JUNE 13 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1830.30 DOWN $41.55

SILVER: $21.30 DOWN $0.62

ACCESS MARKET: GOLD $1819.25

SILVER: $21.09

Bitcoin morning price: $23,660 DOWN 5,317

Bitcoin: afternoon price: $23,276 DOWN 5701

Platinum price: closing DOWN $37.90 to $939.95

Palladium price; closing DOWN $1713.00 at $1807.15

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 172/200

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,871.500000000 USD

INTENT DATE: 06/10/2022 DELIVERY DATE: 06/14/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 2

118 H MACQUARIE FUT 200

323 C HSBC 5

363 H WELLS FARGO SEC 3

407 C STRAITS FIN LLC 1

624 H BOFA SECURITIES 6

657 C MORGAN STANLEY 1

661 C JP MORGAN 172

700 C UBS 3

709 H BARCLAYS 1

732 C RBC CAP MARKETS 3

905 C ADM 3

TOTAL: 200 200

MONTH TO DATE: 22,053

_____________________________________________________________________________________ TOTAL: 200 200 MONTH TO DATE: 22,053

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 200 NOTICE(S) FOR 20000 Oz//0.6220 TONNES)

total notices so far: 22,053 contracts for 2,205,300 oz (68.594 tonnes)

SILVER NOTICES:

12 NOTICE(S) FILED 60,000 OZ/

total number of notices filed so far this month 1615 : for 8,075,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $41.55

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.48 TONNES INTO THE GLD//

INVENTORY RESTS AT 1068.87 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 62 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.399 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1699 CONTRACTS TO 150,044 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR GOOD $0.13 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.13) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS EVEN THOUGH WE HAD A STRONG LOSS OF 649 CONTRACTS ON OUR TWO EXCHANGES, ALL OF THAT LOSS WAS FROM SPECULATOR SHORTS COVERING.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 13 CONTRACTS OR 65,000 OZ//NEW STANDING: 8,405,000 / // V) GIGANTIC SIZED COMEX OI LOSS/(SPECULATOR COVERING)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -1

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 9 days, total 6812, contracts: 34.060 million oz OR 3.784 MILLION OZ PER DAY. (756 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 34.060 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 34.060 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1699 DESPITE OUR STRONG $0.13 GAIN IN SILVER PRICING AT THE COMEX// FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1051 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 65,000 QUEUE JUMP //NEW STANDING: 8,405,000 OZ // .. WE HAD A VERY STRONG SIZED LOSS OF 649 OI CONTRACTS ON THE TWO EXCHANGES FOR 3.240 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 12 NOTICES FILED TODAY FOR 60,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC 14,934 CONTRACTS TO 509,575 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -57 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE HUGE GAIN IN COMEX OI CAME WITH OUR RISE IN PRICE OF $21.40//COMEX GOLD TRADING/FRIDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //JUST SPECULATOR SHORT COVERING FROM OUR STUPID SPECULATORS.

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP//NEW STANDING: 74.068 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $21.40 WITH RESPECT TO THURSDAY’S TRADING

WE HAD A MAMMOTH SIZED GAIN OF 20,933 OI CONTRACTS 65.287 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6056 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 509,575

IN ESSENCE WE HAVE A MAMMOTH SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 20,933, WITH 14,877 CONTRACTS INCREASED AT THE COMEX AND 6056 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 20,990 CONTRACTS OR 65.287TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6056) ACCOMPANYING THE GIGANTIC SIZED LOSS IN COMEX OI (14,877,): TOTAL GAIN IN THE TWO EXCHANGES 20,933 CONTRACTS. WE NO DOUBT HAD 1) CONSIDERABLE SPECULATOR SHORT COVERING ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 25,000 OZ//NEW STANDING: 74.068 TONNES / 3) ZERO LONG LIQUIDATION//CONSIDERABLE SPECULATOR SHORT COVERING //.,4) STRONG SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

36,049 CONTRACTS OR 3,604,900 OZ OR 112.13 TONNES 9 TRADING DAY(S) AND THUS AVERAGING: 4005 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES: 112.13 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 112.13/3550 x 100% TONNES 3.15% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 112.13 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 1699 CONTRACT OI TO 150,043 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1051 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1051 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1700 CONTRACTS AND ADD TO THE 1051 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF 648 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 3.240 MILLION OZ

OCCURRED DESPITE OUR GAIN IN PRICE OF $0.13 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED DOWN 29.28PTS OR 1.42% //Hang Sang CLOSED DOWN 738.60 PTS OR 3.39% /The Nikkei closed DOWN 836.35 OR 3.01% //Australia’s all ordinaires CLOSED DOWN 1.32% /Chinese yuan (ONSHORE) closed DOWN 6.7361 /Oil DOWN TO 118.73dollars per barrel for WTI and UP TO 120.18 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7371 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7584: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GIGANTIC SIZED 14,877 CONTRACTS TO 509,575 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX INCREASE OCCURRED WITH OUR STRONG GAIN OF $21.40 IN GOLD PRICING FRIDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (6056 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ARE CAUGHT. THE COMMERCIALS WILL SLAUGHTER THESE GUYS WHEN THEY THINK THE TIME IS RIGHT

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6056 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :6056 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6056 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A MAMMOTH SIZED TOTAL OF 20,933 CONTRACTS IN THAT 6056 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GIGANTIC SIZED COMEX OI GAIN OF 14,877 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF GOLD $21.40.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (74.086),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.086 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $21.40) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS/COMMERCIAL LONGS// SPECULATOR SHORTS ANNIHILATED//// WE HAVE REGISTERED A MAMMOTH SIZED GAIN OF 65.111 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.068 TONNES)…

WE HAD XXX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 20,932 CONTRACTS OR 2,093,200 OZ OR 65.11 TONNES

Estimated gold volume 229,948/// good/raid

final gold volumes/yesterday 287,429 /good/cpi

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 13

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 163,095.984 oz Brinks JPMorgan Loomis 5000 kilobars 4 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 200 notice(s) 20000 OZ 0.6229 TONNES |

| No of oz to be served (notices) | 1760 contracts 17,600 oz 5.474 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22053 notices 2205300 OZ 68.594 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

3 customer withdrawals:

i) Out of Brinks: 2212.380 oz

ii) Out of JPMorgan: 160,755.000 oz 5,000 kilobars)

iii) Out of LOOMIS: 128.604 oz (4 kilobars)

total withdrawal: 163,095.984 oz

ADJUSTMENTS: 2 dealer to customer

Malca 110,920,950 oz

Manfra: 55,367.987 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1960 contracts having GAINED 222 contracts

We had 28 notices filed on FRIDAY so we GAINED 250 contracts or an additional 25,000 oz will stand for gold in this very active month of June

July has a LOSS OF 84 OI to stand at 2056

August has a GAIN of 12,995 contracts DOWN to 429,489 contracts

We had 200 notice(s) filed today for 20,000 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 200 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 172 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (22,053) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 1960 CONTRACTS ) minus the number of notices served upon today 200 x 100 oz per contract equals 2,381,300 OZ OR 74.068 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (22,053) x 100 oz+ (1960) OI for the front month minus the number of notices served upon today (200} x 100 oz} which equals 2,381,300 oz standing OR 74.068 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74,086 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,331,163.529 oz 72.5 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,389,710.781 OZ

TOTAL ELIGIBLE GOLD: 16,611,948.775 OZ

TOTAL OF ALL REGISTERED GOLD: 17,777,761.606 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,466,598.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 13

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 699,519.170 oz Delaware CNT JPM |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 1,185,661.200 oz CNT Delaware JPMorgan |

| No of oz served today (contracts) | 12CONTRACT(S)60,000 OZ) |

| No of oz to be served (notices) | 66 contracts (330,000 oz) |

| Total monthly oz silver served (contracts) | 1615 contracts 8,075,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) zero dealer deposits

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 3 deposits into the customer account

i) Into JPMorgan: 587,266.200 oz

ii) Into Delaware: 998.200

iii) Into CNT 587,266.2000 oz

total deposit: 1,185,661.200 oz

JPMorgan has a total silver weight: 171.465 million oz/338.6087 million =50.71% of comex

Comex withdrawals: 3

i) Out of CNT 71,468.710 oz

ii) Out of Delaware 989.480 oz

iii) Out of JPMorgan: 627,061.020 oz

total withdrawal 699,519.170 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.984 MILLION OZ

TOTAL REG + ELIG. 338,087 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 78 HAVING LOST 2 CONTRACTS.

