March 16, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

MARCH16

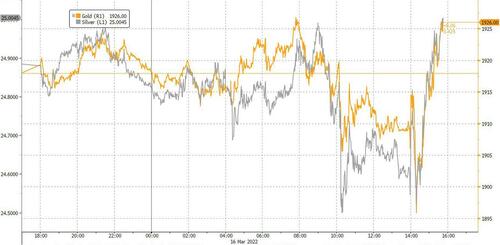

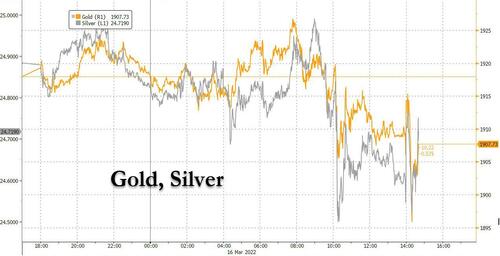

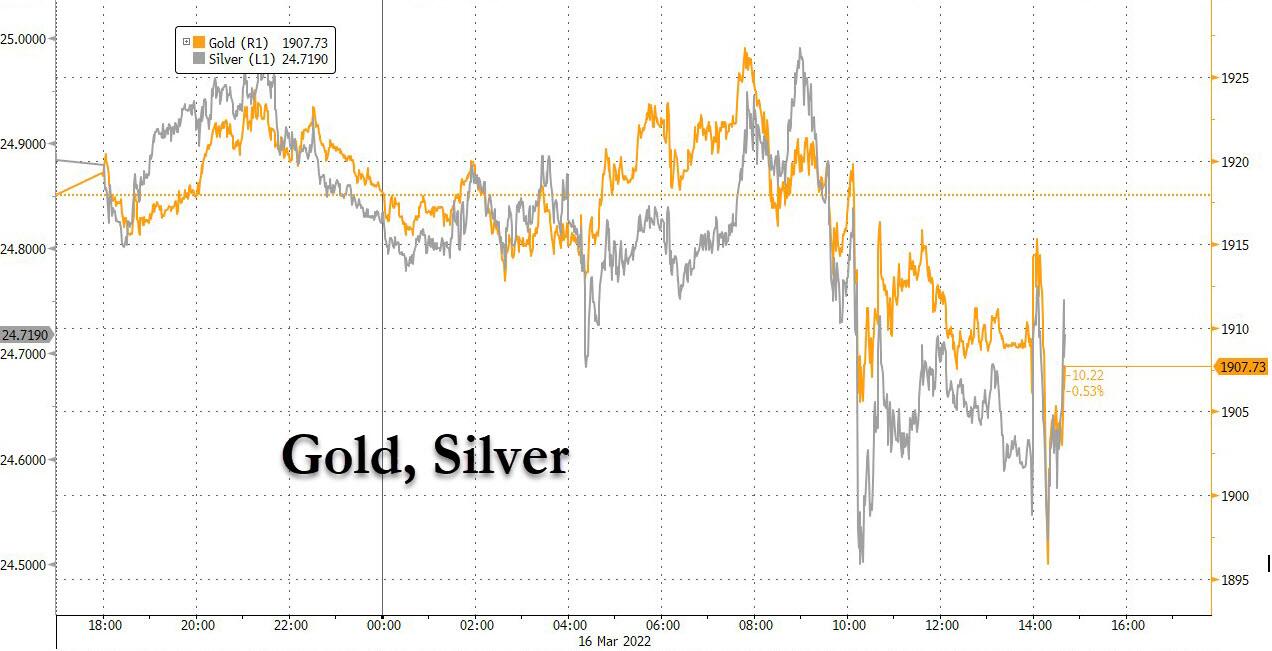

GOLD; $1908.95 DOWN $18.50

SILVER: $24.60 DOWN $0.56

ACCESS MARKET: GOLD $1925.50

SILVER: $25.08

Bitcoin morning price: $40,614 UP 1024

Bitcoin: afternoon price: $40,702 UP 1112

Platinum price: closing DOWN $34.35 to $1009.40

Palladium price; closing DOWN $39.00 at $2397.75

END

end

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

March: JPMorgan stopped/total issued 184/337

DLV615-T CME CLEARING

BUSINESS DATE: 03/15/2022 DAILY DELIVERY NOTICES RUN DATE: 03/15/2022

PRODUCT GROUP: METALS RUN TIME: 20:59:26

EXCHANGE: COMEX

CONTRACT: MARCH 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,928.500000000 USD

INTENT DATE: 03/15/2022 DELIVERY DATE: 03/17/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 4

104 C MIZUHO 7

363 H WELLS FARGO SEC 15

435 H SCOTIA CAPITAL 35

624 H BOFA SECURITIES 27

657 C MORGAN STANLEY 2

657 H MORGAN STANLEY 24

661 C JP MORGAN 334 184

709 C BARCLAYS 32

737 C ADVANTAGE 1 3

905 C ADM 6

TOTAL: 337 337

MONTH TO DATE: 10,654

NUMBER OF NOTICES FILED TODAY FOR Mar. CONTRACT337 NOTICE(S) FOR 33700 OZ (1.0506 TONNES)

total notices so far: 10,654 contracts for 1,065,400 oz (33.138 tonnes)

SILVER NOTICES:

6 NOTICE(S) FILED TODAY FOR 30,000 OZ/

total number of notices filed so far this month 10,372 : for 51,860,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $18.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2.33 TONNES FROM THE GLD

INVENTORY RESTS AT 1061.83 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN $0.56

AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 462,000 OZ

FROM THE SLV.

CLOSING INVENTORY: 545.022 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1224 CONTRACTS TO 159,571 ON DAY 5 OF OUR CONTINUAL RAID, AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR SMALLISH $0.18 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.18) BUT WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A SMALL GAIN OF 306 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A HUGE INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 42.860 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 110,000 OZ //NEW STANDING 52.255 MILLION OZ // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —370

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTACTS for 12 days, total contracts: : 25,788 contracts or 128.940 million oz OR 10.741 MILLION OZ PER DAY. (2149 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 25,788 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 128.940 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 128.940 MILLION OZ//THIS IS GOING TO BE A HUGE EFP ISSUANCE MONTH AND MOST LIKELY WILL SET A RECORD FOR ANY MONTH

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1224 WITH OUR $0.18 LOSS SILVER PRICING AT THE COMEX// TUESDAY THE CME NOTIFIED US THAT WE HAD A VERY STRONG SIZED EFP ISSUANCE OF 1160 CONTRACTS( 1160 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 42.860 MILLION OZ FOLLOWED BY TODAY’S 110,000 OZ QUEUE JUMP//NEW STANDING 52.255 MILLION OZ// /// .. WE HAD A SMALL SIZED LOSS OF 64 OI CONTRACTS ON THE TWO EXCHANGES FOR 0.320 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 6 NOTICES FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 7179 CONTRACTS TO 617,605 AND FURTHER FROM OUR NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –1573 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED DECREASE IN COMEX OI CAME WITH OUR HUGE LOSS IN PRICE OF $30.80//COMEX GOLD TRADING/TUESDAY/.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR HUMONGOUS SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MARCH AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 2400 OZ//NEW STANDING 36.115 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $30.80 WITH RESPECT TO TUESDAY’S TRADING

WE HAD AN STRONG GAIN OF 7858 OI CONTRACTS (24.44 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 15,028 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 617,605.

IN ESSENCE WE HAVE AN STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7858, WITH 7,170 CONTRACTS DECREASED AT THE COMEX AND 15,028 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7858 CONTRACTS OR 24.44 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GIGANTIC SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (15,028) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (7170,): TOTAL GAIN IN THE TWO EXCHANGES 7858 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR MARCH. AT 14.818 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 2400 OZ//NEW STANDING 36.115 TONNES /// 3) ZERO LONG LIQUIDATION ///. ,4) GOOD SIZED COMEX OI. LOSS 5) GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICAL/

LADIES AND GENTLEMEN: THE GOLD COMEX IS ALSO BEING ATTACKED FOR GOLD METAL FROM LONDON ET AL.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MARCH

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

87,912 CONTRACTS OR 8,791,200 OR 273.44 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 733 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 273.44TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 273.44/3550 x 100% TONNES 7,69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 273.44 TONNES INITIAL( THIS WILL PROBABLY BE A RECORD EFP ISSUANCE MONTH. TOMORROW WE WILL SURPASS MARCH 21 AND THEN LATER THIS MONTH WE WILL SURPASS NOV 21, THE ALL TIME RECORD MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL.WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MARCH HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL, FOR GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1224 CONTRACTS TO 159,941 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 4 1/2 YEARS AGO.

