May 19, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1841.95 UP $24.20

SILVER: $21.89 UP $.34

ACCESS MARKET: GOLD $1843.50

SILVER: $21.94

Bitcoin morning price: $29,439 UP 265

Bitcoin: afternoon price: $30,113 UP 939

Platinum price: closing UP $27.05 to $965.95

Palladium price; closing UP $7.65 at $2015.25

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

comex notices percentage of JPMorgan notices filed: 152/158

EXCHANGE: COMEX

CONTRACT: MAY 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,815.900000000 USD

INTENT DATE: 05/18/2022 DELIVERY DATE: 05/20/2022

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 70

657 C MORGAN STANLEY 4

661 C JP MORGAN 152

732 C RBC CAP MARKETS 4

737 C ADVANTAGE 7 2

905 C ADM 77

TOTAL: 158 158

MONTH TO DATE: 5,830

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT 158 NOTICE(S) FOR 15,800 OZ (0.4914 TONNES)

total notices so far: 5830 contracts for 583,000. oz (18.1337 tonnes)

SILVER NOTICES:

34 NOTICE(S) FILED 170,000 OZ/

total number of notices filed so far this month 5153 : for 25,765,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $24.20

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD

INVENTORY RESTS AT 1049.21 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 34 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://A HUGE CHANGE IN SILVER INVENTORY

AT THE SLV.: A WITHDRAWAL OF 1.892 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 563.193 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 511 CONTRACTS TO 145,069 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED DESPITE OUR TINY $0.04 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.04) AND WE ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A NET GAIN OF 977 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 30.170 MILLION OZ FOLLOWED BY TODAY’S 40,000 OZ QUEUE. JUMP //NEW STANDING 27,950,000 MILLION OZ/ // V) GOOD SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -24

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY:

TOTAL CONTACTS for 13 days, total 16,657, contracts: 83.285 million oz OR 6.406 MILLION OZ PER DAY. (1351CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 83.285 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 83.285 MILLION OZ//INCREASING AGAIN

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 511 WITH OUR $0.04 GAIN IN SILVER PRICING AT THE COMEX// WEDENESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 442 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR MAY. OF 30.170 MILLION OZ FOLLOWED BY TODAY;S 40,000 OZ QUEUE. JUMP //NEW STANDING 27.950 MILLION OZ// .. WE HAD A STRONG SIZED GAIN OF 953 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.765 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 34 NOTICE FILED TODAY FOR 170,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4598 CONTRACTS TO 551,158 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: –128 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE GOOD SIZED LOSS IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $2.25//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 5.353 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY”S QUEUE JUMP OF 25,400 OZ//NEW STANDING 19.079 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $2.25 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 10,655 OI CONTRACTS (33.141 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A WHOPPING SIZED 15,253 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 551,158

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,655, WITH 4598 CONTRACTS DECREASED AT THE COMEX AND 15,253 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,783 CONTRACTS OR 33.539 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GIGANTIC SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (15,253) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4598,): TOTAL GAIN IN THE TWO EXCHANGES 10,655 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY. AT 5.353 TONNES FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 25,400 OZ//NEW STANDING 19.079 /// 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) STRONG SIZED COMEX OI. GAIN 5) GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

63,133 CONTRACTS OR 6,313,300 OR 196.37 TONNES 13 TRADING DAY(S) AND THUS AVERAGING: 4856 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES: 196.37 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 196.37/3550 x 100% TONNES 5.52% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 196.37 TONNES INITIAL// INCREASING AGAIN

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GOOD SIZED 511 CONTRACT OI TO 144,534 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 442 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 442 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 511 CONTRACTS AND ADD TO THE 442 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF953 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 4.765 MILLION OZ

OCCURRED DESPITE OUR TINY GAIN IN PRICE OF $0.04 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/cryptocurrencies

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 10.99 PTS OR 0.36% //Hang Sang CLOSED UP 523.60 PTS OR 2.54% /The Nikkei closed DOWN 508.36 OR 1.89% //Australia’s all ordinaires CLOSED DOWN 1.66% /Chinese yuan (ONSHORE) closed UP 6,7505 /Oil DOWN TO 108.07dollars per barrel for WTI and UP TO 108.00 for Brent. Stocks in Europe OPENED ALL ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7505 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7622: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4598 CONTRACTS TO 551,158 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS FAIR COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $2.25 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A GIGANTIC SIZED EFP (15,253 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF MAY.. THE CME REPORTS THAT THE BANKERS ISSUED A WHOPPER SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 15,253 EFP CONTRACTS WERE ISSUED: ;: , . 0 JUNE :15,253 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 15,253 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 10,655 CONTRACTS IN THAT 15,253 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 4598 CONTRACTS..AND YET THE STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF GOLD $2.25.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (19.079),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 19.079 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $2.25) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 33.539 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR MAY (19.079 TONNES)…

WE HAD XX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 10,783 CONTRACTS OR 1,078,300 OZ OR 33.539

TONNES

Estimated gold volume today: 162,967/// poor

Confirmed volume yesterday:167,076 contracts poor

INITIAL STANDINGS FOR MAY ’22 COMEX GOLD //MAY 19

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | COMEX COULD NOTPROVIDE INVENTORY MOVEMENTS TODAY |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | COMEX COULD NOT PROVIDE INVENTORY MOVEMENTS TODAY |

| No of oz served (contracts) today | 158 notice(s)15,800 OZ0.4914 TONNES |

| No of oz to be served (notices) | 304 contracts 30400 oz0.9455 TONNES |

| Total monthly oz gold served (contracts) so far this month | 5830 notices583,000 OZ18.1337 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For today:

dealer deposits XX

total dealer deposit XX oz//

No dealer withdrawals

1 customer deposit

i

total deposits: XXX oz

XX customer withdrawals:

total withdrawal: XXX oz

ADJUSTMENTS:

a) JPM:

XX

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY.

For the front month of MAY we have an oi of 462 contracts having LOST ONLY 31 contracts

We had 285 notices filed on WEDNESDAY, so we gained 254 contracts or AN ADDITIONAL 25,400 oz will stand for delivery in this non active delivery month of May.

June saw a loss of 21,596 contracts down to 217,598 contracts

July has a GAIN OF 12 OI to stand at 335

August has a gain of 16M851 contracts up to 274,525 contracts

We had 158 notice(s) filed today for 15,800 oz FOR THE MAY 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 158 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 152 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAY /2021. contract month,

we take the total number of notices filed so far for the month (5830) x 100 oz , to which we add the difference between the open interest for the front month of (MAY 462 CONTRACTS ) minus the number of notices served upon today 158 x 100 oz per contract equals 613,400 OZ OR 19.079 TONNES the number of TONNES standing in this non active month of MAY.

thus the INITIAL standings for gold for the MAY contract month:

No of notices filed so far (5830) x 100 oz+ (462) OI for the front month minus the number of notices served upon today (158} x 100 oz} which equals 613,400 oz standing OR 19.079 TONNES in this NON active delivery month of MAY.

