May 5, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 5, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

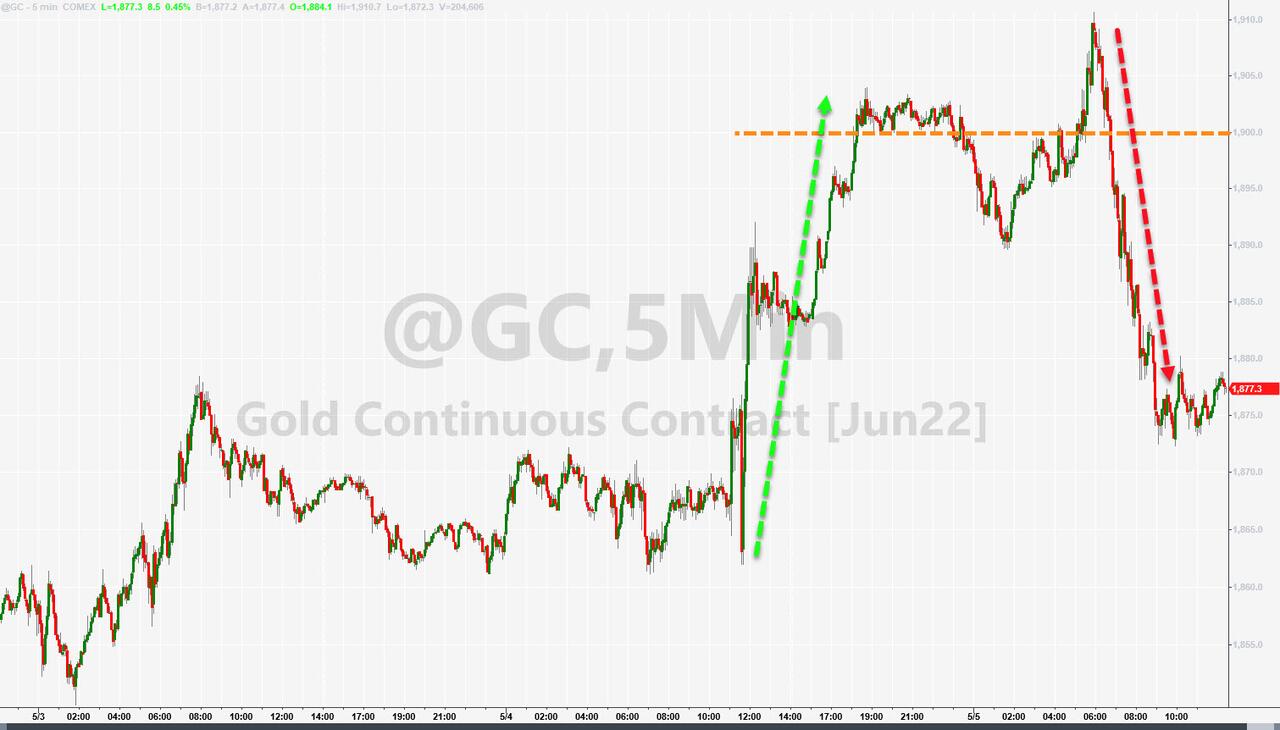

GOLD; $1875.40 up $6.60

SILVER: $22.44 up $.06

ACCESS MARKET: GOLD $1877.50

SILVER: $22.51

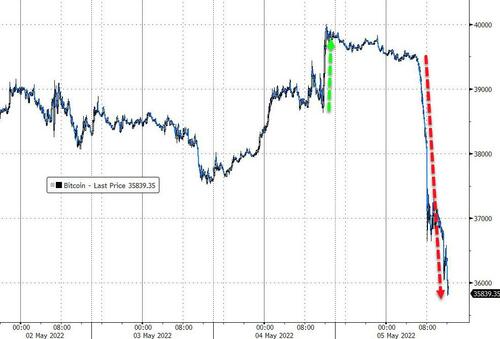

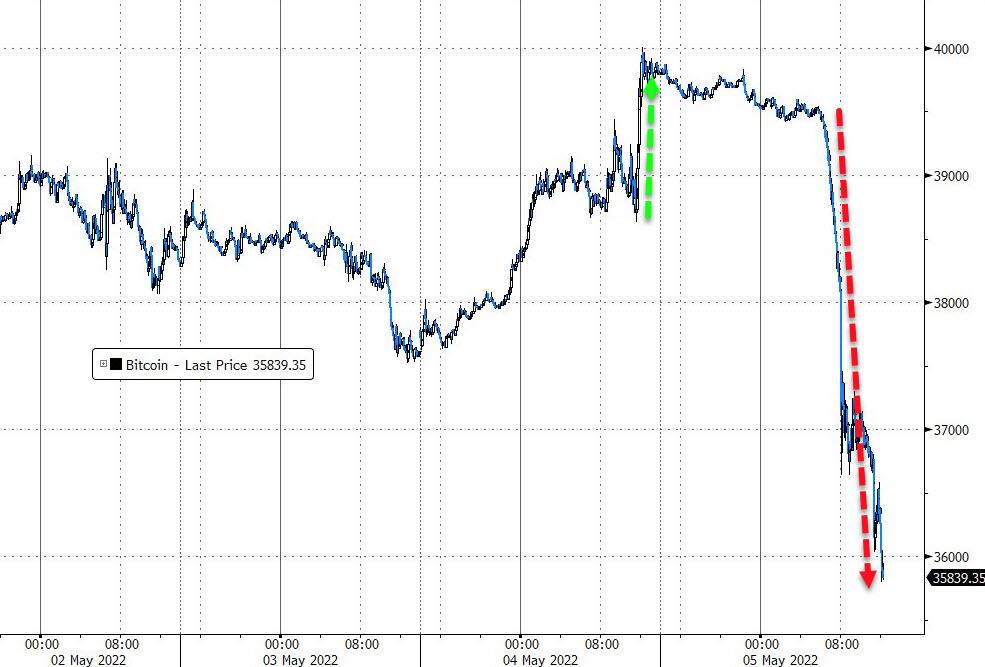

Bitcoin morning price: $39,515 DOWN 333

Bitcoin: afternoon price: $35,612 DOWN 4236

Platinum price: closing down $5.69 to $985.45

Palladium price; closing down at $2187.70

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices: 1/1

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,867.000000000 USD

INTENT DATE: 05/04/2022 DELIVERY DATE: 05/06/2022

FIRM ORG FIRM NAME ISSUED STOPPED

661 C JP MORGAN 1

905 C ADM 1

TOTAL: 1 1

MONTH TO DATE: 1,484

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 1 NOTICE(S) FOR 100 OZ (0.00311 TONNES)

total notices so far: 1484 contracts for 148,400. oz (4.616 tonnes)

SILVER NOTICES:

10 NOTICE(S) FILED 50,000 OZ/

total number of notices filed so far this month 2838 : for 14,190,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $6.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGE IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1089.04 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER up 6

CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF .9300 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.977 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1800 CONTRACTS TO 139,492 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.23) BUT WERE UNSUCCESSFUL IN KNOCKING OUT SOME SILVER LONGS AS WE HAD A VERY STRONG GAIN OF 2670 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 130,000 OZ QUEUE JUMP //NEW STANDING 28.560 MILLION OZ/ // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -1686

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 4 days, total 5061, contracts: 25.305 million oz OR 6.326 MILLION OZ PER DAY. (1265CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 25.305 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 25.305 MILLION OZ//

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1800 DESPITE OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 870 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 130,000 OZ QUEUE JUMP//NEW STANDING 28.560 MILLION OZ// .. WE HAD A HUGE SIZED GAIN OF 2670 OI CONTRACTS ON THE TWO EXCHANGES FOR 13.35 MILLION OZ DESPITE THE STRONG LOSS IN PRICE.

WE HAD 1 NOTICE FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 8545 CONTRACTS TO 568,986 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –4372 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $0.70//COMEX GOLD TRADING/WEDNESDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 100 OZ//NEW STANDING 7,4680 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $0,70 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 10,264 OI CONTRACTS (31.92 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1719 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 573,358.

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 14,636, WITH 12,917 CONTRACTS INCREASED AT THE COMEX AND 1719 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 14,636 CONTRACTS OR 45.525 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1719) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (8545,): TOTAL GAIN IN THE TWO EXCHANGES 10,264 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 100 OZ//NEW STANDING 7.4680 /// 3) ZERO LONG LIQUIDATION //.,4) STRONG SIZED COMEX OI. GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

10,342 CONTRACTS OR 1,034,200 OR 32.167 TONNES 4 TRADING DAY(S) AND THUS AVERAGING: 2586 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES: 32.167 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 32.167/3550 x 100% TONNES 0.905% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 32.17 TONNES INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A HUGE SIZED 1800 CONTRACT OI TO 139,492 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 870 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 870 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1800 CONTRACTS AND ADD TO THE 870 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 2670 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE STRONG GAIN ON THE TWO EXCHANGES 13.35 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.23 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

Amazing: Denmark releases their gold bar list of official reserves without serial numbers!!