EFP ISSUANCE 1160 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 1160 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1160 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1224 CONTRACTS AND ADD TO THE 1160 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 64 OPEN INTEREST CONTRACT FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 0.320 MILLION OZ,

OCCURRED DESPITE OUR $0.18 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

5. Other gold commentaries

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 106.75 PTS OR 3.48% //Hang Sang CLOSED UP 1672.42 PTS OR 9.06 % /The Nikkei closed UP 415.53 PTS or 1.64% //Australia’s all ordinaires CLOSED UP 1.08% /Chinese yuan (ONSHORE) closed UP 6.3495 /Oil DOWN TO 96.62 dollars per barrel for WTI and DOWN TO 99.65 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.3495. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3675: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

A)NORTH KOREA/

b) REPORT ON JAPAN

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 7170 CONTRACTS AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR STRONG LOSS OF $30.80 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A GIGANTIC SIZED EFP (15,028 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE NON ACTIVE DELIVERY MONTH OF MAR.. THE CME REPORTS THAT THE BANKERS ISSUED A GIGANTIC SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 15,028 EFP CONTRACTS WERE ISSUED: ;: , & FEB. 0 APRIL:15,028 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 15,028 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7170 CONTRACTS IN THAT 15,058 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 7170 CONTRACTS..AND THIS STRONG GAIN OCCURRED DESPITE A HUGE LOSS IN PRICE OF $30.80.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAR (36.115),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.115 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $30.80) BUT THEY WERE UNSUCCESSFUL IN FLEECING ANY LONGS AS WE HAVE REGISTERED A STRONG SIZED GAIN OF 7,858 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAR (36.115 TONNES)…

WE HAD –1573 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 7858 CONTRACTS OR 785,800 OZ OR 24.44 TONNES

Estimated gold volume today: 190,825 ///poor

Confirmed volume yesterday: 276,340contracts fair

INITIAL STANDINGS FOR MAR ’22 COMEX GOLD //MARCH 16

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 15,642.561 oz JPMORGAN |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 482,265.000 OZ JPMORGAN 15,000 KILOBARS |

| No of oz served (contracts) today | 337 notice(s) 33,700 OZ 1.0506 TONNES |

| No of oz to be served (notices) | 957 contracts 95,700 oz 2.974 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,654 notices 10,65,400 OZ 33..138 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

1)dealer deposit

total dealer deposit 0 oz

No dealer withdrawal 0

1 customer deposits

i) Into JPMORGAN: 482,265.000 OZ (15,000 KILOBARS= 15 TONNES)

total deposit: 482,265,000 oz

1 customer withdrawal

i) Out of JPMORGAN: 25,642.561 oz

total withdrawals: 25,642.561 oz

ADJUSTMENTS: 1/customer to dealer

Manfra: 32,183.151 oz (1001 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MARCH.

For the front month of MARCH we have an oi of 1294 contracts having LOST 51

We had 75 notices filed yesterday so strangely again on day 12 we gained another queue jump i.e. 24 contracts or an additional 2400 oz will stand for delivery and these guys refused again to be EFP’d over to London. They must

be after large amounts of gold on this side of the pond after Russia cannot//will not supply any precious metals to London. The 2400 oz is represented by 0.0746 tonnes,

April saw a loss of 29,232 contracts down to 274,335.

May saw a gain of 104 contracts to stand at 4252

June saw a GAIN of 21,894 contracts up to 271,695 contracts

We had 337 notice(s) filed today for 78,800 oz FOR THE MAR 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 334 notices were issued from their client or customer account. The total of all issuance by all participants equates to 337 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 184 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 5 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR /2021. contract month,

we take the total number of notices filed so far for the month (10,654) x 100 oz , to which we add the difference between the open interest for the front month of (MAR: 1294 CONTRACTS ) minus the number of notices served upon today 337 x 100 oz per contract equals 1,161,100 OZ OR 36.115 TONNES the number of TONNES standing in this active month of mar.

thus the INITIAL standings for gold for the MAR contract month:

No of notices filed so far (10,654) x 100 oz+ (1294) OI for the front month minus the number of notices served upon today (337} x 100 oz} which equals 1,161,100 oz standing OR 36.115 TONNES in this NON active delivery month of MAR.

TOTAL COMEX GOLD STANDING: 36.115 TONNES (A WHOPPER FOR A MAR (NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

191,133,764.7, oz NOW PLEDGED /HSBC 5.94 TONNES

123,963.792 PLEDGED MANFRA 3.86 TONNES

54,339.114oz PLEDGED JPMorgan no 1 1.690 tonnes

243,923.704, oz JPM No 2 7.58 TONNES

898,821.330 oz pledged Brinks/27,96 TONNES

12,249,333 oz International Delaware: 0..3810 tonnes

Loomis: 18,615.429 oz

total pledged gold: 1,543,044.471 oz 47.99 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 33,611,452.774 OZ (1045.45TONNES)

TOTAL ELIGIBLE GOLD: 16,041,740.345 OZ (498.96 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,569,712.429 OZ (546.49 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 16,026668.0 OZ (REG GOLD- PLEDGED GOLD) 498.49 tonnes

END

MAR 2022 CONTRACT MONTH//SILVER//MARCH 16

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 584,581.100 oz JPMORGAN |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 6CONTRACT(S) 30,000 OZ) |

| No of oz to be served (notices) | 79 contracts (395,000 oz) |

| Total monthly oz silver served (contracts) | 10,372 contracts 51,860,000 oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposits into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 0 deposits into the customer account

total deposit: NIL oz

JPMorgan has a total silver weight: 181.126 million oz/343.403 million =52.70% of comex

ii) Comex withdrawals: 1

A) Out of JPMorgan 584,581.100 oz

total withdrawal 584,581.100 oz

we had 1 adjustments// out of dealer to customer

JPMorgan 178,682.470

the silver comex is in stress!

TOTAL REGISTERED SILVER: 93.126 MILLION OZ

TOTAL REG + ELIG. 343.403 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR MARCH

silver open interest data:

FRONT MONTH OF MARCH OI: 85, HAVING LOST 280 CONTRACTS FROM MONDAY.

WE HAD 302 NOTICES SERVED UPON YESTERDAY, SO WE GAINED 22 CONTRACTS OR AN ADDITIONAL 110,000 OZ WILL STAND

FOR DELIVERY OVER HERE AS THESE GUYS REFUSED TO BE EFP’D TO LONDON.

APRIL HAD A 77 CONTRACT LOSS// CONTRACTS FALLING TO 615

MAY HAD A LOSS OF 868 CONTRACTS DOWN TO 121,943 contracts

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 6 for 30,000 oz

Comex volumes: 39,217// est. volume today//weak/

Comex volume: confirmed yesterday: 52,510 contracts (FAIR )

To calculate the number of silver ounces that will stand for delivery in MAR. we take the total number of notices filed for the month so far at 10,372 x 5,000 oz = 51,860,000 oz

to which we add the difference between the open interest for the front month of MAR (85) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2021 contract month: 10,372 (notices served so far) x 5000 oz + OI for front month of MAR (85) – number of notices served upon today (6) x 5000 oz of silver standing for the MAR contract month equates 52,255,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MARCH 16/WITH GOLD DOWN $18.50//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWALL OF 2.33 TONNES FROM THE GLD///INVENTORY RESTS AT 1061.83 TONNES

MARCH 15/WITH GOLD DOWN $30.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1064.16 TONNES

MARCH 14//WITH GOLD DOWN $22.75, HUGE CHANGES IN GOLD INVENTORY AT THE GLD//STRANGE: A DEPOSIT OF 2.62 TONNES INTO THE GLD.//INVENTORY RESTS AT 1064.16 TONNES

MARCH 11/WITH GOLD DOWN $14.60: A BIG CHANGE IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1061.54 TONNES

MARCH 10//WITH GOLD UP $11.55: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FORM THE GLD///INVENTORY RESTS AT 1063.28 TONNES

MARCH 9/WITH GOLD DOWN $53.85//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.64 TONNES INTO THE GLD//INVENTORY RESTS AT 1067.34 TONNES

MARCH 8/WITH GOLD UP $46.10: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 8.42 TONNES INTO THE GLD///INVENTORY RESTS AT 1062.70 TONNES

MARCH 7/WITH GOLD UP $28.40 A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1054.28 TONNES

MARCH 4/WITH GOLD UP $28.40//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1050.22 TONNES

MARCH 3/WITH GOLD UP $13.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 7.84 TONNES//INVENTORY RESTS AT 1050.22 TONNES

MARCH 2/WITH GOLD DOWN $20.80//A MONSTER CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 13.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1042.38 TONNES

MARCH 1/WITH GOLD UP $42.60: NO CHANGES IN GOLD INVENTORY AT THE GLD: //INVENTORY RESTS AT 1029.32 TONNES

FEB 28/WITH GOLD UP $12.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 25/WITH GOLD DOWN $38.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1029.32 TONNES

FEB 24/WITH GOLD UP $17.35//A HUGE CHANGE AT THE GLD: 5.23 TONNES INTO THE GLD// IN GOLD INVENTORY AT THE GLD/INVENTORY REST AT 1029.32 TONNES

FEB 23/WITH GOLD UP $2.00 : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1024.09 TONNES

FEB 22/WITH GOLD UP $6.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.65 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1024.09 TONNES

FEB 18/WITH GOLD DOWN $1.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 17/WITH GOLD UP $29.50: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 16/WITH GOLD UP 414.60 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 15/WITH GOLD DOWN $12.70 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 14/WITH GOLD UP $27.20 NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1019.44 TONNES

FEB 11/WITH GOLD UP $4.50 A HUGE CHANGE IN GOLD IVNETORY AT THE GLD// A DEPOSIT OF 3.48 TONNES INTO THE GLD//INVENTORY RESTS AT 1019.44 TONES

FEB 10/WITH GOLD UP $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 1015.96 TONNES

FEB 9/WITH GOLD UP $8.05//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 8/WITH GOLD UP $5.95 TODAY: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.36 TONNES INTO THE GLD//INVENTORY RESTS AT 1015.96 TONNES

