May 9, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1859.30 down $24.05

SILVER: $21.88 DOWN $.50

ACCESS MARKET: GOLD $1853.85

SILVER: $21.77

Bitcoin morning price: $32,980 DOWN 2929

Bitcoin: afternoon price: $30.846 DOWN 5063

Platinum price: closing down $16.95 to $968.50

Palladium price; closing down 139.70 at $2048.00

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices:3/3

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,881.200000000 USD

INTENT DATE: 05/06/2022 DELIVERY DATE: 05/10/2022

FIRM ORG FIRM NAME ISSUED STOPPED

661 C JP MORGAN 3

737 C ADVANTAGE 3

TOTAL: 3 3

MONTH TO DATE: 1,912

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 3 NOTICE(S) FOR 300 OZ (0.00933 TONNES)

total notices so far: 1912 contracts for 191,200. oz (5.9471 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED NIL OZ/

total number of notices filed so far this month 3620 : for 18,100,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $24.05

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNESE FROM THE GLD

INVENTORY RESTS AT 1084.98 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 50 CENTS

CENTS

AT THE SLV// A SMALL CHANGE IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF .9300 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 575.977 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A SMALL SIZED 403 CONTRACTS TO 141,187 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR TINY $0.06 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.06) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A SMALL GAIN OF 428 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 470,000 OZ E.F.P JUMP TO LONDON //NEW STANDING 28.130 MILLION OZ/ // V) SMALL SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -6

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 5days, total 7141, contracts: 35.705 million oz OR 7.142 MILLION OZ PER DAY. (1428CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 36.705 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 35.705 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 403 WITH OUR TINY $0.06 LOSS IN SILVER PRICING AT THE COMEX// FRIDAY., TODAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 825 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 470,000 OZ E.F.P JUMP TO LONDON//NEW STANDING 28.130 MILLION OZ// .. WE HAD A SMALL SIZED LOSS OF 428 OI CONTRACTS ON THE TWO EXCHANGES FOR 2.14 MILLION OZ DESPITE THE SMALL GAIN IN PRICE.

WE HAD 0 NOTICE FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY AN UNBELIEVABLE SIZED LOSS 0f 19,111 CONTRACTS TO 554,662 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –322 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE MAMMOTH SIZED DECREASE IN COMEX OI CAME DESPITE OUR STRONG GAIN IN PRICE OF $7.95//COMEX GOLD TRADING/FRIDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 70,500 OZ//NEW STANDING 8.227 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $7.95 WITH RESPECT TO FRIDAY’S TRADING????

WE HAD A STRONG SIZED LOSS OF 16,924 OI CONTRACTS (52.64 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2187 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 554,662.

IN ESSENCE WE HAVE A HUMONGOUS SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16.924, WITH 19,111 CONTRACTS DECREASED AT THE COMEX AND 2187 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 16,924 CONTRACTS OR 52.64 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2187) ACCOMPANYING THE MAMMOTH SIZED LOSS IN COMEX OI (19,111,): TOTAL LOSS IN THE TWO EXCHANGES 16,924 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 70500 OZ//NEW STANDING 8.229 /// 3) HUGE LONG LIQUIDATION??? OR TAS OPERATION??? //.,4) MAMMOTH SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

16248 CONTRACTS OR 1,624,800 OR 50.54 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 3250 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 50.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 50.54/3550 x 100% TONNES 1.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 50.54 TONNES INITIAL//SLIGHTLY INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, fell BY A SMALL SIZED 403 CONTRACT OI TO 141,187 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 825 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 825 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 397 CONTRACTS AND ADD TO THE 825 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF 422 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 2.11 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.6 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 2.58 PTS OR 0.09% //Hang Sang CLOSED /The Nikkei closed DOWN 684.22 OR 2.53% //Australia’s all ordinaires CLOSED DOWN 1.47% /Chinese yuan (ONSHORE) closed DOWN 6,7281 /Oil DOWN TO 07.26 dollars per barrel for WTI and UP TO 109.82 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7281 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7699: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER//

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GIGANTIC SIZED 19,111 CONTRACTS TO 554,662 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $7.95 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2187 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2187 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2187 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2187 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 16,924 CONTRACTS IN THAT 2187 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI LOSS OF 19,111 CONTRACTS..AND THIS LOSS OCCURRED DESPITE OUR GAIN IN PRICE OF GOLD $7.95.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (7.589),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 7.589 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $7.95) BUT WERE SUCCESSFUL IN FLEECING QUITE A FEW LONGS//OR WE HAD ANOTHER OF THOSE TAS MOVES// AS WE HAVE REGISTERED A GIGANTIC SIZED LOSS OF 52.64 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (7.589 TONNES)…

WE HAD 322 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 16,924 CONTRACTS OR 1,692,400 OZ OR 52.64 TONNES

Estimated gold volume today: 229,406/// fair

Confirmed volume yesterday:249,526contracts fair

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 9

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 485.502 oz Manfra JPM includes 12 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 3 notice(s) 300 OZ 0.00933 TONNES |

| No of oz to be served (notices) | 733 contracts 73,300 oz 2.2799 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1912 notices 191,200 OZ 5.947 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

0 customer deposit

2 customer withdrawals:

i) Out of JPMorgan: 385.812 oz (12 kilobars)

ii) Out of Manfra 99.60 oz

total withdrawal: 485.502 oz

ADJUSTMENTS: 1 JPM//dealer to customer 96.454 oz 3 kilobars

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 736 contracts having LOST 220 contracts

We had 425 notices filed on Friday, so we gained 205 contracts or AN ADDITIONAL 20,500 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 32,434 contracts down to 382,426 contracts (makes no sense)

July has a loss of 6 OI to stand at 153

August has a gain of 17,474 contracts up to 118,577 contracts

We had 3 notice(s) filed today for 300 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 3 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (1912) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 736 CONTRACTS ) minus the number of notices served upon today 3 x 100 oz per contract equals 264,500 OZ OR 8.227 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (1912) x 100 oz+ (736) OI for the front month minus the number of notices served upon today (3} x 100 oz} which equals 264,500 oz standing OR 8.227 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 8.227 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

263,958.054, oz JPM No 2 7.58 TONNES

1,063,208.634 oz pledged Brinks/27,96 TONNES

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

Loomis: 32,840.423 oz

total pledged gold: 1,941,626.135 oz (1115,92 TONNES)

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 36,043,787.165 OZ (

TOTAL ELIGIBLE GOLD: 18,232,567.378 OZ

TOTAL OF ALL REGISTERED GOLD: 17,811,219.787 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,869,593.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 9

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 620,999.540 oz JPMorgan CNT Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 2339,330.200 oz HSBC JPMorgan |

| No of oz served today (contracts) | 0CONTRACT(S)NIL OZ) |

| No of oz to be served (notices) | 2006 contracts (10,030,000 oz) |

| Total monthly oz silver served (contracts) | 3620 contracts 18,100,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

ii) Into JPMorgan: 1,150,280.100 oz

iii) Into HSBC: 1,189,050.100 oz

total deposit: 2,339,330.200 oz

JPMorgan has a total silver weight: 177.761 million oz/336.936 million =52.74% of comex

Comex withdrawals: 3

i) Out of JPMorgan 586,762.520 oz

ii) Out of CNT:: 29,167.640 oz

iii) Out of Manfra: 5069.400 oz

total withdrawal 620,999.540 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.067 MILLION OZ

TOTAL REG + ELIG. 336.936 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 2006 HAVING LOST 876 CONTRACTS. WE HAD 782 NOTICES FILED ON FRIDAY

SO WE LOST 94 CONTRACTS OR AN EFP JUMP OF 470,000

JUNE HAD A LOSS OF 90 TO STAND AT 1581

JULY HAD A GAIN OF 262 CONTRACTS UP TO 114,641 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 55,814// est. volume today// fair

Comex volume: confirmed yesterday: 77,177 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 3620 x 5,000 oz = 18,100,000 oz

to which we add the difference between the open interest for the front month of MAY(2006) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 3620 (notices served so far) x 5000 oz + OI for front month of MAY (2006) – number of notices served upon today (0) x 5000 oz of silver standing for the MAY contract month equates 28,130,000 oz. .

