JUNE 10 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1871.85 UP $21.40

SILVER: $21.93 UP $.13

ACCESS MARKET: GOLD $1871.00

SILVER: $21.88

Bitcoin morning price: $29941 DOWN 168

Bitcoin: afternoon price: $28977 DOWN 1032

GOLD; $1847.60

Platinum price: closing DOWN $1.15 to $977.75

Palladium price; closing DOWN $4.20 at $1928.45

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 22/28

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,848.800000000 USD

INTENT DATE: 06/09/2022 DELIVERY DATE: 06/13/2022

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 1

323 H HSBC 3

363 H WELLS FARGO SEC 1

624 H BOFA SECURITIES 1

657 C MORGAN STANLEY 1

657 H MORGAN STANLEY 16

661 C JP MORGAN 22

800 C MAREX SPEC 11

TOTAL: 28 28

MONTH TO DATE: 21,853

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 28 NOTICE(S) FOR 2800 Oz//0.08709 TONNES)

total notices so far: 21,853 contracts for 2,185,300 oz (67.9720 tonnes)

SILVER NOTICES:

15 NOTICE(S) FILED 75,000 OZ/

total number of notices filed so far this month 1588 : for 7,940,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $21.40

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//

INVENTORY RESTS AT 1065.39 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 13 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://A WITHDRAWAL OF 830,000 OZ FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.399 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 4751 CONTRACTS TO 151,743 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE GAIN IN OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.27 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.27) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS WE HAD A VERY STRONG GAIN OF 5549 CONTRACTS ON OUR TWO EXCHANGES

WE MUST HAVE HAD:

I) HUGE BANKER SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 16 CONTRACTS OR 80,000 OZ//NEW STANDING: 8,340,000 / // V) GIGANTIC SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -548

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 8 days, total 5,761, contracts: 28.805 million oz OR 3.600 MILLION OZ PER DAY. (720 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 28.805 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 28.805 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4751 DESPITE OUR STRONG $0.27 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 250 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 80,000 QUEUE JUMP //NEW STANDING: 8,340,000 OZ // .. WE HAD A VERY STRONG SIZED GAIN OF 5001 OI CONTRACTS ON THE TWO EXCHANGES FOR 25.005 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 15 NOTICES FILED TODAY FOR 75,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2602 CONTRACTS TO 494,698 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -156 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE LOSS IN COMEX OI CAME WITH OUR LOSS IN PRICE OF $3.50//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR FAIR SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 7,000 OZ QUEUE JUMP//NEW STANDING: 73.290 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $3.50 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1668 OI CONTRACTS 5.188 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 1824 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 494,698

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1668, WITH 2602 CONTRACTS DECREASED AT THE COMEX AND 4270 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1662 CONTRACTS OR 5.188TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4270) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2602,): TOTAL GAIN IN THE TWO EXCHANGES 1824 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 7,000 OZ//NEW STANDING: 73.290 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) FAIR SIZED COMEX OI. LOSS 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

29,993 CONTRACTS OR 2,999,300 OZ OR 93.29 TONNES 8 TRADING DAY(S) AND THUS AVERAGING: 3749 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES: 93.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 92.29/3550 x 100% TONNES 2.62% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 93.29 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 4751 CONTRACT OI TO 151,743 AND CLOSER TO OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 250 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4751 CONTRACTS AND ADD TO THE 250 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED GAIN OF 5001 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 25.001 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.27 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 48.88PTS OR 1.42% //Hang Sang CLOSED DOWN 62.87 PTS OR 0.29% /The Nikkei closed DOWN 472.24 OR 1.49% //Australia’s all ordinaires CLOSED DOWN 1.32% /Chinese yuan (ONSHORE) closed DOWN 6.6950 /Oil UP TO 122.39dollars per barrel for WTI and UP TO 123.44 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.6950 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7054: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

SHANGHAI CLOSED DOWN 24.84 PT

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2602 CONTRACTS TO 494,698 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $3.50 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (1756 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4270 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4270 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4270 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1668 CONTRACTS IN THAT 4270 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 2602 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF GOLD $3.50.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (73.290),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 73.290 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL 3.50) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS AS WELL AS SPECULATOR SHORTS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 5.673 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (73.290 TONNES)…

WE HAD 156 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1668 CONTRACTS OR 166,800 OZ OR 5.188 TONNES

Estimated gold volume 257,664/// good

final gold volumes/yesterday 142,324 poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 10

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 174,572.855 oz Manfra HSBC JPM Brinks 22 kilobars |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 28 notice(s) 2800 OZ 0.08709 TONNES |

| No of oz to be served (notices) | 1710 contracts 171,000 oz 5.3188 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,853 notices 2,185,300 OZ 67.9720 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

4 customer withdrawals:

i) Out of Brinks: 128.601 oz 4 kilobars

ii) Out of JPMorgan: 161,058.910 oz

iii) Out of Manfra: 2891.891 oz

iv) Out of HSBC: 578.453 oz (18 kilobars)

total withdrawal: 164,572.855 oz

ADJUSTMENTS: 1

Brinks: 19,979.790 oz dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1738 contracts having LOST 1775 contracts

We had 1845 notices filed on THURSDAY so we GAINED A 70 contracts or an additional 7000 oz will stand for gold in this very active month of June

July has a LOSS OF 162 OI to stand at 2140

August has a LOSS of 3205 contracts DOWN to 416,494 contracts

We had 28 notice(s) filed today for 2800 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 28 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 22 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (21,853) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 1758 CONTRACTS ) minus the number of notices served upon today 28 x 100 oz per contract equals 2,356,300 OZ OR 73.290 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (21,853) x 100 oz+ (1758) OI for the front month minus the number of notices served upon today (28} x 100 oz} which equals 2,356,300 oz standing OR 73.290 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 73.290 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,331,163.529 oz 72.5 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,552,806.365 OZ

TOTAL ELIGIBLE GOLD: 16,608,755.822 OZ

TOTAL OF ALL REGISTERED GOLD: 17,944,050.543 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,612,887.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 10

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 154.347.772 oz Brinks Delaware Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 566,832.900 oz JPMorgan |

| No of oz served today (contracts) | 15CONTRACT(S) 75,000 OZ) |

| No of oz to be served (notices) | 65 contracts (325,000 oz) |

| Total monthly oz silver served (contracts) | 1603 contracts 8,015,000, oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) zero dealer deposits

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposits into the customer account

i) Into JPMorgan: 566,832.900 oz

total deposit: 566,832.900 oz

JPMorgan has a total silver weight: 171.492 million oz/337.601 million =50.77% of comex

Comex withdrawals: 3

i) Out of Brinks 23,809.900 oz

ii) Out of Delaware: 1018.343 oz

iii) Out of Manfra: 129,519.529 oz

total withdrawal 129,519.529 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 72.748 MILLION OZ

TOTAL REG + ELIG. 337.601 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 80 HAVING LOST 7 CONTRACTS.

WE HAD 23 NOTICES FILED ON THURSDAY SO WE GAINED 16 CONTRACTS OR AN ADDITIONAL 800,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 4204 CONTRACTS DOWN TO 81,577 CONTRACTS.

