I will be out for most of the day so today’s report will be relatively small. The comex data is accurate

save for the comex inventory movements which are not important. The 4 pm data will not be provided

and the data shown is yesterday. Also GLD and SLV inventory will b provided, plus closing gold and silver prices..

harvey.

May 3, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 3, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1868.10 up $6.05

SILVER: $22.61up $0.04

ACCESS MARKET: GOLD $1863.30

SILVER: $22.56

Bitcoin morning price: $38,385 UP 52

Bitcoin: afternoon price: $38,333 DOWN 100

Platinum price: closing DOWN $11.50 to $937.95

Palladium price; closing DOWN $110.05 at $2210.70

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/ 6/8

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,861.800000000 USD

INTENT DATE: 05/02/2022 DELIVERY DATE: 05/04/2022

FIRM ORG FIRM NAME ISSUED STOPPED

657 H MORGAN STANLEY 2

661 C JP MORGAN 6

690 C ABN AMRO 1

737 C ADVANTAGE 1

905 C ADM 6

TOTAL: 8 8

MONTH TO DATE: 1,450

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 8 NOTICE(S) FOR 800 OZ (0.02488 TONNES)

total notices so far: 1450 contracts for 145,000. oz (4.510 tonnes)

SILVER NOTICES:

1007 NOTICE(S) FILED 5.035,000 OZ/

total number of notices filed so far this month 2759 : for 13,795,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $6.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES FROM THE GLD.

INVENTORY RESTS AT 1092.23 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 47 CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A DEPOSIT OF .878 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 576.049 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 1227 CONTRACTS TO 137,176 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.47 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.47) BUT WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A HUGE GAIN OF 3313 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 370,000 OZ EFP JUMP TO LONDON//NEW STANDING 28.505 MILLION OZ/ // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-xxx

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 2 days, total 3621, contracts: 18.105 million oz OR 9.0525 MILLION OZ PER DAY. (1810CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 18.105 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 18.105 MILLION OZ//

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1227 DESPITE OUR $0.47 LOSS IN SILVER PRICING AT THE COMEX// MONDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1885 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 370,000 MILLION OZ EFP TO LONDON//NEW STANDING 28.505 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 3313 OI CONTRACTS ON THE TWO EXCHANGES FOR 16.565 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 1007 NOTICES FILED TODAY FOR 5,035,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1106 CONTRACTS TO 560,166 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –521 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE SMALL SIZED DECREASE IN COMEX OI CAME DESPITE OUR STRONG LOSS IN PRICE OF $46.20//COMEX GOLD TRADING/MONDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 20,300 OZ//NEW STANDING 6.1866 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR LOSS IN PRICE OF $46,20 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 3719 OI CONTRACTS (11.527 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 4825 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 560,166.

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3719, WITH 1106 CONTRACTS DECREASED AT THE COMEX AND 4825 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3719 CONTRACTS OR 11.567 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4825) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1106,): TOTAL GAIN IN THE TWO EXCHANGES 3719CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 20,300 OZ//NEW STANDING 6.1866 /// 3) ZERO LONG LIQUIDATION //.,4) SMALL SIZED COMEX OI. LOSS 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

6561 CONTRACTS OR 656,100 OR 20.407 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 3281 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 20.407 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 20.407/3550 x 100% TONNES 0.574% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 20.41 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1227 CONTRACT OI TO 137,176 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1885 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1885 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1428 CONTRACTS AND ADD TO THE 1885 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 3112 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.679 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.47 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED UP 12.50 OR 06% /The Nikkei closed //Australia’s all ordinaires CLOSED DOWN 0.47% /Chinese yuan (ONSHORE) closed DOWN 6.6084 /Oil UP TO 103/82 dollars per barrel for WTI and UP TO 106.47 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6064 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6821: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1106 CONTRACTS TO 560,166 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR GAIN OF $46.20 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2844 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4825 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :4825 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4825 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4240 CONTRACTS IN THAT 4825 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A TINY SIZED COMEX OI LOSS OF 585 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR STRONG LOSS IN PRICE OF GOLD $46.20.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (6.1866),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 6.1866 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $46.20) AND WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A STRONG SIZED GAIN OF 13.188 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (6.1866 TONNES)…

WE HAD 521 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3719 CONTRACTS OR 371900 OZ OR 11.517TONNES

Estimated gold volume today: 97,601/// extremely poor

Confirmed volume yesterday:188,075 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 3

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 25,752.951 ozManfra801 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 8 notice(s)800 OZ0.02488 TONNES |

| No of oz to be served (notices) | 539 contracts 53,900 oz1.6765 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1450 notices145,000 OZ4.510 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

2 customer deposits

i) Into HSBC 48,226.500 oz (15,000) kilobars)

ii) Into JPMorgan: 64,334.151 oz (2001 kilobars)

1 customer withdrawals:

i) out of Brinks 200.02 oz

total withdrawal: 200.02 oz

ADJUSTMENTS: 3/ customer to dealer

i) Brinks 15,023.590 ox

ii) Manfra: 5693.190 oz

iii) 6172.992 oz (removed) jpmorgan//192 kilobars

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 547 contracts having GAINED 149 contracts

We had 54 notices filed on Monday, so we gained 203 contracts or 20,300 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 6248 contracts down to 437,730 contracts

July has a gain of 2 OI to stand at 7

August has a gain of 5067 contracts up to 71,757 contracts

We had 54 notice(s) filed today for 5400 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 8 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1450) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 547 CONTRACTS ) minus the number of notices served upon today 8 x 100 oz per contract equals 178,600 OZ OR 5.555 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1450) x 100 oz+ (547) OI for the front month minus the number of notices served upon today (8} x 100 oz} which equals 198,900 oz standing OR 6.1866 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 6.1866 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626,135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,989.255.509 OZ (1119.42 TONNES)

TOTAL ELIGIBLE GOLD: 18,358,705.533 OZ (571.03 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,630,649.576 OZ (548.39 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,689023.0 OZ (REG GOLD- PLEDGED GOLD) 487.99tonnes

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 3

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 861,723.212 ozBrinksCNTManfra |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 1007CONTRACT(S)5,035,000 OZ) |

| No of oz to be served (notices) | 617 contracts (3,085,000 oz) |

| Total monthly oz silver served (contracts) | 2759 contracts 13,795,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 1 deposit into the dealer

i) Into Manfra 116,285.000 oz

total dealer deposits: 116,285.000 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into Brinks 44,630.990 oz

ii) Into JPMorgan: 1,153,260.600 oz

total deposit: 1,197,891.590 oz

JPMorgan has a total silver weight: 174.281 million oz/333.531 million =52.23% of comex

Comex withdrawals: 5

i) Out of CNT 690,254.295 oz

i1) Out of JPMorgan 585,046.500 oz

iii) Out of Delaware: 2173.500 oz

iv) Out of Int. Delaware 90,422.092

v) Out of Manfr: 44,630.990 oz

total withdrawal 1,413,527.377 oz oz

3 adjustments: customer to customer

i) Out of Brinks 24,023.900 oz

ii) Out of Manfra; 4999.659 oz

iii) 965.810 oz removed entire from customer Delaware

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.620 MILLION OZ

TOTAL REG + ELIG. 333.531 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 3949 HAVING LOST 154 CONTRACTS. WE HAD 80 NOTICES FILED ON MONDAY

SO WE LOST 74 CONTRACTS THAT WE EFP’D TO LONDON (370,000 OZ) AS SILVER IS SCARCE OVER HERE.

JUNE HAD A GAIN OF 51 TO STAND AT 1852

JULY HAD A GAIN OF 1197 CONTRACTS UP TO 110,951 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1007 for 5,035,000 oz

Comex volumes: 20,594// est. volume today// extremely poor

Comex volume: confirmed yesterday: 59,058 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 3759 x 5,000 oz = 13,795,000 oz

to which we add the difference between the open interest for the front month of MAY (3949) and the number of notices served upon today 8 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 2759 (notices served so far) x 5000 oz + OI for front month of MAY (3949) – number of notices served upon today (1007) x 5000 oz of silver standing for the MAY contract month equates 28,505,000 oz. .

We lost 74 contracts or 370,000 will not stand for delivery at the comex as these guys were EFP’d to London

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1092.23 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 576.048 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

the big seller of USA treasuries have been the Japanese

(Bloomberg)

Biggest buyer of Treasuries outside U.S. is quietly selling billions

Submitted by admin on Mon, 2022-05-02 11:16Section: Daily Dispatches

By Michael Mackenzie and Chikako Mogi

Bloomberg News

Monday, May 2, 2022

In times of Treasury turmoil, the biggest investor outside American soil has historically lent a helping hand. Not this time round.

Japanese institutional managers — known for their legendary U.S. debt-buying sprees in recent decades — are now fueling the great bond selloff just as the Federal Reserve pares its $9 trillion balance sheet.

