JUNE 7 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1849.20 UP $7.45

SILVER: $22.15 UP $.06

ACCESS MARKET: GOLD $1852.00

SILVER: $22.26

Bitcoin morning price: $29464 DOWN 1853

Bitcoin: afternoon price: $30,193 DOWN 1124

GOLD; $1847.60

Platinum price: closing DOWN $17.60 to $1012.20

Palladium price; closing DOWN $21.80 at $1983.40

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:

no. of contracts issued by JPMorgan: 2196/3680

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,839.200000000 USD

INTENT DATE: 06/06/2022 DELIVERY DATE: 06/08/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 71

118 H MACQUARIE FUT 105

323 C HSBC 147

323 H HSBC 499

332 H STANDARD CHARTE 66

363 H WELLS FARGO SEC 102

435 H SCOTIA CAPITAL 59

624 H BOFA SECURITIES 183

657 C MORGAN STANLEY 1

661 C JP MORGAN 3671 2196

686 C STONEX FINANCIA 23

690 C ABN AMRO 23

700 C UBS 92

709 H BARCLAYS 60

732 C RBC CAP MARKETS 11

800 C MAREX SPEC 3 14

905 C ADM 5 29

TOTAL: 3,680 3,680

MONTH TO DATE: 19,000

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 3680 NOTICE(S) FOR 368,000 Oz//11.4463 TONNES)

total notices so far: 19,000 contracts for 1,900,000 oz (59.097 tonnes)

SILVER NOTICES:

0 NOTICE(S) FILED 10 OZ/

total number of notices filed so far this month 1502 : for 7,510,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $7.45

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.97 TONNES FROM THE GLD

INVENTORY RESTS AT 1063.07 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 6 CENTS

AT THE SLV// A BIG CHANGE IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER IVWENTORY AT THE SLV.: A HUGE WITHDRAWAL OF 2.861 MILLION OZ FROMTHE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.306 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 1305 CONTRACTS TO 147,401 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE GAIN IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.20 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.20) AND ALSO UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A TINY NET LOSS OF194 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 2 CONTRACTS OR 10,000 OZ//NEW STANDING: 8,095,000 / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : +3

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 5 days, total 5,121, contracts: 25.605 million oz OR 5.121 MILLION OZ PER DAY. (1024CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 5.121 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 5.121 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1305 WITH OUR STRONG $0.20 GAIN IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 560 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 10,000 E.F.P JUMP TO LONDON//NEW STANDING:8.095 // .. WE HAD A VERY STRONG SIZED GAIN OF 1865 OI CONTRACTS ON THE TWO EXCHANGES FOR 9.325 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 0 NOTICES FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2626 CONTRACTS TO 495,816 AND FURTHER FROM NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -698 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE LOSS IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $5.85//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 4100 OZ QUEUE JUMP//NEW STANDING: 69.191 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $5.85 WITH RESPECT TO MONDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 5129 OI CONTRACTS 15.95 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7755 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 495,816

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5129, WITH 2626 CONTRACTS DECREASED AT THE COMEX AND 7755 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5827 CONTRACTS OR 18.124 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7755) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2626,): TOTAL GAIN IN THE TWO EXCHANGES 5129 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 4100 OZ//NEW STANDING:69.191 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

22,053 CONTRACTS OR 2,205,300 OZ OR 68.59 TONNES 5 TRADING DAY(S) AND THUS AVERAGING: 4410 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES: 68.59 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 68.59/3550 x 100% TONNES 1.94% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 68.59 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A STRONG SIZED 1305 CONTRACT OI TO 147,401 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 560 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 560 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1305 CONTRACTS AND ADD TO THE 560 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 1865 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 9.325 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.20 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 5.39 PTS OR 0.17% //Hang Sang CLOSED DOWN 122.23 PTS OR 0.54% /The Nikkei closed UP 28.06 OR 0.10% //Australia’s all ordinaires CLOSED DOWN 1.54%% /Chinese yuan (ONSHORE) closed DOWN 6.6708 /Oil UP TO 118.03dollars per barrel for WTI and UP TO 119.19 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6708 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6752: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 12626 CONTRACTS TO 495,816 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $5.85 IN GOLD PRICING MONDAY’S COMEX TRADING. WE NOW DOUBT HAD OUR SPREADER //TAS OPERATION IN FULL SWING ON FRIDAY. WE ALSO HAD A FAIR SIZED EFP (1991 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 7755 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :7755 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7755 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5,129CONTRACTS IN THAT 7755 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 12626 CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $5.85.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (69.191),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 69.191 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $5.85) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A GOOD SIZED GAIN OF 15.95 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (69.191 TONNES)…

WE HAD 698 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5,129 CONTRACTS OR 512900 OZ OR 15.95 TONNES

Estimated gold volume 113,715/// poor

final gold volumes/yesterday 112,039 poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 7

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 142,615.830 oz Brinks Loomis 2436 kilobars and 2000 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 3680 notice(s) 368,000 OZ 11.4463 TONNES |

| No of oz to be served (notices) | 3245 contracts 324,500 oz 10.09 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,000 notices 1,900,000 OZ 59.097 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

dealer deposits 0

total dealer deposit 0 oz//

No dealer withdrawals

0 customer deposits

total deposits: nil oz

12 customer withdrawals:

i) Out of Brinks: 78,319.830 (2436 kilobars)

ii) Out of Loomis: 64,296.000 oz (2,000 kilobars)

total withdrawal: 142,615.830 oz

ADJUSTMENTS: 2 dealer to customer//manfra/

23.438.079 oz//Manfra

5894.389 oz JPMorgan

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 6925 contracts having LOST 574 contracts

We had 615 notices filed on MONDAY so we GAINED 41 contracts

July has a GAIN OF 21 OI to stand at 2093

August has a LOSS of 2093 contracts DOWN to 421,708 contracts

We had 3680 notice(s) filed today for 368,000 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 3671 notices were issued from their client or customer account. The total of all issuance by all participants equate to 3680 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2196 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (19,000) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 6925 CONTRACTS ) minus the number of notices served upon today 3680 x 100 oz per contract equals 2,2245,000 OZ OR 69.191 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (19,000) x 100 oz+ (6925) OI for the front month minus the number of notices served upon today (3680} x 100 oz} which equals 2,224,500 oz standing OR 69.191 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 69.191 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,210,073.763 oz

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,894.885.508 OZ

TOTAL ELIGIBLE GOLD: 16,930,500.475 OZ

TOTAL OF ALL REGISTERED GOLD: 17,954,383.033 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,744,310.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 7

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,292,439.047 oz JPM CNT |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 436,865.146 oz Delaware |

| No of oz served today (contracts) | 0CONTRACT(S) nil OZ) |

| No of oz to be served (notices) | 117 contracts (585,000 oz) |

| Total monthly oz silver served (contracts) | 1502 contracts 7,510,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) zero dealer deposits And now for the wild silver comex results

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into Delaware: 436,865.146 oz

total deposit: 436,865.146 oz

JPMorgan has a total silver weight: 171.057 million oz/336.038 million =50.92% of comex

Comex withdrawals: 2

i) Out of CNT 712,583,447 oz

ii) Out of JPMorgan: 579,855.600 oz

total withdrawal 1,292,439.047 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72,453 MILLION OZ

TOTAL REG + ELIG. 336.038 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 117 HAVING LOST 29 CONTRACTS.

