May 10, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

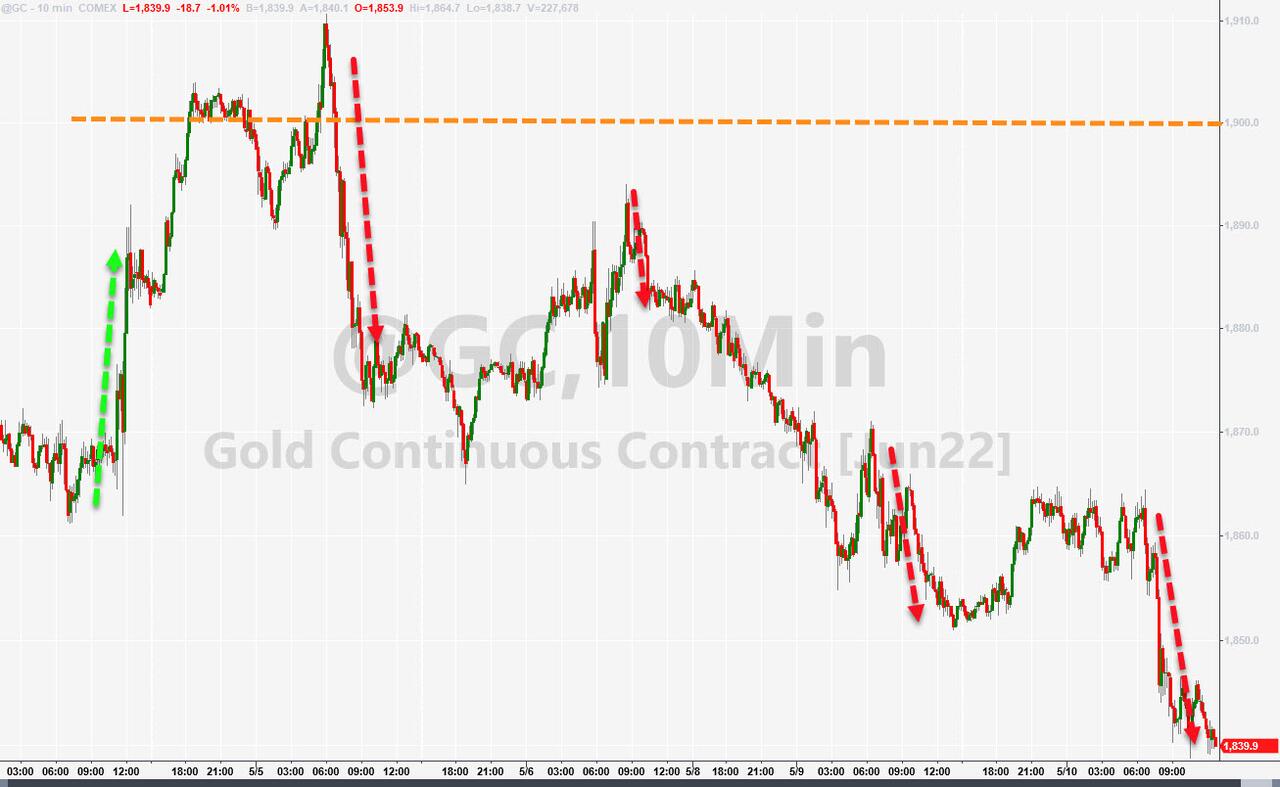

GOLD; $1842.40 down $16.90

SILVER: $21.48 DOWN $.40

ACCESS MARKET: GOLD $1839.30

SILVER: $21.28

Bitcoin morning price: $31,627 UP 781

Bitcoin: afternoon price: $31.424 UP 578

Platinum price: closing UP $4.40 to $972.90

Palladium price; closing UP $28.95 at $2076.95

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices 0/0

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 0 NOTICE(S) FOR 0 OZ (0.0 TONNES)

total notices so far: 1912 contracts for 191,200. oz (5.9471 tonnes)

SILVER NOTICES:

242 NOTICE(S) FILED 1,210,000 OZ/

total number of notices filed so far this month 3862 : for 19,310,000 oz

END

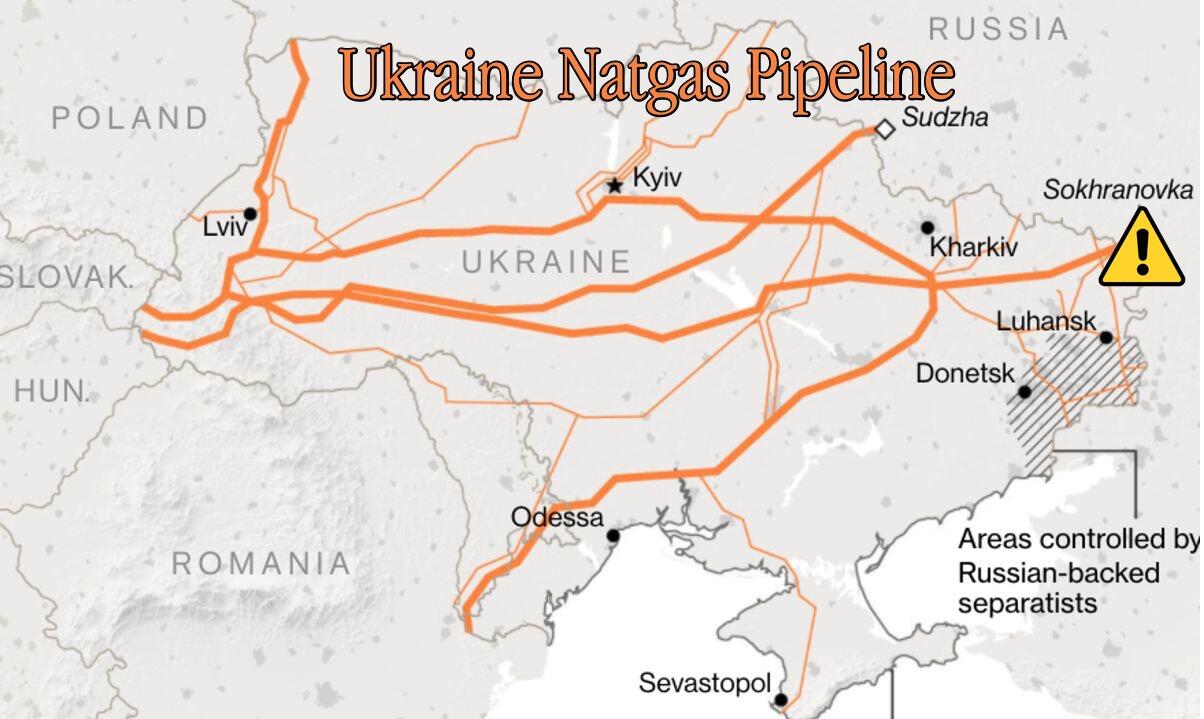

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $16.90

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.10 TONNES FROM THE GLD

INVENTORY RESTS AT 1075.90 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 40 CENTS

CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF .9300 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.977 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 560 CONTRACTS TO 141,747 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.50 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.50) BUT WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A VERY STRONG GAIN OF 2187 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ E.F.P JUMP TO LONDON //NEW STANDING 28.125 MILLION OZ/ // V) GOOD SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : 20

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 6 days, total 8768, contracts: 43.840 million oz OR 7.306 MILLION OZ PER DAY. (1461CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 43.840 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 43.830 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 560 DESPITE OUR STRONG $0.50 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1627 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 5,000 OZ E.F.P JUMP TO LONDON//NEW STANDING 28.125 MILLION OZ// .. WE HAD A VERY STRONG SIZED GAIN OF 2187 OI CONTRACTS ON THE TWO EXCHANGES FOR 10.935 MILLION OZ DESPITE THE STRONG LOSS IN PRICE.

WE HAD 242 NOTICE FILED TODAY FOR 1,210,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1531 CONTRACTS TO 553,131 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –4121 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR STRONG LOSS IN PRICE OF $24.05//COMEX GOLD TRADING/MONDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 28,900 OZ//NEW STANDING 9.1259 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $24.05 WITH RESPECT TO FRIDAY’S TRADING????

WE HAD A FAIR SIZED GAIN OF 3116 OI CONTRACTS (9.69 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4687 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 553,131.

