May 12, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

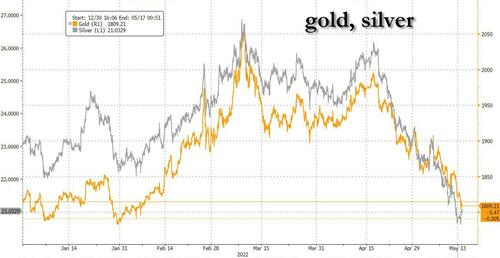

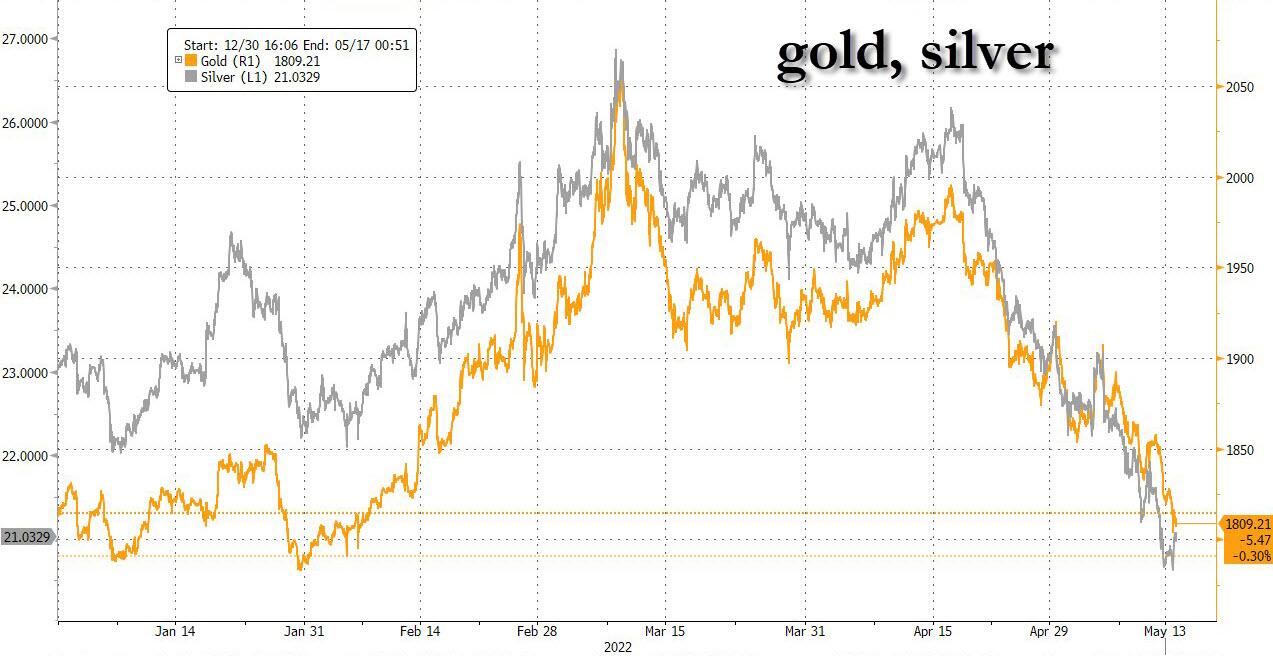

GOLD; $1809.50 DOWN $16.25

SILVER: $20.99 UP $.31

ACCESS MARKET: GOLD $1809.90

SILVER: $21.04

Bitcoin morning price: $30,399 UP 1718

Bitcoin: afternoon price: $30,147 up 1466

Platinum price: closing DOWN $4.10 to $943.60

Palladium price; closing UP $25/70 at $1936.15

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices percentage of JPMorgan notices filed: 83/100

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,823.800000000 USD

INTENT DATE: 05/12/2022 DELIVERY DATE: 05/16/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 100

657 C MORGAN STANLEY 9

657 H MORGAN STANLEY 3

661 C JP MORGAN 83

685 C RJ OBRIEN 1

905 C ADM 4

TOTAL: 100 100

MONTH TO DATE: 5,376

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 100 NOTICE(S) FOR 10,000 OZ (0.31104 TONNES)

total notices so far: 5376 contracts for 537,600. oz (16.7216 tonnes)

SILVER NOTICES:

36 NOTICE(S) FILED 180,000 OZ/

total number of notices filed so far this month 4854 : for 24,295,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $16.25

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.80 TONNES FROM THE GLD

INVENTORY RESTS AT 1060.82 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 31 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://NO CHANGE IN SILVER INVENTORY

AT THE SLV.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 570.439 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 4116 CONTRACTS TO 145,862 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.88 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.88) AND WERE UNSUCCESSFUL IN KNOCKING OUT ANY SILVER LONGS AS WE HAD A HUMONGOUS GAIN OF 6101 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 80,000 OZ E.F.P. JUMP TO LONDON //NEW STANDING 27.840 MILLION OZ/ // V) HUGE SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : 3173

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 9 days, total 14,314, contracts: 71.570 million oz OR 7.952 MILLION OZ PER DAY. (1591CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 71.570 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 71.570 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 943 DESPITE OUR $0.88 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1985 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 80,000 OZ E.F.P. JUMP //NEW STANDING 27.840 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 2928 OI CONTRACTS ON THE TWO EXCHANGES FOR 30.505 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 36 NOTICE FILED TODAY FOR 180,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1618 CONTRACTS TO 573,045 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –7810 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED LOSS IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $26.50//COMEX GOLD TRADING/THURSDAY /.AS IN SILVER WE MUST HAD HUGE BANKER/ALGO SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 8400 OZ//NEW STANDING 16.824 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $26.50 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A VERY STRONG SIZED GAIN OF 8268 OI CONTRACTS (25.716 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2076 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 573,045.

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 458, WITH 1618 CONTRACTS DECREASED AT THE COMEX AND 2076 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 458 CONTRACTS OR 1.424 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2076) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1618,): TOTAL GAIN IN THE TWO EXCHANGES 458 CONTRACTS. WE NO DOUBT HAD 1) HUGE BANKER SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 8400 OZ//NEW STANDING 16.824 /// 3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

40,363 CONTRACTS OR 4,036,300 OR 125.5 TONNES 9 TRADING DAY(S) AND THUS AVERAGING: 4484 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 1 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 125.5/3550 x 100% TONNES 3.54% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 125.5 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 943 CONTRACT OI TO 142,689 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1985 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1985 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4943 CONTRACTS AND ADD TO THE 1985 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF 2928 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 14.660 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.88 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 29.29 PTS OR 0.69% //Hang Sang CLOSED UP 518.43 PTS OR 2.67% /The Nikkei closed UP 678.93 OR 2.64% //Australia’s all ordinaires CLOSED UP 1.97% /Chinese yuan (ONSHORE) closed UP 6,7882 /Oil UP TO 107.57 dollars per barrel for WTI and down TO 109.05 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7882 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8088: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

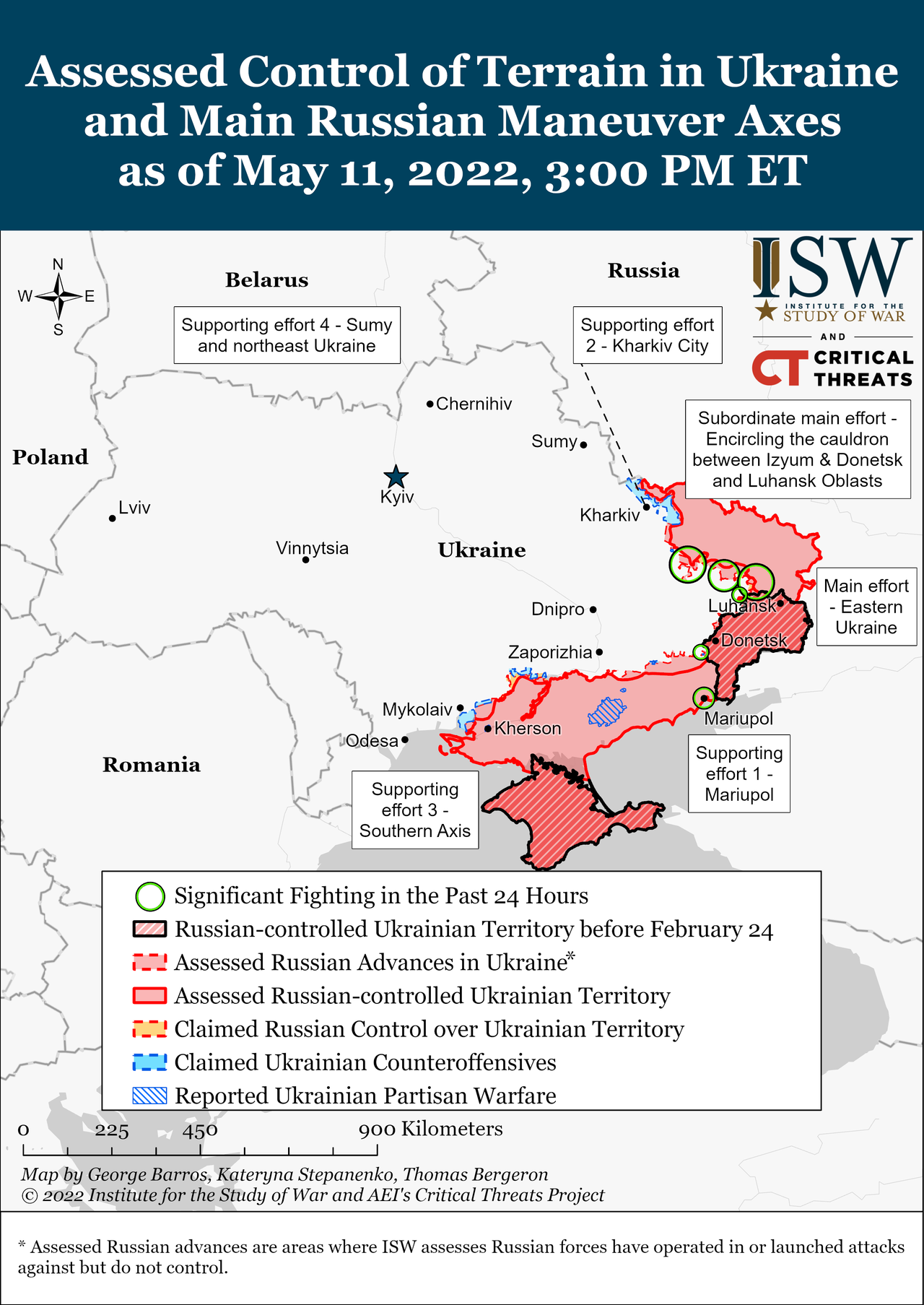

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1618 CONTRACTS TO 573,045 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR STRONG LOSS OF $26.50 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2076 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH.

