JUNE 14 2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1811.80 DOWN $18.80

SILVER: $20.98 DOWN $0.32

ACCESS MARKET: GOLD $1809.30

SILVER: $21.04

Bitcoin morning price: $22,318 DOWN 958

Bitcoin: afternoon price: $22,213 DOWN 1063

Platinum price: closing DOWN $18.80 to $921.15

Palladium price; closing UP$6.85 at $1814.00

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 480/554

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,828.000000000 USD

INTENT DATE: 06/13/2022 DELIVERY DATE: 06/15/2022

FIRM ORG FIRM NAME ISSUED STOPPED

104 C MIZUHO 500

118 C MACQUARIE FUT 6

323 C HSBC 12

363 H WELLS FARGO SEC 8

407 C STRAITS FIN LLC 1

435 H SCOTIA CAPITAL 53

624 H BOFA SECURITIES 15

657 C MORGAN STANLEY 6

661 C JP MORGAN 480

700 C UBS 8

709 H BARCLAYS 5

732 C RBC CAP MARKETS 8

800 C MAREX SPEC 3

905 C ADM 3

TOTAL: 554 554

MONTH TO DATE: 22,607

_____________________________________________________________________________________ TOTAL: 200 200 MONTH TO DATE: 22,053

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 554 NOTICE(S) FOR 55,400 Oz//1.723 TONNES)

total notices so far: 22,607 contracts for 2,260,700 oz (70.317 tonnes)

SILVER NOTICES:

57 NOTICE(S) FILED 285,000 OZ/

total number of notices filed so far this month 1672 : for 8,360,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $18.80

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1068.87 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 32 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.399 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 5289 CONTRACTS TO 155,283 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR HUGE $0.62 LOSS IN SILVER PRICING AT THE COMEX ON FRIDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.62) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS AS THEY REMAIN FIRM IN THEIR BELIEF OF A SILVER FAILURE AS EVEN THOUGH WE HAD A STRONG LOSS OF 649 CONTRACTS ON OUR TWO EXCHANGES, ALL OF THAT LOSS WAS FROM SPECULATOR SHORTS COVERING.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT COVERING AS THEY ARE VERY ANXIOUS TO GET OUT OF DODGE!!/. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 53 CONTRACTS OR 265,000 OZ//NEW STANDING: 8,670,000 / // V) GIGANTIC SIZED COMEX OI GAIN/(SPECULATOR COVERING)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : +172

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 10 days, total 8012, contracts: 40.060 million oz OR 4.00 MILLION OZ PER DAY. (801 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 40.06 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 40.06 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5239 DESPITE OUR HUGE $0.62 LOSS IN SILVER PRICING AT THE COMEX// MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 1200 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 265,000 QUEUE JUMP //NEW STANDING: 8,670,000 OZ // .. WE HAD A GIGANTIC SIZED GAIN OF 6439 OI CONTRACTS ON THE TWO EXCHANGES FOR 32.195 MILLION OZ WITH THE GAIN IN PRICE.

WE HAD 57 NOTICES FILED TODAY FOR 285,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG 9708 CONTRACTS TO 499,867 AND CLOSER TO NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -185 CONTRACTS.

THE BIS HAS ABANDONED THE GOLD COMEX TRADING!!!

.

THE STRONG LOSS IN COMEX OI CAME WITH OUR HUGE FALL IN PRICE OF $41.55//COMEX GOLD TRADING/MONDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD SOME LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 200 OZ E.F.P JUMP TO LONDON//NEW STANDING: 74.062 TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $41.55 WITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3718 OI CONTRACTS 11.564 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5990 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 500,052

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3533, WITH 9523 CONTRACTS DECREASED AT THE COMEX AND 5990 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3718 CONTRACTS OR 11.564 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5990) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (9708,): TOTAL LOSS IN THE TWO EXCHANGES 3718 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 200 OZ//NEW STANDING: 74.062 TONNES / 3) SOME LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) FAIR SIZED COMEX OI. LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

42,039 CONTRACTS OR 4,203,900 OZ OR 130.75 TONNES 10 TRADING DAY(S) AND THUS AVERAGING: 4204 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES: 130.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 130.75/3550 x 100% TONNES 3.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 130.75 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, ROSE BY A GIGANTIC SIZED 5239 CONTRACT OI TO 155,283 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 1200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1200 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5067 CONTRACTS AND ADD TO THE 1200 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF 6439 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 32.195 MILLION OZ

OCCURRED DESPITE OUR LOSS IN PRICE OF $0.62 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)MONDAY MORNING// SUNDAY NIGHT

SHANGHAI CLOSED UP 33.35PTS OR 1.02% //Hang Sang CLOSED UP 0.41 PTS OR 0.00% /The Nikkei closed DOWN 357.58 OR 1.33% //Australia’s all ordinaires CLOSED DOWN 3.39% /Chinese yuan (ONSHORE) closed UP 6.7359 /Oil UP TO 121.65 dollars per barrel for WTI and UP TO 123.21 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7359 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7572: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9708 CONTRACTS TO 499,867 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR HUGE LOSS OF $41.55 IN GOLD PRICING MONDAY’S COMEX TRADING. WE ALSO HAD A STRONG SIZED EFP (5990 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5990 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :5990 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5990 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3718 CONTRACTS IN THAT 5990 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED COMEX OI LOSS OF 9708 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF GOLD $41.55.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING FOR MAY (74.062),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.062 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $41.55) AND WERE SUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED LOSS OF 10.989 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.062 TONNES)…

WE HAD XXX CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3533 CONTRACTS OR 353,300 OZ OR 10.989 TONNES

Estimated gold volume 159,010/// poor/raid

final gold volumes/yesterday 270,314 /poor/raid

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 14

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 87,749.660 oz Delaware, Int. Delaware, JPMorgan., Manfra |

| Deposit to the Dealer Inventory in oz | 32,118.849 OZ Brinks 999 kilobars |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 554 notice(s) 55,400 OZ 1.723 TONNES |

| No of oz to be served (notices) | 1204 contracts 120400 oz 3.745 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,607 notices 2,260,700 OZ 70.317 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 1

i) Into Brinks dealer: 32,118.849 o (999 kilobars)

No dealer withdrawals

0 customer deposits

total deposits: nil oz

5 customer withdrawals:

i) Out of Delaware: 482.265 oz (15 kilobars)

ii) Out of JPMorgan: 5894.389 oz

and JPMorgan enhanced: 802.600 oz

iii)Int. Delaware 225.057 oz (7 kilobars)

iv) Manfra: 80,345.349 oz (2499 kilobars)

total withdrawal: 87,749.660 oz

ADJUSTMENTS: 3 dealer to customer

Malca 119,215.908 oz

Manfra: 11,121.644 oz

JPMorgan 72,730.176 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1758 contracts having LOST 202 contracts

We had 200 notices filed on MONDAY so we LOST 2 contracts or an additional 200 oz will NOT stand for gold in this very active month of June as they were EFP’d to London

July has a LOSS OF 16 OI to stand at 2040

August has a loss of 10,293 contracts DOWN to 419,256 contracts

We had 554 notice(s) filed today for 55,400 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 554 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 480 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (22,607) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 1758 CONTRACTS ) minus the number of notices served upon today 554 x 100 oz per contract equals 2,381,100 OZ OR 74.062 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (22,607) x 100 oz+ (1758) OI for the front month minus the number of notices served upon today (554} x 100 oz} which equals 2,381,100 oz standing OR 74.062 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74,082 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,334,079.570 OZ

TOTAL ELIGIBLE GOLD: 16,809,169.675 OZ

TOTAL OF ALL REGISTERED GOLD: 17,524,909.895 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,105,125.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 14

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,769,434.060 oz Brinks CNT Delaware JPMorgan |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 597,263.200 oz JPMorgan |

| No of oz served today (contracts) | 57CONTRACT(S)285,000 OZ) |

| No of oz to be served (notices) | 62 contracts (310,000 oz) |

| Total monthly oz silver served (contracts) | 1672 contracts 8,360,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposits

total dealer deposits: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposit into the customer account

i) Into JPMorgan: 597,263.200 oz

total deposit: 597,263.200 oz

JPMorgan has a total silver weight: 170.824 million oz/336.915 million =50.69% of comex

Comex withdrawals: 4

i) Out of Brinks 10,105.210 oz

ii) Out of Delaware 927.800 oz

iii) Out of JPMorgan: 1,226,954.760 oz

iv) Out of CNT 531,446.790 oz

total withdrawal 1,769,434.060 oz

1 adjustments: dealer to customer

JPMorgan: 559,007.640 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.395 MILLION OZ

TOTAL REG + ELIG. 336.915 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 119 HAVING GAINED 41 CONTRACTS.