WE HAD 15 NOTICES FILED ON FRIDAY SO WE GAINED 13 CONTRACTS OR AN ADDITIONAL 65,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 8856 CONTRACTS DOWN TO 72,721 CONTRACTS.

AUGUST GAINED 11 CONTRACTS TO STAND AT 983

SEPTEMBER HAD A GAIN OF 6010 CONTRACTS UP TO 53,510 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 12 for 60,000 oz

Comex volumes:103,708// est. volume today// strong//raid

Comex volume: confirmed yesterday: 99,047 contracts ( strong/CPI report )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1615 x 5,000 oz = 8,075,000 oz

to which we add the difference between the open interest for the front month of JUNE(78) and the number of notices served upon today 12 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1615 (notices served so far) x 5000 oz + OI for front month of JUNE (78) – number of notices served upon today (12) x 5000 oz of silver standing for the JUNE contract month equates 8,405,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1065.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 544.399 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

Fatal Macro Warnings: We’re Gonna Need A Bigger Boat

SUNDAY, JUN 12, 2022 – 10:30 AM

Authored by Matthew Piepenburg via GoldSwitzerland.com,

As one who loves metaphor, I can’t help but notice the recent and varying range of metaphorical macro warnings.

JP Morgan’s Jamie Dimon, for example, is now predicting a “market hurricane” ahead, which Peter Schiff has recently upgraded to a “Category 5.”

Meanwhile, the always blunt Michael Burry has compared the trajectory of our market economy and macro warnings to “watching a plane crash.”

In short, the bull vs. bear debate is behind us; even the TBTF banks are now openly alarmed.

The Shark Fins Approach

In fact, current macro warnings are more suggestive of a market shark rather than bear, and borrowing a line from Speilberg’s Jaws, we are all “gonna need a bigger boat” as these dorsal-finned macro warnings begin circling in plain sight.

Specifically, we are seeing three separate macro warnings rising simultaneously, each of which are eerily familiar to the pre-2008 conditions which preceded the last global implosion.

In short: Cue the John Williams music.

Shark-Fin 1: Counterparty Risk

As we’ve argued ever since the September 2019 implosion of the reverse repo market, this was a very big deal.

Of course, the corporate media and politicized Fed tried to downplay the repo crisis as Powell was losing control of the rates markets and banks were losing trust for each other (and each other’s collateral.)

The financial “leadership” were hoping an intentionally confusing and complex reverse repo market would be too difficult for the average citizen-investor to grasp. Thus, the 2019 Fed nervously whistled past that ticking timebomb as it dumped trillions of mouse-click money into the repo morass.

But to make better sense of these repo markets, let’s keep things clean and simple.

The Repo Fins Explained

The reverse repo market is a place where loans keep markets and banks greased in short-term (typically over-night) liquidity, as liquidity (i.e., borrowed money) is the grease that makes our debt-soaked, over-levered and counter-party heavy markets go round.

Given this important “grease,” when the counterparties in the reverse repo markets lose trust in each other, the wheels of the markets start to squeak, shake, rattle and roll…off.

In September of 2019, TBTF Bank 1 essentially stopped trusting TBTF Bank 2’s balance sheet, and thus wouldn’t lend each other money at normal rates.

The distrusting banks chose instead to charge each other painful rates, skyrocketing from the sub 2% range to the 10% range in one trading day.

That’s a counter-party crisis colliding with a liquidity crisis. Or, more simply: A trust crisis.

Net result? The Fed’s money printers came in as a repo lender of last resort, tossing trillions of “loaned” grease into this otherwise dysfunctional repo marriage among the big banks.

Counterparty Dysfunction Explained

Once again, and unbeknownst to just about everybody, those days of dysfunctional liquidity marriages (i.e., distrust) have returned.

As of April 2021, the Fed has been making daily loans into the reverse repo market to the skyrocketing tune of $2T a day.

Please re-read that last line.

The eye-opening chart below looks a lot like a shark fin…

What ghastly data like the above chart boils down to is the Fed is providing the Money Market with mind-numbingly massive doses of daily liquidity to keep it alive. They do this by swapping out Treasuries for Money Market funds in what is the churning equivalent to treading water with fiat dollars.

Some experts claim that this insane level of Fed “support” is due to the TBTF banks off-loading deposits from their balance sheets onto the Fed’s balance sheet in order to meet the Basel 3 requirements.

A more likely scenario, however, boils down to counter-party distrust and hence counter-party risk among Wall Street’s broken moving parts.

That is, fund managers who run Money Market accounts no longer want to park their money with the TBTF banks for the simple reason that they see trouble ahead and frankly don’t trust them.

No wonder Jamie Dimon is so scared of hurricanes…

Stated otherwise: Distrust in the system is rising like a shark fin and the money markets are now swimming toward a “bigger boat”—namely the Fed.

Such distrust among counterparties is a major macro warning. In fact, it was precisely this kind of counterparty distrust/risk (and bad collateral) which brought down Bear Sterns and Lehman in 08.

Just saying…

Shark Fin 2: The Shift from Hysteria to Fear

Markets, no matter how artificially stimulated or can-kicked, move in cycles which are driven by the availability (or unavailability) of liquidity.

When cash is cheap (i.e., when rates are low), markets hysterically rip; and when cash is expensive (i.e., when rates rise), markets fearfully tank.

Ever since November of 2021 when Powell “forward guided” a June 2022 “tightening” of liquidity, markets have been slowly (and fearfully) tanking, as “tightening” is just a fancy way of telegraphing a rate hike.

And as stated above, rate hikes matter…They turn hysteria into fear.

Between 2006 and 2008, for example, we saw a crappy-credit housing market climb in euphoria and then tank in fear.

Today, as rates slowly rise into a Powel 2022 “taper,” today’s too-much-credit housing market will make a similar slow (and then rapid) shift from euphoria to “uh-oh.”

Equally (and eerily) reminiscent of the pre-2008 pivot from euphoria to fear is the teetering “tech will save you” meme, which like Cathie Wood’s ARKK fund, is tanking in real-time despite her rising spin-talk on primetime.

In short, we are seeing signs all over the hype-driven NASDAQ and S&P of a classic bear-trap, of which BTC was just one among many.

What’s far scarier today, however, is that the 2008 crisis (bubble) was limited to real estate; today, we are in an everything bubble, from meme stocks, inflated bonds and over-priced housing to bloated art, over-paid celebrity chefs and pricy used cars.

And remember: ALL bubbles pop, despite what your broker, central banker or 20-something financial journalist might tell you.

Shark Fin 3: MBS Toxic Waste

For those who remember 2008, then you also remember all those crappy mortgages packaged into Mortgage-Backed Securities (MBS) which Wall Street then syndicated to your broker like candy and which the rating agencies equated to magical beans.

You also know those MBS were toxic waste. And as Chernobyl reminds, toxic waste doesn’t just go away—it lingers and festers in deep, dark pits.

Sadly, the MBS waste of the 2008 era is still lingering and festering in the deep and dark pits of the Fed’s toxic and bloated balance sheet.

But now Powell wants to unload that MBS waste.

Great idea, but who wants to buy toxic waste?

How a Real Estate Bubble Dies

If, Powell sticks to his June unloading of unwanted MBS, this will add more supply of an asset class for which there is no demand.

And as high school economics reminds, such a over-supply & drying dynamic means tanking prices for those MBS radiation assets.

But again, who will buy radiation assets?

Sadly, the big banks will, which means they’ll now have more older and crappier MBS added to their balance sheets of the newer, less crappy loans, which they float through Freddie and Fannie to turn into more MBS.

But given the increasing supply and tanking demand for these MBS, their prices will go nowhere but south, which means their yields and hence interest rates (i.e., tomorrow’s mortgages) will have nowhere to go but north.

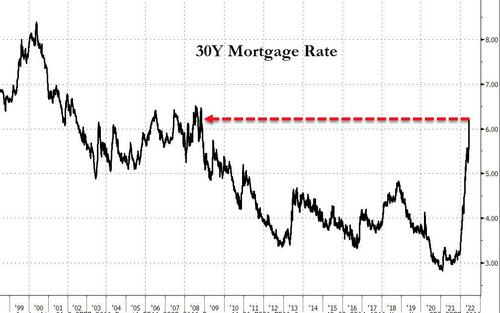

After all, banks survive by lending at a risk premium. As the Fed slowly takes the Fed Funds Rate from zero to 75 bps or more, the mortgage rates must rise at a much greater pace and slope, already climbing from 3% to 5% to date.

And that, folks, is how a housing bubble ends.

Where to Hide?

