June 1, 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1844.85. UP $1.00

SILVER: $21.66 UP $.19

ACCESS MARKET: GOLD $1846.70

SILVER: $21.83

Bitcoin morning price: $31,578 DOWN 113

Bitcoin: afternoon price: $30,262 down 1429

Platinum price: closing UP $28.55 to $1000.20

Palladium price; closing UP $4.55 at $2006.95

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: COMEX

JPMorgan issued 2380/4723

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,842.700000000 USD

INTENT DATE: 05/31/2022 DELIVERY DATE: 06/02/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 136

104 C MIZUHO 4

118 C MACQUARIE FUT 221 122

118 H MACQUARIE FUT 213

132 C SG AMERICAS 12 6

159 C ED&F MAN CAP 2

167 C MAREX 3

226 C DIRECT ACCESS 1

323 C HSBC 194

323 H HSBC 660

332 H STANDARD CHARTE 88

357 C WEDBUSH 128 1

363 H WELLS FARGO SEC 136

435 H SCOTIA CAPITAL 77

624 H BOFA SECURITIES 242

657 C MORGAN STANLEY 4

657 H MORGAN STANLEY 192

661 C JP MORGAN 4100 2380

685 C RJ OBRIEN 11

686 C STONEX FINANCIA 4 30

690 C ABN AMRO 39

700 C UBS 124

DLV615-T CME CLEARING

BUSINESS DATE: 05/31/2022 DAILY DELIVERY NOTICES RUN DATE: 05/31/2022

PRODUCT GROUP: METALS RUN TIME: 22:12:06

709 H BARCLAYS 78

732 C RBC CAP MARKETS 13

737 C ADVANTAGE 4 1

800 C MAREX SPEC 26 22

880 C CITIGROUP 7 4

905 C ADM 60 101

TOTAL: 4,723 4,723

MONTH TO DATE: 8,808

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 4723 NOTICE(S) FOR 472300 Oz TONNES)

total notices so far: 8805 contracts for 880,500 oz (27.396 tonnes)

SILVER NOTICES:

37 NOTICE(S) FILED 185,000 OZ/

total number of notices filed so far this month 1441 : for 7,205,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $1.00

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD/

INVENTORY RESTS AT 1068.836 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.19 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER IVWENTORY AT THE SLV.: A WITHDRAWAL OF 2.538 MILLION OZ FROMTHE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 556.133 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FELL SIZED 68 CONTRACTS TO 147,301 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD GAIN IN OI WAS ACCOMPLISHED WITH OUR $0.42 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.42) BUT ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A STRONG NET GAIN OF1340 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 27 CONTRACTS OR 135,000 OZ//NEW STANDING: 7,770,000 / // V) TINY SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -118

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 1 day, total 1300, contracts: 6.7 million oz OR 6.7 MILLION OZ PER DAY. (1300CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 6.7 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 6.7 MILLION OZ

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 68 DESPITE OUR $0.42 LOSS IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1300 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 135,000 QUEUE JUMP//NEW STANDING:7,770,000 // .. WE HAD A STRONG SIZED GAIN OF 1340 OI CONTRACTS ON THE TWO EXCHANGES FOR 1340 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 37 NOTICES FILED TODAY FOR 185,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6447 CONTRACTS TO 513,972 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – 108 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED LOSS IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $15.10//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $15.10 WITH RESPECT TO TUESDAY’S TRADING

WE HAD A SMALL SIZED GAIN OF 696 OI CONTRACTS 2.166 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6447 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 513,972

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 446, WITH 6001 CONTRACTS DECREASED AT THE COMEX AND 6447 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF446 CONTRACTS OR 1.387 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6447) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (6001,): TOTAL GAIN IN THE TWO EXCHANGES 446 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S EFP JUMP TO LONDON//NEW STANDING: / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) STRONG SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

6447 CONTRACTS OR 644700 OR 20.05 TONNES 1 TRADING DAY(S) AND THUS AVERAGING: 6447 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES: 20.05 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 20.05/3550 x 100% TONNES 0.56% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 20.05 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF MAY.WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (MAR), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A TINY SIZED 68 CONTRACT OI TO 147,301 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1300 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1300 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 68 CONTRACTS AND ADD TO THE 1300 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1232 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.160 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.42 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries/DIESEL

On Diesel, BlackRock & Food Shortages

Inbox

| Robert Hryniak | 9:35 AM (6 minutes ago) | ||

| to |

Something to ponder ….

“KEVIN MOORE rsSnpy9 u27mf A M8 t0l008:aMal · Diesel Peeps Do you know what DEF fluid is? It’s Diesel Exhaust Fluid. Every Diesel truck that has been made since 2010 is required to use it. It’s a product made of 67% Urea fertilizer and 33% distilled water. Every diesel truck you see driving down the road today has to have this product to drive. The engines won’t start without it. There are regulators inside the engine that mix DEF with the Diesel to reduce Diesel emissions. That’s the purpose of DEF. Right now, Russia is the largest exporter of Urea by a wide margin. Qatar is second. Egypt and China are Tied for 3rd. Both Russia and China have decided to no longer export Urea. On top of that, India is the largest manufacturer of Urea in the world even though they consume most of what they make. What little they would export……….they no longer do. They are now stopping the exportation of any and all Urea minus a deal they just cut with Sri Lanka. What does this mean for you and me? Well, first, the United States imports most of it’s Urea fertilizer. We are the third largest importer in the entire world. We depend on other countries to eat, drive and ship our products.

Secondly… Flying J is the largest Service provider for Truckers around the Unites States. I’m sure you’ve seen their massive gas stations when traveling around the country. Flying J gets 70% of their DEF fluid from shipments via Union Pacific railroad. UP has single user access to the Fertilizer plants that Urea/DEF fluid comes from. No other rail provider has access to these distribution points. This means Flying J can’t just go around Union Pacific. Union Pacific is in charge….for a reason I’m gonna mention in a few paragraphs.

Flying J provides 30% of all DEF consumed in the United States. UP has told Flying J to reduce their shipments by a whopping 50%. And if they do not comply then they will be completely embargoed. That would in effect bankrupt FJ. This means that 15% of all DEF consumed by truckers in the US is no longer available at the largest travel service center for the entire trucking industry.

Rome rotted from the inside out. It was easily invaded because it was occupied with internal problems. It appears we have discovered the Trigger. DEF fluid. If this holds up, DEF shortages will be the catalyst that causes food shortages in the coming months. Not only is there a shortage of fertilizer to grow crops in drought-stricken states (See Kansas’ drop in wheat production for 2022)….but….now it looks like, unless the Federal Government intervenes via the Defense Production Act, …which I am no longer confident they will….there is gonna be an absolute massive shortage of trucking in the coming months.

There simply isn’t going to be DEF fluid sufficient to keep the engines running and moving. Home Depot is now limiting the amount of DEF you can buy in their stores.

I would think long and hard about the decisions you are making right now. Where you live. What you spend money on. How you prepare. This is so real that the CEO of Flying J, Shameek Konar was summoned to a Surface Transportation Board hearing to give them all this info.

From what I’m reading….Blackrock is the majority shareholder of Union Pacific railroad. How is that important? Americas biggest fertilizer producer is CF Industries. Their largest shareholder is Blackrock. Blackrock controls the fertilizer industry in the U.S.. Union Pacific has exclusive rights to distribution points of fertilizer. Urea is fertilizer. Flying J needs Urea/DEF. Blackrock is controlling everything.

The Chairman of the BlackRock Investment Institute is Tom Donilon, President Obama’s former National Security Advisor. Tom Donilon’s brother, Mike Donilon is a Senior Advisor to Joe Biden. Tom Donilon’s wife, Catherine Russell, is the White House Personnel Director. Tom Donilon’s daughter, Sarah Donilon, who graduated college in 2019, now works on the White House National Security Council.