We LOST 94 contracts or AN ADDITIONAL 470,000 will NOT stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WIOTHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

GLD INVENTORY: 1082.00 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Fed Has Already Lost The Inflation Fight

MONDAY, MAY 09, 2022 – 09:40 AM

Last week, the Fed raised interest rates by 0.5%. It was the biggest rate increase since the year 2000. But it was hardly aggressive in light of the current bout of inflation. Not only that, Jerome Powell took a future 75 basis point hike off the table. In his podcast, Peter Schiff argued that no matter what the Fed does, it has already lost the inflation fight.

The stock market collapsed on Thursday after digesting the rate hike. That more than erased the rally last Wednesday in the immediate aftermath of the FOMC meeting.

Peter said he thinks the recent Fed actions don’t matter. The markets are going down for reasons other than a 50 or 75 basis point rate hike.

Either hike is inadequate for the task at hand. It doesn’t matter. It’s too little, too late. Fifty, 75, 100 — the Fed is not in a position to raise interest rates anywhere near enough to slow down inflation. But any attempt to raise interest rates, even slightly, will prick the bubble, which it’s already done, and the air is coming out. So, the Fed will succeed in killing the economy, but it will not kill inflation.”

Peter said there were so many debacles in the stock market last Thursday that it was hard to even focus on specifics, but he noted Etsy was down 16.8% and eBay was down 11.7%. Both of these companies sell products online.

Obviously, they don’t sell food. They don’t sell gasoline. And so when people are spending so much money on basic necessities, they don’t have money left over to buy somebody’s used clothes on eBay or whatever they sell on Etsy.”

Shopify is also feeling the pinch for the same reason.

Peter said there is nothing to hang your hat on if you’re looking for a bottom.

The technical picture is bleak and the fundamental picture is even bleaker.”

He said there is no reason to think we are anywhere near the bottom unless the Fed does an about-face. Of course, that is a possibility.

But as long as the Fed is going to pretend that it’s going to fight inflation, the market is going to keep going down.”

At this point, it appears the markets still believe that the Fed is going to do what it claims it’s going to do – keep hiking and beat back inflation. But Peter said what the Fed claims it’s going to do is impossible.

Especially given what it’s saying it’s going to do, which is maybe raise interest rates up to 2.5 or 3 percent. Even if they do that, it is wholly inadequate to bring down an inflation rate that officially is 8 or 9 percent, but unofficially, in reality, is probably closer to twice that level. There is no way the Fed is going to be able to succeed. But what it is succeeding in doing by pretending it can fight inflation is crashing the stock market.”

Meanwhile, productivity just saw its sharpest drop since 1947.

The April jobs numbers hit expectations, but the labor force participation rate unexpectedly dropped. The Fed and others point to the strong labor market as a sign the economy is strong. But it’s important to remember that labor data is a lagging indicator. Once layoffs start, the economy is already in deep trouble.

Peter said he thinks that there is already more than enough evidence to conclude that we’re already in a recession. We had a negative GDP in Q1. If GDP contracts again in Q2, that will mean we are in a recession, and that we were in a recession in Q1.

Think back to 2008. In retrospect, we know the Great Recession started in December of 2007. But in early 2008, all of the pundits were insisting we weren’t in a recession and everything was going to be OK.

If I’m right, and we’re already in a recession now, this recession is going to be worse than that one. In fact, this may not be the worst recession since the Great Depression. This will be the worst recession including the Great Depression because it will be accompanied by very high inflation.”

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

PAM AND RUSS MARTENS

Pam and Russ Martens: These stock patterns are impossible without manipulation SEC ignores

Submitted by admin on Mon, 2022-05-09 11:29Section: Daily Dispatches

Despite their longstanding heroic work, even the Martenses haven’t yet realized that market manipulation conducted by or at the behest of the U.S. government is fully authorized by the Gold Reserve Act of 1934 as amended since then. The law gives market-rigging power to the U.S. Treasury Department’s Exchange Stabilization Fund, which can use the New York Fed or any investment house as its broker.

* * *

By Pam Martens and Russ Martens

Wall Street on Parade

Monday, May 9, 2022

Beginning in November 2008, the Federal Reserve was allowed by Congress to manipulate the U.S. bond market through purchases of bonds with money it creates at the flick of an electronic button. The Fed calls this “quantitative easing” or QE.

Beginning on September 17, 2019 — when overnight lending rates on repo (repo means repurchase agreements between financial institutions) touched 10% instead of the 2.5% that the Fed wanted the market to be at — the Fed began providing repo loans at “administered rates.” It did that by jumping into the repo market with both feet, proceeding to make trillions of dollars in cumulative loans to trading houses on Wall Street, at interest rates as low as 0.10% by the spring of 2020.

During 2020 the Fed also artificially propped up money market mutual funds, commercial paper, exchange-traded funds, and the corporate bond market with emergency lending facilities it created. The Fed did not need a vote in Congress to create those bailout programs. It needed only the permission of Steve Mnuchin, Donald Trump’s wily treasury secretary.

Wall Street On Parade has been witnessing a new pattern in the stock market for several months now where the market plunges at the open and then shortly thereafter, on no major news, turns on a dime and spikes higher.

This suggests one of two things to us: 1) either the New York Fed is manipulating stock trading out of its second office close to the futures markets in Chicago; or 2) big money at Wall Street trading houses and/or hedge funds is doing it. Either way, the Securities and Exchange Commission and the Justice Department have not nipped this activity in the bud. …

… For the remainder of the analysis:

-END-

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

see Andrew/s video below.

Russia’s discounts on energy purchased with gold are draining exchanges, Maguire says

Submitted by admin on Sat, 2022-05-07 23:23Section: Daily Dispatches

11:33p ET Saturday, May 7, 2022

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire, in his weekly interview with Shane Morand for Kinesis Money, says gold and silver prices on the London and New York exchanges no longer represent the markets for the bulk of trading of those metals, which now is happening outside the exchanges and involves large premiums.

By offering large discounts on prices for energy and other commodities purchased with gold, Maguire says, Russia is absorbing so much physical gold that the official London market is effectively restricting daily sales of real metal to just a few tonnes.

Maguire’s interview is 33 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

When buying gold and silver, consider the dealers who support GATA

Submitted by admin on Sun, 2022-05-08 21:51Section: Daily Dispatches

9:52p ET Sunday, May 8, 2022

Dear Friend of GATA and Gold:

Being the only forms of money without counterparty risk, at least when held directly by their owners, gold and silver are often seen as the foundation of a sound investment portfolio.

This principle was put into graphic format by the U.S. economist John Exter, who served as the Federal Reserve Bank of New York’s vice president in charge of international banking and precious metals operations, as well as a member of the Federal Reserve’s Board of Governors, long before suppressing the gold price became the Fed’s primary objective.

In Exter’s inverted pyramid of financial asset risk, gold is the ultimate asset, with all other assets posing greater risk to their owners:

But you can do more than protect yourself when you buy gold and the other monetary metal, silver. You can also help GATA fight the price suppression we long have been exposing, documenting, and sometimes litigating against:

That is you can buy metal from dealers who support GATA and have been recommended by our supporters over the years.