TOTAL COMEX GOLD STANDING: 19.079 TONNES (A STRONG STANDING FOR A MAY ( NON ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,026,795.134 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,793,598.694 OZ

TOTAL ELIGIBLE GOLD: 17,812,062.336 OZ

TOTAL OF ALL REGISTERED GOLD: 17,961,536.365 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,948,662.0 OZ (REG GOLD- PLEDGED GOLD)

END

MAY 2022 CONTRACT MONTH//SILVER//MAY 19

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | XXX oz COMEX COULD NOT PROVIDE THIS DATA TODAY |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | COMEX COULD NOT PROVIDE |

| No of oz served today (contracts) | 34CONTRACT(S)170,000 OZ) |

| No of oz to be served (notices) | 437 contracts (2,185,000 oz) |

| Total monthly oz silver served (contracts) | 5153 contracts 25,765,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: nXX oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have XX deposits into the customer account

total deposit: XXX oz

JPMorgan has a total silver weight: 176.729 million oz/339.387 million =52.12% of comex

Comex withdrawals: XX

total withdrawal XX oz

X adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 80.674 MILLION OZ

TOTAL REG + ELIG. 339.387 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF MAY OI: 471 HAVING LOST 89 CONTRACTS. WE HAD 97 NOTICES FILED ON MONDAY

SO WE GAINED 8 CONTRACTS OR A QUEUE JUMP OF 40,000 OZ

JUNE HAD A GAIN OF 6 TO STAND AT 1549

JULY HAD A GAIN OF 139 CONTRACTS UP TO 113,483 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 34 for 170,000 oz

Comex volumes: 34,067// est. volume today// poor

Comex volume: confirmed yesterday: 43,461 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5153 x 5,000 oz = 25,765,000 oz

to which we add the difference between the open interest for the front month of MAY(471) and the number of notices served upon today 34 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY./2022 contract month: 5153 (notices served so far) x 5000 oz + OI for front month of MAY (471) – number of notices served upon today (34) x 5000 oz of silver standing for the MAY contract month equates 27,950,000 oz. .

We GAINED 8 contracts or AN ADDITIONAL 40,000 OZ will stand for delivery at the comex

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1049.21 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 563.193 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

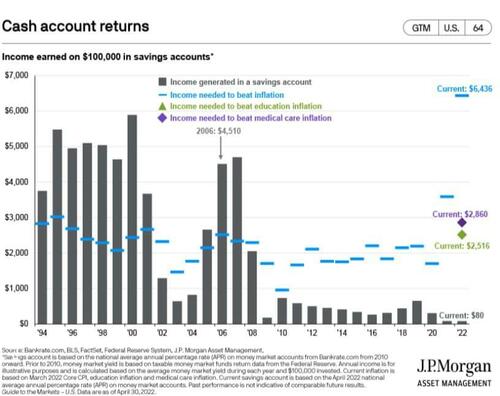

1.PETER SCHIFF

The Fed Has Destroyed Our Savings

THURSDAY, MAY 19, 2022 – 01:20 PM

Authored by Michael Maharrey via SchiffGold.com,

When I was about seven or eight years old, I remember my mom taking me to the bank to open a savings account. She explained that if I put some of my allowance in savings, that money would grow over time.

Well, that doesn’t work anymore.

In fact, if you put your money in a savings account, you’ll end up with less than you started with – at least in terms of real purchasing power.

The last time a cash savings account yielded enough interest income to beat inflation was in 2007.

This provides yet another example of how Federal Reserve monetary policy creates misallocations and distortions in the economy.

Looking closely at the chart, you’ll notice that savings yields fall below the inflation level when the Fed engages in loose monetary policy.

The first dip below the inflation level is in 2002 — in the wake of the bursting dot-com bubble. In 2001, the Fed began pushing interest rates down. It started at 6% in January 2001 and by January 2002, rates were pegged at 1.25%.

We see the next plunge in savings yields in 2008, as the Fed dropped rates to zero and launched quantitative easing in response to the Great Recession.

Since then, savings have never recovered. Cash accounts failed to generate enough income to beat inflation even during the “low inflation” years after the financial crisis.

I often talk about the Federal Reserve creating “misallocations” in the economy. This is one example. Because it is impossible for people to generate a real return simply by sticking money in a savings account, they are forced to chase yield with more risky investments. In this day and age, you can’t put money in the bank and expect to retire in 30 years. You have to wade into the stock market, real estate, or other investments that come with more risk.

It’s not so much that risky investments are bad. The problem is that people are forced to take risks they wouldn’t otherwise take. Artificially low interest rates, incentivize risk-taking behavior.

Looking at the bigger picture, this incentivization of risk contributes to asset bubbles – that eventually pop.

One way to protect your wealth over time is to buy gold. Gold doesn’t generate yield, but it also doesn’t tend to lose purchasing power as the dollar devalues over time. For instance, an ounce of gold bought a nice suit 100 years ago. Today, an ounce of gold will still buy a nice suit.

And gold doesn’t carry a high level of risk. It is a physical asset you can hold in your hand. It is also liquid, meaning you can convert it into dollars quickly should the need arise.

One thing is clear – sticking dollars in the bank isn’t a good investment strategy anymore — not while we have a central bank content to artificially manipulate interest rates and devalue the dollar.

2.LAWRIE WILLIAMS//,//Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, James RICKARDS/

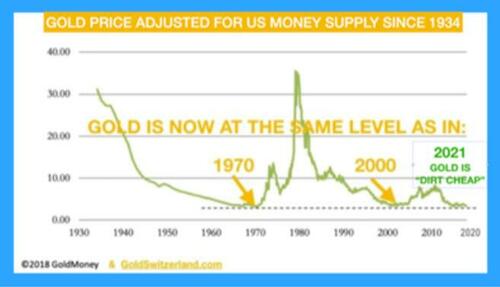

Von Greyerz: Gold As ‘Cheap’ Today As In 1971

THURSDAY, MAY 19, 2022 – 06:30 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

“Specie (gold and silver coin) is the most perfect medium because it will preserve its own level, because having intrinsic and universal value, it can never die in our hands, and it is the surest resource of reliance in time of war.”

– Thomas Jefferson

Since no current President or Prime Minister nor any Central Bank Chairman understands what money is or the relevance of gold, we turn above back to history and Thomas Jefferson, America’s third president for a proper definition.

Jefferson also understood that “Paper is Poverty, It is only the Ghost of Money, and not Money itself.”

As the world economy goes towards an inflationary depression exacerbated not only by epic debts and deficits but now also by war, the significance of gold takes on a whole different dimension.

So let’s dissect Jefferson’s statement:

“(GOLD) Will preserve its own level”

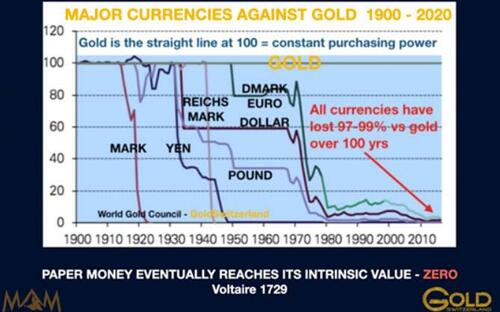

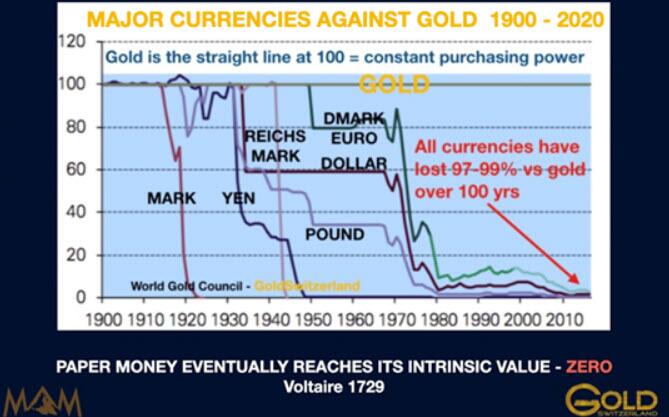

Gold is Constant Purchasing Power. As such, gold doesn’t go up in real terms. An ounce of gold today buys a good suit for a man just like it did in Roman times.

The graph below shows gold as constant purchasing power at the 100 line whilst all the currencies are crashing to the bottom.

All currencies are continuing to lose value against real money although it never takes place in a straight line. With higher interest rates & inflation, higher deficits & debts, poverty, cost of wars and increasing pressures in the financial system, the currency debasement will now accelerate.

