JUNE 8 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

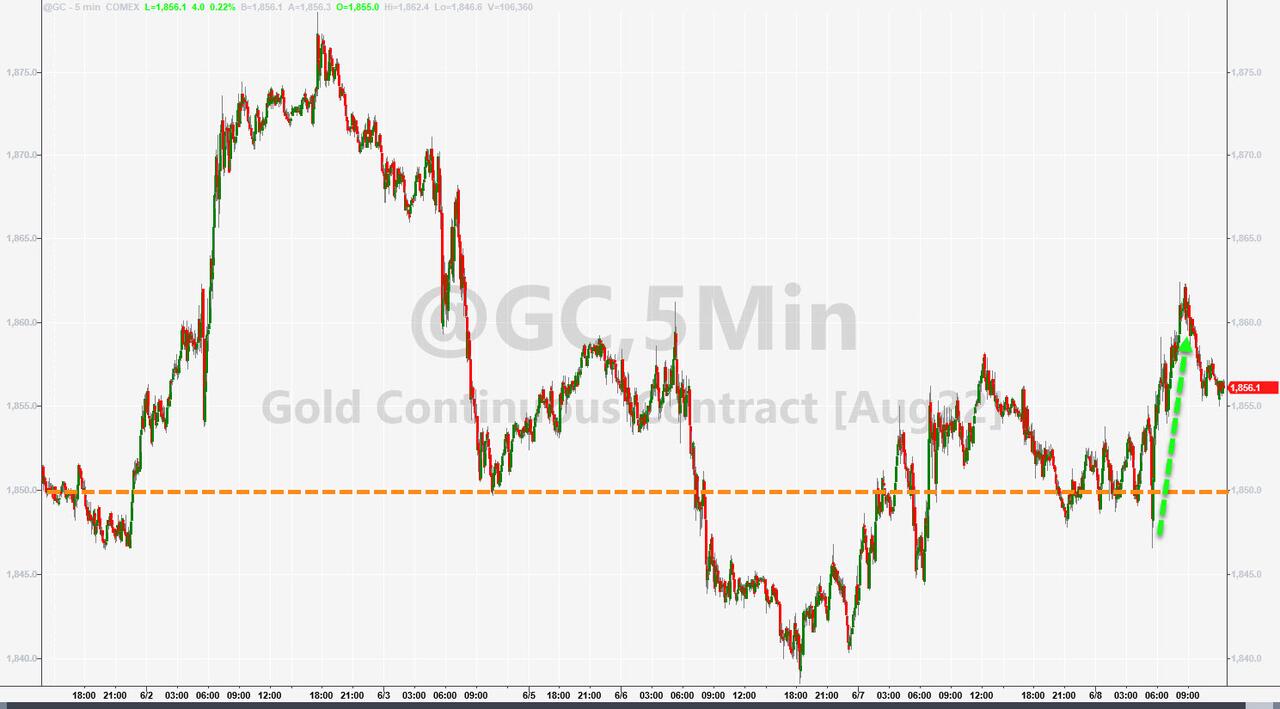

GOLD; $1853.95 UP $4.75

SILVER: $22.07 DOWN $.08

ACCESS MARKET: GOLD $1852.20

SILVER: $22.05

Bitcoin morning price: $30,420 UP 227

Bitcoin: afternoon price: $30,121 DOWN 72

GOLD; $1847.60

Platinum price: closing DOWN $0.90 to $1011.30

Palladium price; closing DOWN $31.50 at $1951.90

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE: 710/980

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,847.500000000 USD

INTENT DATE: 06/07/2022 DELIVERY DATE: 06/09/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 15

323 C HSBC 29

323 H HSBC 98

332 H STANDARD CHARTE 14

363 H WELLS FARGO SEC 20

435 H SCOTIA CAPITAL 11

624 H BOFA SECURITIES 36

657 C MORGAN STANLEY 6

661 C JP MORGAN 710

686 C STONEX FINANCIA 4

690 C ABN AMRO 4

700 C UBS 19

709 C BARCLAYS 960

709 H BARCLAYS 11

732 C RBC CAP MARKETS 2

800 C MAREX SPEC 14 4

905 C ADM 3

TOTAL: 980 980

MONTH TO DATE: 19,980

no. of contracts issued by JPMorgan:

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 980 NOTICE(S) FOR 980,000 Oz//3.048 TONNES)

total notices so far: 19,980 contracts for 1,998,000 oz (62.196 tonnes)

SILVER NOTICES:

63 NOTICE(S) FILED 315,000 OZ/

total number of notices filed so far this month 1565 : for 7,825,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $4.75

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGE IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1063.07 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 8 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER IVWENTORY AT THE SLV.:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.306 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 893 CONTRACTS TO 148,294 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR SMALL $0.06 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.06) AND ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A VERY STRONG GAIN OF 1283 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 3 CONTRACTS OR 15,000 OZ//NEW STANDING: 8,110,000 / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -445

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 6 days, total 5,511, contracts: 27.555 million oz OR 4.5925 MILLION OZ PER DAY. (918 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 4.5925 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 4.5925 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 893 WITH OUR $0.06 GAIN IN SILVER PRICING AT THE COMEX// TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 390 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 15,000 QUEUE JUMP //NEW STANDING:8,110,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 1283 OI CONTRACTS ON THE TWO EXCHANGES FOR 6.415 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 63 NOTICES FILED TODAY FOR 315,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1686 CONTRACTS TO 494,130 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -585 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE LOSS IN COMEX OI CAME DESPITE OUR GAIN IN PRICE OF $7.45//COMEX GOLD TRADING/TUESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S HUGE 103,900 OZ QUEUE JUMP//NEW STANDING: 72.423 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $7.45 WITH RESPECT TO MONDAY’S TRADING

WE HAD A SMall SIZED GAIN OF 228 OI CONTRACTS 0.709 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1914 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 494,130

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 228, WITH 1686 CONTRACTS DECREASED AT THE COMEX AND 1914 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 228 CONTRACTS OR 0.709 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1914) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1686,): TOTAL GAIN IN THE TWO EXCHANGES 228 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 103,900 OZ//NEW STANDING: 72.423 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) SMALL SIZED COMEX OI. LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

23,967 CONTRACTS OR 2,396,700 OZ OR 74.54 TONNES 6 TRADING DAY(S) AND THUS AVERAGING: 3394 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES: 68.59 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 74.54/3550 x 100% TONNES 2.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 74.54 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 893 CONTRACT OI TO 148,294 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 390 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 390 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1348 CONTRACTS AND ADD TO THE 390 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1283 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 6.415 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.06 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

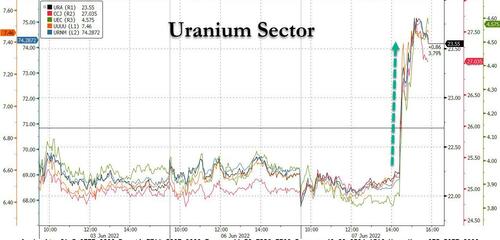

6. Commodity commentaries//URANIUM

Uranium Stocks Soar On Report US Seeking Billions To End Reliance On Russian Enriched Uranium

TUESDAY, JUN 07, 2022 – 04:18 PM

Back in February, when Biden instituted a wholesale ban on Russian energy exports, he explicitly carved out Russian uranium suppliers for the simple reason that the US is very much reliant on Russia for its nuclear power plant needs – after all, Russia is the third-largest source of U.S. uranium, accounting for about 16.5% of total U.S. uranium imports in 2020 and 23% of the enriched uranium needed to power US commercial nuclear reactors.

