May 18, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1817.75 DOWN $2.55

SILVER: $21.55 UP $.04

ACCESS MARKET: GOLD $1816.60

SILVER: $21.40

Bitcoin morning price: $29753 DOWN 476

Bitcoin: afternoon price: $29,174 DOWN 1055

Platinum price: closing DOWN $17.65 to $938.90

Palladium price; closing DOWN $39.00 at $2007.60

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices percentage of JPMorgan notices filed: 244/285

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,818.200000000 USD

INTENT DATE: 05/17/2022 DELIVERY DATE: 05/19/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 285

657 C MORGAN STANLEY 2

657 H MORGAN STANLEY 33

661 C JP MORGAN 244

737 C ADVANTAGE 6

TOTAL: 285 285

MONTH TO DATE: 5,672

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 285 NOTICE(S) FOR 28,500 OZ (0.8864 TONNES)

total notices so far: 5672 contracts for 567,200. oz (17.642 tonnes)

SILVER NOTICES:

97 NOTICE(S) FILED 485,000 OZ/

total number of notices filed so far this month 5022 : for 25,110,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $2.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD

INVENTORY RESTS AT 1049.21 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 4 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 1.892 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 563.193 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG SIZED 1691 CONTRACTS TO 144,534 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE SMALL GAIN IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.22 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.22) AND WE ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE.

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 125,000 OZ E.F.P. JUMP //NEW STANDING 27,910,000 MILLION OZ/ // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -81

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 12 days, total 16,215, contracts: 81.075 million oz OR 6.75 MILLION OZ PER DAY. (1351CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 81.075 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 81.075 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1619 WITH OUR $0.31 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE CONTRACTS: 41 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 125,000 OZ QUEUE. JUMP //NEW STANDING 27.910 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 1741 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.700 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 97 NOTICE FILED TODAY FOR 485,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1547 CONTRACTS TO 555,756 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –203 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $5.40//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR SMALL SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 10,900 OZ//NEW STANDING 18.289 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $5.40 WITH RESPECT TO MONDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 669 OI CONTRACTS (2.0808 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 878 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 555,756.

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 669, WITH 1547 CONTRACTS DECREASED AT THE COMEX AND 878 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 669 CONTRACTS OR 2.0809 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (878) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (1547,): TOTAL LOSS IN THE TWO EXCHANGES 669 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 10,900 OZ//NEW STANDING 18.289 /// 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

47,880 CONTRACTS OR 4,788,000 OR 148.92 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 3990 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 148.92 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 148.92/3550 x 100% TONNES 4.19% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 148.92 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1619 CONTRACT OI TO 144,534 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 41 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 41 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1700 CONTRACTS AND ADD TO THE 41 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF1660 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 8.300 MILLION OZ

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.22 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 7.72 PTS OR 0.25% //Hang Sang CLOSED UP 41.36 PTS OR 0.20% /The Nikkei closed UP 251.45 OR 0.94% //Australia’s all ordinaires CLOSED UP 1.03% /Chinese yuan (ONSHORE) closed DOWN 6,7442 /Oil UP TO 114.454dollars per barrel for WTI and UP TO 113.50 for Brent. Stocks in Europe OPENED ALL MOSTLY RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7442 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.74544: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1547 CONTRACTS TO 555,756 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $5.40 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A SMALL SIZED EFP (878 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 878 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :878 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 878 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 669 CONTRACTS IN THAT 878 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 1547 CONTRACTS..AND YET THIS LOSS OCCURRED WITH OUR GAIN IN PRICE OF GOLD $5.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (18.289),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 18.289 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $5.40) BUT IT SEEMS WERE QUITE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR SHORTS// WE HAVE REGISTERED A SMALL SIZED LOSS OF 2.089 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (18.289 TONNES)…

WE HAD XX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 669 CONTRACTS OR 66,900 OZ OR 2.0808

TONNES

Estimated gold volume today: 162,967/// poor

Confirmed volume yesterday:167,076 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 18

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 197,513.650 oz Brinks Int. Delaware JPMorgan Manfra includes: 2000 kilobars and 15 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 3574.26 oz Brinks |

| No of oz served (contracts) today | 285 notice(s) 28,500 OZ 0.8864 TONNES |

| No of oz to be served (notices) | 208 contracts 20,800 oz 0.6469 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5672 notices 567,200 OZ 17.642 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit nil oz//

No dealer withdrawals

1 customer deposit

i)Into Brinks: 3574.26 oz

total deposits: 3574.26 oz

4 customer withdrawals:

i) Out of Brinks: 160,755.000 oz 5000 kilobars

ii) Out of Int. Delaware: 482.265 oz (15 kilobars)

iii) Out of JPMorgan: 32,702.125 oz

iv) Out of Manfra: 3574.260 oz

total withdrawal: 197,513.650 oz

ADJUSTMENTS:

a) JPM: 64,334.151 oz// customer to dealer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 493 contracts having GAINED 103 contracts

We had 6 notices filed on MONDAY, so we gained 109 contracts or AN ADDITIONAL 10,900 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 11,328 contracts down to 239,194 contracts

July has a GAIN OF 10 OI to stand at 327

August has a gain of 9453 contracts up to 257,678 contracts

We had 285 notice(s) filed today for 28500 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 285 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 244 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (5672) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 493 CONTRACTS ) minus the number of notices served upon today 285 x 100 oz per contract equals 577100 OZ OR 17.9502 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (5672) x 100 oz+ (493) OI for the front month minus the number of notices served upon today (285} x 100 oz} which equals 588,000 oz standing OR 18.289 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 18.289 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,026,795.134 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,793,598.694 OZ

TOTAL ELIGIBLE GOLD: 17,812,062.336 OZ

TOTAL OF ALL REGISTERED GOLD: 17,961,536.365 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,948,662.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 18

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 177,513.650 oz Delaware CNT JPMorgan |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1150,905.812 oz CNT Delaware |

| No of oz served today (contracts) | 97CONTRACT(S) 485,000 OZ) |

| No of oz to be served (notices) | 463 contracts (2,315,000 oz) |

| Total monthly oz silver served (contracts) | 5119 contracts 25,595,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) zero dealer deposits

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into Delaware: 547,017.150 oz

ii) Into CNT 603,858.662 oz

total deposit: 1,150,905.812 oz

JPMorgan has a total silver weight: 176.729 million oz/339.387 million =52.12% of comex

Comex withdrawals: 3

i) Out of CNT 60,373.580 oz

ii) Out of Delaware 926.100 oz

iii) Out of JPMorgan: 116,071.370 oz oz

total withdrawal 177,371.030 oz

2 adjustments: customer to dealer HSBC 5045.85 oz

and Manfra: dealer to customer: 429,842.143 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.674 MILLION OZ

TOTAL REG + ELIG. 339.387 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 560 HAVING LOST 188 CONTRACTS. WE HAD 163 NOTICES FILED ON MONDAY

SO WE LOST 25 CONTRACTS OR AN E.F.P JUMP TO LONDON OF 125,000 OZ

JUNE HAD A GAIN OF 22 TO STAND AT 1543

JULY HAD A GAIN OF 381 CONTRACTS UP TO 113,425 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 97 for 485,000 oz

Comex volumes: 34,067// est. volume today// poor

Comex volume: confirmed yesterday: 43,461 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5119 x 5,000 oz = 25,595,000 oz

to which we add the difference between the open interest for the front month of MAY(560) and the number of notices served upon today 97 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2022 contract month: 5119 (notices served so far) x 5000 oz + OI for front month of MAY (560) – number of notices served upon today (97) x 5000 oz of silver standing for the MAY contract month equates 27,910,000 oz. .

