after a surprise surge in the U.S. Services ISM and record job additions in June were among the upbeat data recently that have bolstered views that an economic recovery is underway, helping the Nasdaq close at a record level on Monday and pushing S&P 500 about 45% from its March lows.

Sentiment also reversed in Europe, where all but one of the 19 industry groups in the Stoxx Europe 600 Index fell, with real estate and technology shares bearing the brunt of the selling after Germany reported far weaker than expected industrial production data. Bayer AG lost 5.5% after its plan for handling future Roundup cancer claims hit a snag.

On the other end, BMW rose as much as 1.4%, and was the best performer on the Stoxx 600 Automobiles & Parts Index, after posting 17% jump in 2Q car sales in China. The index was the only positive segment on broader European share gauge; other gainers as of 12:01pm in Paris include Valeo +1.1%, Faurecia +0.8%, Fiat Chrysler +0.6%, Continental AG +0.5%.

The European Commission gave its starkest warning yet about the impact of the pandemic, with the divergences between richer and poorer countries opening up even further than projected two months ago. Officials now forecast a contraction of 8.7% in the euro area this year, a full percentage point deeper than previously predicted.

Earlier in Asia, while Chinese stocks powered ahead for a sixth day, the rally was at a far slower pace, with the Shanghai Composite Index rising just 0.4% after the 5.7% surge one day earlier, with Maoye Commercial Co Ltd and Hangzhou Jiebai Group posting the biggest advances.

China’s rally fizzled after all four major state-owned financial media outlets had front page commentaries on the stock market today, with all articles saying largely the same – calls on market participants to be rational. Most Asian stocks fell, led by energy and utilities, after rising in the last session, with Hong Kong’s Hang Seng Index and South Korea’s Kospi Index turning red. Trading volume for MSCI Asia Pacific Index members was 111% above the monthly average for this time of the day. The Topix declined 0.3%, with Tosei and Miyakoshi falling the most.

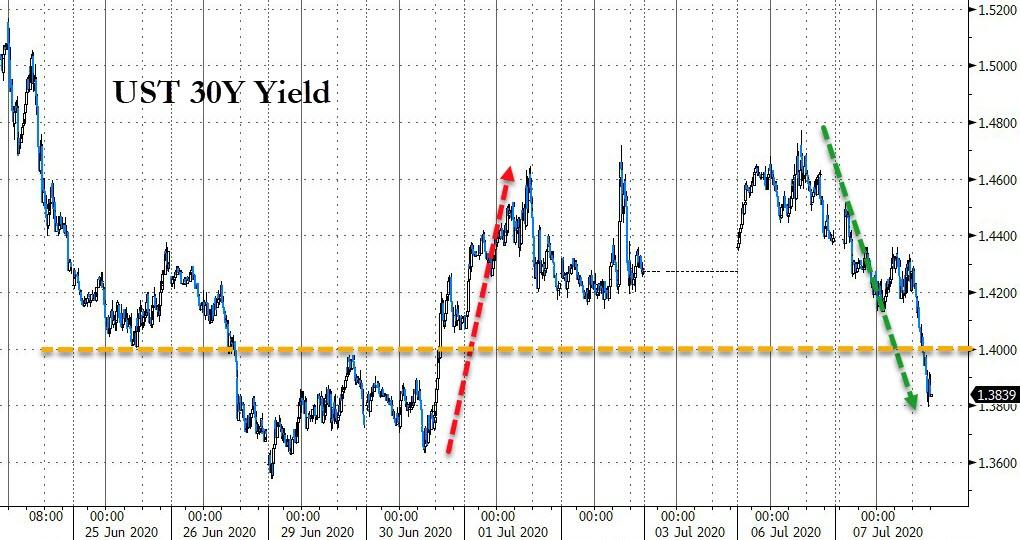

In rates, Treasuries were largely unchanged across the long-end of the curve following mixed performance of Asia stocks; further rally halted with bunds underperforming ahead of EU4b 5-year EFSF deal pricing and looming Irish supply this week. Treasuries also face supply pressure starting with 3-year note auction at 1pm ET, ahead of 10- and 30-year sales to round off the week. Treasury yields were lower by ~1bp across 20- to 3-year sector, little change rest of the curve; 10-year yields around 0.675% while bunds underperform by 1.5bp, gilts trade broadly inline.

