May 20, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1844.20 UP $7.75

SILVER: $21.69 DOWN $.20

ACCESS MARKET: GOLD $1846.00

SILVER: $21.76

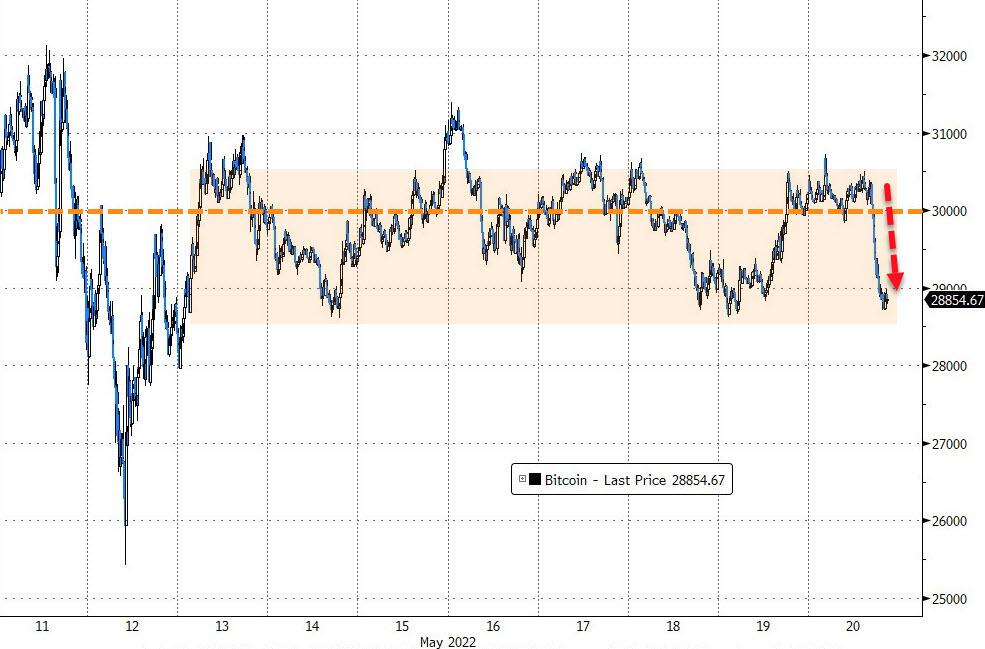

Bitcoin morning price: $30,263 UP 150

Bitcoin: afternoon price: $29,004 DOWN 1109

Platinum price: closing UP $15.10 to $950.85

Palladium price; closing DOWN $56.10 at $1959.15

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,841.200000000 USD

INTENT DATE: 05/19/2022 DELIVERY DATE: 05/23/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 13

435 H SCOTIA CAPITAL 25

657 C MORGAN STANLEY 4

661 C JP MORGAN 121

690 C ABN AMRO 74 22

732 C RBC CAP MARKETS 2

737 C ADVANTAGE 2 1

905 C ADM 28

TOTAL: 146 146

MONTH TO DATE: 5,976

comex notices percentage of JPMorgan notices filed: 121/146

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 146 NOTICE(S) FOR 14,600 OZ (0.4914 TONNES)

total notices so far: 5830 contracts for 583,000. oz (18.1337 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED nil OZ/

total number of notices filed so far this month 5153 : for 25,765,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $7.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A HUGE DEPOSIT OF 6.97 TONNES INTO THE GLD

INVENTORY RESTS AT 1056.18 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 20 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 0.785 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 562.408 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 654 CONTRACTS TO 145,699 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.34 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.34) AND WE ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A NET GAIN OF 747 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 40,000 OZ QUEUE. JUMP //NEW STANDING 27,990,000 MILLION OZ/ // V) GOOD SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -7

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 14 days, total 16,750, contracts: 83.750 million oz OR 5.978 MILLION OZ PER DAY. (1191CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 83.750 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 83.75- MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 661 WITH OUR $0.34 GAIN IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A TINY SIZED EFP ISSUANCE CONTRACTS: 93 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 40,000 OZ QUEUE. JUMP //NEW STANDING 27.990 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 754 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.770 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 0 NOTICE FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 2563 CONTRACTS TO 548,595 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –215 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE FAIR SIZED LOSS IN COMEX OI CAME WITH OUR STRONG GAIN IN PRICE OF $24.20//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 16,900 OZ//NEW STANDING 19.480 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $24.20 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A SMALL SIZED LOSS OF 492 OI CONTRACTS (2.446 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2071 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 548,595

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 492, WITH 2563 CONTRACTS DECREASED AT THE COMEX AND 2071 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 492 CONTRACTS OR 2.466 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2071) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2563,): TOTAL LOSS IN THE TWO EXCHANGES 492 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 16,900 OZ//NEW STANDING 19.480 /// 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

65,204 CONTRACTS OR 6,520,400 OR 202.81 TONNES 14 TRADING DAY(S) AND THUS AVERAGING: 4657 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES: 202.81 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 202.81/3550 x 100% TONNES 5.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 202.81 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 654 CONTRACT OI TO 145,699 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 93 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 93 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 654 CONTRACTS AND ADD TO THE 93 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF747 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 3,735 MILLION OZ

OCCURRED WITH OUR STRONG GAIN IN PRICE OF $0.34 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 10.99 PTS OR 0.36% //Hang Sang CLOSED UP 523.60 PTS OR 2.54% /The Nikkei closed DOWN 508.36 OR 1.89% //Australia’s all ordinaires CLOSED DOWN 1.66% /Chinese yuan (ONSHORE) closed UP 6,7505 /Oil DOWN TO 108.07dollars per barrel for WTI and UP TO 108.00 for Brent. Stocks in Europe OPENED ALL ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7505 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7622: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2563 CONTRACTS TO 548,595 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED DESPITE OUR STRONG GAIN OF $24.20 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2071 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2071 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :2071 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2071 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY TINY SIZED TOTAL OF 277 CONTRACTS IN THAT 2071 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2348 CONTRACTS..AND YET THIS TINY GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG GAIN IN PRICE OF GOLD $24.20.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (19.480),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 19.480 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $24.20) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A SMALL SIZED loss OF 2.466 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (19.079 TONNES)…

WE HAD 215 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 492 CONTRACTS OR 49200 OZ OR 2,466 TONNES

Estimated gold volume today: 170,268/// poor

Confirmed volume yesterday:218,846 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 20

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 1639,701 oz Manfra BRINKS INT DELAWARE INCLUDES 10, 38 AND 3 KILOBARS |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 146 notice(s)14,600 OZ 0.45412 TONNES |

| No of oz to be served (notices) | 287 contracts 28,700 oz 0.8926 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5976 notices 597,600 OZ 18.587 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: 0 oz

3 customer withdrawals:

i) Out of Brink s 321,51 iz (10 kilobars

Int. Delaware 1221.738 oz ( 38 kilobars)

Manfra 96.453 3 kilobars

total withdrawal: 1639.701 oz

ADJUSTMENTS:

a) Manfra: 2607.14 0z

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 433 contracts having LOST ONLY291 contracts

We had 158 notices filed on THURSDAY, so we gained 129 contracts or AN ADDITIONAL 12,900 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 12,291 contracts down to 205,307 contracts

July has a GAIN OF 192 OI to stand at 527

August has a gain of 9537 contracts up to 284,062 contracts

We had 146 notice(s) filed today for 14,600 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 146 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 121 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (5976) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 433 CONTRACTS ) minus the number of notices served upon today 146 x 100 oz per contract equals 626,300 OZ OR 19.48 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (5976) x 100 oz+ (433) OI for the front month minus the number of notices served upon today (146} x 100 oz} which equals 626,300 oz standing OR 19.480 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 19.480 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,064,524.720 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,602,112.786 OZ

