by harveyorgan · in Uncategorized · Leave a comment·Edit

harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1847.25 UP $28.95

SILVER: $21.77 UP $0.46

ACCESS MARKET: GOLD $1833.90

SILVER: $21.69

Bitcoin morning price: $21,143 DOWN 526

Bitcoin: afternoon price: $20,969 DOWN 874

Platinum price: closing UP $10.85 to $955.50

Palladium price; closing UP $26.60 at $1885.90

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

COMEX

no. of contracts issued by JPMorgan: 767/878

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,815.300000000 USD

INTENT DATE: 06/15/2022 DELIVERY DATE: 06/17/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 102 9

323 C HSBC 15

363 H WELLS FARGO SEC 9

624 H BOFA SECURITIES 18

657 C MORGAN STANLEY 26

661 C JP MORGAN 776 767

700 C UBS 8

709 H BARCLAYS 9

732 C RBC CAP MARKETS 8

800 C MAREX SPEC 5

905 C ADM 4

TOTAL: 878 878

MONTH TO DATE: 23,689

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 878 NOTICE(S) FOR 87,800 Oz//2/7399 TONNES)

total notices so far: 23,689 contracts for 2,368,900 oz (73.683 tonnes)

SILVER NOTICES:

71 NOTICE(S) FILED 355,000 OZ/

total number of notices filed so far this month 1762 : for 8,810,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $28.95

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD//

INVENTORY RESTS AT 1063.74 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 46 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 544.399 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 6053 CONTRACTS TO 145,925 AND FURTHER FROM THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE HUGE LOSS IN OI WAS ACCOMPLISHED DESPITE OUR $0.44 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.44) BUT WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 26 CONTRACTS OR 130,000 OZ//NEW STANDING: 8,900,000 / // V) GIGANTIC SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS :-XXX

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 12 days, total 10,177, contracts: 50.535 million oz OR 4.208 MILLION OZ PER DAY. (848 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 50.535 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 50.535 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6053 DESPITE OUR STRONG $0.44 GAIN IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 945 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 130,000 QUEUE JUMP //NEW STANDING: 8,900,000 OZ // .. WE HAD A GIGANTIC SIZED LOSS OF 5108 OI CONTRACTS ON THE TWO EXCHANGES FOR 25.54 MILLION OZ DESPITE THE LOSS IN PRICE.

WE HAD 71 NOTICES FILED TODAY FOR 355,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 5343 CONTRACTS TO 492,113 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -591 CONTRACTS.

.

THE STRONG LOSS IN COMEX OI CAME DESPITE OUR RISE IN PRICE OF $6.50//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 2900 OZ E.F.P. JUMP TO LONDON //NEW STANDING: 74.606 TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $6.50 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 2878 OI CONTRACTS 8.951 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A fair SIZED 2465 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 492,113

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2878, WITH 5343 CONTRACTS DECREASED AT THE COMEX AND 2465 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2878 CONTRACTS OR 8.951 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2465) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (5343,): TOTAL LOSS IN THE TWO EXCHANGES 2878 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP OF 2900 OZ//NEW STANDING: 74.696 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) STRONG SIZED COMEX OI LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

50,000 CONTRACTS OR 5,000,000 OZ OR 155.52 TONNES 12 TRADING DAY(S) AND THUS AVERAGING: 4166 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES: 155.52 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 155.52/3550 x 100% TONNES 4.38% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 155.52 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A GIGANTIC SIZED 6053 CONTRACT OI TO 145,925 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 945 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 945 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 6053 CONTRACTS AND ADD TO THE 945 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF 5108 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 25.54 MILLION OZ

OCCURRED WITH OUR GAIN IN PRICE OF $0.44 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 20.02 PTS OR 0.61% //Hang Sang CLOSED DOWN 462.78 PTS OR 2.13% /The Nikkei closed UP 105.04 OR 0.40% //Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN 6.7149 /Oil DOWN TO 113.77 dollars per barrel for WTI and DOWN TO 116.23 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7149 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7204: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 5343 CONTRACTS TO 492,113 AND CLOSER TO THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $6.50 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (2465 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2465 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :2465 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2465 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2878 CONTRACTS IN THAT 2465 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED COMEX OI LOSS OF 5343 CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF GOLD $6.50.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.606),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.609 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $6.50) AND WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 7113 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.609 TONNES)…

WE HAD 297 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2287 CONTRACTS OR 228,700 OZ OR 7.113 TONNES

Estimated gold volume 170,654/// poor/

final gold volumes/yesterday 215,239 /fair

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 16

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 133,169.434 ozMalcaBrinks4142 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 878 notice(s)87800 OZ2.7309 TONNES |

| No of oz to be served (notices) | 297 contracts 29,700 oz0.9237 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,689 notices2,368,900 OZ73.683 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

2 customer withdrawals:

i) Out of Brinks 257.200 oz 8 kilobars

ii) Out of MALCA: 132,912.234 oz (4134 kilobars)

total withdrawal: 133,169.434 oz

ADJUSTMENTS: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1175 contracts having LOST 233 contracts

We had 204 notices filed on WEDNESDAY so we LOST 29 contracts or an additional 2900 oz will NOT stand for gold in this very active month of June as they were EFP’d to London

July has a GAIN OF 7 OI to stand at 1873

August has a loss of 5573 contracts DOWN to 407,782 contracts

We had 878 notice(s) filed today for 87,800 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 776 notices were issued from their client or customer account. The total of all issuance by all participants equate to 878 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 767 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,689) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 1175 CONTRACTS ) minus the number of notices served upon today 878 x 100 oz per contract equals 2,398,600 OZ OR 74.609 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,689) x 100 oz+ (1175) OI for the front month minus the number of notices served upon today (878} x 100 oz} which equals 2,401,500 oz standing OR 74.609 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74,609 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 34,155,141.645 OZ

TOTAL ELIGIBLE GOLD: 16,642,191.923 OZ

TOTAL OF ALL REGISTERED GOLD: 17,512,949.725 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 15,093154.0 OZ (REG GOLD- PLEDGED GOLD)

END

JUNE 2022 CONTRACT MONTH//SILVER//JUNE 16

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2,077,452.220 ozDelaware HSBCManfraJPMorgan |

| Deposits to the Dealer Inventory | 228,561.000OZManfra |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 71CONTRACT(S)355,000 OZ) |

| No of oz to be served (notices) | 18 contracts (90,000 oz) |

| Total monthly oz silver served (contracts) | 1762 contracts 8,810,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 1 dealer deposit

Into Manfra: 228,361.000 oz

total dealer deposits: 228,361.000 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 4 deposit into the customer account

i) Into Delaware 521,340.466 oz

ii) Into HSBC: 601,976.450 oz

iii) Into JPMorgan: 599,273.224 oz

iv) Into Manfra: 354,861.900 oz

total deposit: 2077,452.224 oz

JPMorgan has a total silver weight: 169,645 million oz/337.252 million =50.29% of comex

Comex withdrawals: 3

i) International Delaware 19,391.09 oz

ii) Malca 551,742.632 oz

iii) Out of JPMorgan: 557,742.632 oz

total withdrawal 1,761,835.722 oz

0 adjustments:

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.395 MILLION OZ

TOTAL REG + ELIG. 337.252 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 89 HAVING GAINED 7 CONTRACTS.

WE HAD 19 NOTICES FILED ON WEDNESDAY SO WE GAINED 26 CONTRACTS OR AN ADDITIONAL 130,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 9023 CONTRACTS DOWN TO 56,768 CONTRACTS.

