May 17, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1820.30 UP $5.40

SILVER: $21.51 UP $.22

ACCESS MARKET: GOLD $1813.60

SILVER: $21.59

Bitcoin morning price: $30,336 UP 533

Bitcoin: afternoon price: $30,229 UP 426

Platinum price: closing UP $13.35 to $956.55

Palladium price; closing UP $28.60 at $2046.60

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices percentage of JPMorgan notices filed: 6/6

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,813.500000000 USD

INTENT DATE: 05/16/2022 DELIVERY DATE: 05/18/2022

FIRM ORG FIRM NAME ISSUED STOPPED

661 C JP MORGAN 6

905 C ADM 6

TOTAL: 6 6

MONTH TO DATE: 5,387

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 6 NOTICE(S) FOR 600 OZ (0.01866 TONNES)

total notices so far: 5387 contracts for 538,700. oz (16.755 tonnes)

SILVER NOTICES:

163 NOTICE(S) FILED 815,000 OZ/

total number of notices filed so far this month 5022 : for 25,110,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $5.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD

INVENTORY RESTS AT 1053.28 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 22 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 565.085 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 372 CONTRACTS TO 142,915 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE SMALL GAIN IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.52 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.31) AND IT SEEMS THAT SILVER SHORT SPECULATORS HAVE ALSO BEEN CAUGHT AS THE COMMERCIALS ARE NOW NET LONG.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE. JUMP //NEW STANDING 28U.035 MILLION OZ/ // V) SMALL SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -16

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 11 days, total 16,174, contracts: 80.870 million oz OR 7.34 MILLION OZ PER DAY. (1470CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 80.87 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 80.87 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 372 DESPITE OUR STRONG $0.31 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 910 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE SPECULATOR SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 195,000 OZ QUEUE. JUMP //NEW STANDING 28.035 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 1298 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.490 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 163 NOTICE FILED TODAY FOR 815,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 9100 CONTRACTS TO 557,303 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –1695 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $5.40//COMEX GOLD TRADING/MONDAY /.AS IN SILVER WE MUST HAD HUGE SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST MASSIVE SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 3200 OZ//NEW STANDING 17.9502 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $5.40 WITH RESPECT TO MONDAY’S TRADING

WE HAD A STRONG SIZED LOSS OF 7461 OI CONTRACTS (23.206 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 5766 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 557,303.

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7461, WITH 9100 CONTRACTS DECREASED AT THE COMEX AND 1939 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 7461 CONTRACTS OR 23.226 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1639) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9100,): TOTAL LOSS IN THE TWO EXCHANGES 7461 CONTRACTS. WE NO DOUBT HAD 1) HUGE SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 3200 OZ//NEW STANDING 16.9502 /// 3) ZERO LONG LIQUIDATION//MASSIVE SPECULATOR SHORT COVERING //.,4) STRONG SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

47,002 CONTRACTS OR 4,700,200 OR 146.19 TONNES 11 TRADING DAY(S) AND THUS AVERAGING: 4272 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES: 146.19 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 146.19/3550 x 100% TONNES 4.11% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 146.19 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A SMALL SIZED 372 CONTRACT OI TO 142,915 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 910 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 910 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 372 CONTRACTS AND ADD TO THE 910 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF1282 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.410 MILLION OZ

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.52 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 19.95 PTS OR 0.65% //Hang Sang CLOSED UP 652.31 PTS OR 3.27% /The Nikkei closed UP 112.70 OR 0.42% //Australia’s all ordinaires CLOSED UP 0.33% /Chinese yuan (ONSHORE) closed UP 6,7244 /Oil UP TO 115.47 dollars per barrel for WTI and UP TO 115.48 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7249 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7349: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9100 CONTRACTS TO 557,303 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS STRONG COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $5.40 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1639 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1639 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :1639 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1639 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5766 CONTRACTS IN THAT 1639 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 7405 CONTRACTS..AND YET THIS GAIN OCCURRED WITH OUR GAIN IN PRICE OF GOLD $5.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (17.9502),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 17.9502 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $5.40) BUT IT SEEMS WERE QUITE SUCCESSFUL IN KNOCKING OFF SPECULATOR SHORTS// WE HAVE REGISTERED A STRONG SIZED LOSS OF 23.206 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (17.9502 TONNES)…

WE HAD 1695 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 7461 CONTRACTS OR 746100 OZ OR 23.206

TONNES

Estimated gold volume today: 148,307/// poor

Confirmed volume yesterday:189,792 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 17

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 36,713.137 oz Brinks Delaware Int. Delaware includes15 kilobars Delaware 24 kilobars Int. Delaware |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 69,610.950 OZ INCLUDES 2000 kilobars Loomis Brinks Delaware Loomis |

| No of oz served (contracts) today | 6 notice(s)600 OZ 0.01866 TONNES |

| No of oz to be served (notices) | 384 contracts 38,400 oz 1.194 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5387 notices538,700 OZ 16.755 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

3 customer deposits

i)Into Brinks: 4410.19 oz

ii) Into Delaware 898.760 oz

iii) Into Loomis: 64,302.000 oz (2,000 kilobars)

3 customer withdrawals:

i) Out of Brinks: 35,459.250 oz

ii) Out of Delaware: 482.265 oz (15 kilobars)

iii) Out of Int. Delaware 771.624 oz (24 kilobars)

total withdrawal: 36,713.137 oz

ADJUSTMENTS: a) Brinks//dealer to customer 58,308.608 oz

b) Manfra: 3672.215 oz//dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 390 contracts having GAINED 27 contracts

We had 5 notices filed on MONDAY, so we gained 32 contracts or AN ADDITIONAL 3,200 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 15,474 contracts down to 250,522 contracts

July has a GAIN OF 110 OI to stand at 313

August has a gain of 6069 contracts up to 248,235 contracts

We had 6 notice(s) filed today for 600 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (5387) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 390 CONTRACTS ) minus the number of notices served upon today 6 x 100 oz per contract equals 577100 OZ OR 17.9502 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (5387) x 100 oz+ (390) OI for the front month minus the number of notices served upon today (6} x 100 oz} which equals 577,100 oz standing OR 17.9502 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 17.9502 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,026,795.134 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,967,538.084 OZ

TOTAL ELIGIBLE GOLD: 17,897,202.217 OZ

TOTAL OF ALL REGISTERED GOLD: 18,070,335.867 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,948,662.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 17

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 919,623.750 oz Brinks CNT JPM Manfra |

| Deposits to the Dealer Inventory | 584,850.320 OZ Int Delaware |

| Deposits to the Customer Inventory | 52,611.387 oz Delaware |

| No of oz served today (contracts) | 163CONTRACT(S)815,000 OZ) |

| No of oz to be served (notices) | 585 contracts (2,925,000 oz) |

| Total monthly oz silver served (contracts) | 5022 contracts 25,110,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) One deposit into the dealer account

i) into Int. Delaware: 584,850.320 oz

total dealer deposits: 584,850.320 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 52,611.347 oz

total deposit: 52,611.347 oz oz

JPMorgan has a total silver weight: 176.885 million oz/338.616 million =52.21% of comex

Comex withdrawals: 4

i) Out of CNT 24,998.920 oz

ii) Out of Brinks 33,412.000 oz

iii) Out of JPMorgan: 578,606.400 oz

iv) Out of Manfra: 202,606.380 oz

total withdrawal 919,623.750 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 81.099 MILLION OZ

TOTAL REG + ELIG. 338.416 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 748 HAVING GAINED 39 CONTRACTS. WE HAD 0 NOTICES FILED ON MONDAY

SO WE GAINED 39 CONTRACTS OR AN QUEUE. JUMP OF 195,000 OZ

JUNE HAD A LOSS OF 12 TO STAND AT 1521

JULY HAD A LOSS OF 39 CONTRACTS DOWN TO 112,963 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 163 for 815,000 oz

Comex volumes: 38,095// est. volume today// fair

Comex volume: confirmed yesterday: 649,187contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5022 x 5,000 oz = 25,110,000 oz

to which we add the difference between the open interest for the front month of MAY(748) and the number of notices served upon today 163 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2021 contract month: 5022 (notices served so far) x 5000 oz + OI for front month of MAY (748) – number of notices served upon today (163) x 5000 oz of silver standing for the MAY contract month equates 28,035,000 oz. .