We LOST 25 contracts or AN ADDITIONAL 125,000 OZ will NOT stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1049.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL O 1.892 MILLION OZ FROM THE SLV//FINVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 563.193 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: Don’t Listen To What The Fed Says; Look At What The Fed Is Doing

WEDNESDAY, MAY 18, 2022 – 06:30 AM

The Fed continues to talk tough about fighting inflation. And the markets seem to be listening. But in his podcast, Peter Schiff said you need to look at what the Fed is actually doing. And it’s not doing much.

Despite a big rally in the stocks on Friday, the stock market finished its sixth consecutive week in the red. It’s the longest streak of consecutive losses since June of 2011.

Peter said despite Friday’s bounce, he still sees a lot of downside in the markets, calling Friday a day of “panic buying.”

Sometimes in bear markets, investors panic to buy. They don’t panic to sell until the end of the bear market. And despite the carnage, I have not really seen any indications of panic selling. I’ve seen more indications of panic buying, which in my mind indicates that there’s still a lot of downside to go.”

Meanwhile, gold continues to languish. During the stock rally Friday, gold dropped again, despite more bad inflation numbers.

The markets are clearly concerned, but Peter said they are concerned about the wrong thing.

What the markets still don’t get is Fed is not really going to fight inflation. It’s pretending it’s going to fight inflation. And that is the problem. Because all the people who were surprised by inflation they didn’t expect now expect the Fed to get rid of it. And the reason they are dumping gold and silver, and in particular gold and silver mining stocks — it’s not because they fear the inflation. They think the inflation is in the past. What they fear is this future inflation fight.”

Why do people think the Fed is going to go through with this fight? Because it says so.

The central bankers have said that they will do what it takes to tame the inflation dragon and bring the CPI back down to 2%, Doing what it takes means a very tight monetary policy with rising interest rates. That’s why the markets are so bearish on gold.

The tighter they perceive future monetary policy is going to get, the more problematic everybody believes that’s going to be for gold and silver, and they’re selling these gold and silver stocks.”

But Peter said even if the Fed does what it claims it will do in terms of raising interest rates and shrinking its balance sheet, it still won’t be enough to bring inflation back down to 2%.

In fact, it’s barely going to reduce the upward trajectory, let alone bring it all the way back down to 2%. And if the Fed actually tried to get inflation back down to 2%, it would not only send the economy into recession, but it would create a financial crisis worse than 2008. The markets still don’t get that. I don’t know why they can’t think that far ahead. All they can see is the Fed is claiming it’s going to fight inflation and it’s going to jack up interest rates. And so, for some reason, they believe that this is going to succeed.”

There is also this myth that the US economy is strong enough to handle the bitter medicine the Fed will have to deliver in order to get inflation under control, despite all the signs that the economy isn’t as strong as everybody imagines.

When the underlying weakness of the US economy is finally laid bare, then all this tough talk about fighting inflation is going to go away because then the Fed is going to concentrate on its other mandate, which is the economy. … Once people start losing their jobs in the recession, then the Fed is going to forget about inflation and start focusing on employment. For some reason, the markets aren’t there yet.”

This is why every time the markets get surprised by hotter than expected inflation, they just assume the Fed is going to have to fight harder.

It never occurs to them that it means the Fed has already lost the fight and it’s going to surrender.”

Peter reiterated that if the Fed’s actions don’t indicate it’s serious about fighting inflation.

I’ve said this many times. It wouldn’t just be talking about fighting inflation. It would be fighting it right now.”

But according to the latest data, the Fed balance sheet expanded by another 2%. In effect, this is more gasoline on the inflationary fire.

If the Fed has acknowledged that the balance sheet is already too big and it needs to be reduced, why are they still making it bigger?”

Why wait until June to begin quantitative tightening? Why are interest rates still below 1%? If we really have an inflation emergency, why so much talk and so little action from the Fed?

The fact of the matter is you’ve got to look at what the Fed is doing, not what the Fed is saying. They have to talk tough. … It’s the opposite of the Teddy Roosevelt strategy. They don’t have a stick. They can’t really fight inflation. So, they have to talk tough as if they’re going to fight it, because they’re hoping their tough talk will do the fighting for them, and they won’t have to reveal the fact that they don’t really have a stick.”

In this podcast, Peter also talks about Jerome Powell’s reappointment as Fed chair, consumers borrowing to make ends meet, and oil positioning for another big move up.

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke at Sprott Money: Comex trade-at-settlement games continue

USED IDENTICALLY AND SAME MECHANISM OF SPREADERS LIQUIDATION

(Craig Hemke)

Submitted by admin on Tue, 2022-05-17 21:54Section: Daily Dispatches

9:54p ET Tuesday, May 17, 2022

Dear Friend of GATA and Gold:

The “trade at settlement” mechanism of controlling gold futures prices by massive legging into and out of the market is operating at full bore again, the TF Metals Report’s Craig Hemke writes tonight at Sprott Money.

Hemke concludes: “There continue to be malevolent forces that manage and manipulate the Comex gold price, primarily for their own profit. This monthly trade-at-settlement abuse is simply the latest weapon they have put in their arsenal.”

Hemke’s analysis is headlined “Comex TAS Games” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-TAS-Games-Craig-Hemke-May-17-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIAMONDS

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7442

OFFSHORE YUAN: 6.7544

HANG SANG CLOSED UP 42.76 PTS OR 0.20%

2. Nikkei closed UP 251.45 OR 0.94%

3. Europe stocks ALL CLOSED MOSTYL RED

USA dollar INDEX UP TO 103.63/Euro FALLS TO 1.0509

3b Japan 10 YR bond yield: FALLS TO. +.238/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.10/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield RISES TO 3.58

3j Gold at $1809.40 silver at: 21.60 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1/3 roubles/dollar; ROUBLE AT 63.27

3m oil into the 113 dollar handle for WTI and 114 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.10 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9972– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0482well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.000 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 3.191 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.94