This prompted us to ask back on March 9 whether Putin would place enriched uranium on the list of banned Russian exports, and why Uranium stocks soared late last week after U.S. Energy Department signaled more aid for current and future nuclear reactors.

One month later, the thorny issue of Russian uranium supply again came to a head when Russia news agency TASS cited deputy prime minister Novak, who said that Russia is considering a ban on Uranium exports, although it never pulled the plug (at least not yet).

Fast forward to today when we now learn that the Biden admin is hoping to remove Russia’s critical leverage to throttle US nuclear power, and is pushing lawmakers to support a $4.3 billion plan to buy enriched uranium directly from domestic producers to wean the US off Russian imports of the nuclear-reactor fuel, according to a person familiar with the matter. Shares of uranium companies surged.

According to Bloomberg, DOE officials met with key congressional staff, where they said such funding – which amounts to one tenth of what the US recently wired to the US military-industrial complex Ukraine – is urgently needed, adding that any interruption in the supply of enriched Russian uranium could cause operational disruptions at commercial nuclear reactors, the person said. US nuclear energy industry participants have also been briefed on the proposal; while the plan requires approval from Congress it is unlikely that lawmakers will refuse these relatively modest demands if the alternative is the threat of widespread blackouts and immediate political career termination.

The proposal, Bloomberg continues, aims to spur development of more domestic enrichment and other steps needed to turn uranium into reactor fuel; It would also create a government buyer directly purchasing enriched uranium, including the type used in a new breed of advanced reactors now under development.

The proposal is dovetails with legislation introduced earlier this year by Senator Joe Manchin, the West Virginia Democrat who serves as a key swing vote, and Senator Jim Risch, an Idaho Republican, that would authorize billions of dollars in funding to increase the country’s domestic uranium enrichment capabilities. Other congressional backers of expanding US enrichment capabilities include Senator John Barrasso, a Wyoming Republican who serves as the top GOPmember of the Energy and Natural Resources Committee.

That said, even with billions in backing, it won’t be easy for the US to jump-start the domestic uranium industry. The country has only one remaining commercial enrichment facility – a New Mexico plant owned by Urenco, a British-German-Dutch consortium.

While the immediate list of companies that would benefit from such a funding boost include Centrus Energy, which is building an enrichment facility in Ohio, and ConverDyn, a joint venture between Honeywell International Inc. and General Atomics that provides uranium conversion services, it is likely that the entire uranium space would move higher as the price of spot uranium will likely soar.

Sure enough, the market reaction was fast and furious, with the broader Uranium space in general and the Global X Uranium ETF in particlar, surging as much as 7% to its highest intraday price in a month on the news. Shares of uranium miners such as Cameco and Energy Fuels also soared with nuclear fuel provider Centrus Energy (LEU).

And while we wait for more details about the plan to emerge so we can pinpoint the biggest beneficiaries, here are some variant perception views from GLJ Research in kneejerk response to the report:

- URANIUM BEAR ARUGMENT: “The announcement today by the US government is just to build more enrichment capacity. Good if you’re LEU. Irrelevant if you’re anyone else. It basically going to all go to the centrifuge project that LEU (odl USEC) has. That was my read of it.”

- RESPONSE FROM URANIUM EXPERT: “That is a completely false statement. If part of this plan is to sanction Russian uranium then LEU will get hit hard right away, as that is their only cash flow. The devil will be in the details, but what this means is that DOE want funding to build a US enrichment capacity which will require at least 10 Million pounds per year of mined U3O8 feed in order to replace Russian enriched uranium. The US doesn’t have that mined capacity in operation so this will be a huge boost to US and Canadian uranium miners. We have no idea based on the news so far whether Centrus will be the one tasked with building enrichment capacity. We need to see the full details of the ask to Congress.”

- URANIUM EXPERT VIEW ON WHAT THIS MEANS FOR PRICES NEAR-TERM: “With SPUT raising a lot of cash today, and already holding nearly $100 Million, there is going to be some big upside in the Spot price over the coming days and weeks. Spot hit $51 today, with is a $5/lb rebound in the past 2 weeks.”

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING// TUESDAY NIGHT

SHANGHAI CLOSED UP 22.03 PTS OR 0.68% //Hang Sang CLOSED UP 482.72 PTS OR 2.24% /The Nikkei closed UP 290.34 OR 1.04% //Australia’s all ordinaires CLOSED UP 0.39% /Chinese yuan (ONSHORE) closed DOWN 6.6892 /Oil UP TO 120.62dollars per barrel for WTI and UP TO 121.62 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6892 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.6923: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1,686 CONTRACTS TO 494,130 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR GAIN OF $7.45 IN GOLD PRICING TUESDAY’S COMEX TRADIN. WE ALSO HAD A FAIR SIZED EFP (1914 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1914 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :1914 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1914 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 803 CONTRACTS IN THAT 1914 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 1111 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR RISE IN PRICE OF GOLD $7.45.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (72.423),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 72.423 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE 7.45) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A SMALL SIZED GAIN OF 0.709 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (72.423 TONNES)…

WE HAD 575 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 228 CONTRACTS OR 22,800 OZ OR 0.709 TONNES

Estimated gold volume 121,218/// poor

final gold volumes/yesterday 128,829 poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 8

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 118,676,299 oz Manfra Brinks Loomis2292 kilobars and 235 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 980 notice(s)98,000 OZ 3.048 TONNES |

| No of oz to be served (notices) | 3304 contracts 330,400 oz 10.276 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,980 notices1,998,000 OZ 62.146 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

3 customer withdrawals:

i) Out of Brinks: 73,690.092 (2292 kilobars)

ii) Out of Loomis: 8198.505 oz (235 kilobars)

iii) Out of Manfra: 37,787.623 oz

total withdrawal: 118,676.220 oz

ADJUSTMENTS: 1 dealer to customer//manfra/

22,474.549 oz//Manfra

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 4284 contracts having LOST 2641 contracts

We had 3680 notices filed on TUESDAY so we GAINED A HUGE 1039 contracts

July has a GAIN OF 120 OI to stand at 2213

August has a LOSS of 674 contracts DOWN to 421,034 contracts

We had 980 notice(s) filed today for 98,000 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 980 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 710 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (19,800) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 4284 CONTRACTS ) minus the number of notices served upon today 980 x 100 oz per contract equals 2,328,400 OZ OR 72.423 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (19,980) x 100 oz+ (4284) OI for the front month minus the number of notices served upon today (980} x 100 oz} which equals 2,328,000 oz standing OR 72.423 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 72.423 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,331,163.529 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,766,209.288 OZ