TOTAL ELIGIBLE GOLD: 17,613,183.558 OZ

TOTAL OF ALL REGISTERED GOLD: 17,643,183.558 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,557,866.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 20

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 487,447.550 oz Brinks CNT Manfra Delaware Int. Delaware JPMorgan |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 974.910 oz Delaware |

| No of oz served today (contracts) | 0CONTRACT(S)nil OZ) |

| No of oz to be served (notices) | 445 contracts (2,225,000 oz) |

| Total monthly oz silver served (contracts) | 5153 contracts 25,765,,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 974.900 oz

total deposit: 974.900 oz

JPMorgan has a total silver weight: 175.84 million oz/337.779 million =52.16% of comex

Comex withdrawals: 5

i) Out of Brinks 9520.210 oz

ii) Out of CNT: 75,526.000 oz

iii) Out of Delaware 2000.19 oz

iv) Out of Int. Delaware 97,967.110 oz

v) Out of JPMorgan: 302,434.05 oz

total withdrawal 487,447.550 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.093 MILLION OZ

TOTAL REG + ELIG. 337.779 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 445 HAVING LOST 26 CONTRACTS. WE HAD 34 NOTICES FILED ON THURSDAY

SO WE GAINED 8 CONTRACTS OR A QUEUE JUMP OF 40,000 OZ

JUNE HAD A LOSS OF 5 TO STAND AT 1544

JULY HAD A GAIN OF 712 CONTRACTS UP TO 114,195 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes: 33,886// est. volume today// poor

Comex volume: confirmed yesterday: 44,604 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5153 x 5,000 oz = 25,765,000 oz

to which we add the difference between the open interest for the front month of MAY(445) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2022 contract month: 5153 (notices served so far) x 5000 oz + OI for front month of MAY (445) – number of notices served upon today (0) x 5000 oz of silver standing for the MAY contract month equates 27,990,000 oz. .

We GAINED 8 contracts or AN ADDITIONAL 40,000 OZ will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1049.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 562.408 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: The Fed Girds For Battle

FRIDAY, MAY 20, 2022 – 12:25 PM

It’s the Fed’s “hold my beer” moment.

After more than a year in which Federal Reserve leadership appeared clueless, pollyannish, and indecisive, the Fed is conducting a full-throated messaging campaign to show that it is as serious as cancer about the inflation surge that is scaring the bejesus out of consumers, investors, and economists.

Their public pronouncements in recent weeks go something like this: “Out of a good faith misreading of post-pandemic data we had concluded, mistakenly as it happens, that the inflation wave, which began in 2021, was transitory. But now that we know it is not, we are moving with great speed and resolve to bring the problem to heel. Given the power of our tools, the underlying strength of our economy, and our hard-earned credibility, we are confident we can get the job done quickly, and without inflicting undue harm on the economy. We will continue until inflation gets closer to our 2% target. And so, if you don’t mind, kind sir, please step aside and let us do the job we were created to do. We got this!”

This newly found resolve may assure many that at least the Fed is no longer in denial and has a plan to get us out of this mess. In reality, these open-mouth operations are simply a desperate Hail Mary designed to convince us that the Fed can do what it clearly has no stomach or power to do. I would suggest that Fed officials hold onto their beers and drink. They are going to need it.

While most observers have focused on Chairman Jerome Powell’s press conference last week as the clearest insight into the Fed’s thinking, I think more can be gleaned from the extensive conversation two days later in Minneapolis between Christopher Waller, a member of the Federal Reserve Board of Governors (a current voting member of the FOMC) and Neel Kashkari, the President of the Federal Reserve Bank of Minneapolis (and an FOMC alternative member). In particular, Waller offered a very clear assessment of the Fed’s battle plan.

Right off the bat, he confronted mounting criticism that the Fed failed to read the economy accurately over the past 18 months, thereby grossly miscalculating policy, which let the inflation genie out of the bottle. His defense, which essentially boils down to “don’t blame us, no one with mainstream credentials in government, economics, or finance saw this coming,” is both bizarre and inadvertently illuminative. Not only does this ignore the 2021 predictions of former Treasury Secretary Larry Summers, who used to have at least some mainstream credibility, but it completely ignores all those like me who had been shouting from the rooftops that this danger was lurking. Waller’s admission, which shows how deeply embedded Fed leaders are in their own echo chamber, is more of an indictment of the entire economic elite rather than an excuse for their errors.

Waller then admitted that inflation data that was released way back in September 2021 revealed to them that the “transitory story’ that they had been spinning since the beginning of 2021, would no longer hold water. He explained that members of the FOMC were so alarmed that they immediately responded with plans to roll out new messaging that hinted strongly at tighter policy. Say what?

They determined nine months ago that very high inflation had been running rampant for the better part of a year, that it showed no signs of slowing, that the Fed Funds rate (which was then at 0%, and likely 800 basis points below the rate of inflation) was adding fuel to the fire, and the only thing they were prepared to do was to start talking tougher?

The Fed did not implement its first rate hike (25 basis points) until March of this year, fully seven months later! And during that entire time, it continued to expand its balance sheet by hundreds of billions of dollars through quantitative easing rather than immediately stopping the program or, better yet, reversing it. That’s insane. Captain, there is a huge gash in the hull of the ship but rather than try to repair the damage now, let’s think about how we are going to word our next few press releases!

Instead of taking bold steps back in the fourth quarter of last year to get ahead of the curve, or to at least not fall far further behind, the Fed irresponsibly took a slow and muted path. Given its admitted understanding of the conditions nine months ago, its actions seem hard to justify.

Despite these past missteps, Waller claims that the Fed is well-suited to make up for lost time. Emboldened by what he sees as a “historically” strong labor market, Waller believes the current economy can absorb the negative effects of higher interest rates without succumbing to recession. As a result, he predicts the Fed will not be deterred by weaker jobs or economic reports that may emerge in the coming months. In fact, he claims such data would be welcome developments. In his view, the economy needs to lose jobs to be put back into balance. Reduced hiring, he argues, will diminish upward wage pressure, which he sees as the root cause of inflation.

To justify his confidence that higher rates will kill inflation but not the broad economy, Waller took pains to draw a sharp contrast between today’s conditions and those that predominated in the late 1970s/early 1980s, which was the last time the Fed confronted nearly double-digit inflation with bold monetary tightening. Back then, the sharp rise in interest rates brought down inflation AND plunged the country into a recession. But as he views the current economy as benefiting from a “historically strong” labor market, he believes that fate will be avoided.

But Waller is looking at the rear-view mirror. He assumes that the economy that arose during the last decade of almost zero percent interest rates and historically stimulative fiscal policy will persist after those props are removed. But now, as rates increase and stimulus is removed, the economy must contract and change. We are already seeing such a change in the more speculative end of the economy. That’s where the problems are usually first manifest.

