JAN 14/2022/

January 13, 2022 · by harveyorgan · in Uncategorized · Leave a comment ·Edit

GOLD; DOWN $5.05 to $1815.85

SILVER: $22.92 DOWN 21 CENTS

ACCESS MARKET: GOLD: 1817.55..

SILVER: $22.92

Bitcoin: morning price: 42,022 up 22

Bitcoin: afternoon price: 42,041 up 41

Platinum price: closing down $1.25 to $972.90

Palladium price; closing down $12.40 at $1880,55

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices//JPMorgan notices filed COMEX//NOTICES FILED 0/2

EXCHANGE: COMEX

CONTRACT: JANUARY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,821.200000000 USD

INTENT DATE: 01/13/2022 DELIVERY DATE: 01/18/2022

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 2

685 C RJ OBRIEN 1

905 C ADM 1

TOTAL: 2 2

MONTH TO DATE: 3,921

NUMBER OF NOTICES FILED TODAY FOR JAN. CONTRACT: 2 NOTICE(S) FOR 200 OZ (0.00622 TONNES)

total notices so far: 3921 contracts for 392,100 oz (12.195 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month 2336 : for 11,680,000 oz

GLD

WITH GOLD DOWN $5.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS): NO CHANGES IN GOLD INVENTORY AT THE GLD

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

CLOSING INVENTORY: 976.21 TONNES/

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 21 CENTS:/:

NO CHANGES IN SILVER INVENTORY:

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY SLV/ TONIGHT: 529.780 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG 732 CONTRACTS TO 146,876 AND RESTS CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020…... WITH THE $0.02 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.02) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 1232 CONTRACTS ON OUR TWO EXCHANGES .

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 10.505 MILLION OZ FOLLOWED BY TODAY’S NIL OZ QUEUE. JUMP V) STRONG SIZED COMEX OI GAIN.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS -19

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN:

TOTAL CONTACTS for 10 days, total contracts: : 5864 contracts or 29.320 million oz OR 2.932 MILLION OZ PER DAY. (586 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 5864 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 29.320 MILLION OZ

.

LAST 8 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 732 WITH OUR 2 CENT LOSS SILVER PRICING AT THE COMEX// THURSDAY THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 500 CONTRACTS( 500 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY:/ AS WELL AS TODAY /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JAN OF 10.505 MILLION OZ FOLLOWED BY TODAY’S NIL QUEUE JUMP //NEW STANDING 13.615, MILLION OZ// .. WE HAD A HUGE SIZED GAIN OF 1232 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.160 MILLION OZ//

WE HAD 0 NOTICES FILED TODAY FOR nil OZ

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GIGANTIC 15,240 TO 531,871, AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -3110 CONTRACTS

.

THE HUGE SIZED DECREASE IN COMEX OI CAME DESPITE OUR SMALL LOSS IN PRICE OF $5.75//COMEX GOLD TRADING/THURSDAY/.AS IN SILVER WE MUST HAVE HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION AS THE TOTAL LOSS ON OUR TWO EXCHANGES TOTALLED A STRONG SIZED 10,570 CONTRACTS…

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 3.5614 TONNES FOLLOWED BY TODAY’S STRONG 7300 OZ QUEUE. JUMP//NEW STANDING: 12.416 TONNES

YET ALL OF..THIS HAPPENED WITH OUR SMAL LOSS IN PRICE OF $5.75 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A HUGE SIZED LOSS OF 14,130 OI CONTRACTS (43.95 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALLED A SMALL SIZED 1110 CONTRACTS:

FOR FEB 1110 ALL OTHER MONTHS ZERO//TOTAL: 1110

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 531,871.

IN ESSENCE WE HAVE A GIGANTIC SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,240, WITH 15,240 CONTRACTS DECREASED AT THE COMEX AND 1110 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,570 CONTRACTS OR 32.877TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1110) ACCOMPANYING THE GIGANTIC SIZED LOSS IN COMEX OI (15,240): TOTAL LOSS IN THE TWO EXCHANGES 14,130 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR JAN. AT 3.7262 TONNES//FOLLOWED BY TODAY’S 7300 OZ QUEUE. JUMP.//NEW STANDING 12.416 TONNES 3)ZERO LONG LIQUIDATION,4) GIGANTIC SIZED COMEX OI. LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JAN HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2021 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN : 25,334 CONTRACTS OR 2,533,400 oz OR 78.80 TONNES (10 TRADING DAY(S) AND THUS AVERAGING: 2533 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 78.80 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 78.80/3550 x 100% TONNES 2.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO DATE

JANUARY: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 145.12 TONNES//INITIAL ISSUANCE//

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 732 CONTRACTS TO 146,876 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 500 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 736 CONTRACTS AND ADD TO THE 500 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 1232 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.160 MILLION OZ,

OCCURRED WITH OUR $0.02 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED DOWN 34.00 PTS OR 0.96% //Hang Sang CLOSED DOWN 46.45 PTS OR 0.19% /The Nikkei closed DOWN 364,85 PTS OR 1.28% //Australia’s all ordinaires CLOSED DOWN 1.03% /Chinese yuan (ONSHORE) closed UP 6.3531 /Oil UP TO 82.53 dollars per barrel for WTI and UP TO 84.98 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3531. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3591: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

A)NORTH KOREA//USA/OUTLINE

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 15,240 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS HUGE COMEX DECREASE OCCURRED WITH OUR SMALL LOSS OF $5.75 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A SMALL EFP (1110 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. LOOKS LIKE OUR BANKERS ARE FINALLY BAILING OUT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF JAN.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 110 EFP CONTRACTS WERE ISSUED: ;: , DEC : 0 & FEB. 1110 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1110 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED 10,570 TOTAL CONTRACTS IN THAT 1110 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED COMEX OI LOSS OF 15,240 CONTRACTS..

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR JAN (12.416),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $5.75)

AND THEY WERE SUCCESSFUL IN FLEECING SOME LONGS AS THE TOTAL LOSS ON THE TWO EXCHANGES REGISTERED 43,95 TONNES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JAN (12.416 TONNES)…

WE HAD – 3110 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 14,130 CONTRACTS OR 1,413,000 OZ OR 43.95 TONNES

Estimated gold volume today: 180,467 poor///

Confirmed volume yesterday: 316,909 contracts fair

INITIAL STANDINGS FOR JAN ’22 COMEX GOLD

JAN 14

COMEX GOLD

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 96.45 ozBrinks 3 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 2 notice(s)200 OZ0.00622 TONNES |

| No of oz to be served (notices) | 71 contracts 7100 oz 0.2208 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3921 notices 3,92,100 OZ12.195 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

No dealer deposit 0

No dealer withdrawal 0

0 customer deposit

1 customer withdrawals

i) Out of Brinks: 96.45 oz (3 kilobars)

ADJUSTMENTS: 2 Dealer to customer

i) Delaware 7519.177 oz

ii) Malca 20,737.395 oz( 645 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JANUARY.

For the front month of JANUARY we have an oi of 73 stand for JANUARY LOSING 1520 contracts. We had 1593 notices filed on THURSDAY, so we GAINED 73 contracts or an additional 7300 oz will stand for

gold in this very non active delivery month of January. The resulting queue jump equates to 0.2270 tonnes,

FEBRUARY LOST 37,601 CONTRACTS TO 241,437

March GAINED 23 contracts to stand at 2322..

We had 2 notice(s) filed today for 200 oz FOR THE JAN 2022 CONTRACT MONTH

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 12 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JAN /2021. contract month,

we take the total number of notices filed so far for the month (3921) x 100 oz , to which we add the difference between the open interest for the front month of (JAN: 73 CONTRACTS ) minus the number of notices served upon today 2 x 100 oz per contract equals 399,200 OZ OR 12.416 TONNES the number of TONNES standing in this NON active month of JAN. (numbers corrected from yesterday)

thus the INITIAL standings for gold for the JAN contract month:

No of notices filed so far (3921) x 100 oz+ (73) OI for the front month minus the number of notices served upon today (2} x 100 oz} which equals 399,200 oz standing OR 12,416 TONNES in this NON active delivery month of JAN.