A list of those dealers is included with every GATA Dispatch and is posted at GATA’s internet site here:

So please give them a chance to meet your investment needs.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

Andrew M’s new video from yesterday

Inbox

| Chris Powell | Sat, May 7, 4:42 PM (2 days ago) | ||

| to me |

—–

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

USA

Office: 860-646-7383

Mobile: 860-305-4013

Attachments area

Preview YouTube video Ep 72: Live From the Vault – LBMA Price ‘Fix’ Rocks the Gold Market

Ep 72: Live From the Vault – LBMA Price ‘Fix’ Rocks the Gold Market

end

5.OTHER COMMODITIES //DIESEL

Diesel price is skyrocketing price

(FreightWaves)

The World Is “Crying Out For Diesel”; Product Tankers Could Win Big

SUNDAY, MAY 08, 2022 – 05:30 PM

By Greg Miller of Freight Waves,

Retail gasoline prices in the U.S. are up 45% year on year. Diesel used by American truckers is up 75% and just hit an all-time high. But this is not just an American problem. Pain at the pump is global. And so-called product tankers — ships designed to transport cargoes such as diesel, gasoline and jet fuel — are in prime position to profit.

Fuel flows globally to where it earns the highest return. Case in point: As U.S. diesel prices have skyrocketed, American exports of diesel have surged, because demand in other countries is higher.

U.S distillate fuel exports hit 1.74 million barrels per day (b/d) in early April, nearing record levels, according to preliminary data from the Energy Information Administration (EIA). Total U.S. exports of all refined products in April rose 28% year on year.

‘Outright panic buying of diesel’

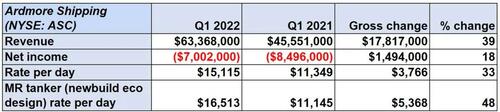

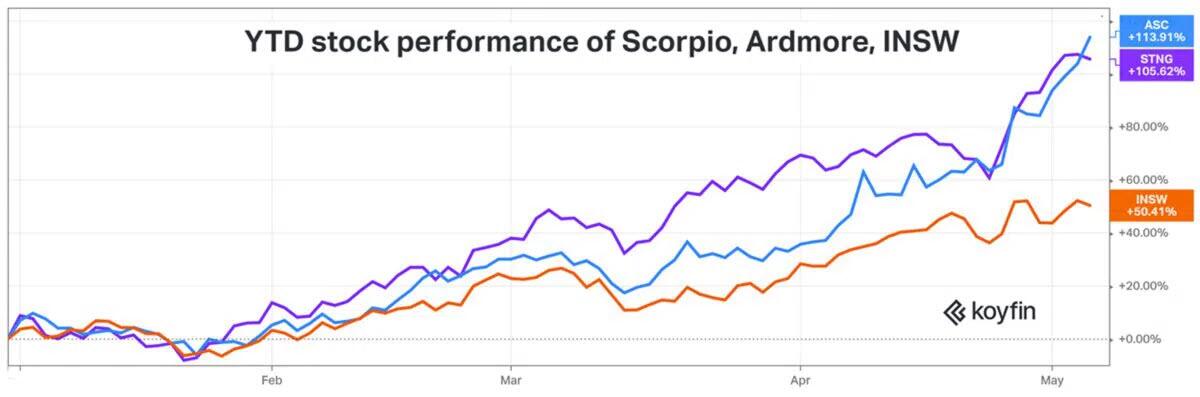

“There has been outright panic-buying of diesel,” said Anthony Gurnee, CEO of product-tanker owner Ardmore Shipping, during a conference call on Wednesday.

Ardmore specializes in MR tankers, a vessel class with capacity ranging from 25,000-54,999 deadweight tons (DWT). Clarksons Platou Securities said that modern-built MRs were earning $49,800 per day in the spot market as of Friday. That’s more than quadruple the average rate for full-year 2021. Clarksons puts the breakeven rate for such vessels at $18,000 per day.

“The world is really crying out for diesel and that’s causing refinery margins to spike,” said Lois Zabrocky, CEO of International Seaways, during a conference call on Wednesday.

INSW’s product tanker fleet primarily consists of MRs and LR1s (55,000-79,999 DWT). Modern LR1s are earning $50,400 per day in the spot market, according to Clarksons, which puts the breakeven rate for such ships at $19,000 per day. Current LR1 rates are almost quadruple their full-year 2021 average.

Larger LR2s (80,000-119,00 DWT) that handle high-volume, long-haul runs are showing even steeper gains. Rates for modern LR2s jumped 21% on Friday to $58,600 per day, said Clarksons.

War exacerbates diesel shortages

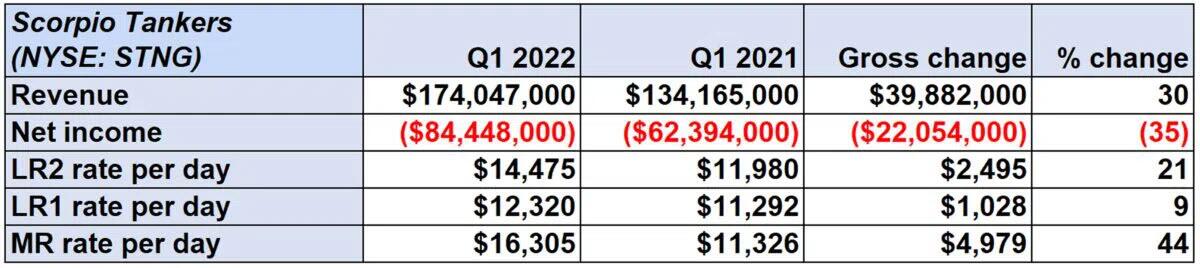

The worldwide diesel market is “extremely tight” and the Russia-Ukraine war “has exacerbated the global diesel shortage,” said James Doyle, head of corporate development at Scorpio Tankers, during a conference call on April 28.

Before the invasion, he said, Russia exported about 1 million b/d of diesel to Europe. That volume has plummeted. “But the diesel shortage in Europe is not new,” he added. “And the shortage extends beyond Europe to Latin America and Africa, which have similar diesel deficits.

“For our MRs, the highest rate increases were for our vessels going from the U.S. Gulf to Latin America, which has less to do with Russia and Ukraine and more to do with increasing demand,” Doyle pointed out.

“We expect the market to tighten further with increased competition for distillate molecules as jet fuel demand returns. This is also having an impact on gasoline. With refineries running in max distillate mode, we are not building significant gasoline inventories ahead of peak driving season. As demand grows and inventories remain low, product tankers will need to be the conduit for filling the global supply-demand imbalance.”

Commodity specialist Argus made the same point on gasoline. “The lack of spare capacity is causing alarm heading into the peak summer driving season,” Argus warned on Thursday. “The situation is compounded by even higher middle-distillate margins, which have boosted supply of diesel over gasoline.”

Inventories drawn through COVID era

Usually, rates for tankers that carry crude oil and rates for tankers that carry petroleum products trend roughly in tandem. And if one outperforms the other, it’s usually crude. This year, product tankers are dramatically outperforming crude tankers; larger crude tankers are still below breakeven.

Both crude and product tankers saw rates collapse during the COVID era. Oil production outstripped demand amid lockdowns. The world’s inventories filled with cheap crude and products bought at the trough.

Ever since, those inventories have been drawn down instead of using tankers to import new supply (because new supply is much more expensive than the petroleum still in storage bought at the trough).

Due to this practice, stockpiles were already historically low months before Russia invaded Ukraine. In November 2021, Alphatanker published a report called “Welcome to the great diesel squeeze,” which warned: “It’s now apparent that global gasoil and diesel markets are tightening at an alarming pace with supply shortfalls now hitting key consumer markets worldwide.”

Then Russia invaded Ukraine. “This event immediately laid bare … the risks of severely depleted inventories,” said Evercore ISI analyst Jon Chappell.

Product tankers vs. crude tankers

Asked why this has boosted product tanker rates so much more than crude tanker rates — given that crude inventories are also historically low — Chappell responded, “Usually the two groups are highly correlated, and usually crude leads and outperforms by measure of magnitude. But we are far from normal times.

“Crude tankers are doing really well in regions directly impacted by Russia’s invasion of Ukraine — the Black Sea, Baltic and the Med — owing to the higher insurance costs and risks of entering those markets. But overall, the crude markets have been balancing new longer trade routes with the inability of OPEC to meet quotas, Russia [being] offline, and China lockdowns. The market is better than it probably should be based on those latter factors, but the low inventories and longer ton-miles [voyage distances] are offsetting some of the macro headwinds.

