GOLD:$: 1971.40 UP $2.20 The quote is London spot price (cash market)

Silver:$24.26// UP 23 CENTS London spot price ( cash market)

Closing access prices: London spot

i)Gold : $1977.00 LONDON SPOT 4:30 pm

ii)SILVER: $24.31//LONDON SPOT 4:30 pm

CLOSING FUTURES PRICES: KEY MONTHS

AUGUST GOLD: $1966.10 CLOSE 1::30 PM SPREAD SPOT/FUTURE AUG (BACKWARD $5.30)

OCT GOLD: $1970.90 CLOSE 1.30 PM// SPREAD SPOT/FUTURE OCT /: BACKWARD: $0.50 (

DEC. GOLD $1975.80 CLOSE 1.30 PM SPREAD SPOT/FUTURE DEC $4.40 ($ 8 BELOW NORMAL CONTANGO)

CLOSING SILVER FUTURE MONTH

SILVER SEPT COMEX CLOSE; $24.55…1:30 PM.//SPREAD SPOT/FUTURE SEPT// : 11 CENTS PER OZ (8 CENTS ABOVE NORMAL CONTANGO)

SILVER DECEMBER CLOSE: $24.44 1:30 PM SPREAD SPOT/FUTURE DEC. : 21 CENTS PER OZ ( 9 CENTS ABOVE NORMAL CONTANGO)

DONATE

COMEX DATA

JPMorgan has been receiving gold with reckless abandon and sometimes supplying (stopping)

receiving today: 823/2142

issued; 0

EXCHANGE: COMEX

CONTRACT: AUGUST 2020 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,962.800000000 USD

INTENT DATE: 07/31/2020 DELIVERY DATE: 08/04/2020

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

072 C GOLDMAN 4

072 H GOLDMAN 401

104 C MIZUHO 171

118 C MACQUARIE FUT 1039

118 H MACQUARIE FUT 7

152 C DORMAN TRADING 21

159 C ED&F MAN CAP 14 2

167 C MAREX 225

332 H STANDARD CHARTE 67

355 C CREDIT SUISSE 15

357 C WEDBUSH 1

657 C MORGAN STANLEY 34 34

657 H MORGAN STANLEY 320

661 C JP MORGAN 503

661 H JP MORGAN 264

685 C RJ OBRIEN 6

686 C INTL FCSTONE 326 2

690 C ABN AMRO 164 60

700 C UBS 63

709 C BARCLAYS 194

709 H BARCLAYS 4

732 C RBC CAP MARKETS 13

737 C ADVANTAGE 88 12

800 C MAREX SPEC 146 11

878 C PHILLIP CAPITAL 15

880 C CITIGROUP 7

905 C ADM 50 1

____________________________________________________________________________________________

TOTAL: 2,142 2,142

MONTH TO DATE: 34,874

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 2142 NOTICE(S) FOR 214,200 OZ (6.66 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 34874 NOTICES FOR 3,487,400 OZ (108.47 TONNES)

SILVER

FOR AUGUST

219 NOTICE(S) FILED TODAY FOR 1,095,000 OZ/

total number of notices filed so far this month: 694 for 3.470 MILLION oz

BITCOIN MORNING QUOTE $11,216 UP 158

BITCOIN AFTERNOON QUOTE.: $11,386 UP 317

GLD AND SLV INVENTORIES:

WITH GOLD UP $2.20 AND NO PHYSICAL TO BE FOUND ANYWHERE:

WITH ALL REFINERS CLOSED//MEXICO ORDERING ALL MINES SHUT: WHERE ARE THEY GETTING THE “PHYSICAL?

NO CHANGES IN GOLD INVENTORY AT THE GLD///

GLD: 1,241.96 TONNES OF GOLD//

WITH SILVER UP 23 CENTS TODAY: AND WITH NO SILVER AROUND:

A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: SURPRISINGLY:

A WITHDRAWAL OF 0.931 MILLION OZ FROM THE SLV//

RESTING SLV INVENTORY TONIGHT:

SLV: 567,161 MILLION OZ./

XXXXXXXXXXXXXXXXXXXXXXXXX

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

IN SILVER THE COMEX OI ROSE BY A HUMONGOUS SIZED 5635 CONTRACTS FROM 187,740 UP TO 193,375, AND CLOSER TO OUR NEW RECORD OF 244,710, (FEB 25/2020. THE HUGE SIZED GAIN IN OI OCCURRED WITH OUR $0.82 GAIN IN SILVER PRICING AT THE COMEX. IT SEEMS THAT THE GAIN IN COMEX OI IS PRIMARILY DUE TO HUGE BANKER SHORT COVERING PLUS A GOOD EXCHANGE FOR PHYSICAL ISSUANCE, ZERO LONG LIQUIDATION, ACCOMPANYING A MONSTROUS INCREASE IN SILVER OZ. STANDING AT THE COMEX FOR AUGUST. WE HAD A HUGE NET GAIN IN OUR TWO EXCHANGES OF 6748 CONTRACTS (SEE CALCULATIONS BELOW).

WE HAVE ALSO WITNESSED A HUGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: SEP 1113 DEC: 0 FOR ZERO ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE 1113 CONTRACTS. WITH THE TRANSFER OF 1113 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1113 EFP CONTRACTS TRANSLATES INTO 11.075 MILLION OZ ACCOMPANYING:

1.THE 82 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST 12 MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

2.955 MILLION OZ STANDING FOR FEBRUARY.:

27.120 MILLION OZ STANDING IN MARCH.

3.875 MILLION OZ STANDING FOR SILVER IN APRIL.

18.845 MILLION OZ STANDING FOR SILVER IN MAY.

2.660 MILLION OZ STANDING FOR SILVER IN JUNE//

22.605 MILLION OZ STANDING FOR JULY

10.025 MILLION OZ INITIAL STANDING IN AUGUST.

43.030 MILLION OZ INITIALLY STANDING IN SEPT. (HUGE)

7.32 MILLION OZ INITIALLY STANDING IN OCT

2.630 MILLION OZ STANDING FOR NOV.

20.970 MILLION OZ FINAL STANDING IN DEC

5.075 MILLION OZ FINAL STANDING IN JAN

1.480 MILLION OZ FINAL STANDING IN FEB

23.005 MILLION OZ FINAL STANDING FOR MAR

4.660 MILLION OZ FINAL STANDING FOR APRIL

45.220 MILLION OZ FINAL STANDING FOR MAY

2.205 MILLION OF FINAL STANDING FOR JUNE

86.470 MILLION OZ FINAL STANDING IN JULY.

5.545 MILLION OZ INITIAL STANDING IN AUGUST

FRIDAY, AGAIN OUR CROOKS USED COPIOUS PAPER IN ORDER TO LIQUIDATE SILVER’S PRICE…AND THEY WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE 82 CENTS ).. AND,OUR OFFICIAL SECTOR/BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO FLEECE ANY SILVER LONGS FROM THEIR POSITIONS. THE HUGE GAIN AT THE COMEX WAS ACCOMPANIED BY : i) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS 2) A MONSTROUS INCREASE IN SILVER OZ STANDING FOR AUGUST, STRONG BANKER SHORT COVERING AND 4) ZERO LONG LIQUIDATION AS WE DID HAVE A HUGE NET GAIN OF 6748 CONTRACTS OR 33.74 MILLION OZ ON THE TWO EXCHANGES! YOU CAN BET THE FARM THAT OUR BANKER ARE DESPERATE TO LIQUIDATE THEIR HUGE SHORT POSITIONS IN SILVER

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS

AUGUST

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY /FOR MONTH OF AUGUST:

1113 CONTRACTS (FOR 1 TRADING DAY(S) TOTAL 1113 CONTRACTS) OR 5.565 MILLION OZ: (AVERAGE PER DAY: 1113 CONTRACTS OR 5.565 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF AUGUST: 5.565 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.13% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2020 TO DATE SILVER EFP’S: 1,276.93 MILLION OZ.

JANUARY 2020 EFP TOTALS SO FAR: 181.61 MILLION OZ

FEB 2020 EFP’S TOTAL : …… 259.600 MILLION OZ

MARCH EFP’S ….. 452.280 MILLION OZ //TOTALS//AND A NEW RECORD FOR THE MONTH)

APRIL EFP 95.355 MILLION OZ. (EX. FOR PHYSICALS BECOMING A LOT LESS)

MAY EFP FINAL: 77.27 MILLION OZ

JUNE EXP 71.15 MILLION OZ.

JULY EXP 133.95 MILLION OZ/ (EXCHANGE FOR PHYSICALS STARTING TO RISE EXPONENTIALLY AGAIN)

AUGUST EXP 5.565 MILLION OZ (EXCHANGE FOR PHYSICALS INCREASING)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5635, WITH OUR 82 CENT GAIN IN SILVER PRICING AT THE COMEX ///FRIDAY… THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1119 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER

TODAY WE GAINED AN ATMOSPHERIC SIZED OI CONTRACTS ON THE TWO EXCHANGES: 6748 CONTRACTS (WITH OUR $0.82 CENT GAIN IN PRICE)//

THE TALLY//EXCHANGE FOR PHYSICALS

i.e 1113 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A HUGE SIZED INCREASE OF 5635 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 82 CENT GAIN IN PRICE OF SILVER/AND A CLOSING PRICE OF $24.03 // FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.9665 BILLION OZ TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW AUGUST DELIVERY MONTH/ THEY FILED AT THE COMEX: 219 NOTICE(S) FOR 1,095,000 OZ OF SILVER.

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 244,196 CONTRACTS ON AUG 22.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $14.70//TODAY’S RECORD OF 244,705 WAS SET WITH A PRICE OF: 18.91 (FEB 25/2020)

.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND FEB 2019: 2.955 MILLION OZ/ MARCH: 27.120 MILLION OZ/ APRIL AT 3.875 MILLION OZ/ A MAY: 18.845 MILLION OZ ..JUNE 2.660 MILLION OZ//JULY 22.605 MILLION OZ; AUGUST 10.025 MILLION OZ/ SEPT 43.030 MILLION OZ//OCT: 7.665 MILLION OZ// NOV: 2.630 MILLION OZ//DEC: 20.970 MILLION OZ; JAN: 5.075 MILLION OZ.//FEB 1.480 MILLION OZ//MAR: 23.005 MILLION OZ/APRIL 4.660 MILLION OZ//MAY 45.220 MILLION OZ//JUNE: 2.205 MILLION OZ// JULY 86.470 million oz//AUGUST 5.545 MILLION OZ//

- THE RECORD PRIOR TO TODAY WAS SET IN FEB 25/2018: 244,710 CONTRACTS, WITH A SILVER PRICE OF $18.90//.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017 RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT)

GOLD

IN GOLD, THE COMEX OPEN INTEREST FELL BY A MONSTROUS SIZED 26,875 CONTRACTS TO 559,375 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE HUGE SIZED LOSS OF COMEX OI OCCURRED DESPITE OUR STRONG RISE IN PRICE OF $17.90 /// COMEX GOLD TRADING// FRIDAY// WE HAD HUGE BANKER SHORT COVERING, A HUMONGOUS SIZED INCREASE IN GOLD TONNAGE STANDING AT THE COMEX FOR AUGUST, ALONG WITH ZERO LONG LIQUIDATION ACCOMPANYING A SMALL EXCHANGE FOR PHYSICAL ISSUANCE AND OUR MONSTROUS CULMINATION OF GOLD SPREADER LIQUIDATION. THIS ALL HAPPENED WITH OUR STRONG GAIN IN PRICE OF $17.90. WE WOULD SUGGEST THAT ALL OF THE COMEX OI LOSS WAS DUE TO THIS SPREADER LIQUIDATION.