TOTAL ELIGIBLE GOLD: 16,834,297.804 OZ

TOTAL OF ALL REGISTERED GOLD: 16,834,297.804 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,503,134.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 8

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 500,681.955 oz HSBC Int. Delaware Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,176,020.200 oz CNT JPM |

| No of oz served today (contracts) | 63CONTRACT(S) 315,000 OZ) |

| No of oz to be served (notices) | 57 contracts (285,000 oz) |

| Total monthly oz silver served (contracts) | 1565 contracts 7,825,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposits into the customer account

i) Into CNT: 609,971.700 oz

ii) Into JPMorgan: 565,067.200

total deposit: 1,176,020.200 oz

JPMorgan has a total silver weight: 171.328 million oz/336.714 million =50.87% of comex

Comex withdrawals: 3

i) Out of HSBC 210,714.150 oz

ii) Out of JPMorgan: 94,034.100 oz

iii) Out of Int. Delaware 195,933.705 oz

total withdrawal 500,681.955 oz

1 adjustments:

Manfra: 295,319.371 oz dealer to customer

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72,245 MILLION OZ

TOTAL REG + ELIG. 336.714 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 120 HAVING GAINED 3 CONTRACTS.

WE HAD 0 NOTICES FILED ON TUESDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 7863 CONTRACTS DOWN TO 93,447 CONTRACTS.

AUGUST GAINED 145 CONTRACTS TO STAND AT 897

SEPTEMBER HAD A GAIN OF 8357 CONTRACTS UP TO 39,497 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 63 for 315,000 oz

Comex volumes:58,840// est. volume today// poor

Comex volume: confirmed yesterday: 72,441 contracts ( fair )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1565 x 5,000 oz = 7,825,000 oz

to which we add the difference between the open interest for the front month of JUNE(120) and the number of notices served upon today 63 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1565 (notices served so far) x 5000 oz + OI for front month of JUNE (120) – number of notices served upon today (63) x 5000 oz of silver standing for the JUNE contract month equates 8,110,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1066.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 544.306 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards

Rickards: The Real Reason Why Gold Has Stumbled

WEDNESDAY, JUN 08, 2022 – 11:45 AM

Authored by James Rickards via DailyReckoning.com,

The world has changed radically in recent years. We’ve had the worst pandemic since 1918, and the third worst in world history. We’ve had a global supply chain breakdown. Inflation is the worst since the early 1980s. Europe is experiencing its worst war since the end of World War II.

That kinetic war in Ukraine is accompanied by a financial and economic war between the U.S., the U.K., the EU and Russia that involves extreme financial sanctions, including seizing the central bank reserves of the world’s 11th-largest economy. That financial war and accompanying sanctions have disrupted supply chains on top of the disruptions already present.

And the world’s second-largest economy, China, has locked down 50 million people in Shanghai and Beijing for most of the past two months in a hopeless and misguided effort to suppress COVID. (Note to China: The virus goes where it wants). The list goes on.

If gold is the ultimate safe haven for investors and the world is dangerously unsafe, then the price of gold must be skyrocketing, right?

Gold Has Lost Its Luster

That’s not the case. Today gold is about $1,844 per ounce (that price fluctuates daily and intraday). That’s more than 10% lower than the $2,069 all-time high of Aug. 6, 2020, and 10% below the interim high of $2,043 of this March 8.

The bottom line is, gold is lower today than it was two years ago. It was $1,870 on July 22, 2020 and it’s $1,844 today almost two years later. There have been some spills and thrills along the way including two peaks over $2,000 and several smashes down into the $1,680 range, but always followed by a reversion to a persistent central tendency that hasn’t moved much at all.

So, we’re back to the original question. With inflation, shortages, and war all around and getting worse, why is gold not surging past $2,000 per ounce and making its way to $3,000 and beyond?

Gold Should Be Soaring

Supply/demand conditions favor higher gold prices. Global production of gold has remained fairly constant for the past six years. Over the same six-year period, during a period when global output was flat, central banks increased their official holdings by 6%.

China has added 1,400 metric tonnes in the past twelve years (that’s the official number; unofficially they probably own far more). Russia has acquired 1,500 metric tonnes over that same period.

Other large buyers include Poland, Turkey, Iran, Kazakhstan, Japan, Vietnam and Mexico. Now, central banks in the Visegard Group (Czech Republic, Hungary, Poland and Slovakia) are buying gold.

What’s curious is that individual investors in the U.S. still seem indifferent to gold as a monetary asset. In theory, central banks are the most knowledgeable about the real condition of the global monetary system. If central banks are buying all the gold they can with hard currency (dollars or euros), it’s not clear what retail investors are waiting for.

Of course, central bank holdings are only about 17.5% of total above-ground gold and there is far more demand from bullion investors and for jewelry (a form of wearable wealth). Still, central banks are arguably the most knowledgeable market participants; and their steady increases in gold holdings is meaningful.

Gold Prices Are Tied to Interest Rates

Interest rates are also poised to play a supporting role. Many of the directional moves in gold prices over the past two years have been tied to interest rate moves. The correlation is not perfect, but it is strong.

The rally in gold prices in late 2020 was tied to a fall in interest rates (yield-to-maturity) on the 10-year U.S. Treasury note from 1.930% on December 19, 2019 to 0.508% on July 31, 2020.

Similarly, the fall in gold prices after February 2021 was tied to an increase in interest rates on the 10-year Treasury note from 1.039% on January 2, 2021 to 3.130% on May 2, 2022. After dropping to 2.722% in late May, rates have rebounded to 3.031% as of today.

But I believe that interest rates on the 10-year Treasury note will fall again and will continue to fall as global growth weakens. That’s good news for gold investors.

Short-term rates are going up because of Fed policy, but long-term rates will go down because investors see that the Fed will cause a recession. That correlates with higher gold prices.

While market supply/demand conditions are favorable for gold, and the overall interest rate environment is also favorable for gold, neither seems to have the power needed to push gold solidly past $2,000 in the short run.

What’s the problem?

Look No Further Than the Dollar

The real headwind for gold and the main reason gold has struggled for the past two years is the strong dollar.

After all, the dollar price of gold is really just the inverse of the strength of the dollar. A weaker dollar means a higher dollar price for gold. A stronger dollar means a lower dollar price for gold.

It may seem paradoxical to imagine a strong dollar in the midst of all the inflation we’re seeing. But that’s the case.

What’s extraordinary over the past two years isn’t that gold hasn’t soared; it’s that gold has held its own in the face of a persistently strong dollar. So that leads to the next question:

What’s behind the strong dollar and what could cause the dollar to suddenly weaken and send gold prices into the stratosphere?

The strong dollar has been driven by a demand for dollar-denominated collateral, mostly U.S. Treasury bills, needed as collateral to support leverage on bank balance sheets and in hedge fund derivatives positions.