We GAINED 73 contracts or an additional 7300 oz of gold will stand for metal on this side of the pond.

TOTAL COMEX GOLD STANDING: 12.416 TONNES (HUGE FOR A JANUARY DELIVERY MONTH

IF THIS HOLDS TO THE END OF THE MONTH, THIS WILL BE THE HIGHEST EVER RECORDED GOLD STANDING FOR A JANUARY, GENERALLY A VERY POOR DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

206,468.649, oz NOW PLEDGED /HSBC 6.42 TONNES

174,041.813 PLEDGED MANFRA 5.41 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690

288,481,604, oz JPM No 2 8.97 TONNES

698,821.330 oz pledged June 12/2020 Brinks/27,96 TONNES

12,244.444 oz International Delaware: 0..3808 tonne

Loomis: 18,615.429 oz

total pledged gold: 1,653,017.372oz 51.42 tonnes

TOTAL REGISTERED AND ELIZ GOLD AT THE COMEX: 33,617,146.897 OZ (1045.63 TONNES)

TOTAL ELIGIBLE GOLD: 16,036,509.928 OZ (498.80 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,580,633.969 OZ (546.83 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,927,616.0 OZ (REG GOLD- PLEDGED GOLD) 495.41 tonnes

END

JANUARY 2022 CONTRACT MONTH//SILVER

INITIAL STANDING FOR SILVER//JAN 14

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 677,776.054 oz BrinksCNTJPM |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 579,003.800 ozJPMorgan |

| No of oz served today (contracts) | 0 CONTRACT(S)nil OZ) |

| No of oz to be served (notices) | 387 contracts (1,935,000 oz) |

| Total monthly oz silver served (contracts) | 2336 contracts 11,680,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We had 1 deposits

i)Into JPMorgan: 579,003.800 oz

total: 579,003.800 oz

JPMorgan has a total silver weight: 184.922 million oz/353.279 million =52.33% of comex

ii) Comex withdrawals: 3

a) out of Brinks: 6763.94 oz

b) Out of JPMorgan: 593,878.164 oz

c) Out of CNT 77133.950 oz

total withdrawal 885,722.405 oz

we had 0 adjustment

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.331 MILLION OZ

TOTAL REG + ELIG. 353.068 MILLION OZ

TOTAL NO OF CONTRACTS SERVED UPON THIS MONTH: 1980 CONTRACTS FOR 45,095,000 OZ

CALCULATION OF SILVER OZ STANDING FOR DECEMBER

NUMBER OF NOTICES FILED TODAY: 185 NOTICES OR 925,000 OZ

silver open interest data:

FRONT MONTH OF JAN//2022 OI: 387 CONTRACTS LOSING 0 contracts on the day

We had 0 notices filed for THURSDAY so we GAINED 0 contracts or NIL additional oz will stand for delivery in this non active delivery month of January.

FOR FEB WE HAD A LOSS OF 9 CONTRACTS DOWN TO 702

FOR MARCH WE HAD A LOSS OF 585 CONTRACTS UP TO 113,911 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 48,681poor// est. volume today

Comex volume: confirmed YESTERDAY: 59,095 contracts (poor)

To calculate the number of silver ounces that will stand for delivery in JANUARY. we take the total number of notices filed for the month so far at 2336 x 5,000 oz =. 11,680,000 oz

to which we add the difference between the open interest for the front month of JAN (387) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JAN./2021 contract month: 2336 (notices served so far) x 5000 oz + OI for front month of JAN (387) – number of notices served upon today (0) x 5000 oz of silver standing for the JAN contract month equates 13,615,000 oz. .

We GAINED 0 contracts or an additional NIL oz will stand for delivery on this side of the pond.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

GLD

JAN 14/ WITH GOLD DOWN $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 13/WITH GOLD DOWN $5.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 12/WITH GOLD UP $8.65//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 976.21 TONNES

JAN 11/WITH GOLD UP $19.25/A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FROM THE GLD/INVENTORY RESTS AT 976.21 TONNES

JAN 10/WITH GOLD UP $2.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.08 TONNES

JAN 7/WITH GOLD UP $8.15//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWLA OF 1.16 TONNES FROM THE GLD////INVENTORY RESTS AT 978.83 TONNES

JAN 6/WITH GOLD DOWN $35.30//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .32 TONNES/INVENTORY RESTS AT 979.99 TONNES

JAN 5/WITH GOLD UP $10.30: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 980.31 TONNES

Jan 4/WITH GOLD UP $14.00//A HUGE CHANGE OF 4.65 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 980.31 TONNES

JAN 3/WITH GOLD DOWN $26.70: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 31/WITH GOLD UP $14.05 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 30/WITH GOLD UP $7.75 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 975.66 TONNES

DEC 29/WITH GOLD DOWN $5.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 975.66 TONNES

DEC 28/WITH GOLD UP $2.00 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 973.63 TONNES

DEC 27/WITH GOLD DOWN $2.05: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 973.63 TONNES.

DEC 23/WITH GOLD UP $9.85 TODAY//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.94 TONNES FROM THE GLD/// INVENTORY RESTS AT 973.63 TONNES

DEC 22/WITH GOLD UP $12.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 21/WITH GOLD DOWN $7.05 TODAY, NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 978.57 TONNES

DEC 20/WITH GOLD DOWN $9.65 TODAY; A BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.37 TONNES INTO THE GLD///INVENTORY RESTS AT 977.20 TONNES

DEC 17/WITH GOLD UP $7.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 977.20 TONNES

DEC 16/WITH GOLD UP $33.05TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.4 TONNES FROM THE GLD////INVENTORY REST AT: 977.20 TONNES

DEC15/WITH GOLD DOWN $7.80 TODAY/ A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.04 TONNES FROM THE GLD////INVENTORY RESTS AT 980.60 TONNES.

DEC 14/WITH GOLD DOWN $18.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 13/WITH GOLD UP $3.20 TODAY/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 982.64 TONNES

DEC 10.WITH GOLD UP $7.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64 TONNES

DEC 9/WITH GOLD DOWN $9.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 982.64.

DEC 8/WITH GOLD UP $5.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 984.38 TONNES

DEC 7/WITH GOLD UP $5.15 TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 984.38 TONNES

DEC 6/WITH GOLD DOWN $3.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 986.17 TONNES//

CLOSING INVENTORY: 976.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SLV.

JAN 14/WITH SILVER DOWN 21 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 529.780 MILLION OZ//

JAN 13/WITH SILVER DOWN 2 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 832,000 OZ FROM THE SLV////INVENTORY RESTS AT 529.780 MILLION OZ

JAN 12/WITH SILVER UP 38 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//

JAN 11/WITH SILVER UP 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ/.

JAN 10/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 7/WITH SILVER UP 17 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.612 MILLION OZ//.

JAN 6/WITH SILVER DOWN 94 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL PF 226,000 OZ FROM THE SLV///INVENTORY RESTS AT 530.612 MILLION OZ?/

JAN 5/WITH SILVER UP 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 4/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 530.838 MILLION OZ//

JAN 3/WITH SILVER DOWN 45 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.219 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 530.838 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 31/WITH SILVER UP 29 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC30/WITH SILVER UP 14 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A HUGE WITHDRAWAL OF 4.624 MILLILON OZ FROM THE SLV.//INVENTORY RESTS AT 533.057 MILLION OZ//

DEC 29/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ/

DEC 28/WITH SILVER UP 9 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.682 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 27/WITH SILVER UP 6 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 537.681

DEC 23/WITH SILVER UP 19 CENTS TODAY:A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 537.681 MILLION OZ//

DEC 22/WITH SILVER UP 29 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.202 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 538.883 MILLION OZ/

DEC 21/WITH SILVER UP 19 CENTS: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.728 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 540.085 MILLION OZ

DEC 20/WITH SILVER DOWN 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 538.282 MILLION OZ

DEC 17/WITH SILVER UP 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 538.282 MILLION OZ//

DEC 16/WITH SILVER UP 91 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 3.33 MILLION OZ FROM THE SLV//INVENTORY REST AT 538.282 MILLION OZ

DEC 15WITH SILVER DOWN 38 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.48 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 541.612 MILLION OZ

DEC 14/WITH SILVER DOWN 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ

DEC 13/WITH SILVER UP 11 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.561 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 543.092 MILLION OZ//

DEC 10.WITH SILVER UP 19 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.653 MILLION OZ..