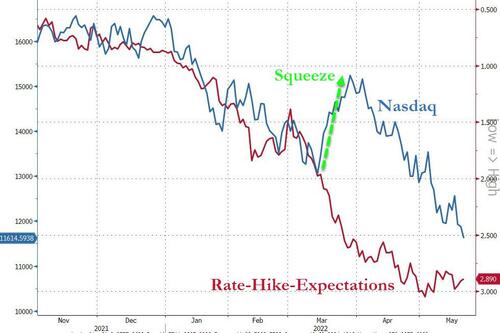

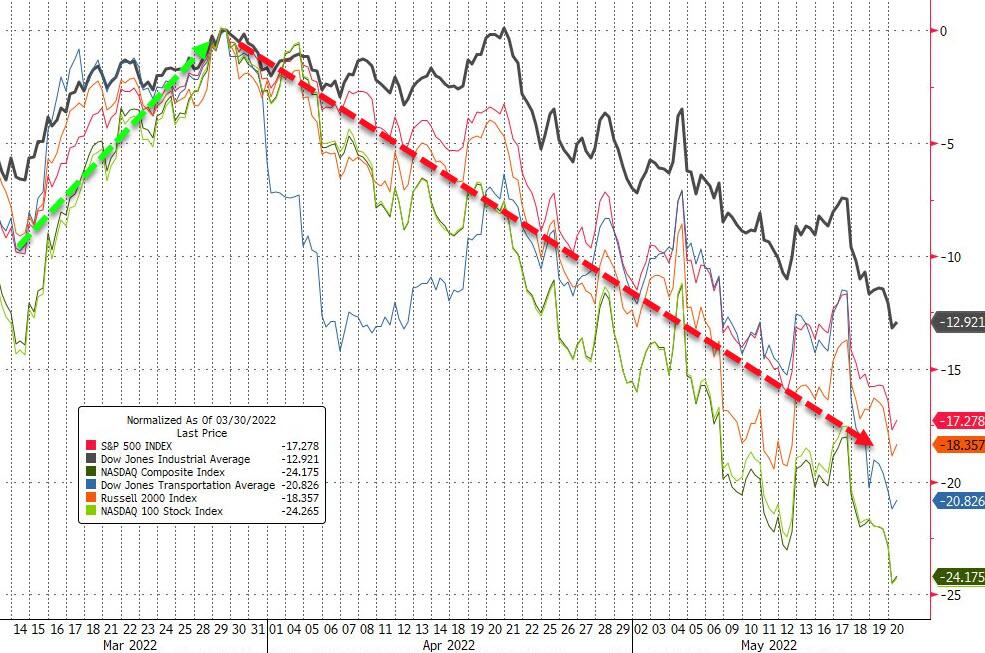

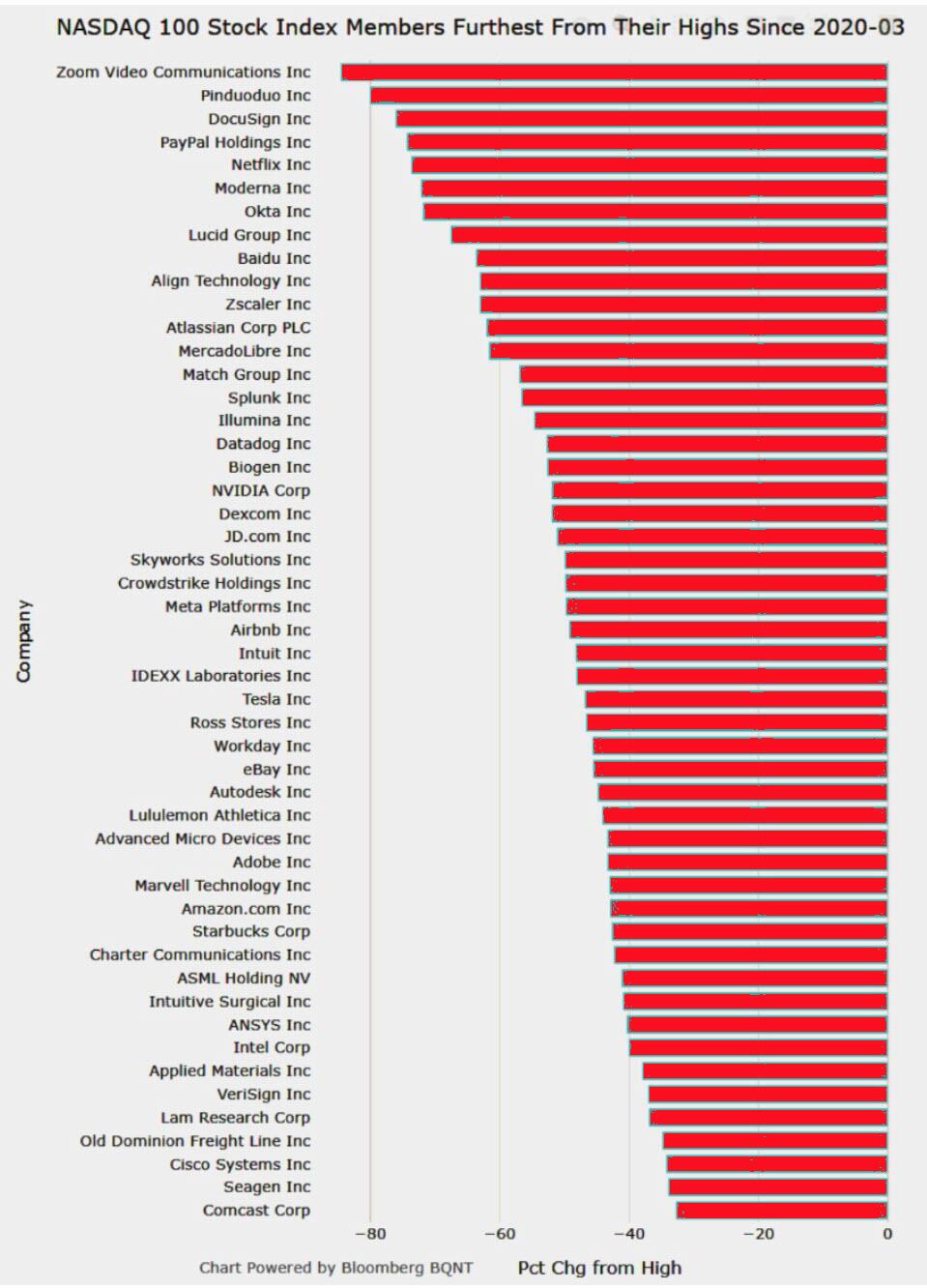

In case you hadn’t noticed, the wheels are coming off the technology and the cryptocurrency sectors. The technology-heavy Nasdaq composite index is down more than 25% thus far this year. The ARK Innovation ETF, which tracks the highest-flying growth-oriented technology, and “new economy” stocks are down 56%. E-commerce bellwethers such as Netflix and Shopify are down even more. The carnage in the crypto space is also spectacular. Although bitcoin is down about 60% from its high, that’s the good news. Lesser-known cryptos are down 70% or 80%. Some have been nearly wiped out completely, even those “stable” coins that were supposed to be pegged to the dollar. The pain extends to the businesses that worked in the crypto space. Financial firm Microstrategies, which borrowed to invest in bitcoin, is down 60% year to date while Coinbase, the crypto trading platform, is down 72%. (Bear in mind that all the losses listed above are just this calendar year. If you started measuring from the November 2021 highs, the losses are significantly greater.)

Recall that the Recession of 2001 and 2002 largely resulted from the implosion of the dot-com bubble when the pain in Silicon Valley rippled through the broader economy. But this time the outsized gains were even bigger and less tethered to reality. Many tech firms have already announced large-scale layoffs. Hundreds of thousands of highly paid workers may suddenly find themselves looking for jobs. Falling stock prices may also encourage recent retirees, who may have been coaxed out of the labor force by oversized stock market gains, or millennials who’ve been trading meme stocks and cryptocurrencies on Robinhood for a living, to join former Netflix, Twitter and Peloton employees in looking for work. Boom will go bust, and the unemployment rate may rise much quicker than Fed models suggest.

Waller also, somewhat bizarrely, believes that the Fed’s job will now be made easier by higher credibility than it had in the late 1970s when Paul Volcker went to war against high inflation. His theory holds that the Fed’s routine failures to confront inflation for much of the 1970s had diminished its credibility, making Volcker’s task that much harder. But by raising rates to nearly 20% in 1980, Volcker restored the credibility, which, in Waller’s view, the Fed holds to this day. He argues that since the Fed has already demonstrated it can do the job, the people are assured it can do it again. This is laughable.