It appears Blackrock is spearheading the dismantling of the US system on behalf of the Globalists. And the first domino they are pushing over is the energy sector. They are using DEF to get the party started. This is one sector of the biggest downfalls in political repercussions this country has ever faced…”

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 4.27 PTS OR 0,13% //Hang Sang CLOSED UP 178,09 PTS OR 0.65% /The Nikkei closed UP 178,09 OR 0.65% //Australia’s all ordinaires CLOSED UP .10%% /Chinese yuan (ONSHORE) closed DOWN 6,6871 /Oil UP TO 116.15dollars per barrel for WTI and UP TO 117050 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6871 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6961: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6001 CONTRACTS TO 513,722 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX DECREASE OCCURRED DESPITE OUR LOSS OF $15.10 IN GOLD PRICING TUESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6447 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6447 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :6447 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6447 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 446 CONTRACTS IN THAT 6001 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 6447 CONTRACTS..AND YET THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF GOLD $15.10.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (68.157),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 68.157 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $15.10) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A SMALL SIZED GAIN OF 446 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (68.157 TONNES)…

WE HAD XXX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 446 CONTRACTS OR 44600 OZ OR 1.387 TONNES

Estimated gold volume 154,015/// poor

Confirmed volume yesterday:215,,494 contracts fair

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 1

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 64,334.150 oz Brinks 2001 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 4723 notice(s) 472,300 OZ 14.690 TONNES |

| No of oz to be served (notices) | 13104 contracts 1,310,400 oz 40.75 tonnes |

| Total monthly oz gold served (contracts) so far this month | 8808 notices 880,800 OZ 27,396 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

1 customer withdrawals:

i) Out of Brinks: 64,334.150 oz 2001 kilobars

total withdrawal: 64,334.150 oz

ADJUSTMENTS: 2

i) dealer to customer: Brinks 2212.380 oz

ii) dealer to customer: Malca 4179.258 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 17,827 contracts having LOST 4441 contracts

We had 4085 notices filed on Friday so we lost 336 contracts or 33,600 oz will not stand as they were EFP’d to London

July has a GAIN OF 262 OI to stand at 2096

August has a loss of 476 contracts down to 432,520 contracts

We had 4723 notice(s) filed today for 4723 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 4100 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4723 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2380 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (8808) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 17,8277 CONTRACTS ) minus the number of notices served upon today 4723 x 100 oz per contract equals 2,191200 OZ OR 68.157 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (8808) x 100 oz+ (17,827) OI for the front month minus the number of notices served upon today (4723} x 100 oz} which equals 2,191200 oz standing OR 68.157 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 68.157 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,144,416.951 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,065,182.309 OZ

TOTAL ELIGIBLE GOLD: 17,044,887.111 OZ

TOTAL OF ALL REGISTERED GOLD: 18,020,295.195 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,991.648.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 1

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 618,738.160 oz JPM CNT |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,672,006.282 oz Brinks CNT JPMorgan |

| No of oz served today (contracts) | 37CONTRACT(S) 185,000 OZ) |

| No of oz to be served (notices) | 113 contracts (565,000 oz) |

| Total monthly oz silver served (contracts) | 1441 contracts 7,205,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

i) Into Brinks: 42,011.75 oz

ii) Into CNT: 605,743.254 oz

iii)_ Into JPMorgan: 582,754.800

total deposit: 1,672m006.282 oz

JPMorgan has a total silver weight: 173.454 million oz/338,231 million =51.27% of comex

Comex withdrawals: 2

i) Out of CNT: 42,712.210 oz

ii) Out of JPMorgan: 576,025.890 oz

total withdrawal 618,738.110 oz

2 adjustments: dealer to customer:

a)Manfra 60,615.480 oz

b) Brinks 14,484.08 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72,438 MILLION OZ

TOTAL REG + ELIG. 338.231 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 150 HAVING LOST 1377 CONTRACTS.

WE HAD 1404 NOTICES FILED ON FRIDAY SO WE GAINED 27 CONTRACTS OR AN ADDITIONAL 135,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 357 CONTRACTS DOWN TO 108,307 CONTRACTS.

AUGUST GAINED 8 CONTRACTS TO STAND AT 8

SEPTEMBER HAD A GAIN OF 854 CONTRACTS UP TO 24,563 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 37 for 185,000 oz

Comex volumes:53,910// est. volume today// poor

Comex volume: confirmed yesterday: 74,841 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1404 x 5,000 oz = 7,020,000 oz

to which we add the difference between the open interest for the front month of JUNE(150) and the number of notices served upon today 37 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 150 (notices served so far) x 5000 oz + OI for front month of JUNE (150) – number of notices served upon today (37) x 5000 oz of silver standing for the JUNE contract month equates 7,770,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1068.36 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FORM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 556.133 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/

LAWRIE WILLIAMS: Another volatile month for gold, equities and bitcoin

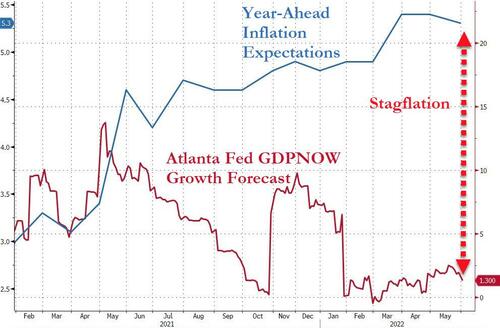

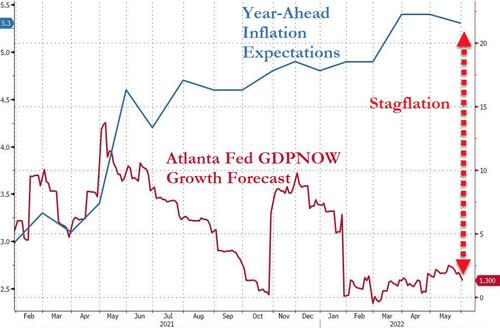

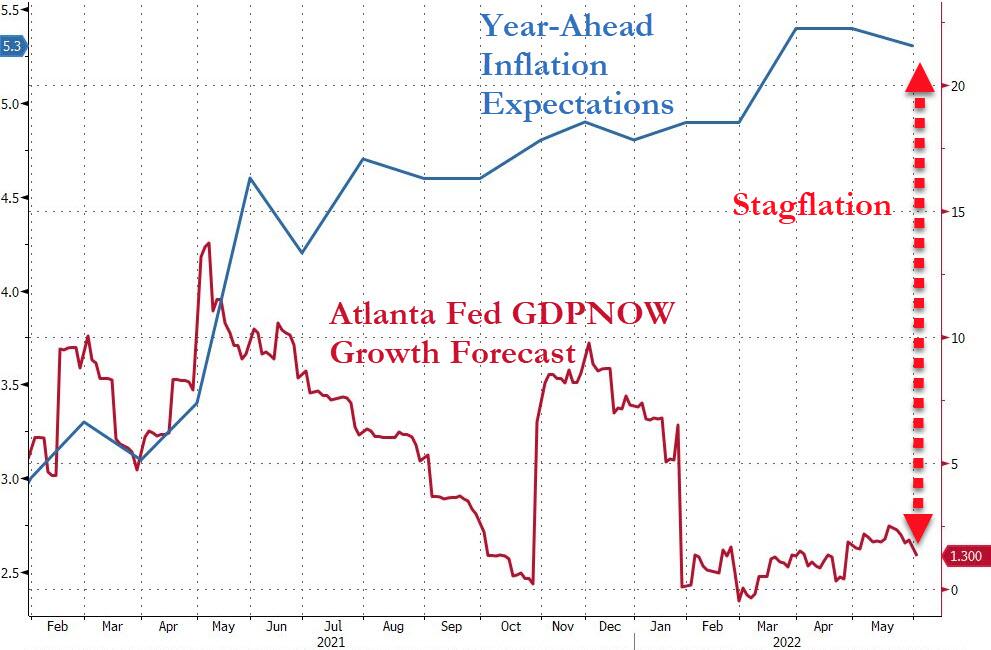

Like April, May has brought little cheer to the equity markets with inflationary pressures, and the Fed’s measures being taken to try and control them, seeming to be inevitably driving the U.S. economy into a period of stagflation, possibly even to be followed by recession. Even the dreaded prospect of a depression to match that of 1929-30 is on some economists’ lips. Equity prices are down quite heavily year to date, but are continually being buoyed up by, in our view, unjustified bullish comments from Wall Street analysts keen to maintain business. Such is what passes for market analysis!

Stagflation, though, is also a word on many lips. It is defined as a period of stagnant growth coupled with high inflation, usually triggered by a sharp rise in energy prices – much as we are seeing today. The fall in unemployment as the U.S. economy began to recover from the Covid-19 pandemic tended to counter this trend, but there is some evidence that this is beginning to turn around again as inflation eats into disposable incomes and consumer spending begins to turn down cutting demand for goods and services. Whether this turns into a full-blown recession is rather less certain, however.

The various movements in prices and indexes over the year to date and the past month are set out in the table below. As can be seen most have trended downwards sharply since the beginning of the year with some notable exceptions, although we don’t expect these to be sustained. Overall movement in the market indexes in particular over the past month seem to have been somewhat muted, or even positive, despite some very sharp interim falls, but again we don’t expect the occasional index recoveries to be sustained unless, of course, the Fed does reverse its tightening and interest raising programmes which some analysts see as likely before the year-end.