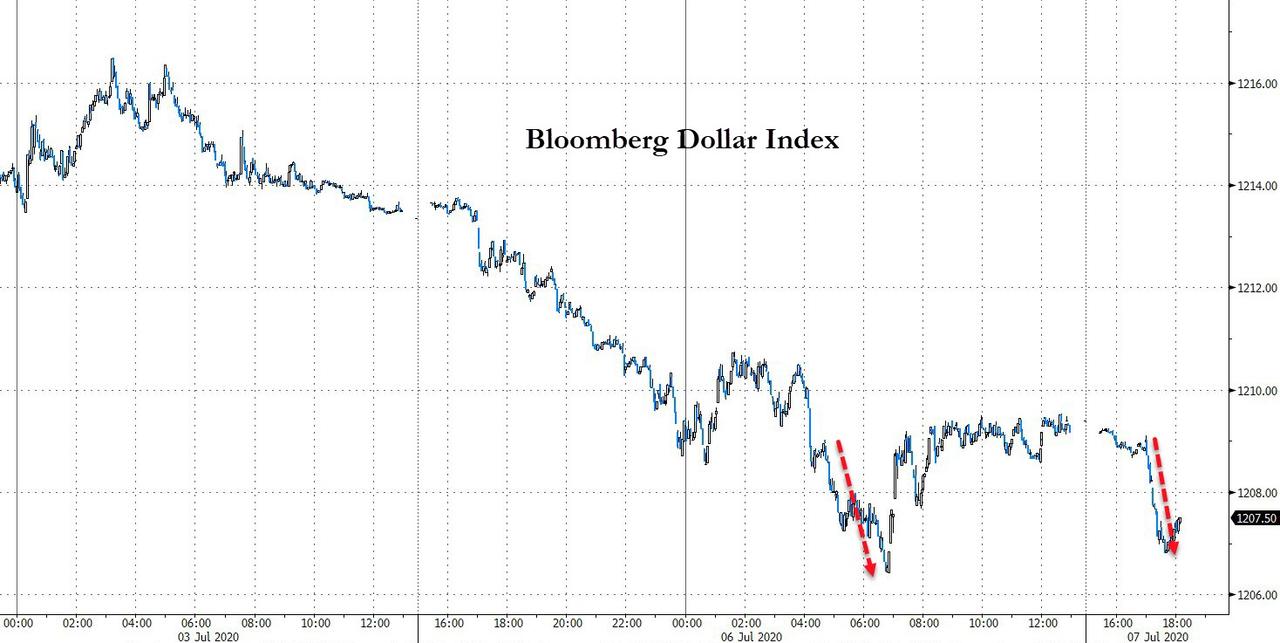

In FX, the Bloomberg Dollar Index snapped a five-day losing streak as the global equity rally paused on Tuesday after a strong start to the week. China’s offshore yuan erased gains after briefly strengthening past the 7 per dollar level for the first time since March 17. The offshore yuan weakened 0.14% as of 6:34 p.m. in Hong Kong. It rose as much as 0.24% to 6.9966 against the greenback in morning session, as Chinese stocks rallied before paring gains in afternoon trade. The currency traded little changed in the onshore market after adding 0.27% earlier Tuesday. A rebounding dollar and renewed concerns about the pandemic after an Australian state announced a lockdown contributed to the yuan’s weakening this afternoon, said Gao Qi, an Asian FX strategist at Scotiabank. But the retreat will likely be a “one-off event,” as bullish sentiment in the stock market will continue to support demand for the currency, he said. “The yuan should advance in the coming sessions to reach 6.90 by the end of July,” he said.

The Australian dollar swung lower after the country’s second- most populous state announced a six-week lockdown to control a wave of infections. Leveraged funds initiated short positions ahead of the lock-down announcement, a trader said, with losses extending after Victoria Premier Daniel Andrews announced a longer-than- expected shutdown. “The local media was suggesting four weeks prior to the announcement, and now it’s six weeks,” said Ray Attrill, head of foreign-exchange strategy at National Australia Bank Ltd. in Sydney. “A justifiable knee jerk, albeit small, negative reaction.”

In commodities, oil dropped and iron ore futures jumped. WTI and Brent crude futures remained on the backfoot, if off lows, as the complex tracks broader market sentiment. Furthermore, the European Commission cutting the EZ and EU growth forecasts added to the bearish factors. WTI Aug resides just above the USD 40/bbl (vs. high 40.79/bbl) having tested the level earlier in the session, whilst Brent Sep relinquished its USD 43/bbl (vs. high 43.19/bbl) handle before finding mild support at the psychological 42.50/bbl. Looking ahead, in the absence of virus/China related headlines, participants will be eyeing the release of the EIA Short-Term Energy Outlook for any potential revisions to global oil demand given the resurging COVID-19 cases, thereafter, focus will turn to the Private Inventory numbers for short-term volatility. Elsewhere, spot gold has fallen victim to the rising Buck as the yellow metal slid from near-8yr highs of around USD 1787/oz to find some solace around the psychological USD 1775/oz. In terms of base metals, Shanghai copper hit a 2020 high amid supply woes coupled with hopes of a rebounding Chinese economy. Similarly, Dalian iron ore was underpinned by China optimism alongside doubts over the prospected of a recovery in Brazilian iron shipments.

Market Snapshot

- S&P 500 futures down 0.8% to 3,148.00

- MXAP down 0.7% to 164.30

- MXAPJ down 0.8% to 541.83

- Nikkei down 0.4% to 22,614.69

- Topix down 0.3% to 1,571.71

- Hang Seng Index down 1.4% to 25,975.66

- Shanghai Composite up 0.4% to 3,345.34

- Sensex up 0.05% to 36,505.16

- Australia S&P/ASX 200 down 0.03% to 6,012.92

- Kospi down 1.1% to 2,164.17

- STOXX Europe 600 down 1.1% to 367.33

- German 10Y yield fell 1.7 bps to -0.448%

- Euro down 0.3% to $1.1277

- Italian 10Y yield fell 1.4 bps to 1.113%

- Spanish 10Y yield fell 1.1 bps to 0.414%

- Brent futures down 1% to $42.69/bbl

- Gold spot down 0.4% to $1,777.09

- U.S. Dollar Index up 0.3% to 97.03

Top Overnight News

- Europe’s economy will suffer more than previously estimated this year and take longer to recover because of a slow easing of coronavirus restrictions, according to the bloc’s executive arm.

- China’s equity market is firmly in the spotlight after an almost unprecedented rally that helped lift global stocks to a one-month high.

- The amount of U.S. bonds and loans trading at distressed levels has increased for a second straight week as corporate borrowers potentially face another round of lockdowns amid a resurgence of the coronavirus.

- France’s decision to give only temporary security approval for fifth-generation mobile equipment shows the government intends to gradually sideline Huawei Technologies Co., a majority party lawmaker said.

Asian equity markets were somewhat choppy as participants began to second guess the viability of the recent Chinese stocks surge which had already reverberated across global counterparts on Monday to lift all major indices on Wall Street and push the Nasdaq to a fresh record high. ASX 200 (U/C) swung between gains and losses as strength in the mining related sectors was initially offset by early weakness in energy, utilities and financials, while second wave fears concerning Australia’s 2nd largest city of Melbourne and the RBA policy announcement further added to the tentative tone. Nikkei 225 (-0.4%) lagged after Household Spending data showed the largest decline on record and the KOSPI (-0.7%) also failed to hold on to early gains as the initial support in Samsung Electronics following a beat in preliminary Q2 results which eventually wore thin. Hang Seng (-1.4%) and Shanghai Comp. (+0.4%) both extended on the prior day’s stellar rally but are off their best levels with the momentum gradually dissipating amid several bearish factors such as another substantial liquidity drain by the PBoC and with Chinese press calling for rationality in the stock markets, while the recent headlines also continued to add to the ongoing China vs. the West narrative including the warning from China’s Ambassador to the UK that it will have to bear the consequences if it treats China as a hostile country. Finally, 10yr JGBs were marginally higher amid underperformance in Japanese stocks following the abysmal Household Spending data and with upside also briefly spurred by mostly firmer results at the 30yr JGB auction.

