May 5, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

May 5, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1883.35 UP $7.95

SILVER: $22.38 DOWN $.06

ACCESS MARKET: GOLD $1883.85

SILVER: $22.36

Bitcoin morning price: $35,745 UP 133

Bitcoin: afternoon price: $35,909 UP 297

Platinum price: closing down $16.95 to $968.50

Palladium price; closing down 139.70 at $2048.00

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

comex notices:336/425

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,874.000000000 USD

INTENT DATE: 05/05/2022 DELIVERY DATE: 05/09/2022

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 2

435 H SCOTIA CAPITAL 2

657 H MORGAN STANLEY 54

661 C JP MORGAN 422 336

709 C BARCLAYS 25

732 C RBC CAP MARKETS 3

737 C ADVANTAGE 3 3

TOTAL: 425 425

MONTH TO DATE: 1,909

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 425 NOTICE(S) FOR 42,500 OZ (1.3219 TONNES)

total notices so far: 1909 contracts for 190,900. oz (5.9377 tonnes)

SILVER NOTICES:

782 NOTICE(S) FILED 3910,000 OZ/

total number of notices filed so far this month 3620 : for 18,100,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

END

GLD

WITH GOLD UP $7.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNESE FROM THE GLD

INVENTORY RESTS AT 1084.98 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 6 CENTS

CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF .9300 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.977 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 2098 CONTRACTS TO 141,590 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR TINY $0.06 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.06) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 5768 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 40,000 OZ QUEUE JUMP //NEW STANDING 28.600 MILLION OZ/ // V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -2415

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 5days, total 6316, contracts: 31.580 million oz OR 6.316 MILLION OZ PER DAY. (1263CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 31.480 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 31.580 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2098 DESPITE OUR TINY $0.06 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1255 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 40,000 OZ QUEUE JUMP//NEW STANDING 28.60 MILLION OZ// .. WE HAD A HUMONGOUS SIZED GAIN OF 3353 OI CONTRACTS ON THE TWO EXCHANGES FOR 28.84 MILLION OZ DESPITE THE SMALL GAIN IN PRICE.

WE HAD 782 NOTICE FILED TODAY FOR 3,910,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 4,787 CONTRACTS TO 573,773 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –9938 CONTRACTS. WHAT AN ABSOLUTE FRAUD!!

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED INCREASE IN COMEX OI CAME WITH OUR GAIN IN PRICE OF $6.60//COMEX GOLD TRADING/THURSDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 3900 OZ//NEW STANDING 7,589 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $6,60 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 8,506 OI CONTRACTS (26.457 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3719 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 573,733.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8,506, WITH 4,787 CONTRACTS INCREASED AT THE COMEX AND 3719 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 8,506 CONTRACTS OR 26.457 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3719) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (4,7287,): TOTAL GAIN IN THE TWO EXCHANGES 8,506 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 3700 OZ//NEW STANDING 7.589 /// 3) ZERO LONG LIQUIDATION //.,4) GOOD SIZED COMEX OI. GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

14,061 CONTRACTS OR 1,406,100 OR 43.74 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 2812 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 43.74 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 43.74/3550 x 100% TONNES 1.23% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 43.74 TONNES INITIAL//SLIGHTLY INCREASING AGGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 2098 CONTRACT OI TO 141,590 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1255 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1255 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2098 CONTRACTS AND ADD TO THE 1255 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 3353 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE HUGE GAIN ON THE TWO EXCHANGES 16.764 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.23 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 20.70 PTS OR .68% //Hang Sang CLOSED DOWN 76.12 OR 0.36% /The Nikkei closed //Australia’s all ordinaires CLOSED UP .98% /Chinese yuan (ONSHORE) closed DOWN TO 6.6200 /Oil UP TO 108.12 dollars per barrel for WTI and UP TO 111.04 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6200 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6525: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 4,787 CONTRACTS TO 573,773 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR SMALLISH GAIN OF $6.60 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (3719 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3719 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :3719 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3719 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 8,506 CONTRACTS IN THAT 3719 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY GOOD SIZED COMEX OI GAIN OF 4,787 CONTRACTS..AND THIS GAIN OCCURRED DESPITE OUR SMALL GAIN IN PRICE OF GOLD $6.60.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (7.589),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 7.589 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $6.60) AND WERE UNSUCCESSFUL IN FLEECING QUITE ANY LONGS AS WE HAVE REGISTERED A GIGANTIC SIZED GAIN OF 57.36 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (7.589 TONNES)…

WE HAD 10,000 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 18,444 CONTRACTS OR 1,844,400 OZ OR 57.36 TONNES

Estimated gold volume today: 229,406/// fair

Confirmed volume yesterday:249,526contracts fair

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 6

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 2,103.240 oz HSBC Int Delaware includes 35 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 425 notice(s)42500 OZ 1.3219 TONNES |

| No of oz to be served (notices) | 531 contracts 53,100 oz 1.6516 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1909 notices 190900 OZ 5.9377 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposit

2 customer withdrawals:

i) Out of HSBC 977.955 oz

ii) Out of Int Delaware 1125.285 oz (35 kilobars)

total withdrawal: 2103.240 oz

ADJUSTMENTS: 1 Manfra//dealer to customer 5,707.724 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 956 contracts having GAINED 38 contracts

We had 1 notice filed on Thursday, so we gained 39 contracts or AN ADDITIONAL 3900 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 5312 contracts down to 414,850 contracts

July has a gain of 18 OI to stand at 159

August has a gain of 13,580 contracts up to 110,106 contracts

We had 425 notice(s) filed today for 42,500 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 422 notices were issued from their client or customer account. The total of all issuance by all participants equate to 425 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 336 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1909) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 956 CONTRACTS ) minus the number of notices served upon today 425 x 100 oz per contract equals 244,000 OZ OR 7.589 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1909) x 100 oz+ (956) OI for the front month minus the number of notices served upon today (425} x 100 oz} which equals 244,000 oz standing OR 7.589 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 7.589 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626.135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 36,044,272.667 OZ (1121.12 TONNES)

TOTAL ELIGIBLE GOLD: 18,232,663.831 OZ (567.11 tonnes)

TOTAL OF ALL REGISTERED GOLD: 17,811,608.836 OZ (554.01 tonnes)

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,866288.0 OZ (REG GOLD- PLEDGED GOLD) 493.508tonnes

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 6

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 771,935.280 oz Brinks HSBC Manfra CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 2425,689.130 oz Brinks Delaware JPMorgan |

| No of oz served today (contracts) | 782CONTRACT(S) 3,910,000 OZ) |

| No of oz to be served (notices) | 2100 contracts (10,500,000 oz) |

| Total monthly oz silver served (contracts) | 3620 contracts 18,100,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

ii) Into JPMorgan: 1,772,982.320 oz

iii) Into Delaware: 429,912.930 oz

i) Into Brinks 223,693.900 oz

total deposit: 2,425,689.1300 oz

JPMorgan has a total silver weight: 177.197 million oz/335.218 million =52.86% of comex

Comex withdrawals: 4

i) Out of JPMorgan 600,063.200 oz

ii) Out of Brinks: 950.63 oz

iii) Out of Manfra: 150,673.840 oz

iv)out of HSBC 20,247.610 oz

total withdrawal 771,935.280 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.067 MILLION OZ

TOTAL REG + ELIG. 335.218 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 2882 HAVING LOST 2 CONTRACTS. WE HAD 10 NOTICES FILED ON THURSDAY

SO WE GAINED 8 CONTRACTS OR A QUEUE JUMP OF 40,000 OZ

JUNE HAD A LOSS OF 85 TO STAND AT 1671

JULY HAD A GAIN OF 1129 CONTRACTS UP TO 114,374 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 782 for 3,910,000 oz

Comex volumes: 55,814// est. volume today// fair

Comex volume: confirmed yesterday: 77,177 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 3620 x 5,000 oz = 18,100,000 oz

to which we add the difference between the open interest for the front month of MAY(2882) and the number of notices served upon today 782 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 3620 (notices served so far) x 5000 oz + OI for front month of MAY (2882) – number of notices served upon today (782) x 5000 oz of silver standing for the MAY contract month equates 28,600,000 oz. .

