June 2 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1867.35 UP $22.50

SILVER: $22.23 UP $.57

ACCESS MARKET: GOLD $1868.50

SILVER: $22.32

Bitcoin morning price: $29,942 DOWN 320

Bitcoin: afternoon price: $30,059 down 203

Platinum price: closing UP $24.80 to $1025.55

Palladium price; closing UP $43.60 at $2050.55

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: COMEX

JPMorgan issued 1086/1854

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,843.300000000 USD

INTENT DATE: 06/01/2022 DELIVERY DATE: 06/03/2022

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 521

104 C MIZUHO 100

118 C MACQUARIE FUT 38

118 H MACQUARIE FUT 54

132 C SG AMERICAS 6

323 C HSBC 75

323 H HSBC 253

332 H STANDARD CHARTE 33

357 C WEDBUSH 1

363 H WELLS FARGO SEC 52

435 H SCOTIA CAPITAL 29

555 C BNP PARIBAS SEC 2

624 H BOFA SECURITIES 93

657 C MORGAN STANLEY 17

657 H MORGAN STANLEY 188

661 C JP MORGAN 980 1046

686 C STONEX FINANCIA 12

690 C ABN AMRO 3 13

700 C UBS 48

709 H BARCLAYS 30

730 C PTG DIVISION SG 3

732 C RBC CAP MARKETS 5

737 C ADVANTAGE 2

800 C MAREX SPEC 22 6

880 C CITIGROUP 45

905 C ADM 9 22

TOTAL: 1,854 1,854

MONTH TO DATE: 10,662

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 1854 NOTICE(S) FOR 185,400 Oz//5.7667 TONNES)

total notices so far: 10,662 contracts for 1,066,200 oz (33.163 tonnes)

SILVER NOTICES:

17 NOTICE(S) FILED 85,000 OZ/

total number of notices filed so far this month 1458 : for 7,290,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $22.50

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD/

INVENTORY RESTS AT 1067.20 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $.57 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER IVWENTORY AT THE SLV.: A WITHDRAWAL OF 2.261 MILLION OZ FROMTHE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 553.872 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 661 CONTRACTS TO 146,640 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GOOD LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.19 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.19) BUT ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A STRONG NET GAIN OF1167 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 17 CONTRACTS OR 85,000 OZ//NEW STANDING: 7,355,000 / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -57

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 2 days, total 3071, contracts: 15.355 million oz OR 7.67 MILLION OZ PER DAY. (1535CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.676 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 7.676 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 661 DESPITE OUR $0.19 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1771 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 85,000 QUEUE JUMP//NEW STANDING:7,355,000 // .. WE HAD A STRONG SIZED GAIN OF 1110 OI CONTRACTS ON THE TWO EXCHANGES FOR 5.550 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 17 NOTICES FILED TODAY FOR 85,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 7868 CONTRACTS TO 505,854 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – 634 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG SIZED LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $1.00//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR GIGANTIC SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 29,100 OZ QUEUE JUMP//NEW STANDING: 69.063 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $1.00 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 4028 OI CONTRACTS 12.528 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3394 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 505,854

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4028, WITH 7868 CONTRACTS DECREASED AT THE COMEX AND 3840 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF4028 CONTRACTS OR 12.528 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3840) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (7868,): TOTAL LOSS IN THE TWO EXCHANGES 4028 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 29,100 OZ//NEW STANDING:69.063 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) STRONG SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

10,287 CONTRACTS OR 1,028,700 OZ OR 31.996 TONNES 2 TRADING DAY(S) AND THUS AVERAGING: 5143 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES: 31.996 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 31.996/3550 x 100% TONNES 0.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 31.996 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 661 CONTRACT OI TO 146,697 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1771 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1771 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 661 CONTRACTS AND ADD TO THE 1771 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1110 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 5.550 MILLION OZ

OCCURRED WITH OUR LOSS IN PRICE OF $0.19 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 13.30 PTS OR 0,42% //Hang Sang CLOSED DOWN 212.81 PTS OR 1.00% /The Nikkei closed DOWN 44.01 OR 0.16% //Australia’s all ordinaires CLOSED DOWN .85%% /Chinese yuan (ONSHORE) closed UP 6,6743 /Oil UP TO 112.24dollars per barrel for WTI and UP TO 113.30 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6743 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6848: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 7868 CONTRACTS TO 505,854 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS SMALL COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $1.00 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6447 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A fair SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3840 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :3840 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3840 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3394 CONTRACTS IN THAT 7234 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 7234 CONTRACTS..AND YET THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF GOLD $1.00.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (69.063),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 69.063 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $1.00) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A FAIR SIZED loss OF 4028 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (69.063 TONNES)…

WE HAD 634 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 4028 CONTRACTS OR 402800 OZ OR 12.528 TONNES

Estimated gold volume 123,634/// poor

Confirmed volume yesterday:164,991 contracts fair

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 2

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 37,198.706 oz Brinks Int. Delaware JPMorgan 1001 kilobars 10 kilobars 146 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 1854 notice(s)185,400 OZ 5.7667 TONNES |

| No of oz to be served (notices) | 11,542 contracts 1,154,200 oz 35.900 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,662 notices1,066,200 OZ 33.163 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

3 customer withdrawals:

i) Out of Brinks: 32,183.150 oz 1001 kilobars

ii) Out of Int. Delaware: 321.510 oz (10 kilobars)

iii) Out of JPMorgan; 4694.046 oz (146 kilobars)

total withdrawal: 37,198.706 oz

ADJUSTMENTS: 2

i) dealer to customer: Brinks 160,980.05 oz

ii) customer to dealer: JPMorgan 150,327.946 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 13,396 contracts having LOST 4432 contracts

We had 4723 notices filed on WEDNESDAY so we GAINED 291 contracts or 29,100 oz will stand at the comex

July has a GAIN OF 29 OI to stand at 2125

August has a loss of 3800 contracts down to 428,720 contracts

We had 1854 notice(s) filed today for 185,400 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 980 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1854 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1046 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (10,662) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 13,396 CONTRACTS ) minus the number of notices served upon today 1854 x 100 oz per contract equals 2,220400 OZ OR 69.063 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (10,662) x 100 oz+ (13,396) OI for the front month minus the number of notices served upon today (1854} x 100 oz} which equals 2,220,400 oz standing OR 69.063 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 69.063 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,144,416.951 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 35,027,983.608 OZ

TOTAL ELIGIBLE GOLD: 17,018,340.509 OZ

TOTAL OF ALL REGISTERED GOLD: 18,009,643.094 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,865,227.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 2

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,480,170.370 oz Brinks Delaware JPMorgan |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 560,935.768 oz CNT |

| No of oz served today (contracts) | 17CONTRACT(S) 85,000 OZ) |

| No of oz to be served (notices) | 13 contracts (65,000 oz) |

| Total monthly oz silver served (contracts) | 1458 contracts 7,290,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

ii) Into CNT: 560,935.768 oz

total deposit: 560,935.768 oz

JPMorgan has a total silver weight: 176.637 million oz/336.312 million =52.51% of comex

Comex withdrawals: 3

i) Out of Brinks: 663,356.370 oz

ii) Out of JPMorgan: 1,815,840.300 oz

iii) Out of Delaware; 973.70 oz

total withdrawal 2,480,170.370 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72,458 MILLION OZ

TOTAL REG + ELIG. 336.312 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 130 HAVING LOST 20 CONTRACTS.

WE HAD 37 NOTICES FILED ON WEDNESDAY SO WE GAINED 17 CONTRACTS OR AN ADDITIONAL 85,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 2313 CONTRACTS DOWN TO 105,994 CONTRACTS.