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2076 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2076 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2076 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY SMALL SIZED TOTAL OF 458 CONTRACTS IN THAT 2076 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD AN GOOD SIZED COMEX OI LOSS OF 1618 CONTRACTS..AND YET THIS GAIN OCCURRED WITH OUR LOSS IN PRICE OF GOLD $26.50. MAKES NO SENSE!! THIS IS HAPPENING FAR SO OFTEN!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (15.569),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 16.824 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $26.50) BUT WERE UNSUCCESSFUL IN FLEECING ANY LONGS// AS WE HAVE REGISTERED A VERY SMALL SIZED GAIN OF 1/424 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (16.824 TONNES)…

WE HAD 7810 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 458 CONTRACTS OR 45800 OZ OR 1.424

TONNES

Estimated gold volume today: 185,998/// poor

Confirmed volume yesterday:332,691 contracts good

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 32,568.960 oz Brinks |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 20,956.105 oz Delaware Loomis |

| No of oz served (contracts) today | 100 notice(s)10000 OZ 0.31104 TONNES |

| No of oz to be served (notices) | 33 contracts 3300 oz 0.1026 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5376 notices 537,600 OZ 16.7216 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

2 customer deposits

i) Into Delaware 977.955 oz

ii) Into Loomis: 19,978.150 oz

1 customer withdrawals:

i) Out of Brinks: 32,568,960 oz

total withdrawal: 32,568.960 oz

ADJUSTMENTS: a) Brinks//dealer to customer 90,762.273 oz

b) customer to dealer: JPmorgan 64,237.693 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 133 contracts having LOST 1107 contracts

We had 1191 notices filed on Wednesday, so we gained 84 contracts or AN ADDITIONAL 8400 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 26,762 contracts down to 276,409 contracts

July has a LOSS OF 2 OI to stand at 176

August has a gain of 25,140 contracts up to 239,047 contracts

We had 100 notice(s) filed today for 100 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 100 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 183 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (5376) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 133 CONTRACTS ) minus the number of notices served upon today 100 x 100 oz per contract equals 540,900 OZ OR 16.824 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (5376) x 100 oz+ (133) OI for the front month minus the number of notices served upon today (100} x 100 oz} which equals 540900 oz standing OR 16.824 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 16.824 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,026,795.134 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,977,798.829 OZ

TOTAL ELIGIBLE GOLD: 18,163,084.651 OZ

TOTAL OF ALL REGISTERED GOLD: 17,814,714.149 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,787,919.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 13

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 612,484.145 oz Brinks CNT Manfra Delaware JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,357,785.655 oz CNT Delaware JPMorgan |

| No of oz served today (contracts) | 36CONTRACT(S) 180,000 OZ) |

| No of oz to be served (notices) | 709 contracts (3,545,000 oz) |

| Total monthly oz silver served (contracts) | 4859 contracts 24,295,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

we had 0 deposit into the dealer

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

i) Into CNT: 562,586.281 oz

ii) Into Delaware; 212,005.875 oz

iii) IntoJPMorgan: 583,198.500 oz

total deposit: 1,357,785.685 oz

JPMorgan has a total silver weight: 177.434 million oz/338.782 million =52.37% of comex

Comex withdrawals: 5

i) Out of JPMorgan 174,600.250 oz

ii) Out of Brinks: 4859.500 oz

iii) Out of CNT 421,030.590 oz

iv) Manfra: 10,127.70 oz

v) Out of Delaware 1876.105 oz

total withdrawal 612,494.145 oz

2 adjustments:

a) dealer to customer Brinks 245,295.670 oz

b) customer to dealer/JPMorgan 10,250.920 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.505 MILLION OZ

TOTAL REG + ELIG. 338.752 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 745 HAVING LOST 102 CONTRACTS. WE HAD 86 NOTICES FILED ON WEDNESDAY

SO WE LOST 16 CONTRACTS OR AN E.F,P. JUMP OF 80,000 OZ TO LONDON

JUNE HAD A GAIN OF 18 TO STAND AT 1549

JULY HAD A GAIN OF 1477 CONTRACTS UP TO 113,466 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 86 for 430,000 oz

Comex volumes: 55,137// est. volume today// fair

Comex volume: confirmed yesterday: 89,839 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 4859 x 5,000 oz = 24,295,000 oz

to which we add the difference between the open interest for the front month of MAY(745) and the number of notices served upon today 36 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 4859 (notices served so far) x 5000 oz + OI for front month of MAY (745) – number of notices served upon today (36) x 5000 oz of silver standing for the MAY contract month equates 27,8400,000 oz. .

We LOST 80 contracts or AN ADDITIONAL 80,000 OZ will NOT stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

APRIL 8/WITH GOLD UP $7.70: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES INTO THE GLD//INVENTORY RESTS AT 1088.75 TONNES

APRIL 7/WITH GOLD UP $13.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1087.30 TONNES

APRIL 6/WITH GOLD DOWN $4.10: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.68 TONNES FROM THE GLD..//INVENTORY RESTS AT 1087.30 TONNES

APRIL 5/WITH GOLD DOWN $5.70: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.75 TONNES FROM THE GLD//INVENTORY RESTS AT 1089.98 TONNES

GLD INVENTORY: 1060.82 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 8/WITH SILVER UP 11 CENTS :NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 7/WITH SILVER UP 27 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 566.352 MILLION OZ//

APRIL 6/WITH SILVER DOWN 9 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 566.352 MILLION OZ

APRIL 5/WITH SILVER DOWN 16 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.386 MILLION OZ INTO THE SLV..//INVENTORY RESETS AT 566.352 MILLION OZ//

INVENTORY TONIGHT RESTS AT 570.439 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Your weekend reading material: topic rising prices

Alasdair Macleod: The most difficult thing in economics is to explain rising prices

Submitted by admin on Thu, 2022-05-12 19:35Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, May 12, 2022

It is apparent from media commentary that there is considerable misunderstanding over the causes behind rising prices and the consequences for interest rates. There are now signs that the official narrative over these issues is misleading at best.

Those who have protected their wealth by investing in financial assets no longer have the following breeze of falling interest rates. Financial bubbles are now bursting. Understanding the causes and therefore being able to assess the likely losses involved is becoming urgent for anyone committed to financial markets.

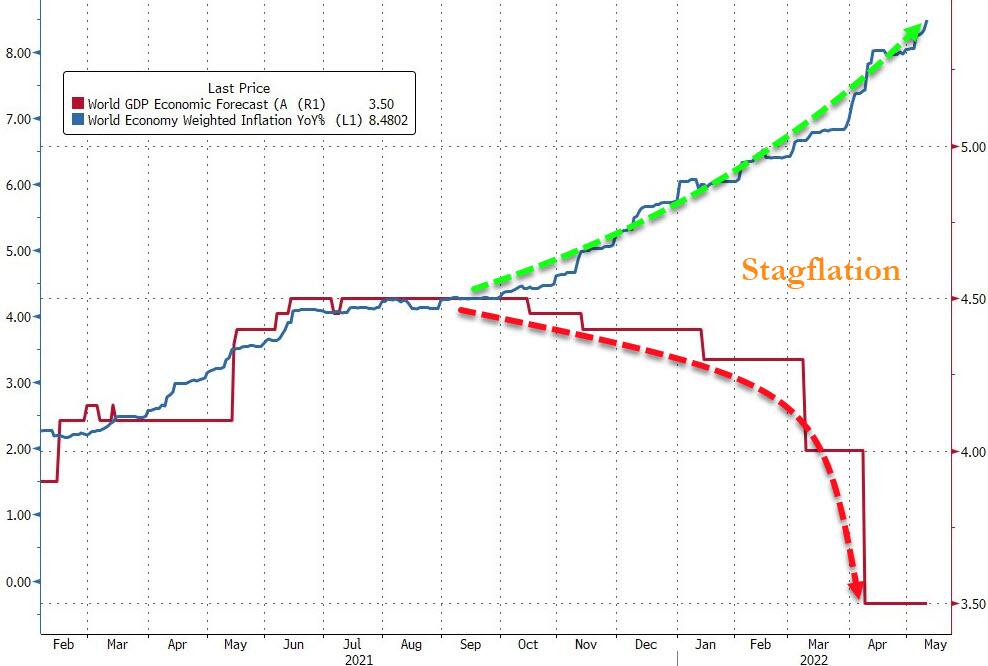

This article explains inflation in its proper context, which is loss of purchasing power for state-issued currencies, so that current conditions are better understood. It dissects the delusions behind monetary policies over both the causes of rising consumer prices and interest rate management.