AUGUST LOST 2 CONTRACTS TO STAND AT 972

SEPTEMBER HAD A GAIN OF 8126 CONTRACTS UP TO 53,500 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 23 for 115,000 oz

Comex volumes:91,239// est. volume today// strong

Comex volume: confirmed yesterday: 86,243 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1603 x 5,000 oz = 8,015,000 oz

to which we add the difference between the open interest for the front month of JUNE(80) and the number of notices served upon today 15 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1603 (notices served so far) x 5000 oz + OI for front month of JUNE (8-) – number of notices served upon today (15) x 5000 oz of silver standing for the JUNE contract month equates 8,340,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1065.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 544.399 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

We Are Hurtling Toward Stagflation

FRIDAY, JUN 10, 2022 – 08:53 AM

Authored by Michael Maharrey via SchiffGold.com,

There are a number of signals that the US economy is getting weaker even as inflation gets stronger.

In other words, we are hurtling toward stagflation.

Target announced plans to cancel orders from suppliers and slash prices to clear out amassed inventory. Why? Because consumers aren’t buying their stuff – particularly hardline goods such as clothing and home goods.

Why have revenues at Target and other retailers plunged, even while retail sales numbers have remained strong? In a nutshell, consumers are paying more and getting less.

- First, people simply don’t have any money left over after paying for essentials such as gasoline and food.

- Second, everything more expensive. Retailers are getting hammered by higher costs.

Some people have concluded that there is a silver lining in this. If Target plans to cut prices to move inventory, that means inflation should come down. That’s the wrong read. These price cuts will only be temporary. In the future, Target won’t carry as much inventory. That means once they blow out this inventory, what’s left will be much more expensive.

Meanwhile, in order to make up for lost revenue on clothing and housewares, Target will likely have to raise prices on the thing it is selling – food.

And at some point, Target will have to begin cutting jobs.

Another storm that’s brewing is the impact of declining inventories on GDP. Inventory builds pump up GDP in the here and now. Inventory declines will suppress GDP moving forward. In fact, the Atlanta Fed just downgraded its Q2 GDP estimate to 0.9%. That would mean a 0.7% contraction in GDP through the first half of the year. This undercuts the Federal Reserve narrative that it can fight inflation because “the economy is strong.”

American consumers are straining under rising prices. To make ends meet, they are turning to credit cards and depleting savings. Consumer debt has risen to record levels, while the savings rate has plunged to the lowest level since 2008.

These numbers prove that everything Joe Biden said last week about a strong economy and US consumers being in great shape was wrong. Consumers are in desperate straits. They are tapped out. Whatever savings they managed to accumulate during the pandemic when the government stuffed their pockets with stimulus money is gone. Now they’re maxing out their credit cards. And what are they buying? They’re only buying the necessities – food, energy, shelter. There is no money left for discretionary spending. This house of cards economy is on the verge of a collapse.

The trade deficit further reveals just how hollowed out the US economy has become. While the $87 billion trade deficit was lower than projected, it was still an extremely high number and on a year-on-year basis, it set another record. This indicates just how completely unbalanced the US economy has become. Decades of artificially low interest rates have incentivized speculation and consumption, and disincentivized savings – the key to capital accumulation. As a result, there has not been enough investment in plants and equipment.

All of this data points to one thing – inflation is putting a massive drag on the economy. And there is no sign that inflation is about to abate.

Government officials, central bankers and talking heads on CNBC can talk about a “strong economy” until they are blue in the face. The data says otherwise. It’s screaming stagflation.

Even the mainstream is starting to worry. The AP recently ran an article headlined “Worry About Stagflation, a Flashback to ’70s, Begins to Grow.” And the World Bank also issued a warning.

The world economy is again in danger. This time, it is facing high inflation and slow growth at the same time. … It’s a phenomenon — stagflation — that the world has not seen since the 1970s.”

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards

LAWRIE WILLIAMS: World Top 20 Gold Producing Countries 2021 and Gold Outlook

Now is the time of year that the world’s major analytical assessors release their respective takes on what has been happening in terms of global gold production over the past year, and what is likely to happen in the year ahead. As can be seen from the table below, gleaned from the 2022 Gold Focus report from one of the world’s leading precious metals consultancy groups, London-based Metals Focus, global gold output has risen over the past year, albeit at a relatively subdued rate, despite talk of peak gold which does not yet appear to be with us, but is close!

In some respects, gold production figures for the past couple of years will have been slightly anomalous in any case because of the differing impacts of the Covid pandemic- related curtailments at many operations. These have been more severely implemented in some countries than in others and will probably have impacted 2020 output volumes more severely than for 2021. Closer examination of the 100-page plus Gold Focus report will indeed show that new mined gold production is estimated to have fallen a little in 2020, and the 2021 amount produced is only close to that of 2019 (if marginally lower) although the consultancy is forecasting a 1.7% increase in the current year. In other words global new mined gold production is virtually flat at the moment despite higher average price levels.

What is apparent from the table though is that China’s position as the world’s top gold producer appears to be under strong threat from Russia, and perhaps also from Australia. We had thought that this might yet be three of four years away, but at the current rate of decline of Chinese gold output that could well happen as soon as the current year, although the sanctions regime as a result of the Russia/Ukraine war could impact Russian gold mine output if key equipment and consumables imports are interrupted as a result.

However, the sharp decline in Chinese gold output last year was largely due to safety-related mine shutdowns in Shandong province. It appears that many of these curtailed operations are now producing again, so we may well see a pick-up in Chinese gold production this year accordingly which should put off any further closure of the national global gold production gap by another year or so.

It is apparent, though, that China, Russia and Australia are way ahead of any other country in terms of national gold production, with Canada coming up strong, but still well behind. It is notable that South Africa, which dominated global gold production for most of the 20th Century, has now fallen to only 10th place according to the latest Metals Focus estimates, and no longer even boasts Africa’s largest gold mines – the DRC’s Kibali and Mali’s Loulo-Gounkoto properties have assumed that position. Interestingly it has been Randgold Resources with effective South African roots, now part of Barrick Gold, which was largely responsible for bringing both these operations into being. There are also other larger African gold mining operations in terms of 2021 gold output elsewhere in Mali, Ghana, Tanzania and Burkina Faso before we get to South Africa’s largest producing gold mine. How the mighty have fallen.

As to the global production and price outlook, Metals Focus is predicting a fairly conservative average gold price of only $1,830 for the current year which can’t be far off the average year to date and is well below the Russia/Ukraine war-boosted averages for March, April and May. The Metals Focus analysts are particularly worried that central banks’ restrictive policy moves may result in severe economic slowdowns, but with inflation staying stubbornly high, which coincides with our view. The resulting loss of disposable incomes could fuel a downward spiral for economies leading first to stagflation, which may already be with us, and then to recession.

In truth the recent volatility in the markets, which is affecting all of precious metals, equities and bitcoin adversely for the most part, makes outlook predictions almost impossible. And, of course, if the Russia/Ukraine war escalates, as some observers fear is inevitable, all price bets are off – particularly for gold. Such escalation could involve Russian military moves against other European sovereign nations or, heaven forbid, the employment of chemical, biological or even nuclear weapons as has been threatened by Russia.

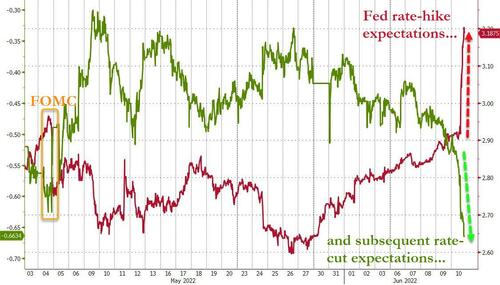

The coming week’s FOMC meeting will thus only scratch the surface of some of the worries facing the international community. We think the Fed’s likely moves and ensuing commentary will hit equities and possibly bitcoin and have a mixed effect on the gold price depending on whether higher rates are seen as positive, or negative, for the dollar. Either is possible. We think the potential vulnerabilities for equities and bitcoin exceed those for gold in particular, but in the current economic environment anything is possible. Hold tight – stormy times ahead!