DEC 9/WITH SILVER DOWN 43 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 2.96 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 546.653 MILLION OZ/

DEC 8/WITH SILVER DOWN 7 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ///

DEC 7/WITH SILVER UP 24 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 543.693 MILLION OZ..

DEC 6/WITH SILVER DOWN 25 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.110 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 543.693 MILLION OZ//

CLOSING INVENTORY: 529.780 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

All Aboard The Inflation Freight-Train, Schiff Says Fed Doing “Too Little, Too Late”

FRIDAY, JAN 14, 2022 – 09:30 AM

December Consumer Price Index data came out on Wednesday (Jan. 12). Month-on-month, it was again even hotter than expected. Peter called it an inflationary freight train that the Fed’s “field of dreams” monetary policy will not stop.

“Transitory” inflation has now been running hot for a full year.

The year-on-year CPI was 7%. It was the biggest annual CPI increase since 1982.

Month-on-month, the CPI spiked another 0.5%. This was hotter than the consensus 0.4% projection.

Core CPI (stripping out food and energy — as if you don’t have to eat or put gas in your car) was up 5.5%.

Goods prices were up a staggering 10.7% That was the biggest 1-year increase since 1975.

Keep in mind, this is using the cooked government CPI formula that understates inflation. If the government was still using the formula that it used in 1982, inflation would be higher in 2021 than it was then. In fact, we’d have the highest level of inflation in history. According to ShadowStats, it would be just over 15%.

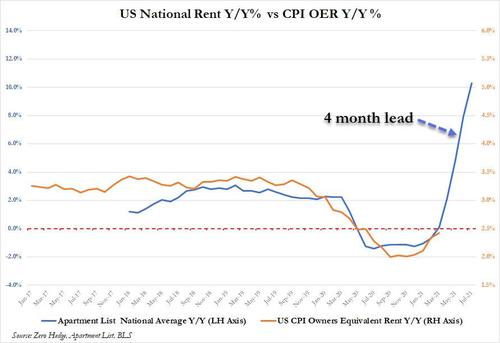

Based on the methodology the government uses to calculate housing prices (owners’ equivalent rent), housing prices were up 3.8% in 2021. Meanwhile, the actual home prices rose about 16.5%. If you take owners’ equivalent rent out and put home prices in the calculation, 2021 CPI suddenly becomes 10%.

Some people have recently claimed we shouldn’t worry about inflation. They say that wages go up along with prices, so it’s basically a wash. But wages are not going up as fast as prices. Real wages (nominal wage increases minus CPI) were down 2.4% in 2021. That means even with your raise, you have lost purchasing power. And you’ve lost even more than the official numbers reveal. If you use an honest inflation measure, real wages were down somewhere in the neighborhood of 10.4%.

As Peter Schiff said, “Consumers are going to have to live in the real world, not in the government’s fantasy world.”

Over the last year, the dollar has gone up and gold has dropped on hot CPI data. Instead of looking at inflation, they were focused on the possibility of Fed rate hikes. But on Wednesday, the dollar got clobbered and gold held steady with modest gains. Peter said he thinks this shows investors are starting to figure out that it doesn’t matter if the Fed hikes rates.

Any rate hikes that we get are going to be too little too late to do anything to derail this inflationary freight train.”

There has been a misperception in the markets over the last year. People have focused on nominal interest rates and ignored real interest rates. In fact, real rates are historically negative.

The real interest rate is -7% using the government CPI number. The Federal Reserve is only talking about slowly raising rates to 2% over the next two years. If inflation remains constant, real rates would still be -5% after two years of hiking.

That is not a positive environment for the US dollar and investors are starting to realize that and they are dumping dollars.”

And while there wasn’t a rush into gold, at least investors didn’t dump it.

Meanwhile, if you thought the Fed was about to embark on a successful war on inflation, Jerome Powell’s Senate testimony should have cleared up any confusion.

Powell admitted that even when the Fed raises rates and ends quantitative easing, monetary policy will still be “accommodative.” Peter questioned that policy.

If we have an inflation problem; if inflation is at 7%; why are we accommodating with easy money? If the Fed really wants to fight inflation, you can’t fight inflation with an accommodative policy. That’s the type of policy you have when there is no inflation. When you’re trying to simulate a weak economy, that’s when you do loose monetary policy.”

Powell is talking out of both sides of his mouth. He’s saying he’s going to fight inflation and continue stimulating the economy. You can’t do both.

You can’t put out a fire with gasoline. But that is what Powell is bluffing that he is going to do.”

Powell is still insisting that “supply chain problems” will resolve in 2022 and lower some of the inflationary pressure.

In other words, even though the Fed, or Powell, has claimed that they were wrong about inflation being transitory, they’re basically still clinging to that lie. Because they’re just saying that the transition is going to take longer than we thought because they think the inflation problem is going to take care of itself.”

Peter called it a “field of dreams” monetary policy.

The Fed is living in this fantasy land and they just think, ‘If we print it, the supply will come.’ They think we can keep on with our easy-money supply, but just eventually, the goods are going to be there. As long as people want to buy stuff, eventually, the stuff for them to buy is somehow going to magically appear. It doesn’t work that way. Stuff has to be produced before it’s consumed.”

In this podcast, Peter also talks about Elizabeth Warren trying to blame inflation on price gouging, makes the case that Democrats are laying the foundation for price controls, and discusses Paul Tudor Jones’s bitcoin forecast.

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,James RICKARDS

3.Chris Powell of GATA provides to us very important physical commentaries

Seems that many pundits are now talking about selling the dollar and buying assets like gold

(Bloomberg/GATA)

‘Sell dollar for everything else’ is echoing across trading rooms

Submitted by admin on Thu, 2022-01-13 11:05 Section: Daily Dispatches

By Ruth Carson and Joanna Ossinger

Bloomberg News

Thursday, January 13, 2022

Sell the dollar and put money into assets such as emerging-market stocks and gold as the world’s economic recovery gathers steam, money managers say.

A growing chorus of investors is betting the world’s reserve currency has reached a peak in a dramatic turnaround from a month ago when positioning in the greenback was the most bullish since 2015.

END

Big Macs may get to $2,000 before gold

Submitted by admin on Thu, 2022-01-13 11:43 Section: Daily Dispatches

11:49a ET Thursday, January 13, 2022

Dear Friend of GATA and Gold:

Despite yesterday’s rather sensational inflation news, inflation isn’t accelerating as much as it is breaking away from the camouflage that long has been thrown over it by the U.S. government and mainstream financial news organizations.

Monetary metals prices remain almost oblivious to all this, on account of the government interventions against the metals that long have been documented by GATA and similarly overlooked by mainstream financial news organizations:

Monetary metals investors may hope that the deception is becoming less sustainable. Indeed, during the great civil rights struggle in the United States in 1968, Martin Luther King quoted the Scottish historian Thomas Carlyle: “No lie can live forever.”

But the lie that there is no official intervention against gold endures this week. It’s not likely to be defeated by the cowardice of the monetary metals mining industry and financial news organizations and analysts.