Firstly, the Fed has largely “won” the battle against inflation in recent years by lying about it.

The CPI has been changed and weakened so many times since 1980 that the index barely resembles the one used by Volcker.

Secondly, the Fed has been routinely backing off from tough choices since the Great Recession of 2008.

The taper tantrum of 2013, its painfully slow decisions to lift rates from zero in 2015, the rapid pivot away from tightening to easing in December of 2018, all speak to its jitters in the face of turmoil.

Thirdly, the Fed’s repeated failures to recognize dangerous bubbles in the stock and real estate markets and its pathetic predictions about the mortgage problems in 2007 being “contained” to subprime, or inflation in 2021 being “transitory,” all add to the vaudevillian nature of its economic insight.

If Powell and Waller believe, despite all its recent failures, that the Fed can draw on a 40-year-old mystique generated by a man who passed away more than two years ago, they are in for a very rude awakening.

Left out of the discussion between Kashkari and Waller about the differences between the 1970s and today is how much more leverage we must contend with today and how much higher stock, bond and real estate prices are in relation to the overall economy. Back in 1980, those asset prices had been falling or stagnant for the better part of a decade. Consequently, there weren’t that many gains left to lose. Now stocks, bonds, and real estate are still not far off from record highs. The bursting of those bubbles, which could result from higher interest rates, will be much more recessionary than what happened in 1980.

So, interest rate increases in 2022 and 2023 may be high enough to burst the debt bubble and plunge the economy into another financial crisis, but they will not be nearly high enough to kill inflation. If the Fed has to reverse course to stimulate an economy in recession, while inflation remains well above its 2% target, the dollar will likely collapse, sending commodity prices and the costs of imported goods upward.

As Fed officials tell us how they are ready for battle and that they have the enemy in their sights, I can’t help thinking about “Baghdad Bob,” the hapless spokesman for Saddam Hussein who boldly pronounced in live interviews how the U.S. invasion was failing even as American tanks lumbered into the scene behind him. We can laugh at their predicament. But we won’t laugh long.

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

Rickards: “We Are On The Precipice”

THURSDAY, MAY 19, 2022 – 09:20 PM

Authored by James Rickards via DailyReckoning.com,

I don’t believe many people grasp the enormity of the global food crisis we’ll be facing in the months ahead. But the world could be on the verge of a massive humanitarian crisis. Let’s dive in…

The supply chain collapse preceded the war in Ukraine, but the war has only intensified the problems. You can see it with your own eyes when you walk into a supermarket and find long stretches of empty shelves in stores that used to be chock-full of food and other merchandise.

Even goods that are available such as gasoline are being sold at much higher prices. Prices for gasoline (and diesel, which is critical for goods transportation) have more than doubled in the past nine months. All of this is clear. The question is will it get worse from here?

Unfortunately, the answer is yes.

Bob Unanue is the CEO of Goya Foods, which is one of the largest food distributors in the world. Few people are better positioned to assess the global food situation than Unanue, who deals with raw food deliveries on the one hand and retail customers on the other.

Unanue is now warning, “We are on the precipice of a global food crisis.” Other experts are quoted making a similar point. That’s not hyperbole or fearmongering, but a serious analysis. Here’s why…

29% of All Wheat Exports in Jeopardy

In the Northern Hemisphere, the planting season for 2022 is well underway. Crops were planted (or not) in March and April. Based on that, you can already form estimates of output next September and October during the harvest season (subject to some variability based on weather and other factors).

Plantings have been far below normal in 2022, either due to a lack of fertilizer or to much higher costs for fertilizer where farmers simply chose to plant less. This predictable shortage is in addition to the much greater shortages due to the fact that Russian output is sanctioned and Ukrainian output is nonexistent because it’s at war.

Russia and Ukraine together account for 29% of global wheat and 19% of global corn exports.

Russia and Ukraine together produce 29% of all the wheat exports in the world. That doesn’t mean they grow 29% of the wheat in the world. It means they grow 29% of the wheat exports.

The U.S., Australia, Canada and others grow a lot of wheat but consume most of it themselves. They export relatively little. Importantly, they don’t simply eat it. They feed it to their farm animals. People don’t often make the connection between grain and animal products, but it’s critical.

Many countries get 70–100% of their grains from either Russia or Ukraine or both. Lebanon gets 100%. Egypt is over 70%. Kenya, Sudan, Somalia, many central African countries and Jordan and other Middle Eastern countries receive much of their grain from Russia or Ukraine.

No Planting, No Crops

But it’s worse than that because not only are many Ukrainian exports shut down now, but the planting season is nearly over. And you’re not going to get any grain in October if you didn’t plant it in April or May. And they didn’t for obvious reasons.

What that means is you project ahead to October, November, December of this year, those countries I mentioned are not going to be able to get their grain supplies. There simply aren’t going to be any, or they’ll be greatly reduced. The combined population of countries that get between 70% and 100% of their imports from Russia or Ukraine is 700 million people.

That’s 10% of the global population. So you’re looking at mass starvation. You’re looking at a humanitarian crisis of unprecedented proportions, probably the worst since the Black Death of the 14th century. That’s coming down the road, even if most people can’t see it coming or fully fathom the depths of the coming crisis.

In short, we know enough now to predict much higher prices, empty shelves and, in some cases, mass starvation in the fourth quarter of this year and beyond.

Beyond the humanitarian aspect of the coming food shortages, there are also potentially serious social and geopolitical ramifications.

Another Arab Spring?

You remember the “Arab Spring” starting in 2010. It started in Tunisia and spread from there. Well, it was triggered by a food crisis. There was a shortage of wheat, which triggered the protests.

There were underlying problems in these societies, but a food crisis was the catalyst for the protests.

Now, many poorer countries in the Middle East and Africa are facing a much greater crisis as the impact of shortages manifests itself later this year and into next year. Will we see even more social unrest than in 2011?

It’s very possible, and it could be even more destabilizing than the Arab Spring. We could also see waves of mass migration from Africa and the Middle East as desperate and hungry people flee their homelands.

Europe endured a wave of mass immigration in 2015. Many migrants were attempting to flee the war in Syria, but there were great amounts of people who weren’t affected by the war. They were just seeking better lives in the welfare states of Europe.

Mass starvation could trigger an even greater migration, which would present Europe with enormous challenges.

The United States could also witness another wave of migration at the southern border, which is currently being inundated by migrants. A global food crisis could send the numbers spiraling to uncontrollable limits.

What if the War Drags On?

And what if the war in Ukraine drags on well into next year? Next year’s growing season would also be disrupted and the shortages could extend into late 2023 and beyond.

Well, maybe some would argue that other nations could pick up the slack and grow additional grain. That’s nice in theory, but it’s not that simple.

Russia is the largest exporter of fertilizer, and sanctions are cutting off supplies. Many farmers cannot get fertilizer at all, and those who can are paying between twice and three times last year’s price.

That means that crops actually produced will have much higher prices because of the higher price of inputs such as fertilizer, and the higher transportation costs due to higher prices for diesel and gasoline.

Like I said earlier, we’re looking at a humanitarian crisis of unprecedented proportions, probably the worst since the black death of the 14th century.

And we’re not prepared to handle it.

END

3. Chris Powell of GATA provides to us very important physical commentaries

it’s very weird!

(Bloomberg GATA)

Gold vaulted at Bank of England trades at rare discount in hint of central bank selling

Submitted by admin on Thu, 2022-05-19 10:59Section: Daily Dispatches

By Eddie Spence and Ranjeetha Pakiam

Bloomberg News

Wednesday, May 18, 2022

Gold stored at the Bank of England has been trading at an unusually low price, in a sign that central banks may be shedding some of their holdings.