It concludes that we are beginning to experience the worst of two worlds simultaneously: while the financial bubble collapses, in anticipation of and the response to an accelerated debasement of fiat currencies, prices of everything from commodities to finished goods will soar as a crackup boom materialises. …

… For the remainder of the analysis:

END

Chris Powell..important read.

(Chris Powell)

When buying gold and silver, consider the dealers who support GATA

Submitted by admin on Thu, 2022-05-12 23:36Section: Daily Dispatches

11:35p ET Thursday, May 12, 2022

Dear Friend of GATA and Gold:

Being the only forms of money without counterparty risk, at least when held directly by their owners, gold and silver are often seen as the foundation of a sound investment portfolio.

This principle was put into graphic format by the U.S. economist John Exter, who served as the Federal Reserve Bank of New York’s vice president in charge of international banking and precious metals operations, as well as a member of the Federal Reserve’s Board of Governors, long before suppressing the gold price became the Fed’s primary objective.

In Exter’s inverted pyramid of financial asset risk, gold is the ultimate asset, with all other assets posing greater risk to their owners:

But you can do more than protect yourself when you buy gold and the other monetary metal, silver. You can also help GATA fight the price suppression we long have been exposing, documenting, and sometimes litigating against:

That is you can buy metal from dealers who support GATA and have been recommended by our supporters over the years.

A list of those dealers is included with every GATA Dispatch and is posted at GATA’s internet site here:

So please give them a chance to meet your investment needs.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4.OTHER GOLD/SILVER COMMENTARIES

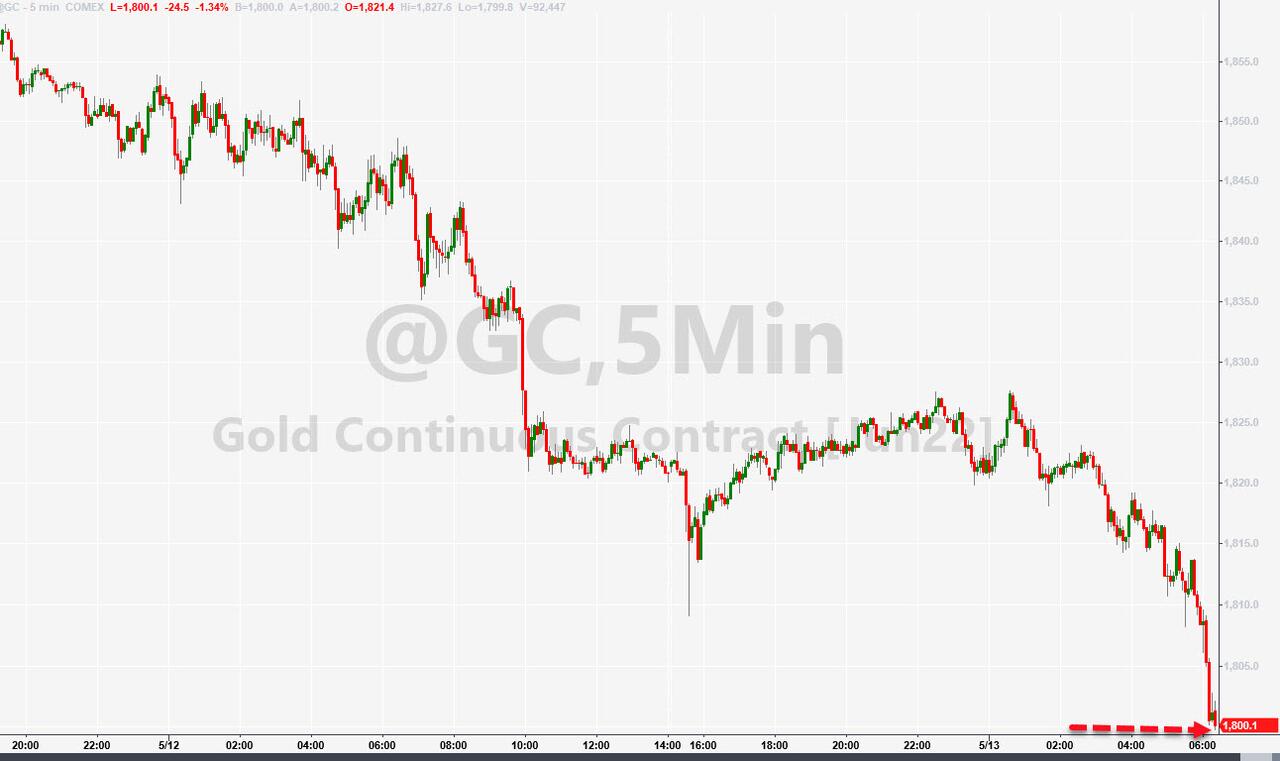

Gold Tumbles Below $1800, Erases All YTD Gains

FRIDAY, MAY 13, 2022 – 09:21 AM

The paper price of the yellow rock sjust tumbled back below $1800 for the first time since early Feb…

This is well below pre-Putin-invasion levels and Gold is now underwater for 2022…

…because nothing says ‘sell paper gold’ like raging global inflation…

And don’t blame the dollar’s rise. With DXY at 100, Gold has traded at $1923, $1700, $1230, $1140, & $330

As Mike Shedlock recently noted, Gold is not an inflation hedge except in extreme cases, notably hyperinflation.

The price of gold fell from $850 to $250 between 1980 and 2000 with inflation every step of the way

Rather, gold is largely a function of faith in central banks, especially the central bank of the major reserve currency country.

Gold fell from 1980 to 2000 as there was great faith in Fed Chair Alan Greenspan, then considered the “great maestro”.

If gold is ‘bet’ on government credibility, then we suspect the 2000-year history of the barbarous relic’s ‘value’ is not different this time.

end

5.OTHER COMMODITIES //COFFEE

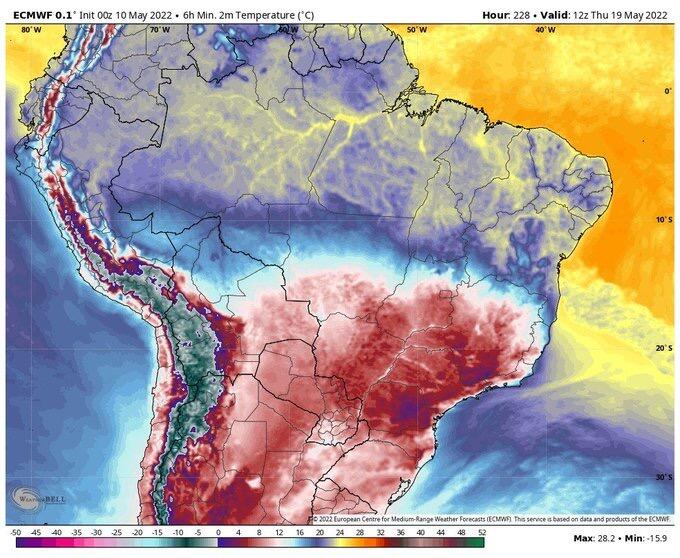

Cold front coming to Brazil which should cause coffee prices to rise

(zerohedge)

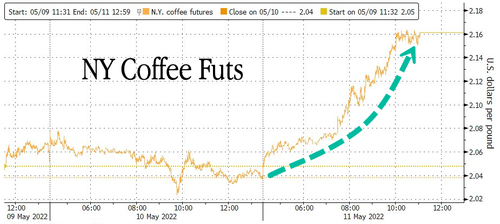

Coffee Prices Jump As “Intense New Cold Front” Threatens Top-Producer Brazil

THURSDAY, MAY 12, 2022 – 08:00 PM

Coffee futures in New York jumped Wednesday as new weather forecasts show the world’s largest producer has increased frost risks in top growing areas.

The National Oceanic and Atmospheric Administration published new forecasts that show low temperatures in Cerrado, Parana state, and Mogiana could record below 5 degrees Celsius (41 degrees Fahrenheit) by May 16. In the south of Minas Gerais and Guaxupe, temperatures may trend even lower through May 19. All of the regions listed are top-producing areas for arabica beans.

Global coffee reporter & independent analyst Maja Wallengren said, “intense new cold front starting to move into all main 2022 Arabica coffee regions in Brazil this week with temp potentially as low as -5 C° from southern Parana, all SM + AM to NW Cerrado + NE Matas in Minas Gerais. R $JO buyers really going to stay short?”

Arabica futures in New York jumped more than 6% to $2.16 per pound on the news. Prices are up 133% since the COVID-19 low of around $1 per pound and have faded from decade highs of $2.60 in March.

The International Coffee Organization (IOC) recently slashed its global 2020/21 supply estimate to a deficit of -3.13 million bags from a 1.2 million bag surplus.

Signs of tighter global coffee supplies have pushed prices to decade highs. Elevated coffee prices may not be immediately pushed to the consumer because of hedging by large US importers.

Starbucks, which buys coffee “12-18 months” ahead, locked-in prices at the lows of early-2021 and are set to expire. This means a cup of coffee at the largest US retail coffee chain could rise further due to supply issues, among the other forms of inflation, such as labor, freight, etc..