We GAINED 8 contracts or AN ADDITIONAL 40,000 will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WIOTHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

GLD INVENTORY: 1089.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Buckle Up For A Crashing Economy And More Inflation

FRIDAY, MAY 06, 2022 – 10:12 AM

Authored by Michael Maharrey via SchiffGold.com,

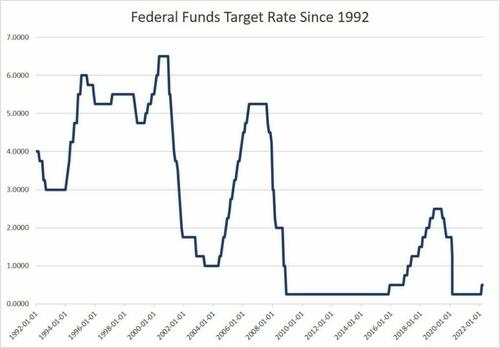

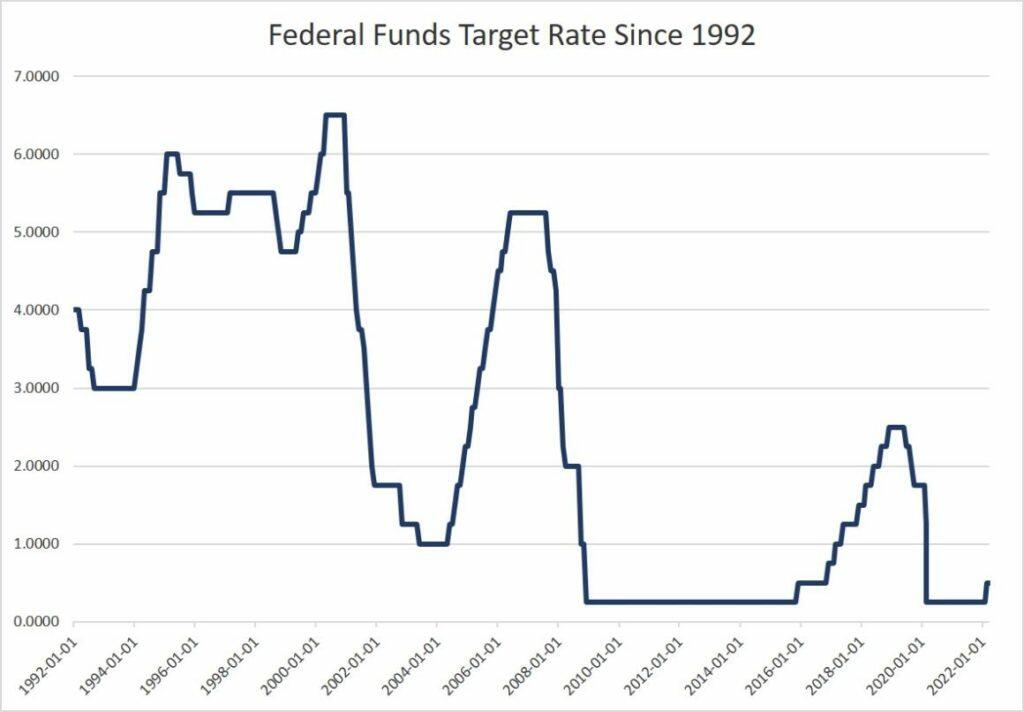

Jerome Powell began hinting that inflation might be a problem last August. In November, Powell retired the word “transitory.” But here we are in May and the Federal Reserve still hasn’t done anything substantive to address the inflation problem.

And now it may be too late. It’s probably time to buckle up for more inflation – and perhaps a crashing economy.

Powell and Company have been talking tough for months, but there hasn’t been a whole lot of action. In March, the central bank raised interest rates a paltry 25 basis points. At the May meeting, the FOMC followed up with a more aggressive 1/2% rate hike but took a 75 basis point rate hike off the table.

Meanwhile, the Fed didn’t even start tapering quantitative easing until January. In mid-April, the balance sheet was still expanding, hitting an all-time high of $8.97 trillion.

At the May FOMC meeting, the Fed unveiled its balance sheet reduction scheme. It was hardly impressive. If the Fed shrinks its balance sheet at the proposed rate, it will be back to pre-pandemic levels in about eight years.

The Fed has targeted a 2.5% interest rate by the end of the year. With GDP already going negative in Q1, it’s questionable that the Fed can get there without completely tanking the economy. There are already signs that the Fed has pricked the housing bubble.

And as Mises Institute senior editor Ryan McMaken pointed out in a recent article, the Fed really needs to push rates much higher than 3%.

One percent may seem high to some market observers of recent rate cycles, but we’re now in a high-inflation environment with price inflation above 8 percent. The Fed is going to have to do more than a mild hike here and there to make a dent in 8 percent CPI (Consumer Price Index) inflation. Even mainstream observers recognize this, and Ken Rogoff this week suggested that the odds of success in bringing down inflation with rate hikes of 2 percent or 3 percent ‘is really unlikely. I think they’re going to have to raise interest rates to 4% or 5% to bring inflation down to 2.5% or 3%.’”

Needless to say, this is also highly unlikely. The Fed funds rate has not risen above 2.5% since the 2008 financial crisis. The last time interest rates were above 5% was August 2007 – as the housing bubble was deflating and setting up the ’08 crash.

McMaken sums it up this way.

So as we look to the May Federal Open Market Committee meeting, the likely scenario is a small rate hike in the face of 8 percent inflation, with no significant changes to the balance sheet. That’s what we’re likely to get after months of increasingly hawkish talk from the Fed: Virtually nothing.”

And as already mentioned, the economy has started to sour, even though the Fed is just getting into the ring for this inflation fight. McMaken said, “It is increasingly clear why the Fed is unwilling to make any sudden movements.”

The economy is increasingly weak, and those in favor of the narrative that the US is in the midst of an economic boom have nothing to stand on but a low unemployment rate.”

Fed Chair Jerome Powell and others continue to harp on low unemployment and a labor shortage as signs of a booming economy. But as McMaken points out, “reciting employment statistics in the midst of forty-year inflation highs and a shrinking economy has its limits.”

