April 28, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

April 28, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1890.20 UP $2.35

SILVER: $23.16 DOWN $0.21

ACCESS MARKET: GOLD $1894.30

SILVER: $23.15

Bitcoin morning price: $39,663 UP 788

Bitcoin: afternoon price: $40,064 UP 1189

Platinum price: closing UP $1.95 to $924.75

Palladium price; closing UP $118.05 at $2227.35

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 464/559

EXCHANGE: COMEX

CONTRACT: APRIL 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,885.900000000 USD

INTENT DATE: 04/27/2022 DELIVERY DATE: 04/29/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 334

132 C SG AMERICAS 1

159 C ED&F MAN CAP 1

624 H BOFA SECURITIES 1

661 C JP MORGAN 464

685 C RJ OBRIEN 1

880 H CITIGROUP 225

991 H CME 91

TOTAL: 559 559

MONTH TO DATE: 27,437

NUMBER OF NOTICES FILED TODAY FOR APRIL. CONTRACT 559 NOTICE(S) FOR 55,900 OZ (1.7387 TONNES)

total notices so far: 27,437 contracts for 2,743,700. oz (85.340 tonnes)

SILVER NOTICES:

1 NOTICE(S) FILED 5,000 OZ/

total number of notices filed so far this month 1361 : for 6,805,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $2.35

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 3.77 TONNES FORM THE GLD/

INVENTORY RESTS AT 1095.72 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 23 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: HUGE CHANGES MIL AT THE SLV//

A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.725 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 6298 CONTRACTS TO 139,240 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR SMALL $0.04 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.04) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A STRONG LOSS OF 5798 CONTRACTS ON OUR TWO EXCHANGES. WITH ALL OF THE LOSS WAS DUE TO CONTINUAL SPREADER LIQUIDATION//TAS IN SILVER TODAY.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 4.305 MILLION OZ FOLLOWED BY TODAY’S QUEUE. JUMP OF 135,000 OZ//NEW STANDING: 6.940,000 MILLION OZ// V) STRONG SIZED COMEX OI LOSS/(ALL OF THE LOSS DUE TO SPREADERS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-3789

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 19 days, total 21,654 contracts: 108.270 million oz OR 5.68 MILLION OZ PER DAY. (1139 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 21,654 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 108.270 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 108.270 MILLION OZ (LOOKS LIKE OUR BANKERS ARE NOW LOATHE TO ISSUE EFP’S)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6298 WITH OUR $0.04 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY., WITH ALL OF THE LOSS DUE TO SILVER SPREADER LIQUIDATION TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 6916 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAR. OF 4.305 MILLION OZ FOLLOWED BY TODAY’S 135,00 OZ QUEUE JUMP//NEW STANDING: 6.940MILLION OZ/// .. WE HAD A GIGANTIC SIZED LOSS OF 5798 OI CONTRACTS ON THE TWO EXCHANGES FOR 28.99 MILLION OZ ACCOMPANYING THE TINY LOSS IN PRICE.

WE HAD 1 NOTICES FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2291 CONTRACTS TO 555,494 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE CROOKS USED TAS CONTRACTS TO RAID GOLD YESTERDAY

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -6140 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $15.35//COMEX GOLD TRADING/WEDNESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 78.33 TONNES ON FIRST DAY NOTICE //FOLLOWED BY TODAY’S QUEUE JUMP OF 22,300 OZ//NEW STANDING 85.340 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $15.35 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 4625 OI CONTRACTS (14,38 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4625 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 555,494.

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4625, WITH 2291 CONTRACTS DECREASED AT THE COMEX AND 6916 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4625 CONTRACTS OR 14.38 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6916) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2291,): TOTAL GAIN IN THE TWO EXCHANGES 4625CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) HUGE INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 78.33 TONNES FOLLOWED BY TODAY’S 22,300 OZ QUEUE JUMP //NEW STANDING 85.340 TONNES/// 3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

53,288 CONTRACTS OR 5,328,800 OR 165.74 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 2804 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES: 165.74 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 165.74/3550 x 100% TONNES 4.64% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 165.74 TONNES (THIS IS GOING TO BE A LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A VERY STRONG SIZED 6298 CONTRACT OI TO 139,240 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 500 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 6298 CONTRACTS AND ADD TO THE 500 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF 5798 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 28.99 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.04 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 17.20 PTS OR 0.58% //Hang Sang CLOSED UP 329.81 OR 1.65% /The Nikkei closed UP 461.27 PTS OR 1.75% //Australia’s all ordinaires CLOSED UP 1.26% /Chinese yuan (ONSHORE) closed DOWN 6.6146 /Oil DOWN TO 101.63 dollars per barrel for WTI and DOWN TO 104.65 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6146 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6536: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2291 CONTRACTS TO 555,494 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $15.35 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2844 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF APRIL.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6916 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :6916 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6916 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 4625 CONTRACTS IN THAT 6916 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2291 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF GOLD $15.35.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR APRIL (85.340),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $15.30) BUT WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A VERY STRONG SIZED GAIN OF 33.483 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR APRIL (85.340 TONNES)…

WE HAD 6140 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4625 CONTRACTS OR 462,500 OZ OR 14.38TONNES

Estimated gold volume today: 163,968/// very poor

Confirmed volume yesterday:191,577contracts poor

INITIAL STANDINGS FOR APRIL ’22 COMEX GOLD //APRIL 28

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | nil oz |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 559 notice(s)55,900 OZ 1.7387 TONNES |

| No of oz to be served (notices) | 0 contracts 0 oz 0.00 TONNES |

| Total monthly oz gold served (contracts) so far this month | 27,437 notices 2,743,700 OZ 85.340 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposits

total customer withdrawals nil oz

0 customer withdrawals:

total withdrawal: nil oz

ADJUSTMENTS: 1

first: dealer to customer JPMorgan 49,774,303 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 559 contracts having LOST 26 contracts

We had 249 notices filed yesterday so we GAINED A WHOPPING 223 contracts or an additional 22,300 oz will stand for delivery at the comex ,

May saw a LOSS of 869 contracts to stand at 1582

June saw a LOSS of 2901 contracts UP to 441,376 contracts

We had 559 notice(s) filed today for 55,900 oz FOR THE APRIL 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 559 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 464 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2021. contract month,

we take the total number of notices filed so far for the month (27,437) x 100 oz , to which we add the difference between the open interest for the front month of (APRIL 559 CONTRACTS ) minus the number of notices served upon today 559 x 100 oz per contract equals 2,743,700 OZ OR 85.340 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:

No of notices filed so far (27,437) x 100 oz+ (559) OI for the front month minus the number of notices served upon today (559} x 100 oz} which equals 2,721,400 oz standing OR 84.646 TONNES in this active delivery month of APRIL.