AUGUST GAINED 11 CONTRACTS TO STAND AT 19

SEPTEMBER HAD A GAIN OF 1773 CONTRACTS UP TO 26,326 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 17 for 85,000 oz

Comex volumes:37,453// est. volume today// poor

Comex volume: confirmed yesterday: 59,002 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1458 x 5,000 oz = 7,290,000 oz

to which we add the difference between the open interest for the front month of JUNE(30) and the number of notices served upon today 17 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1458 (notices served so far) x 5000 oz + OI for front month of JUNE (30) – number of notices served upon today (17) x 5000 oz of silver standing for the JUNE contract month equates 7,355,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

APRIL 29/WITH GOLD UP $20.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1095,72 TONNES

APRIL 28/WITH GOLD UP $2.35: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.77 TONNES FROM THE GLD //INVENTORY RESTS AT 1095.72 TONNES

APRIL 27/WITH GOLD DOWN $15.30//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1099.49 TONNES

APRIL 26/WITH GOLD UP $7.60//HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES INTO THE GLD./INVENTORY RESTS AT 1101.23 TONNES

APRIL 25/WITH GOLD DOWN $36.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1104.13 TONNES

APRIL 22/WITH GOLD DOWN $13.50: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 1104.13 TONNES

APRIL 21/WITH GOLD DOWN $6.80//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1106.74 TONNES

APRIL 20/WITH GOLD DOWN $3.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT IF 6.36 TONNES INTO THE GLD..//INVENTORY RESTS AT 1106.74 TONNES

APRIL 19//WITH GOLD DOWN $26.90//A SMALL CHANGE IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .87 TONNES INTO THE GLD//INVENTORY RESTS AT 1100.36 TONNES

APRIL 18/WITH GOLD UP $11.20: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD..//INVENTORY RESTS AT 1099.44 TONNES

APRIL 14/WITH GOLD DOWN $8.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.32 TONNES INTO THE GLD..//INVENTORY RESTS AT 1104.42 TONNES

APRIL 13/WITH GOLD UP $8.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1093.10 TONNES

APRIL 12/WITH GOLD UP $26.95: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES INTO THE GLD///INVENTORY REST AT 1093.10 TONNES

APRIL 11/WITH GOLD UP $3.40 //A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 1090.49 TONNES

GLD INVENTORY: 1067.20 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

APRIL 29//WITH SILVER DOWN 12 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ/

APRIL 28/WITH SILVER DOWN 23 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.308 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.725 MILLION OZ//

APRIL 27/WITH SILVER DOWN 4 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.385 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 578.033 MILLION OZ

APRIL 26/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ

APRIL 25/WITH SILVER DOWN 69 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.031 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 579.418 MILLION OZ//

APRIL 22/WITH SILVER DOWN 34 CENTS : STRANGE!! A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WHOPPING DEPOSIT OF 3.508 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 581.449 MILLION OZ//

APRIL 21/WITH SILVER UP 57 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ

APRIL 20/WITH SILVER DOWN 15 CENTS : A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.955 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 577.941 MILLION OZ///

APRIL 19/WITH SILVER DOWN 62 CENTS: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .461 MILLION OZ FROM THE SLV INVENTORY…//INVENTORY RESTS AT 574.986 MILLION OZ

APRIL 18/WITH SILVER UP 38 CENTS: A HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.771 MILLION OZ INTO THE SLV./INVENTORY RESTS AT 575.447 MILLION OZ//

APRIL 14/WITH SILVER DOWN 25 CENTS : A MONSTROUS CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.355 MILLION OZ INTO THE SLV.//INVENTORY RESTS AT 569.676 MILLION OZ//

APRIL 13/WITH SILVER UP 27 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 565.521 MILLION OZ

APRIL 12/WITH SILVER UP 66 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 565.521 MILLION OZ//

APRIL 11/WITH SILVER UP 13 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 831,000 OZ FORM THE SLV////INVENTORY RESTS AT 565.521 MILLION OZ

INVENTORY TONIGHT RESTS AT 5563.872 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Demand For American Gold Eagles Explodes

THURSDAY, JUN 02, 2022 – 09:35 AM

Demand for American Gold Eagles exploded in May according to the latest data from the US Mint.

The mint sold 147,000 ounces of American Gold Eagles in varying denominations totaling 200,500 coins. That was a 67% increase from March.

So far this year, the US Mint has sold 661,500 ounces of American Eagles. For the year, gold bullion demand is up a staggering 617%. When you factor out COVID-19-related sales disruptions, bullion sales are up 400% over the 5-year average between 2015 and 2019.

A market strategist told Kitco News that the surge in demand for physical metal reflects growing investor anxiety bubbling under the surface.

Bullion sales better reflect the anxiety investors are feeling right now. When you hear economists talk about a recession, it starts to make sense why bullion sales are so strong. Gold will always be a long-term store of value.”

Peter Schiff has been saying the recession is likely already here.

I don’t think it’s going to be a mild recession. I think this recession is going to be worse than the Great Recession that started following the 2008 financial crisis.”

The mainstream doesn’t seem to have picked up on this yes, but the demand for physical gold may indicate at least some people are beginning to worry.

Institutional investors focus more on the futures market. As Peter noted in a recent video on gold’s recent performance, the mainstream still thinks the Fed is going to successfully fight inflation by raising interest rates and believes the central bank has the tools to get inflation back to 2%.

Rather than fearing inflation, they’re fearing the fight against inflation.” Schiff said. “Because how is the Fed going to fight inflation? It’s going to jack up interest rates. It’s going to have a tight monetary policy. In fact, it’s even going to start shrinking the balance sheet. It’s going to start taking money out of circulation — quantitative tightening. It’s going to reverse all of that inflation. It’s going to suck up that liquidity. And that is what is scaring investors out of buying gold and silver. They still have confidence in the Federal Reserve.”

Peter said faith in the Fed is misplaced, and he emphasized that the Fed is only pretending it’s going to fight inflation.

Because it’s also pretending the economy is strong enough to withstand the fight. It’s not. Even though the fight is inadequate to solve the inflation problem, it’s going to cause a big problem for the economy that is so levered up on debt.”

A senior commodities broker with RJO Futures told Kitco News that he doesn’t think interest rates can go too much higher because of the government’s massive twin deficits – budget and trade.

Gold futures are capped by rising interest rates, but people have been going out to buy the physical metal to have some ‘real money’ stashed away.”

end

2. Lawrie Williams//Pam and Russ Martens/

END

3. Chris Powell of GATA provides to us very important physical commentaries

Silver manipulation as explained by John Adams

(John Adams/Chris Powell)

John Adams: Conquering silver market manipulation

Submitted by admin on Wed, 2022-06-01 12:57Section: Daily Dispatches

12:58p Wednesday, June 1, 2022

Dear Friend of GATA and Gold:

John Adams of As Good As Gold Australia writes that silver market manipulation goes beyond the futures markets to corrupt the physical market, where supply also is exaggerated by enterprises that sell claims to metal they don’t actually possess.

Exposing this physical market manipulation, Adams writes, is crucial to establishing a free-market price for silver.

Adams’ analysis is headlined “Conquering Silver Market Manipulation” and it’s posted at his internet site, Adams Economics, here:

https://www.adamseconomics.com/post/conquering-silver-market-manipulation

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The manipulation of gold/silver explained in USA Gold

(GATA/USA GOLD)

USAGold’s June ‘News & Views’ letter sees ‘the avalanche of history’

Submitted by admin on Wed, 2022-06-01 12:33Section: Daily Dispatches

12:32p Wednesday, June 1, 2022

Dear Friend of GATA and Gold:

USAGold’s “News & Views” letter for June carries many brief excerpts from analysts who are seeing “regime change” in the markets as inflation rages and the Federal Reserve contemplates tightening the money supply.