The various inflation indexes suggest that inflation levels may have eased, marginally, but not sufficiently to suggest an actual prolonged downtrend. The latest such to be announced, the Personal Consumption Expenditure Index (PCE), the Fed’s preferred measure – the cynics might say because it presents the lowest inflation figures – came in at 6.3% year-on-year for April, the same level as February and down from 6.6% in March, but although equities moved higher, gold also moved up a little and it was felt that it would have no impact at all on the Fed’s likely move to raise interest rates at the next Federal Open Market Committee meeting (FOMC) in a couple of weeks’ time.

Past evidence suggests that recession does not usually follow a period of stagflation. But a programme of 50 basis point interest rate increases at successive FOMC meetings, as the Fed seems to be planning, may be sufficient to trigger sharp falls in equity prices across the board and be instrumental in tipping the whole U.S. economy into a recessionary downwards spiral.

Equity downturns can be sharp and severe as we saw in the middle of the past month when the Dow lost over 2,000 points over a 3-day period. Even though we have seen partial recoveries in equities since, similar sharp downturns can’t be ruled out in the weeks and months ahead. A fall in the Dow to below 30,000., the S&P 500 to under 3,750 and the NASDAQ to less than 10,500 over the next month or two cannot therefore be ruled out.

Precious metals seem to have made something of a recovery, but not yet a significant one. Gold moved back above $1,850 at the beginning of the past week, but in a take-down on Tuesday due to some better consumer confidence figures, it was even unable to hold on to this level, while silver continued to disappoint its followers and the pgms continued volatile. We suspect consumer confidence will dissipate as inflation is seen to be continuing and gold, in particular, should recover any lost ground.

Precious metals stocks have tended to outperform their respective metal prices, but only marginally so. Certainly the major precious metals miners should be making strong profits at current metal price levels.

The wild card here seems to be dollar strength. A strong dollar tends to lead to a weaker gold price in U.S. dollar terms, and the dollar has tended to move upwards against competitive currencies in recent weeks despite the apparent weakness in the U.S. economy. This may not necessarily continue and there were some signs of a developing dollar downturn towards the end of the past month.

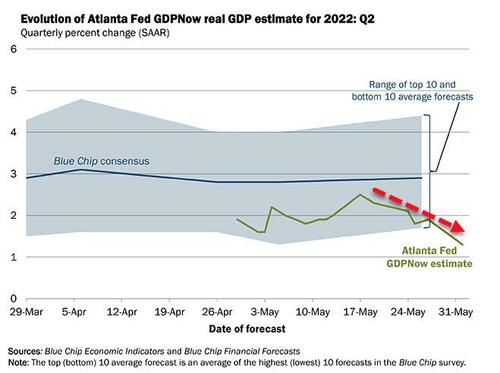

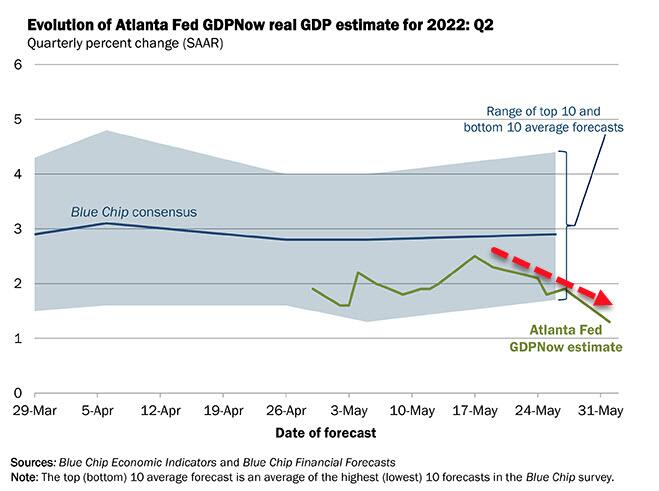

Data released during the month suggested that U.S. Q1 GDP turned negative and the latest projection by the Atlanta Fed is that the Q2 GDP growth estimate has shrunk to a mere 1.8%. Given how unexpected the Q1 fall was it might be no surprise if the Q2 figure ends up flat, or even negative too, and if the latter would tip the U.S. economy into a technical recession. We don’t necessarily expect that this will happen, but investors should perhaps be prepared for the possibility and any negative market fallout resulting.

There is some speculation also that China and Russia, as the world’s top two gold producers by some estimates, may be attempting to introduce a gold-backed global reserve currency to rival the dollar’s current dominant reserve status. Should this speculation be accurate, and a new such reserve currency find acceptance, then the dollar could well enter a period of value decline globally, which would certainly benefit the gold price, at least in dollar terms.

Inflationary trends seem likely to continue to influence equity and precious metals markets despite proposed Fed actions on tightening and interest rate rises. Markets are thus likely to remain volatile as they have been over the past couple of months and will be moved up and down by data releases seen as positive or negative. Equities and bitcoin may well thus continue depressed overall, while gold, in particular, may catch an upwards bid as markets consider the underlying trends. However, uncertainty will likely continue to reign until we see a definitive move by one or other of the key market components.

01 Jun 2022

END

3. Chris Powell of GATA provides to us very important physical commentaries

END

END

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //PALM OIL+ OTHERS

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6871

OFFSHORE YUAN: 6.6961

HANG SANG CLOSED DOWN 120.26 PTS OR 0.56%

2. Nikkei closed UP 178.09% OR .65%

3. Europe stocks ALL CLOSED ALL MIXED

USA dollar INDEX UP TO 102.02/Euro FALLS TO 1.0714

3b Japan 10 YR bond yield: RISES TO. +.233/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 128.11/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield RISES TO 3.58

3j Gold at $1831.85 silver at: 21.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0.50 roubles/dollar; ROUBLE AT 61.40

3m oil into the 116 dollar handle for WTI and 117 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.58DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9620– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0306well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 2.875 UP 3 BASIS PTS

USA 30 YR BOND YIELD: 3.074 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.40