END

COMMODITIES IN GENERAL//

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7882

OFFSHORE YUAN: 6.8088

HANG SANG CLOSED UP 518.43 PTS OR 2.67%

2. Nikkei closed 678.93 OR 2.64%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 104.79/Euro RISES TO 1.0387

3b Japan 10 YR bond yield:FALLS TO. +.24/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.95/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield RISES TO 3.375

3j Gold at $1815.70 silver at: 20.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1.3 roubles/dollar; ROUBLE AT 64.61

3m oil into the 107 dollar handle for WTI and 109 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.06 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning .9997– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0382well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.909- UP 9 BASIS PTS

USA 30 YR BOND YIELD: 3.073 UP 10 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.43

Futures Jump As Crypto Turmoil Fades, Dip Buyers Make Cautious Appearance

FRIDAY, MAY 13, 2022 – 07:56 AM

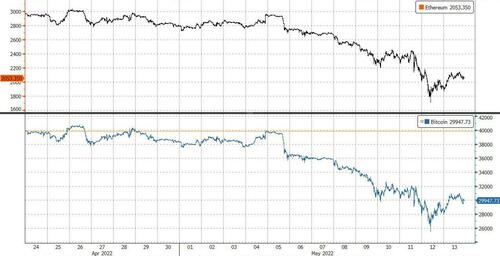

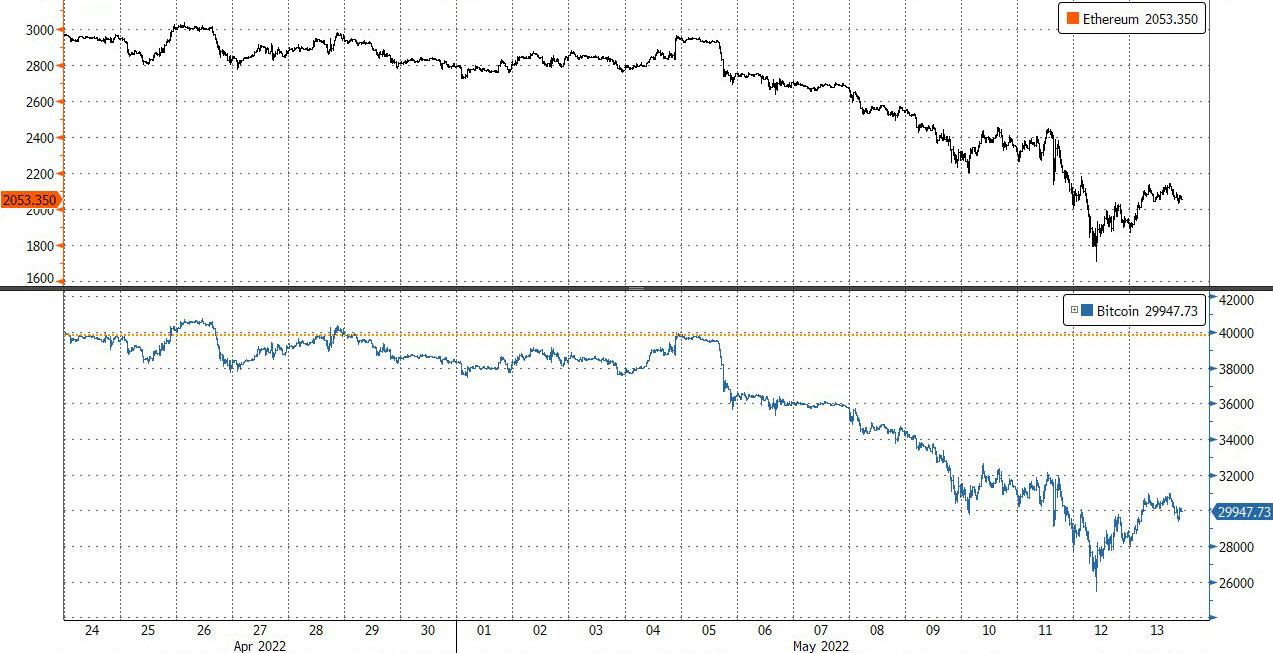

After dropping to the edge of a bear market, with Eminis sliding to precisely 3,855 or exactly 20% lower than the all time high, US index futures rebounded sharply from the brink (the same way they did on Dec 24, 2018 when the S&P spent a few minutes in a bear market) as the stabilization of much of the cryptosphere (where no new stablecoins suddenly cratered to 0) and an overnight easing in Treasury yields provided some relief after a two-day slide. Nasdaq 100 futures climbed 1.7% as of 730 a.m. in New York. S&P 500 futures were also higher, rising 1.1%, as high as 3976 after dropping to 2,855 yesterday. Twitter shares plunged as much as 26% in New York premarket trading after Elon Musk tweeted that his deal for the social media company was “temporarily on hold.” Yields on 10-year US Treasury yields fell for a fourth consecutive day on Thursday, reaching 2.85%, before edging higher again on Friday. The dollar index dipped but remains on course for its longest streak of weekly gains since 2018, while bitcoin and ether reversed several days of harrowing losses to rise back over 30,000 and 2,000, respectively.

Abating panic in the cryptocurrency market was among the highlights of a risk-on environment on the last day of the week. Bitcoin added about $1,800 to top $30,000. US cryptocurrency-exposed stocks including Riot Blockchain Inc. and Marathon Digital Holdings Inc. also rallied premarket.

In notable premarket moves, Twitter slumped 21% after bidder Elon Musk tweeted deal was “temporarily on hold” pending details about fake accounts. On the other end, Robinhood surged 20% after cryptocurrency billionaire Sam Bankman-Fried snapped up a 7.6% stake, while Affirm jumped 30% after earnings. Cryptocurrency-exposed stocks climbed as digital assets started to rebound after the recent rout linked to the implosion of the TerraUSD stablecoin. Coinbase rose 11% despite being sued over its role in the promotion and trading of a stablecoin that purportedly had its value pegged to the price of the Japanese yen. Bank stocks rose in premarket trading Friday, putting them on track to snap a six-day losing streak. Here are all the notable premarket movers:

- Twitter (TWTR US) shares slump as much as 19% premarket after Musk says deal is “temporarily on hold pending details”. Tesla (TSLA US) shares hit a session high, rising nearly 5% on the news

- Megacap tech stocks and semiconductor makers rally in US premarket trading amid a broad rebound across growth sectors, while Korean chip peer Samsung was said to be in talks to hike chipmaking prices. Apple (AAPL US) +2.1%, Meta Platforms (FB US) +2.4%, Microsoft (MSFT US) +1.8%

- Robinhood (HOOD US) shares surge as much as 27% in U.S. premarket trading after cryptocurrency billionaire Sam Bankman-Fried disclosed a new 7.6% stake in the online brokerage

- Cryptocurrency-exposed stocks climb in US premarket trading as digital assets started to rebound after the recent rout linked to the implosion of the TerraUSD stablecoin. Riot Blockchain (RIOT US) +7.9%, Marathon Digital (MARA US) +7.2%

- US-listed Chinese stocks rise in premarket trading, with sentiment boosted by the Fed’s pushback on speculation of steeper interest-rate hikes and Shanghai’s new timeline to end a grueling lockdown. Alibaba (BABA US) +3.3%, JD.com (JD US) +4%, Pinduoduo (PDD US) +4.3%.

- New Relic (NEWR US) declined 9% in postmarket. It delivered a mixed fourth quarter, according to analysts, with revenue growth coming in ahead of consensus, albeit with a lower beat compared to the last period

- Figs (FIGS US) sinks as much as 27% in US premarket trading, with Cowen saying that the scrubs maker’s cut to its full-year 2022 sales growth and Ebitda margin guidance is “well below” previous guidance

- Compass (COMP US) jumpped 7% in extended trading after the real-estate software company reported larger-than-expected revenues in the first quarter, despite guiding toward lower- than-expected second-quarter revenue

- First Solar Inc. (FSLR US) shares gained 2.8% in extended trading on Thursday, as Piper Sandler upgrades the stock to overweight from neutral

Stocks have plunged this year as traders fretted over the impact tighter monetary will have on growth, with the S&P 500 dropping to precisely 20% from its recent peak before bouncing. On Thursday, Fed Chair Jerome Powell on Thursday reaffirmed that the central bank is likely to raise interest rates by a half percentage point at each of its next two meetings, while leaving open the possibility it could do more. The Fed chair also said that whether a soft landing can be executed or not may depend on factors that they cannot control but added they have tools to get inflation under control and that it will ultimately be more painful if high inflation is not dealt with and becomes entrenched. Furthermore, he noted that with perfect hindsight, it would have been better to have hiked rates sooner, according to Reuters.

As the Federal Reserve embarks on interest-rate hikes to tame surging inflation, expensive growth shares, including the tech sector, have suffered as higher rates mean a bigger discount for the present value of future profits. This marks a shift in investor outlook after tech stocks had been some of the market’s best performers for years.

“While we continue to see positives for the market, investor sentiment isn’t likely to turn until we get greater clarity on the 3Rs — rates, recession and risk,” said Mark Haefele, chief investment officer, UBS Global Wealth Management. “Until then, we favor parts of the market that should outperform in an environment of rising policy rates, slowing growth, and geopolitical uncertainty.”

At $1.1 billion, tech stocks suffered their biggest outflows so far this year in the week to May 11, second only to financials, which lost $2.6 billion, Bank of America CIO Michael Hartnett wrote in a note, citing EPFR Global data. By contrast, US stocks overall noted their first inflow in five weeks at $93 million.

It’s a “very tough time,” Kathy Entwistle, managing director at Morgan Stanley Private Wealth Management, said on Bloomberg Television. “We’re holding just still and quiet and patient and waiting for some more insights as to where we’re going. We still see a lot of volatility on the horizon.”

