by harveyorgan · in Uncategorized · Leave a comment·Edit

2022 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1827.85 DOWN $8.60

SILVER: $21.07 DOWN 41 CENTS

ACCESS MARKET: GOLD $1822.50

SILVER: $20.96

Bitcoin morning price: $20,667 DOWN 20

Bitcoin: afternoon price: $20,855 UP 168.

Platinum price: closing DOWN $20.15 to $911.50

Palladium price; closing DOWN $25.90 at $1841.55

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE: 2/12

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,834.300000000 USD

INTENT DATE: 06/22/2022 DELIVERY DATE: 06/24/2022

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 4

624 H BOFA SECURITIES 4

657 C MORGAN STANLEY 11

661 C JP MORGAN 1 2

905 C ADM 2

TOTAL: 12 12

MONTH TO DATE: 23,808

no. of contracts issued by JPMorgan:

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 12 NOTICE(S) FOR 1200 Oz//0.0373 TONNES)

total notices so far: 23,808 contracts for 2,380,800 oz (74.0528 tonnes)

SILVER NOTICES:

9 NOTICE(S) FILED 45,000 OZ/

total number of notices filed so far this month 1818 : for 9,090,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD DOWN $8.60

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//

INVENTORY RESTS AT 1071.77 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 41 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV://BIG CHANGES IN SILVER INVENTORY AT THE SLV//AWITHDRAWAL OF 2.029 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 545.137 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A VERY STRONG SIZED 2754 CONTRACTS TO 142,602 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR SMALL $0.14 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.14) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 6 CONTRACTS OR 30,000 OZ//NEW STANDING: 9,140,000 / // V) STRONG SIZED COMEX OI GAIN/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -549

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 16 days, total 12,117, contracts: 60,585 million oz OR 3.788 MILLION OZ PER DAY. (757 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 60.585 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 60.585 MILLION OZ

RESULT: WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2754 WITH OUR $0.14 LOSS IN SILVER PRICING AT THE COMEX// WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 475 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 55,000 QUEUE JUMP //NEW STANDING: 9,195,000 OZ // .. WE HAD A VERY STRONG SIZED LOSS OF 2270 OI CONTRACTS ON THE TWO EXCHANGES FOR 8.65 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 9 NOTICES FILED TODAY FOR 45,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1008 CONTRACTS TO 499,268 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -156 CONTRACTS.

.

THE SMALL LOSS IN COMEX OI CAME DESPITE OUR SMALL RISE IN PRICE OF $0.15//COMEX GOLD TRADING/WEDNESDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 3900 OZ E.F.P JUMP TO LONDON //NEW STANDING: 74.911TONNES

YET ALL OF..THIS HAPPENED WITH OUR GAIN IN PRICE OF $0.15 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 2585 OI CONTRACTS 8.040 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3593 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 499,269

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2585, WITH 1008 CONTRACTS DECREASED AT THE COMEX AND 3593 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2585 CONTRACTS OR 8.040 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3593) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (852,): TOTAL GAIN IN THE TWO EXCHANGES 2585 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P JUMP OF 3900 OZ//NEW STANDING: 74.9611 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OI LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

57,986 CONTRACTS OR 5,798600 OZ OR 180.36 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 3624 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES: 169.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 180.36/3550 x 100% TONNES 5.08% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 180.36 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A VERY STRONG SIZED 2754 CONTRACT OI TO 142,602 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 475 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 475 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1768 CONTRACTS AND ADD TO THE 475 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED LOSS OF 2270 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 11.35 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.14 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)THURSDAY MORNING// WEDNESDAY NIGHT

SHANGHAI CLOSED UP 52.95 PTS OR 1.62% //Hang Sang CLOSED UP 265.53 PTS OR 1.36% /The Nikkei closed UP 21.70 OR 0.08% //Australia’s all ordinaires CLOSED UP 0.14% /Chinese yuan (ONSHORE) closed UP 6.7071 /Oil UP TO 105.78 dollars per barrel for WTI and UP TO 111.46 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT GERMAN DAX // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7071 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7068: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1008 CONTRACTS TO 499,208 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED DESPITE OUR GAIN OF $0.15 IN GOLD PRICING WEDNESDAY’S COMEX TRADING. WE ALSO HAD A FAIR SIZED EFP (3593 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3593 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :3593 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3593 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2585 CONTRACTS IN THAT 3593 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI LOSS OF 852 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF GOLD $0.15.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.793),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.793 TONNES

THE BANKERS WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT ROSE $0.15) AND WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A FAIR SIZED GAIN OF 2741 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.793 TONNES)…

WE HAD 156 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 2585 CONTRACTS OR 258500 OZ OR 8.040 TONNES

Estimated gold volume 156,332/// poor/

final gold volumes/yesterday 160,402 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 23

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 2,739.949 oz Malca JPMorgan 78 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 12 notice(s)1200 OZ 0.0373 TONNES |

| No of oz to be served (notices) | 238 contracts 23,800 oz 0.7402 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,808 notices 2,380,800 OZ 74.0528 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

total dealer deposit 0

No dealer withdrawals

0 customer deposits

total deposits: nil oz

2 customer withdrawals:

i) Out of Malca: 2507.778 oz (78 kilobars)

ii) Out of JPMorgan: 200.02 oz

total withdrawal: 2739.949 oz

ADJUSTMENTS:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 250 contracts having lost 109 contracts

We had 55 notices filed on WEDNESDAY so we LOST 54 contracts or an additional 5400 oz will NOT stand for gold in this very active month of June

July has a LOSS OF 149 OI to stand at 1452

August has a LOSS of 1821 contracts DOWN to 411,811 contracts

We had 12 notice(s) filed today for NIL 120oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1 notices were issued from their client or customer account. The total of all issuance by all participants equate to 55 contract(s) of which 12 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,808) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 250 CONTRACTS ) minus the number of notices served upon today 12 x 100 oz per contract equals 2,404,600 OZ OR 74.793 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,808) x 100 oz+ (250) OI for the front month minus the number of notices served upon today (12} x 100 oz} which equals 2,404,600 oz standing OR 74.793 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74.793 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,504,694.715 OZ

TOTAL ELIGIBLE GOLD: 16,228,629.994 OZ

TOTAL OF ALL REGISTERED GOLD: 17,276,064.721OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,921,555.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 23

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,410,479.789 oz Brinks CNT Manfra Delaware JPMorgan |

| Deposits to the Dealer Inventory | nilOZ |

| Deposits to the Customer Inventory | 200,607,010 oz Delaware HSBC |

| No of oz served today (contracts) | 9CONTRACT(S)45,000 OZ) |

| No of oz to be served (notices) | 21 contracts (105,000 oz) |

| Total monthly oz silver served (contracts) | 1818 contracts 9,090,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 2 deposit into the customer account

i) Into HSBC 600.635.310 oz

ii) Into Delaware: 99.971.700 oz

total deposit: 700,607.010 oz

JPMorgan has a total silver weight: 169,099 million oz/336/533 million =50.22% of comex

Comex withdrawals: 5

CNT 16,182.610 oz

Delaware 2000.589 oz

JPMorgan 559,007.640 oz

Manfra 60,615.440 oz

total withdrawal 1,410.479.789 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.116 MILLION OZ

TOTAL REG + ELIG. 336/553 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 30 HAVING GAINED 5 CONTRACTS.