WE HAD 12 NOTICES FILED ON FRIDAY SO WE GAINED 53 CONTRACTS OR AN ADDITIONAL 265,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 1870 CONTRACTS DOWN TO 70,851 CONTRACTS.

AUGUST GAINED 9 CONTRACTS TO STAND AT 992

SEPTEMBER HAD A GAIN OF 6852 CONTRACTS UP TO 66,562 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 57 for 285,000 oz

Comex volumes:70,647// est. volume today// good//raid

Comex volume: confirmed yesterday: 113,136 contracts ( strong/big raid )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1672 x 5,000 oz = 8,360,000 oz

to which we add the difference between the open interest for the front month of JUNE(119) and the number of notices served upon today 57 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1672 (notices served so far) x 5000 oz + OI for front month of JUNE (119) – number of notices served upon today (57) x 5000 oz of silver standing for the JUNE contract month equates 8,670,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

MAY 18/WITH GOLD DOWN $2.55//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.07 TONNES FROM THE GLD///INVENTORY RESTS AT 1049.21 TONNES

MAY 17/WITH GOLD UP $5.40:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD////INVENTORY RESTS AT 1053.28 TONNES

MAY 16/WITH GOLD UP $5.40: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.93 TONNES FROM THE GLD///INVENTORY RESTS AT 1055.89 TONNES

MAY 13/ WITH GOLD DOWN $16.25//A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.8 TONNES FROM THE GLD.//INVENTORY RESTS AT 1060.82 TONNES

MAY 12/WITH GOLD DOWN $26.50: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.99 TONNES FROM THE GLD////INVENTORY RESTS AT 1066.62 TONNES

MAY 11/WITH GOLD UP $9.85//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.25 TONNES FROM THE GLD/////INVENTORY RESTS AT 1068.65 TONNES

MAY 10//WITH GOLD DOWN $16.90: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 6.10 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 1075.90 TONNES

MAY 9/WITH GOLD DOWN $24.05: A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.98 TONNES FROM THE GLD..//INVENTORY RESTS AT 1082.00 TONNES

MAY 6/WITH GOLD UP $7.95: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.06 TONNES FROM THE GLD////INVENTORY RESTS AT 1084.98 TONNES

MAY 5/WITH GOLD UP $6.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 4//WITH GOLD UP 70 CENTS TODAY; A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 \TONNES FROM THE GLD//INVENTORY RESTS AT 1089.04 TONNES

MAY 3/WITH GOLD UP $6.05: A BIG CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWL OF 2.32 TONNES//INVENTORY RESTS AT 1092.23

MAY 2/WITH GOLD DOWN $46.20: A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD///INVENTORY RESTS AT 1094.55 TONNES

GLD INVENTORY: 1065.39 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

MAY 18/WITH SILVER UP $0.04 TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL 1.892 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 17/WITH SILVER UP $.22 TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.508 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 16/WITH SILVER UP $.52 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.546 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 568.593 MILLION OZ//

MAY 13/WITH SILVER UP 31 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ/

MAY 12/WITH SILVER DOWN 88 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 570.439 MILLION OZ//

May 11/WITH SILVER UP 8 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 5.487 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 570.439 MILLION OZ//

MAY 10.//WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 9/WITH SILVER DOWN 50 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ

MAY 6/WITH SILVER DOWN 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 5/WITH SILVER UP 6 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .93 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 575.977 MILLION OZ//

MAY 4/WITH SILVER DOWN 27 CENTS TODAY: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .851 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 576.900 MILLION OZ

MAY 3/WITH SILVER UP 4 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF.877 MILLION OZ INTO THE SLV.

MAY 2/WITH SILVER DOWN 47 CENTS: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 554,000 OZ FROM THE SLV.//INVENTORY RESTS AT 575.171 MILLION OZ//

INVENTORY TONIGHT RESTS AT 544.399 MILLION OZ/

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Peak Inflation Was A Fairytale Just Like Transitory Inflation

TUESDAY, JUN 14, 2022 – 07:20 AM

Authored by Michael Maharrey via SchiffGold.com,

Inflation wasn’t transitory.

And inflation hasn’t peaked.

It’s more like peak inflation was transitory.

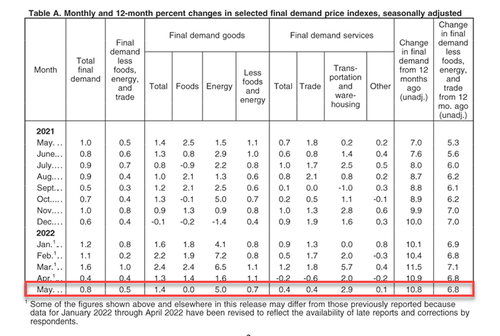

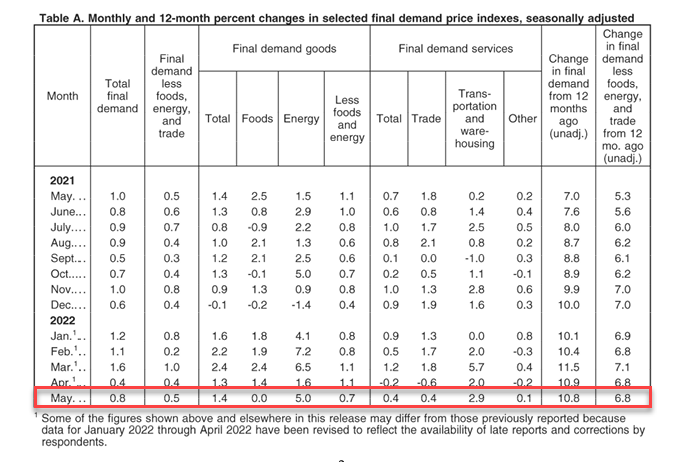

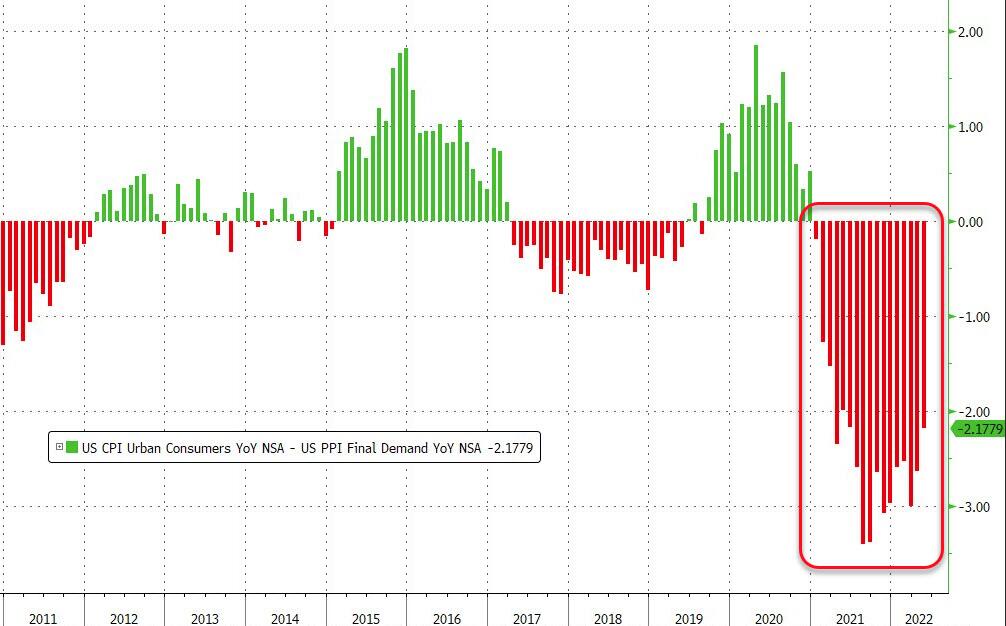

The May Consumer Price Index (CPI) came in higher than expected. The headline year-on-year price increase was 8.6%. The projection was for the CPI to hold steady at the same level as last month — 8.3%. Instead, we got the biggest jump in prices during this inflationary cycle and the highest CPI print since 1981.