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3116, WITH 1531 CONTRACTS DECREASED AT THE COMEX AND 4687 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3116 CONTRACTS OR 9.69 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4687) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1531,): TOTAL GAIN IN THE TWO EXCHANGES 3116 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 28,900 OZ//NEW STANDING 9.1289 /// 3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OI. LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

20,935 CONTRACTS OR 2,093,500 OR 65.11 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 3489 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 65.11 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 65.11/3550 x 100% TONNES 1.83% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 65.11 TONNES INITIAL//SLIGHTLY INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 560 CONTRACT OI TO 141,747 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1627 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1627 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 560 CONTRACTS AND ADD TO THE 1627 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF2187 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.935 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.50 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 31.70 PTS OR 1.06% //Hang Sang CLOSED DOWN 368.27 PTS OR 1.84% /The Nikkei closed DOWN 152.24 OR 0.58% //Australia’s all ordinaires CLOSED DOWN 0.99% /Chinese yuan (ONSHORE) closed up 6,7245 /Oil DOWN TO 101.42 dollars per barrel for WTI and down TO 104.85 for Brent. Stocks in Europe OPENED ALL green // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7245 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7487: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 21531 CONTRACTS TO 553,131 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $24.05 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2187 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2187 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2187 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2187 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3116 CONTRACTS IN THAT 4687 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1531 CONTRACTS..AND THIS LOSS OCCURRED WITH OUR LOSS IN PRICE OF GOLD $24.05.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (9.1259),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 9.1259 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $24.05) BUT WERE UNSUCCESSFUL IN FLEECING ANY LONGS// AS WE HAVE REGISTERED A FAIR SIZED GAIN OF 9.67 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (9.1259 TONNES)…

WE HAD 4121 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 3116 CONTRACTS OR 311,600 OZ OR 9.69 TONNES

Estimated gold volume today: 335,792/// good

Confirmed volume yesterday:295,347 contracts good

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 10

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 5893.20 oz Manfra Brinks |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 0 notice(s)0 OZ 0 TONNES |

| No of oz to be served (notices) | 1022 contracts 102,200 oz3.1788 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1912 notices 191,200 OZ 5.974 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposits

2 customer withdrawals:

i) Out of Brinks: 200.02 oz

ii) Out of Manfra 5693.19 oz

total withdrawal: 5893.20 oz

ADJUSTMENTS: 1 Manfra//dealer to customer 38,497.701 oz

2. Brinks: dealer to customer: 8862.591 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 1022 contracts having GAINED 286 contracts

We had 3 notices filed on Monday, so we gained 289 contracts or AN ADDITIONAL 28900 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 31,450 contracts down to 350,976 contracts

July has a gain of 4 OI to stand at 157

August has a gain of 28,567 contracts up to 147,144 contracts

We had 0 notice(s) filed today for 0 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1912) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 1022 CONTRACTS ) minus the number of notices served upon today 0 x 100 oz per contract equals 293,400 OZ OR 9.1259 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1912) x 100 oz+ (1022) OI for the front month minus the number of notices served upon today (0} x 100 oz} which equals 293,400 oz standing OR 9.1259 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 9.1259 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626.135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 36,037,873.935 OZ

TOTAL ELIGIBLE GOLD: 18,195,207.086 OZ

TOTAL OF ALL REGISTERED GOLD: 17,842,686.869 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,901,060.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 10

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,189,136.690 oz Brinks CNT Manfra JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 242CONTRACT(S) 1,210,000 OZ) |

| No of oz to be served (notices) | 1763 contracts (8,815,000 oz) |

| Total monthly oz silver served (contracts) | 3862 contracts 19,310,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

| month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

ii) Into CNT: 1,185,586.310 oz

total deposit: 1,185,586.310 oz

JPMorgan has a total silver weight: 177.173 million oz/336.933 million =52.56% of comex

Comex withdrawals: 3

i) Out of JPMorgan 587,800.400 oz

ii) Out of CNT:: 3973.400 oz

iii) Out of Manfra: 373,393.400 oz

iv) Out of Brinks 223,969.490 o

total withdrawal 1,189,136.690 oz

2 adjustments:

customer to dealer HSBC 1189,050.100 oz

dealer to customer /JPMorgan 726,199.500 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.530 MILLION OZ

TOTAL REG + ELIG. 336.933 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 2005 HAVING LOST 1 CONTRACT. WE HAD 0 NOTICES FILED ON MONDAY

SO WE LOST 1 CONTRACTS OR AN EFP JUMP OF 5,000

JUNE HAD A LOSS OF 90 TO STAND AT 1491

JULY HAD A GAIN OF 568 CONTRACTS UP TO 115,209 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 242 for 1,210,000 oz

Comex volumes: 69,984// est. volume today// good

Comex volume: confirmed yesterday: 85,841 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 3862 x 5,000 oz = 19,310,000 oz

to which we add the difference between the open interest for the front month of MAY(2005) and the number of notices served upon today 262 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 3862 (notices served so far) x 5000 oz + OI for front month of MAY (2005) – number of notices served upon today (262) x 5000 oz of silver standing for the MAY contract month equates 28,125,000 oz. .

We LOST 1 contract or AN ADDITIONAL 5,000 will NOT stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

GLD INVENTORY: 1075.90 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Lebanon has most of its gold in the Federal Bank of NY. Good luck to them if they want their physical bars back

(Ronan Manly/Bullionstar/GATA)

Ronan Manly: Lack of audits undermines Lebanon’s claim to be Middle East gold heavyweight

Submitted by admin on Mon, 2022-05-09 17:06Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Monday, May 9, 2022

With claimed gold reserves of 286 tonnes, Lebanon’s central bank — Banque du Liban — trumpets itself as being one of the Middle East’s largest sovereign gold holders. In fact, on a regional basis, only the claimed gold reserves of Saudi Arabia are larger.

Indeed, Banque du Liban governor Riad Salameh made this very claim as recently as April 8 to Egypt’s Middle East News Agency, saying that Lebanon has the second largest gold reserves across the Middle East and North Africa

However, what Salameh didn’t mention in his interview is that the portion of Lebanon’s gold claimed to be held in Beirut has not been audited for at least 30 years or even longer, nor did he clarify anything about the remainder of Lebanon’s gold which is said (by a media narrative) to be held in the of that veritable and ever trustworthy privately-owned institution, the Federal Reserve Bank of New York.

In fact, given the choice, it’s difficult to say which is worse — not being able to prove a claim that you have hundreds of tonnes of gold stored domestically, or not being able to prove if the other hundreds of tonnes of gold you claim were entrusted to the New York Fed are actually still there. But unfortunately for the citizens of Lebanon, the Lebanese central bank ticks both boxes.

But that’s just the beginning, because the situation on the ground is even murkier. …

… For the remainder of the analysis:

end

Chris Powell puts Bloomberg’s Dillian in his proper place. Dillian is confused by gold’s “strange behaviour”

Chris Powell/Dillian/Bloomberg

Gold’s ‘strange behavior’ explained once more for Bloomberg News

Submitted by admin on Mon, 2022-05-09 09:18Section: Daily Dispatches

Monday, May 9, 2022

Jared Dillian

c/o Bloomberg News, New York

Dear Mr. Dillian:

This is in response to your commentary today at Bloomberg about gold’s “strange behavior”:

https://www.bloomberg.com/opinion/articles/2022-05-09/personal-finance-gold-s-strange-behavior-shows-it-s-no-haven

You write that “lots of smart and very rational people believe that the price of gold is manipulated.” But it’s more than that. People believe this not so much because they are “smart and very rational” as because it has been extensively documented, as by my organization, the Gold Anti-Trust Action Committee Inc.GATA long has detailed the U.S. government and allied government policy of constantly intervening, largely surreptitiously, against the monetary metal’s price through various mechanisms, primarily involving the futures markets and derivatives. An extensive summary of the price suppression and its objectives can be found here:

https://gata.org/node/20925

Mainstream financial news organizations, including Bloomberg, assist this policy by refusing to acknowledge and report the documentation and to question government agencies about the intervention, no matter how obvious the intervention becomes.