We GAINED 50 contracts or AN ADDITIONAL 250,000 OZ will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1053.28 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 565.085 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

The Bank of England admits it is helpless fighting massive inflation hitting his country

(London Telegraph)

Bank of England admits helplessness against inflation

Submitted by admin on Mon, 2022-05-16 13:17Section: Daily Dispatches

By James Warrington and Giulia Bottaro

The Telegraph, London

Monday, May 16, 2022

The governor of the Bank of England has claimed that policy makers have been left helpless in the face of surging inflation.

Appearing in front of MPs today, Andrew Bailey admitted he had felt helpless to control soaring prices amid an energy market shock and the war in Ukraine, adding: “It;s a very, very difficult place for us to be in.”

Fellow Monetary Policy Committee members Dave Ramsden and Michael Saunders said external factors contributed around 80% of the recent inflation surge and insisted that even if the bank had raised interest rates more aggressively, it’s unlikely inflation would have fallen back to the target of 2%.

The hearing comes amid a slew of attacks by senior Tory MPs on the Bank of England for its handling of the cost-of-living crisis. …

… For the remainder of the report:

end

Interesting: Russia gives Credit Bank a license to export/import gold.

(Reuters)

Russia gives Credit Bank of Moscow license to export gold

Submitted by admin on Mon, 2022-05-16 19:15Section: Daily Dispatches

From Reuters

Monday, May 16, 2022

Credit Bank of Moscow, one of Russia’s largest private lenders, has obtained a gold export licence from the government, it said today, becoming the latest Russian bank to turn to precious metals trade to offset the impact of sanctions.

The main operators of the gold market in Russia and its largest lenders — Sberbank and VTB, have been hit by harsh Western sanctions imposed on Russia after it sent tens of thousands of troops into Ukraine on Feb. 24.

“MKB has a dedicated focus on developing operations with precious metals,” MKB said in a statement. The bank has also been subject to sanctions in the United States but it said they were not “blocking” its activity. …

… For the remainder of the report:

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIAMONDS

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7244

OFFSHORE YUAN: 6.7359

HANG SANG CLOSED UP 652.31 PTS OR 3.67%

2. Nikkei closed 112.70 OR 0.42%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX UP TO 103.33/Euro RISES TO 1.0545

3b Japan 10 YR bond yield: FALLS TO. +.240/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.27/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield FALLS TO 3.54

3j Gold at $1833.75 silver at: 21.75 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 roubles/dollar; ROUBLE AT 63.40

3m oil into the 115 dollar handle for WTI and 115 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.27 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9922– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0463well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

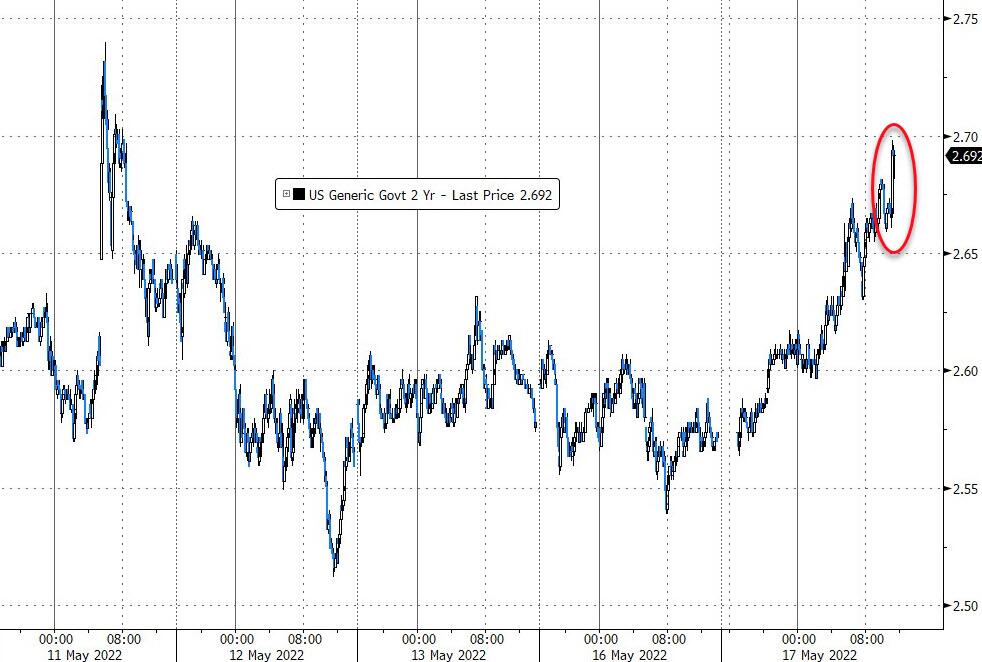

USA 10 YR BOND YIELD: 2.920- UP 4 BASIS PTS

USA 30 YR BOND YIELD: 3.118 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.73

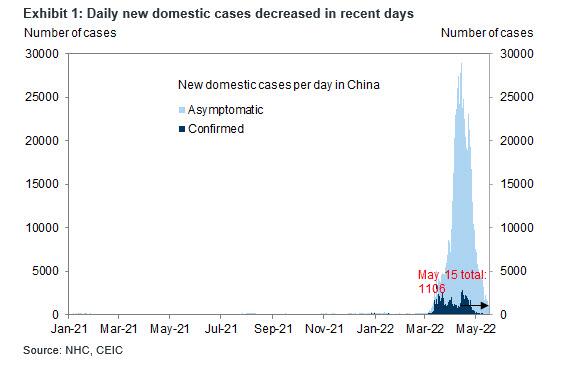

Futures Jump Amid Optimism China’s Covid Lockdowns Are Ending

TUESDAY, MAY 17, 2022 – 07:43 AM

Another day, another dead cat-bouncing, bear market rally.

After Monday’s flattish session which saw tech names slump on fresh inflation fears, Nasdaq futures rebounded on Tuesday, setting up technology stocks for solid gains after a six-week rout as investors were encouraged by China’s easing covid lockdowns and amid speculation that Beijing regulators may ease a yearlong clampdown on internet companies at an upcoming meeting with tech executives. Nasdaq 100 futures jumped 2% by 7:00 a.m. in New York after the underlying gauge sank on Monday on concerns about a slowdown in economic growth; S&P 500 futures rose 1.6%. Treasury yields rose modestly above 2.90%, and the dollar retreated. Bitcoin managed to rebound back over $30K.

