April 29, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

April 29, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1910.25 UP $20.05

SILVER: $23.04 DOWN $0.12

ACCESS MARKET: GOLD $1897.30

SILVER: $22.73

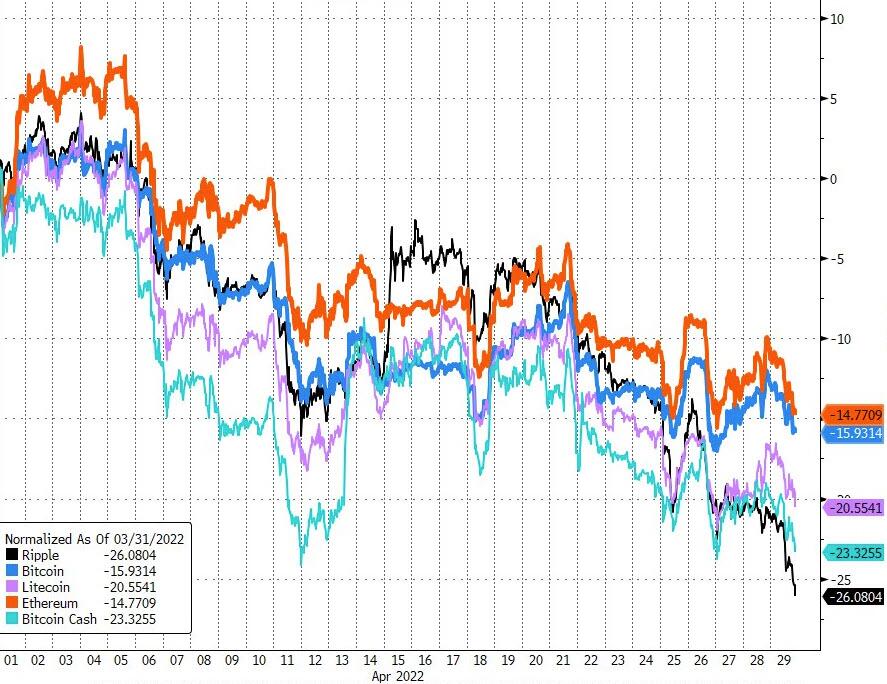

Bitcoin morning price: $38,739 DOWN 1325

Bitcoin: afternoon price: $38,434 DOWN 1630

Platinum price: closing UP $24.70 to $949.45

Palladium price; closing UP $93.40 at $2320.75

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/

: JPMorgan stopped/total issued 299.1388

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,888.700000000 USD

INTENT DATE: 04/28/2022 DELIVERY DATE: 05/02/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 42

132 C SG AMERICAS 20

435 H SCOTIA CAPITAL 14

657 C MORGAN STANLEY 8

657 H MORGAN STANLEY 555

661 C JP MORGAN 1274 299

690 C ABN AMRO 92

709 C BARCLAYS 283

732 C RBC CAP MARKETS 32

737 C ADVANTAGE 43

905 C ADM 114

TOTAL: 1,388 1,388

MONTH TO DATE: 1,388

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 1388 NOTICE(S) FOR 138,800 OZ (4.3172 TONNES)

total notices so far: 1388 contracts for 138,800. oz (4.3172 tonnes)

SILVER NOTICES:

1672 NOTICE(S) FILED 8,360,000 OZ/

total number of notices filed so far this month 1672 : for 8,360,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $20.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1095.72 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 12 CENTS

AT THE SLV// A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: HUGE CHANGES MIL AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.725 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 2349 CONTRACTS TO 136,891 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.21 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.21) AND WAS SOMEWHAT SUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A STRONG LOSS OF 1099 CONTRACTS ON OUR TWO EXCHANGES. NO DOUBT THE LOSS WAS DUE TO FINALIZATION OF SPREADER LIQUIDATION//TAS IN SILVER

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ // V) STRONG SIZED COMEX OI LOSS/(ALL OF THE LOSS DUE TO SPREADERS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-3732

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 20 days, total 22,904 contracts: 114.520 million oz OR 5.73 MILLION OZ PER DAY. (1145 CONTRACTS PER DAY)

TOTAL NO OF OZ UNDERGOING EFP TO LONDON 22,904 CONTRACTS X 5,000 PER CONTRACT:

EQUATES TO: 114.52 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2349 WITH OUR $0.21 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1250 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ .. WE HAD A STRONG SIZED LOSS OF 1099 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.495 MILLION OZ ACCOMPANYING THE LOSS IN PRICE.

WE HAD 1672 NOTICES FILED TODAY FOR 8,360,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3283 CONTRACTS TO 558,777 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -3787 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR SMALL GAIN IN PRICE OF $2.35//COMEX GOLD TRADING/THURSDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $2.35 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 4508 OI CONTRACTS (14.02 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 1225 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 558,777.

IN ESSENCE WE HAVE A VERY GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4508, WITH 3283 CONTRACTS INCREASED AT THE COMEX AND 1225 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4508 CONTRACTS OR 14.02 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1225) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3283,): TOTAL GAIN IN THE TWO EXCHANGES 4508CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES /// 3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OI. GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

54,513 CONTRACTS OR 5,451,300 OR 169.55 TONNES 20 TRADING DAY(S) AND THUS AVERAGING: 2725 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES: 169.55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2020, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 169.55/3550 x 100% TONNES 4.64% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 2349 CONTRACT OI TO 136,891 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1250 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2349 CONTRACTS AND ADD TO THE 1250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 1099 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 5.495 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.21 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 71.58 PTS OR 2.41% //Hang Sang CLOSED UP 813.22 OR 4.01% /The Nikkei closed UP 461.27 PTS OR 1.75% //Australia’s all ordinaires CLOSED UP 1.08% /Chinese yuan (ONSHORE) closed UP 6.5880 /Oil UP TO 106.58 dollars per barrel for WTI and UP TO 108.58 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.5880 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6198: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3283 CONTRACTS TO 558,777 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR GAIN OF $2.35 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2844 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1225 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1225 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1255 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4508 CONTRACTS IN THAT 1225 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3283 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR SMALL GAIN IN PRICE OF GOLD $2.35.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (5.353),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 5.353 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $2.35) AND WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A GOOD SIZED GAIN OF 14.02 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (5.353 TONNES)…

WE HAD 3787 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4508 CONTRACTS OR 450800 OZ OR 14.02TONNES

Estimated gold volume today: 164,944/// very poor

Confirmed volume yesterday:180,666 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //APRIL 29

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 964,53 oz Int. Delaware 30 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1388 notice(s) 138,800 OZ 4.3172 TONNES |

| No of oz to be served (notices) | 333 contracts 33,300 oz 1.0357 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1388 notices138,800 OZ 4.3172 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposits

1 customer withdrawals:

i) out of Int. Delaware 964.53 oz

total withdrawal: 964.53 oz

ADJUSTMENTS: 2/ dealer to customer

i) HSBC 977.955 oz

ii) JPMorgan 385.812 oz (12 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1721 contracts having GAINED 139 contracts

Thus by definition, the initial amount of gold standing for May is as follows:

1721 notices filed x 100 oz per notice = 172,100 oz or 5.353 tonnes

June saw a GAIN of 1503 contracts UP to 442,879 contracts

July has 0 OI

August has a gain of 1812 contracts up to 64,629 contracts

We had 1388 notice(s) filed today for 138,800 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1274 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1388 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 299 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1388) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 1721 CONTRACTS ) minus the number of notices served upon today 1388 x 100 oz per contract equals 172,100 OZ OR 5.353 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1388) x 100 oz+ (1721) OI for the front month minus the number of notices served upon today (1388} x 100 oz} which equals 172,100 oz standing OR 5.353 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 5.353 TONNES (A WHOPPER FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626,135 oz 60.39 tonnes

