May 2, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 2, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1864.05 DOWN $46.20

SILVER: $22.57 DOWN $0.47

ACCESS MARKET: GOLD $1863.30

SILVER: $22.64

Bitcoin morning price: $38,661 UP 227

Bitcoin: afternoon price: $38,333 DOWN 100

Platinum price: closing DOWN $11.50 to $937.95

Palladium price; closing DOWN $110.05 at $2210.70

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices/ 20/54

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,909.300000000 USD

INTENT DATE: 04/29/2022 DELIVERY DATE: 05/03/2022

FIRM ORG FIRM NAME ISSUED STOPPED

657 H MORGAN STANLEY 19

661 C JP MORGAN 20

690 C ABN AMRO 20 3

709 C BARCLAYS 10

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 34 1

TOTAL: 54 54

MONTH TO DATE: 1,442

:

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 54 NOTICE(S) FOR 5,400 OZ (0.1679 TONNES)

total notices so far: 1442 contracts for 144,200. oz (4.4852 tonnes)

SILVER NOTICES:

80 NOTICE(S) FILED 400,000 OZ/

total number of notices filed so far this month 1752 : for 8,750,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD DOWN $46.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD.

INVENTORY RESTS AT 1094.55 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 47 CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF 554,000 OZ

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.171 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 949 CONTRACTS TO 135,949 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.12 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.12) AND WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A STRONG GAIN OF 1031 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 1.295 EFP JUMP TO LONDON//NEW STANDING 28.875 MILLION OZ/ // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : —-222

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTACTS for 1 days, total 1736, contracts: 5.1556 million oz OR 5.1556 MILLION OZ PER DAY. (1736CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 5.1556 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 5.1556 MILLION OZ//

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 949 WITH OUR $0.12 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 705 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 1.295 MILLION OZ EFP TO LONDON//NEW STANDING 28.875 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 787 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.935 MILLION OZ ACCOMPANYING THE LOSS IN PRICE.

WE HAD 80 NOTICES FILED TODAY FOR 400,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2600 CONTRACTS TO 561,272 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –103 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED INCREASE IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $20.05//COMEX GOLD TRADING/FRIDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 6500 OZ//NEW STANDING 5.555 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $20.05 WITH RESPECT TO FRIDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 6463 OI CONTRACTS (20.102 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3968 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 561,272.

IN ESSENCE WE HAVE A VERY GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6568, WITH 2600 CONTRACTS INCREASED AT THE COMEX AND 3968 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6568 CONTRACTS OR 20.102 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3968) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2495,): TOTAL GAIN IN THE TWO EXCHANGES 6463CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 6500 OZ//NEW STANDING 5.555 /// 3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

1736 CONTRACTS OR 173,600 OR 8.680 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 1736 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 8.660 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 8.66/3550 x 100% TONNES 0.243% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 8.66 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 949 CONTRACT OI TO 135,949 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1736 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1736 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 705 CONTRACTS AND ADD TO THE 1736 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 787 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3.935 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.12 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED XX PTS OR XX% //Hang Sang CLOSED XX OR XX% /The Nikkei closed DOWN 29.37 PTS OR 0.11% //Australia’s all ordinaires CLOSED DOWN 1.31% /Chinese yuan (ONSHORE) closed DOWN 6.6084 /Oil DOWN TO 101.69 dollars per barrel for WTI and UP TO 104.10 for Brent. Stocks in Europe OPENED MOSTLY CLOSED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6064 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6747: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2495 CONTRACTS TO 561,272 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR GAIN OF $20.05 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2844 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3968 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :3968 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3968 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6463 CONTRACTS IN THAT 3968 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 2495 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR STRONG GAIN IN PRICE OF GOLD $20.05.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (5.353),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 5.353 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $2.35) AND WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A STRONG SIZED GAIN OF 20.429 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (5.353 TONNES)…

WE HAD 103 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 6463 CONTRACTS OR 646,300 OZ OR 20.102TONNES

Estimated gold volume today: 97,601/// extremely poor

Confirmed volume yesterday:188,075 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 2

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 200.02oz Brinks |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 112,560.651 17,001 kilobars 15,000 kilobars HSBC and 2001 kilobars JPMorgan |

| No of oz served (contracts) today | 54 notice(s)5400 OZ 0.1678 TONNES |

| No of oz to be served (notices) | 344 contracts 34,400 oz 1.0699 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1442 notices144,200 OZ4.4852 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

2 customer deposits

i) Into HSBC 48,226.500 oz (15,000) kilobars)

ii) Into JPMorgan: 64,334.151 oz (2001 kilobars)

1 customer withdrawals:

i) out of Brinks 200.02 oz

total withdrawal: 200.02 oz

ADJUSTMENTS: 3/ customer to dealer

i) Brinks 15,023.590 ox

ii) Manfra: 5693.190 oz

iii) 6172.992 oz (removed) jpmorgan//192 kilobars

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 398 contracts having LOST 1323 contracts

We had 1388 notices filed on Friday, so we gained 65 contracts or 6500 oz will stand for delivery in this non active delivery month of May.

June saw a GAIN of 1099 contracts UP to 443,978 contracts

July has an initial 5 OI to stand at 5

August has a gain of 2048 contracts up to 66,687 contracts

We had 54 notice(s) filed today for 5400 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 54 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 20 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1422) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 398 CONTRACTS ) minus the number of notices served upon today 54 x 100 oz per contract equals 178,600 OZ OR 5.555 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1422) x 100 oz+ (398) OI for the front month minus the number of notices served upon today (54} x 100 oz} which equals 178,600 oz standing OR 5.555 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 5.555 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626,135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,989.255.509 OZ (1119.42 TONNES)

TOTAL ELIGIBLE GOLD: 18,358,705.533 OZ (571.03 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,630,649.576 OZ (548.39 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,689023.0 OZ (REG GOLD- PLEDGED GOLD) 487.99tonnes

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 2

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,413,527.377 oz DELAWARECNT Manfra INT. DELAWARE JPMORGAN |

| Deposits to the Dealer Inventory | 116,285.000OZ MANFRA |

| Deposits to the Customer Inventory | 1,197,891.590oz BRINKS JPMORGAN |

| No of oz served today (contracts) | 80CONTRACT(S)40,000 OZ) |

| No of oz to be served (notices) | 4023 contracts (20,115,000 oz) |

| Total monthly oz silver served (contracts) | 1752 contracts 8,750,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 1 deposit into the dealer

i) Into Manfra 116,285.000 oz

total dealer deposits: 116,285.000 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into Brinks 44,630.990 oz

ii) Into JPMorgan: 1,153,260.600 oz

total deposit: 1,197,891.590 oz

JPMorgan has a total silver weight: 174.281 million oz/333.531 million =52.23% of comex

Comex withdrawals: 5

i) Out of CNT 690,254.295 oz

i1) Out of JPMorgan 585,046.500 oz

iii) Out of Delaware: 2173.500 oz

iv) Out of Int. Delaware 90,422.092

v) Out of Manfr: 44,630.990 oz

total withdrawal 1,413,527.377 oz oz

3 adjustments: customer to customer

i) Out of Brinks 24,023.900 oz

ii) Out of Manfra; 4999.659 oz

iii) 965.810 oz removed entire from customer Delaware

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.620 MILLION OZ

TOTAL REG + ELIG. 333.531 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 4103 HAVING LOST 1931 CONTRACTS. WE HAD 1672 NOTICES FILED ON FRIDAY

SO WE LOST 259 CONTRACTS THAT WE EFP’D TO LONDON (1,295,000 OZ) AS SILVER IS SCARCE OVER HERE.

JUNE HAD A GAIN OF 26 TO STAND AT 1801

JULY HAD A GAIN OF 962 CONTRACTS UP TO 109,757 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 80 for 400,000 oz

Comex volumes: 20,594// est. volume today// extremely poor

Comex volume: confirmed yesterday: 59,058 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 1722 x 5,000 oz = 8,750,000 oz

to which we add the difference between the open interest for the front month of MAY (XXX) and the number of notices served upon today 80 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 1752 (notices served so far) x 5000 oz + OI for front month of MAY (XX) – number of notices served upon today (80) x 5000 oz of silver standing for the MAY contract month equates 30,170,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1094.55 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 575.171 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Schiff: Wages Are Up But You’re Worse Off

MONDAY, MAY 02, 2022 – 12:47 PM

The Bureau of Economic Analysis released the Personal Income and Outlays data for March last week. Incomes and consumer spending were both up. The data had mainstream analysts crowing about a strong economy and good news for American consumers. But digging into the data reveals a very different picture.