AUGUST LOST 2 CONTRACTS TO STAND AT 1001

SEPTEMBER HAD A GAIN OF 2971 CONTRACTS UP TO 71,011 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 71 for 355,000 oz

Comex volumes:61,834// est. volume today// fair

Comex volume: confirmed yesterday: 88,658 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1762 x 5,000 oz = 8,810,000 oz

to which we add the difference between the open interest for the front month of JUNE(89) and the number of notices served upon today 71 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1762 (notices served so far) x 5000 oz + OI for front month of JUNE (89) – number of notices served upon today (71) x 5000 oz of silver standing for the JUNE contract month equates 8,900,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1063.75 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

Will This Be The Last Move In The Fed’s Inflation Fight?

THURSDAY, JUN 16, 2022 – 09:32 AM

Authored by Michael Maharrey via SchiffGold.com,

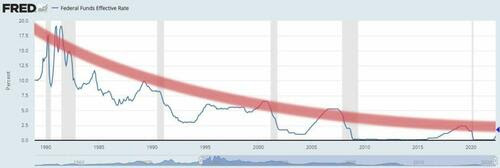

The Federal Reserve took a more aggressive swing at red-hot inflation at its June FOMC meeting, raising interest rates by 3/4%. It was the biggest hike since 1994. The question is will this be the last swing at inflation?

Federal Reserve Chairman Jerome Powell continues to claim a “soft landing” is possible and the Fed can get inflation back to the 2% target without tipping the economy into a recession. He insists the economy remains strong and the American consumer is healthy.

I’m not convinced about any of this.

Keep in mind this is the same guy who told us pumping trillions of dollars into the economy during the pandemic wouldn’t cause inflation and then that inflation was “transitory.” The Fed has a pretty miserable track record when it comes to its economic projections.

The 75 basis-point rate hike wasn’t a complete surprise after the May CPI data came in hotter than expected. Markets immediately began pricing in the hike. But just one month ago, a 3/4% interest rate increase wasn’t even under consideration.

Reading between the lines, I think that the Fed hoped that its meager 50 basis-point hike last month, along with a little tough talk, would rein in the inflation dragon. During his post-meeting press conference, Powell confessed the committee was surprised it didn’t work.

We’ve been expecting progress and we didn’t get that; we got sort of the opposite.”

With the data clearly indicating inflation hasn’t peaked, the Fed had little choice but to get more aggressive.

Powell even left the possibility of another 75 basis-point rate increase on the table. But he also gave the Fed some wiggle room to slow its roll.

Clearly, today’s 75-basis-point increase is an unusually large one, and I do not expect moves of this size to be common. From the perspective of today, either a 50-basis-point or a 75-basis-point increase seems most likely at our next meeting. We will, however, make our decisions meeting by meeting and we’ll continue to communicate our thinking as clearly as we can.”

As far as balance sheet reduction goes, there wasn’t any change in policy. The FOMC statement said, “The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve’s Balance Sheet that were issued in May.”

Powell said, “We are continuing the process of significantly reducing the size of our balance sheet.” [Emphasis added]

Using the word “significantly” seems a bit of an overstatement given the size of the balance sheet. And the plan outlined last month was less than impressive. It’s certainly not significant. If the central bank follows through (and it almost certainly won’t) it would take about eight years to reduce the balance sheet back to prepandemic levels.

The mainstream praised the Fed for its aggressive move against inflation. The stock market even rallied. But in the big scheme of things, this was not particularly aggressive. FOMC members think that pushing rates to 3.5 to 4% should do the trick. Remember, Paul Volker had to run rates up to 20% to slay the inflation dragon of the 1970s. That was well above the CPI at the time, meaning the Fed would need to get rates over 8% to tame the current bout of inflation. (And of course, the actual CPI is much closer to those 1970s levels than the cooked numbers used today indicate.)

I don’t think it will even get rates to 3%.

Pop Goes the Bubble

This economy was built on easy money and debt. Taking away the easy money will pop the bubble and collapse the house of cards economy. In reality, this needs to happen. We need a recession to cleanse all of the misallocations and distortions out of the economy. But that would mean a lot of pain. And for all of the tough talk, I don’t think the Fed has the political will to allow the economy to crash.

Powell seems to be in complete denial about the condition of the economy. During his press conference, he painted a rosy picture completely detached from reality.

Overall spending is very strong. The consumer is in really good shape financially. They’re spending. There’s no sign of a broader slowdown that I can see in the economy. People are talking about it a lot. Consumer confidence is very low. That’s probably related to gas prices and also just stock prices, to some extent, for other people. But that’s what we’re seeing. We’re not seeing a broad slowdown. We see job growth slowing, but it’s still at quite robust levels. We see the economy slowing a bit, but still growth levels—healthy growth levels.”

Meanwhile, the Atlanta Fed just revised its Q2 GDP growth projection to — zero. That follows on the heels of a -1.5 GDP print in the first quarter. Powell is saying he thinks the Fed can slay inflation without pushing the economy into a recession, but the numbers tell us we’re probably already in one. And Powell calls this a “healthy” growth level.

As for consumer spending, retail sales unexpectedly declined in May, despite rapidly rising prices. For the last several months, sanguine pundits pointed to “strong” retail sales as proof the consumer remained healthy. Even then, it was clear that Americans weren’t buying more stuff. They were simply paying more for the things they were buying. Keep in mind that retail sales aren’t inflation-adjusted. Rising prices alone can lift retail sales data. It now appears consumers are reining in spending even more.

To keep up with rising prices, American consumers are charging up their credit cards. Consumer debt hit a record level in April. Despite Powell’s claims, the consumer is not in “good shape” financially.

As Powell alluded to, the consumer isn’t nearly as confident about the economy as the central bankers over at the Fed. In fact, the average American has never been less confident about the economy – at least not in the last 50 years.

The data indicates the economy is at a tipping point. If this rate hike doesn’t push it over the edge, the next one almost certainly will.

Passant Gardant published this graph that indicates the current interest rate is very close to the maximum that the economy can handle before plunging into a recession.

As you can see, the peak of the rate hike cycle gets lower and lower with each subsequent tightening. No matter how emphatically Powell insists that the Fed can raise interest rates, slay inflation and bring us to a soft landing, reality says otherwise. There is nothing to lead us to believe that the Fed can get rates to 2% without crashing the bubble economy, much less hike them to 3.5% or 4%. (And that’s not even enough to slay inflation.)

The Fed is at a crossroads. The question is which direction will it go? Will it continue to fight inflation, despite a crashing economy? Or will it surrender and pivot back to easy money and quantitative easing, letting inflation run wild in order to rescue the economy?

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

END

3. Chris Powell of GATA provides to us very important physical commentaries

Kinross, the bad luck gold miner now faces more problems as they sell off Russian mines but at half the agreed prices

(National Post/Shekter)

Kinross Gold sells off Russian mines but at half the agreed price

Submitted by admin on Wed, 2022-06-15 21:41Section: Daily Dispatches

By Barbara Shecter

National Post, Toronto

Wednesday, June 15, 2022

Kinross Gold Corp. has sold all its Russian assets to the Highland Gold Mining group of companies, but the Canadian miner will realize just half the $680 million in proceeds agreed to in April, following a review by the recently formed Russian Sub-commission on the Control of Foreign Investments.

The Russian sub-commission “approved this transaction for a purchase price not exceeding $340 million,” Kinross said in a statement today.