For example, please note that the U.S. Commodity Futures Trading Commission refuses to answer whether it has jurisdiction over manipulative futures trading undertaken by or at the behest of the U.S. government or whether such trading is authorized by the Gold Reserve Act of 1934 as amended since then. The CFTC has refused to answer this question not only for my organization but also for a member of Congress, U.S. Rep. Alex Mooney, R-West Virginia.

Refusing to answer it for you and Bloomberg, an international news agency, might be more of a problem.

Additionally, CME Group, operator of the major U.S. futures exchanges, maintains, in plain sight, a special mechanism for official but surreptitious manipulation of all its futures markets, its Central Bank Incentive Program.

I know that pursuing such matters might pose risks for market analysts like yourself. But it would be public service on behalf of free and transparent markets, limited and accountable government, and fairness among nations, as well as fairness to ordinary investors.

Of course I’d be glad to provide more information.

Thanks for your consideration.

With good wishes.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIESEL

end

COMMODITIES IN GENERAL//

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7245

OFFSHORE YUAN: 6.7487

HANG SANG CLOSED DOWN 368.27 PTS OR 1.84%

2. Nikkei closed DOWN 152.24 OR 0.58%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 103.84/Euro FALLS TO 1.0565

3b Japan 10 YR bond yield: RISES TO. +.245/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.95/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +1.044%/Italian 10 Yr bond yield FALLS to 3.06% /SPAIN 10 YR BOND YIELD FALLS TO 2.19%…

3i Greek 10 year bond yield FALLS TO 3.58

3j Gold at $1861.90 silver at: 21.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 roubles/dollar; ROUBLE AT 69.24

3m oil into the 101 dollar handle for WTI and 104 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.95 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9935– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0497well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

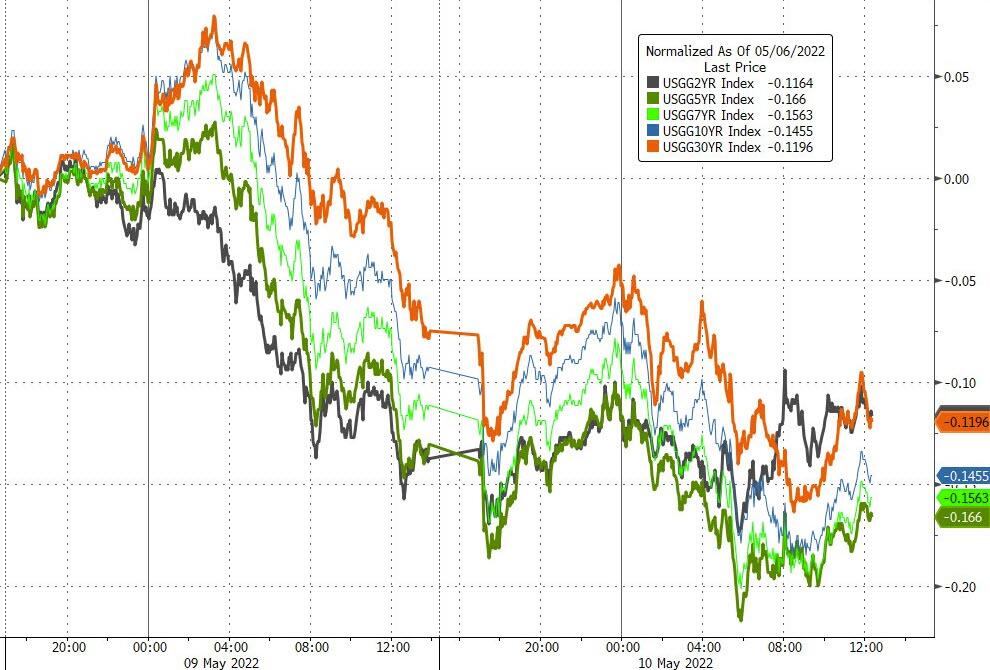

USA 10 YR BOND YIELD: 3.005 DOWN 7 BASIS PTS

USA 30 YR BOND YIELD: 3.140 DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.24

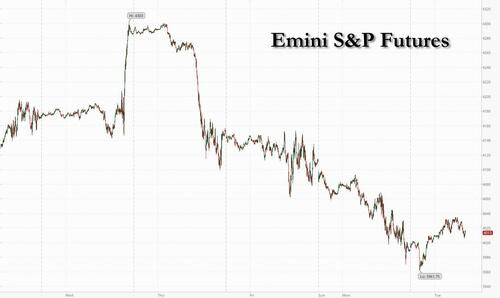

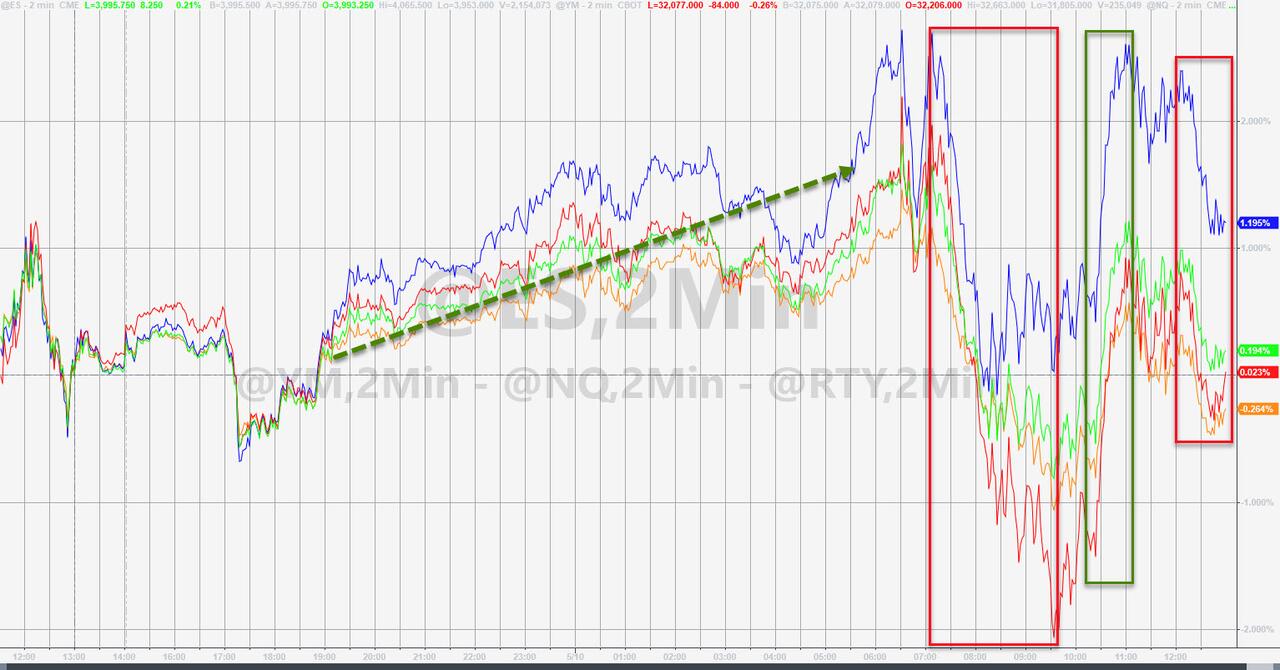

Futures Dead Cat Bounced As BTFDers Emerge On Turnaround Tuesday

TUESDAY, MAY 10, 2022 – 07:57 AM

The relentless rout that erased $3.4 trillion from the Nasdaq 100 in the past month paused on Turnaround Tuesday as battered tech valuations attracted scattered dip buyers, but nothing like the full-throttled BTFD buying parade observed in months gone by. Futures on the tech-heavy gauge advanced as much 1.4% as bargain hunters returned after the Nasdaq 100 slumped to the lowest since November 2020 on Monday, capping three days of major losses. S&P 500 futures were 0.7% higher to 4,016 after rising as much as 1.2% earlier but also after plunging to as low as 3,961.

After rising as high as 3.20% on Monday, 10-year Treasury yields dropped for a second day, sliding below 3.0% and providing further relief to technology shares. The dollar erased a loss and Treasuries edged higher, signaling the return of some haven demand amid nervousness over the path of Federal Reserve policy. European bonds rallied.