“Product tankers are benefiting from localized diesel shortages, high refinery margins … and massive trading arbs [arbitrages] that allow traders to pay much higher freight costs and still make a ton on the arb. Inventories are far too low globally and prices will likely remain elevated, forcing more trading in unusual trade lanes, tightening capacity and lifting that market well before and well above crude.

“Eventually crude tankers will catch up, I think, if supply of crude can meet higher refinery demand. But right now, it’s a unique product story. And talking with my oil analyst, it’s hard to see how these diesel shortages ease or the strong tanker markets end,” said Chappell.

Earnings recap

Among the universe of listed shipowners, Clarksons Platou Securities said that “product tankers are sailing up as the winning sector year to date.” Rates are surging on “exploding refining margins,” said Clarksons. It maintained that “the products sector looks primed to gain further.”

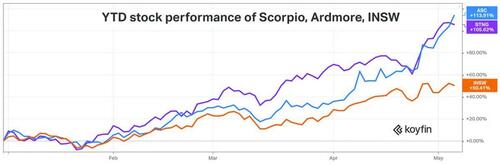

Through Thursday’s close, the stocks of Scorpio Tankers and Ardmore Shipping were up 106% and 114% year to date, respectively. Shares of International Seaways — which owns both crude and product tankers — were up 50% year to date.

Listed product tanker owners have just reported more losses for the first quarter. The rate upswing won’t be fully felt until the current quarter.

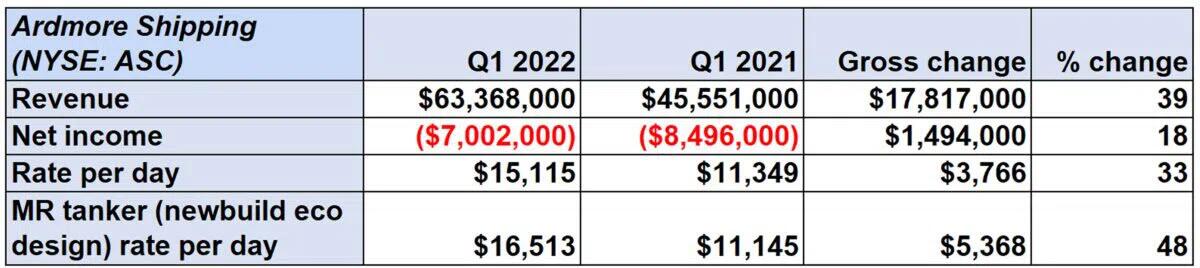

Ardmore Shipping reported a net loss of $7 million for Q1 2022 versus a net loss of $8.5 million in Q1 2021. The adjusted loss of 4 cents per share beat consensus expectations for a loss of 8 cents.

Ardmore has 50% of its Q2 2022 available MR spot days booked at $25,500 per day. That compares to rates of $16,513 per day in Q1 2022.

International Seaways reported a net loss of $13 million for Q1 2022 compared to a net loss of $13.4 million in the same period last year. The adjusted loss of 29 cents per share was slightly better than Wall Street expectations for a loss of 30 cents.

The company has 41% of its available Q2 2022 MR spot days booked at an average of $24,500 per day. That compares to $14,030 per day in the first quarter.

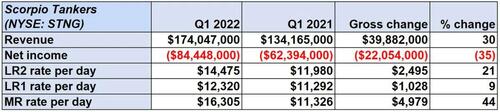

Scorpio Tankers reported a net loss of $84.4 million for Q1 2022 compared to a net loss of $62.4 million in Q1 2021. The adjusted loss per share of 27 cents came in much better than the consensus forecast for a loss of 58 cents.

Scorpio has 42% of its available Q2 2022 spot MR days booked at $30,000 per day. Its MR fleet earned an average of $16,305 per day in the first quarter.

END.

end

COMMODITIES IN GENERAL//

END

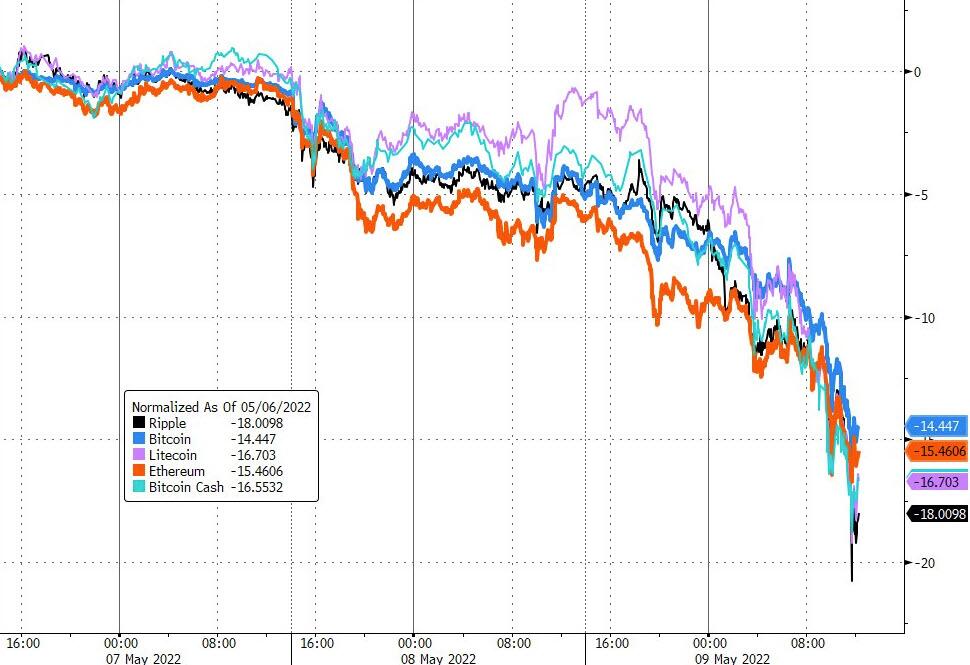

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7281

OFFSHORE YUAN: 6.7699

HANG SANG CLOSED

2. Nikkei closed DOWN 684.22 OR 2.53%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 103.84/Euro RISES TO 1.0539

3b Japan 10 YR bond yield: RISES TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 131.09/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +1.175%/Italian 10 Yr bond yield RISES to 3.22% /SPAIN 10 YR BOND YIELD RISES TO 2.29%…

3i Greek 10 year bond yield RISES TO 3.66

3j Gold at $1860.00 silver at: 21.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 roubles/dollar; ROUBLE AT 69.24

3m oil into the 107 dollar handle for WTI and 109 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 131.09 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9924– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0460well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

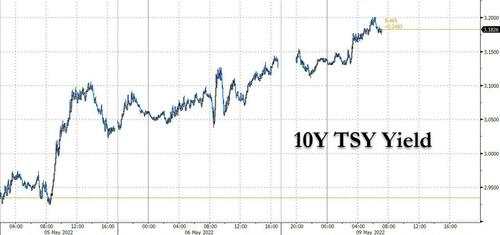

USA 10 YR BOND YIELD: 3.175 UP 5 BASIS PTS

USA 30 YR BOND YIELD: 3.284 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.03

Bloodbath: Futures, Yuan Tumble as 10Y Yields Soar On Global Stagflation Fears

MONDAY, MAY 09, 2022 – 07:50 AM

It’s a bloodbath.

With Bank of America conveniently reminding us over the weekend that markets never bottom on a Friday, and that Mondays tend to be the worst day of the week for markets…

… that’s exactly what is playing out today as risk assets are puking across the globe, with S&P 500 futures crashing, the Chinese yuan tumbling amid a growing slowdown in China, and the US 10-year Treasury yield climbing as high as 3.2% as risk parity funds are getting monkeyhammered… again.