On a month-to-month basis, the CPI rose by 1%. This was above the 0.7% projection. Another spike in fuel and energy costs primarily drove the monthly increase. Energy costs rose 3.9% during the month. Annualized, energy prices are up 34.6%. Fuel oil posted a 16.9% monthly gain, pushing the 12-month surge to 106.7%.

Stripping out more volatile food and energy prices, core CPI rose 0.6%. This equaled last month’s core CPI gain and was double the March core read of 0.3%, which was supposedly signaling peak inflation. If you annualize the last two months, the core CPI would come in at 7.2%.

Year-over-year, core CPI rose 6%. This was slightly above the 5.9% estimate.

Most analysts focus on rising energy prices as the primary driver behind persistent inflation, but prices rose in all 11 CPI categories. Nine of those 11 categories charted price increases above the 12-month average.

Housing costs continue to inch higher, even using the government’s make-believe “owner’s equivalent rent” calculation. The housing index was up another 0.6% on the month and this significantly understates the actual rise in housing costs. It was the fasted one-month gain in shelter costs since 2004. The 5.5% 12-month gain ranks as the biggest rise in housing prices since February 1991,

Americans are feeling the sting of inflation.

According to calculations by Bloomberg Economics, the inflation tax currently costs American households $433 per month. That comes to a $5,200 annual increase in household costs.

Taking into account rising prices, the average consumer took a pay cut from April to May, according to a separate BLS report.

Average hourly earnings rose 0.3%, but real wages fell 0.6%. On a year-on-year basis, real average hourly earnings decreased 3%, seasonally adjusted.

This undercuts the popular narrative that “inflation isn’t really that bad” because wages increase as well. Rising wages don’t keep up with rising prices. As a result, American consumers are running up record levels of debt and burning through savings to make ends meet.

And as bad as these numbers are, it’s actually worse than that. This CPI uses a government formula that understates the actual rise in prices. Based on the CPI formula used in the 1970s, CPI is above 17% — a historically high number.

In March, everybody was talking about peak inflation. Clearly, the CPI didn’t peak in March if it’s higher in May. And there is no reason to think these May numbers will be the peak either.

While the mainstream blames, Russia, COVID, supply chains, excessive demand, and perhaps voodoo for rising inflation, it completely ignores the most significant factor – actual inflation created by the Federal Reserve.

Remember, rising prices are not in and of themselves “inflation.” Inflation is an increase in the money supply. Rising prices are a symptom of inflation. Loose central bank monetary policy drives the money supply up.

The Federal Reserve has been flooding the economy with money — inflation — since 2009. We are drowning in inflation.

The Fed took a weak swing at inflation during its May meeting, raising interest rates by 1/2%. But at .75%, interest rates remain historically low. Meanwhile, the central bank pushed back balance sheet reduction until June. And at the proposed pace, it would take over 7 years to decrease the balance sheet back to pre-pandemic levels. The Federal Reserve hasn’t done nearly enough to mop up all of the excess liquidity in the economy.

As a SchiffGold analyst put it, “This is still highly stimulative, inflationary policy. Interest rates are being held artificially low. And we’re still dealing with all of this inflation that is in the pipeline.”

Meanwhile, President Biden’s inflation-fighting plan basically involves spending more money. That means more borrowing and more debt the Fed will ultimately need to monetize.

It should be clear to you that this won’t fix inflation. In fact, it will only make it worse by raising the inflation tax. Every dollar the government spends comes out of Americans’ pockets — out of your pocket.

If the federal government is going to spend more to fight inflation, it will either have to raise taxes (and not just on the “rich” — that won’t generate enough government revenue) or it will have to borrow more. That means the Federal Reserve will have to print more to monetize the debt. That means more inflation.

All of this tells me that peak inflation was every bit a fairytale as transitory inflation.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

END

3. Chris Powell of GATA provides to us very important physical commentaries

As discussed yesterday, huge selloff hits treasury markets causing yield curve to invert

(Reuters/GATA)

Huge selloff rocks Treasury markets, inverting yield curve

Submitted by admin on Mon, 2022-06-13 10:28Section: Daily Dispatches

By Yoruk Bahceli and Sujata Rao

Reuters

Monday, June 13, 2022

U.S. two-year Treasury yields rose above 10-year borrowing costs today — the so-called curve inversion that often heralds economic recession — on expectations interest rates may rise faster and further than anticipated.

Fears the U.S. Federal Reserve could opt for an even larger rate hike than anticipated this week to contain inflation sent two-year yields to their highest levels since 2007.

But a view is also playing out that aggressive rate hikes may tip the economy into recession. …

… For the remainder of the report:

https://www.reuters.com/business/huge-selloff-rocks-treasury-markets-yield-curve-inverts-2022-06-13/

END

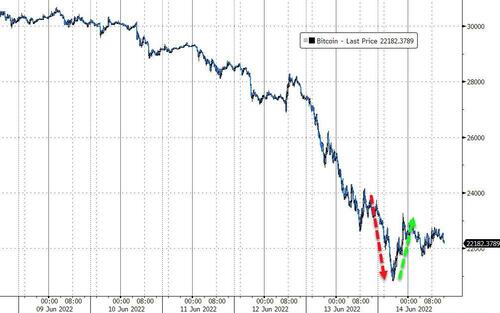

This is what caused cryptos to collapse: Celsius and Binance halts withdrawals

(The Hill/GATA)

Crypto firms Celsius, Binance halt withdrawals as bitcoin plummets

Submitted by admin on Mon, 2022-06-13 10:42Section: Daily Dispatches

By Karl Evers-Hillstrom

The Hill, Washington

Monday, June 13, 2022

Cryptocurrency companies today blocked users from withdrawing funds as the value of bitcoin and other prominent digital assets plunged.

Crypto lending company Celsius Network announced late Sunday night that it would freeze all withdrawals and transfers due to “extreme market conditions.” The move sparked an enormous selloff, with the price of bitcoin falling 12% to its lowest level since December 2020.

Binance, the world’s largest crypto exchange by trading volume, said today it was freezing bitcoin withdrawals due to “due to a stuck transaction causing a backlog.”

Changpeng Zhao, the firm’s CEO, tweeted that the fix would take only 30 minutes but later said that the problem was “going to take a bit longer to fix” than his initial estimate.

Celsius, which says it has 1.7 million customers, made its announcement after numerous cryptocurrencies tanked over the weekend. Ethereum, another popular digital coin, plunged nearly 32 percent from Friday to this morning. …

… For the remainder of the report:

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings TUESDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7359