The Nasdaq’s 14-day relative-strength index (RSI) closed at 33 on Monday, getting closer to the level of 30, which to some analysts indicates a security is oversold and is poised to rise. Another sharp selloff “seems unlikely without an external trigger,” said Ulrich Urbahn, head of multi-asset strategy and research at Berenberg. “Nevertheless, as long as the problems persist, we do not expect a big recovery and have used the relief rally to move our equity exposure to neutral.”

Indeed, traders have been caught between stubbornly high inflation that erodes asset values and central-bank tightening that threatens to slow economic growth, or even push some nations into recession. Recent U.S. data suggesting the Federal Reserve will stay on an aggressive rate-hike path have sparked the latest bout of risk-off trades. Fresh outbreaks of Covid in China, and the nation’s stringent measures to control them, have worsened sentiment.

“For now, investors need to be prepared for continued volatility,” UBS Global Wealth CIO Solita Marcelli wrote in a note. She added “sentiment is bearish” but not capitulating.

In premarket trading, electric vehicle makers are up, with Tesla, Rivian and Lucid set to rebound after losing $188 billion in three days. AMC Entertainment is 6.4% higher after reporting better-than-expected quarterly results as hits like “Spider-Man: No Way Home” lured people back to movie theaters. Bank stocks edge higher in premarket trading amid a broader rebound for equity markets after Monday’s rout. S&P 500 futures are up about 0.8% this morning, while the U.S. 10-year yield retreats for a second day to sit at roughly 3%. In corporate news, BlackRock said it won’t support efforts by shareholders who try to micromanage companies on climate change. Meanwhile, Bitcoin rebounded back above $30,000 after briefly sinking below the closely watched level.

Here are some of the biggest U.S. movers today:

- Most large cap U.S. technology and internet stocks rose in premarket trading, on course to recoup some of the heavy losses they suffered in a steep selloff over the last three sessions. Apple (AAPL US) is up 1.2%, Microsoft (MSFT US) +1.2% and Meta (FB US) +2.8%.

- AMC Entertainment (AMC US) is up 3.8% in premarket trading after reporting better-than-expected quarterly results as hits like “Spider-Man: No Way Home” lured people back to movie theaters.

- Electric vehicle makers Tesla (TSLA US), Rivian (RIVN US) and Lucid (LCID US) are rebounding after losing $188 billion in three days of heavy selling in technology and growth stocks.

- Shockwave Medical (SWAV US) may move after it raised its revenue guidance for the full year, with analysts saying that the company’s performance was boosted by its coronary business. Shares rose 11% in extended trading on Monday.

- Upstart Holdings (UPST US) shares plunge 48% in premarket trading after the cloud-based artificial intelligence lending platform cut full- year revenue guidance on macro uncertainties. Piper Sandler cut the stock to neutral.

- Novavax (NVAX US) is down 21% premarket, with analysts saying that the biotech firm’s revenue for the first quarter missed expectations.

- Plug Power (PLUG US) shares are 5.6% lower premarket after the fuel cell company reported net revenue for the first quarter that missed the average analyst estimate, with KeyBanc noting pressure on margins and higher costs.

- Video game stocks may move after Sony’s earnings fell short of estimates amid supply constraints and component shortages. Watch shares in Activision Blizzard (ATVI US), Electronic Arts (EA US) and Take-Two Interactive (TTWO US).

U.S. stocks and particularly the Nasdaq 100 have been crushed this year (amid a tireless tirade from JPM’s Marko Kolanovic to buy each and every dip) as investors fret over recession risks from the Federal Reserve embarking on aggressive monetary tightening amid surging inflation. In the latest policy comments, Atlanta Fed President Raphael Bostic said he favors continuing to raise rates by half-point moves rather than anything larger. He said the odds for a 75-basis-point hike are low but added he’s taking nothing off the table.

European stocks trade well, with most cash indexes gaining over 1% to recover roughly half of Monday’s losses when the index slumped to its lowest level in two months. Euro Stoxx 50 rose as much as 1.75%, FTSE MIB outperforms slightly, FTSE 100 lags but still adds 1%. Construction, banks and autos lead broad-based Stoxx 600 sectoral gains. The Stoxx 600 energy sub-index edges lower, being one of the worst-performing sectors in a rising broader market for European stocks, as oil keeps falling. Shell declines as much as 1.5%, TotalEnergies SE -1.6%, Equinor -4.5%. Here are some of the biggest European movers today:

- Luxury stocks such as Kering (+0.5%) and Watches of Switzerland (+4.2%) rebounded after the declines of the previous sessions, with investors hopeful that the Covid-19 situation in the key market of China may be slightly improving.

- Hermes rises as much as +1.6%, LVMH +2.4%

- Airbus gains as much as 3.7% in Paris trading after being raised to buy from hold at Societe Generale, with the broker highlighting the planned production ramp-up of the “highly profitable” A320 family.

- Swedish Match rises as much as 28% after Philip Morris International said it’s in talks to buy the company. While a deal would make strategic sense, a counter-bid can’t be ruled out, analysts said.

- Centrica climbs as much as 6.5%, the most since Feb. 25, after the company guided adjusted earnings per share to be at the top end of the consensus range.

- Euroapi soars as much as 9.5% after the Sanofi spinoff is initiated with a buy recommendation and EU20 price target at Deutsche Bank, which sees “good value” and an attractive business.

- E-commerce stocks rise in Europe, with many outperforming the benchmark Stoxx 600 Index, buoyed by dip buyers returning to growth and technology shares that have been battered this year.

- Zalando up as much as 4.9%, Home24 +12%, Moonpig +3.6%

Earlier in the session, Asian stocks extended their decline to a seventh day as the specter of rapid credit tightening in the U.S. and protracted lockdowns in Chinese cities prompted some investors around the region to reduce holdings of riskier assets. The MSCI Asia Pacific Index fell as much as 2.1% to its lowest level since July 2020, weighed down tech shares after a three-day selloff in the Nasdaq 100. Hong Kong’s Hang Seng Index ended 1.8% lower as the market reopened after a holiday, though benchmarks in mainland China rebounded from early-trading lows on hopes for easier monetary conditions.

- MSCI Asia Pacific Index down 0.7%

- Japan’s Topix index down 0.9%; Nikkei 225 down 0.6%

- Hong Kong’s Hang Seng Index down 1.8%; Hang Seng China Enterprises down 2.2%; Shanghai Composite up 1.1%; CSI 300 up 1.1%

- Taiwan’s Taiex index up 0.1%

- South Korea’s Kospi index down 0.5%; Kospi 200 down 0.5%

- Australia’s S&P/ASX 200 down 1%; New Zealand’s S&P/NZX 50 down 1.3%

- India’s S&P BSE Sensex Index down 0.2%; NSE Nifty 50 down 0.4%

“There’s nowhere to escape so it’s pretty tough,” said Yuya Fukue, a trader at Rheos Capital Works. “Economic data appears to be deteriorating of late, though that has seemed to have gone little noticed while the markets were so focused on the Fed’s policy. It feels as if the game is changing.” Among Chinese tech giants, Alibaba tumbled 4.8% in Hong Kong, while Tencent dropped 2.3%. Regional declines were broad, with investors dumping even this year’s star energy shares as oil prices eased. Singapore’s Straits Times Index and Australia’s S&P/ASX 200 both dropped about 1%. The Philippine benchmark ended 0.6% lower, recovering after skidding more than 3%, after Ferdinand Marcos Jr. won a landslide victory in the country’s presidential election. Mainland Chinese shares closed higher after the People’s Bank of China repeated a pledge to proactively address mounting economic pressure and highlighted a drop in deposit rates, which could spur banks to lower the cost of borrowing for the first time in months. “The market was a bit oversold. In addition, PBOC is also mentioning a drop in deposit rates, raising expectations of more room for banks to increase lending,” said Aw Hsi Lien, a strategist at Tokai Tokyo Research.

India’s benchmark equity index slipped to a two-month low amid a weaker trend in Asia as surging oil prices and inflationary pressures weighed on investor sentiment. The S&P BSE Sensex fell 0.2% to 54,364.85 in Mumbai, after swinging between gains and losses several times during the session. The NSE Nifty 50 Index slipped 0.4% to 16,240.05. This is the third consecutive session of declines for the key indexes. Sixteen of the 19 sector sub-indexes compiled by BSE Ltd. dropped, led by metal stocks. Reliance Industries Ltd. slipped 1.7% to a seven-week low and was the biggest drag on the Sensex, which saw 18 out of its 30 member-stocks trading lower. In earnings, among the 27 Nifty 50 companies that have announced results so far, 10 have missed estimates while 17 either exceeded or met forecasts.