Confirming what we said almost three weeks ago, Shanghai reported three days of zero community transmission, a milestone that could lead officials to start unwinding a punishing lockdown. However, flareups elsewhere in China showed how hard it is to tackle the omicron strain.

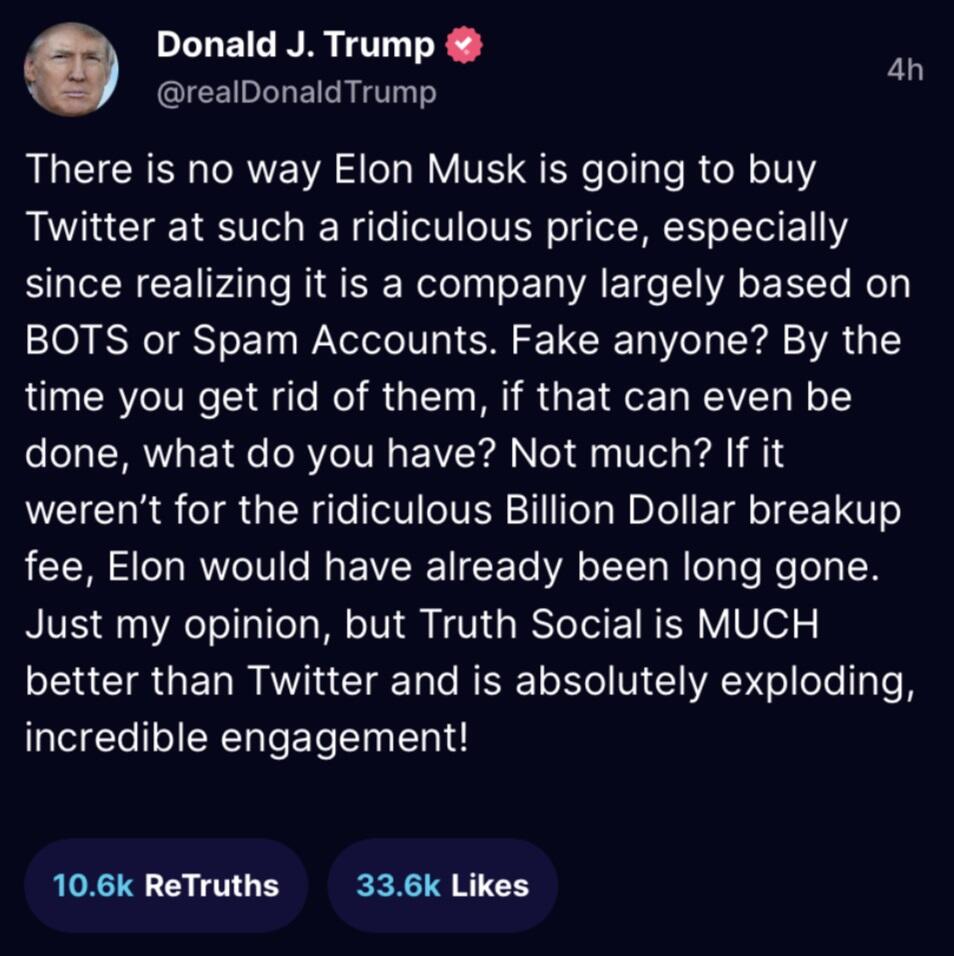

Among notable moves in US premarket trading, Twitter shares fell 3.3%, set to extend declines for an eighth straight session amid uncertainties around the deal with Elon Musk, while Citigroup rose 4.9% after Warren Buffett’s Berkshire Hathaway unexpectedly disclosed a new stake in the lender, a return to banks for the billionaire who purged many of his bank holdings several years ago. Tech names including Advanced Micro Devices, Tesla and Nvidia were among the biggest premarket gainers as growing recession concerns prompt markets to reasses just how many rate hikes the Fed will pull off before it is forced to reverse. Cryptocurrency-exposed stocks climbed as Bitcoin rose above $30,000 on Tuesday in cautious trading, with the fallout from a collapsed stablecoin continuing to keep sentiment in check. Chinese stocks in US jumped across the board in premarket trading on speculation that regulators may ease a yearlong clampdown on internet companies at an upcoming meeting with tech executives. Here are the most notable premarket movers:

- Twitter (TWTR US) shares fell 2.4% in premarket trading, on course to extend their seven-day streak of declines, as uncertainties around a deal by buyer Elon Musk weigh on the stock. Tesla (TSLA US) shares rallied 3% in premarket trading.

- Chinese stocks in US jump across the board in premarket trading on speculation that regulators may ease a yearlong clampdown on internet companies at an upcoming meeting with tech executives. Alibaba (BABA US) +6.2%, JD.com (JD US) +5.6%, Pinduoduo (PDD US) +7% and Baidu (BIDU US) +3.6%

- Cryptocurrency-exposed stocks climb in US premarket as Bitcoin rises above $30,000 on Tuesday in cautious trading, with the fallout from a collapsed stablecoin continuing to keep sentiment in check. Riot Blockchain (RIOT US) +7.8%; Coinbase (COIN US) +6.8%; Marathon Digital (MARA US) +6.1%

- Advanced Micro Devices (AMD US) upgraded to overweight from neutral at Piper Sandler, which says in note that the company’s core businesses are running well and mid-to-long-term catalysts remain intact. Stock gains 3.6% in New York premarket trading.

- United Airlines Holdings’ (UAL US) updated second-quarter guidance is “a solid step in the right direction,” Citi says. United’s shares gained 4.3% in premarket trading.

- Bird Global (BRDS US) shares jump as much as 40% in US premarket trading with DA Davidson noting management’s announcement of a plan to streamline operations.

- Take-Two (TTWO US) reported better-than-expected fourth-quarter earnings helped by popular video games like NBA 2K22. The company’s shares rise 5.4% in premarket trading.

- Global-e Online (GLBE US) shares slump as much as 30% in US premarket trading as analysts slash their price targets on the e-commerce software firm after it lowered its full-year guidance for revenue and gross merchandise value.

- Imperial Petroleum (IMPP US) shares plunge 48% in US premarket trading. The shipping company priced an underwritten public offering of 72.7m units at $0.55 per unit, with expected gross proceeds of ~$40m.

US stocks have been roiled in the past six weeks as the combination of high inflation and hawkish central banks fueled fears of a potential recession. While some strategists including Morgan Stanley’s Michael Wilson expect equities to fall further before finding a floor, they don’t foresee a recession as their base case. The main focus today will be on US retail sales data, which are expected to show a rise of 1% in April.

“Investors’ appetite for riskier assets is on the rise after many welcomed today’s positive unemployment and GDP figures” from the eurozone and UK, said Pierre Veyret, an analyst at ActivTrades Plc. “The improving virus situation in China is also blowing a wind of relief in investors’ trading minds.”

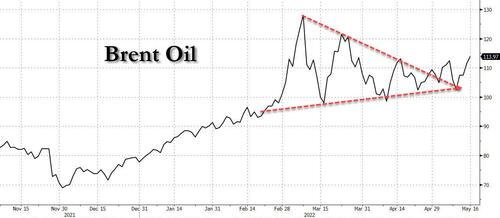

A challenging global economic outlook amid elevated food and record fuel costs, and tightening monetary settings continues to shape sentiment. Oil has jumped to about $114 a barrel and an index of agricultural prices is at a record high. But one bond-market measure – the five-year breakeven rate – is signaling inflation has peaked, while the latest virus developments raised hopes China’s damaging lockdowns may soon be eased.