-END-

Grandich Interview

Videos

Ep 77: Live From The Vault – Time’s up for the dollar! Gold …

I especially enjoyed connecting with Andy again. It was pure joy, reminiscing about GATA and whatever happened to “Tokyo Rose”, who calls us a bunch of names (and worse), claiming there was no manipulation. He’s long gone, while Andy, Bill, and Chris are still worthy commentators.

END

3. Chris Powell of GATA provides to us very important physical commentaries

For your interest (silver)

Ted Butler: Investors have eyes wide shut about silver

Submitted by admin on Thu, 2022-06-09 19:59Section: Daily Dispatches

By Ted Butler

SilverSeek.com

Thursday, June 9, 2022

Paul Krugman, the economist whose work you either love or hate, had a compelling editorial this week in the New York Times titled, “From the Big Short to the Big Scam,” in which he compared the real estate bubble of 2006 and subsequent crash to cryptocurrencies today.

Because the article was behind a subscription paywall, I’ll not link it here, and my purpose today is not to agree or disagree with Krugman’s connection of the real estate bubble/bust to crypto’s but to bring out a most astute observation he made

Krugman made the compelling case that what enabled a relative handful of market participants to recognize and act upon the extreme mispricing of real estate into the 2006 bubble peak and sell short subprime mortgage derivatives contracts was the belief among the majority of market participants that real estate would not collapse.

His term to describe the widespread belief at the time that real estate prices would continue to climb was the “incredulity factor,” and, to use Krugman’s own words, therein was the problem, namely:

“… the sheer scale of the mispricing that the skeptics claimed to see. Even though there was clear evidence that housing prices were out of line, it was hard to believe they were that far out of line — that $6 trillion in real estate wealth would evaporate, that investors in mortgage-backed securities would lose around $1 trillion. It just didn’t seem plausible that markets, and the conventional wisdom saying that markets were OK, could be that wrong. But they were.”

If you get a chance to read the entire article, I’ll leave it up to you to decide if Krugman made the case between the real estate boom/bust of 2006 and crypto’s today. Instead, the lightbulb that went off in my head when reading his piece concerned — what else? — silver. …

… For the remainder of the analysis:

https://silverseek.com/article/eyes-wide-shut

Eyes Wide Shut

June 09, 2022

Ted Butler

Paul Krugman, the economist whose work you either love or hate, had a compelling editorial this week in the NY Times, titled, “From the Big Short to the Big Scam”, in which he compared the real estate bubble of 2006 and subsequent crash to cryptocurrencies today. Because the article was behind a subscription paywall, I’ll not link it here, and my purpose today is not to agree nor disagree with Krugman’s connection of the real estate bubble/bust to crypto’s, but to bring out a most astute observation he made.

Krugman made the compelling case that what enabled a relative handful of market participants to recognize and act upon the extreme mispricing of real estate into the 2006 bubble peak and sell short subprime mortgage derivatives contracts was the belief among the majority of market participants that real estate would not collapse. His term to describe the widespread belief at the time that real estate prices would continue to climb was the “incredulity factor” and to use Krugman’s own words, therein was the problem, namely, –

“…the sheer scale of the mispricing that the skeptics claimed to see. Even though there was clear evidence that housing prices were out of line, it was hard to believe they were that far out of line – that $6 trillion in real estate wealth would evaporate, that investors in mortgage-backed securities would lose around $1 trillion. It just didn’t seem plausible that markets, and the conventional wisdom saying that markets were OK, could be that wrong. But they were.”

If you get a chance to read the entire article, I’ll leave it up to you to decide if Krugman made the case between the real estate boom/bust of 2006 and crypto’s today. Instead, the lightbulb that went off in my head when reading his piece concerned – what else – silver. I was particularly taken with Krugman’s use of the term “incredulity factor” to describe what blinded the majority’s opinion about real estate back then and crypto’s today was the broad and innate belief that then-current market prices couldn’t be that far off from whatever levels they were trading at – when the history of markets strongly suggests that yes, indeed, there are times when markets can be extremely mispriced.

While it’s true that Krugman was using two examples of markets that were or were perceived to be extremely over-priced, that doesn’t automatically exclude the presence of the incredulity factor in an extremely underpriced asset like silver. Simply put, silver’s extremely low price over the past few decades has told, in no uncertain terms, the vast majority of the world’s investors to just move along – that there is nothing to see here. It would defy credulity for the majority not to think that the persistent low price of silver wasn’t due to ample or oversupplied market fundamentals. That’s just normal collective investor behavior.

But even a slightly more in-depth look at silver would result in the realization that the actual supply/demand fundamentals in silver are nowhere near as negative as the low price would suggest. An even deeper review would raise more substantive questions concerning why, of all commodities, silver is still more than half of its non-inflation adjusted price highs of both 42 and 11 years ago. Adjusted for inflation, silver’s low price is downright shocking.

A reasonable person, when presented with silver’s extreme undervaluation compared to its actual fundamentals would conclude something is wrong – but, according to the incredulity factor (referenced by Krugman) therein lies the problem, namely, the vast majority of reasonable people are not even looking, due to the deeply-imbedded collective sense that current market prices can’t be that far off from where they should be. I’ve been asked more times than I could possibly recall why someone big hasn’t bought silver (apart from JPMorgan). The answer is elementary – because the persistent low price has signaled it’s not worth the time to investigate.

Complicating the issue in silver is that the reason most eyes and minds are closed when it comes to questioning the possibility that the persistent low price is that far off from where it should be, is that the answer is particularly hard to accept. After living and breathing the intricacies of silver for close to 40 years, there’s not the slightest doubt in my mind that the low price is a result of an ongoing manipulation by certain large traders on the COMEX, as I’ve tried to document all along. I’ve come to accept most will never go that deep, but broad acceptance of my take is not required.

If any market is extremely mispriced, as I contend that silver is to the downside, then it’s only a matter of time before the mispricing must come to an end. Just like housing’s extreme overvaluation was rectified starting in 2006, so too will silver’s extreme undervaluation be rectified ahead. The really important point here is that just like only a relative handful of market participants profited greatly from the housing bust by going against the majority who didn’t comprehend the extent of the inevitable housing collapse, a similar circumstance is likely to be experienced in silver – with a special twist.

Those that profited mightily in the housing bust did so by dealing in highly-esoteric and complex mortgage derivatives securities way beyond the capacity of the regular investor to understand or have access to. To truly profit from the housing/mortgage bust one would have had to deal in derivatives contracts well-beyond the reach of the average man in the street. In contrast, the beauty of capturing the coming radical upward adjustment in the price of silver is about as easy as falling off a log. In fact, there are almost too many really simple and good ways of buying silver to mention – no need to have to resort to anything complicated or esoteric. A bigger plus factor and advantage would be hard to find.

As was vividly portrayed in the movie and book, “The Big Short”, before real estate prices began their descent after 2006 and derivatives bets against housing began to pay off, many holders of the short derivatives bets were pressed up against the wall, struggling to maintain their short bets and having to meet increasing margin calls to hold on to the positions. I know many silver investors, after so many years of waiting for the actual fundamentals to kick in and bring about the inevitable higher prices to come, must hold similar feelings as faced by the margined holders of what turned out to be the spectacularly profitable results of those that bet on a housing collapse.