Kinross has received $300 million in U.S. dollars in its corporate account and will receive a deferred payment of $40 million on the one-year anniversary of closing.

The $680 million previously agreed to in April was to include an initial payment of $100 million on closing, with the remaining $580 million scheduled to be received in annual payments from 2023 through to 2027. …

… For the remainder of the report:

end

(GATA) Yikes! Gold and silver market rigging gets acknowledged at PDAC

11:55p ET Wednesday, June 15, 2022

Dear Friend of GATA and Gold:

With the Prospectors and Developers Association of Canada resuming its annual convention in Toronto this week, First Majestic Silver CEO Keith Neumeyer tells Stansberry Research’s Daniela Cambone that he sponsored a reception for silver mining executives and investors in part because he wanted them to discuss market manipulation and maybe even try to do something about it.

Neumeyer long has been the only major silver mining executive to acknowledge and protest the manipulation of the monetary metals markets.

But, amazingly, a few minutes later Cambone herself remarks that people in the mining business seem increasingly willing to acknowledge the possibility of gold and silver market manipulation.

Of course it has been only 23 years since GATA began trying to get the dunderheads and their hapless shareholders to look at the overwhelming proof that gold and silver price suppression is longstanding government policy —

— and to protest it to their governments and financial news organizations.

You’ll know that the mining industry is getting serious about defending itself and serving its shareholders when GATA at last is invited to make a presentation at a PDAC conference. That will be when PDAC figures that letting gold and silver investors know what that they are up against is more important than pumping and dumping the shares of companies whose products government is determined to devalue, and that will truly be the day.

Cambone’s discussion with Neumeyer is nine minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch? v=uVQ631gKglY

CHRIS POWELL, Secretary/Treasurer

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED DOWN 6.7149

OFFSHORE YUAN: 6.7204

HANG SANG CLOSED DOWN 462.78 PTS OR 2.13%

2. Nikkei closed UP 105.04% OR 0.40%

3. Europe stocks ALL CLOSED ALL RED

USA dollar INDEX DOWN TO 104.91/Euro FALLS TO 1.0399

3b Japan 10 YR bond yield: RISES TO. +.250/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.79/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN -// OFF- SHORE DOWN

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.907%/Italian 10 Yr bond yield RISES to 4.03% /SPAIN 10 YR BOND YIELD RISES TO 3.03%…ALL BLOWING UP!!

3i Greek 10 year bond yield RISES TO 4.33//

3j Gold at $1822.40 silver at: 21.40 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 4/10 roubles/dollar; ROUBLE AT 56.66

3m oil into the 113 dollar handle for WTI and 116 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 134.49DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

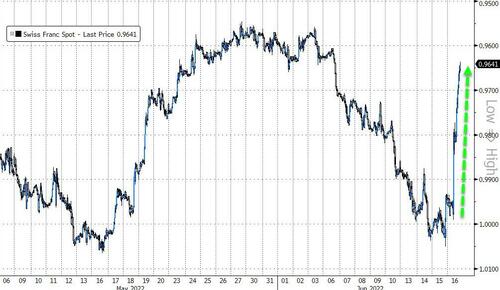

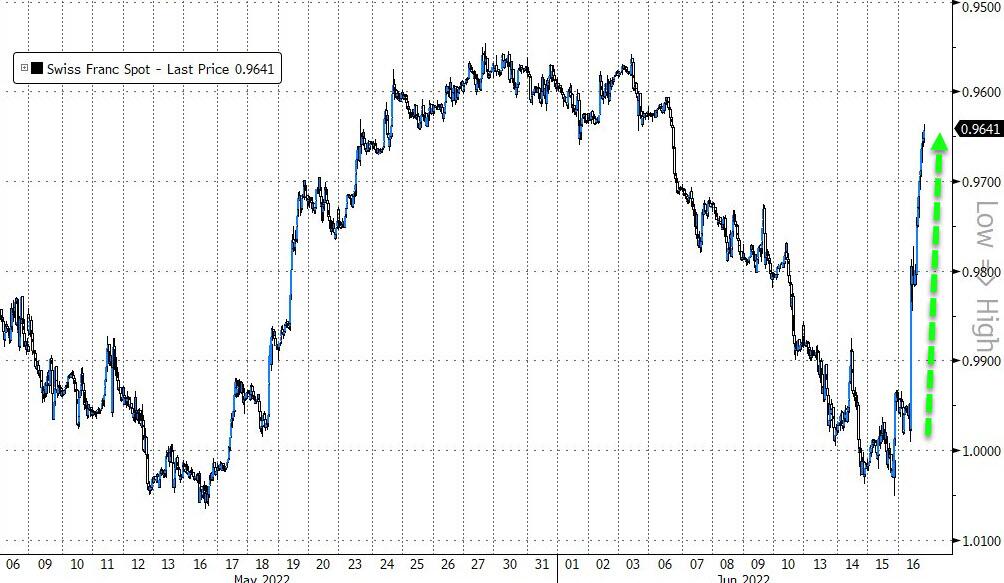

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.98069– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0198well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.468 UP 7 BASIS PTS

USA 30 YR BOND YIELD: 3.474 UP 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.32

Futures Crash, Dow Down 600 As Recession Reality Sets In

THURSDAY, JUN 16, 2022 – 08:25 AM

In our preview of how to trade the Fed’s 75bps rate hike, we said to expect a “kneejerk move higher (especially if we get an outsized hike, hinting the Fed is hoping to catch up to the curve), then a gradual drift lower” (a reco which was later echoed by Goldman). Sure enough, in the aftermath of the FOMC announcement yesterday, we got the knejerk move higher… and then overnight, the drift lower has also appeared tight on schedule, with futures tumbling in the US, undoing the entire post-FOMC move higher, and dragging global stocks lower as traders come to grips with the realization that 75bps of hikes – far from bullish – means that a recession is now on deck. As a result, S&P futures were down 2.2%, tumbling as much as 130 points from overnight session highs, while Dow futures puked a whopping 600 points as central banks lose control over markets. European stocks headed for a 16-month low and Chinese Internet shares dropped in premarket New York trading

And speaking of losing control, while normally yields would be tumbling ahead of a recession, this time they are doing the opposite with 10Y yields blowing out just shy of 3.50%, up 20 bps on the session after sliding following the biggest Fed hike in 28 years, as the bond market is starting to price in the uglier stagflation part of the coming recession, while stocks focus on the collapse in spending.

“The volatility in bond markets is definitely not over,” Jasmin Argyrou, director and portfolio manager at Credit Suisse Private Bank, said on Bloomberg Television. “The likelihood is that policy rates in the US may need to go to a more restrictive stance than even the market is pricing in.”

After the Fed raised interest rates by the most since 1994, Powell indicated a monetary stance similar to that of Paul Volcker, who broke the back of elevated inflation four decades ago but paid a price in the form of soaring unemployment and a credit squeeze. Powell’s comments signaled the Fed’s resolve to continue on an aggressive path of rate hikes, and that bond yields and equity risk premiums must rise to adjust to the new reality.

“It hasn’t taken long for the post-Fed bounce in stocks to fade, and given the gloomier outlook for growth, that is hardly surprising,” said Chris Beauchamp, the chief market analyst at IG Group in London. “We are still living in the same world we were 24 hours ago, one where growth is slowing, earnings are still falling and prices keep on rising. This is not a great environment for stocks.”