WE HAD A VOLUME OF 0 4 -GC CONTRACTS//OPEN INTEREST 58

WE LOST A STRONG SIZED 25,080 CONTRACTS (78.00 TONNES) ON OUR TWO EXCHANGES.

ALL OF THE COMEX OI LOSS WAS DUE TO THE LIQUIDATION OF THOSE SPREADERS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1795 CONTRACTS:

CONTRACT .; AUG 0 AND OCT: 1280 DEC: 1667; FEB: 0 ALL OTHER MONTHS ZERO//TOTAL: 1795. The NEW COMEX OI for the gold complex rests at 559,609. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EXCHANGE DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 26,875 CONTRACTS: 26,875 CONTRACTS DECREASED AT THE COMEX AND 1795 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS OF 25,080 CONTRACTS OR 78.00 TONNES. FRIDAY, WE HAD A GAIN OF $17.90 IN GOLD TRADING……

AND WITH THAT GAIN IN PRICE, WE HAD A HUGE SIZED LOSS IN TOTAL/TWO EXCHANGES GOLD TONNAGE OF 78.00 TONNES!!!!!! THE BANKERS/OFFICIAL SECTOR SUPPLIED INFINITE SUPPLIES OF SHORT GOLD COMEX PAPER WITH RECKLESS ABANDON. THE BANKERS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO LOWER GOLD’S PRICE (IT ROSE $17.90).AND IT ALSO SEEMS THAT THEIR ATTEMPT TO FLEECE ANY GOLD LONGS FROM THE GOLD ARENA WAS ALSO UNSUCCESSFUL AS ALL OF THE LOSS WAS DUE TO THE CULMINATION OF SPREADER LIQUIDATION. AS I STATED ON FRIDAY: “SPREADER LIQUIDATION WILL COME TO ITS CONCLUSION WITH THE UPCOMING MONDAY’S REPORT (FRIDAY’S OFFICIAL NUMBERS)”

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES:

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1795) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI (26,875 OI): TOTAL LOSS IN THE TWO EXCHANGES: 25,080 CONTRACTS. WE NO DOUBT HAD 1 )HUGE BANKER SHORT COVERING, 2.)A MONSTROUS INCREASE IN GOLD TONNAGE STANDING AT THE GOLD COMEX FOR THE FRONT AUGUST MONTH, 3) ZERO LONG LIQUIDATION; 4) HUMONGOUS COMEX OI LOSS AND .5) SMALL EXCHANGE FOR PHYSICAL ISSUANCE 6) CULMINATION OF MONSTROUS GOLD SPREADER LIQUIDATION... AND …ALL OF THIS WAS COUPLED WITH OUR STRONG GAIN IN GOLD PRICE TRADING//FRIDAY//$17.90.

THE DOMINANT FACTOR IF NOT ALL OF THE LOSS OF OI AT THE COMEX WAS DUE TO THE SPREADING LIQUIDATION!!

WE ARE BEGINNING TO WITNESS A LACK OF EXCHANGE FOR GOLD PHYSICALS UNDERWRITTEN DUE TO PREMIUMS STARTING TO REAPPEAR IN THE FUTURE PRICE OF GOLD VS LONDON SPOT. THE COST TO THE BANKERS IS JUST TOO GREAT TO ENGAGE IN THESE VEHICLES ONCE THIS OCCURS.

THE FACT THAT WE ARE CONTINUALLY SEEING A DROP IN COMEX OPEN INTEREST AND VOLUMES COUPLED WITH LESS EXCHANGE FOR PHYSICALS PROBABLY MEANS THAT OUR LONGS ARE ALREADY DEPARTING NEW YORK FOR THE NEW PHYSICAL PLATFORM AT LONDON’S LME.

SPREADING OPERATIONS/NOW SWITCHING TO SILVER

OUR SPREADING OPERATION HAS NOW SWITCHED INTO GOLD…..

SPREADING OPERATION FOR OUR NEWCOMERS:

FOR NEWCOMERS, HERE ARE THE DETAILS:

SPREADING LIQUIDATION HAS NOW COMMENCED IN SILVER AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT.

FOR THOSE OF YOU WHO ARE NEW, HERE IS THE MODUS OPERANDI OF THE SPREADERS AND THE CRIMINAL ELEMENT BEHIND IT:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR;

THE SPREADING LIQUIDATION OPERATION IS NOW OVER FOR GOLD..AND WE WILL NOW MORPH INTO AN ACCUMULATION PHASE OF SPREADING CONTRACTS FOR SILVER. THEY WILL ACCUMULATE CONSIDERABLE AMOUNT OF THE CONTRACTS AND THEN LIQUIDATE ONE WEEK PRIOR TO FIRST DAY NOTICE

MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:

.

AS I HAVE MENTIONED IN PREVIOUS COMMENTARIES:

“AS YOU WILL SEE, THE CROOKS WILL NOW SWITCH TO SILVER AS THEY INCREASE THE OPEN INTEREST FOR THE SPREADERS. THE TOTAL COMEX GOLD OPEN INTEREST WILL RISE FROM NOW ON UNTIL ONE WEEK PRIOR TO FIRST DAY NOTICE AND THAT IS WHEN THEY START THEIR CRIMINAL LIQUIDATION.

HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF AUGUST HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF SEPT FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE IN THIS NON ACTIVE MONTH OF AUGUST. BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN SILVER WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2020 INCLUDING TODAY

AUGUST

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 5.58 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2019, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 5.58/3550 x 100% TONNES =0.157% OF GLOBAL ANNUAL PRODUCTION

ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD HAS DISSIPATED THIS MONTH…THE COST TO THE BANKERS TO CARRY THESE CONTRACTS IN LONDON IS BECOMING TOO GREAT FOR THEM.

ACCUMULATION OF GOLD EFP’S YEAR 2020 TO DATE: 3264.12 TONNES

JANUARY 2220 TOTAL EFP ISSUANCE; : 570.19 TONNES

FEB 2020 TOTAL EFP ISSUANCE : 653.78 TONNES

MARCH TOTAL EFP ISSUANCE 1,098.93 TONNES (*AND A NEW ALL TIME RECORD ISSUANCE//22 DAYS)

APRIL TOTAL EFP. ISSUANCE: 243.45 TONNES (EFP ISSUANCE BECOMING A LOT LESS)

MAY TOTAL EFP ISSUANCE: 248.68 TONNES (EFP ISSUANCE STILL LOW// PREMIUM COST TO THE BANKERS IS HUGE..SO ISSUANCE IS LESS)

JUNE TOTAL EFP ISSUANCE: 192.06 TONNES

JULY TOTAL EFP ISSUANCE; 313.09 TONNES ..(EXCHANGE FOR PHYSICALS REVERSE COURSE AND ARE NOW INCREASING!)

AUGUST TOTAL EFP ISSUANCE; 5.58 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 5635 CONTRACTS FROM 187,740 UP TO 193,375 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 2 3/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.

THE HUGE SIZED GAIN IN OI SILVER COMEX WAS PRIMARILY DUE TO; 1) HUGE BANKER SHORT COVERING , 2) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS (SEE BELOW), 3) ANOTHER HUMONGOUS INCREASE IN SILVER OZ STANDING AT THE SILVER COMEX FOR AUGUST, AND 4) ZERO LONG LIQUIDATION

EFP ISSUANCE 1113 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT: 1113 AND DEC. 0 AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1113 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5635 CONTRACTS TO THE 1113 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC GAIN OF 6748 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 33.74 MILLION OZ, OCCURRED WITH OUR 82 CENT GAIN IN PRICE///

NOBODY IS LEAVING THE SILVER ARENA AND NOBODY IS LEAVING THE GOLD ARENA!!

BOTH THE SILVER COMEX AND THE GOLD COMEX ARE IN STRESS AS THE BANKERS SCOUR THE BOWELS OF THE EXCHANGE FOR METAL..THE EVIDENCE IS CLEAR: HUGE AMOUNTS OF PHYSICAL STANDING FOR BOTH SILVER AND GOLD .

(report Harvey)

2 ) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 57.96 POINTS OR 1.75% //Hang Sang CLOSED DOWN 137.22 POINTS OR 0.56% /The Nikkei closed UP 485.38 POINTS OR 2.24%//Australia’s all ordinaires CLOSED DOWN .09%

/Chinese yuan (ONSHORE) closed UP at 6.9846 /Oil UP TO 40.10 dollars per barrel for WTI and 43.30 for Brent. Stocks in Europe OPENED GREEN// ONSHORE YUAN CLOSED UP // LAST AT 6.9846 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9860 TRADE TALKS STALL//YUAN LEVELS GETTING DANGEROUSLY CLOSE TO 7:1//TRUMP INITIATES A NEW 25% TARIFFS FRIDAY/MAY 10/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED//CORONAVIRUS PANDEMIC// : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /TRADE DEAL NOW DEAD..TRUMP RAISED RATES TO 25%

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

(Jan/zerohedge)

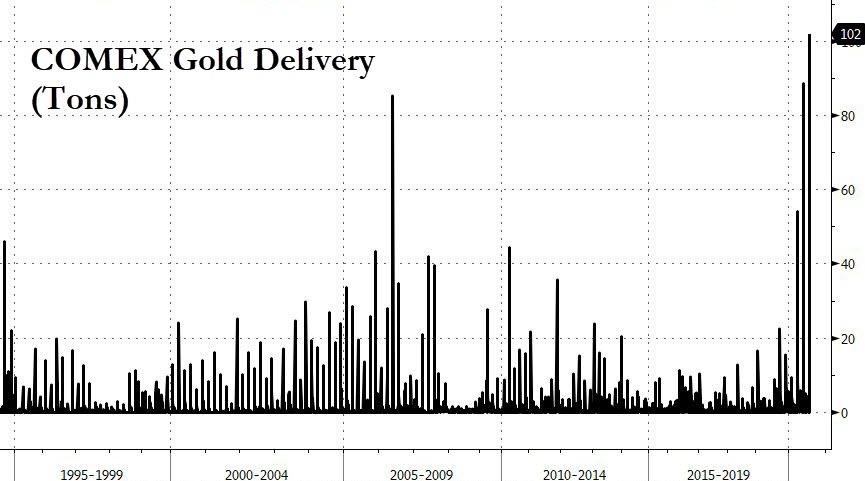

A Record Amount Of Physical Gold Was Just Delivered On COMEX, Here’s Why

Traders on the main gold futures exchange in New York just issued the largest daily physical delivery notice on record.