Investors facing these macro warnings and shark fins need a bigger boat.

Needless to say, our view lies partially in gold, which detractors will attribute to sell-side bias rather than informed conviction, private common sense, or a basic understanding of math or history.

As we’ve warned for years, all fraudulent banking, currency and market systems eventually collapse under their own weight.

This slow collapse is already in play, as the NASDAQ, S&P, TLT and even Muni bonds have all seen near 20% losses thus far into 2022.

Meanwhile, us boring gold investors are having to defend the only primary asset category that has kept its nose above the water level this year; we are constantly asked why gold is not ripping when in fact it has already done a noble job of not tanking.

Gold’s Bull Cycle Is Just Beginning

From its 2009 low to its high late last year, the Fed-created U.S. stock market became the biggest bubble in modern history.

But we believe the gold market’s rise has not even begun. In 1980, when gold topped an 8X move in just 3 years, stocks were flat. If anything, the only “bubble” then was gold itself.

But until recently, the only bubbles in sight were risk assets (from junk bonds to junk tech), which means gold’s time to shine is ahead of us, not behind us.

When considered in the larger backdrop of a commodities cycle, such confidence is an evolution rather than bias.

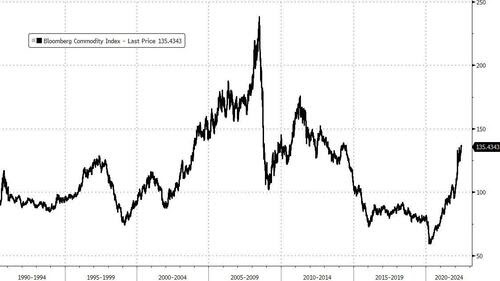

The recent uptrend in the Bloomberg Commodities Index, for example, is admirable, but does not even compare to the highs it reached in 2011 and prior.

In short, commodities in general, and precious metals in particular, are at the beginning of a bull cycle, whereas over-valued risk assets are approaching the traumatic end of theirs.

As for interim price action in gold, we are not promising a straight line. When risk asset markets tank, gold can temporarily follow, as seen in October of 2008 or March of 2020.

But just after joining those tanking markets, gold then divorced the tantrum trend and skyrocketed north. We see an inevitable gold surge in the tumultuous years ahead, and as investors rather than speculators, time is clearly on our side.

Still Trust the Fed?

Of course, there are still those who will trust the Fed and the “magical money theories” (MMT) of the so-called experts.

As the great Janet Yellen sits down with Powell and Biden this week, I wonder if anyone in that Oval Office will remind Yellen that she had described inflation as “transitory” throughout 2021, though now it has reached 40-year highs?

I wonder if anyone will remind her that for the entire first half of her term as Fed Cahir, she kept rates stapled to zero, and then took 2 more years just to reach 1.15%, thereby adding low-rate fuel to the current inflationary fire that always follows cheap debt paid for with mouse-klick money?

And I wonder if anyone will remind her that when she sat as President of the San Francisco Fed, her low-rate policies lead directly to the greatest housing bubble (I was there) in that state’s (and our nation’s) history, despite her continued promises that there was no risk of a housing bubble nor any damage to the broader economy?

Has Janet forgotten 2008?

Trust Hard Facts

But if the politico’s wish to pretend and shirk, we at least can be blunt and direct.

In the last 200+ years, 98% of all countries with a debt to GDP ratio of > 130% have defaulted via inflation, currency devaluation, restructuring or pure default. (Reinhart & Rogoff)

Sadly, the problem for the U.S., based on the global centric nature of USD structures, means the entire world has a sovereign debt problem.

As I have written and spoken many times, it’s my belief that debt-soaked sovereigns will publicly decry inflation while privately seeking more of it as a Main-Street-crushing “strategy” to inflate away their sovereign debt.

Big brother crushing Main Street? No shocker there…

Such “constructive” default via crippling inflation is a way of defaulting without having to publicly (i.e., politically) confess default, and God knows politicians like Yellen et al never admit to any faults.

Follow the Fed

Furthermore, given that natural supply and demand-driven price discovery (along with basic capitalism) died years ago in what is now a central-bank driven market, the only signal (headwind or tailwind) left for tracking future market direction is based upon central bank policy in general and Powell’s Fed in particular.

I mean let’s be honest: It’s a rigged Fed market, not a stock market.

So, what will Powell do? Will he 1) tighten QE into a topping market (and thus create an historical market blow-off and global meltdown) or 2) pivot, reverse course and start creating more fiat money faster than a bat out of Hell?

No one, of course, can know for certain.

Volatility Ahead

The Fed is in such a ridiculous corner that neither option is a sane option, and thus the base-case is to expect more market volatility ahead as investors stand on the razor’s edge of either a tanking market or a dying (inflated, devalued and debased) currency.

Meanwhile, Powell, Biden and Yellen can meet to “plan a strategy,” which in my mind is akin to Mickey Mouse sitting down with Tweedle-Dee and Tweedle-Dumb to diffuse a timebomb.

All three know that the economic data ahead is getting worse not better (all blamed conveniently on Putin and COVID, rather than the cancerous debt that pre-existed both crises and the insanely toxic policy reactions which they pursued).

Given political preferences for re-election self-interest over the public good or personal accountability, it’s hard to imagine any of these political parties actually confessing a recession with a mid-term election on the horizon.

The U.S. administration is already pre-telegraphing weaker economic data for the coming months, preparing the masses for more pain while pointing fingers at Putin or bat-made (man-made?) virus rather than assuming one iota of personal accountability.

In this backdrop, it is possible that the three stooges above may allow markets to tank by sticking to Powell’s QT schedule and hence “fight” money-supply-driven inflation with a tanking market-price-driven “deflation.”

Even if this desperate option is taken, my guess, and it’s only a guess based on human (political) nature and centuries of historical patterns, is that the Fed will then pivot and crank out the money printing once markets spiral into QT.

In short, I see lots of inflationary, deflationary and then again inflationary forces ahead—all screaming volatility ahead.

In short, amidst these clear macro warnings, I think we’re all gonna need a bigger boat—and mine will have a golden rudder.

END

3. Chris Powell of GATA provides to us very important physical commentaries

Daniela Cambone having left Kitco for Stansberry can no mention gold market rigging

(Chris Powell/GATA)

Having left Kitco for Stansberry, Cambone can abide mention of gold market rigging

Submitted by admin on Sat, 2022-06-11 08:46Section: Daily Dispatches

8:56a ET Saturday, June 11, 2022

Dear Friend of GATA and Gold:

Daniela Cambone couldn’t address gold market manipulation when she was doing interviews for Kitco News, and her successors there still can’t, but this week, now that she is at Stansberry Research, she got around to it during an interview in Zurich with Commodity Discovery Fund manager and financial author Willem Middlekoop.

Cambone invited Middlekoop to explain why gold hasn’t exploded with inflation along with other commodities, to which Middlekoop replied: “We know the gold price is managed by selling all these futures, all this paper gold, this silver, through the Comex” — the New York Commodity Exchange. But, Middlekoop noted by way of a graph, the Comex lately has become much more of a physical market with a lot of metal being taken out of it.

Then Middlekoop elaborated a bit uncomforably for Cambone.

“You’ve been in this industry for a long time,” Middlekoop said. “In your previous job maybe you weren’t allowed to discuss this. But there’s a lot of paper out there and many of those ounces have been sold several times.”

Cambone didn’t dispute him.

Middlekoop, one of whose books is “The Big Reset — The War on Gold and the Financial Endgame,” also said he thinks an international financial reset involving gold is already under way, as indicated by renewed central bank purchases of the monetary metal and the steady increase of the gold price in many currencies besides the dollar. The dollar, he said, will be the last currency to yield to gold.

Cambone’s interview with Middlekoop is 24 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch?v=Qr3Dpw9CsW0

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A good interview of Grandich by Maguire

(GATA/Kinesis)

Grandich, Maguire salute GATA, see gold displacing dollar

Submitted by admin on Fri, 2022-06-10 21:48Section: Daily Dispatches

9:49p ET Friday, June 10, 2022

Dear Friend of GATA and Gold:

Financial analyst Peter Grandich is the guest of London metals trader Andrew Maguire on this week’s “Live from the Vault” program from Kinesis Money, and they salute GATA’s work exposing gold market manipulation.

Grandich believes that the U.S. government’s weaponization of the dollar against Russia and other adversaries marks the beginning of the end of the dollar as the world reserve currency, leading to gold’s ascent. Maguire envisions Russia and China increasingly monetizing gold.