But here’s the real beauty of buying and holding silver, as opposed to betting against housing in 2006 – there is no margin or leverage required. Sure, there are opportunities galore for those who choose to “up the ante” by going on margin and deploying leverage when buying silver, but that is not required by those looking to take advantage of what I feel is the single best investment opportunity available. In fact, knowing the stresses associated with borrowing and utilizing leverage to most people, I strongly advise against buying silver on anything but a cash on the barrel basis. Silver is going to explode in price to such an extreme extent that leverage is not required. All that is required is an open mind and eyes.

Ted Butler

June 9, 2022

end

4.OTHER GOLD/SILVER COMMENTARIES

Gold Price Could Be Heading for Another Rally Due to Global Economic Slowdown – Bloomberg

Inbox

| douglas cundey | 7:08 AM (34 minutes ago) | ||

| to Chris, William, Bill, me |

Gold’s Haven Appeal Burnished by Drumbeat of Growth Warnings

Bullion may have another rally this year as stagflation looms Global economic slowdown paves the way for flight to safety

Ranjeetha PakiamJune 7, 2022, 1:46 PM EDT

June 6, 2022, 6:27 PM EDT

Gold may be heading for another rally, with warnings over a global economic slowdown paving the way for a fresh push toward $2,000 an ounce.

A potent mix of decades-high inflation, geopolitical turmoil and growing talk of recession should be bullish for the traditional haven, according to speakers interviewed ahead of a precious metals conference in Singapore this week.

end

5.OTHER COMMODITIES //LITHIUM

German plant may shut down its huge lithium plant over a new EU rule

Paraskova/OilPrice.com

Major Lithium Producer Could Shut German Plant Over EU Rule

FRIDAY, JUN 10, 2022 – 03:30 AM

Authored by Tsvetana Paraskova via OilPrice.com,

Lithium producer Albemarle could be forced to close its plant in Germany if the European Union classifies the key mineral lithium as a hazardous substance that would change the way lithium is processed and stored, the company’s chief financial officer has told Reuters.

The European Commission is currently reviewing and assessing a proposal from the European Chemicals Agency (ECHA) to classify lithium carbonate, lithium chloride, and lithium hydroxide as substances hazardous to human health. An EU committee is meeting early next month to discuss the proposal, while a final decision on the issue is expected toward the end of this year or early next year.

If the EU decides to include the lithium chemicals in the hazardous category, it would deal a blow to its own goals of becoming self-sufficient in batteries this decade and significantly raise the share of electric vehicles on the roads.

The decision would change the way lithium producers and processors work and will add costs to their operations.

In Albemarle’s case, the company “would no longer be able to import our primary feedstock, lithium chloride, putting the entire (Langelsheim) facility in jeopardy of closure,” CEO Scott Tozier told Reuters in an emailed statement.

Albemarle processes lithium products at its Langelsheim factory in Germany, which employs around 550 people.

Albemarle would sustain a financial blow if it had to shut down the German plant.

“With sales of approximately $500 million annually, the economic impact to Albemarle from the potential closure would be significant,” the company’s CEO told Reuters.

The EU is set to meet 69 percent and 89 percent of its growing demand for batteries by 2025 and 2030, respectively, the European Commission said earlier this year. The EU expects to be capable of producing batteries for up to 11 million cars per year, it added.

END

Avocado

Avocado prices hit fresh record highs all due to supply side factors

(zerohedge)

Avocado Prices Hit Fresh Record High Amid “Supply-Side Factors”

FRIDAY, JUN 10, 2022 – 05:45 AM

The great avocado price squeeze began earlier this year and has since sent prices to record highs. Surely anyone who has been to the supermarket, ordered groceries online, or even added an extra topping of avocados on a burrito bowl at Chipotle has been shocked by prices.

Since the start of the year, the price of a 20-pound box of avocados from the state of Michoacan, Mexico (the central hub of Mexican avocado production), has risen from $20 to now $50, a mind-numbing 150% jump in the first five months of the year.

Prices for this time of year are the highest, dating back 24 years of data via Bloomberg. A seasonal price peak tends to be in late July, so there could be more upside in prices into summer.

The reason for such a dramatic rise in prices was explained by Pamela Diaz Loubet, a Mexico City-based economist at BNP Paribas, who told Bloomberg, “Avocado prices have been exacerbated by supply-side factors such as the increase in fertilizer prices.”

Our past reportings have detailed some of the events that have led to soaring prices, including the temporary suspension of all imports of Mexican avocados in early February, production declines, and the cost of soaring fertilizer, diesel, and freight have all led to rising prices.

- USDA Suspends Mexican Avocado Imports, Stokes Yet More Food Inflation

- Chipotle On Brink Of Guacamole Shortage After US Bans Mexican Avocados

- Avocado Prices Rocket To Decade High As Mexican Production Set To Plunge

Now comes the point at what price will demand destruction emerge. It will be tough for millennials to give up avocado and toast.

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.6950

OFFSHORE YUAN: 6.7054

HANG SANG CLOSED DOWN 422.24 PTS OR 1.49%

2. Nikkei closed DOWN 422.24% OR 1.49%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 103.58/Euro RISES TO 1.0581

3b Japan 10 YR bond yield: RISES TO. +.247/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 133.84/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.395%/Italian 10 Yr bond yield RISES to 3.71% /SPAIN 10 YR BOND YIELD RISES TO 2.64%…ALL BLOWING UP!!

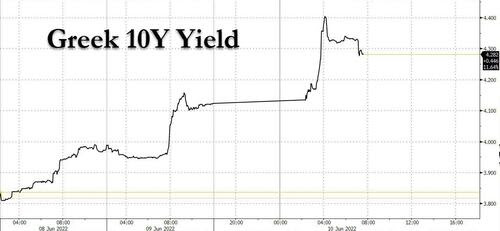

3i Greek 10 year bond yield RISES TO 4.265//BLOWING UP

3j Gold at $1834.35 silver at: 21.35 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1.30 roubles/dollar; ROUBLE AT 58.11

3m oil into the 122 dollar handle for WTI and 123 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 133.87DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9831– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0403well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.038 DOWN 1 BASIS PTS

USA 30 YR BOND YIELD: 3.150 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.08