OFFSHORE YUAN: 6.7572

HANG SANG CLOSED UP 0.41 PTS OR 0.00%

2. Nikkei closed DOWN 357.58% OR 1.33%

3. Europe stocks ALL CLOSED ALL RED

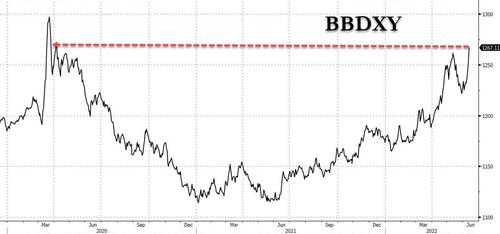

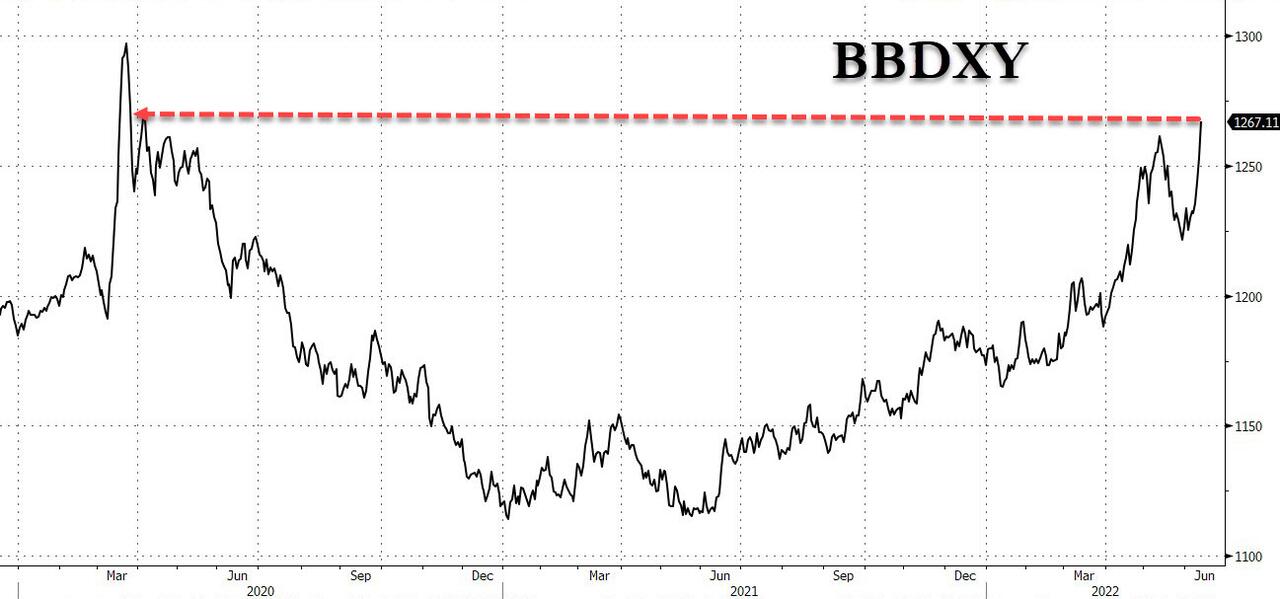

USA dollar INDEX UP TO 104.99/Euro RISES TO 1.0435

3b Japan 10 YR bond yield: FALLS TO. +.252/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 134.51/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN -SHORE CLOSED UP// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

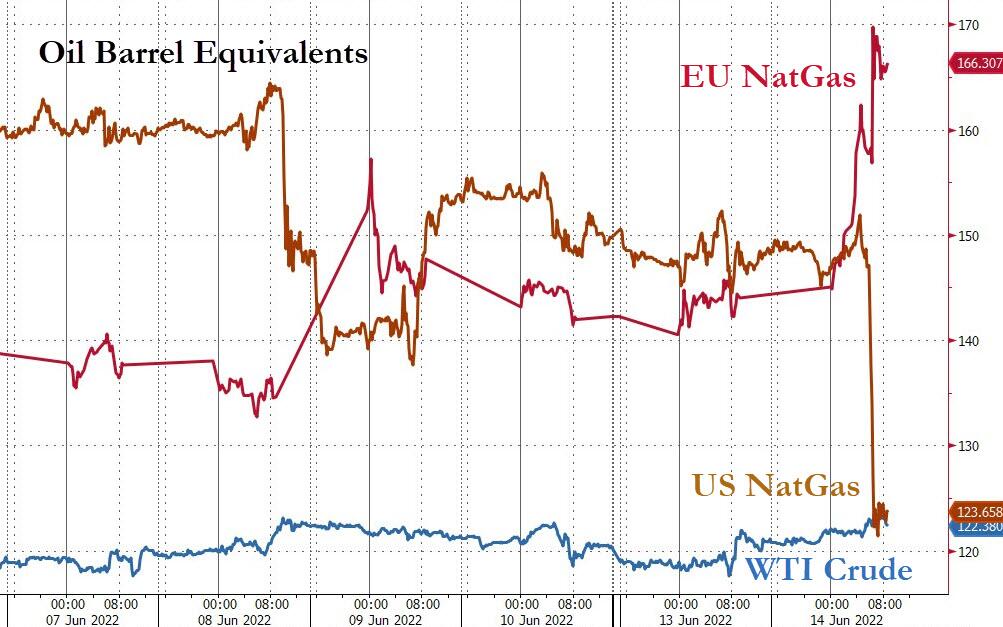

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.66%/Italian 10 Yr bond yield RISES to 4.16% /SPAIN 10 YR BOND YIELD RISES TO 3.03%…ALL BLOWING UP!!

3i Greek 10 year bond yield RISES TO 4.69//BLOWING UP

3j Gold at $1822.05 silver at: 21.17 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1/2 roubles/dollar; ROUBLE AT 56.24

3m oil into the 121 dollar handle for WTI and 123 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.51DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9940– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0373well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.322 DOWN 5 BASIS PTS

USA 30 YR BOND YIELD: 3.326 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.27

Stocks Stage Feeble Attempt At Dead Cat Bounce After Losing $1.3 Trillion In One Day

TUESDAY, JUN 14, 2022 – 07:49 AM

US index futures staged a feeble, fading attempt to bounce on Tuesday, following Monday’s crash that wiped out $1.3 trillion in market cap and topped a furious 4-day selloff that was the worst since March 2020 and culminated in a bear market amid expectations – even from permabull Goldman – that the Fed’s now accepted 75bps rate hike on Wednesday will hurl the economy into a recession. Futures on the S&P 500 rebounded more than 1% in early trading before fading the gain to just 0.24%, while Nasdaq 100 futures climbed 0.5%.

US stocks plunged on Monday to the lowest level since January 2021 and closed more than 20% below its January record high, triggering Joe Biden first official bear market. Global equities sold off after an unexpectedly strong reading Friday on US inflation sparked concern that the Fed will go too far in raising interest rates to tame soaring prices. Bond yields dipped after soaring to a peak last seen in 2011. The yield curve remained flat, however, underscoring worries about an economic downturn sparked by tighter monetary policy, with the 2s10s curve just 1bps away from inverting again. Cryptocurrencies, meanwhile, plunged with bitcoin puking more than 10% to below $21,000 before paring much of the slide as dip buyers emerged. UBS said most long-term owners are now in the red and warned of more losses if coin miners buckle under the pressure and start selling. The dollar was steady near a two-year high. In Japan, the central bank boosted bond-purchase operations to keep yields in check. The yen hovered near a 24-year low against the greenback.

“We remain bearish on equity outlook,” said Marija Veitmane, a senior strategist at State Street Global Markets. “Inflation is still a huge problem and central banks need to be very aggressive to fight it. This is a very negative outlook for stocks, so we would be sellers of any rally.”

Among notable premarket movers, shares of megacap tech companies like Apple, Microsoft, Alphabet, Tesla and Meta Platforms were slightly higher and poised to recoup some of the losses from Monday: Apple (AAPL US) +1.4%, Amazon (AMZN US) +1.7%, Alphabet (GOOGL US) +1.5%, Meta Platforms (META US) +1.9% and Nvidia (NVDA US) +1.8% in premarket trading. Oracle shares rose 13% in premarket trading after the software company reported higher-than-expected fourth-quarter results. Here are the most notable premarket movers:

- AMC Entertainment (AMC US) shares rise as much as 3.7% in US premarket trading, in line with a broader rebound in risk assets, and after the movie theater operator said that last weekend’s admission revenues beat that of the same weekend of 2019.

- Adobe (ADBE US) slides 4.2% in premarket trading as Citi cut its price target on the company to $425, the lowest on Wall Street, citing weaker consumer spending and potentially rising competition.

- US-listed Chinese stocks post broad-based gains in premarket trading, on track to rebound from a three-day drop, as sentiment toward tech stabilizes: Alibaba (BABA US) shares rise 3.8%, Baidu (BIDU US) +4%, Pinduoduo (PDD US) +4.2%, JD.com (JD US) +3.2% and Li Auto (LI US) +6.1%

- Braze (BRZE US) shares jump 8% in premarket trading after the company’s first-quarter revenue beat estimates, and full-year guidance also topped expectations.

- Arista (ANET US) shares decline 4.1% in US premarket trading as Morgan Stanley says in a note that the company, as well as Wiwynn and memory stocks such as SK Hynix and Micron (MU US) are among those most at risk in the semiconductor and networking equipment space when tech firms cut spending on data centers.

- Kaival Brands (KAVL US) shares surge as much as 57% in US premarket trading, after the vaping products distributor reached deal with Philip Morris to distribute electronic nicotine delivery systems products outside of the US.

- Outset Medical (OM US) shares fall 4.6% in premarket trading as their price target was cut to a Street-low at Cowen, after the medical technology firm halted shipments on its Tablo Hemodialysis System for home use. The company also suspended guidance for the year.