In fact, it betrays a sizable level of denial since, as Danielle DiMartino Booth noted on Tuesday, ‘Unemployment is the most lagging of all economic indicators.’ If Powell relies on unemployment numbers to explain why the economy is ‘strong,’ he will simply ‘evicerat[e] his credibility.’”

Peter Schiff questioned the Fed’s credibility in a recent podcast, saying it’s in a very precarious position.

What happens when we end up in a recession? What happens to the Fed’s credibility? Because, after all, they’ve got everything wrong. First, they said there’s no inflation. Then they said inflation is transitory. Then they admit they got that wrong. And now they see this negative GDP number, and basically, they say that’s transitory too.”

In reality, an evaluation of the economic data has to make any honest person scratch their head and wonder just how strong the economy really is. McMaken sums up the situation nicely.

The reality is that the economy is contracting and personal finances are worsening. Inflation is high and wages are not keeping up. Under these conditions, the Fed will desperately want to embrace more easing so as to stave off a full-blown recession. An example of the Fed tightening just as the economy is weakening? That’s practically a unicorn. The big exception, of course, is Paul Volcker who in the economically weak days of the early 1980s embraced true monetary tightening to reduce inflation. It’s hard to see how Powell could do the same, as Powell has continually demonstrated that his Fed is very much a Fed committed to kicking the can down the road to serve short-term political interests. This is an election year, after all.

“That means it’s time to buckle up for more inflation. And, ultimately, we may get a recession anyway since it may be that all that is necessary to send the economy over the cliff is just another rate hike or two of 0.25 or 0.50 percent.”

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS

What else is new?

(Pam and Russ Martens)

Goldman Sachs’ Says Its Dark Pools Are Under Investigation – Along with About Everything Else the Firm Does

By Pam Martens and Russ Martens: May 6, 2022 ~

We’ve been reading SEC filings for more than 35 years. We have to sadly say that the 10-Q that Goldman Sachs filed with the SEC on May 2, for the quarter ending March 31, 2022, shocks even our well-documented assessment of Wall Street as a crime syndicate. Goldman Sachs has listed pretty much everything the firm does as a target of an ongoing investigation, notwithstanding that the company and a subsidiary were criminally charged by the U.S. Department of Justice in the looting and bribery scandal known as 1MDB in October 2020, admitted to the charges, and had to pay over $2.9 billion. The good news is that Goldman Sachs’ Dark Pools are one of the areas it lists as being under a probe.

Dark Pools (also benignly called Alternative Trading Systems or ATS) are effectively unregulated stock exchanges being run by the same megabanks on Wall Street that blew up the U.S. financial system in 2008 and received the largest taxpayer bailout in U.S. history. The radical right in the U.S. Congress apparently believes that unbridled greed and outrageously reckless conduct that craters America’s economy deserves to be rewarded with less regulatory oversight, thus Dark Pools have not been shut down.

Not only are Goldman Sachs, JPMorgan, UBS, Morgan Stanley, Merrill Lynch, and numerous others, allowed to trade hundreds of New York Stock Exchange and Nasdaq listed stocks in their own Dark Pools, but they are also allowed to trade their own bank’s stock in their own Dark Pools. We have asked the SEC for years now how it is legal for a bank to trade its own stock – possibly making a two-sided market in that stock because some of these firms own more than one Dark Pool. We’ve yet to receive an answer. (Dare we hope that this is finally being seriously investigated by Gary Gensler’s SEC?)

The name of Goldman Sachs’ Dark Pool that trades in the U.S. is called Sigma X2. It used to be called simply Sigma X. According to a publicly-available document, Sigma X is now used by Goldman Sachs to designate the Dark Pools it operates in foreign jurisdictions, which include Europe, Japan, Hong Kong and Australia.

According to a “Frequently Asked Questions” document from Goldman Sachs, under the question “Is SIGMA X a dark pool that only matches trades anonymously, without information leakage? Or will information regarding my orders be conveyed to potential liquidity providers,” Goldman says this: “The matching process for SIGMA X is completely internal, and SIGMA X will not disseminate any pre-trade information to internal trading desks or external counterparties. Executed trades are publicly reported where required by applicable rules.”

In other words, this is an unlit market where pre-trade prices are not available to the public and trades are only reported after they have occurred in darkness, if they are reported at all.

How Goldman’s Dark Pool functions was written about in the Michael Lewis bestseller, Flash Boys, and the seminal work on Dark Pools by Wall Street Journal reporter Scott Patterson, Dark Pools: The Rise of the Machine Traders and the Rigging of the U.S. Stock Market.

Michael Lewis related the story in Flash Boys of how Rich Gates, the operator of a mutual fund, together with his colleagues devised a test to see if they entered an order into a Dark Pool they would get ripped off. Lewis writes as follows:

“Gates and his colleagues wound up making hundreds of such tests, with their own money, in several Wall Street dark pools. In the first half of 2010 there was only one Wall Street firm in whose dark pool the test came back positive: Goldman Sachs. In the Goldman dark pool, Sigma X, he got ripped off a bit more than half the time he ran the tests.”

Patterson writes in his book on Dark Pools that the U.S. stock market has degenerated into:

“pools within pools, all connected electronically, forming a single sloshing pool of dark electronic liquidity. By 2012, the amount of stock trading that took place in dark pools and internalizers was a whopping 40 percent of all trading volume – and it was growing every month…

“No one – no one – truly knew what was taking place inside the guts of this Frankenstein’s monster of a market.”

Clearly Patterson is an expert on Dark Pools; but for some reason the Wall Street Journal allows him to report on everything but Dark Pools.

In the early 1930s, following the stock market crash of 1929, the U.S. Senate Banking Committee issued subpoenas and conducted extensive investigations over multiple years into the trading structure and trading practices on Wall Street. The Senate investigations focused on the collusive dealings of “pools,” which have today been reincarnated as Dark Pools. The 1930s Senate investigation found the following:

“A pool, according to stock exchange officials, is an agreement between several people, usually more than three, to actively trade in a single security. The investigation has shown that the purpose of a pool generally is to raise the price of a security by concerted activity on the part of the pool members, and thereby to enable them to unload their holdings at a profit upon the public attracted by the activity or by information disseminated about the stock. Pool operations for such a purpose are incompatible with the maintenance of a free and uncontrolled market.”

The Senate Banking Committee of 1934 concluded as follows:

“The conclusion is inescapable that members of the organized exchanges who had a participation in or managed pools, while simultaneously acting as brokers for the general public, were representing irreconcilable interests and attempting to discharge conflicting functions. Yet the stock exchange authorities could perceive nothing unethical in this situation.”