Top Asian News

- Lebanon’s Economic Crisis Is Spinning Out of Control, Fast

- Samsung’s Profit Beat May Precede Slowing Chip Sales Growth

- Australia Warns Citizens They Risk ‘Arbitrary’ Arrest in China

- SoftBank Hits 20-Year High With $68 Billion Climb Out of Nadir

European stocks have continued to bleed [Euro Stoxx 50 -1.3%], as the mostly positive APAC sentiment dissipated when European players entered the fray. Downside in futures was initially seen overnight as the optimism over China’s recent performance fizzled out amid rising reported cases, which led to the Australian State Premier imposing a six-week lockdown on Melbourne, whilst case numbers remained heightened in other parts of Asia. Furthermore, the European Commission cutting its 2020 and 2021 growth forecasts, due to less swift than expected reopening, only dampened the mood. As such, major bourses trade with broad-based losses of some 1%, but in the periphery, Italy’s FTSE MIB (-0.3%) fares slightly better as losses in banking names were somewhat cushioned by reports the ECB’s Funding to Italian Banks in June rose to EUR 345.226bln vs. EUR 290.963bln in May, although reports noted that the ECB is to consider asking banks to withhold dividend for longer. Sectors remain in negative territory with no clear risk-tone to be derived on that front as cyclicals and defensives remain mixed. Delving deeper into the sectors, a similar performance, but Travel & Leisure resides among the laggard amid the aforementioned dampened sentiment regarding reopening economies. In terms of individual movers, Wirecard (-14%) extended on losses, with reports also noting that payment group Mastercard was warned about Wirecard’s links to an alleged laundering network around four years ago. Micro Focus (-10.3%) holds its place as a laggard after reporting an impairment charge of USD 922.2mln in H1. Bayer (-7%) shares remain pressured after a U.S. judge questioned the Co’s proposed settlement to deal with future claims regarding its weedkiller. On the flip-side, BMW (+1.0%) nursed opening losses after a trading update in which, despite a H1 YY sales decline of 23%, noted that Q2 China sales have exceed the prior and are seeing initial signs of recovery in some markets as of end-Q2. Finally, in terms of commentary, Blackrock has downgraded US equities on risk of fading fiscal stimulus whilst upgrading Europe to overweight.

Top European News

- Europe Sees Deeper Slump With Fresh Warning on Uneven Virus Hit

- Hungary Posts Biggest Increase in Coronavirus Cases in a Month

- France Begins to Sideline Huawei From Its Mobile Networks

- Macron Picks a Government to Rebuild France’s Economy

In FX, a further erosion of bullish risk sentiment has helped the Dollar regain composure and its status as a safe haven following less pronounced gains in Chinese equities overnight and a more mixed session for APAC bourses overall. Hence, the index is back on the 97.000 handle from a low of 96.565 at one stage on Monday and extending recovery gains on the back of a much better than expected services ISM survey.

- AUD – The Aussie is bearing the brunt of the turnaround in risk assets and heightened 2nd wave COVID-19 concerns as Melbourne extends anti-virus measures amidst another rise in cases, with Aud/Usd reversing sharply from just shy of the 0.6900 level towards 0.6920 alongside Usd/CNH bouncing from a fraction below 7.0000. For the record, no surprises from the RBA that reaffirmed wait-and-see guidance, but clearly the economic outlook will be adversely impacted by the aforementioned outbreak in the state of Victoria.

- NZD/EUR/JPY/CAD/CHF/NOK/SEK/GBP – All unwinding more of their recent gains relative to the Greenback, as the Kiwi retreats from around 0.6580 to 0.6520 irrespective of a modest improvement in NZIER Q2 confidence, while the Euro has relinquished 1.1300+ status to test the resolve of decent option expiry interest between 1.1265-75 (1.5 bn). However, the Yen is still pivoting 107.50 and Loonie holding above 1.3600 post-weaker than forecast Japanese household spending data and pre-Canadian Ivey PMIs. Elsewhere, the Franc is hovering circa 0.9450 and 1.0650 vs the single currency, Eur/Nok is near 10.6500 in wake of a steeper decline in Norwegian manufacturing output and Eur/Sek is straddling 10.4500 even though Swedish ip and orders were mixed. Elsewhere, Cable has lost grip of 1.2500 yet again, albeit finding underlying bids ahead of 1.2450 and support some 10 pips below.

- EM – Broad deterioration on the downturn in risk appetite, but the Rand underperforming following a more pronounced than anticipated fall in SA consumer morale.

In commodities, WTI and Brent crude futures remain on the backfoot, albeit off lows, as the complex tracks broader market sentiment, as participants regain focus on rising COVID-19 infection rates which prompted the re-imposition of lockdown measures in some cities, whilst others see their gradual easing plans hindered. Furthermore, the European Commission cutting the EZ and EU growth forecasts added to the bearish factors. WTI Aug resides just above the USD 40/bbl (vs. high 40.79/bbl) having tested the level earlier in the session, whilst Brent Sep relinquished its USD 43/bbl (vs. high 43.19/bbl) handle before finding mild support at the psychological 42.50/bbl. Looking ahead, in the absence of virus/China related headlines, participants will be eyeing the release of the EIA Short-Term Energy Outlook for any potential revisions to global oil demand given the resurging COVID-19 cases, thereafter, focus will turn to the Private Inventory numbers for short-term volatility. Elsewhere, spot gold has fallen victim to the rising Buck as the yellow metal slid from near-8yr highs of around USD 1787/oz to find some solace around the psychological USD 1775/oz. In terms of base metals, Shanghai copper hit a 2020 high amid supply woes coupled with hopes of a rebounding Chinese economy. Similarly, Dalian iron ore was underpinned by China optimism alongside doubts over the prospected of a recovery in Brazilian iron shipments.