If the U.S.government keeps getting its way — and if all major central banks keep cooperating — the price of a Big Mac will reach $2,000 before gold does. For no governments want people to have the option of money that competes strongly with their own.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair Macleod: A euro catastrophe could explode the European Union

Submitted by admin on Thu, 2022-01-13 12:05 Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, January 13, 2022

This article looks at the situation in the euro system in the context of rising interest rates. Central to the problem is role of the European Central Bank, which through monetary inflation embarked on a policy of transferring wealth from fiscally responsible member states to the spendthrift PIGS and France.

The consequences of these policies are that the spendthrifts are now ensnared in irreversible debt traps.

Even in a Keynesian context, the ECB’s monetary policy is no longer to stimulate the economy but to keep the spendthrifts afloat. The situation has deteriorated so that Eurozone commercial banks appear to have credit restricted in New York, evidenced by the reluctance of the U.S. banks to enter into repo transactions with them, leading to the market failure in September 2019 when the Fed had to intervene.

An examination of the numbers strongly suggests that even Eurozone banks, insurance companies, and pension funds are no longer net buyers of Eurozone government debt. This could be because the terms are unattractive. But if that is the case it is an indictment of the ECB’s asset purchase programmes deliberately suppressing rates to the point where they are unattractive, even to normally compliant investors.

Consequently, without any savings offsets, the ECB has gone full Rudolf Havenstein, and is following similar inflationary policies to those that impoverished Germany’s middle classes and starved its labourers and the elderly in 1920-1923.

That the German people are tolerating such an obvious destruction of their currency for the third time in a hundred years is simply astounding. …

… For the remainder of the analysis:

END

END

4.OTHER GOLD STORIES

END

5.OTHER COMMODITIES/

6.CRYPTOCURRENCIES

end

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.3608

OFFSHORE YUAN: 6.3636

HANG SANG CLOSED UP 27.60 PTS OR 0.11%

2. Nikkei closed DOWN 276.53 PTS OR 0.96%

3. Europe stocks ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 94.82/Euro RISES TO 1.1462-

3b Japan 10 YR bond yield: RISES TO. +.131/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.32/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET//

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 82.22 and Brent: 84.38-

3f Gold DON/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE CLOSED DOWN// OFF- SHORE DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO -.0.064%/Italian 10 Yr bond yield FALLS to 1.23% /SPAIN 10 YR BOND YIELD FALLS TO 0.61%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.29: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 1.52

3k Gold at $1821.25 silver at: 23.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3l USA vs Russian rouble; Russian rouble UP 100/100 in roubles/dollar AT 75.58

3m oil into the 82 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.32 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9120– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0454 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 1.743 UP 0 BASIS PTS

USA 30 YR BOND YIELD: 2.083 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 13.59

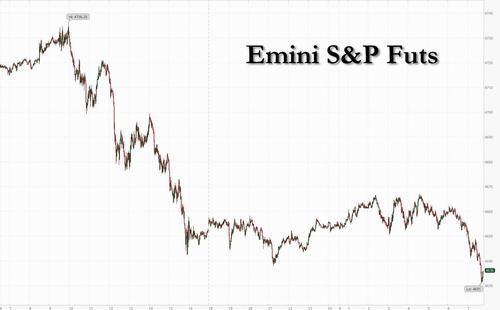

Futures Slide After Disappointing JPMorgan Earnings, Tech Rout Worsens

FRIDAY, JAN 14, 2022 – 08:13 AM

After trading flat for much of the overnight session, S&P futures slumped to session lows shortly after JPM reported earnings that disappointed the market (see our full write up here) and were last trading down 30 points or 0.64%, with Dow futures down 0.3% and Nasdaq futures taking on even more water as the “sell tech” trade was back with a bang. Treasury yields rose 3bps to 1.74% and the dollar reversed an overnight loss. The VIX jumped above 20 and was last seen around 21.

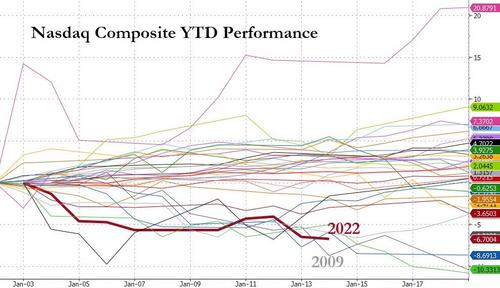

The Nasdaq 100 fell to the lowest in almost three months yesterday as tech came under pressure after Fed Governor Lael Brainard said officials could boost rates as early as March. It looks like the selling will continue today.

“Market sentiment has been shaken by concerns over the prospect of imminent Fed tightening along with record global Covid-19 infection rates, but we don’t expect either of these factors to end the equity rally,” said UBS Wealth Management CIO Mark Haefele in a note. “The fourth-quarter U.S. earnings season, which started this week, could turn investor attention back to strong fundamentals.”

JPMorgan shares dropped in premarket trading after revenues and EPS beat thanks to a $1.8 billion reserve release while FICC trading revenue missed expectations even as its dealmakers posted their best quarter ever and Chief Executive Officer Jamie Dimon gave an upbeat assessment of prospects for growth. Wells Fargo advanced after reporting higher-than-estimated revenue. BlackRock Inc. became the first public asset manager to hit $10 trillion in assets, propelled by a surge in fourth-quarter flows into its exchange-traded funds. Here are some of the other notable pre-movers today:

- U.S.-listed casino stocks with operations in Macau rise after the announcement of much-anticipated changes to the local casino law aimed at tightening government oversight on the world’s largest gaming market. Las Vegas Sands (LVS US) +6.6%; Melco Resorts (MLCO US) +5.5%; Wynn Resorts (WYNN US) +5.6%.

- Apple (AAPL US) shares are up in U.S. premarket trading after Piper Sandler raises its target for the stock, saying that Apple’s set-up for 2022 is favorable. Broker adds that the tech giant’s venture into health-care and automotive markets are the next catalysts to drive the stock to a $4 trillion market cap and beyond.

- NextPlay Technologies (NXTP US) shares jump 19% in U.S. premarket trading after giving an update for fiscal 3Q 2022 late yesterday.

- Domino’s Pizza (DPZ US) is cut to equal-weight from overweight at Morgan Stanley, while Chipotle is upgraded to overweight from equal-weight amid a “mixed” view on restaurant stocks into 2022.

- Amicus Therapeutics (FOLD US) advanced in postmarket trading after being upgraded to outperform from market perform at SVB Leerink, which cited the potential of a treatment for Pompe disease, should it be approved.

- Spirit Realty dropped 4% postmarket after launching a share sale via Morgan Stanley and BofA Securities.

European equities traded poorly and followed the drop in Asia, with most sectors trading lower, weighed down once again by a soft tech sector. Euro Stoxx 50 is down 0.8%, most major indexes dropped over 1% before rising off the lows. Oil & gas is the best Stoxx 600 performer with crude trading well. European technology stocks as well as pandemic winners are leading declines after a U.S. selloff in tech shares resumed Thursday as Federal Reserve officials signaled their intention to combat inflation aggressively. European chipmakers are down in early trading Friday: ASM International -3.5% at 9.17 a.m. CET, Infineon -0.9%, ASML -2.9%, STMicroelectronics -2.3%. Meanwhile, energy and automakers outperformed. Utilities were also in focus as French nuclear energy producer Electricite de France SA (EDF) plunged by a record as the French government confirmed plans to force it to sell more power at a steep discount to protect households from surging wholesale electricity prices, a move that could cost the state-controlled utility 7.7 billion euros ($8.8 billion) at Thursday’s market prices.

There was some good news: a majority of strategists still see the rally in European equities continuing this year. The Stoxx Europe 600 Index will rise about 5.2% to 511 index points by the end of 2022 from Wednesday’s close, according to the average of 19 forecasts in a Bloomberg survey. Equity funds once more led inflows among asset classes in the week through Jan. 12, as investors reduced cash holdings, according to BofA and EPFR Global data.