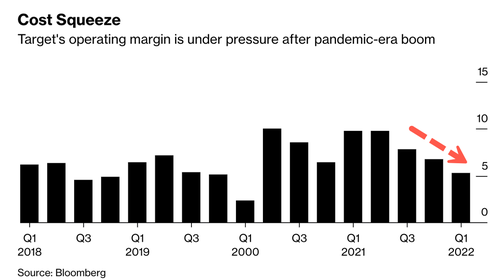

Futures Slide After Dismal Target Earnings, Plunging Mortgage Apps

WEDNESDAY, MAY 18, 2022 – 07:51 AM

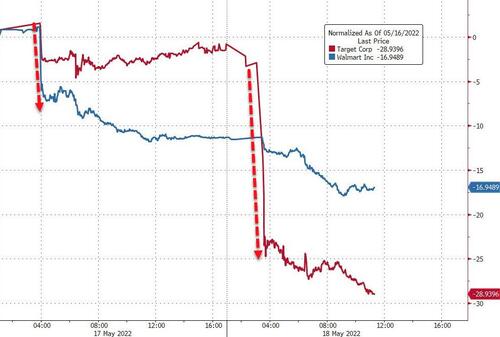

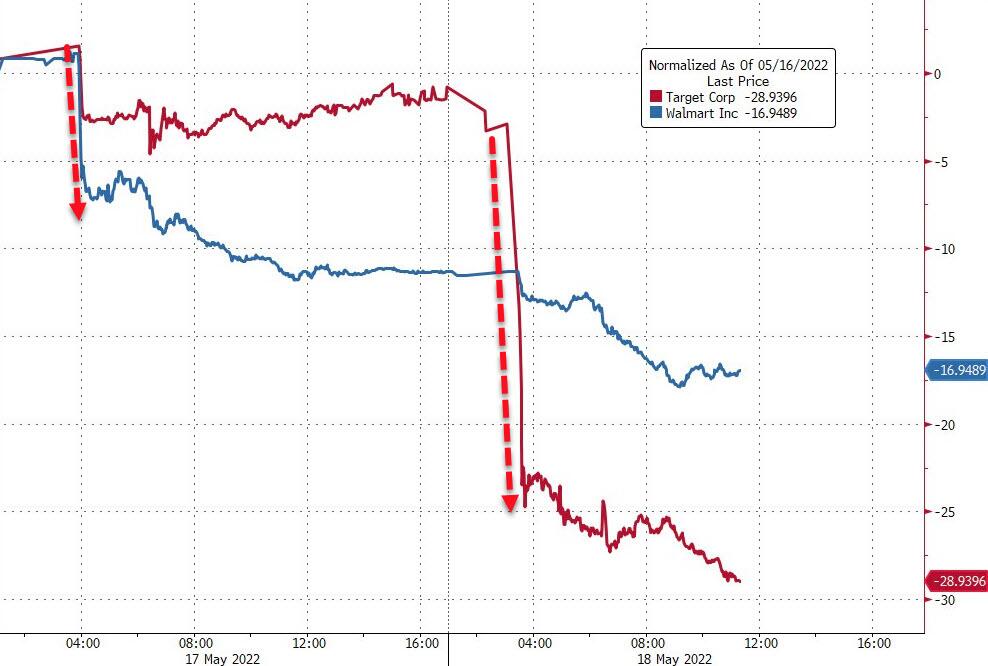

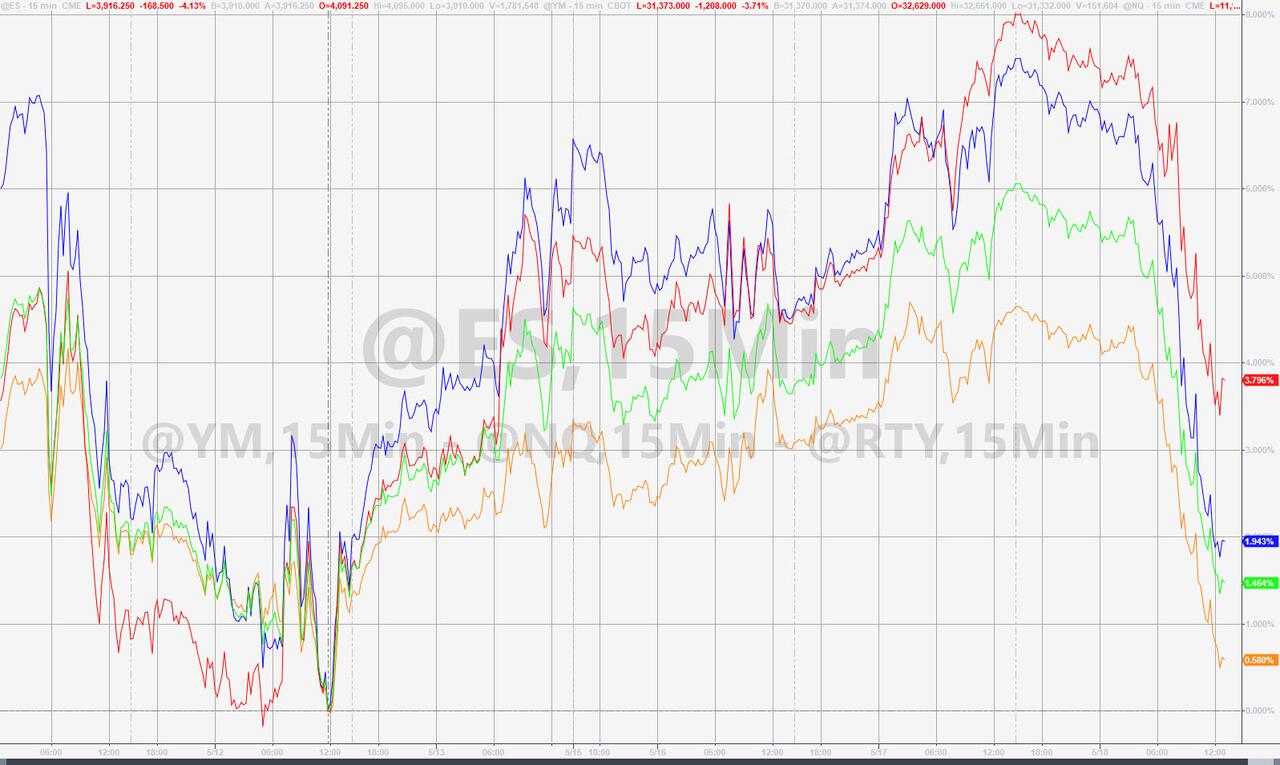

The brief bear market rally in US stocks was set to end with a whimper following Tuesday’s strong dead cat bounce, after Fed Chair Jerome Powell gave his most hawkish remarks to date. Hope that China lockdowns would soon end turned to skepticism, as the yuan slumped after its biggest gain since October, while dismal guidance from Target – which warned that inflation was crushing margins – confirmed what Walmart said yesterday, namely that the US consumer is running on fumes. An 11% plunge in the latest weekly mortgage applications only reaffirmed that a hard-landing is inevitable and just a matter of time. Nasdaq 100 futures dropped 1%, while S&P 500 futures slipped 0.7% after US stocks surged on Tuesday. Treasury yields hit session highs, rising back to 3.0%, and the dollar snapped a three-day losing streak. Bitcoin got hammered again, sliding back under $30k.

Among the biggest premarket movers, Target crashed 22% with Vital Knowledge calling its margin shortfall “more dramatic” than what Walmart posted on Tuesday, citing industry-wide macro problems. The retailer reduced its full-year forecast on operating income margin to about 6% of sales this year. It also reported first-quarter adjusted earnings per share that came in below expectations. Food and gas inflation is drawing money away from discretionary and general merchandise spending, forcing “aggressive” discounting to clear out product in the latter category, Vital’s Adam Crisafulli said in a note.

Elsewhere in US premarket trading, Tesla slipped 1% after its price target was cut at Piper Sandler. Meanwhile, Twitter Inc. also traded slightly lower even as the social media platform’s board said it plans to enforce its $44 billion agreement to be bought by Elon Musk. Here are some other notable premarket movers:

- US tech hardware stocks may be in focus as Jefferies Group LLC strategists have turned bullish on the likes of IBM (IBM US), Cisco Systems (CSCO US) and Microchip Technology (MCHP US) after this year’s steep declines for US information technology shares

- National CineMedia (NCMI US) shares jump as much as 33% in US premarket trading after AMC Entertainment (AMC US) reported a 6.8% stake in the cinema advertising company. AMC shares gain 1.2% in premarket trading.

- DLocal Ltd. (DLO US) shares gain as much as 15% in US premarket trading after the Uruguay-based payment platform posted 1Q revenue that doubled from the year-earlier period and topped expectations.

- Doximity (DOCS US) shares fall as much as 19% in US premarket trading, after the online healthcare platform provider’s forecast for 1Q revenue missed the average analyst estimate, prompting analysts to slash their price targets on the stock.

- Penn National (PENN US) may be active on Wednesday as Jefferies raised the recommendation to buy from hold. The company’s shares rose 4% in premarket trading.