- US Silica (SLCA US) shares may be in focus after they were upgraded to outperform from inline at Evercore ISI following the conclusion of the industrial minerals firm’s review of its Industrial & Specialty Products (ISP) segment.

With just two weeks left until the end of Q2, a dismal picture emerges: this quarter is set to deliver the biggest combined loss for global bonds and stocks on record, according to Bloomberg. The highest inflation in a generation, stoked by supply-chain and commodity-market disruptions amid China’s Covid struggles and the war in Ukraine, is roiling the outlook. According to Bloomberg, the big question is whether the Fed and other major central banks will tip their economies into recession as they tighten financial conditions. We disagree: a recession is now assured; the real big question is how sparking a recession in the US will force Putin to pump more gas.

European gains were shorter-lived: Euro Stoxx 50 reverses a 1.1% bounce to trade down 0.2%, extending its decline to a sixth day, on track for the longest losing streak since the start of the pandemic and the lowest closing level in 15 months. Retail, media and travel are the weakest Stoxx 600 sectors with broad-based sectoral gains fading as the session progresses. Bonds in most of Europe edged lower, but gilts bucked the trend after data showed spending power of UK households plunged as inflation eroded wage increases. Here are the biggest European movers:

- Fortum shares rose as much as 9.5%, while Uniper gained 6.1% as Finland is prepared to give Fortum time to sell its Russian power plants and follow other western energy companies out of Russia.

- Rates-sensitive banking stocks in Europe outperform Tuesday as Treasury yields drop following four consecutive days of increases that lifted the 10-year to the highest level since 2011.

- HSBC shares gain as much as 3.2%, Standard Chartered +3.2%, Nordea Bank +2.7%, ING +2.8%

- Wizz Air shares rise as much as 6.2% after Berenberg upgraded the airline to buy from hold, citing the long-term potential of its business, despite numerous recent challenges.

- Go-Ahead rises as much as 15% amid a potential bidding war. The company accepted a £648m takeover bid from an investor group backed by Australian rival Kinetic, while Kelsian is assessing whether to make offer.

- Saipem gains as much as 8.5% after five sessions of declines; the company and Trevi signed memorandum of understanding for foundation drilling solutions and services for offshore wind farm projects.

- Atos shares plunge as much as 27% after the company announced the departure of newly arrived CEO Rodolphe Belmer and a separation into two publicly listed companies.

- Akzo Nobel shares decline as much as 6.1% after the company reduced 2Q forecasts due to China lockdowns and slower start to EMEA DIY season.

- Air France-KLM shares fall as much as 13% after the company raised EU2.3b in a deeply discounted rights offering to help repay state aid received during the pandemic.

Earlier in the session, Asian stock market indexes hit bleak milestones in quick succession on Tuesday as investor concerns worsened that aggressive interest rate increases in the US could erode corporate earnings. The MSCI Asia Pacific Index dropped as much as 2% to its lowest level in a month after the world equities gauge entered a bear market overnight before paring losses. New Zealand’s stock index extended its decline to 20% from a peak reached last year, entering a bear market, while Singapore’s measure wiped out its gains for 2022. Traders are betting that the Fed will deliver a 75-basis-point rate increase in this week’s meeting — the biggest since 1994 — after US inflation hit a four-decade high in May. This is further muddying the economic outlook at a time supply chains are snarled, weighing on the valuation and profit estimates for the MSCI Asia index, which has lost 17% this year.

“Bets are off for all asset classes as investors brace themselves for tough action from the Fed to counter higher-than-expected inflation,” said Justin Tang, head of Asian research at United First Partners in Singapore. “The renewed lockdowns in China are also not going to be helpful.” Central banks from South Korea and Australia to India have been raising rates in response to accelerating inflation, with the latter two announcing 50-basis-point increases in their latest decisions.

China’s persistent zero-Covid strategy is another factor disproportionately affecting companies in Asia. Singapore’s Straits Times Index is near a correction, down 9.7% from an April high, while Australia’s S&P/ASX 200 Index has dropped 12% over a similar period. Elsewhere, the MSCI Asean Index is inching closer to a 20% drop from a peak reached in January 2021, while South Korea’s Kospi remains mired in a bear market. Still, investors have identified some potential areas of outperformance, as Asia’s stock measure has held up better than global peers as it continues to trade at a lower forward price-to-earnings ratio. And while China has walked back on loosening some Covid-19 restrictions in Beijing and Shanghai, traders see the country’s fiscal and monetary easing stance giving its beleaguered stocks a further boost. “China might outperform global equities, as it did in May and early June,” if consumption resumes in the coming months after a relaxation in lockdowns, said Herald van der Linde, head of APAC equity strategy at HSBC Holdings Plc. Meanwhile, commodity-exporting Southeast Asian countries such as Indonesia, which are also benefiting from border reopenings, are expected to continue to shine. The Jakarta Composite Index rose on Tuesday, taking its advance to 7.1% this year.

India was no exception to the global rout, and stock gauges fell to their lowest levels in 11-months as inflation and interest-rate concerns continued to fuel selloffs across global equity markets. The S&P BSE Sensex fell 0.3% to 52,693.57 in Mumbai after rising as much as 0.5% during the session. The NSE Nifty 50 Index dropped by an similar measure to its lowest since July 28. Both benchmarks have dropped more than 14% from October peaks. Foreign institutional investors have taken out $24.2 billion from local stocks this year through June 10, and the selloff is headed for its ninth consecutive month. However, the key indexes have still outperformed Asia Pacific and emerging-market peers this year, helped by net $26.4 billion of stock purchases by domestic investors, which include mutual funds and insurance companies. Consumer-price inflation in India has stayed above the central bank’s target in May while wholesale prices accelerated for a third-straight month as input costs continue to rise for manufacturers. “High inflationary environment, fresh curbs in China and rising crude oil prices are likely to keep the markets under pressure for a while,” Motilal Oswal analyst Siddhartha Khemka wrote in a note. Reliance Industries contributed the most to the Sensex’s decline, decreasing 1.3%. Among the 30 shares in the Sensex Index, 15 rose, 14 fell and one was unchanged.

In FX, the Bloomberg Dollar Spot Index fell as the greenback weakened against most of its Group-of-10 peers. The euro rose from a one-month low against the dollar but still failed to retrace the recent plunge in a meaningful way. German June ZEW expectations came in at -28.0 versus estimate -26.8. Norway’s krone slumped to a fresh 4-week low against the euro after Norges Bank’s regional network report showed businesses were expecting growth to slow. Sweden’s krona got a temporary boost after inflation figures for May came in higher than the median estimate in a Bloomberg survey. A Riksbank survey showed businesses, which are seeing sharp cost increases, are concerned that the coming wage bargaining rounds will lead to higher salary costs than in previous collective agreements. The Swiss franc led G-10 gains as it pared most of yesterday’s drop against the dollar. The pound edged up from a two-year low against the dollar. Sterling remained on the back foot after UK labour market data showed limited further tightening in the jobs market, suggesting that the BOE may raise interest rates by 25bps this week, rather than 50bps. Australian sovereign bonds plunged in catch-up to a two-day rout in Treasuries as the specter of a 75bps Fed hike on Wednesday loomed large. Aussie steadied following a bounce in US stock futures. USD/JPY consolidated. The Bank of Japan ramped up the defense of its policy framework after yields came under renewed upward pressure, unveiling a further set of unscheduled buying operations, including purchases of much longer maturities

In rates, treasuries bull steepened with front-end yields richer by 8.5bp on the day into US morning session. S&P futures slightly higher, although remain near Monday session lows as investors continue to position ahead of Wednesday’s Fed decision. Swaps market prices in just under 200bp of rate hikes over the next three meetings with 70bp priced into Wednesday’s decision. Three-month Libor fix jumps over 17bp. US yields richer by 8.5bp to 5bp across the curve with front-end led gains steepening 2s10s, 5s30s spreads by 2.1bp and 1.5bp; 10-year yields around 3.30% and outperforming bunds by 7bp on the day. IG dollar issuance slate; projections for the session remain murky amid markets turmoil and after a number of deals were put on ice Monday. Gilts put in a ~6bps parallel richening move across the curve. Bunds buck the trend, bear-steepening ahead of scheduled comments from ECB’s Schnabel on euro-area bond market fragmentation due later.