Gold is not an investment. Gold is eternal money. As such gold maintains its REAL value whereas paper money loses all its value over time. For 5000 years gold has outlived all other forms of money including paper money.

We must remember that every paper currency in history has gone to ZERO, with no exception. The current monetary system is currently taking its last breaths. With the dollar and most currencies having lost 99% since the Fed was founded in 1913 and 98% since Nixon closed the Gold Window in 1971, it is guaranteed that the remaining 1-2% will be lost in the next few years.

But as I often point out, a loss of the remaining 1-2% means a 100% fall from today.

Anyone who doesn’t understand that is guaranteed to lose all his paper wealth within the next 5-10 years and possibly sooner.

“Intrinsic and universal value, it can never die in our hands”

Throughout history, Gold has never and will never become worthless. Gold is nature’s money and eternal.

Crypto currencies have for many become a religion or cult. For the ones who got in early, there were spectacular gains to be made. I do see that the blockchain could be useful technology but it could never be real money.

So cryptos have nothing to do with real money – gold. Also, they do not serve as a true form of wealth preservation. Bitcoin halving and Luna “dying in investors’ hands” and crashing to zero is certainly not conducive to protecting your wealth.

I am sure that central banks around the world will introduce Central Bank Digital Currencies – CBDCs. But these new currencies are just another form of Fiat money. As such they can and will be created in unlimited amounts and lose most of their value over time just like paper money. The one advantage for governments is of course the ability to track all transactions in their desire to control us all in a dystopian 1984 scenario.

But totalitarian societies do not survive since they are both against the laws of nature and human nature. Nevertheless they can create a very unpleasant period for many people.

The WEF’s (World Economic Forum) objective to create a society in which everybody will be poor and happy is total nonsense which would fail miserably just as a totalitarian society.

Yes, the WEF has a lot of billionaires and political leaders who love mixing with each other under the command of their leader Klaus Schwab, also a billionaire.

But the WEF will collapse as the billionaires lose most of their wealth and the Trudeaus of this world are thrown out in the greatest wealth transfer in history.

“Surest resource of reliance in time of war”

In every crisis in history, gold has always been money, both for nations and individuals. Since gold is universal money, it is the best medium of exchange for people fleeing from a war torn country. Since wars also often produce inflation and debasement of paper money, gold is the “surest resource” and is accepted in all countries.

So why is gold not going up and why don’t more people buy gold if it is so cheap?

I get these questions regularly.

All the ingredients are certainly in place for gold to go up:

INFLATION

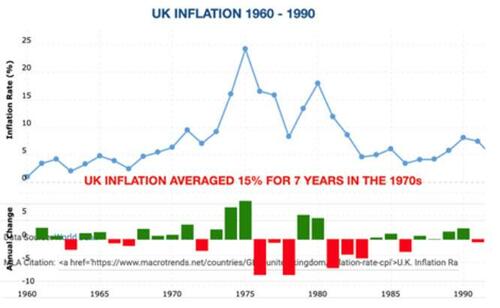

Inflation is increasing rapidly and most certainly soon reaching into the teens in many countries.

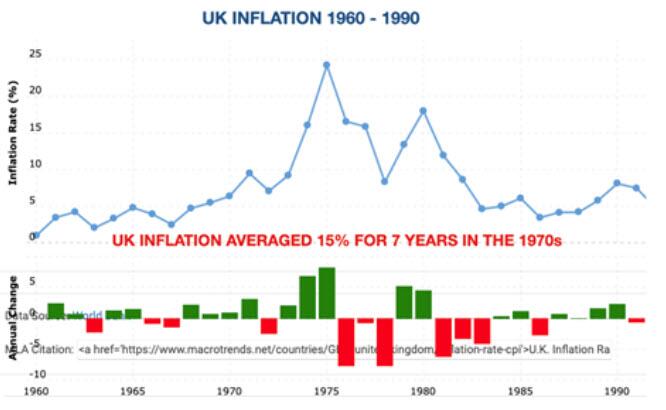

Having experienced inflation in the 1970s in the UK, I know how quickly it can accelerate. Between 1974 and 1981 UK inflation stayed above 10%, peaking at 24%. The average during that period was around 15%.

At an annual inflation rate of 15%, prices double every 5 years.

I would be surprised if inflation in many countries in the West doesn’t reach the 15% level.

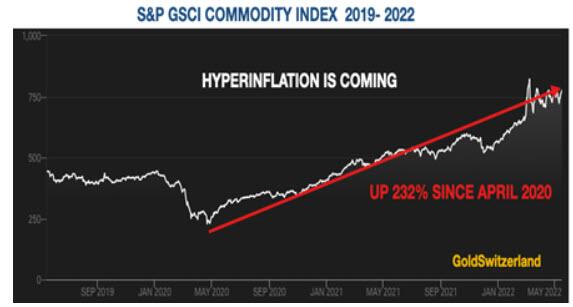

Commodity Shortages

There is a global shortage of commodities. Prices already started to rise in April 2020. The GSCI Commodity Index has gone up 232% since April 2020. Since the Ukrainian crisis started on February 20 this year, commodity prices are up 18%. The UN Food Agency stated already in the autumn of 2021 that the situation of food shortages was catastrophic and that was before the cut off of major supplies from Ukraine and Russia.

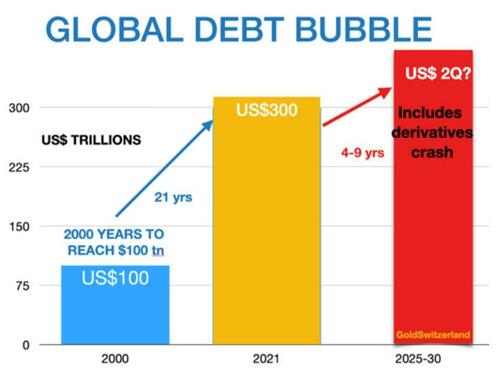

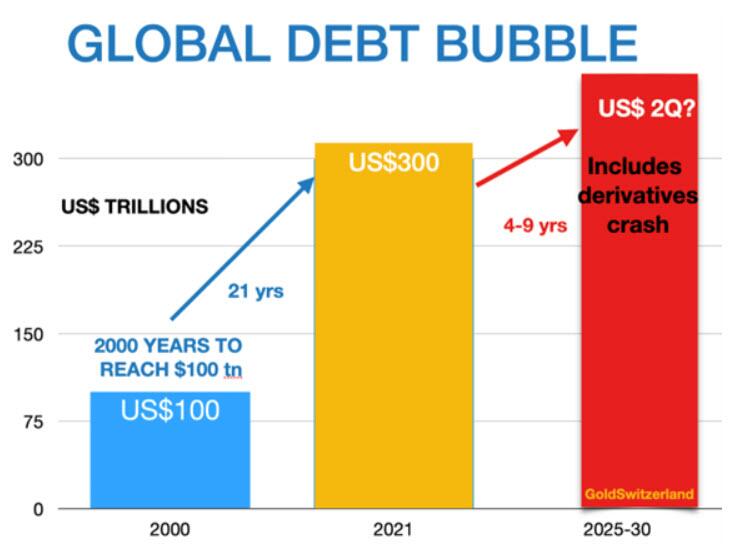

Growth of Global Debt & Money Supply

Global debt is growing exponentially and has trebled in this century. Growth in debt and money supply above GDP growth has over time a direct impact on inflation rates.

Most of the money created since the Great Financial Crisis 2006-9 has not reached consumers but gone into asset markets like stocks, bonds and property. That has kept the velocity of money at very low levels and until recently not affected consumer prices. But that is all about to change with rapid inflation increases to follow.

Nobody Owns Gold!

So if gold is the best performing asset class in this century why are only 0.5% of world financial assets invested in physical gold?

The simple answer is that most investors neither understand nor follow gold, which is why it is so cheap.