WE HAD 6 NOTICES FILED ON WEDNESDAY SO WE GAINED 11 CONTRACTS OR AN ADDITIONAL 55,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 9866 CONTRACTS DOWN TO 35,556 CONTRACTS.

AUGUST GAINED 87 CONTRACTS TO STAND AT 1103

SEPTEMBER HAD A GAIN OF 6847 CONTRACTS UP TO 88,192 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 6 for 30,000 oz

Comex volumes:94,325// est. volume today// STRONG

Comex volume: confirmed yesterday: 80,623 contracts ( good )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1818 x 5,000 oz = 9,090,000 oz

to which we add the difference between the open interest for the front month of JUNE(30) and the number of notices served upon today 9 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1818 (notices served so far) x 5000 oz + OI for front month of JUNE (30) – number of notices served upon today (9) x 5000 oz of silver standing for the JUNE contract month equates 9,195,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1073.80 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545/137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 545.137 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

The Inflation Solutions Are Even Worse Than The Problem

THURSDAY, JUN 23, 2022 – 08:45 AM

Authored by Michael Maharrey via SchiffGold.com,

As Americans labor under the burden of inflation, the Biden administration keeps telling us the economy is just fine. White House press secretary Karine Jean-Pierre recently said we are “transitioning” to “steady and stable growth.” As a result, she claims the American people are in a place where they can “take on inflation.”

Americans aren’t buying it. In fact, they’re buying less of everything as rising prices squeeze their wallets. Consumer confidence has plunged to historically low levels. But as bad as things are, the worst could still be yet to come because the proposed solutions are worse than the problem.

In the first place, it’s important to understand that the impacts of inflation are far worse than the official numbers indicate. The government uses a cooked CPI formula that understates rising prices. Back in 1998, the government significantly revised the CPI metrics. Even the Bureau of Labor Statistics (BLS) admitted the changes were “sweeping.” Measured using the old formula, CPI would be running closer to 17%.

For instance, we’ve seen a staggering increase in housing prices over the last year or so. The average price of an existing home topped $400,000 for the first time ever in May. Rent has also gone through the roof. But the CPI doesn’t capture the full impact of rising home prices. The government uses a made-up number known as “owner’s equivalent rent” to calculate housing prices. This number understates the cost of housing and it makes up about 1/3 of the CPI calculation. Actual home prices are up about 20%. Rent is up over 15%. The CPI calculation for shelter is only up about 5.5%. It simply doesn’t reflect reality.

No matter how the talking heads spin it, we know the economy is a mess. We live it every day. More distressing, it’s probably going to get worse because the plans to tackle inflation are more of what caused it in the first place.

Solutions Worse than the Problem

So, what is the plan to tame inflation?

Senate Finance Committee Chair Ron Wyden (D) plans to introduce legislation to impose a surtax on “excessive” oil company profits. According to one popular narrative coming out of the Democratic Party, oil company price gouging is causing inflation. But this doesn’t stand up to scrutiny.

And while punishing “greedy” oil companies certainly has populist appeal, it won’t do anything to solve the problem. You could confiscate all of the oil company profits and hand them out to the American people and they would hardly notice the difference.

Furthermore, if you take the profit out of drilling for oil, nobody will drill for oil. It would ultimately create an even bigger supply problem than we have right now.

The inflation-fighting plan announced by the White House mostly involves spending more money. In a Wall Street Journal op-ed, President Biden claimed, “We can lower the cost of child and elder care to help parents get back to work.” Lowering the cost of childcare is code for government-subsidized childcare. He also alluded to the stalled “Build Back Better” bill, which is basically a $2.2 trillion spending plan. Biden wrote, “We can also reduce the cost of everyday goods by fixing broken supply chains, improving infrastructure…”

But government spending isn’t the solution. It’s the problem. The White House press secretary lauded the “American Rescue Plan” as the first step toward recovery. But in reality, Americans need rescuing from that rescue plan.

In effect, governments shut down the economy and handed out money for people to spend. Supplies were squeezed because nobody was producing goods and services. But demand never dropped because everybody had their pocket stuffed with stimulus money. In effect, the government flooded the economy with money even as it starved it of goods. Of course, prices went through the roof. This was entirely predictable.

Now the Biden administration wants spend more – the exact policy that got us in this inflation mess to begin with.

The Federal Reserve appears equally feckless. It took a more aggressive stance during the last FOMC meeting, raising interest rates by 75 basis points. But it remains so far behind the inflation curve that it can’t even see it.

To truly tame inflation, real interest rates need to rise above the level of inflation. Paul Volker raised rates to 20% in order to slay the inflation dragon. The current 1.5% rate is spitting into the wind in the face of an 8.6% CPI (which is understating inflation.)

Given all of the debt in the economy, the Fed can’t possibly raise rates to that level without popping the bubbles and toppling the house of cards economy. The Fed is at a crossroads – either continue the inflation fight and plunge us into a deep recession or surrender to inflation and destroy the dollar.

Neither scenario is particularly desirable. So brace yourself because things will likely get worse before they get better.

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

-END-

END

3. Chris Powell of GATA provides to us very important physical commentaries

This is interesting: Manly writes that Russia is mobilizing its gold in support of war, while the EU appears to be trying to prevent Russia from doing just that

(Ronan Manly)

Ronan Manly: Russia mobilizes its gold for war, EU moves to block it

Submitted by admin on Tue, 2022-06-21 23:10Section: Daily Dispatches

11:10p ET Tuesday, June 21, 2022

Dear Friend of GATA and Gold:

Bullion Star’s Ronan Manly writes tonight that Russia appears to be preparing mechanisms for mobilizing its gold in support of war, while the European Union appears to be moving to prevent Russia from doing just that.