In FX, the Bloomberg Dollar Spot Index fell 0.1% after climbing to a two-year high on Monday, and the greenback was steady or weaker against all of its Group-of-10 peers. The euro consolidated and the region’s yields fell as Italian bonds led an advance. The pound was steady against both the dollar and euro while gilts outperformed peers. Domestic focus is on the Queen’s speech laying out the government’s agenda for the next parliamentary session and Brexit risks after reports the U.K. is preparing to scrap parts of the Northern Ireland protocol. U.K. retail sales are falling on an annual basis for the first time since the start of last year as the cost of living crisis crushes consumer confidence and puts the brakes on spending. Scandinavian currencies led gains among G-10 pairs after both currencies fell to the weakest level in around two years versus the dollar on Monday. The Australian and New Zealand dollars also bounced off two-year lows as stock indexes trimmed an intraday decline. Aussie’s gains were tempered as iron ore fell for a third day to bring the three-day slide to about 15%. The yen edged lower as Treasury yields recovered from a sharp overnight drop. Bonds pared earlier gain after the 10-year debt sale. Bank of Japan Executive Director Shinichi Uchida says that widening the central bank’s yield target band would be equivalent to a rate hike and wouldn’t be favorable for Japan’s economy

In rates, Treasuries rose in early U.S. trading with belly leading gains and the curve flattening modestly after Monday’s bull-steepening. Yields are richer by ~4bp across in belly of the curve, steepening 5s30s spread by ~3bp as long-end yields lag; 10-year trading just around 3%, richer by ~3bp on the day, trailing gilts by ~7bp in the sector. Core European rates outperform led by gilts while stocks and U.S. futures recover a portion of Monday’s steep losses. Bunds bull-flatten, while peripheral spreads tightened to Germany with short-dated BTPs outperforming. Treasury auction cycle begins with 3-year note sale, and several Fed speakers are slated. U.S. new-issue auction cycle consists of $45b 3-year note, followed by 10- and 30-year sales Wednesday and Thursday. WI 3-year yield ~2.800% is higher than auction stops since 2018 and ~6bp cheaper than last month’s, which stopped through by 0.1bp. Three-month dollar Libor +0.13bp at 1.39986%

In commodities, crude futures are choppy, WTI dips back into the red having stalled near $104. The outlook for crude remains clouded after the European Union softened some proposed sanctions on Russia. In cryptocurrencies, Bitcoin traded near $31,300 after earlier sliding below $30,000. Spot gold rises ~$9 near $1,863/oz. Much of the base metals complex trades poorly. LME copper outperforms, holding in the green but off best levels after a test of $9,400/MT.

Bitcoin reclaimed the $31K handle, but is yet to make a concerted move higher.

Looking ahead, we get the April NFIB Small Business Optimism print (93.2, Exp. 92.9), Chinese M2, Speeches from Fed’s Williams, Waller, Bostic, Barkin, Kashkari, Mester, ECB’s de Guindos & BoE’s Saunders, Supply from the US. Earnings from Norwegian Cruise Line & Warner Music. Biden speaks on soaring inflation at 11am EDT. Biden will also meet with Italian Prime Minister Draghi at the White House, and the UK state opening of Parliament is taking place, where the government outlines its legislative programme for the year ahead. Of course, the big event is tomorrow morning when the US CPI print comes.

Market Snapshot

- S&P 500 futures up 1.1% to 4,031.75

- STOXX Europe 600 up 1.2% to 422.32

- MXAP down 0.8% to 159.98

- MXAPJ down 0.8% to 523.71

- Nikkei down 0.6% to 26,167.10

- Topix down 0.9% to 1,862.38

- Hang Seng Index down 1.8% to 19,633.69

- Shanghai Composite up 1.1% to 3,035.84

- Sensex up 0.4% to 54,674.30

- Australia S&P/ASX 200 down 1.0% to 7,051.16

- Kospi down 0.5% to 2,596.56

- German 10Y yield little changed at 1.07%

- Euro little changed at $1.0564

- Brent Futures up 0.8% to $106.83/bbl

- Gold spot up 0.5% to $1,862.69

- U.S. Dollar Index little changed at 103.65

Top Overnight News from Bloomberg

- The EU is considering the issuance of joint debt to finance Ukraine’s long-term reconstruction, which may end up costing hundreds of billions of euros, according to an EU official familiar with the plan

- China’s provinces are set to sell a historic amount of new special bonds by the end of June as part of an infrastructure investment push intended to rescue an economy stymied by Covid outbreaks and lockdowns

- Hungarian Prime Minister Viktor Orban’s talks with the head of the EU about proposed sanctions on Russian oil imports made progress, but failed to reach a breakthrough, according to both sides

- Investor confidence in Germany’s pandemic rebound improved, but remained deeply negative as the war in Ukraine darkens the outlook for Europe’s largest economy. The ZEW institute’s gauge of expectations rose to -34.3 in May from -41 the previous month, defying expectations for a third straight deterioration. An index of current conditions worsened

- Saudi Arabia’s oil minister warned that spare capacity is decreasing in all sectors of the energy market, as prices of products from crude to diesel and natural gas trade at or near multi-year highs in the wake of Russia’s invasion of Ukraine

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly negative after the resumed sell-off on Wall St where the S&P 500 slipped beneath the 4,000 level for the first time since March 2021. ASX 200 briefly gave up the 7,000 status with notable underperformance in the energy and mining-related sectors. Nikkei 225 slumped from the open although moved off its lows as participants digested stronger than expected Household Spending data and after BoJ’s Uchida dismissed the prospects of a tweak to the BoJ’s 50bps yield target band. Hang Seng and Shanghai Comp both initially joined in on the selling with heavy losses in the tech sector contributing to the underperformance in Hong Kong on return from the extended weekend, although the downside in the mainland was later reversed after the recent policy support efforts by China’s MIIT and CBIRC.

Top Asian News

- China Tech Stocks Slide as Growth Woes, Global Rout Grip Traders

- Investor’s Guide to the 2022 Philippine Presidential Election

- ArcelorMittal Evaluating Bidding for ACC, Ambuja: ET Now

- Philippine Stocks Fall as Traders Weigh Marcos Win, Global Rout

European equities feel some reprieve following the prior session’s selloff; Euro Stoxx 50 +1.2%. Relatively broad-based gains are seen across the majors with some mild underperformance in the FTSE 100. Sectors show some of the more defensive sectors at the bottom of the bunch – alongside energy – whilst Construction, Autos, Banks, and Industrial Goods reside as the current winners. US equity futures are firmer across the board, ES +1.0%, with the NQ narrowly outpacing peers after underperforming yesterday.

Top European News

- Russian Gas Flows to Europe Remain Steady on Key Links

- Highest Inflation in Three Decades Boosts Czech Rate Hike Case

- BPER Banca Soars After Earnings Beat, With Fees as Highlight

- Russia’s Economy Facing Worst Contraction Since 1994

FX

- The Dollar retains a firm underlying bid ahead of another slew of Fed speakers; risk sentiment remains fluid and fragile.

- The Swiss Franc has hit a fresh 2022 peak vs the Greenback; USD/JPY is consolidating around 130.00.

- EUR/USD was unfazed by mixed German ZEW data but later lost ground under 1.0550.

- Cable rotates either side of 1.2350 awaiting Brexit/N. Ireland news, further political fallout and more comments from BoE hawk Saunders.

- Crude and commodity FX have gleaned a degree of traction from partial recoveries or stabilisation in underlying prices.

- CBRT and regulator have asked banks to undertake FX transactions with corporate clients between 10:00-16:00, when the market is liquid, via Reuters citing bankers.

Fixed Income

- Core benchmarks bounce further after a brief breather early on, with little in way of fresh fundamentals behind the upside.

- Initial highs were faded pre-UK/German issuance; once this cleared, Bunds and Gilts lifted to 152.50+ and 119.00+ peaks.