That high-quality collateral is in short supply (partly because U.S. Treasury issuance is lower due to smaller than expected deficits). As banks scramble for scarce collateral, they need dollars to pay for the Treasury bills. That fuels dollar demand.

The scramble for collateral also speaks to weaker economic growth, fears of default, decreasing creditworthiness of borrowers and fear of a global liquidity crisis. We’re not there yet, but we’re getting close with no relief in sight.

As weak growth turns into a global recession, a new financial panic will be on the horizon. At that point, the dollar itself may cease to be a safe haven, especially given the aggressive use of sanctions by the U.S. and the desire of major economies such as China, Russia, Turkey, and India to avoid the U.S. dollar system if possible.

When this panic hits and the dollar is deemed no longer reliable, the world will turn to gold.

Frustration with the sideways movement of gold prices is understandable. But behind the curtain, a new liquidity crisis is brewing.

Investors should consider today’s prices a gift and perhaps a last chance to acquire gold at these prices before the real safe haven race begins.

Gold is so cheap right now, it’s practically a steal.

END

3. Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke: When money dies all over again

Submitted by admin on Tue, 2022-06-07 14:00Section: Daily Dispatches

2p ET Tuesday, June 7, 2022

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing today at Sprott Money, excerpts some passages from Adam Fergusson’s classic economic history of the 1920s, “When Money Dies” — passages that seem to evoke our own era of infinite money creation.

Hemke’s commentary is headlined “When Money Dies” and is posted at Sprott Money here:

https://www.sprottmoney.com/blog/When-Money-Dies-Craig-Hemke-June-07-2022

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Northwest Territorial Mint fraudsters get years in prison

Submitted by admin on Tue, 2022-06-07 21:43Section: Daily Dispatches

$30 Million in Missing Gold Bars, a Couple on the Lam from the FBI, and a Corgi Nicknamed Nugget: The Inside story of a Precious Metal Ponzi Scheme

By Lukas I. Alpert

MarketWatch, New York

Tuesday, June 7, 2022

A precious metals dealer who recently went on the lam after being convicted in a $30 million Ponzi scheme involving gold and silver bars has been sentenced to 11 years in federal prison.

Bernard Ross Hansen, 61, and his vault manager and girlfriend, Diane Renee Erdmann, 49, were found guilty by a federal jury in July 2021 of defrauding over 3,000, mostly-elderly customers out of more than $30 million in a gold and silver bullion investment scheme.

The pair failed to show up for their original sentencing hearing in April and went on the lam for 11 days before being caught by Federal Bureau of Investigation agents at a motel north of Seattle with three loaded handguns, boxes of collectible coins, and a pet corgi nicknamed Nugget in their car, authorities said.

“Every day he was on the run was one more free day,” investigators say Hansen told them after he was arrested, according to court filings.

The couple finally faced the music Monday, with Hansen receiving an 11-year sentence and Erdmann five years. Hansen was ordered to pay $33.7 million in restitution and Erdmann $32.1 million. …

… For the remainder of the report:

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //FERTILIZER+ OTHERS

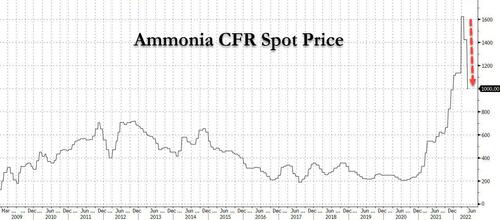

“The Summer Of Starvation”: Soaring Fertilizer Prices Unleash Chaos, Hunger Worldwide

WEDNESDAY, JUN 08, 2022 – 03:44 PM

One of the most pernicious consequences – if primarily for the anti-Russia west – resulting from the Ukraine war, has been the unprecedented spike in fertilizer prices which among other things, has sparked a historic surge in food prices and collapse in supply chains around the globe, as we discussed in these articles published over the past few months:

- Fertilizer Prices Hit Record Highs, May Pressure Food Inflation Even Higher

- “Fertilizer Is Out Of Control” – US Farmers Ditch Corn For Soy To Save On Costs

- Poop-Boom: Manure Supplies Tighten As Fertilizer Prices Soar

- World’s Largest Fertilizer Company Warns Crop Nutrient Disruptions Through 2023

Fast forwarding to today, when we have some good, some bad and some pretty terrible news. The good news it that fertilizer prices have eased modestly from all time highs, as the following chart of Tampa Ammonia CFR spot prices shows.

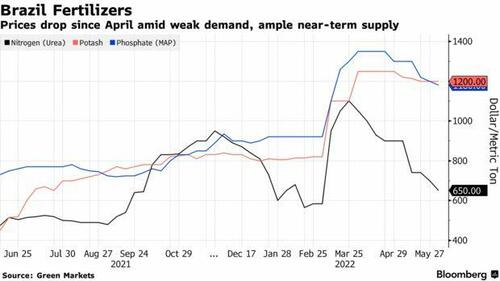

The bad news is that the the price hasn’t dropped nearly enough: according to Bloomberg, the glut of fertilizers piling up at the biggest Brazilian ports signals that the price of the nutrients has to drop further before farmers start buying.

In Paranagua, private warehouses reached their maximum storage capacity of 3.5 million tons, Luiz Teixeira da Silva, Paranagua’s operations director told Bloomberg. A terminal operated by VLI Logistics, one of the two at Santos port that store fertilizers, is also full, according to people with knowledge of the matter who asked not to be named as the information isn’t public.

As noted above, the price of fertilizers across the globe has exploded to unprecedented levels, and Brazil has been no exception.

That’s a problem because the agriculture-heavy country and food-source for half the globe, imports nearly 85% of its fertilizer and Russia is the main origin. As supplies have normalized, prices have declined over the past weeks, but farmers still aren’t buying. They are waiting for further price cuts, according to Marina Cavalcante, an analyst at Bloomberg’s Green Markets.

“Farmers have the expectation that prices will keep falling after declines last week and in the previous one,” she said. “So they’ll wait for further decreases to buy.”

And here is an example in supply/demand game theory: Brazil is the world’s biggest shipper of several crops, including soybeans. Farmers can delay their purchases until the eve of the soybean seeding in September. But if they all wait too long, a last-minute rush could lead to inland transportation bottlenecks that may leave some of them empty-handed anyway.

There is another problem: there just may not be enough actual fertilizer coming out of Russia, which has decided to punish the world by sending food prices for western nations to record highs and spark social unrest in the process. After all, the biggest reason prices are so high is because there is just not enough supply. And while speculators may have pushed prices somewhat higher than they should be, any farmers hoping that prices will fully renormalize will be disappointed.

Which leaves us with “demand destruction”, only as Rabobank’s Michael Every reminds us, when it comes to food “demand destruction” – especially at poor, third world countries – it has a different, less pleasant name: starvation.

Consider what is going on in Chad: as DW reports, Africa’s fifth-largest country declared a food emergency due to a lack of grain supplies. The landlocked African nation on Thursday urged the international community to help its population cope with rising food insecurity.