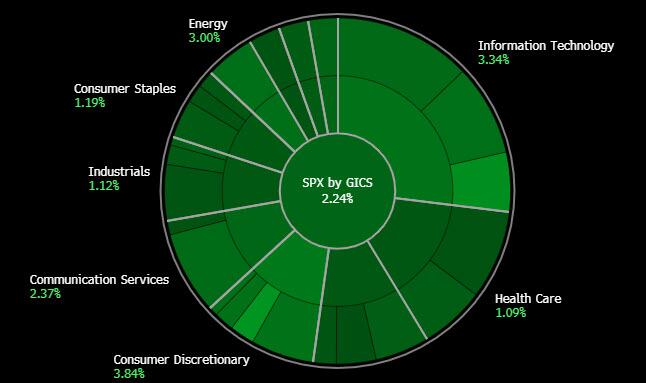

In Europe, the Stoxx 600 Index rose 1.2% as the lowest valuations since the start of the pandemic drew buyers. Banks and technology stocks led gains, while autos and telecommunication shares underperformed. Here are Europe’s biggest movers:

- Evotec shares rise as much as 9.5% after Deutsche Bank analyst Falko Friedrichs raised the recommendation to buy from hold, citing a unique opportunity to invest in a firm with an entire partnered drug pipeline “for free.”

- Deutsche Telekom shares advance 1.8% after raising full-year outlook for adjusted Ebitda after leases, reflecting higher forecasts for T-Mobile US.

- Freenet shares gain as much as 4.8% 1Q results show a good start to the year, and there may be scope for a guidance upgrade in 1H22, Citi (buy) writes in note

- Fortum shares advance as much as 11% on Friday — the biggest intraday gain since 2009 — after SEB and Danske Bank raised their recommendation on the stock citing the Finnish utility’s Russia exit and de-risking related to Uniper gas contracts.

- UCB shares fall as much as 17% after the company said the US FDA said it can’t approve UCB’s psoriasis treatment bimekizumab in its current form, forcing the company and analysts to reasses 2022 expectations.

- Drax falls as much as 7.6% and is among weakest performers in the Stoxx 600 on Friday after Credit Suisse gives the stock its only negative rating, moving to underperform on elevated power prices.

- SalMar drops as much as 4%, falling alongside peers in the Norwegian salmon and seafood sector, after a slew of several companies in the sector reported 1Q earnings that came in below expectations.

- Unipol and UnipolSai drop in Milan trading after releasing first-quarter results and the 2022-2024 strategic plan; analysts note lower-than-expected cumulative dividends in plan for UnipolSai.

European Union nations said it may be time to consider delaying a push to ban Russian oil if the bloc can’t persuade Hungary to back the embargo. Wheat production in Ukraine, one of the biggest growers, will fall by one-third compared to last year, according to a US forecast.

Earlier in the session, Asian stocks rallied as battered technology shares bounced back, with the regional benchmark still on track for its worst weekly losing streak since 2015 on worries about higher interest rates and lockdowns in China. The MSCI Asia Pacific Index rose as much as 1.8%, advancing with US futures as comments from Federal Reserve Chair Jerome Powell signaled rate hikes of more than 50 basis points may be unlikely. SoftBank was among the biggest boosts after its results, along with Tencent and TSMC. Traders said Friday’s rebound was largely driven by the unwinding of short positions following the recent selloff, with many still nervous about how China’s virus measures can complicate the already murky global economic outlook. The Asian equity measure was on track for its sixth-straight weekly decline, down 2.5% in the past five sessions.

“We have to be watchful on the impact of China’s lockdowns, that’s going to have an effect on inflation as well as on growth,” said Jumpei Tanaka, a strategist at Pictet. “Up until now, the earnings outlook hasn’t been lowered that much. The market has been adjusting valuations because of the Fed’s rate hikes. The next key point is how corporate earnings will be affected.” Japan’s Nikkei rose 2.6%, boosted by gains in Tokyo Electron after strong profits as well as SoftBank. In Hong Kong, the Hang Seng Tech Index jumped 4.5%.

India’s key equity indexes fell for a 6th straight session and posted their longest stretch of weekly losses in two years as investors’ appetite faded on the back of the local currency’s plunge to a record low and disappointing earnings. The S&P BSE Sensex declined 0.3% to 52,793.62 in Mumbai after erasing advance of as much as 1.6% during the session. The NSE Nifty 50 Index retreated 0.2% to its lowest level since July 30. Both gauges have retreated 3.7% and 3.8% for the week respectively and fallen for a fifth straight week, their longest run of losses since April 2020. “The fear of rising inflation and expectations of more rate hikes in the near term are weighing on investors’ minds,” according to Kotak Securities analyst Amol Athawale.“Traders are selling at every opportunity given that there seems to be no respite from the negative news flows.” The Sensex and Nifty are now about 14.5% off their peak levels in Oct. Ten of the 19 sector sub-indexes compiled by BSE Ltd. dropped on Friday, led by metal companies. For the week, utilities stock gauge was the worst performer, dropping about 11%. ICICI Bank contributed the most to the Sensex’s decline, easing 2.7%. Out of 30 shares in the Sensex index, 15 rose while rest fell.

In rates, Treasuries were pressured lower as stock futures pushed through Thursday’s session highs, following gains across European equities. 10-year TSY yields rose to around 2.90%, cheaper by 5bp on the day and sitting close to session highs into early session — both bunds and gilts underperform slightly across the sector. Risk sentiment was boosted by a rebound in cryptocurrencies, leaving Treasury yields cheaper by up to 6bp across long-end of the curve where 20-year sector underperforms. Long-end led losses steepening 5s30s by 2bp on the day and 2s10s by 2.8bp. The Dollar issuance slate is empty so far; six deals were priced for $11.5b Thursday, taking weekly total to $21.7b vs. $30b projected — two names decided to stand down. Bund, gilt and UST curves bear-steepen. Peripheral spreads widen, short-dated BTPs lag, widening 5bps to core. Yields on Japan’s debt fell even as those on Treasuries rise across the curve in Asia amid higher equities.

In FX, the Bloomberg Dollar Spot Index slumped and the greenback weakened against all of it Group-of-10 peers apart from the yen as investor demand for haven assets ebbed after Federal Reserve Chair Jerome Powell pushed back against speculation of more aggressive interest-rate hikes. Risk sensitive Scandinavian currencies as well ask the Australian dollar led gains. The main theme in the FX options space Friday is gamma selloff following the large swings this week. Still, demand for low-delta exposure on a haven basis remains better bid, with greenback topside in good demand versus the euro and the pound. European government bonds followed US Treasuries lower, snapping a recent rally. Treasury yields rose by 3-7 bps as the curve bear- steepened. The yen pared early weakness after BOJ’s Kuroda stressed FX stability. China’s yuan strengthens against the dollar following warnings from the CBIRC with gains fading following soft loan data.

In commodities, Crude futures advance, WTI gains stall near $108. Base metals trade poorly with much of the LME complex down over 1%. Spot gold trades in a narrow range near $1,823/oz.

In crypto, Bitcoin rose back above $30,000. Binance said that withdrawals for Lunar and UST will open when the market becomes more stable, will suspend spot trading for LUNA/BUSD and UST/BUSD at 09:30BST, May 13th.

To the day ahead now, and data releases include Euro Area industrial production for March, along with the University of Michigan’s preliminary consumer sentiment index for May. Otherwise, central bank speakers include the Fed’s Kashkari and Mester, as well as the ECB’s Centeno, Nagel and Schnabel.

Market Snapshot

- S&P 500 futures up 1.1% to 3,970.75

- STOXX Europe 600 up 1.2% to 429.53

- MXAP up 1.7% to 160.25

- MXAPJ up 1.9% to 522.21

- Nikkei up 2.6% to 26,427.65

- Topix up 1.9% to 1,864.20

- Hang Seng Index up 2.7% to 19,898.77

- Shanghai Composite up 1.0% to 3,084.28

- Sensex up 1.2% to 53,564.26

- Australia S&P/ASX 200 up 1.9% to 7,075.11

- Kospi up 2.1% to 2,604.24

- German 10Y yield little changed at 0.91%

- Euro up 0.2% to $1.0403

- Brent Futures up 0.8% to $108.30/bbl

- Gold spot up 0.0% to $1,822.04

- U.S. Dollar Index down 0.25% to 104.59

Top Overnight News from Bloomberg

- Calls are growing for China’s government to sell more bonds to pay for extra stimulus to boost an economy facing its greatest challenges since the initial few months of the pandemic in 2020

- For global investors trying to gauge the fallout from surging interest rates and slowing economic growth, Hong Kong is quickly emerging as a must-watch market. While Hong Kong’s $466 billion foreign-reserves stockpile and plentiful interbank liquidity suggest little chance of an imminent crisis, signs of financial stress are building

- UK Chancellor of the Exchequer Rishi Sunak said the Brexit settlement in Northern Ireland is causing economic and political harm and called on the European Union to be flexible, comments likely to be seen as an attempt to publicly align himself with Boris Johnson after reports of a rift

- With the U.K. wilting under the fastest inflation in three decades, supermarkets are raising prices at an even quicker rate, according to a new analysis prepared for Bloomberg. That’s turning the screws on shoppers who are already grappling with higher gas and heating bills and falling real incomes

- Some EU nations are saying it may be time to consider delaying a push to ban Russian oil so they can proceed with the rest of a proposed sanctions package if the bloc can’t persuade Hungary to back the embargo

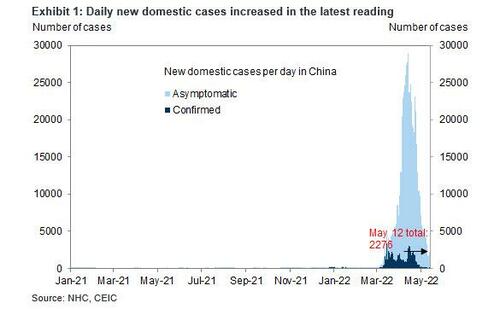

- Beijing reported a slight increase in new Covid-19 cases after officials late Wednesday denied the city will be locked down amid growing concern the Chinese capital’s response to a persistent outbreak is about to be intensified

- Investors are deep in risk-off mood with outflows from stocks, bonds, cash and gold, Bank of America strategists said, citing EPFR Global data

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were firmer as risk momentum picked up following on from the volatile session on Wall St where the major indices finished mixed but almost wiped out all losses after a late ramp up heading into the close. ASX 200 traded with respectable gains and back above the 7,000 level with tech frontrunning the advances. Nikkei 225 outperformed as focus remained on earnings, while SoftBank surged amid buyback hopes and despite a record loss. Hang Seng and Shanghai Comp joined in on the elated mood with Hong Kong led by strength in tech, although the advances in the mainland were moderated by the mixed COVID headlines with Beijing to conduct the next round of mass COVID testing, while Shanghai aims to achieve zero community spread by the middle of this month and is considering expanding the scale of output resumption.