WE HAD 27 NOTICES FILED ON MONDAY SO WE LOST 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL NOT STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 1901 CONTRACTS DOWN TO 101,310 CONTRACTS.

AUGUST GAINED 142 CONTRACTS TO STAND AT 752

SEPTEMBER HAD A GAIN OF 3220 CONTRACTS UP TO 31,140 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes:68,679// est. volume today// poor

Comex volume: confirmed yesterday: 57,071 contracts ( poor )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1510 x 5,000 oz = 7,510,000 oz

to which we add the difference between the open interest for the front month of JUNE(117) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1510 (notices served so far) x 5000 oz + OI for front month of JUNE (17) – number of notices served upon today (0) x 5000 oz of silver standing for the JUNE contract month equates 8,095,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1066.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.167 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 547.167 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peter Schiff: America Has Never Been In A Weaker Position To Fight Inflation

TUESDAY, JUN 07, 2022 – 12:40 PM

Federal Reserve Chairman Jerome Powell, President Biden and other government officials insist the US economy is in a strong position to handle an inflation fight. In his podcast, Peter Schiff explains why they are wrong. In fact, America has never been in a weaker position to take on an inflation fight.

There are a lot of people already claiming inflation has peaked and that the Federal Reserve is winning the war against inflation. But on what evidence?

Certainly, just looking at the price of oil, we’ve done nothing to combat inflation. In fact, if you look at actual evidence that’s out there, we are further behind the inflation curve than we were when the Fed began its fight. And that’s because it’s a fake fight. The Fed is talking, but they’re not acting. They’re dragging their feet on both rate hikes and quantitative tightening.”

There is some evidence that the central bank may have finally started trying to shrink its balance sheet. We saw a slight drop in total assets held by the Fed in April. But how long can it keep up quantitative tightening?

How long before they call it off and go back to quantitative easing? Because that is ultimately going to happen. And the way that you know that’s going to happen is because nobody in Congress is talking about major tax increases for the middle class. Nobody is talking about significant cuts to government spending, including middle-class entitlements like Social Security and Medicare. Because that’s what would be required in order for the Fed to actually follow through on its commitment to shrink the balance sheet. Because after all, if the Fed is going to shrink the balance sheet, how is the government going to sell all of these bonds if it continues to spend the same amount of money?”

The government depends on the central bank to create artificial demand for its bonds. When the Fed shrinks its balance sheet, it will go from being one of the biggest bond buyers to a bond seller. Instead of helping the Treasury sell bonds, it will become a competitor in the marketplace. Even if the Fed doesn’t actually sell Treasuries, but simply allows bonds to roll off its books without replacing them, it’s a difference without a distinction. That still means the Fed will have to sell more Treasuries to make up for what the Fed is no longer purchasing.

Absent Fed buying, interest rates will have to continue to skyrocket in order to entice people to buy all of the Treasuries necessary to finance government spending. The government cannot afford to have its borrowing costs increase.

So, the only alternative is to replace the Federal Reserve with the taxpayer. So, we need to have more taxes, or we have to cut spending. But since neither of those is under consideration, that quantitative tightening can’t happen. They can start, but they can’t complete it.”

Peter said this is also how you know we won’t make any headway in this inflation fight.

Because raising interest rates again is not enough. And the Fed is not raising interest rates enough anyway because they have to make interest rates higher than the inflation rate. They need real interest rates to be positive, and we’re not going to get anywhere close to positive. We’re not even going to get to zero real interest rates.”

In April, the CPI was 8.3% on an annual basis. That means the Fed needs to raise rates to over 8.3% just to get the real rate to zero. And that’s using the cooked government CPI formula that understates inflation.

President Joe Biden keeps saying he’s committed to fighting inflation. But you can’t be committed to fighting inflation without a commitment to cutting government spending or raising taxes. And not just raising taxes on the rich. That won’t generate enough revenue. They would have to raise taxes on the middle class — something Biden says he won’t do.

If the government has been relying on inflation as its source of funding, if that’s how all of this government is being paid for, well, if we’re going to stop creating inflation, then we need an alternative way for paying for government, or in the alternative, we have to reduce the size of government because there’s no way to pay for it.”

Peter said the public needs to understand that there is no free lunch.

Any government we have, we have to pay for. The government doesn’t support the people. The people must support the government. Right now, we’re supporting the government with inflation. That’s the tax that we’re paying. Prices are going up because the government is spending all this money and not collecting taxes. So, the only way to get relief from the inflation tax is to either get relief on the cost of government by having the government cut spending, or we have to pay higher taxes as a tradeoff for lower inflation. So, all these politicians that claim they want lower inflation — unless they also claim they want higher taxes or less government spending — they are lying.”

Biden claims we’re going into this inflation fight in a position of economic strength, thanks to his policies.

The opposite is actually true. Not only is the US economy not in a strong position to fight inflation; we are in a weak position. In fact, we have never been in a weaker position to fight inflation than we are right now.”

Again — in order to fight inflation, you have to raise interest rates and shrink the money supply.

But the US economy is more addicted to cheap money now and low interest rates than ever before. How can you fight inflation when we have so much debt? How can you raise interest rates high enough to fight inflation when there’s so much debt and nobody can afford to pay an interest rate high enough to effectively fight inflation? And when you are running record budget deficits, how do you pull the rug out from under that? How do you fight inflation, meaning shrinking the money supply, when the government is running the biggest budget deficits in its history? Sure, they’re slightly smaller than they were at their absolute peak during the COVID pandemic. But relative to where they’ve been historically, and relative to our current level of taxation, we have enormous budget deficits. And so, how do we fight inflation with such big deficits when fighting inflation is going to require the elimination of those deficits? It’s never going to happen.”