Manly’s analysis is headlined “Russia Lines Up Its State Fund of Precious Metals for Military Mobilization” and it’s posted at Bullion Star here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4.OTHER GOLD/SILVER COMMENTARIES

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings THURSDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.7071

OFFSHORE YUAN: 6.7068

HANG SANG CLOSED UP 265.53 PTS OR 1.26%

2. Nikkei closed UP 21.70% OR 0.08%

3. Europe stocks ALL CLOSED ALL GREEN EXCEPT GERMAN DAX

USA dollar INDEX UP TO 104.34/Euro FALLS TO 1.0497

3b Japan 10 YR bond yield: FALLS TO. +.226/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.138/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.478%/Italian 10 Yr bond yield FALLS to 3.52% /SPAIN 10 YR BOND YIELD FALLS TO 2.56%…

3i Greek 10 year bond yield FALLS TO 3.75//

3j Gold at $1825.75 silver at: 21.13 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 roubles/dollar; ROUBLE AT 53.18

3m oil into the 105 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.14DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9663– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.0144well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.132 DOWN 2 BASIS PTS

USA 30 YR BOND YIELD: 3.225 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.36

Futures Rebound As Hopes Of Imminent Recession Spark “Bad News Is Good News” Reversal

THURSDAY, JUN 23, 2022 – 07:50 AM

In a world where bad news is good news, and where the looming recession means an end to rate hikes and a start to easing, it didn’t take algos long to bid stocks up as treasury yields tumbled after comments by Jerome Powell and dismal PMI data in Europe justified fears that a global downturn is now just a matter of when, not if. After initially sliding more than 1% late on Wednesday, futures rebounded and recovered all losses and were last trading near Wednesday’s session highs, up 0.7% or 27 point to 3,790, while Nasdaq futs were up 0.9% at 11,375 as of 715am ET.

10Y yield initially dumped below 3.10% – near a two week low, after trading at 3.50% one week ago – before bouncing modestly, while the Dollar pushed higher as the euro tumbled after after a series of very poor European PMI prints confirmed that Europe’s runaway inflation is pushing the continent into a stagflationary recession, which in turn sent the yield on German 10-year bonds slumping as much as 21 basis points, poised for the biggest two-day decline since November 2011. US 10-year rates traded near a two-week low.

In premarket trading, US-listed Chinese stocks climbed as bullish sentiment around the group continues to grow amid calls from strategists and fund managers that Beijing’s regulatory crackdowns are easing. JPMorgan Asset Management became the latest to voice its support for Chinese tech shares, saying “the worst is over” when it comes to regulatory crackdowns. Here are some other notable premarket movers:

- KB Home (KBH US) shares climb 4.7% in premarket trading after the homebuilder reported earnings per share and revenue for the second quarter that beat the average analyst estimate.

- US-listed shares of Chinese electric-vehicle makers rallied in premarket trading after Chinese state television reported that the government may extend tax exemptions on electric-car purchases.

- Li Auto (LI US) +6%, Xpeng (XPEV US) +5.3% and Nio (NIO US) +2.6% in premarket trading.

- Cryptocurrency-exposed stocks rebounded in premarket trading as Bitcoin recovered to remain over the closely watched $20,000 level.

- Coinbase (COIN US) +3%, Riot Blockchain (RIOT US) +3.7%, Marathon Digital (MARA US) +4.4%, Block (SQ US) +0.7%.

- EBay (EBAY US) shares decline 2.1% in premarket trading as Morgan Stanley assumed coverage of the stock with a recommendation of underweight and a price target of $36, the lowest on Wall Street.

- Energy companies slide in US premarket trading as oil eases anew amid concerns of slowing global growth.

- Exxon Mobil (XOM US) -1%, Chevron (CVX US) -1.1%, Imperial Petroleum (IMPP US) -3.1%, Camber Energy (CEI US) -2.4%.

- Westinghouse Air Brake (WAB US) and AGCO (AGCO US) shares may be in focus as Morgan Stanley cuts them to equal-weight and resumes coverage of Cummins (CMI US) at equal-weight in a note trimming its PTs across most of its machinery and construction coverage.

On Wednesday, in the first day of his Congressional testimony, Powell accepted that steep rate increases could trigger a US recession, and said the task of engineering a soft economic landing is “very challenging” (day two follows). Policy makers are taking drastic steps to cool inflation at a four-decade high and the Fed chair repeated his resolve to get consumer price growth back down to the 2% target.

“Market optimism couldn’t survive Jerome Powell’s testimony yesterday, but most of the negative pricing is certainly done by now,” said Ipek Ozkardeskaya, a senior analyst at Swissquote.

“The reaffirmation of the Fed’s commitment to bringing inflation down and that recession is a risk are adding to growth worries, which is the dominant fear again,” said Esty Dwek, chief investment officer at Flowbank.

Traders are now debating how far the Fed will stretch its rate cycle in the face of an economic downturn. Money markets indicate diminished odds the central bank will raise rates beyond year-end, and rising odds of a rate cut from May 2023. The Federal Reserve “is well served by keeping some hawkishness there,” Steven Major, global head of fixed income research at HSBC Holdings Plc, said in an interview with Bloomberg Television. “Because if they appear that they’ve reached the peak, then financial conditions will loosen and the policy won’t work. So they need a couple more months of this.”

European equities traded flat having erased earlier losses of more than 1%. Real estate, autos and banks are the weakest Stoxx 600 sectors; travel is a rare bright spot. European energy stocks slipped for a second session with crude prices under pressure as concerns over a global economic slowdown intensified. The Stoxx 600 Energy index falls as much as 1.9%; TotalEnergies and Shell the biggest drags on the index on Thursday, with wind- turbine firm Vestas and Italy’s Eni also slipping. Here are some of the biggest European movers today:

- Aroundtown stock drops as much as 11% after being cut to underweight from neutral at JPMorgan, which also lowered its PT to EU3.6 from EU6 due to excessive downside exposure for the German landlord.

- Vantage Towers falls as much as 7.6% after Morgan Stanley cut the stock to equal-weight from overweight, saying the shares have outperformed despite challenges in its outlook.

- Saipem trims losses after declining as much as 21% following the announcement of a EU2b capital increase on Wednesday; Italy’s Consob warns of volatility in the stock when the rights issue starts.

- Rheinmetall falls as much as 6.3% after HSBC downgraded the German automotive and defense group to hold from buy due to it being temporarily held back by its automotive division

- Naked Wines slumps as much as 40% after the online wine merchant forecast fiscal 2023 sales of £345m-£375m. The midpoint of the guidance is ~10% lower than what Jefferies analysts had been expecting.