As for the other areas in which Goldman Sachs is under a government investigation or named as a defendant in a lawsuit, the 10-Q filing offers this:

“[Goldman Sachs] Group Inc. and certain of its affiliates are subject to a number of other investigations and reviews by, and in some cases have received subpoenas and requests for documents and information from, various governmental and regulatory bodies and self-regulatory organizations and litigation and shareholder requests relating to various matters relating to the firm’s businesses and operations, including: “securities offering process and underwriting practices”; “firm’s investment management and financial advisory services”; “Research practices, including research independence and interactions between research analysts and other firm personnel, including investment banking personnel, as well as third parties”; “Transactions involving government-related financings and other matters, municipal securities, including wall- cross procedures and conflict of interest disclosure with respect to state and municipal clients, the trading and structuring of municipal derivative instruments in connection with municipal offerings, political contribution rules, municipal advisory services and the possible impact of credit default swap transactions on municipal issuers”; “The offering, auction, sales, trading and clearance of corporate and government securities, currencies, commodities and other financial products and related sales and other communications and activities, as well as the firm’s supervision and controls relating to such activities, including compliance with applicable short sale rules, algorithmic, high-frequency and quantitative trading, the firm’s U.S. alternative trading system (dark pool), futures trading, options trading, when-issued trading, transaction reporting, technology systems and controls, communications recordkeeping and recording, securities lending practices, prime brokerage activities, trading and clearance of credit derivative instruments and interest rate swaps, commodities activities and metals storage, private placement practices, allocations of and trading in securities, and trading activities and communications in connection with the establishment of benchmark rates, such as currency rates”; “Insider trading, the potential misuse and dissemination of material nonpublic information regarding corporate and governmental developments and the effectiveness of the firm’s insider trading controls and information barriers.”

The above is not a complete listing, just the highlights.

The involvement of Goldman Sachs in the implosion of the family office hedge fund, Archegos Capital Management, in March of last year has not gone away either. Goldman Sachs reports the following in its 10-Q:

“GS&Co. is among the underwriters named as defendants in a putative securities class action filed on August 13, 2021 in New York Supreme Court, County of New York, relating to ViacomCBS Inc.’s (ViacomCBS) March 2021 public offerings of $1.7 billion of common stock and $1.0 billion of preferred stock. In addition to the underwriters, the defendants include ViacomCBS and certain of its officers and directors. GS&Co. underwrote 646,154 shares of common stock representing an aggregate offering price of approximately $55 million and 323,077 shares of preferred stock representing an aggregate offering price of approximately $32 million. The complaint asserts claims under the federal securities laws and alleges that the offering documents contained material misstatements and omissions, including, among other things, that the offering documents failed to disclose that Archegos Capital Management (Archegos) had substantial exposure to ViacomCBS, including through total return swaps to which certain of the underwriters, including GS&Co., were allegedly counterparties, and that such underwriters failed to disclose their exposure to Archegos. The complaint seeks rescission and compensatory damages in unspecified amounts. On November 5, 2021, the plaintiffs filed an amended complaint, and, on December 22, 2021, the defendants filed motions to dismiss the amended complaint. On January 4, 2022, the plaintiffs moved for class certification.

“[Goldman Sachs] Group Inc. is also a defendant in putative securities class actions filed beginning in October 2021 and consolidated in the U.S. District Court for the Southern District of New York. The complaints allege that Group Inc., along with another financial institution, sold shares in Baidu Inc. (Baidu), Discovery Inc. (Discovery), GSX Techedu Inc. (Gaotu), iQIYI Inc. (iQIYI), Tencent Music Entertainment Group (Tencent), ViacomCBS, and Vipshop Holdings Ltd. (Vipshop) based on material nonpublic information regarding the liquidation of Archegos’ position in Baidu, Discovery, Gaotu, iQIYI, Tencent, ViacomCBS and Vipshop, respectively. The complaints generally assert violations of Sections 10(b), 20A and 20(a) of the Exchange Act and seek unspecified damages.

“On January 24, 2022, the firm received a demand from an alleged shareholder under Section 220 of the Delaware General Corporation Law for books and records relating to, among other things, the firm’s involvement with Archegos and the firm’s controls with respect to insider trading.”

For more on the Archegos matter, see our recent report: Justice Department and SEC Portray Serially-Charged Banks on Wall Street as Hapless Victims of Archegos Fraud. Nobody’s Buying It.

-END-

LAWRIE WILLIAMS: Less downbeat FOMC boosts gold and equities but latter could be false dawn

Tuesday and Wednesday’s U.S. Federal Open Market Committee (FOMC) meeting deliberations ended with a statement from Fed chair Jerome Powell which somehow eased the worst market fears as to the likely future effects of Fed policies to ease the current severe inflationary trends afflicting the U.S. economy and equity markets. We do not think the content of the post FOMC press release and Powell’s subsequent statement should have done so, and that the ensuing equity market recoveries as a result are in any way sustainable.

These statements were indeed taken as less hawkish in that they appeared to rule out 75 basis point rate increase impositions at future FOMC meetings, which some had been considering as likely after increasingly disappointing inflation news. Indeed Powell had hinted that inflation control was likely to be challenging and that further 50 basis point rate increases were thus likely to be imposed at at least the next couple of FOMC meetings. Only a few days ago such news would have depressed the equity markets, but because some market analysts had been perhaps expecting worse, the markets breathed a sigh of relief and regained most of their losses sustained over the previous few days. We doubt that this recovery can be retained and anticipate they will come back again sharply over the next few days as reality strikes and the new CPI and PPI figures are released next week.

As for gold. initial reaction took the price back up over $1,900 again, albeit briefly, but it managed to remain in the high $1,890s in European trade and was testing $1,900 again at the time of writing. European equity markets were following their U.S. counterparts upwards, a trend not followed by Asian stocks which were rather more circumspect in their reactions to the FOMC news and the big U.S. market gains, with both the Nikkei and Hang Seng indexes falling back, although neither substantially. Early US equity market reaction was to see the Dow down quite sharply – we think Wednesday’s sharp gains were an over-reaction and something of a miscalculation of what the real impact of the Fed moves were likely to mean in the markets,

We had assumed that the post FOMC markets would steady with gold perhsps running a little higher, as has proved to be the case, but equities probably falling back for which the reverse has occurred so far, but with even a 50 basis point interest rate rise probably doing little, or nothing, to arrest the ongoing rise in inflation, leading to more and more of the same medicine being applied through the remainder of the year, portents for equities going forwards do not look good. Investors have become used to mostly positive markets, but with inflation cutting into disposable incomes, some kind of economic turndown looks to be inevitable to this observer, with the only likely beneficiary likely to be traditional safe havens like gold in an attempt to protect one’s wealth against the ever declining purchasing power of one’s domestic currency.

05 May 2022

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material and a must read. It is really good

(Alasdair Macleod/GATA)

Alasdair Macleod: Financial war takes a nasty turn

Submitted by admin on Thu, 2022-05-05 11:31Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, May 5, 2022

The chasm between Eurasia and the Western defence groupings (NATO, Five Eyes, AUKUS, et al.) is widening rapidly. While media commentary focuses on the visible side of the conflict in Ukraine, the economic and financial aspects are what really matter.

There is an increasing inevitability about it all. China has been riding the inflationist Western tiger for 40 years and now that it sees the dollar’s debasement accelerating wonders how to get off.

Russia perhaps is more advanced in its plans to do without dollars and other Western currencies, hastened by sanctions. Meanwhile, the West is increasingly vulnerable with no apparent alternative to the dollar’s hegemony.

By imposing sanctions on Russia, the West has effectively lined up its geopolitical opponents into a common cause against an American dollar-dominated faction. Russia happens to be the largest exporter of energy, commodities, and raw materials. And China is the world’s supplier of semi-manufactured and consumer goods. The consequences of the West’s sanctions ignore this vital point.