The Bank of England’s vaults contain 5,676 tons of bullion, one of the largest stockpiles in the world, which it holds on behalf of other central and commercial banks. Gold held by central banks is typically bought and sold between large institutions in bilateral trades at prices usually within a few cents of the market rate.

In recent days, however, gold at the BOE traded as much as a dollar an ounce beneath benchmark London prices, according to traders familiar with the matter. Such a big discount usually indicates a big institution like a central bank selling a sizable amount of reserves to raise US dollars or other currencies, one of the traders said. …

The BOE gold discount has narrowed since the dollar-an-ounce margin, but remains large by normal standards, said the people, who asked not be identified discussing private information. Bullion has slipped more than 12% since peaking in March, leaving it close to unchanged this year.

A spokesperson for the BOE declined to comment on the discount.

… For the remainder of the report:

* * *

end

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIAMONDS

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6758

OFFSHORE YUAN: 6.6859

HANG SANG CLOSED UP 596.56 PTS OR 2.96%

2. Nikkei closed UP 336.19 OR 1.27%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX DOWN TO 102.94/Euro FALLS TO 1.0579

3b Japan 10 YR bond yield: RISES TO. +.240/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 127.97/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield FALLS TO 3.53

3j Gold at $1841.80 silver at: 21.93 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 3 & 1/15 roubles/dollar; ROUBLE AT 58.75

3m oil into the 112 dollar handle for WTI and 112 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 127.94 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9707– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.027well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.869 UP 1 BASIS PTS

USA 30 YR BOND YIELD: 3.075 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.88

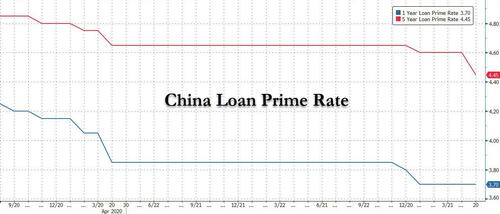

Futures Jump After China Cuts Main Lending Rate By Most On Record But $1.9 Trillion Op-Ex Looms…

FRIDAY, MAY 20, 2022 – 08:02 AM

After months of endless jawboning and almost no action, overnight China finally cut its main mortgage interest rate by the most on record since the rate was introduced in 2019, as it tries to reduce the economic impact of Covid lockdowns and a property sector slowdown. The five-year loan prime rate was lowered from 4.6% to 4.45% on Friday (even as the 1 Year LPR was unchanged at 3.70%) . The reduction in the rate, which is set by a committee of banks and published by the People’s Bank of China, will directly reduce the borrowing costs on outstanding mortgages across the country (the move wasn’t much of a shock as the central bank had kept the 1-Year MLF Rate unchanged earlier in the week and effectively cut interest rates for first-time homebuyers by 20bps on Sunday).

The rate cut was long overdue for China’s property market which has experienced 8 straight months of home-price reductions with developers under extreme pressure. There was more bad news for China’s embattled tech sector as Canada banned Huawei Technologies and ZTE equipment from use in its 5G network.

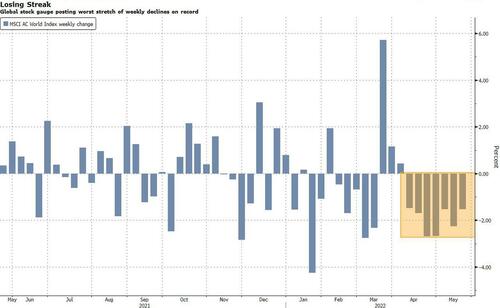

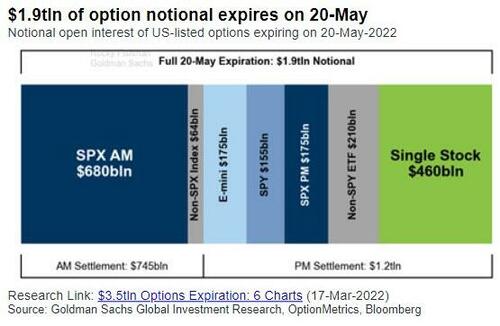

The good news is that China’s easing helped push Asian stocks higher, while European markets and US stock index futures also rose on Friday as buyers returned after a selloff fueled by recession fears saw the underlying S&P 500 lose more than $1 trillion in market value this week. Contracts on the S&P 500 advanced 1.1% as of 7:15a.m. in New York suggesting the index may be able to avoid entering a bear market (which would be triggered by spoos sliding below 3,855) at least for now, although today’s $1.9 trillion Option Expiration will likely lead to substantial volatility, potentially to the downside.

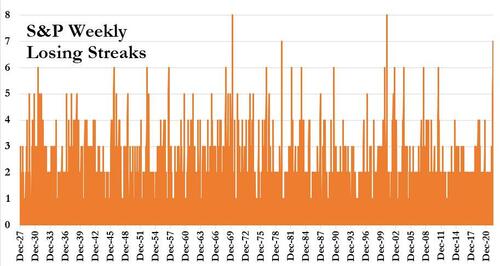

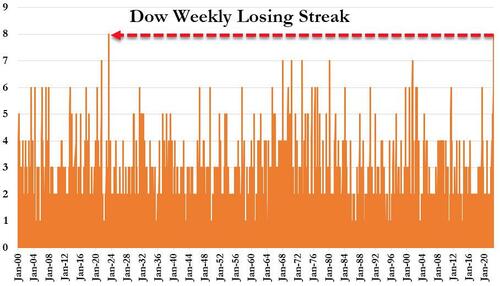

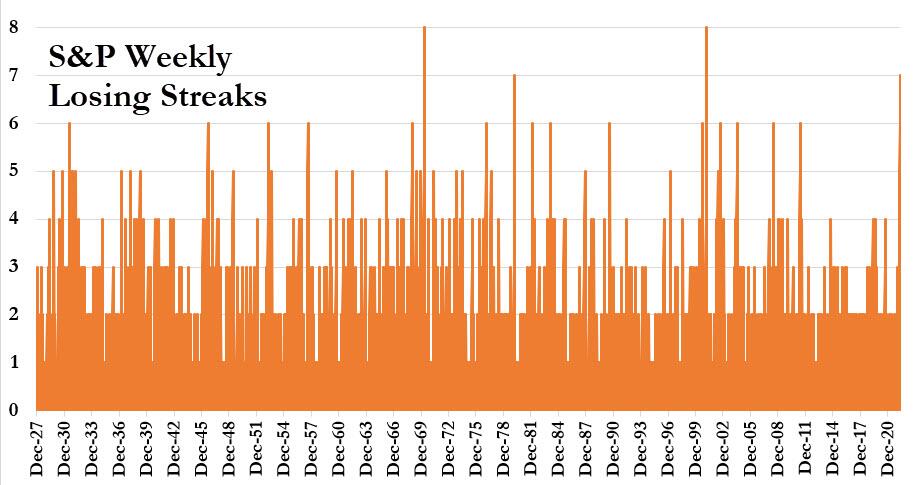

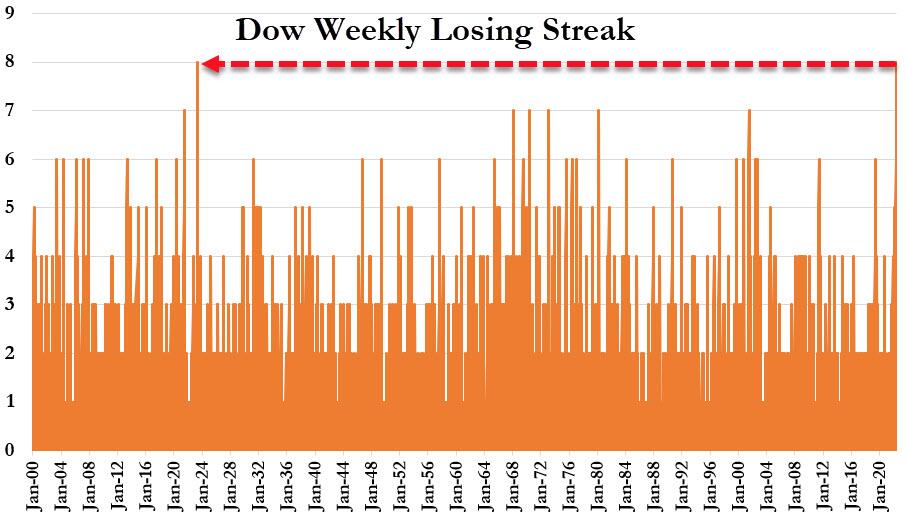

Even with a solid jump today, should it not reverse as most ramps in recent days, the index – which is down almost 19% from its January record – is on track for a seventh week of losses, the longest such streak since March 2001. Futures on the Nasdaq 100 and Dow Jones indexes also gained. 10Y TSY yields rebounded from yesterday’s tumble while the dollar was modestly lower. Gold and bitcoin were flat.