In this podcast, Peter also talks about the May jobs numbers and points out that employment is a lagging economic indicator.

2. Lawrie Williams//Pam and Russ Martens/

END

3. Chris Powell of GATA provides to us very important physical commentaries

India’s May gold imports surge a huge 677% from a year ago.

(Reuters/GATA)

India’s May gold imports surge 677% to $5.83 billion

Submitted by admin on Mon, 2022-06-06 10:53Section: Daily Dispatches

From Reuters

via The Hindu, Chennai

Monday, June 6, 2022

India’s gold imports in May jumped 677% from a year ago to the highest level in a year as a correction in prices just before a key festival and wedding season boosted retail jewellery purchases, a government source said today.

Higher imports by the world’s second-biggest bullion consumer could support benchmark gold prices, but the surge could increase India’s trade deficit and put pressure on ailing rupee.

India imported 101 tonnes of gold in May, compared to 13 tonnes a year earlier, the source said on condition of anonymity as he is not authorised to speak to media.

In value terms, May imports surged to $5.83 billion from $678 million a year ago, he said.

“Retail consumers were waiting for a price correction. As prices corrected during Akshaya Tritiya festival, they rushed to jewellery shops,” said Harshad Ajmera, the proprietor of JJ Gold House, a wholesaler in the eastern Indian city of Kolkata. …

… For the remainder of the report:

end

USA hedge fund, Elliott and Associates are suing the LME for $456 million for cancelling nickel trades that forced the exchange to suspend its nickel market

(zerohedge)

Hedge fund sues LME for $456 million over nickel trade cancellations

Submitted by admin on Mon, 2022-06-06 10:38Section: Daily Dispatches

By Selena Li and Eric Onstad

Reuters

Monday, June 6, 2022

U.S. hedge fund Elliott Associates is suing the London Metal Exchange (LME) for $456 million for cancelling nickel trades after chaotic trading in March that forced the exchange to suspend its nickel market, the LME said today.

The legal action piles more pressure on the exchange, which is being probed by regulators and is struggling to restore trust and volumes in its nickel market.

Elliott said the LME should not have halted trading and erased deals after prices more than doubled to over $100,000 a tonne in a matter of hours on March 8.

The LME and LME Clear Ltd. were named as defendants in the judicial review claim filed in a British court by Elliott Associates and Elliott International last week, the LME’s parent company Hong Kong Exchanges and Clearing Ltd said. …

… For the remainder of the report:

END

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //DIESEL+ OTHERS

END

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6708

OFFSHORE YUAN: 6.6732

HANG SANG CLOSED DOWN 122.23 PTS OR 0.56%

2. Nikkei closed UP 28.06% OR 0.10%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 102.76/Euro RISES TO 1.0672

3b Japan 10 YR bond yield: RISES TO. +.243/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.81/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +1.258%/Italian 10 Yr bond yield RISES to 3.34% /SPAIN 10 YR BOND YIELD FALLS TO 2.40%…

3i Greek 10 year bond yield FALLS TO 3.81

3j Gold at $1848.05 silver at: 22.06 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0.25 roubles/dollar; ROUBLE AT 60.78

3m oil into the 118 dollar handle for WTI and 119 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 132.81DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9768– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0423well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.029 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 3.181 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 16.76

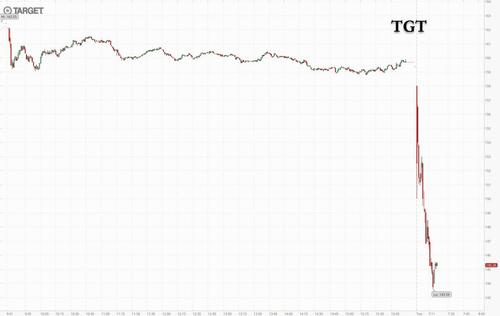

Futures Slide As Sell-The-Rippers Emerge, Encouraged By Target’s Dismal Update

TUESDAY, JUN 07, 2022 – 08:03 AM

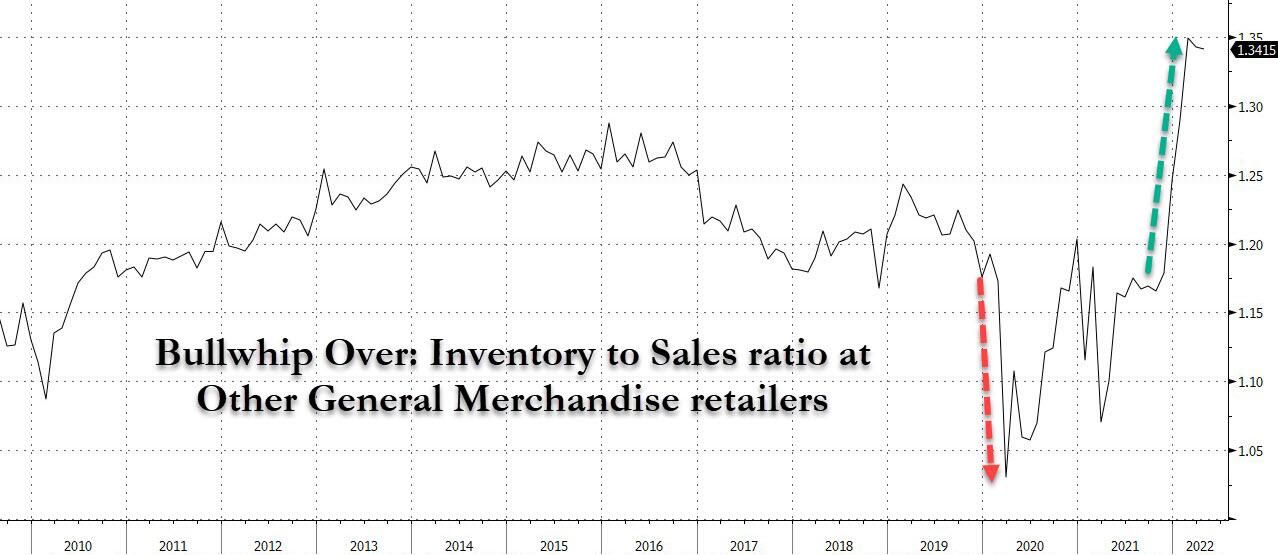

It was a relatively quiet session for stocks with futures trading modestly lower overnight as yields eased their Monday surge and when the biggest news was Australia’s unexpected 50bps rate hike (double consensus) before all hell broke loose at 7am, when Target cut guidance for the second time in two weeks due to the infamous bullwhip effect we had warned about just a few weeks ago, sending TGT stock crashing more than 9% and encouraging the cold risk-off wind that pushed S&P futures 0.8% lower to session lows around 4,080…

… while Nasdaq 100 futures fell 1% as Treasury yields hovered around 3.05%, their highest in nearly a month. Europe’s Stoxx Europe 600 Index slipped as telecom and technology stocks weighed.