(zerohedge)

Jan Nieuwenhuijs: Denmark releases gold bar list but serial numbers are missing

Submitted by admin on Wed, 2022-05-04 11:28Section: Daily Dispatches

11:24a ET Wednesday, May 4, 2022

Dear Friend of GATA and Gold:

Gold researcher Jan Nieuwenhuijs writes today that central banks are slowly increasing transparency with their gold reserves but that Denmark just took a step away from transparency, publishing a list of its gold bars without including their serial numbers.

Nieuwenhuijs’ analysis is headlined “Denmark Releases Gold Bar List But the Serial Numbers Are Missing” and it’s posted at the Gainesville Coins internet site here:

https://www.gainesvillecoins.com/blog/denmark-releases-gold-bar-list

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Rouble exceeds its 2 year high as Europe undergoes more sanctions. Exporters fearful that the strengthening of the rouble would eat into their holdings, bought the rouble which increased its value

(zerohedge)

Ruble exceeds 2-year high vs. dollar and euro despite more EU sanctions

Submitted by admin on Wed, 2022-05-04 18:39Section: Daily Dispatches

From Reuters

Wednesday, May 4, 2022

The Russian rouble jumped on Wednesday to a more than two-year high against both the dollar and euro, retaining the support of hefty capital controls as the European Union proposed a new package of sanctions against Russia over events in Ukraine.

Movements on Russian markets are affected by the rouble being propped up by capital controls, while stocks are trading with a ban on short selling and foreign players barred from ditching shares in Russian companies without permission.

European Commission President Ursula von der Leyen proposed a phased oil embargo on Russia, as well as sanctioning its top bank and banning its broadcasters from European airwaves, in a bid to deepen Moscow’s isolation.

But with markets returning to action for a few days in the middle of Russia’s long May holidays and no concrete signs that the central bank will scale back controls any time soon, exporters were actively selling foreign currency, concerned that further rouble strengthening would eat into their holdings. …

… For the remainder of the report:

end

‘Gold Matters’ — The timely new book from Egon von Greyerz and Matthew Piepenburg

Submitted by admin on Wed, 2022-05-04 21:46Section: Daily Dispatches

By Egon von Greyerz

Matterhorn Asset Management, Zurich

Tuesday, May 3, 2022

Matterhorn Asset Management principals Egon von Greyerz and Matthew Piepenburg are pleased to announce the release of their co-authored book, “Gold Matters,” in e-Book and paperback versions at Amazon here:

The book includes a foreword by Grant Williams and Ronni Stoeferle.

For our newsletter followers, please know that the e-Book will be available at just $1.99 for a limited promotional-period. We are confident that “Gold Matters” encapsulates the core themes of our consistent message for owning physical gold.

In the first week of the book’s release, we would greatly appreciate your feedback (as well as Amazon book reviews, made here —

— on what we hope will become a leading work in precious metals investing.

“Gold Matters” is a much-needed examination of gold as a timeless wealth preservation asset in a modern setting of unprecedented financial risk. Never before have financial systems been stretched this dangerously thin. Never before have investors faced a future of such epic change demanding immediate solutions. …

… For the remainder of the commentary:

end

5. Other gold commentaries

.

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 20.70 PTS OR .68% //Hang Sang CLOSED DOWN 76.12 OR 0.36% /The Nikkei closed //Australia’s all ordinaires CLOSED UP .98% /Chinese yuan (ONSHORE) closed DOWN TO 6.6200 /Oil UP TO 108.12 dollars per barrel for WTI and UP TO 111.04 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6200 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6525: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 8,545 CONTRACTS TO 568,986 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR TINY GAIN OF $0.70 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1719 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1719 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1719 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1719 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 14,636 CONTRACTS IN THAT 1719 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED COMEX OI GAIN OF 10,264 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR TINY GAIN IN PRICE OF GOLD $0.70.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (7.4680),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 7.468 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.70) AND WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A GIGANTIC SIZED GAIN OF 45.5247 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (7.468 TONNES)…

WE HAD 4372 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 10,264 CONTRACTS OR 1,026,400 OZ OR 31,92TONNES

Estimated gold volume today: 231,744/// fair

Confirmed volume yesterday:192,767 contracts fair

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 5

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | NIL oz |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 76,862.305 oz HSBC |

| No of oz served (contracts) today | 1 notice(s) 100 OZ 0.00311 TONNES |

| No of oz to be served (notices) | 917 contracts 91700 oz 2.852 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1484 notices 148,400 OZ 4.61586 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

1 customer deposit

i) Into HSBCL 76,862.305 oz

0 customer withdrawals:

total withdrawal: nil oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 918 contracts having LOST 32 contracts

We had 33 notices filed on Monday, so we gained 1 contract or 100 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 4741 contracts down to 420,192 contracts

July has a gain of 17 OI to stand at 141

August has a gain of 15,259 contracts up to 98,660 contracts

We had 1 notice(s) filed today for 100 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 30 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1484) x 100 oz , to which we add the difference between the open interest for the front month of (MAY xxx CONTRACTS ) minus the number of notices served upon today 1 x 100 oz per contract equals 240,000 OZ OR 7.4680 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1484) x 100 oz+ (918) OI for the front month minus the number of notices served upon today (1} x 100 oz} which equals 240,100 oz standing OR 7.4680 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 7.4680 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626.135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 36,046.375.907 OZ (1121.19 TONNES)

TOTAL ELIGIBLE GOLD: 18,238,460.914 OZ (567.29 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,807,914,993 OZ (553.906 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,866288.0 OZ (REG GOLD- PLEDGED GOLD) 493.508tonnes

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 5

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 300,092.900 oz CNT |

| Deposits to the Dealer Inventory | 39,755.700 OZ Manfra |

| Deposits to the Customer Inventory | 1,768,665.280 oz JPMorgan |

| No of oz served today (contracts) | 10CONTRACT(S) 50,000 OZ) |

| No of oz to be served (notices) | 2874 contracts (14,370,000 oz) |

| Total monthly oz silver served (contracts) | 2838 contracts 14.190,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

ii) Into JPMorgan: 1,768,265.280 oz

total deposit: 1,768,265.280 oz

JPMorgan has a total silver weight: 176.025 million oz/333.564 million =52.77% of comex

Comex withdrawals: 1

i) Out of CNT; 300,092.900 oz

total withdrawal 300,092.900 oz

3 adjustments:

customer to dealer: HSBC 10,022.89 oz

dealer to customer:(a) JPMorgan 597,506.600 oz

and (b) Loomis: 4854.810 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.067 MILLION OZ

TOTAL REG + ELIG. 333.564 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 2884 HAVING LOST 43 CONTRACTS. WE HAD 69 NOTICES FILED ON WEDNESDAY

SO WE GAINED 26 CONTRACTS OR A QUEUE JUMP OF 130,000 OZ

JUNE HAD A LOSS OF 38 TO STAND AT 1756

JULY HAD A GAIN OF 1061 CONTRACTS UP TO 113,245 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes: 72,074// est. volume today// good

Comex volume: confirmed yesterday: 61,948 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 2828 x 5,000 oz = 14,190,000 oz

to which we add the difference between the open interest for the front month of MAY(2884) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 2838 (notices served so far) x 5000 oz + OI for front month of MAY (2884) – number of notices served upon today (1) x 5000 oz of silver standing for the MAY contract month equates 28,560,000 oz. .