A slide in US stock futures set up Wall Street’s main indexes to extend weeks of declines on concerns of a recession amid monetary tightening and surging inflation. Contracts on the S&P 500 fell 2.1% as of 7:15 a.m. in New York, trading at session lows, as the MSCI gauge of world stocks extended its retreat from a November peak to 16% as a wave of risk aversion continues to sweep through global markets after Friday’s U.S. jobs data left little room for a change of course in the Fed’s rate-increase and quantitative-tightening plans. Sentiment took a further knock over the weekend as Chinese Premier Li Keqiang warned the nation’s employment situation had turned grave because of Covid restrictions. The greenback extended a two-year high, rising on Monday against all of its major peers. Oil declined more than 2.5% as concern over slowing demand in Asia outweighed a Group-of-Seven pledge to ban Russian oil. Most Treasuries fell, with the five-year rate briefly jumping to the highest since 2008.

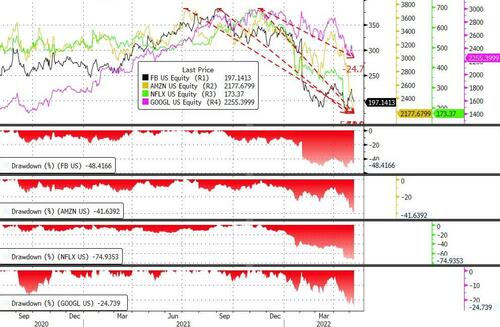

Nasdaq 100 futures slipped 2.5%, putting the tech-heavy index on course to extend its six-week streak of declines, with major tech stocks again down in premarket trading after Apple and Amazon.com closed lower for six straight weeks as the Federal Reserve tightens policies to fight inflation amid a spate of disappointing earnings and weak forecasts. The tech sector also remains pressured by rising bond yields and concerns over an economic slowdown. Apple fell as much as 2.6% premarket, after closing down to record its longest declining streak since November 2018. Amazon was 2.7% lower premarket, after closing at its lowest level in more than 2 years. Microsoft -2.5%, Alphabet -2.7%, Meta Platforms -2.6%, Netflix -2.5% and Nvidia -3% premarket.

- In other notable premarket moves, Rivian Automotive tumbled as much as 9.6% after a media report that Ford was selling 8 million shares in the electric-pickup maker at a discount.

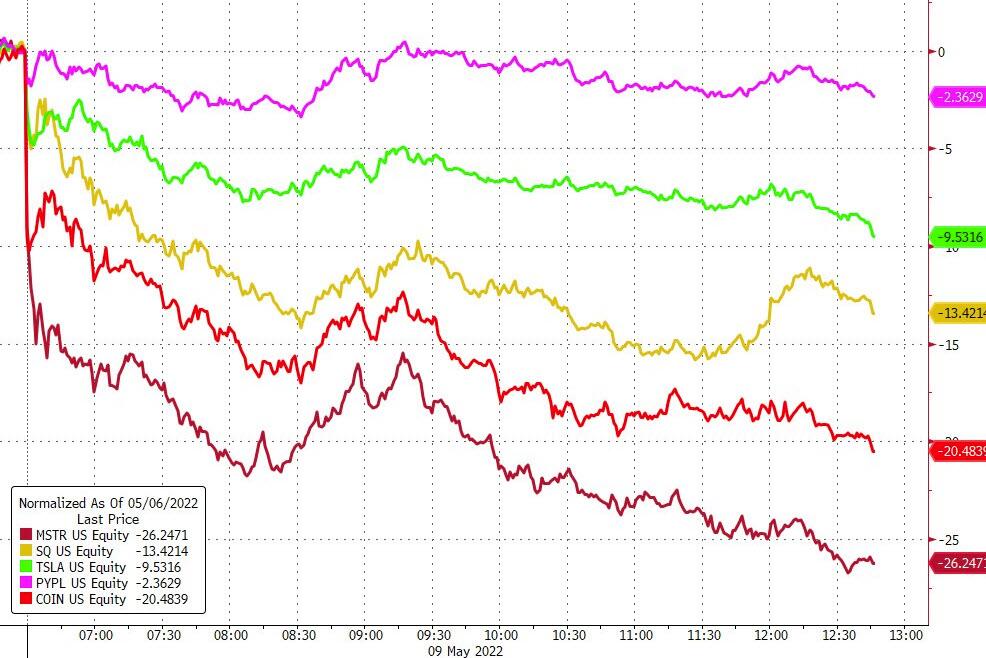

- Cryptocurrency-exposed shares decline as Bitcoin is falling toward levels last seen in July 2021, part of a wider retreat in digital tokens. Riot Blockchain (RIOT US) -6.1%, Marathon Digital (MARA US) -6.3%, MicroStrategy (MSTR US) -4.8%.

- Uber (UBER US) shares down 4% in U.S. premarket trading as CEO Dara Khosrowshahi says company has made progress in terms of profitability but the goal posts have changed and now it’s about free cash flow and getting there fast, CNBC reports, citing an email to staff on May 8.

- Faraday Future (FFIE US) shares rose 9.3% in premarket trading on Monday after the Special Committee completed its previously announced review.

- Rivian (RIVN US) falls as much as 9.6% in U.S. premarket trading as a post-IPO lockup on the stock expires, while CNBC reported Ford and another investor are looking to sell shares in the electric-pickup maker at a discount..

- Prestige Consumer Healthcare (PBH US) upgraded to outperform from perform at Oppenheimer, which says the over-the- counter medications maker looks attractively valued after a recent pullback in its shares and .

- Zanite (ZNTE US) shares climb 13% in U.S. premarket after its shareholders approved the business combination with Embraer’s urban air mobility subsidiary.

- Southwest Gas (SWX US) shares could be active management after activist investor Carl Icahn reached a deal with the utility owner at the weekend to oust its CEO and name up to four directors to its board.

The S&P 500 capped its fifth week of declines on Friday, its longest losing streak since June 2011, as initial optimism following the Federal Reserve’s meeting faded. Growth-linked and technology stocks continue to be under pressure with the yield on U.S. five-year Treasury notes hitting the highest level since September 2008 as investors fear higher yields will threaten future earnings growth.

Not helping matters is the continued surge in benchmark 10Y yields which rose to 3.20% this morning and are just a few basis points away from taking out their November 2018 highs of 3.24%.

The Nasdaq 100 Index is down 22% this year, one of the worst performers among global gauges, despite a brief relief rally last week as Fed Chair Jerome Powell quelled fears of a 75-basis point rate hike.

“Lots of Fed watchers, both professional and amateur, have opined that Powell is delusional because the only way to bring inflation down is to cause a recession,” Ed Yardeni, president of Yardeni Research Inc., wrote in a note. “Of course, this crowd remains very bearish on both bonds and stocks.”

Strict lockdowns in China to curb the coronavirus have also been weighing on investor appetite. Chinese Premier Li Keqiang warned over the weekend of a “complicated and grave” employment situation as Beijing and Shanghai tightened curbs in the country’s most important cities. Goldman Sachs Group Inc. strategists, including David Kostin, said the outlook for U.S. stocks isn’t particularly bright, even if an outright recession is avoided.

The short-term outlook for stocks “is still messy and there may be more downside as markets worry about a significant economic slowdown or ‘hard landing’ and aggressive interest-rate hikes,” Diana Mousina, senior economist at AMP Investments, wrote in a note.

In Europe, the Stoxx 600 fell 2.1% with with miners, travel and real estate the worst-performing sectors. 524 Stoxx 600 members were down, and just 59 up. Here are some of the biggest European movers today:

- BBVA shares rise as much as 2.3% as Deutsche Bank upgrades the stock to buy from hold, noting that the Spanish lender’s performance remains robust in most units.

- EuroAPI gains as much as 7.5% as JPMorgan initiates coverage with an overweight rating, calling the Sanofi spinoff a “transformation story with significant upside”

- Ideagen surges as much as 47% after the software company agrees to be acquired by funds managed by Hg Pooled Management for 350p/share in cash.