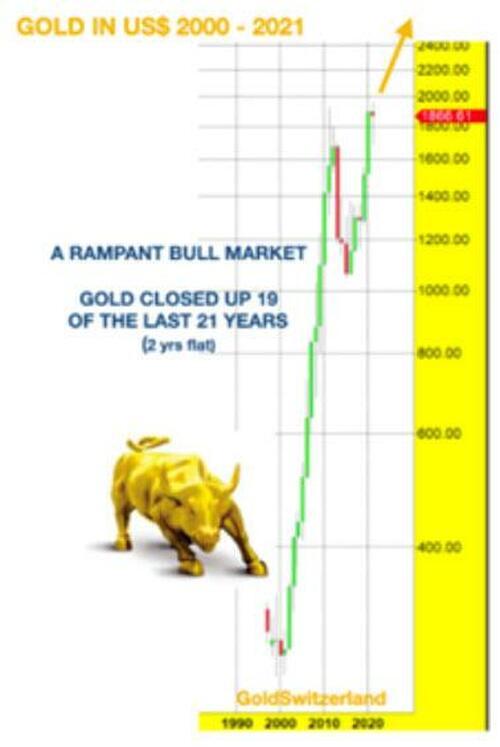

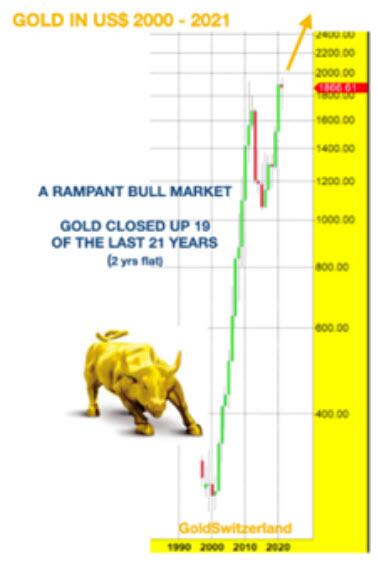

Virtually no investor is aware that gold has been the best performing asset class in the last 22 years.

But as inflation continues to rise, institutional investors in particular will be required to buy inflation protection. Stocks, bonds and property have become bubble assets with a massive downside risk and offering ZERO inflation protection.

Many investors will therefore turn to physical gold and precious metals mining stocks.

The total value of the 33 biggest mining stocks is only $210 billion with only 6 worth more than $10 billion.

Global stock market capitalisation is just over $90 trillion so gold mining stocks represent only 0.2% of that.

And if we add the total value of physical gold for private investment, total investable gold assets amount to $2.5 trillion. With global financial investment assets at $220 trillion, the physical gold investment market is only just over 1% of global assets.

What is clear is that the total sums in gold mining stocks or physical gold is minuscule compared to global financial investments.

So when institutional and other investors move into the gold market and increase their holdings from 0.5% to 1% of world financial assets, that would involve a $1.1 trillion investment in gold and gold mining stocks which at today’s prices would represent 50% of that market globally. And if the gold investments went from 0.5% to 1.5% of global assets, that would mean buying all the gold available in the world for investment.

It is self-evident that those quantities would not be available. The only way to satisfy increasing demand in the gold sector would be at a much higher price which could easily be 10x higher than current prices.

Gold on the Cusp of a Major Move

Gold went up 25x in the 1970s and then paused for almost 20 years as stock markets moved up substantially. Gold then bottomed in 1999-2000 at $250. Since then gold has outperformed stocks and most other asset markets.

Measured against paper money, gold went up around 8x since between 1999 and the 2011-12 peak.

It feels like gold has corrected for a very long time since the 2011-2 peak. But if we look at the annual chart of gold in dollars below, we find that the correction only lasted for 3 years in 2013 to 2015.

Studying the chart closely we find that between 2001 and today, there have only been three down years (red bars).

So what we are looking at is a very strong performance already and that is before we will see the effect of all the positive factors for gold mentioned above.

To measure gold in debasing fiat money does not serve much purpose. If I say that gold will go to $25,000, it is meaningless if we don’t relate the price to inflation or purchasing power.

I stated many years ago that gold will go to at least $10,000 in today’s money and that is still a realistic forecast bearing in mind all the positive factors for gold currently.

Or expressed more correctly, the negative factors for fiat money and for the world.

So when will Gold go up then?

Having been properly invested in physical gold for ourselves and our investors since early 2002, we never worry about the shorter term.

Gold is for long term wealth preservation and not for short term gratification.

Still, I know that many gold investors as opposed to wealth preservationists are still impatient.

Short term gold could be finishing a corrective move this week or in the next few weeks. $1,800 is support but as we know, support lines are often tested in order to drive out the longs.

So whatever happens in the short term is of little significance.

Long term I have not changed my mind that gold will reach levels which few can imagine.

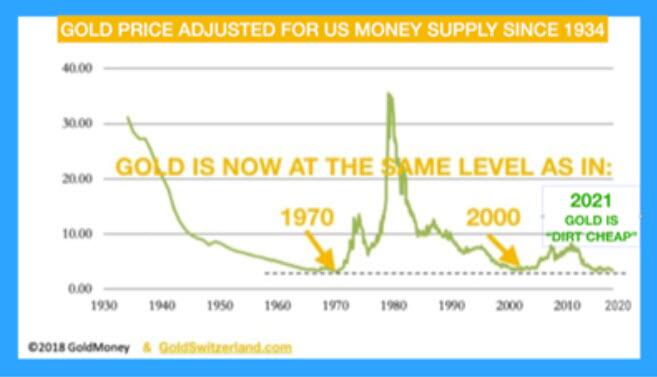

GOLD AS CHEAP AS IN 1971 AND 2000

Finally my favourite chart which shows that gold is a cheap today relative to US money supply as in 1971 when the price was $35 and in 2000 when gold was $290…

-END-

3. Chris Powell of GATA provides to us very important physical commentaries

Good luck to Portugal if we want to obtain their half of its gold reserves stored at the Bank of England

(Reuters)

Portugal says more than half of its gold is at Bank of England

Submitted by admin on Wed, 2022-05-18 20:18Section: Daily Dispatches

So why doesn’t the country’s central bank try showing it off there instead?

* * *

Portugal’s Central Bank Opens Its Vaults for Rare Glimpse of Gold Bars

By Sergio Goncalves and Pedro Nunes

Reuters

Wednesday, May 18, 2022

LISBON — Portugal’s central bank has opened up its heavily guarded vaults in a small commuter town near Lisbon, giving a rare glimpse of where some of the country’s gold reserves are kept.

The 67,000-square-metre compound in Carregado houses an ultra-secure vault where the Bank of Portugal stores 382.6 tonnes of gold, 45% of its reserves. The remaining 55% is abroad, mostly in the Bank of England in London

“Gold is an important asset for central banks as it is a refuge asset and has no credit risks,” said Bank of Portugal board member Helder Rosalino said Tuesday during the rare media visit to the facility, guarded by armed police officers. …

… For the remainder of the report:

end

How stupid can these guys get?

(Spence/Bloomberg/GATA)

Swiss gold refiner MKS PAMP plans to try to become environmental enforcer

Submitted by admin on Wed, 2022-05-18 20:34Section: Daily Dispatches

Maybe countries that want to remain independent will have to open their own refineries and take charge of their own carbon-emission standards.

* * *

Gold Refiner to Stop Working With Mines That Miss Carbon Goals

By Eddie Spence

Bloomberg News

Wednesday, May 18, 2022

One of the biggest gold refineries will look to stop sourcing metal from mines that fail to meet standards on carbon emissions.

MKS PAMP SA plans to curb emissions that come from its supply chain by 27.5% before the end of the decade, the company said in a statement today. As a result the Geneva-based firm may have to refuse gold from mines that create too much carbon dioxide.