We GAINED 26 contracts or 130,000 will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

APRIL 4/WITH GOLD UP $.70//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1091.73 TONNES

APRIL 1///WITH GOLD DOWN $19.00 : A SMALL CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES INTO THE GLD///INVENTORY RESTS AT 1091.73 TONNES

MARCH 31/WITH GOLD UP $13.30 TODAY: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD FROM MONDAY A WITHDRAWAL OF 1.71 TONNES FROM THE GLD:INVENTORY RESTS AT 1091.44

MARCH 28/WITH GOLD DOWN $14.65: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.18 TONNES

MARCH 25/WITH GOLD DOWN $7.60 : A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.52 TONNES INTO THE GLD///INVENTORY RESTS AT 1093.18 TONNES

MARCH 24/WITH GOLD UP $24.95: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.06 TONNES INTO THE GLD..//INVENTORY RESTS AT 1087.66 TONNES

MARCH 23/WITH GOLD UP $15.75//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1083.60 TONNES

MARCH 22/WITH GOLD DOWN $7.75: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.16 TONNES OF GOLD DEPOSITED INTO THE GLD//INVENTORY RESTS AT 1083.60 TONES

CLOSING INVENTORY FOR THE GLD//1089.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

APRIL 4/WITH SILVER DOWN 5 CENTS TO CHANGES IN SILVER INVENTORY AT THE SLV//: A DEPOSIT OF 6.326 MILLION OZ//INVENTORY REST AT 564.966 MILLION OZ//

APRIL 1/WITH SILVER DOWN 39 CENTS A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.302 MILLION OZ INTO THE SLV////INVENTORY REST AT 558.647 MILLION OZ//

MARCH 31/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 2.171 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 556.345 MILLION OZ

MARCH 28/WITH SILVER DOWN 30 CENTS TODAY: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.847 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 554.167 MILLION OZ//

MARCH 25/WITH SILVER DOWN 20 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 24/WITH SILVER UP 54 CENTS TODAY; A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.092 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 552.320 MILLION OZ//

MARCH 23/WITH SILVER UP 24 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

MARCH 22/WITH SILVER DOWN $0.29 TODAY : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 550.288 MILLION OZ//

SLV FINAL INVENTORY FOR TODAY: 575.977MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

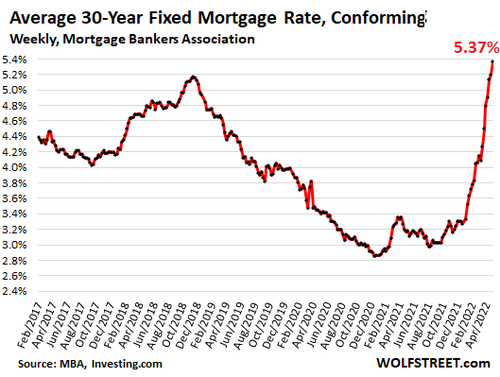

Has The Fed Already Pricked The Housing Bubble?

WEDNESDAY, MAY 04, 2022 – 03:00 PM

The Federal Reserve has raised rates once – a mere 25 basis points (with another hike on the table today). So, it’s just getting started, but has it already popped the housing bubble? It sure looks that way. The question is how long will it take for the air to really start coming out.

As mortgage rates push up, mortgage applications continue to fall. As of last week, applications were down 17%, and at the lowest level since May 2020 when the economy was shut down for COVID, according to last week’s Mortgage Bankers Association’s weekly Purchase Index. The index has dropped 30% from peak demand in late 2020 and early 2021.

Meanwhile, pending home sales in February dropped 4% and another 1.2% in March. It was the fifth consecutive month of sagging home sales.

The average interest rate for 30-year fixed-rate mortgages conforming to Fannie Mae and Freddie Mac limits with 20% down jumped to 5.37% last week, the highest since August 2009. In December 2020, mortgage rates were below 3%.

Between surging mortgage rates and inflated housing prices, more and more buyers are being squeezed out of the market. The MBA report projected continued falling home sales in the months ahead.

The drop in purchase applications was evident across all loan types. Prospective home buyers have pulled back this spring, as they continue to face limited options of homes for sale along with higher costs from increasing mortgage rates and prices. The recent decrease in purchase applications is an indication of potential weakness in home sales in the coming months.”

WolfStreet broke down some numbers to show just how much housing costs have skyrocketed in the last year.

The mortgage on a home purchased a year ago at the median price (per National Association of Realtors) of $326,300, and financed with 20% down over 30 years, at the average rate at the time of 3.17%, came with a payment of 1,320 per month. The mortgage on a home purchased today at the median price of $375,300, and financed with 20% down, at 5.37% comes with a payment of $1,990.”

In other words, buying the same house today will cost you $670 per month more than it did if you bought it last year. That represents a 50% jump in mortgage payments for the same home. This is another example of how CPI understates actual increases in prices.

The Federal Reserve blew up this housing bubble when it artificially suppressed interest rates and bought billions of dollars in mortgage-backed securities. Now the central bank has pricked the bubble by allowing rates to rise ever-so-slightly.

What the Fed giveth, the Fed taketh away.

Looking at the chart, you can see that mortgage rates began to fall in late 2018 as the economy tanked and the Federal Reserve ended its post-2008 rate hike cycle. Rates continued to fall as the Fed pivoted back to quantitative easing and then dropped through the floor with the rate cuts and QE infinity in response to the coronavirus. The big spike in mortgage rates started as the Fed began talking up monetary tightening to tackle raging inflation.

A housing market bust will reverberate through the economy as rising housing prices squeeze Americans already struggling to make ends meet with CPI well over 8%.

Rising mortgage rates also shut off a potential source of cash for millions of Americans. When rates drop, people often refinance their mortgages. But as Peter Schiff pointed out in a recent podcast, rising rates have already squeezed virtually everybody out of the refi market.

There’s nobody who can now refinance their mortgage into a lower rate because everybody’s got a better rate than what they can get now. And that refi lifeline has been a major lifeline for the economy because it’s given households a source of income.”

Refinancing not only provides a lump sum of cash to spend but also lowers mortgage payments, taking some strain off the monthly budget.

There was a wave of refinancing in 2019 after the Fed’s monetary U-turn started pushing mortgage rates lower. But over the last several months, the refi market has collapsed. Mortgage refinances have dropped 70% from a year ago and 80% from the peak in March 2020. That means we no longer have mortgage refinancing to support consumer spending.

The impact of rising rates and falling home sales are already rippling through the mortgage industry. Last week, Wells Fargo, one of the largest mortgage lenders in the US, announced layoffs. Other lenders have trimmed staff as well, including Softbank-backed mortgage “tech” startup Better.com, PennyMac Financial Services, Movement Mortgage and Winnpointe Corp.

As WolfStreet put it, “that boom is over.”

And the Fed has just now begun to push up interest rates, way too little and way too late, but it is finally plodding forward in order to deal with this rampant four-decade high inflation, after 13 years of rampant money-printing – an inflation of the magnitude the majority of Americans has never seen before.”

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

‘Gold Matters’ — The timely new book from Egon von Greyerz and Matthew Piepenburg

Submitted by admin on Wed, 2022-05-04 21:46Section: Daily Dispatches

By Egon von Greyerz

Matterhorn Asset Management, Zurich

Tuesday, May 3, 2022

Matterhorn Asset Management principals Egon von Greyerz and Matthew Piepenburg are pleased to announce the release of their co-authored book, “Gold Matters,” in e-Book and paperback versions at Amazon here:

The book includes a foreword by Grant Williams and Ronni Stoeferle.

For our newsletter followers, please know that the e-Book will be available at just $1.99 for a limited promotional-period. We are confident that “Gold Matters” encapsulates the core themes of our consistent message for owning physical gold.

In the first week of the book’s release, we would greatly appreciate your feedback (as well as Amazon book reviews, made here —

— on what we hope will become a leading work in precious metals investing.

“Gold Matters” is a much-needed examination of gold as a timeless wealth preservation asset in a modern setting of unprecedented financial risk. Never before have financial systems been stretched this dangerously thin. Never before have investors faced a future of such epic change demanding immediate solutions. …

… For the remainder of the commentary:

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //FERTILIZER

World’s Largest Fertilizer Company Warns Crop Nutrient Disruptions Through 2023

THURSDAY, MAY 05, 2022 – 04:15 AM

The world’s largest fertilizer company warned supply disruptions could extend into 2023. A bulk of the world’s supply has been taken offline due to the invasion of Ukraine by Russia. This has sparked soaring prices and shortages of crop nutrients in top growing areas worldwide; an early indication of a global food crisis could be in the beginning innings.

Bloomberg reports Canada-based Nutrien Ltd.’s CEO Ken Seitz told investors on Tuesday during a conference call that he expects to increase potash production following supply disruptions in Russia and Ukraine (both major fertilizer suppliers). Seitz expects disruptions “could last well beyond 2022.”

Seitz said the conflict plus Western sanctions on Russia and Belarus has reduced fertilizer supply on global markets and could reshape crop nutrient trade, thus creating even more supply uncertainty.

“Could there be a change in global trade patterns as a result? We think that’s a possibility,” he said.

Fertilizer disruptions could be a multi-year event. Already, farmers worldwide are reducing fertilizers, which may threaten yields come harvest time. The repercussions could be huge: Lower yields may exacerbate the food crisis.

Here are the latest signs commercial farmers worldwide are reducing fertilizer usage because of higher prices or shortages.

Revealed last week, SLC Agricola SA, one of Brazil’s largest farming operations, managing fields of soybeans, corn, and cotton fields in an area larger than the state of Delaware, will reduce the use of fertilizer by 20% and 25%.