Incomes were up 0.5% month-on-month. That seems like a solid gain — until you factor in rising prices. According to the Personal Consumption Expenditure (PCE) index, prices were up 0.9% in March. That means real incomes were down 0.4%.

Looking at the bigger picture, incomes were up, but not nearly as much as prices. Once again, we see price increases eating up income gains and then some. That means your standard of living is falling.

The Federal Reserve loves the PCE. That’s because it is probably the most dishonest of all the government’s dishonest inflation measures. It is manipulated to understate rising prices. So, real incomes are falling even faster than the data indicates.

Peter Schiff pointed out that American consumers would be better off in incomes were down 0.5% and prices fell 0.9%. Rising wages aren’t helpful if prices go up even faster.

What counts is not how much you’re paid, but how much you can buy. It’s the difference between what you earn and what you spend that counts. So, if wages are falling, but prices are falling even more, that’s a good thing because workers are better off.”

As it is, you’re working more and earning more, but you’re falling further and further behind. Real wages are collapsing.

Personal spending blew away expectations in March. Spending was up 1.1%. But where did that big increase in spending come from? It didn’t come from higher wages. It came from savings. The savings rate fell to 6.2% in March, the lowest in nine years. Schiff said he thinks savings will hit an all-time low before the year is over.

Consumers are dipping into a very shallow saving pool to try to keep their economic necks above water as prices are going up.”

Americans are also running up their credit cards. Revolving credit, primarily credit card debt, rose by a whopping 20.7% in February. (the March data will be out in the next week or so.) American consumers added $18 billion to their credit card bills in February alone.

Mainstream pundits spun rising consumer spending as a sign of a strong economy. But with prices up 0.9%, real spending was only up 0.2% in March. And as Schiff points out, prices being only up 0.9% “is a fantasy.”

They’re up much more than that. And so, spending is actually down. People are buying less stuff. They’re just paying more for the stuff they’re buying. And because they’re paying so much more for food, and energy, and rent, and insurance, and stuff like that, they don’t have enough money left over to go shopping on Amazon, which is why Amazon reported such bad earnings.”

This is why Schiff says a significant recession is likely on the horizon.

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

LAWRIE WILLIAMS: Volatile month sees enormous swings in gold, silver and equities

Maybe the long-predicted equities crash has already begun, although a lower than anticipated Fed interest rate rise at this week’s FOMC meeting might result in something of a recovery, But, at the moment our warnings that rising inflation would likely be the principal market depressor is coming true – perhaps sooner than many had suspected. The Russian invasion of Ukraine has certainly helped raise market uncertainty and also contributed to the inflation rises by the indirect effects on the supply chain resulting from the war itself and to the effects, real and projected, of sanctions on Russian exports.

The table below looks at the performance over the past month of the major equity indexes, precious metals, oil, natural gas and the copper price – of all the base metals copper is considered the best guide to likely economic growth, or otherwise, ahead. As can be seen nearly all have been marked down in the past month and year to date – equities and bitcoin particularly so, but the major precious metals too certainly have not been immune in April apart from palladium, where Russia is the world’s No.1 exporter and sanctions impositions could severely disrupt deliveries.

We had anticipated that perhaps gold and silver would emerge from an equities meltdown relatively unscathed – particularly the former – but had also warned that liquidity needs could force some investors and funds to unload good assets along with bad ones to stay afloat. This happened the last time there was a serious market meltdown back in 2008, but gold investors should perhaps take comfort in that the yellow metal did recover quickly at that time and went on to attain new highs within the next 2-3 years. Gold is up a little year-to-date, but down in April and ended the month hugely below its March peak.

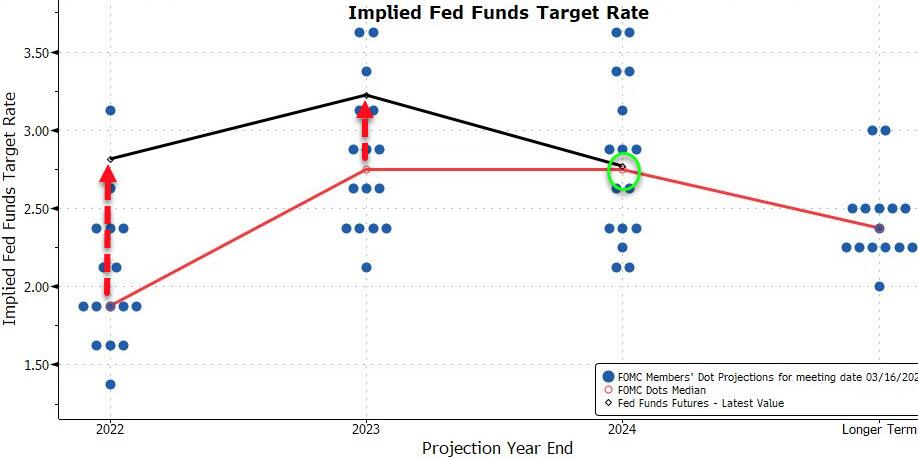

Markets have been nervous, though, ahead of the forthcoming U.S. Federal Open Market Committee (FOMC) meeting, which commences on Tuesday, at which the U.S. Federal Reserve will set out its likely more aggressive interest rate policy. The nervousness arises because even the widely predicted 50 basis point interest rate increase, likely to be followed by the prospect of another similarly- sized rise at the June FOMC meeting, coupled with the ending of the Fed’s bond and mortgage security-buying programmes (Quantitative Tightening or QT) could possibly see U.S. equities markets dive further.

U.S. businesses have become so used to several years of the Fed effectively supporting them with near-zero interest rates and with effectively pumping funds into the markets, that bringing all this to an abrupt end may provide a severe shock. Perhaps they should be glad that Fed chair Jerome Powell is unable to mete out the kind of medicine Paul Volcker did in 1979/80, which certainly defeated inflation but drove the U.S. economy into a deep recession. The current enormous debt level (estimated at around $30.4 trillion) the U.S. has built up has made the Volcker remedy, which saw interest rates rise to near 20%, financially untenable. The costs of servicing such a high debt level at this kind of interest rate would rapidly bankrupt the country.

April has thus been a particularly volatile month for both equities and metals with this combination of factors affecting the equities markets which mostly fell back – particularly in the past week despite a couple of recovery attempts. Indeed it has perhaps been surprising that there had not been even more market disruption earlier in the month given the potentially serious impact of the two principal driving forces which have come to the fore. The two are also connected in that the one is seriously affecting the other as well, as we noted above at the start of this article.

As a result, very few asset classes are still in positive territory this year. Gold is up a little under 4% since the end of December 2021, despite falling in price in April. It had seemed to be starting to improve Friday, but the core Personal Consumption Expenditure (PCE) inflation index, which is the Fed’s preferred measure, came in that day at a better than expected 5.2% annual increase and the gold price dipped back below $1,900 in later trade. The overall PCE, which includes food and energy prices, came in at a worrying 6.6% annual rate though, up another 0.3% on the previous month’s figure,

Palladium, for which Russia is comfortably the world’s largest producer, bucked the trend accordingly and was up nearly 14%, but was pretty much flat in April. Most base metals fell in price – even much-touted copper which is seen as something of a bellwether for the likely forward path of the economy.