We GAINED 22,300 additional oz that will stand for delivery on this side of the pond

TOTAL COMEX GOLD STANDING: 85.340 TONNES (A WHOPPER FOR AN APRIL ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626,135 oz 60.39 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,877,859.418 OZ (1115,95 TONNES)

TOTAL ELIGIBLE GOLD: 18,387,059.162 OZ (571.91 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,490,800.246 OZ (544.03 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,549,173.0 OZ (REG GOLD- PLEDGED GOLD) 483.64tonnes

END

APRIL 2022 CONTRACT MONTH//SILVER//APRIL 28

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,847,310.670 oz Brinks CNT Manfra Int Delaware |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,740,742,565 oz Delaware JPMorgan |

| No of oz served today (contracts) | 1CONTRACT(S)5,000 OZ) |

| No of oz to be served (notices) | 27 contracts (135,000 oz) |

| Total monthly oz silver served (contracts) | 1361 contracts 6,805,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into Delaware: 595,140.755 oz

ii) Into JPMorgan: 1,145,601.800 oz

total deposit: 1,740,742.555 oz

JPMorgan has a total silver weight: 173.322 million oz/332.878 million =52.07% of comex

Comex withdrawals: 4

i) Out of CNT 598,936.200 oz

ii) Out of Brinks 12,595.390 oz

iii) Out of Int Delaware 200,235.870 oz

iv) Out of JPMorgan 1,035,543.210 oz

total withdrawal 1,847,310.670 oz

4 adjustments: dealer to customer

i) Brinks 493,846.510 oz

ii) Out of CNT: 74,960.866 oz

iii) JPMorgan 205,009.550

iv) Out of Manfra: 23,939.300 o

the silver comex is in stress!

TOTAL REGISTERED SILVER: 83.70 MILLION OZ

TOTAL REG + ELIG. 332.985 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL OI: 28, HAVING GAINED 24 CONTRACTS FROM TUESDAY. We had 3 notices filed yesterday,

so we GAINED 27 contracts or an additional 135,000 oz will stand on this side of the pond

MAY HAD A LOSS OF 7841 CONTRACTS DOWN TO 9641 contracts

JUNE HAD A GAIN OF 143 TO STAND AT 1563

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes: 64,088// est. volume today// good

Comex volume: confirmed yesterday: 81,880 contracts ( very good/spreader liquidation )

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1361 x 5,000 oz = 6,805,000 oz

to which we add the difference between the open interest for the front month of APRIL (x28) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL./2021 contract month: 1361 (notices served so far) x 5000 oz + OI for front month of APRIL (x28) – number of notices served upon today (1) x 5000 oz of silver standing for the APRIL contract month equates 6,940,000 oz. .

We GAINED 27 contracts or an additional 135,000 oz will stand on this side of the pond

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1095.72 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTSS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 575.725 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Oops! Our Bad! IMF Director Admits “We Printed Too Much Money”

THURSDAY, APR 28, 2022 – 09:24 AM

Authored by Michael Maharrey via SchiffGold.com,

Mostly we get lies, spin and obfuscation from central bankers, politicians and bureaucrats. But every once in a while, one of these people accidentally wanders into the truth.

IMF Director Kristalina Georgieva did just that during a recent panel discussion hosted by CNBC. She conceded that central banks globally “printed too much money and didn’t think of unintended consequences.”

I think we are not paying sufficient attention to the law of unintended consequences. We take decisions with an objective in mind and rarely think through what may happen that is not our objective. And then we wrestle with the impact of it.

“Take any decision that is a massive decision, like the decision that we need to spend to support the economy. At that time, we did recognize that maybe too much money in circulation and too few goods, but didn’t really quite think through the consequence in a way that upfront would have informed better what we do.”

How this economic brain trust missed failed to consider that injecting trillions into the economy would cause prices to rise is a bit of a head-scratcher. This is economics 101. Expanding the money supply pushes prices higher than they otherwise would be. I knew this would happen. Peter Schiff knew this would happen. Heck, you probably knew this would happen. But the people charged with running the global economy didn’t?

These people are either wildly incompetent, or they are lying to you.

Either way, they are “bad economists” as defined by Frédéric Bastiat.

Between a good and a bad economist this constitutes the whole difference — the one takes account of the visible effect; the other takes account both of the effects which are seen, and also of those which it is necessary to foresee.”

Good on Georgieva, I guess. They say admitting your problem is the first step on the road to recovery. So, you might think this confession is a step forward. But I assure you, it’s not. The ego, arrogance, and hubris that make these people think they can micromanage the global economy remain firmly in place. They just think they need to try a little bit harder.

Although Georgieva admits a mistake, the rest of her comment reveals she hasn’t learned the lesson.

We act sometimes like eight years old playing soccer. Here is the ball, we are all at the ball. And we don’t cover the rest of the field.

“Our ability to deal with more than one crisis at one time is very, very limited. and we have to zero in on the really big things that could determine the future and keep our attention on them.”

Basically, she’s saying, “Oops! Our bad! We messed up because we didn’t consider the unintended consequences. But we’re going to do better next time because our focus is going to be right on point.”

Georgieva, Powell, Biden, LaGarde, and the whole lot of these central planners don’t understand that it is impossible for them to take into account all of the unintended consequences of a given policy prescription. That’s why central planning is always doomed to failure.

Economist F.A. Hayek got to the root of the problem in his seminal paper, “The Use of Knowledge in Society.” In a nutshell, Hayek concluded that central planning will always fail because it is impossible for the central planners to possess all of the information necessary to factor in all of the ramifications of any given policy.

The knowledge of the circumstances of which we must make use never exists in concentrated or integrated form, but solely as the dispersed bits of incomplete and frequently contradictory knowledge which all the separate individuals possess.”

Or as FEE put it in its introduction to Hayek’s work:

Hayek points out that sensibly allocating scarce resources requires knowledge dispersed among many people, with no individual or group of experts capable of acquiring it all.”

Simply put, unintended consequences are inevitable in central planning. No matter how hard the central planner try, they are going to miss stuff. No matter how smart an individual or a group of individuals might be, they don’t have all of the knowledge they need. They can’t have it. It’s impossible.

The problem is that people like Georgieva don’t understand this. They they their crew is smart enough, wise enough and that they care enough to get the job done. If the make a mistake, they just need to try harder.

And that’s where they’re wrong. They need to quit trying, get out of the way and let the market function.