FEB 7/WITH GOLD UP $14.00 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.24 TONNES FROM THE GLD/////INVENTORY RESTS AT 1011.60 TONNES//

FEB 4/WITH GOLD UP $3.40 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD////INVENTORY RESTS AT 1014.84 TONNES

FEB 3/WITH GOLD DOWN $5.55: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD////INVENTORY RESTS AT 1016.59 TONNES

FEB 2/WITH GOLD UP $7.95//A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.78 TONES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1018.04 TONNES

FEB 1/WITH GOLD UP $5.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1014.26 TONNES

CLOSING INVENTORY FOR THE GLD//1061.83 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 16/WITH SILVER DOWN 56 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 462,000 OZ FROM THE SLV//INVENTORY RESTS AT 544.560 TONNES

MARCH 15/WITH SILVER DOWN 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.022 TONNES

MARCH 14/WITH SILVER DOWN 64 CENTS TODAY; STRANGE A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.125 MILLION OZ/INVENTORY RESTS AT 545.022 TONNES

MARCH 11/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 TONNES

MARCH 10/WITH SILVER UP 39 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 542.897 MILLION OZ/

MARCH 9/WITH SILVER DOWN 88 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.174 MILLION OZ OF FAKE SILVER.//INVENTORY RESTS AT 542.897 MILLION OZ//

MARCH 8/WITH SILVER UP 88 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.217 MILLION OZ INTO THE SLV////INVENTORY RESTS A 548.071 MILLION OZ//

MARCH 7/WITH SILVER UP 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 4/WITH SILVER UP 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ/

MARCH 3/WITH SILVER UP 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.32 TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 198,000 OZ FROM THE SLV//INVENTORY RESTS AT 545.854 MILLION OZ//

MARCH 1/WITH SILVER UP $1.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 546.052 MILLION OZ//

FEB 28/WITH SILVER UP 31 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 546.052 MILLION OZ//

FEB 25/WITH SILVER DOWN 64 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.510 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 546.052 MILLION OZ/

FEB 24/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ

FEB 23/WITH SILVER UP 22 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 22/WITH SILVER UP 30 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 350,000 OZ INTO THE SLV///INVENTORY RESTS AT 551.597 MILLION OZ//

FEB 18/WITH SILVER UP 7 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.017 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 551.227 MILLION OZ

FEB 17/WITH SILVER UP 31 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.402 MILLION OZ//INVENTORY RESTS AT 550.210 MILLION OZ/

FEB 16/WITH SILVER UP 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLIONOZ

FEB 15/WITH SILVER DOWN 46 CENTS TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.808 MILLION OZ//

FEB 14/WITH SILVER UP 49 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.235 MILLION OZ INTO THES LV////INVENTORY RESTS AT 547.808 MILLION OZ

FEB 11/WITH SILVER DOWN 18 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ///

SLV/FEB 10/WITH SILVER UP 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 9/WITH SILVER UP 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 8/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.143 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 544.573 MILLION OZ//

FEB 7/WITH SILVER UP 52 CENTS TODAY: A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.218 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 541.430 MILLION OZ/

FEB 4/WITH SILVER UP 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 539.212 MILION OZ

FEB 3/WITH SILVER DOWN 35 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT539.212 MILLION OZ//

FEB 2/WITH SILVER UP 15 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.411 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 539.212 MILLION OZ/

FEB 1/WITH SILVER UP 18 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 533.801 MILLION OZ

SLV FINAL INVENTORY FOR TODAY: 544.560 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

The Fed’s Feckless Inflation Fight

WEDNESDAY, MAR 16, 2022 – 08:10 AM

Authored by Michael Maharrey via SchiffGold.com,

The Fed is supposedly about to step into the ring to fight inflation. But all indications are it’s going to be a feckless fight.

Gold flirted with an all-time record high last week driven in part by safe-haven demand due to the geopolitical uncertainty caused by Russia’s invasion of Ukraine. But as the war drags on and the panic subsides, that safe-haven bid seems to be unwinding.

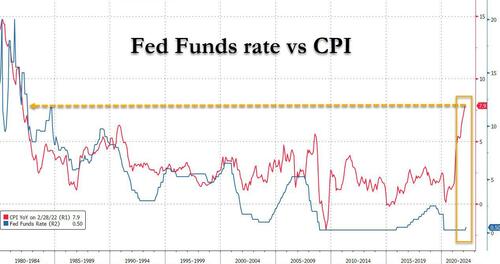

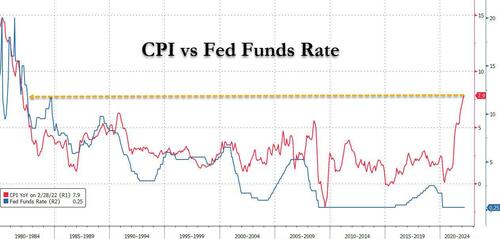

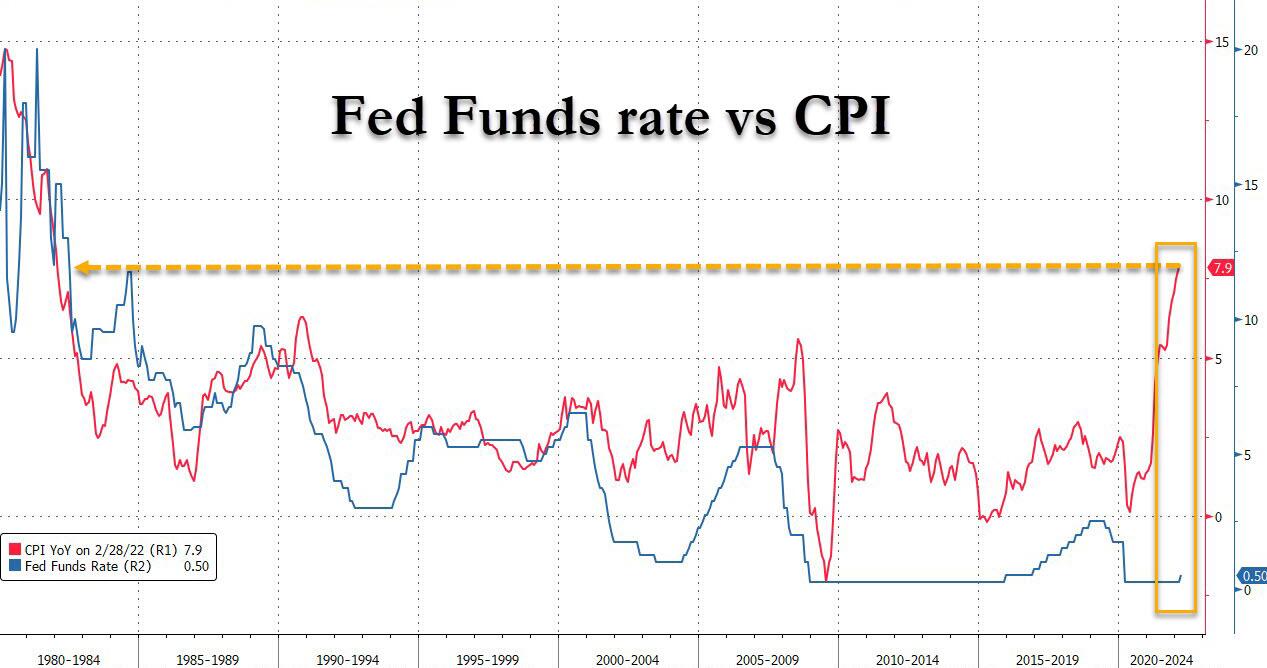

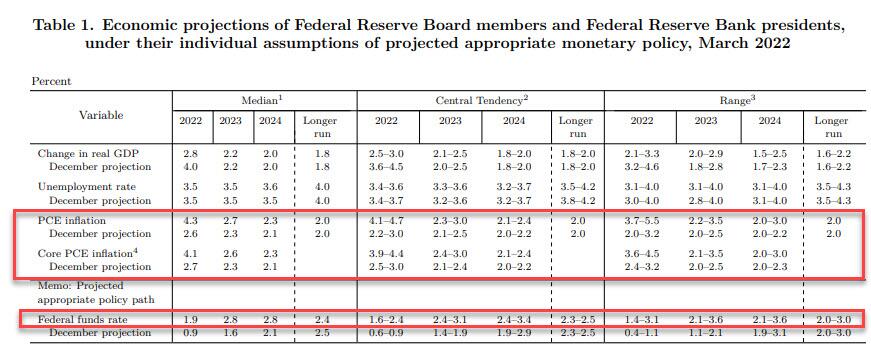

Now investors have turned their attention back to the Fed. When the war broke out, people thought it could slow the central bank’s monetary tightening plans. But with a 7.9% CPI print for February, the mainstream is back on the tightening bandwagon. They’re betting the central bank is going to tighten fast and hard, and they’re selling gold on the expectation of higher interest rates.

But even if the Fed does what the market is betting it will do, it’s not going to put a dent in inflation, and interest rates will not rise high enough to undermine gold.

According to a Reuters article:

A key money market indicator is now pricing US interest rates peaking at a higher level than previously forecast, as traders bet that the Federal Reserve will prioritize stamping out inflation over fretting about risks to economic growth.”

And just how high are they betting interest rates will rise?