Coffee farmers in Brazil, Nicaragua, Guatemala, and Costa Rica, some of the largest coffee-producing countries, are expected to spread less fertilizer because of high costs and shortages. A coffee cooperative representing 1,200 farmers in Costa Rica predicts coffee output could slip 15% next year because of soaring fertilizer costs.

The International Fertilizer Development Center (IFDC) warned a reduction in fertilizer use would shrink yields of rice and corn come harvest time. Farmers in China, India, Bangladesh, Indonesia, and Vietnam — the largest rice-producing countries — are spreading less fertilizer, and may result in a 10% reduction in output, equating to about 36 million tons of rice, or enough food to feed a half billion people.

Fertilizer prices in North America have surged hundreds of percent since the summer of 2020.

“Maybe it will be a two-year problem and even then it will take two to four years after that for the deficit to catch up,” The Mosaic Company’s CEO Joc O’Rourke told investors during a call on Tuesday. Mosaic is a top fertilizer company in the US

END.

Looks like there is going to be more turmoi in the commodity field

(zerohedge)

Jamie Dimon Warns Turmoil In Commodity Market Could Get “Much Worse”

THURSDAY, MAY 05, 2022 – 07:00 AM

Like the old saying goes: Hindsight is 20/20. That’s especially true for financial markets and the Federal Reserve. So, while investors wait to see whether the Fed will signal the possibility of a 75 bp rate hike at its next meeting, JPM CEO Jamie Dimon is telling Bloomberg (and its audience) that investors should take a deep breath and trust the Fed, while acknowledging that there’s “a chance” of a policy mistake that could trigger a punishing recession.

On that front, Dimon told Bloomberg during a recent interview that the Fed should have moved more quickly to raise interest rates as inflation rattles the world economy. His comments echoed those made by Ken Griffin during his recent appearance at the Milken conference in LA.

“We’re a little late,” Dimon said. “The sooner they move the better.”

He added that “we have a very strong US economy” and that “businesses are in very good shape.” While the Fed is “a little late”, Dimon said that the “sooner they move, the better”.

“If they can, they are going to need to slow down the economy enough so that 8% starts to come down over time,” Dimon said.

While Dimon said he isn’t a “betting man,” he believes there’s roughly a one-third chance of a “soft landing”, and a one-third chance that the Fed sends the US economy into a “mild recession” – although there’s a chance that a recession could be “much harder than that”.

Asked if he’s afraid of a Fed policy mistake, Dimon insisted that he’s “not afraid of the Fed”, before launching into a diatribe about the importance of “rational, thoughtful” fiscal policy (something he has been preaching about for years).

In addition to a 50bp hike at the close of its latest policy meeting on Wednesday, it’s widely expected that the central bank will announce the start of its balance sheet tapering.

But before investors get too critical, Dimon said they should “take a deep breath” and give the Fed a chance.

But an even bigger risk than the Fed’s rate hike plans is the war in Ukraine, which could take years to play out.

“Global energy is precarious,” he said. “If oil goes to $185 that’s a huge problem for people and we should do everything we can today. We need to pump more oil and gas.”

He said the US government should be more focused on national security, including its energy and food resources.

“The Cold War is back,” Dimon said, who was speaking from the bank’s 2022 CEO Forum. “National security is always the most important thing.”

But the interview with BBG wasn’t Dimon’s only interview on Wednesday. He also gave an interview to the Irish Times, which focused more on the war in Ukraine and its impact on international commodity markets (particularly energy).

“And then you’ve got Ukraine. First and foremost, our hearts go out to the Ukrainian people because of the humanitarian crisis. But it’s a war and we don’t know how it’s going to end. It could get worse. The sanctions could get worse. It’s causing complete turmoil in commodity markets around the world and that could get much worse. That’s what we have to be prepared for.”

He added that the turmoil in international commodity markets could get “much worse” if the war in Ukraine drags on. Because of this, Dimon said the “global energy is precarious” and added that “if oil goes to $185 that’s a huge problem for people and we should do everything we can today. We need to pump more oil and gas.”

Meanwhile, on top of warning about the global risks posed by the war in Ukraine, Dimon also said the “Cold War is back” and that “national security is always the most important thing.”

end

Towards a Global Food Disaster, Engineered through Acts of Political Sabotage: F. William Engdahl – Global ResearchGlobal Research – Centre for Research on Globalization

Inbox

| Robert Hryniak | 2:55 PM (7 minutes ago) | ||

| to |

Wait until real food inflation prices hit this fall. The shock will not be just at the gas pumps.

https://www.globalresearch.ca/biden-cynically-uses-ukraine-cover-food-sabotage/5778694

Cheers

Robert

end

COMMODITIES IN GENERAL//

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6200

OFFSHORE YUAN: 6.6525

HANG SANG CLOSED DOWN 76.12 OR 0.36%

2. Nikkei closed

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 103.16/Euro RISES TO 1.0580

3b Japan 10 YR bond yield: RISES TO. +.224/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129,78/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.0.944%/Italian 10 Yr bond yield RISES to 2.88% /SPAIN 10 YR BOND YIELD RISES TO 2.01%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 1.91: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO : 3.43

3j Gold at $1897.90 silver at: 22.99 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP .23 roubles/dollar; ROUBLE AT 66.07

3m oil into the 108 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.78 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9778– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0345well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

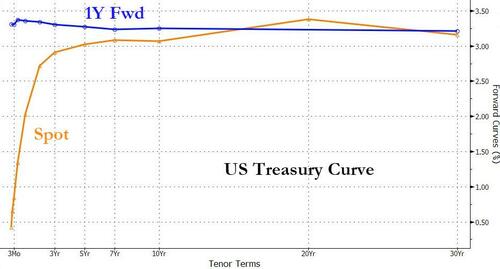

USA 10 YR BOND YIELD: 2.942 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 3.018 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.86

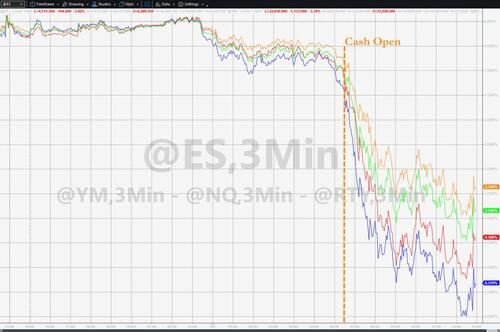

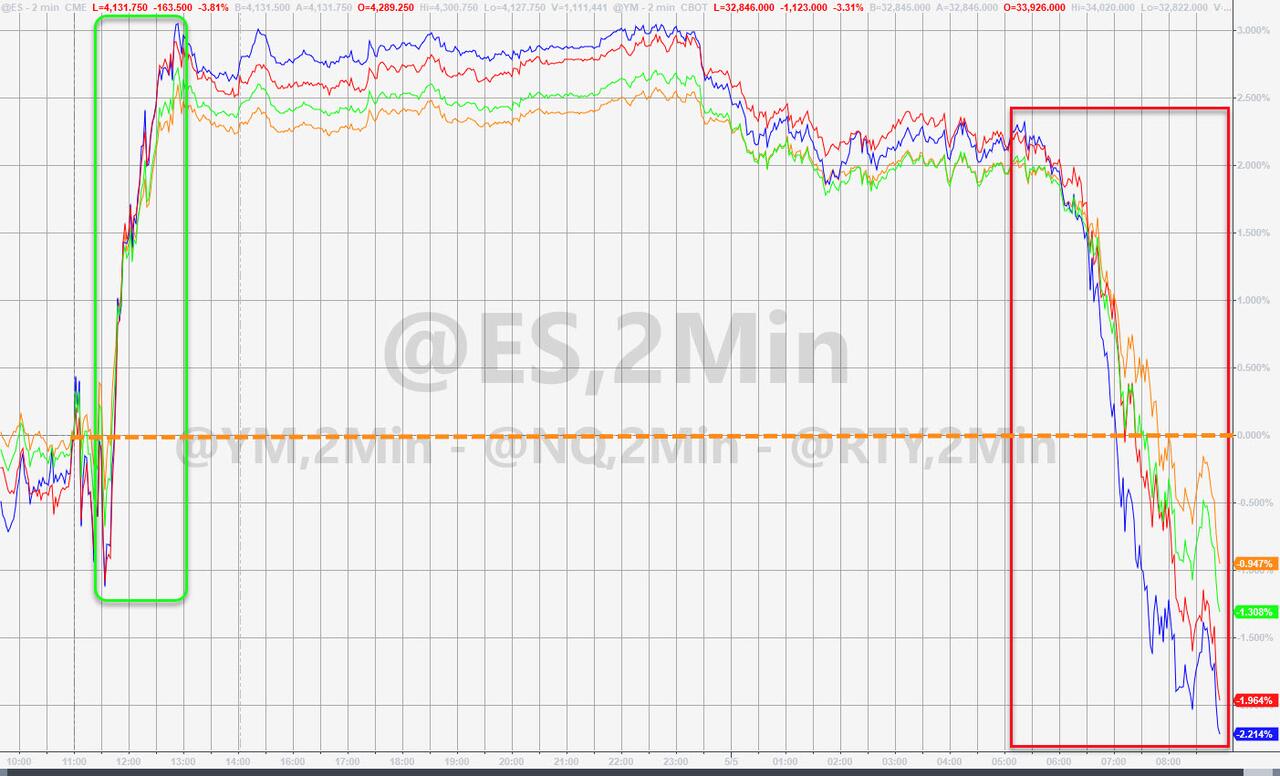

Futures Slip As Traders Read Between Powell’s Lines

THURSDAY, MAY 05, 2022 – 08:13 AM

After yesterday’s torrid, Powell-inspired meltup which saw the S&P soar the most since May 2020 (just days after its biggest drop since June 2020)…