The discussion is 47 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings MONDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7361

OFFSHORE YUAN: 6.7584

HANG SANG CLOSED DOWN 728.60 PTS OR 3.39%

2. Nikkei closed DOWN 836.35% OR 3.01%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX UP TO 104.75/Euro FALLS TO 1.0451

3b Japan 10 YR bond yield: RISES TO. +.253/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 134.54/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED DOWN// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +1.395%/Italian 10 Yr bond yield RISES to 3.71% /SPAIN 10 YR BOND YIELD RISES TO 2.64%…ALL BLOWING UP!!

3i Greek 10 year bond yield RISES TO 4.404//BLOWING UP

3j Gold at $1854.20 silver at: 21.58 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 roubles/dollar; ROUBLE AT 58.80

3m oil into the 118 dollar handle for WTI and 120 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.54DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9930– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0388well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.280 UP 12 BASIS PTS

USA 30 YR BOND YIELD: 3.280 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.27

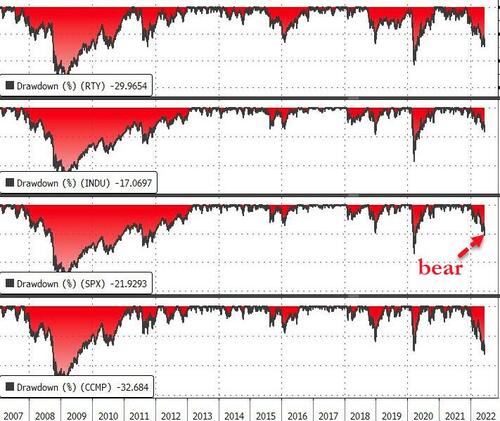

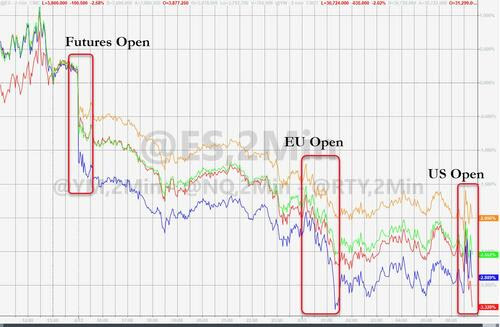

Black Monday: All Hell Breaks Loose As Stocks Plunge Into Bear Market, Curve Inverts, Cryptos Crater

MONDAY, JUN 13, 2022 – 07:57 AM

For all those claiming that stocks had priced in 3 (or more) 50bps (or more) rate hikes, we have some bad news.

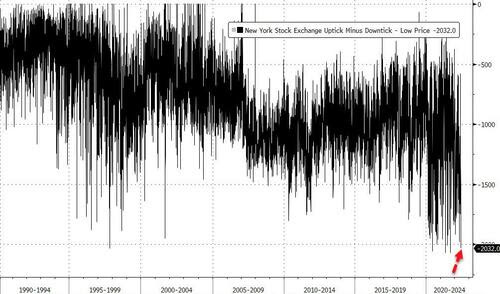

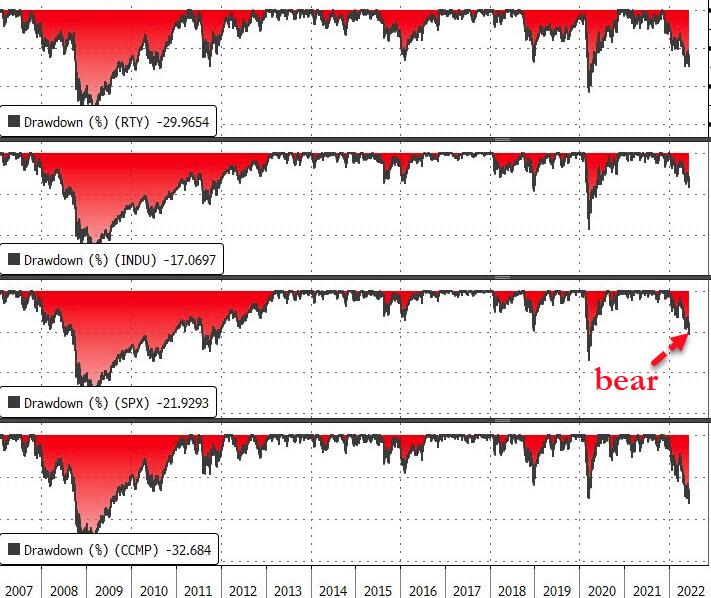

All hell is breaking loose on Monday, with futures tumbling (again) into bear market territory, sliding below the 20% technical cutoff from January’s all time high of 3,856 and tumbling as low as 3,798.25 – taking out the May 10 intraday low of 3,810 – before reversing some modest gains. S&P 500 futures sank 2.5% and Nasdaq 100 contracts slid 3.1%, in a session that has seen virtually everything crash. Dow futures were down 567 points at of 730am ET.

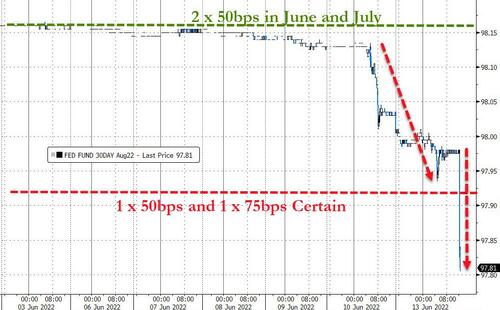

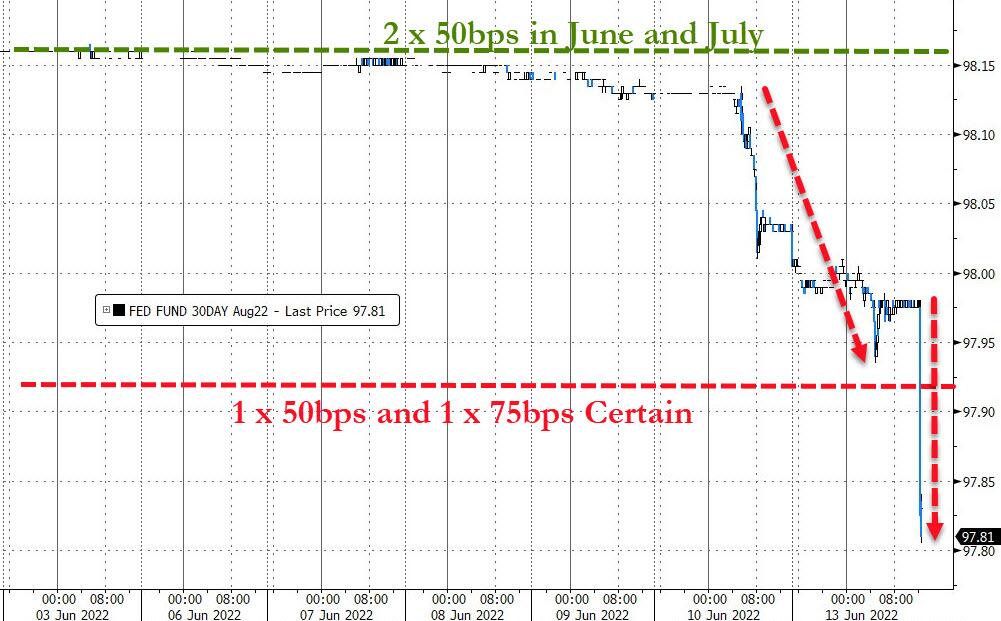

The global selloff – which has dragged Asian and European markets to multi-month lows and which was sparked by a hotter than expected US CPI print which heaped pressure on the Federal Reserve to step up monetary tightening – accelerated on Monday as panicking traders now bet the Fed will raise rates by 175 bps by its September decision, implying two 50-bp moves and one hike of 75 bps, with Barclays and now Jefferies predicting such a move may even come this week. If that comes to pass it would be the first time since 1994 the Fed resorted to such a draconian measure.