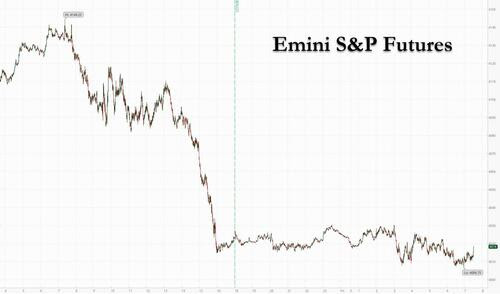

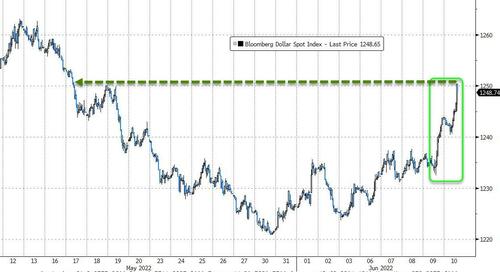

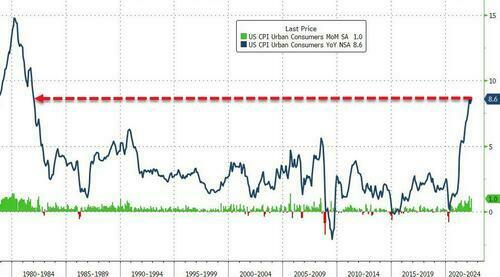

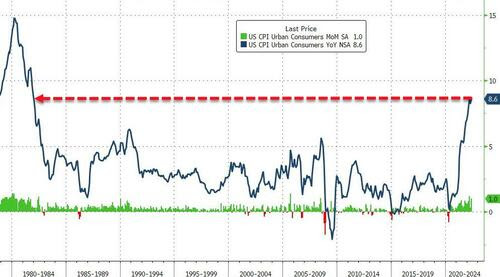

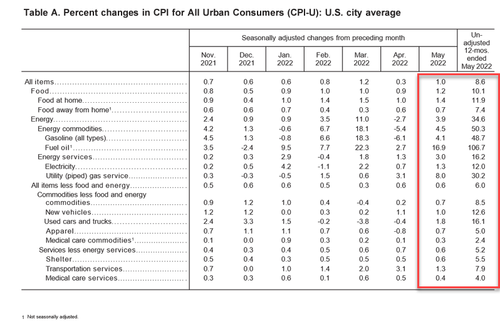

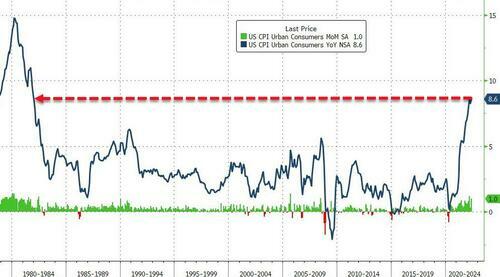

Futures Brace To Spike Higher (Or Lower) Depending On Today’s CPI Number

FRIDAY, JUN 10, 2022 – 07:51 AM

After a furious late-day selloff on Thursday as markets digested the probability of another red hot inflation number, S&P Futures traded in a narrow range on Friday ahead of the crucial May CPI Print which will dictate the path of Federal Reserve policy (it means the difference between a 25bps and 50bps Sept rate hike… or 0bps), and which is expected to come in 8.3% Y/Y and 0.7% M/M for headline and 5.9% Y/Y and 0.5% M/M for core. S&P 500 contracts fluctuated between modest gains and losses, while Nasdaq 100 futures rose about 0.4% as of 7:30 a.m. ET. The dollar rose slightly, although it has been trading largely flat throughout the session. The yield on the 10-year Treasury is unchanged at 3.04%, while the 2-year Treasury yield rose about 3.4 basis points to 2.8455%. Gold and bitcoin fell. Oil rose.

In premarket trading, DocuSign slumped 25% after the e-signature company earnings missed expectations and cut its full-year billings outlook. Netflix and Roblox declined after Goldman Sachs analysts cut their recommendations on the stocks to sell from neutral amid macroeconomic concerns. Bank stocks are lower in pre-market trading Friday as investors await the release of key inflation data later this morning. In corporate news, Credit Suisse shares hovered near the lowest in at least three decades after State Street Corp. denied that it is interested in taking over the Swiss lender. Here are some other notable premarket movers:

- Stitch Fix (SFIX US) slides 14% in premarket trading as analysts cut their price targets on the online styling platform operator after the company reported earnings that missed estimates and confirmed plans to cut 15% of its salaried workforce.

- Advanced Micro Devices (AMD US) shares rose 1.2% in premarket trading after the chipmaker hosted an analyst event where it outlined long-term financial targets, Xilinx synergies and its plans to take more market share from peers.

- Chinese stocks in US bounce back in premarket trading, a day after the group posted its biggest one-day drop since May. Alibaba (BABA US) rises 3.8% as investors assess whether Beijing’s easing in regulatory crackdown on internet firms supports speculation that Ant’s IPO may be revived.

Investors will be closely watching the US inflation reading. An upside surprise would be a setback for both the Fed and markets, raising doubts about how well rates are working to subdue prices rising at a clip of more than 8%.

Policymakers “are looking for ‘clear and convincing evidence’ that inflation in the US is going to start falling back from its eye-watering level,” Nick Chatters, investment manager at Aegon Asset Management, wrote in a note. “Wishful thinking?”

“In an environment where most major developed market central banks are taking aggressive action to bring inflation down, risk assets are likely to remain volatile and struggle to sustain rallies,” said UBS Global Wealth Management CIO Mark Haefele in a note. “This dynamic should persist until there is clear indication that inflation is trending lower, which may not occur until well into the second half of the year.”

Meanwhile, Bank of America strategists said investors are putting billions of dollars into cash and stock funds as they seek protection from surging inflation, citing EPFR Global data. US equities were the primary beneficiaries of inflows with about $13 billion, while bond fund outflows resumed, the data showed.

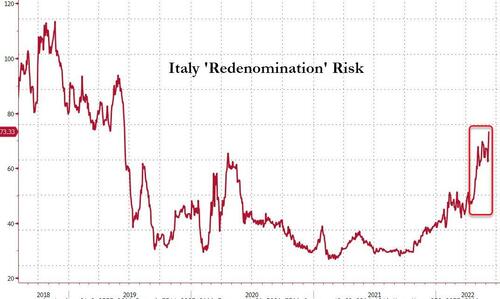

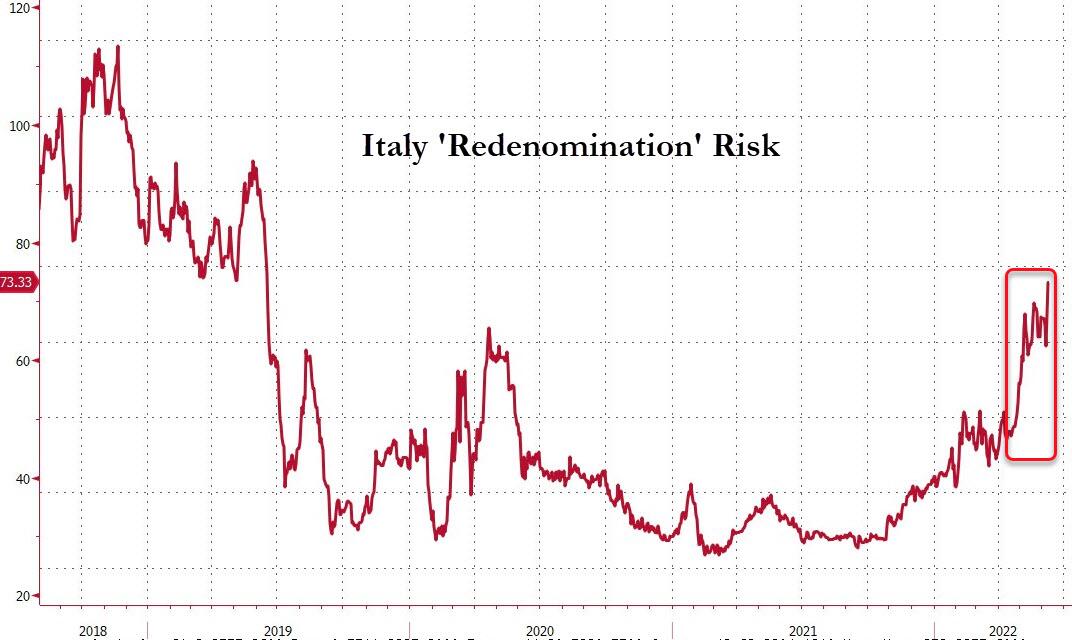

While US rates were also rangebound, Euro-area peripheral spreads continued blowing out as the ECB left a wide room for interpretation on what their anti-fragmentation policy might be while they begin to raise rates. 10y BTP/Bund widens ~6bps to 222bps, short end lags. Bund, Treasury and gilt curves all bull flatten while Greek bond yields hit the highest level since early 2019.