- Stateside, USTs are bolstered but far from best, with the curve re-flattening into today’s 3yr sale and yet more Fed speak.

Commodities

- Crude futures have come under renewed pressure in recent trade after seeing some gains in the European morning.

- The initial downside coincided with the mixed Germany ZEW reports alongside the downbeat commentary from Hungary regarding an imminent oil ban; albeit, benchmarks are off overnight USD 100.44/bbl and USD 103.19/bbl respective lows.

- Saudi Energy Minister says it is “mind-boggling” why focus is on high oil prices and not on gasoline, diesel or others. World needs to wake up to an existing reality that it is running out of energy capacity at all levels, via Reuters.

- UAE Energy Minister says oil prices could double or triple in “chaotic” market.

- US officials reportedly asked Brazil’s Petrobras in March to boost output, but it the oil Co. said it could not, according to Reuters sources.

- China’s Shenghong Petrochemical has started a trial operation at its (320k BPD) greenfield refining complex in east China, according to Reuters sources.

- Germany is said to be shifting away from plans for a strategic national coal reserve, according sources cited by Reuters.

- Spot gold holds onto mild gains as DXY pulled back from the fresh YTD highs set yesterday.

- LME futures post mild gains following yesterday’s downside with the market still looking somewhat fragile.

DB’s Jim Reid concludes the overnight wrap

It’s school photo day today. After discussing it with my kids last night I said to them that I’d dig out my old school photos so they could see me at school. Without hesitation and with a straight face Maisie said, “Are they in black and white Daddy?”. I was half amused and half depressed.

Markets are pretty black at the moment with little white on show. Actually the only bright colour is a sea of red. Indeed after a rocky few weeks in markets, there’s been a further rout over the last 24 hours as investor jitters about the global growth outlook have continued to escalate. There has been some respite in Asia but markets remain very shaky. There wasn’t really a single catalyst to yesterday’s steep declines, but ultimately there’s been a growing scepticism in markets as to whether the Fed and other central banks will actually be able to achieve a soft landing without a recession as they seek to bring down inflation. One interesting development though was that rates rallied as the equity slump intensified, rather than both selling off as has been the norm in recent weeks.

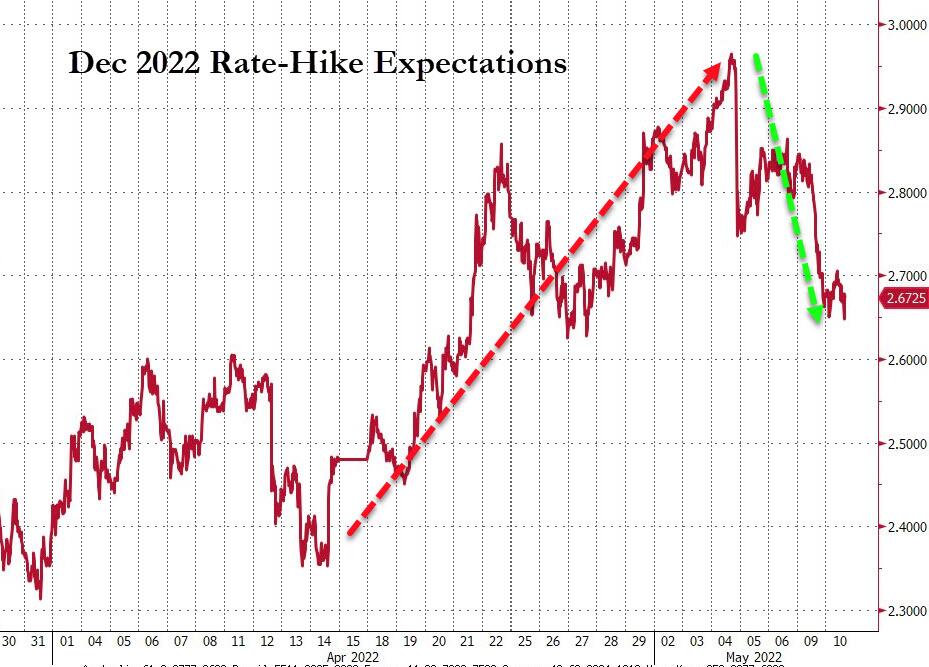

Although the day lacked a single catalyst, the bond market moves seem to turn around the same time as Atlanta Fed President Bostic spoke. He picked up where Chair Powell left things after last week’s press conference. Bostic signaled that +50bp hikes were part of his core view, placing low odds on anything larger, stating +50bp hikes were “already a pretty aggressive move.” Like other Fed speakers, he signaled a desire to get policy to neutral and then assess. While he isn’t a voter this year, his voice does carry weight at the hawkish end of the committee so the price action likely reflected the market believing that a consensus continues to build for 50bps, and not 75bps, even among the hawks.

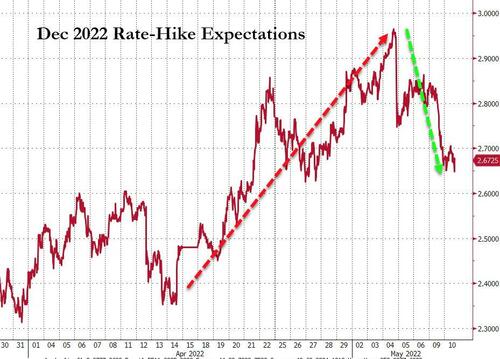

Sovereign bonds were actually seeing a strong sell-off before his comments but rallied fairly fiercely from around the same time. 10yr Treasury yields hit an intraday high of 3.20% during the European morning (+7.5bps on the day) but ended up closing -9.3bps lower at 3.03%, showing that wide intraday ranges and volatility continue to grip the market. With the Fed continuing to put a perceived ceiling on the near-term pace of hikes, 2yr yields rallied -13.7bps on the day with the curve steepening another +5.3bps. The amount of Fed hikes priced in by the December meeting down by -15.5bps. As I type, 10yr US yields are fairly flat in Asia.

The move echoed in Europe, where 10yr bunds rallied -3.5bps to 1.09%. The broader risk-off move meant that there was a further widening in spreads yesterday, with the gap between Italian 10yr BTPs over bunds widening by +4.9bps to 205bps, which is the widest they’ve been since May 2020. And that widening was seen on the credit side as well, where iTraxx Main moved above 100bps for the first time since April 2020 in trading, before falling back somewhat to settle at 98bps (+1.4bps).

Against this backdrop, the S&P 500 fell by a sizeable -3.20% that takes the index to its lowest level in over a year. That comes on the backs of 5 consecutive weekly losses, which is already the longest run in over a decade, and given the performance yesterday it would take a strong comeback over the remaining four days this week to avoid that run extending to 6 weeks. See my Chart of the Day yesterday (link here) for more on how rare it has been to see an 11 year run without a 5 successive weekly decline.

Energy was the worst performing US sector, falling an astonishing -8.30%, in its worst one-day performance since June 2020, after the fall in oil (more below). The sector is still by far the best performing S&P sector YTD, up +36.79%, with every other sector in the red. Despite the rate rally, it was a bad day for mega-cap and other growth tech stocks. Indeed, the NASDAQ fell a further -4.29% to its lowest level since November 2020, whilst the FANG+ index of 10 megacap tech stocks fell an even larger -5.48%. For reference, that now takes the FANG+ index’s decline since its all-time high in November to a massive -38.22%. Even a high quality component like Amazon is now down -35.75% since March 29th and is pretty much back to pre-covid levels. Over the other side of the pond, Europe saw some sizeable declines as well, with the STOXX 600 down -2.90% to leave the index not far away from its recent lows in early March.

With the Fed set to continue their hiking cycle, just as the ECB are still pondering on when to even start hikes and China’s growth prospects are fading, the US dollar has continued to benefit. Yesterday, the Japanese Yen (+0.21% vs USD) was the top-performing G10 currency, in line with its traditional status as a safe haven, but Bitcoin continued to lose ground, falling to its lowest level since July last year, after falling to $31,562. It briefly fell below 30k this morning. It’s been interesting that Bitcoin is not getting much mention with all the inflationary issues seen in recent months. It seems to be suffering from a higher dollar, higher real yields and a tech related sell-off.