In this article we look at the current state of the world’s financial system and assess where it is headed. It summarises the condition of each of the major actors: the West, China, and Russia, and the increasing urgency for the latter two powers to distance themselves from the West’s impending currency, banking, and financial asset crisis.

We can begin to see how the financial war will play out. …

… For the remainder of the analysis:

end

Finally mining and movie mogul Giustra earns his tin foil hat by claiming now he sees that USA/European banks undergoing manipulation in the gold and silver precious metals markets

(Giustra/Kitco/GATA)

Zillionaire Giustra earns his tinfoil hat and brings Kitco’s Makori along for the ride

Submitted by admin on Thu, 2022-05-05 13:55Section: Daily Dispatches

2p ET Thursday, May 5, 2022

Dear Friend of GATA and Gold:

Give that man a tinfoil hat!

Mining and movie entrepreneur and zillionaire Frank Giustra has gone full “conspiracy nut” in an interview today with Michelle Makori of Kitco News, surpassing his previous cautious assertions that the gold price is “managed” by central banks and saying now that the price is “outright manipulated.”

Giustra tells Makori that “you’re never going to find a smoking gun on this.” But, if so, that’s only because neither he nor Makori will ever visit GATA’s documentation summary here:

After all, the summary just has too much documentation to sort through unless one aims to be sincere.

But better 20 years late than never, so let’s take what we can get, especially since Giustra’s enlistment in the tinfoil hat brigade has brought along Kitco, which long has striven to avoid mention of gold market manipulation and especially to avoid interviewing GATA Chairman Bill Murphy, despite GATA’s many requests. Telling gold investors the truth — that is, as Jim Rickards said in CNBC many years ago, “When you own gold you’re fighting every central bank in the world” — may be bad for the gold business until it decides to stand up for itself.

Kitco’s interview with Giustra is headlined “Gold Price Is Manipulated by the Fed, Suspects Mining Tycoon Frank Giustra, But Suppression Can’t Last Forever” and it can be found here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //FERTILIZER

END.

end

COMMODITIES IN GENERAL//

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6710

OFFSHORE YUAN: 6.67085

HANG SANG CLOSED DOWN 791.44 OR 3.81%

2. Nikkei closed UP 185.03 OR .68%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 103.44/Euro RISES TO 1.0575

3b Japan 10 YR bond yield: RISES TO. +.195/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 130.40/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +1.065%/Italian 10 Yr bond yield RISES to 3.17% /SPAIN 10 YR BOND YIELD RISES TO 2.16%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.11: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3i Greek 10 year bond yield RISES TO 3.51

3j Gold at $1882.75 silver at: 22.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 2/25 roubles/dollar; ROUBLE AT 69.24

3m oil into the 110 dollar handle for WTI and 113 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 130.40 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9847– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0415well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.089 UP 2 BASIS PTS

USA 30 YR BOND YIELD: 3.174 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 14.95

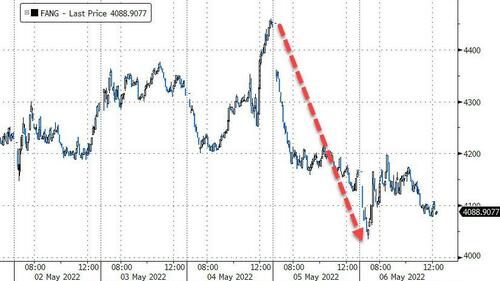

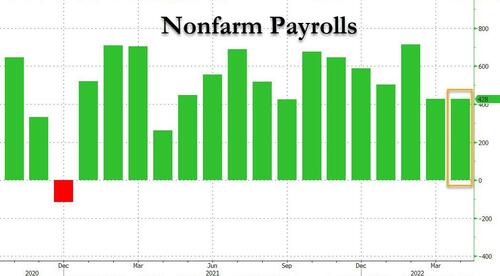

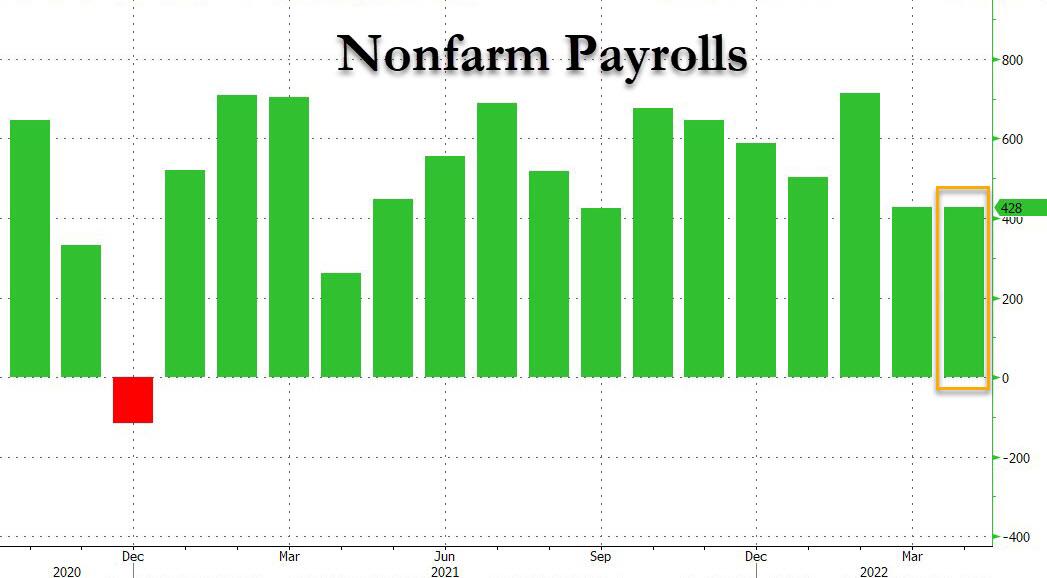

Futures Slide Ahead Of Payrolls And Six Fed Speakers

FRIDAY, MAY 06, 2022 – 08:01 AM

The market crash will continue until Biden’s approval rating improves.

US futures extended their slide on Friday, signaling continuation of a drop in tech stocks following the Nasdaq 100’s biggest selloff since September 2020, ahead of today’s jobs report (which bulls pray comes in at around minus 1 million to put a premature end to Powell’s market-crashing tightening) and ahead of no less than six Fed speakers, as investors grappled with fears of a stagflationary recession against tightening monetary policy. Nasdaq 100 futures were 0.9% lower and S&P 500 futures traded at session lows, down 0.7% as of 7:30 a.m. EDT as panicked traders sell first and don’t even bother to ask questions. Ten-year U.S. Treasury yield continued to climb, trading at 3.1%, near the highest since November 2018. The dollar continued its relentless ascent, while cryptos continued to tumble. Perhaps even more concerning to traders than the jobs report is that six Fed speakers are lined up including Williams, Kashkari, Bostic, Bullard, Waller and Daly.

Stocks plunged on Thursday, completely erasing their gains from the prior session amid a broad-based selloff in risk assets. The S&P 500 Index sank 3.6% on Thursday, while the tech-heavy Nasdaq 100 Index plunged 5.1%, its biggest decline since September 2020. Still, some investors say that concerns may be overblown. “Looking back at just the past two days, it’s not really all that dramatic,” said Mattias Isakson, head of strategy and allocation at Swedbank, adding that indexes were roughly back to where they were compared to before the Fed press conference. “The overall market outlook hasn’t changed at all: interest rates and inflation worries will continue to create volatility in the short term,” Isakson said.