The bond turmoil depressed European markets which saw the stoxx 600 slump 1.5% to session lows, with Italy’s FTSE MIB underperforming regional peers in a weak session for European equities. Euro Stoxx 50 slumps as much as 1.7%. FTSE 100 outperforms but remains down ~1.3%. Real estate, banks and insurance are the worst performing sectors. Italian stocks underperformed as the country’s bonds slid, banks plunged: the FTSE MIB was the worst-performing index among major European countries Friday, with banks dropping the most as Italian bonds slide, following the ECB meeting on Thursday. FTSE MIB -3.5% vs a decline of 1.4% at the Stoxx Europe 600 Index. BPER -11%, BAMI -6.9%, Unicredit -6.7%, Intesa -6.5%.

Here are the biggest European movers:

- Just Eat Takeaway.com shares rise as much as 9.1% after a Bloomberg report that its US unit Grubhub is attracting preliminary interest from private equity firms including Apollo.

- Scandic shares rise as much as 13% after the Swedish hotel group flagged “very strong earnings development” during the second quarter on a “greatly improved” hotel market.

- SAS shares surge as much as 46% after the Danish government reiterated its support for the ailing Scandinavian airline, forgiving and converting its debt and increasing its ownership share.

- Aryzta shares advance as much as 4.2% after Kepler Cheuvreux upgraded the Swiss baker to hold from reduce, citing “credible” new financial targets and improved balance sheet.

- Ericsson shares fall as much as 4.6% after the Swedish telecommunications manufacturer said the US SEC will open an investigation into the company’s handling of a 2019 corruption scandal.

- Shipping stocks drop again, with Maersk down as much as 5.8% and Hapag-Lloyd as much as 7.2% lower, amid ongoing concerns about demand and the normalization of freight rates.

- Swisscom shares slump as much as 4.6% after UBS cut the telecommunication company to a sell recommendation from neutral, citing “a number of headwinds.”

- Credit Suisse shares fall as much as 6% on Friday, extending yesterday’s 5.6% slump after State Street said it is not pursuing any acquisition of the Swiss lender.

- Ageas shares fall as much as 2.5% as ING initiates coverage on the insurer with a hold recommendation, saying that while the potential is there, the “timing is not right.”

Earlier in the session, Asian stocks dropped, giving up gains for the week, as chipmakers slid amid renewed concerns about inflation and Covid lockdowns in Shanghai. The MSCI Asia Pacific Index declined as much as 1.2%, with tech and financials sectors the biggest drags. Most major benchmarks in the region were down, with gauges in Japan, South Korea, Australia, India, the Philippines and Indonesia each falling more than 1%. The region’s semiconductor heavyweights, TSMC and Samsung Electronics, were the largest contributors to the Asian stock benchmark’s decline. China’s tech shares reversed early losses as investors bet the worst of Beijing’s crackdown on the sector may be over even as the nation’s regulator denied a Bloomberg News report that it started early-stage discussions on reviving the initial public offering of Ant Group.

Asian shares also slumped after the European Central Bank opened the door to a half-point interest-rate hike in the fall. In addition, sentiment was fragile as investors monitored virus flare-ups in China. Read: Covid Flares Again in Shanghai, Putting Areas Back in Lockdown “We are seeing a reversal in several developments that had helped markets rebound in the past weeks,” said Heo Pil-Seok, chief executive officer at Midas International Asset Management in Seoul. “With China possibly entering lockdowns again and the ECB moving to raise interest rates, all of these are pouring cold water on markets which believed fear about inflation had eased.” Asia’s equities benchmark is on course for its first weekly loss in four weeks, paring a rebound from a two-year low hit in May

Australian stocks tumbled, with the S&P/ASX 200 index falling 1.3% to 6,932.00, its lowest level since Jan. 27. The gauge notched its biggest weekly loss since April 2020, down 4.2%. Global growth concerns and the RBA’s larger-than-expected rate hike weighed on investor sentiment. All sectors dropped Friday, with real estate and consumer discretionary shares leading declines. In New Zealand, the S&P/NZX 50 index fell 0.7% to 11,136.28.

In FX, the Bloomberg Dollar Spot Index was steady after rising to the highest in three weeks in the previous session. NZD and AUD are the strongest performers in G-10 FX, CAD and GBP underperform. USD/JPY drifts back up toward a 134-handle. Economists see US consumer costs rising 8.3% year-on-year in May when data is released later Friday. Investors are taking profits on dollar-long bets, said Patrick Bennett, strategist at Canadian Imperial Bank of Commerce in Hong Kong. “Dollar gains have dominated recently, there appears to be some squaring into US CPI”.

In rates, the Treasuries curve has extended Thursday’s flattening move ahead of today’s CPI print, with 10Y yield trading roughly unchanged from yesterday at 3.04%, and 2s10s, 5s30s near session lows in early US trading following a wider flattening move seen across German curve as markets continue to digest Thursday’s ECB policy announcement. Into front-end Treasuries underperformance, 2- and 3-year yields reach year-to-date highs. US yields are cheaper by up to 3.5bp across front-end of the curve while 7-year out to long-end are richer by up to 2bp with 20- year sector outperforming — 2s10s, 5s30s spreads flatter by 4.3bp and 2.2bp at ~18bp and ~7bp respectively. IG dollar issuance slate empty so far; Thursday session was quiet and Friday also expected to be subdued with CPI data release. In Europe, the German 2s10s, 5s30s curve are both flatter by over 5bp while bunds outperform Treasuries by ~1.5bp over early European session.

In commodities, oil rose after erasing an earlier loss triggered in part by new restrictions in Shanghai. Chinese President Xi Jinping called on his government to adhere “unwaveringly” to its Covid Zero policy, while at the same time striking a balance with the needs of the economy. WTI rose 0.3% to trade near $121.80. Most base metals trade in the red; LME nickel falls 1.5%, underperforming peers. Spot gold falls roughly $5 to trade near $1,842/oz.

Bitcoin is softer on the session, though only modestly so, and as such remains in recent ranges which continue to pivot USD 30k.