Cereal prices across Africa surged because of the slump in exports from Ukraine — a consequence of the war in Ukraine and a raft of international sanctions on Russia which have disrupted supplies of fertilizer, wheat and other commodities from both Russia and Ukraine.

DW spoke with one couple in Chad who are dealing with the effects of collapsing food supplies:

Cedric Toralta and Anne Non-Assoum live in the Boutalbagar neighborhood of Chad’s capital, N’Djamena. Non-Assoum — who had just returned from the market — expressed her dissatisfaction with rising food prices.

”Look what I bought: Here is meat for 1,500 CFA francs ($2.45, €2.28), rice for 1,000 and spices for 600 — that’s more than 3,000 CFA francs only for lunch for four people,” she said.

She told DW that in the past, the same purchase would have cost around 2,000 CFA francs. “My husband and I spent 60,000 CFA a month on food, but now, even 90,000 is not enough!”

The dire situation has forced Toralta to take drastic nutrition measures that are not without consequences.

“We can’t make ends meet, even though I decided to increase our food ration by 30,000 CFA francs. So I’m forced to reduce the amount we eat every day — and you see it’s affecting the children,” Toralta told DW.

”We need urgent food aid for the population,” Non-Assoum said, stressing the urgency. “If even the middle-income population in the capital can’t cope with this situation, how can the rural population? It’s very complicated, and we need the international community to help us.”

The prices of basic necessities have also risen significantly in Chad’s neighbor to the northwest, Niger. Milk, sugar, oil and flour are the products whose prices have skyrocketed there. The cost of fertilizer has also increased dramatically.

At a recent meeting with Russian President Vladimir Putin, the African Union chairperson, Macky Sall, said the continent was bearing the brunt of the war in Ukraine due to a shortage of grain and fertilizer.

As a report from the ground (not from a well-fed Western journalist working from home) puts it: “In the village of Falke, some 665km (413 miles) from the capital Niamey, Tassiou Adamou, a farmer, told DW that this year’s harvest will likely be poor because producers cannot afford to buy enough fertilizer.

“Groundnuts, which are our main cash crop, need fertilizer,” Adamou pointed out. “Until last season, a bag of fertilizer cost 17,000 CFA francs. This year, it has reached 30,000,” he said, adding that it is impossible to produce much for those in the countryside.

“If you used to use three bags of fertilizer for your field, today, you can only have one bag with the same amount. Where you used to harvest 50 bunches of millet, you can barely produce 30 bunches without fertilizer.”

Much of Africa, Every writes, is in the same boat… and it is rapidly sinking, and the irony is that everyone needs much more fertilizer now to avoid a global food crisis, yet they either can’t afford it, or are hoping it falls some more in price. Unfortunately, that will not happen and instead marginal buyers will keep pushing the scarce commodity.

What happens next? We give the mic to Every, who summarized the current debacle best: “the global rich, who set rates, have to decide if they will sacrifice their asset prices to help the global poor eat. If we won’t say that, can we at least say that we have a choice between putting calories in rich people’s cars or in poor people’s mouths?”

To conclude, markets say “demand destruction”, but won’t say it can mean “mass starvation”. Some are now able to say “stagflation”, but many in markets weren’t allowed to until recently. Some can say “recession”, but many in markets and politics still aren’t allowed to. Yet nobody wants to say “depression” because there is *still* the assumption that, bad as things are, somehow a ‘hockey-stick’ bounce lies on the other side. Not sticks, stones, burning torches, and pitchforks.

Here, some may argue that “torches and pitchforks” is a euphemism, but put several hundred million people on food “demand destruction” for a few weeks, and watch as the next Arab Spring won’t be “Arab” and won’t be in the spring: it will be a Global Summer of starvation.

END

END

END

COMMODITIES IN GENERAL/

END

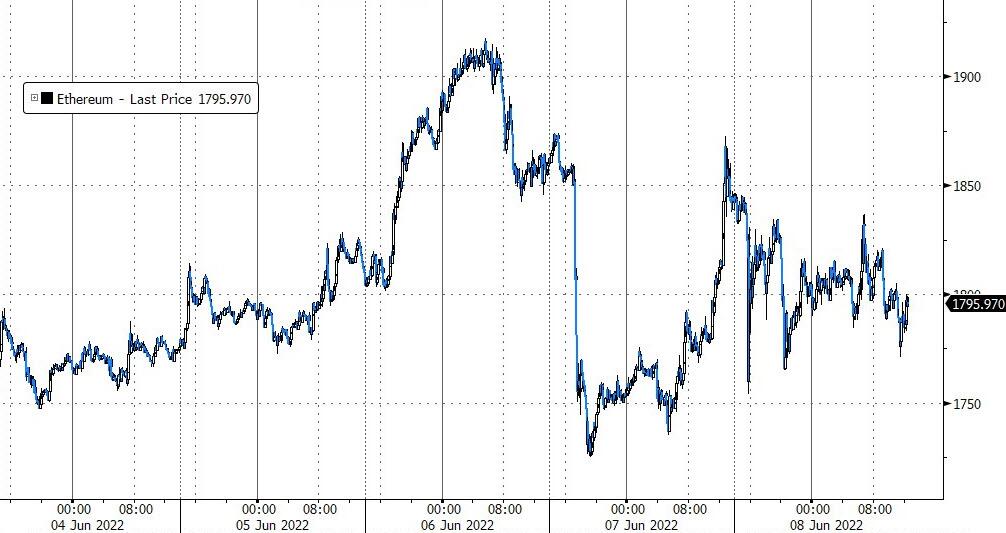

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings WEDNESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6892

OFFSHORE YUAN: 6.6923

HANG SANG CLOSED UP 482.72 PTS OR 2.24%

2. Nikkei closed UP 290.34% OR 1.04%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 102.38/Euro RISES TO 1.0731

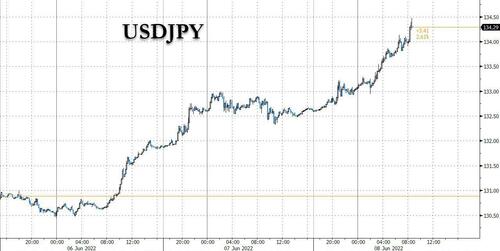

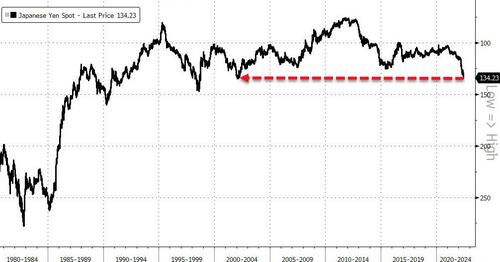

3b Japan 10 YR bond yield: RISES TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.31/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