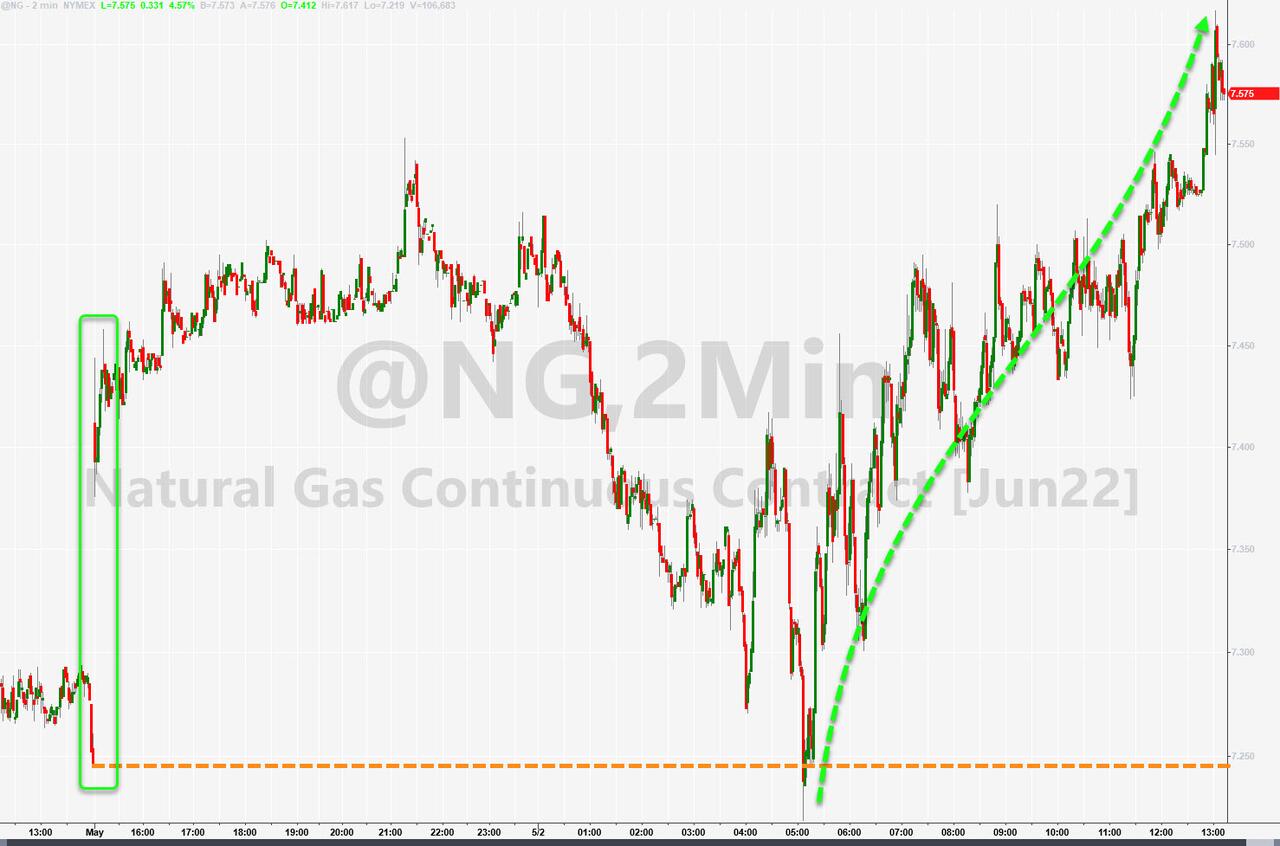

Of the major stock indexes we have looked at most are down year-on-year, the only gainer being the FTSE 100 in the UK, which perhaps has benefited marginally from Brexit insulating it from some of the tribulations which have afflicted other European economies. The biggest gainer of all we have listed was natural gas, for which Russia provides around 40% of mainland Europe’s supply, where prices have risen over 95% year-to-date. Oil, where Russia is also a dominant exporter, particularly also to Europe, has risen in price by around 31.5%. Not surprisingly in view of these statistics, the increase in energy prices has been the most significant component in the global rise in inflation.

The two principal overall market drivers are, of course, rapidly rising global inflation and the Russian invasion of Ukraine. The first was already beginning to impact markets quite severely from late last year as nations were beginning to exit from the strictures which had been imposed to try and help control the spread of the Covid-19 pandemic.

The Ukraine war has not only created huge geopolitical uncertainty in Europe in particular, but has led to some extremely stringent economic sanctions being applied to the Russian economy to try and persuade President Putin to end his attacks on Ukraine, with seemingly little effect so far.

As Russia is a key global supplier of metal and energy commodities, foodstuffs and fertilizers, and Ukraine the latter two, the sanctions and war disruptions are having also an adverse effect on the economies of nations importing these products. Supplies are being cut off and need to be replaced by more expensive alternatives from elsewhere assuming these are even available. Even nations like the U.S., which are reasonably self-sufficient in most, but not all, areas are not immune from the inflationary pressures thus created.

The latest confirmation of the adverse effects of all this on the U.S. economy arose with the Bureau of Labor Statistics’ latest Consumer Price Index (CPI) and Producer Price Index (PPI) data announcements mid-month which came in at 8.5% and 11.2% year-on-year increases respectively, the worst for 40 years or more. The big worries here are what steps will the U.S. Fed take to try and bring these excessive inflation levels, which still seem to be rising, down to its target of around 2%.

The standard tools for combating inflation are to raise interest rates, and to cut back on any other accommodative bond and security-buying programmes. But the big problem facing the Fed is that interest rates have been ultra-low (near zero) for so long and although QT on its accommodative bond and mortgage security buying programs is already starting to be implemented, many economists consider it as being too little too late.

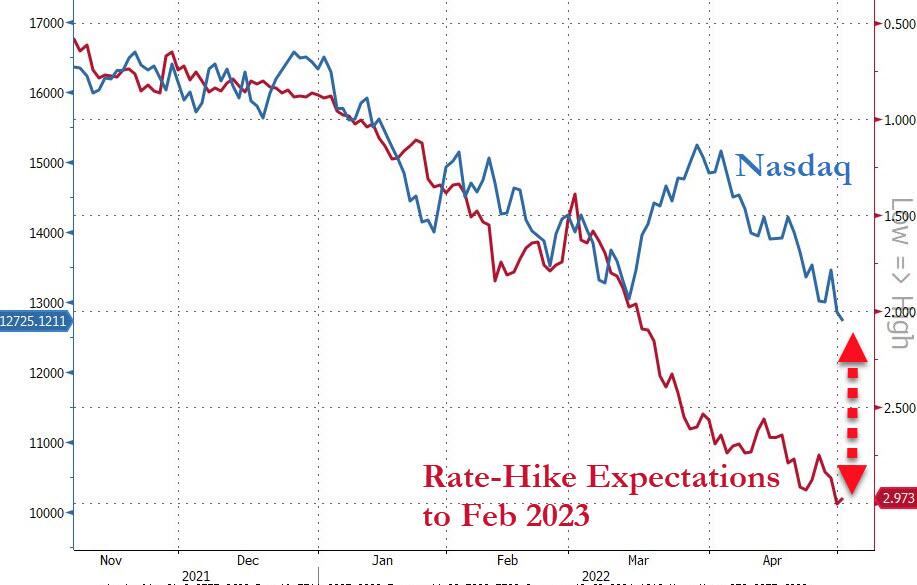

Even a succession of above-the-norm interest rate rises through the remainder of the year at the kinds of levels the Fed seems to be contemplating, continuing into next, may still be insufficient to even start to bring down inflation without also driving the U.S. economy sharply downwards. American businesses have become far too used to easy money flowing from the Fed into the markets and ultra-low interest rates supporting them. This has seen equity markets rise to levels which many consider unsustainable. Some well- respected commentators are even predicting a serious recession within the next couple of years – or perhaps sooner. The recent sharp equity price falls suggest it may have even already begun despite occasional partial recoveries. And as the world’s leading economy, what happens in the U.S. tends to set the pattern elsewhere in the world.

The resurgence of the Covid-19 pandemic in China, resulting in draconian measures to try and keep it under control, is also contributing to supply-chain worries and further resultant inflation fears. This has been having an additional adverse impact on the markets.

In theory – in the writer’s opinion at least – the markets should be far more worried about inflation and potential Fed moves to bring it down than they appear to have been up until the past few days. Such moves could see Federal Fund interest rate levels raised at a faster rate than at any time in the past three to four decades. There is even talk of a 75 basis point rate increase being imposed at the forthcoming FOMC meeting, although the consensus opinion is still for the 50 basis point rise as suggested by Fed chair Jerome Powell. But even this could be high enough to put an additional serious dent in equity market valuations, particularly if the Fed forecasts more of the same medicine to come during the remainder of the year, and beyond, which seems distinctly possible. Equity investors in particular should perhaps be prepared for a difficult few months, if not years, ahead.