Earlier in the session, Asian stocks slid as investors offloaded technology shares on growing speculation the Federal Reserve will raise interest rates in March. The MSCI Asia Pacific Index fell as much as 1.3% before paring losses to 0.7% in afternoon trading. Alibaba, Keyence and Sony Group were among the largest contributors to the benchmark’s slide. The Hang Seng Tech Index, which tracks China’s biggest tech firms, closed down 0.5%. Electronics makers also dragged down indexes in Japan and South Korea, with benchmarks in both nations leading the region’s drop. China’s CSI 300 Index closed at its lowest since November 2020. Asian stocks have been whipsawed this year by remarks from Fed officials as investors try to gauge the timing and scope of the anticipated interest rate hikes. The renewed weakness on Friday was triggered by comments from Fed Governor Lael Brainard, who said officials could boost rates as early as March to ensure that price pressures are brought under control. “This kind of hawkishness and a rush for rate hikes is, of course, a minus for share prices,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank in Tokyo. If the Fed were to increase rates in March, “investors will want to make sure the economy remains strong despite the monetary tightening before making their move,” Sera added. With Friday’s moves, Asia’s benchmark is set to pare its weekly gain to about 1.6%, which would still be its best weekly performance since October. In Japan, sentiment worsened as Tokyo raised its Covid alert to the second-highest of four levels as virus cases surged. South Korea’s Kospi was also weighed down as the central bank increased its policy rate for the third time in just five months

In rates, Treasuries pared declines with stock index futures under pressure as U.S. day begins. Yields beyond the 2-year reached session highs inside Thursday’s ranges amid a global government bond selloff. Treasury yields are cheaper by 3bp to 4bp across the curve with 10- year yields around 1.7274%, fading a bigger loss earlier and slightly underperforming bunds and gilts. Asia session featured speculation about tighter global monetary policy. IG dollar issuance slate empty so far and expected to remain light ahead of U.S. holiday weekend with markets closed Monday; four names priced $3.8b Thursday.

In FX, the Bloomberg dollar spot is little changed around worst levels for the week, while NOK, JPY and CAD top the G-10 scoreboard. The yen advanced, and is set for its largest weekly advance in more than a year as speculation about a shift in the Bank of Japan’s policy spurred a further unwinding of dollar longs. The five-year Japanese government bond yield climbed to a six-year high. The volatility term structure in dollar-yen shifted higher Friday and inverted. The euro was little changed around $1.1460 and European sovereign bond yields rose, with the core underperforming the periphery. Norway’s krone and the Canadian dollar advanced as oil prices rose, with Brent trading above $85 per barrel, while the Australian and New Zealand dollars were the worst performers. The pound extended its longest winning streak in nearly two months as the U.K. economy surpassed its pre-pandemic size in November for the first time. Sweden’s krona inched down, shrugging off data showing that the nation’s inflation rate rose to the highest level in 28 years

In commodities, crude futures rally with WTI recovering to Wednesday’s best levels near $83 and Brent putting in fresh highs near $85.40. Spot gold is little changed a brief retest of the week’s highs, trading near $1,823/oz. Base metals are mixed: LME nickel adds about 2% extending its recent surge; copper holds a narrow range in the red

Looking at the day ahead now, data releases include US retail sales, industrial production and capacity utilisation for December, along with the University of Michigan’s preliminary consumer sentiment index for January and the UK’s GDP for November. Central bank speakers include ECB President Lagarde and New York Fed President Williams. Lastly, earnings releases include Citigroup, JPMorgan Chase, Wells Fargo and BlackRock.

Market Snapshot

- S&P 500 futures up 0.3% to 4,667.00

- STOXX Europe 600 down 0.5% to 483.71

- MXAP down 0.8% to 195.28

- MXAPJ down 0.5% to 639.13

- Nikkei down 1.3% to 28,124.28

- Topix down 1.4% to 1,977.66

- Hang Seng Index down 0.2% to 24,383.32

- Shanghai Composite down 1.0% to 3,521.26

- Sensex up 0.1% to 61,320.31

- Australia S&P/ASX 200 down 1.1% to 7,393.86

- Kospi down 1.4% to 2,921.92

- German 10Y yield little changed at -0.08%

- Euro up 0.1% to $1.1467

- Brent Futures up 0.8% to $85.16/bbl

- Gold spot up 0.1% to $1,823.97

- U.S. Dollar Index little changed at 94.73

Top Overnight News from Bloomberg

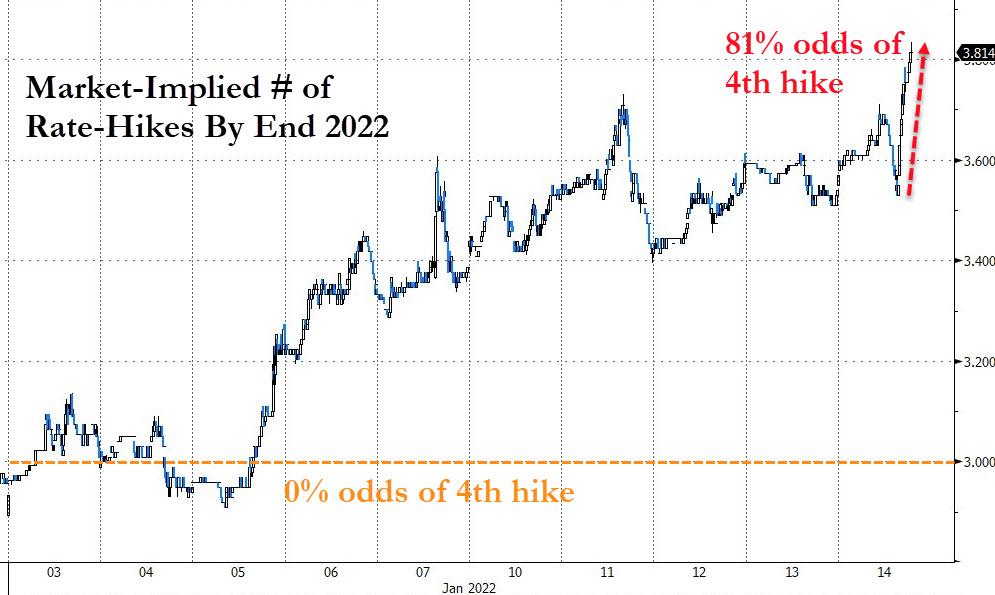

- Federal Reserve Governor Christopher Waller said that three interest-rate increases this year was a “good baseline” but there may be fewer or even as many as five moves, depending on inflation

- The U.K. and the European Union agreed to intensify post-Brexit negotiations over Northern Ireland, as Foreign Secretary Liz Truss led the British side for the first time in a meeting at her official country residence

- Germany’s economy contracted by as much as 1% in the final quarter of 2021 as the emergence of the coronavirus’s omicron strain added to drags on output from supply snarls and the fastest inflation in three decades

- Japan’s Government Pension Investment Fund, the world’s largest, may mull investing in Chinese government bonds if the market situation improves, GPIF President Masataka Miyazono says at a press conference in Tokyo

- Ukraine said a cyberattack brought down the websites of several government agencies for hours. Authorities didn’t immediately comment on the source of the outage, which comes as tensions with Russia surge over its troop buildup near the border

- Russia won’t wait “endlessly” for a security deal with NATO and progress depends on the U.S., Foreign Minister Sergei Lavrov said Friday, keeping up pressure after a week of high-level talks with the West failed to yield noticeable progress

- Turkey’s newly appointed finance chief said the country’s inflation will peak months earlier and at a level far lower than predicted by top Wall Street banks

- The global pressures driving inflation higher represent a “major change in trends” and will keep price growth high for the foreseeable future, Bank of Russia Governor Elvira Nabiullina said

- North Korea appears to have fired two ballistic missiles into waters off its east coast– in what could be its third rocket-volley test in less than 10 days — hours after issuing a fresh warning to the Biden administration