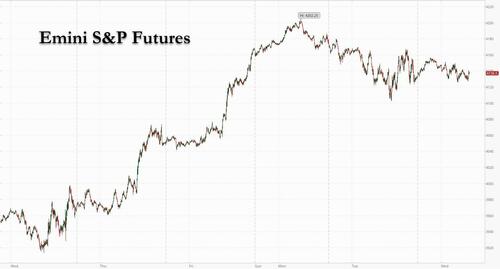

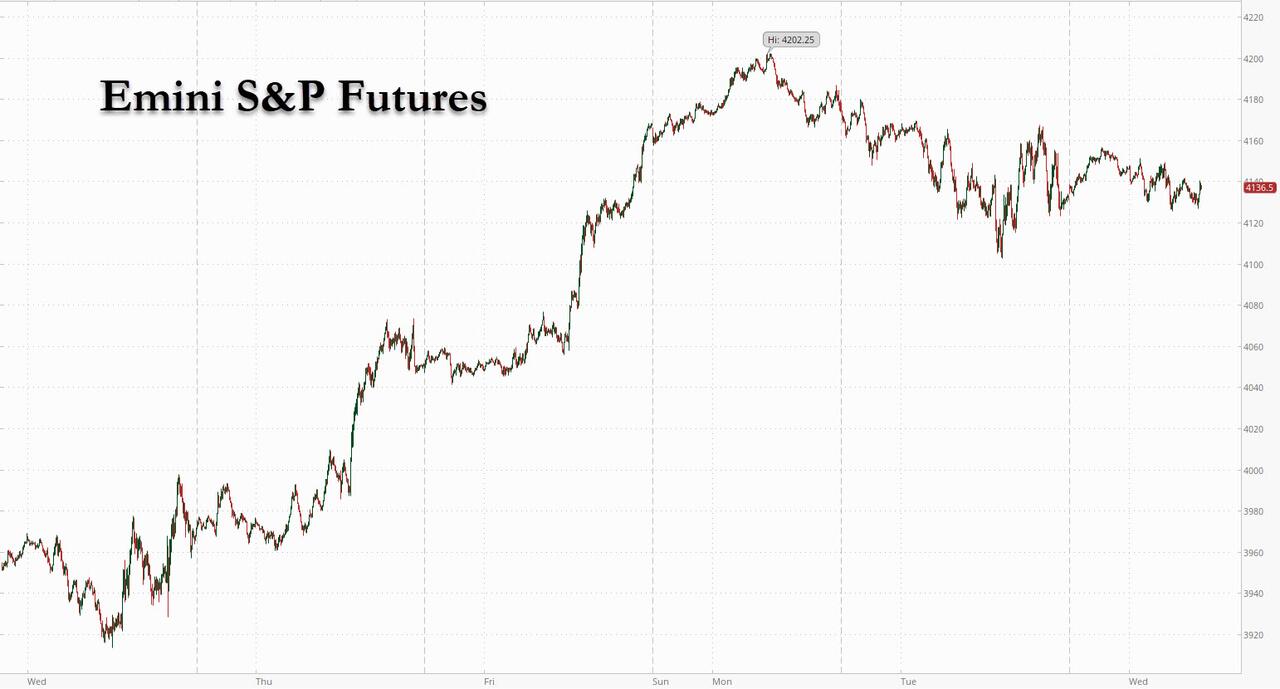

Futures Start New Month Flat As Fed’s QT2 Begins

WEDNESDAY, JUN 01, 2022 – 07:50 AM

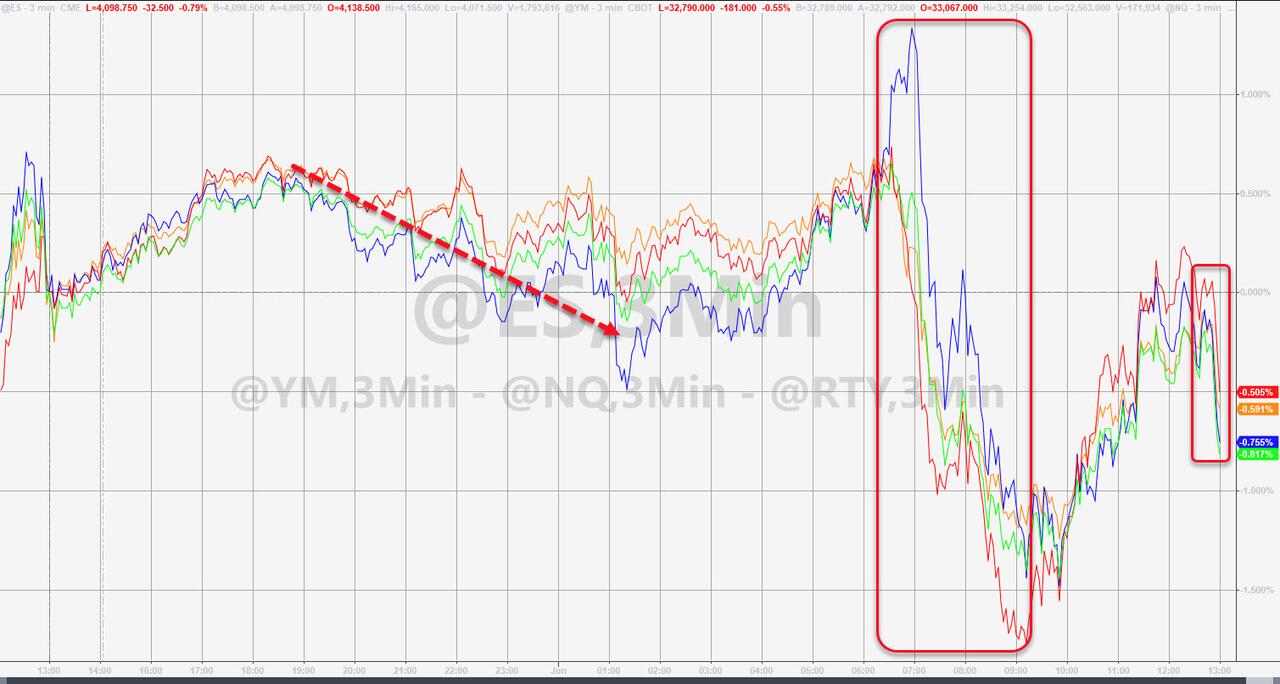

Stocks traded off session highs as weaker-than-average volumes mark the beginning of summer, and as traders awaited the jobs report later this week and eyed the official start of the Fed’s second Quantitative Tightening program (which will end as “gloriously” as the first one) which will drain the Fed’s balance sheet by $95BN per month.

Contracts on the S&P 500 were 0.2% higher by 730 a.m. in New York, after the underlying index finished May up exactly 0.1%; Nasdaq 100 futures were up 0.1%. European bourses and Asian stocks were modestly in the red to stgart the new quarter. The latest drop in Treasuries pushed 10-year yields closer to 2.9% as traders raised bets on Federal Reserve interest-rate hikes. The dollar advanced against major peers, and bitcoin traded around $31,500. Oil rose as investors assessed the future of OPEC+ unity, just as ministers from the group prepare to meet on Thursday to discuss its supply policy for July. Crude advanced about 10% in May, stoking more inflation worries.

Concerns that the Fed’s rate hikes may induce a recession are keeping investors guessing about the outlook for the economy as rising food and energy costs squeeze consumers, and volatility has picked up.

“US markets, and by default, global markets, will still indulge in schizophrenic swings in market sentiment as the FOMO dip-buyers become increasingly frantic in their attempts to pick a cyclical low in equity markets,” said Jeffrey Halley, a senior market analyst at Oanda Asia Pacific Pte.

On Tuesday, Joe Biden used a rare meeting with Federal Reserve Chair Jerome Powell to declare that he’s respecting the central bank’s independence and to throw Powell under the bus for any continued high inflation. The meeting came ahead of US payroll numbersFriday.

“There are heightened concerns around inflation and where central banks are likely to go trying to combat inflation,” Kristina Hooper, Invesco Advisers chief global markets strategist, said on Bloomberg Radio. “This has gone from just an inflation scare to a growth scare. Uncertainty has grown.”

In premarket trading, Salesforce shares jumped 8.3% after the software company raised its full-year forecast for adjusted earnings. HP will be in focus after the company reported better-than-expected sales and profit driven by steady demand for computer systems. Other notable premarket movers:

- Digital Turbine (APPS US) fell 4.1% in New York premarket trading on Wednesday after the mobile services platform’s fourth-quarter results and first-quarter forecast. Roth Capital Partners analyst Darren Aftahi says the company provided soft guidance, but noted that its commentary around SingleTap licensing should be supportive.

- View (VIEW US) shares surge as much as 30% in US premarket trading, after the glass manufacturing firm reported its full-year results late Tuesday, with the company saying it expects to file its delinquent 10-K and 10-Q on or before June 30.

- ChargePoint (CHPT US) analysts noted that the EV charging network firm’s margins came under pressure due to rising costs and supply-chain disruption, leading some brokers to trim their targets on the stock. ChargePoint shares dropped 2.7% in US postmarket trading on Tuesday after posting a 1Q lossthat was wider than expected.

- Victoria’s Secret (VSCO US) analysts were positive on the lingerie company’s results, with Wells Fargo saying that its turnaround is on track despite a tough macroeconomic environment, while VitalKnowledge said that the update was a “big victory” amid the retail gloom. The shares gained 7.3% post-market Tuesday.

- HP (HPQ US) shares edged up in extended trading on Tuesday, after the company reported better-than- expected sales and profit driven by steady demand for computer systems. Analysts lauded the company’s execution as it navigates a challenging supply and macroeconomic environment.

- Ambarella (AMBA US) shares fell 5.6% in extended trading on Tuesday after the semiconductor device company issued a tepid second-quarter revenue forecast as lockdowns in China weigh on its near-term outlook. Analysts said that there is weakness in the near-term, but the long-term thesis remains intact.