END

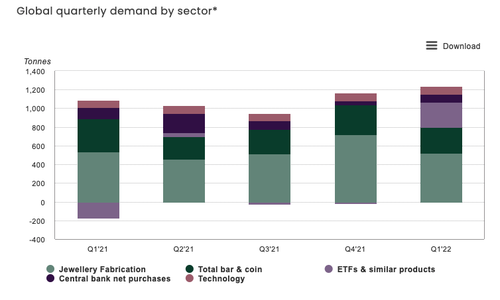

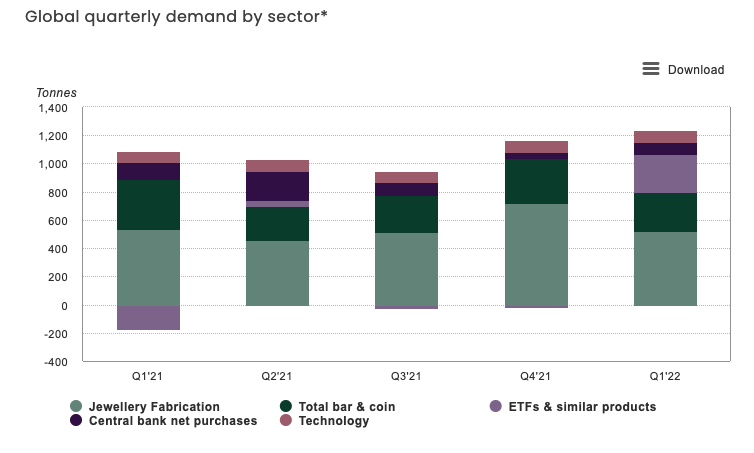

Gold Demand Surges In First Quarter

THURSDAY, APR 28, 2022 – 02:00 PM

Gold demand surged to kick off the year, up 34% year-on-year in the first quarter of 2022.

Total demand came in at 1,234 tons in Q1. That was the highest quarterly demand since Q4 2018, according to the World Gold Council’s Gold Demand Trends report. Demand in the first quarter of this year was 19% above the 5-year average.

According to the WGC, surging inflation and the Russian invasion of Ukraine were key factors driving demand.

The price of gold was up 8% in Q1.

Gold inflows into ETFs charted their strongest quarterly number since the third quarter of 2020. Safe-haven demand fueled the 269-ton increase in ETF gold holdings. This more than reversed the 174-ton outflow from gold-backed funds in 2021.

Demand for gold coins and gold bars came in at 282 tons. That was 20% down from a very strong first quarter last year, but it was still 11% higher than the five-year quarterly average.

While physical investment gold demand in the US and Europe were both strong, China was key to explaining the y-o-y decline. A drop in Chinese demand for gold bars and coins due to new government COVID-19 lockdowns put a drag on physical gold investment in that country. Record gold prices in some currencies also resulted in profit-taking. This was particularly true in Japan and Turkey.

Softer demand in China and India also stalled the recovery in the gold jewelry market. Q1 demand was down 7% year-on-year, coming in at 474 tons.

Central banks added a modest amount of gold to their holdings in Q1. On net, central banks globally increased their gold reserves by 84 tons. This doubled the increase from Q4 but was 29% down from the first quarter of 2020. Several central banks made large sales in Q1, pulling the net increase lower.

Demand for gold by industry rose by 1% year on year. It was the best Q1 for industrial gold demand since 2018.

While the technology sector has recovered somewhat from the impact of the pandemic, COVID-related headwinds remain thanks to China’s draconian policies. Dozens of cities in China are under total or partial lockdown, with major industrial and financial hubs such as Shanghai impacted. China’s zero-COVID policy also coincided with the Chinese New Year holiday. According to the WGC, this will potentially impact the electronics supply chain throughout 2022. The war in Ukraine could also impact the global electronics market moving into the second quarter.

Looking ahead, the WGC says that with so many factors in play, it’s difficult to determine gold demand trends moving forward.

Jewelry and industrial demand could see deteriorating market conditions if the war in Ukraine continues. But we could also see quickly improving conditions with a resolution of that conflict. It’s also hard to predict how governments will respond to any resurgence in COVID-19. More lockdowns would put additional drag on these sectors.

On the other hand, the World Gold Council says it expects investment demand to be higher this year than last year due to high inflation and geopolitical instability.

You can read the entire World Gold Council report HERE.

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS:

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

END

END

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES PALM OIL

end

COMMODITIES IN GENERAL//DIAMONDS

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6146

OFFSHORE YUAN: 6.6536

HANG SANG CLOSED UP 329.81 PTS OR 1.65%

2. Nikkei closed UP 461.29 PTS OR 1.75%

3. Europe stocks ALL GREEN

USA dollar INDEX UP TO 103.70/Euro FALLS TO 1.0495

3b Japan 10 YR bond yield: FALLS TO. +.193/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 127.99/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.830%/Italian 10 Yr bond yield FALLS to 2.58% /SPAIN 10 YR BOND YIELD RISES TO 1.81%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.75: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield FALLS TO : 3.04