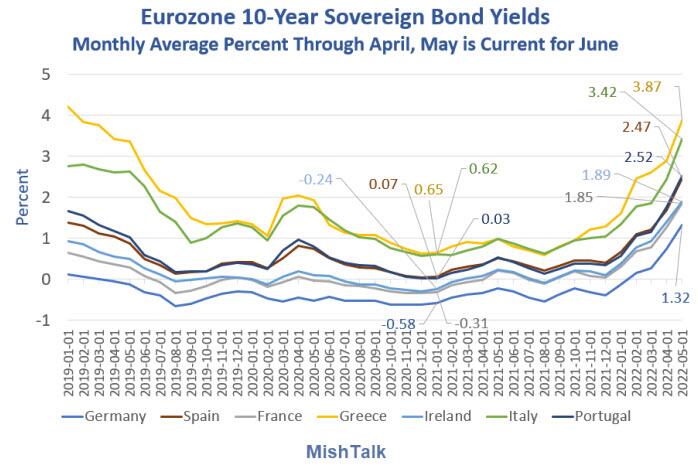

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +1.258%/Italian 10 Yr bond yield RISES to 3.34% /SPAIN 10 YR BOND YIELD FALLS TO 2.40%…

3i Greek 10 year bond yield RISES TO 3.86

3j Gold at $1852.05 silver at: 22.00 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1.10 roubles/dollar; ROUBLE AT 59.94

3m oil into the 120 dollar handle for WTI and 1121 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 133.91DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9764– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0475well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.007 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 3.155 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.17

Futures Drop As Yields Push Higher, Hawkish ECB Looms

WEDNESDAY, JUN 08, 2022 – 08:09 AM

After yesterday’s bizarro rally, US futures and European bourses dipped ending two days of gains, as yields reversed Tuesday’s slide and climbed ahead of highly anticipated CPI data on Friday and a hawkish ECB meeting tomorrow, as traders try to predict the Federal Reserve’s policy path. Nasdaq 100 futures were flat at 7:30 a.m. in New York, with contracts on the S&P 500 and Dow Jones also modestly lower. European markets also dipped, with Credit Suisse shares tumbling after the Swiss bank announced that it expects a loss in the 2Q and is weighing a fresh round of job cuts. Meanwhile, Asian stocks rose as Beijing’s move to approve a slew of new video games bolstered bets that the outlook is improving for the Chinese technology sector. The yield on the 10-year US Treasury resumed its advance, climbing to 3%, while the dollar rose as the yen cratered to fresh 20 year lows, flat and bitcoin traded around $30K again.

Among notable premarket movers, energy companies’ extended their Tuesday gains with Imperial Petroleum rising 8.3% and Energy Focus adding 20%. Western Digital shares climbed 4.1% in US premarket trading after the chipmaker said that it’ll consider splitting its main units as part of a review of “strategic alternatives” following talks with activist investor Elliott. US-listed Chinese stocks jump in premarket trading, on track for a third day of gains, after China approved a second batch of video games this year, providing a signal of policy support to the the country’s internet sector; Alibaba (BABA US) gained 5.8%, JD.com (JD US) +4.4%, Pinduoduo (PDD US) +5.9%, Baidu (BIDU US) +2.7%. Other notable premarket movers:

- Intel (INTC US) shares fell 1.9% in premarket trading as Citi lowered its estimates on the chipmaker after the company’s management mentioned at a conference that circumstances are worse than expected during the quarter.

- Altria Group (MO US) stock slid 2.4% in premarket trading as Morgan Stanley downgraded it to underweight, citing increasing macro pressures and competitive risks.

- Western Digital (WDC US) shares rise 4.1% in premarket trading, after the chipmaker said that it will consider splitting its main units as part of a review of “strategic alternatives”.

- Smartsheet (SMAR US) stock fell about 7% in premarket trading as analysts said the software company delivered a mixed set of results with billings growth decelerating to top estimates by a slimmer margin than in previous quarters.

- Novavax (NVAX US) shares jump as much as 22% in US premarket trading after the company’s coronavirus vaccine won support from an FDA advisory panel.

- DBV Technologies ADRs (DBVT US) gain as much as 22% in US premarket trading after a trial for the biotech firm’s peanut allergy treatment met its primary endpoint.

Sentiment remains fragile on concerns rising rates will spark a recession as corporate earnings are set to slide. Thursday the ECB is set to wind down trillions of euros of asset purchases in a prelude to a rate hike expected in July that will mark the end of eight years of negative interest rates. “Higher yields will inevitably resume the pressure on valuations,” said Roger Lee, head of UK equity strategy at Investec Bank.

Inflation now exceeds 8% in the euro area, and is expected to stay above that level in the US when May data comes out on Friday, increasing pressure on central banks to stick to aggressive rate hikes. “Recent bouts of optimism can only be short-lived for now, as they were based on the wrong assumptions, that lower growth would push central bankers to ease their aggressive path,” Olivier Marciot, a portfolio manager at Unigestion SA, wrote in a report. Yet some argue that central banks will be forced back into dovish mode, among them hedge fund founder Ray Dalio. The billionaire said central banks across the globe will be required to cut interest rates in 2024 after a period of stagflation.

On Friday, focus will turn to the US CPI reading for hints on the Fed’s tightening path following the central bank’s outsized hike on May 4. The data is expected to show inflation picked up from a month ago, but slightly slowed from a year earlier. Complicating the task of policy makers trying to arrest runaway inflation without choking off growth, the war in Ukraine shows no signs of ending. That’s ignited higher food and energy prices across the world, despite the best efforts of central banks to use higher rates to cool economies.

In Europe, the Stoxx 600 Index was down 0.4%, with shares of basic resources companies and financial sector stocks leading the drop, while the region’s bonds fell as traders braced for a crucial European Central Bank meeting. Credit Suisse shares tumbled as much as 7.6% after the Swiss bank announced that it expects a loss in the 2Q. In addition, people familiar with the matter said that the lender is weighing a fresh round of job cuts. European mining stocks also underperformed the Stoxx 600 benchmark as copper declines, while iron ore fluctuates with investors weighing signs of demand recovery against caution that China may seek to stabilize commodity prices. The Stoxx Europe 600 Basic Resources sub-index slid 1.1% as of 9:45 a.m. in London after rising to the highest since April on Tuesday. Here are the most notable European movers:

- Prosus’s shares jump as much as 8.6% in Amsterdam trading after China approved its second batch of video games this year, with a total of 60 titles.

- Naspers, which holds a 29% stake in Tencent through Prosus, up as much as 9.8%.

- Inditex shares gain as much as 5.3% after the Zara owner reported 1Q results. Analysts were impressed by the sales beat, with Bryan Garnier calling the company a “safe-haven choice” in the retail sector.

- UK and European retail stocks rise after Inditex’s results helped boost sentiment, with the retail segment the biggest gainer in the Stoxx 600 Index. Asos gained as much as +3.9%, Boohoo +3.1%, JD Sports +2.5%.

- Voestalpine shares rise as much as 4.5% after the company reported strong results for the business year, even as its guidance for FY23 points at a lack of visibility for fiscal 2H, according to analysts.