In commodities, oil held above $120 a barrel as investors evaluated a tight supply outlook and the impact of China’s eventual return from virus curbs. WTI adds 0.7% to trade near $121.71, Brent holds above $123. Spot gold trades a narrow range, fading after hitting $1,830/oz. Base metals are mixed; LME tin falls 5.1% while LME zinc gains 0.3%.

To the day ahead now. The ECB’s Schnabel speaks, while in data we get UK jobless claims, ILO unemployment rate, ZEW surveys for the Eurozone and Germany, US NFIB small business optimism and PPI, and Canadian manufacturing sales. Hold on to your hats.

Market Snapshot

- S&P 500 futures up 1.1% to 3,790.50

- STOXX Europe 600 up 0.1% to 413.07

- MXAP down 0.9% to 159.98

- MXAPJ down 0.6% to 529.25

- Nikkei down 1.3% to 26,629.86

- Topix down 1.2% to 1,878.45

- Hang Seng Index little changed at 21,067.99

- Shanghai Composite up 1.0% to 3,288.91

- Sensex down 0.2% to 52,743.72

- Australia S&P/ASX 200 down 3.5% to 6,686.03

- Kospi down 0.5% to 2,492.97

- Brent Futures up 0.7% to $123.15/bbl

- Gold spot up 0.6% to $1,829.72

- U.S. Dollar Index down 0.34% to 104.72

- German 10Y yield little changed at 1.62%

- Euro up 0.6% to $1.0473

- Brent Futures up 0.7% to $123.17/bbl

Top Overnight News from Bloomberg

- The latest jumps in consumer prices and inflation expectations will probably spur Federal Reserve officials to consider the biggest interest-rate increase since 1994 when they meet this week, after Chair Jerome Powell previously signaled a smaller move was the likely outcome

- JPMorgan Chase & Co. and Goldman Sachs Group Inc. are withdrawing from handling trades of Russian debt after the Biden administration’s surprise announcement last week it’s banning US investors from scooping up such assets

- As the BOJ escalates attempts to keep a lid on bond yields, BlueBay is betting the central bank will be forced to abandon a policy that’s increasingly out of sync with global peers. The BOJ’s so- called yield curve control is “untenable,” according to Mark Dowding, BlueBay’s London-based chief investment officer

- Investor fears of stagflation are at the highest since the 2008 financial crisis, while global growth optimism has sunk to a record low, according to Bank of America Corp.’s monthly fund manager survey

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were pressured following the global stock and bond slump as the aftershock from recent hot US inflation reverberated across risk assets and spurred further expectations for a 75bps Fed rate hike this week. ASX 200 was the worst performer as the losses caught up to the index on return from the extended weekend and with the declines led by underperformance in tech and metals. Nikkei 225 extended its declines despite the BoJ’s efforts to cap yields and with the recent rapid currency moves adding to the uncertainty. Hang Seng and Shanghai Comp. were negative as lockdown concerns lingered with China’s Vice Premier Sun suggesting it is necessary to strengthen COVID-19 prevention and control of key places, while Shanghai’s Minhang district plans to conduct mass testing on Saturday.

Top Asian News

- Shanghai’s Minhang district is planning mass COVID-19 testing on Saturday, according to Bloomberg.

- BoJ announced additional bond purchases for Wednesday in which it will increase purchases of JGBs across several maturities, while it will continue to conduct additional buying as needed, according to Reuters.

European bourses began on the front-foot but quickly slipped into negative territory, Euro Stoxx 50 -0.8%; since the post-open dip, price action has steadily deteriorated further. However, while US futures are directionally in-fitting they remain in positive territory, ES +0.3%; albeit, well of highs and the ES resides around 3760 currently awaiting Fed clarity amid increasing speculation for 75bp. Oracle Corp (ORCL) Q4 2022 (USD): Adj. EPS 1.54 (exp. 1.37), Revenue 11.8bln (exp. 11.66bln). Cloud License And On-Premise License: 2.54bln (exp. 2.19bln). Cloud Services And Licenses Support: 7.6bln (exp. 7.77bln). Total Hardware Revenues: 856mln (exp. 857.71mln). Total Services Revenues: 833mln (exp. 847.89mln). Added USD 15.8bln after Cerner acquisition and it expects cloud business to grow by over 30% in FY23; Co. expects Q1 rev. including Cerner to grow 17%-19%. (PR Newswire) +12% in the pre-market. German cartel office has commenced proceedings against Apple (AAPL) re. tracking regulations for 3rd party apps, via Reuters.

Top European News

- The EU is set to launch three separate lawsuits against the British government after it published its plans to override the protocol, according to the Telegraph. One option would reportedly see the EU end financial equivalence for the City of London.

- US urged the UK and EU to return to talks to resolve differences over the Northern Ireland Protocol and said it remains a priority to protect gains of the Good Friday Agreement.

- White House said proposed changes to N. Ireland Protocol won’t be an impediment to potential US-UK trade deal or trade dialogue talks in Boston, according to Reuters.

- UK PM Johnson is not looking to lower household taxes until inflation is brought under control, as such action is unlikely before next year, according to the Telegraph.

FX

- Dollar consolidates after Monday’s melt up to new multi year peaks as clock ticks down to FOMC and US PPI data; DXY hovers around 105.00 and just shy of new 105.290 YTD high.

- Franc outperforms following suspension of trade in Russia against Rouble and Greenback; Usd/Chf probes 0.9000 to downside after pulling up only pips short of parity yesterday.

- Euro rebounds amidst more hawkish commentary from ECB’s Knot and irrespective of German ZEW survey misses; EUR/USD back above 1.0400 and decent option expiries between 1.0420-15.

- Aussie undermined by waning risk appetite and ongoing covid outbreaks in China, but underpinned by RBA Governor Lowe underlining determination to get inflation back to target, AUD/USD towards lower end of 0.6970-18 range.

- Pound fades after brief upturn in bigger than expected rise in UK employment as other labour market metrics fall short of expectations and EU rift over NI protocol persists; Cable on the cusp of 1.2100 after fleeting breach of round above, EUR/GBP crosses 0.8600 to set fresh 2 month apex.

Fixed Income

- Recovery in EZ debt derailed by supply and hawkish remarks from ECB’s Knot as Bunds retreat to 145.00 within a 145.58-144.51 range

- Gilts and 10 year T-note hold up better between 112.97-29 and 116-03/115-01+ parameters in consolidation after Monday’s rout and ahead of US PPI data

- ** BTP/Bund** spread blows out beyond 250 bp in advance of ECB’s Schnabel on fragmentation in bond markets

Commodities

- WTI and Brent are firmer by circa. USD 1.0/bbl at present and reside towards the mid-point of a USD ~2.00/bbl range with specific newsflow thin and broader developments on familiar themes.

- Themes which include China COVID and travel demand, for instance; but, factors which are overshadowed by broader anticipation going into Wednesday’s FOMC.

- US and Saudi Arabia will announce on Tuesday that US President Biden will visit Saudi Arabia on July 15th and 16th, according to NBC’s Pegram citing sources.

- China’s state planner is to increase retail prices of gasoline and diesel by CNY 390/tonne and CNY 375/tonne respectively as of June 15th, via NDRC.

- Spot gold is essentially unchanged on the session around USD 1820/oz after falling below the 10-, 21- & 200-DMAs yesterday; Copper softer amid broader risk.

US Event Calendar

- 08:30: May PPI Final Demand MoM, est. 0.8%, prior 0.5%; YoY, est. 10.9%, prior 11.0%

- 08:30: May PPI Ex Food and Energy MoM, est. 0.6%, prior 0.4%; YoY, est. 8.6%, prior 8.8%

- 08:30: May PPI Final Demand

DB’s Jim Reid concludes the overnight wrap

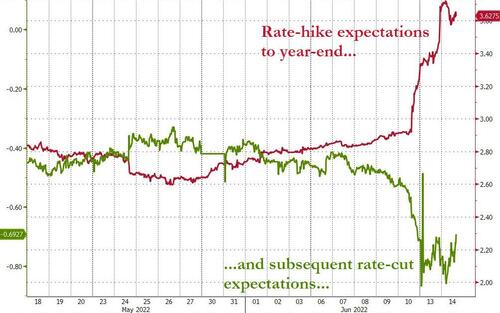

Where do we start this morning after as action packed a 24 hours as I can remember. The global equity and bond sell-off would have been bad anyway but the late US session headlines from a WSJ article (written by a journalist close to the Fed) that suggested the FOMC may need to surprise with a +75bp hike tomorrow was the last straw. Before we delve into the article and more detail on markets let’s take a one para overview of all the main market highlights.