Nvidia, Tesla, Netflix, GM, Amazon, Ford, Apple and Microsoft were among the worst performers in premarket trading, as major US technology and internet stocks fell, poised to erase all or most of Wednesday’s gains. Apple -2.2%, Microsoft -2.5%, Amazon.com -2.5%, Alphabet -2.3%, Meta Platforms -2.3%, Nvidia -3.2%. Shares in Twitter rose ahead of a reported company-wide meeting between Tesla CEO Elon Musk and employees of the social media firm. Here are some other notable premarket movers:

- AC Immune (ACIU) shares slump 23% after the pharma firm said that its Alzheimer’s treatment Crenezumab did not meet its primary endpoints in a study.

- Arthur J Gallagher (AJG) is upgraded to outperform from sector perform at RBC Capital Markets, with broker citing the insurance broker’s growth, visibility and strong cash flows. Shares declined 2%.

- AutoZone and Dollar General (DG) are upgraded to overweight from equal- weight at Morgan Stanley, while AirSculpt Technologies and Sally Beauty Holdings see downgrades, as broker shuffles ratings to favor “defensive stocks with offensive characteristics.” Shares decline 1%.

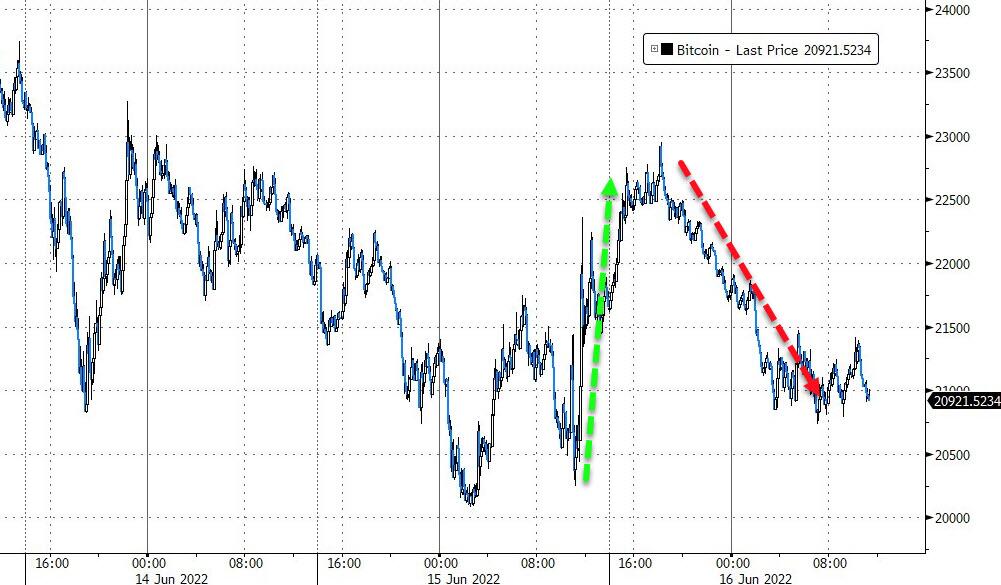

- Cryptocurrency-related stocks resumed their slump on Thursday as a broad-based selloff in risk assets sent Bitcoin lower for a 10th straight session, its longest losing streak ever, according to data compiled by Bloomberg going back to 2010. Coinbase (COIN) shares decline 4%.

- Electric-vehicle stocks fall in US premarket trading as worries over rising inflation and the possibility of a recession hit shares in high-growth companies, while Jefferies cut its global EV sales estimates for this year and next. Tesla falls 4% in US premarket trading, Rivian -3%, Lucid -3%, Nikola -4%

- Twitter (TWTR) shares rise 2% in premarket trading, outperforming declines for most big tech stocks, ahead of a reported company-wide meeting between Tesla CEO Elon Musk and employees of the social media firm the billionaire agreed to buy for $44 billion in April.

- Volta Inc. (VLTA) is downgraded to neutral from overweight at Cantor Fitzgerald, which cites recent management changes at the electricvehicle charging company. Shares decline 1.3%.

- Chinese Internet companies NetEase Inc. and Pinduoduo Inc. slid at least 4.5% each in early New York trading. Technology shares were among the biggest losers on Thursday globally as their higher valuations relative to other sectors turned unappealing on the back of rising bond yields.

Growth stocks are likely to suffer even more in the near-term, according to Richard Carter, head of fixed income research at Quilter Cheviot. “Investors are understandably concerned that such a sharp pace of monetary tightening will lead to a recession and markets are likely to remain volatile until we reach a peak in inflation,” he said.

In Europe, retailers and tech companies were among the biggest decliners in the Stoxx Europe 600 Index, which fell 2.1% to a fresh 16-month low; the Euro Stoxx 50 slumped over 2.5%, with Germany’s DAX underperforming and losing as much as 2.8%. Losses are broad based with all Stoxx 600 sectors in the red. Retail is the standout underperformer, dropping over 4.5%; tech and chemical sectors decline over 3.5%. Chipmaker ASML Holding dropped 4.9% in Amsterdam. Here are other notable movers:

- Online retailers drop across the board after Asos cut its forecast for full-year sales, while peer Boohoo recorded the first UK sales decline in its history. Asos shares slid as much as 30%, Boohoo -19%, Zalando -12%, AO World -7.7%

- THG falls as much as 23% after Nick Candy walked away from making an offer, just hours after a rival consortium also dropped its pursuit.

- Philips declines as much as 9.1% after UBS downgraded the stock to sell from hold, saying overhangs from legal issues related to the DreamStation recall will continue to weigh on shares in the foreseeable future.

- Thule drops as much as 8.8%, taking the YTD slump in the bike rack and cargo-carrier maker’s shares to about 50%. Nordea trimmed its estimates “again.”

- Atos slumps as much as 10% after Bryan Garnier slashed its PT for the French IT services company to a Street low of EU13 from EU24, saying the stock will look unattractive for a year.

- European chemicals stock index drops as much as 4% amid a broad decline in markets. BASF underperforms, while beyond the index Synthomer sinks on a downgrade from Barclays. BASF shares down as much as 6.6%, Synthomer -7.9%

- Tech stocks in Europe slide amid fears of a more likely recession, with the Federal Reserve committed to bring down raging inflation. ASML shares slide as much as 5.1%, Infineon -5.2%, Just Eat -6.3%, Deliveroo -5.6%

- Euronext climbs as much as 4.2% after the stock-market operator was upgraded to overweight from neutral at JPMorgan due to “increasingly” attractive valuation and improving earnings momentum.

- Inchcape jumps as much as 6.5% after the automotive distributor published a trading statement, which Peel Hunt said was “positive.”

In the UK, the Bank of England raised interest rates by 25 basis points, a smaller move than what most global central banks are delivering. That affirmed policymakers’ worries over the potential for recession, sending the pound tumbling as much as 1% against the dollar.

Earlier in the session, Asian stocks were mostly positive and followed suit to the gains on Wall Street. ASX 200 traded higher but with gains capped as participants reflected on the latest data releases including a mixed jobs report and a further rise in consumer inflation expectations. Nikkei 225 shrugged off mixed trade data as Japan seeks to raise the minimum hourly wage above JPY 1000 and is also looking to implement steps to increase tourist demand next month. Hang Seng and Shanghai Comp. were choppy with COVID-related concerns stoked by an increase in cases in Hong Kong and with Shanghai to conduct weekly community COVID testing across all districts until end-July, while property names lagged after Chinese house prices contracted Y/Y.