The June edition is headlined “The Avalanche of History” and it’s posted at USAGold here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

South Africa’s Gold Fields buys Yamana in a $6.7 billion deal

(Reuters/GATA)

South Africa’s Gold Fields to buy Yamana Gold in $6.7 billion deal

Submitted by admin on Tue, 2022-05-31 10:39Section: Daily Dispatches

From Reuters

via CNBC, New York

Tuesday, May 31, 2022

South African miner Gold Fields today agreed to buy Canada-based precious metals miner Yamana Gold in an all-share deal, valuing the Toronto-listed company at $6.7 billion.

Gold Fields said its shareholders will own about 61% of the combined group, while Yamana Gold shareholders will own around 39% after the deal completes.

The South African miner said Yamana’s board has unanimously approved the deal and recommended that its shareholders vote in favor of the offer.

The offer consists of new shares or newly issued American Depositary Shares in Gold Fields at a fixed exchange ratio of 0.6 of a Gold Fields share for each Yamana share outstanding. …

… For the remainder of the report:

https://www.cnbcafrica.com/2022/s-africas-gold-fields-to-buy-yamana-gold-in-6-7-bln-deal/

* * *

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //PALM OIL+ OTHERS

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6743

OFFSHORE YUAN: 6.6848

HANG SANG CLOSED DOWN 212.81 PTS OR 1.00%

2. Nikkei closed DOWN 44.01% OR .16%

3. Europe stocks ALL CLOSED MOSTLY GREEN

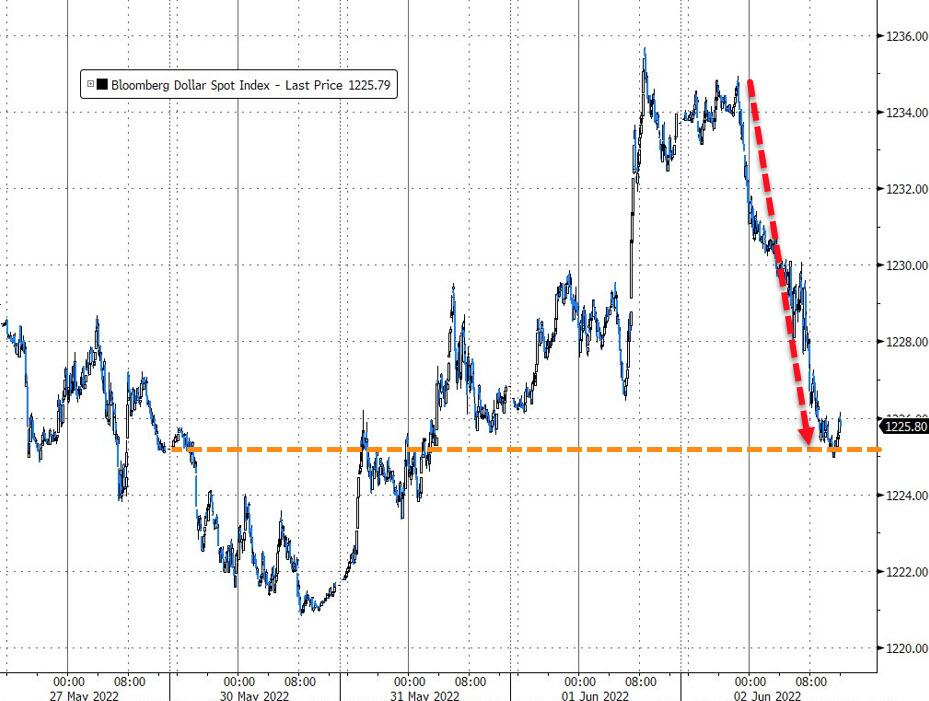

USA dollar INDEX UP TO 102.21/Euro RISES TO 1.0689

3b Japan 10 YR bond yield: RISES TO. +.239/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 129.69/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: UP -SHORE CLOSED DOWN// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +0.859%/Italian 10 Yr bond yield FALLS to 2.75% /SPAIN 10 YR BOND YIELD FALLS TO 1.90%…

3i Greek 10 year bond yield RISES TO 3.66

3j Gold at $1857.15 silver at: 22.15 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0.40 roubles/dollar; ROUBLE AT 61.67

3m oil into the 112 dollar handle for WTI and 113 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 129.67DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9599– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0261well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

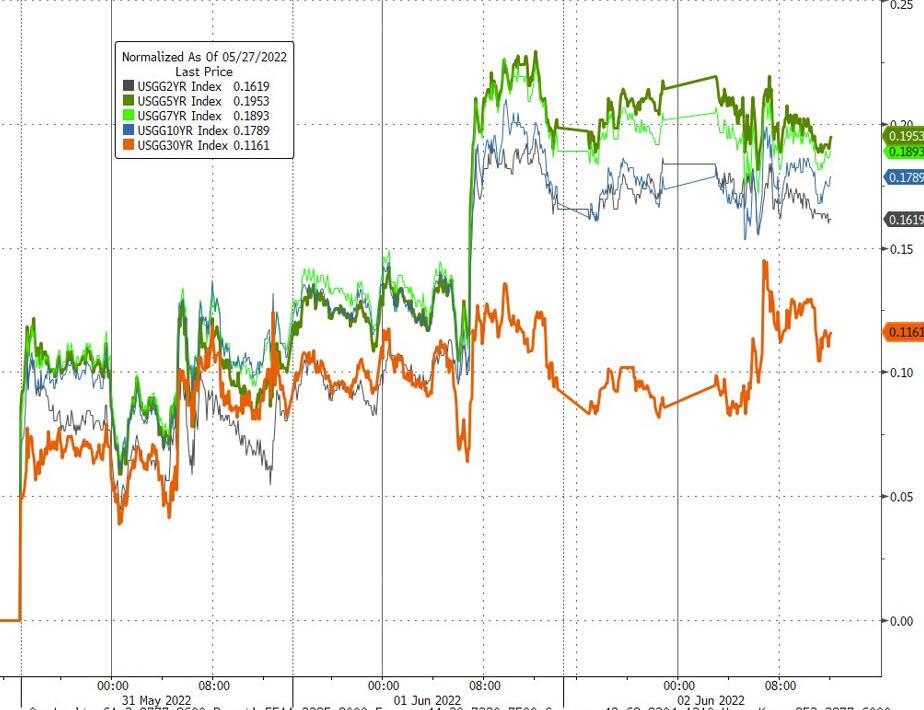

USA 10 YR BOND YIELD: 2.909 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 3.052 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.47