In the latest sign of how the market’s norms have been upended by the price disconnect that struck in March, Bloomberg reports that traders on Thursday declared their intent to deliver 3.27 million ounces (over 100 tonnes) of gold against the August Comex contract, the largest daily notice in bourse data going back to 1994…

Source: Bloomberg

While millions of ounces of gold trade on the futures market every day, typically only a tiny fraction of that goes to delivery. But in recent months, huge amounts of bullion have flowed into New York and the COMEX has seen record deliveries.

Source: Bloomberg

As Jan Nieuwenhuijs of Voima Gold explains,three elements cause physical delivery on the COMEX to have reached record highs this year:

- strong demand for futures in New York,

- a persisting spread between the price of futures in New York versus spot gold in London,

- and arbitrage.

Physical delivery on the largest gold futures exchange in the world, the COMEX in New York, has reached all time highs this year. Usually, delivery is “negligible.” What has changed?

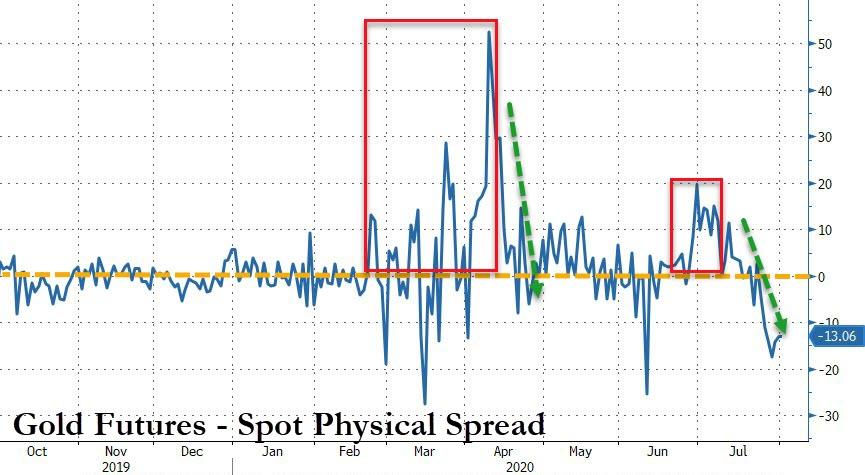

An important change in the global gold market occurred on March 23, 2020. On that day the price of gold futures in New York started drifting higher than the price for spot gold in London. Ever since, the spread has persisted, though it continuously widens and narrows. The reason for this disturbance in the market can be read in my previous article “What Caused the New York vs. London Gold Price Spread and Why it Persists.”

To understand the shift in deliveries, first let’s have a look at how the global gold market operated before March 23, when things still ran smoothly.

The Global Gold Market Before March 23, 2020

The world’s most dominant gold spot market is the London Bullion Market, where mostly “loco London” gold is traded. Meaning the metal is physically settled within the environs of the M25 London Orbital Motorway. The most dominant gold futures market is located in New York, where metal can be physically delivered within a 150-mile radius of the City of New York.

Before March 23, the price in London (spot) and the price in New York (near month futures contract) always traded in tight lockstep because of arbitrage. If, for example, the futures price would trade above spot, arbitragers would “buy spot and sell futures” until the spread was closed. Arbitragers would hold their positions—long spot, short futures—until maturity of the futures contract, because at expiry the price of the futures contract was guaranteed to converge with the spot price. In this example we can see that strong demand in New York would be translated into spot buying in London.

Worth noting is that when a futures trader rolled its position into the next month, and his initial futures buying was translated into spot buying in London by an arbitrager, on a systemic level the arbitrager would roll its position as well.

Of course, the opposite happened as well. When futures traded below spot, arbitragers would “buy futures and sell spot” until the spread was closed.

So far, a simplified version of the market before March 23.

The Global Gold Market After March 23, 2020

Since March 23 of this year, futures have persistently been trading above spot, though the spread isn’t constant. As a result, arbitragers aren’t assured the futures price in New York will converge with the spot price in London. An arbitrage trade as described above, through a position in both markets, incurs risk.

What arbitragers currently do to profit from the spread is buy spot, sell futures, fly the metal to New York, and physically deliver the gold. This is how the profit is locked in. If the spread between spot and futures is $40 per ounce, the arbitrager’s profit is $40 minus costs for transport, insurance, storage, etc.

Now you can see why the persistent spread between New York and London has increased physical delivery on the COMEX through arbitrage.

Conclusion

Physical delivery on the COMEX is elevated because of the current unusual situation in the global gold market. The gold delivered in New York has been imported from spot markets such as Singapore, Switzerland and Australia. U.S. imports directly from the U.K. are rare, because in London 400-ounce bars are traded and the main futures contract in New York requires smaller bars for delivery.

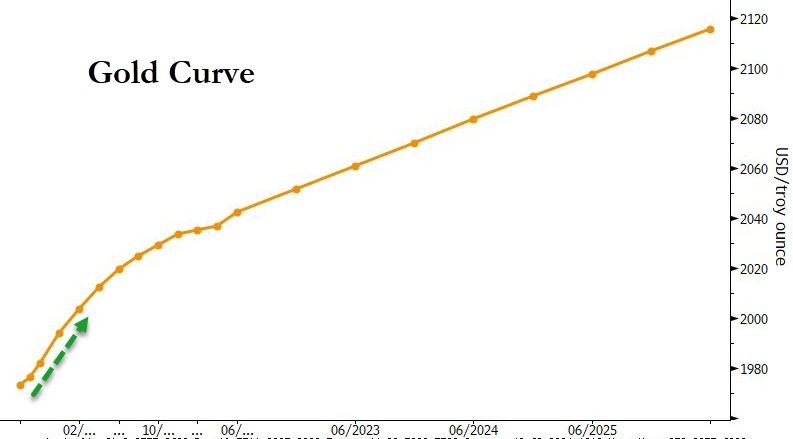

You might wonder who takes delivery from arbitragers that make delivery on the COMEX. Possibly, these are arbitragers, too. In the chart below you can see the spread between the “near month futures contract” and the “next near month futures contract.” This spread has also blown out on March 23. Arbitragers can buy the near month, and sell the next near month for a higher price. Subsequently, they take delivery of the near dated contract and make delivery of the further dated contract.

At the time of writing the near month (August) is trading at $1,973, while the most active month (December) trades at $1,994 dollars.

Arbitragers can buy long August and sell short December to collect $21 dollars per ounce.

One reason I can think of why the spreads persist, is because bullion banks are currently less active on the COMEX. Previously, bullion banks—having access to cheap funding—often performed the arbitrage trades.

* * *

end

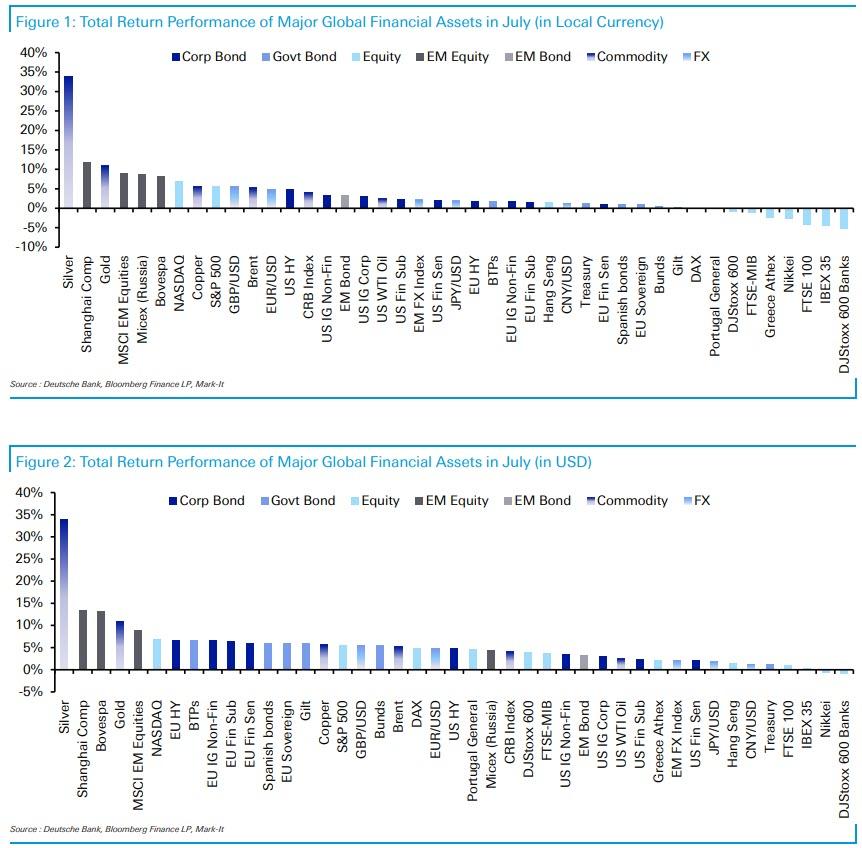

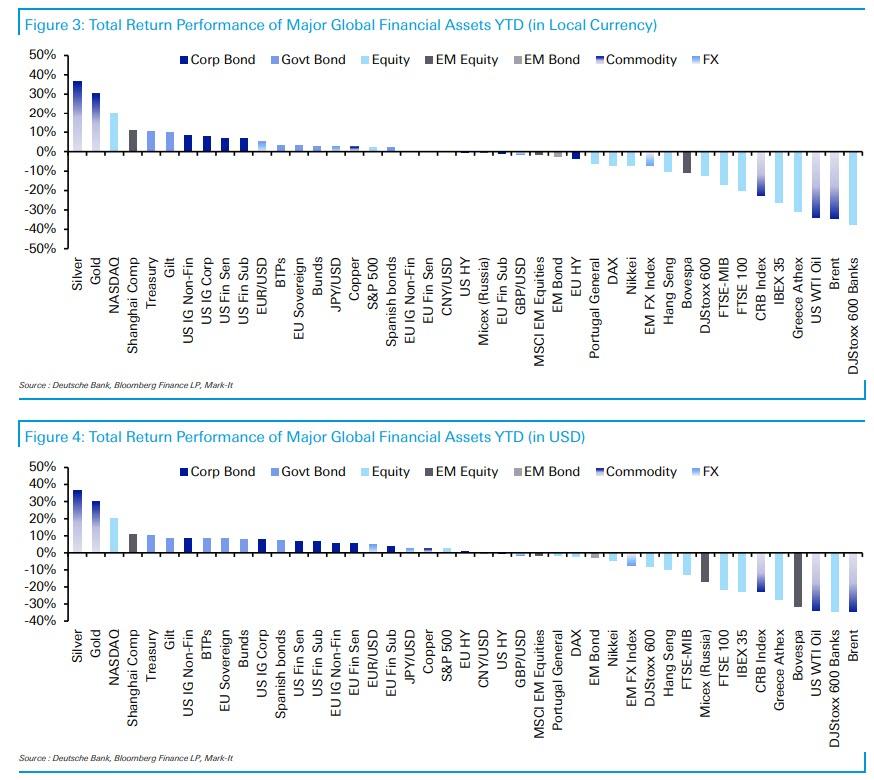

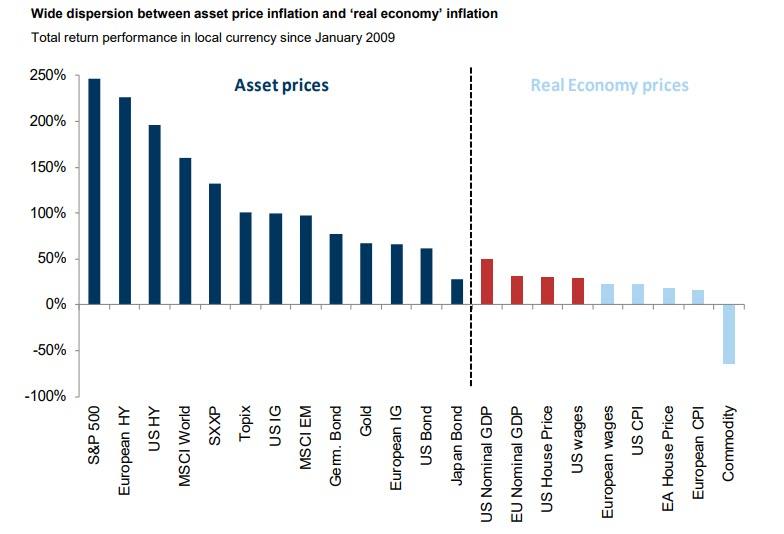

Silver Just Had Its Best Month In 40 Years: Here Are July’s Best And Worst Performing Assets