Japanese stocks climbed amid relief over the Federal Reserve’s plan for interest rate hikes as investors awaited a decision from the Bank of Japan due Friday. The Topix rose 0.6% to close at 1,867.81, while the Nikkei advanced 0.4% to 26,431.20. The yen resumed weakening against the dollar. Toyota Motor Corp. contributed the most to the Topix gain, increasing 2.9%. Out of 2,170 shares in the index, 1,414 rose and 657 fell, while 99 were unchanged.

“Relief that the FOMC rate hike passed without a hitch, mostly within market expectations, is pushing Japanese stocks higher,” said Shogo Maekawa, a strategist at JPMorgan Asset Management, who will not be happy when he sees today’s action. “The focus from here in the market will be on how far inflation can be contained by the FOMC before the US economy slows, but the outlook still remains uncertain.”

In Australia, rhe S&P/ASX 200 index swung to a loss of 0.2% to close at 6,591.10, weighed by declines in banks and healthcare shares. Seven of the 11 subgauges ended lower, while mining stocks rebounded to end a four-day losing streak. In New Zealand, the S&P/NZX 50 index rose 0.1% to 10,646.58

India’s key stock indexes plunged to their lowest level in over a year on concerns aggressive interest rate hikes by global central banks will begin to hurt demand amid higher cost pressures on companies. The S&P BSE Sensex fell 2% to 51,495.79 in Mumbai, after rising as much as 1.1% earlier in the session. The NSE Nifty 50 Index declined 2.1%. Both measure have dropped nearly 17% from their October peaks. Reliance Industries Ltd. fell 1.4% to its lowest level in nearly a month. It was the biggest drag on the Sensex which saw all but one of its 30-member stocks trading lower. All 19 sectoral indexes compiled by BSE Ltd., fell, led by a measure of metal companies. “Analysts are already prepping for earnings downgrades as central banks around the world step up with large rate hikes to keep inflation tethered,” said Abhay Agarwal, a fund manager at Piper Serica Advisors. The US Federal Reserve raised rates 75 basis points Wednesday, in line with the most recent projection of economists, stepping up its fight against inflation. In India, consumer-price inflation is above the central bank’s target, while input costs continue to rise for manufacturers. “A double whammy of higher costs and lower demand due to rate hikes would mean lower margins for companies,” Agarwal said

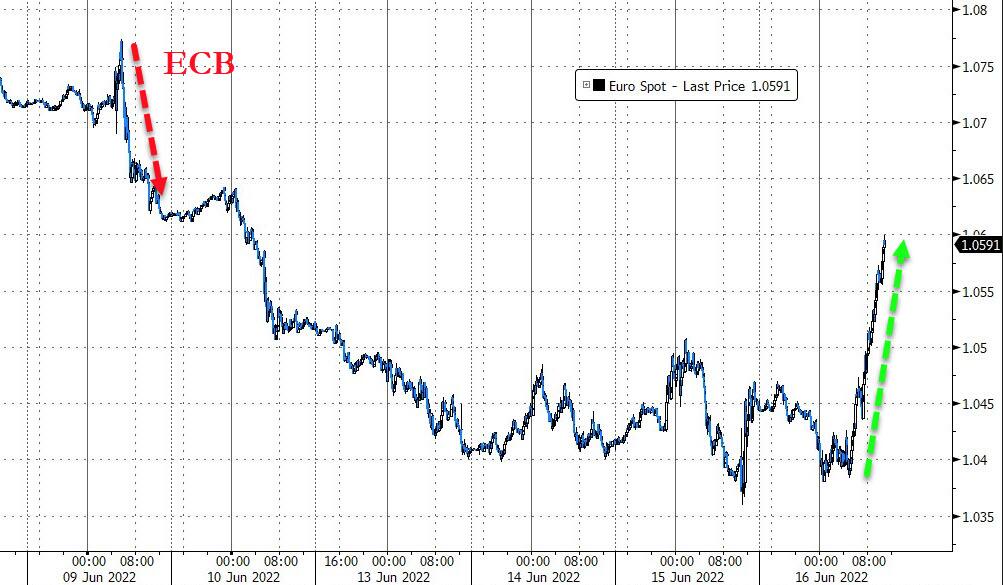

In FX, the Bloomberg Dollar Spot Index rose as the greenback strengthened against all of its Group-of-10 peers apart from the yen and the Swiss franc. European currencies were the worst performers, with Sweden’s krona slumping to a three-month low against the euro. The Swiss franc advanced by as much as 1.7% against the dollar and 2.1% versus the euro after SNB’s announcement. SNB President Thomas Jordan said the central bank would be prepared to purchase foreign currency if there were to be an excessive appreciation of the Swiss franc and also consider selling foreign currency if the Swiss franc were to weaken. The euro traded around $1.04 after earlier touching a day low of 1.0381. German bonds and euro-area peers tumbled led by the belly of the curve and money markets cranked up ECB rate hike bets on the back of the SNB’s move. Treasuries also slid while UK bonds erased gains and sterling fell against the dollar and the euro ahead of the BOE monetary policy announcement. Cable one-day volatility hit its highest level since 2020 Wednesday, rising toward the 30 vols handle.

In rates, Treasuries tumbled to fresh lows, with yields cheaper by 10bp to 15bp across the curve while post-Fed rally in stocks also fades. US 10-year yields around 3.435%, cheaper by 14bp on the day with bunds lagging by 3bp on the sector and gilts outperforming by 7bp; in Treasuries, front- and belly led declines flattens 2s10s, 5s30s spreads. Losses led by front-end of the curve as another 75bp rate hike gets priced back in for the July meeting. Gilt extended losses after Bank of England raised benchmark rate to 1.25% in a 6-3 vote. Fed-dated swaps price in 75bp of rate hikes for the July meeting and an additional 280bp of hikes by the end of the year. IG dollar issuance slate empty so far; Thursday’s activity may include some corporate issuers offering short-duration bonds.

In commodities, crude oil fell as traders weighed the outlook for supply and demand amid Fed tightening and rising US crude output. Crude futures declined with WTI hitting lows for the week near $114.50. Spot gold is little changed at $1,830/oz. Base metals are mixed; LME aluminum falls 1.1% while LME lead gains 0.4%. Bitcoin dropped and traded closer to $21,000 apiece.

Looking at the day ahead now, and one of the highlights will be the aforementioned BoE decision. In addition, there’s an array of ECB speakers including Vice President de Guindos, along with the ECB’s Visco, Villeroy, Panetta, Vasle, Knot, Centeno, De Cos and Makhlouf. Data releases include US housing starts and building permits for May, the weekly initial jobless claims, and the Philadelphia Fed’s business outlook survey for June.