- Intertek falls as much as 4.1% after Deutsche Bank cuts the stock to sell, saying many structural trends that underpinned growth for testing and inspection companies are reversing. Eurofins gains as much as 4.2% on an upgrade to hold.

- Atos gains as much as 11% after a report that Thales has the support of the French state in its effort to buy French tech company’s cybersecurity business.

- Ubisoft rises as much as 2.5% before paring gains, as Deutsche Bank initiates coverage with a buy rating, saying there’s “good scope” to beat revenue and margins expectations for fiscal 2024 and 2025.

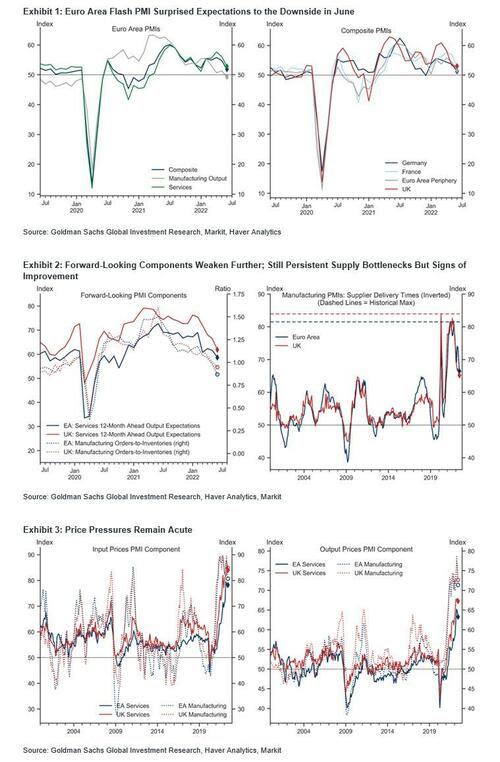

As noted above, the latest let of European PMIs were dismal, dropping across the board and all (except the UK) missing expectations:

- Euro Area Composite PMI (June, Flash): 51.9, consensus 54.0, last 54.8.

- Euro Area Manufacturing PMI (June, Flash): 52.0, consensus 53.8, last 54.6.

- Euro Area Services PMI (June, Flash): 52.8, consensus 55.5, last 56.1.

- Germany Composite PMI (June, Flash): 51.3, consensus 53.0, last 53.7.

- France Composite PMI (June, Flash): 52.8, consensus 55.9, last 57.0.

- UK Composite PMI (June, Flash): 53.1, consensus 52.4, last 53.1.

Earlier in the session, Asian stocks edged higher, with an improving outlook in China offering support even as the prospect of a global downturn weighed on some export-reliant markets. The MSCI Asia Pacific Index was up 0.2% with China’s internet giants and automakers contributing to the gains. South Korea and Taiwan, the two tech-heavy markets that have seen foreigners flee amid rising global rates, fell more than 1%. Traders digested Federal Reserve Chair Jerome Powell’s Wednesday comments that steep rate increases could trigger a US recession. China stocks were the region’s best performers, extending a recent trend, as President Xi Jinping pledged to meet economic targets for the year.

Hong Kong stocks gained after a report that the city’s incoming leader is working on a strategy to reopen its borders. Japanese stocks were little changed. “We’re sort of in a bottoming out phase here in Asia, where China is going to eventually support us again,” Robeco Asia-Pacific Chief Investment Officer Arnout van Rijn said in a Bloomberg TV interview. “The rest of Asia, with its better macroeconomic policies and lower interest rates, should at least outperform a weaker global market.” The Fed’s recent rate hike and comments have been especially hard on growth shares, with a gauge of Asia’s tech stocks falling to its lowest level since September 2020. China’s stocks have outperformed the broader region amid hopes for continued fiscal and monetary support.

Japanese equities struggled for direction as investors worried over Federal Reserve Chair Jerome Powell’s comments on the risks of a recession. The Topix closed down les than 0.1% at 1,851.74, while the Nikkei advanced 0.1% to 26,171.25. Out of 2,170 shares in the index, 1,295 rose and 775 fell, while 100 were unchanged. “We’re in a very difficult phase,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management. “The market is still focused on what will happen to prices in the US and whether the economy can cope with a larger interest rate hike.”

Indian shares rose to mark their third day of gains in four after a retreat in crude oil prices eased concerns about vehicle demand in Asia’s third-biggest economy. Maruti Suzuki India Ltd. and Mahindra & Mahindra Ltd. were among the top gainers on the S&P BSE Sensex, which climbed 0.9% to close at 52,265.72 in Mumbai. The NSE Nifty 50 Index rose by an equal measure. Both indexes have risen for three of four sessions this week. All but two of the 19 sub-sector gauges compiled by BSE Ltd. advanced, led by auto companies. Regional peers were mixed after Federal Reserve Chair Jerome Powell acknowledged the risk of a recession. West Texas Intermediate sank toward $104 a barrel after closing at a six-week low on Wednesday. Tata Consultancy contributed the most to the Sensex’s gains, increasing 2.7%. Out of 30 shares in the index, 27 rose and 3 fell.

In rates, Treasury futures traded above Wednesday’s highs after tracking steeper gains for bunds sparked by weaker-than-expected euro-zone growth data, before fading much of the move. US yields richer by 3bp-5bp across the curve led by belly, richening the 2s5s10s fly by 3.5bp on the day; 10-year richer by ~3bp at 3.125% vs 16bp slide for German 10-year, widening spread ot ~165bp. Elevated recession risk put German 10-year yields on track for their biggest decline in more than three months. US auctions include $18b 5-year TIPS reopening at 1pm ET; ahead of the sale 5-year breakeven inflation is ~2.75%, near lowest level since January. Focal points of US session include Fed Chair Powell’s second day of congressional testimony and manufacturing survey data. Bunds futures rally, trading over a 300 tick range in high volumes before stalling close to 148.00. Yield curves bull steepen aggressively. German 2y yields crater over 20bps near 0.82%, trading 10bps richer to gilts and ~15bps richer to USTs. Peripheral spreads widen with short-end Portugal underperforming.

In FX, Bloomberg dollar spot index rose 0.3% as the EUR tumbled on poor PMI data. The yen extended its rise as comments from an ex-policy official spurred bets that the Bank of Japan may intervene to halt the currency’s slide. Japan’s currency gained as much as 0.8% after Takehiko Nakao, the former head of foreign exchange policy at the finance ministry, said the possibility of the authorities intervening directly in foreign-exchange markets can’t be ruled out. Sterling eased against a broadly stronger dollar as a slide in global share prices prompted investors to sell riskier assets. Markets await UK PMI data, which is expected to show a drop in manufacturing and services sectors, adding to signs of a slowing economy.