… U.S. futures paused their surge after Jerome Powell eased fears that the Federal Reserve will unleash an even more aggressive tightening path and took a 75bps rate hike off the table. As of 745am EDT, S&P 500 futures dropped 0.6%, while Nasdaq 100 contracts fell 0.8%, as investors digested Powell’s vow to curb inflation, while acknowledging it could inflict some “pain” to the economy. In fact, an example of just what the Fed is fearing came earlier today when the BOE hiked 25bps as expected, but warned a stagflationary recession is be imminent as the central bank now expects GDP to contract while inflation rises double digits in the coming months, which is precisely what happens when central banks are far behind the curve.

In other assets, the dollar jumped to session highs as cable tumbled to July 2020 lows, 10Y yields were flat around 2.95 while bitcoin traded off yesterday’s highs between 39K and 40K.

“Alongside tightening monetary policy, a number of risks – persistently high inflation, indications that consumer demand is softening, and the economic consequences of the Russian invasion of Ukraine – have raised investors’ concerns about the strength of future economic growth,” said Richard Flynn, U.K. managing director at Charles Schwab. “In this context, market volatility is likely to continue.”

For those who missed yesterday’s white knuckle session, the US central bank raised the benchmark rate by a half percentage point on Wednesday, the steepest increment since 2000, in order to keep inflation under control. By ruling out a more aggressive hike, the central bank gave a boost to equity markets, with the S&P 500 posting its biggest daily advance since 2020. The Nasdaq 100 closed 3.4% higher, but is still down 17% this year.

“We are puzzled why the market thinks that Fed hikes are going to stop inflation,” said Nancy Davis, founder of Quadratic Capital Management. “We see inflation as driven by massive government spending, supply chain disruptions and, more recently, by Russia’s invasion of Ukraine.”

Sure, the Fed is powerless to do anything against inflation, but it has to do something. Policy makers are trying to juggle the need to quell the fastest inflation in four decades against hard-won economic growth. In Europe, German factory orders plummeted, highlighting the toll from the war. The soaring price of commodities further complicates efforts to subdue price pressures.

“The combination of high inflation and a weakening global economic outlook has fueled concerns about how far central banks will be able to raise interest rates without overburdening the economy,” Fraser Lundie, head of public fixed income markets at Federated Hermes, wrote in a note to clients.

In premarket trading, EBay plunged 6.9% as analysts said macro headwinds, including the war in Ukraine, inflation and consumer confidence, will pressure results in the near term. The e-commerce firm gave a lackluster sales and profit outlook for the second quarter, as a pandemic-driven sales bump fades. U.S.-listed Chinese stocks dropped again as investors mulled an expanding list of firms that face potential security delistings and the Federal Reserve’s rate decision. JD.com (JD US) shares trade down 2.8%, Pinduoduo (PDD US) -3.5% and Bilibili (BILI US) -5% in premarket. Some other notable premarket movers:

- Albemarle (ALB US) shares jump 14% in premarket trading after the company boosted its profit and sales guidance for the full year, citing continued strength in pricing in the Lithium and Bromine businesses. .

- Hycroft Mining (HYMC US) shares surge as much as 36% in U.S. premarket trading after the precious metals producer gave an update for the first quarter, with the firm saying that its strengthened balance sheet allows it to cut debt, complete technical studies and launch an exploration program.

- Qorvo (QRVO US) analysts said that guidance from the radio frequency solutions fell short of expectations amid weakness in China and high inventory, prompting price target cuts among brokers. Qorvo shares fell 4.9% in postmarket trading on Wednesday after forecasting adjusted earnings per share for the first quarter that missed the average analyst estimate.

- Booking Holdings (BKNG US) impressed analysts with April bookings topping 2019 levels and positive comments on summer travel. The shares rose 7.7% in postmarket trading after the company’s first-quarter revenue and gross bookings both beat the average analyst estimate.

- Twilio (TWLO US) analysts highlighted the gross margin performance and reiteration of guidance as encouraging points in the communication-software provider’s results, though some were left wanting more from the firm’s revenue beat. The shares rose 3.8% in after-hours trading Wednesday after adjusted earnings per share for the first quarter beat the average analyst estimate.

- Fortinet (FTNT US) analysts lauded the infrastructure software company’s solid quarter in light of continued supply chain pressures. The company’s shares rose 7% in extended trading on Wednesday after it reported first-quarter results and raised its full-year forecast.

- Etsy (ETSY US) analysts were overall positive on the e-commerce firm’s results, though noted that challenges relating to the macroeonomic backdrop and the reopening of economies weighed on the company’s outlook. Etsy shares fell 10% in postmarket trading Wednesday after its forecast for second-quarter revenue fell short of the average analyst estimate.

In Europe, the Stoxx 600 was up 1% after rising as much as 1.8%. FTSE 100 up 1.1%, and DAX +1.4%, with most indexes well off session highs. Tech, real estate and industrials were the strongest performing sectors, autos and insurance underperform as gains are faded. Positive results from large caps including Airbus SE, Shell Plc, UniCredit SpA and ArcelorMittal SA also helped brighten the mood. Some notable European movers:

- Airbus jumps as much as 8.5% on a “solid” 1Q, with adjusted Ebit “significantly” above consensus, Bernstein says, with Jefferies noting key highlight is plan to ramp up A320 production.

- Shell shares rise as much as 3.6% after company reports record profit for the quarter. Jefferies said the results signaled “strong” second-half buyback acceleration.

- UniCredit jumps as much as 7.6%, the most intraday since March 29, after reporting revenue for the first quarter that beat estimates. Analysts note “solid” earnings ex-Russia.

- S4 Capital shares soared as much as 20% on Thursday after Martin Sorrell’s media company said it will publish its results for last year tomorrow, following a lengthy delay.

- Outokumpu shares rise as much as 9.3% after the Finnish steel maker presented its latest earnings, which included several beats to consensus estimates, including on adjusted Ebitda.

- Argenx shares rise as much as 6.7% after the Belgian immunology firm posted its latest earnings, which included a large beat on sales for its key drug Vyvgart (efgartigimod).

- Netcompany shares rise as much as 6.1%, the most intraday in a month, after the software developer reported 1Q earnings that are broadly in line with estimates.

- Verbund dropped the most in two months after the Austrian Chancellor said he’s asked the finance and economy ministries to develop new rules to administer windfall profits at state-controlled companies.

- Virgin Money shares slide as much as 6.7% after the lender reported first-half results. Goodbody linked the share price drop to several factors, including the bank not announcing a buyback.

- Hikma Pharmaceuticals fell as much as 11%, the most since April 2020, after the company reduced guidance for its generics division. Peel Hunt calls update “obviously disappointing.”

Earlier in the session, Asia’s stock benchmark rose, poised to snap a three-day decline, as the Federal Reserve’s policy announcement calmed fears about super-sized hikes. The MSCI Asia Pacific Index climbed as much as 1.2% before paring gains to around 0.4%. Tech and materials were the biggest boosts to the Asia gauge as most sectors rose, with TSMC and Infosys hauling up the measure. Bucking the trend, China’s stock gauge closed lower after a three-day holiday in a sign that Beijing’s vow to boost growth has failed to alleviate concerns over the outlook. The Fed delivered a 50-basis-point increase that was in line with expectations on Wednesday, and said a bigger hike was not being actively considered. Benchmarks in the Philippines and Vietnam were among the top gainers in the region. Japan and South Korea markets were closed for holidays. Tech stocks will likely “see a further rally until the next U.S. consumer price inflation reading next week,” said Jessica Amir, a market strategist at Saxo Capital Markets Australia. “The rate hikes weren’t as much as feared,” bond yields have pared and volatility is subsiding, she added. The rally marked a reprieve for Asia’s beaten-down shares, which remain mired in a bear market. The regional benchmark is underperforming U.S. and European peers this year, hurt by the impact of China’s strict Covid-19 restrictions and rising inflation around the region.