When looking at the torrid market performance in July, Deutsche Bank’s Jim Reid notes that silver (+35%) had its best month since December 1979 while the dollar the worst for a decade. US equities had a good month in spite of rising virus caseloads due to a strong earnings season relative to expectations, especially in tech towards the end of the month. YTD Silver, Gold and the NASDAQ have been the three best performers while at the bottom of the leaderboard Brent, WTI and European Banks are all down at least 30%.

Below we present some of the key highlights from Deutsche Bank’s July 2020 performance review

While July proved to be another decent month for risk assets, it was the performance of two other assets in particular which caught the eye. The first was Silver, which had its strongest month since December 1979. The second was the weakness in the USD, which ended with the USD spot index dropping by the most in a single month since September 2010.

Indeed the impact of the latter was fully felt when looking at returns in USD terms, with 36 of the 38 assets in DB’s sample finishing with a positive total return. In local currency terms, that number dropped to a still-impressive 30 assets. As markets move into August, typically a more subdued month for volumes but perceived to be a weaker month for risk, the focus remains on the reopening of economies on the one hand and signs of rising cases in certain countries on the other.

First, let’s look at silver, which rallied +34.0% during July, pushing it straight to the top of Deutsche Bank’s YTD leaderboard with a +36.6% advance. Gold also had a strong month, in part helped by the tailwind of the weaker USD, rising +10.9% for its biggest monthly gain since February 2016. In fact it was a good month for

commodities all round, with Copper (+5.7%), Brent (+5.2%) and WTI (+2.5%) also up, while the broader commodity index gained +4.1%.

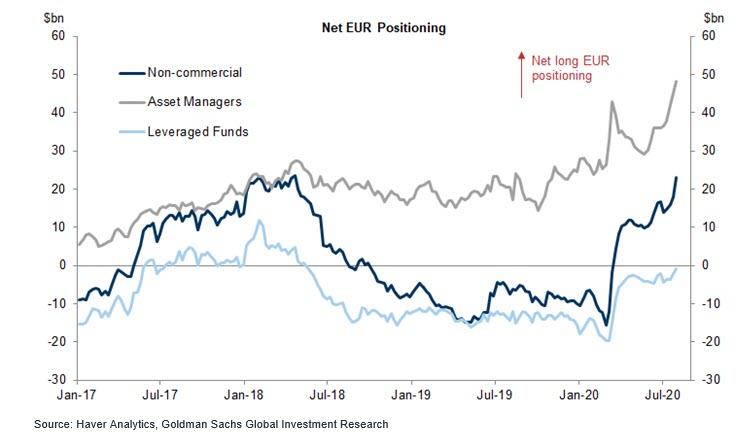

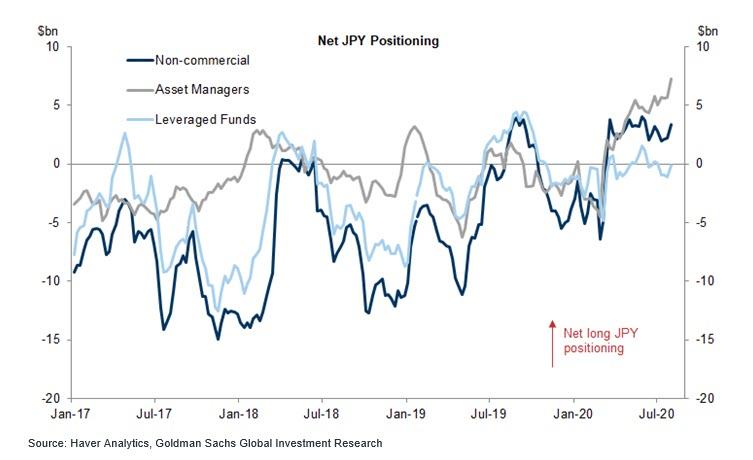

As mentioned, the other big mover was the USD with GBP, EUR and the JPY strengthening +5.5%, +4.8% and +2.0%, respectively, versus the greenback. EM FX also gained +2.1%. In USD terms, that move saw equity markets in Europe post gains of anywhere from 1% to 5% (with the exception of European Banks, which returned -0.8%) with the STOXX 600 up +3.9%; however, in local currency terms returns were flat to -4%.

As for US equity markets, it was another strong month for the tech sector with the NASDAQ returning +6.9% while the S&P 500 finished with a total return of +5.6%. It was more of a mixed story in Asia with the Shanghai Comp returning +12.0% in local currency terms while in contrast the Hang Seng returned just +1.5% and the Nikkei -2.6%.

Finally, as for bond markets, another month of declining yields and in some cases record-low yields meant returns were anywhere from +0.4% for Gilts to +1.7% for BTPs. Again, the weaker USD propelled USD returns last month, up to +6.7% for BTPs and +5.5% for Bunds. For completeness Treasuries returned +1.2%. Last but not least, it was a similar story for credit, where in local currency terms USD outperformed EUR by 1-2 percentage points, with USD HY outperforming IG.

A quick recap of where things stand YTD. In local currency terms 18 of the 38 assets in our sample have a positive total return while in USD terms that number rises to 20. Silver, Gold and the NASDAQ have been the three best performers while at the bottom of the leaderboard Brent, WTI and European Banks are all down at least 34%.

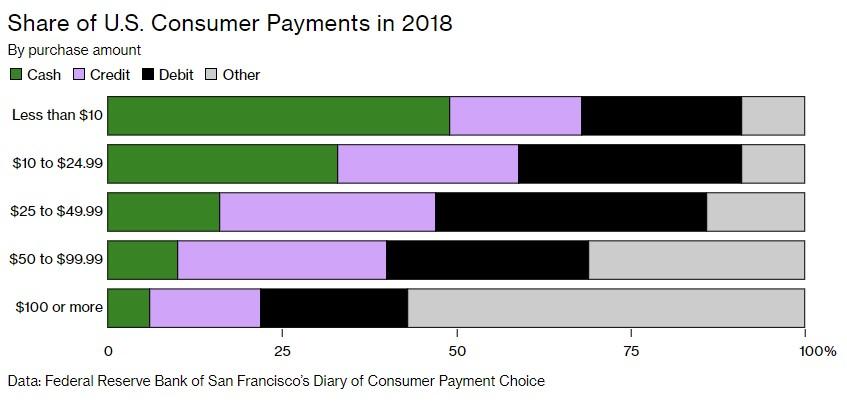

Coin shortage is getting worse:

(zerohedge)

America’s Coin Shortage Is Getting Worse

The nation’s coin shortage, prompted by less cash circulating as a result of Covid-19 – is getting worse.

And believe it or not, cash is still being used in 49% of payments that are $10 or below, according to a recent study by the Federal Reserve Bank of San Francisco, reported on by Bloomberg.

The irony of the situation lies in the fact that the Fed can print trillions for bonds, but can’t come up with a couple of quarters to do its laundry. Despite the Fed’s best efforts to keep money circulating, there is still a coin shortage in the U.S. The effects are being felt in places like laundromats, where coins are used to do laundry.

Brian Wallace, president and CEO of the Coin Laundry Association (we swear this is an actual organization), said: “This is just an unexpected wrench in the works that I don’t think any of us could have anticipated, finding ourselves short on quarters.”

Only about 20% of laundromats offer a card option and 27% accept credit cards. In other words, most laundromats still rely on coins to do business.

“The people that show up to the laundromat each weekend are there for a purpose. It’s an essential service. Anything that impedes that progress certainly impacts tens of millions of families that use vended laundry each week,” Wallace continued.

Coinstar, which processed $2.7 billion worth of coins last year, collects an 11.9% fee from customers. The company has said its business has decreased during the lockdown, but it is now starting to see a slight bounce back. And despite operating in Japan, Canada, Italy, and several other European countries, it hasn’t seen the same issues outside the U.S.

“There’s something unique about the U.S. that we can’t figure out why this has come to this crisis,” says Jim Gaherity, chief executive officer of Coinstar. “I don’t refer to it as a shortage, I refer to it as ‘We don’t have coin moving.’ It’s there, it’s just not in the right place.”

Jerome Powell said in June that the shortage would be temporary, while at the same time U.S. mints spool up more production.

The Fed has, in the interim, put together a “coin task force” to liaise with companies like Coinstar to help come up with solutions. Organizations like the Coin Laundry Association have suggested the Fed distributing additional coins and prioritizing to “consumer businesses in the essential critical infrastructure workforce.”