Futures Rise For The First Time This Week As Oil Slumps

THURSDAY, JUN 02, 2022 – 08:03 AM

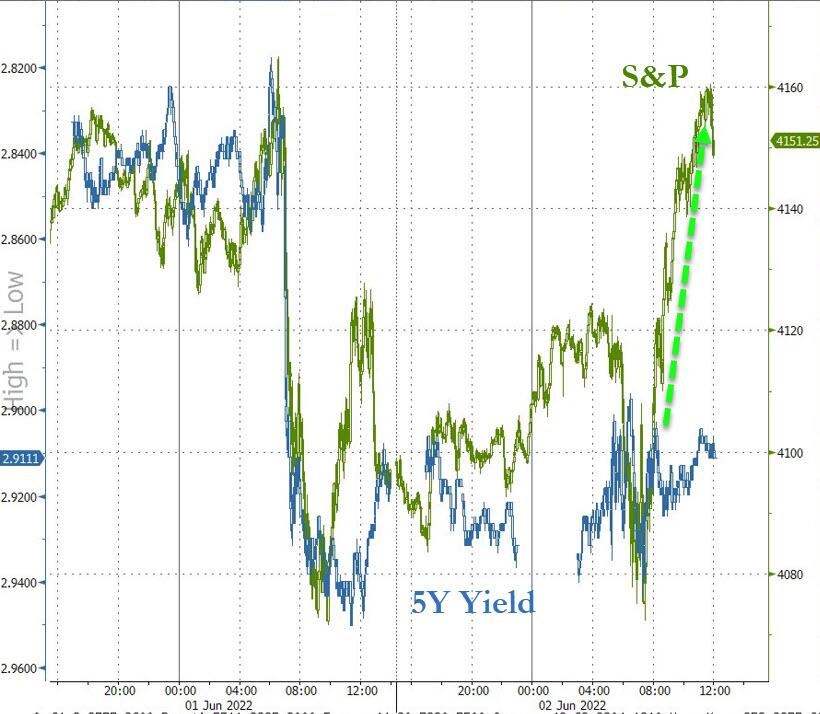

US futures advanced for the first time this week, as investors tentatively bought the dip and were cheered by a drop in oil prices. S&P 500 futures were 0.6% higher by 7:30 am in New York, while Nasdaq 100 futs gained 0.7%. Already light trading volumes are even lower, with UK markets shut for a long weekend holiday to mark Queen Elizabeth II’s Platinum Jubilee. Stocks slumped Wednesday after JPMorgan CEO Jamie Dimon’s warning to investors to prepare for an economic “hurricane”, reversing his cheerful comments from just one week earlier, and disagreeing with JPMorgan’s permabullish strategist, Marko Kolanovic, who expects stocks to rebound by the end of the year and the US to avoid recession. Treasuries held losses, with 10-year yields above 2.90%. The dollar slipped while the yen held near 130 per dollar after its recent decline on the prospect of widening interest rate differentials with the US.

Oil dropped on a rehashed report – this time from the FT which echoed an almost verbatim report from the WSJ one day earlier – that Saudi Arabia could pump more crude should Russian output drop substantially due to increasing sanctions over its invasion of Ukraine. It could, of course, but it won’t for various reasons we will discuss in a post shortly. In any case, OPEC+ meeting members are set to meet Thursday for their monthly gathering where no break up of OPEC+ is going to happen.

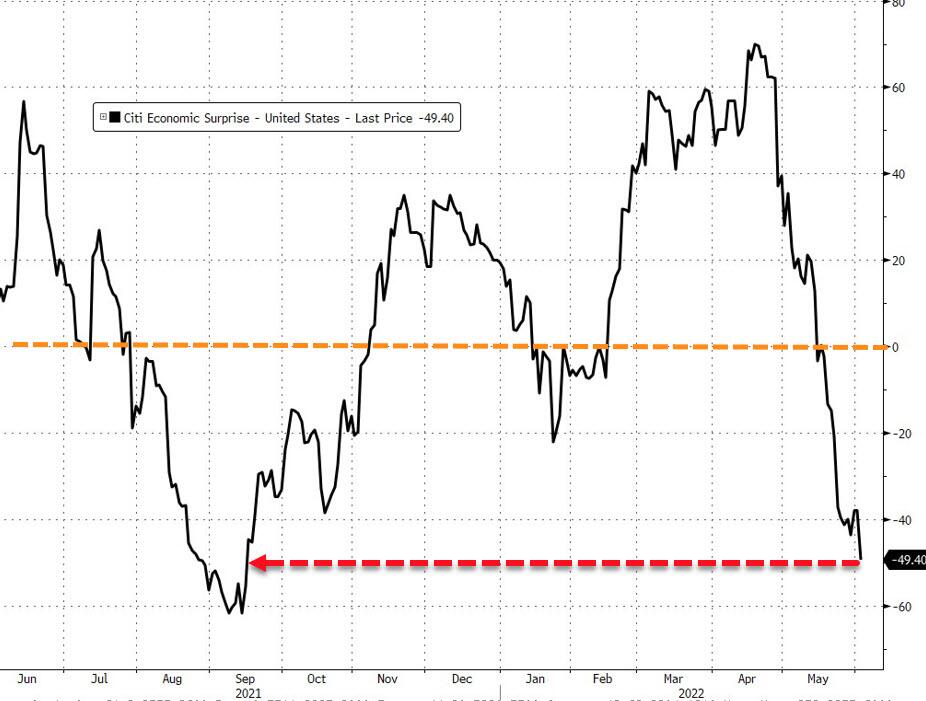

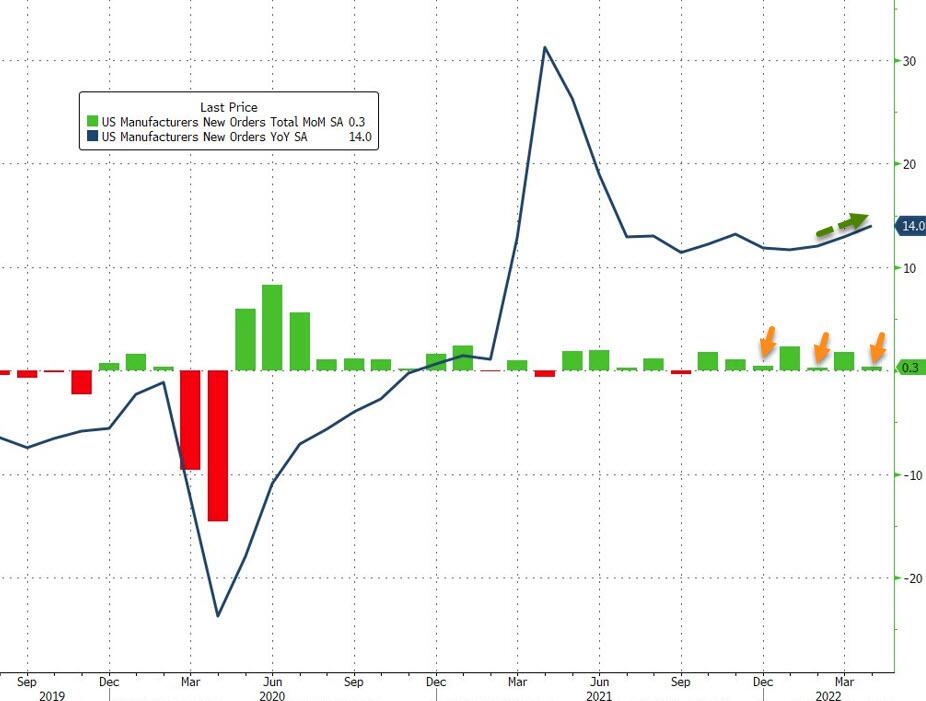

Oil’s decline helped to steady sentiment after US manufacturing activity and job openings data Wednesday fueled concern the Federal Reserve will need to get more restrictive to slow runaway price gains.

“There’s been a large correction in some stocks; those corrections led to valuations that are way more attractive that can benefit medium-to long-term investors, especially in Europe and the emerging-markets space,” Vanguard Asset Services Ltd. Investment Strategist Giulio Renzi Ricci said on Bloomberg TV, summarizing prevailing sentiment among the BTFD crowd.

In premarket trading, bank stocks are higher as the US 10-year Treasury yield rises for a third straight day to about 2.91%. Elsewhere, Repare Therapeutics will be in focus as shares soared 20% in postmarket after it announced a worldwide license and collaboration agreement with Roche for Camonsertib, while GameStop reported mixed results in the first quarter as it shifts to cryptocurrencies and non-fungible tokens. In corporate news, tech-bloated hedge fund Tiger Global Management’s losses for the year reached 51.8% amid turbulent markets. Here are some other notable premarket movers:

- Hewlett Packard Enterprise (HPE US) drops as much as 8.1% in US premarket trading on Thursday after the computer hardware and storage company lowered its adjusted earnings per share forecast for the full year.

- Chewy (CHWY US) shares are up 16% in pre- market trading after the online pet products retailer reported quarterly adjusted Ebitda and net sales that topped analysts’ expectations. Jefferies called the results “impressive.”