On Monday, New York Fed President John Williams on Monday downplayed deteriorating liquidity conditions in financial markets, saying it was to be expected as investors grapple with uncertainty over global events and shifting U.S. monetary policy. No less than six Fed speakers – including Chair Jerome Powell – are due to speak later Tuesday.

In Europe, technology and basic-resources stocks led a broad-based advance of the Stoxx Europe 600 following a rally in Chinese tech shares on optimism Beijing may ease up on a yearlong clampdown. Italy’s FTSE MIB adds 1.6%, FTSE 100 lags, adding 0.7%. Miners, financial services and banks are the strongest-performing sectors. Equities were also buoyed by data showing the euro-area economy expanded more than initially estimated at the start of the year as the region moved past a wave of Covid-19 infections and defied headwinds from the early days of the war in Ukraine. Here are the biggest European movers:

- Clariant shares rise as much as 8.7% after the specialty chemical company announced its governance agreement with SABIC will expire at the June 24 AGM, and won’t be renewed.

- Imperial Brands climbs as much as 7.9% after the tobacco company reduced its losses from next-generation products and continued on a turnaround plan.

- Daimler Truck gains as much as 7.8% in Frankfurt; Oddo BHF notes strong 1Q report that will reassure in the current environment, while Citi says the company delivered an “encouraging” set of results.

- Engie rises as much as 6.9%, hitting the highest since March 1, after the French energy company boosted its profit guidance on higher European energy prices.

- CaixaBank advances as much as 5.4% after the Spanish lender released a new strategic plan that predicts a jump in a key profitability metric and announced a EU1.8b share buyback program.

- Prosus and Naspers both raised to overweight from neutral at JPMorgan following the broker’s upgrade of Tencent. Prosus shares gain as much as 6.5% in Amsterdam, Naspers climbs as much as 6.7% in Johannesburg.

- ContourGlobal gains as much as 34% after US private equity firm KKR agreed to buy the power generation business for 263.6p/share in cash, representing a premium of 36% to Monday’s close.

- Vodafone erases losses after dropping as much as 4.2% as the telecom operator’s forecast for adjusted Ebitda after-leases missed consensus estimates at mid- point.

Earlier in the session, Asian stocks advanced for a third day — its longest winning streak since mid-March — amid a jump in some technology firms on the back of hopes for an unwind of Chinese lockdowns that have hurt the global economic outlook as well as a dialing back of Beijing’s regulatory crackdowns. The MSCI Asia-Pacific Index climbed as much as 1.5%, on track for a third day of gains. Chinese tech giants Tencent and Alibaba contributed most to the gain, while chipmakers TSMC and Samsung also helped. Shanghai reported no new Covid infections in the broader community for a third day, hitting a crucial milestone toward reduced restrictions. China’s top political advisory body is hosting a meeting Tuesday with some of the nation’s largest private-sector firms, sparking hopes for an improved business climate.

“The mood in Asia is risk on,” said Xue Hua Cui, a China equity analyst at Meritz Securities in Seoul. “Whether this remains a dead cat bounce or not depends on how quickly demand recovers following the end of Shanghai lockdowns.” Hong Kong outperformed, with the Hang Seng Index rising more than 3%. Benchmarks in India also advanced more than 2%, even as state-run insurer Life Insurance Corporation of India dropped in its Mumbai trading debut after a record initial public offering for the nation.

Japanese equities gained with Asian peers amid hopes that China will ease up on Covid lockdowns and regulatory crackdowns. The Topix rose 0.2% to close at 1,866.71. Tokyo time, while the Nikkei advanced 0.4% to 26,659.75. Recruit Holdings contributed the most to the Topix gain, rising 2% after its earnings report. Out of 2,172 shares in the index, 1,164 rose and 932 fell, while 76 were unchanged.

Australia’s S&P/ASX 200 index rose 0.3% to close at 7,112.50, taking its winning run to a third session. Miners and banks contributed the most to the gauge’s advance. Beach Energy was among the top performers, climbing with other energy shares as oil rallied. Brambles was the biggest laggard after saying CVC won’t be putting forward a proposal for the pallet maker. Investors also assessed minutes from the RBA’s May meeting. The central bank said it considered three options for the size of its first interest-rate increase since 2010. In New Zealand, the S&P/NZX 50 index fell 0.2% to 11,137.88.

India’s key gauges surged on Tuesday, boosted by Reliance Industries Ltd. which climbed the most since early March. Still, Life Insurance Corp. of India, the country’s biggest listing so far, slumped on debut. The S&P BSE Sensex rose 2.5%, its biggest jump in three months, to 54,318.47 in Mumbai, while the NSE Nifty 50 Index advanced 2.6%. All of the 19 sector sub-indexes compiled by BSE Ltd. climbed, led by a gauge of metal companies. Reliance Industries advanced 4.2%, providing the biggest boost to the Sensex, which had all 30 members trading higher. “It’s a much-needed breather for the bulls after five weeks of slide and we may further rise,” said Ajit Mishra, vice-president research at Religare Broking Ltd. “Since all the sectors are participating in the rebound, we suggest focusing more on stock selection. Despite strong gains in the broader market, shares in the state-controlled insurer plunged 7.8%, following a $2.7 billion IPO, India’s biggest on record. The stock trimmed losses from the low, but failed to touch the listing price in the session. LIC’s first-day performance makes for the second-worst debut among 11 global companies that listed this year after raising at least $1 billion through first-time share sales.

In FX, the Bloomberg Dollar Spot Index fell a third consecutive day and the greenback weakened against all of its Group-of-10 peers apart from the yen. The pound lead G-10 gains followed by Scandinavian and Antipodean currencies. The pound rallied and gilts slumped across the curve after a stronger-than-expected reading of the UK employment data stoked speculation that a tighter labor market may prompt the BOE to continue its monetary tightening cycle beyond a widely expected rate rise next month. Average weekly earnings surged 7% in the three months through March, compared to the 5.4% figure economists had expected. The euro rose on the back of a broadly weaker dollar. Bunds slid as haven demand was unwound. Italian bonds also tumbled as money markets wagered on up to 98bps of ECB hikes by December. The Aussie strengthened for a third day while Australia’s sovereign bonds fell after minutes from RBA’s May meeting indicated the central bank considered an outsized rate hike. The RBA said it considered three options for the size of its first interest-rate increase since 2010, according to minutes of its May 3 policy meeting, when it raised the cash rate by 25 basis points. The Australian and New Zealand dollars also benefitted from expectations that Covid lockdowns in Hong Kong and Shanghai will be lifted. The yen gave up earlier gains as US yields resumed their climb, which also weighed on Japan government bonds.