TOTAL REGISTERED AND ELIG GOLD AT THE COMEX: 35,876,894,878 OZ (1115,92 TONNES)

TOTAL ELIGIBLE GOLD: 18,385,595.205 OZ (571.86 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,491,289.173 OZ (544.05 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,549,173.0 OZ (REG GOLD- PLEDGED GOLD) 483.64tonnes

END

MAY 2022 CONTRACT MONTH//SILVER//APRIL 29

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,432,128.82 oz HSBC CNT JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 2,185,668.922 oz CNT Delaware JPMorgan |

| No of oz served today (contracts) | 1672CONTRACT(S)8,360,000 OZ) |

| No of oz to be served (notices) | 4362 contracts (21,810,000 oz) |

| Total monthly oz silver served (contracts) | 1672 contracts 8,360,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

i) Into Delaware: 419,003.222 oz

ii) Into JPMorgan: 1,166,623.700 oz

iii) Into CNT 600,042.000

total deposit: 2,185,668.922 oz

JPMorgan has a total silver weight: 173.713 million oz/333.633 million =51.85% of comex

Comex withdrawals: 3

i) Out of CNT 45,947.47 oz

i1) Out of JPMorgan 785,806.450 oz

iii) Out of HSBC: 600,374.800 oz

total withdrawal 1,432m128.82 oz

4 adjustments: dealer to customer

i) Brinks 907,234.370 oz

ii) Out of HSBC: 24,247.610 oz

iii) JPMorgan 116,071.370 oz

iv) Out of Manfra: 464,040.969 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.475 MILLION OZ

TOTAL REG + ELIG. 333.632 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 6034 HAVING LOST 3607 CONTRACTS

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS ACTIVE DELIVERY MONTH OF MAY IS AS FOLLOWS:

6034 NOTICES X 5000 OZ PER NOTICE = 30,170,000 OZ

JUNE HAD A GAIN OF 212 TO STAND AT 1775

JULY HAD A GAIN OF 1231 CONTRACTS UP TO 108,792 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1672 for 8,360,000 oz

Comex volumes: 47,943// est. volume today// poor

Comex volume: confirmed yesterday: 69,128 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1672 x 5,000 oz = 8,360,000 oz

to which we add the difference between the open interest for the front month of MAY (6034) and the number of notices served upon today 1672 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 1672 (notices served so far) x 5000 oz + OI for front month of MAY (6034) – number of notices served upon today (1672) x 5000 oz of silver standing for the MAY contract month equates 30.170,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1095.72 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 575.725 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS:

Another Raid of Deutsche Bank, Another Dead Whistleblower

By Pam Martens and Russ Martens: April 29, 2022 ~

The Financial Times is reporting this morning that “Germany’s federal police office, criminal prosecutors and the country’s financial watchdog BaFin are raiding Deutsche Bank’s headquarters in Frankfurt” this morning, according to a statement from prosecutors.

The raid comes just four days after the body of Valentin (Val) Broeksmit, 46, was discovered at about 7 a.m. Monday at Woodrow Wilson High School in El Sereno, just outside of Los Angeles. Val Broeksmit was the son of William Broeksmit who was found hanged in his London home on January 26, 2014. The senior Boreksmit was a senior executive at Deutsche Bank involved in assessing risk on the bank’s balance sheet. (See our report: Documents Emerge in Senate Hearing from William Broeksmit, Deutsche Exec Alleged to Have Hanged Himself in January.)

According to a profile of Val Broeksmit written by David Enrich in the New York Times on October 1, 2019, the younger Broeksmit had obtained “a cache of confidential bank documents” left by his father that provided a “tantalizing” look into the internal workings of Deutsche Bank. Val Broeksmit was sharing the documents with the FBI.

Enrich explains what was going on around Deutsche Bank at that time:

“Federal and state authorities were swarming around Deutsche Bank. Some of the scrutiny centered on the lender’s two-decade relationship with President Trump and his family. Other areas of focus grew out of Deutsche Bank’s long history of criminal misconduct: manipulating markets, evading taxes, bribing foreign officials, violating international sanctions, defrauding customers, laundering money for Russian billionaires.”

Russian billionaires are now back in the news and Donald Trump is being fined $10,000 per day for failure to turn over documents to the New York State Attorney General’s office.

David Enrich had written an earlier piece in May of 2019 for the New York Times describing how a Deutsche Bank whistleblower, Tammy McFadden, and four of her colleagues, had their efforts blocked by the bank when they tried to file suspicious activity reports on bank accounts affiliated with Donald Trump and his son-in-law/advisor Jared Kushner. The suspicious activity reports (SARs) should have been filed with the Federal agency known as FinCEN (Financial Crimes Enforcement Network) but were quashed by a unit of the bank that manages money for the super wealthy.

The coroner has not yet released a cause of death for the younger Broeksmit. His father’s death was ruled a suicide. The two Broeksmits are not the only individuals connected to Deutsche Bank to have turned up dead. On October 24, 2014 the body of Calogero Gambino, 41, was found by his wife hanging from a stairway banister in their Manhattan home. Gambino was a lawyer for Deutsche Bank who had been cooperating with U.S. regulators on Deutsche Bank’s involvement in the rigging of the interest rate benchmark, Libor.

Nor is this the first time that Deutsche Bank’s headquarters have been raided. As we previously reported, on November 29, 2018, Deutsche Bank’s headquarters in Germany were raided by 170 members of law enforcement. Prosecutors said at the time that “Deutsche Bank helped customers found offshore organizations in tax havens by transferring illegally acquired money without alerting authorities to suspected money laundering.” On September 24, 2019 the German police raided Deutsche Bank headquarters for the second time in less than a year.

Deutsche Bank is a major derivatives counterparty to Wall Street’s mega banks. The Bank was having serious problems throughout 2019 and in the days before its trading unit, Deutsche Bank Securities Inc., began to secretly tap trillions of dollars in cumulative loans from the Fed’s repo loan bailout facility.

Deutsche Bank’s attempt to merge with Commerzbank fell through in April 2019. It announced a plan to fire 18,000 workers in July 2019 and had plans to create a good bank/bad bank, isolating off toxic assets that it planned to sell. Deutsche Bank had incurred losses in three of the prior four years. Its share price had lost 90 percent of its value over the prior dozen years and was trading close to an historic low in September 2019. The Monday after the emergency repo loan operations began, Deutsche Bank announced that it would be moving clients and staff from its prime broker unit (that makes loans to hedge funds) to BNP Paribas along with its electronic trading operations.

Newly released documents from the Fed show that on September 17, 2019, the first day of the Fed’s emergency repo loan operations, Deutsche Bank borrowed $1.5 billion in a one-day loan. By September 24, Deutsche Bank had upped its one-day repo loans to $7 billion. By September 25, Deutsche Bank increased its one-day borrowing to $9 billion. On September 27, Deutsche Bank took a $3 billion 14-day term loan and rolled over $6 billion in a 3-day loan.

Later documents released by the Fed show that Deutsche Bank borrowed a cumulative, term-adjusted total of $1.39 trillion from the Fed’s repo loan program in the fourth quarter of 2019 and another $1.24 trillion in the first quarter of 2020. The Fed will release data for the second quarter of 2020 on June 30 of this year. The Fed is releasing the information on a quarterly basis following a two-year lag.