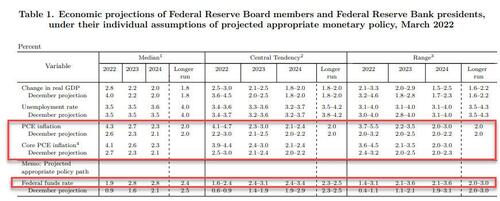

2.5%

That’s it.

They think the Fed will push interest rates to 2.5% by mid-2023.

Goldman Sachs economist Sven Jari Stehn is betting on the high side. He thinks the so-called “terminal rate” will come in between 2.75 and 3%.

This is supposed to “stamp out” 7.9% inflation. (Which is really 15-plus percent inflation is measured honestly.)

Paul Volker went to war against inflation in the early 80s. He pushed interest rates to 20%. He had to in order to get ahead of the inflation curve.

In other words, if we accept the government’s 7.9% CPI, the Fed would have to push interest rates to at least 9% to get above the inflation rate in order to “go to war” with inflation.

And they’re talking about 2.5% as if it were some kind of nuclear bomb.

The thinking here is muddled and silly.

Nevertheless, any rate hike is seen as a negative for gold. Whenever interest rates tick up slightly, the mainstream is quick to inform us that “rising interest rates increase the opportunity cost of holding gold.” This is why we’re seeing another selloff in gold as everybody gears up for the March FOMC meeting.

So, what exactly is the mainstream thinking here?

Holding gold does not generate interest income like a bond or a bank account. If interest rates rise and you’re holding gold, you’re forgoing the interest income you could earn if you instead owned a bond or put dollars in a money market account. That’s why rising interest rates tend to create headwinds for gold. And it’s why we saw gold sell off on every bit of high inflation news last year. The markets expect the Fed to fight inflation with rate hikes, thus raising the opportunity cost of holding gold.

This makes sense on the surface, but there is a problem with this mainstream analysis. They are not thinking in terms of real interest rates.

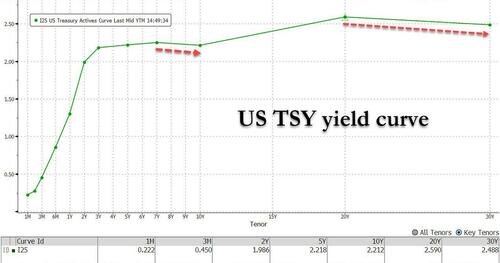

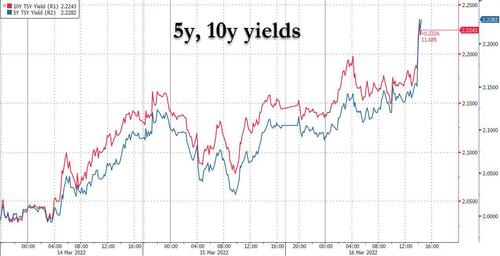

Consider the 10-year Treasury. Currently, the yield is around 2.1%. With a 7.9% inflation rate, the real interest rate on the 10-year is -5.8%.

To state the obvious, there is no “opportunity cost” in holding gold when real rates are deeply negative. You are losing real money holding bonds that aren’t yielding enough interest income to keep up with inflation.

At some point, the markets will figure this out.

It’s also highly unlikely that the Fed will ever get to 2.5%. As you’ll recall, when the Fed started tightening in earnest after the 2008 meltdown, it barely got above 2% before the economy went wobbly. The stock market tanked in the fall of 2018 and the central bank went right back to rate cuts and QE.