In the premarket, shares of Target tumbled as much as 10% after the retailer cut its profit outlook for the second time in three weeks amid an inventory surplus. The news sent retailers such as Walmart and Costco also sliding premarket; WMT was down as much as 4.3% ahead of the bell, COST -2.9%, Kroger -1.3%, Macy’s -3%. Among other notable movers, cryptocurrency-exposed stocks tumbled in premarket trading as Bitcoin slid back below $30,000. Meanwhile Kohl’s shares rose 12% in premarket trading as the company holds exclusive talks with Franchise Group regarding a deal that would value the retail chain at about $8 billion. Here are some other notable premarket movers:

- Cryptocurrency-exposed stocks decline in premarket trading as Bitcoin slides back below $30,000, with another attempt at upward momentum losing traction amid risk-off markets. Riot Blockchain (RIOT US) -5%, Marathon Digital (MARA US) -3.7%.

- Kohl’s (KSS US) shares jump 12% in US premarket trading as the company holds exclusive talks with Franchise Group regarding a deal that would value the retail chain at about $8 billion.

- Peloton’s (PTON US) shares rose 1.4% in US after-hours trading on Monday. Former vice president of Amazon Web Services Liz Coddingtonis “well-positioned” to help Peloton in its next stage of growing subscribers, Citi says, after the exercise machine maker appointed Coddington CFO.

- Gitlab (GTLB US) shares rose 9.8% in postmarket trading on Monday after the software company’s first-quarter report.

- HealthEquity (HQY US) shares climbed 5.8% in postmarket Monday. It boosted its revenue guidance for the full year as its results beat the average analyst estimate in what RBC analyst Sean Dodgesaid could be the start of a years-long upside driven by rising interest rates.

- ProFrac (PFHC US) shares could be active after analysts initiated coverage of oil services firm with three overweight ratings and one buy, with both Piper Sandler and Morgan Stanley positive on the company’s valuation and vertical business model.

- Veru Inc. (VERU US) gained 2.8% in postmarket trading after Tang Capital Partners LPdisclosed a 5.2% passive stake in the firm.

On Monday, investors once again sold the rip, showing their reluctance to take on risk amid fears policy to subdue inflation will go overboard and kill off economic recoveries, rather than cooling off price pressures in a so-called soft landing.

“This debate around ‘are we going to see a recession, are we going to see a soft landing?’ — that’s really keeping markets relatively range bound,” Laura Cooper, a senior investment strategist at BlackRock Inc., said in an interview with Bloomberg TV. “We likely need to see a dovish pivot from policymakers to really have conviction that we’re going to a sustained rally in equities.”

Rising bond yields are adding to worries about risks to economic growth as central banks ratchet up policy tightening. US benchmark Treasury yields stabilized near 3%, a psychological threshold that may burden new supply due this week before crucial inflation data.

“The combo of declining growth, rising rates and falling liquidity is pretty ugly for equities,” said James Athey, investment director at abrdn. “Reluctant as investors in those market are to admit, the outlook for multiples and earnings isn’t great and is probably getting worse.”

Meanwhile, Friday’s CPI reading for May will be crucial for clues on the Federal Reserve’s pace of monetary tightening, especially the clothing and apparel component where we expect prices to plunge amid the inventory liquidation. Strong hiring data last week already cleared the way for the central bank to remain aggressive in its fight against inflation by raising interest rates. Higher rates particularly hurt growth sectors that are valued on future profits, like tech.

In Europe, the benchmark Stoxx 600 Index also resumed losses on Tuesday led by drops of more than 1% in technology and travel shares. European equities traded poorly with several indexes giving back over half of Monday’s gains. Euro Stoxx 50 drops as much as 0.8%, cash DAX underperforming at the margin. Tech, retail and telecoms are the weakest Stoxx 600 sectors. FTSE 100 trades flat. The European Central Bank on Thursday is set to end trillions of euros of asset purchases and cement a path to exiting eight years of negative interest rates.

Earlier in the session, Asian stocks declined with chipmakers coming under pressure as traders reassessed the outlook for demand, offsetting Japan’s boost from a weak yen. The MSCI Asia Pacific Index dropped as much as 1.2%, with TSMC and Samsung Electronics the biggest drags. Most sectors traded lower, while some Chinese internet giants and Japanese automakers were among the notable gainers. Tech hardware stocks fell as worries about demand for handsets and other gadgets outweighed hopes for a recovery in China on the easing of Covid lockdowns. South Korean equities dropped as the market reopened after a holiday, while shares in Australia slumped after the Reserve Bank of Australia blindsided the market with an outsized hike to combat rising costs. The RBA responded to price pressures with its biggest rate increase in 22 years — predicted by just three of 29 economists — and indicated it remained committed to “doing what is necessary” to rein in inflationary pressures.

There are persistent worries about demand for semiconductors as the market consensus is that a demand slowdown for handsets and other consumer electronics is highly likely,” said Lee Jinwoo, chief strategist at Meritz Securities in Seoul. Most Chinese tech stocks finished lower in volatile trading after climbing Monday following a report that regulators are concluding their investigation of transport firm Didi. Japanese shares rose as the yen weakened to its lowest level in two decades, boosting exporters such as Toyota and Honda. Read: Yen Slides to Two-Decade Low, Reigniting Focus on Intervention Asian stocks are down in June after posting their first monthly gain in five months in May. Traders will be assessing the inflation and growth outlook ahead of the Federal Reserve’s meeting next week while monitoring the state of Covid restrictions in China. “Stock market valuations have de-rated quite significantly and from our perspective, there is a lot of the bad news largely in the price. Possibly there’s more to go,” Chetan Seth, Asia Pacific equity strategist at Nomura Holdings said at a conference in Singapore

In FX, Bloomberg dollar spot rises as much as 0.4% and the dollar was steady or higher against all of its Group-of-10 peers; NOK is the weakest G-10 performer. JPY softness extends, briefly trading at 133/USD. The yen extended its slump to a fresh 20- year low near 132.60/USD as BOJ’s Kuroda continued to emphasize persistent easing commitment. Senior Japanese government officials said they were closely watching currency markets with a sense of urgency Tuesday as they returned to a heightened state of alert following a renewed slide in the yen to fresh two-decade lows. The dollar’s steep rally to the 133 handle versus the yen and the Australian central bank’s biggest rate hike in 22 years make the case for long-volatility exposure in the major currencies and traders follow suit. The pound fell to an almost three-week low versus the greenback before paring losses to trade around $1.25. The gilt yield curve bull flattened. The euro was little changed, trading around $1.07. Bunds and European bonds reversed opening losses even as wagers earlier crossed half the way toward calling a historic half-point.