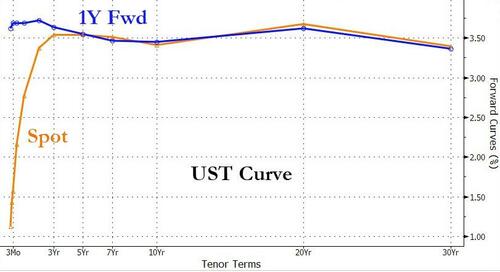

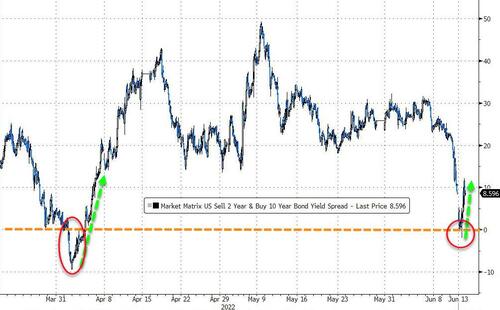

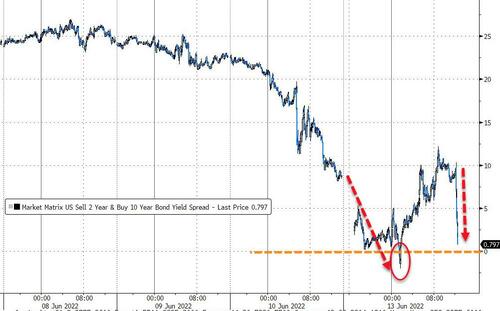

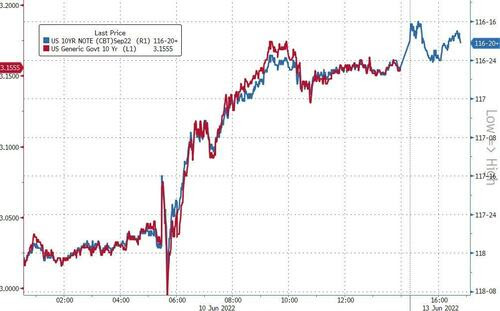

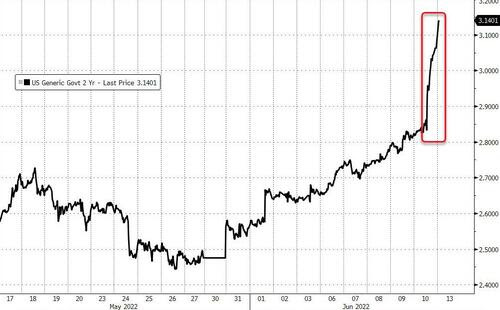

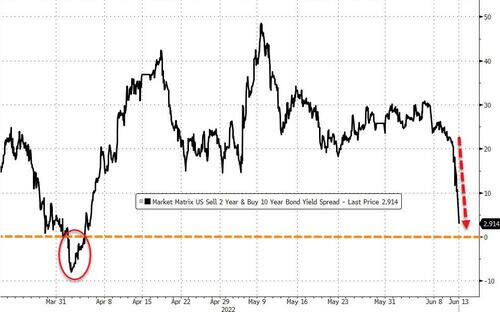

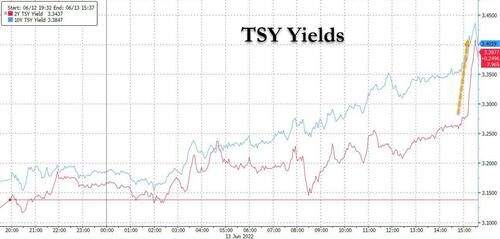

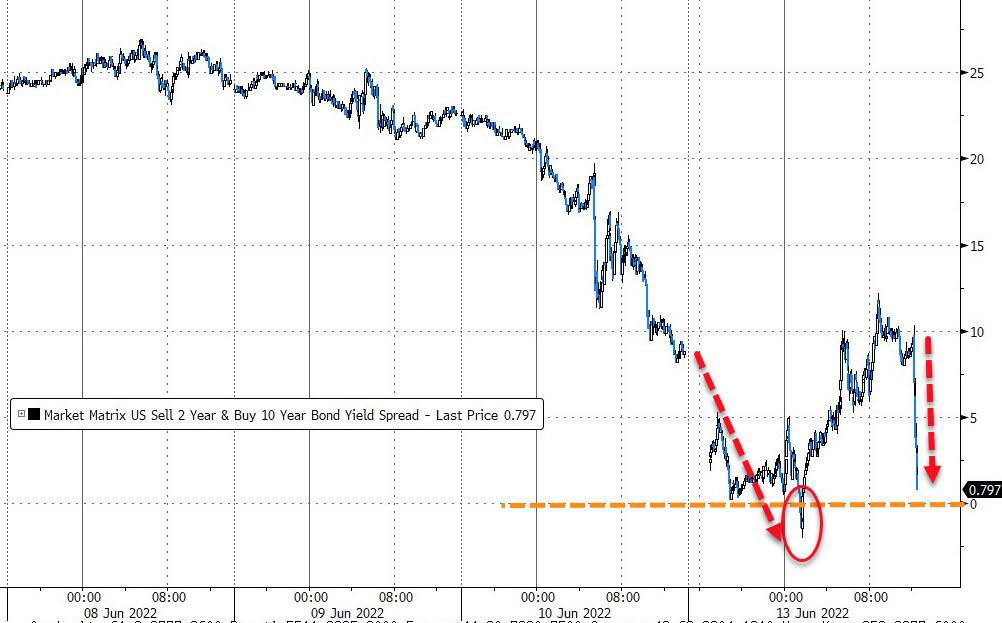

The selling in stocks was matched only by the puke in Treasuries, as yields on 10-year US Treasuries reached 3.24%, the highest since October 2018, yet where 2Y yields sold off more, sending the 2s10s curve to invert again…

… for the second time ahead of the coming recession, an unprecedented event.

Meanwhile, the selloff in European government bonds also gathered pace, with the yield on German’s two-year government debt rising above 1% for the first time in more than a decade and Italian yields exploding and nearing 4%, ensuring that another European sovereign debt crisis is just a matter of time (recall that all Italian net bond issuance in the past decade has been monetized by the ECB… well that is ending as the ECB pivots away from QE and NIRP).

The exodus from stocks and bonds is gaining momentum on fears that central banks’ battle against inflation will end up killing economic growth. Inversions along the Treasury yield curve point to fears that the Fed won’t be able to stave off a hard landing.

“The Fed will not be able to pause tightening let alone start easing,” said James Athey, investment director at abrdn. “If all global central banks deliver what’s priced there are going to be some significant negative shocks to economies.”

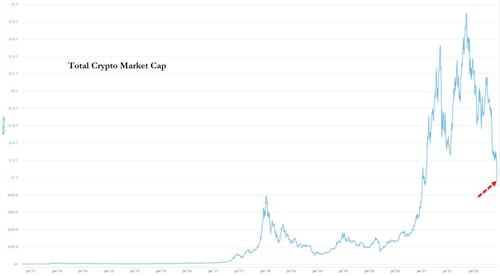

Going back to the US market, big tech stocks slumped in US premarket trading as bets that the Federal Reserve hikes rates more aggressively sent bond yields higher, and Nasdaq futures dropped. Cryptocurrency-exposed stocks cratered as Bitcoin continued its recent decline to hit an 18- month low, precipitated by news that crypto lender Celsius had halted withdrawals…

… which sent Ethereum to the most oversold level in 4 years.

Here are some of the biggest U.S. movers today:

- Apple shares (AAPL US) -3.1%, Amazon (AMZN US) -3.4%, Microsoft (MSFT US) -2.8%, Alphabet (GOOGL US) -3.7%, Netflix -3.8% (NFLX US), Nvidia (NVDA US) -4.5%

- Tesla (TSLA US) shares dropped as much as 3.1% in US premarket trading amid losses across big tech stocks, while the electric-vehicle maker also filed to split shares 3-for-1 late Friday.

- MicroStrategy (MSTR US) -18.4%, Riot Blockchain (RIOT US) -15%, Marathon Digital (MARA US) -14%, Coinbase (COIN US) -12.5%, Bit Digital (BTBT US) -10%, Silvergate Capital (SI US) -11%, Ebang (EBON US) -4%

- Bluebird Bio (BLUE US) shares surge as much as 86% in US premarket trading and are set to trim year-to- date losses after the biotech firm’s two gene therapies won backing from an FDA advisory panel.

- Chinese education stocks New Oriental Education (EDU US) and Gaotu Techedu (GOTU US) jump 8.3% and 3.4% respectively in US premarket trading after peer Koolearn’s endeavors into livestreaming e-commerce went viral and sent its shares up 95% in two sessions.

- Astra Space (ASTR US) shares slump as much as 25% in US premarket trading, after the spacetech firm’s TROPICS-1 mission saw a disappointing launch at the weekend.

- Invesco (IVZ US) and T. Rowe (TROW US) shares may be in focus today as BMO downgrades its rating on the two companies in a note saying it favors alternative asset managers over traditional players as a way to hedge beta risk against the current macro backdrop.

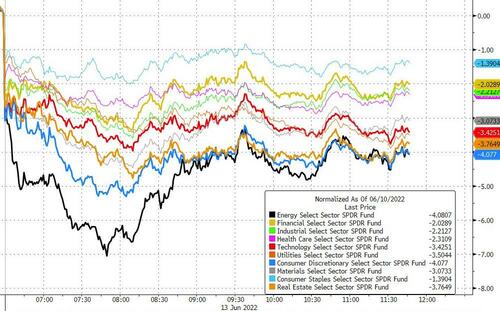

In Europe, the Stoxx 600 also extended declines to a three-month low, plunging mover than 2%, with over 90% of members declining, as meeting-dated OIS rates price in 125bps of tightening, one 25bps move and two 50bps hikes by October. Tech leads the declines as bond yields rise, with cyclical sectors such as autos and consumer products also lagging as recession risks rise. The Stoxx 600 Tech Index falls as much as 4.3% to its lowest since November 2020. Chip stocks bear the brunt of the selloff: ASML -3%, Infineon -4.2%, STMicro -3.6%, ASM International -2.9%, BE Semi -2.8%, AMS -5.3% as of 9:36am CET. As if inflation fears weren’t enough, French banks tumbled after a first round of legislative elections showed that President Emmanuel Macron could lose his outright majority in parliament. Here is a look at the biggest movers:

- Atos shares decline as much as 12%; Oddo says the company’s reported decision to retain and restructure its legacy IT services business in a separate legal entity is bad news for the company.

- Getinge falls as much as 7.6% after Kepler Cheuvreux cut its recommendation to hold from buy, cautioning that headwinds and supply chain challenges may intensify as Covid-related tailwinds abate.

- Elior plunges as much as 15% amid renewed worries over inflation and rising interest rates impacting a caterer that’s still looking for a new CEO following the unexpected departure of the previous one.

- Valneva falls as much as 27% in Paris after saying its effort to salvage an agreement to sell Covid-19 shots to the European Union looks likely to fail.

- Subsea 7 drops as much as 13% after the offshore technology company lowered its 2022 guidance, with analysts noting execution challenges on some of its offshore wind projects.

- French banks decline after a first round of legislative elections showed that President Emmanuel Macron could lose his outright majority in parliament.

- Societe Generale shares fall as much as 4.5%, BNP Paribas -4.2%

- Euromoney rises as much as 4.4% after UBS raises the stock to buy from neutral, saying the financial publishing and events firm’s “ambitious” growth targets for 2025 are broadly achievable.

Earlier in the session, Asian stocks also declined across the board following the hot US CPI data and amid fresh COVID concerns in China. Nikkei 225 fell below the 27k level with sentiment not helped by a deterioration in BSI All Industry data. Hang Seng and Shanghai Comp. conformed to the downbeat mood with heavy losses among tech stocks owing to the higher yield environment and with mainland bourses constrained after the latest COVID outbreak and containment measures.

The Emerging-market stocks index dropped about 3%, falling for a third day in the steepest intraday drop since March, as a fresh high in US inflation sparked concerns that the Fed may need to be more aggressive with rate hikes.

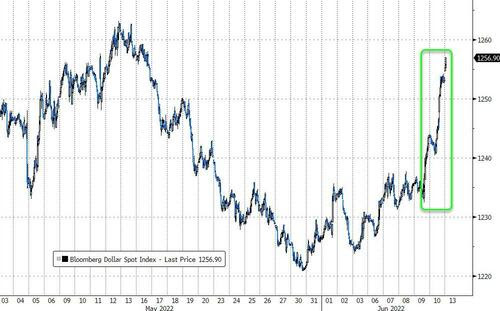

In FX, the Bloomberg dollar rose a fourth day as the dollar outperformed all its Group of 10 peers apart from the yen, which earlier weakened to a 24-year low with NOK and AUD the worst G-10 performers. In EMs, currencies were led lower by the South Korean won and the South African rand as the index fell for a fifth day, the longest streak since April. The onshore yuan dropped to a two-week low as a jump in US inflation boosted the dollar and China moved to re-impose Covid restrictions in key cities. India’s rupee dropped to a new record low amid a selloff in equities spurred by continuous exodus of foreign investors. The euro fell for a third day, touching an almost one-month low of 1.0456. Sterling fell after weaker-than-expected UK GDP highlighted the risks to the economy, with a global risk-off mood adding pressure on the currency, UK GDP fell 0.3% from March. The yen erased earlier losses after earlier falling to a 24-year low while Japanese bonds tumbled, prompting a warning from the Bank of Japan as its easy monetary policy increasingly feels the strain of rising interest rates globally. Bank of Japan Governor Haruhiko Kuroda said a recent abrupt weakening of the yen is bad for the economy and pledged to closely work with the government hours after the yen hit the lowest level since 1998.

Bitcoin is hampered amid broad-based losses in the crypto space with the likes of Celsius pausing withdrawals/transfers due to the “extreme market conditions”. Currently, Bitcoin is at the bottom-end of a USD 23.7-27.9 range for the session.

In rates, the US two-year yield exceeded the 10-year for the first time since early April, an unprecedented re-inversion. The 2-year Treasury yield touched the highest level since 2007 and the 10-year yield the highest since 2018.

Treasuries continued to sell off in Asia and early European sessions, leaving 2-year yields cheaper by 15bp on the day into the US day as investors continue to digest Friday’s inflation data. Into the weakness a flurry of block trades in futures added to soaring yields. Three-month dollar Libor jumps 8.4bps. US yields remain close to cheapest levels of the day into early US session, higher by 13bp to 6bp across the curve: 2s10s, 5s30s spreads flatter by 5bp and 5.5bp on the day — 5s30s dropped as low as -16.6bp (flattest since 2000) while 2s10s bottomed at -2bp. US 10-year yields around 3.235%, remain cheaper by 8bp on the day and lagging bunds, gilts by 2.5bp and 5bp in the sector. Fed-dated OIS now pricing in one 75bp move over the next three policy meetings with 175bp combined hikes priced by September, while 55bp — or 20% chance of a 75bp move is priced into Wednesday’s meeting. A selloff of European government bonds gathered pace as traders priced in a more aggressive pace of tightening from the ECB, with traders now wagering on two half-point hikes by October.

The Bank of Japan announced it would conduct an additional bond-buying operation, offering to purchase 500b yen in 5- to 10-year government bonds Tuesday after 10-year yields rose above the upper limit of its policy band.