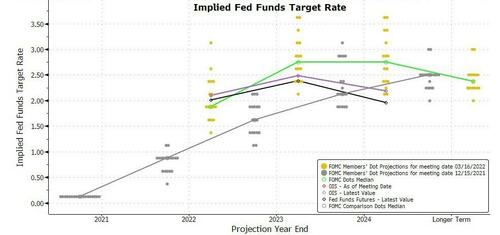

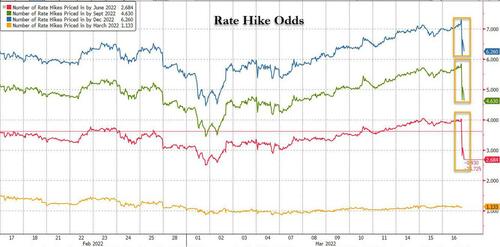

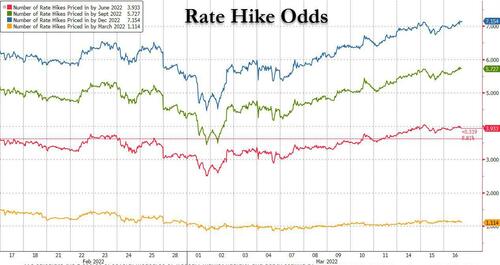

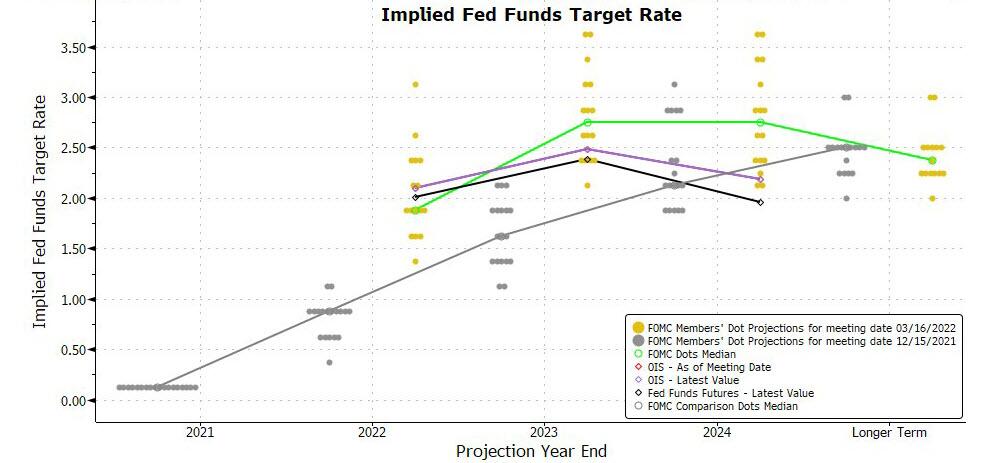

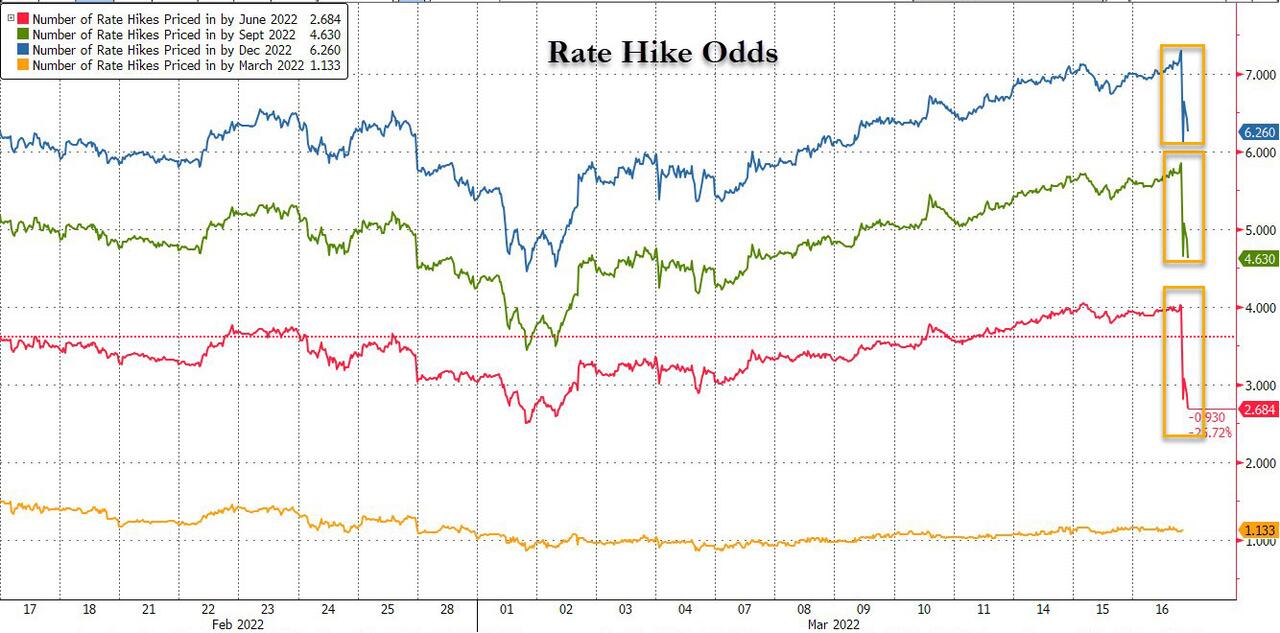

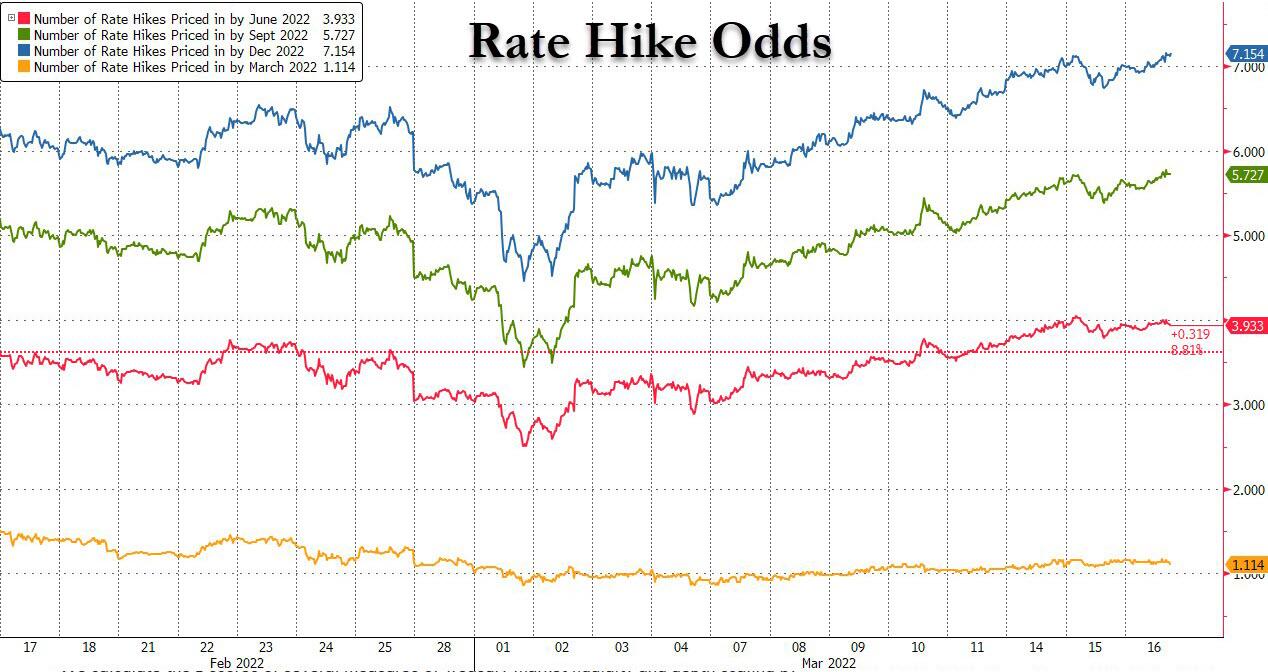

[ZH: On a side note, the market is pricing in 1 hike today, a 60% chance of a 50bps hike in May, and 7 rate-hikes in 2022…

[ZH: But, it is also pricing in rate-cuts next year and more in 2024…

Today, the bubbles are even bigger. The levels of debt are even higher. How will the Fed raise rates substantially in this environment? I think they’ll be doing good to even get to 1%.

Here’s a question to ask yourself: do you think the Fed will keep hiking rates if the markets tank and the economy slides toward recession?

[ZH: The market really does not believe The Fed will keep hiking…

Most people aren’t paying any attention to real interest rates — at least not yet. Right now, they’re distracted by negligible nominal interest rate hikes in the Fed’s feckless “war” on inflation. But this will almost certainly change soon.

The markets can remain delusional for a long time. But they can’t remain delusional forever.

END

2.LAWRIE WILLIAM//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS:

5-Count Felon JPMorgan Is at the Center of a New, Multi-Billion Dollar Trading Scandal

By Pam Martens and Russ Martens: March 15, 2022 ~

JPMorgan Chairman and CEO, Jamie Dimon, Sits in Front of Trading Monitor in his Office (Source — 60 Minutes Interview, November 10, 2019)

Traders who feel they were robbed of their profits trading nickel last week at the London Metal Exchange (LME) have taken to Twitter to verbally accuse the LME of favoring their “cronies” and behaving like “slime balls.”

Lining up as crony suspect Number 1 are units of JPMorgan Chase who, together, hold the largest number of Class B shares in the London Metal Exchange than any other member. Those units are J.P. Morgan Markets Limited with 25,000 shares; J.P. Morgan Metals Limited with 19,100 shares; and J.P. Morgan Securities with 25,000 shares for a total of 69,100 Class B shares, according to a listing of shareholders on the LME’s website.

In addition, the CEO of the Hong Kong Stock Exchanges and Clearing (HKEX), which bought the LME in 2012, is Nicolas Aguzin. He joined the HKEX last May after spending 31 years at JPMorgan. Aguzin also serves as a Board Member of the LME, where his bio notes that “from 2013 to 2020, Mr. Aguzin was CEO, J.P. Morgan, Asia Pacific where he was responsible for all the firm’s business across 17 markets.”

The reason that both the LME and JPMorgan are taking the heat from traders who say they were “robbed” of their profits, is that one of JPMorgan’s clients – the Chinese nickel and steel producer Tsingshan Holding Group – had secretly built up a massive short position in nickel, using both contracts at the LME and also over-the-counter derivative contracts with JPMorgan and other banks. When the price of nickel began to spike dramatically higher last Tuesday, the banks scurried to try to close out their short positions in nickel by buying back the contracts. That heavy buying pushed the price of nickel to a record $100,000 a metric ton and the banks could no longer afford to keep buying to close their short positions.

Bloomberg News has named JPMorgan as the largest counterparty to the Tsingshan trades while the Wall Street Journal has indicated that Standard Chartered and BNP Paribas are also involved.

It is believed that at some point last Tuesday the banks came clean with the LME as to what their total derivative exposure was and to the massive losses they would experience if the trading that occurred last Tuesday was allowed to stand. What is not in dispute is that the LME suspended trading in nickel last Tuesday and cancelled all of the thousands of trades that had occurred last Tuesday prior to the suspension of trading. The cancelled trades benefited the short positions but left other traders with profitable long positions out in the cold. (You can read all of the LME’s pronouncements about cancelled nickel trades and the like at this official link.)

In addition, to give JPMorgan and the other banks involved time to figure out a solution to their self-made mess, the LME has suspended trading in nickel since last Tuesday. Yesterday, the LME posted a notice stating that “trading in LME Nickel Contracts will resume at 08:00 [a.m.] London time on Wednesday 16 March 2022.”

As our readers might recall, it was secret derivative contracts in concentrated positions of certain stocks held by the big banks on behalf of the Archegos hedge fund last March that cost major global banks over $10 billion in losses. And yet, here we are again talking about secret derivative contracts and potentially heavy losses for banks.

Tsingshan’s controlling shareholder is Xiang Guangda, who is believed to have been behind the idea of going short billions of dollars in nickel. Yesterday, Bloomberg News reported that Guangda had “reached a deal with his banks for a standstill agreement to avoid further margin calls. During the standstill period, Xiang Guangda’s Tsingshan Group Holding Co. and its banks will continue discussions about a secured credit facility to cover the company’s nickel margin and settlement requirements….”

As we pointed out in our past reporting on Archegos, margin loans are supposed to be federally-regulated so that systemically-important banks like JPMorgan Chase don’t blow themselves up and leave the taxpayer on the hook for a bailout. We emailed the Financial Conduct Authority (FCA) in the U.K., which oversees the LME, as well as the U.S. Commodity Futures Trading Commission (CFTC) that oversees commodity trading at JPMorgan, to see if they were involved in providing oversight to this dangerous mess. The FCA responded promptly, and in a typical fashion, the CFTC remained silent.

The FCA said this:

“As a regulated investment exchange, the London Metal Exchange (LME) is responsible for the maintenance of fair and orderly markets. Together with the Bank of England, we have been engaging with LME’s exchange and clearing house, as well as other market participants, on an orderly resumption of the market in nickel.”

The FCA statement might give us some comfort were it not for the fact that the biggest bank involved in this mess – JPMorgan Chase – has admitted to five criminal felony counts brought by the U.S. Department of Justice since 2014. The man at the helm of the bank as its Chairman and CEO throughout that crime spree, Jamie Dimon, was not only allowed to keep his job but was handed a $50 million bonus by the bank’s Board of Directors.

Three of the felony counts involved the rigging of markets: one felony count the bank admitted to in 2015 was for its role in rigging foreign exchange trading. On September 29, 2020, the Justice Department charged JPMorgan Chase with two more felony counts involving rigged trading, to which it admitted, and fined the bank $920 million of shareholders’ money. One count was for rigging the precious metals market and the other was for rigging trading in U.S. Treasury securities.

And this is not the first time that megabanks on Wall Street have come under scrutiny for crony conduct at the London Metal Exchange and playing an improper role in physical commodity markets. The U.S. Senate’s Permanent Subcommittee on Investigations conducted a two-year investigation and released a stunning 396-page bipartisan report in 2014.

Findings from the report include the following regarding JPMorgan:

“The Subcommittee report details how JPMorgan amassed physical commodity holdings equal to nearly 12 percent of its Tier 1 capital, while telling regulators its holdings were far smaller; and that at one point it owned an amount equal to more than half the aluminum used in North America in a year.”

That JPMorgan is at the center of yet another trading scandal is an indictment of Congress and federal regulators to meaningfully reform Wall Street

-END-

Why Gold Will Rise — The Financial System Has Changed

Matthew Piepenburg

March 16, 2022

Despite massive price volatility of late, gold will rise.

The Perfect Gold Storm

Not long ago, I wrote a piece on why gold was not rising.

As I said then, and will repeat again now, gold’s then-yawning price moves in an otherwise ideal inflationary and negative real rate environment was just a momentary calm before the storm.

In other words, gold’s rise –and perfect storm–was coming.