US Event Calendar

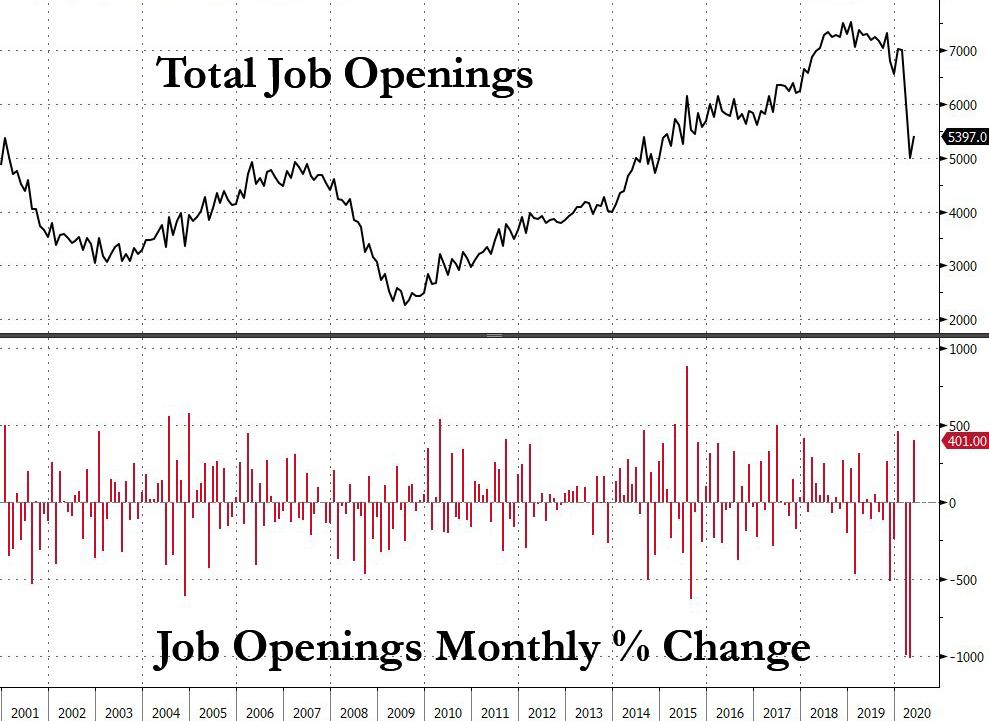

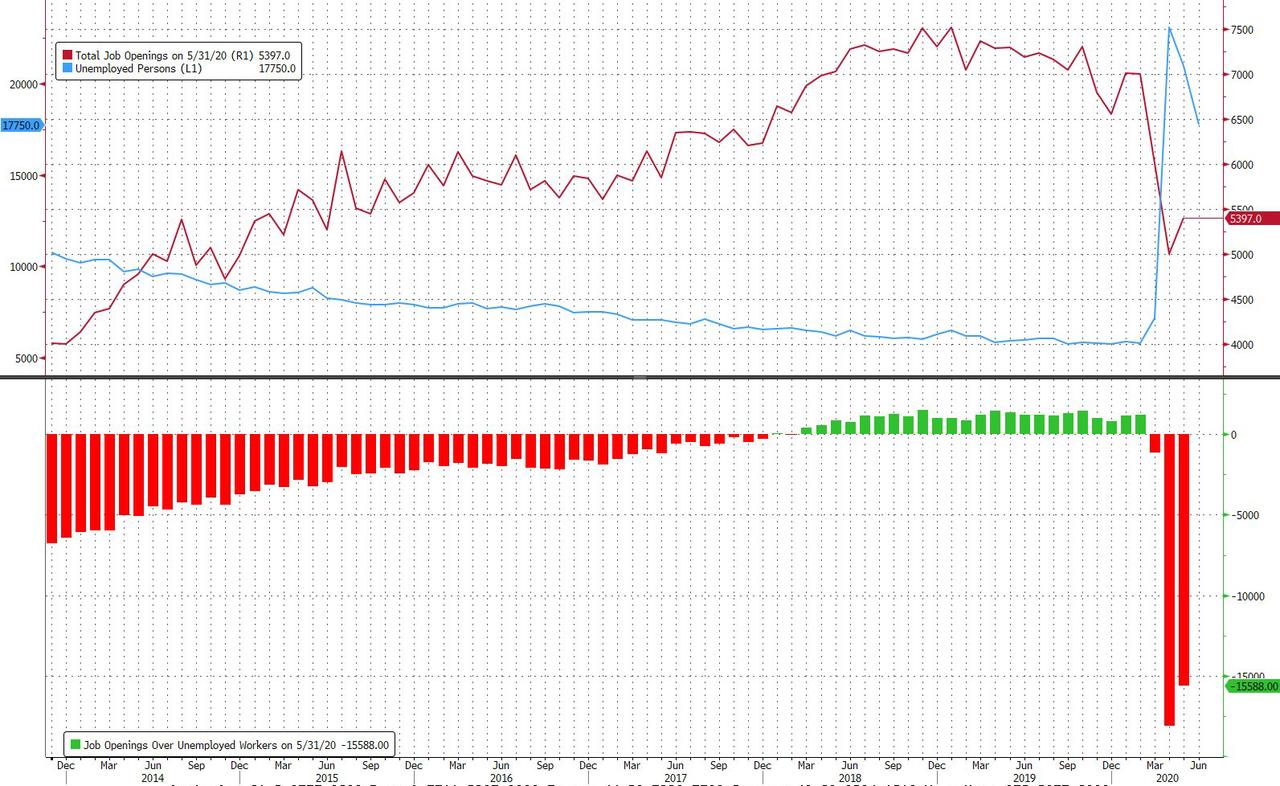

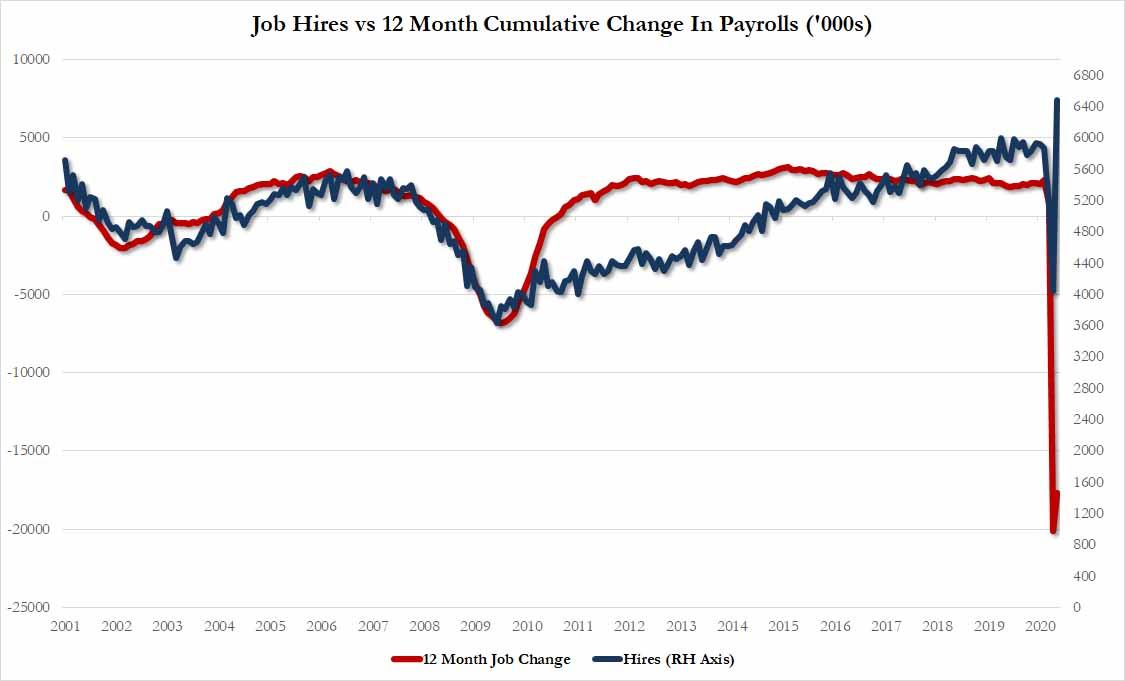

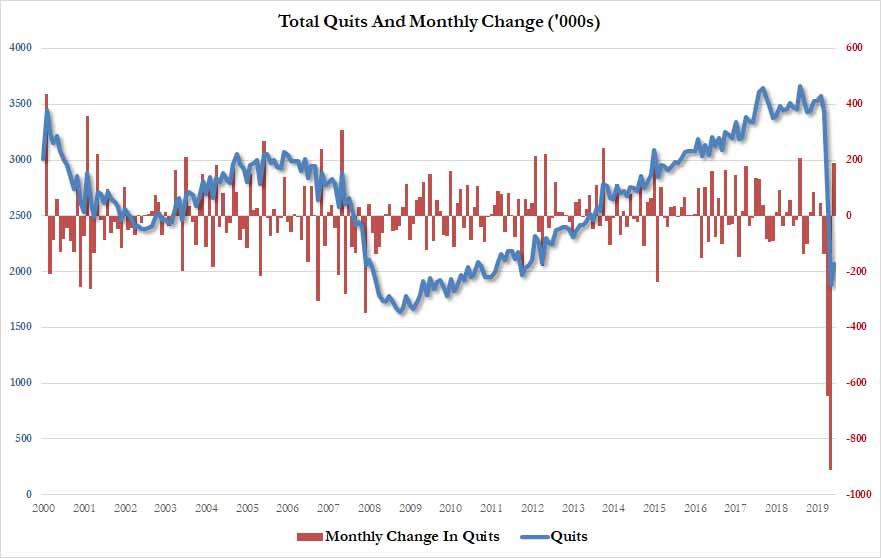

- 10am: JOLTS Job Openings, est. 4,500, prior 5,046

- 9am: Fed’s Bostic Takes Part in Webinar on Economy

- 1pm: Fed’s Quarles Makes Financial Stability Board Remarks

- 2pm: Fed’s Daly and Barkin Takes Part in NABE Talk on Economy

DB’s Jim Reid concludes the overnight wrap

It was Sports Day yesterday at school and like all major sporting events at the moment it was behind closed doors. Maisie told us she won a race but wasn’t particularly specific as to which one. I’m hoping it was the straight sprint but it could obviously be the egg and spoon, beanbag, or wheelbarrow races. In practice over the last month she hasn’t come first in any of the races so I’m proud she’s a big match performer. No point wasting energy when it doesn’t matter. Hopefully lots of ice cream wasn’t on the banned substance list or the medal may eventually be stripped.

The main story in markets yesterday was a race towards a new record for the NASDAQ and a fifth successive rise for the S&P 500 for the first time since December. By the end of the session, the S&P was up +1.59%, with the NASDAQ (+2.21%) closing at an all-time high, something that caught the attention of President Trump, who tweeted about the fact not long after the US session opened. It was one of the quietest days in quite some time for the S&P. After the large overnight move, the index traded within a 27pt range the rest of the day compared to the 55pt average daily range over the last month. In fact, the S&P has only traded within a 27pt range for the entire day 4 other times since it was at