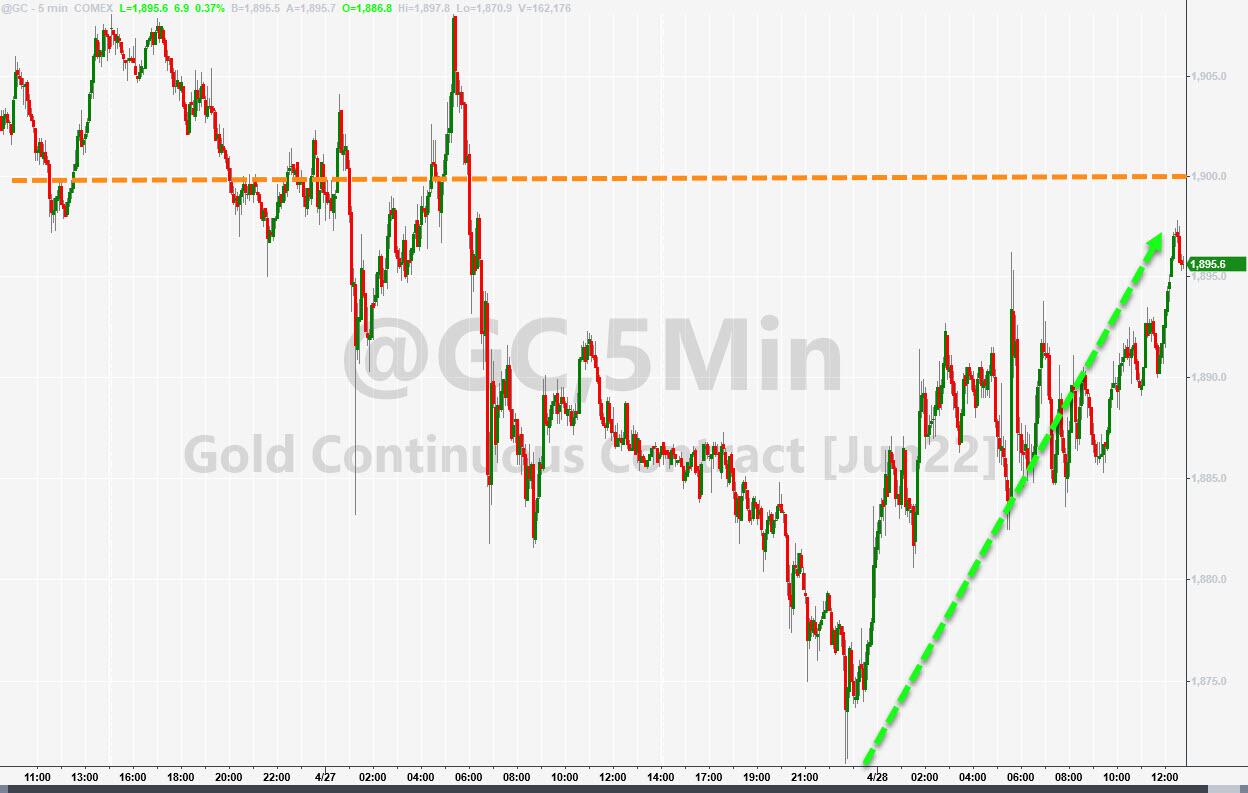

3j Gold at $1885.30 silver at: 23.06 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 41/100 roubles/dollar; ROUBLE AT 72.37

3m oil into the 103 dollar handle for WTI and 104 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 130.77 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9727– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0212well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.817 DOWN 0 BASIS PTS

USA 30 YR BOND YIELD: 2.914 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.81

Futures Rebound As Facebook Soars; Dollar Steamrolls Higher As Yen Crashes

THURSDAY, APR 28, 2022 – 07:46 AM

U.S. index futures, European bourses and Asian markets all rose as “good enough (if hardly stellar)” earnings reports from Facebook parent Meta Platforms and Qualcomm boosted sentiment (just don’t look at the collapse in Teladoc). As we hit the peak of earnings season, with Apple, Amazon and Twitter set to report earnings today, S&P futures jumped 1.5%, while he Nasdaq futs jumped 2.2%, fuelled by a nearly 20% surge in Meta, which would be its biggest post-earnings jump since 2013. Investors were happy after Facebook added more users than projected in the first quarter, even if revenue growth slowed to just 7%, the lowest since the IPO. The dollar continued its relentless ascent, boosted by a plunge in the yen (more here) rising to the highest level in more than five years thanks to nominal US yields which are the highest in developed markets. WTI futures traded at around $102 a barrel. The 10-year Treasury yield was down some 2 basis points to 2.8147%. Bitcoin climbed, trading just below $40,000.

U.S. chip stocks traded higher in the premarket as Qualcomm, the biggest maker of chips that run smartphones, surged on a strong sales forecast easing fears about demand and the macroeconomic environment, while PayPal shares gained after it reported better-than-expected revenue and active user figures. Here are some other notable premarket movers:

- Airline stocks gain in premarket trading after Southwest Airlines Co. said it expects a rebound in domestic travel to carry into the summer.

- PayPal (PYPL US) rises 3.6% in premarket trading after the payments firm reported better-than-expected first-quarter revenue and active user figures.

- Pinterest shares (PINS US) rise 9% in premarket trading after quarterly earnings beat estimates, though analysts cut price targets amid questions over user engagement.

- Teladoc Health (TDOC US) plunges 40% in premarket trading after cutting its revenue and earnings guidance, with analysts saying the outlook fuels the bear argument for the health-care technology company. Cathie Wood’s ARK Investment Management holds a stake.

- Ford’s (F US) first- quarter results that were mixed, according to analysts. A “modest” beat in 1Q was mostly driven by European operations. Shares rise 2.8% in pre-market trading.

- Atomera (ATOM US) surges as much as 18% in premarket trading, after the semiconductor materials and technology company entered into a new joint development agreement with a leading foundry partner.

- Statera BioPharma (STAB US) soars 81% in U.S. premarket trading, after the biotech company announced a strategic agreement with Immune Therapeutics (IMUN US).

- Sundial Growers (SNDL US) shares jump 11% in premarket trading after the cannabis producer reported 4Q adjusted Ebitda from continuing operations and net revenue that beat the average analyst estimate.

- Amgen (AMGN US) drops 5.9% in postmarket trading after an IRS probe of prior tax years, the biotechnology company also left its annual outlook unchanged despite a first-quarter earnings beat.

“The bullish mood is very much earnings related after some of the disappointing news earlier in the week,” said Roger Lee, head of U.K. Strategy at Investec. “Meta, Qualcomm, Paypal helped reassure following on from Microsoft’s good numbers.”

Thursday’s relief rally punctuates a week of nerves marked by China’s struggle to suppress Covid, Russia’s war in Ukraine, halts of Russian gas exports to Poland and Bulgaria, and worries that Federal Reserve monetary tightening may tip the U.S. economy into a recession. Almost 70 companies in Europe are due to publish results Thursday. About 61% of the companies that have reported so far have beaten estimates.

Despite the rebound in the past two days, US stocks have had a very rough month, with the S&P 500 set for its worst monthly return in two years, while the tech-heavy Nasdaq 100 is set for a 12% loss this month, its worst performance since October 2008. That may reverse if Amazon.com and Apple – which are among the companies set to report quarterly numbers on Thursday – report blowout earnings.

“Ironically the better the corporate earnings backdrop, the less recession risk there is, so the Fed can increase rates more aggressively and all the implications that will have on valuations,” said Roger Lee, a strategist at Investec. “Paradoxically good corporate news could ultimately be bad news for the market.”

It was an exciting session for central bank watchers with the BOJ surprising markets with an announcement that it would hold daily, unlimited fixed-rate operations to defend Yield Curve Control, in the process crushing the yen. Meanwhile, Sweden’s central bank surprised most by raising its benchmark rate to send the krona soaring.

European stocks also rallied – the Stoxx 600 rose as much as 1.4% led by autos, tech and the banking sector although every industry group was in the green. Big individual contributors included TotalEnergies, Glencore and Capgemini, which all posted gains on buoyant earnings. DAX and CAC gain as much as 2%. Here are some of the biggest European movers today:

- Standard Chartered shares rise as much as 17% in London, the most since November 2020, following a rally in Hong Kong. The lender delivered a “stunning” 44% beat versus quarterly pretax profit consensus, according to Investec.

- Glencore gains as much as 2.7% in London after the commodity giant’s first-quarter production report; Morgan Stanley analysts say an uplift to marketing guidance overshadows weaker output.

- Barclays climbs as much as 3.7% after reporting what Citi described as an “impressive set of results” for 1Q. The broker highlighted the investment banking segment, noting that its performance was the main driver for the pretax profit beat.