In rates, yields rose as Treasuries cheapened with losses led by front-end of the curve, following a sharper bear flattening move across EGBs after ECB Governing Council member Klaas Knot said he supports a quarter-point increase in interest rates in July and that a bigger move may be justified if data show inflation worsening. US Treasury yields cheaper by up to 5.5bp across front-end of the curve, the 10Y TSY trading at 2.91% last and flattening 2s10s spread by 2.2bp on the day; 2-year German yields cheaper by 23bp on the day following Knot comments while German 10s are cheaper by 4bp vs. Treasuries. In U.S. session, focus on a stacked Fed speaker slate led by Chair Jerome Powell who will be interviewed during a Wall Street Journal live event in the afternoon. The Dollar issuance slate includes Export Development Canada 5Y SOFR, OKB 3Y SOFR and JICA 5Y SOFR; six deals priced $9.1n Monday in order books that were 3.3x oversubscribed

In commodities, WTI drifts 0.2% higher to trade at around $114. Spot gold rises roughly $3 to trade above $1,825/oz. Base metals are mixed; LME tin falls 1.6% while LME zinc gains 2.4%. European gas prices hit four-week low after EU revised guidelines for purchases of Russian supplies.

To the day ahead now, and there’s an array of central bank speakers including Fed Chair Powell, along with the Fed’s Bullard, Harker, Kashkari, Mester and Evans, ECB President Lagarde and BoE Deputy Governor Cunliffe. Data releases include US retail sales, industrial production and capacity utilisation for April, along with the NAHB’s housing market index for May. Elsewhere, there’s also the UK unemployment reading for March. Finally, earnings releases include Walmart and Home Depot.

Market Snapshot

- S&P 500 futures up 1.3% to 4,057.75

- STOXX Europe 600 up 1.6% to 440.47

- MXAP up 1.4% to 162.83

- MXAPJ up 2.2% to 535.18

- Nikkei up 0.4% to 26,659.75

- Topix up 0.2% to 1,866.71

- Hang Seng Index up 3.3% to 20,602.52

- Shanghai Composite up 0.6% to 3,093.70

- Sensex up 2.1% to 54,080.42

- Australia S&P/ASX 200 up 0.3% to 7,112.53

- Kospi up 0.9% to 2,620.44

- German 10Y yield little changed at 0.99%

- Euro up 0.4% to $1.0480

- Brent Futures up 0.3% to $114.53/bbl

- Gold spot up 0.2% to $1,827.11

- U.S. Dollar Index down 0.42% to 103.75

Top Overnight News from Bloomberg

- The euro-area economy grew more than initially estimated at the start of the year as the region moved past a wave of Covid-19 infections and defied headwinds from the early days of the war in Ukraine. Economic output rose 0.3% in the first quarter, exceeding a flash reading of 0.2%, according to Eurostat data released Tuesday. Employment, meanwhile, gained 0.5% during same period

- The UK will lay out its plan to amend its post-Brexit trade deal Tuesday in a direct challenge to the European Union, which is insisting that Prime Minister Boris Johnson must honor the agreement he signed

- China’s main bond trading platform for foreign investors has quietly stopped providing data on their transactions, a move that may heighten concerns about transparency in the nation’s $20 trillion debt market after record outflows

- The American and European Union chambers of commerce in separate briefings said their members are rethinking their supply chains and whether to expand investment in the face of China’s zero tolerance approach to combating Covid-19

- Turkish President Recep Tayyip Erdogan said he won’t allow Sweden and Finland to join NATO because of their stances on Kurdish militants, throwing a wrench into plans to strengthen the western military alliance after Russia’s invasion of Ukraine

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were positive but with gains capped after the uninspiring lead from Wall St and growth concerns. ASX 200 was kept afloat by strength in the commodity-related sectors after recent gains in underlying prices. Nikkei 225 traded marginally higher with Japan seeking to pass an extra budget by month-end and will begin permitting entry to a small number of tourists. Hang Seng and Shanghai Comp were both firmer with tech spearheading the outperformance in Hong Kong amid hopes of an easing of the crackdown on the sector, while the mainland lagged amid economic concerns and despite Shanghai reporting no cases outside of quarantine for a 3rd consecutive day.

Top Asian News

- China’s state planner said China’s economy faces increasing downward pressure, while it will step up support for manufacturing companies, contact-intensive services, small companies and home businesses, according to Reuters.

- Senior Chinese officials are to meet with tech industry chiefs today amid talk of crackdown easing, according to Nikkei. It was later reported that China’s top political consultative body began a conference on promoting the sustainable and healthy development of the digital economy, according to state media.

- Hong Kong Chief Executive Carrie Lam said they will proceed with the planned COVID curbs easing on May 19th, according to Bloomberg.

- BoJ Deputy Governor Amamiya said it is important to continue current powerful easing to firmly support the economy and that long-term interest rates have been stable since the adoption of fixed-rate operations, while he added that if monetary easing is reduced now, it would make the 2% price goal an even more distant target, according to Reuters.

- Japan is to permit small groups of tourists to visit this month as a trial ahead of its border reopening, according to Japan Times.

European bourses are firmer across the board, Euro Stoxx 50 +1.7%, taking impetus from and extending on a positive APAC handover as the regions COVID situation improves. Stateside, futures are firmer across the board, ES +1.8%, following yesterday’s relatively lacklustre session with participants awaiting numerous Fed speak, including Chair Powell. Twitter (TWTR) prospective purchaser Musk says that his offer was based on the Co.’s SEC filing being accurate, however, yesterday the CEO refused to show proof of less than 5% of fake/spam accounts; deal cannot move forward until this has been disclosed. -3.5% in the pre-market. Home Depot Inc (HD) Q1 2023 (USD): EPS 4.09 (exp. 3.67/3.67 GAAP), Revenue 38.9bln (exp. 36.71bln); Raises Fiscal 2022 Guidance. +2.5% in the pre-market

Top European News

- UK Foreign Secretary Truss is to declare her intention to bring forward legislation that rips up parts of the post-Brexit trade deal on Northern Ireland, according to LBC. Expected around 12:30BST/07:30ET

- Irish Foreign Minister Coveney says he spoke with UK Foreign Minister Truss on Monday, notes the EU and UK sides haven’t met since February and says it is “time to get back to the table”

- ECB is expected to raise the deposit rate in July according to 39 out of 39 respondents in a Reuters survey, while 26 out of 48 economists see the deposit rate at 0% in Q3 and 21 out of 48 see the deposit rate at 0.25% in Q4.

FX

- Pound the standout G10 performer in wake of outstanding UK labour report; Cable clears string of resistance levels on the way towards 1.2500 and EUR/GBP probes 0.8400 after breaching technical supports .

- Kiwi and Aussie relish renewed risk appetite and latter also helped by hawkish RBA minutes; NZD/USD above 0.6350 and 1.3bln option expiries at 0.6300, AUD/USD back on 0.7000 handle.

- Greenback concedes ground ahead of top tier US data and raft of Fed speakers including chair Powell, DXY down to 103.470 vs 104.320 at best; latest session low in wake of ECB’s Knot.

- Franc, Euro and Loonie all up at the expense of the Buck but latter also fuelled by WTI topping USD 115/bbl; USD/CHF sub-parity, EUR/USD surpassing 1.05 in wake of hawk-Knot and USD/CAD near 1.2800.

- Yen lags as risk sentiment improves and yields outside of Japan rebound firmly; USD/JPY rebounds through 129.00 and just over 129.50.

- Norwegian Crown boosted by Brent in stark contrast to crude import dependent Turkish Lira and Indian Rupee; EUR/NOK under 10.1500, USD/TRY touches 15.8850 and USD/INR crosses 78.0000 to set fresh ATH

Fixed Income

- Bonds make way for risk revival and brace for US data amidst a raft of global Central Bank speakers.