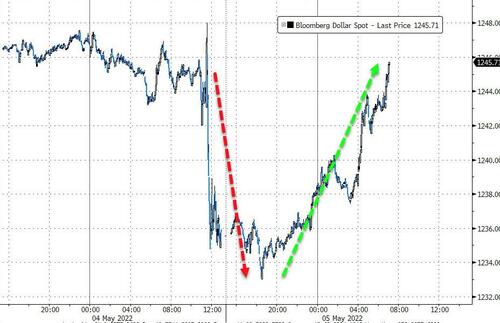

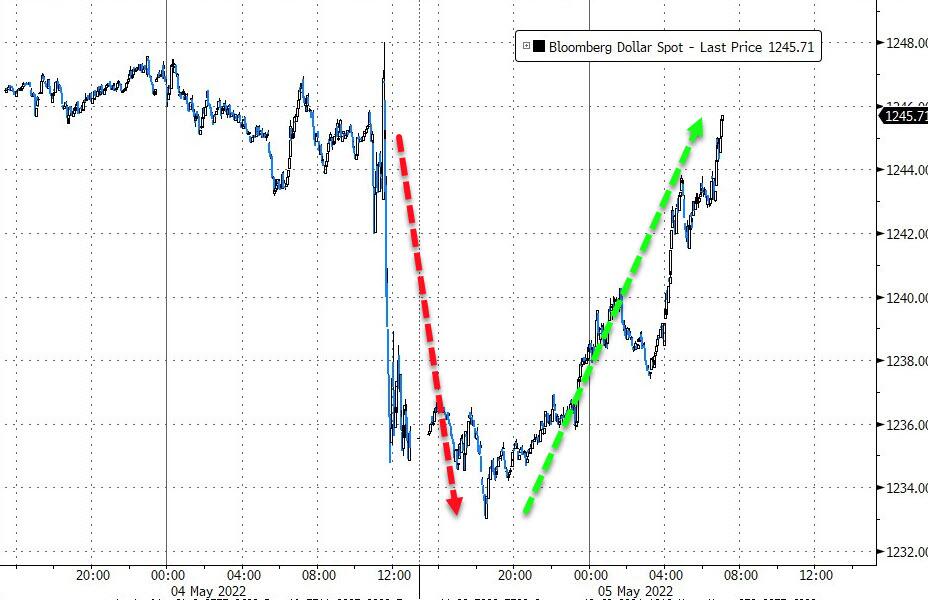

In FX, the Bloomberg Dollar Spot Index jumped as cable tumbled on the BOE’s recession warning, clawing back some of its post-FOMC losses when Powell ruled out a more aggressive pace of monetary tightening. The greenback traded higher against all of its Group-of-10 peers and the Treasury yield curve bear-flattened, trimming some of Wednesday’s aggressive bull steepening which followed the FOMC outcome. The euro fell back below $1.06 and yields on short-dated European bonds fell as ECB hike bets were pared. German factory orders plummeted, highlighting the toll from the war. The pound plunged after the Bank of England warned of a stagflationary recession even as it hiked another 25bps. Norway’s krone held a loss after the central bank kept its key policy unchanged, as widely expected among analysts, and confirmed its plan to deliver a fourth increase in borrowing costs next month. Australia’s dollar pared yesterday’s gains; weaker-than- expected Chinese economic data raised concerns over demand for the nation’s commodity exports and weighed on the Australia’s sovereign bond yields.

China’s yuan dropped as weak economic data hit sentiment. The USD/CNH rose 0.4% to 6.6489; USD/CNY gains 0.2% to 6.6194 after China’s services activity slumped to its weakest level in more than two years in April as Covid outbreaks and lockdowns continued to pummel consumer spending and threaten economic growth. The Caixin China Services purchasing managers’ index crashed to 36.2 in April, the lowest since February 2020, as Covid outbreaks and lockdowns continued to pummel consumer spending, threatening economic growth.

In rates, the Treasury front-end briefly extends losses, following move in gilts after Bank of England hiked 25bp with three voters looking for a bigger 50bp move. U.S. 10-year yields traded around 2.95%, little changed after retreating from day’s high; gilts outperform. Yields cheapened as much as 6bp across front-end of the curve before retreating; U.K. 2-year yields erased the 3bp increase that followed the Bank of England policy announcement; front-end led losses flatten 2s10s, 5s30s spreads by ~2bp and ~4bp on the day. Bear-flattening move has 5s30s spread near session lows into early U.S. session, unwinding portion of Wednesday’s post-Fed bull-steepening. Fed speakers resume Friday with six events slated.

In the aftermath of Wednesday’s policy announcement, overnight swaps are now pricing in close to 50bp rate hikes at the next three policy meetings. Dollar issuance slate empty so far; session has potential to be busy given a number of expected issuers have so far stood down this week. Three-month dollar Libor dropped -3.54bp at 1.37071%, its first decline since April 5.

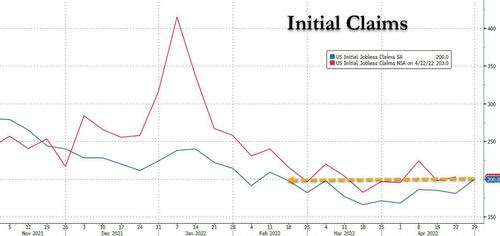

Looking at today’s calendar, we get the BoE policy decision (a hike of 25bps as noted earlier, but accompanied by a very dovish warning of recession in late 2022) and UK local elections. Otherwise from central banks, we’ll hear from the ECB’s Lane, Holzmann and Centeno. Data releases include the weekly initial jobless claims from the US and nonfarm productivity. Finally, earnings releases today include Shell.