- NCC Group shares rise as much as 1.6% to outperform a falling tech sector after the company says sales in 2H will be substantially higher than 1H.

- Solutions 30 shares rise as much as 4.1% after BNP Paribas Exane resumes coverage with an outperform rating, citing new profitable growth cycle and a potential buyout.

- Miners’ shares underperform the broader equity gauge in Europe as iron ore and copper decline after weak Chinese property data and a jobs warning from Premier Li Keqiang.

- Rio Tinto falls as much as 4.5%, Anglo American -4.2%, Glencore -5.4%, ArcelorMittal -5%, SSAB -6%

- Crypto-exposed shares decline as Bitcoin falls toward levels last seen in July 2021, part of a wider retreat in digital tokens

- Argo Blockchain -12%, Safello -6.8%, Northern Data -9.4% and On-Line Blockchain -10%

- Grifols falls as much as 9%, giving back all of Friday’s gains that were fueled by 1Q earnings from the Spanish maker of pharmaceutical products.

- Rightmove drops as much as 7.2% after the company said its chief executive officer Peter Brooks-Johnson will step down in 2023.

In the latest Russia-related developments, the G7 most-industrialized countries pledged to ban the import of Russian oil. The European Union is working on a similar plan but Hungary remains a holdout and the bloc’s talks are set to continue.

Earlier in the session, Asian stocks headed for a sixth day of declines as investors shunned risk assets fretting over the economic fallout from China’s lockdowns, rising global inflation and higher U.S. interest rates. The MSCI Asia Pacific Index slid as much as 1.8% in a broad rout that saw all major country benchmarks in the red, led by Indonesia. Materials and industrials were the worst-performing index groups, while tech names like TSMC and Sony were among the biggest drags in terms of individual stocks. A stronger dollar added to woes for Asian investors, who have already seen rising input costs and supply chain disruptions eating into company profits. The MSCI Asia gauge is down more than 17% this year and at its lowest levels since July 2020. Traders are keenly awaiting the U.S. consumer inflation data due Wednesday, given its implications for the Federal Reserve’s policy. “We are not getting any reprieve” as markets are possibly pricing peak Fed hawkishness and uncertainty from China’s lockdowns and the Russia-Ukraine war, Stefanie Holtze-Jen, Asia-Pacific chief investment officer at Deutsche Bank International Private Bank. told Bloomberg Television. Indonesia’s equity benchmark plunged 4.4% as the market reopened after a week-long holiday. Japan’s Nikkei 225 lost more than 2.5% as Prime Minister Fumio Kishida joined other G-7 leaders to impose a ban on crude over the Kremlin’s invasion of Ukraine. Chinese stocks edged lower — though faring better than the Asian benchmark index — after Premier Li Keqiang warned of a grave employment situation over the weekend amid shutdowns in Beijing and Shanghai. Hong Kong was closed for a holiday, as was the Philippines where a presidential election is under way.

In rates, the Treasuries curve continued to aggressively steepen with front-end yields richer on the day while long-end cheapens by up to 7bp and global stocks falling after Chinese Premier Li’s jobs warning. Treasuries curve steeper with 2s10s, 5s30s spreads wider by ~10bp and ~6bp on the day; on outright basis 2-year yields are richer by 4bp while 10s are at 3.18%, cheaper by 5.5bp but outperforming gilts ~by 2.5bp U.S. session has few scheduled events, although this week’s Treasury auctions and expected busy issuance slate could keep yields moving higher. Dollar issuance slate empty; some desks are expecting a busy week with as much as $40b in new deals coming if market conditions allow. Three-month dollar Libor -0.33bp at 1.39857%.

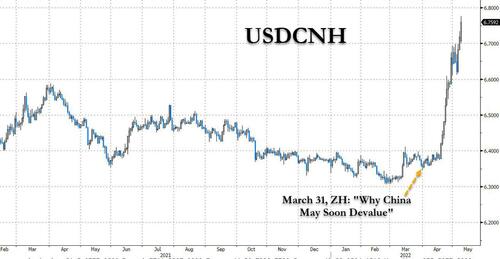

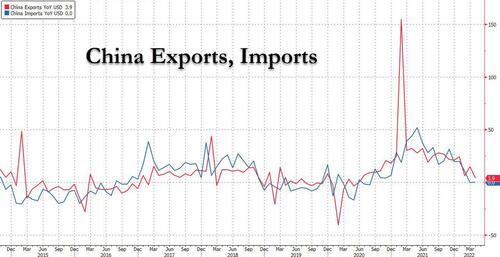

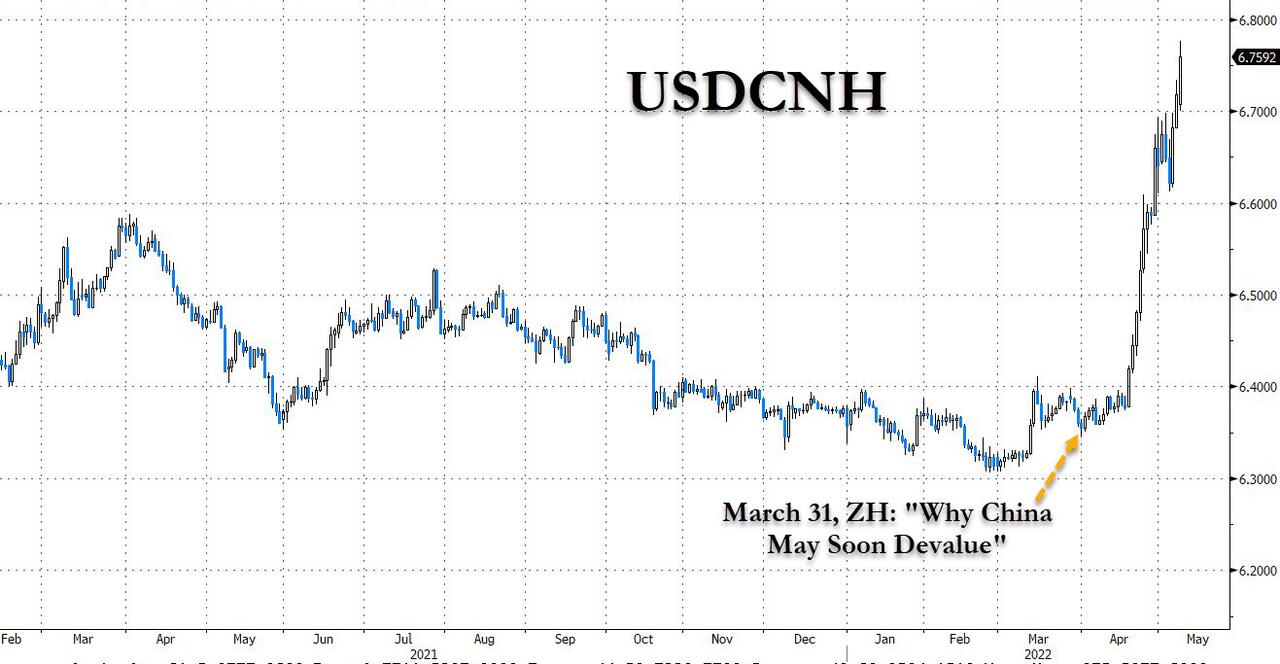

In FX, the big mover was the China yuan, whose selloff accelerated after breaking 6.7 per dollar for the first time since 2020, as Chinese exports grew at their slowest pace in nearly two years and amid the absence of support from state banks. The USDCNY rose as much as 1% to 6.7321, the highest since November 2020; USD/CNH jumps 0.9% to 6.7763.

Export growth in April slowed to 3.9% in dollar terms from a year earlier, compared to an increase in March of 14.7%. That’s the weakest pace since June 2020 but faster than the median estimate of a 2.7% gain in a Bloomberg survey of economists

Despite demand from some exporters, it was not enough to stop yuan from weakening, according to three traders who requested anonymity discussing confidential matters. The lack of notable dollar selling from state-owned banks also weighs on sentiment, they added.