Banks and businesses are also offering premiums and deals for turning in your coins. One Wisconsin bank is offering a $5 bonus for every $100 worth of coins that are turned in. Recall, days ago, we wrote that Chick-Fil-A was giving away free food to customers who paid in coins.

end

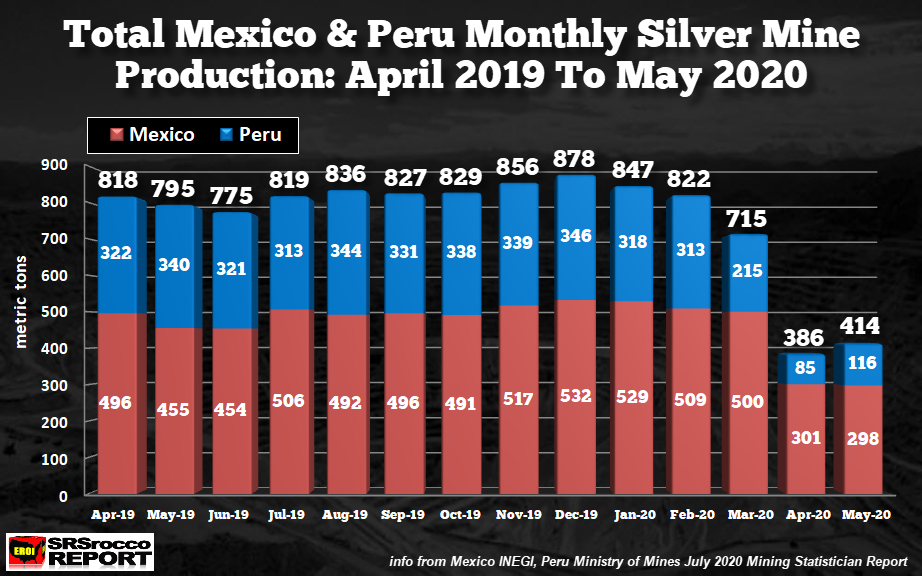

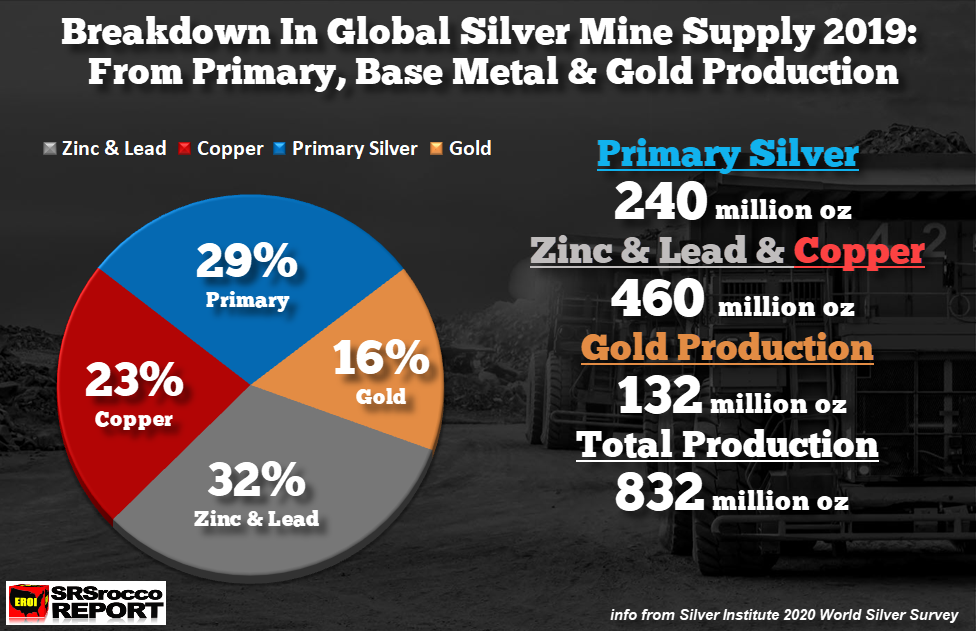

Silver production from our two biggest producers, Mexico and Peru is playing havoc to our bankers who need physical supplies badly.

(Steve St Angelo/SRSRocco report)

CHART OF THE WEEK: Mexico & Peru Silver Production Big Declines Again In May

According to the data released by Mexico and Peru’s governmental mining data, domestic silver production continued to be depressed in May. Interestingly, the production data just released from Mexico’s INEGI shows that the country’s silver production in May was even less than what they reported for April.

I first wrote about this in my article, World’s Two Largest Silver Producers Mine Supply Cut Drastically In April. The combined silver production loss from Mexico and Peru in April was 432 metric tons or 53% versus the same month last year. Peru accounted for the largest of the decline in April at 237 metric tons (mt) compared to 195 mt for Mexico.

However, Mexico’s silver production in May dropped to 298 mt compared to 301 mt in April. Here is the combined silver production by Mexico and Peru from April 2019 to May 2020:

The net loss of silver production from Mexico and Peru over the last three month period (March to May) is 770 mt, or 32% less than it was during the same period last year. Thus, just these two countries have lost nearly 25 million oz of silver production. I imagine once we factor in losses of silver production from other countries, we could see upwards of 35-40+ million oz decline so far.

But, this is only PHASE ONE of the collapse in global silver production. I stated that as the U.S. and the global economy begin to roll-over in the second half of 2020, and onwards, we are going to see a reduction in base metal demand. With so many people becoming unemployed, the global recession-depression will cause a significant decrease in copper, zinc, and lead demand. Thus, in PHASE TWO, demand for base metals will decline, and with it, the curtailment of copper, zinc, and lead production.

With 55% of global silver mine supply as a by-production of base metal mining, any reduction of copper, zinc, and lead production will negatively impact the silver market.

With the negative fundamentals for global silver supply continuing in the future, along with increased investment demand, the world will eventually find out that silver is one of the most undervalued assets in the world.

Yes, it’s true that demand for silver in Jewelry and Industrial applications has likely fallen significantly in Q2 2020. Still, with over $450 trillion held in global Stocks, Bonds, and Real Estate, total global silver investment is a fraction of a fraction. According to the World Silver Survey, there is about 2.5 billion oz of “Identifiable Above-Ground” silver investment stocks in the world. I provided some simple silver valuations below:

2.5 Billion oz Silver Investment Stocks X $25 per oz = $62.5 billion

5.0 Billion oz Silver Investment Stocks X $25 per oz = $130 billion

If just $1 trillion of that $450 trillion attempted to move into silver, that would push the silver price up nearly eight times… almost $200 per oz. But, that is if all that 5 billion oz of silver was able to be accessed. I would imagine a large percentage of that silver will continue to stay in STRONG HANDS.

end

J Johnson’s commodity report// (silver/gold)

Trust is Everything in The Game of Confidence!

Posted August 3rd, 2020 at 8:59 AM (CST) by J. Johnson & filed under General Editorial.

Great and Wonderful Monday Morning Folks,

Gold is trading higher, but nowhere near the opening rally, with the trade at $1,986.40, up 50 cents after hitting another N-LoCH (New Life of Contract High) at $2,009.50 with the low nearby at $1,982. Silver is still leading the rally, after hitting the early-trade-high at $25.275, with the price right now at $24.37, up 15.4 cents after being knocked down to $24.16. The US Dollar is getting that overseas support, even while we are printing it (to cause that eventual drop), with the current value pegged at 93.725, up 40.4 points and close to the high at 93.815 with the low down at 93.295. Of course, all this happened before 5 am pst, the Comex open, the London close, and after a weekend of no news by the Leftist Media who chose to ignore all the Court Docs alleging Bill Clinton visited Epstein Island. Maybe this explains why fewer and fewer are getting the news from the media.

In Venezuela, Gold is now priced at 19,839.17 Bolivar, pulling back 54.93 from Friday’s quote with Silver at 243.395, it too getting a 1.049 Bolivar pullback. Argentina’s currency is now pricing Gold at 143,642.95 dropping 170.70 Peso’s with Silver losing 4.91 with the last trade at 1,762.27 A-Peso’s. The Turkish Lira’s price for Gold last traded at 13,871.83 Lira, dropping 14.28 from Friday’s value with Silver losing 0.416 of a T-Lira with the price now at 170.190.

August Silver’s Delivery Demands now has a post of 914 fully paid for contracts up on the board, unchanged from Friday’s count, waiting for receipts and with a Volume of 1 and with no price attached to it. Friday’s delivery activities happened in between $24.385 and $23.565 with the last buy at $24.189 up 84.9 cents with a Volume of 220 (swaps) that were completed by the end of the day. This proves NO drop in the demand count at all! So, did 220 contracts get a jump in deliveries ahead of the supposed FIFO (First In-First Out) claims of engagement? Silver’s Overall Open Interest now sits at 187,741 Overnighters going against the physicals proving a drop of 76 after the Sunday night drop, from the high.

August Gold’s Delivery Demands now sit at 47,211 fully paid for contracts waiting for receipts. Ironically the delivery count is also unchanged from Friday’s numbers with a Volume of 310 already up on the board with a trading range between $1,984.30 and $1,963.10 with the last buy at $1,967 up $4.20 so far today. Friday’s full trading day had a Volume of 2,914 up on the board with a trading range between $1,981.10 and $1,948 with the last buy at $1,962.80, settling the day out with a $20.50 gain. Gold’s Overall Open Interest declined by 1,076 short contracts leaving 586,484 Overnighters going against the price.

Australia got the bio-bug! The premier of Victoria plunged the region into a “state of disaster” on Sunday, announcing even stricter lockdown measures, introducing a nightly curfew and banning virtually all trips outdoors after Australia’s second largest state recorded 671 new infections in a single day. We’re 6 months into a bug release from a level 4 bio-lab and still no confirmation on anything except all the masksperts making idiots out of both sides as we all learn about this together.

Real or not, the Bio has caused immeasurable amounts of damage to the controllers of debt all over the world with the latest claim that more than 60% of Global Debt now yields less than 1% ROI. Also of note; HSBC crashed to an 11 Year low as their profits plunged and as the loss of reserves expands, with low export trades, now and in the future, causing a drop of 6.4% in share value already today. This bank seems to have a trust problem lately. Trust is everything in the game of confidence and that confidence is gone. That should lead to the debt of a nation being untrustworthy too. Then today, our VOM2 Money Stock came in and it ain’t good at all, yet the price of our currency stays in place (for now).

Got Silver and Gold? Have a great day no matter what! Keep that smile going for all you may see, as you keep safe distance and as we make it thru another month of debt issues and precious metals risings. As always …

Stay Strong!

Jeremiah Johnson

More J.Johnson content is available with purchase of a JSMineset subscription.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

March 4.2019

Parker City News

JP Morgan faces potential class action lawsuit after guilty pleas by a former metals trader

Traders from across the U.S. are banding together to accuse J. P. Morgan Chase of manipulating precious metals markets for years.

At least six lawsuits, all making similar allegations against the nation‘s largest bank, have been filed in New York federal court in the past month, since federal prosecutors in Connecticut with a former J. P. Morgan Chase metals trader.

The cases could potentially include thousands of people who traded in the precious metals market. The White Plains, N.Y., law firm Lowey Dannenberg is asking the court to combine the cases and name it as the lead.

The law firm‘s commodities group is led by Vincent Briganti, the attorney who filed the first lawsuit on behalf of Dominick Cognata, a New York resident who alleges he suffered losses due to J. P. Morgan‘s trading conduct in the silver and gold futures and options markets.

A combined case, seeking class action status, would include anyone who purchased or sold futures contracts or an option on NYMEX platinum or palladium or COMEX silver or gold between at least Jan. 1, 2009, and Dec. 31, 2015. The lawyers believe that “at least hundreds, if not thousands” of traders would be eligible to join the case.

Named as defendants in all of the lawsuits are John Edmonds, a 36-year old former metals trader at J. P. Morgan, a group of yet-to-be-identified precious metals traders and the bank.

Edmonds, a New York resident, pleaded guilty in October to one count of conspiracy to defraud the market and manipulate prices of precious metals futures contracts and one count of commodities fraud. In the criminal plea, Edmonds admitted that he and other “unnamed co- conspirators” at J. P. Morgan, fraudulently manipulated precious metals markets from 2009 to 2015, the same time frame covered in the class action suits.