- Smith & Nephew rises as much as 4.2% after reporting earnings that included beats in both overall revenue and all business areas. RBC notes the results were “well ahead” of both its own and consensus estimates.

- Albioma advances as much as 16% after U.S. private equity firm KKR agreed to acquire the French solar and biomass power producer for EU50/share plus EU0.84 dividend, in a deal valued at around EU1.6b.

- Whitbread gains as much as 4.9%, among the top performers in the Stoxx 600 Travel & Leisure Index, after the U.K. hotel operator reported results that Bernstein says show a “very strong start” to FY23.

- J Sainsbury drops as much as 6.9% after the U.K. grocer reported FY22 results and forecast FY23 adjusted pretax profit in the range of GBP630m- GBP690m. The guidance suggests cuts to consensus, according to Morgan Stanley.

- Delivery Hero falls as much as 12%, reversing an earlier 9% gain, with Goldman Sachs saying the company’s decision to stop reporting orders won’t be welcomed by investors. Analyst Rob Joyce notes that otherwise the company’s 1Q release was above guidance.

- Elior falls as much as 5% after UBS lowered its price target on the French caterer to EU3.30 from EU6.60, citing the impact on business from the omicron Covid-19 variant as well as uncertainty over new management and targets. The stock is now down 54% YTD.

- Weir Group drops as much as 6.4%, with analysts flagging the short-term hit for the mining-equipment firm related to its exit from Russia.

Asian stocks rose with Japan leading after the country’s central bank kept its easing stance unchanged, while the stabilizing of Covid cases in China also helped investor sentiment. The MSCI Asia Pacific Index advanced as much as 1%, rebounding from its lowest since mid-2020. Australian miner BHP Group and Chinese internet giant Alibaba provided the biggest boosts to the benchmark, with financials and materials leading the sectoral advances. Japan stocks outperformed in the region as the yen tumbled to the 130 per dollar level for the first time since 2002, bolstering exporters including Toyota Motor, which was the third-biggest contributor to the Asian measure’s gain.

The Bank of Japan “didn’t shift to a tightening policy bias and the yen fell as a result so that helped to boost Japanese stocks,” said Fumio Matsumoto, chief strategist at Okasan Securities. “Materials shares were doing well and I think their gains reflect easing of concerns over the global economic outlook, as cases in Shanghai are falling and iron ore prices seem to be rebounding,” Matsumoto said. Stocks in China gained for a second day after fresh policy pledges to promote internet platform firms and easing virus outbreaks in Beijing and Shanghai buoyed sentiment. Equity gauges across Australia, South Korea and India also advanced. The MSCI Asia Pacific Index is still poised for a fourth-straight weekly decline and its steepest monthly drop since March 2020

Japanese stocks jumped after the Bank of Japan maintained its ultra-easy monetary policy and the yen tumbled below the 130 per dollar level for the first time since 2002. The central bank kept its yield curve control settings and the scale of its asset purchases unchanged and said it would buy an unlimited amount of bonds at fixed-rates every business day to protect a 0.25% ceiling on 10-year government debt yields. The Japanese currency tumbled 1.4% against the greenback, bolstering the outlook for the nation’s exporters.

“It’s now abundantly clear to markets that Governor Kuroda, who is very strong-willed, and the BOJ will continue to insist that only when domestic wages rise more fully will inflation be persistent,” Nikko Asset Management strategist John Vail. “Until then, the BOJ will continue to cap bond yields, but some moderate policy tightening will likely occur later this year.” The Topix climbed 2.1% to close at 1,899.62, while the Nikkei advanced 1.7% to 26,847.90. Toyota Motor Corp. contributed the most to the Topix gain, increasing 3.2%. Out of 2,172 shares in the index, 1,720 rose and 395 fell, while 57 were unchanged

India’s benchmark equities index rose, tracking peers across Asia, buoyed by gains in Reliance Industries Ltd. The S&P BSE Sensex advanced 1.2% to 57,521.06, a one-week high, while the NSE Nifty 50 Index also climbed by a similar magnitude. Reliance added 1.5% to rise to a record and was the biggest boost to the Sensex, which had 26 of 30 member-stocks trading higher. All but one of 19 sectoral sub-indexes compiled by BSE Ltd. gained, led by a gauge of consumer goods companies. In earnings, of the 12 Nifty 50 firms that have announced results so far, five have missed, while seven have either met or beat analyst estimates.

In rates, Treasuries advanced across the curve, clawing back a portion of Wednesday’s losses. Session highs were reached late in Asia session after the BOJ pledged to buy unlimited amount of bonds at a fixed rate every business day to cap 10-year yields at 0.25%. 10Y TSY Yields are richer by 1bp-2bp across the curve with curve spreads little changed, the 10-year yield around 2.815% outperforms bunds by 3.5bp, gilts by 3bp. The week’s coupon auction cycle concludes with $44b 7-year note sale at 1pm ET; Wednesday’s 5- year tailed by 0.9bp. European fixed income rallied after a soft Spanish inflation print, although the bulk of the move in the rates space is subsequently faded. German curve bear flattens, cheapening 2-3bps across the short end. Gilts bear steepened a touch. Peripheral spreads tighten with the belly of the Italian curve outperforming peers.

In FX, Bloomberg dollar spot index rises 0.4%, trading off the late Asia high. SEK outperforms in G-10, rallying after a surprise rate hike and more hawkish guidance. JPY is the standout underperformer with USD/JPY stalling near 131 after BOJ Kuroda’s press conference. JPY trades off worst levels after official comments that Japan will take appropriate action on FX if needed, describing the latest moves as warranting extreme concern. Some more details:

- The yen plunged, hitting a 20-year low against the dollar after the Bank of Japan pledged to keep rates at rock-bottom levels, sparking more demand for the greenback. USD/JPY continued to climb in the European session, up as much as 2% to hit 131.01, its highest since April 2002, before pulling back after a Japanese finance ministry official said it will act appropriately on FX if needed. USD/JPY has jumped 7.3% so far this month, its best performance since late 2016. Jerky moves in the yen suggest that its Ministry of Finance will continue to jawbone the currency as it approaches the next key level of 135. “Markets will likely next test intervention possibilities and at what level such warnings may appear,” according to Yoshifumi Takechi, chief analyst at Money Partners in Tokyo. If the currency pair rises past 135, then the probability of intervention may rise, he said

- The greenback boosted broadly, led higher on expectations that the Fed will raise interest rates by 50 basis points next week, embarking on an aggressive monetary tightening cycle. U.S. Treasuries advance, pushing two-year yield 2 basis points lower. “The focus of FX markets has primarily been on rate differentials and how bonds are adjusting given the continuous shift in growth conditions,” says Simon Harvey, head of FX analysis at Monex Europe, He adds that volatility in the bond market has also boosted the USD on safe-haven demand, suggesting that expectations for outperformance in U.S. rates is not the only driver of the stronger dollar. The Bloomberg Spot Dollar Index hits nearly 2-year high of 1,250 and is poised to post a near 5% gain in April, its best monthly performance since May 2012.