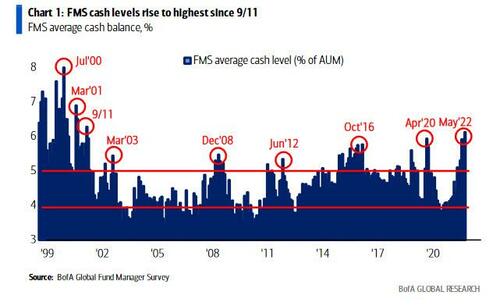

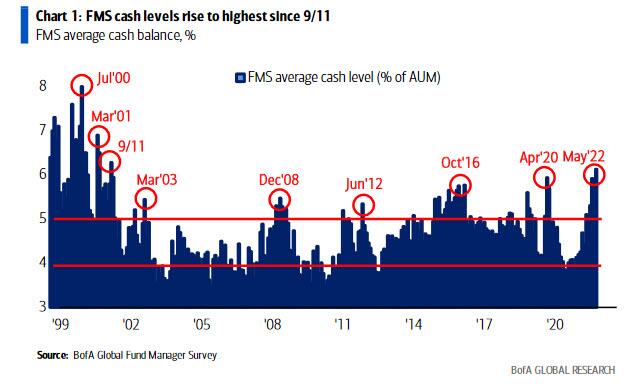

On Tuesday, Powell said the Fed will keep raising interest rates until there is “clear and convincing” evidence that inflation is in retreat, which initially pushed stocks lower but then was faded as risk closed near session highs as nothing Powell said was actually new. The S&P 500 is emerging from the longest weekly slump since 2011 as investors have been gripped by fears of hawkish monetary policy and surging inflation driving the economy into a recession. As also discussed yesterday, Bank of America’s survey published yesterday showed that fund managers are the most underweight equities since May 2020 and are piling into cash.

“This is one of the most challenging markets I have been in in my career,” Henry Peabody, fixed income portfolio manager at MFS Investment Management, said on Bloomberg Television. “I suspect at a certain point of time we’re going to have the liquidity of the markets challenged. They really haven’t been thus far.”

As the Fed embarks on interest-rate hikes, frothy growth shares, including the tech sector, have suffered in particular as higher rates mean a bigger discount for the present value of future profits. This marks a major shift in investor outlook after tech stocks had been some of the market’s best performers for years.

“Investor sentiment and confidence remain shaky, and as a result, we are likely to see volatile and choppy markets until we get further clarity on the 3Rs — rates, recession, and risk,” Mark Haefele, chief investment officer at UBS Global Wealth Management, wrote in a note.

Rebounds in risk sentiment are proving fragile amid tightening monetary settings, Russia’s war in Ukraine and China’s Covid lockdowns. In what’s seen as his most hawkish remarks to date, Powell said that the US central bank will raise interest rates until there is “clear and convincing” evidence that inflation is in retreat.

“We’ll have this kind of volatility as people jump in and look at opportunities to buy as markets decline,” Shana Sissel, director of investments at Cope Corrales, said on Bloomberg Television, referring to the Wall Street bounce. The Fed is going to struggle to achieve a soft economic landing, she added.

In Europe, the Stoxx 600 Index was little changed, with energy stocks outperforming. Spain’s IBEX outperformed, adding 0.5%. ABN Amro slumped almost 10% after the Dutch lender reported first-quarter results burdened by rising costs. The Stoxx Europe 600 Basic Resources sub-index drops, underperforming other sectors in the broader regional benchmark on Wednesday as base metals ended a three-day rebound and as iron ore declined. Base metals paused a recovery from this year’s lows, with copper and aluminum stalling after hawkish remarks from Federal Reserve Chair Jerome Powell. Iron ore futures declined as investors weighed China’s faltering economy and the prospect of support measures amid a mixed outlook for steel demand. Basic resources index -0.6%, halting three days of gains; broader benchmark little changed. Siemens Gamesa jumped as much as 15% as Siemens Energy weighs a bid for the shares of the troubled Spanish wind-turbine maker it doesn’t already own. Here are the most notable movers:

- European oil and gas stocks rise amid higher crude prices and broker upgrades, while renewables rallied after Siemens Energy confirmed it was considering a buyout offer for Siemens Gamesa. Shell gains as much as 1.8%, BP +1.8%, Equinor +3.4%, Gamesa +15%, Vestas +7.7%

- Air France-KLM shares rise as much as 7.5% in Paris on news that container line CMA CGM intends to take a stake of up to 9% in the French carrier following the signing of a long-term strategic partnership in the air cargo market.

- Rockwool shares gain as much as 8.3%, most since Feb. 15, as the company boosts its sales in local currencies forecast for the full year.

- British Land shares rise as much as 4.2%, as the company’s results show a strong recovery and a good performance in the UK landlord’s portfolio, analysts say.

- Vistry shares climb as much as 8% with analysts saying the UK homebuilder’s trading update looks positive, particularly the robust momentum in its sales rate.

- The Stoxx Europe 600 Basic Resources sub-index drops, underperforming other sectors in the broader regional benchmark on Wednesday as base metals ended a three-day rebound and as iron ore declined. Rio Tinto slips as much as 1.5%, Antofagasta -2.7%, Anglo American -1.5%

- Prosus shares fall as much as 4.2% and Naspers sinks as much as 6.7% after Tencent reported first- quarter revenue and net income that both missed analyst expectations.

- TUI shares drop as much as 13% in London after the firm announced an equity raise in order to repay a chunk of government aid that helped see it through the coronavirus crisis.

- ABN Amro shares declined as much as 11% after the lender reported 1Q earnings that showed higher costs related to money laundering.

- Experian shares fall as much as 5.1% after the consumer-credit reporting company reported full-year results, with Citi saying organic growth missed consensus.

Meanwhile, UK inflation rose to its highest level since Margaret Thatcher was prime minister 40 years ago, adding to pressure for action from the government and central bank. The pound weakened and gilt yields fell as traders speculated that the Bank of England will struggle to rein in inflation and avoid a recession.

Elsewhere, the Biden administration is poised to fully block Russia’s ability to pay US bondholders after a deadline expires next week, a move that could bring Moscow closer to a default. Sri Lanka, meantime, is on the brink of reneging on $12.6 billion of overseas bonds, a warning sign to investors in other developing nations that surging inflation is set to take a painful toll.

Earlier in the session, Asian stocks advanced for a fourth session as strong US economic data allayed worries about the global growth outlook, while Chinese equities slipped. The MSCI Asia-Pacific Index rose as much as 1%, extending its rebound from an almost two-year low reached last Thursday. Materials shares led the gains, with Australia’s BHP Group climbing 3.2%. Benchmarks in most markets were in the black, with Indonesia, Taiwan and Singapore chalking up gains of at least 1%. Upbeat retail sales and industrial production data from the US underpinned sentiment, so much so that investors barely reacted to hawkish comments from Federal Reserve Chair Jerome Powell. He indicated that policy makers won’t hesitate to raise interest rates beyond neutral levels to contain inflation.

Equities in China bucked the trend. Property shares paced the drop after data showed the decline in China’s new home prices accelerated in April, while tech shares also lost steam ahead of Tencent’s earnings which missed expectations and slumped. Local investors may be underwhelmed by a lack of details from Chinese Vice Premier Liu He’s fresh vow to support tech firms. Liu said the government will support the development of digital economy companies and their public listings, in remarks reported by state media after a symposium with the heads of some the nation’s largest private firms.

Lee Chiwoong, chief economist at Mitsubishi UFJ Morgan Stanley Securities, said Liu’s comments point to an easing of the crackdown on internet firms. “The Chinese government is stepping up measures to support the economy following the slowdown,” Lee said. “As bottlenecks stemming from lockdowns in Shanghai ease, that impact will gradually show up in the economy,” Lee added. “We should be able to clearly see an economic recovery in the second half of this year.”