Market Snapshot

- S&P 500 futures down 1.8% to 3,721.25

- STOXX Europe 600 down 1.4% to 407.43

- MXAP down 0.3% to 158.95

- MXAPJ down 0.9% to 524.81

- Nikkei up 0.4% to 26,431.20

- Topix up 0.6% to 1,867.81

- Hang Seng Index down 2.2% to 20,845.43

- Shanghai Composite down 0.6% to 3,285.39

- Sensex down 1.5% to 51,771.21

- Australia S&P/ASX 200 down 0.2% to 6,591.10

- Kospi up 0.2% to 2,451.41

- German 10Y yield little changed at 1.75%

- Euro down 0.6% to $1.0385

- Brent Futures up 0.4% to $118.97/bbl

- Brent Futures up 0.4% to $118.97/bbl

- Gold spot down 0.1% to $1,832.27

- U.S. Dollar Index up 0.14% to 105.31

Top Overnight News from Bloomberg

- The Swiss National Bank unexpectedly increased interest rates for the first time since 2007, shifting away from a battle to tame a stronger currency to focus on inflation that threatens to get out of hand

- The ECB will raise interest rates from historic lows in a gradual and sustained fashion to bring inflation back to the 2% target, according to Governing Council member Francois Villeroy de Galhau

- Investors shouldn’t question the ECB’s resolve to undue prevent panic on government bond markets as interest rise from record lows, according to Vice President Luis de Guindos

- European authorities will announce that Greece is on track to exit its enhanced surveillance status in August in a statement later Thursday, Greek Finance Minister Christos Staikouras says in an interview with state-run radio Proto Programma

- Banque Pictet & Cie is expanding the scope of financial derivatives that it trades on behalf of clients, in a move that underscores how wealth managers are seeking new ways to protect assets against global shocks

- The first batch of a Chinese offshore yuan sovereign bond sale saw the strongest demand in nearly two years, defying a recent stream of outflows at a time when the global debt market is showing deepening levels of stress

- Hungary unexpectedly hiked the country’s key interest rate after the forint fell to a record this week

- Taiwan’s central bank raised the discount rate to banks by 0.125 percentage points to 1.5%, less than the estimate 1.625%

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive and followed suit to the gains on Wall Street in the aftermath of the FOMC meeting where the Fed hiked rates by 75bps and lifted its Fed funds rate projections, while markets found relief from Fed Chair Powell’s press conference as he does not expect 75bp moves to be common and kept the door open for either a 50bps or 75bps hike in July. ASX 200 traded higher but with gains capped as participants reflected on the latest data releases including a mixed jobs report and a further rise in consumer inflation expectations. Nikkei 225 shrugged off mixed trade data as Japan seeks to raise the minimum hourly wage above JPY 1000 and is also looking to implement steps to increase tourist demand next month. Hang Seng and Shanghai Comp. were choppy with COVID-related concerns stoked by an increase in cases in Hong Kong and with Shanghai to conduct weekly community COVID testing across all districts until end-July, while property names lagged after Chinese house prices contracted Y/Y.

Top Asian News

- HKMA raised its base rate by 75bps to 2.00%, as expected, following the earlier Fed rate hike.

- China’s NDRC said it will ensure reasonable economic growth in Q2 to provide a firm foundation for H2 and will expand the scope of use of funds raised by local government special bonds to include high-tech infrastructure for the first time, according to Reuters.

- White House official said US President Biden will keep his mind open regarding relaxing tariffs on Chinese goods, according to Reuters.

- China is to continue expanding high-level opening up, according to MOFCOM’s Shu and is confident foreign trade will be in a reasonable range.

- Hong Kong reports 1085 (prev. 1047) new COVID cases.

European bourses and US futures are hampered following a surprise SNB hike, Euro Stoxx 50 -2.4%; an announcement that exacerbated the modest pressure seen at the European cash open, in-spite of initial modest upside in the regions futures. Stateside, losses are relatively broad-based though the NQ -2.5%, lags its peers modestly given the pronounced upside in yields.

Tesla (TSLA) has raised US prices for all vehicles, according to its website, confirming an earlier report in Electrek; by as much as USD 6k. Samsung Electronics (005930 KS) has temporarily reduced procurement amid inventory pressure, Nikkei reports; has asked component makers and others to delay shipments. Toyota (7203 JT) is to suspend some domestic plant operations from June 17th; remains difficult to look ahead given the shortage of semis. Global production plan for June to be revised to ~750k units.

Top European News

- Villeroy Backs Gradual, Sustained Rate Hikes: ECB Update

- Ferrari Unveils Spending Push to Speed Up Electric Shift

- CEZ Says It Covered Gap in Gazprom Supplies From Other Sources

- Pictet Widens Derivatives Bets to Hedge Against Turmoil

- Air France CEO Says Business Travel Is Returning This Summer

- Putin’s Economic Team Puts on a Brave Face at Shrunken Forum

FX

- Franc soars as SNB strikes with half point hike to prevent further rise in inflation and spread to Swiss goods and services. Bank also removes highly valued tag even as USD/CHF tanks from high 0.9900s to sub-0.9800 and EUR/CHF probes 1.0200 vs 1.0400+.

- Yen rebounds strongly as risk sentiment sours significantly on the eve of BoJ; USD/JPY through 132.50 compared to 134.65+ peak and a Fib retracement (133.42) along the way.

- Dollar revival from post-FOMC lows derailed irrespective of deteriorating market tone and 75 bp rate rise, DXY back down around 105.000 within a 105.500-104.700 range.

- Pound precarious pre-BoE on premise that MPC will stick to steady 25bp policy normalisation steps; Cable choppy either side of 1.2100 and EUR/GBP pivoting 0.8600.

- Kiwi undermined by negative NZ Q1 GDP print and Aussie labours even though jobs data was largely better than expected; NZD/USD under 0.6300 and AUD/USD below 0.7000.

- Brazilian Central Bank raised the Selic rate by 50bps to 13.25%, as expected, through a unanimous decision and it left the door open for further monetary tightening, while it sees another rate increase of equal or lesser magnitude at the next meeting.

- Russian First Deputy PM said Rouble is overvalued and industry would be more comfortable if it fell between 70-80 against the Dollar, while Russian Y/Y inflation will be around 15% in December 2022, according to TASS.

Fixed Income

- Bonds collapse as SNB unexpectedly strikes against inflation with a 50bp rate hike

- Bunds recoil from 145.00+ to sub-142.00 at worst as ECB tightening expectations rise and BTPs reverse gains made on anti-fragmentation efforts between 119.20-116.01 parameters

- Gilts caught in the cross-fire ahead of BoE and down below 112.00 vs 113.12 at one stage even though MPC is seen maintaining 25 bp pace

- US Treasuries revert to bear-flattening after dovish reaction to FOMC overall and await housing data, jobless claims and Philly Fed

Commodities

- Crude benchmarks are hampered in-fitting with the global tone as markets digest the shock 50bp hike from the SNB.

- Currently, WTI and Brent are lower by just shy of USD 1.00/bbl and holding just above yesterday’s troughs.

- US Department of Energy requested to meet with refiners regarding prices no later than June 21st, according to Reuters sources.

- US reportedly fears the EU and UK ban on insuring Russian oil tankers could result in surging crude prices and urges European capitals to seek ways to ease the impact of their ban on insuring Russian oil cargoes, according to FT.

- Ukraine’s energy minister said gas production could fall to 16-17 BCM in 2022 from around 20 BCM in 2021, according to Reuters.

- Russian Deputy PM Novak says Russian can raise oil output in July; Russian oil production is restoring as oil flows are redirected.

- OPEC+ document shows Russian oil output at 9.27mln BPD in May, according to Reuters; OPEC+ was producing 2.695mln BPD beneath its targets in May, document says.

- China will set up a centralised iron ore buyer to counter the dominance of Australia as it hopes bulk buying will secure lower prices, according to FT.

- Spot gold is relatively contained in a sub-USD 10/oz range in-spite of the pronounced price action in the USD and Fixed Income spaces; with any upside for the metal capped again by a cluster of DMAs between USD 1840-46/oz.