Top Asian News

- Shanghai Vice Mayor said they aim to have no community spread of coronavirus by mid-May and are considering expanding the scale of production resumption, while they will aim to open up, ease traffic restrictions and open shops in an orderly manner, according to Reuters.

- Shanghai is to prioritise resuming classes for grades 9, 11 and 12, while supermarkets, convenience and department stores will resume offline operations in an orderly manner and other services such as hairdressing will open gradually, according to Global Times.

- China Banking and Insurance Regulatory Commission says the Yuan’s weakening is not sustainable, adding do not bet on the unilateral devaluation and appreciation or you could face unnecessary losses; retreat in the Yuan was normal market reaction..

- BoJ Governor Kuroda said Japan still hasn’t achieved a situation where inflation is stably and sustainably at 2%, while the expected rise in inflation is driven mostly by energy costs and is lacking sustainability. Kuroda reiterated the BoJ must continue monetary easing to reach its price target and it is premature to debate an exit from ultra-easy policy, while he also said it is appropriate to maintain the current dovish forward guidance on interest rates, according to Reuters.

- North Korea said around 350k have shown fever symptoms of an ‘unknown cause’ and 187.8k are being treated in isolation, while it reported 18k COVID-19 cases and 6 died from a fever in which one was confirmed as a COVID death, according to KCNA and Yonhap.

European bourses are firmer as the rebound from Thursday’s selloff continues, Euro Stoxx 50 +1.3%. US futures are similarly bolstered across the board, NQ outpacing peers modestly as Tech recoups, ES +0.9%. Samsung (005930 KS) is reportedly in talks to hike chipmaking prices by up to 20%, according to Bloomberg sources. Elon Musk says the Twitter (TWTR) deal is temporarily on hold, pending details supporting the calculation that spam/fake accounts represent less than 5% of users. Pressure in TWTR subsequent extended to -13% in the pre-market; extending to -19% after five-minutes.

Top European News

- UK PM Johnson is considering as many as 90k job cuts in civil service, according to ITV.

- GVS Shares Rise After Agreeing to Buy Haemotronic for EU212m

- EU Starts to Consider Oil Sanctions Delay as Hungary Digs In

- UCB Plunges After FDA Says It Can’t Approve Psoriasis Drug Now

- Black Bankers Fight to Hold Finance Accountable for Its Promises

FX

- Dollar and Yen shed some safe haven gains as risk sentiment recovers ahead of the weekend; DXY slips from fresh 2022 peak at 104.920, though still positive, and USD/JPY up near 129.00 vs new retracement low circa 127.50.

- Aussie takes advantage of pickup in risk appetite and Yuan bounce amidst verbal intervention; AUD/USD hovering under 0.6900 from sub-0.6850 yesterday, USD/CNH and USD/CNY around 6.8000 vs 6.8370 and 6.8110.

- Euro, Pound and Franc regroup, but remain vulnerable around psychological levels; 1.0400, 1.2200 and parity in EUR/USD, Cable and USD/CHF respectively.

- Loonie off recent lows post hawkish BoC comments and pre Q1 Loans Survey, USD/CAD close to 1.3000 and 1.1bln option expiry interest between 1.2990 and the round number.

- Peso underpinned after 50 bp Banxico hike as 1 of the 5 voters dissented for 75 bp.

- Czech Koruna caught between CNB minutes underlining dovish leaning of new head and Holub opining that May’s hike may not be the final one.

Fixed Income

- Bonds bounce after conceding ground to recovering risk assets.

- Bunds find support just ahead of 154.00, Gilts in the low 120.00 zone and 10 year T-note at 119-07.

- Curves re-steepen after decent US 30 year sale completes the Quarterly Refunding remit and attention turns to 20 year and 10 year TIPS auctions next week.

Commodities

- WTI and Brent are firmer moving with the broad rebound in risk-assets, however, upside is capped amid the EU considering omitting the proposed Russia oil embargo from the 6th sanctions round.

- WTI resides around USD 107/bbl (106.29-108.13 intraday range) and Brent trades just under USD 109/bbl (107.79-109.79 intraday range).

- Spot gold is contained around USD 1820/oz, though it is coming under modest pressure as the DXY picks up most recently.

US Event Calendar

- 08:30: April Import Price Index MoM, est. 0.6%, prior 2.6%; YoY, est. 12.2%, prior 12.5%

- 08:30: April Export Price Index MoM, est. 0.7%, prior 4.5%; YoY, est. 19.2%, prior 18.8%

- 10:00: May U. of Mich. Sentiment, est. 64.0, prior 65.2; Current Conditions, est. 69.3, prior 69.4; Expectations, est. 61.5, prior 62.5

- 10:00: May U. of Mich. 1 Yr Inflation, est. 5.5%, prior 5.4%; 5-10 Yr Inflation, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

As those working in this industry know, spreadsheet errors can have consequences – often costly ones. My fiancée doesn’t spend as much time on Excel as I do, but with our wedding coming up in July, she’s been using a spreadsheet to keep track of the number of guests. I privately regard this sheet to be an abomination, so in the interests of our future marriage I’ve tried to avoid the subject. But a couple of weeks ago I was told that we needed more guests and had to extend further invites, since we were up against the reception venue’s minimum. This I duly did, although having already invited my friends, I mostly resorted to being a lot more generous on my plus-one policy. At the weekend however, she showed me the spreadsheet. It turned out she hadn’t extended the range on the guest list sum function, and we were already comfortably above what we needed. I won’t tell you how much these extra invites have cost us. Thankfully as a primary school teacher she doesn’t teach Excel to her 5- and 6-year-olds, although I then discovered with even more alarm that she’s considered the spreadsheet expert at her school…