A more detailed look at global markets courtesy of Newsquawk

Asian equity markets weakened amid headwinds from the US where all major indices declined led by losses in tech and consumer discretionary amid a slew of hawkish Fed speak, while mixed Chinese trade data added to the cautiousness in the region. ASX 200 (-1.1%) traded lower as tech and consumer stocks mirrored the underperformance of stateside peers and with nearly all industries on the back foot aside from utilities and gold miners. Nikkei 225 (-1.3%) briefly gave up the 28k level amid a firmer currency and source reports that BoJ policy makers are said to debate how soon they can begin signalling a rate hike. In terms of the notable movers, Fast Retailing was the biggest gainer after it reported a record Q1 net, followed by Seven & I Holdings which also benefitted post-earnings, while Hitachi Construction was at the other end of the spectrum after news that parent Hitachi will offload half its majority stake. KOSPI (-1.4%) eventually underperformed after the Bank of Korea hiked rates by 25bps for a third time in the current tightening cycle to 1.25%, as expected. BoK also noted that CPI is to stay in the 3% range for a while and BoK Governor Lee made it clear that rates will continue to be adjusted which has fuelled speculation of similar action at next month’s meeting. Hang Seng (-0.2%) and Shanghai Comp. (-1.0%) were also pressured with participants digesting the latest trade figures which showed weaker than expected Imports although Exports topped estimates. Nonetheless, the downside was somewhat limited amid ongoing expectations for PBoC easing to support the economy as the Fed moves closer towards a rate lift off and with some encouragement after Evergrande averted its first onshore debt default whereby bondholders approved a six-month postponement of bond redemption and coupon payments. Finally, 10yr JGBs retreated beneath the 151.00 level following the source report that suggested debate within the BoJ on how soon a rate increase can be signalled which could occur ahead of the 2% price target, while this coincided with an increase in the 5yr yield to a 6-year high and a weaker than previous 20yr JGB auction.

Top Asian News

- Chinese Developer R&F Downgraded to Restricted Default by Fitch

- Macau Cuts Casino License Tenure, Caps Float as Controls Tighten

- Inflation Irks Asia as Japan Yields Hit Six-Year High, BOK Hikes

- China Builders’ Dollar Bonds Slump Further; Logan, KWG Lead

The major cash equity indices in Europe remain subdued but off worst levels (Euro Stoxx 50 -0.7%; Stoxx 600 -0.6%) as the downbeat APAC mood reverberated into the region amid a slew of hawkish Fed speak, while the mixed Chinese trade data added to the concerns of a slowdown ahead of next week’s GDP metrics. Newsflow had overall been quiet during the European session ahead of the start of US earnings season, but geopolitical tensions remain hot on the radar after North Korea fired its third missile of the year (albeit landing outside Japan’s EEZ), whilst Russia closed all communication channels with the EU and exerted some time-pressure on Washington with regards to Moscow’s security demands. Back to trade, a divergence is seen between Europe and the US as the former catches up to the late accelerated sell-off on Wall Street yesterday; US equity futures have been consolidating with mild broad-based gains seen across the ES (+0.2%), YM (+0.2%), NQ (+0.2%) whilst the RTY (Unch) narrowly lags. Delving into Europe, the UK’s FTSE 100 (-0.1%) is cushioned by gains across its Oil & Gas and Financial sectors as crude oil prices and yields clamber off intraday lows, whilst the SMI (-0.3%) sees some losses countered by its heavyweight healthcare sector. Sectors in Europe are mostly in the red with a slight defensive tilt, although Oil & Gas stands as the top gainer and the only sector in the green. The downside meanwhile sees Tech following a similar sectorial underperformance seen on Wall Street and APAC overnight. In terms of individual movers, DAX-heavyweight SAP (-0.3%) conforms to the losses across tech after initially rising as a result of upgraded guidance and the announcement of a share buyback programme of up to EUR 1bln. The most notable mover of the day has been EDF (-17.5%) as the Co. withdrew guidance after noting the impact of new French price cap measures is forecast to be around EUR 8.4bln on FY22 EBITDA.

Top European News

- EDF Slumps by Most on Record on Hit From Price Cap

- U.K. Economy Surpasses Pre-Pandemic Size With November Surge

- German Recovery Lags Rest of Europe on Supply Snarls, Inflation

- HSBC Markets Chief Georges Elhedery To Take Six-Month Sabbatical

In FX, another lower low off a lower high does not bode well for the index and Buck more broadly, but some technicians will be encouraged by the fact that chart supports in the form of a Fib retracement and 100 DMA have only been breached briefly. Meanwhile, Friday may provide the Greenback with a prop via pre-weekend position squaring and US data could lend a hand if upbeat or better than expected at the very least. For now, the DXY is restrained between 94.887-626 confines, with the upside capped by a major trendline that falls just below 95.000 around 94.980, and the Dollar also hampered by pressure emanating outside the basket from the likes of the Yuan, crude oil and other commodities.

- CAD/JPY/GBP – The Loonie has reclaimed 1.2500+ status in line with a rebound in WTI towards Usd 83/brl, but still faces stiff trendline resistance vs its US counterpart at 1.2451 and probably conscious that several multi-billion option expiries roll off either side of the 1.2500 level today. Conversely, the Yen has cleared the psychological 114.00 hurdle with some fundamental impetus coming from hawkish BoJ source reports contending that policy-setters are contemplating how soon the Bank can telegraph a rate hike that is likely to be delivered prior to inflation reaching its 2% target. Elsewhere, Sterling remains elevated above 1.3700, though unable to scale 1.3750 even with tailwinds from stronger than forecast UK GDP and IP or a narrower than feared trade gap amidst ongoing political uncertainty.

- CHF/EUR/NZD/AUD – All narrowly divergent and contained against their US rival, with the Franc straddling 0.9100 and Euro holding within a 1.1483-51 range and immersed in hefty option expiry interest spanning 1.1395 to 1.1485 (see 7.01GMT post on the Headline Feed for details). On the flip-side, the Aussie and Kiwi have both lost a bit more momentum after probing 0.7300 and approaching 0.6900 respectively yesterday, and Aud/Usd appears to have shrugged off robust housing finance data in the run up to China’s trade balance revealing sub-consensus imports.

- SCANDI/EM – Firmer than anticipated Swedish CPI and CPIF metrics have not offered the Sek much support, as the stripped down core ex-energy print was in line and bang on the Riksbank’s own projection. However, the Huf has been underpinned by hot Hungarian inflation and the Cnh/Cny in wake of the aforementioned Chinese trade data showing a record surplus for December and 2021 overall. In Turkey, the Try is flattish following the latest CBRT survey that predicts a weaker year-end Lira from current levels, but above record lows and still well above target CPI, while in Russia the Rub is benefiting from Brent’s rise above Usd 85.50/brl (in keeping with the Nok) against the backdrop of geopolitical and diplomatic strains as the country’s Foreign Minister declares that all lines of communication with the EU have ended.

In commodities, WTI and Brent front-month futures have been on an upward trajectory since the Wall Street close, with the former now above USD 83/bbl (vs 81.58/bbl low) and the latter north of USD 85.50/bbl (vs 83.99/bbl low) in European hours. Overall market sentiment has been a non-committal one amid a lack of fresh macro catalysts, however, geopolitical updates have been abundant: namely with Russia’s punchy rhetoric surrounding its security demand from NATO and Washington, whilst North Korea fired what is said to be ballistic missiles which landed just outside Japan’s Exclusive Economic Zone (EEZ). On the demand side of the equation, eyes remain on China’s economic and COVID situations, with the import figures indicating China’s annual crude oil imports drop for the first time in 20 years, whilst the nation grounded further flights between the US due to its zero-COVID policy. On the supply side, reports suggested that China will release oil stockpiles in the run-up to the Lunar New Year (dubbed as the largest human migration). The release is part of a coordinated plan with the US and other major consumers, according to the reports, which cited sources suggesting China will likely ramp up its releases if prices top USD 85/bbl. Turning to metals, spot gold is trading sideways and prices waned after again hitting the resistance zone around USD 1,830/oz flagged earlier this week. LME copper meanwhile remains under USD 10,000/t – subdued by the sharp slowdown in Chinese imports suggesting weaker demand, albeit annual imports of copper concentrate hit a historic high in 2021. The trade data also indicated a fall in iron ore imports as a factor of the steel production curbs imposed last year to tackle pollution and high iron ore prices.