all-time highs on February 19. The NASDAQ’s new record was assisted by Amazon, which rose by +5.77% to its own record high, with the company’s share price climbing above $3,000 for the first time thanks to an incredibly strong +65.44% YTD performance. Meanwhile in Europe, the STOXX 600 was up +1.58% at its highest level in nearly a month. Banks (+3.89%) and Autos (+2.56%) led the index higher, as there continues to be a strong value and cyclical theme to the European equity recovery.

The risk-on move was given some added fuel after the ISM non-manufacturing index from the US came in at a much stronger-than-expected 57.1 (vs. 50.2 consensus), a number that was above every estimate on Bloomberg’s survey. And this also comes after last week’s manufacturing ISM rose to 52.6. That said, it’s worth noting that the employment number was not as strong, at just 43.1 (up from May’s 31.8), and already the rise in cases in many US states has led to a reversal in the mobility data, which presents a serious downside risk when it comes to the economic recovery.

The last bit of fuel for yesterday’s US move was word out of Washington D.C. that Senate Majority Leader Mitch McConnell foresees Congress passing another round of fiscal stimulus by the end of this month. The Senator had been fairly circumspect on wanting to see whether the economy needed further action before increasing federal spending, but signaled yesterday that it is indeed needed, saying “This is not over. We are seeing a resurgence in a lot of states… I think the country needs one last boost.” Senate Republicans have called a $3.5trl Democrat-sponsored bill that passed the House in May a nonstarter and are assembling a package with closer to $1trl in total spending.