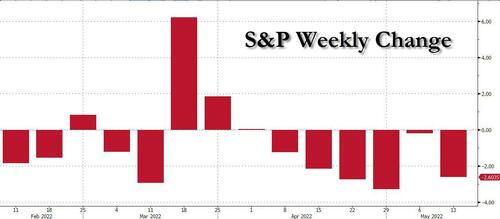

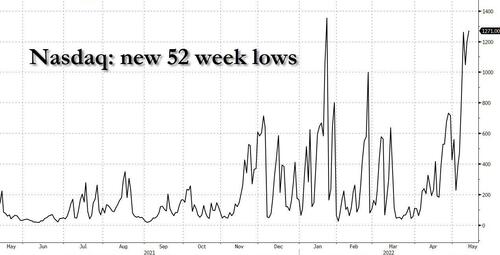

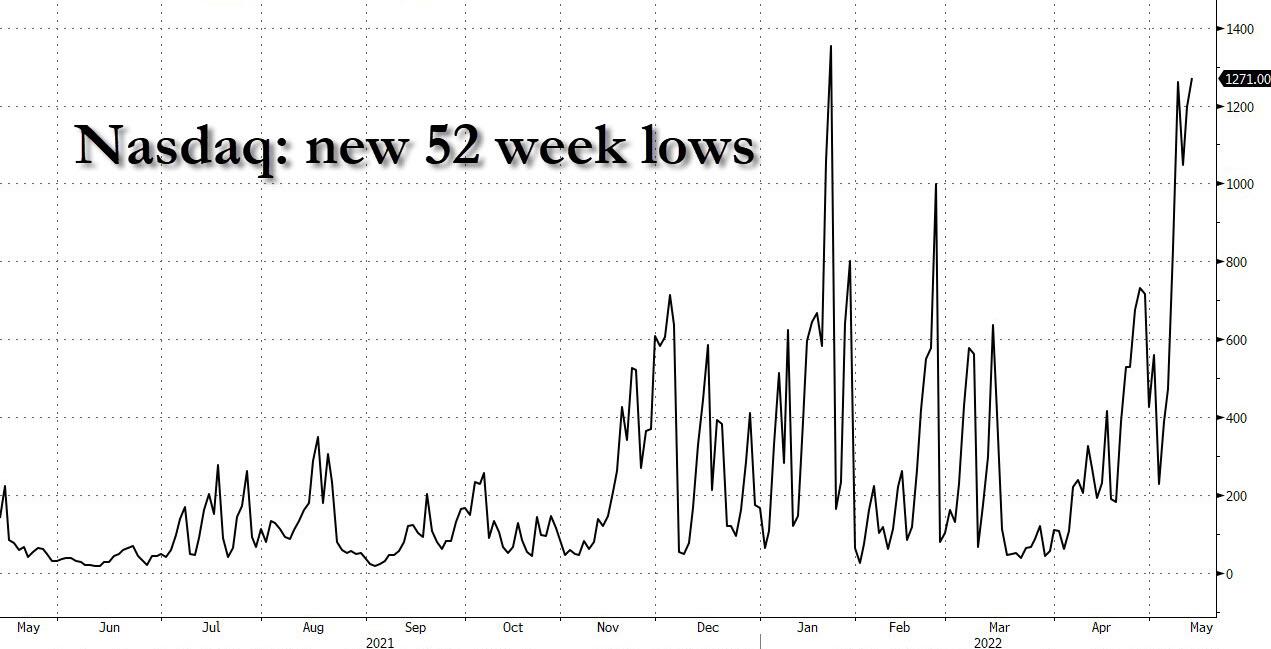

It’s been a costly few weeks in markets too as investors have priced in growing recession risks, and over the last 24 hours we’ve seen some incredible intraday volatility across a range of asset classes. At one point in the New York afternoon, the S&P 500 had been down -1.94% at the lows, which left it just shy of a -20% decline since its all-time closing peak that would mark the formal start of a bear market. But then in the final hour there was a major recovery that meant the index only saw a modest -0.13% fall on the day, even if that still marked a fresh one-year low. Futures markets are implying we’re going to see that rally extended today, with those for the S&P up +0.92% this morning. But even if we do see a recovery of that sort of magnitude, then the major losses we’ve already seen this week mean it would still be the first time in over a decade that the index has posted 6 consecutive weekly declines.

That pattern of deep losses followed by a late recovery was echoed more broadly yesterday, with the NASDAQ paring back losses of more than -2% on the day to eke out a marginal +0.06% advance. For the FANG+ index (-0.30%), the late recovery wasn’t enough to bring it back into positive territory, and there was a significant milestone reached since its latest slump means it’s now more than -40% beneath its all-time high, which surpasses its losses during the Covid selloff of 2020 when it was “only” down by -34% from peak to trough. European equities lost ground too, and the STOXX 600 (-0.75%) similarly saw a second-half recovery, having been as low as -2.41% earlier in the day.

Unlike in April, when the equity declines were triggered by the prospect of a more aggressive Fed tightening cycle and went hand-in-hand with sovereign bond losses, this week’s declines have much more obviously surrounded global growth risks, which you can see in the way that Fed Funds futures are now beginning to take out some of the tightening they’d been pricing in over the year ahead. Only yesterday, the futures-implied rate by the FOMC’s December meeting came down by -5.3bps to still be beneath its level from 3 weeks earlier, which marks a change from the almost relentless march higher we’ve seen over the last 8 months. In fact the only major interruption to that trend so far has come from Russia’s invasion of Ukraine in late-February, before the inflationary consequences of the conflict reasserted themselves on market pricing.

With investors expecting less monetary tightening and seeking out safe havens, yesterday witnessed a major sovereign bond rally across countries and maturities. The 10yr Treasury yield came down -7.3bps to 2.85%, and at the front-end of the curve, 2yr yields were down -7.8bps to 2.56%. This came on a day with another round of Fed speakers sounding the same tune of late, including Chair Powell who said that +50bp hikes at the next two meetings were probably appropriate. Meanwhile, he sounded an even more pessimistic tone on the path of the economy given the impending tightening, noting that getting inflation back to target would “include some pain” and that whether a soft landing can be arranged is up to matters beyond the Fed’s control.

Over in Europe the declines were even larger, with yields on 10yr bunds (-14.6bps) undergoing their biggest daily move since the start of March, as yields on 10yr OATs (-13.8bps), BTPs (18.4bps) and gilts (-16.5bps) saw similar declines. A noticeable feature of the recent sovereign bond rally is how investors’ expectations of future inflation have come down significantly over recent days, with the 10yr German breakeven falling from a peak of 2.98% on May 2 to just 2.29% yesterday, which is an even faster decline than the one seen during the initial phase of the Covid pandemic in March 2020.

That flight to havens was evident in foreign exchange markets too, where the dollar index strengthened a further +0.97% to levels not seen since 2002. Conversely, that saw the euro close beneath the $1.04 mark for the first time since late-2016, although the traditional safe haven of the Japanese Yen was the top-performing G10 currency yesterday, strengthening +1.27% against the US Dollar and +2.61% against the Euro. When it came to cryptocurrencies, Bitcoin hit an intraday low of $25,425 shortly after the European open, which is the first time it’s traded that low since late 2020, before recovering its losses to end the session higher at $28,546, and this morning it’s rebounded another +6.34% to hit $30,356.

Overnight in Asia we’ve seen a significant rebound in equity markets too, with the Nikkei (+2.52%), the Hang Seng (+2.00%) and the KOSPI (+1.72%) all seeing sizeable advances, and the Shanghai Comp (+0.56%) also posting a solid gain. Those earlier comments from Chair Powell after the US close have supported risk appetite, particularly since he echoed his previous comments about the Fed being on course for further 50bp hikes at the next couple of meetings, rather than moving towards 75bps in the aftermath of the stronger-than-expected CPI reading. A number of yesterday’s other moves have also begun to unwind, with the Japanese Yen down -0.50% against the US Dollar this morning, whilst yields on 10yr Treasuries have risen +3.6bps overnight. Separately in Shanghai, officials said that they planned to stop community spread of Covid-19 and start reopening by May 20, which is the first time that a timeline has been put forward as to when the lockdown might end.

Elsewhere yesterday, there was a significant +13.50% rise in European natural gas futures after Gazprom said that gas flows wouldn’t be able to go through the Yamal pipeline because of Russian-imposed sanctions on European companies. But on the other hand, Bloomberg reported that some EU nations were considering a delay in sanctioning Russian oil in light of Hungarian opposition, and instead pushing ahead with the rest of the sanctions package. There were also further signs of the geopolitical shifts as a result of Russia’s invasion, after Finland’s President and Prime Minister endorsed NATO membership, saying the country should apply “without delay”.

Staying on the political sphere, tensions have continued to fester between the UK and the EU over the Northern Ireland Protocol, and yesterday’s statements from the two sides indicated there was a difficult phone call between UK Foreign Secretary Truss and EU Commission Vice President Šefčovič. The UK Foreign Office’s readout of the call said that “if the EU would not show the requisite flexibility … we would have no choice but to act.” Then Šefčovič said in his own statement that it was “of serious concern that the UK government intends to embark on the path of unilateral action.” So one to watch into next week given press reports we could hear more from the UK side then.

Looking at yesterday’s data, the US PPI reading added to the picture of elevated inflationary pressures. The headline monthly gain for April came in at +0.5% as expected, but the March reading was revised up two-tenths to +1.6%, meaning that the year-on-year figure only came down to +11.0% (vs. +10.7% expected). We also had the weekly initial jobless claims for the week through May 7, which came in at 203k (vs. 193k expected). And in the UK, the Q1 GDP reading was a bit below consensus at +0.8% (vs. +1.0% expected), and looking at the monthly reading for March specifically there was actually a -0.1% contraction (vs unchanged expected).

To the day ahead now, and data releases include Euro Area industrial production for March, along with the University of Michigan’s preliminary consumer sentiment index for May. Otherwise, central bank speakers include the Fed’s Kashkari and Mester, as well as the ECB’s Centeno, Nagel and Schnabel.

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 29.29 PTS OR 0.69% //Hang Sang CLOSED UP 518.43 PTS OR 2.67% /The Nikkei closed UP 678.93 OR 2.64% //Australia’s all ordinaires CLOSED UP 1.97% /Chinese yuan (ONSHORE) closed UP 6,7882 /Oil UP TO 107.57 dollars per barrel for WTI and down TO 109.05 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7882 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8088: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///SOUTH KOREA

This is will inflation throughout the world:

(zerohedge)

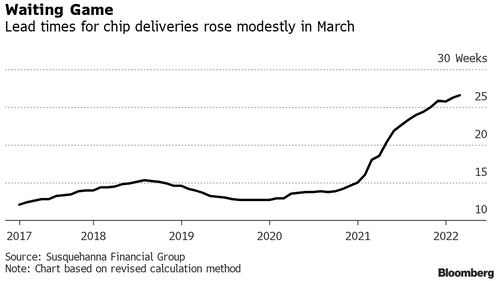

Samsung Set To Imminently Hike Semiconductor Prices By 20%

FRIDAY, MAY 13, 2022 – 09:05 AM

Samsung Electronics is preparing to increase prices for chip contract manufacturing in the second half of this year which comes as no surprise given skyrocketing cost pressures eating away at the company’s margins.

Samsung’s contract-based chip prices are set to increase between 15-20% given the level of manufacturing complexity, Bloomberg said, citing people familiar with the matter, adding the new pricing model has been discussed and negotiated with clients.

Samsung’s decision comes as the cost of energy, raw materials, equipment, freight, and labor are rapidly soaring. The move was “inevitable,” said Masahiro Wakasugi, a Bloomberg Intelligence analyst.

Another component driving the price hikes is the ongoing global chip shortage. Then there are lockdowns in China driving lead times — the lag between when a semiconductor chip is ordered and delivered — to 26.6 weeks, a record high.

Rising chip prices will only increase consumer costs for smartphones, tablets, computers, game consoles, televisions, smart speakers, automobiles, and the list goes on and on. Samsung is the world’s second-largest chip contract manufacturer.

TSMC, short for Taiwan Semiconductor Manufacturing Company, is the world’s largest contract chip manufacturer and recently notified clients of price increases of 5% to 8% next year, following a 20% price hike last year.