US Event Calendar

- 8:30am: Dec. Import Price Index YoY, est. 10.8%, prior 11.7%; MoM, est. 0.2%, prior 0.7%

- Export Price Index YoY, est. 16.0%, prior 18.2%; MoM, est. 0.3%, prior 1.0%

- 8:30am: Dec. Retail Sales Advance MoM, est. -0.1%, prior 0.3%

- Dec. Retail Sales Ex Auto MoM, est. 0.1%, prior 0.3%

- Dec. Retail Sales Ex Auto and Gas, est. -0.2%, prior 0.2%

- Dec. Retail Sales Control Group, est. 0%, prior -0.1%

- 9:15am: Dec. Industrial Production MoM, est. 0.2%, prior 0.5%

- Capacity Utilization, est. 77.0%, prior 76.8%

- Manufacturing (SIC) Production, est. 0.3%, prior 0.7%

- 10am: Nov. Business Inventories, est. 1.3%, prior 1.2%

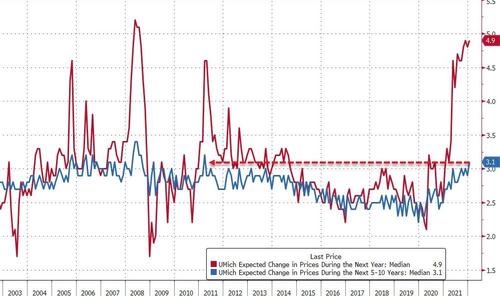

- 10am: Jan. U. of Mich. Sentiment, est. 70.0, prior 70.6; Expectations, est. 67.0, prior 68.3; Current Conditions, est. 73.8, prior 74.2

- U. of Mich. 1 Yr Inflation, est. 4.8%, prior 4.8%; 5-10 Yr Inflation, prior 2.9%

DB’s Jim Reid concludes the overnight wrap

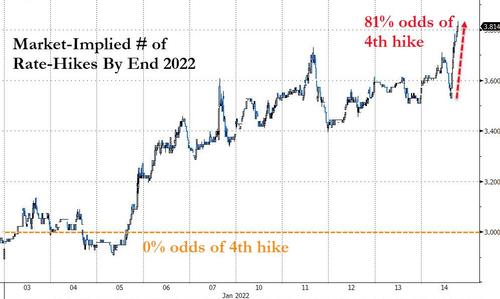

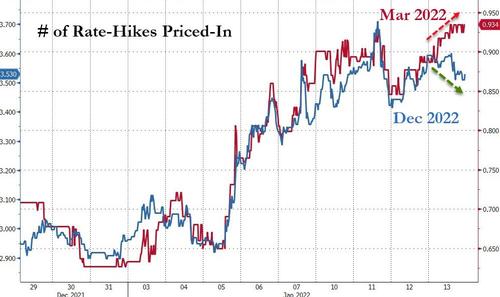

There was no rest for markets either yesterday as the tech sell-off resumed in earnest, which came as fed funds futures moved to price in a 93% chance of a March rate hike, the highest closing probability to date. At the same time, however, the US dollar continued to weaken and has now put in its worst 3-day performance in over a year, having shed -1.25% in that time. And all this is coming just as earnings season is about to ramp up, with a number of US financials scheduled to report today ahead of an array of companies over the next few weeks.

Starting with sovereign bonds, yields on 10yr Treasuries fell a further -3.9bps yesterday, their biggest decline since mid-December, to their lowest closing level in a week, at 1.704%, with most of the price action again happening during the New York afternoon. Lower inflation breakevens helped drive the decline, with the 10yr breakeven down -3.4bps after the producer price inflation data for December came in softer than expected. Indeed, the monthly gain of +0.2% (vs. +0.4% expected) was the slowest since November 2020, and in turn that left the year-on-year measure at +9.7% (vs. +9.8% expected), which is actually a modest decline from the upwardly revised +9.8% in November. As with the previous day’s CPI reading though, there was a more inflationary interpretation for those after one, as the core PPI measure came in at a monthly +0.5% as expected, leaving the year-on-year change at an above-expected +8.3% (vs. +8.0% expected). So something for everyone but no massive surprises either way.

The latest inflation data came as numerous Fed speakers continued to match the recent hawkish tone, which helped strengthen investor conviction in the odds of a March hike as mentioned at the top. Philadelphia Fed President Harker said at an event that “My forecast is that we would have a 25 basis-point increase in March, barring any changes in the data”, and that he had 3 hikes pencilled in but “could be convinced of a fourth if inflation is not getting under control.” Separately, we heard from Governor Brainard, who appeared before the Senate Banking Committee as part of her nomination hearing to become Fed Vice Chair. She signalled that she would be open to a March hike as well, saying that they would be in a position to hike “as soon as asset purchases are terminated”, which they’re currently on course to do in March. Even President Evans, one of the most dovish members of Fed leadership, said a March rate hike and multiple hikes this year were a possibility. As it happens, today is the last we’ll hear from various Fed speakers for a while, as tomorrow they’ll be entering their blackout period ahead of the next FOMC announcement later in the month.

Staying on the Fed, Bloomberg reported overnight that President Biden has picked three nominees for the vacant slots. They include Sarah Bloom Raskin, previously Deputy Secretary of the Treasury, who’s reportedly going to be nominated to become the Vice Chair of supervision, as well as Lisa Cook and Philip Jefferson, who’d become governors. Cook is an economics professor at Michigan State University, and Jefferson is an economics professor at Davidson College in North Carolina. All 3 would require Senate confirmation, and bear in mind those choices haven’t been officially confirmed as of yet.

Over on the equity side, the main story was a further tech sell-off that sent both the NASDAQ (-2.51%) and the FANG+ index (-3.72%) lower for the first time this week, and taking the former to a 3-month low. That weakness dragged the S&P 500 (-1.5%) lower, though despite the stark headline numbers, it was only just over half of the shares in the index that were in the red on the day. Meanwhile in Europe, the STOXX 600 (-0.03%) also saw a modest decline, though the STOXX Banks (+1.10%) hit a fresh 3-year high after advancing for the 8th time in the last 9 sessions. Sovereign bond yields echoed the declines in the US too, with those on 10yr bunds (-3.1bps), OATs (-3.3bps) and BTPs (-4.6bps) all moving lower.

Following that tech-driven fall overnight on Wall Street on the back of those hawkish comments, Asian stock markets are trading lower this morning. Japan’s Nikkei (-1.42%) extended the previous session’s losses while briefly falling over -2%, as the Japanese Yen found a renewed bid amid the risk-off mood. Additionally, the Kospi (-1.37%) widened its losses, after the BOK lifted borrowing costs by 25bps to 1.25% amidst rising concerns about inflationary pressure. That takes the benchmark rate back to pre-pandemic levels after the central bank’s 25bps rate increase in August and November last year. Meanwhile, the Korean government unveiled a supplementary budget worth 14 trillion won in size to continue providing support to the economy. Elsewhere, the Hang Seng index (-0.86%), CSI (-0.60%) and Shanghai Composite (-0.53%) have all moved lower as well. Data released in China showed that exports went up +20.9% y/y in December (vs +20.0% market expectations) albeit imports in December rose +19.5% y/y less than +28.5% as anticipated. That meant that they posted a trade surplus of $94.46bn last month, above the consensus forecast for a $74.50bn surplus. Looking ahead, futures on both the S&P 500 (-0.19%) and DAX (-0.79%) are pointing to further losses later on.