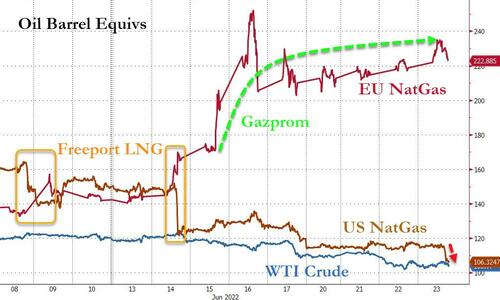

In commodities, oil dipped initially in early trading before paring the entire loss, Brent crude back above $111 a barrel. Most base metals are trade lower: LME copper drops ~2%, LME tin underperforms declining over 8%. Spot gold drifts lower near $1,830/oz.

Bitcoin is firmer overall but continues to pivot the USD 20k mark and has struggled to gain any real traction during brief forays either side.

Looking to the day ahead now, and the main data highlight will be the rest of the flash PMIs for June, along with the US weekly initial jobless claims, the Q1 current account balance, and the Kansas City Fed’s manufacturing activity for June. From central banks, Fed Chair Powell will be speaking before the House Financial Services Committee, the ECB will publish their Economic Bulletin, and we’ll hear from the ECB’s Nagel and Villeroy. Finally, EU leaders will be meeting in Brussels.

Market Snapshot

- S&P 500 futures down 0.2% to 3,755.75

- STOXX Europe 600 down 1.2% to 401.04

- MXAP up 0.1% to 156.60

- MXAPJ up 0.2% to 519.03

- Nikkei little changed at 26,171.25

- Topix little changed at 1,851.74

- Hang Seng Index up 1.3% to 21,273.87

- Shanghai Composite up 1.6% to 3,320.15

- Sensex up 0.7% to 52,208.76

- Australia S&P/ASX 200 up 0.3% to 6,528.45

- Kospi down 1.2% to 2,314.32

- German 10Y yield little changed at 1.47%

- Euro down 0.6% to $1.0503

- Brent Futures down 1.7% to $109.80/bbl

- Gold spot down 0.2% to $1,834.49

- U.S. Dollar Index up 0.46% to 104.67

Top Overnight News from Bloomberg

- Germany elevated the risk level in its national gas emergency plan to the second-highest “alarm” phase, following steep cuts in supplies from Russia.

- India’s central bank appears to have ramped up intervention in the forwards market to slow the rupee’s decline and preserve its hard-earned reserves.

- Russia faces yet another bond payment test this week, with just days remaining before it potentially slides into its first foreign default in a century.

- India’s central bank appears to have ramped up intervention in the forwards market to slow the rupee’s decline and preserve its hard-earned reserves.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive after risk appetite slightly improved from the uninspiring lead from Wall St where stocks were choppy as tailwinds from lower oil prices and softer yields were offset by recession fears. ASX 200 was led higher by strength in real estate and consumer stocks, while Manufacturing PMI data remained in a firm expansion. Nikkei 225 swung between gains and losses with the index hampered by currency inflows. Hang Seng and Shanghai Comp. were kept afloat with auto manufacturers lifted after China’s cabinet pledged to boost the auto industry, while markets also shrugged off initial cautiousness brought on by COVID concerns after Shenzhen required PCR tests for anyone entering a public venue.

Top Asian News

- China’s Shenzhen is to require PCR tests for anyone entering a public venue, according to Bloomberg.

- US State Department warned about reconsidering travel to China due to COVID lockdown risks, according to Reuters.

- Former Japanese FX chief Nakao said continuing with YCC has many negative effects and that it is clear monetary policy is playing a role in the weak JPY, according to Bloomberg.

European bourses are pressured overall, but well off lows going into the US session, Euro Stoxx 50 -0.2%; pressure was seen post-PMIs which missed expectations and featured pessimistic internal commentary. The sectoral breakdown is mixed as such while individual movers are affected by numerous broker moves. Stateside, futures are now firmer on the session, ES +0.4%, having shrugged off the French/German/EZ flash-PMI induced risk move ahead of Powell’s second day of testimony.

Top European News

- Majority of economists expect the ECB to hike the deposit rate by 25bps in July and 50bps in September, while the Deposit Rate is seen at 0.75% at year-end (prev. 0.25%) and there is a median 34% (prev. 30%) chance of a recession in 12 months, according to a Reuters poll.

- Bulgarian Turmoil Deepens as Premier Loses Confidence Vote

- Norway Steps Up Action With First Half-Point Hike Since 2002

- Hedge Fund Trader Shah Struck Cum-Ex Trades With DekaBank

- UK June Flash Services PMI 53.4; Est 52.9

FX

- Poor preliminary Eurozone PMIs pull rug from under Euro; EUR/USD sub-1.0500 at worst, EUR/JPY under 142.00 vs almost 144.00 peak and EUR/GBP probes 0.8600 from circa 0.8641.

- Buck benefits indirectly alongside Yen as risk aversion intensifies on heightened recession anxiety; DXY towards top end of 104.780-050 range, USD/JPY vice-versa between 136.25-135.12 parameters.

- Pound pares some declines with assistance of solid UK services PMI, Cable keeps tabs on 1.2200 handle.

- Franc makes way for rebounding Dollar, Loonie, Aussie and Kiwi bear brunt of ongoing losses in underlying commodities; USD/CHF back above 0.9650 from sub-0.9600, USD/CAD hovering under 1.3000, AUD/USD capped into 0.6900 and NZD/USD around 0.6250.

- Norwegian Crown underpinned by bigger than expected 50bp Norges Bank hike and loftier rate path with caveats, EUR/NOK pivots 10.4800 vs near 10.5300 peak and 10.4400 trough.

Central Banks

- Norges Bank Key Policy Rate (June-MPR): 1.25% vs. Exp. 1.00% (Prev. 0.75%); points to a 25bps hike in August (interim meeting). Click here for full details, reaction and newsquawk analysis.

- Norges Bank Governor Bache says cannot rule out increasing rates by more than 25bps in future meetings.

- NBH keeps its one-week deposit rate unchanged at 7.25%

Fixed Income

- Bunds and OATs front-run latest broad and big bond bounce as PMI miss consensus by some distance.