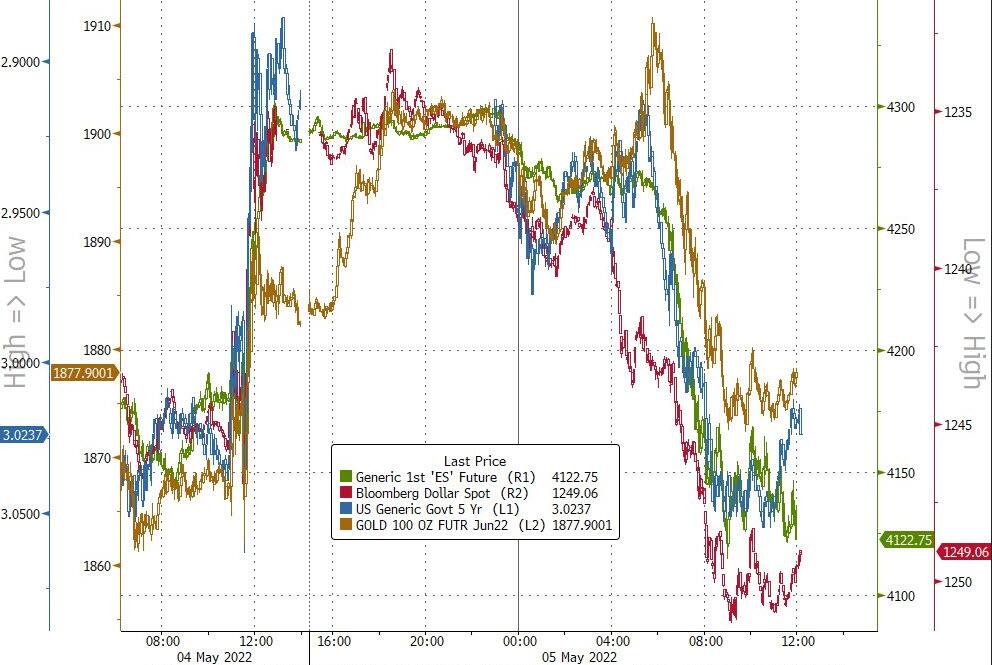

Market Snapshot

- S&P 500 futures down 0.7% to 4,267.00

- MXAP up 0.4% to 167.94

- MXAPJ up 0.4% to 556.06

- Nikkei down 0.1% to 26,818.53

- Topix little changed at 1,898.35

- Hang Seng Index down 0.4% to 20,793.40

- Shanghai Composite up 0.7% to 3,067.76

- Sensex up 0.3% to 55,834.32

- Australia S&P/ASX 200 up 0.8% to 7,364.65

- Kospi down 0.1% to 2,677.57

- STOXX Europe 600 up 1.2% to 446.50

- Brent Futures up 0.4% to $110.56/bbl

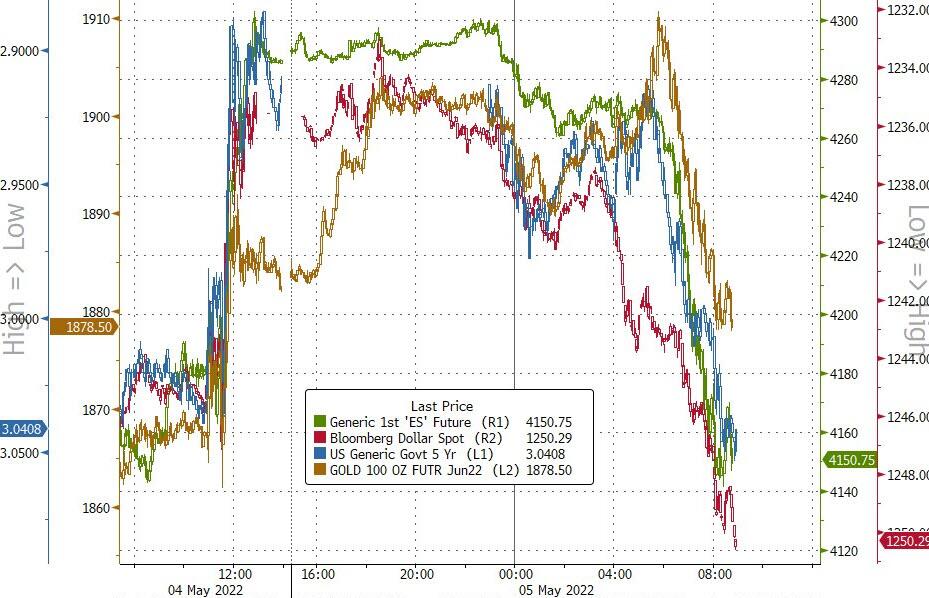

- Gold spot up 0.5% to $1,890.84

- U.S. Dollar Index up 0.34% to 102.94

- German 10Y yield little changed at 1.01%

- Euro down 0.3% to $1.0587

Top Overnight NEws from Bloomberg

- ECB Executive Board member Fabio Panetta said economic expansion has almost ground to a halt in the euro area and faces further “high costs” as policy makers battle record inflation

- On the eve of the 25th anniversary of its independence, the U.K. central bank is widely expected to hike interest rates to 1% — the highest since the financial crisis — and lay out how it intends to take uncharted steps toward unwinding more than a decade of bond purchases

- U.K. Prime Minister Boris Johnson will meet his Japanese counterpart Fumio Kishida in London where they are expected to discuss a plan to support Asian nations in diversifying away from Russian oil and gas

- Boris Johnson has been engulfed by scandal for months and came close to being ousted by members of his Conservative Party. On Thursday, voters across the U.K. are likely to give him their own kicking. Local election results typically deliver losses for ruling parties, especially if they’ve been in power for 12 years as the Tories have

- The Reserve Bank of New Zealand’s Monetary Policy Committee will return to a full complement of seven for the first time this year when it meets later this month. Assistant Governor Karen Silk joins the RBNZ on May 16 and will be an internal member of the committee from that date

- The dollar fell Wednesday by the most in nearly a month on a trade-weighted basis following the latest Federal Reserve policy decision yet pairs some of those losses as the move was more down to short-term positioning

A more detailed breakdown of global markets courtesy of Newsquawk

Asia-Pac stocks traded positively as the region reacted to the FOMC meeting where the Fed hiked rates by 50bps as expected and announced to begin reducing the balance sheet from next month, while Fed Chair Powell dispelled concerns of a more aggressive 75bps rate hike. ASX 200 was firmer with gold miners buoyed by higher prices and as the energy sector benefitted from the proposed Russian oil embargo. Hang Seng and Shanghai Comp were higher following the mainland’s return from the Labour Day holidays but with advances initially contained by several headwinds including an extension of COVID restrictions in Beijing, the deterioration in Caixin Services and Composite PMIs, while the US SEC added over 80 companies to its list for possible delisting and HKMA also hiked its base rate by 50bps in lockstep with the Fed.

Top Asian News

- Concerns Mount Over Asset Sales; Stocks Fall: Evergrande Update

- S&P 500 Remains Expensive Despite Yield-Driven Drop: Macro View

- North Korea Lifts Sweeping Lockdown After One Day, Yonhap Says

- India’s Surprise Rate Hike Spurs Aggressive Tightening Bets

European bourses are firmer across the board, Euro Stoxx 50 +1.3%, benefitting from the perceived less-hawkish Fed and associated Wall St./APAC performance. Stateside, futures are softer across the board though the likes of the ES remain in relative proximity to overnight best levels, ES -0.5%. Back to Europe, sectors are mostly positive with Real Estate and Tech the outperformers while defensive-biased names are lagging.

Top European News

- UniCredit Takes $2 Billion Hit on Russia to Cover Potential Exit

- U.K. April Composite PMI 58.2 vs Flash Reading 57.6

- BMW Profit Beats Estimates on Strong Demand for Top-End Cars

- Norway Rate Hike Locked and Loaded for June to Quell Inflation

FX:

- Dollar finds its feet after FOMC fall out on less hawkish than factored in policy guidance from Fed chair Powell, DXY back within reach of 103.000 vs 102.340 low.

- Aussie* undermined by much weaker than forecast building approvals, mixed trade, technical and psychological resistance; AUD/USD closer to 0.7200 than 0.7250 and AUD/NZD fades just shy of 1.1100.

- Sterling weak on super BoE Thursday on prospects that MPC may be more circumspect after latest 25 bp hike; Cable down around 1.2550 vs 1.2635 peak and EUR/GBP firm on 0.8400 handle.

- Euro underpinned by rebound in EGB yields and option expiries as 1.8 bn rolls off 1.0600.

- Loonie cushioned by crude alongside Norwegian Crown after no change in rates by Norges Bank that is sticking to schedule for next quarter point hike in June; USD/CAD mostly sub-1.2750 and EUR/NOK capped below 9.9000.

- Turkish Lira deflated as CPI soars even further beyond target and PPI over 100%.

- Polish Zloty awaits 100 bp hike from NBP and Czech Koruna 50 bp courtesy of CNB.

- Brazil’s Central Bank raised the Selic rate by 100bps to 12.75%, as expected, while it left the door open to further monetary tightening at a slower pace and considered it appropriate to advance the process of monetary tightening significantly into even more restrictive territory. BCB also stated that inflationary pressures arising from the pandemic period have intensified due to problems related to the new COVID-19 wave in China and the Ukraine war, according to Reuters.

- Norges Bank: Key Policy Rate 0.75% (exp. 0.75%, prev. 0.75%). Reiterates that the next hike will “most likely” occur in June. Adds, the Krone has recently depreciated and is now weaker than projected.

Fixed Income

- Very volatile moves in bonds between the FOMC, BoE and NFP, with Treasuries flipping from bull-to-bear steepening.

- 10 year note soft within wide 119-09+/118-19+ range, Bunds flat between 153.79-152.74 parameters and Gilts firm in catch-up trade either side of 118.00.

- Bonos and Oats off best levels after digesting Spanish and French multi-tranche debt issuance

Commodities

- WTI and Brent have been pivoting relatively narrow ranges ahead of today’s JMMC/OPEC+ gatherings, currently posting gains of USD 0.30/bbl.

- OPEC+ is expected to maintain its policy of increase the output quota by 432k BPD in June, lifted from the 400k BPD in May as part of the pacts terms; newsquawk preview here.

- Spot gold is bid but lost the USD 1900/oz mark in early-European trade, a figure it has spent the morning modestly below.

- Norway’s labour unions said initial wage talks with oil firms broke down and they will proceed with mediation, according to Reuters.

Crypto

- Bitcoin is subdued and returned to existing session lows of USD 39.4k amid coverage of the below WSJ story; more broadly, Bitcoin has been steady at the lower-end of the morning’s ranges.

- US Senators Warren and Smith have sent a letter to Fidelity over its Bitcoin 401(k) plan which would allow investors to allocate as much as 20% of their portfolios into Bitcoin, according to WSJ; senators suggest that Bitcoin could be too risky for savers.