- NetApp Inc. (NTAP US) shares gained in extended trading Wednesday. Analysts remain cautious about the outlook for the cloud business after the storage hardware and software company reported adjusted fourth-quarter earnings that were higher than analysts’ expectations.

- C3.ai Inc. (AI US) tumbled 22% postmarket after the AI software company forecast revenue for fiscal 2023 that fell short of estimates. Piper Sandler’s analyst Arvind Ramnani cut his recommendation to neutral from overweight.

- Veeva (VEEV US)shares advanced 4.2% in postmarket trading Wednesday as it lifted its revenue forecast for the full year.

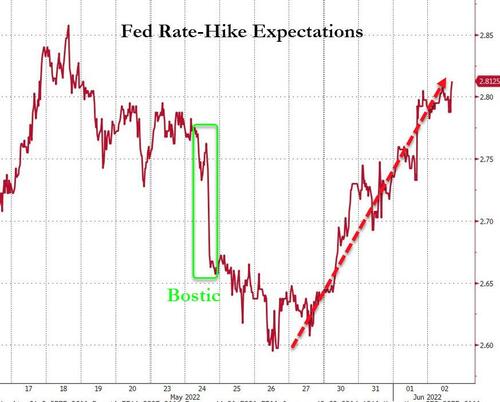

Investors have been on edge over when (not whether) the US central bank’s tighter policies will induce a recession. A chorus of Fed officials has fallen behind calls to keep hiking to counter price pressures. Mary Daly of the San Francisco Fed and her more hawkish colleague James Bullard of St. Louis both backed a plan to raise rates by 50 basis points this month, while Richmond’s Thomas Barkin said it made “perfect sense” to tighten policy.

“We do see the rise in probability of a recession in the second half of this year, potentially persisting into 2023 as the Fed continues to battle inflation,” Tracie McMillion, Wells Fargo Investment Institute head of global asset allocation strategy, said on Bloomberg Television.

In Europe, the Stoxx 600 Index advanced amid low session volumes with the London market closed in commemoration of the Queen’s Jubilee festivities. Here are some of the biggest European movers today:

- Remy Cointreau shares advance as much as 5.6% after the spirits company reported FY earnings that Morgan Stanley called “reassuring.” Peer Pernod Ricard also climb, as much as 3.1%.

- Calliditas Therapeutics rise as much as 16% after Pareto Securities initiated with a buy recommendation, calling the Swedish biotechnology firm “highly undervalued” and a potential acquisition target.

- European energy stocks underperformed as oil slipped following a report that Saudi Arabia is ready to pump more should Russian output decline substantially.

Earlier in the session, Asian markets were dragged lower by the technology sector, as strong US economic data bolstered the case for aggressive interest-rate hikes by the Federal Reserve. The MSCI Asia Pacific Index dropped as much as 1.2% as most sectors fell, with tech shares including TSMC and Alibaba among the biggest drags. South Korea led declines in the region as traders returned from a holiday, while China stocks eked out gains after authorities urged banks to set up a 800 billion yuan ($120 billion) line of credit for infrastructure projects. An unexpected advance in US manufacturing activity and still-high job openings added to investor concerns about monetary tightening in the country and its impact on global growth. James Bullard of the St. Louis Fed urged policy makers to raise interest rates to 3.5% this year to try and curb inflation. The US policy outlook adds to pressure on Asian firms, whose earnings prospects have dimmed on higher costs and China’s economic slowdown. The MSCI regional benchmark is down 13% this year, largely tracking the S&P 500’s 14% loss.

“We do think near term it’s likely to be bumpy,” Sunil Koul, Apac equity strategist at Goldman Sachs, told Bloomberg Television. “This combination of quantitative tightening, raising rates, combined with some growth risks we are seeing and a stronger dollar is what is causing pain in the markets.”

Japanese stocks fell as the persistent risk of global inflation and the prospects of tighter monetary policy in the US damped sentiment. The Topix closed 0.6% lower at 1,926.39 at the 3pm close in Tokyo, while the Nikkei 225 declined 0.2% to 27,413.88. Sony Group contributed the most to the Topix’s decline, decreasing 3.2%. Out of 2,171 shares in the index, 675 rose and 1,402 fell, while 94 were unchanged. “There are still worries over inflation in the US and rate hikes, so it will be quite hard for stocks to enter an upward trend,” said Hitoshi Asaoka, a senior strategist at Asset Management One.

Stocks in India overcame concerns over hawkish central bank moves to snap two days of declines as a drop in oil prices and attractive valuations buoyed investors. The S&P BSE Sensex rose 0.8% to 55,818.11 in Mumbai, while the NSE Nifty 50 Index advanced 0.6%. Reliance Industries provided the biggest boost to the key gauges, surging 3.5%, followed by software majors Infosys and Tata Consultancy Services. Of the 30 member stocks on the Sensex, 20 rose, while 10 declined. All but four of the 19 sectoral indexes compiled by BSE Ltd., rose, led by a measure of energy companies. Stocks in Asia were mostly lower after strong US economic data bolstered the case for aggressive interest-rate hikes by the Federal Reserve. However, the trend soon changed as investors assessed attractive valuations, while crude oil slid to $113 a barrel before the monthly OPEC+ meeting later today. “Nifty valuations are now at a sweet spot where they offer good potential returns,” DSP Mutual Fund said in note. About half of the NSE Nifty 500 Index’s members have corrected more than 30%, which creates selective opportunities, the asset manager said.

In Australia, the S&P/ASX 200 index fell 0.8% to close at 7,175.90, following US shares lower after Fed officials reinforced a hawkish stance and JPMorgan’s Jamie Dimon cautioned on the economy. Megaport led a drop in technology shares. Woodside was the top performer after a block trade. In New Zealand, the S&P/NZX 50 index fell 0.2% to 11,349.54.

In FX, the Bloomberg Dollar spot Index fell as the greenback traded weaker against all of its Group-of-10 peers. The euro snapped two days of losses and approached $1.07. One-week options in euro-dollar now capture the next ECB meeting, and implied volatility in the euro heads for its strongest close since mid-May. The pound retraced about half of Wednesday’s loss, with UK markets shut for a holiday. Australia’s bonds dropped amid speculation that the Reserve Bank of Australia will follow its Canadian counterpart and keep raising rates aggressively. The yen fell to a three-week low before reversing losses.

US Treasuries were flat in early US trading as equity futures rose for the first time this week. The 10Y Yield is trading unch at 2.91%, outperforming most euro-zone counterparts, with 2- to 5-year yields cheaper by 1bp-2bp with 10- to 30-year yields little changed, flattening 5s30s by ~2bp. IG dollar issuance slate empty so far; nine borrowers priced $14.6b Wednesday, largest daily total since May 17. European bonds posted modest losses after a steady start.

As noted above, crude oil slid on a report that Saudi Arabia is ready to pump more oil if Russian output declines. OPEC+ is scheduled to meet to discuss supply policy, where it is not expected to surprise anyone. At last check, Brent was trading just above $113, and although the benchmark lifted around $1/bbl off of its overnight troughs, this has marginally pulled back.