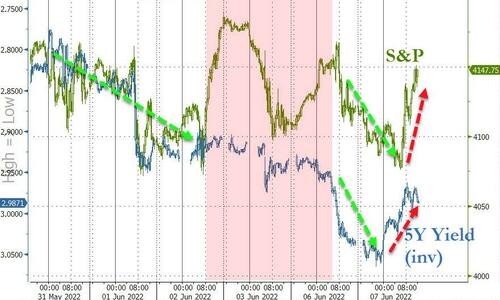

In rates, treasuries swung from losses to gains, sending yields as much as 3bps lower as the yield curve flattened. Treasury futures rose led led by the long-end amid weakness in European stocks and S&P 500 futures.Bloomberg notes that gains were helped by block trade in 10-year note futures as cash yield eases back toward 3%. US yields were richer by nearly 3bp across long-end of the curve, flattening 2s10s, 5s30s by ~1bp; 10-year, down ~2bp to 3.02%, outperforms bunds slightly, while gilt is little changed. German bunds outperform, richening ~3bps from the 5y point out, gilts are relatively quiet. Peripheral spreads are slightly tighter to core, semi-core widens a touch. Australian bond yields soared and the Aussie briefly reversed a loss after the central bank surprised investors by raising its cash rate by 50 basis points — the biggest increase in 22 years — to 0.85%, a result predicted by just three of 29 economists. It also committed itself to “doing what is necessary” to rein in inflationary pressures.

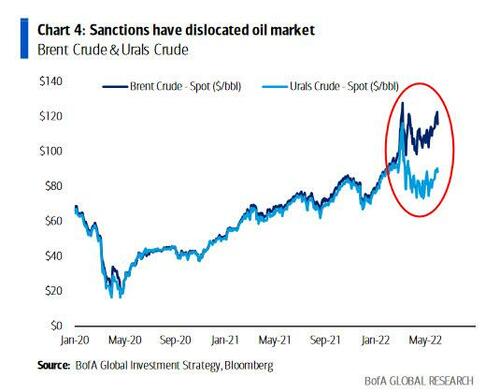

In commodities, crude futures drift higher with WTI near $120 and Brent back around $122. Spot gold adds ~$6 to near $1,847/oz. Base metals are in the red with LME nickel down over 3%.

Bitcoin is pressured and back below the USD 30k mark and incrementally below last week’s trough of USD 29.04k.

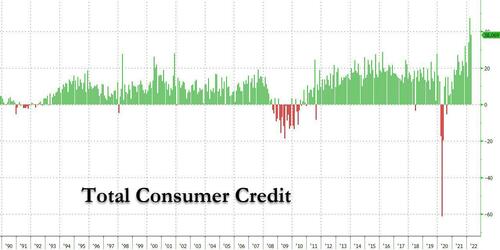

Looking to the day ahead now, and data releases include German factory orders for April, the final UK services and composite PMI for May, as well as the US trade balance and consumer credit for April. Otherwise central bank speakers include the ECB’s Wunsch.

Market Snapshot

- S&P 500 futures down 0.4% to 4,106.00

- STOXX Europe 600 down 0.4% to 442.31

- MXAP down 0.9% to 167.50

- MXAPJ down 1.1% to 552.94

- Nikkei up 0.1% to 27,943.95

- Topix up 0.4% to 1,947.03

- Hang Seng Index down 0.6% to 21,531.67

- Shanghai Composite up 0.2% to 3,241.76

- Sensex down 1.2% to 55,018.56

- Australia S&P/ASX 200 down 1.5% to 7,095.74

- Kospi down 1.7% to 2,626.34

- Brent Futures up 0.3% to $119.88/bbl

- Gold spot up 0.1% to $1,843.79

- U.S. Dollar Index up 0.10% to 102.54

- German 10Y yield little changed at 1.30%

- Euro little changed at $1.0694

Top Overnight News

- The ECB will begin a new era of monetary policy this week as officials complete their pivot to confront the threat of inflation running out of control. Armed with new forecasts and with prices rising at a record pace, President Christine Lagarde and her colleagues will end trillions of euros of asset purchases and cement a path to exiting eight years of negative interest rates

- The yen has tumbled to a two-decade low against the dollar, caught in the crossfire between the two wildly different monetary policy regimes in Japan and the US. The Bank of Japan is pinning interest rates to zero in a bid to boost a sputtering economy and spur price growth, while the Federal Reserve is hiking furiously to beat back raging inflation

- Investors from Tokyo to New York are betting on further weakness in Japan’s currency, which is already wallowing at a two-decade low against the greenback

- Bank of Japan Governor Haruhiko Kuroda walked back some of his comments that consumers are now more willing to accept higher prices after criticism on social media and a grilling in parliament

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded cautiously amid recent upside in yields and ahead of upcoming risk events. ASX 200 declined with losses exacerbated after the RBA delivered a larger-than-expected rate hike. Nikkei 225 swung between gains and losses although a weak JPY boosted the index above 28k. Hang Seng and Shanghai Comp. were varied as the mainland was kept afloat by reopening optimism and with Hong Kong subdued by property names, although tech benefitted from hopes Beijing may be easing its crackdown on the sector with China reportedly to conclude the cybersecurity probe into certain companies.

Top Asian News

- China’s Tianjin city reopened all subway stations that were closed due to COVID, while Shanghai Port’s daily volume rose to 95% of the normal level, according to local press.

- Labor Advisory Committee urged US President Biden to extend China tariffs, according to Axios.

- Japan set up a team to monitor land sales near bases and nuclear plants or on strategically located islands under a new law designed to prevent hostile foreigners from affecting national security, according to Nikkei.