On Friday, shares of US-listed Chinese firms extended losses in premarket trading amid growing concerns about the country’s economic growth prospects and continued weakness in tech shares. Peloton shares dropped premarket after the company was said to be considering selling a stake of around 20%. Meanwhile, DoorDash jumped after earnings and Tesla gained after planning to boost car production at its Shanghai plant. Here are some more details on the biggest premarket movers today:

- Tesla (TSLA US) shares gain as much as 1.1% in U.S. premarket trading, leaving them set to bounce back following Thursday’s losses, after the electric-vehicle maker was said to be making plans to boost car production at its Shanghai plant as soon as mid-May.

- Shares of U.S.-listed Chinese firms extend losses in premarket trading amid growing concerns about the country’s economic growth prospects and continued weakness in tech shares. Alibaba (BABA US) -1.9%, Baidu (BIDU US) -2.4%, JD.com (JD US) -2%.

- Peloton (PTON US) shares fall as much as 1.7% in U.S. premarket trading after the maker of indoor exercise bikes was said to be considering selling a stake of around 20% as part of a turnaround.

- Cloudflare (NET US) shares drop 9.3% in U.S. premarket despite a boosted full-year revenue guidance; analysts say the outlook implies a significant deceleration for lead metrics. At least 3 analysts cut their price targets on the stock.

- Digital Brands Group (DBGI US) shares decline 50% in U.S. premarket trading after pricing an offering of 37.4m shares at $0.25 apiece, representing a discount of ~50% to Thursday’s close.

- DoorDash (DASH US) shares jump as much as 6.9% in U.S. premarket trading, with analysts positive on the food-delivery firm’s first-quarter update given tough pandemic comparisons and a difficult macroeconomic environment, though some trimmed price targets amid higher investments.

- Block Inc. (SQ US) shares rise 7% after 1Q results, with analysts upbeat on demand for the company’s Square and Cash App payment services as the fintech company displays resilience amid a challenging market.

- Live Nation (LYV US) shares gained 4% in postmarket trading. Its leading indicators like ticket sales, show counts and committed sponsorships remain robust, according to Guggenheim analyst Curry Baker.

- Opendoor (OPEN US) jumps as much as 16% in U.S. premarket trading after the real estate platform provider forecast revenue for the second quarter that beat the average analyst estimate.

- Zillow (ZG US) shares decline 6.7% in U.S. premarket trading after underwhelming guidance disappoints analysts, who believe that rising mortgage rates will cool the U.S. housing market. At least 3 analysts cut their price targets with one saying he doubts the real-estate technology firm’s ability to achieve its 2025 targets.

According to BofA, the global market selloff has further to run, as every asset class saw outflows in the week prior to the Federal Reserve’s meeting this week, with real estate posting its biggest outflow on record – $2.2 billion – and investors piling into safe havens like Treasuries although one wouldn’t know it judging by where yields are trading.

“The Fed is attempting to land a B52 bomber on a piece of string and most risk markets still have their fingers in their ears and their hands over their eyes,” said James Athey, a London-based investment director at abrdn. “Hope is not a strategy.”

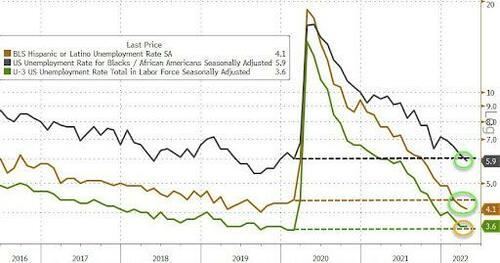

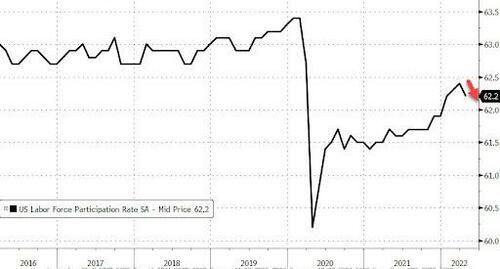

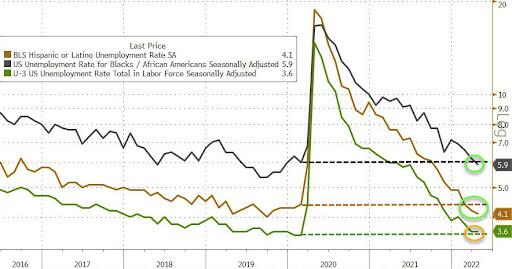

The next key event for markets is Friday’s U.S. jobs report (full preview here), which will be closely watched for signs that rising wage costs are adding to the inflationary pressures rattling investors. Estimates by economists are looking for payrolls to expand by 380,000 in April, and the unemployment rate to fall to 3.5%, although whisper numbers are lower.

A print higher than 500,000 in non-farm payrolls will provoke U.S. dollar buying as equities and bonds sell-off, while less than 300,000 should see the reverse, says Jeffrey Halley at OANDA. “A sharp divergence, up or down, from the median forecast, should produce a very binary outcome,” he says. “It’s that sort of market.”

“Any upward pressure on the average hourly earnings could lead to another spike of U.S. yields and therefore add negative pressure on equities and especially tech stocks,” said Christophe Barraud, chief economist at Market Securities LLP in Paris.

In Europe, the Stoxx 600 Index followed the Wall Street rout and was set for its worst weekly drop in two months, with consumer, retail and travel and leisure among the biggest decliners. FTSE MIB posts the smallest decline. Retailers, consumer products and media are the worst performing sectors. Traders will be watching job data, while Cigna, Dish, NRG Energy and Under Armour are among companies reporting earnings. Here are the biggest European movers today:

- Grifols rose as much as 9.3%, to the highest since November, after the Spanish maker of pharmaceutical products derived from blood plasma gave a business update that Citi said supports its buy rating on the stock.

- Leonardo rose as much as 4.4% after reporting earnings. Deutsche Bank said 1Q numbers were solid, while Intesa Sanpaolo said the company delivered “a sound start” to 2022.

- S4 Capital shares gained as much as 9.9% after the digital advertising agency released delayed FY results that showed limited audit adjustments. Revenue was ahead of analyst expectations.

- SKF shares advanced, breaking a seven-session declining streak, after Danske Bank upgraded the shares to buy, saying they “could generate good return in the coming 3-12 months.”

- Krones shares surged as much as 11%, the most since October 2019, after the machinery company reported 1Q Ebitda that beat estimate, with analysts noting scope for upgrades.

- Ambu shares dropped as much as 17% after the Danish health care equipment firm cut its outlook. Handelsbanken says the new guidance may lead to a 30% drop in FY Ebit estimates.

- Adidas shares fell more than 6% after the German sportswear maker cut its margin outlook for the year. Analysts noted the impact of lockdowns in China. Peer Puma also fell.

- IAG fell as much as 12%, the most intraday since November. The British Airways parent posted a 1Q operating loss that Citi analysts said was worse than consensus and their own expectations.