Deutsche Bank units were also secretly bailed out by the Fed during and after the 2008 financial crisis. According to an audit conducted by the Government Accountability Office, Deutsche Bank units borrowed a total of $354 billion in cumulative loans from the Fed’s bailout programs, with the bulk of that amount coming from the Term Securities Lending Facility (TSLF) which ran from March 11, 2008 through February 1, 2010.

As Wall Street On Parade has previously reported, Deutsche Bank has also acquired an unseemly history of fines for its illicit activities. Below is a sampling:

April 23, 2015: Deutsche Bank pleads guilty to the U.S. Department of Justice for its role in rigging the benchmark interest rate known as Libor. It pays fines of $2.519 billion to various regulators.

January 17, 2017: Deutsche Bank reaches a settlement with the U.S. Department of Justice in which it agrees to pay $7.2 billion in fines and restitution for its improper “packaging, securitization, marketing, sale and issuance of residential mortgage-backed securities (RMBS) between 2006 and 2007.”

January 30, 2017: Deutsche Bank is fined a total of $630 million by U.S. and U.K. regulators over claims it laundered upwards of $10 billion on behalf of Russian investors.

January 29, 2018: Deutsche Bank is ordered to pay $30 million by the Commodity Futures Trading Commission for manipulating trading in the precious metals market.

November 8, 2019: Nomura and Deutsche Bank, along with numerous employees, were convicted in a trial in Italy for helping the Tuscan bank, Monte dei Paschi di Siena, commit fraud in derivatives deals to help it hide losses.

January 18, 2020: The Commodity Futures Trading Commission fines Deutsche Bank $10 million to settle two cases: one involving failure to properly report swap transactions and the other for spoofing.

July 7, 2020: The New York State Department of Financial Services settles a state civil matter with Deutsche Bank for $150 million over its involvement with child sex trafficker Jeffrey Epstein.

October 13, 2020: The Frankfurt, Germany Public Prosecutor’s Office fined Deutsche Bank €13.5 million for failing to submit Suspicious Activity Reports in a timely fashion regarding potential money laundering activities.

January 8, 2021: The Justice Department and Securities and Exchange Commission settle charges against Deutsche Bank for $120 million for violating the Foreign Corrupt Practices Act. The charges related to paying bribes to foreign officials to obtain business.

Why the Fed continues to prop up a serial miscreant is a question that every concerned American should be asking their representatives in Congress.

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

A must read

Ed Steer

Ed Steer: The nearly comprehensive complicity in monetary metals price suppression

Submitted by admin on Thu, 2022-04-28 11:37Section: Daily Dispatches

Canadian mining and media mogul and zillionaire Frank Giustra, quoted below in an excerpt from GATA board member Ed Steer’s market letter today, has declined over the years several requests to help GATA or just acknowledge its work. But then as a respectable figure in the world’s financial establishment and a pal and major financial benefactor of former President Bill Clinton —

— Giustra would have a lot to lose by doing anything to liberate the monetary metals markets and thereby liberate all markets.

* * *

By Ed Steer

Ed Steer’s Gold and Silver Digest

Thursday, April 28, 2022

Here’s a Tweet from Frank Giustra via Daniela Cambone [of Stansberry Research] that I found on Wall Street Silver yesterday evening. I thought it worth sharing.

“I have never been a fan of conspiracies but my 45 years’ experience in trading markets tells me that someone is deliberately suppressing the gold price, especially in the past two years. I suspect we will see a reset in the global monetary system some time soon.”

This isn’t the first time Giustra has made this remark, as I heard him say it live at one of the Vancouver investment conferences years ago, when he stated virtually the same thing on stage:

https://www.gata.org/node/17223

The fact of the matter is that the entire precious metals industry knows that the price fix has been in for decades but refuses to say so in public, or lift a finger to do anything about it.

That includes all the miners, with the notable exception of Keith Neumeyer at First Majestic Silver, plus a decent percentage of the so-called precious metal “analysts” out there, with Peter Schiff, Doug Casey, and Rick Rule being the poster boys for that. But there are many others besides them.

They are being intellectually dishonest and hypocritical — and their silence or denial has not helped our cause.

But they aren’t at the top of the list of enemies of free-market prices for the precious metals. That place is reserved for the World Gold Council and the Silver Institute. Their very purpose, as GATA’s Chris Powell said long ago, is to ensure that real world gold or silver councils never spring up — councils that work in the best interests of the miners.

Both these organizations — and a decent number of their members — are controlled or infested by the Deep State and their ilk. They have no interest whatsoever in pursing the truth, even though it is now obvious to all.

That’s one of the reasons that Keith pulled First Majestic out of the Silver Institute. I’m sure he was hoping to change things but the Silver Institute obviously wasn’t interested.

As a group all these organizations, miners, and so-called precious metal “experts” are no more than silent co-conspirators in this decades-long price management scheme. By their very silence or denial they are all complicit.

END

Your weekend reading material

(Alasdair Macleod/GATA)

Alasdair Macleod: Building a better banking system

Submitted by admin on Thu, 2022-04-28 12:54Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, April 28, 2022

This article anticipates the rapidly approaching time when we might be engulfed in a combined currency, asset, and banking crisis. It is becoming clear that such an event can no longer be ruled out.

Economists of the Austrian school have argued that sound money would have prevented a crisis of this sort, and without it the crisis becomes inevitable. The argument for sound money, in other words, a credible gold coin exchange system for banknotes, has already been made. But the question remains over how bank credit, whose fluctuations for a long time have been behind the boom and bust of the business cycle, should be addressed.

Some Austrians argue in favour of a dual banking system, split into separate functions of custodians of deposits and arrangers of finance. They say this arrangement would banish bank credit expansion and the destructive business cycle with it.

But credit creation is not restricted to banks and is common in all economic activities. Banning banks from dealing in credit cuts across established law over credit which has evolved since Roman times. By doing so, banks of deposit would probably fail as a permanent solution and could turn out to be impractical as well.

I suggest that there is a better answer, which is to remove limited liability status from banks and other dealers in credit. They would be less likely to carry excessive balance sheets relative to their own capital. This simple measure would have the merit of making credit available without the excesses we have seen in the past and render much of current banking regulation unnecessary. …

… For the remainder of the analysis:

END

Tennessee becomes the 42 state to end sales taxes on gold and silver

(Gleason/MME/GATA)

Tennessee becomes 42nd state to end sales taxes on gold and silver

Submitted by admin on Thu, 2022-04-28 13:05Section: Daily Dispatches

By Stefan Gleason

Money Metals Exchange, Eagle, Idaho

via Coin Week, Ormond Beach, Florida

Thursday, April 28, 2022

Both houses of the Tennessee legislature yesterday overwhelmingly passed bills that would make the Volunteer State the 42nd state in the U.S. to remove sales taxes from constitutional sound money — gold and silver).

The Tennessee House’s Bill 1874 and Senate Bill 1857, introduced by Rep. Bud Hulsey and Sen. Frank Niceley, now head to Governor Bill Lee for approval. The new precious metals sales tax exemption will take effect immediately upon the governor’s signature.

Overwhelming grassroots support appears to have tipped the balance in this long-running effort in Tennessee. During the Senate vote, Sen. Janice Bowling commented, “I’d like to thank the senator for carrying this bill and also half of the state of Tennessee that contacted us.” …

… For the remainder of the report:

END

Extremely important!! The Kremlin now confirms their intention to back the rouble with gold and commodities

(Ronan Manly/GATA)

Ronan Manly: Kremlin confirms intention to back the ruble with gold and commodities

Submitted by admin on Thu, 2022-04-28 20:14Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Thursday, April 28, 2022

On Tuesday, April 26, in an interview with newspaper Rossiyskaya Gazeta, the secretary of the Russian Federation’s Security Council, Nikolai Patrushev, said that Russian experts are working on a project to back the Russian ruble with gold and other commodities.