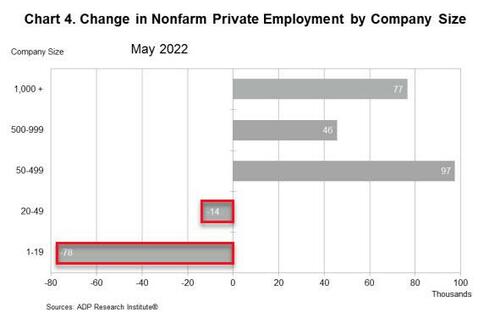

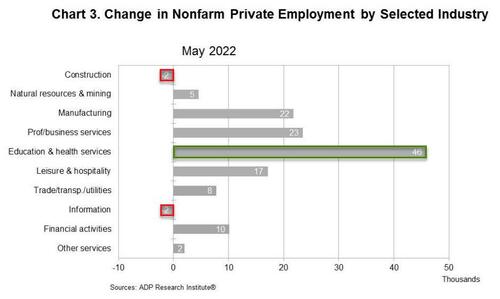

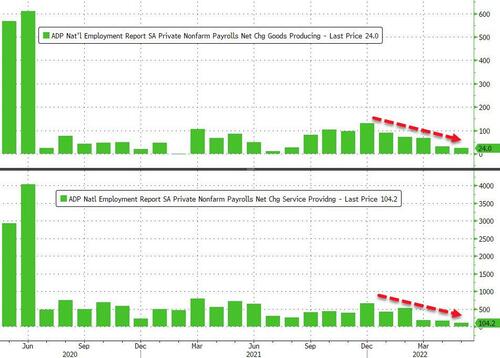

Looking at the day ahead, the economic data slate includes May Challenger job cuts (7:30am), ADP employment change (8:15am), 1Q final nonfarm productivity and initial jobless claims (8:30am) and April factory orders (10am). Fed speakers slated include Logan (12pm) and Mester (1pm).

Market Snapshot

- S&P 500 futures up 0.5%

- STOXX Europe 600 up 0.5%

- MXAP down 0.7% to 167.84

- MXAPJ down 0.8% to 552.13

- Nikkei down 0.2% to 27,413.88

- Topix down 0.6% to 1,926.39

- Hang Seng Index down 1.0% to 21,082.13

- Shanghai Composite up 0.4% to 3,195.46

- Sensex up 0.8% to 55,825.08

- Australia S&P/ASX 200 down 0.8% to 7,175.94

- Kospi down 1.0% to 2,658.99

- German 10Y yield up 2bps to 1.21%

- Euro up 0.4% to $1.0689

- Brent futures down 2.3% to $113.65/bbl

- Gold spot up 0.3% to $1,851.88

- U.S. Dollar Index down 0.3% to 102.23

Top Overnight News

- President Joe Biden is likely to visit Saudi Arabia later this month as part of an international trip for NATO and Group of Seven meetings, according to people familiar with the matter, with record high US gas prices weighing on his party’s political prospects

- The ECB must pare back stimulus as inflation is too strong and too broad, Governing Council member Francois Villeroy de Galhau said

- EU efforts to approve a partial ban on Russian oil imports hit an obstacle after Hungary raised new or already rejected demands, further slowing a push to clinch a deal, according to people familiar with the negotiations

- The pound is coming off the first positive month of 2022, but the mood in the market is as bleak as ever. Scorching inflation, an economy teetering on the edge of recession and a scandal-prone government are feeding into a view that the UK currency is vulnerable

- After years of pushing exports to China and building up energy links to Russia, Germany’s economy faces a poisonous cocktail of risks. Its heavy reliance on manufacturing makes it more vulnerable than European peers to war-related disruptions in Russian energy supplies and bottlenecks in trade. The upshot is risk of contraction and even higher prices squeezing unsettled consumers

- Beijing is turning to state-owned policy banks once again to help rescue an economy under strain, ordering them to provide 800 billion yuan ($120 billion) in funding for infrastructure projects

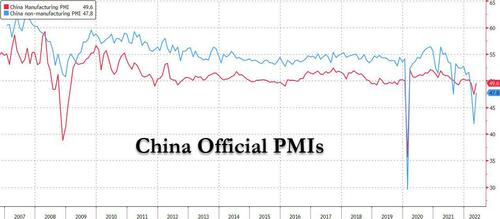

- Chinese officials have vowed to carry out a slew of government policies to stimulate growth following Premier Li Keqiang’s recent call to avoid a Covid- fueled economic contraction this quarter

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks followed suit to the subdued performance seen in global peers after the recent upside in yields and hawkish central bank rhetoric. ASX 200 was dragged lower by underperformance in tech and weakness in financials, with sentiment also not helped by frictions with China. Nikkei 225 lacked firm direction with automakers indecisive following sharp declines in their US sales last month. Hang Seng and Shanghai Comp traded mixed ahead of the Dragon Boast Festival tomorrow and with Hong Kong suffering from notable losses in property names and tech, while losses in the mainland were pared amid COVID-related optimism and after the latest support efforts in which Beijing announced CNY 800bln of increased credit quotas for state-owned policy banks to fund the construction of infrastructure projects.

Top Asian News

- China’s Ambassador to Australia said that Beijing is prepared to talk with Australia without preconditions but added that trade sanctions on Australia will not be removed until there is an improvement in the political relationship, according to AFR.

- China’s Global Times tweeted that Chinese Coast Guard vessels patrolled the territorial waters off the Diaoyu Islands (Senkaku Islands) on Thursday, which is a disputed territory with Japan.

- Japan’s Chief Cabinet Secretary Matsuno confirmed that the government wants to increase the average minimum wage to JPY 1000, according to Reuters.

- China’s Commerce Ministry, on the US considering adding additional firms to the blacklist, says they will adopt measures to protect Chinese firms.

- A group of nations are to make a request for an international labour organisation mission to China to probe alleged violation in Xinjiang at a meeting today, according to Reuters sources.

- Chinese Officials Vow to Carry Out Plans for Economic Stimulus

- Toshiba Reveals Buyout Bids as Privatization Chances Rise

- Hong Kong Quarantine Backtrack Stokes Fears of Covid Zero Return

European bourses are posting modest gains, Euro Stoxx 50 +0.6%, though volumes are lighter given UK Spring Bank Holiday. Stateside, futures are firmer across the board, ES +0.5%, with action similarly contained ahead of a busy PM docket featuring ADP and Fed’s Mester.

Top European News

- Deutsche Bank CEO’s Fixer Hoops Takes Another Leap as DWS Chief

- Ukraine Latest: Russia Ready to Settle Eurobond Payment Claims

- Euro Options Into ECB Meeting Are Now Most Overpriced in a Month

- Swiss Exchange Investigates Swissquote for Disclosure Delay

FX

- Pound pounces on Dollar downturn to reclaim 1.2500 handle as UK prepares for Platinum Jubilee celebrations.

- DXY sub-102.500 amidst broad bounce in index components led by Franc initially; USD/CHF reverses around 0.9600 axis in wake of Swiss inflation data showing bigger overshoot vs SNB targets.

- Euro eyes 1.0700, but capped by hefty option expiry interest from round number up to 1.0740.

- Kiwi and Aussie boosted by recovery in risk sentiment, but Loonie lags as WTI sags on reports of Saudi Arabia standing ready to cover any shortfall in Russian oil output; NZD/USD probes 0.6500, AUD/USD approaches 0.7200 and Usd/Cad 1.2650+

- Yen retrieves some losses as Greenback retreats and US Treasury yields slip from peaks ahead of busy pm agenda, USD/JPY circa 129.70 compared to 130.24 overnight peak.

Fixed Income

- Bunds and Eurozone peers extend recent losing streak to set deeper cycle lows in futures/high yields, without Liffe support and despite steady US Treasuries.

- 10 year German benchmark down to 150.29 and 1.21%+ in cash terms.

- Multi-tranche Spanish and French issuance draw mixed covers irrespective of concession.

- T-note holds around par within 118-30+/18+ range awaiting slew of US data and more Fed speakers.

Commodities

- WTI and Brent remain pressured after overnight FT reports re. Saudi being prepared to pump more oil if Russian output declines.

- Though, the benchmarks have lifted around USD 1/bbl off of their respective overnight troughs at best; however, this has marginally pulled back.

- Reminder, the JMMC commences from 13:00BST/08:00ET with the OPEC+ event following ~30-minutes later.

- US Private Energy Inventory Data (bbls): Crude -1.2mln (exp. -1.4mln), Gasoline -0.3mln (exp. +0.5mln), Distillate +0.9mln (exp. +1.0mln), Cushing +0.2mln.