Central banks

- Swiss SNB Policy Rate (Q2) -0.25% vs. Exp. -0.75% (Prev. -0.75%); cannot rule out further rate increases. Inflation Forecasts: 2022 2.8% (prev. 2.1%), 2023 1.9% (prev. 0.9%), 2024 1.6% (prev. 0.9%). Exemption Threshold: 28x (prev. 30x). Click here for newsquawk analysis and reaction.

- SNB’s Jordan: tighter monetary policy is aimed at preventing inflation from spreading more broadly to goods and services in Switzerland; CHF is no longer highly valued.

- BoJ fixed rate bond buying operation receives take-up of JPY 733bln.

- ECB’s Visco says price rises are being mostly driven by energy and gas, not being driven by higher demand.

- ECB’s de Guindos says inflation expectations are “quite anchored”.

- NBH hikes one-week deposit rate to 7.25% (prev. 6.75%) at the weekly tender.

- CBR’s Nabiullina says there will not be a ban on USD and foreign currency accounts within Russia; FY economic contraction will be smaller than thought in April, are in discussions with many nations on settlements in national currencies. Do not currently have the technical ability to purchase EUR or USD.

US Event Calendar

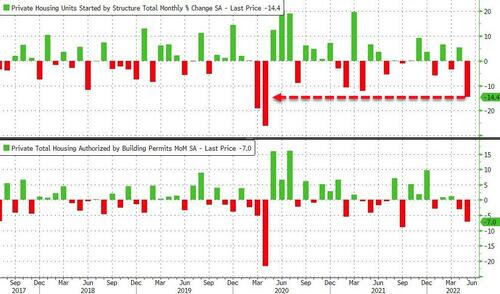

- 08:30: May Building Permits MoM, est. -2.5%, prior -3.2%, revised -3.0%

- 08:30: May Housing Starts MoM, est. -1.8%, prior -0.2%

- 08:30: June Continuing Claims, est. 1.3m, prior 1.31m

- 08:30: May Building Permits, est. 1.78m, prior 1.82m, revised 1.82m

- 08:30: May Housing Starts, est. 1.69m, prior 1.72m

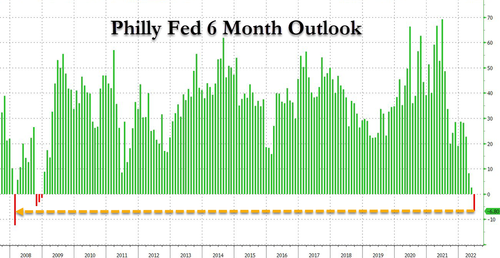

- 08:30: June Philadelphia Fed Business Outl, est. 5.0, prior 2.6

- 08:30: June Initial Jobless Claims, est. 216,000, prior 229,000

DB’s Jim Reid concludes the overnight wrap

There is an assembly for grandparents at school today and as our kids don’t have any anymore we as parents are invited instead. However I turned it down as I can’t face the prospect of going and finding some grandparents younger than me. However given I started in banking in 1995, at least until yesterday I was young enough to have never worked in a 75bps Fed hike world. That changed overnight though as the Fed met their leaked, 48-hour earlier, forward guidance and did their first 75bps move since 1994.

Our economists have reviewed the meeting here but let’s go through the highlights. The one thing we should all learn to ignore is forward guidance. However the key market reaction to the meeting was a big rally in rates, especially at the front end, and a decent rebound in equities, as Powell suggested 50bps in July was still possible just as the market had fully priced 75bps. So forward guidance is dead, long live forward guidance. A key phrase was that “I don’t expect these moves to be common”. This seemed to have a big impact. More later on this but let’s review chronologically.

Before the press conference, the statement and dots were more or less in line with what the market came to price ahead of the meeting. But the Fed is now painting a central scenario that is getting much closer to a hard landing, with unemployment getting revised as high as 4.1% by year-end 2024 – a number I’d expect to rise more as they try to tame inflation. PCE inflation was revised almost a full percentage point higher for this year, to 5.2%, with end-2023 inflation hitting 2.6%.

In the press conference, the Chair again emphasised the Fed’s commitment to bringing down inflation, and admitted the path to doing so whilst engineering a soft landing was getting more and more difficult. Indeed, the statement notably omitted the line: “With appropriate firming in the stance of monetary policy, the Committee expects inflation to return to its 2 percent objective and the labor market to remain strong”, which the Chair explained by asserting that monetary policy alone would not be able to engineer a soft landing. Unemployment looks like it will need to rise in order to slow demand. Powell suggested it would also need help from a supply-side expansion, citing shocks such as the war, runaway oil prices, and supply chains sensitive to China’s Covid lockdowns. Without this, the landing would be hard, it was inferred. A theme he referred to time and again in the presser.

Another key focus of the press conference was the appropriate pace of rate hikes going forward. The Chair explained the Committee broke from its overwhelming communications for a 50bp hike in reaction to the CPI and University of Michigan inflation expectations that surprised to the upside and accelerated further during the blackout period. The path for rate hikes will be dependent on the month-over-month path for inflation, effectively making every inflation data release a ‘live’ event over the near-term. On appropriate hike sizes, markets cheered the fact the Chair said 75bp hikes are not normal and didn’t expect them to become commonplace (as discussed at the top), and that the July hike was in all likelihood between 50bp or 75bp. Later however, the Chair did not explicitly rule out hikes larger than 75bps. So it was forward guidance of sorts but highly uncertain.

This morning, Fed funds futures are pricing in 66bps of tightening in July, versus pricing 74bps at the close Tuesday. One wonders what would have happened if the answer not ruling out hikes larger than 75bps came earlier. Nevertheless, Treasury yields reversed some of the recent selloff, with 2yr yields falling -23.6bps (the most since October 2008) and 10yr yields down -18.9bps (the most since March 2020). Notably, 10yr breakevens were only +2.3bps higher despite the pricing out of tightening. And this morning there’s only been a modest reversal, with 10yr yields up +3.6bps to 3.32%. Risk assets were supported and the S&P 500 climbed +1.46%, almost all of which came during the press conference, with interest rate sensitive sectors leading the way. In line with that, the NASDAQ (+2.50%) and FANG+ (+3.66%) outperformed. It’s worth remembering it was not so long ago that the Chair ruled out completely 75bps for this meeting, so what may look like the modal path for rate policy today could change very quickly.

Whilst the Fed provided the main headlines yesterday, there was also an enormous rally in European sovereign bonds after the ECB Governing Council held an ad hoc meeting where they reiterated their pledge to act against fragmentation risks. Our European economists put out a piece summarising the announcement and implications herebut we’ll run through the takeaways.In their statement, they said that they “will apply flexibility in reinvesting redemptions coming due in the PEPP portfolio”, and that they would also “accelerate the completion of the design of a new anti-fragmentation instrument” for their consideration. So although we didn’t get a formal tool announced, it’s clear that this is on the ECB’s mind, and has helped reassure investors whose concern has grown about Europe’s debt sustainability over recent days. Around the US close, Reuters reported that the planned anti-fragmentation measures were not likely to come with burdensome conditionality, which should support the periphery. Our European economics team noted that with the anti-fragmentation tool coming earlier than expected, the ECB can embark on an even faster rate hike cycle, which prompted our team to add a third +50bp hike this December to their call.