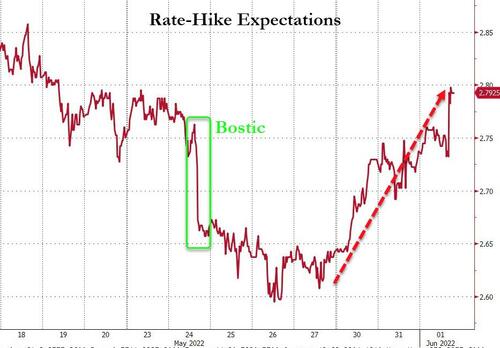

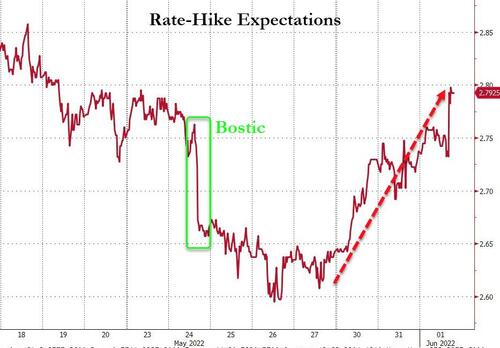

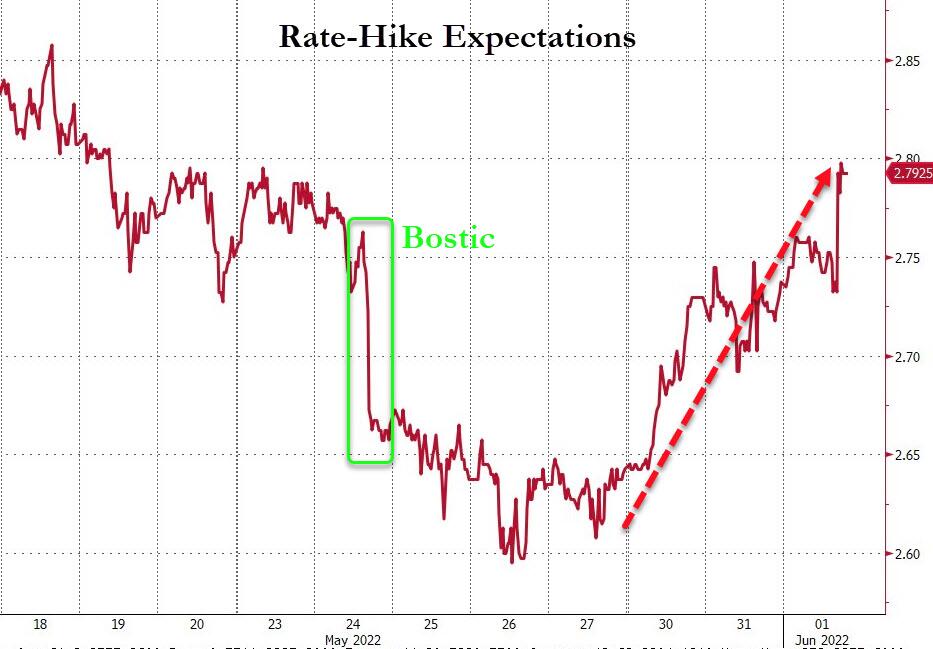

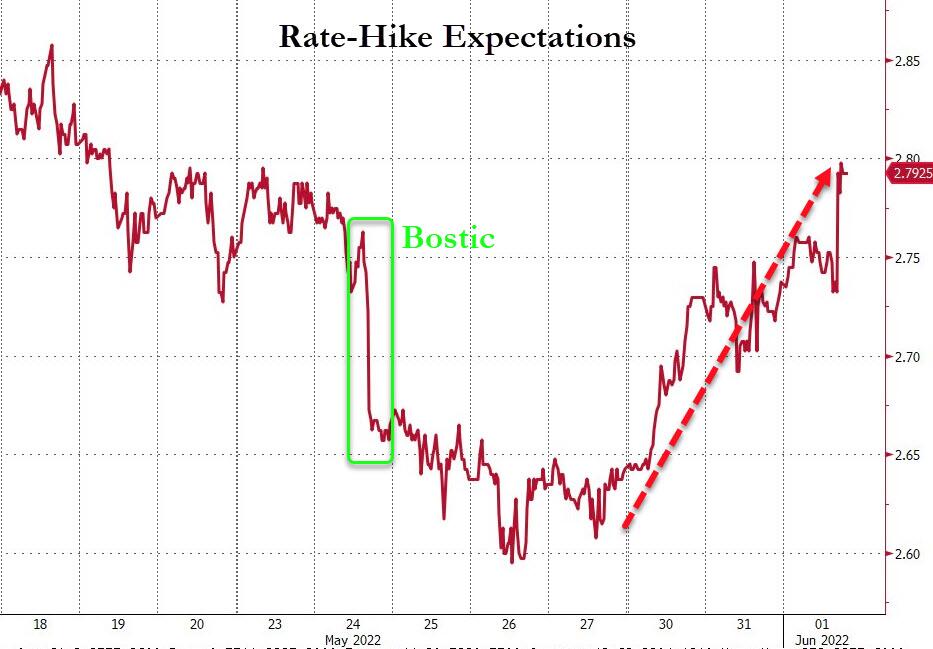

Late on Tuersday, Fed’s Bostic said there could be a significant reduction in inflation this year and that his suggestion for a pause in September should not be interpreted as a “Fed put” or belief that the Fed would rescue markets, according to an interview in MarketWatch. Elsewhere, Treasury Secretary Yellen said US President Biden’s top concern is inflation and shares the Fed’s priority of slowing inflation, while she added she was wrong about the path inflation would take and doesn’t expect the same pace of job gains going forward, according to Reuters.

Citigroup Inc. strategists said that after a difficult first five months of 2022, the pain may not be over yet for global equity markets. The prospect of downward revisions to earnings estimates is the latest headwind to face stock investors, already rattled by runaway inflation and the potential impact of central-bank tightening aimed at controlling it, the strategists led by Jamie Fahy wrote in a note.

In Europe, the Stoxx 600 Index erased earlier gains to trade 0.2% lower a day after euro-zone figures showed a record jump in consumer prices and on investor concerns that record inflation will pressure the European Central Bank to act more aggressively, increasing the risk of an economic slump. The DAX outperformed, adding 0.3%. Miners, utilities and real estate are the worst-performing sectors. Autos are the day’s best performing sector and one of few rising subgroups amid declining markets; the Stoxx 600 Automobiles & Parts Index rises 2.1% as of 1:10pm CET, rebounding after a session of declines on Tuesday and on course for a fifth day of gains in six. Carmakers such as Stellantis, Renault and Volkswagen lead the advances. Stellantis +3.4%, VW +3.4%, Renault +3.4%, Porsche Automobil Holding SE +3.2%, BMW +2.8%, Volvo Car +2.5%, Mercedes-Benz Group +2.5%. Here are the biggest European movers:

- Dr. Martens shares surge as much as 30%, the most since January 2021, after the UK bootmaker reported pretax profit for the full year that beat the average analyst estimate.

- Lanxess shares rise as much as 2.5%, adding to an 11% gain on Tuesday. The chemicals group is raised to buy from hold at Stifel. Berenberg also hikes its PT on the stock.

- Societe Generale shares up as much as 2.6% after UBS upgrades the investment bank to buy from neutral, noting the company’s valuation is “too cheap to ignore.”

- Capricorn Energy shares rise after company reached an agreement on the terms of a recommended all-share combination with Africa-focused oil and gas developer Tullow Oil.

- Stadler Rail shares jump as much as 4.3%, most since March, after it signed a contract to deliver up to 510 FLIRT trains to the Swiss Federal Railways, according to a statement.

- OVS gains as much as 7.1% to highest since end of March after Banca Akros upgrades its rating to buy, saying in note that May appears to have been a strong month for the Italian fashion retailer.

- Saint-Gobain shares fluctuate after the building material company agreed to buy Canadian siding producer Kaycan for $928m to strengthen its position in the North American building-products market.

- Zalando shares fall as much as 5.1% after being downgraded to equal- weight from overweight at Barclays, which cites near-term challenges for the online fashion retailer.

Earlier in the session, Asian stocks edged lower after fluctuating in a narrow range, as traders assessed China’s easing virus restrictions and the persistent risk of global inflation. The MSCI Asia Pacific Index was down less than 0.1%, with declines in technology and utilities shares offsetting gains in consumer discretionary stocks. Japan’s Topix Index rose more than 1% as the yen weakened, while indexes in Malaysia and the Philippines fell the most. China’s shares were slightly lower after a private gauge showed factory activity in May contracted from the previous month as both production and new orders fell. Meanwhile, Shanghai’s Covid-19 cases continued to decline as most parts of the city reopened after two months under one of the world’s most restrictive pandemic lockdowns.

Asian equities completed their first monthly advance this year in May amid optimism China’s easing lockdowns will improve the region’s growth outlook, even as soaring oil prices and global inflation fuel concerns of tighter monetary policies. Near-term concerns over inflation, economic growth and China’s Zero Covid policy are likely to persist, but investors can expect a “stabilization in 3Q as valuations reset and positive catalysts emerge,” Chetan Seth, Asia Pacific equity strategist at Nomura, wrote in a note. Markets in South Korea and Indonesia were closed for holidays.

In FX, the Bloomberg Dollar Spot Index rose 0.1% as the greenback strengthened against all its Group-of-10 peers apart from the Australian dollar. The yen was the worst performer and fell to a two-week low. The euro neared the $1.07 handle before paring losses. Bunds were little changed with focus on ECB rate hike pricing and possible comments by policy makers including President Christine Lagarde before the ‘quiet’ period kicks ahead of next Thursday’s policy decision. The Aussie inched up and Australian bonds fell as data showed the economy grew faster than expected in the fourth quarter. Rising Treasury yields also weighed on Aussie debt.