The latest data from BMO Capital Markets show the largest overseas holder of Treasuries has offloaded almost $60 billion over the past three months. While that may be small change relative to the Japan’s $1.3 trillion stockpile, the divestment threatens to grow.

That’s because the monetary path between the U.S. and the Asian nation is diverging even more, the yen is plumbing 20-year lows, and market volatility stateside is breaking out. All that is ramping up currency-hedging costs and completely offsetting the appeal of higher nominal U.S. yields, especially among large life insurers.

The upshot: Japanese accounts are contributing to the historic Treasury rout and may not return en masse until the benchmark 10-year yield trades firmly above 3%. In fact, near-zero-yielding bonds at home look ever-more appealing even as U.S. debt offers some of the highest rates in years. …

… For the remainder of the report:

END

Kranzler, Turk, many others featured in USAGold’s ‘News & Views’ for May

Submitted by admin on Mon, 2022-05-02 11:54Section: Daily Dispatches

11:54a ET Monday, May 2, 2022

Dear Friend of GATA and Gold:

USAGold’s “News & Views” letter for May emphasizes recent comments from Dave Kranzler of Investment Research Dynamics and GoldMoney’s James Turk, but it is also full of a score of brief items of financial news and opinion. It’s posted in the clear here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

Stating The Obvious!

Posted May 2nd, 2022 at 11:34 AM (CST) by Bill Holter & filed under Bill Holter.

For many years I have written articles with charts, graphs, data, etc. to connect dots and come to a conclusion. Many topics were complicated and we tried to simplify for the average reader to understand. Occasionally we wrote opinion pieces, but for the most part the articles contained proven facts that when accompanied by other factual data could lead to logical conclusions. This article could be considered an opinion piece as I do not care to footnote or prove anything I say. You can either believe I am correct or not. I write this because I would like to be on the record one last time. Let me start with the conclusion: our way of life is over! No matter who you are, how wealthy or connected, your life will change dramatically and will certainly become more difficult going forward. Interest rates have exploded on a percentage basis from the lows over the last couple of years (which had been in place for many years). Another way of saying this bluntly is that bond markets have crashed. Some will say “so what”, few understand. Credit has become THE foundation for both the financial system and real economy. The foundation used to be gold and silver, now it consists entirely of promises to pay. As interest rates rise and bond prices collapse, the “foundation” is being hollowed out.

Stocks have been hit pretty hard, even some of the “generals” that held the indices up for so many years are beginning to falter. We even have some indices like the Russell already making 52 week lows. We also see the sales volume in real estate beginning to dry up. In case you have forgotten, “price ALWAYS follows volume”. Mortgage rates were 2.75% just a year ago, now they are 5.4%, twice as high! If you have not made the connection, a doubling of interest rates basically means a halving of what someone’s income qualifies to borrow. In other words, for those who need to borrow to purchase real estate, their purchasing power just dropped 50%.

We were laughed at and maligned for many years and still somewhat today by those who refuse to pull their head out of their ass to see real world happenings. A short but devastating list of real world happenings where little to no debate is needed; inflation of nearly every single good or service we need to live, deflation of assets has already begun but most importantly of bond prices, we are on the cusp of WWIII as the west seems hell bent for conflict (to point at as the reason for economic and financial failure?), central banks and sovereign treasuries have destroyed their own balance sheets and own failed/failing paper or owe more than can ever be repaid, market liquidity at extremely low levels even though tens of trillions have been pumped into the system, moral and ethical decay as never seen before, work ethic has never been lower, knowledge of basic survival skills has become lost. Hell, a good part of the country cannot (or refuses to) define the difference between male and female!? It has gotten so bad that the current administration feels the need to establish a “ministry of truth” to silence (punish?) anyone with differing albeit truthful and realistic views.

Volatility in markets has exploded because liquidity seems to be drying up and credit more difficult to come by. If you are a student of history, then you’ll know that prior to every single market panic, volatility exploded before the event was understood by the vast majority. This is exactly where we are now in my opinion. Do we get a bounce from here? I do not know and will tell you it does not matter because this “credit cake” has already been baked and in the process of burning to a crisp! Of course, a .50 basis point rate hike by the Fed going into recession should solve ALL the problems?

To conclude, I believe you should either blissfully enjoy the precious little time left in fantasyland or, prepare for the sudden impact that is mathematically coming. In my mind, it is not if but when …and only a matter of how bad it will get? Do we go Mad Max? In late 2006, a Mad Max scenario was not an odds on favorite because society was not as fractured as it is today. Now that drag queen shows and so many other perversions are promoted by those paid by tax dollars to babysit our children, the fabric has already been torn. Not to mention the concerted efforts to cancel The Constitution of the United States? You can either believe the current fantasyland is normal and will continue throughout your lifetime, or you can believe that things real ..are, well, real? Maybe it would be easier to be ignorant and blissful? I guess it would be until it’s not? But then of course it is too late, I suppose you can always show up on your crazy friend’s/relative’s doorstep and hope they forgot you consistently called them an idiot and prepared enough for you both? It is here, it is now, and nothing you do will prevent it. Your only alternative is to do your best to prepare …NOW!

Standing a fearful watch,

Bill Holter

5.OTHER COMMODITIES PALM OIL

end

COMMODITIES IN GENERAL//DIAMONDS

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6085

OFFSHORE YUAN: 6.6821

HANG SANG CLOSED

2. Nikkei closed

3. Europe stocks ALL CLOSED MOSTLY GREEN

USA dollar INDEX UP TO 103.52/Euro RISES TO 1.0516

3b Japan 10 YR bond yield: RISES TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 130.09/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.941%/Italian 10 Yr bond yield RISES to 2.85% /SPAIN 10 YR BOND YIELD RISES TO 2.00%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.91: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO : 3.37

3j Gold at $1862.70 silver at: 22.68 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 roubles/dollar; ROUBLE AT 70.96

3m oil into the 103 dollar handle for WTI and 106 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 130.09 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9757– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0257well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.965 DOWN 3 BASIS PTS

USA 30 YR BOND YIELD: 3.015 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.89