Japanese equities gained as investors assessed strong US economic data and comments by Federal Reserve Chair Jerome Powell on the outlook for interest rate hikes. The Topix Index rose 1% to close at 1,884.69. Tokyo time, while the Nikkei advanced 0.9% to 26,911.20. Sony Group Corp. contributed the most to the Topix gain, increasing 2.9%. Out of 2,172 shares in the index, 1,345 rose and 749 fell, while 78 were unchanged. Chinese stocks erased losses intraday after earlier disappointment over a much-anticipated meeting between Vice Premier Liu He and some of the nation’s tech giants. Overnight, data showed US retail sales grew at a solid pace in April, while factory production rose at a solid pace for a third month.

Australia’s stocks also gained, with the S&P/ASX 200 index rising 1% to close at 7,182.70, extending its winning streak to a fourth day. Miners contributed the most to its advance. All sectors gained, except for consumer staples and financials. Eagers slumped after saying that its 1H profit will be lower than it was a year ago and flagged reduced new vehicle deliveries. Wage data was also in focus. Australian wages advanced at less than half the pace of consumer-price gains in the first three months of the year, reinforcing the RBA’s signal that it will stick to quarter-point hikes. In New Zealand, the S&P/NZX 50 index rose 1.1% to 11,258.28

India’s benchmark equities index fell, snapping two sessions of gains, weighed by declines in engineering company Larsen & Toubro Ltd. The S&P BSE Sensex dropped 0.2% to close at 54,208.53 in Mumbai, after rising as much as 0.9% earlier in the session. The NSE Nifty 50 Index fell 0.1% to 16,240.30. Larsen & Toubro slipped 2% and was the biggest drag on the Sensex, which saw 17 of its 30 member stocks decline. Sixteen of 19 sectoral sub-indexes compiled by BSE Ltd. dropped, led by a gauge of realty shares. State-run Life Insurance Corporation, which debuted Tuesday, rose 0.1% to 876 rupees, still below the issue price of 949 rupees. In earnings, of the 34 Nifty 50 firms that have announced results so far, 20 have either met or exceeded analyst estimates, while 14 have missed. Consumer goods company ITC Ltd. is scheduled to announce results on Wednesday.

In FX, the Bloomberg Dollar Spot Index reversed an early loss and the greenback advanced versus all of its Group-of-10 peers apart from the yen. The pound was the worst G-10 performer, tracking Gilt yields lower and paring the previous day’s gains. A widely expected jump in UK inflation prompted investors to pare back bets on BOE rate hikes. Money markets are pricing around 120bps of BOE rate hikes by December, down from 130bps from the previous day. UK inflation rose to its highest level since Margaret Thatcher was prime minister 40 years ago, adding to pressure for action from the government and central bank. Consumer prices surged 9% in the year through April. The euro fell for the first day in four and weakened beyond $1.05. The Bund curve has twist flattened as traders bet on a faster pace of ECB tightening after Bank of Finland Governor Olli Rehn said there’s broad agreement among members of the Governing Council that policy rates should exit sub-zero terrain “relatively quickly.” That’s to prevent inflation expectations from becoming de- anchored, he said. The Aussie swung between gains and losses while Australia’s bonds trimmed earlier declines after a report showed wage growth last quarter was less than economists forecast. The wage price index climbed an annual 2.4% last quarter, trailing economists’ expectations and coming in well below headline inflation of 5.1%. The yen rose as US yields declined amid fragile risk sentiment. Japanese government bonds were mixed, with a decent five-year auction lending support while an overnight rise in global yields weighed on super-long maturities.

In rates, Treasuries were under pressure, though most benchmark yields remained within 1bp of Tuesday’s closing levels. 10-year yields rose just shy of 3.00%, higher by less than 1bp with comparable bund yield +3.3bp and UK 10-year flat. TSY futures erased gains amid a series of block trades in 5- and 10-year note contracts starting at 5:20am ET, apparently selling flow. According to Bloomberg, six 5-year block trades and two 10-year block trades — all 5,000 lots — have printed since 5:20am, apparently seller-initiated as cash yields concurrently rebounded from near session lows. Wednesday’s $17b 20-year new-issue auction at 1pm ET may also weigh on the market. 20-year bond auction is this week’s only nominal coupon sale; WI yield ~3.37% exceeds all 20-year auction stops since then tenor was reintroduced in 2020, is ~27.5bp cheaper than last month’s result. Elsewhere, the UK yield curve bull-steepened with the short end richening ~5bps, while pound falls after inflation surged to a four-decade high. Money markets pare BOE rate-hike wagers. Bund curve bear-flattens while money markets bet on a faster pace of ECB tightening after ECB’s Rehn said the central bank needs to move quickly from negative rates.

In commodities, WTI trades within Tuesday’s range, adding 1.6% to around $114. Most base metals are in the red; LME tin falls 1.5%, underperforming peers, LME aluminum outperforms, adding 1%. Spot gold is little changed at $1,815/oz.

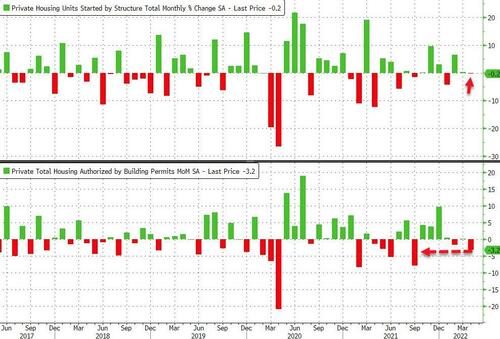

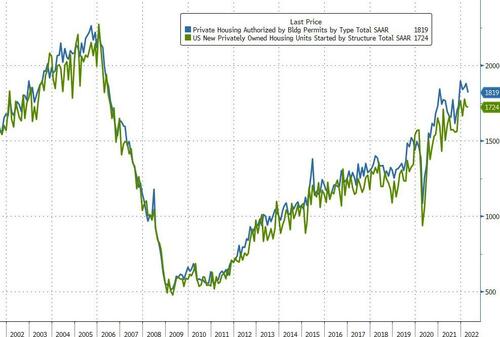

Looking to the day ahead now, and data releases include the UK and Canadian CPI readings for April, along with US data on housing starts and building permits for the same month. Central bank speakers include the Fed’s Harker and the ECB’s Muller. Earnings releases include Cisco, Lowe’s, Target and TJX. Finally, G7 finance ministers and central bank governors will be meeting in Germany.

Market Snapshot

- S&P 500 futures down 0.5% to 4,065.50

- STOXX Europe 600 down 0.2% to 438.11

- MXAP up 0.8% to 164.43

- MXAPJ up 0.7% to 539.81

- Nikkei up 0.9% to 26,911.20

- Topix up 1.0% to 1,884.69

- Hang Seng Index up 0.2% to 20,644.28

- Shanghai Composite down 0.2% to 3,085.98

- Sensex up 0.3% to 54,469.39

- Australia S&P/ASX 200 up 1.0% to 7,182.66

- Kospi up 0.2% to 2,625.98

- German 10Y yield little changed at 1.03%

- Euro down 0.4% to $1.0505

- Brent Futures up 1.5% to $113.66/bbl

- Gold spot down 0.0% to $1,815.04

- U.S. Dollar Index up 0.33% to 103.70

Top Overnight News from Bloomberg

- Sweden’s biggest pension company has begun buying government bonds amid a “paradigm shift” in the market that pushed yields to their highest level since 2018. The CIO views Treasuries as “quite attractive” after a prolonged period of razor-thin yields that forced the company into alternative and riskier asset classes to preserve returns across its $117 billion portfolio