Elsewhere in markets, yesterday saw another surge in European natural gas futures (+13.71%), albeit still at levels which are less than half of the peaks seen in mid-December. The latest moves came as Russia’s deputy foreign minister Sergei Ryabkov said that talks with the US had reached a “dead end”, amidst strong tensions between the two sides with Russia rejecting any further expansion of NATO as well as calls to pull back its forces from near Ukraine’s border. In response, the Russian ruble weakened -2.31% against the US dollar yesterday, whilst the MOEX stock index (-4.05%) suffered its worst daily performance since April 2020.

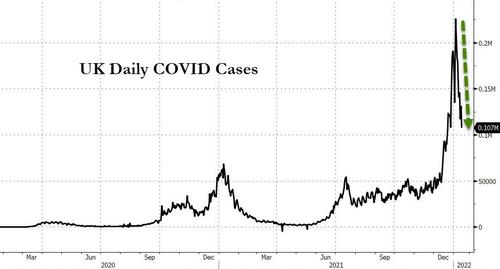

Turning to the Covid-19 pandemic, the decline in UK cases continued to accelerate yesterday, with the number of cases over the past week now down -24% relative to the previous 7-day period. Looking at England specifically, the total number of Covid-19 patients in hospital is now down for a 3rd day running, and in London the total number in hospital is down to its lowest level since New Year’s Eve.

To the day ahead now, and data releases include US retail sales, industrial production and capacity utilisation for December, along with the University of Michigan’s preliminary consumer sentiment index for January and the UK’s GDP for November. Central bank speakers include ECB President Lagarde and New York Fed President Williams. Lastly, earnings releases include Citigroup, JPMorgan Chase, Wells Fargo and BlackRock.

3. ASIAN AFFAIRS

i)FRIDAY MORNING THURSDAY NIGHT

SHANGHAI CLOSED DOWN 34.00 PTS OR 0.96% //Hang Sang CLOSED DOWN 46.45 PTS OR 0.19% /The Nikkei closed DOWN 364,85 PTS OR 1.28% //Australia’s all ordinaires CLOSED DOWN 1.03% /Chinese yuan (ONSHORE) closed UP 6.3531 /Oil UP TO 82.53 dollars per barrel for WTI and UP TO 84.98 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3531. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3591: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN AND OFF SHORE TRADING STRONGER AGAINST USA DOLLAR

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

After North Korea fires two hypersonic missiles, the USA is set to Kim et al with more sanctions.

(zerohedge)

US Hits N.Korea With More Sanctions As Kim Hails Tests Of Hypersonic Nuclear “War Deterrent”

THURSDAY, JAN 13, 2022 – 05:40 PM

Following two North Korean missile launches which came within the last week, with the Tuesday test being claimed by Pyongyang to have been it’s third ‘successful’ hypersonic projectile test, the Biden administration extended US sanctions on North Korean as well as Russian officials believed involved in Pyongyang’s ballistic missile program.

The fresh Treasury Department sanctions target five individuals responsible for procuring parts for North Korea’s “weapons of mass destruction (WMD)” program, as the statement reads. Further it described the new punitive actions “in line with U.S. efforts to prevent the advancement of the DPRK’s WMD and ballistic missile programs” and which “impede attempts by Pyongyang to proliferate related technologies.”January 11, 2022 photo released by KCNA, via Reuters

The Treasury counted “the DPRK’s six ballistic missile launches since September 2021, each of which violated multiple United Nations Security Council Resolutions (UNSCRs).”

Amid completely stalled Washington-Pyongyang talks, which haven’t been a reality since the Trump administration – and as Seoul has recently pushed for the resumption of direct dialogue on denuclearizing the Korean peninsula – US Secretary of State Antony Blinken has lately vowed to use “every appropriate tool” to go after North Korea’s weapons programs, “which constitute a serious threat to international peace and security and undermine the global nonproliferation regime.”

The Wednesday Treasury statement still held out hope for the possibility of “dialogue and diplomacy” with the DPRK; however, the latest missile tests are seen as a direct message to the West that King Jong-un is expanding his arsenal and capability.

ABC News details of Tuesday’s launch which went in the direction of Japan, based on state media sources:

The Korean Central News Agency said Tuesday’s launch involved a hypersonic glide vehicle, which after its release from the rocket booster demonstrated “glide jump flight” and “corkscrew maneuvering” before hitting a sea target 1,000 kilometers (621 miles) away. Photos released by the agency showed a missile mounted with a pointed cone-shaped payload soaring into the sky while leaving a trail of orange flames and Kim watching from a small cabin with top officials, including his sister Kim Yo Jong.

The projectile is believed to have reached Mach 10, alarming intelligence agencies in the West, and which even briefly resulted in an FAA order to ground commercial flights on the US West coast (for an estimated five to seven minutes).KCNA via Reuters

Kim this week hailed the country’s claimed hypersonics program, which officials in the West remain skeptical of – doubting that it’s very far along at all – as part of increasing North Korea’s nuclear “war deterrent”.

END

3B JAPAN

end

3c CHINA

CHINA/COVID

true death toll in China is 366 times the official figures states economist:

China’s True COVID-19 Death Toll 366 Times Higher Than Official Figure, Economist Says

Inbox

| Robert Hryniak | 8:01 AM (14 minutes ago) | ||

| to |

Like always there is no truth from China

4/EUROPEAN AFFAIRS

//UKCOVID/VACCINE

How Boris fumbled on the COVID creating a crisis in the UK.

(Bill Blain)

UK In Crisis: Should COVID Claim Another Victim While Self-Righteous Wrath Sets The Tone?

FRIDAY, JAN 14, 2022 – 03:30 AM

Authored by Bill Blain via MorningPorridge.com,

“My chances of being PM are about as good as the chances of finding Elvis on Mars, or my being reincarnated as an olive.”

Boris apologised – but is it too late? Resolving the innumerable crises facing the UK requires political focus, and less of the politically expedient indignation being displayed in parliament. It won’t make anything better, threatens further destabilisation, and diminish the UK’s global competitiveness..

The objective of the Morning Porridge is to connect the dots on markets – so let me ask the most pertinent question today: Would you be a buyer of UK plc? Probably not.

The optics from Westminster look terrible. The prospects for the nation look even worse. Its situation normal: FUBAR!

Coronavirus was a terrible and tragic event for innumerable families. Many people are justifiably angry having watched from afar as loved ones died alone. Yet, the events in parliament yesterday were a masterpiece of staged-managed faux indignation. The self-appointed Covid Truth and Reconciliation Committee has a whole list of names pricked, queued for the tumbril, and a terminal appointment on the Tower’s chopping board – like that is going to change anything…

The problem is such grandstanding while the government is on the ropes doesn’t achieve much – except make a bad situation worse. While Boris flounders, we can forget any meaningful effort to deal with the impact of soaring Energy prices on consumers, addressing the insatiable appetite of the NHS for more and more cash to do less and less, and as for the perceived benefits of Brexit? Well, that’s a boat that’s already sailed….

None of the critical crises blighting an increasingly dysfunctional Blighty look likely to be fixed as government lurches from crisis to catastrophe.

Every politician is looking to their own survival or advancement. Prime Minister in Waiting, Rishi Sunak, made sure he was out of London and singularly failed to post support for the PM. The leader of the Scottish Conservatives wisely put the boot in with the first call to resign – knowing Scots will love him for it. Et tu Brute? As new Tory MP spilloried the prime minister in the hope they might be able to hold on to “Red Wall” seats, something extraordinary happened in Parliament yesterday: Labour party leader Sir Kier Starmer looked almost competent and actually scored some telling blows.

The latest polls say Labour is leading the Tories. There was a time that would have caused me to rejoice – but now? Years of Tory rule has shown them mired in scandal, disregard for rules, and arrogance. But Labour shows little sign of a becoming a credible government.