- RBA hiked rates by 50bps to 0.85% (exp. 25bps increase) and said inflation in Australia has increased significantly, while it is committed to doing what is necessary to ensure that inflation in Australia returns to the target over time. RBA added that inflation is likely to be higher than was expected a month ago and the Board expects to take further steps in normalising monetary conditions over the months ahead with the size and timing of future interest rate increases to be guided by the incoming data and the assessment of the outlook for inflation and the labour market. Furthermore, it noted the Australian Economy is resilient although one source of uncertainty about the economic outlook is how household spending evolves, given the increasing pressure on Australian households’ budgets from higher inflation.

- Japan’s Economy Minister Yamagiwa says they are closely watching any impact of FX movements on the economy, wants to refrain from commenting on FX levels, via Reuters.

European bourses are modestly pressured, Euro Stoxx 50 -0.9% , with newsflow relatively limited once more and participants looking ahead to the week’s risks events. Stateside, performance is in-fitting with this directionally, though marginally more contained in terms of magnitudes, with a limited US docket ahead; ES -0.5%. EU lawmakers have come to an agreement on a single mobile charging point, via Reuters; will be USB-C by fall-2024.

Top European News

- UK PM Johnson won the confidence vote, as expected, with total votes at 211 vs 148, according to Reuters. However, the Telegraph highlights that Johnson is not “out of the woods yet” given that he has lost the support of so many backbenchers.

- UK PM Johnson said he is grateful for colleagues’ support and that they need to come together as a party now. PM Johnson added that they can now focus on what they are doing to help people in the country and have a chance to continue strengthening the economy, while he responded that is certainly not interested when asked about a snap election, according to Reuters.

- Subsequently, the 1922 Committee is, according to the understanding of UK MP Ellwood, looking at altering party rules to allow another no-confidence vote within a one-year period, via Sky’s Degenhardt.

- Barclaycard UK May consumer spending rose 9.3% Y/Y, which reflected the rising cost of living and base effects, according to Reuters.

FX

- Dollar takes time out after rallying further on yield factors and frailty of others, DXY midway between 102.830-450 range.

- Yen continues to underperform on rate and relative BoJ policy dynamics, with Franc also feeling the heat from SNB vs Fed, ECB etc policy divergence; USD/JPY touches 133.00 before easing back, USD/CHF tops 0.9675 and EUR/CHF crosses 1.0400.

- Kiwi hit by abrupt turnaround in AUD/NZD tide after RBA exceeded market expectations with a 50bp hike compounded by hawkish guidance; NZD/USD sub-0.6500 around 0.6450, AUD/NZD above 1.1100 and AUD/USD within sight of 0.7200.

- Sterling volatile after PM Johnson wins confidence vote, but significant minority of Conservative Party want him out; Cable choppy either side of 1.2500 and EUR/GBP whipsaws around 0.8550.

- Loonie softer with oil ahead of Canadian trade data and Ivey PMIs, USD/CAD near 1.2600 after probe beyond round number.

- Lira continues to slide after Turkish President Erdogan repeats intention to keep cutting rates irrespective of ongoing rise in inflation, USD/TRY tests 14.7500.

Fixed Income

- Firm bounce in bonds following extension of bear run to new cycle lows.

- Bunds lead the way in core debt circles with a near full point recovery to 149.80, while BTPs remain to the fore at the margins between 121.27-122.86 bounds.

- Gilts flat after falling short of 115.00 before solid 2025 DMO auction, T-note a tad firmer and curve flatter for choice ahead of 3 year sale.

Commodities

- Crude benchmarks have waned from initial upside stemming from bullish bank commentary amid a broader easing in risk sentiment.

- Thus far, WTI and Brent have been as low as USD 117.76/bbl and USD 118.62/bbl respectively, circa. USD 2.00/bbl from initial highs.

- Goldman Sachs hiked its Q3 Brent oil forecast to USD 140/bbl from USD 125/bbl and increased its Q4 forecast to USD 130/bbl from USD 125/bbl.

- Morgan Stanley’s base case view is for Brent to reach USD 130/bbl during Q3 with an upside to the bull case estimate of USD 150/bbl.

- Spot gold languished near the prior day’s lows amid a firmer greenback.

- JPMorgan continues to see gold trading softer towards USD 1,800/oz in Q3 2022 on an expected rebound in investor risk sentiment and continued push higher in US yields.

- Spot gold is firmer but capped by USD 1850/oz, which now coincides with its 10-DMA, after losing the level late on Monday; base metals are generally pressured, amid risk aversion and following yesterday’s price action.

US Event Calendar

- 8:30am: Revisions: Trade Balance

- 8:30am: April Trade Balance, est. -$89.5b, prior -$109.8b

- 3pm: April Consumer Credit, est. $35b, prior $52.4b

DB’s Jim Reid concludes the overnight wrap

Yesterday I published the 24th Annual Default Study. While nothing much will change for the remainder of 2022, we think we might be coming to the end of the ultra-low default world we’ve discussed so much in previous editions. First, we will likely have a cyclical US recession to address in 2023, and after that, a risk of the reversal of trends that have made the last 20 years so subdued for defaults.

We see US HY defaults peaking at just over 10% in 2024 with Europe just under 7% helped by a higher BB weighting. After that we see many of the trends of the last couple of decades reversing, helping to leave the ultra-low default era behind. You can read all about this in the note but these factors include: higher structural inflation, less ability for central banks to be as aggressive across all fixed income – they will be forced to pick their battles (eg Peripherals), less global FX reserve accumulation, a turn up in the free float of global government bonds, higher term premium, a structural fall from peak corporate profits, and shorter gaps between recessions. None of this need be a disaster just a change in the long-term trend. Clearly our view relies a lot on inflation being sticky and helping set off a 2023 recession and then remaining sticky after this, and thus changing the landscape of the last 20 years. If we’re wrong on both, the ultra-low default world will survive. See the report here.

The biggest story yesterday was a surge in yields but before we get there, a big curiousity to those of us in the UK, albeit with very limited implications for global markets, was the confidence vote last night for Prime Minister Boris Johnson from within his own party. That came after the threshold of 15% of his own MPs called for a vote, and the final result saw him win by just 211-148, meaning that 41% of his own party’s MPs voted against him. For reference, that’s more than the 37% of MPs who voted against his predecessor Theresa May in a similar vote in December 2018, and it was only 5 months later that she announced her resignation after failing to deliver Brexit and witnessing a dramatic turn in the Conservatives’ poll ratings. The next big hurdle for Johnson will likely be two by-elections on June 23rd, one of which is in a “Red Wall” seat that the Conservatives gained off Labour for the first time in decades to win their majority at the last election, whilst the other is in a traditionally safe Devon seat for the Conservatives but where the bookmakers have the Liberal Democrats as the favourite to win. So bad showings in those two would keep questions about Johnson’s leadership in the headlines and further intensify the pressure on him. In theory the Conservative leadership rules give him another year before a repeat confidence vote can happen, but history tells us that once this process gets set in motion it is incredibly difficult to reverse the negative momentum, and both Theresa May and Margaret Thatcher resigned well within a year even though they also won a majority of their own MPs at the confidence vote. Sterling actually climbed around +0.5% in the morning as the vote was officially triggered before giving back half these gains as the day progressed. However even after the surprise result at 9pm last night Sterling didn’t move, and this morning it’s just -0.09% lower, trading at 1.252 against the US dollar.