- Norway’s Hammerfest liquefied natural gas plant has restarted LNG production following a fire 20 months ago, according to Equinor (EQNR NO).

- Spot gold is bid but has failed to gain much additional traction after breaching USD 1850/oz and the 10-DMA at USD 1851.3/oz; base metals are bid ahead of the long Chinese weekend for Dragon Boat Festival.

US Event Calendar

- 8:15am: U.S. ADP Employment Change, May, est. 300k, prior 247k

- 8:30am: U.S. Initial Jobless Claims, May 28, est. 210k, prior 210k; Continuing Claims, May 21, est. 1340k, prior 1346k

- 8:30am: U.S. Nonfarm Productivity, 1Q F, est. -7.5%, prior -7.5%

- 10am: U.S. Durable Goods Orders, April F, est. 0.4%, prior 0.4%

- 10am: U.S. Factory Orders, April, est. 0.6%, prior 2.2%, revised prior 1.8%; -Less Transportation, April F, est. 0.3%, prior 0.3%

- 10am: U.S. Cap Goods Orders Nondef Ex Air, April F, est. 0.4%, prior 0.3%

- 10am: U.S. Cap Goods Ship Nondef Ex Air, April F, no est., prior 0.8%

DB’s Tim Wessel concludes the overnight wrap

Filling in while the UK is on holiday, I hope my use of “Z’s” and neglect of “U’s” does not prove jarring to regular readers. The start of the month was jarring to many asset holders, as bond and equities both sold off with more evidence that labor markets are historically tight while inflation remains well above target. Meanwhile, the Fed’s beige book provided anecdotes of slowing growth in some districts, while a majority of districts had respondents expecting growth to slow in the near future. St. Louis Fed President and Hawk Emeritus James Bullard joined San Francisco Fed President to echo previous Fed communications that policy would expeditiously get to neutral, while the CEO of J.P. Morgan gave the gloomy growth narrative his imprimatur. The mix drove policy pricing higher and all but one sector in the S&P lower. North of the border, the Bank of Canada hiked rates another +50bps, layering hawkish guidance into the statement such as “the risk of elevated inflation becoming entrenched has risen.” While in Europe, ECB Governing Council member Holzmann sang the virtues of a +50bp hike (in line with our Europe team’s updated ECB call, found here).

Stepping through the developments. The rate selloff began in earnest following the mid-morning data dump in the US, which included May ISM manufacturing and April JOLTS data. The ISM print surprised to the upside at 56.1 versus expectations of 54.5, while prices paid printed at 82.2 versus expectations of 81.0. Meanwhile, the JOLTS data across quits, hiring, and opening painted an historically tight labor market picture, with the vacancy yield (hires-per-job opening) hitting a record low. The March revisions also leaned tighter. The data re-emphasized that policy would need to get much tighter to do the work of actually bringing inflation down despite bubbling fears that the growth outlook was on shaky footing. The Treasury curve sold off and flattened, with 2yr yields gaining +8.5bps and the 10yr yield increasing +6.2bps, with real yields gaining +6.1bps in line with the tighter expected policy path.

Two of the more germane policy path questions – how to size the September hike and what is terminal – moved tighter, in turn. The odds of a +50bp September move reached a month-high 65%, while terminal pricing moved back north of 3.1%. Presidents Bullard and Daly, typically taking opposing corners in the ideological ring, both re-emphasized the need to tighten policy expeditiously to neutral in light of runaway inflation. While policymakers debate where neutral is and what to do once there, support to get there fast is robust; it is best to heed their harmonious message the next time growth fears or falling risk assets drive policy pricing lower. Balance sheet policy will augment tightening as June marks the start of the Fed’s balance sheet normalization process, or QT. For more details on what that entails, I published a playbook on QT in conjunction with US rates and economics colleagues, found here.

Steeper policy paths gripped north of the border and across the Atlantic as well. On the latter, Austrian central bank governor Holzmann said that “a 50 basis-point rise would send the necessary clear signal that the ECB is serious about fighting inflation”, leading OIS rates to price in +38bps by the July meeting. Longer-dated sovereign yields sold off in concert, with 10yr bunds (+6.4bps), OATs (+6.6bps) and BTPs (+8.5bps) hitting fresh multi-year highs. The spread of 10yr Italian yields over bunds also moved back above 200bps. The Bank of Canada hiked rates +50bps as expected, though weaved in restrictive guidance that gave the meeting a hawkish hue. Namely, the central bank warned they could be “more forceful” if needed, updating their statement to note that the economy was “clearly operating in excess demand”, which risked elevated inflation becoming yet more entrenched, as mentioned.

The daily stew got a dose of anecdotal growth fears with the release of the beige book and comments from the CEO of J.P. Morgan warning that an economic “hurricane” was on the horizon. The beige book had a majority of Fed districts with contacts reporting growth or recession fears. The impact was to bring 10yr yields around 5bps below their intraday highs. Those yields are less than a basis point higher from those levels as we go to press this morning.

The mixture drove equities lower on both sides of the Atlantic. The S&P 500 retreated -0.75% to start the month, with all but one sector in the red. The NASDAQ was in line, falling -0.72%, though mega cap growth FANG+ felt the impact of higher discount rates, falling -0.92%. In Europe, stocks underperformed as the continent countenances yet tighter monetary policy, with the STOXX 600 falling -1.04%.

Energy was the sole gainer in the S&P, though that outperformance may be short lived as the FT reported overnight that Saudi Arabia was primed to pump more oil onto the market should Russian exports be crimped by sanctions. Brent crude futures are -1.67% lower ahead of the OPEC+ meeting today.

Asian equity markets are trading lower following yesterday’s selloff. Across the region, the Hang Seng (-1.72%) is the largest underperformer after the local government decided to revive its toughest Covid-Zero measures as Covid variants flare. US stock futures are swinging between gains and losses with contracts on the S&P 500 (+0.04%), NASDAQ 100 (+0.07%) virtually unchanged.

Elsewhere, early morning data showed that Australia’s April trade surplus swelled to A$10.5 bn (v/s A$9.0 bn) from the A$9.7 bn.

In terms of yesterday’s other data, German retail sales fell by a larger-than-expected -5.4% (vs. -0.5% expected). Otherwise, the final manufacturing PMIs for May only diverged slightly from the flash readings. The Euro Area manufacturing PMI was revised up to 54.6 (vs. flash 54.4), but the US manufacturing PMI was revised down to 57.0 (vs. flash 57.5).

To the day ahead now, and data releases include the Euro Area’s PPI for April, as well as the US weekly initial jobless claims, April’s factory orders, and the ADP’s report of private payrolls for May. Central bank speakers include the ECB’s Villeroy and Hernandez de Cos, along with the Fed’s Mester.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 13.30 PTS OR 0,42% //Hang Sang CLOSED DOWN 212.81 PTS OR 1.00% /The Nikkei closed DOWN 44.01 OR 0.16% //Australia’s all ordinaires CLOSED DOWN .85%% /Chinese yuan (ONSHORE) closed UP 6,6743 /Oil UP TO 112.24dollars per barrel for WTI and UP TO 113.30 for Brent. Stocks in Europe OPENED MOSTLY GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6743 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6848: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/

3B JAPAN

end

3c CHINA

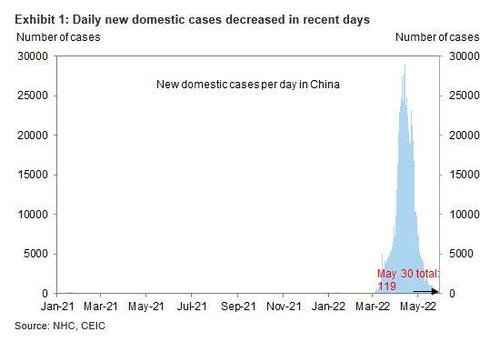

Shanghai reopens after a two month COVID lockdown

(zerohedge)

“The Nightmare Has Ended”: Shanghai Reopens After Two-Month COVID Lockdown

WEDNESDAY, JUN 01, 2022 – 05:05 PM

Relieved residents danced in the streets after Shanghai on Wednesday officially lifted a two-month virus lockdown that triggered public outrage while dealing a huge blow to the economy, sending it reeling to depths not seen since the global shutdown in Q1 2020.