In premarket trading, shares of gigacap tech giants rose, poised to recover some of the losses they incurred this week. Nasdaq 100 futures advanced 1.7%. The tech heavy benchmark has wiped out about $1.3 trillion in market value this month. Apple (AAPL US) is up 1.3% in premarket trading on Friday, Tesla (TSLA US) +2.6%.Palo Alto Networks jumped after topping estimates. Continuing the retail rout, Ross Stores cratered after the discount retailer cut its full-year outlook and first quarter results fell short of expectations. Here are some other notable premarket movers:

- Chinese stocks in US look set to extend this week’s gains on Friday after Chinese banks cut the five-year loan prime rate by a record amount, an effort to boost mortgage and loan demand in an economy hampered by Covid lockdowns. Alibaba (BABA US) +2.6%, Baidu (BIDU US) +1.1%, JD.com (JD US) +2.6%.

- Palo Alto Networks (PANW US) rises 11% in premarket trading on Friday after forecasting adjusted earnings per share for the fourth quarter that exceeded the average of analysts’ estimates.

- Applied Materials (AMAT US) falls 2.1% in premarket trading after its second-quarter results missed expectations as persistent chip shortages weighed on the outlook. However, Cowen analyst Krish Sankar notes that “while the macro/consumer data points have weakened, semicap demand is still healthy.”

- Ross Stores Inc. (ROST US) shares sank 28% in US premarket trade on Friday after the discount retailer cut its full-year outlook and 1Q results fell short of expectations, prompting analysts to slash their price targets.

- Foghorn Therapeutics (FHTX US) shares plunged 26% in postmarket trading after the company said the FDA has placed the phase 1 dose escalation study of FHD-286 in relapsed and/or refractory acute myelogenous leukemia and myelodysplastic syndrome on a partial clinical hold.

- Wix.com (WIX US) cut to equal-weight from overweight at Morgan Stanley as investors are unlikely to “give credit to a show-me story” in the current context which limits upside catalysts in the near term, according to note.

- Deckers Outdoor (DECK US) jumped 13% in US postmarket trading on Thursday after providing a year sales outlook range with a midpoint that beat the average consensus estimate.

- VF Corp’s (VFC US) reported mixed results, with analysts noting the positive performance of the company’s North Face brand, though revenues did miss estimates amid a tricky macro backdrop. The outdoor retailer’s shares rose 2.2% in US postmarket trading on Thursday.

“The ‘risk-on’ trading mood has registered a solid rebound during the last couple of hours as traders cheered the significantly dovish monetary decision from China after the PBoC cut one of the key interest rates by a record amount,” said Pierre Veyret, a technical analyst at ActivTrades. “This will provide a fresh boost to the economy, helping small businesses and mitigate the negative impacts of lockdowns in the world’s second-largest economy.”

Still, the broader market will have to fend off potential risks from options expiration, which is notorious for stirring up volatility. Traders will close old positions for an estimated $1.9 trillion of derivatives while rolling out new exposures on Friday. This time round, $460 billion of derivatives across single stocks is scheduled to expire, and $855 billion of S&P 500-linked contracts will expire according to Goldman.

Rebounds in risk sentiment have tended to fizzle this year. Investors continue to grapple with concerns about an economic downturn, in part as the Federal Reserve hikes interest rates to quell price pressures. Global shares are on course for an historic seventh week of declines.

“The risk-on trading mood has registered a solid rebound during the last couple of hours as traders cheered the significantly dovish monetary decision from China,” said Pierre Veyret, an analyst at ActivTrades. “This move significantly contrasts with the lingering inflation and recession risks in Western economies, where an increasing number of market operators and analysts are questioning the policies of central banks.”

In Europe, the Stoxx Europe 600 index added 1.5%, erasing the week’s losses. The French CAC 40 lags, rising 0.9%. Autos, travel and miners are the strongest-performing sectors, rebounding after two days of declines. Basic resources outperformed as industrial metals rallied. Consumer products was the only sector in the red as Richemont slumped after the Swiss watch and jewelry maker reported operating profit for the full year that missed the average analyst estimate and its Chairman Johann Rupert said China is going to take an economic blow and warned the Chinese economy will suffer for longer than people think. The miss sent luxury stocks plunging: Richemont -11%, Swatch -3.8%, Hermes -3.2%, LVMH -1.9%, Kering -1.7%, Hugo Boss -1.7%, etc. These are the biggest European movers:

- Rockwool rises as much as 10% as the market continued to digest the company’s latest earnings report, which triggered a surge in the shares, with SocGen and BNP Paribas upgrading the stock.

- Valeo and other European auto stocks outperformed, rebounding after two days of losses. Citi says Valeo management confirmed that auto production troughed in April and activity is improving.

- Sinch gained as much as 5.4% after Berenberg said peer’s quarterly results confirmed the cloud communications company’s strong positioning in a fast-growing market.

- Lonza shares gain as much as 4.1% after the pharmaceutical ingredients maker was raised to outperform at RBC, with the broker bullish on the long-term demand dynamics for the firm.

- THG shares surge as much as 32% as British entrepreneur Nick Candy considers an offer to acquire the UK online retailer, while the company separately announced it rejected a rival bid.

- Maersk shares rise as much as 4.6%, snapping two days of declines, as global container rates advance according to Fearnley Securities which says 2H “looks increasingly promising.”

- PostNL shares jump as much as 8.2% after the announcement that Vesa will acquire sole control of the Dutch postal operator. Analysts say reaction in the shares is overdone.

- Dermapharm shares gain as much as 6.1%, the most since March 22, with Stifel saying the pharmaceuticals maker is “significantly undervalued” and have solid growth drivers.

- Richemont shares tumble as much as 14%, the most in more than two years, after the luxury retailer’s FY Ebit was a “clear miss,” with cost increases in operating expenses. Luxury peers were pulled lower alongside Richemont after the company’s disappointing earnings report, in which its CEO also flagged the Chinese market will lag for longer than people assume.

- Instone Real Estate shares drop as much as 12% as the stock is downgraded to hold from buy at Deutsche Bank, with the broker cutting its earnings estimates for the property developer

Earlier in the session, Asia-Pac stocks picked themselves up from recent losses as risk sentiment improved from the choppy US mood. ASX 200 gained with outperformance in tech and mining stocks leading the broad gains across industries. Hang Seng and Shanghai Comp strengthened with a rebound in tech setting the pace in Hong Kong and with the mainland also lifted following the PBoC’s Loan Prime Rate announcement in which it defied the consensus by maintaining the 1-Year LPR at 3.70% but cut the 5-Year LPR by 15bps to 4.45%, which is the reference for mortgages. Nonetheless, this wasn’t much of a shock as the central bank had kept the 1-Year MLF Rate unchanged earlier in the week and effectively cut interest rates for first-time homebuyers by 20bps on Sunday.