US Event Calendar

- 08:30: 1Q Unit Labor Costs, est. 10.0%, prior 0.9%

- 08:30: 1Q Nonfarm Productivity, est. -5.3%, prior 6.6%

- 08:30: April Continuing Claims, est. 1.4m, prior 1.41m

- 08:30: April Initial Jobless Claims, est. 180,000, prior 180,000

DB’s Jim Reid concludes the overnight wrap

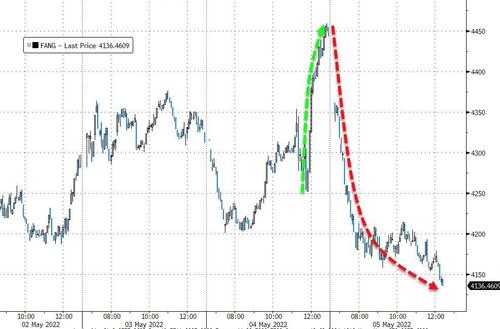

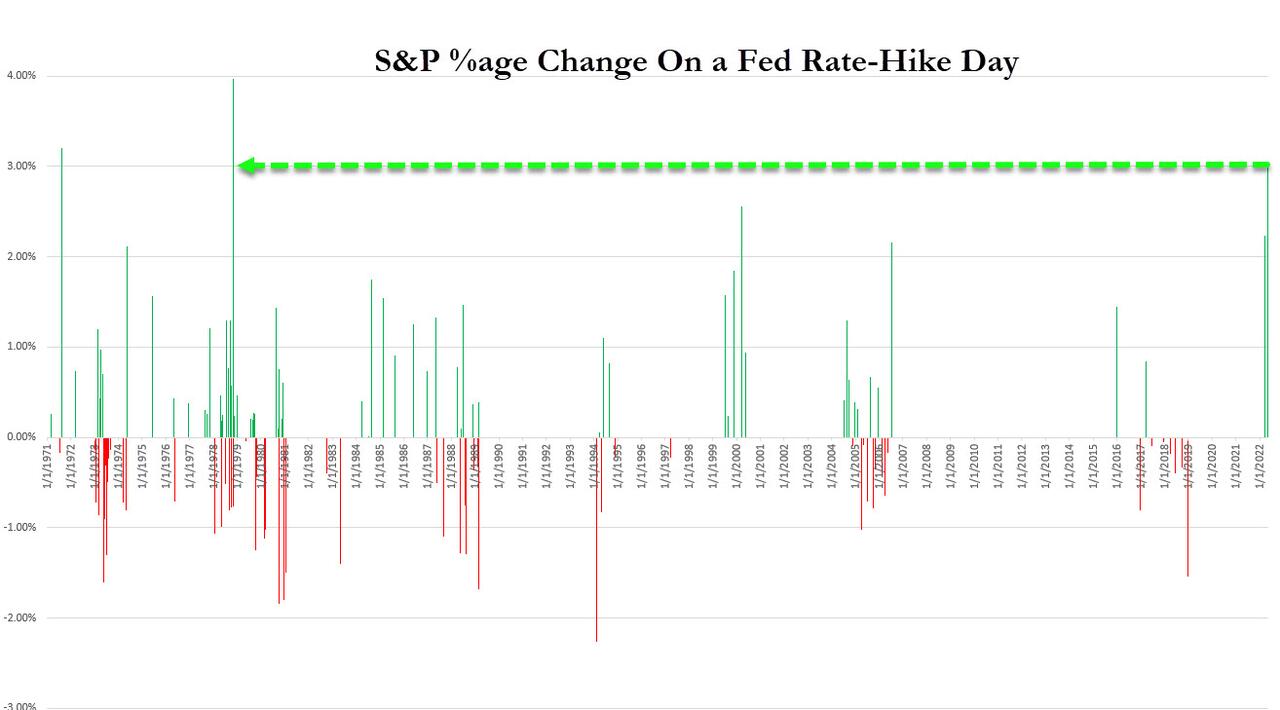

I’m normally asleep at around 945pm each evening but tense football games often disturb that equilibrium and last night was the ultimate sleep disrupter. I was just about to close down my iPad in bed and fall asleep as Man City we’re two goals ahead in injury time in the Champions League semi. I stayed the extra minute and in that minute Real Madrid scored twice, took the game into extra time and ultimately won a stunning tie. I finally turned my iPad off 10 minutes before the end but couldn’t sleep so turned it on again after they won. Liverpool vs Real Madrid will be an epic final! So all in all a hectic evening trying to watch the Fed while my wife and I watched Ozark (stressful in its own right) and then the football. I’m worn out this morning.

So after all that, the Fed intentionally or unintentionally decided that the market has had enough stress for now and clamped down on the more hawkish potential near-term paths for policy. As a result equities soared, yields fell (especially at the front-end), credit tightened, the dollar slumped and oil built on its earlier rally.

Let’s very briefly get the boring bit out of the way in a line or two. Basically the FOMC rose rates by +50bps and signalled they would begin to reduce the size of their balance sheet in June, both in line with our expectations (Our full US econ review is here).

However the most pressing question for markets was how willing the Committee was to consider future rate increases of +75bps. Market participants didn’t have to wait long for an answer, as Chair Powell quickly noted that +75bp hikes were not actively being considered, while +50bp hikes were on the table for the “next couple” of meetings. In line, market pricing for the next two meetings ended the day at +100bps, having stripped out any of the small, but recently growing, premium priced in for +75bps over the June and July meetings. The firm rebuke led to a rally in Treasury yields, led by the short-end, as 2yr yields fell -14.0bps, while 10yr yields were a relatively benign -3.7bps by comparison. The move in nominal 10yrs again masked divergence in the decomposition driven by the market’s dovish interpretation, with breakevens widening +4.9bps to 2.88%, while real yields fell -8.6bps, still managing to finish the day in positive territory at 0.05% though.

Elsewhere in the presser, the Chair made multiple mentions of the Committee’s intention to “expeditiously” get policy towards more neutral levels given the monumental inflation-fighting task at hand. He demurred when asked if policy would ultimately need to reach a restrictive rather than just neutral stance, but did not rule it out. He still maintained hope that the Fed could engineer a soft landing after this hiking cycle, but to be fair, it is hard to imagine him saying anything else. He cited strong household and consumer balance sheets as reasons for why the economy could withstand the hiking cycle, when indeed, that very strength when inflation is at multi-decade highs is why policy will probably need to reach restrictive levels not currently appreciated by market pricing. In my opinion the Fed can control the near-term market expectations but beyond that it is all about the inflation data. If it doesn’t improve then 50bps will be live at every meeting and not just the “next couple”, and 75bps risks will be back on the table. This is all for another day though.

When all was said and done, the market took -11.7bps out of policy tightening during 2022, with futures implying fed funds hitting 2.77% after the December meeting. Futures are still implying that the Fed will hit its terminal rates sometime in the third quarter next year, but that rate was around -18bps lower following the meeting at 3.24%.

Indeed the breathing space given by the removal of the price hike premiums sent US equities on a tear. Little changed heading into the meeting, the S&P 500 ended the day +2.99% higher, its largest one-day gain since May 2020. Every sector ended in the green, with a full 477 companies posting gains, the most since February. The gains were broad-based, with every sector but real estate (+1.09%) gaining at least 2%, though energy (+4.12%), communications (+3.68%) and tech (+3.51%) were the standouts. In line, the NASDAQ (+3.19%) and FANG+ index (+3.40%) outperformed, on the drop in discount rates.

In Asia, mainland Chinese stocks returned following a few days of holidays and are in positive territory with the Shanghai Composite (+0.95%) and CSI (+0.28%) higher. Meanwhile, the Hang Seng (+0.76%) is trading up, but paring its early morning gains. Elsewhere, the S&P/ASX 200 (+0.67%) is climbing while the Japanese and Korean markets are closed for public holidays. Outside of Asia, contracts on the S&P 500 (-0.08%) and NASDAQ 100 (-0.07%) are fractionally lower. Stoxx 50 futures are +2.4% due to a post Fed catch-up effect.

Early morning data showed that China’s services sector activity contracted further in April as the Caixin services PMI tumbled to 36.2, its lowest level since the initial onset of the pandemic in February 2020 and compared to March’s reading of 42.

Back now to life pre the Fed. Earlier we had seen sovereign bonds sell off in Europe, with yields on 10yr bunds marginally up +0.7bps to 0.97%, having regularly traded above the 1% mark during the session. Those moves were echoed across the continent and there was a further widening in peripheral spreads, with the gap between Italian 10yr yields over bunds widening by +6.7bps to 198bps. That’s their 11th consecutive move wider, and takes the spread to its highest closing level in almost two years. We’ve also seen a similar move with the Spanish spread, which is at its highest in nearly two years as well, at 109bps. It is likely we’ll get a decent reversal this morning though.