Extraction of the metal forms the bulk of gold’s carbon footprint. Miners emitted almost a ton of carbon dioxide per ounce mined in 2019, according to S&P Global. The industry as a whole accounts for about 0.2% of the world’s emissions, Wood Mackenzie wrote in a report. …

… For the remainder of the report:

end

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIAMONDS

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7505

OFFSHORE YUAN: 6.7622

HANG SANG CLOSED DOWN 523.60 PTS OR 1.89%

2. Nikkei closed DOWN 508.36 OR 1.89%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 103.41/Euro RISES TO 1.0517

3b Japan 10 YR bond yield: FALLS TO. +.238/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 127.94/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield FALLS TO 3.53

3j Gold at $1829.90 silver at: 21.70 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 & 4/10 roubles/dollar; ROUBLE AT 62.03

3m oil into the 108 dollar handle for WTI and 108 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 127.94 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9765– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0267well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.838 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.021 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 15.99

Market Rout Extends With Futures Tumbling To Verge Of Bear Market

THURSDAY, MAY 19, 2022 – 08:02 AM

US stock futures slumped again, extending yesterday’s brutal selloff that erased $1.5 trillion in market value on concerns about everything from slowing growth, to Chinese lockdowns, to soaring inflation and tightening monetary policy. Contracts on the S&P 500 were down 1.2% 7:30 a.m. in New York, having earlier dropped to 3,856, one point away sliding 20% from January’s all time highs, and triggering a bear market. The underlying index tumbled 4% on Wednesday, the most since June 2020, as consumer shares cratered after Target slashed its profit forecast due to a surge in costs. Nasdaq 100 futures were down 1.2%. 10Y TSY Yields slumped about 7bps, dropping to 2.833, while the dollar also dropped after yesterday’s surge; bitcoin was flat around $29K.

The retail rout continued on Thursday: shares of US retailers again tumbled in premarket trading amid growing worries over the impact of rising inflation and the ability of companies to pass on higher costs to consumers; with Bath & Body Works becoming the latest retailer to cut its guidance. Major technology and internet stocks were also down, pointing to further losses in major technology and internet stocks a day after the tech-heavy Nasdaq slumped to its lowest since November 2020. Apple (AAPL US) -1.2%, Microsoft (MSFT US) -1.2%, Meta Platforms (FB US) -1.1%, Netflix (NFLX US) -0.9% and Nvidia (NVDA US) -2.2% in premarket trading. US rail stocks may be in focus as Citi cuts ratings on Norfolk Southern (NSC US), Union Pacific (UNP US) and US Xpress Enterprises (USX US) to neutral from buy, while lowering 2023 estimates “across the board.”Here are some other notable movers:

- Cisco Systems (CSCO US) plunged 13% in premarket trading after the network-gear maker spooked investors with a warning that Chinese lockdowns and other supply disruptions would wipe out sales growth in the current quarter. Shares of networking equipment makers drop after Cisco cuts outlook, with Broadcom (AVGO US) -3.6% and Juniper Networks (JNPR US) -5.9% in premarket trading.

- Synopsys (SNPS US) rises 3.8% in premarket trading after the supplier of software used to design semiconductors boosted its profit and revenue guidance for the full year.

- Target (TGT US) shares fall 2.2% in premarket trading, Walmart (WMT US) -0.3%; Kohl’s (KSS US) is in focus after two senior executives depart

- Under Armour (UAA US) shares dropped as much as 6% in US premarket trading, with analysts saying that the departure of the sportswear maker’s CEO Patrik Frisk is a surprise and adds uncertainty.

- Bath & Body Works’s (BBWI US) outlook cut was a little greater than expected, though analysts noted that it was due to higher costs and investment. The company’s shares fell almost 4% in premarket trading.

- United Wholesale Mortgage (UWMC US) will struggle to main its 1Q earnings level in coming quarters, Piper Sandler says in a note downgrading the stock to underweight from neutral. Shares drop as much as 7% in US premarket trading.

The S&P 500 is on track for its longest weekly losing streak since 2001 as traders flee risk assets over fears that the Federal Reserve will push the economy into a recession as it tries to curb inflation. The benchmark is close to falling into a bear market, after dropping 18% from a record high in January.

“The US selloff was rather orderly and the market isn’t oversold, yet. That tells us that we are likely not at the bottom yet,” said Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. “Consumer sentiment remains depressed and we are seeing consumers retrenching on some discretionary spending.”

Speaking on Tuesday in his most hawkish remarks to date, Fed Chair Jerome Powell said the US central bank will keep raising interest rates until there is “clear and convincing” evidence that inflation is in retreat. JPMorgan’s Marko Kolanovic, meanwhile, said – what else – that things can get better for US stocks. “There will be no recession this year, some summer increase in consumer activity on the back of reopening, China increasing monetary and fiscal measures,” he said. Bolstering his opinion is a conviction that US inflation has probably peaked, or is about to do so, paving the way for a pullback in price pressures that will eventually allow the Federal Reserve to moderate the pace of monetary tightening.

“Since we are pricing in a growth scare but not yet a recession, we could see further downside in the coming weeks, but we are starting to price in a very negative picture already, suggesting we should, at some point, be closer to the bottom,” said Esty Dwek, chief investment officer at Flowbank SA. US stock investors are pricing in stronger odds of a recession than are evident from positive macroeconomic indicators, according to Goldman Sachs strategists.

“A recession is not inevitable,” Goldman strategists led by David J. Kostin wrote in a note. “Rotations within the US equity market indicate that investors are pricing elevated odds of a downturn compared with the strength of recent economic data.”

Bets that robust earnings can help investors weather this year’s turbulence were thrown in doubt after US consumer titans signaled growing impact of high inflation on margins and consumer spending. Meanwhile, Federal Reserve officials reaffirmed that tighter monetary policy lies ahead, and investors fretted over stagflation risks.

“We are pricing in a growth scare,” Lori Calvasina, the head of US equity strategy at RBC Capital Markets, told Bloomberg TV. “There is a lot of uncertainty in this market right now about whether or not that recession is going to come through or if it’s going to be another near-death experience.”

There was some more good news on the China covid lockdown front: Shanghai Vice Mayor said Shanghai port throughput recovered to around 90% of the levels a year ago and that Shanghai will expand work resumption in areas with no COVID risk in early June. Furthermore, Shanghai is to gradually restore inter-district public transport from May 22nd and will require residents to show negative PCR tests taken within 48 hours before using public transport, while an economy official said Shanghai will reduce rents for small and medium-sized enterprises by more than CNY 10bln and the city extended CNY 72.3bln of loans to over 10,000 firms since March, according to Reuters.

In Europe, the Stoxx 600 retreated 1.8%, after sliding more than 2% earlier, with all industry sectors in the red and personal care and financial services leading the decline as Wednesday’s retailer trouble in the U.S. spills over into Europe. FTSE 100 lags regional peers, dropping 2%. Here are some of the biggest European movers today:

- HomeServe shares jump as much as 12% after Brookfield agrees to buy the home emergency and repair services company for GBP4.1b.

- Societe Generale shares rise as much as 1.5%, as it was raised to outperform from market perform at KBW, with the broker saying the sale of Russian activities removes a key overhang for the bank and should result in a re-rating.

- Generali shares rose as much as 1.4% after 1Q profit beats analyst estimates as EU136m impairments on Russian investments were more than offset by higher operating income.

- PGNiG shares rise as much as 6.2% after reporting 1Q results that, according to analysts, support Polish gas company’s outlook.

- Nestle shares drop as much as 5.3% after Bernstein downgraded the stock to market perform from outperform, saying the shares will “struggle” if market sentiment improves and investors exit havens.

- Royal Mail shares fall as much as 14% after the postal group’s FY results slightly missed estimates and analysts said its outlook is “disappointing.”

- National Grid shares fall as much as 2.5%, erasing gains from yesterday’s record high, after the utility company reported full-year results.