Briganti filed the initial class action on Nov. 7, just one day after the Justice Department unsealed Edmonds‘ plea in the U.S. District Court of Connecticut.

Edmonds admitted in his guilty plea that he deployed the illegal trading scheme hundreds of times with the direct knowledge and consent of his immediate supervisors. Plaintiffs say they have suffered economic injury, including monetary losses, as a direct result of actions by Edmonds and the other unnamed J. P. Morgan metals traders in the futures and options contracts.

One of the suits alleges that “the number of unlawful trades that JP Morgan traders executed in precious metals futures markets is at least in the thousands.”

J. P. Morgan declined to comment. Lowey Dannenberg did not respond to a request for comment by CNBC.

The Justice Department‘s criminal investigation is still ongoing and recently caused a separate related civil case to be put on hold for at least six months while the government continues its investigation. That civil lawsuit, which also accuses J. P. Morgan of rigging the precious metals market, was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders.

After reviewing the details of the plea agreement, David Kovel, the attorney for Shak‘s suit, sought to re- interview Edmonds, along with two other current and former senior traders at the bank. However, the government argued that reopening questioning would be detrimental to the ongoing criminal investigation. The federal judge overseeing the proceedings ordered a six-month stay in the civil case.

Kovel declined to comment.

Edmonds was originally scheduled to be sentenced in Hartford, Conn., on Wednesday, Dec. 19, but a court filing on Nov. 27 shows the sentencing has been postponed until June. A spokesman for the U.S. Attorney for Connecticut could not elaborate on why the sentencing was postponed since the court filing is under seal.

-END-

S&P Futures Jump To Five Month High, Dollar Spikes In Bullish Start To New Month

World stocks rose and US futures jumped to the highest level since late February even as U.S. lawmakers struggled to agree on the next round of coronavirus aid while Covid cases around the globe continued to rise, while a squeeze on crowded short positions left the dollar clinging to a tentative bounce.

S&P 500 futures turned higher, reversing earlier losses with Microsoft rising in pre-market trading as it tried to salvage a deal for the U.S. operations of TikTok. Marathon Petroleum jumped after agreeing to sell its gasoline-station business for $21 billion. Still, investors remained jittery amid the lack of a progress on the stimulus package and White House Chief of Staff Mark Meadows not optimistic about a deal.

“Three months to go until the U.S. Presidential election! Surely Congress will want to get something over the line regarding new stimulus in the U.S. driven more by politics than necessarily economics,” said Chris Bailey, European strategist at Raymond James.

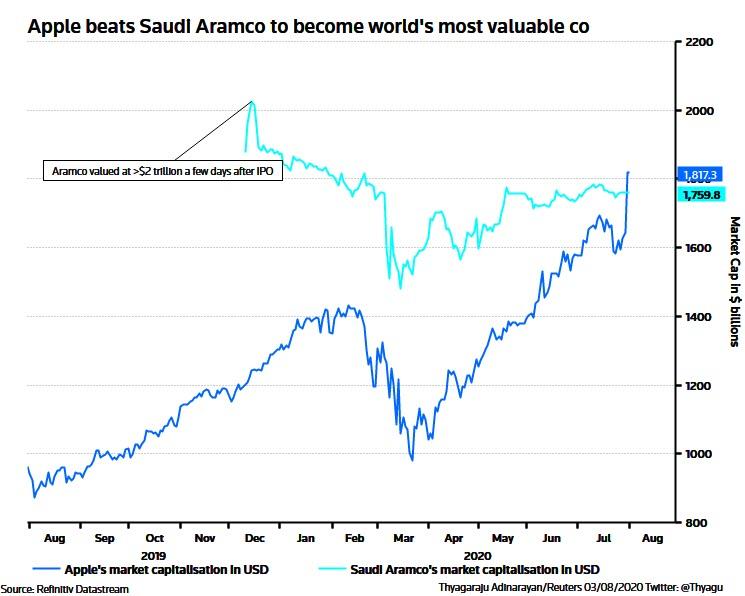

On Friday, Fitch Ratings cut the outlook on the United States’ triple-A credit rating to negative from stable and said the direction of fiscal policy depends in part on the November election and the resulting makeup of Congress, cautioning that policy gridlock could continue. However, as Reuters notes, those concerns have hardly hit the U.S. technology sector, evident in Friday’s record highs, with Apple overtaking Saudi Aramco to become the world’s most valuable company.

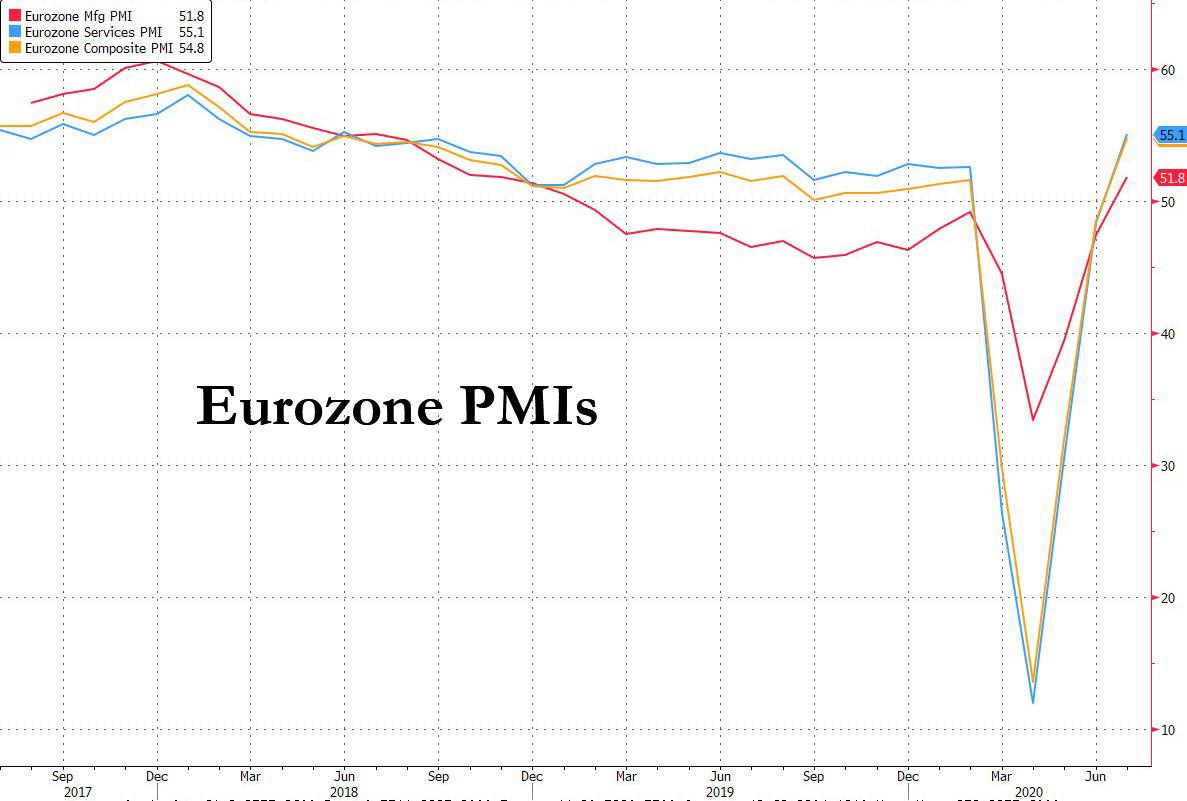

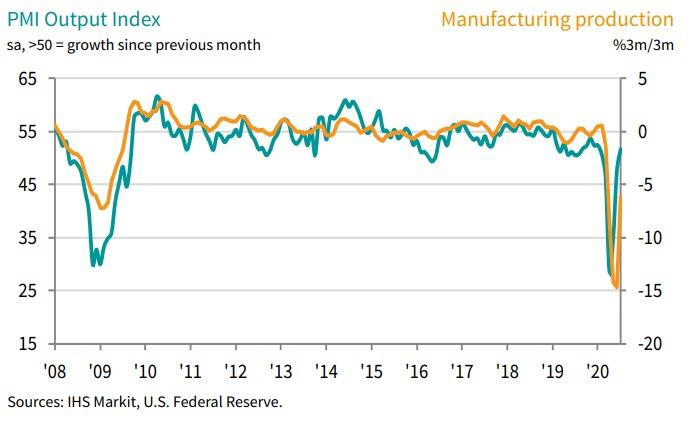

In Europe, stocks were up over 1% with all but four sector indexes advancing, with gains led by automakers, technology and chemicals sub- indexes, which are all up at least 1.7%. Travel and leisure stocks are the worst performers. Technology stocks rallied on positive read-across from peers on the other side of the Atlantic, while automobile shares jumped after the euro area recorded its first manufacturing expansion in one-and-a-half years when the final Eurozone mfg PMI printed at 51.8, above the 51.1 expected.

Spanish stocks, meanwhile, declined on Monday as the country saw the biggest jump in coronavirus cases since a national lockdown was lifted in June, while data showed international tourist arrivals to the country fell 98% year on year in June. “Second wave virus concerns are building in Australia, Europe etc. but no huge risk-aversion move,” said Bailey.

European gains were also limited by a selloff in big banks’ shares, with index heavyweight HSBC falling 5% to a fresh 11 year low after it warned that its bad debt charges could surge to as much as $13 billion, and France’s Societe Generale reported a 1.26 billion euro ($1.48 billion) second-quarter loss.

Earlier in the session, Asian stocks also gained, led by communications and health care, after falling in the last session. Most markets in the region were down, with Jakarta Composite dropping 2.8% and Singapore’s Straits Times Index falling 1.9%, while Japan’s Topix Index gained 1.8%. The Topix gained 1.8%, with ISB and ITmedia rising the most. The Shanghai Composite Index rose 1.8%, with Raytron Technology and Piesat Information Technology Co Ltd posting the biggest advances as investor margin debt resumed its climb.

Factory activity data from China showed the fastest pace of expansion in nearly a decade.

That helped China’s blue chips rally 1.6%, offsetting worries about U.S.-China relations. Japan’s Nikkei meanwhile added 2.2%, courtesy of a pullback in the yen.

“There is going to be a recovery — we shouldn’t lose track of that as we go through this period,” Anne Anderson, head of fixed income at UBS Asset Management Australia, said on Bloomberg TV. “But returning to where we were before we started is going to be a real challenge and is going to require ongoing monetary and fiscal support. It’s a long way out of here.”

Meanwhile, tension between the U.S. and China emerged as another threat to risk appetite. The Trump administration will announce measures shortly against “a broad array” of Chinese-owned software deemed to pose national-security risks, U.S. Secretary of State Michael Pompeo said. Even so, shares advanced in Japan and China, where mainland-listed technology stocks surged on expectations of support from Beijing in response to U.S. moves against Chinese-owned software companies.