Dozens of cities across China have been under full or partial lockdown for months as the country with the “zero covid” policy battled its worst COVID-19 outbreak since early in the pandemic. But the Shanghai shutdown was the biggest, with most of the city’s 25 million residents confined to their homes since late March, turning the once-bustling metropolis into a ghost town.

That changed at midnight on Wednesday, when Shanghai authorities started taking down metal barriers and yellow plastic blockades that had blanketed one of the world’s biggest cities. Residents spilled into the streets to celebrate what was for many their first taste of freedom since the lockdown orders.

As the Nikkei reports, some residents cheered and posed for photos, others danced and drank in the streets until the early hours of Wednesday morning while parks filled up with kids and their parents. The end of the lockdown meant a green light for neighborhood businesses and major manufacturers to restart operations. But dining inside restaurants was still banned, bars are open but don’t serve alcohol, and movie theaters and gyms remain closed. Supermarkets, convenience stores and pharmacies were to reopen gradually with capacity limits.

Restarted public transit filled up with white-collar workers making their way back to the office. “I am glad the nightmare has ended,” said a banker surnamed Chen as he returned to work in the Lujiazui financial district. “But only about half of the staff will be back to the office this week due to COVID-prevention rules before we fully resume next week,” Chen said.

Chen was among hundreds of thousands of unlucky people hauled off to makeshift quarantine facilities after being suspected of coming into contact with a virus-infected person. He described his two-week stay at the bare-bones site as a “horrifying experience.”

Some more details from Nikkei:

Shanghai lifted the lockdown after confirmed infections this week plunged into the low double digits from highs topping 20,000 a day in April.

But the draconian measures sparked widespread anger as they left some homebound people jobless and others desperately struggling to keep businesses afloat. Food shortages and limited access to medical care aggravated the outrage, which often spilled on to social media despite government efforts to portray the shutdown as orderly and well managed.

The restrictions in Shanghai and other cities, including the capital Beijing, have taken a bite out of the economy and raised questions about whether China can hit its 5.5% growth target this year. There were signs, however, that factory activity was rebounding modestly as production shutdowns and other virus restrictions are eased.

To be sure, China is already “benefiting” from the reopening, with the latest PMI print seeing a bounce from recent lows. Expect these numbers to rise materially in coming months as more lockdowns ease.

On Wednesday, people walked their dogs on Shanghai’s streets and seniors practiced tai chi in public squares while barbers welcomed shaggy-haired residents in need of a trim. But the jubilation was mixed with caution, as many feared another outbreak could prompt nervous authorities to bring back restrictions.

“We feel happy, but at the same time we worry about another outbreak,” a husband and wife duo told Nikkei Asia as they walked along the Bund, Shanghai’s historic riverside district. “Many people think the pandemic is over … but it is clearly not.”

Some shopping malls threw open their doors Wednesday, while many retailers spent the day cleaning and disinfecting shops before welcoming back shoppers.

“Customers will likely to stay away for the first few weeks, just like what we went through in 2020,” said Jia Hong, a hot bun seller in the Jing’an central business district. “Many are wary about the risks of eating outside.”

China’s biggest lockdown tested President Xi Jinping’s signature zero-COVID policy, which relies on heavy restrictions, including mass testing and lockdowns, to quash outbreaks at any cost.

The government has said it is sticking with that approach in a bid to save lives and stop its health care system from being overwhelmed, even as much of the world moves toward living with the virus. That means Shanghai residents must now take a PCR test every three days at one of thousands of temporary screening booths in order to use public transit or enter shops.

“We will have to do this endlessly,” said Bai Ying, a property agent who was getting tested. “The risk of catching the virus is higher here than at home, but we have no choice.”

END

Shanghai’s Local Authorities Hesitate To Lift Lockdowns As Ordered, Concerned Over Blame For Inevitable Next Outbreak

THURSDAY, JUN 02, 2022 – 10:45 AM

Authored by Sophia Lam via The Epoch Times,

Shanghai, China’s economic and commercial hub with a population of over 24 million, has been in a hard lockdown for the past two months, which has only just been lifted by the municipal government. Production activities were halted, businesses shut down, and residents were barred from leaving their homes.

Residents have decried the absolute and heavily enforced restrictions, some unnecessary, imposed by their communities, while government staffers from Shanghai’s many local community committees deferred residents’ complaints by saying they were just following “orders from above”—referring to the municipal and central government authorities.

Community committees are the grassroots level of the Chinese regime’s government structure, and are under the direct supervision of subdistrict offices. They take charge of almost all civil affairs in the community, including enforcement of the regime’s policies such as family planning, maintenance of social security, and distribution of aid, among others.

Despite Shanghai’s announcement that it was lifting lockdown restrictions on June 1, many residents have expressed doubt over whether their local community committees will actually follow through with the relaxing the restrictions.

Several Shanghai residents told the Chinese-language edition of The Epoch Times that their community committees have continued to imposing strict lockdowns to avoid responsibility for any possible spreading of COVID-19.

Tang Hua (an alias) from Shanghai’s Hongkou District said in an interview on May 31 that there has been no notice from her community committee about allowing residents to move around freely again.

“Now the municipal government says to lift the restrictions. But who will be responsible for the relaxation? What prevention measures should be taken? They (community committee management) have said nothing. We in the community are still required to take nucleic acid testing today,” she told The Epoch Times.

A resident looks out from her window during a COVID-19 lockdown in the Jing’an district of Shanghai on May 25, 2022. (Hector Retamal/AFP via Getty Images)

At a regular presser on May 31, the municipal officials announced that, effective from June 1, only visitors from other districts would be required to do PCR COVID-19 tests. But residents from Fengxian District, Pudong District, and Songjiang District told The Epoch Times that they are still required to undergo PCR testing and also don’t expect their community committees to relax many restrictions.

Mr. Li (pseudonym) from Songjiang District said that his community committee told their residents that PCR testing was “a unified arrangement from higher above.” They were not able to present any documentation of the order when Mr. Li asked for it.

“There hasn’t been any single positive case in our compound in the past 50 days, so what’s the point of continuing with the tests when there is no positive case at all?” Mr. Li complained to his community committee.

Municipal Government Shirking Responsibility

Gu Guoping, a retired university teacher and rights activist based in Shanghai, said that the city’s municipal government let the community committees decide on their own restriction measures as a means of deferring any blame.

“They have put the blame on the grassroots level by doing so,” Guo told The Epoch Times in an interview. “But the community committee dare not take it upon themselves to impose the restrictions; they have to follow instructions from their superiors.”

“The government does this with one benefit: [the lockdown] isn’t done by the government, but by the community committee, which is meant to be elected by residents,” Gu added.

According to a document issued in 2010 by the general offices of the CCP’s Central Committee and of the State Council, the community committees, under the CCP leadership, have five to nine members who are elected by residents. Their work expenses and personnel remuneration, and the costs for establishing and maintaining information networks are included in the financial budget of the government. It is also stipulated that local governments should set up a community committee where there are 100 to 700 households.

“But in reality, the committee members are chosen by the government; we haven’t elected them,” Gu said.

Hardship and Suffering

Residents in Shanghai have suffered depression and people have died due to a lack of medical treatment during the lengthy and heavy-handed lockdown.

Chinese news portal NetEase released a survey on May 5 that found that 40 percent of residents had reported signs of depression.