Earlier in the session, shares of Asian retailers follow their US counterparts lower after Target became the second big retailer in two days to trim its profit forecast.

- Australia: JB Hi-Fi retreats 6.6%, Wesfarmers -7.8%, Harvey Norman -5.5%, Woolworths -5.6%

- South Korea: E-Mart – 3.4%; apparel makers Hansae -9.4%, F&F -4.2%, Youngone -8.2%

- Japan: Fast Retailing – 3.1%, MatsukiyoCocokara -1.4%, Ryohin Keikaku -1.7%, Nitori -3%

- Singapore: Grocery chain operator Sheng Siong slips as much as 1.3%

- Hong Kong: Sun Art Retail down as much as 4.1%

In China, Tencent Holdings Ltd. plunged 6.6% after warning it will take time for Beijing to act on promises to prop up the Chinese tech sector. Cisco Systems Inc. slid in extended US trading on a disappointing revenue outlook.

Japan’s Nikkei 225 suffered firm losses amid reports the ruling coalition is considering increasing the corporate tax rate and after several data releases in which Machinery Orders topped estimates but Exports missed as China-bound exports declined by the fastest pace since March 2020.

Indian stocks declined to a ten-month low, tracking a sell-off across Asia, on concerns the US Fed’s hawkish stance on inflation may cool economic activity and hurt consumer demand. The S&P BSE Sensex plunged 2.6% to 52,792.23, its lowest level since July 30, in Mumbai, while the NSE Nifty 50 Index slipped 2.7% to 15,809.40 Software exporter Infosys Ltd. fell 5.4% to a 11-month low and was the biggest drag on the Sensex, which had 27 of 30 member stocks trading lower. All 19 sector indexes compiled by BSE Ltd. declined, led by S&P BSE Information Technology index, that dropped the most in over two years. “Deteriorating macro sentiment such as soaring inflation, recession fears, and the prospect of the Federal Reserve getting even more hawkish will continue to keep benchmarks on the edge,” Prashanth Tapse, an analyst at Mehta Equities Ltd., wrote in a note. In earnings, of the 36 Nifty 50 firms that have announced results so far, 21 have either met or exceeded analyst estimates, while 15 have missed forecasts.

In Australia, the S&P/ASX 200 index fell 1.7% to close at 7,064.50, tumbling with global shares as concerns over inflation, interest-rate hikes and Ukraine piled up. All sectors dropped, except for health. Consumer shares were among the worst performers, following their US peers lower after Target became the second big retailer in two days to trim its profit forecast. Aristocrat rose after it released its 1H results and unveiled buyback plans. In New Zealand, the S&P/NZX 50 index fell 0.5% to 11,206.93

And in emerging markets, Sri Lanka fell into default for the first time in its history as the government struggles to halt an economic meltdown that prompted mass protests and a political crisis. An index of developing-nation stocks slumped more than 2%.

In FX, the Bloomberg dollar spot index declines, with all G-10 majors rising against the greenback. CHF is the strongest G-10 performer with USD/CHF snapping lower on to a 0.97 handle and EUR/CHF slumping below 1.03. The Swiss franc diverged from Japanese yen and dollar after hawkish comments from SNB’s Thomas Jordan Wednesday, which assured traders CHF rates could follow EUR higher. Options trades may also be behind the latest move in the spot market.

In rates, Treasury yields dropped about seven basis points as investors sought insurance against further declines in risk assets. Treasury yields richer by up to 6bp across belly of the curve, richening the 2s5s30s fly by 2.2bp on the day; 10-year yields around 2.83% with German 10-year outperforming by 2.5bps. Treasuries extended Wednesday’s rally as stocks resume slide with S&P 500 futures dropping under 3,900 to lowest level in a year; on the curve, the belly led the advance while bunds outperform in a more aggressive bull-flattening move as European stocks tumble. US session highlights include 10-year TIPS reopening at 1pm ET. Flurry of block trades during London session follows a spate of trades Wednesday; five blocks worth a combined cash-equivalent $1.2m/DV01 between 3:38am and 5:35am similarly entailed price action consistent with sales. Most European bonds also gained, with the yield on German 10-year securities falling more than basis points. German yield curve bull-flattens: 30-year yield drops ~9bps before stalling near 1.05% which has acted as support for much of May so far.

The Dollar issuance slate empty so far; eight borrowers priced $8.5b Wednesday, and new issue activity is expected to be muted during remainder of the week. Three-month dollar Libor +2.69bp to 1.50486%. Economic data slate includes May Philadelphia Fed business outlook and initial jobless claims (8:30am), April existing homes sales and leading index (10am).

In commodities, crude oil extended declines, while most industrial metals were in the red as global growth fears damped the demand outlook. WTI reverses Asia’s gains, dropping back below $110 but holding above Wednesday’s lows. Spot gold is comparatively quiet, holding above $1,810/oz. Most base metals trade in the green; LME tin rises 2.1%, outperforming peers while copper held near a seven-month low and zinc extended losses.

Bitcoin is modestly softer in a relatively contained range that lies just shy of the USD 30k mark. Crypto exchange FTX to start rollout of new stock-trading service on Thursday, WSJ reports; will not accept payment for order flow on stock trades.

Looking to the day ahead now, and data releases from the US include the weekly initial jobless claims, along with April’s existing home sales and the Philadelphia Fed’s business outlook survey for May. Central bank speakers include ECB Vice President de Guindos, the ECB’s Holzmann and the Fed’s Kashkari. Finally, the ECB will be publishing the minutes from their April meeting.

Market Snapshot

- S&P 500 futures down 1.1% to 3,879.25

- STOXX Europe 600 down 1.7% to 426.41

- MXAP down 1.8% to 161.60

- MXAPJ down 2.2% to 527.30

- Nikkei down 1.9% to 26,402.84

- Topix down 1.3% to 1,860.08

- Hang Seng Index down 2.5% to 20,120.68

- Shanghai Composite up 0.4% to 3,096.97

- Sensex down 2.4% to 52,926.71

- Australia S&P/ASX 200 down 1.6% to 7,064.46

- Kospi down 1.3% to 2,592.34

- Gold spot down 0.1% to $1,814.49

- U.S. Dollar Index down 0.28% to 103.52

- German 10Y yield little changed at 0.96%

- Euro up 0.3% to $1.0496

- Brent Futures down 0.1% to $109.00/bbl

Top Overnight News from Bloomberg

- President Joe Biden is set to meet on Thursday with Finland’s President Sauli Niinisto and Swedish Prime Minister Magdalena Andersson at the White House to discuss the Nordic nations’ NATO bids.

- China’s top diplomat again warned the US over its increased support for Taiwan, showing the island democracy remains a major sticking point between the world’s biggest economies as Beijing sent more military aircraft toward the island

- Sri Lanka fell into default for the first time in its history as the government struggles to halt an economic meltdown that prompted mass protests and a political crisis

- The yuan’s outlook is finally looking more balanced after a 6.5% dive versus its major trading partner currencies since March.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were pressured on spillover selling after the worst day on Wall St in almost two years. ASX 200 was led lower by consumer staples following the retailer woes stateside and mixed Australian jobs data. Nikkei 225 suffered firm losses amid reports the ruling coalition is considering increasing the corporate tax rate and after several data releases in which Machinery Orders topped estimates but Exports missed as China-bound exports declined by the fastest pace since March 2020. Hang Seng and Shanghai Comp initially weakened with the Hong Kong benchmark dragged lower by heavy losses in tech after Tencent’s profit declined by more than 50% and with the mainland pressured as Beijing conducts a fresh round of mass COVID testing, although the mainland bourse recovered most of its losses after Shanghai announced a further gradual easing of restrictions. Xiaomi (1810 HK) Q1 adj. net profit CNY 2.859bln (vs 6.069bln Y/Y), Q1 revenue CNY 73.4bln (vs. 76.9bln Y/Y); global smartphone shipments -10.5% Y/Y at 38.5mln units.