01 May 2022

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Nabiullina is still western trained. There is a differing of opinion linking the rouble to gold with the Krelim saying one thing and the central bank chief another.

(Bloomberg/GATA)

Russian central bank chief rejects linking ruble to gold, differing with Kremlin

Submitted by admin on Fri, 2022-04-29 11:47Section: Daily Dispatches

From Bloomberg News

Friday, April 29, 2022

Bank of Russia Governor Elvira Nabiullina today dismissed the idea of pegging the ruble to gold after the Kremlin said it was a proposal under consideration.

“It is not being discussed in any way,” Nabiullina told reporters at a briefing after the central bank cut the key interest rate by 300 basis points.

The ruble must continue to have a floating exchange rate, she said, though volatility of the currency will be higher amid capital controls imposed after Russia began its invasion of Ukraine

Her comment appeared to contradict President Vladimir Putin’s spokesman, Dmitry Peskov, who said earlier today that “this question is now being discussed.” Peskov pointed to comments by Security Council Secretary Nikolai Patrushev on linking the currency to gold and other commodities in an interview with a state-run newspaper this week, while offering no further details. …

… For the remainder of the report:

END

Interesting read on what one Chinese official believes:

Ambrose Evans Pritchard

(London Telegraph..GATA)

Ambrose Evans-Pritchard: China faces double disaster, caught between virus and Putin

Submitted by admin on Fri, 2022-04-29 12:36Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Friday, April 29, 2022

China should abandon all illusions that the West is in terminal decline, or that a new world order of authoritarian regimes is dawning.

It should ditch Vladimir Putin immediately. The country should not be tainted by the retrograde adventurism of a loser. Beijing should instead seek a new concordat with Washington, acting as a conciliatory stakeholder power.

So concluded a sizzlingly cogent essay by Chinese foreign policy guru Hu Wei in March after Russia’s blitzkrieg failed to take Kyiv. Prof Hu heads the Shanghai Public Policy Research Institute, linked to reformers at the State

The essay circulated for several days in China before being expunged, a sign of powerful dissent against the pro-Putin policies of President Xi Jinping. The Carter Centre ran an English version.

Prof Hu says the Ukraine war will be a watershed moment, but not in the way that Xi imagined when he issued his Sino-Russia manifesto for the new world order in February, proclaiming “no limits” to China’s bond with Putin’s Russia — the green light for the invasion of Ukraine.

“The power of the West will grow significantly, NATO will continue to expand, and U.S. influence in the non-Western world will increase,” said Prof Hu.

“The West will possess more ‘hegemony,’ both of military power and in terms of values and institutions; its hard power and soft power will reach new heights.”

He even expects a resurrection of Francis Fukuyama’s Hegelian dream of democratic liberalism as the end-state for mankind, though Fukuyama himself (spooked by Trump) has since lost faith in the End of History.

Xi ignored the warnings and now faces a grave strategic reverse. …

… For the remainder of the analysis:

https://www.telegraph.co.uk/business/2022/04/29/china-faces-double-disaster-caught-covid-putin/

end

this is a must view

Andrew Maguire and Alasdair Macleod at the vault:

(Kinesis/GATA)

Maguire and Macleod discuss defections from Western financial system

Submitted by admin on Fri, 2022-04-29 23:09Section: Daily Dispatches

11:08p ET Friday, April 29, 2022

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire interviews GoldMoney research director Alasdair Macleod on this week’s edition of Kinesis Money’s “Live from the Vault” program, discussing the defection of China, Russia, and other countries from the Western financial system.

Macleod and Maguire see a “commodification” of currencies as the Western system collapses, leading to a revaluation of gold.

The discussion is 57 minutes long and can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The rise in the USA dollar( % this year) is leading to a huge trail of destruction

(Reuters/GATA)

Dollar’s surge leaves a trail of destruction

Submitted by admin on Fri, 2022-04-29 23:20Section: Daily Dispatches

By Saikat Chatterjee and Sujata Rao

Reuters

Friday, April 29, 2022

LONDON — The dollar’s race to two-decade highs is leaving a trail of destruction in its wake, exacerbating inflation in other countries and tightening financial conditions just as the world economy confronts the prospect of a slowdown in growth.

This year’s 8% gain by the dollar against a basket of currencies is driven partly by bets that the U.S. Federal Reserve will raise interest rates faster and further than other developed countries, and partly by its status as a safe haven in times of turbulence

.It is also supported by Japan’s reluctance to ditch its super-easy policies, and fears of recession in Europe.

Here are some areas affected by the dollar’s muscle-flexing. …

… For the remainder of the report:

https://www.reuters.com/business/dollar-surge-leaves-trail-destruction-2022-04-29/

end

Stress beginning to emerge in treasuries with collateral fails

(Dizard/London’s Financial Times)

Stress emerges again in Treasuries market

Submitted by admin on Sat, 2022-04-30 20:09Section: Daily Dispatches

By John Dizard

Financial Times, London

Saturday, April 30, 2022

When the world’s biggest and most liquid market shows signs of stress, investors should take note.

At the beginning of this month, major financial market participants trading in the U.S. Treasury bond market had difficulty meeting the demands for collateral made by their counterparties.

The alarm bell was reported in the Federal Reserve Bank of New York’s Primary Dealer Statistics, in the weekly report for “fails” for U.S. Treasury securities. A “fail” occurs when a market participant breaks a promise to receive or deliver securities when they are obliged to do so.

In the week ended April 6, there were a total of $507 billion in fails reported by the primary dealers, a sharp rise from $358 billion in the previous week ended March 30. The level fell back down again to $275 billion in the subsequent week and was far below the $5.3 trillion peak of fails seen in one October week in the 2008 financial crisis.

But the jump this month was notable — the highest level of fails since March 2020.

During that March, you will recall, financial markets very publicly ground to a halt due to Covid-19 lockdowns. This time, though, there was no particular, visible trigger event. …

… For the remainder of the analysis:

https://www.ft.com/content/0ecb9244-46e8-4feb-b4c2-d9b277140d4f

end

4.OTHER GOLD/SILVER COMMENTARIES

5.OTHER COMMODITIES PALM OIL

end

COMMODITIES IN GENERAL//DIAMONDS

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6085

OFFSHORE YUAN: 6.6747

HANG SANG CLOSED

2. Nikkei closed DOWN 29.37 PTS OR 0.11%

3. Europe stocks ALL CLOSED

USA dollar INDEX UP TO 103.43/Euro FALLS TO 1.0523

3b Japan 10 YR bond yield: RISES TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.96/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSEDDOWNP// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.918%/Italian 10 Yr bond yield RISES to 2.81% /SPAIN 10 YR BOND YIELD RISES TO 1.98%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.89: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO : 3.36

3j Gold at $1874.50 silver at: 22.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 roubles/dollar; ROUBLE AT 70.96

3m oil into the 101 dollar handle for WTI and 104 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.96 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9739– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0248well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

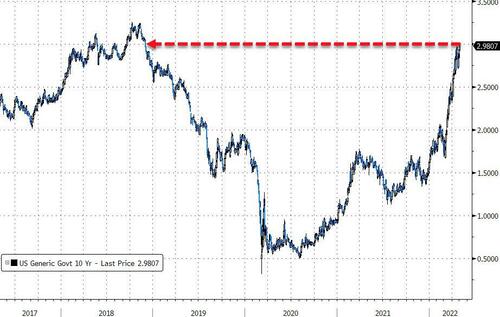

USA 10 YR BOND YIELD: 2.918 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 2.989 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.88