Well, that storm is gathering strength and gold will rise—but not in a straight line.

Despite inevitable (and extreme) volatility (war and inflation-driven) and legalized price fixing (including $100 intra-day price moves) from the increasingly discredited paper COMEX markets, gold will keep rising as CPI inflation hits 7.9%.

Nearer term, gold’s price will gyrate depending on whether tensions in the Ukraine escalate or de-escalate.

But as we discuss below, Western financial responses to the crisis in the Ukraine have just changed the global system—yet no one noticed. Longer-term, this bodes extremely well for gold and its potential to rise.

But First: A Nod to Goldman’s Jeff Currie

Although it’s easy to poke fun at Goldman Sachs (as I’ve done in the past, apologies to my daughter), I am pleased to confess that Jeff Currie, Goldman’s Global Head of Commodities Research, has correctly addressed what he calls “the perfect storm for gold.”

That is, a near-perfect convergence of three key gold demand forces (or “weather fronts”) are in now in motion.

The first of these weather fronts is the growing (and inflation/recession fear-based) retail investor demand for gold. ETF trade volume is ripping north and poised to increase by another 600 tones.

The next weather front is coming from central bank gold buying, which is already up 750 tones for the year and marking an all-time record.

China and Turkey, for example, are buying gold in a not-so-surprising move to de-dollarize (see below) as other nations, like Brazil and India, are buying gold to diversify.

The third and final weather front is the spiking demand for physical gold, lead primarily by China and India—and let’s not forget Russia, whatever you may think of it…

All three gold channels (retail, central bank and physical markets) are objectively the strongest they have ever been, stronger even than in 2010-2011 when gold rallied by 70%.

Goldman’s price target for gold is now $2500—a substantial rise.

We think it will go much higher…

Why?

Because regardless of what you think of Putin, Russia, the absolute horrors of war, the confusion of headlines or the wisdom of the West, the EU and Uncle Sam just shot themselves and the global financial system in its collective foot—and no one even seemed to notice.

Weaponized Finance—Be Careful of the Safety Trigger

Despite the fact that Putin had been warning the West for eight years to keep the Ukraine out of NATO with the same passion that Kennedy had warned the Soviets to keep missiles out of Cuba, the West somehow seemed shocked that “brilliant statesmen” like Kamala Harris could not outthink Putin.

Despite nearly every U.S. State Dept official since the late 90’s warning that a Ukraine in NATO would be suicide, the West is feigning shock today.

Rather than diplomatically addressing the Ukraine NATO alliance (which is about as obsolete in the post-Stalin era as a rotary dial phone), the Vice President (chosen for optics rather than experience) landed in Europe and doubled-down on a bad NATO hand (as well as embarrassing grasp of European geography).

War rather than compromise quickly followed.

But unlike Iraq, Syria, Libya or even Afghanistan (where US doubling down has been an epic failure), the great minds of the West decided to play chicken with a nuclear power, which, well complicates things, no?

Given that conventional proxy wars aren’t so easy when dealing with a nuclear adversary, the West’s only viable option once the inevitable (Putin-pre-warned) invasion of the Ukraine occurred, was to weaponize finance rather than flirt with nuclear red buttons.

But as anyone familiar with weapons knows, once you unlock the safety trigger, unforeseen risks emerge.

And unbeknownst to almost everyone ingesting the main stream media’s daily pablum, the financial weapons unleashed by the West have dangerous consequences.

In fact, and while most of us weren’t looking, the entire financial system of the last 4 decades (i.e., globalization, an artificial bond bull market and manipulated disinflation) just died, soon to be replaced by a multi-polar and multi-currency new inflationary world—all of which point toward a notable rise in gold price.

How did this happen?

Well, let’s ignore the politicians, the COMEX and standard headlines and examine cold reality.

The Catalyst No One Sees

As the holder of the global reserve currency and the almighty USD, Washington has been able to export inflation and bully little guys like Iran and Venezuela with all kinds of clever financial sanctions with relative impunity/effect for years.

But when you start poking at Russian (and indirectly, Chinese) tails by freezing FX reserves, you unleash a world of mess and a domino chain of unintended (but obvious) consequences which are far too complex for the 30-something financial journalists at the NYT or CNN to grasp.

Recently, and with all the chest-puffing of bringing a knife to a gun fight, the US and EU bravely announced that sovereign debt held as FX reserves outside one’s own national borders ($7-8T) is now subject to seizure by Uncle Sam and Aunt Marianne (i.e., the EU).

Such bold financial saber rattling is impressive; but by totally discrediting sovereign debt as an FX reserve, the US and EU have effectively just announced to Russia (and the world) that they are killing the post-war financial system—which also means you should buy more gold…

Such grossly misunderstood moves by the West are now forcing Russia (and soon China) to do what they’ve already been advocating for the last decade, namely forcing the global financial system toward a reserve neutral asset (gold) that floats in price in all currencies.

After all, if the West can freeze Russian FX reserves (i.e., its accumulated trade savings) today, China now clearly knows the West can and will do the same to them tomorrow if they, for example, look sideways at Taiwan…

An no, this doesn’t make me “Pro-Putin” or “Pro-China,” just pro candor.

Even if the horrific war in the Ukraine de-escalates, the extreme financial moves made by the West since late February will never be forgotten. That genie can’t be put back into the bottle.

Even the Swiss decision to abandon centuries of neutrality by joining “woke” (i.e., US-pressured) sanctions against Russia is the equivalent of a placing a massive, neon flashing sign atop the Matterhorn which reads: “Don’t buy CHF, Buy Gold.”

In short, the financial world has now changed, and there’s no turning back.

Let’s see why.

De-Dollarization Coming Full Circle to Bite the West

Russia, and soon China, must now turn to SWIFT alternatives which will not only alter the global payment systems, but undermine the USD’s global reserve status, which, well, kinda matters…

This is not just my/our humble opinion, but warned as well by Citadel’s chief executive and JP Morgan’s Jamie Dimon.

That is, the West has just forced Russia even further into the arms of China in more ways than one.

Rather than look toward northern California for software solutions, for example, Russia will look toward China.

But as Dimon warned, there are far greater consequences ahead as the USD becomes less “global” less of a “reserve” and less of a “currency.”

Dimon’s concerns, moreover were shared by President’s Biden’s former boss in August of 2015, when President Obama accurately warned of the “unintended consequences” of a SWIFT/financial war:

“We cannot dictate the foreign, economic and energy policies of every major power in the world. In order to even try to do that, we would have to sanction, for example, some of the world’s largest banks. We’d have to cut off countries like China from the American financial system.

And since they happen to be major purchasers of our debt, such actions could trigger severe disruptions in our own economy, and, by the way, raise questions internationally about the dollar’s role as the world’s reserve currency. That’s part of the reason why many of the previous unilateral sanctions were waived.”

In short, somewhere between 2015 and today, American common sense, leadership and options took a nose dive.

What’s also about to take a nose dive is the American economy in general and markets in particular.

Do you want to see why?

The FED—No Where to Go but Crazy

Dramatic words are not enough, so let’s stick to dramatic facts and a quick glance at a simple graph of the Fed’s embarrassing balance sheet…

Although the media and headlines ignored the staggering repo crisis of September of 2019 as a minor “glitch in the plumbing,” it was, in fact, a neon flashing sign of a looming/brewing credit and (hence) financial crisis.

When US commercial banks in the autumn of 2019 were staring down the barrel of a rising USD and rising (i.e., unaffordable) interest rates, they stopped trusting each other’s collateral to make over-night loans.

As expected, the Fed stepped in as the lender of last resort and began mouse-clicking hundreds of billions of dollars out of thin air per month to backstop the bank(er)s who created the Fed back in 1913.

Such money printing explains the parabolic (and fatal) move up and to the right of the balance sheet plotted above.

That is, the Fed had to create money to buy its own Treasuries which foreign buyers no longer wanted.

But what almost no one is noticing today is that the problem’s facing the Fed and Uncle Sam’s otherwise unloved and unwanted IOUs in 2019 have only been made exponentially worse.

That is, the recent actions by the US and EU to Freeze Russian FX reserves for not towing the Western line is telegraphing to the rest of the world (i.e., China) not to trust US Treasuries.

Needless to say, if US Treasuries are now the ugliest girl at the global dance, who else is gonna buy them, and with what money?

The sad answer is simple: The Fed will buy them with more debased dollars created out of thin air.

Crazy?

Yep.

Recession and Leverage Ahead—Will Gold Rise?

Given the sad yet media-ignored fact that the US (with a debt to GDP ratio of 122%) is effectively broke yet spending like a teenager with Dad’s Amex card (nod to my son), the future, as well as policies ahead, are not hard to see.

It’s worth asking how US spending for entitlements, defense and treasury outlays will be paid for.

In short: Where will the money come from?

Will Uncle Sam cut spending?

Given that US spending accounts for 25% of its GDP, any spending cuts will put the US in recession for the simple reason that such cuts will send yields and rates up and hence bonds and stocks to the basement.

Can the US raise taxes? This too would only slow growth and invite recession.

Can the Fed raise rates to finance Uncle Sam’s deficits?

No, because his bar tab is too high to stomach rising rates, and that too triggers a recession and a debt crisis.

So, what can Uncle Sam do?

As realists rather than paid (i.e., censored) journalists, we here see only one or two obvious yet sad options ahead, all of which make an equally obvious case for a rise in gold.