Top Asian News

- Shanghai Vice Mayor said Shanghai port throughput recovered to around 90% of the levels a year ago and that Shanghai will expand work resumption in areas with no COVID risk in early June. Furthermore, Shanghai is to gradually restore inter-district public transport from May 22nd and will require residents to show negative PCR tests taken within 48 hours before using public transport, while an economy official said Shanghai will reduce rents for small and medium-sized enterprises by more than CNY 10bln and the city extended CNY 72.3bln of loans to over 10,000 firms since March, according to Reuters.

- Japanese MOF official said China’s COVID curbs are among the factors that caused a decline in China-bound exports from Japan which fell by the fastest pace since March 2020, while Japan’s April imports reached the largest amount on record, according to Reuters.

- Japan’s ruling coalition is reportedly considering increasing the corporate tax rate, according to Jiji.

- New Zealand sees 2021/22 OBEGAL at NZD -18.98bln (prev. forecast -20.44bln), 2021/22 net debt at 36.9% of GDP (prev. forecast 37.6%) and Cash Balance at NZD -31.78bln (prev. forecast -34.10bln), while Finance Minister Robertson said the economy is expected to be robust in the near term and they see a return to OBEGAL surplus in 2024/25, according to Reuters.

European bourses are pressured across the board in a broader risk-off moves after yesterday’s Wall St. sell off, as European players look past the brief respite seen overnight on Shanghai’s reopening; Euro Stoxx 50 -2.3%. Stateside, the magnitude of the downside is somewhat more contained given newsflow has been limited since Wednesday’s downside commenced, ES -1.2%.

Top European News

- EU is reportedly considering a targeted trade war on troublesome Brexiteer MPs and Tory ministers to force UK PM Johnson to do a U-turn on the Northern Ireland protocol, according to The Telegraph.

- Top UK Economist Defends BOE’s Handling of Inflation Crisis

- EasyJet Bookings Pick Up Ahead of Uncertain Summer Season

- Apax-Owned Rodenstock Acquires Spanish Rival Indo

- European Gas Slips With LNG Imports Helping Boost Stockpiles

In FX

- Franc resurgence and re-emergence as a safe haven currency continues; USD/CHF touches 0.9750 vs 1.0060+ peak on Monday, EUR/CHF sub-1.0250 vs circa 1.0500 at one stage only yesterday.

- Dollar loses momentum as US Treasury yields retreat further and curve re-flattens amidst ongoing risk rout, DXY ducks under 103.500 after peaking just shy of 104.000 on Wednesday.

- Kiwi and Aussie find positives via fiscal and fundamental factors to evade aversion; NZD/USD back above 0.6300 after NZ budget and AUD/USD hovering around 0.7000 post- Aussie jobs data.

- Yen retains underlying bid irrespective of mixed Japanese data, USD/JPY below 128.00 again.

- Euro firmer beyond EUR/CHF cross ahead of ECB minutes and Sterling off UK inflation data lows awaiting retail sales on Friday, EUR/USD retains sight of 1.0500 and Cable near 1.2400.

- Rand meandering ahead of SARB in anticipation of 50 bp rate hike, USD/ZAR around 16.0000, irrespective of Gold taking firmer hold of USD 1800/oz handle.

Fixed Income

- Debt resumes safe-haven rally as market mood continues to sour.

- Bunds top 154.00, Gilts get close to 120.00 and 10 year T-note even nearer the same psychological level.

- BTPs lag amidst the ongoing aversion to risk, while OATs and Bonos reflect on somewhat mixed auction results.

Commodities

- WTI and Brent are pressured in-fitting with broader sentiment as initial resilience on demand-side positives re. China/COVID were overpowered by the risk move.

- However, the benchmarks are around USD 1.00/bbl off lows of USD 104.36/bbl and USD 106.76/bbl respectively, following reports that China is discussing the purchase of Russian crude.

- China is said to be in talks with Russia to purchase oil for strategic reserves, according to Bloomberg sources; detailed on terms and volume reportedly not decided yet

- Qatar Energy was reportedly selling July Al-Shaheen crude at premiums of USD 5.80-6.40/bbl above Dubai quotes which is the highest in 2 months, according to Reuters sources.

- Spot gold is bid as it draws haven allure, with the yellow metal marginally surpassing USD 1830/oz.

US Event Calendar

- 08:30: May Initial Jobless Claims, est. 200,000, prior 203,000; Continuing Claims, est. 1.32m, prior 1.34m