- Bunds down to 152.74, Gilts hit 119.25 and 10 year T-note as low as 119-08 before paring some heavy declines

- UK DMO gets welcome reception for 2015 issuance, but new German Schatz receives cold shoulder even before hawkish comments from ECB’s Knot not ruling out a 50 bp July hike if data warrants more than 25 bp

- China’s main bond trading platform is said to have stopped the reporting of bond trades by foreigners following the market downside, according to Bloomberg.

Commodities

- WTI and Brent are firmer in-fitting with broader risk appetite and the aforementioned China COVID improvement; posting gains of circa USD 0.80/bbl.

- However, upside remains capped amid the ongoing standoff between the EU and Hungary over a Russian import embargo.

- Iran set June Iranian light crude price to Asia at Oman/Dubai + USD 4.25/bbl, according to a Reuters source

- OPEC+ production was 2.6mln below quotas in April, according to a report cited by Reuters; Russian production 1.28mln below the required level in April, sources add.

- Spot gold is firmer, taking impetus from the USD pressure; though, the yellow metal is yet to move out of earlier ranges.

- Base metals are bid on risk while Wheat declined amid reports that India is easing some of its export restrictions.

Central Banks

- ECB’s Knot says a 25bp hike in July is realistic; says a 50bp rate hike should not be excluded if data in the next few months suggests that inflation is broadening and accumulating.

- NBH’s Virag says they will increase rates further, via Reuters citing slides.

- NBP’s Kotecki says that interest rates will continue to move higher but it is currently difficult to define their target level.

US Event Calendar

- 08:30: April Retail Sales Advance MoM, est. 1.0%, prior 0.5%, revised 0.7%

- April Retail Sales Ex Auto MoM, est. 0.4%, prior 1.1%, revised 1.4%

- April Retail Sales Ex Auto and Gas, est. 0.7%, prior 0.2%, revised 0.7%

- April Retail Sales Control Group, est. 0.7%, prior -0.1%, revised 0.7%

- 09:15: April Industrial Production MoM, est. 0.5%, prior 0.9%

- 09:15: April Manufacturing (SIC) Production, est. 0.4%, prior 0.9%

- 10:00: March Business Inventories, est. 1.9%, prior 1.5%

- 10:00: May NAHB Housing Market Index, est. 75, prior 77

Fed Speakers

- 08:00: Fed’s Bullard Discusses Economic Outlook

- 09:15: Fed’s Harker Discusses Healthcare as Economic Driver

- 12:30: Fed’s Kashkari Takes Part in a Moderated Townhall Discussion

- 14:00: Powell Interviewed During Wall Street Journal Live Event

- 14:30: Fed’s Mester Gives Opening Remarks to Panel on Inflation

- 18:45: Fed’s Evans Discusses the Economic Outlook

DB’s Jim Reid concludes the overnight wrap

Recession fears have continued to dominate markets over the last 24 hours, but Deutsche Bank Research is still the only bank to actually forecast one in the US. The tone was set for the day after some incredibly weak data out of China that we discussed yesterday, but that was then followed up with disappointing survey data from the US, which arrived ahead of an array of central bank speakers today (including Fed Chair Powell).

Although markets in Asia are bouncing a little this morning, the S&P 500 (-0.39%) last night followed up its run of 6 consecutive weekly declines with a further loss. It was another volatile day that saw stocks trade in a 1.5% range, including going into positive territory briefly in the afternoon before slipping into the close. Sector dispersion was pretty wide, with energy shares gaining +2.62% and consumer discretionary stocks falling -2.12%, led by Tesla retreating -5.88%. Tech was the next biggest laggard, with the NASDAQ (-1.20%) and FANG+ index (-1.34%) underperforming the broader universe. That still leaves the S&P 500 index around 2% above its recent closing low on Thursday, but remember that if we get another week in negative territory, it would still be the first time since 2001 that the S&P has posted 7 consecutive weekly declines. After opening the week much lower, the STOXX 600 did recover through that day to post a slight +0.04% gain yesterday, continuing its recent outperformance.

The prevailing risk-off mood meant that longer-dated sovereign bond yields also ended the day lower for the most part. Those on 10yr Treasuries were down -3.6bps to close at 2.88%, having already fallen by -20.8bps over the previous week as investors priced in a growing risk of recession over Fed and inflation concerns. The decline was split between breakevens and real yields. To be fair 10yr yields have gained +3.3bps this morning in Asia, thus almost reversing yesterday’s losses so far.

At the short-end, the amount of tightening priced in over the near-term has subsided somewhat of late, as it seems investors are searching high and low for a Fed put following a poor run of risk asset performance and the prior relentless repricing towards a more aggressive monetary tightening. Indeed if you were to stop the month right now, it would be the first month in 10 that the rate priced in by the December 2022 meeting has actually fallen rather than risen. That’s been echoed further out the curve as well, with investors now barely expecting the Fed Funds rate to get above 3% in 2023 at all, even though inflation has proven much stickier than the consensus expected over recent months. As Chair Powell put it in an interview last week, getting inflation back to target will “include some pain”. Markets are starting to price some of that out though.

Over in Europe longer-dated sovereign bond yields also moved slightly lower, including those on 10yr bunds (-0.8bps), OATs (-1.4bps) and BTPs (-0.8bps). That came as we heard from Bank of France Governor Villeroy, who said to expect “a decisive June meeting, and an active summer”, which fits into the broader debate recently whereby markets are increasingly expecting an initial hike as soon as July. This saw the 2yr bund increase +3.0bps to 0.12%. Another point of interest were also his comments on the exchange rate, saying that “A euro that is too weak would go against our price-stability objective”.

In line with the broader theme this year, one asset class that wasn’t impacted by the risk-off tone was commodities, and both Brent crude (+2.41%) and WTI (+3.36%) moved back above $114/bbl yesterday. This morning, both are seeing slight losses though (-0.36% and -0.46%, respectively). There were major gains for wheat futures (+5.94%) too, which saw a significant daily rise following India’s move over the weekend to restrict their exports. And that went alongside other rises in agricultural goods yesterday including corn (+3.6%) and sugar (+2.66%), which is an incredibly important story for emerging markets in particular given the much higher share of disposable income that consumers put towards food in those countries.

Another asset class that has had a bad time of late is Bitcoin, shedding another -3.58% to $29,909 yesterday. This morning it is climbing back above the $30k threshold. Marion Laboure in my team published a piece yesterday looking at the recent selloff in crypto, adding some much needed context for what this means for broader adoption efforts. See here for more.

Overnight in Asia, it has been a good start for the Hang Seng (+2.23%) amid optimism that today’s meeting between China’s corporates and regulators may lead to an easing of draconian measures on tech companies. Hong Kong is also on track to ease covid curbs on May 19th, a theme that also lifted the Shanghai Composite (+0.29%) after the city reported a third day of no new infections in the broader community, a threshold that allows it to roll back some of the restrictions. The sentiment is upbeat elsewhere in Asia too, with the Nikkei (+0.35%) and the KOSPI (+0.80%) also rising. This optimism is shared by S&P 500 futures, up +0.31%.

Elsewhere, it’s likely that Brexit will be back in the headlines today as UK Foreign Secretary Liz Truss is expected to make a statement to parliament announcing a new law that would override parts of the Northern Ireland Protocol. For reference, the Protocol is a part of the Brexit deal which the UK and the EU agreed ahead of the UK’s departure, but has been a persistent source of controversy since. Northern Irish unionists view it as undermining their place in the UK because it places an economic border between Northern Ireland and Great Britain, and the DUP (the second-largest party in the Northern Ireland Assembly) are refusing to help form an executive following their recent elections unless action is taken on the Protocol. The EU have continued to warn the UK against any unilateral action, and there’s been fears of an UK-EU trade war if the row gets worse.