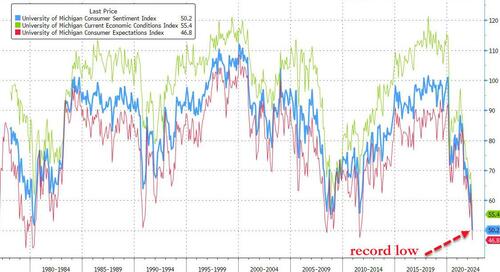

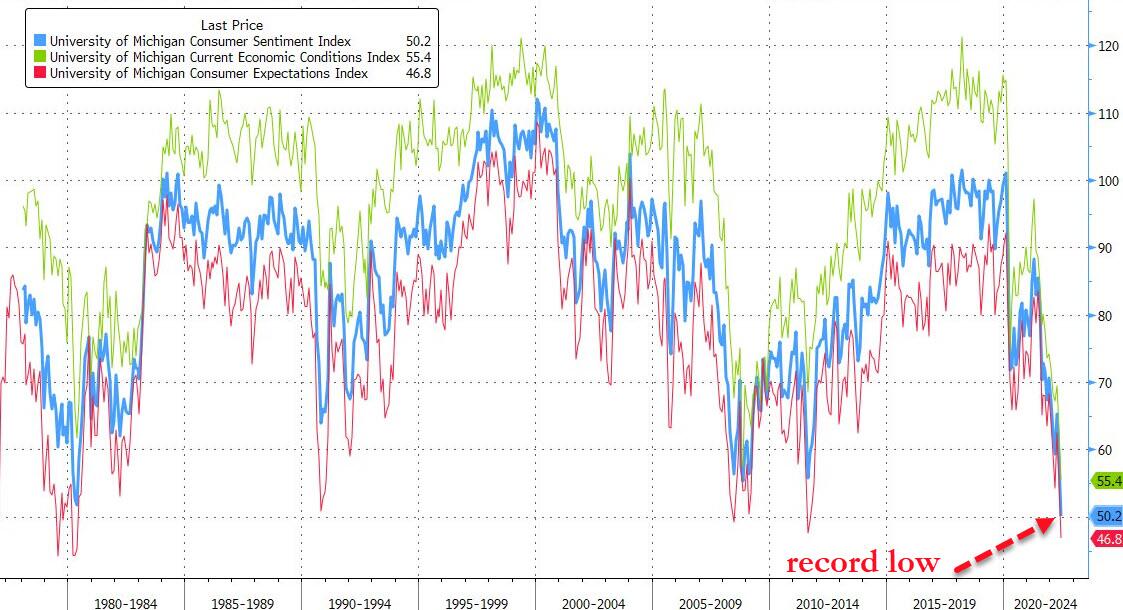

Looking at the day ahead now, economic data slate includes May CPI (8:30am), June University of Michigan sentiment (10am) and May monthly budget statement (2pm). Central bank speakerss include the ECB’s Holzmann and Nagel.

Market Wrap

- S&P 500 futures up 0.2% to 4,022.75

- STOXX Europe 600 down 1.3% to 428.90

- MXAP down 0.9% to 166.71

- MXAPJ down 0.8% to 551.64

- Nikkei down 1.5% to 27,824.29

- Topix down 1.3% to 1,943.09

- Hang Seng Index down 0.3% to 21,806.18

- Shanghai Composite up 1.4% to 3,284.83

- Sensex down 1.8% to 54,330.71

- Australia S&P/ASX 200 down 1.3% to 6,931.98

- Kospi down 1.1% to 2,595.87

- Brent Futures little changed at $122.99/bbl

- German 10Y yield little changed at 1.40%

- Euro little changed at $1.0618

- Gold spot down 0.1% to $1,846.06

- U.S. Dollar Index little changed at 103.24

Top Overnight News from Bloomberg

- Shanghai will briefly lock down most of the city this weekend for mass testing as Covid-19 cases continue to emerge, causing more disruption and triggering a renewed run on groceries days after exiting a grueling two-month shutdown.

- Investors are putting billions of dollars into cash and stock funds as they seek protection from surging inflation.

- A selloff in Europe’s weakest bond markets is showing no signs of easing, piling pressure on the European Central Bank to make clearer how it plans to keep diverging borrowing costs contained.

- Public confidence in the Bank of England is at an all-time low, with Britons expecting above-target inflation to persist for years

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly negative after the glum mood rolled over from global counterparts with a hawkish ECB meeting and fresh COVID restrictions in Beijing stoking growth slowdown concerns. ASX 200 was dragged lower by the energy and mining-related sectors after recent declines in underlying commodity prices and with participants taking risk off the table ahead of the extended weekend in Australia. Nikkei 225 retreated beneath the 28k level amid the broad risk aversion and as the domestic currency found some reprieve from its weakening trend. Hang Seng and Shanghai Comp. were both initially subdued after weak earnings and Ant Group’s denial regarding plans to relaunch its mammoth IPO, while participants also digested the mixed inflation data from China and the latest COVID restrictions in Beijing, although the mainland then spent the session recouping lost ground.

Top Asian News

- South Korean Transport Ministry held a meeting with the trucker union leadership on Friday and is holding a working-level meeting with the union, while it added that about 7,500 unionised truck drivers were expected to strike today. It was also reported that striking South Korean truckers halted and turned around non-union truckers from trying to enter the Ulsan petrochemical complex and the movement of containers through South Korea’s Ulsan port was totally suspended amid the trucker strike, according to Reuters.

- Beijing City reports 21 (prev. 3) cases during the 15 hours to 3pm on June 10th, according to an official, via Reuters.

- Japan Officials Fire Warning on Forex With Yen Near 1998 Low

- Top Toyota Supplier Denso Mulls $3 Billion Chip Unit Spinoff

- China’s Moderating Inflation Leaves Room for More Easing

- Covid Lab Leak Theory Needs More Inquiry, WHO Advisers Say

The mood across European equities remains downbeat as the region plays catch-up to yesterday’s Wall Street tumble; Euro Stoxx 50 -1.6%. European cash bourses trade lower across the board with the Dutch AEX and UK’s FTSE 100 slightly more cushioned. Sectors in Europe are all lower but largely hold a defensive bias; EZ Periphery banks continue to lag post-ECB while Luxury slips on China/COVID updates. US equity futures trade with modest gains with the ES -0.2% just about holding onto the 4,000 handle. TSMC (2330 TW) – May (TWD): Sales 185.7bln, +65% YY, +7.6% MM. January-May Sales 849.3bln, +44.9% YY.

Tesla (TSLA) CEO Musk says the next FSD beta version will be coming out in two weeks. Amazon (AMZN) is planning to pull out of the USD 7.7bln race for IPL cricket rights, according to Bloomberg.

Top European News

- On the ECB decision, one dovish member said “impression is everybody lost”, described the EGB and EUR downside as “..not what you want”; conversely, a hawk described the meeting as having gone very well. Additionally, re. QT, a dovish member does not believe this will happen any time soon, according to FT.

- UK employers hired staff at the slowest pace since early 2021, according to a survey by REC cited by Reuters which showed the measure declined for a sixth consecutive month to 59.2 from 59.8 M/M but remained in expansion territory above the 50 benchmark level.

- Former UK Brexit Minister Frost has warned that PM Johnson must deliver a “new Conservative vision for Britain” or risk being removed from his position by the autumn, according to the Telegraph.

FX

- DXY recovers from overnight lows of 103.04 heading into the US CPI release.

- Antipodeans stand as the current G10 outperformers with NZD leading the charge, with the AUD/NZD cross subsequently paring back recent ground and falling under 1.1100.

- CAD is under some pressure pre-jobs data; USD/CAD today sees its 100 DMA at 1.2700, 21 DMA at 1.2722, and 50 DMA at 1.2723.

- EUR and GBP are now under pressure as the dollar recovers from early losses.

- The Yen attempts to claw back some ground after the BoJ, MoF, and FSA expressed concern in a joint release.

Fixed Income

- BTP-Bund spread continues to widen, out to 234bp thus far, though, offset amid incremental Bund upside via Holzmann.

- Hawk Holzmann took perhaps an incrementally more ‘dovish’ line than usual re. September’s hike increment, alluding to a non-standard increment move.

- USTs are essentially unchanged at 117.30+ pre-CPI though the yield curve continues to flatten in-line with EGBs and after well received long-end issuance.

Commodities

- WTI and Brent futures are choppy with relatively modest intraday gains following yesterday’s China-induced weakness.

- WTI Jul’ resides just under USD 122/bbl (vs low 120.09/bbl), whilst Brent Aug’ trades around USD 123.50/bbl (vs low 121.60/bbl).