- While outright China bulls may be hard to find, shifts in positioning at least point to improving sentiment. Bearish bets on stocks are being abandoned in Hong Kong, expectations for yuan volatility are falling, domestic equity traders have stopped unwinding leverage and foreigners have slowed their once-record exit from government bonds

- The EU is set to unveil a raft of measures ranging from boosting renewables and LNG imports to lowering energy demand in its quest to cut dependence on Russian supplies. The 195 billion-euro ($205 billion) plan due Wednesday will center on cutting red tape for wind and solar farms, paving the way for renewables to make up an increased target of 45% of its energy needs by 2030, according to draft documents seen by Bloomberg that are still subject to change

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed as the regional bourses only partially sustained the momentum from global peers. ASX 200 was led higher by outperformance in the mining and materials related sectors, while softer than expected wage price data reduced the prospects of a more aggressive RBA rate hike next month. Nikkei 225 briefly reclaimed the 27,000 level but retreated off its highs as participants digested GDP data which printed in negative territory, albeit at a narrower than feared contraction. Hang Seng and Shanghai Comp were subdued with large-cap tech stocks pressured in Hong Kong including JD.com despite beating earnings expectations and with Tencent bracing for the expected slowest revenue growth since its listing, while the mainland was hampered by the mixed COVID-19 situation as Shanghai registered a 4th consecutive day of zero transmissions outside of quarantine, although Beijing was said to lockdown some areas in its Fengtai district for 7 days.

Top Asian News

- Shanghai authorities issued a new white list containing 864 financial institutions permitted to resume work, according to sources cited by Reuters.

- China, on May 20th, is to remove some COVID test requirements on travellers to China from the US, according to embassy.

- China’s Foreign Ministry says the BRICS foreign ministers are to meet on May 19th.

- Goldman Sachs downgrades its 2022 China GDP growth forecast to 4.0% from 4.5%.

European bourses are rangebound and relatively directionless, Euro Stoxx 50 U/C, taking impetus from a mixed APAC session which failed to sustain US upside. Stateside, futures are modestly softer and a firmer Wall St. close; ES -0.2%. Limited Fed speak due and near-term focus on retail earnings. Tencent (0700 HK) Q1 2022 (CNY): adj. net profit 25.5bln (exp. 26.4bln), Revenue 135.5bln (exp. 141bln). Lowe’s Companies Inc (LOW) Q1 2023 (USD): EPS 3.61 (exp. 3.22/3.23 GAAP), Revenue 23.70bln (exp. 23.76bln). SSS: Lowe’s Companies: -4.0% (exp. -2.5%); Lowe’s Companies (US): -3.8% (exp. -3.7%). -0.2% in the pre-market

Top European News

- UK Chancellor Sunak is reportedly mulling bringing forward the 1p income tax cut to the basic rate by one year, according to iNews citing Treasury insiders. Other reports suggest that Sunak is putting plans together to raise the warm home discount by hundreds of GBP in July ahead of lowering taxes in autumn to assist with the cost of living crisis, according to The Times.

- EU is to offer the UK new concessions on the Northern Ireland protocol but has threatened a trade war if UK PM Johnson refuses to agree to a compromise, according to The Telegraph.

In FX

- Sterling slides to the bottom of the major ranks as fractionally sub-forecast UK CPI dampens BoE rate hike expectations; Cable reverses from just over 1.2500 to sub-1.2400, EUR/GBP nearer 0.8500 after dip below 0.8400 only yesterday.

- Hawkish Fed chair Powell helps Buck bounce ahead of US housing data, DXY towards the upper end of 103.770-180 range.

- Aussie hampered by softer than expected wage metrics that might convince the RBA to refrain from 40bp hike in June, AUD/USD heavy on the 0.7000 handle.

- Yen relatively resilient in wake of Japanese GDP showing less contraction in Q1 than feared, USD/JPY closer to 129.00 than 129.50.

- Euro loses momentum irrespective of comments from ECB’s Rehn echoing Summer rate hike guidance as final Eurozone HICP is tweaked down, EUR/USD fades from 1.0550+ to test support around 1.0500.

- Loonie treads cautiously before Canadian inflation metrics as oil prices come off the boil, USD/CAD back above 1.2800 within 1.2795-1.2852 range.

In Fixed Income

- Gilts sharply outperform as UK CPI falls just shy pf consensus and dampens BoE tightening expectations.

- 10 year UK bond rebounds towards 119.50 from sub-119.00 lows, while Bunds lag below 152.50 and T-note under 119-00.

- Record high cover for 2052 German auction and low retention sets high bar for upcoming 20 year US offering.

Central Banks

- ECB’s Rehn says June forecasts are seen near the adverse scenario from March, first rate increase will likely take place in the summer. Many colleagues back stance for quick moves.

- ECB’s de Cos says the end of APP should be finalised early in Q3, first hike shortly afterwards. Further rises could be made in subsequent quarters of medium-term outlook remains around target; the build-up of price pressures in EZ in recent months raises the likelihood of second-round effects, which have not strongly materialised.

In commodities

- WTI and Brent are modestly supported after yesterday’s lower settlement; currently, firmer by just over USD 1.00/bbl.

- Focus has been on the narrowing WTI/Brent spread, particularly going into US driving season; see link below for ING’s views.

- US Energy Inventory Data (bbls): Crude -2.4mln (exp. +1.4mln), Cushing -3.1mln, Gasoline -5.1mln (exp. -1.3mln), Distillates +1.1mln (exp. unchanged).

- Spot gold and silver are modestly firmer but capped by a firmer USD, yellow metal just shy of USD 1820/oz.