First, it’s highly likely that the Fed will suspend SLR (Supplementary Leverage Ratios) previously imposed on commercial banks.

In plain English, this just means banks will be allowed to use more leverage to buy Uncle Sam’s debt from within at no charge.

No shocker there.

As we’ve written elsewhere, governmental guarantees of commercial bank lending are already in play –and this just means more leverage, more debt, more risk and more autocratic rather than natural markets.

In addition, expect more QE as well, which means the inherent value (as opposed to relative strength) of the USD, like all other fiat currencies, is getting weaker by each inflationary second, minute and hour.

Got gold?

LAWRIE WILLIAMS:

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

We brought this major story to you yesterday but it is worth repeating. Saudi Arabia, angry at Biden is considering accepting yuan

instead of dollars for Chinese oil sales. That will defacto end the USA Petrodollar scheme

(Wall Street Journal/GATA)

Saudi Arabia considers accepting yuan instead of dollars for Chinese oil sales

Submitted by admin on Tue, 2022-03-15 10:08Section: Daily Dispatches

By Summer Said and Stephen Kalin

The Wall Street Journal

Tuesday, March 15, 2022

Saudi Arabia is in active talks with Beijing to price its some of its oil sales to China in yuan, people familiar with the matter said, a move that would dent the U.S. dollar’s dominance of the global petroleum market and mark another shift by the world’s top crude exporter toward Asia.

The talks with China over yuan-priced oil contracts have been off and on for six years but have accelerated this year as the Saudis have grown increasingly unhappy with decades-old U.S. security commitments to defend the kingdom, the people said.

The Saudis are angry over the U.S.’s lack of support for their intervention in the Yemen civil war and over the Biden administration’s attempt to strike a deal with Iran over its nuclear program. Saudi officials have said they were shocked by the precipitous U.S. withdrawal from Afghanistan last year.

China buys more than 25% of the oil that Saudi Arabia exports. If priced in yuan, those sales would boost the standing of China’s currency.

END

Ed Steer discusses the default that occurred in nickel on the London Metals Exchange

(Ed Steer/GATA)

GATA’s Steer discusses default in London Metals Exchange nickel contract

Submitted by admin on Tue, 2022-03-15 16:01Section: Daily Dispatches

4p ET Tuesday, March 15, 2022

Dear Friend of GATA and Gold:

GATA board member Ed Steer, interviewed by Jim Goddard for “This Week in Money” at HoweStreet.com, discusses the default of the nickel contract on the London Metals Exchange, as well as the action in the monetary metals. The interview starts at the 10:35 mark at HoweStreet.com here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke goes over what I have been describing over the last three years: how spread trades/TAS are knocking gold down ahead of options expiry

(Craig Hemke/GATA)

Craig Hemke: How ‘spread’ trades are used to knock gold down ahead of option expiration

Submitted by admin on Tue, 2022-03-15 16:17Section: Daily Dispatches

4:25p ET Tuesday, March 15, 2022

Dear Friend of GATA and Gold:

The TF Metals Report’s Craig Hemke, writing today at Sprott Money, details how the “trade at settlement” mechanism appears to be heavily used by “spread” traders to knock the gold price down ahead of option expirations and contract rolls, as has just happened, to discourage traders from taking delivery of actual metal.

Hemke surmises that a similarly engineered smash will be unleashed around March 28.

His analysis is headlined “Updating Comex Gold Trade at Settlement” and it’s posted at Sprott MOney here:

https://www.sprottmoney.com/blog/Updating-COMEX-Gold-Trade-at-Settlement-March-15-2022

Today’s edition of Thom Calandra’s “The Calandra Report” quotes your secretary/treasurer about today’s odd rise in gold mining shares despite another day of pummeling to gold futures prices:

“‘I imagine it’s because the bullion banks executing government short trades in the gold and silver futures markets knew that today would be the last day of the big attack and they could make some quick money buying gold and silver mining shares at the bottom,’ he says from New England just now.

“‘Of course I’m a ‘conspiracy theorist’ who foolishly believes that government does things in secret and that there is some innocent if unknown reason why I’m not allowed to observe the trading rooms at the Federal Reserve Bank of New York and the Bank for International Settlements in Basel,’ he says.”

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Another major story tonight. Russian Central bank suspends the buying of gold from banks allowing citizens to mop up the gold. It also means that Russia has accumulated enough gold for itself

Probably 2 to 3 times its official status of 2300 tonnes.

(Reuters)

Russian central bank leaves banking system’s gold for household demand

Submitted by admin on Tue, 2022-03-15 21:27Section: Daily Dispatches

From Reuters

Tuesday, March 15, 2022

The Russian central bank said it will suspend the buying of gold from banks from today to meet increased demand for the precious metal from households, its latest attempt to weather the storm on Russian markets in the face of Western sanctions.

he central bank raised the key rate to 20% from 9.5% on Feb. 28 as the rouble crashed to record lows and people rushed to withdraw money from banks after the West imposed unprecedented sanctions against Russia for what the Kremlin calls a “special operation” to disarm Ukraine. …

… For the remainder of the report:

END

4.OTHER GOLD/SILVER COMMENTARIES

huge story!!Putin has acquired sufficient gold for himself. How he wants his citizens to buy gold

(INTERFAX)

Russian Central Bank suspends purchasing gold from banks in order to meet population’s demand for it

MOSCOW. March 15 (Interfax) – The Central Bank of Russia (CBR) as of March 15, 2022, has suspended purchasing gold from credit institutions in order to create conditions to meet demand of the population, the regulator said in a statement.

“Demand on the part of the population for purchasing physical gold bullion has currently increased owing particularly to the removal of VAT on these transactions,” the CBR noted.

The CBR resumed purchasing gold on the domestic precious-metals market on February 28, 2022, nearly two years after having suspended the operations on April 1, 2020.

The CBR has been purchasing gold since 2014, and has been a leader among global central banks in terms of purchases.

end

(ZERO HEDGE/SAME STORY AS ABOVE)

So Many Russians Are Buying Gold That Central Bank Halts Bank Purchases

TUESDAY, MAR 15, 2022 – 11:00 PM

Russia’s central bank announced that it will suspend purchases of gold from banks due to overwhelming demand from households, Reuters reports. The purchasing pause will take effect Tuesday with no end date set.

“Currently, households’ demand for buying physical gold in bars has increased, driven, in particular, by the abolition of value-added tax on these operations,” reads a statement from the central bank.

On Feb. 28, the central bank raised the key rate from 9.5% to 20% as the ruble crashed to record lows amid the Kremlin’s so-called “special operation” in Ukraine. The announcement is a flip-flop from a February announcement that the financial authority would resume gold purchases after commercial banks were hit with Western sanctions in response to the invasion.

“With the goal of diversifying the central bank’s reserves, at the moment there is no sense in building up reserves in gold,” according to VTB analysts, who added that the banking sector’s structural liquidity deficit had contracted to under 4 trillion rubles (US$36 billion), down from a record 7 trillion rubles.

Before the rush into gold, many wealthy Russians had been purchasing luxury items such as watches and other jewelry in order to defend against the ruble’s tumble. While cryptos were also purchased aggressively, there is little insight into who much bitcoin Russians currently own.

Analysts from BCS suggested that the gold purchases will help reduce the amount of cash in circulation, and will help banks’ liquidity.

In lieu of funding via gold purchases, Russia’s central bank has been providing liquidity to banks through more conventional operations such as holding daily repo auctions at lending institutions. So far, these have proven sufficient.

end

THE CRADLE

A VERY IMPORTANT READ…

Say hello to Russian gold and Chinese petroyuan

The Russia-led Eurasian Economic Union and China just agreed to design the mechanism for an independent financial and monetary system that would bypass dollar transactions.

By Pepe Escobar

March 15 2022

Russia says half its gold assets were frozen – is this for real or a slick play by Moscow?

Photo Credit: The Cradle

It was a long time coming, but finally some key lineaments of the multipolar world’s new foundations are being revealed.

On Friday, after a videoconference meeting, the Eurasian Economic Union (EAEU) and China agreed to design the mechanism for an independent international monetary and financial system. The EAEU consists of Russia, Kazakhstan, Kyrgyzstan, Belarus and Armenia, is establishing free trade deals with other Eurasian nations, and is progressively interconnecting with the Chinese Belt and Road Initiative (BRI).

For all practical purposes, the idea comes from Sergei Glazyev, Russia’s foremost independent economist, a former adviser to President Vladimir Putin and the Minister for Integration and Macroeconomics of the Eurasia Economic Commission, the regulatory body of the EAEU.

Glazyev’s central role in devising the new Russian and Eurasian economic/financial strategy has been examined here. He saw the western financial squeeze on Moscow coming light-years before others.

Quite diplomatically, Glazyev attributed the fruition of the idea to “the common challenges and risks associated with the global economic slowdown and restrictive measures against the EAEU states and China.”

Translation: as China is as much a Eurasian power as Russia, they need to coordinate their strategies to bypass the US unipolar system.

The Eurasian system will be based on “a new international currency,” most probably with the yuan as reference, calculated as an index of the national currencies of the participating countries, as well as commodity prices. The first draft will be already discussed by the end of the month.