- Gilts and US Treasuries tag along with a lag post-solid UK services PMI and pre-US jobless claims, PMIs and Fed Chair Powell part 2.

- Bunds reach 147.89 from 144.81 low, Gilts 113.36 vs 111.93 and 10 year T-note 117-16 compared to 116-25+.

- Italy raises EUR 9.45bln with the BTP Italia bond, via Reuters.

Commodities

- Crude complex remains pressured with specific newsflow limited and focused on known themes, WTI/Brent -0.5% having benefitted from the recent pick up in broader sentiment; note, the EIA release has been delayed.

- Private US Energy Inventory Data (bbls): Crude +5.7mln (exp. -0.6mln), Gasoline +1.2mln (exp. -0.5mln), Distillates -1.7mln (exp. +0.3mln), Cushing -0.4mln.

- US EIA said product releases scheduled this week will be delayed due to system issues, while it added the nat gas storage report will be released as scheduled on June 23rd but all other releases will be delayed, according to Reuters.

- Germany reportedly fears that a planned ‘maintenance’ shutdown of the Nordstream 1 pipeline could be used by Russia to shut off gas supplies completely to Germany which would threaten its efforts to build stores ahead of winter, according to FT.

- Germany declares Phase Two of Emergency Gas Plan due to supply cuts from Russia and high prices.

- Spot gold is back below the DMAs it briefly surmounted yesterday, downside in wake of post-PMI USD upside.

US event Calendar

- 08:30: June Initial Jobless Claims, est. 226,000, prior 229,000

- 08:30: June Continuing Claims, est. 1.32m, prior 1.31m

- 08:30: 1Q Current Account Balance, est. -$275b, prior -$217.9b

- 09:45: June S&P Global US Services PMI, est. 53.2, prior 53.4

- 09:45: June S&P Global US Manufacturing PM, est. 56.0, prior 57.0

- 11:00: June Kansas City Fed Manf. Activity, est. 12, prior 23

Central Bank Speakers

- 10:00: Powell Testifies Before House Financial Services Panel

DB’s Jim Reid concludes the overnight wrap

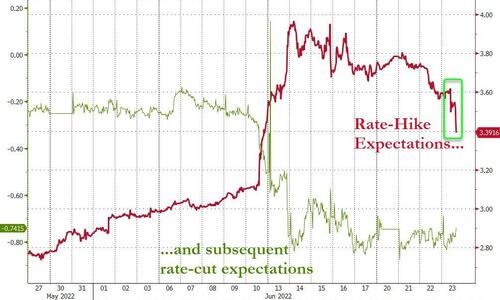

It’s been another eventful 24 hours in markets, with recession fears making a prominent return after Fed Chair Powell made some of his most pessimistic comments to date on whether the Fed would be able to successfully engineer a soft landing. Appearing before the Senate Banking Committee as part of the Fed’s semiannual Monetary Policy Report to Congress, Powell said that a recession was “a possibility”, whilst the soft landing the Fed is seeking will be “very challenging”, which is a long way from what the Fed were saying at the start of the year. Similarly, Powell said that the Fed “know we need to have restrictive policy, and that’s where we’re headed”, which is in line with what the Report itself said last week, in that the FOMC’s price stability commitment was “unconditional”. So a further reiteration that the Fed are prepared to keep hiking rates to bring down inflation, and an acknowledgement that there could well be a bumpy ride as they do so.

However, even as Powell emphasised the Fed’s willingness to deal with inflation, those growing fears of a recession meant that Fed funds futures became more doubtful on the Fed’s ability to take policy into restrictive territory. For instance, the rate priced in by the December meeting actually came down -10.5bps yesterday, and since early last week we’ve seen nearly a full 25bp hike taken out of market pricing. The expected terminal rate also came down, with futures only seeing a peak of 3.61% in April 2023 before subsequent cuts.

With investors becoming increasingly sceptical about the Fed taking policy far into restrictive territory, sovereign bonds rallied strongly yesterday, with yields on 10yr Treasuries down -11.9bps to 3.16%. That was driven by a decline in both real rates and inflation breakevens, and interestingly, the 10yr breakeven fell to its lowest level since Russia’s invasion of Ukraine began in late February yesterday, closing at 2.54%. In terms of the curve’s slope, the 2s10s steepened +2.2bps to 9.4bps, so still pretty close to inversion territory that has traditionally been a leading indicator of a recession. Meanwhile, if you look at the Fed’s preferred yield curve indicator that Powell has cited of the near-term forward spread (which looks at the 18m forward 3m yield minus the current 3m yield), that came down by -18.9bps yesterday to 176bps, which is the lowest it’s been in over 3 months, even if it still remains some way out of inversion territory.

Equities put in a mixed performance against this backdrop, with the S&P 500 oscillating between gains and losses before ending the day down -0.13%. Energy stocks were a major laggard after oil prices fell to a one-month low, with Brent crude down -2.54% over yesterday’s session to close at $111.74/bbl. And this morning those losses have accelerated further, with Brent crude down -2.52% to trade at $108.92/bbl, which is now -13% beneath its intraday peak above $125/bbl seen last week. Over in Europe the tone was even more negative, with the major indices including the STOXX 600 (-0.70%) and the DAX (-1.11%) all seeing noticeable declines. That coincided with growing fears on the energy side, and Germany’s economy minister Habeck said yesterday that “we must assume that Putin is ready to reduce the gas flow further”. Natural gas futures in Europe (+1.28%) hit a 3-month high against that backdrop, and this is only set to become more of an issue as we move closer towards the colder months of the year.

Staying on Europe, there was a similar rally in sovereign bonds to the US, with yields on 10yr bunds (-13.6bps) coming down from their post-2014 high on Tuesday. That was echoed elsewhere, whilst a fresh narrowing in peripheral spreads saw the gap between Italian 10yr yields over bunds reach their tightest in nearly a month, with a -2.0bps move to 191bps. Over in credit though, growing fears of a recession led to a widening in spreads, and iTraxx Crossover widened +15.4bps after 3 consecutive moves tighter.

Overnight in Asia, equities are similarly struggling to gain traction in light of those warnings about a US recession. Both the Nikkei (-0.33%) and the Kospi (-0.84%) have moved lower for a second consecutive session, although Chinese equities have put in a stronger performance, with the Shanghai Composite (+0.58%) and the CSI (+0.49%) both trading in positive territory with the Hang Seng (+0.96%) maintaining its morning gains. Outside of Asia, US equity futures have continued to move between gains and losses, but contracts on the S&P 500 (-0.23%) and NASDAQ 100 (-0.25%) are both pointing lower this morning.