- EUR/USD slides to a five-year low of 1.0483 hit in early European trade, before pulling back to around 1.0505. EUR on track to lose more than 5% vs USD in April, its worst month since 2015.

- Swedish krona rallies after the Riksbank raises interest rates by 25 basis points from zero and signals up to three more hikes this year. EUR/SEK drops roughly 1% to 10.25, a one-week low, before paring move

- GBP/USD drops 0.7% to touch 1.2462, lowest since July 2020, as rate differentials continue to favour the USD

In commodities, oil edged higher with West Texas Intermediate futures around $103 a barrel. Crude prices have struggled for direction this week as China’s spreading virus outbreak continued to weigh on the outlook for global demand. Natural gas prices in Europe declined following two days of gains as buyers considered options to keep getting supply from Russia without violating sanctions. Spot gold pared losses, now little changed at $1,888/oz. Base metals are mixed; LME nickel falls 0.9% while LME aluminum gains 0.7%.

Looking at the the day ahead, data releases will include German CPI for April and US Q1 GDP reading, alongside the weekly initial jobless claims. From central banks, we’ll hear from ECB Vice President de Guindos and the ECB’s Wunsch, and the ECB will also be publishing their Economic Bulletin. Finally, earnings releases include Apple, Amazon, Mastercard, Eli Lilly, Merck & Co., Thermo Fisher Scientific, Comcast, Intel, McDonald’s, Caterpillar and Twitter.

Market Snapshot

- S&P 500 futures up 1.6% to 4,248.25

- STOXX Europe 600 up 1.3% to 450.14

- MXAP up 0.9% to 165.94

- MXAPJ up 1.2% to 548.04

- Nikkei up 1.7% to 26,847.90

- Topix up 2.1% to 1,899.62

- Hang Seng Index up 1.7% to 20,276.17

- Shanghai Composite up 0.6% to 2,975.49

- Sensex up 1.5% to 57,691.20

- Australia S&P/ASX 200 up 1.3% to 7,356.89

- Kospi up 1.1% to 2,667.49

- German 10Y yield little changed at 0.83%

- Euro down 0.1% to $1.0543

- Brent Futures down 0.3% to $105.00/bbl

- Gold spot down 0.2% to $1,882.45

- U.S. Dollar Index up 0.29% to 103.25

Top Overnight News from Bloomberg

- The ascendant U.S. dollar headed for its best month in a decade, as renewed yen selling cemented the greenback’s strength against major peers

- As inflation fears surge, holders of U.S. government debt are having a rough ride. Investors have abandoned the market en masse, making the first quarter the worst on record and devastating the value of bond portfolios. But now fixed- income returns are starting to get a lift from that same boogeyman

- The yen’s plunge to a 20-year low threatens to leave it significantly weaker for years to come, shaking up global money flows and undermining Japan’s efforts to get its fragile economy back on track

- Russia’s war in Ukraine has created new bottlenecks and these “are exacerbated by additional supply chain difficulties stemming from new pandemic measures in Asia,” ECB Vice President Luis de Guindos tells lawmakers in Brussels

- “My assessment is that we are very close to the peak and that we will start to see inflation decline in the second half of the year,” ECB Vice President Luis de Guindos says in Brussels

- The spike in energy costs was behind recent inflation-forecasting mistakes by the ECB, including the biggest in its history, according to new research from the institution

- “We expect underlying inflation to continue to rise, driven by high imported goods inflation, limited spare capacity in the Norwegian economy and prospects for rising wage growth,” Norges Bank Governor Ida Wolden Bache says in a statement

- Turkey central bank raised its end-2022 inflation estimate to 42.8%, from 23.2% in previous inflation report

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were higher across the board amid a slew of earnings updates and a dovish BoJ. ASX 200 gained with mining stocks mostly underpinned following production updates. Nikkei 225 benefitted as the BoJ reaffirmed its dovishness and kept its ultra-loose policy. Hang Seng and Shanghai Comp are both higher but with gains capped in the mainland due to ongoing lockdown fears with Hangzhou city to conduct mass testing and after China’s Qinhuangdao city in the Hebei province locked down its district due to COVID.

Top Asian News

- China Stocks Rise for Second Day as Shanghai Covid Cases Decline

- StanChart Shares Soar 14% as Lender Raises Revenue Outlook

- China Cuts Coal Import Tariffs to Zero to Increase Supply

- Huawei’s Profit Dives 67% After U.S. Sanctions Wallop Phone Arm

Equities in Europe continue to gain heading into month-end, with overall sentiment across stocks bolstered by Meta (+17% pre-market) earnings yesterday. All sectors are in the green to varying degrees and clearly portray an anti-defensive bias – with the exception of Basic Resources, which sits at the bottom of the bunch after heavily outperforming yesterday. Stateside, US equity futures are firmer across the board, with the NQ clearly outpacing its peers.

Top European News

- Erdogan Plans Meeting With Saudi Crown Prince to Revive Ties

- Erdogan Says Jailed Businessman Kavala Is ‘Turkey’s Soros’

- JPM Quants Expects Global Earnings Downgrades and Volatility

- Riksbank Hikes Rate in U-Turn to Join Global Central Banks

FX:

- The Buck’s bull run continues, with DXY up to 103.700, Euro losing 1.0500+ status and Sterling testing sub-1.2500 Fib before retracements.

- Swedish Krona soars after surprise Riksbank rate hike, higher repo path and slowdown in QE.

- Japanese Yen extends losing streak following no change from ultra accommodative BoJ policy before partial recovery on extreme concern from Japan’s MOF.

- Japanese MOF official says excess FX volatility is undesirable, recent FX moves are “extremely worrying”; will take appropriate action if needed, communicating closely with the BoJ and foreign currency authorities, via Reuters .

- Yuan is weaker again as China increases efforts to contain covid and PBoC sets another softer onshore reference rate.

Fixed Income

- EU debt rattled to a degree by Riksbank decision to taper QE and US Treasuries to a lesser extent

- Bunds nearer 155.00 than 156.00, Gilts towards base of 119.68-08 range and 10 year T-note under 120-00 within a 120-01/119-19 band

- BTPs outperform on the eve of month end auctions after breaching, but unable to retain 133.00+ status

- Treasury curve flat ahead of 7 year issuance that normally entices foreign buyers even when the Dollar is not so elevated

Commodities

- WTI June and Brent July post modest intraday gains, but in the grander scheme, prices are consolidating.