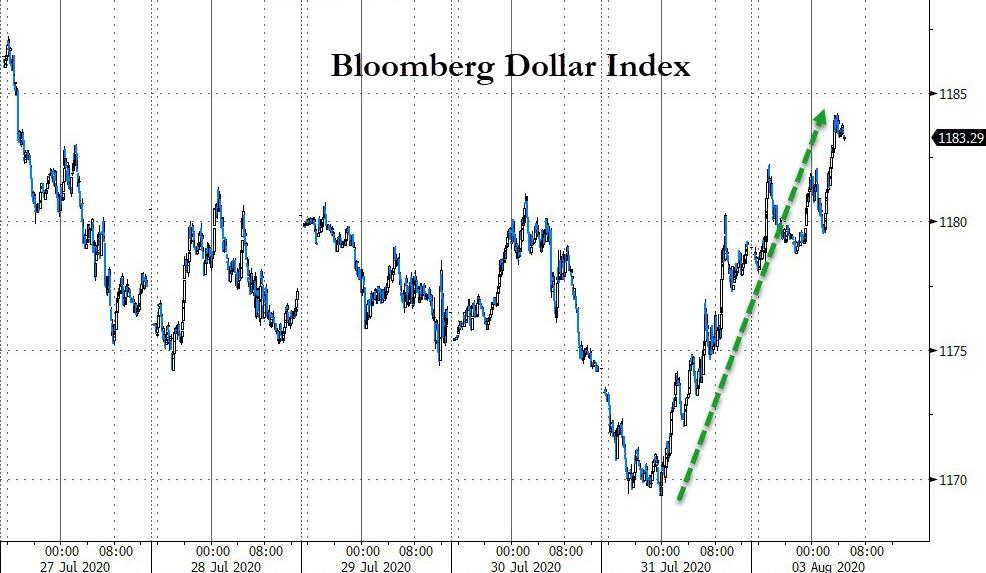

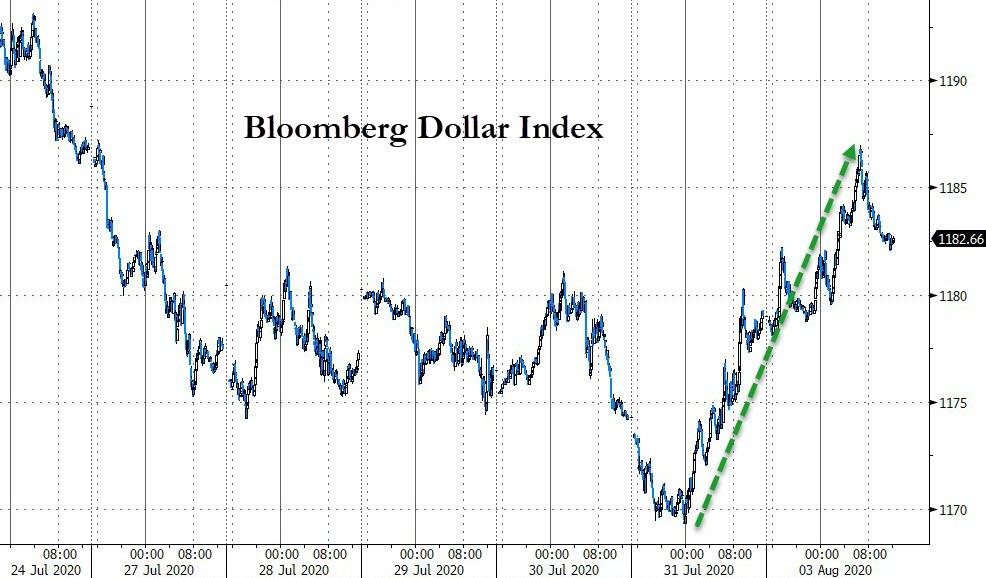

In FX, Dollar bears also took some profits as short positions hit an 11 year high, with the Bloomberg Dollar Spot Index heading for its biggest two-day gain in seven weeks, with the greenback rising against all Group-of-10 peers except the Swedish krona and the yen.

but any further gains were capped by the slowing U.S. economic recovery from COVID-19 and real rates breaking below -1% for the first time.

The real 10Y rate hit a record low amid a marked flattening of the yield curve as investors wager on more accommodation from the Federal Reserve.

The euro and the pound were down only slightly with the dollar at $1.1755 per euro and $1.3065 per pound. Both the currencies recorded their best monthly gain in nearly a decade in July.

“Amid improvements in business sentiment, signals are emerging that the initial boost from pent-up demand is fading and consumer confidence is slipping lower,” economists at Barclays wrote in a note. “Together with concerns about labour market and virus developments, this clouds the outlook and could be exacerbated if U.S. fiscal support is not renewed in time.”

In rates, 10-year Treasury yields were higher at 0.5576% after touching the lowest level since March last week. German government bond yields rose slightly to -0.527%. Treasuries bear steepened as month-end support came out of the market and investors looked ahead to Wednesday’s supply announcement where record sales of notes and bonds are expected. Yields higher by up to 3bp across long-end of the curve with front-end broadly anchored, steepening 2s10s, 5s30s by ~1.5bp each; 10-year yields around 0.545%, cheaper by 1.5bp vs. Friday close while bunds, gilts outperform by ~2bp each. Yields on 30-year U.S. Treasuries are set for the biggest daily increase since June 30 as U.S. equity futures advance and the bond curve bear-steepens. As Bloomberg adds, a busy week of IG corporate issuance also expected, adding to downside pressure on Treasuries along with delta hedging large option package.

The recent decline in the dollar combined with super-low real bond yields has been a boon for gold, which hit $1,984 an ounce on Monday and seemed on track to take out $2,000 soon.

In other commodities, oil prices eased on concerns about oversupply as OPEC and its allies are due to pull back from production cuts in August while an increase in COVID-19 cases raised fears of slower pick-up in fuel demand. Brent crude futures dipped 46 cents to $43.06 a barrel, while U.S. crude eased 51 cents to $39.76.

On today’s calendar, economic data include ISM and Markit manufacturing data. Ferrari is among today’s scheduled earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 3,260.50

- STOXX Europe 600 up 0.4% to 357.57

- MXAP up 0.3% to 165.11

- MXAPJ down 0.4% to 549.24

- Nikkei up 2.2% to 22,195.38

- Topix up 1.8% to 1,522.64

- Hang Seng Index down 0.6% to 24,458.13

- Shanghai Composite up 1.8% to 3,367.97

- Sensex down 1.7% to 36,967.20

- Australia S&P/ASX 200 down 0.03% to 5,926.09

- Kospi up 0.07% to 2,251.04

- Brent Futures down 0.6% to $43.24/bbl

- Gold spot down 0.2% to $1,972.89

- U.S. Dollar Index up 0.1% to 93.44

- German 10Y yield rose 0.4 bps to -0.52%

- Euro down 0.03% to $1.1775

- Brent Futures down 0.6% to $43.24/bbl

- Italian 10Y yield rose 4.2 bps to 0.887%

- Spanish 10Y yield rose 0.2 bps to 0.342%

Top Overnight News from Bloomberg

- Factories across the euro area saw a stronger return to growth in July than initially reported, marking the region’s first manufacturing expansion in one-and-a-half years while economies from Germany to Italy beat expectations. In the U.K., although numbers were slightly below flash estimates, manufacturing grew at the fastest pace in almost three years as the nation’s lockdown eased

- Gold’s spot and futures prices opened the week by hitting records, with the metal for immediate delivery closing in on $2,000 an ounce as the search for haven assets continues amid the coronavirus pandemic

- Microsoft chief executive Satya Nadella attempted to salvage a deal for the U.S. operations of TikTok by speaking with President Donald Trump by phone

- Oil edged below $40 a barrel in New York as OPEC and allied producers started to unwind output cuts even as many countries are still struggling to contain the virus

Asian equity markets began the new trading month mixed after last Friday’s positive close on Wall St where the tech sector rallied following earnings from the industry giants including Apple which rose to a fresh record high, but with upside in the region restricted ahead of this week’s risk events and after continued stalemate in US coronavirus relief discussions. ASX 200 (flat) was subdued as gains in commodity related sectors were offset by underperformance in the top weighted financials and with trade hampered by reduced liquidity due to bank holiday in New South Wales, while risk appetite was also weighed by a state of disaster declaration in Victoria with the state capital of Melbourne to be subjected to tougher restrictions including a curfew through to at least September 13th. Nikkei 225 (+2.2%) was the stellar performer as it coat-tailed on recent favourable currency flows and after Q1 Final GDP topped estimates, although there were some notable losses seen in Shinsei Bank and Mazda post earnings, as well as Seven & I on news it is to acquire Speedway convenience stores from Marathon Petroleum in a deal valued around USD 18.9bln. Hang Seng (-0.6%) and Shanghai Comp. (+1.8%) were mixed after PBoC inaction resulted to a CNY 100bln liquidity drain and as participants digested a more than 50% drop in HSBC HY profits, as well as the highest Chinese Caixin Manufacturing PMI reading since 2011. There was also plenty of focus around tech after reports that President Trump is to allow 45 days for ByteDance to negotiate the sale of TikTok to Microsoft and will reportedly take action on Chinese software companies that threaten national security in the approaching days. Finally, 10yr JGBs were lower amid a surge in Japanese stocks and with the BoJ present in the market for JPY 450bln of JGBs predominantly focused on 1yr-3yr maturities, while the central bank recently announced its buying intentions for August in which it maintained the current pace of purchases for all maturities.

Top Asian News

- Why Investors Keep Losing Money Betting Against the Hong Kong Dollar Peg

- Goldman, BofA Left Off Ant IPO for Work With Alibaba Rivals

- SoftBank, Naver to Start Joint Tender Offer for Line on Aug. 4

Mixed trade in the European equity sphere (Euro Stoxx 50 +0.6%) after a similar lead from APAC markets, as participants remain on standby for this week’s key risk events – including US ISM and labour market report alongside any updates on fiscal stimulus talks. Core EU bourses saw some upside in the run-up to the Final Manufacturing PMIs, potentially on optimism for higher revisions, but indices have since remained contained. UK’s FTSE 100 lags the core markets on currency dynamics, and with the Financial sector hit on the back of dismal earnings from HSBC (-5.1%) where Q2 profit slumped and loan loss provisions rose almost seven-fold. Furthermore, SocGen (-3.1%) adds to the woes in the sector after posting a surprise loss due to pandemic impact on equity trading. Energy names have also lost steam amid price action in the complex, but overall European sectors remain mixed with no clear risk tone to be derived. The sectoral breakdown sees Travel and Leisure at the bottom as second wave fears materialise in the sector. Elsewhere of note, AI company Shanghai Zhizhen Network Technology is suing Apple for around USD 1.4bln over virtual assistant patent violations, WSJ reported.

Top European News

- U.K. Manufacturing Grows as Sector Starts Long Road to Recovery

- Euro-Area Factories Returned to Growth Amid Severe Jobs Cuts

- Real Estate Stocks Fall on Lockdown Concerns, Negative Sentiment

In FX, mixed macro impulses for the Franc as Swiss CPI was considerably firmer than forecast, but the manufacturing PMI fell short of expectations and the key 50.0 mark to leave Usd/Chf eyeing 0.9200 and Eur/Chf even closer to 1.0800 following yet another rise in weekly bank sight deposits. Moreover, the cross has rebounded amidst Eurozone manufacturing PMIs that beat consensus and underpinned EU stocks alongside economic recovery hopes. Conversely, the COVID-19 escalation in Melbourne, Victoria has prompted a state of disaster amidst tougher restrictions and a curfew in the capital until September 13, at the earliest, on the eve of the RBA policy meeting – full preview of the event available on the headline feed – to the detriment of the Aussie that is holding just above 0.7100 vs the Greenback compared to last Friday’s 0.7200+ new ytd peak.