Asian markets are trading a bit more mixed this morning with the Nikkei (-0.45%) and Kospi (-0.27%) down while in contrast the Hang Seng (+0.12%), ASX (+0.68%) and Shanghai Comp (+1.32%) are up. The CSI 300 is also up +1.82% so there’s been little let up in the rally for Chinese equities and that comes despite China’s Securities Times striking a slight more balanced tone overnight by running a story suggesting that investors should be mindful of potential risks and not use the market as a way to make a fortune. Elsewhere, futures on the S&P 500 are down -0.18% and crude oil prices are down c. -0.30%. In terms of data out this morning, Japan’s May household spending fell by -16.2% yoy (vs. -11.8% expected), the biggest fall in data going back to 2001. This was even as businesses began to reopen and more people ventured out after a nationwide state of emergency was lifted.

Here in the UK, details of Chancellor Sunak’s speech tomorrow are emerging slowly with Bloomberg reporting overnight that he will announce GBP3bn of investments into environmental projects. The treasury has already said that the Chancellor will also announce GBP1.6bn of measures for arts and culture sector as well as spending of c. GBP1bn on tripling the number of traineeships nationwide and doubling the number of work coaches in job centers.

In other overnight news, Hong Kong asserted broad new police powers including warrant-less searches, online surveillance and property seizures under the new security law with City’s Chief Executive Carrie Lam saying that “This law will be enforced very stringently and people’s concerns will be eased.” Lam also reaffirmed that much of the implementation of the law would be managed in secret, saying that a committee created to oversee it wouldn’t release details from future meetings.

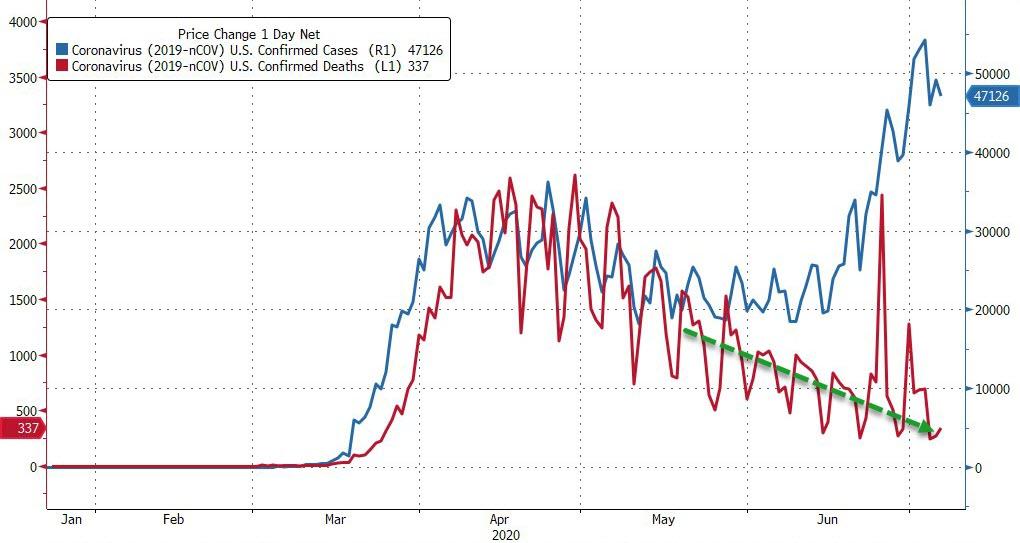

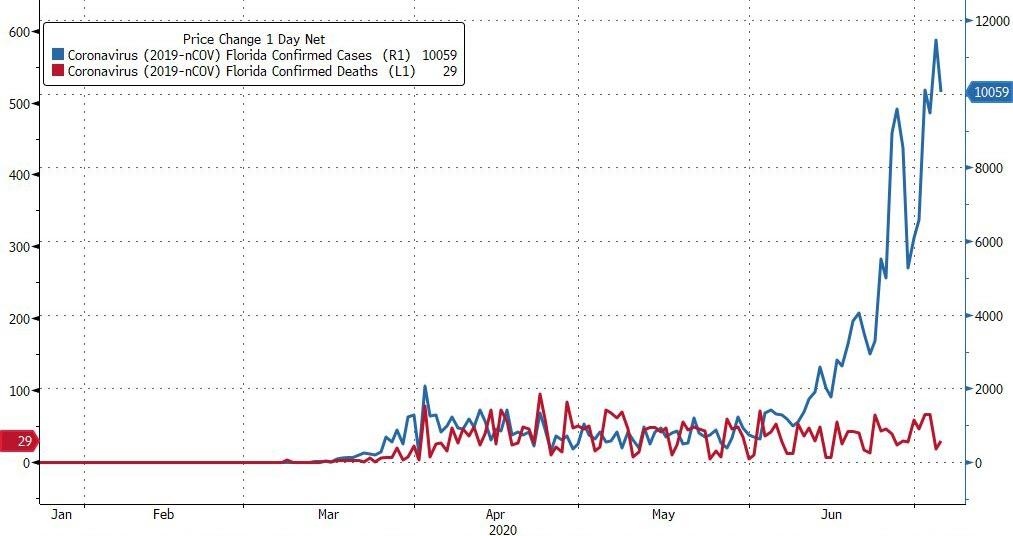

Moving on. When it comes to the coronavirus, yesterday saw the typical slower Monday rise in new cases across many US states due to weekend effects. However the more concerning news for the country is that more states are seeing effective transmission rates (Rt) above 1.0 than in recent weeks. As of yesterday, rtlive estimated that 41 of the 50 states had an Rt value over 1.0, compared to roughly 30 over the past 2 weeks. There is a large amount of uncertainty however, as only one state has a confidence interval entirely under 1.0 (Connecticut) while just three have intervals entirely over 1.0 (WY, WI, MT), though Florida is very close. Specifically cases in Florida rose by a further 3.2% yesterday, but well under the weekly average of 5.1%. Monday has recently seen the week’s lowest daily rise in cases so we would expect to see a sharper rise over the coming days. A similar story emerged in Arizona where new cases rose by 3.4%, below the 4.1% 7 day average. The state also released confirmation that 61% of total cases involve people under 44 years old.

Obviously we need to track the data carefully over the next couple of days as they’ll likely be some catch up from the long weekend in the US. For now you can see the latest state of play in our daily case and fatality tables by clicking “view report” at the top. This also shows that India is now the third most infected country, with confirmed cases nearly at 700K.