In rates, Treasury yields inched up with the curve slightly bear-flattenning, before the Federal Reserve starts its quantitative-tightening program today. The Fed will start shrinking its balance sheet at a pace of $47.5 billion a month before stepping that up to $95 billion in September. Treasuries were slightly cheaper across the curve, with yields off session highs in early US session. Yields are up 2bp-3bp across the curve, led higher by 5-year sector; the 10-year yield is at 2.87% underperforms bunds and gilts. Economists expect a second straight half-point rate increase from the Bank of Canada at 10am ET; swaps market prices in 52bp and 184bp by year-end. IG dollar issuance slate empty so far; six entities priced a total of $12.6b Tuesday, and two stood down. Bunds and Italian bonds are little changed, with the 10-year yields on both trading off session high after ECB’s Holzmann said new inflation record backs need for a 50bps hike. Money markets are pricing a cumulative 119bps of tightening in December.

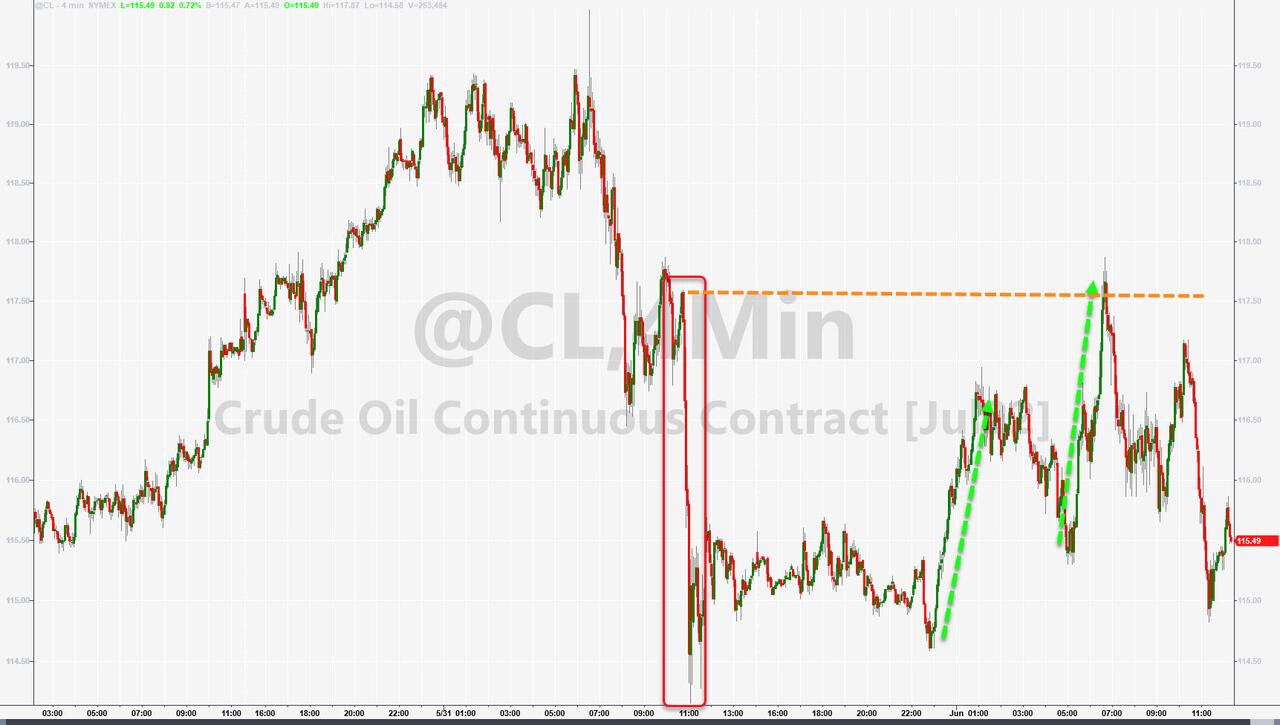

In commodities, WTI trades within Tuesday’s range, adding 1.6% to above $116. Most base metals are in the red; LME nickel falls 2.4%, underperforming peers. Spot gold falls roughly $8 to trade around $1,829/oz.

Looking the day ahead now, data releases include the global manufacturing PMIs for May and the US ISM manufacturing reading for May. Otherwise, there’s German retail sales for April, the Euro Area unemployment rate for April, US construction spending for April, the JOLTS job openings for April and, May ISM manufacturing and the latest Fed Beige Book. From central banks, the Bank of Canada will be making its latest policy decision and the Fed will be releasing their Beige Book. Otherwise, speakers include ECB President Lagarde and the ECB’s Knot, Villeroy, Panetta and Lane, the Fed’s Williams and Bullard, and PBoC Governor Yi Gang.

Market Snapshot

- S&P 500 futures little changed at 4,133.50

- STOXX Europe 600 down 0.3% to 442.18

- MXAP down 0.1% to 169.26

- MXAPJ down 0.5% to 556.42

- Nikkei up 0.7% to 27,457.89

- Topix up 1.4% to 1,938.64

- Hang Seng Index down 0.6% to 21,294.94

- Shanghai Composite down 0.1% to 3,182.16

- Sensex down 0.4% to 55,336.61

- Australia S&P/ASX 200 up 0.3% to 7,233.98

- Kospi up 0.6% to 2,685.90

- German 10Y yield little changed at 1.14%

- Euro little changed at $1.0727

- Brent Futures up 1.4% to $117.23/bbl

- Gold spot down 0.2% to $1,834.26

- U.S. Dollar Index up 0.16% to 101.92

Top Overnight News from Bloomberg

- The latest all-time high for euro-zone inflation strengthens the case for the European Central Bank to lift interest rates by a half-point in July, according to Governing Council member Robert Holzmann

- Croatia is about to find out whether it’s in good enough shape to become the euro zone’s 20th member. Progress made by country will be assessed in reports due Wednesday from the ECB and the European Union’s executive arm

- Sweden’s main stock exchange venue, Nasdaq Stockholm, is looking into a new service that will provide clearing for inflation-linked swaps in Swedish kronor

- China’s financial capital reported its fewest Covid-19 cases in almost three months as residents celebrated a significant easing of curbs on movement, while some companies took a more cautious approach, maintaining some restrictions in factories

- China’s factory activity in May contracted from the previous month as both production and new orders fell, although the slowdown wasn’t as fast as in April, a private gauge showed Wednesday

- Treasury Secretary Janet Yellen gave her most direct admission yet that she made an incorrect call last year in predicting that elevated inflation wouldn’t pose a continuing problem

- President Joe Biden said he’ll give Ukraine advanced rocket systems and other US weaponry to better hit targets in its war with Russia, ramping up military support as the conflict drags into its fourth month

- New Zealand’s central bank is seeking feedback on whether its monetary policy remit is “still fit for purpose,” Deputy Governor Christian Hawkesby said. “It’s not about should it still be about price stability and maximum sustainable employment,” he said. “It’s more about have we got the right inflation targets, are we measuring it the right way, what horizon are we trying to achieve it over, what other things should we have regard to.”

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mixed as risk sentiment only mildly improved from the lacklustre performance stateside as the region digested another slew of data releases including the continued contraction in Chinese Caixin Manufacturing PMI. ASX 200 was kept afloat by strength in industrials, telecoms and the top-weighted financials sector, while better-than-expected Q1 GDP data provides some mild encouragement. Nikkei 225 was underpinned by further currency depreciation and with BoJ Deputy Governor Wakatabe reiterating the BoJ’s dovish tone. Hang Seng and Shanghai Comp were indecisive after Chinese Caixin Manufacturing PMI remained in contraction territory and amid mixed COVID-related developments with Shanghai reopening from the lockdown whilst Beijing’s Fengtai district tightened curbs and required all residents to work remotely.

Top Asian News

- Beijing reports two COVID cases during 15hrs to 3pm local time on June 1st

- Hong Kong Retail Sales Unexpectedly Rebound as Covid Curbs Ease

- Sri Lanka’s President Won’t Be Stepping Down Soon, Minister Says

- Europe, Asian Factories Under Pressure on China, War in Ukraine

- Philippine IPO’s Stellar Gain May Wane With Inflation: ECM Watch

European bourses are mixed, Euro Stoxx 50 +0.1%, and have struggled to find a clear direction after mixed APAC trade with a busy docket ahead. Stateside, futures are posting similar performance and looking to a busy data and Central Bank afternoon session, ES +0.2%.

Top European News

- UK government is drawing up plans that will task the BoE with stepping in and handling the implosion of a stablecoin in preparation for future crises in the crypto markets, according to The Times.