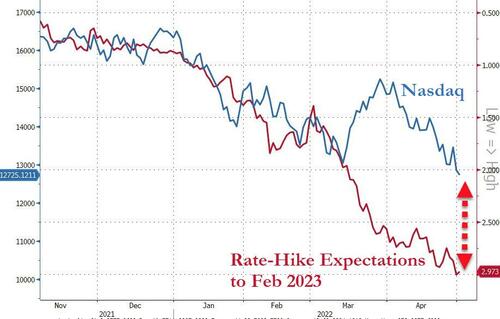

Futures Struggle To Rebound With Fed Set To Hike 50 Into A Recession

MONDAY, MAY 02, 2022 – 07:54 AM

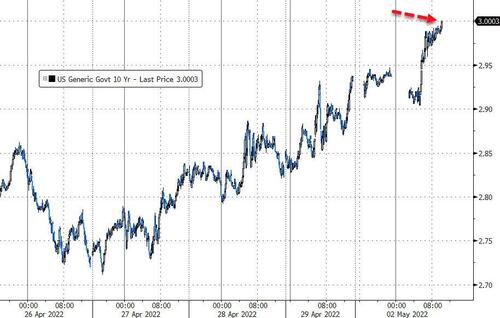

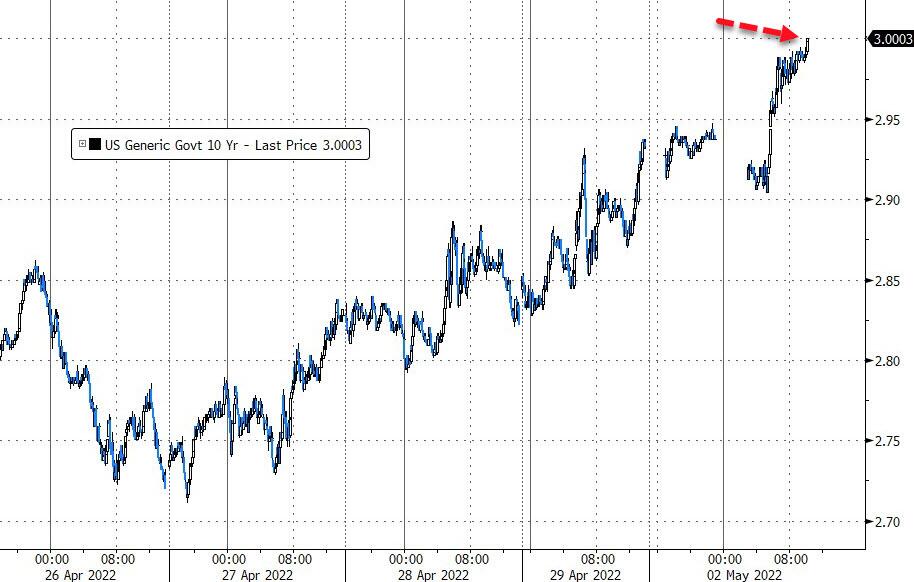

One trading day after epic carnage shook global markets, US index futures staged a modest recovery on Monday after Wall Street’s worst selloff in almost two years. S&P 500 Index contracts rose 0.1% from an 11-month low, while Nasdaq 100 futures gained 0.4% with volumes thinned by holidays in several markets including the UK, China and Hong Kong. European and Asian stocks fell as disappointing corporate earnings, expectations of global monetary tightening, poor data from China and the prospect of sanctions on Russian oil weighed heavily on risk appetite. The VIX remained elevated, trading above 33, as investors braced for a week that’s likely to see a global round of monetary-policy tightening that will add to concerns about global growth. 10Y Treasury yields pushed higher again, rising to 2.94% before easing ahead of this week’s key event, the Fed’s upcoming 50bps rate hike. The dollar gained as worries over high inflation and China’s Covid lockdowns contributed to investor caution, and sent the offshore yuan sliding to just shy of 6.69m the lowest since November 2020. Gold extended its slump and Brent oil dropped about $2 to trade around $104.50.

Focus has shifted back to the Fed’s policy outlook after last Friday’s pledge by China to boost economic stimulus damped demand for havens on Friday. The week’s main event will take place on May the 4th (be with you), when the Fed is expected to lift rates by 50bps, the first “double-hike” since May 2000, and will announce it will let its balance sheet start to shrink at a pace that will quickly step up to $95 billion a month. Odds of 75bps rate hike in June remain at 50%. Bond yields may stay “elevated for the foreseeable future” due to inflation and the Fed’s sharp rate hikes allied with balance-sheet reduction, Seema Shah, chief global strategist at Principal Global Investors, wrote in a note. Japanese institutional managers – known for their legendary U.S. debt buying sprees in recent decades – are now fueling the great bond selloff just as the Federal Reserve pares its $9 trillion balance sheet.

In premarket trading, Activision Blizzard gained 2% after Warren Buffett snapped up more of the stock in a merger arbitrage bet (yes, Berkshire is a merger-arb powerhouse now, how long until Berkshire does Twitter). Here are some other notable movers:

- Comerica (CMA) upgraded to overweight and KeyCorp (KEY) cut to underweight at Piper Sandler as the broker shuffled ratings to reflect its post-earnings preferences

- Piper Sandler analyst Alexander Twerdahl cut the recommendation on Community Bank System (CBU) to underweight, becoming the first broker to downgrade the company with a sell-equivalent rating since July 2020

- Piper Sandler analyst Arvind Ramnani raised the recommendation on Epam Systems (EPAM) to overweight, citing healthy demand for digital IT services

In Europe, the automotive and tech sectors led the Stoxx Europe 600 Index down 1%, extending its losses this year to 8.6% with focus on the potential for the European Union to propose a ban on Russian oil by year-end as well as concerns over China’s economy. Vestas fell 5.9% in Copenhagen after the Danish maker of wind turbines cut its revenue outlook for the full year and forecast its first loss in a decade. Confidence in the euro-area economy fell to the lowest in a year as the impact of the war in Ukraine drained overall sentiment from industry to consumers.

Among individuals moves in Europe, Adler Group SA shares plunged more than 40% after KPMG said it was unable to give an audit opinion and Vestas Wind Systems A/S slumped after forecasting its first loss in a decade.

Earlier in the session, Asian stocks slid on delayed reaction to the Friday carnage after underwhelming earnings guidance from U.S. tech giants fueled worries about a further slowdown in a global economy already smarting from the Federal Reserve’s policy tightening and China’s lockdowns to curb the coronavirus. The MSCI Asia Pacific Index dropped as much as 0.8%, weighed down by losses in financials and technology. The key gauge in Australia fell the most ahead of Tuesday’s local central bank policy meeting that is expected to raise rates for the first time since 2010.

Markets in China, Hong Kong, Taiwan and Singapore were closed for holidays. Chinese economic activity contracted sharply in April, data released Saturday showed, weighing on regional investor sentiment even after the Politburo pledged to meet economic targets. Fed Chair Jerome Powell has as good as promised that U.S. officials will deliver a 50 basis-point interest-rate increase this week.

“The U.S. economy appears to be peaking while markets expect almost four 50-basis-points rate hikes by the Federal Reserve in upcoming policy meetings,” said Norihiro Fujito, chief investment strategist at Mitsubishi UFJ Morgan Stanley Securities. “China’s PMI announced over the weekend was terrible. When you have the world’s two largest economies in conditions like this, there will be pressure on corporate earnings.”

Asian tech stocks were weak after Amazon.com Inc. plunged on Friday by the most since 2006 on a sales forecast that fell short of analyst estimates. IPhone maker Apple Inc. warned last week of a hit of up to $8 billion in its second-quarter revenue as China’s Covid-19 lockdowns undermine the world’s supply lines

Japanese equities fell slightly ahead the Federal Reserve’s planned interest-rate hike this week and amid continued concern over the impact of China’s lockdowns to curb the coronavirus. Japanese markets will be closed Tuesday through Thursday for Golden Week holidays. The Topix fell 0.1% to close at 1,898.35 Monday, while the Nikkei declined 0.1% to 26,818.53. Nintendo Co. contributed the most to the Topix decline, decreasing 2.4%. Out of 2,172 shares in the index, 1,110 rose and 973 fell, while 89 were unchanged.