US Event Calendar

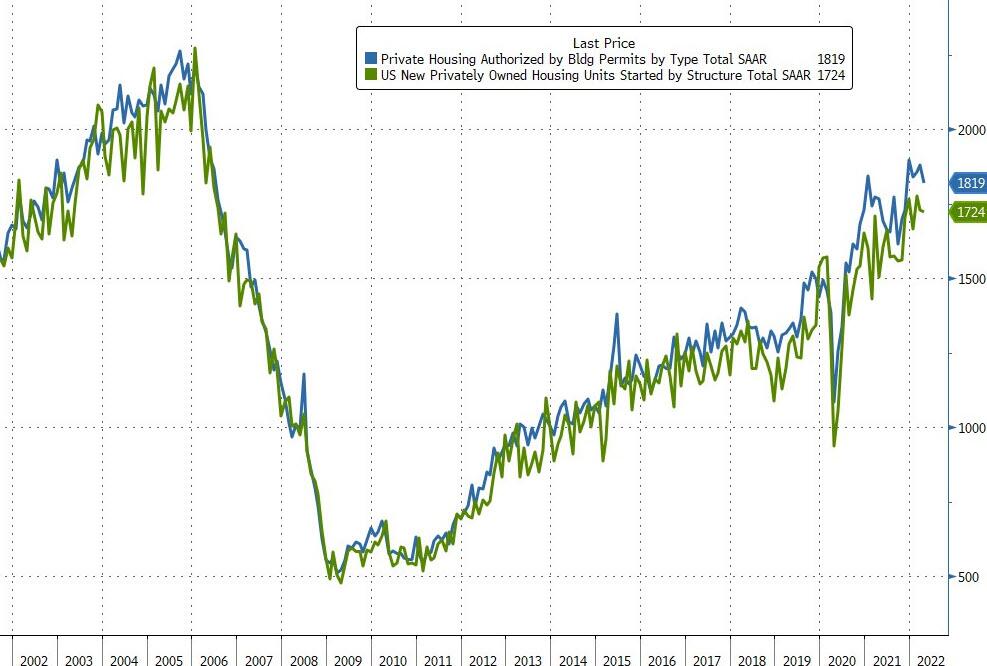

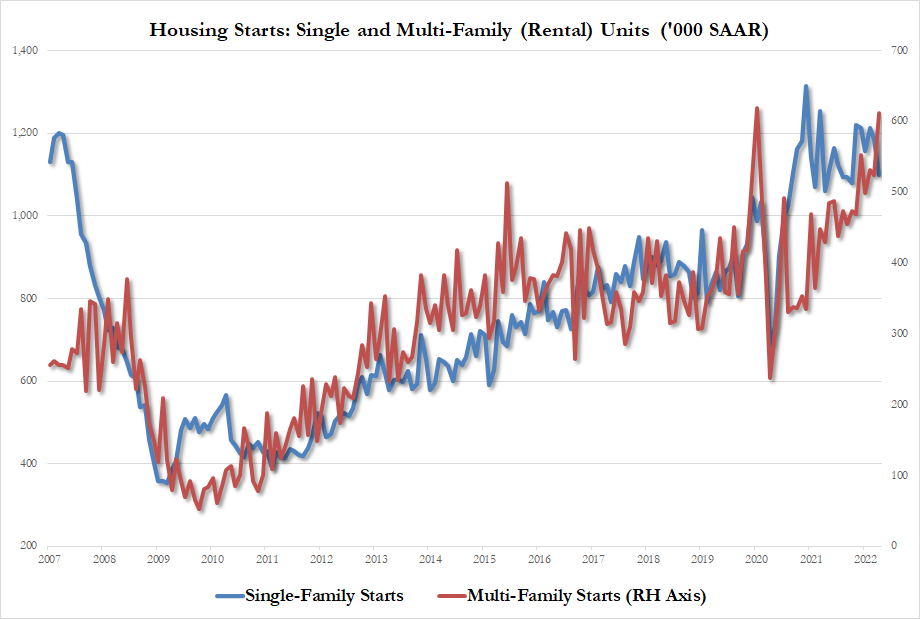

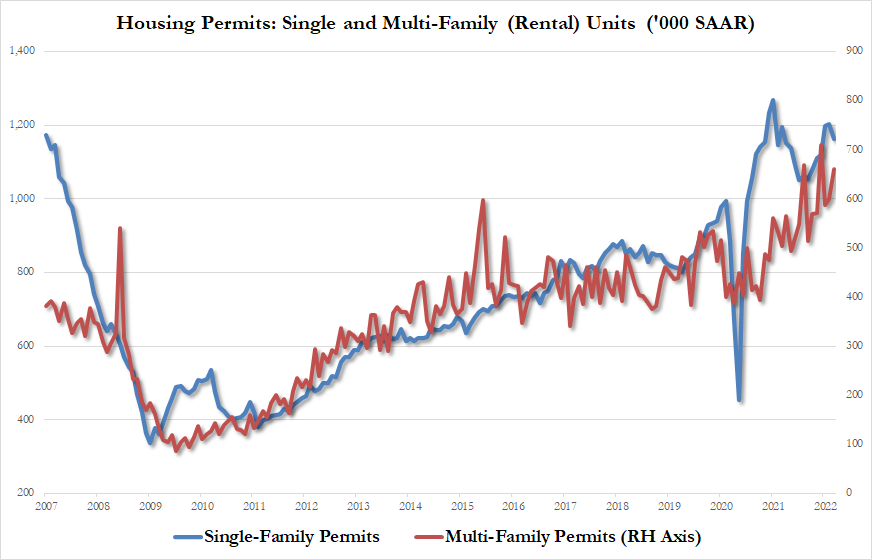

- 07:00: May MBA Mortgage Applications, prior 2.0%

- 08:30: April Building Permits MoM, est. -3.0%, prior 0.4%, revised 0.3%

- 08:30: April Housing Starts MoM, est. -2.1%, prior 0.3%

- 08:30: April Building Permits, est. 1.81m, prior 1.87m, revised 1.87m

- 08:30: April Housing Starts, est. 1.76m, prior 1.79m

DB’s Jim Reid concludes the overnight wrap

Another reminder of my webinar replay from last week discussing our recession call for 2023 and an update on credit spreads. In it I said that while we have high conviction that HY spreads would be +850bp in H2 2023, the outlook over the next few weeks and months may actually be positive from this starting point. I would say I am nervous of that view but I still don’t think that the real economic pain comes until deeper into 2023 when the lagged impact of an aggressive Fed starts to bite. Click here to view the webinar and to download the presentation.

Good luck to Glasgow Rangers and Eintracht Frankfurt in tonight’s Europa League final. These are not teams that any would have expected to reach this final and I will watch with stress free divided loyalties. My father’s family were all from the former and supported Rangers while the latter play at the fabulously named Deutsche Bank Park. So good luck to both. I suspect I’ll be less stress free in 11 days’ time when Liverpool are out for revenge against Real Madrid in the Champions League Final. At the moment I’m feeling nervously optimistic.

Talking of which, investor optimism has returned to markets over the last 24 hours as more positive data releases raised hopes that the US economy might be more resilient in the near-term than many have feared. The economic concerns won’t go away, but stronger-than-expected numbers on retail sales and industrial production helped the S&P 500 (+2.02%) close at its highest level in over a week. Remember monetary policy acts with a lag and it would be very unusual historically if the data rolled over imminently. By this time next year it will likely be a very different story.

The higher yield momentum was reinforced by a Powell speech after Europe went home but there was a steady march of slightly hawkish central bank speakers through the day. Before we review things keep an eye out for UK CPI just after this goes to press. The headline rate is expected to be a huge 9.1%. Expect a lot of headlines reporting of 40 year highs.

With regards to Powell, most in focus was his claim that policy rates would rise above neutral if that was required to tame inflation. While the sentiment was not necessarily new, his explicit comment that neutral rates are “not a stopping point” garnered focus, noting that the Fed was looking for “clear and convincing evidence” that inflation was subsiding. The rates market have already priced terminal policy rates above the Fed’s estimate of neutral, but a combination of the risk on, and stronger data meant that equities could go up alongside yields.

Earlier in the day we got a smattering of communications from Fed regional Presidents, none of which registered as materially but it reinforced the direction of travel after a month to date where markets have repriced the Fed lower. Indeed, even resident hawk, St Louis Fed President Bullard, reiterated Powell’s message in that the Fed was on course for 50bp hikes at the upcoming meetings and said that “I think we have a good plan for now”.

Sovereign bonds had already sold off significantly ahead of all that Fedspeak, aided by the broader risk-on tone yesterday, but continued drifting higher through the US session. Yields on 10yr Treasuries closed +10.4bps to a one-week high of 2.99%, driven by a +7.9bps rise in real yields to 0.24%. The moves were more pronounced at the front-end however, and the 2yr yield rose by a larger +13.1bps as investors priced in a more aggressive path of hikes over the next 12 months after data showed the economy was performing stronger than the consensus had anticipated. In terms of the headlines, retail sales were up by +0.9% in April (vs. +1.0% expected), but the growth in March was revised up to +1.4% (vs. +0.5% previously). Retail sales excluding autos and gas were up by +1.0% as well (vs. +0.7% expected), whilst the industrial production number was another that came in above expectations at +1.1% (vs. +0.5% expected).

Europe also had a large move in yields, which followed comments by Dutch central bank Governor Knot who became the first member of the Governing Council to openly float the idea of a 50bp hike. Although he said that “my preference would be to raise our policy rate by a quarter of a percentage point”, he said that “bigger increases must not be excluded” if data were to show inflation “broadening further or accumulating”. So even though he’s one of the more hawkish members of the council, that’s still a significant milestone in that larger moves are being openly discussed, and echoes what we saw with the Fed at the turn of the year when the policy trajectory became increasingly aggressive.