Markets continue to fall in Asia but US futures are up. Hang Seng (-3.06%) is the largest underperformer, but is paring its losses after falling more than -4% as the market returned after a holiday with the Chinese listed tech firms among the worst hit. Elsewhere, the Nikkei (-0.93%) and Kospi (-0.95%) are down. Meanwhile, mainland Chinese stocks are trading in positive territory with the Shanghai Composite (+0.17%) and CSI (+0.15%) somewhat recovering from opening losses. Looking ahead, S&P 500 (+0.56%), NASDAQ 100 (+0.92%) and DAX (+0.25%) futures are moving higher.

Early morning data showed that Japan’s household spending declined -2.3% y/y in March, its first drop in three months albeit the fall was less than -3.3% estimated by Bloomberg and followed +1.1% growth in February.

Back to inflation and one potentially problematic indicator came from the New York Fed’s latest consumer survey, which found that median inflation expectations for 3 years ahead rose to +3.9%, which is the highest since December, and up from +3.5% back in January. It’s still not as high as the +4.2% readings back in September and October, but will obviously be unwelcome news to the Fed whose path to a soft landing is in part reliant on inflation expectations remaining well anchored around target.

Turning to the situation in Ukraine, a key risk event yesterday had been Russia’s Victory Day parade, where it was speculated that President Putin would move towards a general mobilisation. However, in reality it finished with surprisingly little news, and whilst not showing a path towards de-escalation, didn’t move to escalate things further. Separately, it was reported by Bloomberg that the EU would soften its proposed sanctions package on Russian oil exports, with an article saying that they would drop the proposal to ban EU-owned vessels transporting Russian oil to third countries. The sanctions package has already come under criticism from some member states, and the article said that Hungary and Slovakia had been offered a longer time period lasting until end-2024 to comply with the proposals to ban Russian oil imports, with Hungary in particular saying more talks were needed to support oil-related sanctions. So with no further escalation and a softening in sanctions, oil prices fell back significantly amidst weak risk appetite more generally. Brent crude was down -5.74%, whilst WTI fell -6.09%, which follows 2 consecutive weekly gains for both. This morning oil prices are again lower with Brent and WTI futures -1.74% and -1.68% lower respectively.

To the day ahead now, and central bank speakers include the Fed’s Williams, Barkin, Waller, Kashkari and Mester, along with ECB Vice President de Guindos and Bundesbank President Nagel. Data releases include Italy’s industrial production for March and Germany’s ZEW survey for May. Finally on the political side, President Biden will meet with Italian Prime Minister Draghi at the White House, and the UK state opening of Parliament is taking place, where the government outlines its legislative programme for the year ahead.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 31.70 PTS OR 1.06% //Hang Sang CLOSED DOWN 368.27 PTS OR 1.84% /The Nikkei closed DOWN 152.24 OR 0.58% //Australia’s all ordinaires CLOSED DOWN 0.99% /Chinese yuan (ONSHORE) closed up 6,7245 /Oil DOWN TO 101.42 dollars per barrel for WTI and down TO 104.85 for Brent. Stocks in Europe OPENED ALL green // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7245 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7487: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA

END

3B JAPAN

Now it is Japan’s turn to report more suspected cases of unexplained and rare acute hepatitis in children. My guess is that all the children were vaccinated.

The spike protein attacks the liver

(Fredly/EpochTimes)

Japan Reports More Suspected Cases Of Unexplained Acute Hepatitis In Children

MONDAY, MAY 09, 2022 – 07:10 PM

Authored by Aldgra Fredly via The Epoch Times (emphasis ours),

At least seven possible cases of acute hepatitis—inflammation of the liver—in children have been identified in Japan, the Health Ministry said Friday, but the cause of the cases is yet unknown.A file image of a woman with a pushchair walking with children at a park in Tokyo. (Yoshikazu Tsuno/AFP via Getty Images)

The first case was reported on April 25, followed by the second on April 28. Four more possible cases were reported on May 6, the ministry said in a statement (pdf). The patients are all under the age of 16.

One of them tested positive for COVID-19, and another Adenovirus Type 1, the ministry said according to The Japan Times, without mentioning whether these were two separate people or one person who caught both viruses.

It stated that the seven recorded cases comprised children admitted to hospitals between October, 1. 2021 and May, 6. 2022, with some having already been discharged. None of the patients received a liver transplant.

The World Health Organization (WHO) told news outlets on May 3 that there were at least 228 probable cases of hepatitis worldwide in at least 20 countries, including Denmark, the United States, the United Kingdom, Italy, and France.

WHO stated on April 23 that the cases involved children aged one month to 16 years old, many of whom developed gastrointestinal symptoms, including abdominal pain, diarrhea, and vomiting preceding presentation with severe hepatitis and jaundice (yellowing skin and eyes).

“The common viruses that cause acute viral hepatitis (hepatitis viruses A, B, C, D, and E) have not been detected in any of these cases. International travel or links to other countries based on the currently available information have not been identified as factors,” it said.

In Indonesia, a mysterious form of hepatitis has been linked to the deaths of three children ages two, eight, and 11, The Jakarta Post reported on May 3. The Health Ministry said the children developed diarrhea and jaundice, adding that the case was still under investigation.

The U.S. Centers for Disease Control and Prevention (CDC) said Friday that it was investigating more than 10 cases of a mysterious form of hepatitis in children, saying that five have died so far.

Dr. Jay Butler, the CDC’s deputy director of infectious diseases, said during a briefing said the agency is investigating 109 cases of acute hepatitis in 24 U.S. states and Puerto Rico. The cause of the outbreak is not yet clear, he stressed, adding that about half of the children had adenovirus infections.

The UK Health Security Agency reported that (pdf) the country’s case count had risen to 163, dating back to early January, adding that 11 children have received liver transplants so far. UK officials ruled out the COVID-19 vaccine as a potential cause.

“There are fewer than five older case-patients recorded as having had a COVID-19 vaccination prior to hepatitis onset,” the report said, adding that most of the impacted children are too young to receive the shot. “There is no evidence of a link between COVID-19 vaccination and the acute hepatic syndrome.”

Jack Phillips contributed to this report.

3c CHINA

COVID/SHANGHAI/LOCKDOWNS

Tesla reportedly halts its Shanghai production again due to supply issues

(zerohedge)

Tesla Reportedly Halts Shanghai Production Again, This Time Due To “Issues With Supplies”

MONDAY, MAY 09, 2022 – 11:10 PM

No sooner did it seem Tesla got back up and running in Shanghai than its plant is apparently halting production yet again, according to an exclusive from Reuters late Monday night. The halt is due to “issues with supplies,” according to the report.

It comes just three weeks after the plant resumed production after shutting down due to Covid lockdowns. The plant was closed for a total of 22 days, Reuters noted.

Shanghai is in its sixth week of lockdowns, the report notes, and as of now it is “unclear when the supply issues can be resolved and when Tesla can resume production”.

Wire harness maker Aptiv is one supplier who is currently facing issues due to “infections found among its employees”.

Tesla had just started to eye resuming double shifts at its plant, we noted last Friday. The plant was making plans to “resume double shifts” at its Shanghai factory as soon as mid-May after starting back up in mid April.

Upon the April restart, workers were living on site to reduce Covid risk. Workers returned to work under this system were working 12 hour shifts, six days a week, we wrote.

Management had been “canvassing the willingness of staff to leave their residential compounds” and “looking at daily door-to-door shuttle buses that would allow some workers to return home after their shift rather than sleep at the factory”.

We’re guessing that plans for the double shifts have likely been shelved for the time being…

We also wrote on Friday that the plant had “remained challenged” by parts shortages, pushing back waits for new Model 3 Teslas to 20 to 24 weeks, instead of their normal wait time of 4 to 6 weeks.

Recall, back on April 19, we wrote that Shanghai had re-opened. Additionally, we noted days ago that Elon Musk was eerily quiet about China’s lockdowns, after in 2020, Musk slammed stay-at-home orders in the U.S., labeling them “fascist”. Musk called shelter-in-place orders “forcibly imprisoning people in their homes against all their constitutional rights,” CNBC reported at the time.