To start with, 2yr USTs capped their largest two-day move (+54.3bps, +29.1bps yesterday), since the week following Lehman’s collapse, while 10yr Treasuries have risen +31.8bps over the last two days (+20.4bps yesterday), the largest such move since December 2010, bringing the 10yr to 3.36%, the highest since 2011. Meanwhile, the 2s10s yield curve swung around violently before closing in inverted territory (-0.3bps) again for the first time since the first days of April and for only the 15th day out of the 3907 business days since May 2007. The historic moves didn’t end with the Treasury market, as Italian 10yr BTP yields (+26.2bps) crossed 4.0% for the first time since 2014, the crossover index widened +32.3bps to 534bps, its widest level since 2012 outside of peak initial Covid widening, Bitcoin fell -15.13% to its lowest since late 2020 and is down another -5.23% this morning, the S&P 500 (-3.88%) finally entered bear market territory (-21.8% from its YTD peaks), while the dollar index surged to its highest level since 2002. So quite a ride although as we’ll see below risk is doing a bit better this morning with yields relatively flat.

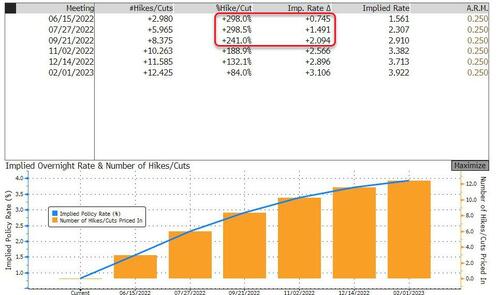

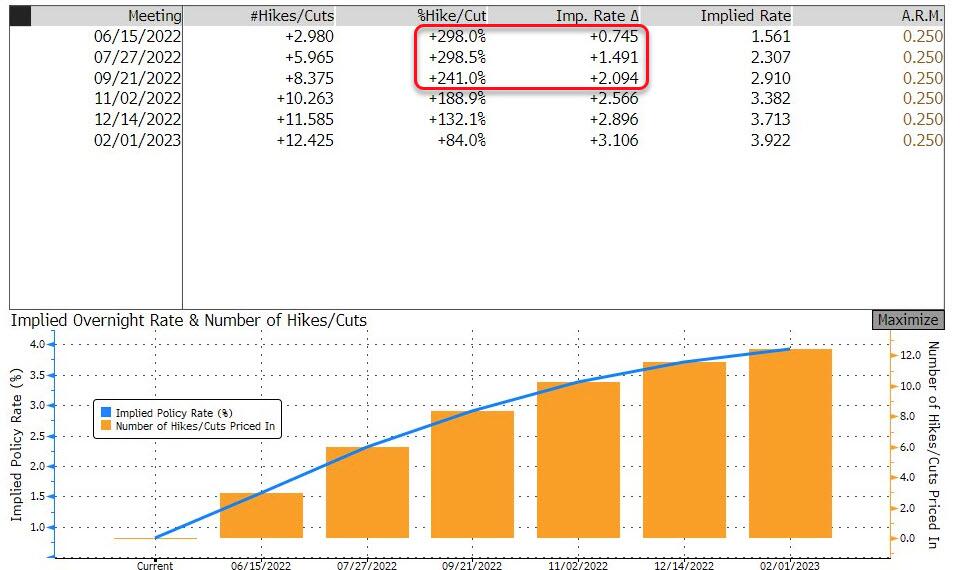

Going through things in more detail, the Treasury market has been at the epicentre of this sell-off after the shocking CPI from last Friday. Yields were drifting higher all day as some on the Street officially updated their call for +75bp on Wednesday and openly considered whether the Fed will need a +100bp hike. The WSJ report then later threw gasoline on the already raging fire, noting the Fed was indeed “considering surprising markets with a larger-than expected” +75bp hike as early as this week given Friday’s alarming CPI and inflation expectations data. All-in, Fed funds futures moved to price in a 94% chance of a +75bp hike on Wednesday. So a +75bp hike on Wednesday won’t come as a surprise anymore.

At the end of the day, 2yr yields gained +29.1bps yesterday and +25.2bps Friday, bringing the rate to 3.35%. The 2s10s yield curve inverted, closing the day at -0.3bps, as 10yr yields climbed +11.4bps Friday and +20.4bps yesterday, bringing rates to 3.36%, their highest level since April 2011. As we go to press this morning, 2yr yields are up another 2bps with 10yr yields fractionally higher, thus inverting the curve a little more. US PPI today will be closely watched for the next inflation impulse.

The policy rate at end 2022 implied by fed funds futures closed at 3.72%, its highest to date by some margin, and implies just shy of +300bps of tightening over 5 meetings. Markets also moved to price in a terminal rate above 4% in the middle of next year, closer to DB’s call which has been the most aggressive on the street. It’s perhaps an understatement to say the market will be hyper focused on how the Fed communicates the near-term path of policy at this week’s FOMC, especially including what size rate hikes they’re considering as adequate for the rest of the year.

The selloff was echoed in Europe, where 10yr bunds (+11.5bps), OATs (+15.4bps), and BTPs (+26.2bps) all soldoff, even before the blockbuster WSJ report. ECB speakers returned to the docket after last week’s meeting, where Governing Council member Kazmir noted there was a clear need for a +50bp hike in September, in line with our European economics team’s call. Kazmir went on to warn that the economy faces weak growth for several quarters, piling onto what the market had already deduced – the sharp global repricing in monetary policy would weigh on growth. One of the major fears following the ECB meeting was that absent a new tool designed to stem fragmentation, peripheral spreads would widen out, and yesterday brought a fresh round of peripheral widening, with 10yr Italian spreads widening +14.6bps to bunds, with Spanish bonds widening +9.9bps. Indeed, 10yr BTPs crossed 4.0% for the first time since 2014.

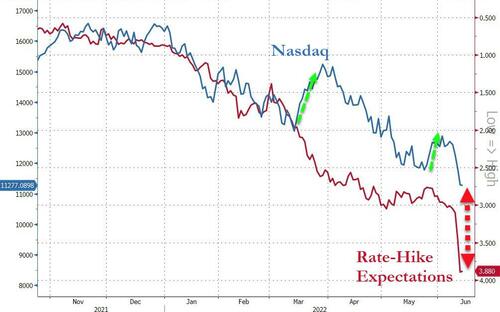

Equity markets got the message, selling off across the Atlantic, with the S&P 500 falling -3.87% into bear market territory, down -21.82% from the all-time highs reached in early January, with the STOXX 600 down -2.41%. At one point, every single share in the S&P 500 was lower, though the index staged a heroic rally leaving 5 shares higher on the day. That’s the lowest amount since June 11, 2020 when only one share advanced. Unsurprisingly, every S&P 500 sector was lower, with all but two sectors declining by more than 3%. The NASDAQ fell -4.68% on the hit from higher discount rates, now -32.68% from its November high. Mega-cap shares bore the brunt of higher discount rates, with the FANG+ falling -6.50%, its worst day since September 2020, and -40.98% lower from its own all-time highs reached in November. Markets are trying to bounce this morning with S&P 500 futures +1% and Nasdaq futures +1.15%

As we discussed yesterday, this sharp rates repricing is partly due to another attempt at forward guidance from the Fed. Having signalled 50bps at the next two meetings a few weeks ago they reduced volatility. However when it became clear that this guidance may be insufficient it has opened up a market attack. The last man standing continues to be the BoJ and to be honest the more the market attacks the Fed and the ECB the more likely it is that the BoJ own forward guidance (in the form of YCC) will end very messily with huge implications for global rates. If the BoJ throws in the towel in H2 then global bond markets lose a huge anchor. Certainly one to watch for every morning when you wake up! Indeed the BOJ ramped up its scheduled purchases of 5-to-10-year debt today from an expected ¥500 billion to ¥800 billion as the yield on the 10yr JGBs jumped to 0.255%, edging past the upper end of the central bank’s 0.25% target range.