- JCDecaux shares slumped as much as 12% after its 2Q organic revenue growth target of more than 15% fell short of analyst expectations amid lockdowns in China.

Earlier in the session, Asian stocks were on track for five straight days of losses, as traders questioned whether the Federal Reserve’s interest rate hike was enough to tackle inflation and Chinese leaders warned against doubting their Covid-Zero stance. The MSCI Asia Pacific Index declined by as much as 1.8%, poised for its longest losing streak since January and lowest closing level since July 2020. The broad-based selloff followed steep declines in U.S. shares overnight, with benchmarks in Australia, Taiwan and Vietnam each declining more than 1.7%.

“Volatility comes from doubts whether the 50 basis-point hike can be enough to curb inflation,” said Lee Han-Young, chief fund manager at DS Asset Management, a Seoul-based hedge fund. For market volatility to ease, CPI or other inflation-related data needs to peak or slow down, he said. “Before that, volatility seems inevitable.” Stock indexes in Hong Kong and mainland China were the worst performers in the region after the Politburo’s supreme Standing Committee reaffirmed its support for a lockdown-dependent approach on Thursday. Still, declines in Asia were less than the rout in U.S. shares, with generally smaller-sized market reactions to the Fed’s policy statement Wednesday. China’s economic slowdown and regulation of its tech industry are also playing on investors’ minds, with the Hang Seng Tech Index sliding amid a lack of concrete steps to support the industry. Overall, tech and financial stocks were among the biggest drags on the MSCI Asia Pacific Index. The measure is on track to fall about 2.6% this week, the largest weekly slide since mid-March. Bucking the regional trend, Japanese equities rose after a three-day holiday.

India’s benchmark stocks index registered its worst weekly decline in more than five months as growing concerns over higher borrowing costs to curb inflation dented risk sentiment. The S&P BSE Sensex declined 1.6% to 54,835.58 in Mumbai on Friday, taking its loss this week to 3.9%, the biggest five-day drop since the period ended Nov. 26. The NSE Nifty 50 Index slipped 1.6% to 16,411.25. HDFC Bank Ltd. fell 2.6% and was the biggest drag on the Sensex, which had 24 of the 30 member stocks trading lower. All but two of 19 sectoral sub-indexes compiled by BSE Ltd. fell, led by a gauge of realty companies. The Reserve Bank of India raised its policy rate by 40 basis points in an out-of-cycle move this week after keeping it at a record-low level of 4% for the past two years. “This suggests that the scales of growth versus inflation is tilted towards inflation and can be leading indicator of further rate hikes in FY23,” Shibani Kurian, head of equity research at Kotak Mahindra Asset Management Co. wrote in a note. She expects market participants to focus on earnings and commentary on demand and margins from companies. The U.S. Federal Reserve and Bank of England also raised rates to tackle rising inflation. In earnings, of the 24 Nifty 50 firms that have announced results so far, 17 either met or exceeded analysts’ estimates, while seven missed forecasts. Reliance Industries Ltd., the nation’s largest company, is scheduled to announce its results Friday.

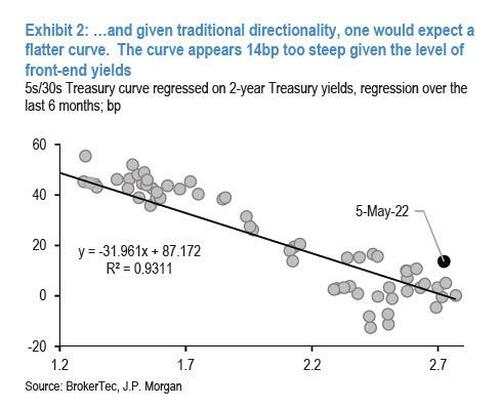

In rates, Treasuries extended Thursday’s bear-steepening move, with yields cheaper by 2bp to 4bp across the curve, amid bigger losses for German bonds after ECB’s Villeroy said above-zero rates are “reasonable” by year-end, and that there are signs inflation expectations are less anchored. US 10-year yields around 3.09%, cheaper by ~3bp on the day with 2s10s steeper by ~2.5bp; front-end yields outperform, higher by ~2bp at around 2.72%. Dollar issuance slate empty so far and expected to be muted because of jobs report; four names priced $7.6b Thursday taking weekly total above $16b, shy of $20b-$25b expected range. Peripheral spreads eventually tighten slightly to core after 10y BTP/Bund briefly widening through 200bps

In FX, a gauge of the dollar’s strength was little changed as traders awaited a U.S. jobs report on Friday. Bloomberg Dollar Spot Index gained 0.2% as traders awaited the U.S. jobs report due on Friday. Ten-year Treasury yields rose 2 basis points to 3.05%. The yen underperformed most G-10 currencies as Japan’s markets reopened following a three-day holiday. Leveraged funds initiated long dollar-yen positions heading into U.S. payrolls data, according to an Asia-based FX trader

Long gamma exposure in the major currencies meets a fresh round of demand following the Bank of England’s policy decision, which is contributing to continued erratic moves in the options space into the U.S. report. Real money and hedge funds both net USD buyers, according to three Europe-based traders, with demand for USD calls in the likes of EUR, AUD and MXN.

In commodities, WTI trades within Thursday’s range, adding 1.6% to trade near $110. Spot gold rises roughly $5 to trade above $1,880/oz. Most base metals trade in the red. Bitcoin continues to slide, and was last trading below $36,000, after cracking to key support levels yesterday.

Looking at the day ahead now, the main highlight will be the aforementioned US jobs report for April. Other data releases include German industrial production and Italian retail sales for March. From central banks, we’ll hear from the ECB’s Villeroy, Nagel, Elderson and Rehn, the Fed’s Williams, Kashkari and Bostic, and the BoE’s Pill and Tenreyro.

Market Snapshot

- S&P 500 futures little changed at 4,140.00

- STOXX Europe 600 down 0.9% to 434.26

- MXAP down 1.6% to 164.46

- MXAPJ down 2.7% to 538.32

- Nikkei up 0.7% to 27,003.56

- Topix up 0.9% to 1,915.91

- Hang Seng Index down 3.8% to 20,001.96

- Shanghai Composite down 2.2% to 3,001.56

- Sensex down 1.4% to 54,941.03

- Australia S&P/ASX 200 down 2.2% to 7,205.64

- Kospi down 1.2% to 2,644.51

- German 10Y yield little changed at 1.07%

- Euro up 0.3% to $1.0570

- Brent Futures up 1.3% to $112.39/bbl

- Gold spot up 0.1% to $1,879.09

- U.S. Dollar Index down 0.31% to 103.43

Top Overnight News from Bloomberg

- European Central Bank Governing Council member Francois Villeroy de Galhau said interest rates may be raised back above zero this year if the euro-zone economy doesn’t suffer another setback.

- The European Union has proposed a revision to its Russia oil sanctions ban that would give Hungary and Slovakia an extra year, until the end of 2024, to comply, according to people familiar with the matter.

- China has ordered central government agencies and state-backed corporations to replace foreign- branded personal computers with domestic alternatives within two years, marking one of Beijing’s most aggressive efforts so far to eradicate key overseas technology from within its most sensitive organs.