With that in mind, peripheral debt led the moves lower in yields yesterday, with those on 10yr Italian (-36.4bps) and Greek (-45.5bps) debt seeing astonishing declines on the day. Spain (-23.0bps) and Portugal (-25.6bps) followed with what were still outsized moves by normal standards, whilst bunds saw one of the more subdued performances as yields “only” came down by -11.1bps. Indeed, the decline in the spread of 10yr Italian yields over bunds was the largest in a single day in over two years. That performance was mirrored on the equity side too, with Italy’s FTSE MIB (+2.87%) outperforming the broader STOXX 600 (+1.42%) as it snapped a run of 6 consecutive daily declines.

The euro itself initially strengthened in reaction to that ECB meeting happening, before falling around the statement, and then re-strengthened to +0.36% versus the dollar following the FOMC. Separately Bitcoin fell -1.48% in its 9th consecutive decline, having been nearly -9% lower earlier in the day and hitting an intraday low of $20,081, before rebounding along with risk after the FOMC to close at $21,640, and this morning it’s advanced further to reach $22,244.

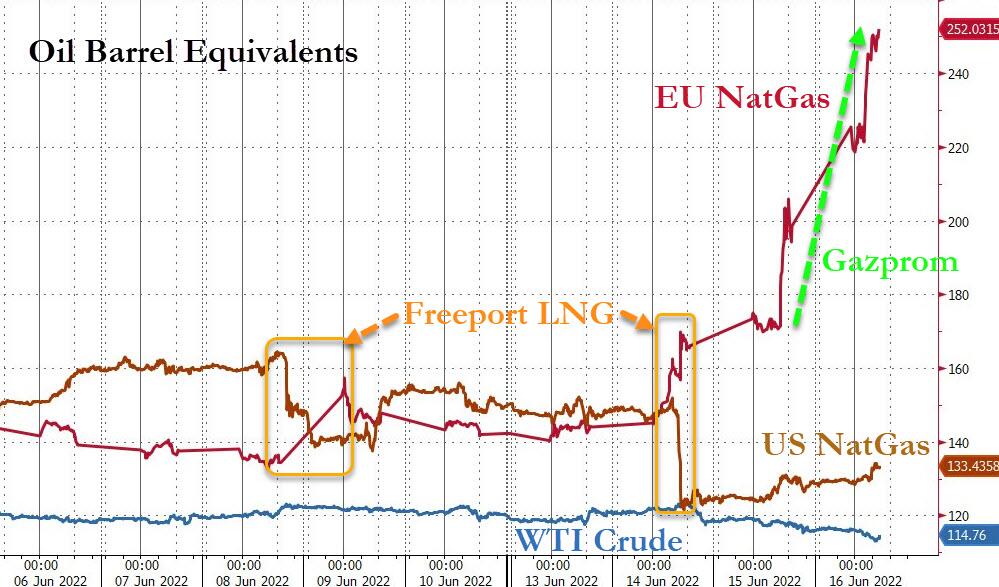

Another significant story in Europe came on the energy side yesterday, with natural gas futures up by +24.00% (on top of the 16.35% rise on Tuesday) after Russia further squeezed gas supplies to Europe via the Nord Stream pipeline, with a cap in supplies to 67m cubic metres per day. That leaves futures at €120.33/MWh, which is the most they’ve been since late-March and represents a further piece of unwelcome news for policymakers trying to deal with inflation.

Those moves higher in equities have been echoed overnight in Asian markets, with investors focusing on Chair Powell’s comment that he did not “expect moves of this size to be common.” In terms of the moves, the Nikkei (+1.41%) has advanced thanks to a rally in auto and tech stocks whilst the Kospi (+1.46%), Shanghai Composite (+0.25%) and CSI (+0.32%) have also moved higher. The only exception is the Hang Seng (-0.40%), which has reversed its initial gains following the open. DM equity futures are pointing higher as well, although similarly we’ve seen a decline over the last couple of hours whereby S&P futures have gone from being up +1.05% to just +0.32% at time of writing. Oil prices have rebounded this morning too, with Brent futures +0.49% up at $119.09/bbl, after falling to its lowest closing level in nearly two weeks.

Looking forward, central bankers will stay in the spotlight today since we’ll get the Bank of England’s latest decision at midday in London. Like the Fed and the ECB, they’re facing similar inflationary pressures with UK CPI rising to a multi-decade high of +9.0% in April, and our economist expects they’ll continue their campaign of rate hikes with a further 25bp move, which would take Bank Rate up to a post-GFC high of 1.25%. Market pricing is between a 25bp move and a larger hike, with overnight index swaps placing a 43% chance that we’ll get a 50bp move instead. Indeed, last time 3 of the 9 members on the committee wanted 50bps rather than 25bps, so it’ll be interesting to see what the vote breakdown looks like.

On the data side, yesterday’s main release came from the US retail sales for May, where the headline number unexpectedly contracted -0.3% (vs. +0.1% expected), and the previous month’s expansion was also revised down two-tenths to +0.7%. That’s the first monthly contraction so far this year as well. Elsewhere in the US, the NAHB’s housing market index for June fell to a 2-year low of 67 as expected. Otherwise, the Euro Area saw industrial production grow by +0.4% in April (vs. +0.5% expected).

To the day ahead now, and one of the highlights will be the aforementioned BoE decision. In addition, there’s an array of ECB speakers including Vice President de Guindos, along with the ECB’s Visco, Villeroy, Panetta, Vasle, Knot, Centeno, De Cos and Makhlouf. Data releases include US housing starts and building permits for May, the weekly initial jobless claims, and the Philadelphia Fed’s business outlook survey for June.

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 20.02 PTS OR 0.61% //Hang Sang CLOSED DOWN 462.78 PTS OR 2.13% /The Nikkei closed UP 105.04 OR 0.40% //Australia’s all ordinaires CLOSED DOWN 0.03% /Chinese yuan (ONSHORE) closed DOWN 6.7149 /Oil DOWN TO 113.77 dollars per barrel for WTI and DOWN TO 116.23 for Brent. Stocks in Europe OPENED ALL RED // ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.7149 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7204: /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER/

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

Today bond yields in Japan broke wide open with its yield rising from .25 to .347 as the dam broke

This should cause massive losses on bond yields by insurers and investors

Reynolds/Bloomberg

Bond Meltdown’s Next Driver Is BOJ Policy Implosion

THURSDAY, JUN 16, 2022 – 01:25 PM

By Garfield Reynolds, Bloomberg Markets Live Commentator and Reporter

The pace of this week’s Treasuries rout – and post-FOMC relief – has focused most eyes squarely on US markets, but the real action going forward is just as likely to be in Tokyo. The Bank of Japan’s massive debt purchases to cap yields may have already passed their use-by date, and that threatens to unleash fresh storms on global bond markets that are about as stressed as they have ever been.

While the Fed’s 75-basis-point hike came with mild-enough forward guidance to soothe panicked markets, the BOJ still faces pressure from a widening policy gap to at least acknowledge it’s time to tweak its own settings when it concludes its own meeting on Friday.

BOJ Governor Haruhiko Kuroda is nothing if not determined, and he has been sticking to his line that the recent pickup in Japanese inflation will be transitory — a word that has fallen out of favor with his peers — meaning that he considers it premature to adjust the world’s loosest policy.

The central bank is doubling and tripling down on buying up ever-greater chunks of what is left of the Japanese bond market to cap 10-year yields at 0.25% and maintain curve control. This week has seen cries that this can’t go on for much longer reach a crescendo.

The yen tumbled through 135 per dollar this week to a 24-year low, which adds to the stickiness for inflation as well as taking the currency down so far that the real-world impacts counteract much of the benefits of easier policy, including by crippling consumer confidence.