- USD – The Dollar has handed back some of its pre-month end gains after the DXY rebounded further from fresh 2020 lows (92.546) to 93.708 and is now pivoting 93.500, with additional support coming via M&A flows due to deals amounting to Usd 16.4 bn and Usd 21 bn for US companies from German and Japanese rivals respectively. Ahead, the final Markit manufacturing PMI, ISM equivalent and construction spending before a duo of Fed speakers (Bullard and Evans).

- JPY/GBP/NZD – All intiailly firmer against the Buck, or off worst levels to be more precise, as the Yen regains composure following its aggressive reversal from the low 104.00 area to 106.40+, while Sterling revisited 1.3100 from not far off 1.3050 even though the final UK manufacturing PMI was revised down a tad and the coronavirus outbreak in Northern England has reached ‘major incident’ proportions in Greater Manchester. Elsewhere, the Kiwi is benefiting from the aforementioned Aussie travails to an extent given Aud/Nzd pulling back below 1.0750 to keep Nzd/Usd more buoyant on the 0.6600 handle despite reports that hedge funds are implementing bearish positions ahead of the RNBZ later in August.

- EUR/CAD/SEK/NOK – Some traction for the Euro within 1.1796-42 parameters vs the Greenback in wake of the better than prelim/anticipated Eurozone manufacturing PMIs, but no confirmed breach of resistance in the form of the 100 HMA (1.1779), while the Loonie is sub-1.3400 amidst another downturn in crude prices that is also hampering the Norwegian Krona relative to its Swedish counterpart after the manufacturing PMI reclaimed 50.0+ status and retail sales picked up pace. Indeed, Eur/Nok is hovering around 10.7500 in contrast to Eur/Sek testing 10.3100 vs highs of 10.7860 and 10.3515 respectively.

- EM – The Yuan is keeping its head above 7.0000 on the back of China’s Caixin manufacturing PMI exceeding forecast at 52.8 for the strongest print since January 2011 and the Rouble is consolidating off recent lows circa 74.0000 awaiting the latest CBR MPR, but the Rand is lagging near 17.3000 after a steep decline in SA tax receipts for the fy through end July.

In commodities, WTI and Brent front-month futures remain subdued in early European trade with little by way of fresh fundamental catalysts, but with that being said, OPEC+ are poised to ease the magnitude of the agreed-upon cuts this month which will see an additional 1.9mln BPD of supply entering the market – this was reflected by the Russian oil and gas condensate output for the first half of August. It is also worth bearing in mind that the extra supply comes against the backdrop of rising second-wave fears which have prompted some cities to re-enter lockdown, whilst others deferred their reopening plans. Elsewhere, spot gold remains uneventful after testing support at USD 1970/oz (vs. fresh high 1987.94), with the yellow metal decoupled from Dollar dynamics (for now) as prices remain near record highs. Spot silver sees similar lacklustre action sub 24.50/oz. Turning to base metals, Dalian iron ore futures rose in excess of 4% to hit 12-month highs on a firm demand outlook. Conversely, copper touched a three-week low despite the strong Chinese factory data, with some citing second wave fears.

US Event Calendar

- 9:45am: Markit US Manufacturing PMI, est. 51.3, prior 51.3

- 10am: ISM Manufacturing, est. 53.5, prior 52.6

- 10am: Construction Spending MoM, est. 1.0%, prior -2.1%

- Wards Total Vehicle Sales, est. 14m, prior 13.1m

DB’s Jim Reid concludes the overnight wrap

A happy August to you all. This morning’s EMR is brought to you by the powers of paracetamol and ibuprofen as I played my one and only game of cricket this season over the weekend. It was President’s Day and I’m the President of my club so I couldn’t really avoid coming out of semi-retirement for a game I played pretty much every summer weekend from around 1983 to 2011. Running, diving, throwing, bowling, eating a big tea all took a big toll out of me.

My performance certainly wasn’t as good as markets were in July, unless the dollar was my benchmark. Craig (who is still in a state of shock after Arsenal won the FA Cup final on Saturday) has already published July’s performance review this morning (link here) where the highlights were a bumper month for Silver and Gold and a poor month for the dollar. Silver (c.+35%) had its best month since December 1979 and the dollar the worse for a decade. US equities had a good month in spite of rising virus caseloads due to a strong earnings season relative to expectations, especially in tech towards the end of the month. YTD Silver, Gold and the NASDAQ have been the three best performers while at the bottom of the leaderboard Brent, WTI and European Banks are all down at least 30%.

In terms of how August is faring so far, it’s been a mixed start in Asia with the Nikkei (+1.95%) and Shanghai Comp (+1.08%) both posting decent gains, the Hang Seng (-0.95%) down and the Kospi and ASX little changed. Meanwhile, yields on 10yr USTs are up +1.3bps and futures on the S&P 500 are down -0.08%. In terms of data releases, China’s June Caixin manufacturing PMI came in at 52.8 (vs. 51.1 expected) which was the highest reading since Jan 2011 while Japan’s final manufacturing PMI reading was confirmed at 45.2 (vs. 42.6 in preliminary read). We also got Japan’s final annualized 1Q GDP print this morning, printing at -2.2% qoq (vs. -2.8% qoq expected).

In terms of weekend news, US Secretary of State Michael Pompeo has said that the White House will announce measures against “a broad array” of Chinese-owned software deemed to pose national-security risks. This follows President Trump saying on Friday that he intends to ban music-video app TikTok from the US. Meanwhile, on the fiscal stimulus negotiations in the US, there are reports that Democrats and Republicans continue to remain far apart on the plan to restore a $600-per-week jobless benefit that expired last week. Negotiations will continue today.

Looking at coronavirus numbers for the weekend, growth rates for new cases slowed in the US to an average of 1.13% per day (vs. average growth of 1.70% over last 5 weekends). The same was true for the most populous states like Texas, Florida, California and Arizona. The fatalities growth rate also slowed in Texas (1.35% vs. 1.89%) and Arizona (0.96% vs. 2.45%) but continues to remain high in Florida (1.75% vs. 1.34%) and California (1.13% vs. 0.73%). Meanwhile, the White House coronavirus task force head Deborah Birx said the pandemic is in a “new phase” as it spreads across U.S. rural and urban areas. In Asia, Australia’s Victoria state declared a state of disaster and has ordered Melbourne’s residents to stay home except for work, medical care, provisions or exercise. The city is now under curfew between 8 p.m. and 5 a.m and the new restrictions will be in force for six weeks. The state reported 671 new cases in the past 24 hours. Please see the regular case and fatalities table in the PDF for more. Finally, the latest on a possible vaccine is that the Serum Institute of India received approval for conducting phase two and three clinical trials of the Covid-19 vaccine candidate developed by the University of Oxford and AstraZeneca in the country.

Looking ahead to this week now, the release of PMIs from around the world (today and Wednesday mostly) will set the tone, before the July US jobs report on Friday rounds out the week. On the central bank front, we will hear the monetary policy decision from the Bank of England and Governor Bailey’s ensuing press conference on Thursday. The market also enters the second half of Q2 earnings season, which has already seen a record number of beats in the S&P 500.

Going through in more detail now, the majority of manufacturing PMIs are out on today, before services and composite PMIs come out on Wednesday for the most part. There’ll also be the ISM manufacturing index from the US (today). The key here will be to see how differentiated PMIs are given that some governments around the world are cautiously easing restrictions with others needing to tighten. For the countries where we already have a flash PMI reading, they generally showed that the recovery has more momentum in Europe than in the US. Many of the flash European levels were the strongest in at least two years, while both manufacturing and services PMIs in the US failed to meet expectations. As ever caution is required as these are diffusion indices which simply monitor whether activity is better or worse than the previous month. Remember that the US was never as shutdown as Europe so momentum was always likely to be more in the latter’s favour regardless of the recent rise in cases.

In terms of payrolls on Friday, markets are generally expecting a third straight month of gains, though likely at a slower rate than we saw in June. DB are looking for a further +900k gain in the headline, below consensus estimates at +1.578m. This follows last month’s blowout +4.8m increase. Our economists also see the unemployment rate falling to 10.5% from 11.1%, in line with the median estimate. This data will give some insight into how the renewed spread of the coronavirus through the US, especially in the South and West have affected the US economy. The rest of the key data can be found in the day by day week ahead guide at the end.

On the central bank front, one highlight will be the Bank of England meeting and Governor Bailey’s ensuing press conference on Thursday. While our DB economists are not expecting any change to the policy rate this meeting, there is a chance for a dovish surprise on the overall commentary and tone. Focus will be on the central bank’s economic projections, the ongoing review of the effective lower bound, and the path of QE. See their preview here .

Elsewhere in central banks, India and Brazil are also releasing their policy decisions on Wednesday and Thursday, respectively. The two countries have the highest confirmed coronavirus caseloads outside the US, and are expected to lower interest rates in light of the continued economic impact of the pandemic. Following the FOMC last week and the lifting of the blackout period, we will hear from the Fed’s Bullard, Evans, Mester and Kaplan.

Earnings will continue to be in focus, with 133 companies reporting from the S&P 500 and a further 95 from the STOXX 600. Among the releases include HSBC, Heineken, Siemens, Berkshire Hathaway, and Ferrari today. Then tomorrow markets will hear from Bayer, Diageo, Fidelity, BP, Walt Disney and Activision Blizzard. Wednesday will see Deutsche Post, Allianz, Humana, Bayerische Motoren, Regeneron Pharmaceuticals, CVS Health, MetLife and Fiserv release earnings. Following that, Thursday includes Merck, AXA, Siemens, adidas, Bristol-Myers Squibb, Novo Nordisk, Becton Dickinson & Co, Zoetis, T-Mobile, Illumina. Finally on Friday, Standard Life Aberdeen, Norwegian Cruise Line, Royal Caribbean Cruises and Ventas. So another busy week.

To review last week now, global equity markets were bifurcated with US stocks outperforming after beating low earning expectations, particularly in tech. The S&P 500 rose +1.73% (+0.77% Friday) led primarily by the mega cap tech stocks which reported towards the end of last week. With Apple, Facebook, and Amazon in particular surprising on earnings, the tech-focused Nasdaq outperformed this week as the index rose +3.69% (+1.49% Friday). Over 60% of the S&P have now reported and the index has seen a record of just under 85% of companies beat EPS estimates. Remember that the issue with this earnings season was that analysts didn’t increase their estimates in June as macro surprises beat. This left a great set up for earnings versus expectations.

Risk assets in Europe did not fare as well with European equities down -2.98% (-0.89%) over the 5 days, pushing the index down -1.11% for July. It was the first monthly loss since March as cyclical sectors led the declines following more concerns on the economic outlook and small rises in cases across the continent.