- Kuwait set July KEC crude OSP for Asia at Oman/Dubai +USD 6.15/bbl vs prev. premium of USD 4.35/bbl in June, according to Reuters.

- A minimum of four north-Asian refiners are facing crude oil supply cuts from Saudi in July, according to Reuters sources.

- Peruvian communities said they are ready to end the 51-day shutdown at MMG’s (1208 HK) Las Bambas mine and allow the copper mine to restart, while the mine will not begin construction of the Chalcobambas pit during a 30-day truce and the Peru government will lift the state of emergency in the Las Bambas mine area, according to Reuters.

- Metals markets are relatively tentative and uneventful; spot gold trades on either side of its 21 DMA (1,844/oz), while base metals similarly hold a mild downside bias.

US Event Calendar

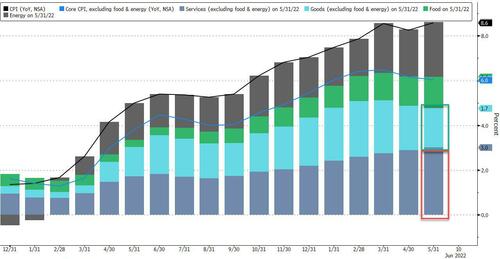

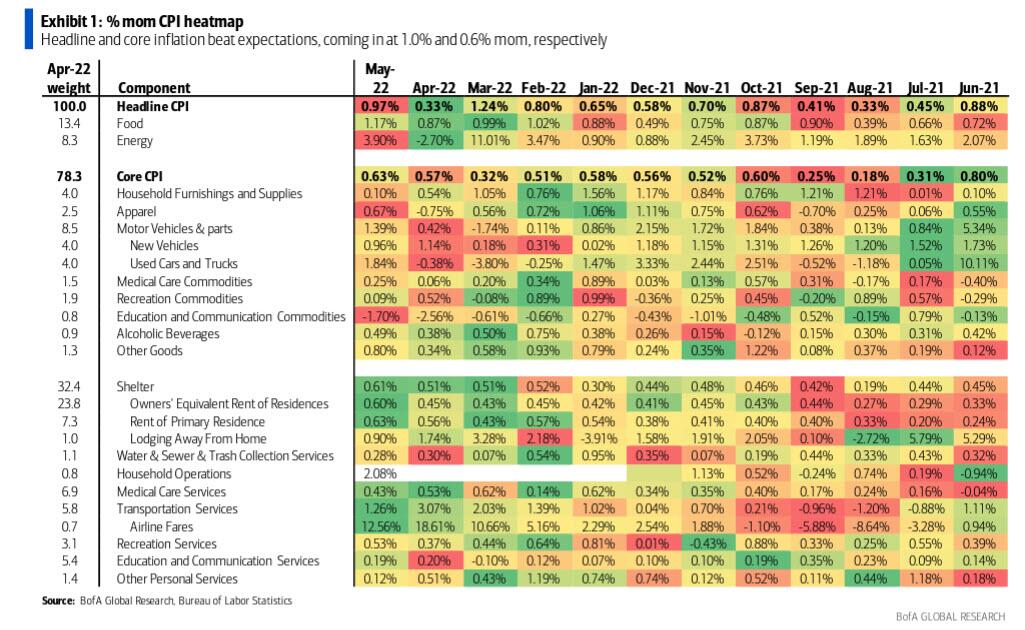

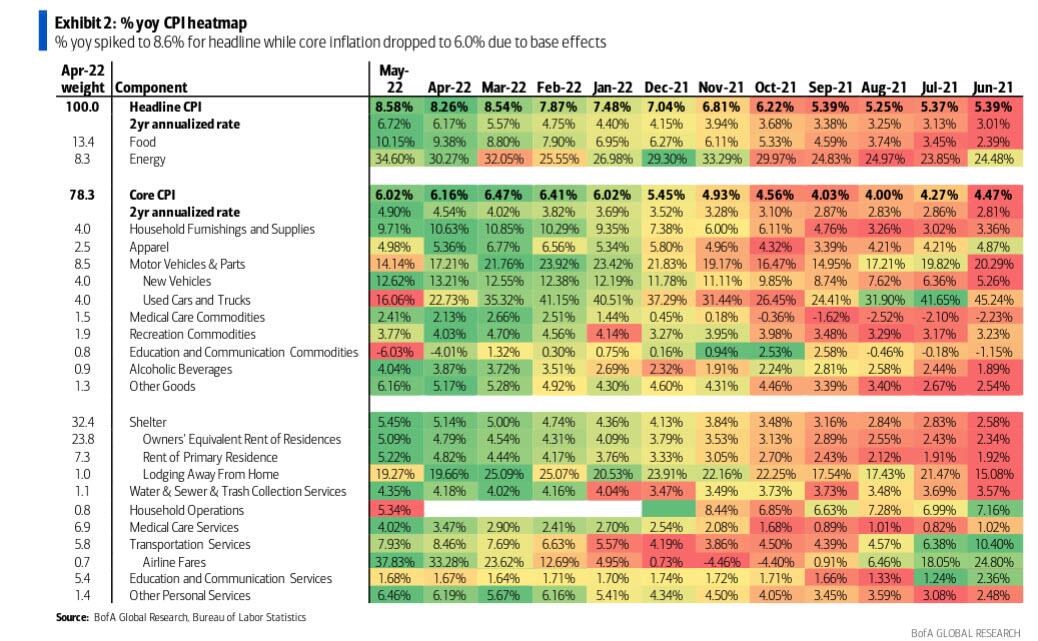

- 8:30am: US CPI MoM, May, est. 0.7%, prior 0.3%; YoY, May, est. 8.3%, prior 8.3%

- 8:30am: US CPI Ex Food and Energy MoM, May, est. 0.5%, prior 0.6%; YoY, May, est. 5.9%, prior 6.2%

- 2pm: US Monthly Budget Statement, May, est. -$136.5b, prior -$132.0b

DB’s Jim Reid concludes the overnight wrap

I’ll be another year older on Sunday which is a sobering thought. In addition, yesterday marked 10 years since I proposed to my wife up the top of a mountain. I wasn’t 100% sure I was doing the right thing at the time but am certain of it now! She was 100% certain it was the happiest day of her life back then, but now she’s not so sure. Anyway, we shall be celebrating both tomorrow night in a rare evening out alone.

It’s been another dramatic 24 hours in markets as the ECB kicked off an incredibly busy week ahead of macro events, including US CPI today, by laying the groundwork for a sustained campaign of rate hikes starting next month. Our European economists’ full ECB wrap, and all new updated rates call, is available here.

The immediate headlines of their decision were much as expected, with a confirmation that net asset purchases would conclude at the end of the month, and that their conditions for rates liftoff had been satisfied. But looking forward, not only did they confirm their intent to hike by 25bps in July, they formally opened the door to a 50bps increase at the subsequent meeting in September, saying that the “a larger increment will be appropriate at the September meeting” if the inflation outlook “persists or deteriorates”. It seems by “persists”, all that need to happen is for their staff inflation forecast for 2024 to at least remain at 2.1%, the level it got upgraded to yesterday. Core CPI was projected to be at +2.3% that year, a bigger move than expected.

More broadly, the ECB’s statement and President Lagarde’s press conference struck a hawkish tone, and the first paragraph of the statement openly acknowledged the inflation challenge and the need to return it back to target. And when it came to a potential tool to deal with fragmentation in bond markets, Lagarde said that they would “deploy either existing or new instruments that will be made available.”