Moving on to economic data, it’s an eventful day ahead as we get the flash PMIs for June. But we’ve already had the numbers out of Japan, where the services PMI hit its highest since October 2013 at 54.2, whilst the composite reading also accelerated to 53.2, which is the highest since November. The numbers from Australia showed a modest decline in June however, with the flash composite PMI down three-tenths on May’s reading to a 5-month low of 52.6.

Here in the UK, the main news yesterday came from the May CPI reading, where annual inflation rose to +9.1% in line with expectations. That’s the highest rate since March 1982, although core CPI did fall a bit more than expected to 5.9% (vs. 6.0% expected). Staying on the UK, there’s a couple of important political contests taking place in the form of two by-elections to the House of Commons as well. Both are in seats that had been won by the Conservatives at the last election, but where opposition parties are making a challenge, and represent an important test for Prime Minister Johnson’s authority, not least since he saw 41% of his party’s MPs vote no confidence in him at the start of the month. The one in Wakefield will be of particular interest, since that is a so-called “Red Wall” seat that Labour held for the entire post-war period before Johnson’s Conservatives gained it at the 2019 election. So an important bellwether as we move closer to the next election.

Looking at yesterday’s other data, the European Commission’s preliminary consumer confidence indicator for the Euro Area in June unexpectedly fell to -23.6 (vs. -20.5 expected), which is its lowest level since April 2020 at the height of the initial wave of the Covid pandemic. Separately, we saw Canadian CPI surprise on the upside, with the annual number coming in at +7.7% in May (vs. +7.3% expected), which is the fastest since 1983.

To the day ahead now, and the main data highlight will be the rest of the flash PMIs for June, along with the US weekly initial jobless claims, the Q1 current account balance, and the Kansas City Fed’s manufacturing activity for June. From central banks, Fed Chair Powell will be speaking before the House Financial Services Committee, the ECB will publish their Economic Bulletin, and we’ll hear from the ECB’s Nagel and Villeroy. Finally, EU leaders will be meeting in Brussels.

THURSDAY /WEDNESDAY NIGHT

SHANGHAI CLOSED UP 52.95 PTS OR 1.62% //Hang Sang CLOSED UP 265.53 PTS OR 1.36% /The Nikkei closed UP 21.70 OR 0.08% //Australia’s all ordinaires CLOSED UP 0.14% /Chinese yuan (ONSHORE) closed UP 6.7071 /Oil UP TO 105.78 dollars per barrel for WTI and UP TO 111.46 for Brent. Stocks in Europe OPENED ALL GREEN EXCEPT GERMAN DAX // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.7071 OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7068: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

3 a./NORTH KOREA/ SOUTH KOREA

///NORTH KOREA/SOUTH KOREA/

3B JAPAN

3c CHINA

CHINA/

Bank Runs Happening Across China, People Complain Hard to Obtain Cash

After nearly one million Chinese people were unable to access their bank deposits in central China’s Henan province earlier this year, residents in east China’s Shanghai, south China’s Shenzhen, north China’s Dandong, and central-east China’s Jiujiang reported the difficulties they faced when trying to withdraw cash from their bank accounts.

Some banks will only serve a limited number of customers per day, some banks limit each client’s withdrawal to no more than 1,000 yuan (about $149), and others closed their branches. Even the ATM machines are empty.

Bank runs have been happening in the world’s second largest economy for over a week, which is unusual in China because most of the banks are state-run.

“The reason why the bank run issue hasn’t been solved is that China’s economic system is in crisis and the Chinese regime doesn’t have the ability to solve it,” Wang He, U.S.-based China affairs commentator, told The Epoch Times on June 22.

Zheng Yongnian, one of the economic advisors to Chinese leader Xi Jinping, published an essay on June 1, in which he pointed out that China’s economy is facing critical challenges, including over half of the foreign investments having left China, and China’s private businesses are struggling for survival due to a supply chain crisis and lack of cash.

Unsurprisingly, Zheng’s essay was removed from China’s internet soon after it was published, as Beijing’s propaganda system doesn’t allow people to comment on China’s economy.

Shenzhen Residents

“I have an account with the Agricultural Bank of China. In recent two days, people lined up in front of the branch. This is the first time I have seen such a long queue,” Chen, a resident in Shenzhen in south China’s Guangdong Province, told NTD Television, The Epoch Times’ sister media, on June 21.

The Agricultural Bank of China is one of the four main state-run banks in China. The other three are Industrial and Commercial Bank of China, Bank of China, and China Construction Bank. Chen said that he was told the bank had mistakenly frozen customers’ accounts. To unfreeze an account, the bank asked its customers to submit their Shenzhen resident card in person.

The resident card is a method the Chinese regime uses to control people’s moving from site to site. In general, the regime uses a household registration system to lock a person in one city. The person won’t have the basic resident’s rights if he/she doesn’t have a local household registration card. If a person works for a big company in another city for six months, the employer can apply for a resident card for the employee.

Hao, a resident in Longgang district in Shenzhen, told The Epoch Times on June 22 that freezing accounts is a method banks use to stop people from withdrawing cash.

“It’s hard to find an ATM machine that has cash inside [in Shenzhen now]. Actually, since about two months ago, it has been difficult to withdraw cash. I have tried the Agricultural Bank of China and the China Construction Bank. It’s not easy to withdraw cash,” Hao said.

In a video that went viral on June 21, a man said that in a Shiyan neighborhood in Bao’an district in Shenzhen, people lined up outside the Bank of China at 6:00 a.m., but were told that the bank had run out of money when it opened at 9:00 a.m.

The bank didn’t explain why it had run out of cash.

Bank Runs in Other Cities

Dandong is a city neighboring North Korea across the Yalu River in northeastern China’s Liaoning Province. In recent weeks, people in Dandong complained that they couldn’t get cash from their bank accounts no matter how high their balances were.

“It has been a week. Every morning, there’s a long line [of people] waiting to withdraw cash. However, when it’s our turn in the afternoon, the bank has run dry,” a Dandong resident said in a social media video on June 20.

The man who shot the video said that employers in Dandong deposit salaries into their employee’s bank accounts in the Dandong Bank. Employees in turn, withdraw the cash for their daily living expenses. Being unable to access cash will make it difficult for them.

Another Dandong resident complained in a video that he went to several banks but was unable to get any cash.

In Jiujiang city of Jiangxi Province, residents reported that Agricultural Bank of China branches only allow customers to withdraw 1,000 yuan (about $149) or less if they don’t have a local household registration.

In eastern China’s Shanghai, people are also waiting in line outside the banks.