The Eurasian system is bound to become a serious alternative to the US dollar, as the EAEU may attract not only nations that have joined BRI (Kazakhstan, for instance, is a member of both) but also the leading players in the Shanghai Cooperation Organization (SCO) as well as ASEAN. West Asian actors – Iran, Iraq, Syria, Lebanon – will be inevitably interested.

In the medium to long term, the spread of the new system will translate into the weakening of the Bretton Woods system, which even serious US market players/strategists admit is rotten from the inside. The US dollar and imperial hegemony are facing stormy seas.

Show me that frozen gold

Meanwhile, Russia has a serious problem to tackle. This past weekend, Finance Minister Anton Siluanov confirmed that half of Russia’s gold and foreign reserves have been frozen by unilateral sanctions. It boggles the mind that Russian financial experts have placed a great deal of the nation’s wealth where it can be easily accessed – and even confiscated – by the “Empire of Lies” (copyright Putin).

At first it was not exactly clear what Siluanov had meant. How could the Central Bank’s Elvira Nabiulina and her team let half of foreign reserves and even gold be stored in Western banks and/or vaults? Or is this some sneaky diversionist tactic by Siluanov?

No one is better equipped to answer these questions than the inestimable Michael Hudson, author of the recent revised edition of Super Imperialism: The Economic Strategy of the American Empire.

Hudson was quite frank: “When I first heard the word ‘frozen,’ I thought that this meant that Russia was not going to expend its precious gold reserves on supporting the ruble, trying to fight against a Soros-style raid from the west. But now the word ‘frozen’ seems to have meant that Russia had sent it abroad, outside of its control.”

Essentially, it’s all still up in the air: “My first reading assumed that Russia must be doing something smart. If it was smart to move gold abroad, perhaps it was doing what other central banks do: ‘lend” it to speculators, for an interest payment or fee. Until Russia tells the world where its gold was put, and why, we can’t fathom it. Was it in the Bank of England – even after England confiscated Venezuela’s gold? Was it in the New York Fed – even after the Fed confiscated Afghanistan’s reserves?”

So far, there has been no extra clarification either from Siluanov or Nabiulina. Scenarios swirl about a string of deportations to northern Siberia for national treason. Hudson adds important elements to the puzzle:

“If [the reserves] are frozen, why is Russia paying interest on its foreign debt falling due? It can direct the “freezer’ to pay, to shift the blame for default. It can talk about Chase Manhattan’s freezing of Iran’s bank account from which Iran sought to pay interest on its dollar-denominated debt. It can insist that any payments by NATO countries be settled in advance by physical gold. Or it can land paratroopers on the Bank of England, and recover gold – sort of like Goldfinger at Fort Knox. What is important is for Russia to explain what happened and how it was attacked, as a warning to other countries.”

As a clincher, Hudson could not but wink at Glazyev: “Maybe Russia should appoint a non-pro-westerner at the Central Bank.”

The petrodollar game-changer

It’s tempting to read into Russian Foreign Minister Sergey Lavrov’s words at the diplomatic summit in Antalya last Thursday a veiled admission that Moscow may not have been totally prepared for the heavy financial artillery deployed by the Americans:

“We will solve the problem – and the solution will be to no longer depend on our western partners, be it governments or companies that are acting as tools of western political aggression against Russia instead of pursuing the interests of their businesses. We will make sure that we never again find ourselves in a similar situation and that neither some Uncle Sam nor anybody else can make decisions aimed at destroying our economy. We will find a way to eliminate this dependence. We should have done it long ago.”

So, “long ago” starts now. And one of its planks will be the Eurasian financial system. Meanwhile, “the market” (as in, the American speculative casino) has “judged” (according to its self-made oracles) that Russian gold reserves – the ones that stayed in Russia – cannot support the ruble.

That’s not the issue – on several levels. The self-made oracles, brainwashed for decades, believe that the Hegemon dictates what “the market” does. That’s mere propaganda. The crucial fact is that in the new, emerging paradigm, NATO nations amount to at best 15 percent of the world’s population. Russia won’t be forced to practice autarky because it does not need to: most of the world – as we’ve seen represented in the hefty non-sanctioning nation list – is ready to do business with Moscow.

Iran has shown how to do it. Persian Gulf traders confirmed to The Cradle that Iran is selling no less than 3 million barrels of oil a day even now, with no signed JCPOA (Joint Comprehensive Plan of Action agreement, currently under negotiation in Vienna). Oil is relabeled, smuggled, and transferred from tankers in the dead of night.

Another example: the Indian Oil Corporation (IOC), a huge refiner, just bought 3 million barrels of Russian Urals from trader Vitol for delivery in May. There are no sanctions on Russian oil – at least not yet.

Washington’s reductionist, Mackinderesque plan is to manipulate Ukraine as a disposable pawn to go scorched-earth on Russia, and then hit China. Essentially, divide-and-rule to smash not only one but two peer competitors in Eurasia who are advancing in lockstep as comprehensive strategic partners.

All the blather about “crashing Russian markets,” ending foreign investment, destroying the ruble, a “full trade embargo,” expelling Russia from “the community of nations,” and so forth –that’s for the zombified galleries. Iran has been dealing with the same thing for four decades, and survived.

Historical poetic justice, as Lavrov intimated, now happens to rule that Russia and Iran are about to sign a very important agreement, which may likely be an equivalent of the Iran-China strategic partnership. The three main nodes of Eurasia integration are perfecting their interaction on the go, and sooner rather than later, may be utilizing a new, independent monetary and financial system.

But there’s more poetic justice on the way, revolving around the ultimate game-changer. And it came much sooner than we all thought.

Saudi Arabia is considering accepting Chinese yuan – and not US dollars – for selling oil to China. Translation: Beijing told Riyadh this is the new groove. The end of the petrodollar is at hand – and that is the certified nail in the coffin of the indispensable Hegemon.

Meanwhile, there’s a mystery to be solved: where is that frozen Russian gold?

5.OTHER COMMODITIES/

end

NICKEL UPDATE

LME reopens at the lower limit and then proceeds even below the limits which should not have happened. The exchange was halted and trades cancelled

still a mess

(zerohedge)

LME Re-Opens Nickel Trading; Quickly Halts Again On Limit-Down Band “System Error”

WEDNESDAY, MAR 16, 2022 – 07:28 AM

Update (0650ET): “What a debacle,” said Ole Hansen, head of commodities strategy at Saxo Bank A/s. “The LME is not doing itself any favors.”

After reopening the LME for nickel trading this morning, following the bailout of Chinese commodity tycoon Xiang Guangda, the Chinese-owned (HKEX) exchange was forced to suspend trading soon after the open due to a “system error” which had led to some trades to be executed below the new price limits laid out by the exchange.

As Bloomberg reports, only 206 lots, or 1,236 tons of nickel, changed hands before the market stopped trading within seconds on Wednesday morning. Most of those trades took place at the limit price of $45,590 a ton. Several trades appeared to be at prices below the 5% limit.

“In some sense it went as expected, in that we all expected it to fall, but it was just a question of how quickly,” Colin Hamilton, managing director for commodities research at BMO Capital Markets, said by phone from London.

The LME introduced price limits before reopening today to prevent a repeat of the chaos last Tuesday, when it suspended trading as prices roared to record highs above $100,000 a tonne. In a statement the exchange said:

“As the market opened, the uncrossing algorithm discovered an opening price of $45,590 (which was the lower daily price limit, i.e. 5% below the prices published in Notice 22/067) for 3-month Nickel.

“Unfortunately due to a systems error, LMEselect then allowed a small number of trades to be executed below this lower daily price limit.

“The LME immediately decided to suspend Nickel trading on LMEselect while the system error is investigated.”

The LME said that all nickel trades executed at the lower price on LMEselect, its trading system, would now be cancelled.

This ‘cancellation’ decision follows the highly controversial move from the LME to cancel $3.9bn worth of trades last Tuesday as the market surged.

* * *

As Emel Khan detailed for The Epoch Times earlier, Nickel trading resumed on the London Metal Exchange (LME) on March 16 after being suspended for more than a week.

The exchange took an unprecedented step to halt trading in the nickel market on March 8 after a Chinese metal tycoon faced billions of dollars in losses due a large short position.

Last week, nickel’s price skyrocketed, crossing the $100,000-a-ton mark for the first time. This was a big spike compared to the prices that averaged $24,016 per metric ton in February. The extreme volatility forced the LME to suspend trading for the first time since 1988.

The base metal is an increasingly important component in the production of next-generation electric vehicle batteries for companies like Tesla. Advocates of green energy push see rising nickel prices as a threat to President Joe Biden’s climate agenda.

To avoid large swings in price, the exchange also announced that it would apply daily upper and lower price limits.

The huge spike in nickel price last week was mainly driven by a short squeeze centered on Chinese tycoon Xiang Guangda, founder of Tsingshan Holding Group, one of the world’s biggest nickel and stainless steel producers.

Nicknamed “Big Shot” in China, Xiang is known for having confidence in making huge bets, according to Bloomberg. He believes that the prices of nickel would fall due to a dramatic increase in supplies. Many hedge fund managers, however, don’t share the same view.

When nickel’s trading price surged dramatically last week, Tsingshan struggled to pay margin calls, putting its creditors in a difficult position. The price rise was further fueled as brokers and bankers of Tsingshan rushed to buy back nickel contracts to stem losses. The exchange stopped nickel trading after several small brokers claimed that they would default if prices remained at record levels, according to a Wall Street Journal article.