- Germany is ready to support eastern European nations in their efforts to wean themselves off Russian energy to secure broader support for sanctions targeting the country’s oil and gas sector, Chancellor Olaf Scholz said Thursday

- The cost of living in Tokyo rose at the fastest pace in almost three decades in April, as the impact of soaring energy prices became clearer, an outcome that complicates the Bank of Japan’s messaging on inflation and the need for continued stimulus

- China’s top leaders warned against questioning Xi Jinping’s Covid Zero strategy, as pressure builds to relax virus curbs and protect the economic growth that has long been a source of Communist Party strength

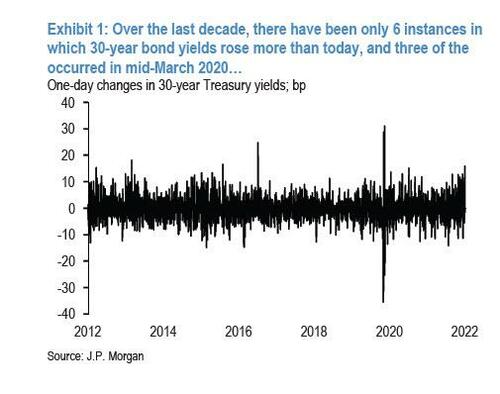

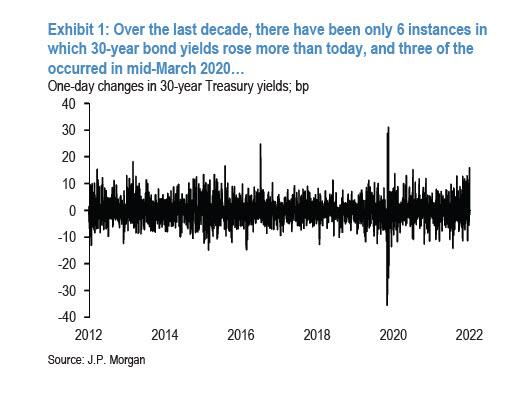

- An escalating selloff in long-end Treasuries pushed yields to fresh multi-year highs Thursday, with the benchmark 10-year rate closing above 3% for the first time since 2018 as concern over inflation rattled the bond market

- Having plunged by the most on record in offshore trade last month, China’s yuan is now facing the threat of selling pressure from the nation’s companies

- The Federal Reserve will need to raise short-term interest rates to at least 3.5% to bring surging inflation under control, former Vice Chairman Richard Clarida said

- South Korea needs to act preemptively on risk factors while monitoring situations in the economy and markets, as there are concerns local financial and FX markets will react sensitively according to various factors, Vice Finance Minister Lee Eog-weon says

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly lower amid spillover selling from the sharp declines on Wall Street. ASX 200 was heavily pressured in which the losses in tech led the broad declines across all sectors. Nikkei 225 initially declined on return from the Golden Week holidays but then pared all its losses as currency weakness persisted with Japan also planning to introduce tax incentives, as well as ease border measures in June. Hang Seng and Shanghai Comp conformed to the downbeat mood with tech and property names dragging the Hong Kong benchmark lower, while China also remained steadfast in its “dynamic COVID clearance” policy.

Top Asian News

- Adidas Shares Drop Amid ‘Dialed-Down’ Outlook: Street Wrap

- JAL Sees Return to Profit as Japan Moves to Reopen Borders

- Food Prices Hold Near Record as Ukraine War Upends Global Trade

- Nine in 10 Central Banks Exploring Own Digital Money, BIS Says

European bourses are subdued across the board, Euro Stoxx 50 -1.1%, reacting to the late-doors pressure in Wall Street. Currently, US futures are modestly softer but relatively tentative overall going into the NFP release and subsequent Fed speak. US regulatory officials have arrived in China for “late-stage” audit deal talks, according to Reuters sources. China’s auto sales in April are estimated to have plunged 48.1% y-o-y to 1.17 million units, data from CAAM revealed. The recent Omicron outbreak has disrupted the auto sector, in particular in the Yangtze River Delta region, according to Global Times.

Top European News

- EU Plan to Ban Russian Oil Means Windfall for Hungarian Refiner

- BNP Paribas Offers Up to EU400m Non-Dilutive Convertible Bonds

- ECB’s Villeroy Says Above-Zero Rates ‘Reasonable’ This Year

- Sorrell Pledges Changes After S4’s ‘Embarassing’ Results Lag

In FX

- ECB officials ramp up hawkish rhetoric to boost Euro; EUR/USD makes round trip to high 1.0580 area from sub-1.0500.

- Pound continues to flounder as UK election results spell trouble for already under pressure PM Johnson and Tory Party, Cable under 1.2300 at one stage and EUR/GBP cross over 0.8550.

- Buck reverses all and more post-Fed losses pre-payrolls before Euro rebound knocks DXY back below 104.000, index down to new 103.340 low vs 104.070 peak.

- Aussie slumps despite hawkish RBA SOMP, Yen weak regardless of firmer than forecast Tokyo inflation data and return of Japanese markets from Golden Week; AUD/USD under 0.7100 and USD/JPY over 130.00.

- Loonie cushioned by strong crude prices ahead of Canadian LFS, USD/CAD within 1.2814-67 range and close to 1.29bln option expiries between 1.2835-40.

- Swedish Krona rangy after Riksbank minutes highlighting divergent views; EUR/SEK straddling 10.5000.

Fixed Income

- EZ debt downed by latest hawkish ECB guidance, Bunds below 152.00 and periphery underperforming.

- Gilts hold up better on the 118-00 handle awaiting BoE commentary after super Thursday.

- US Treasuries dragged down by Eurozone bonds to an extent, as 10 year T-note pivots 118-00 ahead of NFP.

Commodities

- WTI and Brent are bid in an exacerbation of APAC price action although, specific bullish-drivers have been somewhat sparse.

- Much of the focus has been on the potential EU Russian oil import embargo, particularly Hungary’s ongoing opposition and the EU’s attempts to appease them.

- Brazilian President Bolsonaro said a fresh hike in fuel prices by Petrobras could bankrupt Brazil and urged Petrobras not to increase fuel prices again, according to Reuters.

- PetroChina (0857 HK) says they have no plans to buy discounted Russian oil or gas, according to an executive.

- China is to sell 341k tonnes of imported soybeans from state reserve on May 13, according to the trade centre.

- Spot gold is bid but has failed to derive much traction above the 100- and 10-DMAs at USD 1883.08/oz and USD 1885.1/oz respectively.

Central Banks

- ECB’s Villeroy says too weak EUR would go against ECB inflation target; inflation is not only higher but broader; core inflation is firmly above target. Case for APP beyond June is not obvious. Adds, it is possible to raise rates into positive territory (i.e. above zero) by year-end.

- ECB’s Nagel says current inflation too high, confident it can get back to 2% target in the medium-term; adds, window to act is closing. Is optimistic re. a 2022 move. Does not buy the argument that policy should hold back because of the economy right now, via FAZ.

- ECB’s Holzmann said the ECB is planning to raise rates which they will discuss and probably do at the June meeting, while he added that rates will rise this year, by how much and when, will be discussed intensively in June, according to Reuters.