Huang, a local resident, told NTD Television on June 21 that banks will only serve 300 customers a day and this started on June 1 when the city officially opened up after a COVID lockdown. People have to go to the bank early in the morning, otherwise they won’t even enter the bank.

“I met a man in his 80s who began waiting in front of the bank between 4:00 a.m. and 5:00 a.m. He was counted as the 107th client of the day when the bank opened at 9:00 a.m. He had to stay there for several more hours because the bank wouldn’t allow him to enter if he missed his turn,” Huang said.

Unlike the United States, a lot of Chinese residents pay their gas, electricity, and water bills at a bank, and most retired people rely on cash because they don’t know how to make a payment using the internet or a smart phone, or how to pay for groceries using a bank card.

Nicole Hao is a Washington-based reporter focused on China-related topics. Before joining the Epoch Media Group in July 2009, she worked as a global product manager for a railway business in Paris, France.

4/EUROPEAN AFFAIRS//UK AFFAIRS/

EUROPE

Europe is now in contraction phase as the PMI’s sent the Euro tumbling!

(zerohedge)

“Horror-Show” PMIs Send Euro Tumbling And Europe To Edge Of Recession

THURSDAY, JUN 23, 2022 – 09:26 AM

Many Wall Street analysts were keeping a close eye on today’s PMI barrage around the globe – among the most popular leading indicators for key economic inflection points – for the latest indication that the economy is sliding into recession. They got that and more when the latest PMI data out of Europe was nothing short of a “Horror-show” as Bloomberg called it.

The Euro area composite flash PMI decreased by 2.9pt to 51.9 in June, far below consensus expectations of 54.0 and below the May print of 54.8.

Here are the key numbers (as an aside, responses were collected between 13 and 21 June):

- Euro Area Composite PMI (June, Flash): 51.9, consensus 54.0, last 54.8.

- Euro Area Manufacturing PMI (June, Flash): 52.0, consensus 53.8, last 54.6.

- Euro Area Services PMI (June, Flash): 52.8, consensus 55.5, last 56.1.

- Germany Composite PMI (June, Flash): 51.3, consensus 53.0, last 53.7.

- France Composite PMI (June, Flash): 52.8, consensus 55.9, last 57.0.

- UK Composite PMI (June, Flash): 53.1, consensus 52.4, last 53.1.

As Goldman explains in its PMI post-mortem, “the weakening was broad-based across countries and sectors, but skewed towards France and services.” Today’s data showed moderating momentum in services and a weak manufacturing sector, where the levels of PMI have now fallen into contractionary territory (i.e. recession).

The composition of the June report was squarely weaker than in May, with new orders, employment, new export and backlogs all declining in June. Notably, both new orders and new export orders are now at levels below 50, reflecting a slowdown in both domestic and foreign demand. Firms’ expectations also decreased further, with the gap between expected future and current output (a measure of pent-up momentum) currently around 1.4 standard deviation below its historical average. Suppliers’ delivery times improved for the third consecutive month in a sign of continued easing of bottlenecks in the manufacturing sector and, while price components moderated slightly, they remain near all-time highs.

Regional breakdown:

- The German composite PMI decreased by 2.4pt to 51.3 in June, below consensus expectations. The composite decline was broad-based across sectors, with manufacturing output falling to levels below 50 again after a slight recovery last month. The composition of the June report showed broad-based declines across components, with new orders, employment, new export orders, and backlogs all declining in June. Firms’ expectations also edged down on the back of a weaker outlook for the manufacturing sector. Price pressures remain acute as both input and output price components remain near all-time highs but bottlenecks in the manufacturing sector continue to ease as suppliers’ delivery times improved further in June.

- The French composite PMI decreased by 4.2pt to 52.8 in June, well below consensus expectations. As in Germany, the composite decline was broad-based across sectors, reflecting a moderation in services and a contraction in manufacturing output. The composition of the June report showed declines across new orders, employment, new export orders, as well as backlogs. Firms’ expectations of year-ahead output also declined meaningfully—after improving consecutively for the last two months—to below their historical average, reflecting a less optimistic outlook across both sectors. Suppliers’ delivery times improved slightly but both the input and output price components remain near all-time highs despite a slight moderation in the latter. The downside surprise in the June flash PMI is consistent with some components of the INSEE survey (also released this morning), which also showed a decline in its services and headline index, below consensus expectations, but at odds with the INSEE manufacturing index, which improved in June, ahead of consensus expectations for a decline.

The extent of the deceleration observed today was larger than expected and thus today’s data is consistent with expectations of moderating growth in services and further weakening in the manufacturing sector, eventually transforming into a full-blown recession. As such Goldman continues to forecast weak growth in the second half of the year and see risks as skewed towards the downside, particularly in Germany, if gas flows from Russia do not pick up following the end of the pipeline maintenance period in mid-July.

The dismal news understandably sent the EUR tumbling back below 1.05…

… while the sharp slowdown in Europe’s economy put German 10-year yields on track for their biggest decline in more than three months.

The biggest question, however, is whether Europe will slide into recession before the ECB has even had a chance to follow through with any of its hikes, which are supposed to begin as soon as next month… which is also when the European economy is now widely expected to contract, in another dire repeat of the events that pushed the continent into the sovereign debt crisis.

ECB

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS/

SWEDEN/FINLAND/NATO//RUSSIA

NATO Chief Calls For Sweden And Finland To Join ‘As Soon As Possible’

THURSDAY, JUN 23, 2022 – 09:07 AM

Why is NATO so anxious to induct multiple countries near the borders of Russia into the fold without concern for the geopolitical consequences? Probably because the war in Ukraine is not going so well. Or, perhaps the goal is to deliberately create an even wider conflict. Either way, NATO’s behavior suggests that there is considerable information that is not being revealed to the general public.

NATO Chief General Jens Stoltenberg has been pushing for swift approval of applications from Sweden and Finland, with Department of Defense officials in the US calling on the Senate Foreign Relations Committee to quickly approve the requests.

With mainstream media propaganda constant for the past few months when it comes to the Ukraine situation, it has been hard to gauge the facts surrounding the conflict. Only in recent weeks have there been admissions from Ukrainian leadership hinting at the true conditions on the ground. President Volodymyr Zelenskyy himself acknowledge that Ukrainian casualties are high: 60 – 100 per day. Other sources indicate casualties of 100 – 200 soldiers per day. The Ukrainians have to present a number that’s large enough to warrant more NATO armaments and money while making sure it’s not so high that it demoralizes their troops in the field.