END

CHINA//

4/EUROPEAN AFFAIRS//UK AFFAIRS/EU

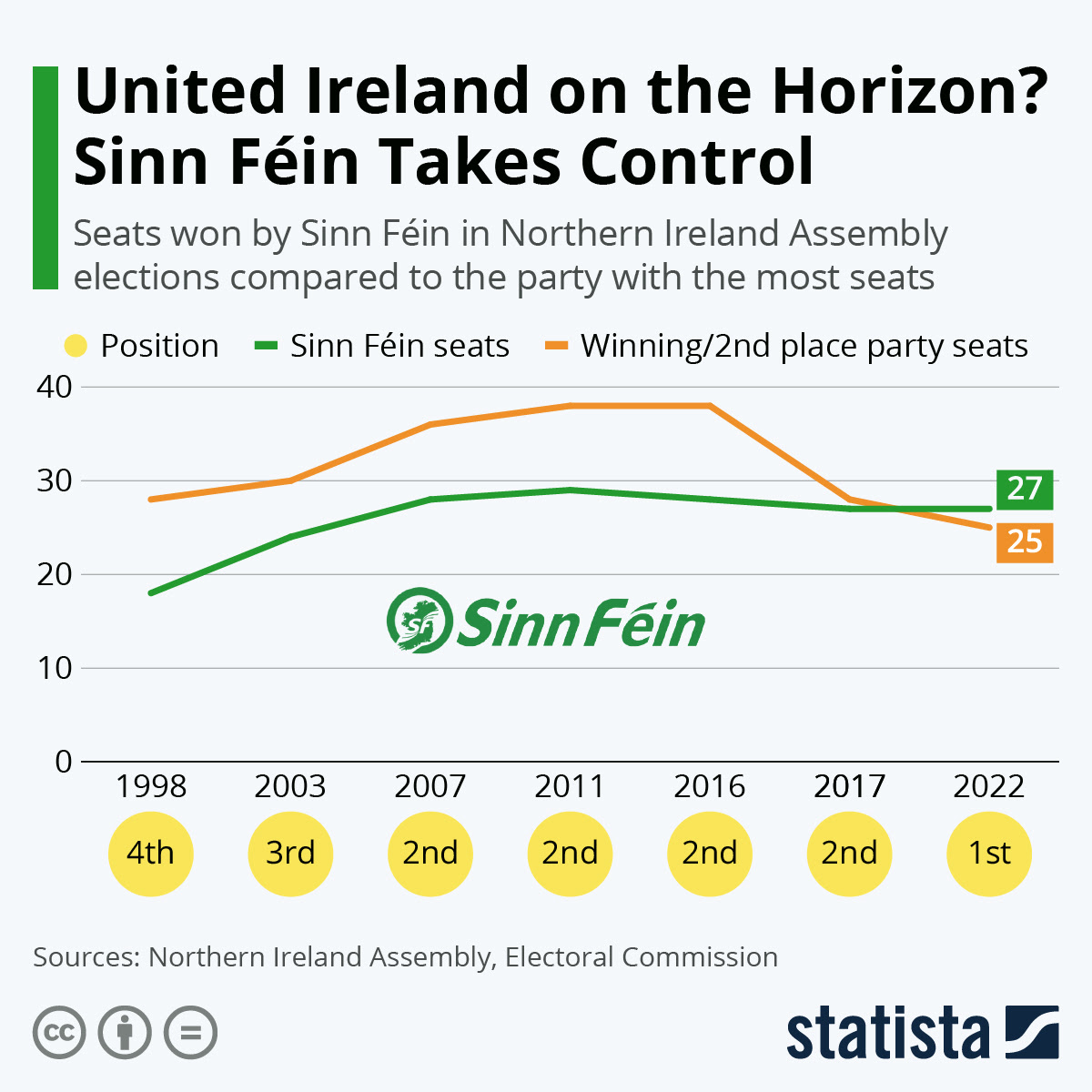

IRELAND

With the election of Sinn Fein, Ireland is now one step closer to a unified Ireland

(zerohedge)

United Ireland On The Horizon? Sinn Féin Takes Control For First Time

TUESDAY, MAY 10, 2022 – 02:45 AM

For the first time since the first election of the Northern Ireland Assembly in 1998, the Irish nationalist party Sinn Féin has won more seats than any other party after the vote held on May 5.

Sinn Féin aims to reunify Northern Ireland with the Republic of Ireland and is now close to installing party vice-president Michelle O’Neill as first minister.

As Statista’s Martin Armstrong shows in the infographic below, Sinn Féin were just the fourth most-popular party in 1998, taking 18 seats compared to the winning Ulster Unionist Party’s 28. Having established itself as the second largest party in the years since, 2022 represents the first time it has gained control of the most seats, and the first time a nationalist party has won since Northern Ireland was founded in 1921.

You will find more infographics at Statista

So does this mean we are now a significant step closer to a united Ireland?

O’Neill avoided focusing on this issue during campaigning, instead choosing to prioritize the cost of living crisis. Before we see what her focus is while in office though, the parties have to form an Executive – something which the opposition unionist party the DUP has indicated it may not do with a nationalist first minister such as O’Neill. If no government is formed within six months, new elections will have to take place.

What this election does signify however, is a shift towards nationalist politics in Northern Ireland.

END

EU/UKRAINE

Now its Europe’s turn to launder money through the Ukraine. They plan on issuing $15 billion in short term financing needs

(zerohedge)

European Commission Plans New EU Debt Issuance To Cover Ukraine’s Short-Term €15BN Financing Needs

TUESDAY, MAY 10, 2022 – 05:45 AM

The World Bank recently estimated that Russia’s ongoing bombardment of the country, which has lately appeared to focus on degrading the country’s rail and power infrastructure, has caused at least at least $60 billion in damage.

That “does not include the growing economic costs to Ukraine’s economy,” World Bank president David Malpass said weeks ago. Ukrainian President Volodymyr Zelensky had also at the time told a World Bank ministerial conference his country needs some $7 billion per month just to make up for the destruction, “And we will need hundreds of billions of dollars to rebuild all of this later.” And that doesn’t include what’s needed simply to keep state services afloat.Outside European Parliament

Zelensky followed those comments by this month attempting to put a figure to the total that Ukraine needs, citing a ballpark $600 billion to rebuild. “I’m sure after victory we will do everything quite fast, and Ukraine will be more beautiful than before,” he remarked a week ago during a virtual appearance before The Wall Street Journal’s CEO Council Summit in London.

And then there’s much more short-term and immediately urgent matters of keeping up with public wages, pensions, and things like funding public facilities which receive the internally displaced, now estimated at over 7 million people.

Washington has been first out of the gate in pledging massive relief – to the tune of up to one third of the estimated €15 billion (or over $15.8 billion) needed just to cover Ukraine’s short-term financing needs over the next three months, according to a fresh IMF estimate.

Politico details in its latest reporting:

The United States has pledged to provide a third of that sum, which would leave €10 billion uncovered. The Commission briefed EU ambassadors Friday on a plan to bridge that gap, which would entail the Commission issuing debt on the back of guarantees provided by EU countries. That’s similar to the so-called SURE program used during the pandemic to raise funds for the short-term unemployed, the diplomats said.

At the time, the Commission asked €25 billion in guarantees to raise €100 billion.

One diplomat made the following observation to the publication: “Whenever there’s a problem with money, [the Commission] says SURE!”

Whether it’s the massive and unprecedented billions in military and humanitarian aid for Ukraine that Washington has already approved, or the €15 billion debt relief the EU is now mulling, the elephant in the room (and among mainstream media talking points that seems to have been forgotten) remains: whatever happened to what was for years widely understood as an assumed fact – the notorious corruption of Ukraine’s political class?

And now billions upon billions is set to flow through its coffers from the West. Add to this that in a time of war (as the recent examples of Afghanistan and Iraq have proven), huge sums of money and “aid” have a habit of going unaccountable and disappearing.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

/UKRAINE/USA/RUSSIA

Pentagon to give the Ukraine high precision laser guided rockets. That should annoy Russia again

(zerohedge)

Pentagon To Give Ukraine High-Precision Laser-Guided Rockets

MONDAY, MAY 09, 2022 – 06:50 PM

On Monday The Washington Post is reporting that for the first time the Pentagon will provide Ukrainian forces “high-precision laser-guided weapons” as part of the recently approved mammoth arms package amid Russia’s invasion.