There aren’t alternatives to the world’s largest chipmakers. This means companies that require chips to power their products have no leverage and are stuck with expensive chips, which will only mean the cost of consumer electronics will go higher.

END

3B JAPAN

3c CHINA

COVID//LOCKDOWNS/

China Tightens Restrictions On Overseas Travel While Shanghai Aims For ‘Zero COVID’ By Mid-May

FRIDAY, MAY 13, 2022 – 11:15 AM

In what was interpreted as good news by traders, Shanghai is finally looking to unwind certain lockdown measures, while simultaneously tightening the city’s restrictions on “non-essential” overseas travel for its citizens to help contain the worst coronavirus outbreak the country has seen in the past two years.

China has said it will impose tight restrictions on “non-essential” overseas travel for its citizens to help contain the worst coronavirus outbreak the country has seen.

Shanghai Vice Mayor said the city is aiming to stamp out all community spread of the virus by mid-May and is considering expanding the scale of production resumption, while they will aim to open up, ease traffic restrictions and open shops in an orderly manner, according to the SCMP.

A statement on the agency’s website said the meeting had been called to relay the decisions taken at a meeting of the Politburo Standing Committee chaired by President Xi Jinping on May 5, where the leadership doubled down on China’s zero-COVID policy saying it “will stand the test of time”.

The city, meanwhile, is expected to prioritize resuming classes for grades 9, 11 and 12, while supermarkets, convenience and department stores will resume offline operations in an orderly manner and other services such as hairdressing will open gradually.

Shanghai is to prioritize the resumption of classes for grades 9, 11 and 12, while supermarkets, convenience and department stores will resume operating offline.

The immigration authorities on Thursday said the curbs were designed to stop infections crossing the border and would include a more rigorous approval process for passports and other travel documents and a crackdown on illegal border crossings.

A meeting of the National Immigration Administration on Tuesday heard that China’s COVID situation had reached a “significant and urgent point” and that the city of Beijing was the “most important of the important” places.

END

CHINA/LOCKDOWNS//CREDIT CREATION

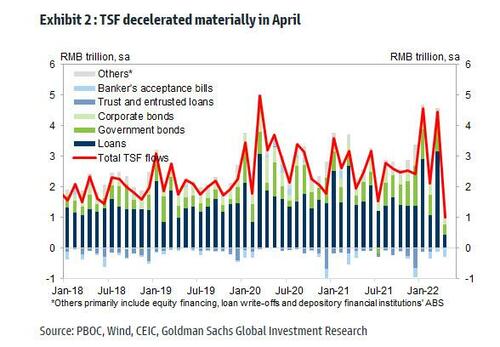

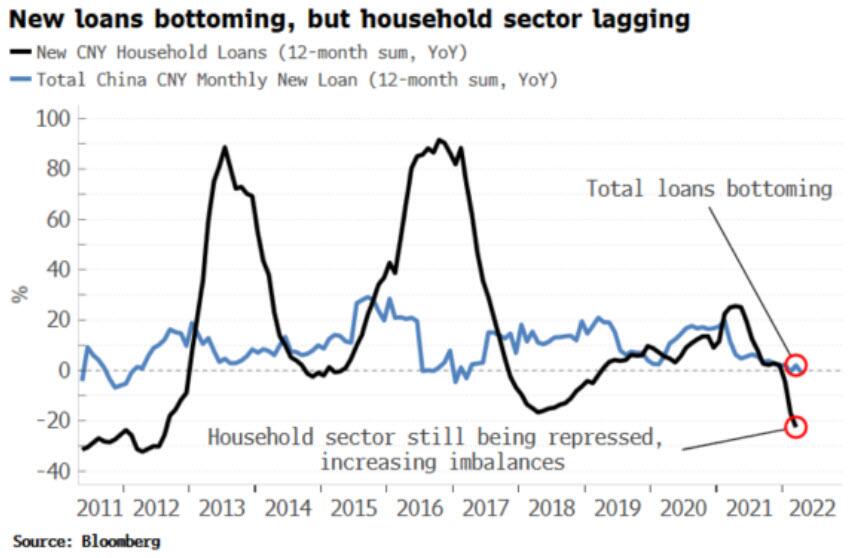

China Credit Creation Craters, Sparking Speculation Of A Growth, Stock Bounce

FRIDAY, MAY 13, 2022 – 03:05 PM

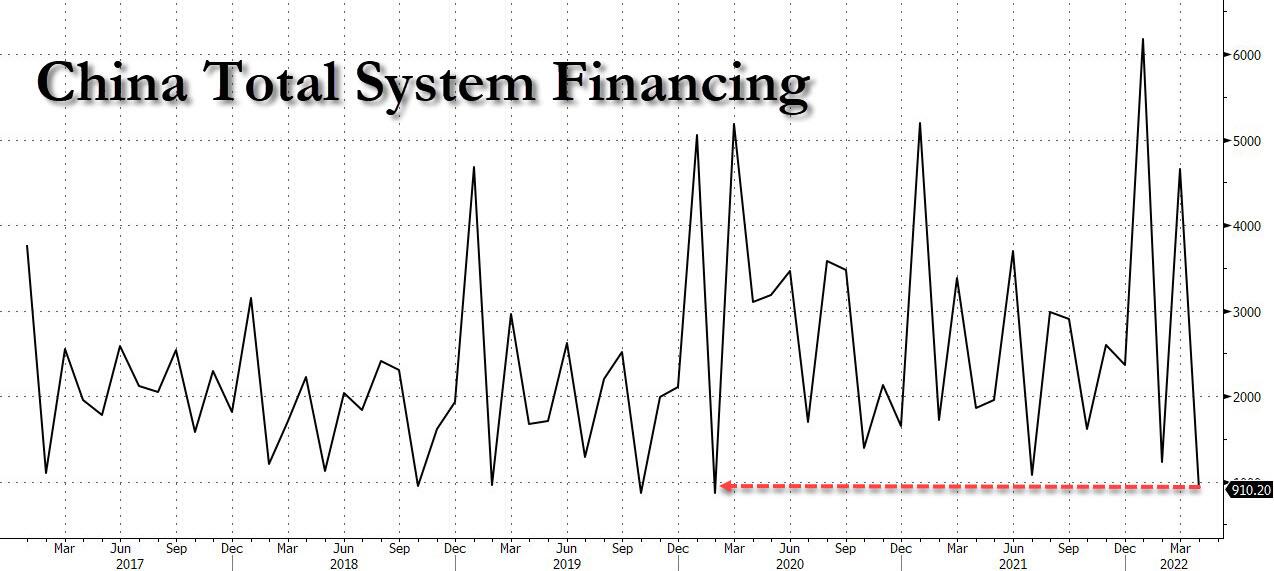

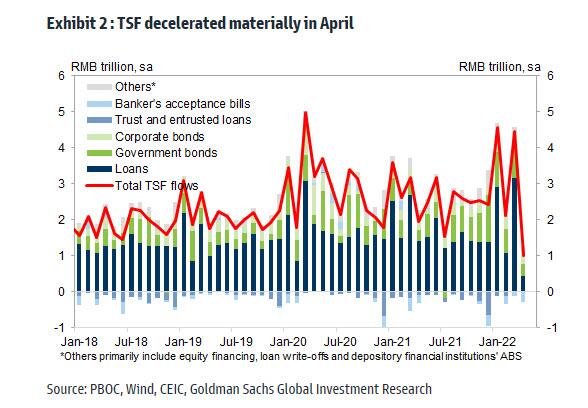

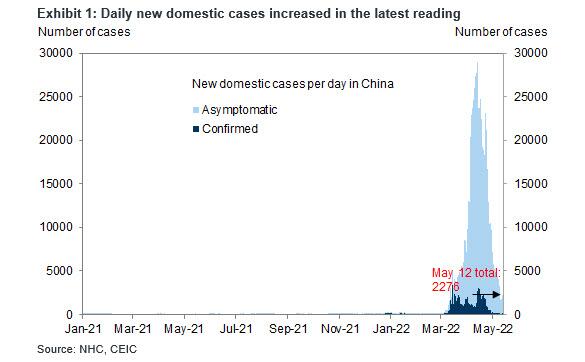

While we wait for China’s economic data dump due Monday, when industrial production and retail sales are expected to crater to deep negative territory as a result of the ongoing covid lockdowns, this morning we got a harsh reminder just how hard the world’s 2nd biggest economy has been hit when Beijing reported that April total social financing and RMB loans came in much below market expectations, even as M2 growth accelerated and was above market expectations on the back of the RRR cut and more expansionary fiscal policy stance.

Here are the details:

- New CNY loans: RMB 645.4 bn in April, badly missing consensus of RMB 1520bn. Outstanding CNY loan growth: 10.9% yoy in April vs March 11.4% yoy; Overall CNY loans growth decelerated materially and grew 6.6% mom annualized sa from 18.1% in March.

- Total social financing RMB 910bn in April, badly missing consensus growth of RMB 2200bn; Total social financing (TSF) was well below expectations after a strong acceleration in March. The sequential growth of TSF stock decelerated to 3.9% mom annualized in April, the slowest sequential growth in the past decade.

- TSF stock growth was 10.2% yoy in April, slower than the 10.6% in March. The implied month-on-month growth of TSF stock decelerated to 3.9% from 14.4% in March.

- M2: 10.5% yoy in April vs. above consensus of 9.9% yoy. March: 9.7% yoy; M2 year-on-year growth accelerated on the other hand to 10.5% yoy in April, vs 9.7% in March, and expanded by 13.8% in month-over-month annualized terms, vs 24.4% in March.