India’s key equity gauges fell on Monday, dragged by information technology stocks and index heavyweight Reliance Industries while corporate earnings performance for March quarter remains mixed. The S&P BSE Sensex fell 0.2% to 56,975.99 in Mumbai, while the NSE Nifty 50 Index also retreated by an equal measure. The key gauges fell 2.6% and 2.1% in April, respectively and have retreated in three of four months this year. Indian markets will be shut on Tuesday due to a local holiday. Ten of the 19 sector sub-indexes compiled by BSE Ltd. declined, led by consumer durables. Metal and basic material companies were the best performers.

Foreign investors, who have been net sellers of Indian stocks since end of September, dumped about $3.4 billion in month through April 28. The global funds have sold a total of $21.7 in the preceding 7 months as surging inflation and a war in Ukraine dented global risk-appetite for equities. Infosys contributed the most to the index decline, decreasing 1.7%. Out of 30 shares in the Sensex index, 11 rose and 19 felf.

In rates, Treasuries reopened slightly richer across the curve when trading resumed following holiday closures across Europe. 10-year TSY yields were around 2.915% is richer by ~2bp vs Friday’s close, vs 2.5bp for German 10-year. U.S. 10-year sector slightly outperforms front-end where 2-year yields are lower by 1bp on the day; curve spreads remain within ~1bp of last week’s close. Bunds outperform with gilts closed for U.K. bank holiday. Dollar issuance slate empty so far; estimates for the week are around $25b, and some expect a historically busy month with $125b-$150b of IG credit supply.

In FX, a gauge of the dollar’s strength advanced, outperforming most other Group-of-10 currencies. Trading volumes thinned with holidays in countries including the U.K. China’s manufacturing and services activity plunged to their worst levels since February 2020, according to purchasing managers surveys. The Bloomberg Dollar Spot Index gains 0.1%; cash Treasuries are closed until U.S. hours. “There’s a good chance that we would go towards parity in euro-dollar,” Union Investment’s Christian Kopf said in an interview with Bloomberg Television on Monday. Elsewhere, the yen underperformed all its G-10 peers/ The Australian and New Zealand dollars dropped amid momentum selling and liquidation of longs by leveraged funds, traders said. “As long as the Fed doesn’t blink, the dollar stays bid,” ING Groep NV analysts including Chris Turner wrote in a note. The offshore yuan weakened in the wake of data signaling a sharp contraction in Chinese economic activity amid idled factories and snarled supply chains.

In commodities, WTI and Brent fell with downside occurring alongside the pressure in equities; downside was exacerbated by the loss of multiple psychological support levels. Newsflow has been heavily focused on a potential Russian oil/gas embargo, with Hungary remaining heavily opposed; however, Politico reports of a potential compromise for such member nations.

A missile attack on an oil refinery in Iraq’s Erbil hit an oil tank and caused a fire although the fire was put under control, according to Reuters citing security forces. Iraq’s oil exports reached a total of 101mln bbls in April which raised USD 10.55bln in revenues, while exports averaged 3.4mln bpd.

Bitcoin prices are marginally higher and rebounded from beneath the 38,500 level.

Looking at today’s calendar, we get the April manufacturing PMI and US ISM Manufacturing data, new car registrations, US March construction spending. We also get earnings from NXP Semiconductors, Devon Energy, Expedia, MGM resorts, SolarEdge.

Market Snapshot

- S&P 500 futures down 0.1% to 4,125.75

- STOXX Europe 600 down 1.4% to 444.02

- MXAP down 0.6% to 167.87

- MXAPJ down 0.6% to 556.31

- Nikkei down 0.1% to 26,818.53

- Topix little changed at 1,898.35

- Hang Seng Index up 4.0% to 21,089.39

- Shanghai Composite up 2.4% to 3,047.06

- Sensex down 0.5% to 56,783.95

- Australia S&P/ASX 200 down 1.2% to 7,346.99

- Kospi down 0.3% to 2,687.45

- German 10Y yield down 3bps to 0.91%

- Euro down 0.2% to $1.0526

- Brent futures down 2.6% to $104.32/bbl

- Gold spot down 0.8% to $1,881.25

- U.S. Dollar Index up 0.41% to 103.38

Top Overnight News from Bloomberg

- A gauge of the dollar advanced as traders positioned for the Federal Reserve to deliver its biggest rate hike since 2000 this week.

- Australian bonds sold off as investors anticipate the nation’s central bank will raise interest rates on Tuesday for the first time since 2010.

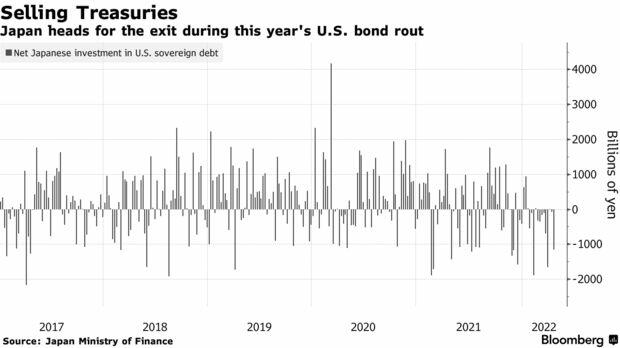

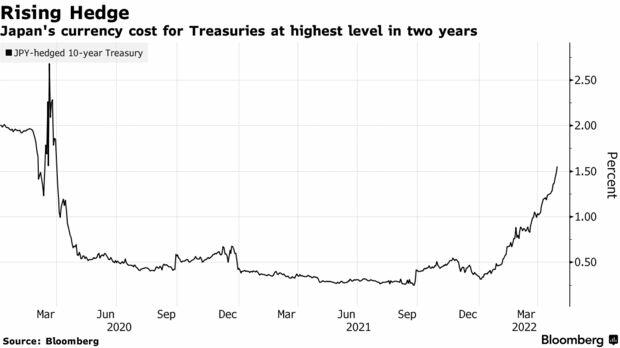

- In times of Treasury turmoil, the biggest investor outside American soil has historically lent a helping hand. Not this time round.

- Oil slipped at the start of the month as investors weighed the impacts of China’s measures to contain the coronavirus and moves by Europe to cut its reliance on fuel from Russia

- In times of Treasury turmoil, the biggest investor outside American soil has historically lent a helping hand. Not this time round

- China’s factory activity fell to the lowest level in more than two years in April, underscoring the economic damage caused by Covid outbreaks and lockdowns and escalating concerns about further disruption to global supply chains

- A widespread sell-off in China is rippling through emerging markets, threatening to snuff out growth and drag down everything from stocks to currencies and bonds

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks declined amid mass holiday closures, weak Chinese PMIs and upcoming key risk events including central bank meetings. ASX 200 underperformed with all sectors pressured as yields edged higher ahead of an expected rate lift-off by the RBA tomorrow. Nikkei 225 was subdued after stalling on approach to the 27,000 level and with participants tentative ahead of a three-day closure. Hang Seng and Shanghai Comp remained shut due to Labour Day holidays but will reopen on Tuesday and Thursday, respectively.