Market pricing reflected that shift yesterday, and for the first time overnight index swaps were pricing in that the ECB would hike by more than 100bps by their December meeting and thus catching up with the DB House View. That growing belief behind additional hikes led to a fresh selloff in sovereign bonds, with those on 10yr bunds (+10.9bps), OATs (+10.5bps) and BTPs (+11.7bps) all moving higher. The biggest moves were seen from gilts (+15.0bps) however, which followed data that pointed to an increasingly tight labour market in the UK, and overnight index swaps nearly doubled the probability of a 50bp rate hike from the BoE in June, with the odds moving from 17% on Monday to 33% yesterday.

Over in equities, stronger risk appetite led to a significant rebound yesterday, with the S&P 500 (+2.02%) hitting a one-week high, whilst the NASDAQ (+2.76%) saw an even larger rebound in spite of the simultaneous rise in yields. Walmart (-11.38%) was by far the worst performer in the S&P, which came as it cut its earnings per share forecast, which it now expected to decrease by 1%, relative to previous guidance that expected it to rise by the mid single-digits. But that was the exception, and every sector except consumer staples moved higher on the day, with the more cyclical areas leading the advance. Over in Europe the STOXX 600 (+1.22%) posted a strong performance of its own, bringing its advance to more than +5% since its recent closing low just over a week ago.

Overnight in Asia, performance in regional stock indices is diverging partly on the back of economic data. Japan’s Q1 GDP (-1.0%) contracted less than expected (-1.8%), lifting the Nikkei (+0.50%) this morning. In China, though, rising covid cases and waning optimism about government’s support of tech companies weighed on the Shanghai composite (-0.37%) and the Hang Seng (-0.66%). New home prices (-0.30%) in the country also slid for an eighth month in a row. This slight souring of sentiment has extended to S&P 500 futures (-0.23%) with the US 10y yield edging back lower by -2.2bps.

Elsewhere, tensions over Brexit ratcheted up again yesterday after UK Foreign Secretary Truss announced plans to introduce legislation that would override parts of the Northern Ireland Protocol. Truss said that the UK’s preference “remains a negotiated solution with the EU” and that the bill would contain an “explicit power to give effect to a new, revised Protocol if we can reach an accommodation”, but that “the urgency of the situation means we can’t afford to delay any longer.” Unsurprisingly the EU did not react happily, and Commission Vice President Šefčovič said in a statement that if the UK moved ahead with the bill, then “the EU will need to respond with all measures at its disposal.”

Staying on the UK, the latest employment data out yesterday pointed to an increasingly tight labour market, with the unemployment rate falling to 3.7% in the three months to March (vs. 3.8% expected), which is the lowest it’s been since 1974. Furthermore, the number of vacancies was larger than the total number of unemployed for the first time, and the more up-to-date estimate of payrolled employees in April saw an increase of +121k (vs. +51k expected). Elsewhere in Europe, the latest estimate of Euro Area GDP growth in Q1 showed a bigger than expected expansion of +0.3% (vs. +0.2% previously).

Elsewhere the chances of a Russian sovereign debt default increased, following the Treasury department confirming a temporary waiver that allowed Russia to pay US creditors would expire on May 25. Meanwhile, the US is reportedly considering a tariff on Russian oil in conjunction with European allies, as the saga about banning imports to Europe drags on.

To the day ahead now, and data releases include the UK and Canadian CPI readings for April, along with US data on housing starts and building permits for the same month. Central bank speakers include the Fed’s Harker and the ECB’s Muller. Earnings releases include Cisco, Lowe’s, Target and TJX. Finally, G7 finance ministers and central bank governors will be meeting in Germany.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 7.72 PTS OR 0.25% //Hang Sang CLOSED UP 41.36 PTS OR 0.20% /The Nikkei closed UP 251.45 OR 0.94% //Australia’s all ordinaires CLOSED UP 1.03% /Chinese yuan (ONSHORE) closed DOWN 6,7442 /Oil UP TO 114.454dollars per barrel for WTI and UP TO 113.50 for Brent. Stocks in Europe OPENED ALL MOSTLY RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7442 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.74544: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA//COVID

With no vaccinations in North Korea, this country can reach full immunity from COVID. However, Kim’s cure is not good and their citizens are in poor health with less immunity to fight COVID

(zerohedge)

Kim Mobilizes Military To Tackle “Explosive” North Korean COVID Outbreak, Infected Told To ‘Gargle Saltwater’

TUESDAY, MAY 17, 2022 – 11:25 PM

North Korea first acknowledged an “explosive” outbreak of COVID-19 last week, with health officials instructing residents to ‘gargle’ saltwater to treat the virus as medical supplies remain limited and a non-existent vaccine program, Reuters reports.

Leader Kim Jong Un blasted health officials over the slow response to counter the virus and the lack of medication for not reaching people quickly. Kim had to mobilize the army’s medical corps to “stabilize the supply of medicines in Pyongyang City,” according to the state news agency KCNA.

On Monday, North Korean health authorities reported more than 1.2 million have been fever-stricken, with 50 deaths.

With very few COVID treatments, state media have instructed people to use antibiotics, painkillers, and other remedies, such as gargling saltwater and drinking willow leaf tea.

Kim has placed himself in the spotlight of the country’s infectious disease response team, overseeing daily meetings on the outbreak, which he already said has caused “great upheaval.”

North Korea has rejected international help and vaccines for the last 2.5 years. Without immediate help, fatality and infection rates could soar in a country with one of the world’s worst hospital systems.

Most people in the country remain unvaccinated and don’t have strong immune systems because of poor appetite and depressed living standards.

Kim has taken a page out of China’s book and issued a nationwide lockdown to stop the spread.

Some suspect North Korea is significantly underestimating infections and fatalities.

“When people die, North Korean authorities will say they’ve died of overwork or from natural deaths, not because of COVID-19,” Nam Sung-wook, a professor at Korea University in South Korea, told ABC News. He said Kim is likely understating the outbreak to protect his “dignity.”

South Korea’s unification ministry has offered to send masks, test kits, and vaccines, but the North hasn’t acknowledged its neighbor to the south.

Considering the lack of medical treatment, malnourishment and chronic poverty of the vast majority of the population, and lack of a credible hospital system, North Korea could be entering COVID hell.

end

3B JAPAN

3c CHINA

COVID//LOCKDOWNS/SHANGHAI

Yuan initially surges on speculation that Shanghai COVID lockdowns will end soon. It did not last as the yuan closed down.

(zerohedge)

Yuan Surges On Speculation China’s Covid Lockdowns Will End Soon

TUESDAY, MAY 17, 2022 – 07:25 PM

Three weeks ago, when looking at the pattern in China’s covid data, we said that China’s covid panic is almost over…

… a view we repeated a week ago when we warned all those who were short oil – on the “thesis” that China’s lockdowns would last indefinitely – to cover.

Fast forward to today when after more than a month of growing lockdown (and mangled supply chain) fears, there was finally a glimmer of hope at the end of China’s covid tunnel and possibly for Chinese markets.

As Bloomberg notes, Chinese lockdown conditions have improved over May 1-11, versus the April average, with the Goldman Effective Lockdown Index declining to 33.1 points for data so far in May, versus an average of 37.3 over April 1-25. The index is on a declining trend, and bits and pieces of news are mildly encouraging.

Most recently, Shanghai reported no new Covid-19 infections in the broader community for a third consecutive day, a long-awaited milestone which authorities have said will allow them to start unwinding the lockdown (even though most residents will have to put up with confinement for a while longer before resuming more normal life).