There wasn’t much in the way of data yesterday, although the Empire State manufacturing survey for May underwhelmed with a reading of -11.6 (vs. 15.0 expected), which was beneath every estimate in Bloomberg’s survey. There was some easing in the prices paid index though, which fell to a 14-month low of 73.7.

To the day ahead now, and there’s an array of central bank speakers including Fed Chair Powell, along with the Fed’s Bullard, Harker, Kashkari, Mester and Evans, ECB President Lagarde and BoE Deputy Governor Cunliffe. Data releases include US retail sales, industrial production and capacity utilisation for April, along with the NAHB’s housing market index for May. Elsewhere, there’s also the UK unemployment reading for March. Finally, earnings releases include Walmart and Home Depot.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 19.95 PTS OR 0.65% //Hang Sang CLOSED UP 652.31 PTS OR 3.27% /The Nikkei closed UP 112.70 OR 0.42% //Australia’s all ordinaires CLOSED UP 0.33% /Chinese yuan (ONSHORE) closed UP 6,7244 /Oil UP TO 115.47 dollars per barrel for WTI and UP TO 115.48 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7249 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7349: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER//

3 a./NORTH KOREA/ SOUTH KOREA

///SOUTH KOREA

3B JAPAN

3c CHINA

COVID//LOCKDOWNS/

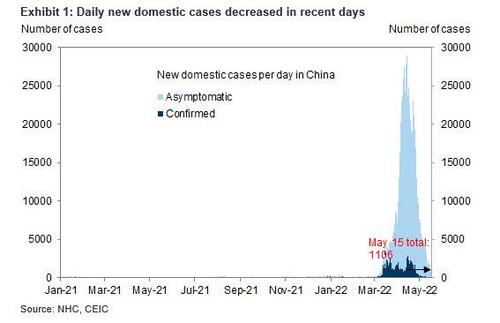

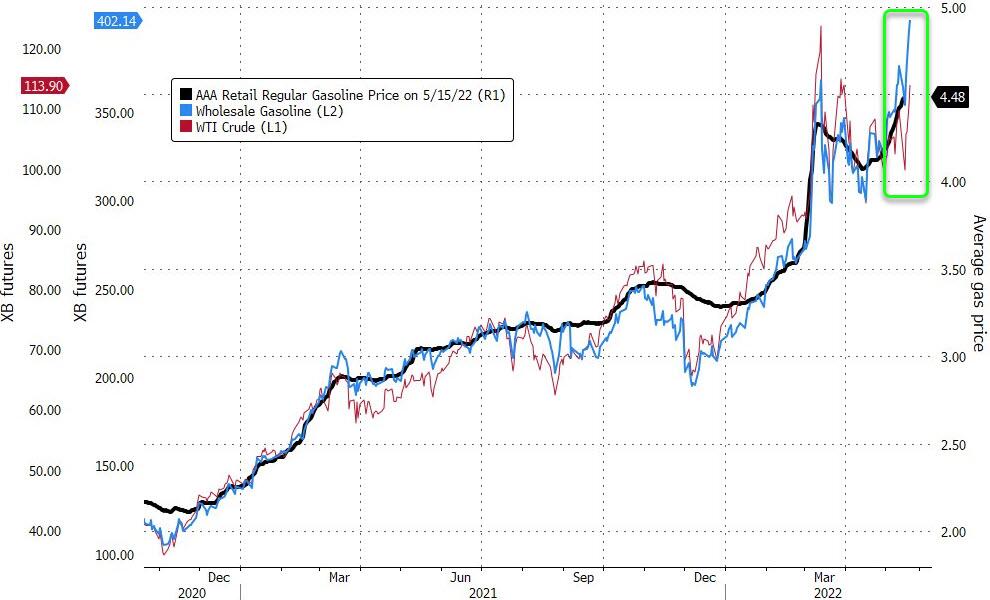

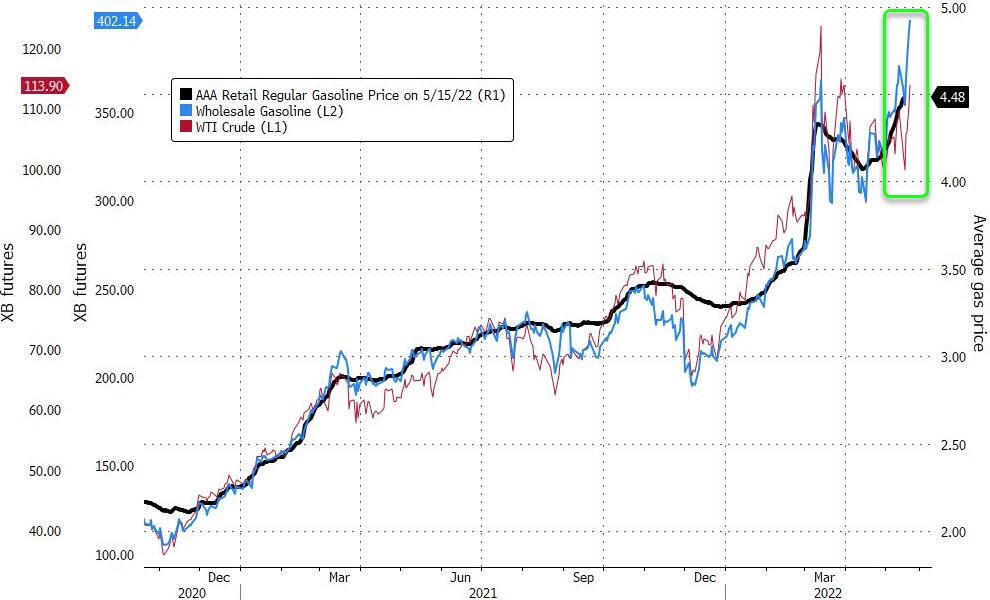

Oil prices now surge past $115 (Tuesday morning) as Shanghai signals an end to the lockdowns.

Oil Prices Surge Past $115 As Shanghai Signals End Of Lockdown

MONDAY, MAY 16, 2022 – 05:05 PM

By Charles Kennedy of OilPrice.com,

Oil prices have topped $115 per barrel on optimism that China’s lockdowns are coming to an end and demand will not take a prolonged hit.

In early afternoon markets Monday, news that Shanghai was seeing a strong recovery from COVID cases, with plans in place to ease lockdown restrictions beginning this week, outweighed a litany of bearish news for oil.

Last night: Brent was at $113.97 per barrel on 3:20 pm EST, while WTI was trading at $113.77. (this morning $115.48)

WTI neared $115…

Authorities in Shanghai on Monday said restrictions would finally ease, in stages, after nearly six weeks of lockdowns that have shaken the Chinese economy and disrupted global supply chains.

On 1 June, Shanghai is scheduled to see lockdowns end, with a gradual easing beginning on May 21st.

“From June 1 to mid- and late June, as long as risks of a rebound in infections are controlled, we will fully implement epidemic prevention and control, normalise management and fully restore normal production and life in the city,” the Guardian quoted deputy mayor Zong Ming as saying Monday.