- Haldex shares rise as much as 45% after SAF-Holland offers SEK66 in cash per share for the Swedish brake and air suspension products maker, representing a 46.5% premium to its closing price on Tuesday.

- Wizz Air shares fall as much as 8.6% after the company reported results that were in line with expectations but flagged an operating loss for the 1Q of fiscal year 2023.

- European mining stocks underperform the Stoxx 600 benchmark as copper declines, while iron ore fluctuates. Anglo American shares fell as much as 1.7%, Rio Tinto -1.8%, Glencore -1.7%, Antofagasta -3.3%.

- Orpea shares declined as much as 5.9% as the company said that French police investigators began an evidence-gathering raid on Wednesday at its headquarters.

Asian stocks rose as Beijing’s move to approve a slew of new video games bolstered bets that the outlook is improving for the Chinese technology sector. The MSCI Asia Pacific Index advanced as much as 1.1%, with Alibaba and Tencent providing the biggest boosts. Benchmarks in Hong Kong outperformed on the approvals news, while Japanese equities climbed as the yen continued to weaken. Stocks in India fell after the country’s central bank raised interest rates as expected while Thai shares inched up after the Bank of Thailand kept its benchmark rate unchanged. China approved more games in a step toward normalization after a months-long freeze amid the government’s crackdowns on the tech sector. The news follows a report earlier this week that regulators are preparing to conclude an investigation of ride-hailing giant Didi.

“We think the significant dangers have passed” in Chinese equities markets, said Eric Schiffer, chief executive officer at California-based private equity firm Patriarch Organization, which holds positions in Alibaba and JD. “The approval on the game titles signals that policymakers are following through on their intention to back off tech regulation and reverse the pain that caused investors to leave the sector.” Optimism toward a less-harsh regulatory environment and China’s post-Covid economic reopening has helped Hong Kong’s tech stocks outperform US peers recently. The Hang Seng Tech Index is up more than 17% the past month compared with little change in the Nasdaq 100. The rebound in Chinese equities also helped the MSCI Asia Pacific Index stage a bigger recovery than the S&P 500 in the same period.

Japanese equities advanced for a fourth straight day, as the yen’s weakness provided support for the nation’s exporters. The Topix rose 1.2% to 1,969.98 as of market close, while the Nikkei advanced 1% to 28,234.29. Toyota Motor Corp. contributed the most to the Topix gain, increasing 1.8%. Out of 2,170 shares in the index, 1,646 rose and 435 fell, while 89 were unchanged.

Stocks in India declined as the Reserve Bank of India said it would withdraw pandemic-era accommodation to quell inflation after raising borrowing costs for a second straight month. The S&P BSE Sensex dropped 0.4% to 54,893.84, as of 2:46 p.m. in Mumbai, while the NSE Nifty 50 Index fell 0.6%. Both gauges erased gains of as much as 0.8% reached during the central bank’s briefing and are heading for a fourth day of declines. Of 30 shares in the Sensex, 13 rose and 17 fell. Sustained high prices could unhinge inflationary expectations and trigger second-round effects, central bank Governor Shaktikanta Das said in an online briefing, emphasizing that preserving price stability is key to ensuring lasting economic growth. Reliance Industries was the biggest drag on the Sensex, while State Bank of India gave the biggest boost. All except two of BSE’s 19 sector sub-gauges declined, with telecom and energy groups the worst performers as realty and metals gained

In FX, Yen weakness extends in European trade, with JPY hitting the weakest level since 2002 at 133.77/USD after BOJ’s Kuroda reiterated easing stance. The dollar strengthened against all its group-of-10 peers with the yen and Australian and New Zealand dollars as the worst performers. The euro fluctuated around the $1.07 handle while bunds and Italian bonds fell alongside Treasuries, paring some of Tuesday’s gains. Australian and New Zealand dollars both weakened amid greenback strength and falling US stock futures. Aussie further was weighed by local yields giving up Tuesday’s RBA-driven gains.

In rates, Treasuries drifted lower, giving back a portion of Tuesday’s gains and following bigger losses for bunds, which underperformed ahead of Thursday’s ECB policy meeting. Yields are cheaper by 2bp-3bp across the curve with front-end marginally outperforming, steepening 2s10s spread by ~1.5bp and building curve concession for the auction; bunds underperform by 1.5bp in 10-year sector. Focal points of US session include 10-year auction, following soft results for Tuesday’s 3-year. $33b 10-year reopening at 1pm ET is second of this week’s three auctions; $19b 30-year reopening is ahead Thursday. WI 10-year yield ~3.015% is above auction stops since 2011 and ~7bp cheaper than May’s, which tailed by 1.4bp. JGBs little changed, with benchmark 10-year bonds trading again after no transactions on Tuesday. Peripheral spreads widen to Germany; Italy lags, widening ~3bps to core at the 10y points ahead of the ECB on Thursday.

In commodities, WTI drifts 0.6% higher to trade at around $120. Most base metals are in the green; LME tin rises 2.8%, outperforming peers. Spot gold falls roughly $5 to trade at $1,848/oz.

Looking at To the day ahead now, and it’s a fairly quiet one on the calendar, but data releases include German industrial production and Italian retail sales for April, as well as the UK construction PMI for May and the final reading of US wholesale inventories for April.

Market Snapshot

- S&P 500 futures down 0.4% to 4,144.00

- STOXX Europe 600 down 0.3% to 441.39

- MXAP up 0.8% to 169.14

- MXAPJ up 1.1% to 559.98

- Nikkei up 1.0% to 28,234.29

- Topix up 1.2% to 1,969.98

- Hang Seng Index up 2.2% to 22,014.59

- Shanghai Composite up 0.7% to 3,263.79

- Sensex down 0.4% to 54,907.55

- Australia S&P/ASX 200 up 0.4% to 7,121.10

- Kospi little changed at 2,626.15

- Brent Futures up 0.3% to $120.92/bbl

- Gold spot down 0.3% to $1,847.71

- U.S. Dollar Index up 0.34% to 102.67

- German 10Y yield little changed at 1.33%

- Euro down 0.2% to $1.0686

Top Overnight News from Bloomberg

- Boris Johnson plans to press ahead with legislation giving him the power to override parts of the Brexit deal, three people familiar with the matter said, a move likely to anger some of his MPs and the EU

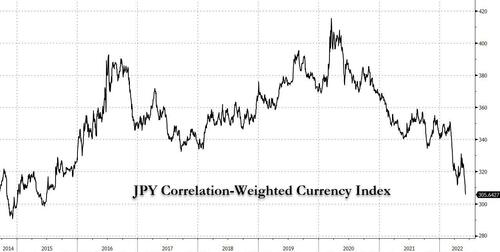

- The yen’s historic weakness is spreading from the dollar into other currency crosses as the Bank of Japan’s policy isolation grows. Bloomberg’s Correlation-Weighted Currency Index for the yen — a gauge of its relative strength against a broad basket of Group-of-10 peers — slumped to a seven-year low Wednesday