Another asset class that did well yesterday was commodities, with Brent Crude up +0.70% near a 4-month high, copper rising a further +1.19% to reach a fresh 5-month high, and gold rising +0.49% to close at a 7-year high. Meanwhile in fixed income, there was a continued narrowing in sovereign bond spreads following last week’s moves. Indeed, the spread of Greek 10yr yields over bunds was down by -1.2bps to 158bps, its lowest level since worries about the pandemic in Europe began in earnest in late February. Core bond yields edged slightly higher however, with 10yr Treasuries up +0.7bps.

Looking at Europe’s data releases yesterday, the main item was the Euro Area retail sales print for May, which surpassed expectations with a +17.8% increase, even if this is still down -5.1% on a year-on-year basis. Over in Germany, factory orders rose by a less-than-expected +10.5% in May (vs. +15.4% expected), with the year-on-year number still down -29.3%. Finally, we got the construction PMIs from Germany and the UK. The German reading only saw a small increase to 41.3, but in the UK there was a big jump to 55.3 (vs. 28.9 in May), its strongest reading since July 2018.

To the day ahead now, and the data highlights include German industrial production and Italian retail sales for May, along with the US JOLTS job openings for the same month. Otherwise, central bank speakers include the Fed’s Bostic, Daly and Barkin, along with the BoE’s Haldane.

3A/ASIAN AFFAIRS

I)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 12.46 POINTS OR 0.37% //Hang Sang CLOSED DOWN 363.50 POINTS OR 1.38% /The Nikkei closed DOWN 99.75 POINTS OR 0.44%//Australia’s all ordinaires CLOSED UP .01%

/Chinese yuan (ONSHORE) closed UP at 7.0257 /Oil UP TO 40.21 dollars per barrel for WTI and 42.83 for Brent. Stocks in Europe OPENED MOSTLY RED// ONSHORE YUAN CLOSED UP // LAST AT 7.0257 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 7.0204 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY PAST 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED //CORONAVIRUS/PANDEMIC : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

3 a./NORTH KOREA/ SOUTH KOREA

South Korea

b) REPORT ON JAPAN

3 C CHINA

CHINA VS USA

Niall Ferguson: a very important commentary explaining that China and the USA are already in Cold War ii

(Niall Ferguson/Bloomberg)

Niall Ferguson: China Has Already Declared Cold War On US

Authored by Niall Ferguson, op-ed via Bloomberg.com,

America and China Are Entering the Dark Forest

To know what the Chinese are really up to, read the futuristic novels of Liu Cixin.

“We are in the foothills of a Cold War.”Those were the words of Henry Kissinger when I interviewed him at the Bloomberg New Economy Forum in Beijing last November.

The observation in itself was not wholly startling. It had seemed obvious to me since early last year that a new Cold War — between the U.S. and China — had begun. This insight wasn’t just based on interviews with elder statesmen. Counterintuitive as it may seem, I had picked up the idea from binge-reading Chinese science fiction.

First, the history.

What had started out in early 2018 as a trade war over tariffs and intellectual property theft had by the end of the year metamorphosed into a technology war over the global dominance of the Chinese company Huawei Technologies Co. in 5G network telecommunications; an ideological confrontation in response to Beijing’s treatment of the Uighur minority in China’s Xinjiang region and the pro-democracy protesters in Hong Kong; and an escalation of old frictions over Taiwan and the South China Sea.

Nevertheless, for Kissinger, of all people, to acknowledge that we were in the opening phase of Cold War II was remarkable.

Since his first secret visit to Beijing in 1971, Kissinger has been the master-builder of that policy of U.S.-Chinese engagement which, for 45 years, was a leitmotif of U.S. foreign policy. It fundamentally altered the balance of power at the mid-point of the Cold War, to the disadvantage of the Soviet Union. It created the geopolitical conditions for China’s industrial revolution, the biggest and fastest in history. And it led, after China’s accession to the World Trade Organization, to that extraordinary financial symbiosis which Moritz Schularick and I christened “Chimerica” in 2007.

How did relations between Beijing and Washington sour so quickly that even Kissinger now speaks of Cold War?

The conventional answer to that question is that President Donald Trump has swung like a wrecking ball into the “liberal international order” and that Cold War II is only one of the adverse consequences of his “America First” strategy.

Yet that view attaches too much importance to the change in U.S. foreign policy since 2016, and not enough to the change in Chinese foreign policy that came four years earlier, when Xi Jinping became general secretary of the Chinese Communist Party. Future historians will discern that the decline and fall of Chimerica began in the wake of the global financial crisis, as a new Chinese leader drew the conclusion that there was no longer any need to hide the light of China’s ambition under the bushel that Deng Xiaoping had famously recommended.

When Middle America voted for Trump four years ago, it was partly a backlash against the asymmetric payoffs of engagement and its economic corollary, globalization. Not only had the economic benefits of Chimerica gone disproportionately to China, not only had its costs been borne disproportionately by working-class Americans, but now those same Americans saw that their elected leaders in Washington had acted as midwives at the birth of a new strategic superpower — a challenger for global predominance even more formidable, because economically stronger, than the Soviet Union.

It is not only Kissinger who recognizes that the relationship with Beijing has soured. Orville Schell, another long-time believer in engagement, recently conceded that the approach had foundered “because of the CCP’s deep ambivalence about the way engaging in a truly meaningful way might lead to demands for more reform and change and its ultimate demise.”

Conservative critics of engagement, meanwhile, are eager to dance on its grave, urging that the People’s Republic be economically “quarantined,” its role in global supply chains drastically reduced. There is a spring in the step of the more Sinophobic members of the Trump administration, notably Secretary of State Mike Pompeo, deputy National Security Adviser Matt Pottinger and trade adviser Peter Navarro. For the past three and a half years they have been arguing that the single most important thing about Trump’s presidency was that he had changed the course of U.S. policy towards China, a shift from engagement to competition spelled out in the 2017 National Security Strategy. The events of 2020 would seem to have vindicated them.