Back to the main event, which was the global rates sell-off, where 10yr Treasury yields poked back up above 3% for the first time in nearly a month, whilst European yields hit fresh multi-year highs of their own ahead of this Thursday’s ECB meeting. There’ve been a couple of catalysts behind those moves higher, but a key one over the last week and a half has been the perception that near-term recession risks (at least in 2022) are fading back again, which in turn is set to give central banks the space to continue hiking rates and thus take bond yields higher. On top of that, the fact that recent inflation data has proven stickier than expected has also pushed yields higher, and investors are eagerly awaiting to see if we get another upside surprise from the US CPI reading out on Friday.

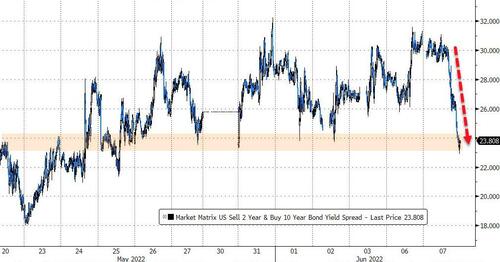

All-in-all, those moves sent the 10yr Treasury yield up by +10.3bps yesterday to 3.04%, with a rise in real yields of +8.3bps behind the bulk of the move. That came as investors dialled back up their bets on Fed tightening over the rest of the year, with the implied rate by the December FOMC meeting at a 1-month high of 2.85%, whilst the rate priced in by the Feb-2023 meeting went back above 3% for the first time in a month as well. But it was in Europe where there were even more significant milestones, with the amount of ECB rate hikes priced in by December exceeding 125bps for the first time, meaning that markets are fully pricing in at least one 50bp hike by year-end, assuming the ECB begins liftoff at the July meeting.

That prospect of a 50bp hike from the ECB sent yields on 10yr bunds up +4.9bps to 1.32%, which is their highest level since mid-2014, whilst the German 2yr yield (+3.0bps) hit its highest level since 2011. It was a similar picture elsewhere on the continent, with yields on 10yr OATs (+4.1bps) at a post-2014 high, and those on 10yr BTPs (+1.3bps) at a post-2018 high. Gilts underperformed however, with 10yr yields up +9.2bps as investors moved to price in at least one 50bp hike from the BoE by year-end.

Those moves have gained further momentum overnight after the Reserve Bank of Australia hiked rates by a larger-than-expected 50bps, helping 10yr Treasury yields to rise a further +1.9bps this morning to hit 3.06%. Their statement also pointed to further tightening ahead, and said that they expect “to take further steps in the process of normalizing monetary conditions in Australia over the months ahead”, and that they were “committed to doing what is necessary to ensure that inflation in Australia returns to target over time.” Unsurprisingly, the Australian dollar is also the top-performing G10 currency this morning, up +0.50% against the US Dollar.

The strong rise in bond yields wasn’t enough to stop equities from posting a decent start to the week, although they did pare back their initial gains following the US open. By the close, the S&P 500 (+0.31%) had held onto a broad-based advance, with 8 of 11 sectors advancing, even after paring back gains as high as +1.5% in the morning. Tech stocks fared slightly better than the broader index, with the NASDAQ gaining +0.40%. The clearest split was between mega- and small-cap shares, as mega-cap shares were clear outperformers as the FANG+ Index ended the day +1.68% higher while the small-cap Russell 2000 (+0.36%) lagged behind. It was much the same story in Europe too, where the STOXX 600 (+0.92%), the DAX (+1.34%) and the CAC 40 (+0.98%) all moved higher as well.

Whilst equities were making further gains, there wasn’t much respite on the inflation side since commodities continued their advance, with Bloomberg’s Commodity Spot Index (+1.86%) hitting a fresh record on the back of the latest moves. Admittedly, Brent Crude (-0.18%) and WTI (-0.31%) oil prices fell back slightly, and we also saw European natural gas prices (-1.75%) fall to their lowest levels since Russia’s invasion of Ukraine began. But US natural gas prices surged another +8.37% to a fresh post-2008 high, whilst agricultural goods also saw some serious movements, with futures on corn (+2.13%), wheat (+5.10%) and sugar (+1.40%) all rising on the day. This morning we’ve seen even further momentum behind commodity prices, with Brent crude moving back above the $120/bbl mark thanks to a +0.69% gain.

Overnight in Asia, equity markets have put in a pretty mixed performance as they grappled with that monetary tightening mentioned above. The Nikkei (+0.51%), the CSI 300 (+0.65%) and the Shanghai Comp (+0.48%) have all moved higher, but the Hang Seng (-0.12%) has posted a marginal decline and the Kospi (-1.37%) has lost significant ground. Meanwhile in Australia, the S&P/ASX 200 has deepened its loses since the RBA’s hawkish decision, and is currently down -1.63%, whilst futures in the US are also pointing lower, with those on the S&P 500 down -0.59% this morning. On the FX side, we’ve also seen the Japanese Yen fall to a 20-year low against the US Dollar of 131.88 by the close yesterday, and this morning it’s lost further ground to hit 132.86. That comes as the BoJ stands out among its global peers in not tightening policy, which is leading to a widening interest rate differential as other central banks continue hiking.

Finally we started on credit so let’s end there too before the day ahead preview. Our colleagues in the European Leveraged Finance Research team have just published their quarterly top trade ideas. You can find the report here.

To the day ahead now, and data releases include German factory orders for April, the final UK services and composite PMI for May, as well as the US trade balance and consumer credit for April. Otherwise central bank speakers include the ECB’s Wunsch.

end

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 5.39 PTS OR 0.17% //Hang Sang CLOSED DOWN 122.23 PTS OR 0.54% /The Nikkei closed UP 28.06 OR 0.10% //Australia’s all ordinaires CLOSED DOWN 1.54%% /Chinese yuan (ONSHORE) closed DOWN 6.6708 /Oil UP TO 118.03dollars per barrel for WTI and UP TO 119.19 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6708 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6752: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/USA/JAPAN

US & S.Korean Jets In Large ‘Show Of Force’ As White House Warns Kim Against Nuclear Test

TUESDAY, JUN 07, 2022 – 10:20 AM

So far this year alone has seen North Korea launch at least 18 rounds of missiles, which included its first intercontinental ballistic missile tests since 2017, in significant timing given also the world’s attention has been focused on the Russian invasion of Ukraine.