- EU Commission President von der Leyen will, on Wednesday, approve Poland’s national recovery plan; however, Politico reports that commissioners, including Timmermans and Vestager, will raise objections to this as Poland has not taken the necessary steps for Commission approval.

- UK House Prices Defy Slowdown Fears With 10th Consecutive Gain

- ECB Half-Point Hike Seen as Deutsche Bank Breaks With Consensus

- Wood to Sell Built-Environment Unit to WSP for $1.9 Billion

- BT’s Sport TV Deal With Warner Bros. Discovery Gets UK Probe

FX

- Yen extends losses through more technical support levels, 129.0O and 129.50 as BoJ reiterates dovish stance and maintains that it is undesirable for monetary policy to target FX rates.

- Dollar drifts otherwise after month end squeeze as attention turns to busy midweek agenda and run in to NFP on Friday, DXY retracts into tighter 102.060-101.760 range.

- Aussie outperforms on the back of firmer than forecast Q1 GDP data, but hampered by decent option expiry interest sub-0.7200 vs Greenback.

- Euro unable to glean much impetus from hawkish ECB Holzmann as option expiries sit between 1.0740-75.

- Loonie pivots 1.2650 pre-BoC awaiting confirmation of the 50bp hike expected or something more hawkish.

- Marked slowdown in Hungarian manufacturing PMI piles more pressure on Forint following half point NBH rate rise vs 60bp consensus, EUR/HUF inching closer to 400.00, at circa 398.50.

Commodities

- WTI and Brent are recovering from yesterday’s WSJ source report induced downside, with participants awaiting clarity/details at Thursday’s OPEC+ gathering.

- Currently, the benchmarks are holding around/above USD 117/bbl, vs respective lows of USD 114.58/bbl and USD 115.40/bbl respectively.

- Russian Foreign Minister Lavrov met with his Saudi counterpart on Tuesday in which they both praised the level of cooperation in OPEC+, while they noted stabilising effect that tight Russia-Saudi coordination has on the global hydrocarbon market, according to Reuters.

- UAE is considering a plan to increase its oil capacity by an additional 1mln bpd to a total 6mln bpd by 2030, according to Energy Intel.

- JMMC on Thursday now scheduled for 13:00BST (prev. 12:00BST), OPEC+ at 13:30BST, via Argus’ Itayim.

- Police clashed with communities blocking MMG’s Las Bambas copper mine in Peru.

- China’s State Planner says renewable energy consumption is to reach circa. 1bln/T of standard-coal-equivalent by 2025, equal to 20% of total consumption; aims to secure around 33% of electricity from renewable sources by 2025.

- Spot gold is modestly softer amid ongoing USD upside and continuing to draft from a cluster of DMAs above USD 1840/oz, with base metals broadly lower as well.

Central Banks

- ECB’s Holzmann says the record Eurozone inflation print backs the need for a 50bps hike, decisive action is required in order to avoid harsher steps later. A clear rate signal could support EUR.

- BoJ Deputy Governor Wakatabe said the BoJ must maintain powerful monetary easing and sustain an environment where wages can rise, while he added that the BoJ shouldn’t rule out additional easing steps if risks to the economy materialise. Wakatabe also noted that most goods prices aren’t increasing with recent inflation driven mostly by energy and some food price increases, as well as noted that consumer inflation has not yet achieved the BoJ’s price goal in a sustained and stable manner, according to Reuters. Adds, it is undesirable to target FX in guiding monetary policy; desirable for FX to reflect fundamentals.

US Event Calendar

- 07:00: May MBA Mortgage Applications, prior -1.2%

- 09:45: May S&P Global US Manufacturing PM, est. 57.5, prior 57.5

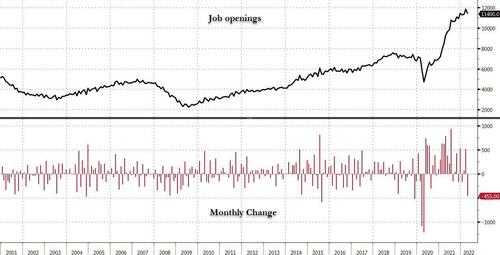

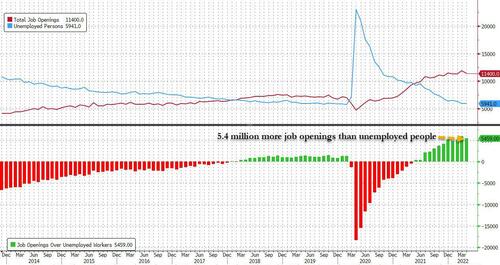

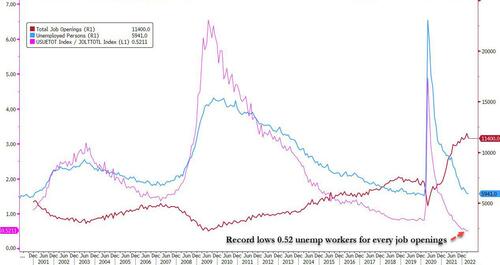

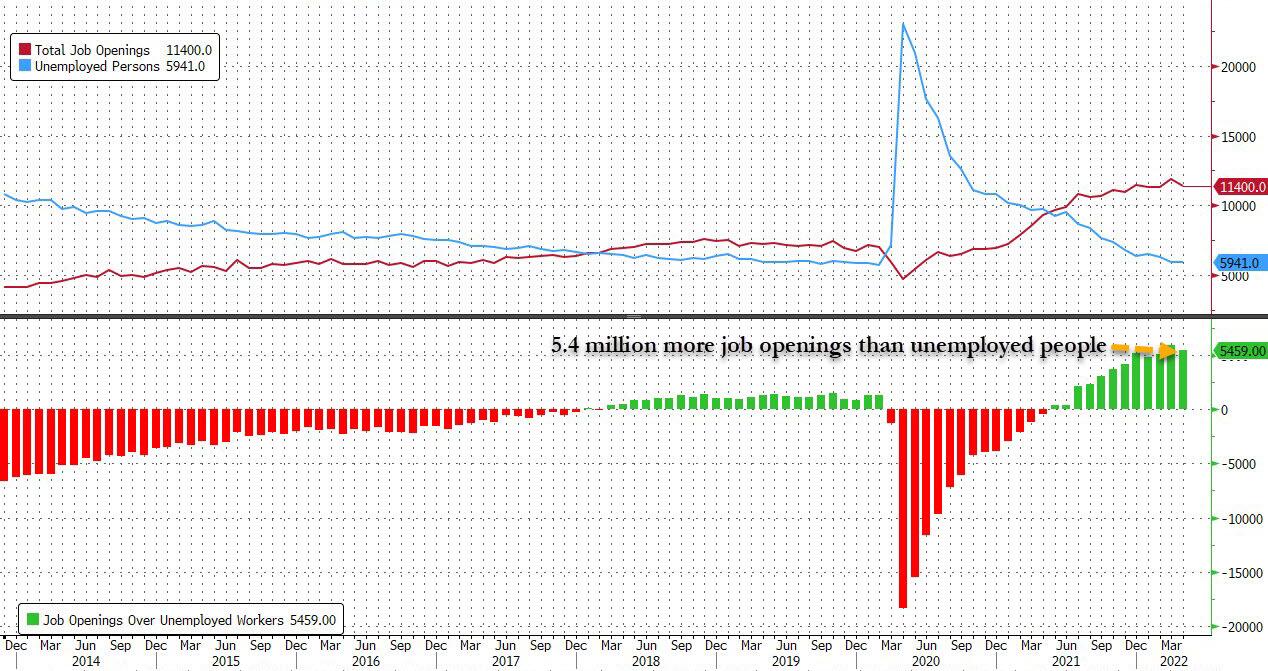

- 10:00: April JOLTs Job Openings, est. 11.3m, prior 11.5m

- 10:00: April Construction Spending MoM, est. 0.5%, prior 0.1%

- 10:00: May ISM Manufacturing, est. 54.5, prior 55.4

- 14:00: U.S. Federal Reserve Releases Beige Book

Central Banks

- 11:30: Fed’s Williams Makes Opening Remarks

- 13:00: Fed’s Bullard Discusses the Economic and Policy Outlook

- 14:00: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

We’ll be off here in the UK tomorrow and Friday as we’ll be celebrating the Queen being on the throne for an astonishing 70 years. I find the best way to celebrate is via the medium of golf! To put things in perspective, when I get to 100 years old I’ll be celebrating exactly 70 years at DB. In our absence Tim will still be publishing the EMR for the next couple of days.