Japanese stocks regain footing in the wake of Thursday’s selloff, after Chinese banks cut a key interest rate for long-term loans by a record amount. The Topix rose 0.9% to 1,877.37 at the 3 p.m. close in Tokyo, while the Nikkei 225 advanced 1.3% to 26,739.03. Toyota Motor Corp. contributed the most to the Topix’s gain, increasing 2.1%. Out of 2,171 shares in the index, 1,511 rose and 567 fell, while 93 were unchanged.

In Australia, the S&P/ASX 200 index rose 1.2% to close at 7,145.60 on the eve of Australia’s national election. Technology shares and miners led sector gains. Chalice Mining climbed after getting approvals for further exploration drilling at the Hartog-Dampier targets within its Julimar project. Novonix advanced with other lithium-related shares after IGO announced its first and consistent production of battery grade lithium hydroxide from Kwinana. In New Zealand, the S&P/NZX 50 index rose 0.5% to 11,267.39

India’s benchmark stocks index rebounded from a 10-month low and completed its first weekly gain in six, boosted by an advance in Reliance Industries. The S&P BSE Sensex jumped 2.9% to 54,326.39 in Mumbai. The NSE Nifty 50 Index also rose by a similar magnitude on Friday. Stocks across Asia advanced after Chinese banks lowered a key interest rates for long-term loans. Reliance Industries climbed 5.8%, the largest advance since Nov. 25, and gave the biggest boost to the Sensex, which had all 30 member stocks trading higher. All 19 sector indexes compiled by BSE Ltd. advanced, led by a gauge of realty stocks. “Stocks in Asia and US futures pushed higher today amid a bout of relative calm in markets, though worries about a darkening economic outlook and China’s Covid struggles could yet stoke more volatility,” according to a note from SMC Global Securities Ltd. In earnings, of the 36 Nifty 50 firms that have announced results so far, 21 have either met or exceeded analyst estimates, while 15 have missed forecasts.

In FX, the Bloomberg Dollar Spot Index inched higher as the greenback traded mixed against its Group-of-10 peers. Treasuries fell modestly, with yields rising 1-2bps. The euro weakened after failing to hold on to yesterday’s gains that pushed it above $1.06 for the first time in more than two weeks. Inversion returns for the term structures in the yen and the pound, yet for the euro it’s all about the next meetings by the European Central Bank and the Federal Reserve. The pound rose to a session high at the London open, coinciding with data showing UK retail sales rose more than forecast in April. Retail sales was up 1.4% m/m in April, vs est. -0.3%. Other showed a plunge in consumer confidence to the lowest in at least 48 years. The Swiss franc halted a three-day advance that had taken it to the strongest level against the greenback this month. Australia’s sovereign bonds held opening gains before a federal election Saturday amid fears of a hung parliament, which could stifle infrastructure spending. The Australian and New Zealand dollar reversed earlier losses. The offshore yuan and South Korean won paced gains in emerging Asian currencies as a rally in regional equities bolstered risk appetite.

In rates, Treasuries were slightly cheaper as S&P 500 futures advanced. Yields were higher by 2bp-3bp across the Treasuries curve with 10- year around 2.865%, outperforming bunds and gilts by 1.7bp and 3.5bp on the day; curves spreads remain within 1bp of Thursday’s closing levels. Bunds and Italian bonds fell, underperforming Treasuries, as haven trades were unwound. US session has no Fed speakers or economic data slated. UK gilts 2s10s resume bear-flattening, underperforming Treasuries, after BOE’s Pill said tightening has more to run. Gilts 10y yields regain 1.90%. Bund yield curve-bear steepens. long end trades heavy with 30y yield ~6bps cheaper. Peripheral spreads widen to core with 5y Italy underperforming. Semi-core spreads tighten a touch.

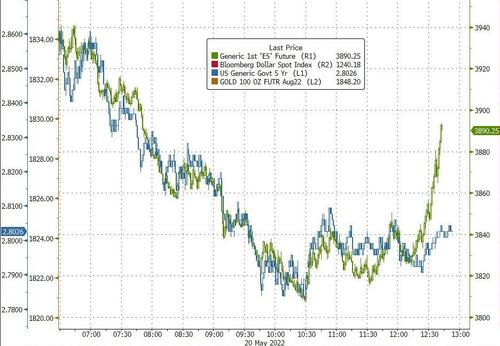

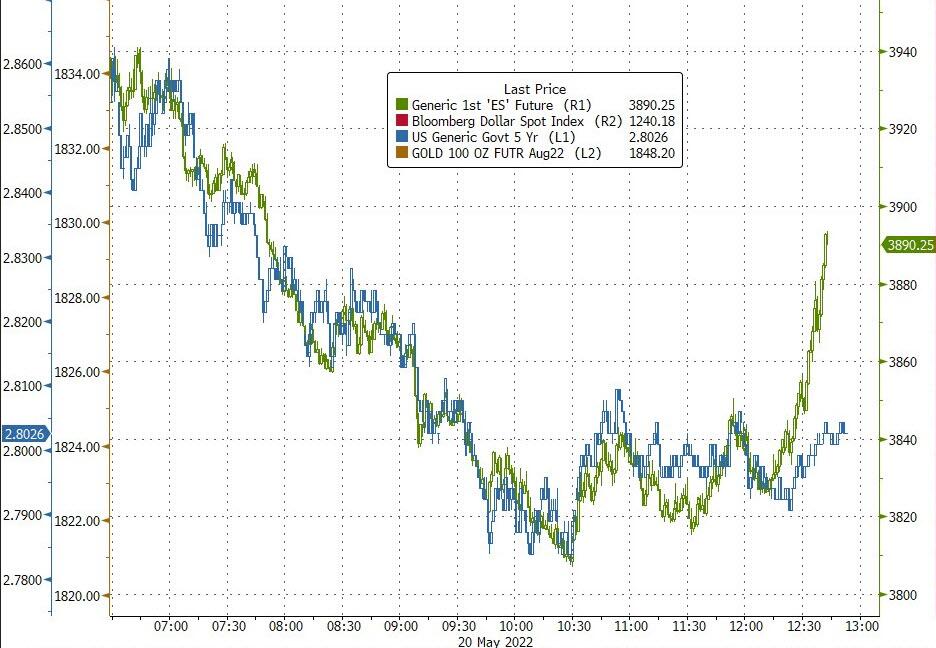

In commodities, WTI trades within Thursday’s range, falling 0.5% to around $111. Most base metals trade in the green; LME lead rises 2.6%, outperforming peers. LME nickel lags, dropping 1.5%. Spot gold is little changed at $1,844/oz. KEY HEADLINES:

Looking at the day ahead, there is no macro news in the US. Central bank speakers include the ECB’s Müller, Kazāks, Šimkus, Centeno and De Cos, along with the BoE’s Pill. Finally, earnings releases include Deere & Company.