Top Asian News

- Billionaire Cannon-Brookes to Seek Stake in Australia’s AGL

- Asian Factories Defy China Slowdown as Euro Area Loses Momentum

- Marcos Jr. Keeps Lead Ahead of Philippine Presidential Poll

- Australia Yields Hit Highest Since 2014 With RBA, Fed Hikes Seen

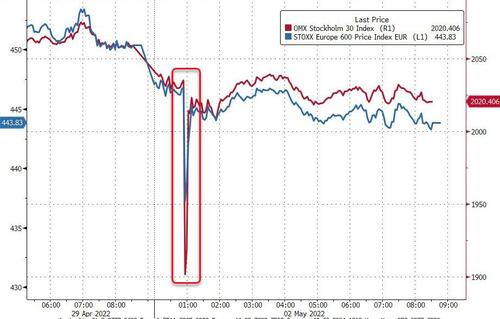

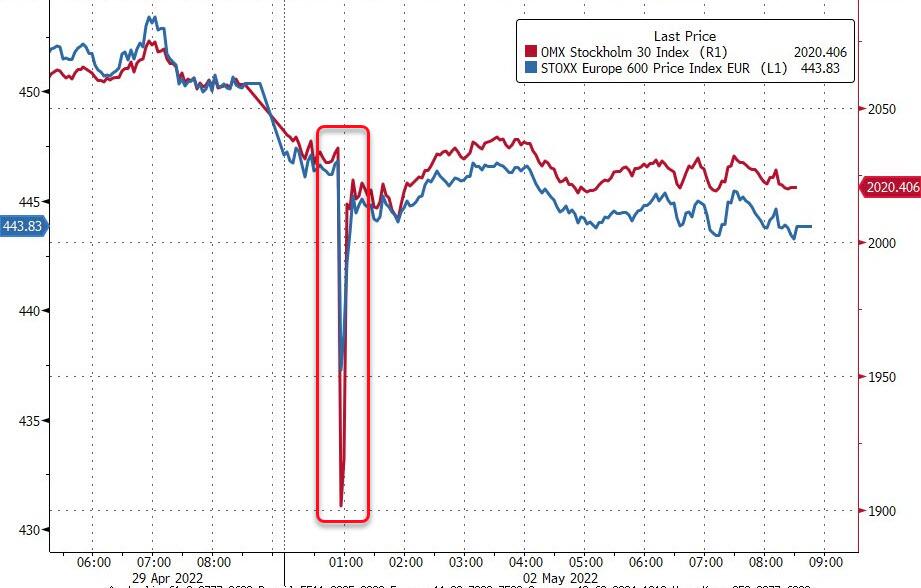

European bourses are lower across the board, Euro Stoxx 50 -1.60%, following a subdued APAC handover amid holiday thinned conditions, soft data and COVID concerns. US futures are firmer across the board, ES +0.3%, but relatively contained ahead of the FOMC and an expected 50bp hike. US and Japan are to increase cooperation in constructing supply chains for cutting-edge semiconductors, via Nikkei. Nasdaq has decided to call for stressed market conditions on all Swedish equity and index derivatives until further notice or at the longest until close of business as of May 2, 2022.

Top European News

- Deutsche Bank AGM Shouldn’t Absolve Leaders, Advisor Says

- Spanish Prime Minister’s Phone Hacked With Spy Software in 2021

- Credit Suisse Falls Most in 2 Months; Outpaces Drop in Swiss SMI

- Partners Group Declines 9.3%, Most in Two Years

FX :

- Specs add to Buck longs before FOMC and NFP, but DXY slips a tad further from 103.930 peak into range above the round number – index meandering from 103.530-100.

- Euro hampered by mixed Eurozone manufacturing PMIs and weaker than forecast sentiment indices as it retreats from 1.0550+ and 0.8400+ vs Dollar and Sterling respectively.

- Recoil in oil undermines Loonie and Norwegian Crown, USD/CAD elevated mostly above 1.2850 and EUR/NOK 9.9000+.

- Aussie underpinned ahead of anticipated RBA hike, AUD/USD straddling 0.7050 and AUD/NZD cross pivoting 1.0950.

- Offshore Yuan weak amidst clean sweep of contractionary Chinese PMIs, USD/CNH not far from retest of 6.7000.

Fixed Income:

- Holiday-thinned trading volumes compound choppy price action as bonds brace for big week to begin May.

- Bunds whipsaw within 154.12-153.25 range, BTPs and Bonos undermined by sub-forecast Italian and Spanish PMIs with 10 year debt futures flattish between 130.71-129.71 and 143.05-140.50 parameters.

- USTs mostly softer and curve steeper awaiting Fed and NFP following the final manufacturing PMI, ISM and construction spending; T-note just under 119-00 vs 119-01 high and 118-22+ low.

Commodities:

- WTI and Brent are pressured with downside occurring alongside the pressure in equities; downside was exacerbated by the loss of multiple psychological support levels.

- Newsflow has been heavily focused on a potential Russian oil/gas embargo, with Hungary remaining heavily opposed; however, Politico reports of a potential compromise for such member nations.

- A missile attack on an oil refinery in Iraq’s Erbil hit an oil tank and caused a fire although the fire was put under control, according to Reuters citing security forces.

- Iraq’s oil exports reached a total of 101mln bbls in April which raised USD 10.55bln in revenues, while exports averaged 3.4mln bpd. It was also reported that Iraq’s Basra Oil Company said a third oil pipeline at the Khor Al-Amaya oil terminal in southern Iraq will be operational by end-2023 with a capacity of 600k bpd, according to Reuters.

- Libya’s NOC announced a temporary resumption of work and lifting of the force majeure at the Zueitina oil terminal to reduce stock and free up storage capacity, according to Reuters.

- Spot gold has lost the USD 1900/oz mark, as yields continue to climb ahead of the FOMC.

US Event Calendar

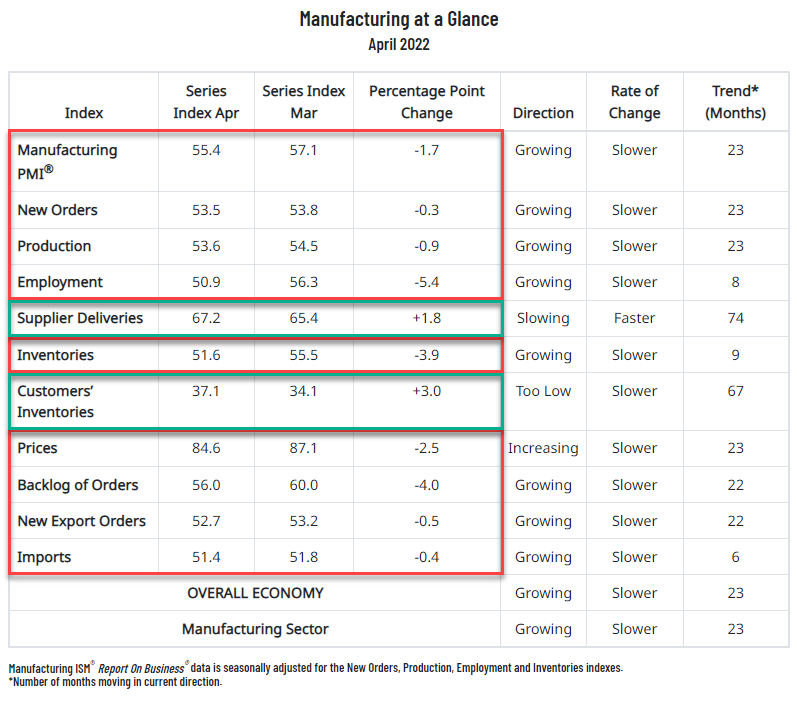

- 09:45: April S&P Global US Manufacturing PMI, est. 59.7, prior 59.7

- 10:00: March Construction Spending MoM, est. 0.8%, prior 0.5%

- 10:00: April ISM Manufacturing, est. 57.6, prior 57.1

- April ISM Employment, est. 55.0, prior 56.3

- April ISM Prices Paid, est. 87.4, prior 87.1

- April ISM New Orders, est. 54.1, prior 53.8

DB’s Jim Reid concludes the overnight wrap

Filling in on the May Day bank holiday as we enter a new month. Despite the holiday, the industrious Henry Allen on our team has put out the April month asset performance review, link available here. The US dollar was among the best performing assets on the month, following the Fed’s anticipated supercharged tightening combined with fluttering risk sentiment, making it the top performing G10 currency YTD. Elsewhere, brent and WTI crude gained for the fifth month in a row, the latest run aided by growing speculation that Europe is prepared to countenance Russian energy embargos. Agricultural goods rounded out the top performers. On the downside, equities and sovereign bonds both lost ground over the month, with the S&P 500 posting its worst monthly return since covid seized markets in March 2020. Credit and EM assets were also down over the volatile month.