Believe it or not it’s now June! It only seems like yesterday it was Xmas. Perhaps 70 years isn’t so long after all. Since it’s the start of the month, our usual performance review for the month just gone will be out shortly. A number of financial assets began to stabilise in May, helped by a combination of factors such as easing Covid restrictions in China and the potential that the Fed wouldn’t hike as aggressively as some had feared. That said, it’s still been an awful performance on a YTD basis, with the S&P 500 having seen its biggest YTD loss after 5 months since 1970, whilst most of the assets in our main sample are still beneath their levels at the start of the year.

But after some respite over the last couple of weeks, the last 24 hours have seen equities and bonds sell off in tandem once again as inflation fears cranked up another notch. The main catalyst was the much stronger-than-expected flash CPI reading for the Euro Area, which at +8.1% was the fastest annual pace since the single currency’s formation.

In terms of that Euro Area CPI reading, the main headline number of +8.1% was some way above the +7.8% reading expected, whilst core CPI also rose to a record +3.8% (vs. +3.6% expected). Unsurprisingly, this has only intensified the debate on how rapidly the ECB will hike rates, and Slovakian Central Bank Governor Kazimir became the latest member of the Governing Council to say that he was “open to talk about 50 basis points”, even if his baseline was still for a 25bps move in July. The investor reaction was evident too, and overnight index swaps moved to price in 119bps worth of ECB hikes by the December meeting, which is the highest to date. It also implies that the ECB would do more than simply four 25bp moves from July, which would only sum to 100bps. The European economics team published a blog taking a deep dive into underlying inflation across the continent (link here). There are lots of different cuts of the data in the piece, but the headline is a number of underlying metrics are scoring record highs, and that a lot of the pressure is being produced domestically and not just from external shocks. In particular, Germany registers above the rest of the continent with record high underlying inflation readings. All of this underscores the call for tighter ECB policy.

Speaking of which, as previewed at the top, DB’s European economists released their ECB preview ahead of next week’s meeting yesterday, and they are now expecting the ECB to implement at least one +50bp rate hike by September, the first shop to take such a stance according to the latest Bloomberg survey. They note a +50bp hike is more likely in September but there’s a risk it comes in July. There is actually a precedent for 50bps from the ECB, although you have to go all the way back to June 2000 to find the last time they moved so quickly at a single meeting, and a +50bp hike is consistent with the reaction function President Lagarde outlined in her recent blog. Our economists also believe the ECB will be underestimating inflation with their forecast updates at next week’s meeting, necessitating a bigger rate increase early in their hiking cycle. Additionally, they expect the ECB to get rates 50bps above neutral by the middle of next year for a modestly restrictive policy stance to fight inflation. For next week’s meeting, they believe the GC will signal the end of net APP (asset purchases), clearing the way for a July liftoff. They also expect the ECB staff to raise 2024 inflation forecast to 2% and confirm the expiration of TLTRO discounts.

Elsewhere on the inflation front, it appeared that Brent crude futures were set for a 9th consecutive daily gain and their second highest close in over a decade. However a post-European close Wall Street Journal article reported that OPEC was considering exempting Russia from its oil production deal in light of sanctions, which would pave the way for other members to pump a lot more oil. This drove an intraday reversal in Brent and WTI which closed down -1.14% and -0.35%, respectively having been up +2.97% and +4.27% at their peaks for the day.

Growing fears that inflation will prove even stickier than previously hoped led to a major selloff among sovereign bonds on both sides of the Atlantic yesterday. In Europe, yields on 10yr bunds (+6.7bps), OATs (+7.5bps) and BTPs (+12.1bps) all moved higher thanks to a rise in both real rates and inflation breakevens. Meanwhile in the US, yields on 10yr Treasuries were up +10.6bps to 2.84% as markets caught up following the Memorial Day holiday and then added a bit more for good measure. We’re another +1.5bps higher this morning. As it happens, today also marks the start of the Fed’s quantitative tightening process, which starts at a pace of $30bn per month for Treasuries, and $17.5bn for MBS, although those numbers will both double after 3 months. For those wanting more details, Tim on my team released a playbook for the process a couple of weeks back (link here).

That prospect of stickier inflation and thus more aggressive rate hikes from central banks meant that equities took a knock yesterday as well. The S&P 500 was down -0.63% following its strongest weekly performance since November 2020, and small-cap stocks suffered in particular as the Russell 2000 shed -1.26%. It was a different story for the megacap tech stocks however, with the FANG+ index advancing another +0.69%, having gained more than +12% since its recent closing low last week. Over in Europe, the main indices also lost ground following their Monday gains, with the STOXX 600 (-0.72%), the DAX (-1.29%) and the CAC 40 (-1.43%) all falling back on the day. Equity futures are indicating a more positive start with contracts on the S&P 500 (+0.39%), NASDAQ 100 (+0.30%) and DAX (+0.64%) all higher.

Asian equity markets are mixed this morning. The Hang Seng is down -0.67% in early trade, tracking declines in US equity markets along with a pullback in Chinese listed tech stocks. Additionally, in mainland China, the Shanghai Composite (-0.10%) and CSI (-0.13%) are also lagging. Elsewhere, the Nikkei (+0.71%) is leading gains as the Japanese yen weakened -0.32% to 129.08 against the US dollar. Markets in South Korea are closed today for a holiday. Meanwhile, in Australia, the S&P/ASX 200 (+0.12%) is edging higher after Q1 GDP advanced +0.8% from the final three months of last year (v/s +0.7% expected), taking the annual pace to +3.3% and outpacing the pre-pandemic average of around +2%.

Other data showed that South Korea’s exports accelerated, growing +21.3% y/y in May (v/s +18.4% expected), against April’s upwardly revised +12.9% increase as shipments to Europe and US improved offsetting disruptions with China’s trade. Separately, China’s Caixin manufacturing PMI improved to 48.1 from 46.0 in April.

Back to yesterday on the data front, the Conference Board’s consumer confidence indicator for May surprise to the upside at 106.4 (vs. 103.6 expected), although it was still a decline on the previous month. Otherwise in the US, the FHFA house price index for March came in at just +1.5% month-on-month (vs. +2.0% expected), but the S&P CoreLogic Case-Shiller 20-city index surprised on the upside with a +21.2% year-on-year gain (vs. +20.0% expected). Then the MNI Chicago PMI also surprised to the upside with a 60.3 reading (vs. 55.0 expected). Finally, the number of UK mortgage approvals in April fell to their lowest in nearly 2 years at 66.0k (vs. 70.5k expected).

To the day ahead now, and data releases include the global manufacturing PMIs for May and the US ISM manufacturing reading for May. Otherwise, there’s German retail sales for April, the Euro Area unemployment rate for April, US construction spending for April and the JOLTS job openings for April. From central banks, the Bank of Canada will be making its latest policy decision and the Fed will be releasing their Beige Book. Otherwise, speakers include ECB President Lagarde and the ECB’s Knot, Villeroy, Panetta and Lane, the Fed’s Williams and Bullard, and PBoC Governor Yi Gang.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED DOWN 4.27 PTS OR 0,13% //Hang Sang CLOSED UP 178,09 PTS OR 0.65% /The Nikkei closed UP 178,09 OR 0.65% //Australia’s all ordinaires CLOSED UP .10%% /Chinese yuan (ONSHORE) closed DOWN 6,6871 /Oil UP TO 116.15dollars per barrel for WTI and UP TO 117050 for Brent. Stocks in Europe OPENED ALL MIXED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6871 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6961: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/

3B JAPAN

end

3c CHINA

END

Apple Shifts Ipad Production Out Of China For First Time

WEDNESDAY, JUN 01, 2022 – 01:05 PM

Even though the Shanghai government announced plans to lift COVID restrictions on Wednesday and reopen the city after two months of lockdowns, Apple has decided to diversify some of its product supply chains out of China.

Nikkia Asia reports that some iPad production will be moved out of Shanghai and surrounding areas to Vietnam for the first time to safeguard against any future supply chain disruptions caused by Beijing’s strict COVID restrictions.

Apple was already planning future iPad production lines in Vietnam. One of the top iPad assemblers, China’s BYD, assisted the world’s most valuable tech company in building production lines in Vietnam, with series production beginning in small numbers in the near term.

Apple has already shifted AirPods earbud production to the Southeast Asian country. The iPad would be the second major production line as the company diversifies out of China.

Besides diversifying its China-centric supply chain, the company has requested suppliers of components, such as semiconductor chips and mechanical and electronics parts based around Shanghai and surrounding regions, to quickly build inventory to mitigate supply chain disruptions for the upcoming release of the new iPhone.