The interview, which is in Russian, can be seen on the newspaper’s website here:

For those who don’t know the name Nikolai Patrushev, he is one of the Russia’s most powerful security and intelligence officers and a close ally of President Vladimir Putin. After serving between 1999 and 2008 as director of the Russian Federal Security Service (the successor to the KGB), Patrushev became secretary of the Russian Security Council. In fact, Patrushev took over as sirector of the FSB in 1999 from Putin.

The Security Council of the Russian Federation is chaired by Putin, with Patrushev as secretary, overseeing the Security Council and answering directly to Putin. The deputy chairman of the Security Council is Dmitry Medvedev, the former Russian president and prime minister. Among the other members of the Security Council are the current Russian prime minister, Mikhail Mishustin, and Russian foreign minister Sergei Lavrov.

So when Nikolai Patrushev says that Russia is working on a plan to back the ruble with gold and commodities, it is not just anyone saying this. It is being said at the highest echelons of the Russian government. …

… For the remainder of the report:

END

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES PALM OIL

end

COMMODITIES IN GENERAL//DIAMONDS

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.5880

OFFSHORE YUAN: 6.6198

HANG SANG CLOSED UP 813.22 PTS OR 4.01%

2. Nikkei closed UP 461.29 PTS OR 1.75%

3. Europe stocks ALL GREEN

USA dollar INDEX DOWN TO 103.03/Euro RISES TO 1.0562

3b Japan 10 YR bond yield: RISES TO. +.213/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.93/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.911%/Italian 10 Yr bond yield RISES to 2.76% /SPAIN 10 YR BOND YIELD RISES TO 1.94%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.85: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO : 3.33

3j Gold at $1918.40 silver at: 23.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

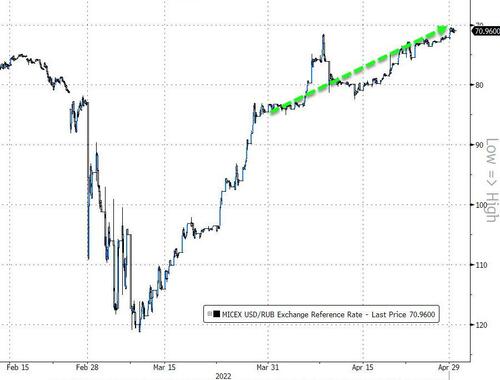

3k USA vs Russian rouble;// Russian rouble UP 1 AND 40/100 roubles/dollar; ROUBLE AT 70.68

3m oil into the 106 dollar handle for WTI and 108 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.93 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9714– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0257well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

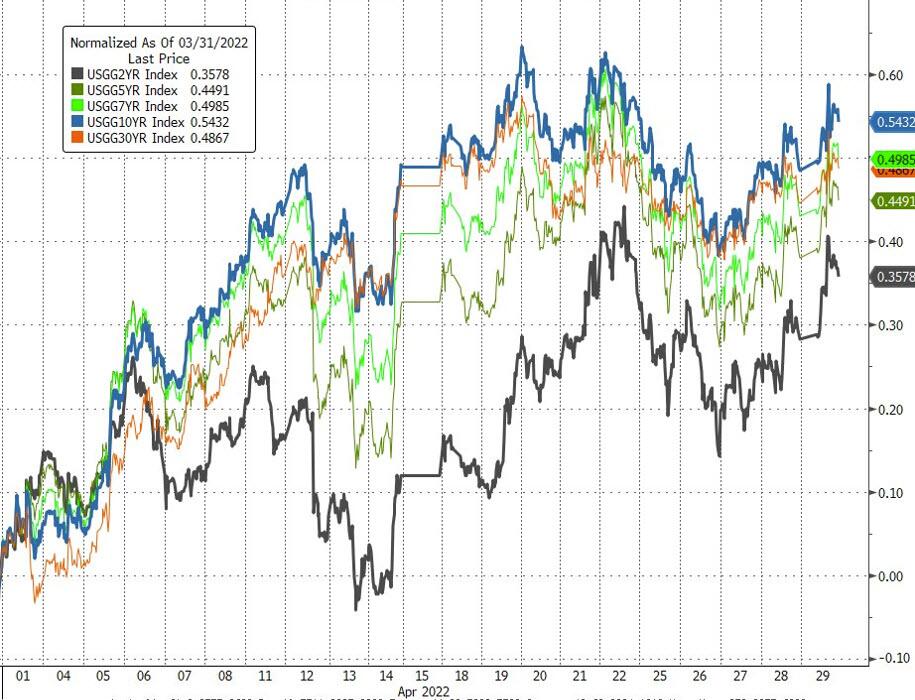

USA 10 YR BOND YIELD: 2.858 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 2.922 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.83

Futures Slide As Amazon, Apple Slump; Nasdaq Set For Worst Month Since Nov 2008

FRIDAY, APR 29, 2022 – 07:33 AM

It has been an illiquid, rollercoaster session on the last day of the week and month, which first saw US index futures modestly rise alongside European stocks propped up by surging Chinese and Asian markets following Beijing’s latest vow to use new tools and policies to spur growth, however the initial move higher quickly faded as markets remembered that not only did Amazon report dismal earnings (with Apple also sliding on weak guidance) but the Fed is set to hike 50bps (or maybe 75bps) next week, and put a lit on any upside follow through. As a result, S&P500 futures dropped 0.9%, while Nasdaq futures retreated 1.1% on the last trading day of April, adding to their 9.3% decline so far this month and on pace for the worst monthly performance since November 2008 as fears of rising rates hurt bubbly growth shares and fuel risks for future profits. The yen snapped a slide while staying near 20-year lows. The yuan, euro, pound and commodity-linked currencies made gains while the dollar dipped. 10Y TSY yields rose, rising by about 4bps to 2.87% while gold moved back above $1900. Bitcoin tumbled as usual, and last traded back under $39,000.

In premarket trading, Amazon.com plunged 9%, after projecting dismal second-quarter sales growth, while the world’s largest company Apple dropped 2.8% after warning on supply constraints. Tesla shares gained 4.2% premarket after CEO Elon Musk said he doesn’t plan on selling any more stock after a $4 billion stake sale. Twitter shares also rebounded from yesterday’s selloff as a Musk takeover now looks much more likely. Here are some other notable premarket movers:

- Intel (INTC US) shares slide 3.1% premarket as analysts flag “light” guidance for the chipmaker’s second quarter, stoking worries over the impact of waning demand for PCs. Intel’s second-quarter forecast missed the average estimate.

- Robinhood (HOOD US) shares are set to open at a record low Friday as a lockdown-driven boom in retail trading continues to fade and a stock market selloff squeezes out some clients.

- Tesla (TSLA US) shares rise as much as 4.2% premarket, after CEO Elon Musk said he doesn’t plan on offloading any more Tesla stock after selling ~$4b of shares in the electric vehicle maker following his deal to buy Twitter.

- Accolade (ACCD US) plummets 36% premarket after the company’s 2023 revenue forecast fell short of estimates, with Morgan Stanley downgrading the healthcare software provider to equal-weight after the loss of a key customer.

- Finch Therapeutics (FNCH US) shares soar as much as 54% premarket after the biotech announced that the FDA removed the clinical hold on Finch’s investigational new drug application for CP101.

- Piper Sandler cut its recommendation on Mastercard (MA US) to underweight, becoming the first broker to downgrade the company with a sell-equivalent rating since August. Shares down 1.1% premarket.