Talking of Asia, equity markets are lower this morning but markets are trying to fight back. The Nikkei (-2.00%) is the largest underperformer with the Hang Seng (-1.15%) and Kospi (-1.11%) also lagging. In mainland China, the Shanghai Composite (-1.60%) and CSI (-1.86%) are also lower. Elsewhere, the S&P/ASX 200 is -4.54% lower after returning to trade following a holiday yesterday.

In such a broad-based selloff, many would have been interested in how crypto assets would hold up, supposedly uncorrelated with traditional assets. However, digital assets did not escape the wrath of plummeting risk sentiment, with bitcoin falling -15.13% and down another -5.28% this morning as we type. At one point this morning, Bitcoin fell about -10% to trade at $20,823 before recovering a little. There were reports that some exchanges were having trouble liquidating holdings of various crypto assets. This is a classic deleveraging and unwinding of a bubble trade.

To the day ahead now. The ECB’s Schnabel speaks, while in data we get UK jobless claims, ILO unemployment rate, ZEW surveys for the Eurozone and Germany, US NFIB small business optimism and PPI, and Canadian manufacturing sales. Hold on to your hats.

3. ASIAN AFFAIRS

i)TUESDAY MORNING// MONDAY NIGHT

SHANGHAI CLOSED UP 33.35PTS OR 1.02% //Hang Sang CLOSED UP 0.41 PTS OR 0.00% /The Nikkei closed DOWN 357.58 OR 1.33% //Australia’s all ordinaires CLOSED DOWN 3.39% /Chinese yuan (ONSHORE) closed UP 6.7359 /Oil UP TO 121.65 dollars per barrel for WTI and UP TO 123.21 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7359 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7572: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

SOUTH KOREA

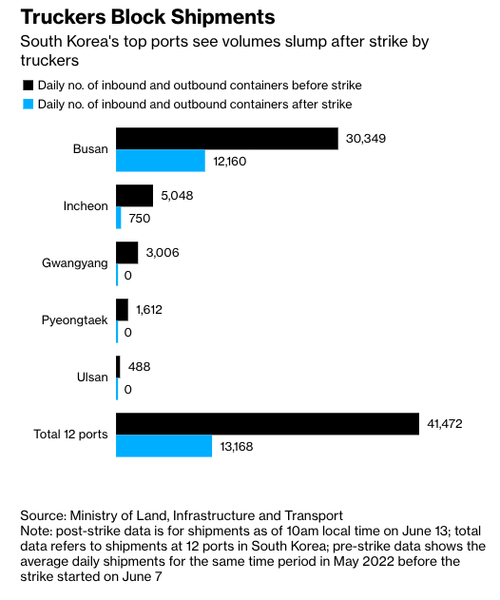

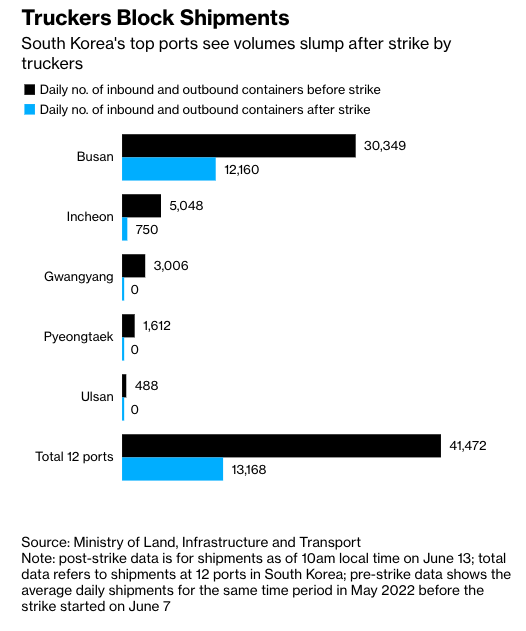

This could very well spark economic turmoil for the world as a nationwide trucker strike broadens.

(zerohedge)

Trucker Strike In South Korea Sparks Economic Turmoil, Risks Global Spillover

MONDAY, JUN 13, 2022 – 06:00 PM

The epicenter of the next global supply chain snarl could be in South Korea as a nationwide trucker strike broadens and is hindering domestic economic activity, which may spill over to the rest of the world.

Bloomberg reports that the Cargo Truckers Solidarity Union entered its seventh day of strikes on Monday, causing $1.6 billion in disruptions for auto, petrochemical, steel, and other top industries.

South Korean steel-making company POSCO, the world’s fourth-largest steelmaker, has already limited production at some factories while the impacts are spreading across the economy.

The strike has impacted companies in Seoul the hardest. Shares of Posco slumped nearly 4%, Hyundai Motor Co. fell 5%, Petrochemical company Hanwha Corp. 4%, and LG Chem Ltd. slipped 3.6%.

Reuters said about a third of the union members (7,000) were striking Monday, and there is no end in sight.

Deliveries of automobiles, fuels, steel, and materials for semiconductor chips have been suspended or delayed. Continued disruption of domestic shipments and factories limiting production could have ripple effects across the globe, especially since South Korea is the top exporter of memory chips.

The strike’s impact could be more severe this week as the fourth round of negotiations between the striking truckers and government officials failed on Sunday. The union demands minimum pay guarantees and is furious about soaring diesel prices.

“We are thinking of a complete blockade,” union leader Kim Jae-gwang told Reuters, indicating they intend to block coal shipments to a power plant in Gunsan, North Jeolla Province. Reuters noted impacts to power would be limited but shows an intensification of truckers’ actions.

Signs of global spillovers are materializing as container volume transported to and from the nation’s 12 ports plunged 68% on Monday compared with the average for May, according to the Ministry of Land, Infrastructure, and Transport. At Port of Busan, the largest port in the country and the world’s seventh busiest port, inbound and outbound volumes were halved versus their average amount.

Besides semiconductors, the auto industry could be heavily impacted by the strike.

Hyundai Motor Group said Friday that partial production disruptions were reported at its Ulsan factory, with Chosun Ilbo reporting that 50% of production was halted.

An analyst at the Korea Institute for Industrial Economics & Trade, Cho Chuel, warned the strike could “worsen inflation with fewer supplies available,” adding it’s still too early to tell what economic damages will be.

South Korea could throw another wrench in chaotic global supply chains, already reeling from COVID, fallout of the Ukrainian conflict, and the mess in Shanghai.

3B JAPAN

end

3c CHINA

CHINA/TAIWAN

Xi widens the legal basis for Chinese troop deployments as Taiwan tensions escalate.

(zerohedge)

Xi Widens Legal Basis For PLA Troop Deployments Amid Soaring Taiwan Tensions

MONDAY, JUN 13, 2022 – 08:00 PM

At a moment the Pentagon is warning Beijing about its heightened military maneuvers around Taiwan, China’s President Xi Jinping has just signed an order which fundamentally expands the conditions under which People’s Liberation Army (PLA) troops can be deployed.

The freshly signed and promulgated order introduces a legal framework to deploy troops in “non-war military actions” which takes effect Wednesday, according to state media. It could have significant repercussions for tensions with the US and Washington allies like Australia or Japan in places like the South China Sea and the Taiwan Strait, given the order loosens the conditions under which it’s possible to initiate “military operations other than war” which involves operations that do not explicitly involve direct conflict or combat.

According to a list in state-run Global Times, the Xi-backed initiative will seek to standardize usage of PLA troops in non-military situations such as the following:

“disaster relief, humanitarian aid, escort, and peacekeeping, and safeguard China’s national sovereignty, security and development interests…”

And additionally, “The outlines aim to prevent and neutralize risks and challenges, handle emergencies, protect people and property, and safeguard national sovereignty, security and development interests, and world peace and regional stability, the Xinhua News Agency reported on Monday.”

Concerning this last justification on the list (and perhaps taking a page from America’s ‘Global War on Terror/GWOT’ playbook), it’s the “counter-terrorism” angle that could perhaps prove most elastic, and up for wide interpretation as Beijing readies potential new ways to wield the PLA as a blunt and powerful force enacting policy.

As GT writes, “The Chinese armed forces are also responsible for counter-terrorism, anti-pirate and peacekeeping missions, including regular escort missions in the Gulf of Aden and waters off Somalia as well as UN peacekeeping missions, providing public security goods to the international community, the expert said.”