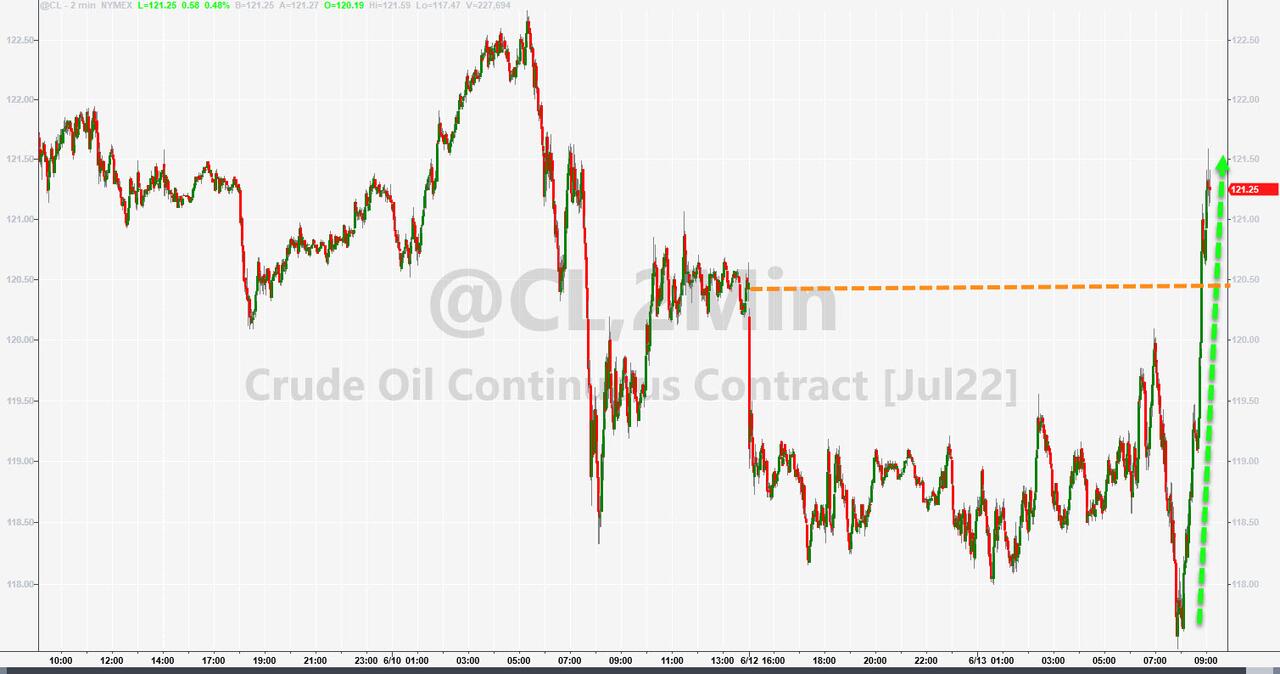

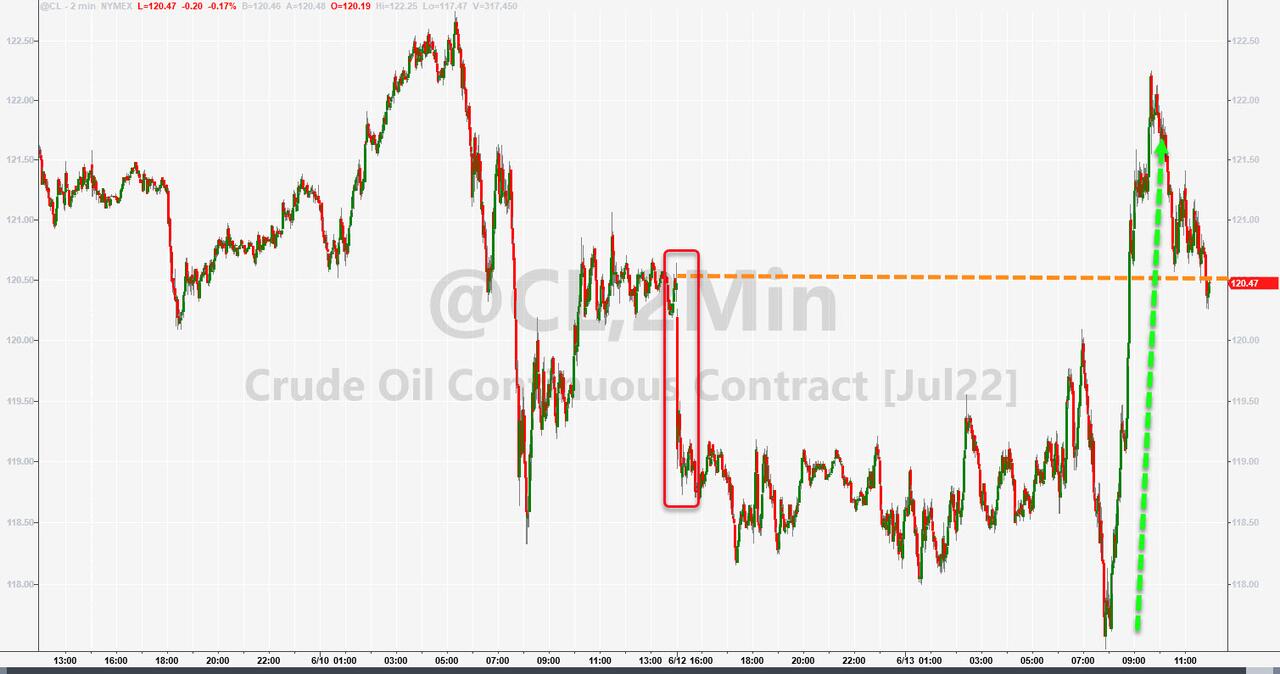

In commodities, oil and iron ore paced declines among growth-sensitive commodities; crude futures traded off worst levels. WTI remains ~1% lower near 119.30. Spot gold gives back half of Friday’s gains to trade near $1,855/oz. Base metals are in the red with LME tin lagging

While it’s a busy week ahead, with the FOMC meeting on deck where the Fed is set to hike 50bps, or maybe 75bps and even 100bps, there is nothing on Monday’s calendar. Fed Vice Chair Lael Brainard will discuss the Community Reinvestment Act in a pre-recorded video and an audience Q&A; she is not expected to discuss monetary policy given the FOMC blackout period.

Market Snapshot

- S&P 500 futures down 2.4% to 3,803.50

- STOXX Europe 600 down 2.0% to 414.12

- MXAP down 2.7% to 161.61

- MXAPJ down 2.8% to 534.45

- Nikkei down 3.0% to 26,987.44

- Topix down 2.2% to 1,901.06

- Hang Seng Index down 3.4% to 21,067.58

- Shanghai Composite down 0.9% to 3,255.55

- Sensex down 3.2% to 52,585.17

- Australia S&P/ASX 200 down 1.3% to 6,931.98

- Kospi down 3.5% to 2,504.51

- Brent Futures down 1.9% to $119.71/bbl

- Gold spot down 0.8% to $1,857.56

- U.S. Dollar Index up 0.39% to 104.55

- German 10Y yield little changed at 1.54%

- Euro down 0.3% to $1.0484

- Brent Futures down 1.9% to $119.69/bbl

Top Overnight News

- “Sell everything but the dollar” is resounding across trading desks as investors reprice the risk that the Federal Reserve hikes rates more aggressively than previously thought

- Investors rushed to price in more aggressive Federal Reserve rate hikes Monday as the US inflation shock continued to reverberate, sending two-year Treasury yields to a 15-year high and strengthening the dollar

- UK Prime Minister Boris Johnson risks reopening divisions that tore his Conservative Party apart in 2019, with his government set to propose a law that would let UK ministers override parts of the Brexit deal he signed with the European Union

- Crypto lender Celsius Network Ltd. paused withdrawals, swaps and transfers on its platform, fueling a broad cryptocurrency selloff and prompting a competitor to announce a potential bid for its assets

- French President Emmanuel Macron has a week to convince voters to give him an outright majority in parliament to ease the way for the controversial social and economic reforms he promised. Shares in France fell on the results

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks declined across the board following the hot US CPI data which rose to a 40-year high and amid fresh COVID concerns in China. Nikkei 225 fell below the 27k level with sentiment not helped by a deterioration in BSI All Industry data. Hang Seng and Shanghai Comp. conformed to the downbeat mood with heavy losses among tech stocks owing to the higher yield environment and with mainland bourses constrained after the latest COVID outbreak and containment measures.

Top Asian News

- Beijing government said the scale of Beijing’s latest outbreak linked to bars is ferocious and explosive in nature after the city reported 166 cases in a bar cluster and with 6,158 people determined as close contacts linked to the bar cluster, while Beijing announced to halt offline sports events from today and the district of Chaoyang is to launch mass COVID testing on June 13th-15th, according to Reuters.

- Shanghai re-imposed a ban on dine-in restaurant services in most districts and punished officials for a management lapse at a quarantine hotel, according to Business Times.

- At least three Chinese cities of Beijing, Nanjing and Wuhan are trialling a shorter quarantine period of 7+7 days for international arrivals at entry points, according to Global Times.

- Beijing government spokesperson says that the Beijing COVID-19 bar outbreak still presents risks to the community; Beijing City reports 45 new local cases of 3pm, according to a health official, via Reuters, adding that the COVID-19 bar outbreak is still developing and epidemic control is at a critical juncture.

- Chinese Defence Minister Wei said China firmly rejects accusations and threats by the US against China, while he added the US Indo-Pacific strategy will create confrontation and that Taiwan is first and foremost China’s Taiwan. Wei also said those that pursue Taiwan’s independence will come to no good end and that China will fight to the end if anyone attempts to secede Taiwan from China, according to Reuters. Furthermore, Wei reiterated that Beijing views the annexation of Taiwan as a historic mission that must be achieved which its military would be willing to fight for but added that peaceful unification remained the biggest hope of the Chinese people and they are willing to make the biggest effort to achieve it, according to FT.

- China urges local governments to raise revenue and sell assets to resolve debt risks, via Reuters. Urges local govt’s to lower the debt burden; adding, they will crackdown on illegal debt raising.

- Japanese Defence Minister Kishi met with his Chinese counterpart in Singapore and said Japan and China agreed to promote defence dialogue and exchanges, while Japan warned China against attempting to alter the status quo in the South and East China sea, according to Reuters.