- Japanese investors sold US Treasuries for the sixth consecutive month in April, underscoring waning appetite for the securities as the Federal Reserve sticks to its aggressive monetary tightening path

- Inflation in Hungary exceeded 10% for the first time in more than 20 years, putting pressure on the central bank to tighten monetary policy further and prop up the forint

- Australian inflation is likely to breach 6% and potentially could go “well above” that level and remain there for the rest of the year, Secretary to the Treasury Steven Kennedy said Wednesday

- Economists and investors criticized Australia’s central bank for confusing communications after it raised interest rates by twice as much as expected, having previously signaled a preference for quarter-point moves

- The RBI delivered a 50 basis-point rate hike as predicted by 17 of 41 economists in a Bloomberg survey

- A slew of China video game approvals is giving stock bulls renewed hope that a nascent rebound in tech shares could become a sustainable rally. The Hang Seng Tech Index jumped more than 4% Wednesday after the government approved 60 licenses

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly higher following the gains on Wall St and optimism of China easing its tech crackdown. ASX 200 recovered from the prior day’s RBA-induced selling with nearly all sectors in the green, although financials underperformed. Nikkei 225 extended further above the 28k level on currency weakness and with Q1 GDP data revised upwards to a narrower contraction. Hang Seng and Shanghai Comp. traded mixed with tech fuelling the gains in Hong Kong after China’s NPPA approved the publishing licences for 60 games this month, while sentiment in the mainland gradually soured despite support efforts as an official also warned that China’s foreign trade stabilisation faces uncertainties and large pressure.

Top Asian News

- China Vice Commerce Minister Wang said China’s foreign trade stabilisation faces uncertainties and a large pressure from domestic and external factors. Furthermore, he sees global demand growth as low, while he added that China will accelerate export tax rebates and MOFCOM will assist foreign trade companies in securing orders, according to Reuters.

- Chinese Retail Passenger Car Sales (May) +30% M/M, according to PCA’s Prelim data cited by Bloomberg.

- Japan’s CDP has, as expected, submitted a no-confidence motion against the governing administration within the Lower House, motion will be put to a vote on June 9th, via Asahi; Asahi adds that the move is not expected to go anywhere

European bourses have trimmed initial upside, Euro Stoxx 50 -0.2%, with macro newsflow limited and the initial strength primarily a continuation of APAC/Wall St. leads. In specifics, Credit Suisse (-5%) issued a Q2 profit warning for the group and its Investment Bank division while noted Retail name Inditex (+4%) provided a positive update. Stateside, futures are modestly pressured overall but well within overnight ranges ahead of a slim docket; ES -0.4%. DiDi (DIDI) is in advanced discussions to own a one-third stake of Sinomach Zhijun, a China state-backed EV maker, according to Reuters sources.

Top European News

- Euro-Zone Economy Grew More Than Estimated at Start of Year

- Even the ECB’s Most Dire Forecast May Have Been Too Optimistic

- Euro Options Point to Most-Pivotal ECB Meeting Since 2019

- Ireland Accuses Johnson of Acting in ‘Bad Faith’ on Brexit Deal

- Saudi Wealth Fund Makes Second $1 Billion Bet on Swedish Gaming

Central banks

- RBI hiked the Repurchase Rate by 50bps to 4.90% (exp. 40bps hike) via unanimous decision and dropped mention of “staying accommodative”, while RBI Governor Das noted that inflation has increased above upper tolerance levels and they remain focused on bringing down inflation. Das added they will control inflation without losing sight of growth and that further monetary policy measures are necessary to anchor inflation, as well as noted that upside risk to inflation had intensified and materialised sooner than expected.

- RBI Governor says they dropped the word “accommodative” from their stance, but they remain accommodative; liquidity withdrawal going forward will be calibrated and gradual.

- BoJ’s Kuroda says rapid weakening of JPY as seen recently is undesirable; various macroeconomic models show that a weak JPY is positive. I It is important for FX to move stably, reflecting fundamentals.

- BoJ is expected to maintain its view that the domestic economy is picking up as a trend and will likely continue improving, according to Reuters sources.

- PBoC international department official Zhou said the PBoC will keep guiding financing costs lower, while the PBoC also announced that China will extend the trading hours of the interbank FX market, according to Reuters.

FX

- Buck bounces as Yen rout continues after soft verbal intervention from BoJ Governor and Japanese Economy Minister; DXY back around 102.500 axis, USD.JPY climbs to circa 133.86 at one stage.

- More Lira depreciation on multiple negative factors including unconventional easing policy stance aimed at returning inflation to target, USD/TRY touches 17.1500.

- Aussie and Kiwi undermined by Greenback rebound and fade in general risk sentiment; AUD/USD loses 0.7200+ status again, NZD/USD sub-0.6450.

- Franc and Pound down, but Euro and Loonie resilient as former awaits ECB and latter leans on strong crude prices; USD/CHF just shy of 0.9790, Cable under 1.2550, EUR/USD probing 1.0700 and USD/CAD pivoting 1.2550.

- Forint and Zloty underpinned post-strong Hungarian CPI metrics and pre-NBP that is expected to hike 75bp; EUR/HUF & EUR/PLN around 389.60 and 4.5700 respectively.

Fixed Income

- Bunds and Gilts pare some losses after testing round and half round number levels at 149.00 and 114.50 respectively, with added incentive after solid demand for 10 year German and UK supply.

- US Treasuries await 2032 issuance with caution given a lukewarm reception at 3 year auction.

- 10 year note just off base of 118-03/13 overnight range.

Commodities

- WTI and Brent have been moving in-line with broader risk; however, following the UAE Minister the benchmarks have extended to the upside and post gains in excess of USD 1.50/bbl.

- US Energy Inventory Data (bbls): Crude +1.8mln (exp. -1.9mln), Cushing -1.8mln, Gasoline +1.8mln (exp. +1.1mln), Distillates +3.4mln (exp. +1.1mln)

- Brazilian government is considering measures to monitor fuel prices at distributors, according to Reuters sources.

- UAE Energy Minister says situation is not encouraging when it comes to the amounts of crude OPEC+ can bring to the market, via Reuters; Notes conformity with the OPEC+ deal is more than 200%, are risks when China is back, in talks with Germany and other nations to see if they are interested in UAE natgas.

- Spot gold is essentially unchanged, and continues to pivot its 10-DMA, while base metals are primarily tracking broader risk sentiment.

US Event Calendar

- 07:00: June MBA Mortgage Applications -6.5%, prior -2.3%

- 10:00: April Wholesale Trade Sales MoM, prior 1.7%

- 10:00: April Wholesale Inventories MoM, est. 2.1%, prior 2.1%

DB’s Henry Allen concludes the overnight wrap

A reminder that Jim’s annual default study was released yesterday. His view is that while nothing much will change for the remainder of 2022, we might be coming to the end of the ultra-low default world discussed in previous editions. First, there’ll likely be a cyclical US recession to address in 2023, and after that, a risk that various trends reverse that have made the last 20 years so subdued for defaults. See the report here for more details.