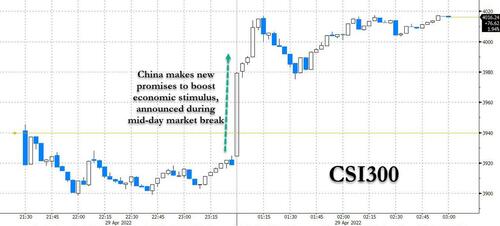

- U.S.-listed Chinese stocks rally across the board in premarket trading after China’s top leaders pledged more support to spur economic growth and vowed to contain Covid outbreaks. Alibaba (BABA US) +13%, JD.com (JD US) +16%.

- Zymeworks (ZYME US) climbs 30% premarket; All Blue Capital made a non-binding offer at $10.50 per share in cash for the biotech company, Reuters reports, citing people familiar with the matter.

Outside of the flagship tech giant earnings misses, the results season has been reassuring so far. S&P 500 earnings growth is tracking 4.3% year-on-year, with 86% of companies beating estimates, according to Barclays strategists. “With continued solid U.S. growth prospects, robust earnings, and relatively strong household balance sheets, a recession in the next 12 months is not in our base case,” said UBS Wealth Management CIO Mark Haefele.

Meanwhile, as reported earlier, China’s top leaders promised to boost economic stimulus to spur growth. While China’s announcement brought some relief for markets, many risks remain. They span China’s ongoing Covid challenges, the impact of the Fed on the U.S. economy and Russia’s war in Ukraine.

“The Fed’s record on soft landings is not that strong,” Carol Schleif, deputy chief investment officer at BMO Family Office LLC, said on Bloomberg Television. “Markets are watching very, very carefully to see if we can thread that needle.”

The latest U.S. data showed that the world’s largest economy unexpectedly shrank for the first time since 2020. That reflected an import surge tied to solid consumer demand, suggesting growth will return imminently. The figures underscore the debate about how much scope the U.S. central bank has to tighten policy before the economy cracks. Markets continue to project a half-point Fed rate hike next week.

“A year from now, 10-year yields are most likely going to be lower than where we are today,” Jimmy Chang, chief investment officer at Rockefeller Financial LLC, said on Bloomberg Television, referring to Treasuries. “I do believe at some point the economy starts to weaken, the Fed will be less hawkish, perhaps even go into a pause mode by, say, early next year.”

Meanwhile, China’s latest vow to prop up markets helped support European stocks (in addition to Asian and Chinese stocks of course), also spurred by a robust earnings season. The Stoxx Europe 600 Index climbed 0.8%, trimming a monthly decline. The Euro Stoxx 50 gains as much as 1.5% with most cash equity indexes gaining over 1% before stalling. Tech, consumer products and financial services are the strongest performing sectors. Here are some of the biggest European movers today:

- Novo Nordisk shares gain as much as 7.3% after the Danish pharmaceutical giant reported its latest earnings, which included a large beat on its blockbuster obesity drug Wegovy. The company also hiked its outlook.

- BBVA rises as much as 5.6% after better-than-expected first-quarter earnings, as the Spanish lender’s performance in Turkey showed signs of vindicating Chief Executive Officer Onur Genc’s bet on the country.

- Johnson Matthey jumps as much as 36%, the steepest gain since at least 1989 when Bloomberg’s records started, after Standard Industries Inc. bought a stake in the company.

- Remy Cointreau climbs as much as 3.8% after the French distiller reported 4Q sales that were in line with consensus. Analysts noted the strong start to the current fiscal year and a limited impact so far from a Covid-19 resurgence in the key Chinese market.

- Spie shares climb as much as 5.1% after the French company reported 1Q figures that Bryan Garnier said were “substantially” above expectations, with planned European investments for energy independence also viewed as a potential headwind.

- AstraZeneca shares decline as much as 1.3% after the company’s first-quarter earnings included a beat on core EPS and overall revenue, but also a slight miss on Alexion rare disease medication and key growth drugs such as Imfinzi.

- Neste falls as much as 8.7% even as the Finnish maker of renewable diesel reported first-quarter results that beat estimates. Jefferies (hold) said the lack of longer-term (full-year 2022) margin guidance could disappoint.

- Henkel tumbles as much as 10% after what RBC says was a “substantial profit warning” for 2022.

- NatWest falls as much as 6% after its 1Q results got a mixed response from analysts. Some were impressed with the performance of the bank’s Go-Forward business, while others highlighted the very low mortgage spread and miss in the CET1 capital ratio.

- Orsted drop as much as 3.2% despite reporting a 1Q profit beat, with analysts focusing on the project delays due to supply chain shortages as well as the impact of high input costs.

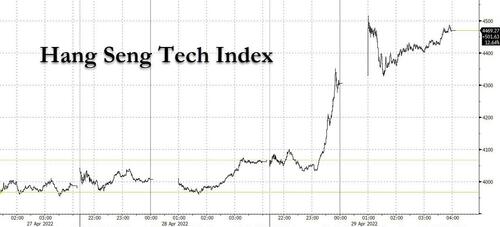

Earlier in the session, Asian stocks climbed for a second day led by a jump in Chinese technology shares, amid a series of new policy promises from the country’s top leaders to bolster the economy and markets. The MSCI Asia Pacific Index advanced as much as 1.7%, with Tencent and Alibaba among the biggest gainers. The Hang Seng Tech Index soared more than 10%, rebounding from earlier losses, as the country vowed to support healthy growth of platform companies. As reported earlier, China’s Politburo, led by President Xi Jinping, vowed to meet economic targets in a sign that it may step up stimulus to support growth. Shortly before the measures were unveiled, Chinese tech stocks reversed earlier losses as traders speculated about a possible relaxation of the yearlong regulatory clampdown. Chipmakers in Taiwan and South Korea also climbed, helping the region’s tech sector. A Bloomberg index of Asian semiconductor stocks rallied as much as 2.4%, its biggest gain in more than two weeks. A key technical indicator suggested that the sector is still oversold after Intel’s disappointing profit forecast.

“After recent selloffs in the semiconductor sector, the price levels have become attractive for dip buyers,” said Seo Jung-Hun, a strategist at Samsung Securities, adding that the rebound may be limited ahead of the U.S. Federal Reserve meeting next week. Stocks in South Korea, Taiwan and Australia advanced while those in Japan were closed for a holiday. Asia’s equity benchmark was still poised for its steepest monthly drop since March 2020 and its fourth monthly decline.

Australian stocks also advanced, paring the week’s decline. The S&P/ASX 200 index rose 1.1% to 7,435.00, paring the week’s loss. Technology and communications sectors gained the most Friday. Pointsbet gained the most in almost a month, snapping a five day losing streak after reporting turnover for the third quarter. Domino’s Pizza fell for a fourth day, dropping the most in a month. New Zealand, the S&P/NZX 50 index was little changed at 11,884.30.

India’s benchmark equities index completed a third monthly slide this year as higher oil prices weighed on sentiment. The S&P BSE Sensex fell 0.8% to 57,060.87 in Mumbai on Friday, taking its loss in April to 2.6%. Axis Bank Ltd. dropped 6.6% after reporting earnings and was the biggest drag on the Sensex, which saw 23 of 30 member-stocks fall. The NSE Nifty 50 Index also slipped 0.8% to 17,102.55. All 19 sectoral sub-indexes compiled by BSE Ltd. slipped, led by a gauge of oil and gas companies. “We’ve been seeing the index oscillating in a broader range for the last two weeks and there’s no clarity over the next directional move yet,” Ajit Mishra, vice president for research at Religare Broking Ltd., wrote in a note. The brokerage maintains a cautious view, with focus on earnings, auto sales data and the initial share sale of Life Insurance Corporation next week. Of the 15 Nifty 50 firms that have announced earnings results so far, 10 either met or exceeded analysts’ expectations, while five missed.

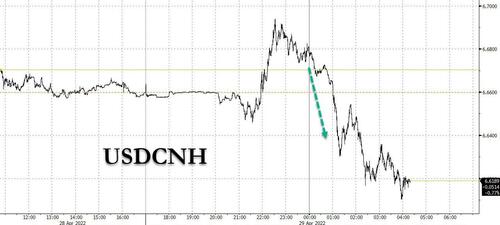

In FX, the Bloomberg Dollar Spot Index fell after touching an almost two-year high yesterday as the greenback weakened against all of its Group-of-10 peers. Treasuries underperformed European bonds, with 3-year yields rising by 7bps. Scandinavian currencies were the top performers as they were supported by month-end flows. The Australian dollar extended intra-day gains after China’s top leaders promised to boost economic stimulus to spur growth and vowed to contain the country’s worst Covid outbreak since 2020, which is threatening official targets for this year. The euro snapped six days of losses against the dollar but was still set for its worst monthly performance in almost four years. Bunds extended losses and yields rose by up to 5 bps after data showed euro-area consumer prices rose by 7.5% from a year earlier in April, in line with the median estimate in a Bloomberg survey. A gauge excluding volatile items such as food and energy jumped to 3.5%. The pound advanced against the dollar, trimming a weekly decline of 2.2%. The cost of hedging against swings in the pound over a one-week period rose to the highest since December 2020. Gilts outperformed bunds and Treasuries, as money markets pared BOE tightening wagers. The yen rose on demand over the currency fix in Tokyo but it remains on track for its worst monthly performance since 2016

In rates, Treasuries hold losses into the U.S. session leaving yields down by as much as 6bps across front-end as the curve flattens. 10-year TSY yields were around 2.86%, cheaper by 4bp vs. Thursday close while 2s10s, 5s30s spreads flatten 2bp and 2.5bp amid front-end and belly-led weakness. German short-end cheapens roughly 5 bps to 0.24% as euro-area core inflation accelerated higher than expected. In Europe, peripherals underperform and lead bond losses while Estoxx50 climbs following better sentiment across Asia stocks after China’s pledge to ramp up stimulus. Dollar issuance slate empty so far; two names priced $4.5b Thursday, taking weekly volumes through $8b vs. $20b forecast. Expectations are for $20b to $25b next week and a total of $125b to $150b for the month of May

In commodities, WTI rose 1.2% higher to trade near $107. Saudi Aramco is expected to lower its official selling prices for June-loading crudes, market sources told S&P Global Commodity Insights; following tepid Asian demand fundamentals, with the OSP differentials retreating from the record highs. North Sea Crude oil grades underpinning dated Brent Benchmark to average 540k BPD in June (prev. 755k BPD), according to programmes. Indian firms are reportedly seeking oil import deals with Russia, according to sources cited by Reuters; three refiners looking to buy up to 16mln bbl per month of oil from Russia. Spot gold rises roughly $20 to trade around $1,915/oz. Most base metals trade in the green.

Bitcoin prices are softer as usual and briefly retreated beneath the 39,000 level.

Looking at the day ahead now, and data releases include the flash CPI estimate for the Euro Area in April, as well as the first look at Q1 GDP for the Euro Area, Germany, France and Italy. Otherwise from the US, we’ll get March’s data on personal spending and personal income, the Q1 employment cost index, the NI Chicago PMI for April, and the University of Michigan’s final consumer sentiment index for April. From central banks, we’ll hear from the ECB’s de Cos, and the Central Bank of Russia will be making its latest policy decision. Finally, earnings releases include ExxonMobil, Chevron, AbbVie, Bristol-Myers Squibb, Honeywell International, Charter Communications, Aon and NatWest.

Market Snapshot

- S&P 500 futures down 0.9% to 4,242.00

- STOXX Europe 600 up 1.0% to 451.55

- MXAP up 2.0% to 169.00

- MXAPJ up 2.6% to 561.33

- Nikkei up 1.7% to 26,847.90

- Topix up 2.1% to 1,899.62

- Hang Seng Index up 4.0% to 21,089.39

- Shanghai Composite up 2.4% to 3,047.06

- Sensex up 0.5% to 57,796.94

- Australia S&P/ASX 200 up 1.1% to 7,435.01

- Kospi up 1.0% to 2,695.05

- German 10Y yield little changed at 0.88%

- Euro up 0.7% to $1.0574

- Brent Futures up 0.9% to $108.51/bbl

- Brent Futures up 0.9% to $108.51/bbl

- Gold spot up 1.1% to $1,915.10

- U.S. Dollar Index down 0.66% to 102.94

Top Overnight News from Bloomberg

- More than six years after China’s shock 2015 devaluation roiled global markets and spurred an estimated $1 trillion in capital flight, the yuan is weakening at a similar pace. Onshore it’s lost nearly 4% in eight days, while the offshore rate is heading for its worst month relative to the greenback in history. Selling momentum is the strongest since the height of Donald Trump’s trade war in 2018

- Geopolitical turmoil is reviving the dollar’s status as a haven, extending gains seen earlier this year as traders shifted to the U.S. to seize on rising interest rates from the Federal Reserve. On Thursday, one gauge of the greenback pushed through to the strongest level since 2002, swept up by a wave of demand for the world’s reserve currency

- Russia’s war with Ukraine may persuade the Swiss National Bank to adjust its monetary policy if inflation accelerates, SNB President Thomas Jordan said

- Economic expansion in the euro zone began 2022 on a weak footing — underscoring the damage from soaring energy costs and worsening supply snarls following Russia’s invasion of Ukraine. Output increased 0.2% from the previous quarter in the three months through March — matching the median estimate in a Bloomberg survey

- U.K. house prices rose for a ninth consecutive month in April as the housing market continued to defy an escalating cost of living crisis. The 0.3% gain marked the longest winning streak since 2016

- Oil is poised for a fifth monthly gain after another tumultuous period of trading that saw prices whipsawed by the fallout from Russia’s war in Ukraine and the resurgence of Covid-19 in China

A More detailed look at global markets courtesy of Newsquawk

APAC stocks gained after the firm lead from the US where stocks looked past the surprise contraction in US GDP, but with advances in the region capped heading into month-end and next week’s mass closures. ASX 200 was firmer as tech mirrored the outperformance of the Nasdaq stateside and with gold miners following closely behind after the precious metal reclaimed the psychological USD 1900/oz level. Hang Seng and Shanghai Comp were initially indecisive ahead of next week’s holiday closures including in the mainland where markets will remain closed through to Wednesday, while participants also digested the surprise contraction in Hong Kong’s exports and imports data. However, a surge in Hong Kong tech stocks and policy pledges by China’s Politburo helped shake off the indecision.

Top Asian News

- Bets of Easing Crackdown Spur Dizzying Jump in China Tech Stocks

- Grab Gets Malaysia Digital Bank License as Five Bids Win

- CATL Posts Sharp Drop in Earnings in Abrupt Reversal of Fortune

- China Plans Symposium With Big Tech Firms After Labor Day: SCMP

European equities remained on the front foot on the last trading day of the month. In terms of sectors, tech currently stands as the clear outperformer amid the sectoral gains on Wall Street yesterday alongside the surge in Chinese Tech. Overall, sectors have a slight anti-defensive bias. State-side futures were dented overnight amid after-hours losses in Amazon (-9% pre-market) and Apple (-2.4% pre-market) following disappointing guidance and inflationary headwinds. Thus, the NQ (-0.8%) currently lags.

Top European News

- Russia Offers Dual-Payment Plan for Oil, Other Trade With India

- Germany Says Won’t Block Embargo on Russian Oil to Punish Putin

- UBS Wealth Says Too Early to Bet on Recession, Fed’s Failure

- U.K. House Prices Deliver Longest Winning Streak Since 2016

FX

- Dollar bulls book profits into month end and DXY pulls back further from near 104.000 peak in the process.

- High betas, cyclical and activity currencies grab the chance to recoup losses vs Buck.

- Euro rebounds amidst more hot Eurozone inflation data, but could be hampered by big option expiries.

- Yuan regroups as Chinese Government promises stimulus measures and aid for sectors of the economy suffering worst covid contagion

- Central Bank of Russia (CBR) cuts key rate by 300bps to 14.00% (exp. 15.00%); sees key rate in 12.5-14.00% range this year (prev. 9.0-11.0%).

- Russia’s Kremlin, when asked about the idea of pegging the RUB to gold prices, says it is under discussion, according to Reuters.

Fixed Income

- Bonds suffer another inflation setback after early EU rebound.

- Bunds some 100 ticks down from 154.69 peak, Gilts flattish between 119.34-118.73 parameters and 10 year T-note nearer 119-04+ low than 19-24 high.

- BTPs weak after so-so reception at end of month Italian auctions – US PCE data also adds to caution as Fed’s preferred measure of inflation.

Commodities

- WTI and Brent front-month futures have been gaining during the European morning.

- Saudi Aramco is expected to lower its official selling prices for June-loading crudes, market sources told S&P Global Commodity Insights; following tepid Asian demand fundamentals, with the OSP differentials retreating from the record highs. (S&PGlobal)

- North Sea Crude oil grades underpinning dated Brent Benchmark to average 540k BPD in June (prev. 755k BPD), according to programmes.

- Indian firms are reportedly seeking oil import deals with Russia, according to sources cited by Reuters; three refiners looking to buy up to 16mln bbl per month of oil from Russia.

- Spot gold has been rising in tandem with a pullback in the Buck but ahead of the US March PCE metric.

- Overnight, base metals saw gains in Shanghai, with some also citing a demand front-load ahead of the Chinese Labour Day.

US Event Calendar

- 08:30: 1Q Employment Cost Index, est. 1.1%, prior 1.0%

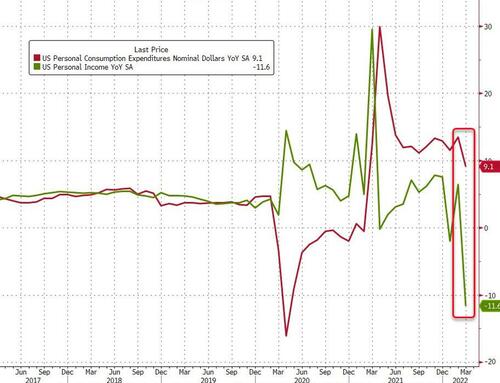

- 08:30: March Personal Income, est. 0.4%, prior 0.5%

- March Personal Spending, est. 0.6%, prior 0.2%

- March Real Personal Spending, est. -0.1%, prior -0.4%

- March PCE Deflator MoM, est. 0.9%, prior 0.6%

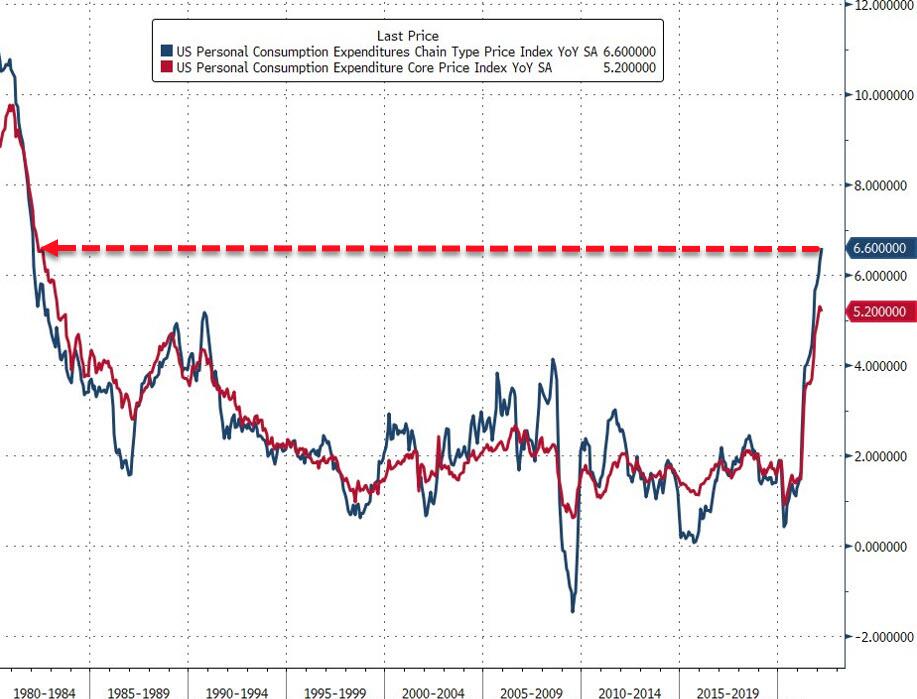

- March PCE Deflator YoY, est. 6.7%, prior 6.4%

- March PCE Core Deflator MoM, est. 0.3%, prior 0.4%

- March PCE Core Deflator YoY, est. 5.3%, prior 5.4%

- 09:45: April MNI Chicago PMI, est. 62.0, prior 62.9

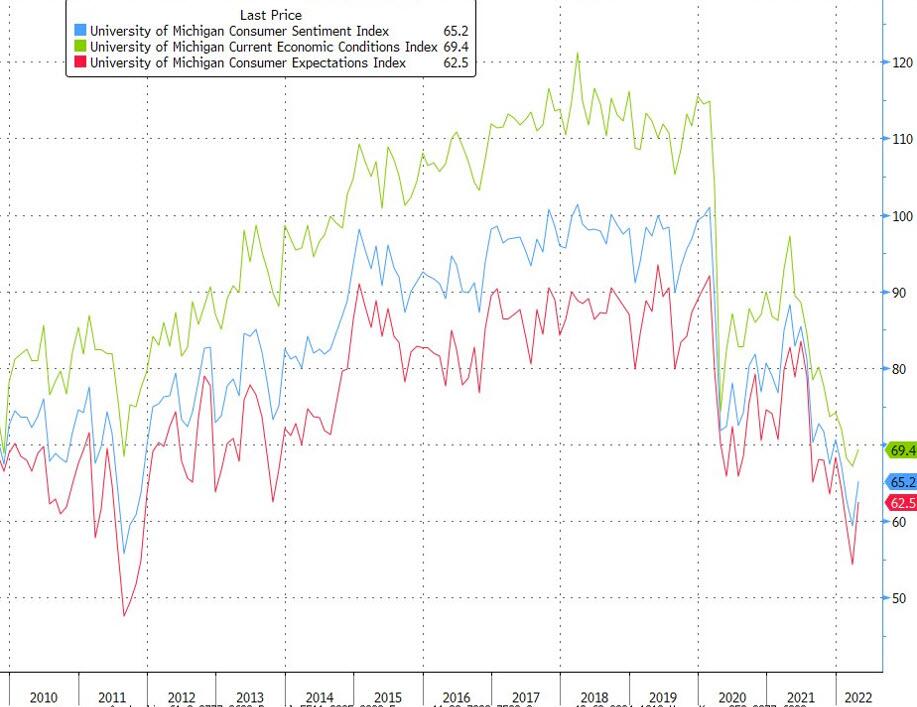

- 10:00: April U. of Mich. Sentiment, est. 65.7, prior 65.7

- U. of Mich. Expectations, est. 64.1, prior 64.1

- U. of Mich. Current Conditions, est. 68.0, prior 68.1

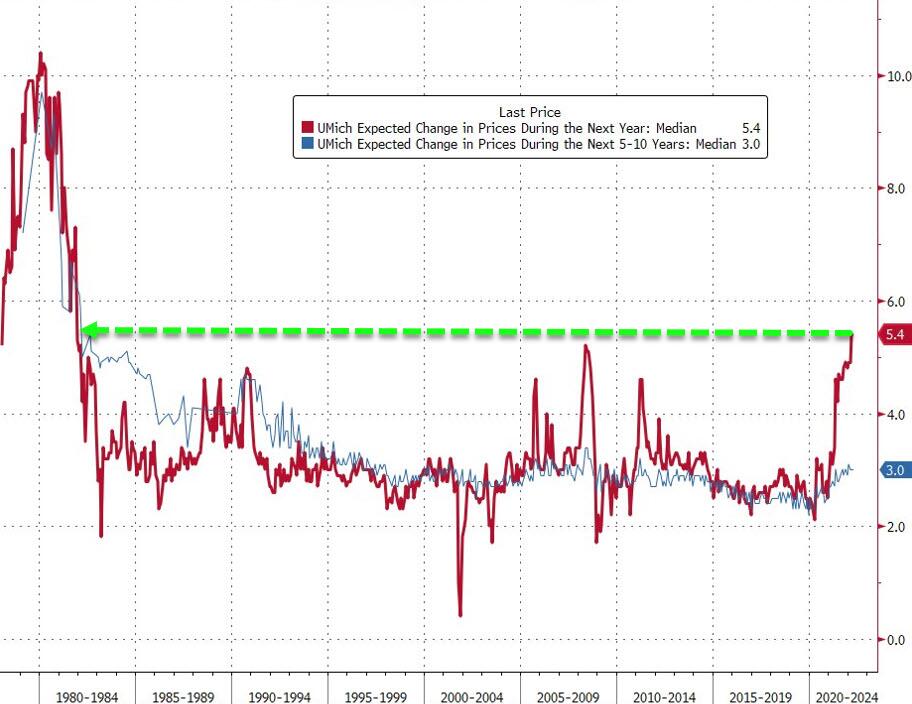

- U. of Mich. 1 Yr Inflation, est. 5.5%, prior 5.4%; 5-10 Yr Inflation, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

By the time you’re reading this I’ll be lying down with straps around my ankles and wrists and making strange noises while I get manipulated by someone very strict. No I’m not remaking “50 Shades” but instead starting “Reformer Pilates” for the first time at a very early physio appointment. The miracle worker of a back consultant that has for now cured my debilitating sciatica with one simple injection has recommended it as a way of preventing a relapse. At this point, I will do absolutely anything he says so I’m prepared to humiliate myself on a regular basis going forward. So feel free to picture this as you read this.

Some of the bearish chains have been loosened in risk markets over the last 24 hours but volatility remains elevated. We’ve seen another major European bond selloff, the highest German inflation since 1950, a further surge in the dollar, an unexpected US economic contraction in Q1, poor Amazon earnings, as well as growing geopolitical tensions as speculation continues about a Russian oil embargo in Europe. In spite of all that however, major equity indices have continued to advance from their Tuesday lows, with the S&P 500 (+2.47%) staging a huge comeback as investors focused on the more positive stories from recent corporate earnings releases.

This was before Amazon missed sales expectations after the bell and revised down sales expectations for the second-quarter, fueling fears that consumer spending may slow despite evidence of robust activity in yesterday’s GDP data. Amazon shares were -9.15% lower after hours. However, Apple reported earnings that beat estimates on strong iPhone sales, despite supply chain issues coinciding with China’s lockdowns. Shares were -2.19% lower after hours. Overall sentiment still remains fragile with NASDAQ 100 futures (-1.04%) and S&P 500 futures (-0.43%) moving lower in the overnight trade.

This followed the best day for the S&P 500 (+2.47%) since the bounceback after the initial invasion in early March, with every sector more than +1.00% higher. Megacap tech stocks led the way as the FANG+ index rose +4.78%, its best day since mid-March. Europe also saw decent gains, although missing most of the rally that took place in the New York afternoon, with the STOXX 600 (+0.62%), the DAX (+1.35%) and the FTSE 100 (+1.13%) all higher. Given the big run-up in the New York afternoon, the S&P 500 was ‘only’ around +0.8% higher as Europe closed.

Bond markets were again lively with most of the action in Europe, with a significant selloff after the German CPI print for April surprised on the upside yet again. Looking at the details, the year-on-year measure rose to +7.8% using the EU-harmonised method (vs. +7.6% expected), which is certainly the fastest pace of inflation since German reunification, and at the same level briefly seen in West Germany after the first oil shock in 1973. Indeed if you’re looking for German inflation faster than that, you’ve got to go all the way back to the 1950s, since West Germany had much more success than the US or UK for example in keeping inflation in the single-digits even during the 1970s. We’ll have to see what the flash CPI reading for the entire Euro Area brings today, but as I mentioned in my Chart of the Day yesterday (link here), this brings home just how far the ECB is behind the curve, since the last time inflation was around these levels in the 70s, the Bundesbank certainly didn’t have a negative deposit rate.

With the inflation reading coming in above expectations, that catalysed a fresh bond selloff that took the 10yr bund yield up by +9.8bps to 0.89%. This echoes some of the other big moves higher in yields we’ve seen over the last couple of months, but it still leaves them beneath the peak of 0.97% at the end of last week. What was also noticeable was the fresh widening in spreads that speaks to the building minor stresses in European markets right now, with the gap between Italian and German 10yr yields up a further +4.2bps to 181bps, a level not seen since June 2020. As in the previous session, those moves were seen in the credit space too, with the iTraxx Crossover widening +3.7bps to 418bps, leaving it just shy of its recent peak at 421bps in early March.

Another cause for concern in European markets have been the ongoing tensions between Russia and the West over Ukraine, with the Euro falling by a further -0.55% yesterday to $1.0499, the first close below $1.05 since early 2017, although this morning it has moved back up to $1.0514. Conversely the dollar index (+0.65%) continued its upward march, strengthening for the 19th time in the last 21 sessions, and closing at its strongest level since 2002. That comes as the latest reports indicate that a Russian oil embargo is moving closer, with Brent crude ending the day up +2.16% at $107.59/bbl after Dow Jones reported that Germany had dropped its opposition to an embargo, and this morning, Brent has risen further to $108.00/bbl. We also heard from President Biden, who requested $33bn from Congress for further assistance to Ukraine, including $20.4bn on security and military assistance, $8.5bn on economic assistance, and $3bn on humanitarian assistance.

Overnight in Asia, equity markets are mostly trading higher following the strong performance on Wall Street, with tech stocks leading the way. The Hang Seng (+2.04%) has seen one of the strongest performances, far outpacing mainland Chinese indices including the Shanghai Composite (+0.37%) and the CSI 300 (-0.06%). That comes amidst persistent concerns over the country’s lockdowns, with Shanghai seeing an increase in Covid-19 cases for the first time in 6 days, and overnight we also heard from China’s Politburo, with CCTV reporting that they’re urging efforts to meet the economic growth targets. Elsewhere, the Kospi (+0.78%) is trading up while markets in Japan are closed for a holiday today.