The announcement comes shortly after downward pressure was put on oil prices over new releases of weak Chinese economic data and signals that the European Union’s plans to ban Russian oil had faltered.

On Monday, China published official economic data, showing a significant slowdown, with industrial output falling by nearly 3% year-on-year in April, and retail sales down by around 11%. Shanghai’s port volumes were also down by 40%, according to DW.

All of this has led to a decline in demand for oil coming out of China.

However, according to new data from the Saudi Arabia-based Joint Organizations Data Initiative (JODI), global oil demand surpassed pre-pandemic levels in March, at 101%, despite declines in Chinese demand. However, the report noted that crude oil production was at 97% of pre-COVID levels. The data is based on submissions that account for 70% of global oil demand and 55% of global crude production.

end

Tesla/Shanghai

Major problems in Shanghai still persist for Tesla

(zerohedge)

100,000 More Recalls And Even More Shanghai Delays Sting Tesla To Start The Week

MONDAY, MAY 16, 2022 – 07:25 PM

Just as it started to look like everything had finally been sorted out for Tesla in Shanghai, we reported last week that the company once again had to halt its production due to “issues with supplies”.

Starting off this week, it doesn’t look like things are getting any better. First, Bloomberg reported that “no vehicles were sold in Shanghai last month” as a result of the lockdown, according to an auto-seller association in the city.

Meanwhile, Tesla’s plans to restart Shanghai to its pre-pandemic production levels have been pushed back another week, Reuters reported this weekend. Citing an internal memo, Reuters wrote that Tesla is still planning on just one shift for its plant this week and a daily output of about 1,200 units.

Tesla is aiming for 2,600 units per day by May 23.

Additionally, it was reported Monday that Tesla would be recalling over 100,000 vehicles in China. 107,293 vehicles in China will be recalled “due to safety risks”, according to the China People’s Daily.

The recall, which relates to a defect in the central touchscreen during fast charging, “involves Model 3 and Model Y vehicles produced in the country between Oct 19, 2021, and April 26, 2022,” the report says.

Recall, Tesla’s most recent Shanghai shutdown came just three weeks after the plant resumed production. The plant was closed for a total of 22 days, Reuters noted. Shanghai is now in its seventh week of lockdowns, and we noted last week that it was “unclear when the supply issues can be resolved and when Tesla can resume production”.

Wire harness maker Aptiv is one supplier who is currently facing issues due to “infections found among its employees”, we reported last week. Meanwhile, Tesla had just started to eye resuming double shifts at its plant, we noted two weeks ago. The plant was making plans to “resume double shifts” at its Shanghai factory as soon as mid-May after starting back up in mid April.

end

This is new: we are starting to see a rift between the WHO and China on how to handle to virus

(Tucker/Brownstone)

The New Rift Between WHO And China

MONDAY, MAY 16, 2022 – 07:45 PM

Authored by Jeffrey Tucker via The Brownstone Institute,

From the beginning of the pandemic, the World Health Organization and China’s CCP have worked and spoken hand-in-glove, culminating in the Potemkin Village junket of mid-February 2020. The WHO-sponsored travel report—how wonderfully China had performed!—was written and signed by American public health officials who recommended Wuhan-style lockdowns, a disastrous policy that further inspired most governments in the world to do the same.

Twenty-six months later, it turns out that China in fact had not “eliminated the virus fully within its borders,” contrary to the over-the-top claims of TV pundit Devi Sridhar in her new book “Preventable.” They only pushed cases into the future, as the CCP discovered when positive tests appeared all over Shanghai, leading to 7 weeks of brutal lockdowns.

This move on China’s part has been a disaster for the country and the world economy, and presently endangers the financial and technological future of the entire country.

For Xi Jinping, lockdowns and zero-covid were his greatest achievement, one which was celebrated the world over, causing his political pride to swell beyond all bounds. Now, he cannot back off lest he face possible losses in upcoming party elections.

Just this past weekend, he made it clear to the entire government that there would be no backing off the zero-covid policy: the CCP will “unswervingly adhere to the general policy of ‘dynamic zero-Covid,’ and resolutely fight against any words and deeds that distort, doubt or deny our country’s epidemic prevention policies.”

The problem is acute: vast numbers in China likely need to acquire natural immunity via exposure. The lockdown policy likely puts a damper on the achievement of endemicity. That means long-term damage to China’s future.

Sensing this problem, the head of the WHO, Tedros Adhanom Ghebreyesus, offered a mild criticism:

“Considering the behavior of the virus, I think a shift will be very important,” adding that he had discussed this point with Chinese scientists.

What happened next is truly fascinating: Tedros’s comments were censored all over China and searches for the name Tedros were immediately blocked within the country.

Implausibly, merely by stating the incredibly obvious point, Tedros has made himself an enemy of the state.

Meanwhile, another WHO/China partisan, Bill Gates, has been sheepishly saying something very similar in interviews, namely that the virus cannot be eradicated.

It’s not just Tedros and Gates who are trying to flee their advocacy of lockdowns. Anthony Fauci himself denied that the United States ever had “complete lockdowns”—which is technically correct but not because he didn’t demand them.

On March 16, 2020, Fauci faced the national press and read from a CDC directive: “In states with evidence of community transmission, bars, restaurants, food courts, gyms and other indoor and outdoor venues where groups of people congregate should be closed.”

In fact, one gets the strong sense that governments around the world are pretending as if the whole pathetic and terrible affair never happened, even as they are attempting to reserve the power to do it all over again should the need arise.

On May 12, 2022, many governments around the world gathered for a video call and agreed to pour many billions more into covid work, and reaffirm their dedication to an “all-of-society” and “whole-of-government” approach to infectious disease. The U.S. government under the administration readily agreed to this idea.

Leaders reinforced the value of whole-of-government and whole-of-society approaches to bring the acute phase of COVID-19 to an end, and the importance of being prepared for future pandemic threats. The Summit was focused on preventing complacency, recognizing the pandemic is not over; protecting the most vulnerable, including the elderly, immunocompromised people, and frontline and health workers; and preventing future health crises, recognizing now is the time to secure political and financial commitment for pandemic preparedness.

The Summit catalyzed bold commitments. Financially, leaders committed to provide nearly $2 billion in new funding—additional to pledges made earlier in 2022. These funds will accelerate access to vaccinations, testing, and treatments, and they will contribute to a new pandemic preparedness and global health security fund housed at the World Bank.

Is it progress to see these people throwing around language from the much-criticized but now wholly vindicated Great Barrington Declaration? Doubtful. You can’t make a bad policy better by tossing around words. There is every indication from this statement that there will be no apologies, no regrets, and no changes in the default position that governments must always and everywhere have maximum power to control any pathogen of their choosing.

Despite Tedros’s censored words, it’s no wonder that Xi Jinping continues to feel vindicated and affirmed, and sees no real political danger in choosing his own power over the health and well-being of his people. Governments around the world still cannot muster the courage to make a full-throated and solid attack on zero-covid, for fear of the implications of such a concession. Nudges and hints, even from the WHO, will not do it.

end

4/EUROPEAN AFFAIRS//UK AFFAIRS/EU

GERMANY/RUSSIA //GAS

German Industry President warns that cutting off Russian gas would be “catastrophic”

(zerohedge)

Cutting Off Russian Gas Would Be “Catastrophic”, German Industry President Warns

TUESDAY, MAY 17, 2022 – 04:15 AM