- Spot gold briefly dipped under its 100 DMA (USD 1,877.50/oz) to a current low of around USD 1,871/oz as the Buck was rampant at the time.

- Base metals markets are relatively mixed with some underperformance seen in LME nickel.

- China is to grant zero-tariff on coal imports from May 1 2022 to March 31 2023 to increase supply.

US Event Calendar

- 08:30: April Initial Jobless Claims, est. 180,000, prior 184,000; Continuing Claims, est. 1.4m, prior 1.42m

- 08:30: 1Q GDP Annualized QoQ, est. 1.0%, prior 6.9%

- 1Q Personal Consumption, est. 3.5%, prior 2.5%

- 1Q GDP Price Index, est. 7.2%, prior 7.1%

- 1Q PCE Core QoQ, est. 5.5%, prior 5.0%

- 11:00: April Kansas City Fed Manf. Activity, est. 35, prior 37

DB’s Jim Reid concludes the overnight wrap

We’ve also released our April survey results this morning (see link here). This was our first survey since Russia’s invasion of Ukraine, and you can see the impact across a number of answers. More than 60% of respondents expect the next US recession by 2023, in line with our out of consensus house view, while inflation expectations were revised higher in the US and EU. The survey results also show expectations for bonds and the S&P 500 to dip from current levels along with much more, so do peruse the full results.

Whilst global growth concerns remain prominent in markets, with investors having to navigate Chinese lockdowns, major geopolitical tensions and the prospect of a Fed-induced hard landing, equities begun to stabilise yesterday and the S&P 500 managed to eke out a +0.21% gain, albeit only after another second-half selloff that saw the index move down from its intraday high of +1.56% around the US lunchtime. Even with the equity gains however, geopolitical developments led to a weaker performance among a broader section of European assets, with the Euro itself nearing the $1.05 mark for the first time in nearly 5 years as multiple signs pointed to a further escalation between the EU and Russia on the energy side.

In terms of those developments, markets woke up to the news that Gazprom would be stopping gas flows to Poland and Bulgaria, which saw European natural gas futures surge more than 20% following the open. Russia said this was because they hadn’t agreed to pay for gas in rubles, but European Commission President von der Leyen said in a statement that Russia was using “gas as an instrument of blackmail”, and warned companies not to accede to Russia’s demands to pay in rubles. Later in the session it was even reported by Bloomberg that Germany was prepared to support an EU ban on Russian oil, on the condition it was gradual and came with a transition period, so this fits into the pattern over recent days of an acceleration in the EU’s attempts to eliminate its dependence on Russian energy. According to the report, the Russian oil ban would be part of the sixth package of sanctions, and proposals could be put forward as soon as next week.

By the end of the session, European natural gas futures had pared back their initial gains, and “only” closed up +4.09% at €107.43/MWh. But as mentioned at the top, the bigger damage was seen to the Euro’s value, which closed at a 5-year low of $1.0557, having started the month above $1.10, and this morning is down yet further at $1.0515. Those declines also came in spite of remarks from ECB President Lagarde, who leant into recent suggestions that we could get a rate hike as soon as July. In her remarks, she said that asset purchases would be concluding “probably in July”, and that would also be the time to “look at interest rates and an increase in interest rates.”

European sovereign bonds had a pretty mixed performance against this backdrop, but there was a consistent story of widening spreads as investors favoured bunds over peripheral debt. In fact, the gap between Italian 10yr yields over bunds widened by +2.8bps to 177bps yesterday, which is the widest its been since June 2020. Similar moves were seen in credit markets too, where Itraxx Crossover widened +4.0bps to 414bps, which is just shy of its recent peak at 421bps on March 7, and up from 333bps just over 3 weeks ago. Havens were the beneficiary of yesterday’s moves though, with yields on 10yr bunds down -1.2bps, and the US Dollar index (+0.64%) strengthened for the 18th time in the last 20 sessions, surpassing its March 2020 peak to close at levels not seen since early 2017. This morning that trend has accelerated following the Bank of Japan’s policy decision (more on which below), and the index has risen a further +0.50% to trade at levels not seen since 2002, at 103.47.

These signs of stress weren’t as evident in equity markets yesterday, which begun to recover from their Tuesday slump on both sides of the Atlantic. The S&P 500 rose +0.21%, which meant it was no longer in negative territory on a rolling annual basis, which it had been the previous session for the first time since May 2020, whilst Europe’s STOXX 600 (+0.73%) also posted a decent advance. That said, the S&P 500 is still down -7.65% over the month of April, keeping it on track for its worst monthly performance since the initial phase of the pandemic in March 2020. The equity reversal caused the Vix to retreat -1.92ppts but still finished above 30 for only the second time since mid-March. And on top of that, US Treasuries snapped their gains from Monday and Tuesday, with the 10yr yield up +11.1bps to 2.83%, as a rise in real yields (+8.5bps) drove the move higher on another day of heightened rates volatility ahead of next week’s FOMC.

After the close, Meta posted sales slightly below analyst estimates with earnings beating. Shares were more than +13% higher after the close, after Facebook’s daily users surprised to the upside and the firm cut their expense outlook. Like many other firms that have reported, the war, current inflation, and issues with supply chains have forced some of the platform’s advertisers to cut spending.

Overnight in Asia, the main news comes from the Bank of Japan’s decision, where they left their main policy interest rates unchanged, but did announce a decision to buy unlimited 10-yr JGBs at 0.25% every business day. They also raised their inflation forecasts, now projecting core CPI to to reach +1.9% in the current fiscal year ending in March 2023, before moderating to +1.1% in the following two fiscal years. So a big difference in stance to the other major central banks like the Fed and the ECB which have been progressively moving in a hawkish direction over recent months, and this saw the Japanese Yen weaken further, currently trading at 129.69 per US dollar, which is a level unseen since 2002.

Against that backdrop, the Nikkei (+1.32%) is leading the equity gains in Asia, although other indices including the Hang Seng (+1.22%), the CSI 300 (+0.37%), the Shanghai Composite (+0.25%) and the Kospi (+0.81%) are all in positive territory this morning. Meanwhile oil prices have lost ground as concerns about Chinese demand persist, and Brent Crude is down -1.41% this morning to $103.84/bbl. Looking forward, equity futures in the US are pointing towards further gains today, with those on the S&P 500 (+0.74%) and the NASDAQ 100 (+1.34%) moving higher.

Looking forward, we’ve got a couple of important data releases today. One is the first look at US GDP in the first quarter, for which our US economists have published a preview (link here). They see the reading coming in at exactly 0.0. The other is the German CPI reading for April, which comes ahead of the flash CPI reading tomorrow for the entire Euro Area. Our economist has also published a preview for that one (link here).