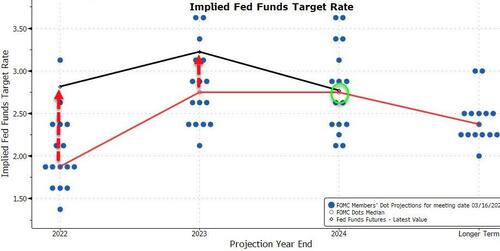

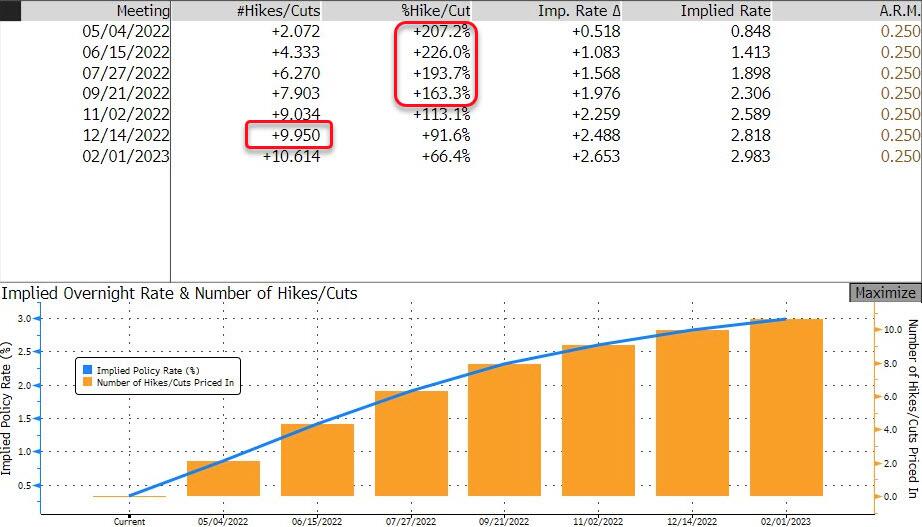

From the month gone to the packed week ahead. The highlight is Wednesday’s FOMC meeting, which our US economics team has previewed in full, here. They believe the Fed will kick tightening up a notch, lifting the fed funds target range by +50bps. The market agrees, and then some, with +51.8bps of tightening priced for the meeting, suggesting some market participants believe there’s still some risk of an even larger hike. Our US econ team believes the Chair will signal this is but the first of a series of potential +50bp hikes, as the Fed tries to get policy to neutral as quickly as possible in light of historic inflation. With the question of how fast the Fed needs to raise rates generally understood (answer: very), focus will shift to how far they need to hike rates to tighten financial conditions adequately.

That task will be augmented by balance sheet rundown, as the Fed has also signaled they will announce the beginning of QT, with the first assets likely rolling off the Fed’s portfolio in June. Our estimates are that QT will proceed through next year, adding around three additional +25bp hikes of tightening, only to stop once the economy careens into recession at the end of 2023.

The BoE is similarly expected to raise rates and signal tighter balance sheet policy on Thursday. Our UK economist full preview can be found here. The team expects the MPC to continue wrestling with the trade-off between slowing growth and intensifying inflation, with the latter winning out and bringing a +25bp Bank Rate hike, along with two more hikes coming this year. On the balance sheet, our team thinks the MPC will confirm its intention to sell gilts later this year, with more guidance coming over the next few meetings and sales beginning in September.

There’s no rest for the weary, as the week ends with the US employment situation report, where our US economists expect nonfarm payrolls to gain +465k, the unemployment rate to tick down to +3.5%, and average hourly earnings to gain +0.2%. Unemployment figures from Europe are also due this week. Production data, starting with ISM manufacturing out later today, also feature this week.

After last week’s mega-cap deluge, this week’s earnings are a sample platter drawing from travel, hospitality, and energy firms.

Available Asian stock markets are trading lower after China’s downbeat PMI data released over the weekend is weighing on the regional investor sentiment. The Nikkei (-0.53%), Kospi (-0.60%) are both trading in negative territory.

The Chinese official manufacturing PMI for April worsened to a level of 47.4 (v/s 49.5 in March), a second straight month of contraction and notching its lowest level since February 2020 as the nation has been severely challenged by the resurgence of Covid-19, leading some firms to reduce or halt production. Additionally, the official non-manufacturing segment slumped by 6.5 percentage points to a level of 41.9 in April, with 19 of the 21 sectors surveyed in the contraction range. Also, a private survey also showed further deterioration in Chinese factory activity with the Caixin manufacturing PMI for April coming in at 46.0, declining from 48.1 in March. This follows last week’s reports that President Xi vows to step up government support in response to the slowdown.

Wrapping up last week’s action. The intensification of China’s lockdowns to stanch the most recent covid outbreak pushed the offshore renminbi -1.72% lower (+0.27% Friday) against the US dollar. The anticipated slowdown in Chinese activity drove global growth fears, prompting cross-asset volatility as investors layer in slower growth into the anticipated central bank reaction function.

US equity volatility reached levels not seen since Russia’s initial invasion of Ukraine, with the Vix picking up +5.18pts to 33.39 (+3.41pts Friday). The macro backdrop interacted with mega-cap tech earnings which painted a mixed outlook, that saw the S&P 500 down -3.27%, a full-3.63% lower on Friday’s month end trading. The STOXX 600 proved more resilient, retreating just -0.64% (+0.74% Friday).

Crude oil prices started the week lower on global demand fears, but eventually recovered following tensions around Russian energy exports to Europe ratcheting higher. Brent crude finished the week +6.92% higher (+1.63% Friday) at $109.34/bbl.

In data, the US employment cost index increased +1.4% versus +1.1% expectations, while core PCE gained +0.3% month-over-month, in line with expectations. Nominal 10yr Treasury yields were up a relatively tame +3.5bps over the week, but the on net figure masks intraweek volatility. 10yr yields were -18.8bps lower intraweek on the growth fears, before selling off more than +11bps on both Wednesday and Friday to finish the week. 10yr bunds were -3.4bps lower over the week (+3.8bps Friday), after hitting much lower troughs as well. Italian spreads widened +14bps to +184bps over 10yr bunds.

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED XX PTS OR XX% //Hang Sang CLOSED XX OR XX% /The Nikkei closed DOWN 29.37 PTS OR 0.11% //Australia’s all ordinaires CLOSED DOWN 1.31% /Chinese yuan (ONSHORE) closed DOWN 6.6084 /Oil DONW TO 101.69 dollars per barrel for WTI and UP TO 104.10 for Brent. Stocks in Europe OPENED MOSTLY CLOSED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6064 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6747: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

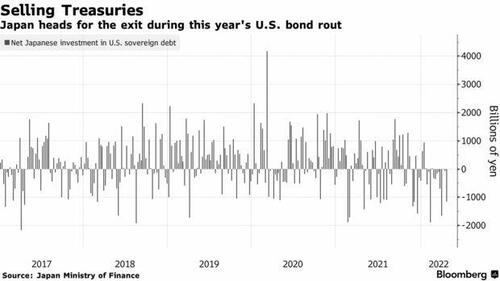

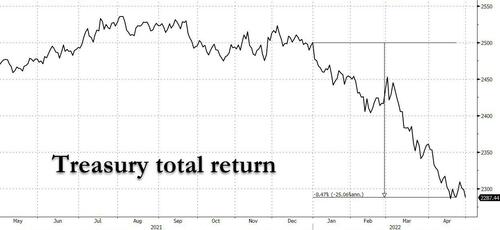

Japan emerges as the biggest driver behind the recent surge in treasury yields.

(zerohedge)

Japan Emerges As Biggest Driver Behind Recent Surge In Treasury Yields

MONDAY, MAY 02, 2022 – 02:43 PM

It was about a year ago, when the calendar was moving from the end of the first quarter of 2021 and into the second quarter, when we first observed something unexpected about the single biggest catalyst behind the forceful emergence of the “reflation trade” in the first quarter, which many interpreted as markets pricing in higher long-term inflation and strong growth. Yet in reality as we reported last year, the move which coincided perfectly with the end of Japan’s fiscal year on March 31..

… was largely, if not exclusively, a byproduct of Japan’s giant pension fund, the GPIF, drastically shifting out of treasuries as it slashed its US Treasury exposure by a record amount.

This left to a blow out in yields, which also coincided with that infamous “failed” 7Y auction in Feb 2021, and was extremely material as most investors mistook the rise in yields as validation for a super-hot economy, and the consensus bought into the idea that 10-year yields were headed above 2%. Of course, as we cautioned investors, yields had overshot relative to the economic reality and over the coming weeks, economic data in the US couldn’t keep up with unrealistic expectations, and 10-year yields started grinding lower (similar to what we expect will happen in the next few months as the market realizes that the US is sliding into recession).