On Monday for the first time this year, the US and South Korea “answered” Pyongyang’s latest Sunday launches of eight missiles by firing precisely eight missiles of their own. Sunday’s launches were the biggest single-day testing event all year. On Tuesday US and South Korean forces have continued a ‘show of force’ by flying dozens of fighter jets over waters off the Korean Peninsula.

The flights also included aircraft from Japan. The Associated Press describes, “Extending the countries’ joint displays of military might, four U.S. F-16 fighter jets flew in formation with 16 South Korean planes — including F-35A stealth fighters — over waters off South Korea’s eastern coast, an exercise aimed at demonstrating an ability to quickly respond to North Korean provocations, South Korea’s Joint Chiefs of Staff said.”

“The United States and Japan conducted a separate drill involving six aircraft — four Japanese F-15 fighters and two American F-16s — above waters between the Korean Peninsula and Japan, Japan’s Defense Ministry said,” the report adds.

Meanwhile, US Deputy Secretary of State Wendy Sherman is in Seoul for talks with her Korean counterparts. She took the opportunity to again warn Pyongyang against holding a nuclear test, which hasn’t occurred in a half-decade. She said there would be a “swift and forceful” counterresponse of the north moves forward with conducting a nuclear explosion.

The warning appeared timed and coordinated with the larger than usual joint flights among US allies in regional waters. Without doubt it got Pyongyang’s attention, though it remains to be seen whether there will be escalation or a walking back of ratcheting tensions.

“Any nuclear test would be in complete violation of U.N. Security Council resolutions. There would be a swift and forceful response to such a test,” Sherman said. “We continue to urge Pyongyang to cease its destabilizing and provocative activities and choose the path of diplomacy.”

She and South Korean representatives, including Vice Foreign Minister Cho Hyun-dong, are expected to discuss North Korea’s nukes with Japanese Vice Foreign Minister Mori Takeo on Wednesday.

Within the last month Western media reports have begun sounding the alarm over resumed construction and expansion at North Korean nuclear sites.

While not confirmed, the allegations that Pyongyang is seeking to revive some long-dormant sites are based on open-source satellite imagery, as CNN previously detailed:

North Korea appears to have resumed construction at a long-dormant nuclear reactor in recent weeks that, if completed, would dramatically increase its capacity to produce plutonium for nuclear weapons, according to new satellite images obtained by CNN and a source familiar with recent US intelligence reporting on the matter.

The satellite images, which were captured by Maxar during April and May of this year, show North Korea has restarted construction of the second reactor at its Yongbyon nuclear complex after years of inactivity, experts at the Middlebury Institute of International Studies who analyzed the photos said.

The reactor is about 10 times larger than the existing nuclear reactor at Yongbyon, which has been operating since the late 1980s.

On Monday, International Atomic Energy Agency (IAEA) chief Rafael Grossi issued a briefing at a quarterly meeting of the IAEA, saying that work at the north’s main nuclear site at Yongbyon is advancing, amid fears of a return to nuclear saber-rattling by the Kim Jong Un regime.

3B JAPAN

end

3c CHINA

4/EUROPEAN AFFAIRS//UK AFFAIRS/

POLAND

Poles told to burn wood to keep warm in the winter as inflation rips through their country.

“Collect Branches For Fuel” – Poles Told To Burn Wood To Keep Warm Amid ‘Putinflation’

TUESDAY, JUN 07, 2022 – 05:45 AM

In early 2019, just before the COVID-lockdown crisis hit the world, the southern Polish city of Kraków introduced a ban on burning coal and wood in a campaign against smog.

The move means residents face fines for using such fuel in their stoves, boilers, fireplaces and even for cooking on stationary barbecues. Lighter, portable barbecues are exempt.

Inspectors will monitor air pollution levels using a drone, thermal imaging camera and a dust monitor, state news agency PAP reported.

Fast-forward three years, with millions of refugees surging across the border from Ukraine and energy prices at record-er and record-er highs, it appears the Polish government has changed its mind on ‘smog’ and ‘climate change’ as it reminded citizens on Friday they can forage firewood from forests to keep warm.

The government said it was taking steps to make it easier for people to collect firewood in an effort to ease the pressure created by sky-rocketing energy bills and shortages of coal.

“It is always possible, with the consent of foresters, to collect branches for fuel,” said deputy climate and energy minister Edward Siarka.

However, it’s not quite as ‘easy’ as wondering into the forest with your axe.

The polish government demands that those wishing to gather wood must first undergo training and obtain permission from the local forestry unit. Additionally, they went on to clarify that people can only take branches already lying on the ground, and cannot cut down trees.

“Only branches can be gathered. At the same time, the collected branches cannot be thicker than seven centimeters,” said Katowice Directorate of State Forestry official Marek Mroz.

Interestingly, while Prime Minister Mateusz Morawiecki’s government is blaming the Russian invasion of Ukraine for driving up costs (Putinflation), as Euronews reports, critics, however, say the war is only partially to blame. They argue that costs have risen for seven years under Law and Justice’s social spending policies, which include cash handouts to families with children and the elderly.

“We will all be collecting brushwood,” said Donald Tusk, leader of the opposition Civic Platform on Friday.

“Because this seems to be the latest idea to prevent Polish poverty that Law and Justice has prepared for all of us.”

The Law and Justice party has said it is seeking ways to alleviate the energy crisis, stating that eight ships carrying more than 700,000 tonnes of coal are on their way to Poland.

Greta will not be happy at all!! (has anyone else noticed how quiet she has been during this crisis). Who cares about the ‘climate’ when your fingers have frostbite and you can’t heat your food…

end

UK

Huge story: huge inflation in the UK could cause 500,000 small businesses to go bust

(zerohedge)

“Ticking Timebomb”: 500,000 UK Small Businesses Could Imminently Go Bust

TUESDAY, JUN 07, 2022 – 02:45 AM

As a stagflationary storm looms over the UK economy, the Federation of Small Businesses (FSB) chairman warned of a tsunami of small business closings without new support packages from the government.