- 08:30: May Philadelphia Fed Business Outl, est. 15.0, prior 17.6

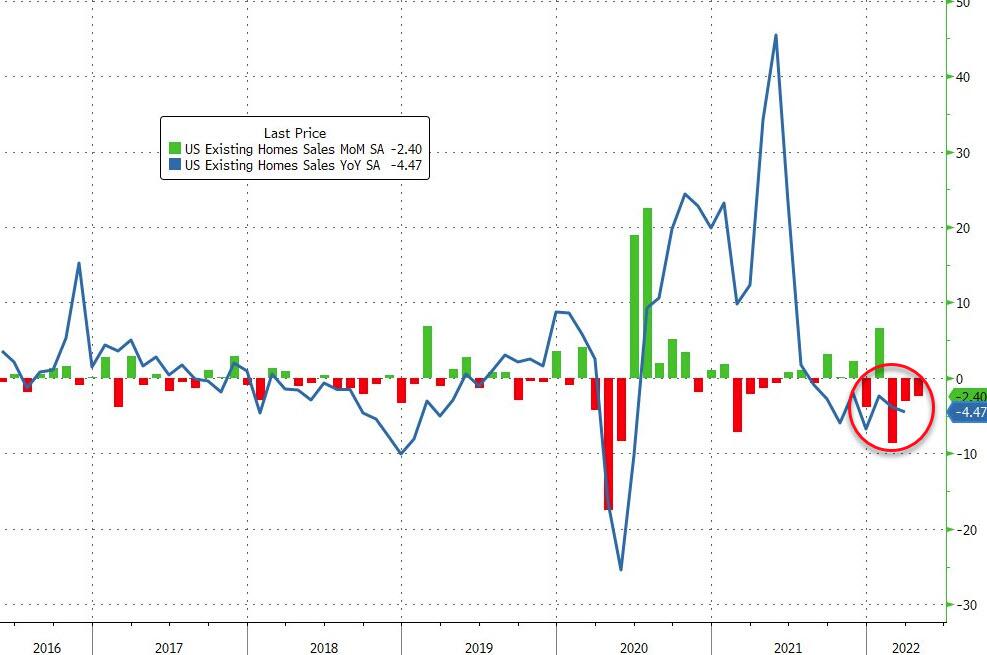

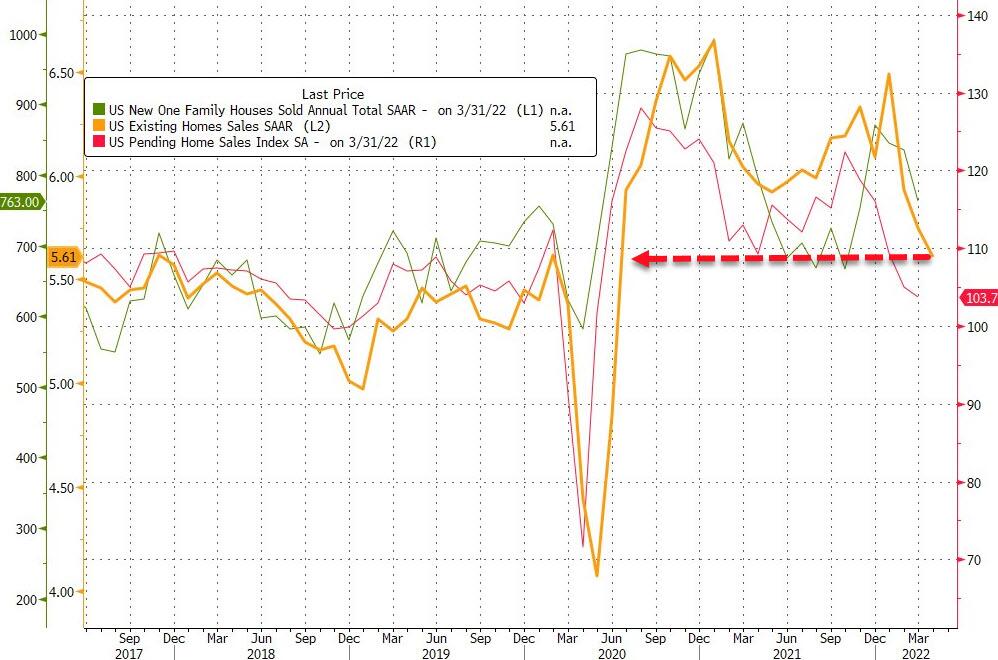

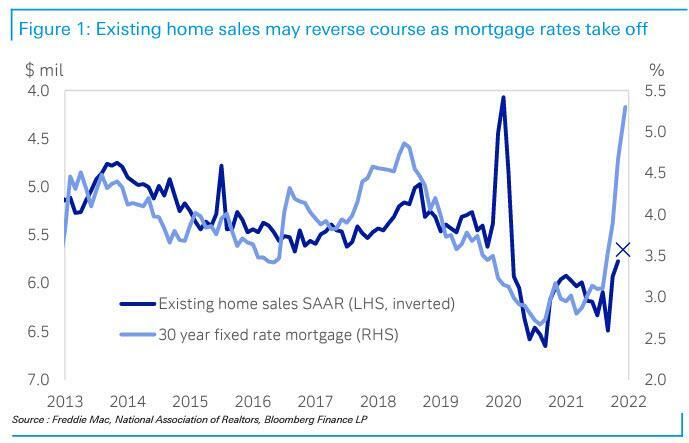

- 10:00: April Existing Home Sales MoM, est. -2.2%, prior -2.7%; Home Resales with Condos, est. 5.64m, prior 5.77m

- 10:00: April Leading Index, est. 0%, prior 0.3%

DB’s Jim Reid concludes the overnight wrap

Today is my last day at work this week before I head up to Cambridge tomorrow for my Masters’ graduation. Before you send in a flood of congratulations though, I didn’t actually do any work for this qualification, with not even a single hour of revision. Now at this point you’re probably thinking I’m either a genius or guilty of some serious academic malpractice. I’m hoping the former. But the truth is that I’m benefiting from a quirky tradition that somehow means Cambridge, Oxford and Dublin will upgrade your Bachelors into a Masters after a few years. With the wedding two months away, it appears as though I’m losing all my bachelor status at once.

Markets seem ready for a holiday too after the last 24 hours, with the selloff resuming at pace after the brief respite on Tuesday. In fact it was nothing short of a rout with the S&P 500 ending the day down -4.04%, marking its worst daily performance since June 2020, and leaving the index at a fresh one-year low. There wasn’t a single catalyst behind the slump, but weak housing data out of the US along with Target’s move to cut its profit outlook helped feed investor concern that the consumer might not be in as strong a position as previously thought. And that’s on top of all the other worries of late that the global economy is heading in a stagflationary direction amidst various supply-chain issues, alongside the prospect that tighter central bank policy is going to further dent growth and risks tipping various economies into recession.

In terms of the specific moves, the S&P 500 gradually tumbled as the day went on, with its -4.04% decline more than reversing its +2.02% bounceback on Tuesday. The decline was an incredibly broad-based one, with just 8 constituents in the index ending the day higher, which is the lowest number since November. That earnings report we mentioned at the top meant that Target (-24.93%) saw the worst performance in the entire S&P 500, after saying they now expected their full-year operating income margin rate to be around 6%. That follows a disappointing report from Walmart the previous day, and meant that consumer staples (-6.38%) and consumer discretionary (-6.60%) were the worst-performing sectors in the S&P yesterday. The latest declines also mean that the S&P is back on track for a 7th consecutive weekly decline, having shed -2.49% since the start of the week, and S&P 500 futures are only up by +0.18% this morning. If the S&P 500 does see a 7th week in negative territory, then that would be the longest run of weekly declines for the index since 2001. Other indices lost ground too given the risk-off move, with the Dow Jones (-3.57%), the NASDAQ (-4.73%), and the small-cap Russell 2000 (-3.56%) all experiencing sizeable declines of their own. European indices had a better performance after closing before the worst of the US declines, and the STOXX 600 was “only” down -1.14% to just remain in positive territory for the week.

With recessionary concerns back in focus, sovereign bonds rallied on both sides of the Atlantic as investors sought out safe havens. Yields on 10yr US Treasuries fell by -10.2bps to 2.88%, with the decline mostly led by a -9.6bps move lower in real yields, and nominal yields are only back up +2.5bps this morning. The yield curve also continued to flatten and the 2s10s slope (-6.9ps) fell to its lowest in over two weeks, at 21.0bps, although it’s been over 6 weeks now since the curve last traded in inversion territory. We did get some Fedspeak but to be honest there weren’t any major headlines relative to what we already knew, with Chicago Fed President Evans saying it was “quite likely” the Fed would be at a neutral setting by year-end, whilst Philadelphia Fed President Harker was making the case for more gradual rate hikes after the next few 50bp hikes are delivered. More important for the outlook was the release of various housing data yesterday, where housing starts fell to an annualised rate of 1.724m in April (vs. 1.756m expected), and that was from a downwardly revised 1.728m in March. That comes against the backdrop of rising mortgage rates, and the MBA reported that mortgage purchase applications fell -11.9% in the week ending May 13, leaving them at their lowest levels since May 2020 when the numbers were still recovering from the pandemic slump.

Over in Europe, sovereign bond curves also became flatter as investors became increasingly aggressive on the near-term ECB rate path. Indeed the amount of ECB rate hikes priced in by the December meeting hit a fresh high of 108bps, or equivalent to at least four rate hikes of 25bps by year-end. That came amidst further ECB speakers over the last 24 hours, including Finnish central bank governor Rehn, who had already endorsed a July hike and said yesterday that the initial hike was “likely to take place in the summer”. Furthermore, he said that it seemed “necessary that in our policy rates we move relatively quickly out of negative territory”. We also heard from Estonian central bank governor Muller, who also endorsed a July hike and said he “wouldn’t be surprised” if the deposit rate were in positive territory by year-end. However, Spanish central bank governor De Cos said that rate hikes should be gradual as he called for APP purchases to end at the start of Q3, with rate hikes to follow shortly afterwards.

Those growing expectations of tighter policy saw shorter-dated yields move higher in Europe once again, with 2yr German yields hitting their highest level since 2011 despite only a marginal +0.1bps move to 0.36%. However, the broader risk-off tone meant it was a different story for their longer-dated counterparts, and yields on 10yr bunds (-1.6bps) and OATs (-2.2bps) both moved lower on the day. Peripheral spreads widened as well, whilst iTraxx Crossover neared its recent highs with a +26.2bps move to 468bps.

In terms of the fight against inflation, there was a potential boost on the trade side yesterday as US Treasury Secretary Yellen confirmed ahead of a meeting of G7 finance ministers and central bank governments that the she favoured removing some tariffs on goods that are not considered strategic. Separately the risk-off move also saw oil prices move lower for a 2nd day running yesterday, with Brent crude down -2.52%, although it’s since taken back a decent chunk of that loss this morning with a +1.51% move higher to $110.76/bbl.