Market Snapshot

- S&P 500 futures up 1.1% to 3,940.00

- STOXX Europe 600 up 1.2% to 433.00

- MXAP up 1.6% to 164.68

- MXAPJ up 2.1% to 539.85

- Nikkei up 1.3% to 26,739.03

- Topix up 0.9% to 1,877.37

- Hang Seng Index up 3.0% to 20,717.24

- Shanghai Composite up 1.6% to 3,146.57

- Sensex up 2.5% to 54,115.12

- Australia S&P/ASX 200 up 1.1% to 7,145.64

- Kospi up 1.8% to 2,639.29

- German 10Y yield little changed at 0.97%

- Euro down 0.2% to $1.0567

- Gold spot up 0.2% to $1,845.64

- U.S. Dollar Index up 0.25% to 102.98

- Brent Futures down 0.4% to $111.55/bbl

Top Overnight News from Bloomberg

- BOE Chief Economist Huw Pill said monetary tightening has further to run in the UK because the balance of risks is tilted toward inflation surprising on the upside

- ECB Governing Council Member Visco says a June hike is ‘certainly’ out of the question while July is ‘perhaps’ the time to start rate hikes

- China’s plans to bolster growth as Covid outbreaks and lockdowns crush activity will see a whopping $5.3 trillion pumped into its economy this year

- Chinese banks cut a key interest rate for long- term loans by a record amount, a move that would reduce mortgage costs and may help counter weak loan demand caused by a property slump and Covid lockdowns

- China’s almost-trillion dollar hedge fund industry risks worsening the turmoil in its stock market as deepening portfolio losses trigger forced selling by some managers. About 2,350 stock-related hedge funds last month dropped below a threshold that typically activates clauses requiring them to slash exposures, with many headed toward a level that mandates liquidation

- Investors fled every major asset class in the past week, with US equities and Treasuries a rare exception to massive redemptions

- Ukraine’s central bank is considering a return to regular monetary policy decisions as soon as next month in a sign the country is getting its financial system back on its feet after a shock from Russia’s invasion

- The Group of Seven industrialized nations will agree on more than 18 billion euros ($19 billion) in aid for Ukraine to guarantee the short-term finances of the government in Kyiv, according to German Finance Minister Christian Lindner

- The best may already be over for the almighty dollar as growing fears of a US recession bring down Treasury yields

A more detailed look at global markets courtesy of Newsquqawk

Asia-Pac stocks picked themselves up from recent losses as risk sentiment improved from the choppy US mood. ASX 200 gained with outperformance in tech and mining stocks leading the broad gains across industries. Nikkei 225 was underpinned following the BoJ’s ETF purchases yesterday and despite multi-year high inflation. Hang Seng and Shanghai Comp strengthened with a rebound in tech setting the pace in Hong Kong and with the mainland also lifted following the PBoC’s Loan Prime Rate announcement in which it defied the consensus by maintaining the 1-Year LPR at 3.70% but cut the 5-Year LPR by 15bps to 4.45%, which is the reference for mortgages. Nonetheless, this wasn’t much of a shock as the central bank had kept the 1-Year MLF Rate unchanged earlier in the week and effectively cut interest rates for first-time homebuyers by 20bps on Sunday.

Top Asian News

- Chinese Premier Li vows efforts to aid the resumption of production, via Xinhua; will continue to build itself into a large global market and a hot spot for foreign investment, via Reuters.

- US and Japanese leaders are to urge China to reduce its nuclear arsenal, according to Yomiuri. It was also reported that Japanese PM Kishida is expected to announce a defence budget increase during the summit with US President Biden, according to TV Asahi.

- Offshore Yuan Halts Selloff With Biggest Weekly Gain Since 2017

- Hong Kong Dollar Traders Brace for Rate Spike Amid Intervention

- Shanghai Factory Output Fell 20 Times Faster Than Rest of China

- Japan’s Inflation Tops 2%, Complicating BOJ Stimulus Message

European indices have started the week’s last trading day positively and have extended on gains in early trade. Swiss SMI (+0.5%) sees its upside capped by losses in Richemont which provided a downbeat China outlook. European sectors are almost wholly in the green with a clear pro-cyclical bias/anti-defensive bias – Healthcare, Personal & Consumer Goods, Telecoms, Food & Beverages all reside at the bottom of the chart, whilst Autos & Parts, Travel & Leisure and Retail lead the charge on the upside. US equity futures have also been trending higher since the reopening of futures trading overnight

Top European News

- Holcim, HeidelbergCement Said to Compete for Sika US Unit

- Prosus Looking to Sell $6 Billion Russian Ads Business Avito

- European Autos Outperform in Rebound, Driven by Valeo, Faurecia

- Volkswagen Pitted Against Organic Farmer in Climate Court Clash

FX

- DXY bound tightly to 103.000, but only really firm relative to Yen on renewed risk appetite.

- Yuan back to early May peaks after PBoC easing of 5 year LPR boosts risk sentiment – Usd/Cny and Usd/Cnh both sub-6.7000.

- Kiwi outperforms ahead of anticipated 50 bp RBNZ hike next week and with tailwind from Aussie cross pre-close call election result.

- Euro and Pound capped by resistance at round number levels irrespective of hawkish ECB commentary and surprisingly strong UK consumption data.

- Lira lurching after Turkish President Erdogan rejection of Swedish and Finnish NATO entry bids.

- Japanese PM Kishida says rapid FX moves are undesirable, via Nikkei interview; keeping close ties with overseas currency authorities, via Nikkei.

Fixed Income

- Debt futures reverse course amidst pre-weekend risk revival, partly prompted by PBoC LPR cut.

- Bunds hovering above 153.00, Gilts sub-119.50 and T-note just over 119-16.

- UK debt also taking on board surprisingly strong retail sales metrics and EZ bonds acknowledging more hawkish ECB rhetoric.

Commodities

- WTI and Brent July futures consolidate in early European trade in what has been another volatile week for the crude complex.

- Spot gold has been moving in tandem with the Buck and rose back above its 200 DMA

- Base metals are mostly firmer, with LME copper re-eyeing USD 9,500/t to the upside as the red metal is poised for its first weekly gain in seven weeks

- Russia’s Gazprom continues gas shipments to Europe via Ukraine, with Friday volume at 62.4mln cubic metres (prev. 63.3mbm)

Central Banks

- BoE Chief Economist Pill says inflation is the largest challenge faced by the MPC over the past 25 years. The MPC sees an upside skew in the risks around the inflation baseline in the latter part of the forecast period. Pill said further work needs to be done. “In my view, it would be preferable to have any such gilt sales running ‘in the background’, rather than being responsive to month-to-month data news.”, via the BoE.

- ECB’s Kazaks hopes the first ECB hike will happen in July, according to Bloomberg.

- ECB’s Muller says focus needs to be on fighting high inflation, according to Bloomberg.

- ECB’s Visco says the ECB can move out of negative rate territory; a June hike is “certainly” out of the question but July is perhaps the time to start

- Chinese Loan Prime Rate 1Y (May) 3.70% vs. Exp. 3.65% (Prev. 3.70%); Chinese Loan Prime Rate 5Y (May) 4.45% vs. Exp. 4.60% (Prev. 4.60%)

- Fed’s Kashkari (2023 voter) said they are removing accommodation even faster than they added it at the start of COVID and have done quite a bit to remove support for the economy through forward guidance. Kashkari stated that he does not know how high rates need to go to bring inflation down and does not know the odds of pulling off a soft-landing, while he is seeing some evidence they are in a longer-term high inflation regime and if so, the Fed may need to be more aggressive, according to Reuters

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

The good thing about having all these injuries in recent years is that when it comes down to any father’s football matches or sport day races I now know that no amount of competitive juices make getting involved a good idea. However my wife has not had to learn her lesson yet and tomorrow plays her first netball match for 37 years in a parents vs schoolgirls match. The mums had a practise session on Tuesday and within 3 minutes one of them had snapped their ACL. I’ll be nervously watching from the sidelines.

Markets were also very nervous yesterday after a torrid day for risk sentiment on Tuesday. Although equities fell again yesterday it was all fairly orderly. This morning Asia is bouncing though on fresh China stimulus, something we discussed in yesterday’s CoTD here. More on that below but working through things chronologically, earlier the Stoxx 600 closed -1.37% lower, having missed a large portion of the previous day’s US selloff, but generally continues to out-perform. US equities bounced around, with the S&P 500 staging a recovery from near intraday lows after the European close, moving between red and green all day (perhaps today’s option expiry is creating some additional vol) before closing down -0.58%.