On yesterday’s data, the US goods trade deficit for March rose to a record of $125.3bn (vs. $105.0bn expected). Otherwise, the number of pending home sales fell -1.2% in March, marking a 5th consecutive monthly decline.

To the day ahead, and data releases will include the aforementioned German CPI for April and US Q1 GDP reading, alongside the weekly initial jobless claims. From central banks, we’ll hear from ECB Vice President de Guindos and the ECB’s Wunsch, and the ECB will also be publishing their Economic Bulletin. Finally, earnings releases include Apple, Amazon, Mastercard, Eli Lilly, Merck & Co., Thermo Fisher Scientific, Comcast, Intel, McDonald’s, Caterpillar and Twitter.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 17.20 PTS OR 0.58% //Hang Sang CLOSED UP 329.81 OR 1.65% /The Nikkei closed UP 461.27 PTS OR 1.75% //Australia’s all ordinaires CLOSED UP 1.26% /Chinese yuan (ONSHORE) closed DOWN 6.6146 /Oil DOWN TO 101.63 dollars per barrel for WTI and DOWN TO 104.65 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6146 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6536: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

Big news of the morning: the Yen craters to 130.77 to the dollars as the Bank of Japan stuns the markets with a daily fixed rate operations to defend the yield curve” i.e. buy bonds at a rate of .25% daily which will ensure a currency collapse

(zerohedge)

Yen Craters To 20 Year Low As BOJ Stuns Markets With Daily Fixed-Rate Operations To Defend YCC

THURSDAY, APR 28, 2022 – 06:06 AM

It was a little over a month ago – on March 24 – when we first laid out the big dilemma facing the Bank of Japan, which on one hand was hoping to avoid a currency collapse (for obvious reasons) and prevent a crash in the yen, while on the other hand, was also hoping to keep the 10Y yield below its extremely dovish 0.25% yield curve control rate ceiling. The problem is that while the BOJ can control one or the other, it can’t control both; this is what we said then:

Japan, that paragon of MMT crackpots everywhere, suddenly finds itself trapped in a lose-lose dilemma: intervene in the bond market and spark a furious, potentially destabilizing and uncontrolled plunge in the yen which would also lead to galloping (if not worse) inflation, which could collapse what little faith remains in the BOJ, or do nothing and contain the slump in the yen while risking far higher yields which in a country where the debt is orders of magnitude greater than GDP, could also spell fiscal and monetary doom.

As a result, the market – having long gotten used to amicable interventions from the BOJ – will now surely test one of these two outcomes, and how the BOJ responds could have dramatic consequences for this original MMT test case. Should the BOJ’s reaction spark further erosion of faith in either Japan’s fiscal or monetary policies, the outcome for the world’s most indebted nation would be disastrous.

Sure enough, the market did test both outcomes, and after pushing the 10Y JGB yield to the upper bound of the YCC corridor of 0.25% and finding the BOJ willing to defend Japanese yields from further spikes, decided to focus its hammering on the yen instead, pushing it to two decade lows.

It’s also why we were paying particularly close attention to what the BOJ would announce in its decision early on Thursday – would it double down on Yield Curve Control defense, or would it finally turn its attention to the crashing yen and prop it up, perhaps by extending the YCC ceiling from 0.25% to 0.50% or higher (in line with what all other developed central banks are doing)?

Well, we got the answer and it was a doozy: the Bank of Japan on Thursday sparked a furious sell-off in the yen (and also the yuan) after shocking the market by doubling down on its Yield Curve Control and keeping its loose monetary policy intact, despite the crashing of the yen and growing pressure of inflation due to costlier imports.

The yen cratered below 130 against the U.S. currency for the first time in 20 years in afternoon trading in Tokyo, when rather than introducing flexibility to its monetary policy, the central bank in a statement reiterated its commitment to the 10-year yield target, saying it will conduct an unlimited fixed-rate operation to buy 10-year Japanese government bonds at 0.25% every day, effectively ensuring a currency collapse.

Specifically, the BOJ maintained the status quo across all monetary policy parameters, including yield curve control (YCC), asset purchase programs, and forward guidance (some market observers were expecting adjustments to forward guidance). The central bank decided by an 8-1 majority vote to maintain the YCC, and by a unanimous vote to maintain guidelines for asset purchases. In regard to YCC, BOJ member Kataoka cast the dissenting vote (as he usually does), saying that it was desirable to lower short- and long-term interest rates “with a view to encouraging firms to make active business fixed investment for the post-COVID-19 era.”

In a separately released economic outlook report, the board members offered a median forecast of sharply higher inflation coming at 1.9% for fiscal 2022, compared with 1.1% predicted just three months ago, and 1.1% for the next fiscal year. Economic growth is forecast to slow sharply to 2.9% for the current fiscal year, versus 3.8% predicted three months ago. The BOJ’s outlook assumes core CPI inflation will continue to fall short of the inflation target of +2%, calling for +1.1% in both FY2023 and FY2024, while it expects new core CPI inflation (excludes fresh food and energy) to grow steadily, calling for +0.9% in FY2022, +1.2% in FY2023, and +1.5% in FY2024, respectively.

But the highlight, as noted above, is what the BOJ said regarding YCC, where it explicitly added to the statement that “the Bank will offer to purchase 10-year JGBs at +0.25% every business day through fixed-rate purchase operations, unless it is highly likely that no bids will be submitted” cementing the bank’s commitment to keeping yields in the world’ most indebted country (relatively speaking) at or below 0.25%

On policy rates, the BOJ maintained forward guidance indicating that it “expects short- and long-term policy interest rates to remain at their present or lower levels.” Commenting on the move, Goldman said that “while the BOJ introduced daily fixed-rate operations to keep consistency with this forward guidance, in our view, we think the market is likely to view it as a strong dovish message. Indeed, post the MPM, the 10-year yield is down and the yen depreciated against the US dollar.”

It sure is, but more on that in a second.

- Speaking at a press conference later in the day, BOJ Governor Kuroda focused on the two key issues: inflation and the daily fixed-rate ops. Here are the highlights:

- Kuroda said “It Will Take Some Time to Get Sustainable Inflation” adding that current cost-push inflation will not be sustained as oil prices won’t keep rising.

- Kuroda said that “while inflation will rise temporarily to 2%, it won’t last as the effect of energy prices will ease”, that “”Inflation expectations are rising, but are centered on the short-term”

- The BOJ governor emphasized that the surge in inflation is not sustainable, saying “cost-push inflation isn’t sustainable” and that the “current rise in inflation expectations is also not sustainable”

- And even though risks are tilted to the upside for prices right now, and are tilted to the downside for the economy, there is no need to seek an exit from monetary stimulus now given the BOJ’s outlook for prices today

In short, the BOJ is quadrupling down on the wrong assumption that inflation is transitory. It won’t be the first catastrophic mistake the BOJ has made.