- Australian and Chinese defence ministers met in Singapore on Sunday for the first time in three years at the sidelines of the Shangri-La Dialogue summit with the talks described as an important first step following a period of strained ties, according to AFP News Agency.

European bourses are hampered across the board, Euro Stoxx 50 -2.5%, in a continuation of the fallout from Friday’s US CPI and amid fresh COVID concerns in China. US futures are in-fitting with this price action, ES -2.4% (sub-3800 at worst), ahead of the FOMC where the likes of Barclays now look for a 75bp hike after the May inflation release. Sectors in Europe are all in the red and feature Travel & Leisure as the underperformer given further cancellations going into the summer period.

Top European News

- UK Northern Ireland Secretary Lewis said the government will publish legislation on the Northern Ireland Protocol on Monday and that the bill will rectify the issues in the protocol, according to Reuters. Reports suggest that the new law could see European judges blocked from having the final say on Northern Ireland-related disputes, according to the Telegraph.

- UK Tory MPs accused PM Johnson of ‘damaging the UK and everything the Conservatives stand for’ as he plans to release legislation on Monday to tear up the Northern Ireland protocol, according to FT.

- UK government ministers are drawing up plans to cut the link between gas and electricity to help reduce household bills for millions of families, according to The Times.

- UK Foreign Minister Truss says she has spoken to EU VP Sefcovic about the Nothern Ireland protocol and the preference is for a negotiated solution; adding, the EU needs to be willing to change the protocol.

- French President Macron’s majority in parliament is at risk as an IFOP initial estimate showed that Macron’s centrist camp is seen qualified for winning 275-310 out of 577 seats after the first round of the French lower house elections, while the IPSOS initial estimate shows the centrist camp is qualified for winning 255-295 seats, according to Reuters. Note, 289 seats are required for a majority

FX

- Greenback extends US inflation data gains as near term Fed hike expectations crank up; DXY hits 104.750 to eclipse May 16 high and expose 105.010 YTD peak.

- Pound undermined by negative UK GDP and output prints plus NI protocol jitters, Cable perilously close to 1.2200 and EUR/GBP tops 0.8575.

- Aussie hit by heightened Chinese Covid concerns and demand implication for commodities, Kiwi feeling contagion and Loonie lurching as oil prices retreat; AUD/USD sub-0.7000, NZD/USD near 0.6300 and USD/CAD just shy of 1.2850.

- Euro and Franc make way for outperforming Buck, but Yen claws back losses on risk dynamics allied to technical retracement; EUR/USD under 1.0500, USD/CHF above 0.9900 and USD/JPY below 134.50 vs 135.20 apex overnight.

- Yuan falls as Beijing suffers ferocious and explosive virus outbreak and Shanghai reimposes restrictions in most districts, USD/CNH pivots 6.7500 and USD/CNY straddles 6.7350.

Commodities

- WTI & Brent are hampered amid the broader market pressure; though, did experience a fleeting move off lows during a break in the newsflow.

- Currently, the benchmarks are lower by circa. USD 2.00/bbl given Friday’s CPI, China COVID, geopolitics around US-China-Taiwan and Iran-IAEA developments (or lack of) following last week’s camera removal.

- Iraq set July Basrah medium crude OSP to Asia at a premium of USD 3.30/bbl vs Oman/Dubai average and set OSP to Europe at a discount of USD 7.60/bbl vs dated Brent, while it set OSP to North and South America at a discount of USD 1.70/bbl vs ASCI, according to Reuters citing Iraq’s SOMO.

- Libya’s Minister of Oil and Gas Aoun said Libya is currently losing more than 1.1mln bpd of oil production and that most oil fields are closed except for the Hamada field and the Mellitah complex, while the Al-Wafa field continues operations from time to time, according to The Libya Observer.

- QatarEnegy signed an agreement with TotalEnergies (TTE FP) for the North Field East expansion project, while it will announce subsequent signings with partners in the gas field expansion in the near future and possibly at the end of next week, according to Reuters.

- Norwegian Oil and Gas Association reached an agreement in principle with three unions of offshore workers to avert a strike although two of the unions will ask members before signing a deal, according to Reuters.

- Spot gold is pressured by circa. USD 15/oz amid a stronger USD and pronounced yield action; however, the yellow metal is yet to drop below USD 1850/oz and the 10-, 21- & 200-DMAs at USD 1852, 1847 & 1842 respectively.

Fixed Income

- Bond bears still in control and pushing futures down to fresh troughs, at 145.85 for Bunds, 112.33 for Gilts and 115-30+ for 10 year T-note.

- Cash yields test or breach psychological levels, like 1.50%, 2.5% and 3.25%, while 2-10 year US spread inverts briefly on rising recession risk.

- Monday agenda very light, but big week ahead including top tier data and multiple Central Bank policy meetings.

Central Banks

- BoJ announces new offer for bond buying programme in which it is to purchase JPY 500bln in 5yr-10yr JGBs tomorrow and will increase amount of offers for its bond buying as needed.

- BoJ fixed-rate bond purchases exceed JPY 1tln, at their highest since 2018, via Bloomberg; Further reported that the BoJ accepts JPY 1.5tln of bids for the daily offers to purchase 10yr bonds.

- BoJ Governor Kuroda says they must support the economy with monetary easing to achieve higher wages; adding, the domestic economy is still in the midst of a COVID recovery. Increasing raw material costs are increasing downward pressure, recent sharp JPY dalls are undesirable. Additionally, Japan’s Finance Minister says a weak JPY has both merits and demerits.

- BoJ buys JPY 70.1bln in ETF, according to a disclosure.

DB’s Jim Reid concludes the overnight wrap

This week is squarely and firmly all about the FOMC meeting on Wednesday. We go into it with the 2yr US note up +25bps on Friday and another c.+10bps this morning in Asia. The 2s10s curve has flattened around 20bps since Friday morning to c.2bps as we type. So some dramatic moves.

The problem as we enter the next couple of Fed and ECB meetings is that the central banks haven’t quite been able to let go of forward guidance and are a little trapped. To recap, forward guidance has prevented the Fed and the ECB from hiking as early as they needed to, largely because both saw the need to gradually wind down asset purchases over several months first as promised. However this hasn’t deterred them, and they have continued to try to flag their intentions to the market in advance with the Fed having previously all but signalled a 50bps this Wednesday, as well as in July, with the ECB now signalling 25bps in July and a strong possibility of 50bps in September.

Providing clarity is admirable but in the wake of another shocking US CPI print on Friday, should a 75bps hike not be a serious consideration? It seems strange that most think policy needs to be restrictive but that it’s going to take several meetings to get there from a still highly accommodative position. Without the recent Fed guidance, 75bps would be firmly on the table for Wednesday. This is highly unlikely this week, but our economists think they could break cover from their own guidance and leave the door open for 75bps in July.

DB Research has long been at the hawkish end on inflation and the Fed, and on Friday our US economists further raised their hiking expectations. In addition to 50bps at the next two meetings they have now added 50bps in September and November, before a return to 25bps in December (to 3.125%). They now see the peak at 4.125% in mid-2023. This is closer to the 5% view in the “Why the upcoming recession will be worse than expected” (link here) that David Folkerts-Landau, Peter Hooper and myself published back in April. If we do have a terminal Fed rate approaching a 5-handle it does raise the question as to where 10yr yields top out. My guess would be a slightly inverted curve but it would likely mean the 4.5-5% range discussed in the note from April, mentioned above, is within reason.

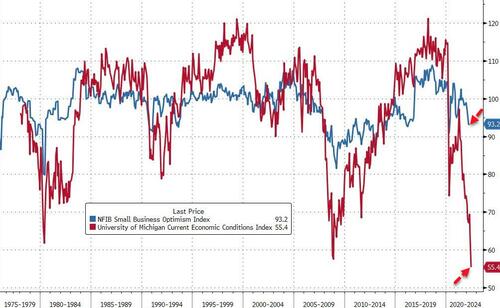

We’ll recap details of the big US CPI print in last week’s recap in the second half of this piece, but it wasn’t just this that was the problem on Friday, as the University of Michigan long-term inflation expectations series hit 3.3% (3.0% last month) which was the highest since 2008. This series first hit 3% last May so has actually been range trading for a year, which has been a hope for the doves. However it now risks breaking out to the upside.

It’s not just the Fed this week as the BoE (Thursday) and the BoJ (Friday) will also meet. For the UK, a preview from our UK economists can be found here. The team expects a +25bps hike this week and have updated their terminal rate forecast from 1.75% to 2.5%. Staying in the UK, labour market data releases will be out tomorrow with retail sales on Friday.