The Covid-19 pandemic has done more than intensify Cold War II. It has revealed its existence to those who last year doubted it. The Chinese Communist Party caused this disaster — first by covering up how dangerous the new virus SARS-CoV-2 was, then by delaying the measures that might have prevented its worldwide spread.

Yet now China wants to claim the credit for saving the world from the crisis it caused. Liberally exporting cheap and not wholly reliable ventilators, testing kits and face masks, the Chinese government has sought to snatch victory from the jaws of a defeat it inflicted. The deputy director of the Chinese Foreign Ministry’s information department has gone so far as to endorse a conspiracy theory that the coronavirus originated in the U.S. and retweet an article claiming that an American team had brought the virus with them when they participated in the World Military Games in Wuhan last October.

Just as implausible are Chinese claims that the U.S. is somehow behind the recurrent waves of pro-democracy protest in Hong Kong. The current confrontation over the former British colony’s status is unambiguously Made in China. As Pompeo has said, the new National Security Law Beijing imposed on Hong Kong last Tuesday effectively “destroys” the territory’s semi-autonomy and tears up the 1984 Sino-British joint declaration, which guaranteed that Hong Kong would retain its own legal system for 50 years after its handover to People’s Republic in 1997.

In this context, it is not really surprising that American public sentiment towards China has become markedly more hawkish since 2017, especially among older voters. China is one of few subjects these days about which there is a genuine bipartisan consensus. It is a sign of the times that Democratic presidential candidate Joe Biden’s campaign clearly intends to portray their man as more hawkish on China than Trump. (Former National Security Adviser John Bolton’s new memoir is grist to their mill.) On Hong Kong, Nancy Pelosi, the Democratic speaker of the House, is every bit as indignant as Pompeo.

I have argued that this new Cold War is both inevitable and desirable, not least because it has jolted the U.S. out of complacency and into an earnest effort not to be surpassed by China in artificial intelligence, quantum computing and other strategically crucial technologies. Yet there remains, in academia especially, significant resistance to my view that we should stop worrying and learn to love Cold War II.

At a forum last week on World Order after Covid-19, organized by the Kissinger Center for Global Affairs at Johns Hopkins University, a clear majority of speakers warned of the perils of a new Cold War.

- Eric Schmidt, the former chairman of Google, argued instead for a “rivalry-partnership” model of “coop-etition,” in which the two nations would at once compete and cooperate in the way that Samsung and Apple have done for years.

- Harvard’s Graham Allison, the author of the bestselling “Destined for War: Can America and China Escape Thucydides’s Trap?”, agreed, giving as another example the 11th-century “frenmity” between the Song Emperor of China and the Liao kingdom on China’s northern border. The pandemic, Allison argued, has made “incandescent the impossibility of identifying China clearly as either foe or friend. Rivalry-partnership may sound complicated, but life is complicated.”

- “The establishment of a productive and predictable US/China relationship,” wrote John Lipsky, formerly of the International Monetary Fund, “is a sine qua non for strengthening the institutions of global governance.” The last Cold War had cast a “shadow of a global holocaust for decades,” observed James Steinberg, a former deputy secretary of state. “What can be done to create a context to limit the rivalry and create space for cooperation?”

- Elizabeth Economy, my colleague at the Hoover Institution, had an answer: “The United States and China could … partner to address a global challenge,” namely climate change. Tom Wright of the Brookings Institution took a similar line: “Focusing only on great power competition while ignoring the need for cooperation will not actually give the United States an enduring strategic advantage over China.”

All this sounds eminently reasonable, apart from one thing. The Chinese Communist Party isn’t Samsung, much less the Liao kingdom.

Rather — as was true in Cold War I, when (especially after 1968) academics tended to be doves rather than hawks — today’s proponents of “rivalry-partnership” are overlooking the possibility that the Chinese aren’t interested in being frenemies. They know full well this is a Cold War, because they started it.

To be sure, there are also Chinese scholars who lament the passing of engagement. The economist Yu Yongding recently joined Kevin Gallagher of Boston University to argue for reconciliation between Washington and Beijing. Yet that is no longer the official view in Beijing. When I first began talking publicly about Cold War II at conferences last year, I was surprised that no Chinese delegates contradicted me. In September, I asked one of them — the Chinese head of a major international institution — why that was. “Because I agree with you!” he replied with a smile.

As a visiting professor at Tsinghua University in Beijing, I have seen for myself the ideological turning of the tide under Xi. Academics who study taboo subjects such as the Cultural Revolution find themselves subject to investigations or worse. Those who take a more combative stance toward the West get promoted.

Yan Xuetong, dean of the Institute of International Relations at Tsinghua, recently argued that Cold War II, unlike Cold War I, will be a purely technological competition, without proxy wars and nuclear brinkmanship. Yao Yang, dean of the National School of Development at Peking University, was equally candid in an interview with the Beijing Cultural Review, published on April 28.

“To a certain degree we already find ourselves in the situation of a New Cold War,” he said. “There are two basic reasons for this. The first is the need for Western politicians to play the blame game” about the origins of the pandemic.

“The next thing,” he added, “is that now Westerners want to make this into a ‘systems’ question, saying that the reason that China could carry out such drastic control measures [in Hubei province] is because China is not a democratic society, and this is where the power and capacity to do this came from.”

This, however, is weak beer compared with the hard stuff regularly served up on Twitter by the pack leader of the “wolf warrior” diplomats, Zhao Lijian. “The Hong Kong Autonomy Act passed by the US Senate is nothing but a piece of scrap paper,” he tweeted on Monday, in response to the congressional retaliation against China’s new Hong Kong security law. By his standards, this was understatement.

The tone of the official Chinese communiqué released after Pompeo’s June 17 meeting in Hawaii with Yang Jiechi, the director of the Communist Party’s Office of Foreign Affairs, was vintage Cold War. On the persecution of the Uighurs, for example, it called on “the US side to respect China’s counter-terrorism and de-radicalization efforts, stop applying double standards on counter-terrorism issues, and stop using Xinjiang-related issues as a pretext to interfere in China’s internal affairs.”

And this old shrillness, so reminiscent of the Mao Zedong era, is not reserved for the U.S. alone. The Chinese government lashes out at any country that has the temerity to criticize it, from Australia — “gum stuck to the bottom of China’s shoe” according to the editor of the Party-controlled Global Times — to India to the U.K.