Elsewhere in FX, Australia’s currency fell below 70 U.S. cents for the first time since January, and India’s rupee hit a record low against the dollar, with the central bank said to be intervening to defend the currency. The dollar rose against all of its Group-of-10 peers, with the Bloomberg Dollar Spot Index trading at its highest level in two years. China’s export growth in April in dollar terms slowed to 3.9% from a year earlier, compared to an increase in March of 14.7%, customs data showed Monday. That’s the weakest pace since June 2020 but faster than the median estimate of a 2.7% gain in a Bloomberg survey of economists. The Japanese yen fell to a fresh 20-year low against the dollar; USD/JPY rose as much as 0.6% to 131.35.

Bitcoin came under noted pressure over the weekend and has continued to decline during the European session, dropping to a low just above the USD 33k mark.

In commodities, oil fell, surrendering half of last week’s gains. Crude is being buffeted by the demand hit from China’s outbreak and supply risks linked to Russia’s war in Ukraine. WTI trades within Friday’s range, falling 1.1% to around $108. Spot gold falls roughly $18 to trade above $1,865/oz. Most base metals are in the red with much of the complex down over 2% on LME.

Looking at today’s calendar we get US March wholesale trade sales. Simon property group, BioNTech, Infineon, Palantir, AMC are among the companies reporting earnings.

Market Snapshot

- S&P 500 futures down 1.4% to 4,061.75

- MXAP down 1.7% to 161.32

- MXAPJ down 1.4% to 529.60

- Nikkei down 2.5% to 26,319.34

- Topix down 2.0% to 1,878.39

- Hang Seng Index down 3.8% to 20,001.96

- Shanghai Composite little changed at 3,004.14

- Sensex down 0.8% to 54,395.62

- Australia S&P/ASX 200 down 1.2% to 7,120.65

- Kospi down 1.3% to 2,610.81

- STOXX Europe 600 down 1.3% to 424.33

- German 10Y yield little changed at 1.14%

- Euro down 0.4% to $1.0512

- Brent Futures down 0.8% to $111.50/bbl

- Gold spot down 0.8% to $1,869.61

- U.S. Dollar Index up 0.35% to 104.03

Top Overnight News from Bloomberg

- Russian President Vladimir Putin justified his faltering 10-week- old invasion of Ukraine as a battle comparable to the fight against Nazi Germany

- Leaders of the Group of Seven most industrialized countries pledged to ban the import of Russian oil in response to President Vladimir Putin’s war in Ukraine

- Hungary continued to block a European Union proposal that would ban Russian oil imports, holding up the bloc’s entire package of sanctions meant to target President Vladimir Putin over his war in Ukraine, according to people familiar with the talks

- Saudi Arabia cut oil prices for buyers in Asia as coronavirus lockdowns in China weigh on demand, countering uncertainty around Russia’s supplies as the Ukraine war drags on

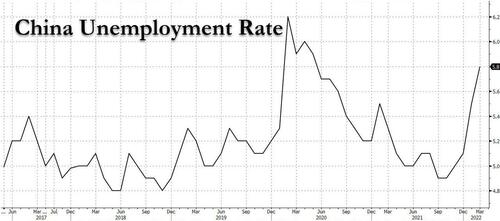

- Chinese Premier Li Keqiang warned of a “complicated and grave” employment situation as Beijing and Shanghai tightened curbs on residents in a bid to contain Covid outbreaks in the country’s most important cities

- Bill Gates said interest rates are likely to rise enough to cause a global economic slowdown, triggered by Russia’s invasion of Ukraine and fallout from the Covid-19 pandemic

- The European Central Bank should start raising borrowing costs in July to prevent inflation expectations becoming de- anchored, said Governing Council member Olli Rehn.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks declined amid recent upside in yields and as participants digested a slowdown in Chinese trade data. ASX 200 was dragged lower amid underperformance in the real estate and tech sectors. Nikkei 225 underperformed with a weaker currency and higher than expected wages doing little to offset the losses. Shanghai Comp was indecisive with initial pressure seen after reports of tighter COVID controls in China’s two largest cities and as Hong Kong remained closed for holiday, while the latest Chinese trade data was mostly better than expected but showed a significant slowdown in Exports amid the ongoing COVID-19 woes and curbs.

Top Asian News

- China’s Imports From Russia Hit Record on Energy Price Rises

- BP to Buy Stake in $36 Billion Hydrogen Hub, Australian Says

- Miners Fall With Iron Ore and Metals on China Property Fears

- Thailand Sees Foreign Arrivals Jumping to 1m a Month

European bourses are lower across the board, Euro Stoxx 50 -1.4%, in a continuation of the APAC handover amid multiple fundamental narratives. Stateside, US futures are similarly hindered, ES -1.7%, with the NQ marginally lagging given yield upside; Fed speak remains in focus and inflation metrics are due for the region and China later in the week. European sectors feature Tech underperforming given yields and following Infineon earnings in-spite of them raising guidance again, defensive names are the relative outperformers.

Top European News

- European Gas Drops as Russia Tries to Calm Clients Over Payments

- BBVA Gains as Deutsche Bank Upgrades on Robust Performance

- Siemens Breakup Would Reap $60 Billion in Value: Bernstein

- Cost of Default Hedges in Europe Tops Level Last Seen in 2020

FX

- Buck continues bull run on combination of risk, further upside in Treasury yields and curve steepening plus other positive factors. DXY extends beyond 104.000 to test or take out multiple technical, key and psychological levels.

- Aussie and Kiwi underperform as high beta and commodity currencies, AUD/USD probes 0.7000 and NZD/USD hovers around 0.6350.

- Franc and Yen suffering more adverse consequences of carry; USD/CHF approached 0.9950 and USD/JPY climbs to new YTD high of circa. 131.35.

- Pound politically challenged after UK local elections and Sinn Fein success at Northern Ireland assembly, Cable under 1.2300 and closer to June 2020 base at 1.2252.

- Euro soft awaiting further talks on Russian oil embargo and following worse than forecast Eurozone Sentix index, EUR/USD in low 1.0500 area and briefly under.

- Loonie undermined by pullback in crude ahead of Canadian building permits, USD/CAD hits 1.2950 before paring back a bit.

- Yuan slides after mixed Chinese trade data and tighter COVID restrictions in two largest cities, USD/CNY settles above 6.7200 and USD/CNH over chart resistance towards 6.7800.

Fixed income

- Bonds whippy and multi-directional with Bunds holding above par within 151.37-150.75 range, but Gilts and 10 year T-note mostly softer between 117.64-14 and 117-27/11 parameters.

- BTPs also weak awaiting mid-month Italian auction details.

- UST curve steeper before Quarterly Refunding and CPI data.

- UK debt eyeing a speech from one hawkish BoE dissenter as Saunders is scheduled later.

Commodities

- WTI and Brent are pressured amid broader risk sentiment though Russian President Putin’s Victory Day speech was relatively uneventful.

- Currently, the benchmarks are lower by around USD 2.00/bbl; familiar catalysts incl. China-COVID, EU Russian oil import embargo, remain in focus among other drivers.

- Saudi Arabia lowered June Arab light oil prices to Asia to a premium of USD 4.40/bbl vs Oman/Dubai from a premium of USD 9.35/bbl, while it lowered the price to Europe to a premium of USD 2.10/bbl vs ICE brent from a premium of USD 4.60/bbl and kept the price premium to the US at USD 5.65/bbl vs ASCI, according to Reuters.

- Saudi Energy Minister says the difference between crude prices and fuel mobility prices is around 60% due to refining capacity, via Reuters.

- Russian Deputy PM Novak says Russian oil output was up in early May vs April; situation with Russian oil has stabilised, via Ria; considering expanding capacity of oil-exporting ports.