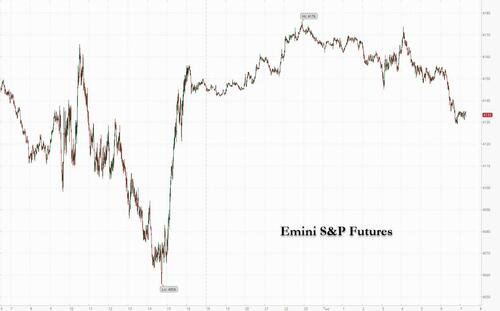

Futures Slump As Fed’s Rate Hiking, QT-ing Meeting Begins

TUESDAY, MAY 03, 2022 – 07:51 AM

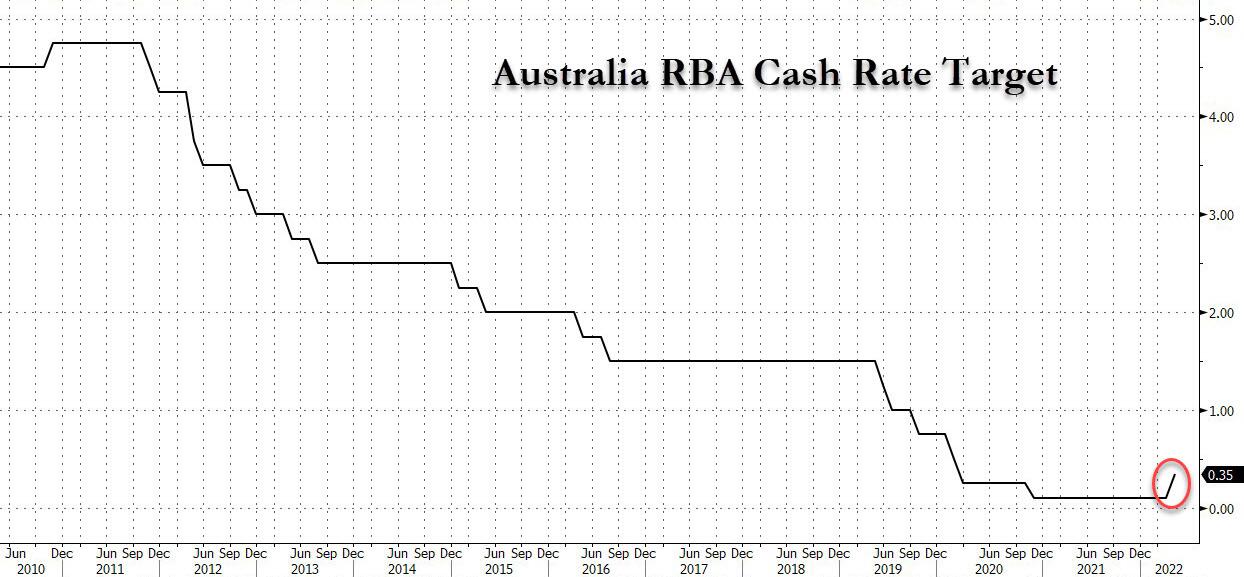

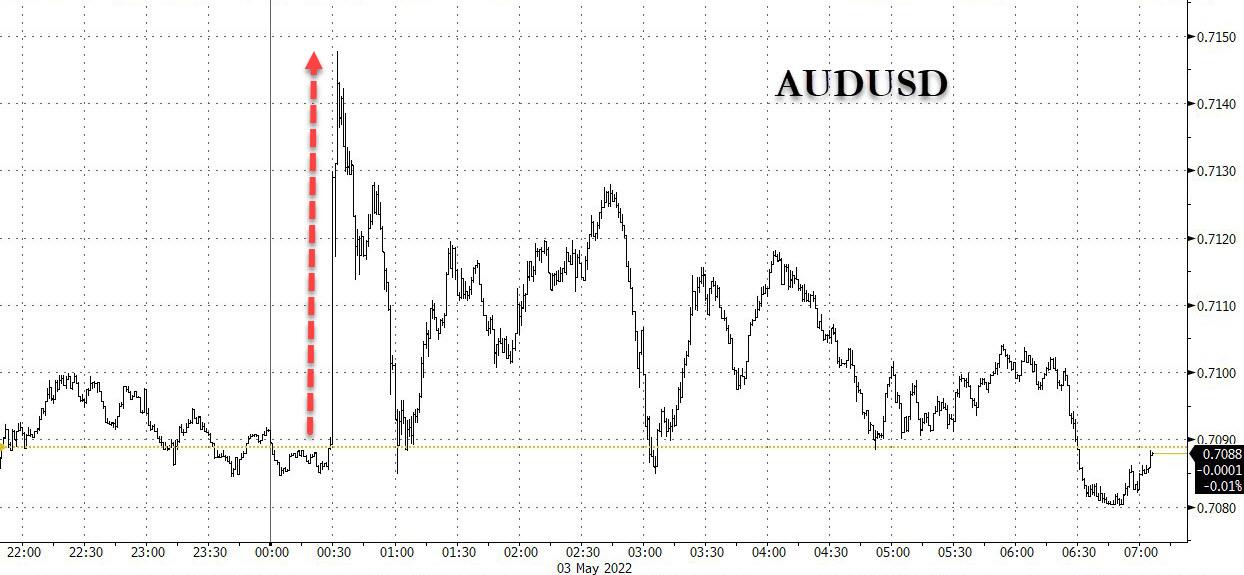

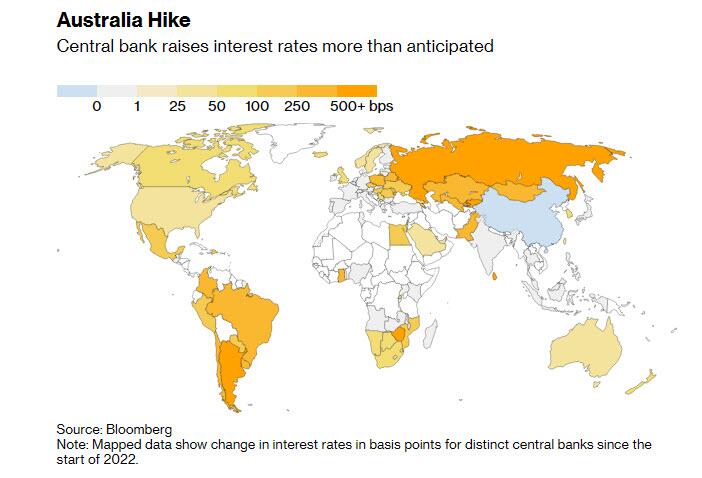

After initially trading higher, extending the momentum of yesterday’s last-hour meltup which saw US stocks close near session highs after plunging earlier, on Tuesday US futures hit an air pocket shortly after the European open, and slumped 0.5% at 715am EDT, as investors braced for more hawkish shocks from the Federal Reserve whose two-day meeting start today and is expected to announce its biggest rate hike since 2000. Tightening turmoil slammed bond markets: 10Y TSYs traded just below 3% after hitting the 4-year old milestone on Monday. Germany’s benchmark rate rose above 1% for the first time since 2015, while the corresponding yield on U.K. bonds climbed above 2% earlier on Tuesday. Australian bonds slid, and the currency jumped, after the nation’s central bank hiked rates costs by more than all economists had expected. The US dollar dipped, oil was lower while cryptos and gold traded flat.

In premarket, NXP Semiconductors rose with analysts lauding the company’s strong results and second- quarter revenue forecast driven by robust demand through a difficult three months, while Kellogg and Tyson were cut to underweight from neutral by Piper Sandler. Pfizer and Starbucks are among the many companies reporting earnings Tuesday. Here are some other notable premarket movers:

- Pfizer (PFE) dropped 3% after the company reported Paxlovid revenue for the first quarter that missed the average analyst estimate. The company’s covid-19 vaccine revenue $13.23 billion, estimate $10.6 billion

- Nvidia (NVDA US) could be active after Morgan Stanley resumed coverage with a recommendation of equal- weight, citing concerns about deceleration in gaming and the company’s high valuation compared to peers.

- Kellogg (K US) and Tyson (TSN US) were cut to underweight from neutral by Piper Sandler analyst Michael S. Lavery, who cites shifting consumer habits caused by inflation pressures and valuations that are ahead of their historical averages.

- MGM Resorts International (MGM US) rose 1.3% in extended trading after reporting adjusted earnings per share for the first quarter that beat the consensus estimate. Analysts had been expecting the company to report an adjusted loss per share for the period, according to the average of projections compiled by Bloomberg.

- Chegg (CHGG US) slumped 32% in extended trading after the online education company lowered its revenue and adjusted Ebitda guidance for the full year.

- Clorox Co. (CLX US) declined 2% in postmarket trading after the company lowered its outlook for full-year earnings amid stubbornly rising costs while reporting profit in its latest quarter that exceeded market expectations.

- Expedia (EXPE US) shares gained 1.5% in extended trading, after the online travel agency reported its first-quarter results. Adjusted Ebitda came in ahead of expectations, and the company said it sees positive indicators for a strong recovery in leisure travel.

- Alibaba (BABA) briefly dipped as much as 9.4% in Hong Kong, wiping off about $26 billion of market value, after a state broadcaster reported that authorities had imposed curbs on an individual surnamed Ma. Shares erased the majority of the losses after police reports indicated the accused person’s name was spelled differently to Alibaba co-founder Jack Ma

US stocks have started off May flattish after slumping in April as investors were worried about the Fed pursuing overly aggressive tightening to curb surging inflation. Morgan Stanley’s Michael Wilson has warned that the S&P 500 will sink to at least 3,800 in the near term and may fall as low as 3,460, a drop of over 16% from Monday’s close. In contrast, JPMorgan Chase & Co. strategists say that the negativity in the U.S. stock market has become so overwhelming that a rebound may not be far off.

Markets are getting whipsawed between concerns around persistent inflationary spirals and risks to global growth from rising yields, China’s Covid lockdowns and Russia’s war in Ukraine. The Federal Reserve’s plans to raise rates and reduce its balance sheet have ended an era of cheap money and forced money managers to reassess valuations.

“The right strategy right now is to position for inflation — a clear and present fact — rather than recession, which is still only a possibility,” Solita Marcelli, chief investment officer for the Americas at UBS Global Wealth Management, wrote clearly unwilling to admit the writing on the wall.

“Investors are already welcoming the prospect of new monetary measures from central banks to combat inflation,” said Pierre Veyret, technical analyst at ActivTrades, adding that “bull traders are buying the recent dips on stocks this morning after most markets fell back to their weekly low, with many betting on the anticipation of tightening monetary conditions to mitigate rising prices. It is likely that most investors have already priced in tomorrow’s FOMC meeting where a record half-point rate hike is widely expected.”

In Europe, the Stoxx Europe 600 Index was little changed, erasing an earlier advance of as much as 0.8% which saw stocks bounce after a flash crash sent shares tumbling on Monday. Europe tracked declines for U.S. futures. Basic resources stocks lled the retreat in Europe, down 1.4%, real estate -1.2%; Energy outperforms, +1.9%; autos +1%, banks +0.9%. Here are the biggest European market movers:

- BP shares rise as much as 3.7% after reporting first-quarter results that were received positively by analysts, who highlight the expanded share buyback and overall strong results.

- BNP Paribas shares climbed Tuesday after the French lender reported what Jefferies called a “massive earnings beat” on strong revenue, with all subdivisions outpacing expectations.

- Stellantis gains as much as 3.2% after the company said it will acquire the Share Now car-sharing joint venture formed by BMW and Mercedes- Benz, to tap new revenue streams.

- ISS rises as much as 8%, the day’s biggest winner on the Stoxx Europe 600 Index, after the cleaning company reported 1Q earnings that beat estimates and raised its FY outlook.

- Electrolux rise the most in a month, after Kepler Cheuvreux raised its recommendation to buy from reduce, seeing a “buying opportunity” in a share where most negatives are already priced in.

- Bayer climbs after Citi re-opens a positive catalyst watch on Bayer ahead of its 1Q earnings, which the broker expects to be ahead of guidance and consensus expectations.

- Alstom also rises as much after Citi opens a positive catalyst watch ahead of the company’s full-year results on May 11, expecting Alstom to generate positive cash flow in 2H22.

- Wizz Air gains as much as 4.4% in London after reporting monthly data traffic for April, with Goodbody noting the airline carried 3.62m passengers last month, up 6 times vs a year ago.

Earlier in the session, Asian stocks were mixed amid holiday-thinned trading, as investors braced for a potential increase in U.S. interest rates later this week. The MSCI Asia Pacific Index dipped as much as 0.5%, with markets including China, Japan, Singapore and India closed for holidays. Australian shares retreated after the Reserve Bank increased interest rates by more than economists anticipated and signaled further hikes. RBA Governor Lowe said he expects further interest rate increases will be necessary in the months ahead; does not preclude a bigger or smaller rate move in the future, and has an open mind on how fast rates need to increase, a more normal level of interest rate would be 2.50%.

“Once again the RBA has proven its ability to quickly pivot the policy direction,” wrote Kerry Craig, global market strategist at JPMorgan Asset Management, in a note. “A material slow-down in economic activity could see a reassessment of the path for policy normalization and there is a high degree of uncertainty.”

Hong Kong’s benchmark eked out a small gain as the city accelerated its reopening plans after Covid cases dropped. Hong Kong Chief Executive Lam said they will reopen bars in the second phase of easing COVID-19 restrictions on May 19th. Shares of Alibaba Group Holding pared losses after a brief bout of concern over the status of its co-founder Jack Ma triggered wild price swings, underscoring continued investor anxiety toward China’s tech sector. Investors are waiting for what could be the U.S. Federal Reserve’s biggest rate hike Wednesday since 2000, one of many central bank decisions this week. The 10-year Treasury yield has climbed above 3% before the decision.

In FX, the Bloomberg Dollar Spot Index eased 0.1% to trim Monday’s gain as the greenback traded mixed versus its Group-of-10 peers. The Australian dollar led gains over G-10 pairs after the Reserve Bank raised rates 25 basis points, to 0.35%, defying expectations for a hike of 15 basis points and signaled more hikes to come to rein in inflation. The nation’s bonds tumbled and the 3-year yield rose above 3% for the first time since 2014. The euro fluctuated around $1.05 and European bonds underperformed Treasuries and peripheral spreads widened. German 10-year yields touched 1% for the first time since 2015, as markets brace for a faster pace of tightening from the ECB.The pound advanced while gilts tumbled, sending the 10-year yield surging above 2% for the first time since April 22 as they catch up with Monday’s bund and Treasury declines when U.K. markets were closed for a holiday.

In rates, the global bond rout deepened as traders take cues from Australia’s hawkish pivot ahead of the Federal Reserve and Bank of England meetings later this week. German 10-year yield rose above 1% for the first time since 2015, subsequently drifting off the highs. U.S. 10-year yields stall again near 3% and 10-year gilts briefly rose to 2%.

Treasuries extended declines as trading kicked off Tuesday, driving the 10-year yield above 3% as investors braced for the Fed’s biggest interest-rate hike since 2000. The Treasury curve unwound Monday’s 2s10s steepening move with front-end yields cheaper on the day and belly to long-end yields slightly richer, following similar flattening in German curve. Treasury yields are cheaper by ~1bp at front-end of the curve, richer by 1bp-2bp from belly out to long-end, flattening 2s10s by ~3bp, 5s30s by ~1bp; 10-year around 2.96%, outperforming comparable bunds by 1bp, gilts by 8bp. Gilts reopen after Monday holiday, underperforming in catch-up to Monday’s Treasuries and bund declines. The Dollar issuance slate empty so far; five names priced $5b Monday with as many as seven others electing to stand down as conditions deteriorated.

In commodities, WTI and Brent were pressured on demand-side concerns as the COVID situation in China remains in focus and Beijing has asked residents not to leave the are unnecessarily. Currently, the benchmarks are holding marginally above session troughs of USD 103.41/bbl and USD 105.62/bbl respectively. Spot gold falls roughly $7 to trade above $1,855/oz. Most base metals are in the red.

Bitcoin is little changed in European trade, pivoting narrow parameters above the USD 38k mark.

Looking at today’s calendar, we’ll get PPI data from the Eurozone, German unemployment figures, and JOLTS and durable goods data from the US. It’s a heavy slate for earnings, with results due from Pfizer, Norsk Hydro, AMD, S&P Global, Airbnb, Estee Lauder, Starbucks, BP, BNP Paribas, Eaton, Deutsche Post, Marathon Petroleum, AIG, KKR, Hilton, DuPont, Teva, and Lyft.

Market Snapshot

- S&P 500 futures down 0.2% to 4,138.5

- STOXX Europe 600 up 0.7% to 446.83

- MXAP down 0.1% to 167.81

- MXAPJ down 0.2% to 556.12

- Nikkei down 0.1% to 26,818.53

- Topix little changed at 1,898.35

- Hang Seng Index little changed at 21,101.89

- Shanghai Composite up 2.4% to 3,047.06

- Sensex down 0.1% to 56,975.99

- Australia S&P/ASX 200 down 0.4% to 7,316.19

- Kospi down 0.3% to 2,680.46

- Brent Futures down 1.3% to $106.13/bbl

- Gold spot down 0.5% to $1,852.78

- U.S. Dollar Index down 0.22% to 103.51

- German 10Y yield little changed at 0.99%

- Euro little changed at $1.0512

Top Overnight News from Bloomberg

- Citigroup Inc.’s London trading desk was a behind a flash crash that sent shares across Europe tumbling on Monday, dealing a fresh setback to the bank’s years-long efforts to improve controls

- Russia’s closely watched dollar payments on two bonds are moving ever closer to creditors as the country races to unblock the transfers and avoid a default. At least one international clearinghouse has received and processed payments for eurobonds due in 2022 and 2042, according to a person familiar with the transaction who wasn’t authorized to speak publicly on the matter

- The RBA’s shift is a blow to Australia’s center-right government that’s trailing in opinion polls as campaigning intensifies for a May 21 ballot

- South Korea’s inflation accelerated to the fastest pace since 2008 in April, prompting the central bank to issue a statement as pressure intensifies for it to raise interest rates further at this month’s policy meeting

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed and lacked direction amid key market closures and looming risk events. ASX 200 was subdued heading into the RBA meeting and was pressured after the central bank delivered a larger than expected hike to the Cash Rate Target which was lifted by 25bps to 0.35%. Hang Seng initially declined on return from an extended weekend amid heavy losses in tech including Alibaba on speculation its founder Jack Ma could be the individual mentioned in Chinese press surnamed Ma who was subjected to compulsory measures for collusion with anti-China hostile forces However, sources later denied that the person was Jack Ma which helped pare some of the losses, while the announcement of looser COVID restrictions in Hong Kong from May 19th also provided encouragement.

Top Asian News

- Shares Up on Support Vow, Sales Slump Deepens: Evergrande Update

- HSBC Shares Rise in Hong Kong as Top Holder Supports Split

- Another Kakao Company Is Working on a Seoul Listing: ECM Watch

- Hong Kong Wealth Fund Hit by $7 Billion Quarterly Loss

European bourses are firmer across the board, Euro Stoxx 50 +0.6%, following late-door Wall St. upside; though, the FTSE 100 -0.5% lags as it catches up from Monday’s holiday.Stateside, futures are modestly firmer/flat on the session but have been rangebound throughout the European morning ahead of Wednesday’s FOMC. In Europe, sectors are primarily positive with Energy outperforming post-BP earnings and Banks supported on yield upside. US Securities and Exchange Commission (SEC) will boost the size of its special unit devoted to investigating cryptocurrency frauds, according to WSJ.

Top European News

- Ukraine Latest: Pope Francis Pushing for Direct Talks With Putin

- Covestro Shares Plunge After Company Cuts Forecast

- Morgan Stanley Overtakes Goldman to Lead in EMEA Equity Sales

- Electrolux Up as Kepler Upgrades, Sees Negatives Priced In

FX:

- RBA hikes in front of Fed to give Aussie a leg up vs Greenback and advantage over Kiwi that is labouring ahead of NZ jobs data; AUD/USD hovers around 0.7100, AUD/NZD probes 1.1050 from lows circa 100 pips below and NZD/USD pivots 0.6450.

- DXY firm around 103.500 awaiting FOMC, with passing interest provided by US factory orders 103.930 is near term resistance, with some charts also citing 103.807 as a long term hurdle.

- Sterling rebounds on return from long UK holiday weekend and in anticipation of another 25bp rate hike on super Thursday, Cable back above 1.2500 and EUR/GBP retreats from 0.8400+ again.

- Euro clinging to 1.0500 against Buck with aid of higher EGB yields and some technical support, 10 year German cash touches 1% and EUR/USD underpinned by 1.0494 ascending trendline.

- Yuan fends off another attack on 6.7000 vs Dollar and Won looking for boost from BoK following strong SK inflation data.

Fixed Income

- Debt futures bounce from new long term lows in some cases; Bunds back over 153.00 vs 152.66, Gilts 117.75 from 117.39 and 10 year T-note 118-12+ vs 118-04+.

- Benchmark yields touch or top psychological levels at 1%, 2% and 3% respectively before retracement.

- Treasury curve re-flattens marginally on the eve of the Fed, 2/10 year -4 bp and 2/30 year in -5 bp.

Commodities:

- WTI and Brent are pressured on demand-side concerns as the COVID situation in China remains in focus and Beijing has asked residents not to leave the are unnecessarily.

- Currently, the benchmarks are holding marginally above session troughs of USD 103.41/bbl and USD 105.62/bbl respectively.

- Spot gold is softer as yields continue to climb, but remains above USD 1950/oz as the USD struggles to derive traction.

- Similarly to crude, base metals are impacted on demand-side concerns re. China’s COVID backdrop.

US Event Calendar

- April Wards Total Vehicle Sales, est. 14.1m, prior 13.3m

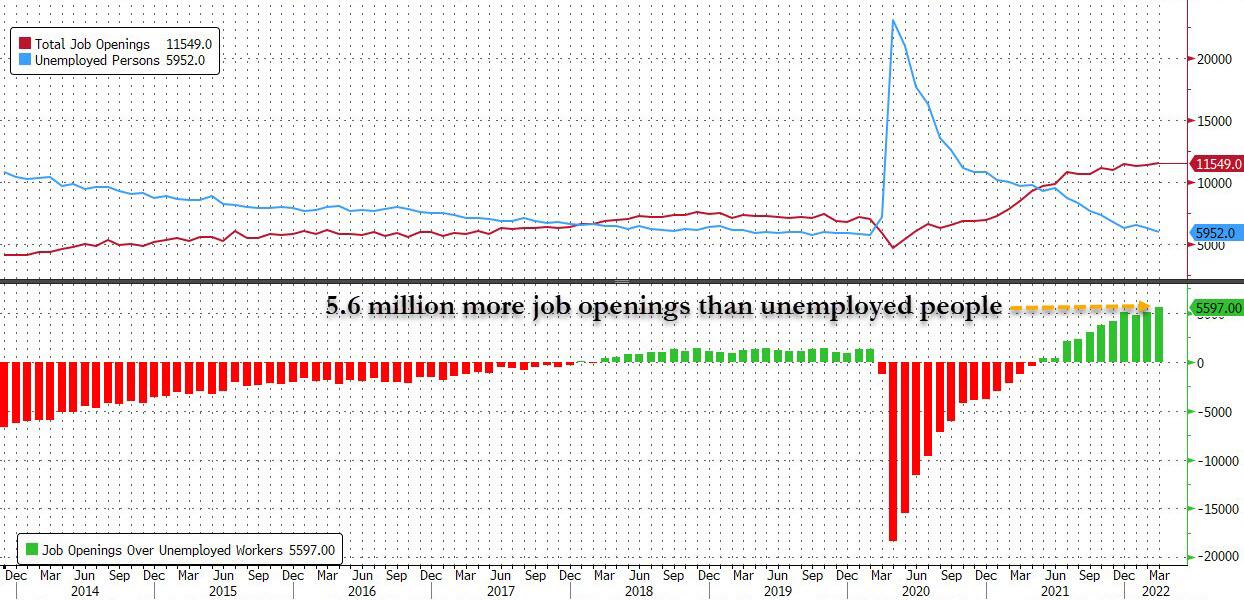

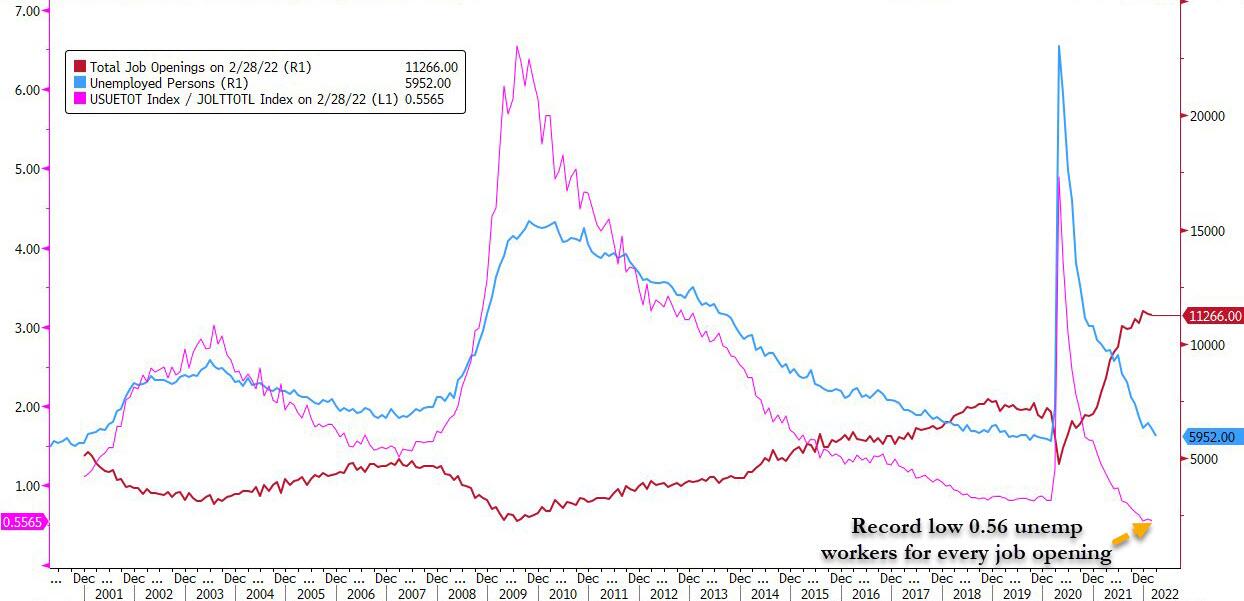

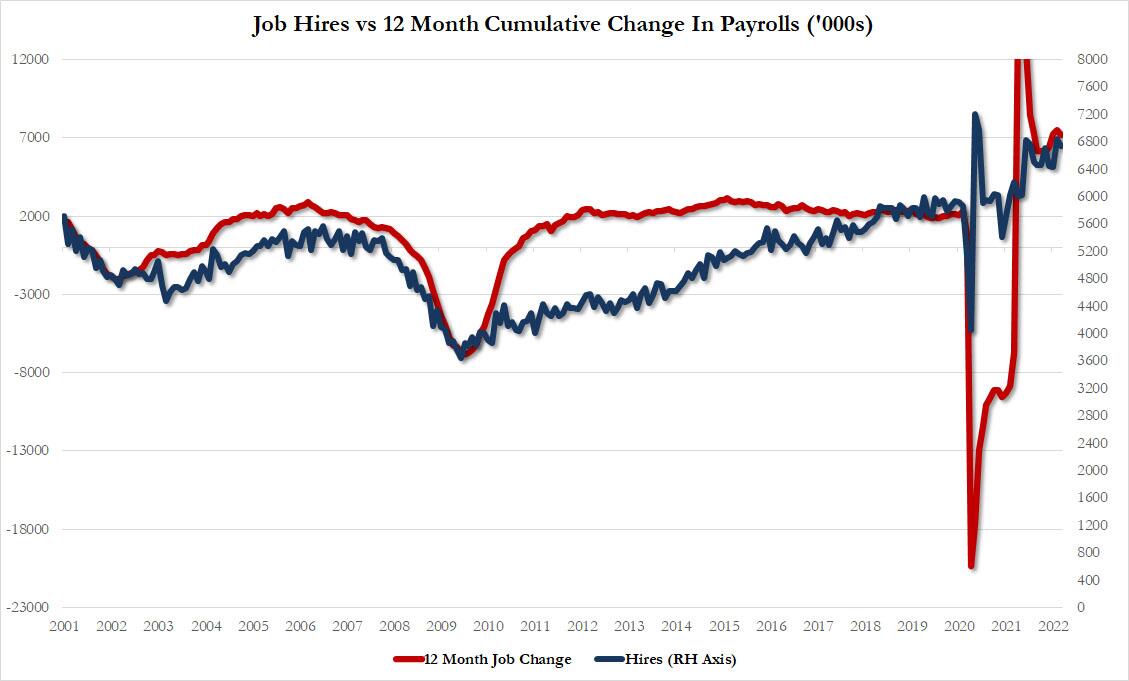

- 10:00: March JOLTs Job Openings, est. 11.2m, prior 11.3m

- 10:00: March Factory Orders, est. 1.2%, prior -0.5%; Factory Orders Ex Trans, prior 0.4%

- Durable Goods Orders, est. 0.8%, prior 0.8%; -Less Transportation, est. 1.1%, prior 1.1%

- Cap Goods Orders Nondef Ex Air, est. 1.0%, prior 1.0%

- Cap Goods Ship Nondef Ex Air, prior 0.2%

DB’s Jim Reid concludes the overnight wrap

We had a bank holiday here in the UK yesterday and for once an extra round of golf didn’t make me a pariah as when the twins were out all afternoon with mum on Sunday I did a surprise recording session with 6-year-old Maisie, putting her first ever self-penned song on record. She keeps on making up little songs in the car and l’d spotted a loop or two that I thought were quite good so I created a backing track and got her to sing it into my studio mic and then mixed it together with a video. We then surprised mum when she got home. Mum cried with joy, and I quickly booked in a season of golf competitions in the diary whilst she was overcome with emotion. In the unlikely event you’d like to see and hear it please see the link on my Bloomberg header or email me and I’ll send it to you.

Talking of the bank holiday, for those missing yesterday here are the brief highlights of what’s left in a busy week ahead. Tomorrow sees the FOMC decision, where a +50bp hike and the start of QT are expected. The Fed is followed on Thursday by the BoE who are expected to lift rates (+29.3bps are priced in). We also have US payrolls on Friday and 161 S&P 500 companies reporting through the week. On that, our equity team published their Q1 earnings takeaways so far late last week, link here. While the season has been noisy so far, the median beat has been solid at 6.2% despite some notable outliers dragging the average down to 2.6%, below historical average. However 81% of companies have beat consensus. Earnings growth is in line with historical norms at 11.3% YoY. Margins have remained near record highs despite input price pressures.

Price action on the first day of May rhymed with what we saw over April. US Treasury yields continued their march higher, with yields increasing above 3% on benchmarks from 5 to 30 years intraday during the New York session, ahead of tomorrow’s FOMC. Ten-year yields gained +4.7bps, closing at 2.98%, but as mentioned managed to breach 3% for the first time since 2018 at one point. Similar to the price action last week, the nominal figure masked divergence in the decomposition. Real yields gained +15.6bps ahead of the Fed’s anticipated QT announcement tomorrow, punching through to positive territory for the first time since March 2020’s whipsawing price action, closing at +0.15%. 10yr breakevens, thus narrowed -10.9bps to 2.83%. European sovereign yields trended in a similar direction, with bunds (+2.7bps) and OATs (+3.2bps) picking up ground at the 10yr point, with 10yr BTPs continuing their recent run of spread widening, climbing +5.8bps over bunds yesterday, to 189bps, their widest level in two years. This comes following fears on global growth taking hold, but also with the market revising its expectation toward an earlier exit of ECB accommodation. Indeed, our Europe economists changed their call last week, now expecting APP net purchases to finish in June, with liftoff following in July, with 100bps of hikes in 2022 now pencilled in. See the link for more details.

Stocks were broadly lower in Europe, catching down with a very poor US close on Friday, with the STOXX 600 pulling back -1.46% and every sector lower on the day. The DAX (-1.13%) managed to slightly outperform, while the CAC (-1.66%) fared slightly worse. Europe did survive a morning flash crash though caused by an erroneous trader entry. American stocks were saved from starting May the way they ended April with a late rally in New York, leaving the S&P 500 +0.57% higher. There was a clear divergence between underperforming defensives and outperforming cyclical stocks, as real estate (-2.55%), staples (-1.29%), utilities (-1.04%), and health care (-0.68%) were the four worst performing sectors, while communications (+2.43%), tech (+1.56%) and energy (+1.37%) led the rebound. The large intraday swing ensured the Vix stayed above 30 for another session, closing the day at 32.34pts.

Despite the strong showing from US energy stocks, brent crude oil also started the month lower, falling -1.61%. Again, the dollar index marched to its highest level since 2002, gaining +0.76% yesterday, meaning the index has gained at least +.50% in 6 of the last 7 sessions, and cleared +0.6% in 4 of those.

Overnight in Asia, the biggest news is just coming through as I type with the RBA hiking rates by 25bps, a bit more than expected. 2yr Aussie notes are up +11bps in the immediate aftermath and the Aussie Dollar is soaring. Elsewhere news of upcoming covid rules easing in Hong Kong is lifting the Hang Seng (+0.12%) with the KOSPI (+0.0%) unchanged while exchanges in Japan and China are closed for holidays. S&P 500 futures (+0.38%) are trading in positive territory.

On data yesterday, US ISM Manufacturing surprised to the downside in April, with the index realising at 55.4 versus expectations of 57.6. The survey responses were replete with examples of supply chain pressures still plaguing industry. The US PMI figure came in at 59.2, just missing the 59.7 expectations.

To the day ahead, we’ll get PPI data from the Eurozone, German unemployment figures, and JOLTS and durable goods data from the US. It’s a heavy slate for earnings, with results due from Pfizer, Norsk Hydro, AMD, S&P Global, Airbnb, Estee Lauder, Starbucks, BP, BNP Paribas, Eaton, Deutsche Post, Marathon Petroleum, AIG, KKR, Hilton, DuPont, Teva, and Lyft.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED UP 12.50 OR 06% /The Nikkei closed //Australia’s all ordinaires CLOSED DOWN 0.47% /Chinese yuan (ONSHORE) closed DOWN 6.6084 /Oil UP TO 103/82 dollars per barrel for WTI and UP TO 106.47 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6064 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6821: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

3c CHINA

CHINA//SHANGHAI/LOCKDOWNS/USA

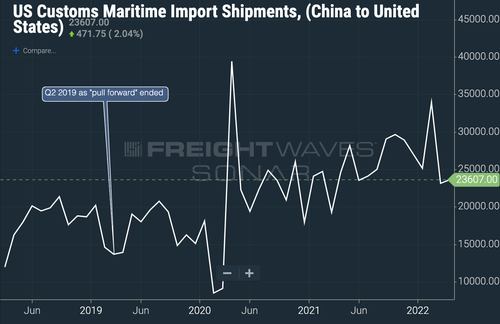

Xi’s lockdowns will have a devastating effect on USA truckers this summer

(Fuller/Freightwaves)

Xi’s Lockdowns Will Pull The Rug Out From Under US Truckers This Summer

TUESDAY, MAY 03, 2022 – 05:00 AM

By Craig Fuller, CEO of FreightWaves

Whenever the trucking market slows, truck drivers look for someone to blame. Normally, a slowdown is just a function of supply and demand. The market has too much dispatchable capacity compared to the total number of loads on any given day.

This summer, the trucking market could have one of its steepest declines in recent years and there is an entity that deserves much of the blame – the Chinese Communist Party and its draconian and inhumane lockdowns.

While the motivations of the Chinese government are unclear, one thing is certain – anyone subjected to a Chinese state lockdown compares it to being imprisoned in their own homes. As seen in several widely shared media posts, the Chinese government has started to erect metal barricades to block people from leaving their homes, preventing passage even for food or medicine.

While Americans watch in horror as innocent Chinese citizens are caught up in an ill-conceived, reckless, or nefarious – take your pick – act by the Chinese Communist Party, there is little Americans can do about it. But like most geopolitical events these days, the lockdowns in Shanghai and other Chinese cities are also a supply chain story that will have a dramatic effect on domestic freight markets.

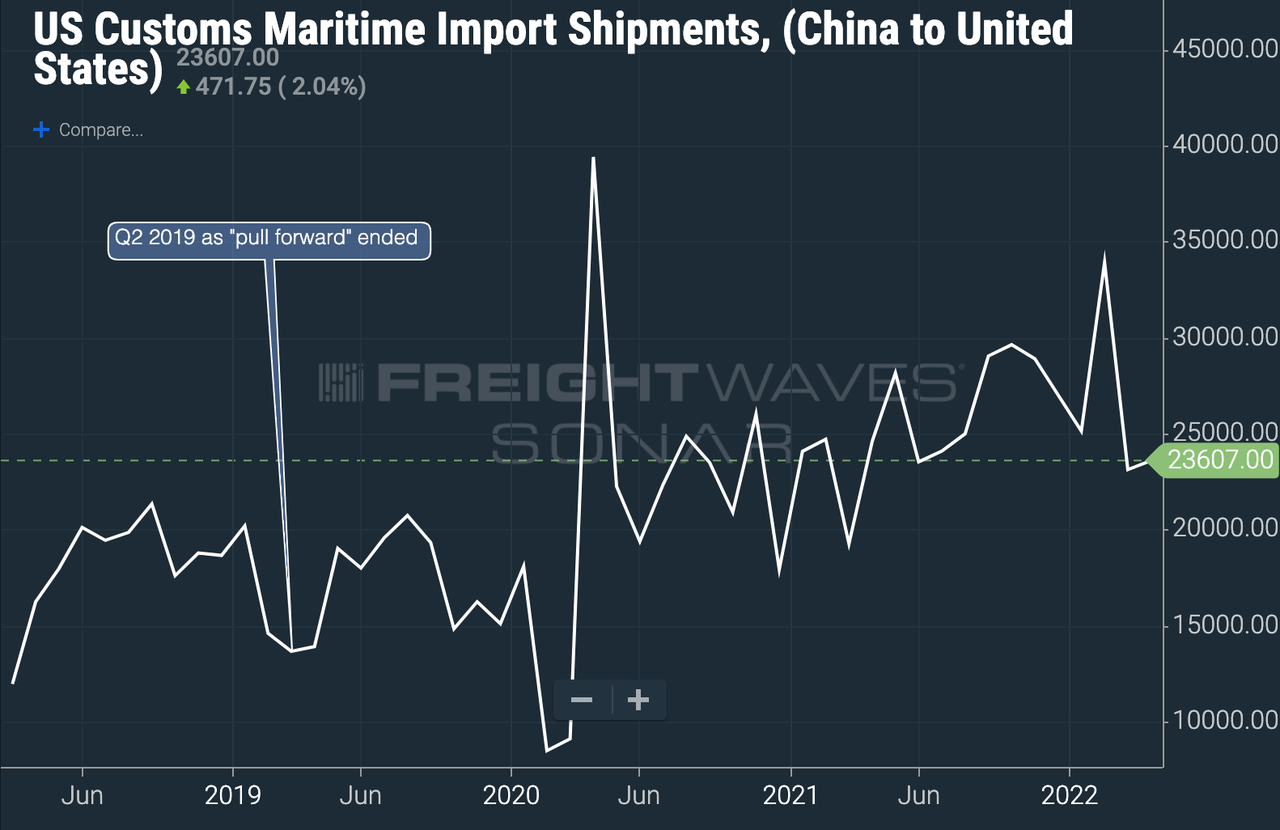

The recent slowdown in U.S. truckload markets is likely a precursor to a steeper decline in the coming weeks. The lockdowns in China were not a factor in slowing U.S. truckload volumes in February and March, as evidenced by record container imports at nearly all major U.S. ports.

But that shouldn’t give anyone comfort because the slowdown is about to hit U.S. ports – and the trucking companies that service them – in a dramatic way. FreightWaves estimates that container imports from China represent approximately 16% of U.S. truckload volumes and an even larger percentage of U.S. dry van truckloads. After all, nearly half of the containers that come into the United States originate in China.

The lockdowns in Shanghai began on April 2 and the lockdowns in Guangzhou began on April 11. As geopolitical analyst Peter Zeihan described the situation on Twitter:

Beijing, which is the political capital of China, was expected to be spared the lockdowns by many analysts. This appears to be wishful thinking and Twitter lit up on April 24 with reports of Chinese state police starting to implement similar measures to those seen in the preparation for lockdowns in other cities.

The three largest cities in China are going to be removed from the world market. According to analysts, at least 40% of China’s GDP has been taken offline and this was before lockdowns began in Beijing. The vast majority of this GDP is directly related to global manufacturing. Removing it means removing the flow of containers from the world economy.

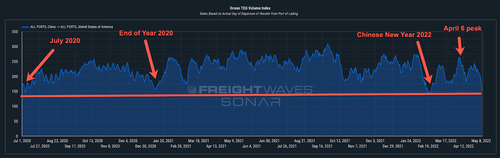

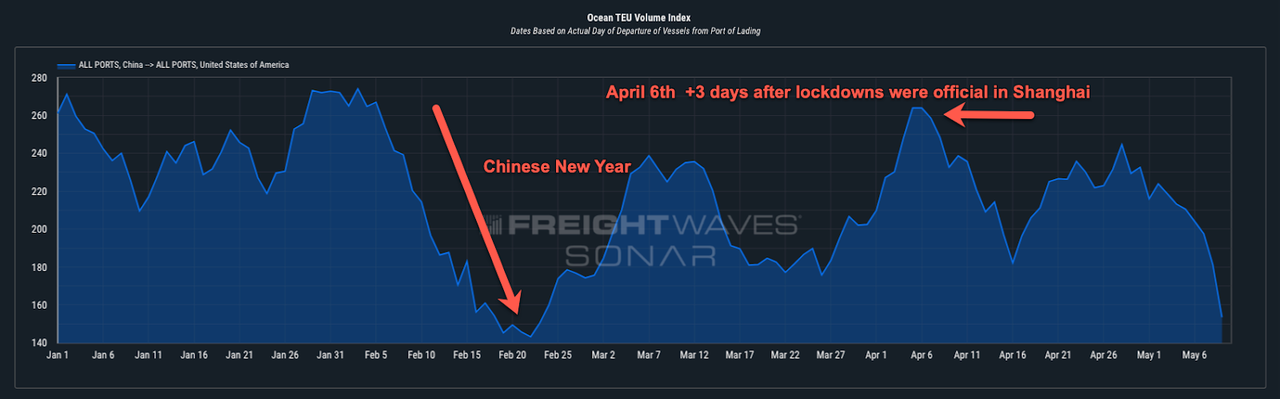

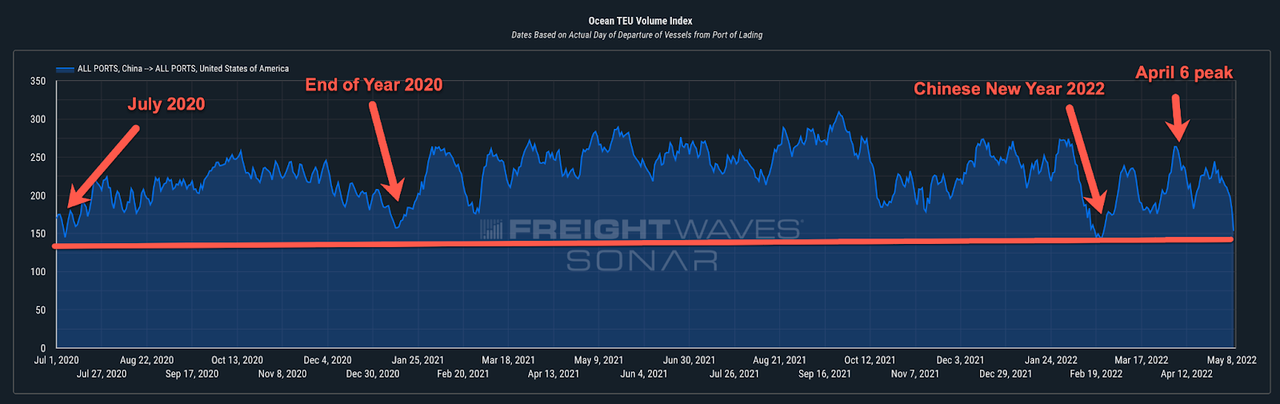

Container volumes from China to the United States started to fall on April 6. It hasn’t been a direct line down; more like a roller coaster. In the first 10 days, container volumes dropped by 31%. Volumes have since rebounded about halfway, to “just” a 16% drop. But according to FreightWaves SONAR’s volume booking forecast, volumes have started to drop once again and could fall to 50% of the April 6 number by May 9. This would be nearly the same level of a drop that China to U.S. exports saw during the Chinese New Year in 2022 and lower than any other point since July 2020.

Chinese ports are operating, but the bigger risk is with Chinese trucking operations. According to a report in Bloomberg, only 20% of Shanghai’s trucking capacity is operating. Trucking is a bigger part of the flow of containers in and out of the Chinese ports than in the United States. Over 75% of container volumes in China ports enter or exit on a truck, while in the U.S. both trucks and railroads move freight from our ports.

The loss of trucking capacity in China means that raw materials and components can’t get from the ports to factories and finished goods can’t leave the factories to the ports to be put on ships for export. The temporary blip (dead cat bounce) was likely containers that were already in the queue at the port prior to the lockdowns.

Since factories can’t receive new components or raw materials, they will also stop operating once their supplies are exhausted. Supply chains involve large webs of suppliers that are interconnected and just because one supplier is online does not mean that other suppliers are. Once they shut down, it will take much longer to bring them up to full productivity.

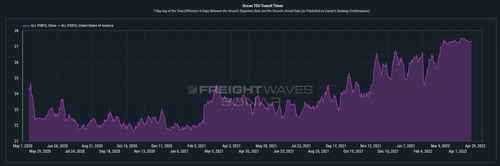

According to SONAR’s ocean intelligence dashboard, it currently takes 27 days for a vessel to travel from a Chinese port to a U.S. port. Since the volume of containers from China to the U.S. started its drop on April 6, it will likely be May 3 before U.S. ports experience a drop in volume.

It takes approximately 10 days to three weeks after a vessel arrives in the U.S. before the containers that traveled on board enter the domestic surface freight market. This would put a slowdown in trucking freight volumes related to Chinese imports between May 13 and May 24.

We have seen this play out before.

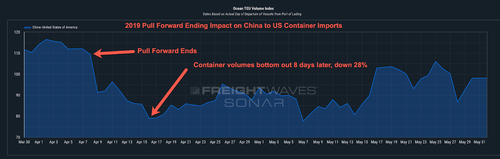

During the second half of Donald Trump’s presidency, the U.S. declared a trade war on Chinese imports. The first tariffs on Chinese goods were set at 10% and went into effect in December 2018. That was intended to be a shot across the bow and had little effect on import volumes. However, President Trump also threatened that if his demands for Chinese policy changes were not met, he would raise the tariffs to 25% by March 31, 2019.

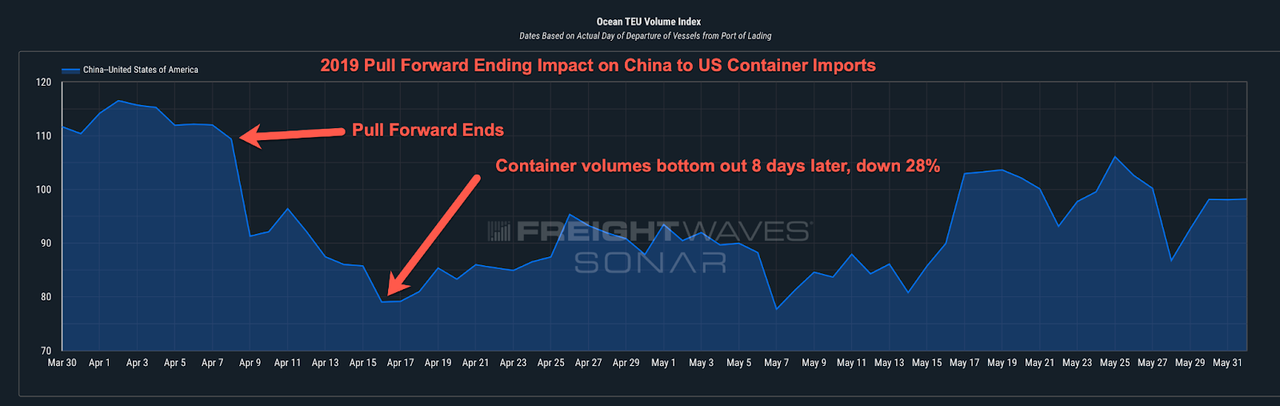

Reacting to a threat that most importers and Chinese manufacturers thought had legitimacy, a surge of goods started to flow from China to the U.S. in what was described as a “pull-forward.”

The last of the “pull-forward” surge containers to leave Chinese ports was on April 7, 2019. SONAR’s Ocean TEU Volume Index of containers leaving Chinese ports to the U.S. dropped by 28% from April 8, 2019 to April 16, 2019.

The first signs of U.S. trucking volumes dropping took place 35 days after the drop in container volumes out of China. From May 9, 2019, to May 16, 2019, U.S. national contract truckload volumes (OTVI.USA) dropped by 6%.

In Asian import-heavy Los Angeles, the drop was much worse. Truckload volumes dropped by an astounding 28% from May 8, 2019 to May 16, 2019. The drop was so significant that I wrote my first article warning of the freight recession and stated that “Conditions for fleets are deteriorating and it will get bloody.”

The recent drop in container volumes is eerily similar to the one that took place in 2019.

The drop in 2019 started with the same speed and depth as the one we are currently facing. The trucking industry had just come through one of the hottest freight markets in history in 2018, with more new fleets entering the market than in any previous period in history.

The abrupt drops in container outflows from China in 2019 and 2022 happened almost exactly three years to the day, which means the freight market seasonal calendar was roughly identical and makes for easy comparables.

Since April 2019, maritime shipments from China to the U.S. have grown by 28%, while U.S. truckload volumes have increased by 24% in that same timeframe.

A slowdown in freight volumes from China in May 2022 will be more equitably distributed throughout the U.S. and less concentrated in Southern California, as compared to the 2019 slowdown.

Why? While Southern California’s ports are still the primary ports of entry for Chinese goods, recent port congestion has encouraged importers to shift volumes away from the ports of Los Angeles and Long Beach. This is showing up in SONAR’s truckload market share data (OTMS).

In April/May 2019, the Los Angeles and Ontario freight markets represented 7.69% of all U.S. contracted truckload shipments. Today, those two markets represent just 6.74%.

Watching daily market conditions will be critical to fleet operators in their search for headhaul markets. A headhaul market is a freight market in which there are more loads than dispatchable trucks. In SONAR, this map is updated daily and markets are shaded in blue. The deeper the blue, the better conditions for fleets.

We always coach trucking companies to go “blue to blue” to stay loaded, and since the data comes from tenders and not load board activity, it is far more accurate of current conditions in the market because it avoids “ghost loads” from brokers.

Eventually, the lockdowns will end and Chinese production will begin once again. However, the longer China stays offline, the longer it will take for production to ramp up. Supply chains don’t come online instantly.

And just how long it takes for the lockdowns to end and the supply chains to begin operating again is a guessing game. But there is reason to believe that the Chinese lockdowns are far from over.

FreightWaves’ Eric Kulisch reported on April 15, 2022, that BBVA suggested that the lockdowns in China could continue until June. If this prediction plays out, it will be a difficult summer for many U.S. trucking operators.

END

END

4/EUROPEAN AFFAIRS//UK AFFAIRS/EU

HUNGARY//SLOVAKIARUSSIA//EU//GAS PURCHASES

With a threat of a veto the EU now considers exemptions for Russian oi purchases by Hungary and Slovakia

(Paraskova/OilPrice.com)

EU Considers Exemptions As Hungary Threatens To Veto Russian Oil Ban

TUESDAY, MAY 03, 2022 – 03:30 AM

Authored by Tsvetana Paraskova via OilPrice.com,

As Hungary threatens to veto a European Union-wide ban on Russian energy products, the bloc is now considering exemptions for Hungary and Slovakia, or a longer timeframe for the two countries to reduce their heavy reliance on Russia.

Slovakia and Hungary have been among those EU members staunchly opposed to a ban on Russian oil due to their very high dependence on Russian imports. On Monday, a senior Hungarian government official said that Hungary could be ready to veto an EU embargo on Russian oil imports, Bloomberg reported.

Hungarian Cabinet Minister Gergely Gulyas told HirTV on Sunday that an EU-wide ban would require unanimity, and as such, “it makes no sense for the commission to propose sanctions affecting natural gas and crude oil that would restrict Hungarian procurements”.

“We’ve made it clear that we’ll never support,” Gulyas added.

An exemption or an extended period for Hungary – or Slovakia – could help overcome resistance, however.

The European Commission is currently discussing the sixth package of sanctions against Russia, and those sanctions are increasingly likely to include an embargo on Russian oil imports that would start by the end of this year. Slovakia and Hungary could be given exemptions or more time to find alternative supply, EU officials told Reuters on Monday, as the EU seeks a united front in sanctions against Russia.

Since the start of the Russian war in Ukraine, the EU has been split on a ban on Russian energy imports. The biggest European economy—Germany—has resisted an immediate oil embargo, saying an oil ban would plunge Germany, and Europe, into a deep recession. While Germany, Hungary, and Austria, as well as some other EU members, have opposed an immediate outright ban on Russian oil, Germany signaled last month that it could end its dependence on Russian oil and stop importing Moscow’s oil entirely by the end of this year. Germany has now reportedly dropped its opposition to a ban, if given time to procure alternatives.

Last week, German Economy Minister Robert Habeck said that a full embargo is now “manageable” for Germany and that the country hoped to find a replacement for Russian oil within days. According to Habeck, Germany is now “very, very close” to making a full Russian oil embargo a reality.

The shift in Germany’s position on a Russian oil embargo could encourage other still hesitant EU members to support a ban on Russian oil imports, analysts have said.