- Spot gold is hindered amid USD and yield dynamics, moving further away from the 100DMA

DB’s Jim Reid concludes the overnight wrap

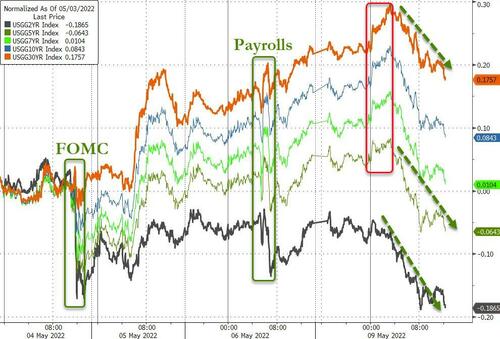

Last week was another tough one for risk parity or 60/40 type strategies as equities and bonds fell around the world. The S&P 500 was actually one of the outperformers and ‘only’ fell -0.21% but this still made it the fifth successive weekly decline – the worse run since 2011. Meanwhile 10yr US yields were up +19.9bps, most of it after the Fed. The relatively small move in US equities masked huge volatility though and losses in both assets intensified as the dust settled after the “dovish” Fed where they effectively ruled out 75bps hikes in the foreseeable future. I spent some time over the weekend (whilst twiddling my thumbs at a 5 year old’s birthday party) trying to work out whether markets would have been calmer or even worse had the Fed kept 75bps firmly on the table. How did I conclude this epic debate with myself? Well I ended up having no idea. Sticking to 50bps increments over the next couple of meetings provides a level of perceived control and shows no panic whilst 75bps suggests a level of panic but if inflation is as sticky as we expect it to be, it might ultimately be the best thing to do medium term. Regardless of this debate, it’s fairly obvious that the “Fed Put” is going to be difficult to rely on for this cycle.

We won’t have to wait too long for the next blockbuster event to help shape the debate as US CPI on Wednesday takes center stage this week with PPI the following day. There are lots of Fed speakers too to put some nuance to last week’s FOMC announcement. Outside of this geopolitics will be key. Today marks the annual “Victory Day” in Russia where there will be a parade and a speech from Putin. It’s anyone’s guess what tone the President will take in this landmark speech but it could shape the next phase of the war. Staying with geopolitics, Finland may decide whether to apply for NATO membership this week and Sweden is due to publish its security policy assessment before Friday.

We will also get a pulse check on economic sentiment in May from the ZEW survey for the Eurozone and Germany (tomorrow) and, for the US, the University of Michigan survey on Friday. China inflation data on Wednesday will be interesting. In an otherwise quiet week for economic data, the UK will be an exception with a data-packed Thursday. It will be a slow week for corporate earnings too now as the bulk of US/European companies have reported and we will instead focus on Japan’s corporate giants. As well as Fed speakers there are a number of ECB equivalents, with all comments pertaining to a possible July hike watched out for.

In terms of US CPI midweek, DB’s US economists are expecting a +7.9% reading, down from the four-decade-high 8.5% print in March, not least due to base effects. From here it should all be about the pace of the declines as things like the extreme YoY prices in used cars roll out of the data. However on the other side it is important to see how prolonged the rise in rents are. Remember that rents make up a third of the CPI basket and 40% of core. Used cars only make up a few percentage points. A reminder that the day by day calendar of events is at the end as usual.

Just a few words on earnings with around 90% and 75% having reported in the US and Europe. According to our equity strategist Binky Chadha (report link here), the season has been pretty strong, especially in Europe which benefits from a better sector mix (eg Energy and Materials concentration and limited Tech which held the US back). One consistent theme in both regions is that margins remained strong suggesting that firms are for now still able to pass on inflationary pressures. On the macro front this makes it harder for the rate of inflation to fall sharply as price rises are being embedded into the economies for now. It won’t last forever as excess savings/liquidity will be run down but seems to be holding for now.

Asian stock markets opened sharply lower this morning following the broadly negative cues from Wall Street on Friday along with the ongoing impact of China’s Covid lockdown policies. The Nikkei (-2.08%) is leading losses across the region with the Kospi (-0.96%) also trading in negative territory. Mainland Chinese stocks are showing a mixed performance with the Shanghai Composite (+0.08%) marginally higher while the CSI (-0.65%) is moving lower after the release of China’s trade data. China’s exports grew +3.9% y/y in April, exceeding market estimates of a +2.7% increase but slowing from a +14.7% growth recorded in the preceding month. Meanwhile, the nation’s trade surplus increased less than expected to +$51.12bn in April (v/s +$53.45bn Bloomberg estimates). It followed a surplus of +$47.38bn in March. Elsewhere, markets in Hong Kong are closed today for a holiday. Outside of Asia, equity futures in the US point to further losses with contracts on the S&P 500 (-0.97%) and NASDAQ 100 (-0.79%) in the red. 10-yr USTs are around +1bps higher at 3.136% as I type with the 2s10s +2bps higher and above +40bps again.

In other economic news, real wages in Japan shrank -0.2% y/y in March, its first decline since December but compared to market estimates of a -0.6% drop. Meanwhile, the nominal cash earnings increased +1.2% y/y in March as against the same rate in February and compared to market expectations of a +0.9% gain.

Overnight, G7 nations committed to ban or phase out imports of Russian oil with the US unveiling sanctions against Gazprombank executives and other businesses as part of a new package of sanctions designed to further punish Moscow for its war in Ukraine.

A quick rewind to last week now. A few major central bank decisions injected yet more cross-asset volatility into markets. First, the Fed hiked rates by +50bps for the first time in two decades, announced the beginning of its balance sheet rundown, and seemingly ruled out hikes of larger magnitude in the near-term. Then, the BoE hiked Bank Rate by +25bps, coupled with 3 dissenting opinions who favoured a larger hike, and 2 members who wanted to signal no more hikes were forthcoming. They’re also starting to consider gilt sales, and released a forecast that show UK growth tipping negative next year. Adding the to mix, the RBA hiked their policy benchmark +25bps as well.

All told, 10yr Treasuries gained +17.9bps (+2.1bps Friday) concentrated all in real yields which climbed +27.7bps (+5.3bps) as the market appeared to start coming around to our view that the Fed has much more tightening to do. 10yr bunds were +17.3bps (+6.4bps Friday) higher, while Gilts picked up +6.5bps (+0.7bps Friday). Italian spreads widened all week to bunds, with 10yr BTPs increasing +36.2bps (+9.7bps Friday), to reach a spread of 200bps over bunds, their widest since June 2020. Money markets closed the week pricing year-end policy rates of 2.83% for the Fed, 0.33% for the ECB, and 2.16% for the UK. That marked a decline in the UK, so the 2s10s gilts curve climbed +14.7bps (+4.5bps Friday). Not to be outdone, the 2s10s Treasury curve also steepened with the aggressive back end sell off, climbing +17.7bps (+3.2bps Friday).

The S&P 500 managed its fifth weekly loss in a row for the first time since 2011, falling -0.21% (-0.57% Friday), after a particularly wild ride following the FOMC. Tech and mega cap shares fared even worse given the selloff in duration, with the Nasdaq falling -1.54% (-1.40% Friday) and the FANG+ down -2.21% (-2.02% Friday). The Vix closed the week above 30 at 30.19 given the renewed volatility. European shares fared worse (partly catch up to a weak US close the previous week), as the Stoxx 600 fell -4.55% over the week (-1.91% Friday), with the DAX moving -2.73% (-1.36% Friday) lower, and the CAC falling -4.06% (-1.57% Friday).

EU President Von der Leyen’s proposed gradual ban of Russian oil imports drove brent futures +3.55% higher over the week (+1.34% Friday) to $112.39/bbl. This morning, oil prices maintained their upward trajectory with Brent futures +0.16% higher as I go to press.

Finally, on data Friday, the American economy added +428k jobs to nonfarm payrolls in April, a little ahead of consensus forecasts, while the unemployment rate remained stable at +3.6%. Average hourly earnings decelerated slightly to +0.3% on a month-over-month basis.

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT