by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD; $1828.30 UP $0.45

SILVER: $21.17 UP 10 CENTS

ACCESS MARKET: GOLD $1826.50

SILVER: $21.13

Bitcoin morning price: $21,095 UP 240

Bitcoin: afternoon price: $21,214 UP 359.

Platinum price: closing UP $0.35 to $911.50

Palladium price; closing UP $37.00 at $1841.55

END

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX EXCHANGE:EXCHANGE:

EXCHANGE: COMEX

CONTRACT: JUNE 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,825.700000000 USD

INTENT DATE: 06/23/2022 DELIVERY DATE: 06/27/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 108

363 H WELLS FARGO SEC 15

365 H ED&F MAN CAPITA 1

624 H BOFA SECURITIES 18

661 C JP MORGAN 12

700 C UBS 1

732 C RBC CAP MARKETS 1

905 C ADM 10

991 H CME 50

TOTAL: 108 108

MONTH TO DATE: 23,916

no. of contracts issued by JPMorgan: 12/108

_____________________________________________________________________________________

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT 108 NOTICE(S) FOR 10800 Oz//0.3359 TONNES)

total notices so far: 23,916 contracts for 2,391,600 oz (74.388 tonnes)

SILVER NOTICES:

2 NOTICE(S) FILED 10,000 OZ/

total number of notices filed so far this month 1820 : for 9,100,000 oz

END

Russia is a major supplier of silver to London while Mexico supplies the COMEX

With the sanctions, London has no way to obtain silver other than compete with NY.

GLD

WITH GOLD UP $0.45

WITH RESPECT TO GLD WITHDRAWALS: (OVER THE PAST FEW MONTHS):

GOLD IS “RETURNED” TO THE BANK OF ENGLAND WHEN CALLING IN THEIR LEASES: THE GOLD NEVER LEAVES THE BANK OF ENGLAND IN THE FIRST PLACE. THE BANK IS PROTECTING ITSELF IN CASE OF COMMERCIAL FAILURE

ALSO INVESTORS SWITCHING TO SPROTT PHYSICAL (phys) INSTEAD OF THE FRAUDULENT GLD//

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//

INVENTORY RESTS AT 1063.07 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 10 CENTS

AT THE SLV// ://BIG CHANGES IN SILVER INVENTORY AT THE SLV//A WITHDRAWAL OF 3.127 MILLION OZ INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 542.000 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A VERY STRONG SIZED 1042 CONTRACTS TO 141,555 AND CLOSER TO THE NEW RECORD OF 244,710, SET FEB 25/2020 AND THE STRONG LOSS IN OI WAS ACCOMPLISHED WITH OUR STRONG $0.41 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.41) AND WERE SUCCESSFUL IN KNOCKING OFF SOME SILVER LONGS//BUT MAINLY WE HAD ADDITIONAL SPECULATOR ADDITIONS.

WE MUST HAVE HAD:

I) HUGE SPECULATOR SHORT ADDITIONS /. II)WE ALSO HAD SOME REDDIT RAPTOR BUYING//. iii) A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) A STRONG INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 7.635 MILLION OZ FOLLOWED BY TODAY’S QUEUE JUMP OF 6 CONTRACTS OR 30,000 OZ//NEW STANDING: 9,225,000 / // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI SILVER TODAY: CONTRACTS : -59

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTACTS for 17 days, total 12,890, contracts: 64.035 million oz OR 3.764 MILLION OZ PER DAY. (758 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 64.035 MILLION OZ

.

LAST 11 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE AND WE ARE STILL GOING STRONG THIS MONTH.

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 64.035 MILLION OZ

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1042 WITH OUR $0.41 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE CONTRACTS: 690 CONTRACTS ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS THE DOMINANT FEATURE TODAY: /HUGE BANKER SHORT COVERING AS THEY GET OUT OF DODGE//// WE HAVE A HUGE INITIAL SILVER OZ STANDING FOR JUNE. OF 7.635 MILLION OZ FOLLOWED BY TODAY’S 30,000 QUEUE JUMP //NEW STANDING: 9,225,000 OZ // .. WE HAD A SMALL SIZED LOSS OF 352 OI CONTRACTS ON THE TWO EXCHANGES FOR 1.76 MILLION OZ WITH THE LOSS IN PRICE.

WE HAD 2 NOTICES FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2405 CONTRACTS TO 501,712 AND FURTHER NEW RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: -39 CONTRACTS.

.

THE SMALL GAIN IN COMEX OI CAME DESPITE OUR STRONG FALL IN PRICE OF $8.60//COMEX GOLD TRADING/THURSDAY / WE MUST HAVE HAD SOME SPECULATOR SHORT COVERING ACCOMPANYING OUR STRONG SIZED EXCHANGE FOR PHYSICAL ISSUANCE. WE HAD ZERO LONG LIQUIDATION //AND SOME SPECULATOR SHORT COVERING

WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 69.26 TONNES ON FIRST DAY NOTICE /FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW STANDING: 74.786TONNES

YET ALL OF..THIS HAPPENED WITH OUR LOSS IN PRICE OF $8.60 WITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A STRONG SIZED GAIN OF 6457 OI CONTRACTS 20.083 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4052 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 501,712

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6495, WITH 2405 CONTRACTS INCREASED AT THE COMEX AND 4052 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6457 CONTRACTS OR 20.083 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4052) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (2405,): TOTAL GAIN IN THE TWO EXCHANGES 6457 CONTRACTS. WE NO DOUBT HAD 1) SOME SPECULATOR SHORT COVERING AND SOME ADDITION TO SPECULATOR SHORTS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE. AT 69.26 TONNES FOLLOWED BY TODAY’S E.F.P JUMP OF 3900 OZ//NEW STANDING: 74.9611 TONNES / 3) ZERO LONG LIQUIDATION//SOME SPECULATOR SHORT COVERING//SOME SPECULATOR SHORT ADDITIONS //.,4) SMALL SIZED COMEX OI GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

62,038 CONTRACTS OR 6,203,800 OZ OR 192.96 TONNES 17 TRADING DAY(S) AND THUS AVERAGING: 3624 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES: 169.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 192.96/3550 x 100% TONNES 5.43% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 192.96 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF SILVER

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF APRIL HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF MAY, FOR SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JULY), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A STRONG SIZED 1042 CONTRACT OI TO 141,555 AND FURTHER FROM OUR COMEX RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 690 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 690 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1042 CONTRACTS AND ADD TO THE 690- OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED LOSS OF 352 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 1.76 MILLION OZ

OCCURRED WITH OUR FALL IN PRICE OF $0.41 .

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold commentaries

end

6. Commodity commentaries//

3. ASIAN AFFAIRS

i)FRIDAY MORNING// THURSDAY NIGHT

SHANGHAI CLOSED UP 29.60 PTS OR 0.89% //Hang Sang CLOSED UP 445.12 PTS OR 2.09% /The Nikkei closed UP 320.72 OR 1/23% //Australia’s all ordinaires CLOSED UP 1.06% /Chinese yuan (ONSHORE) closed UP 6.6958 /Oil UP TO 106.11 dollars per barrel for WTI and UP TO 111.75 for Brent. Stocks in Europe OPENED ALL GREEN // ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.6958 OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6910: /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 2405 CONTRACTS TO 501,673 AND FURTHER FROM THE RECORD THAT WAS SET IN JANUARY/2020: {799,541 OI(SET JAN 16/2020)} AND PREVIOUS TO THAT: 797,110 (SET JAN 7/2020). AND THIS COMEX DECREASE OCCURRED WITH OUR LOSS OF $8.60 IN GOLD PRICING THURSDAY’S COMEX TRADING. WE ALSO HAD A GOOD SIZED EFP (4052 CONTRACTS). . THEY WERE PAID HANDSOMELY NOT TO TAKE DELIVERY AT THE COMEX AND SETTLE FOR CASH. IT NOW SEEMS THAT THE COMMERCIALS HAVE GOADED THE SPECS TO GO SHORT BIG TIME AND THEY ADDED TO THEIR SHORT POSITIONS

WE NORMALLY HAVE WITNESSED EXCHANGE FOR PHYSICALS ISSUED BEING SMALL AS IT JUST TOO COSTLY FOR THEM TO CONTINUE SERVICING THE COSTS OF SERIAL FORWARDS CIRCULATING IN LONDON. HOWEVER, MUCH TO THE ANNOYANCE OF OUR BANKERS, THE COMEX IS THE SCENE OF AN ASSAULT ON GOLD AS LONDONERS, NOT BEING ABLE TO FIND ANY PHYSICAL ON THAT SIDE OF THE POND, EXERCISE THESE CIRCULATING EXCHANGE FOR PHYSICALS IN LONDON AND FORCING DELIVERY OF REAL METAL OVER HERE AS THE OBLIGATION STILL RESTS WITH NEW YORK BANKERS. IT SEEMS THAT ARE BANKERS FRIENDS ARE EXERCISING EFP’S FROM LONDON AND NOW THEY ARE LOATHE TO ISSUE NEW ONES.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW MOVING TO THE ACTIVE DELIVERY MONTH OF JUNE.. THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4052 EFP CONTRACTS WERE ISSUED: ;: , . 0 AUG :4052 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4052 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6457 CONTRACTS IN THAT 4052 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED COMEX OI GAIN OF 2405 CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR FALL IN PRICE OF GOLD $8.60.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING JUNE (74.793),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL SO FAR THIS YEAR (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.793 TONNES

THE BANKERS WERE SUCCESSFUL IN LOWERING GOLD’S PRICE //// (IT FELL $8.60) BUT WERE UNSUCCESSFUL IN KNOCKING OFF SPECULATOR LONGS/COMMERCIAL LONGS BUT SPECULATOR SHORTS CONTINUED TO ADD TO THEIR POSITIONS//// WE HAVE REGISTERED A STRONG SIZED GAIN OF 6452 TONNES ON TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR HUGE GOLD TONNAGE STANDING FOR JUNE (74.793 TONNES)…

WE HAD 39 CONTRACTS REMOVED FROM COMEX TRADES. THESE WERE REMOVED AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 6457 CONTRACTS OR 645700 OZ OR 20.083 TONNES

Estimated gold volume 137,760/// poor/

final gold volumes/yesterday 176,400 /poor

INITIAL STANDINGS FOR JUNE ’22 COMEX GOLD //JUNE 24

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz | 187,532.727 oz Manfra Loomis HSBC 27 kilobars |

| Deposit to the Dealer Inventory in oz | nilOZ |

| Deposits to the Customer Inventory, in oz | 1488.84 oz Brinks |

| No of oz served (contracts) today | 108 notice(s)10800 OZ .3359 TONNES |

| No of oz to be served (notices) | 130 contracts 18,400 oz 0.4043 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,916 notices 2,391600 OZ 74.388 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

| xxx oz |

total dealer deposit 0

No dealer withdrawals

1 customer deposit

i) Into Brinks: 1488.84 oz

total deposits: 1488.84 oz

3 customer withdrawals:

i)Out of HSBC 129,486.312 oz

ii) Out of Loomis: 868.077 oz (27 kilobars)

iii) Out of Manfra: 56,856.827 oz

total withdrawal: 187,532.727 oz

ADJUSTMENTS:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 238 contracts having lost 12 contracts

We had 12 notices filed on THURSDAY so we LOST 0 contracts or an additional NIL oz will stand for gold in this very active month of June

July has a LOSS OF 76 OI to stand at 1376

August has a GAIN of 374 contracts UP to 412,185 contracts

We had 108 notice(s) filed today for NIL 10,80 oz FOR THE JUNE 2022 CONTRACT MONTH.

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 108 contract(s) of which 12 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2021. contract month,

we take the total number of notices filed so far for the month (23,916) x 100 oz , to which we add the difference between the open interest for the front month of (JUNE 238 CONTRACTS ) minus the number of notices served upon today 108 x 100 oz per contract equals 2,404,600 OZ OR 74.793 TONNES the number of TONNES standing in this active month of JUNE.

thus the INITIAL standings for gold for the JUNE contract month:

No of notices filed so far (23,916) x 100 oz+ (238) OI for the front month minus the number of notices served upon today (108} x 100 oz} which equals 2,404,600 oz standing OR 74.793 TONNES in this active delivery month of JUNE.

TOTAL COMEX GOLD STANDING: 74.793 TONNES (A STRONG STANDING FOR A JUNE ( ACTIVE) DELIVERY MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,419,784.828 oz 75.26 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 33,318,650.828 OZ

TOTAL ELIGIBLE GOLD: 16,042,586.107 OZ

TOTAL OF ALL REGISTERED GOLD: 17,276,064.721OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 14,921,555.0 OZ (REG GOLD- PLEDGED GOLD)

END

SILVER/COMEX/JUNE 24

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3,348,842.466 oz Brinks CNT HSBC Int. Delaware |

| Deposits to the Dealer Inventory | ni lOZ |

| Deposits to the Customer Inventory | 608,289.756 oz CNT |

| No of oz served today (contracts) | 2CONTRACT(S)10,000 OZ) |

| No of oz to be served (notices) | 25 contracts (125,000 oz) |

| Total monthly oz silver served (contracts) | 1820 contracts 9,100,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

And now for the wild silver comex results

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: nil oz

We have 1 deposit into the customer account

i) Into CNT 608,289.756 oz

total deposit: 608,289.756 oz

JPMorgan has a total silver weight: 169.099 million oz/337.812 million =50.02% of comex

Comex withdrawals: 4

CNT 100,002.056 oz

Brinks: 2,628,947.960 oz

HSBC 600,000.000???

Int. Delaware: 19,922.450 oz

total withdrawal 3,348,842.466 oz

adjustments: 2

dealer to customer

HSBC: 136,860.000 oz

Loomis: 126,994.666

the silver comex is in stress!

TOTAL REGISTERED SILVER: 71.116 MILLION OZ

TOTAL REG + ELIG. 336/553 MILLION OZ

CALCULATION OF SILVER OZ STANDING FOR JUNE

silver open interest data:

FRONT MONTH OF JUNE OI: 27 HAVING LOST 3 CONTRACTS.

WE HAD 9 NOTICES FILED ON THURSDAY SO WE GAINED 6 CONTRACTS OR AN ADDITIONAL 30,000 OZ WILL STAND IN THIS NON ACTIVE

DELIVERY MONTH OF JUNE

JULY HAD A LOSS OF 7148 CONTRACTS DOWN TO 28,408 CONTRACTS.

AUGUST GAINED 83 CONTRACTS TO STAND AT 1186

SEPTEMBER HAD A GAIN OF 5712 CONTRACTS UP TO 93,904 CONTRACTS.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 6 for 30,000 oz

Comex volumes:99,287// est. volume today// STRONG

Comex volume: confirmed yesterday: 103,356 contracts ( strong )

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1820 x 5,000 oz = 9,100,000 oz

to which we add the difference between the open interest for the front month of JUNE(27) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE./2022 contract month: 1820 (notices served so far) x 5000 oz + OI for front month of JUNE (27) – number of notices served upon today (2) x 5000 oz of silver standing for the JUNE contract month equates 9,225,000 oz. .

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS:

JUNE 24/WITH SILVER UP 45 CENTS TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 8.70 TONNES FROM THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 23/WITH GOLD DOWN $8.60:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD//INVENTORY RESTS AT 1071.77 TONNES

JUNE 22/WITH GOLD UP 15 CENTS:BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD////INVENTORY RESTS AT 1073.80 TONNES

JUNE 21/WITH GOLD DOWN $2.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 1075.54 TONES

JUNE 17/WITH GOLD DOWN $11.25: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.60 TONNES INTO THE GLD.///INVENTORY RESTS AT 1075.54 TONNES

JUNE 16/WITH GOLD UP $28.95: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.74 TONNES

JUNE 15/WITH GOLD UP $6.50/BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.65 TONNES FROM THE GLD////INVENTORY RESTS AT 1063.74 TONNES

JUNE 14/WITH GOLD DOWN $18.80/NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 13/WITH GOLD DOWN $41.55: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 10/WITH GOLD UP $21.40: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1065.39 TONNES

JUNE 9/WITH GOLD DOWN $3.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 1065.39 TONNES

JUNE 8/WITH GOLD UP $4.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 7/WITH GOLD UP $7.45: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1063.07 TONNES

JUNE 6/WITH GOLD DOWN $5.85: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 3/WITH GOLD DOWN $19.75//A BIG CHANGE IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD//INVENTORY RESTS AT 1066.04 TONNES

JUNE 2/WITH GOLD UP $22.50: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.64 TONNES FROM THE GLD//INVENTORY RESTS AT 1067.20 TONNES

JUNE 1/WITH GOLD UP $1$ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AWITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 1068.36 TONNES

MAY 31/WITH GOLD DOWN $15.10: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 27/WITH GOLD UP $4.95//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1069.81 TONNES

May 26/WITH GOLD UP $2.10/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 1069.81 TONNES

MAY 25/WITH GOLD UP @$2.70: A HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 11.89./INVENTORY RESTS AT 1068.07 TONNES

MAY 20/WITH GOLD UP $7.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.97 TONNES INTO THE GLD/INVENTORY RESTS AT 1056.18 TONNES

MAY 19/WITH GOLD UP $24.20; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 1049.21 TONNES//

GLD INVENTORY: 1063.07 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 24/WITH SILVER UP 10 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.137 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 542.000 MILLION OZ

JUNE 23/WITH SILVER DOWN 41 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 2.029 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 545.137 MILLION OZ//

JUNE 22/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 547.166 MILLION OZ.

JUNE 21/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.506 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 547.166 MILLION OZ//

JUNE 17/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 739,000 OZ FROM THE SLV./:INVENTORY RESTS AT 543.660 MILLION OZ/

JUNE 16/WITH SILVER UP 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 15/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ

JUNE 14/WITH SILVER DOWN 32 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 13/WITH SILVER DOWN 62 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 10.WITH SILVER UP 13 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 830,000 Z FROM THE SLV//INVENTORY RESTS AT 544.399 MILLION OZ//

JUNE 9/WITH SILVER DOWN 27 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 923,000 OZ INTO THE SLV////INVENTORY RESTS AT 545.229 MILLION OZ

JUNE 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 544.306 MILLION OZ//

JUNE 7/WITH SILVER UP 6 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 544.306 MILLION OZ/

JUNE 6/WITH SILVER UP 20 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 6.459 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 547.167 MILLION OZ//

JUNE 3/WITH SILVER DOWN $.34: A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITTHDRAWAL OF 246,000 OZ FORM THE SLV//INVENTORY RESTS AT 553.626 MILLION OZ..

JUNE 2/WITH SILVER UP 57 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.261 MILLION OZ FORM THE SLV.//INVENTORY RESTS T 553.872 MILLION OZ

JUNE 1/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV//: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 556.133 MILLION OZ//

MAY 31/WITH SILVER DOWN $.41 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST S AT 558.071 MILLION OZ//

MAY 27/WITH SILVER UP 10 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 558.071 MILLION OZ///

MAY 26/WITH SILVER UP 8 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.515 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 558.071 MILLION OZ

MAY 25/WITH SILVER UP 20 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .922 MILLION OZ FROM THE SLV/ //INVENTORY RESTS AT 561.486 MILLION OZ//

MAY 20.WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WIHDRAWAL OF .785 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 565.085 MILLION OZ//

MAY 19/WITH SILVER UP 34 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 565.085 MILLION OZ//

CLOSING INVENTORY 542.000 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1.PETER SCHIFF

2. Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg

(Egon von Greyerz)

Von Greyerz: Concurrent Deflation & Hyperinflation Will Ravage The World

FRIDAY, JUN 24, 2022 – 06:30 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

FLATION will be the keyword in coming years. The world will simultaneously experience inFLATION, deFLATION, stagFLATION and eventually hyperinFLATION.

I have forecasted these FLATIONARY events, which will hit the world in several articles in the past. Here is a link to an article from 2016.

With most asset classes falling rapidly, the world is now approaching calamities of a proportion not seen before in history. So far in 2022, we have seen an implosion of asset prices across the board of around 20%. What few investors realise is that this is the mere beginning. Before this bear market is over, the world will see 75-90% falls of stocks, bonds and other assets.

Since falls of this magnitude have not been seen for more than three generations, the shockwaves will be calamitous.

At the same time as bubble assets deflate, prices of goods and services have started an inflationary cycle of a magnitude that the world as whole has never experienced before.

We have seen hyperinflation in individual countries previously but never on a global scale.

Currently the official inflation rate is around 8% in the US and Europe. But for the average consumer in the West, prices are rising by at least 25% on average for their everyday needs such as food and fuel.

A CALAMITOUS WORLD

So the world is now approaching calamities on many fronts.

As always in periods of crisis, everybody is looking for someone to blame. In the West most people blame Putin. Yes, Putin is the villain and it is his fault that food and energy prices are surging. Nobody bothers to analyse what or who prompted Russia to intervene, nor do politicians or main stream media understand the importance of history, which is the key to understanding current events.

In troubled times, everyone needs someone to blame. Many Americans will blame Biden who has both lost his grip on most US events as well as his balance. In the UK, the people blame Boris Johnson who has lost control of Britain since Partygate. In France the people are blaming Macron who just lost his majority in parliament, and in Germany people blame Scholz for sending money to Ukraine for weapons and money to Russia for gas.

This blame game is only just beginning. Political turmoil and anarchy will be the rule rather than the exception as the people will blame the leaders for higher prices and taxes and deteriorating services in all areas.

No country will be able to provide social security payments in line with galloping inflation. Same with unfunded or underfunded pensions, which will fall dramatically or even disappear totally as the underlying asset base of stocks and bonds implodes.

As a consequence, many countries will be anarchic.

Deflationary implosion of investment markets

Stocks

The everything bubble has come to an end. It was only possible due to the benevolence of central banks in creating the most perfect manipulation of the instruments that they control, namely money printing and interest rates.

The result of free money has meant a trebling of global debt in this century to $300 trillion at virtually zero interest cost.

This has been real Manna from heaven for investors, both big or small. Everything investors touched went up and at every correction in the market, more Manna was produced.

For investors it was always “Heads I win, Tails I win.”

This Shangri-La of markets makes everyone an investment guru. Even a fool became rich.

Speaking to investor friends today, they might be slightly unsettled but see no reason why the long term bull trend won’t continue. As far as investors are concerned, Greenspan, Bernanke, Yellen and Powell have been their best friends and the Fed’s main purpose is to keep investors happy and rich. Therefore most investors are sitting tight in spite of 20% falls or more across the board. They will regret it.

So most investors are relying on being saved yet another time and don’t realise that this time it is really different.

As we know, it is NOT the fact that central bankers have done a volte face (about turn) in raising rates and also reversed quantitive easing into tightening which has led to investment markets crashing.

No, these geniuses running the Central Banks can never see anything coming before it is too late. Inflation hitting the world with a vengeance was clear to many of us for quite a while–but obviously not to the people running monetary policy. They are clearly not paid to see anything coming before it has actually happened.

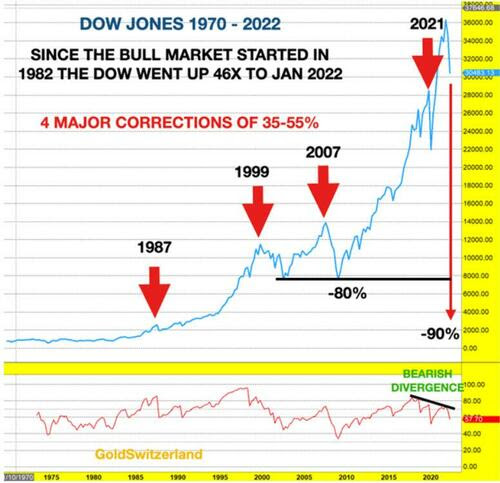

The chart below shows the Dow since 1970. In 1982, the current 40 year bull market started. Since then investors have seen a dramatic 46X increase in their stock portfolios.

There have been four frightening corrections of between 35% and 55%. I remember well the first one in October 1987. It was Black Monday and I was in Tokyo for the listing of Dixons in Japan, the UK FTSE 100 company I was Vice-Chairman of. The market crashed 23% on October 19th and over a 12 day period the Dow was down 40%.

Not the best timing for a listing on the Tokyo stock exchange .

.

If we look at 1987 in the chart below, we can see that the massive fall we experienced at the time is hardly visible.

Another very important technical factor on this chart is the bearish divergence on the Relative Strength Index – RSI. Since 2018, I have pointed out that the RSI on this quarterly chart has made lower highs since 2018 as the Dow has made new highs. This is a very bearish signal and will inevitably result in a major fall of the Dow as we are now seeing.

My long standing forecast of a 90% fall in stocks in real terms has not changed. This fall is no bigger than the 1929-32 one with dramatically worse conditions today both in debt markets and in the global magnitude of the bubbles . Just a return to the 2002 and 2009 lows would involve an 80% fall from the top.

The Wilshire 5000 representing all US stocks has lost $11 trillion or 23% since the beginning of 2022. See chart below. Additional trillions have been lost in bond markets.

Bonds

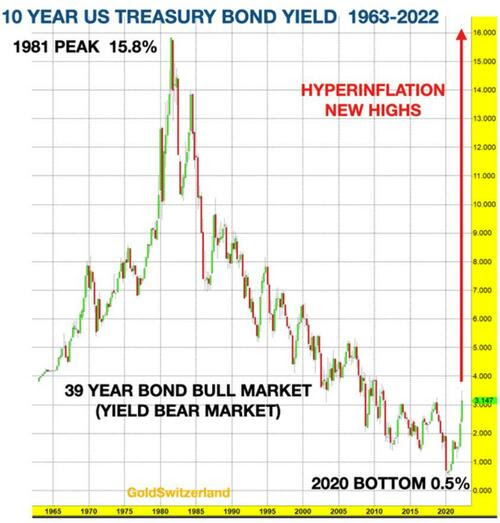

The 39 year bull market in bond prices (bear market in interest rates) has now come to an end. In fact it ended in 2020 at 0.5% having fallen all the way from 15.5% in 1981.

I expect rates to surpass the 1981 level as the biggest debt market in history implodes.

Many debtors, both sovereign and private will fail and bond rates will reach infinite levels as bond prices collapse.

This implosion of bond markets will obviously have major repercussions for the financial system and markets with banks and other financial institutions defaulting.

After more than a decade of long struggle to raise inflation up to 2%, central bankers like Yellen and Lagarde got the shock of a life time with official inflation rapidly surging to over 8% with real inflation probably around 20-25% for most people.

This increase in inflation was such a shock to the Bank heads that they were in denial for many weeks, calling it transitory.

These Fed and ECB chiefs have this uncanny ability not to see anything that they haven’t projected. And since they never project one single market trend correctly, they will inevitably always take the wrong road.

They would be more successful it they just rolled the dice. Over time they would then at least have a 50% chance of being right. Instead they have a perfect record of being 100% wrong.

As I state over and over again, central banks should not exist. The laws of nature and supply and demand would do a much better job at regulating markets. Without central banks and their manipulation, markets would be self correcting rather than the extreme peaks and troughs that the banks create.

The absurdity of central banks’ disastrous manipulation is clearly exposed in credit markets. We have for years had credit surging with rates being around zero or negative.

It is obvious to any student of economics that high demand for credit would lead to a high cost of borrowing. These would be the obvious consequences of supply and demand in a free and non-manipulated market.

The inverse would clearly also be the case. If there is no demand for credit, interest rates would come down and stimulate demand.

I wonder what they teach students of economics today since no market functions properly with the current blatant manipulation. I suppose that our woke society is rewriting the books also in economics just as they have done with history.

I would hate to be a student today under those conditions.

INVESTMENT MARKETS – NOWHERE TO HIDE

So what are the consequences of these calamitous times?

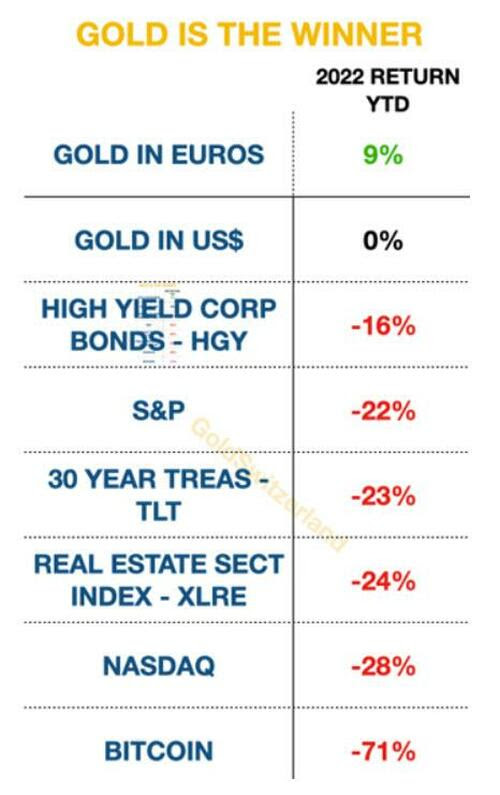

Well, in 2022 virtually every single investment class is down around 20%, as the table below shows. And the era of successful dip buying has ended as everything is collapsing.

With panic in markets and already some blood in the streets, investors are paralysed. They hope that the Fed and other central banks will save them but they fear that it might be different this time. This is just the very beginning. Much more panic and blood to come.

Both private and institutional investors are totally lost. All sectors are falling together. There just is nowhere to turn.

Just look at the table below:

Gold in euros as well as gold in most other currencies have had a positive return in 2022 so far.

But just look at the rest – from Corporate Bonds to Treasuries to Stocks, Real Estate, Tech Stocks and Cryptos etc they have all seen double digit losses in 2022 from 16% to 71%.

And nobody realises that this is just the beginning.

The majority of investors are totally paralysed. They are all hoping for the rapid April-2020-style recovery but they will be very, very disappointed. IT JUST WON’T COME!

Investors are neither mentally nor financially prepared for what is coming.

The selling we are currently seeing is just marginal. Most investors are staying put and will ride the market down by 50% or more before they realise that this is serious. And at that point they will hope and pray since they will believe it is too late to get out.

Sadly no one will understand that it is really different this time and that most asset classes will fall by 90% or more in real terms.

EPIC SUPER BUBBLES ALWAYS HAVE AN UNHAPPY ENDING

Epic super bubbles can only end badly. But no investor has the experience of such a massive implosion of bubbles because it has never happened before in history.

I have discussed the consequences in many articles, and they will be devastating.

Sadly Cassandras are never taken seriously until it is too late. This time will be no different.

And don’t believe there is anyone there to help. The Fed, which has reacted at least 10 years too late in tightening, will not save investors. Instead, they will offer more pain in the form of higher rates and more tightening.

Yes, of course the Fed will react at some point and in panic lower rates and inject fake money into the system. But that will be much too late. Also, no amount of fake money can save a system which is morally and financially bankrupt.

A morally and financially bankrupt western world has created this coming calamity, and we will now have to suffer the consequences.

Sadly, this this is the only way that it can end. A rotten and debt infested system can only end in a calamity.

Debts will implode and assets will implode. Society will not function nor will social security, pensions etc. This will create human suffering of a magnitude, which will be devastating for everyone.

Global population will also come down dramatically. In the mid 1800s there were 1 billion people on earth with very slow growth for the previous thousands of years. Then population exploded over the next 170 years to 8 billion. A chart that look like a spike up normally always corrects up to 50% down. The reasons for a reduction of world population are obvious: Economic collapse, misery, famine, disease and wars.

Such a singularity event is necessary for the world to clean up the rotten system and start a new era with green shoots and stronger moral and ethical values.

WEALTH PROTECTION A NECESSITY

For the few people who have assets to protect, physical gold and some silver will perform much better than all conventional asset markets which will collapse. That trend has already started as the table above shows.

Stocks will tank and commodities will soar.

For investors this is best illustrated in the Dow/Gold Ratio. This ratio is currently 16.5 and is likely to find long turn support at 0.5. Reaching that target would involve a 97% fall of the Dow relative to gold. Sounds incredible today but bearing in mind the circumstances this level is certainly possible. See my article.

An 0.5 Dow/Gold ratio could for example mean Dow 5,000 and Gold $10,000

GOLD – THE ULTIMATE INSURANCE AGAINST WEALTH DESTRUCTION

Anyone who has experienced hyperinflation also knows that the only money that survives such a calamity is gold. I met a year ago a man from former Yugoslavia who recognised me and told my friends who were with me that physical gold saved his family from total devastation. My friends sadly did not take his advice.

But remember that any protection or insurance must be acquired before disaster hits you.

Your most important assets are your brain, heart and soul. There are always opportunities for individuals who apply those assets wisely.

And as always in periods of crisis, being with and helping family and friends is your most important task.

-END-

My goodness!! JPMorgan’s derivatives at a six yr high of $60 trillion

(Pam and Russ Martens)

JPMorgan Chase’s Derivatives Spike by $14 Trillion in First Quarter to Six-Year High of $60 Trillion

By Pam Martens and Russ Martens: June 24, 2022 ~

Add JPMorgan Chase, the biggest bank in the United States with an unprecedented five criminal felony counts since 2014, to the growing list of debacles of which the Fed has lost control.

The Fed has its bank examiners pouring over the books of JPMorgan Chase on an ongoing basis, but somehow the bank’s dangerous book of derivatives has been allowed to spike by $14.42 trillion in the first quarter of this year, soaring from $45.84 trillion on December 31, 2021 to $60.26 trillion on March 31, 2022. That’s an increase of 24 percent in a three-month span. That information comes from page 18 of the newly-released report on derivatives in the banking system from the Office of the Comptroller of the Currency (OCC).

The Dodd-Frank Act of 2010 was supposed to stop the insanity of unfathomable amounts of risky derivatives being held at federally-insured banks. Under the so-called “push-out” rule in Dodd-Frank, derivatives were supposed to be moved out of the federally-insured bank to other parts of the bank holding company so that they could be wound down in a bankruptcy proceeding without endangering the federally-insured bank. Citigroup and its lobbyists succeeded in getting that provision repealed in a sneak maneuver in December 2014.

Then there was Dodd-Frank’s promise that all of these dangerous derivatives would become centrally-cleared in short order instead of being opaque over-the-counter contracts with bespoke (custom) terms that regulators and the public could not make heads or tails of. Well, that didn’t happen either. The current OCC report tells us that 71 percent of JPMorgan Chase’s equity derivatives are not centrally cleared; 100 percent of its precious metals contracts are not centrally cleared; and 96 percent of its foreign exchange derivative contracts are not centrally cleared.

The Fed and its fellow regulators deserve a grade of F for brazenly ignoring the intent of Congress when it passed the Dodd-Frank Act in 2010. Twelve years after its passage, dangerous derivatives are still not centrally cleared and instead of shrinking, their quantities and threat to financial stability are growing.

According to the official report from the Financial Crisis Inquiry Commission, which was statutorily mandated to investigate and report on the Wall Street financial collapse of 2008, derivatives played a central role in the crash. The report summarized its findings as follows:

“We conclude over-the-counter derivatives contributed significantly to this crisis. The enactment of legislation in 2000 to ban the regulation by both the federal and state governments of over-the-counter (OTC) derivatives was a key turning point in the march toward the financial crisis…without any oversight, OTC derivatives rapidly spiraled out of control and out of sight, growing to $673 trillion [globally] in notional amount. This report explains the uncontrolled leverage; lack of transparency, capital, and collateral requirements; speculation; interconnections among firms; and concentrations of risk in this market. OTC derivatives contributed to the crisis in three significant ways.

“First, one type of derivative—credit default swaps (CDS)—fueled the mortgage securitization pipeline. CDS were sold to investors to protect against the default or decline in value of mortgage-related securities backed by risky loans. Companies sold protection—to the tune of $79 billion, in AIG’s case—to investors in these newfangled mortgage securities, helping to launch and expand the market and, in turn, to further fuel the housing bubble.

“Second, CDS were essential to the creation of synthetic CDOs. These synthetic CDOs were merely bets on the performance of real mortgage-related securities. They amplified the losses from the collapse of the housing bubble by allowing multiple bets on the same securities and helped spread them throughout the financial system. Goldman Sachs alone packaged and sold $73 billion in synthetic CDOs from July 1, 2004, to May 31, 2007…

“Finally, when the housing bubble popped and crisis followed, derivatives were in the center of the storm. AIG, which had not been required to put aside capital reserves as a cushion for the protection it was selling, was bailed out when it could not meet its obligations. The government ultimately committed more than $180 billion because of concerns that AIG’s collapse would trigger cascading losses throughout the global financial system. In addition, the existence of millions of derivatives contracts of all types between systemically important financial institutions—unseen and unknown in this unregulated market—added to uncertainty and escalated panic, helping to precipitate government assistance to those institutions.”

As an example of just how lax regulators have been when it comes to reining in the threat of derivatives at the megabanks on Wall Street which, like JPMorgan Chase, own the largest federally-insured banks in the country, consider the research report that was released by the Office of Financial Research (OFR) on July 12, 2021. (OFR was also created under the Dodd-Frank Act to keep U.S. regulators informed about threats to financial stability.)

The OFR report is titled: “Counterparty Choice, Bank Interconnectedness, and Systemic Risk.” The researchers, Andrew Ellul and Dasol Kim, examined 18 different over-the-counter (OTC) derivative markets and concluded the following:

“Bank interconnectedness through the OTC derivative markets was identified as an important factor that contributed to the severity of the Great Financial Crisis… and remains an area of fragility of systemically important banks on which we have very limited understanding. The trading of OTC derivatives is notoriously concentrated in the largest banks, which are also the ones for which we have data. One important feature is the substantial counterparty risk that banks face, in our context the most important counterparty risk is that faced by banks trading with non- bank entities.”

Just how concentrated are these risky derivatives at the megabanks? The current report from the OCC tells us this:

“A total of 1,291 insured U.S. national and state commercial banks and savings associations reported trading and derivatives activities at the end of the first quarter of 2022. A small group of large financial institutions continues to dominate trading and derivatives activity in the U.S. commercial banking system. During the first quarter of 2022, four large commercial banks represented 89.0 percent of the total banking industry notional amounts [of derivatives] and 68.8 percent of industry net current credit exposure (NCCE).”

Notional means face amount of derivatives. As of March 31, 2022, the four federally-insured commercial banks that held 89 percent of all derivatives in the banking system were as follows: JPMorgan Chase with $60.26 trillion; Goldman Sachs Bank USA with $49.75 trillion; Citibank (part of Citigroup) with $45.74 trillion; and Bank of America NA with $22.48 trillion.

Yesterday, Fed Chairman Powell appeared before the House Financial Services Committee to deliver his monetary policy report. During the hearing, Powell was asked a question about systemic risks in the financial system by Congressman Jim Himes, a Democrat from Connecticut. The exchange went as follows:

Himes: “In my remaining minute I’m going to ask you a question I ask you a lot, Mr. Chairman. We’re obviously seeing pretty dramatic swings in the financial markets. Money is no longer free. We’re seeing that in the SPAC market, in the high yield market, the equities market, cryptocurrency. In my very short remaining time Mr. Chairman, what should we be focused on. What is concerning you with respect to systemic risk that may develop in the face of rising rates and rising inflation?”

Powell: “Basically, the financial markets have been functioning well and the banking system in particular is very strong, well-capitalized, has lots of liquidity, better understanding and management of its risks….”

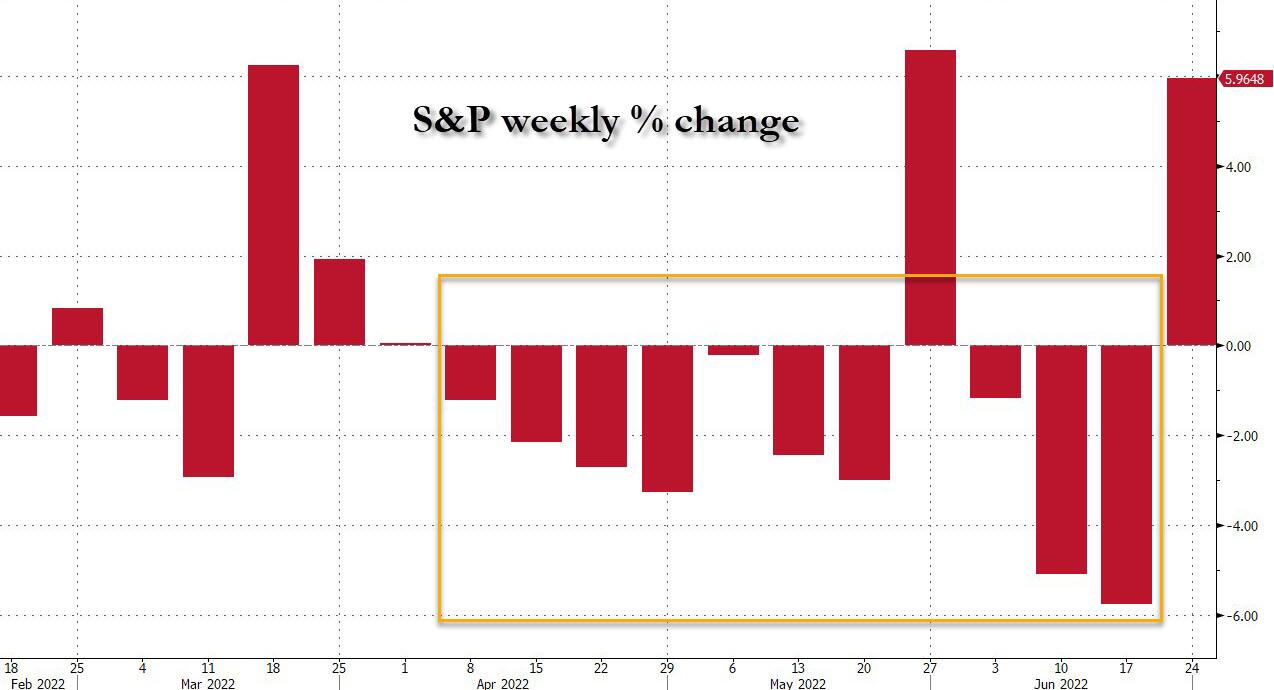

Consider that statement from Powell against this headline from May 27: “Dow Ends Biggest Losing Streak Since 1932 as Tech Prevails.” Not to put too fine a point on it, but 1932 was the early days of the Great Depression – the worst economic collapse in U.S. history.

Under Powell’s tenure at the helm of the Fed, the Fed has lost control of inflation, which is now hovering at a 40- year high. The Fed lost control of policing its own officials, triggering the biggest trading scandal in the Fed’s 109-year history. (Investigative findings regarding that scandal, by the way, have yet to be released by any federal body after nine months.) Instead of reining in the trading abuses on Wall Street, the Fed has encroached further into markets with its own trading activities. See our report: The New York Fed Has Quietly Staffed Up a Second Trading Floor Near the S&P 500 Futures Market in Chicago.

Powell also permitted the biggest, secret, bailout of the megabanks and their derivative counterparties beginning in September 2019 – months before there was any reported case of COVID-19 anywhere in the world. And, somehow, when the names of the banks that received these windfall repo loans from the Fed were finally released two years later, there was a blanket news blackout by mainstream media. Only Wall Street On Parade, a two-person investigative team, has documented this bailout, graphed the data, and named names. (See our archive of more than 100 articles on these Fed bailouts.)

Senator Elizabeth Warren is the only member of Congress with the courage to tell the simple truth to the American people about Fed Chairman Powell: He’s a “dangerous man.”

END

3. Chris Powell of GATA provides to us very important physical commentaries

The age of central bank credibility is now over.

A good piece from John Authers

(John Authers/GATA)

John Authers: The age of central bank credibility is over

Submitted by admin on Thu, 2022-06-23 11:54Section: Daily Dispatches

By John Authers

Bloomberg News

Thursday, June 23, 2022

Monetary regimes don’t fall often.

Half a century ago, in 1971, Richard Nixon ended the Age of Gold by formally eliminating the dollar’s peg to the precious metal. Since then, the dollar and other currencies have rested on fiat — they’re worth something because governments say they are.

You could call this the Age of Credibility. In place of gold, currency’s anchor is the trust in the central banks that issue them.

Now credibility appears to be at an end. With central banks desperately ripping up their playbooks to try to rein in inflation that has veered far beyond target, they’re admitting they have been wrong, and giving up on trying to steer the markets on their plans for the future.

That’s alarming, because the precedent of the 1970s is not encouraging. Oil briefly took over from gold as the anchor for currencies, and the world suffered through a period of protracted stagflation.

The new Age of Credibility arrived courtesy of Paul Volcker, who as chairman of the Federal Reserve raised rates repeatedly at the turn of the ’80s and managed to squeeze inflation out of the system.

For the four decades since, central bankers’ credibility has been the anchor. Provided everyone trusts central bankers to do what it takes to protect the buying power of the money, fiat currencies can work. …

… For the remainder of the commentary:

end

Your weekend reading material

Alasdair Macleod…

Alasdair Macleod: Russia is winning the financial war

Submitted by admin on Thu, 2022-06-23 11:48Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, June 23, 2022

Sanctions have backfired on those described by Vladimir Putin as the unfriendly nations. It is setting in train a series of events likely to undermine the whole Western financial system, as prices rise driving interest rates higher, and economic activity shrinks. These developments alone are leading to contracting bank credit, crashing stock markets, and sharply higher bond yields.

Last week, I wrote about the impact on the banking system and the likely consequences. Russia, China, and associated nations who depend upon them for trade and economic development are now moving to protect themselves from what is emerging as a full scale systemic and fiat currency crisis for the dollar and the entire Western financial system.

These developments are hastening the end of the petrodollar era and the dollar’s role as a reserve currency. A central Asian replacement is planned to be a new super-currency used for cross-border payments, based on an index of a basket of commodities and currencies of the participating nations. Including currencies is a mistake, but otherwise the proposition has merit.

This article explains why and how a properly constructed scheme would work. I demonstrate why it could act as a de facto gold standard.

Its designers intend this new trade currency to appeal to other important nations, such as Saudi Arabia, into using a commodity-linked currency for settling their trade payments, replacing the dying petrodollar. But its success could prove to be fatal for the fiat dollar and other Western currencies. With the demise of the dollar, the new super-currency can be expected to lead eventually to some national currencies adopting gold standards. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/russia-is-winning-the-financial-war

4.OTHER GOLD/SILVER COMMENTARIES

GATA Chairman Murphy interviewed by Andrew Maguire on ‘Live from the Vault’

9:14a ET Friday, June 24, 2022

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy is the guest in this week’s interview with London metals trader Andrew Maguire on Kinesis Money’s “Live from the Vault” program, discussing the longstanding manipulation of the gold and silver markets and GATA’s work exposing it. The interview is 40 minutes long and can be viewed at YouTube here:

https://www.youtube.com/watch? v=BxSwl_7GOrY

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

5.OTHER COMMODITIES //LITHIUM

END

COMMODITIES IN GENERAL/

END

6.CRYPTOCURRENCIES

7. GOLD/ TRADING

Your early currency/gold and silver pricing/Asian and European bourse movements/ and interest rate settings FRIDAY morning 7:30 AM

ONSHORE YUAN: CLOSED UP 6.6958

OFFSHORE YUAN: 6.6910

HANG SANG CLOSED UP 445.12 PTS OR 2.09%

2. Nikkei closed UP 320.72% OR 1.23%

3. Europe stocks ALL CLOSED ALL GREEN

USA dollar INDEX DOWN TO 104.09/Euro RISES TO 1.0535

3b Japan 10 YR bond yield: FALLS TO. +.215/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.03/JAPANESE FALLING APART WITH YEN FALTERING AS WELL AS LONG TERM YIELDS RISING BREAKING THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP -// OFF- SHORE UP

3f Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. EIGHTY percent of Japanese budget financed with debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +1.482%/Italian 10 Yr bond yield RISES to 3.58% /SPAIN 10 YR BOND YIELD FALLS TO 2.52%…

3i Greek 10 year bond yield RISES TO 3.80//

3j Gold at $1824.20 silver at: 20.88 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1/4 roubles/dollar; ROUBLE AT 53.21

3m oil into the 106 dollar handle for WTI and 111 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 135.03DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this morning 0.9569– as the Swiss Franc is still rising against most currencies. Euro vs SF 1.00080well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.111 UP 4 BASIS PTS

USA 30 YR BOND YIELD: 3.229 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 17.37

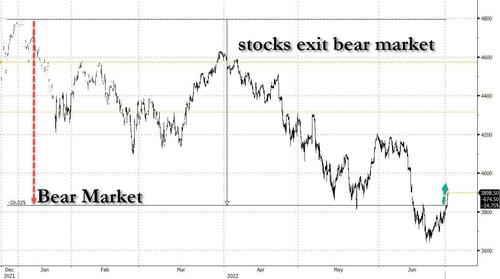

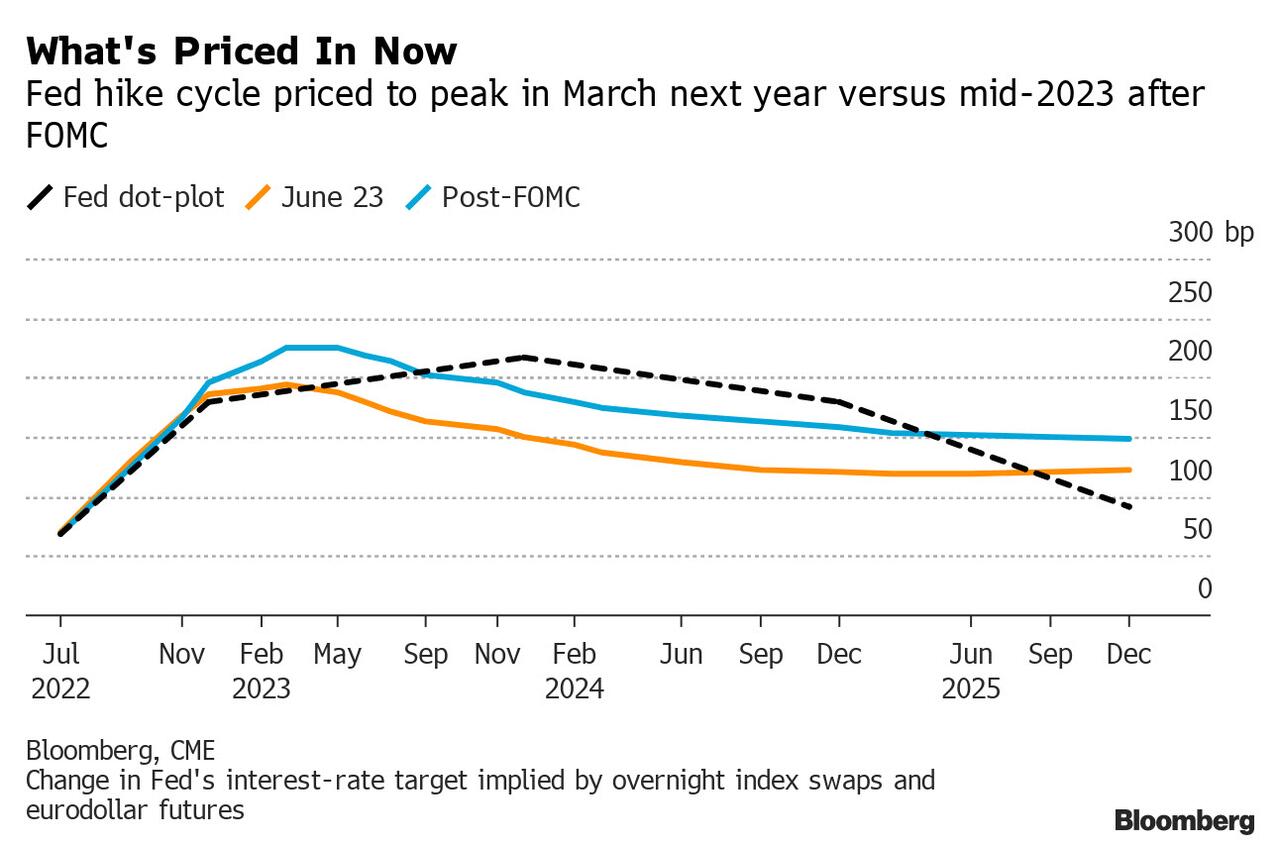

Futures Surge To Two Week High As Traders Eye End Of Fed’s Hiking Cycle

FRIDAY, JUN 24, 2022 – 11:53 AM

Futures are pointing to solid close to the week – now that a recession and earlier rate cuts are assured…

…. with a continuation of the rally which has pushed stocks to two week highs, with Tech continuing to lead while Chinese Tech is helping to fuel the global risk-on rally to end the week. Tech-heavy Nasdaq 100 futures added 1% while contracts on the S&P 500 gained 0.9%, trading near session highs at 3,833 after the main US stock gauge closed near session highs Thursday, adding more than 3% in three days. In Europe, the Stoxx Europe 600 rose 1.5%, with the benchmark set for a small bounce this week. 10-year Treasury yields rose to 3.13% after earlier sliding as low as 3.04%.

In premarket trading, software maker Zendesk Inc. soared over 50% on reports it’s close to reaching a deal to be acquired by a group of buyout firms led by Hellman & Friedman and Permira. Bank stocks were mostly higher as well after the latest stress test that results showed all 34 participating banks had passed (of course). In corporate news, Coinbase will launch its first crypto derivative product on Monday in the midst of the current crypto winter. US-listed Chinese stocks rise in premarket trading, on track for their best week since April as more market watchers turn positive on the group amid a gradual easing in Beijing’s crackdown on tech. Alibaba (BABA US) +3%, Nio (NIO US) +2.8%. Here are some other notable premarket movers:

- FedEx Corp. (FDX US) shares gained in premarket trading with analysts mostly welcoming its annual earnings forecast that was above expectations amid higher package prices and resolution on some operation issues related to labor shortage. Nevertheless, they still maintained caution amid cost pressures and macroeconomic uncertainty.

- US bank stocks may be volatile Friday after the Federal Reserve announced after the close of trading on Thursday that all banks had passed its annual stress test.

- Blackberry (BB CN) gained in postmarket trading after it reported an adjusted basic loss per share for the first quarter of 5c, in line with estimates.

- LendingTree (TREE US) shares dropped 10% in extended trading on Thursday, after the consumer finance company cut its second-quarter forecast for both revenue and adjusted Ebitda.

- Sarepta Therapeutics (SRPT US) shares may be under pressure after it announced that the FDA has placed a clinical hold on the company’s peptide-conjugated phosphorodiamidate morpholino oligomer to treat patients with Duchenne muscular dystrophy. That said, analysts believe this is mostly a hiccup and that the stock should get a lift once data from the company’s NT gene therapy is disclosed.

In his market wrap note, JPM’s Andrew Tyler asks “Does this rally have legs” and answers: “The next major catalyst is the June 30 PCE data. This current rally is seeing Tech and Defensive sectors as the largest outperformers. While some investors may play momentum, there seems to be a collective lack of conviction with many believing that this rally fizzles. Traders are looking for confirmation from a breakout above ~3900 resistant level.”

To be sure, investors are grappling with the question of what comes next if an economic downturn takes hold. One scenario – the bullish one – predicts cooling price pressures and thus scope for central banks to ease up on the pace of interest-rate hikes. In the other one, Jerome Powell hardened his resolve to cool inflation in testimony to lawmakers this week, after acknowledging that a recession may be the price to pay.

“In spite of the hawkish remarks from Fed officials, the growing worries that their hikes would trigger a recession actually meant that investors priced in a shallower pace of rate hikes over the coming 12-18 months,” Deutsche Bank AG strategists led by Jim Reid wrote in a note. “That had a knock-on impact on Treasuries.” We discussed this extensively last night. The rising probability of a peak in rates put the policy-sensitive US two-year yield on course for one of its biggest weekly drops since March 2020. Meanwhile, traders are starting to price out any Fed action on rates beyond the December meeting, scaling back the additional tightening they expect and flirting with the possibility of cuts by in 2023.

In Europe, equities traded well with the Stoxx rising 1.5% and the Euro Stoxx 50 1% higher back near Thursday’s highs. CAC 40 outperforms peers. Health care and media are the strongest sectors, autos and retail names lag. Here are some of the biggest European movers today:

- European health care stocks jump, outperforming the broader market. Societe Generale says the fundamentals of the European pharma sector are healthier than US peers. Roche rises as much as 3.4%, Novo Nordisk +3.2% and AstraZeneca +2.6% among the biggest contributors to the gain

- Ultra Electronics shares rise as much as 13% after a statement that the UK government is leaning toward approving Cobham’s planned takeover of the British defense-technology specialist.

- LVMH shares rise as much as 2.9% on Bernstein’s top luxury pick at a time of macroeconomic and geopolitical uncertanties, thanks in part to the French giant’s Dior mega-brand, which analyst Luca Solca says is one of the industry’s biggest success stories

- Telenet shares rise as much as 6.4%, with Barclays and New Street Research both noting that the stock is cheap and it may become more attractive for majority holder Liberty Global to consider buying the rest of the shares.

- Zalando shares sink as much as 18%, hitting the lowest since Jan. 2019. The online retailer warning on its sales and earnings outlook was not a total surprise, but the scale of the downgrade to its expectations was more significant than anticipated, analysts say. Fast fashion and online retailers decline in Europe following another warning in the sector, this time from Germany’s Zalando. HelloFresh slumps as much as -9.7%, Delivery Hero -6.0%, Deliveroo -2.7%.

- Fertilizer stocks sink in Europe with Morgan Stanley flagging the industry’s exposure to surging gas prices, gas supply uncertainties and related government measures in Europe to prevent shortages. K+S shares fall as much as 4.9%, Yara down as much as 4.8% and OCI down 3.9%

Earlier in the session, Asian stocks headed for a second day of gains as technology shares staged a comeback amid falling yields, with investors continuing to weigh the prospect of higher inflation and monetary tightening. The MSCI Asia Pacific Index rose as much as 1.2%, lifted by tech-heavy markets such as South Korea. A gauge of Asian tech stocks jumped, rallying from the lowest level since September 2020. A Chinese tech measure in Hong Kong advanced 4%. Consumer and health care names also contributed to Friday’s gains amid a global shift to defensive stocks. Asian equities headed for their first weekly gain in three, as the market took a breather from intense selling pressure fueled by fears that aggressive monetary tightening will push the US economy into a recession. Federal Reserve Chair Jerome Powell in testimony to lawmakers stressed his “unconditional” commitment to bringing down inflation.

Stocks have fared relatively better in Asia than in other regions as China’s move to dial back Covid restrictions supports market sentiment. Asia’s benchmark is down about 6% this month, compared with at least 8% declines in the S&P 500 Index and the Euro Stoxx 50. “The growth differentials are going to open up between China and the rest of the world,” Kinger Lau, chief China equity strategist at Goldman Sachs, said in a Bloomberg TV interview. Chinese equities “tend to do quite well going into the party congress, three to six months before that. Right now seems like we are in the sweet spot.”

Japanese stocks climbed as investors assessed hawkish comments by Fed Chair Jerome Powell on further interest rate hikes and a rally in Treasuries that sent yields lower, boosting tech shares. The Topix Index rose 0.8% to 1,866.72 as of market close Tokyo time, while the Nikkei advanced 1.2% to 26,491.97. Japan’s Mothers index rallied as much as 5.8%. Nidec Corp. contributed the most to the Topix Index gain, increasing 6.5%. Out of 2,170 shares in the index, 1,540 rose and 550 fell, while 80 were unchanged.

In Australia, the S&P/ASX 200 index completed a weekly gain of 1.6% to close at 6578.70, as technology shares staged a comeback amid falling yields. The tech benchmark had a weekly gain of 8.1%, the most since August. Nine of the 11 subgauges ended Friday higher, with only energy and mining stocks sliding after a gauge of commodities retreated. New Zealand’s market was closed for a public holiday

In FX, the Bloomberg dollar spot index dipped into the red, poised for its first weekly decline in a month as investors gauge whether aggressive Federal Reserve rate hikes would tip the US economy into a recession; the Bloomberg Dollar Spot Index fell 0.5% this week while the policy-sensitive US two-year yield is on course for its biggest weekly drop since March 2020. The Japanese yen was the only Group-of-10 currency to fare worse than the dollar, sliding back under 135. “The dollar is undermined by the weakness in PMI data and growing concerns that aggressive rate hikes will eventually cause growth slowdown,” said Akira Moroga, manager of currency products at Aozora Bank in Tokyo. “US yields are also stabilizing from recent sharp climb to weigh on the dollar,” he said. NOK and SEK are the strongest in G-10 FX, JPY is the weakest.

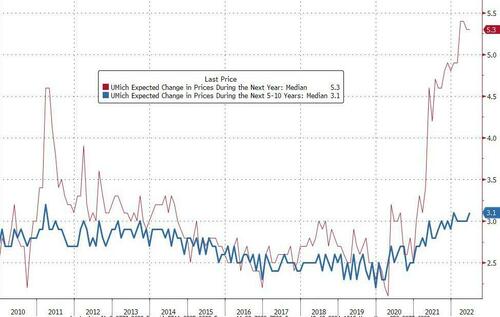

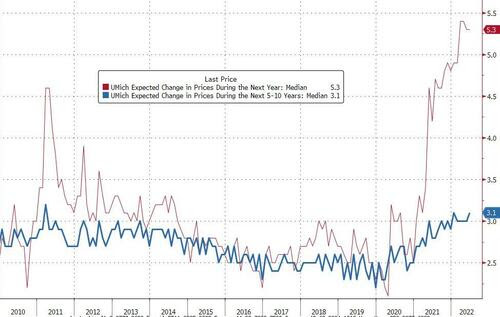

Rates erase initial gains, with Treasuries now slightly cheaper across the curve as US stock futures advance beyond Thursday’s highs, while core European bond gains fade and European stocks rally. US yields cheaper by 1bp-3bp across the curve and spreads within a basis point of Thursday’s close; 10-year higher by 1.5bp at 3.10%, bunds in the sector by an additional 3.5bp. Bunds futures complete a ~150 tick round trip, rallying near 149.00 before returning toward 147.50. Cash curves remain bear-steeper, long end bunds cheapen ~3bps having initially richened ~5bps. Cash USTs and gilts are comparatively quiet after following bunds price action in early trade. Italian bonds lag peers, widening the 10y BTP/Bund spread back above 200bps. Focal points of US session include early Bullard comments and University of Michigan inflation expectations, cited by Fed Chair Powell in latest policy decision.

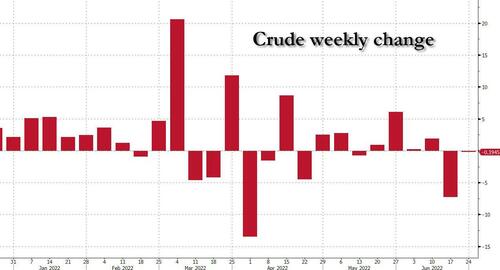

In commodities, crude futures advance, albeit holding within a relatively narrow range. West Texas Intermediate crude traded near $105 a barrel after retreating over the previous two sessions. The US benchmark has lost almost 4% this week, putting prices on course for their first monthly drop since November. Base metals complex is under pressure, LME tin drops over 12%, nickel down over 6%. Spot gold rises roughly $4 to trade near $1,827/oz. Bitcoin traded rangebound on either side of the 21,000 level.

Sliding raw materials prices have contributed to a moderation in market-based measures of inflation expectations. Oil headed for its first back-to-back weekly loss since early April amid a broader selloff in commodities markets.

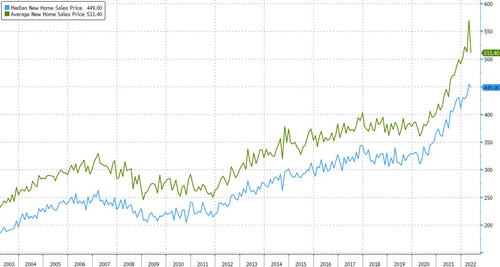

To the day ahead now, and data releases include Germany’s Ifo business climate indicator for June, Italian consumer confidence for June, and UK retail sales for May. Over in the US, there’s also the University of Michigan’s final consumer sentiment index for June, and new home sales for May. From central banks, we’ll hear from the ECB’s Centeno and de Cos, the Fed’s Bullard and Daly, the BoE’s Pill and Haskel, and BoJ Deputy Governor Amamiya.

Market snapshot

- S&P 500 futures up 0.7% to 3,826.75

- STOXX Europe 600 up 1.1% to 406.65

- German 10Y yield little changed at 1.40%

- Euro little changed at $1.0525

- Brent Futures up 0.4% to $110.51/bbl

- Gold spot up 0.2% to $1,826.53

- MXAP up 1.1% to 159.08

- MXAPJ up 1.3% to 527.68

- Nikkei up 1.2% to 26,491.97

- Topix up 0.8% to 1,866.72

- Hang Seng Index up 2.1% to 21,719.06

- Shanghai Composite up 0.9% to 3,349.75

- Sensex up 0.7% to 52,652.22

- Australia S&P/ASX 200 up 0.8% to 6,578.70

- Kospi up 2.3% to 2,366.60

- U.S. Dollar Index little changed at 104.35

Top Overnight News from Bloomberg

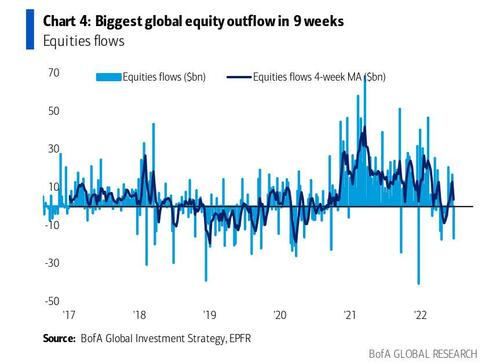

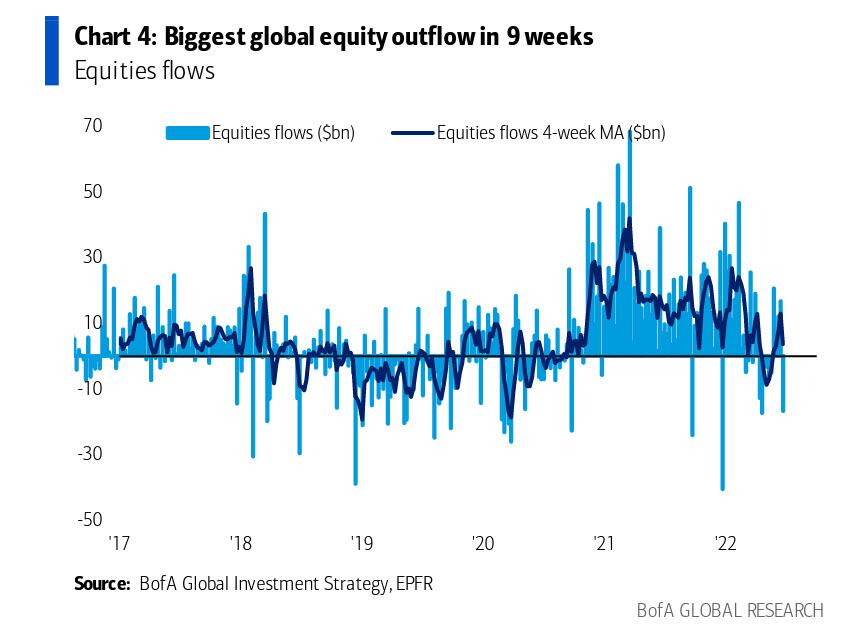

- Global equity funds saw their biggest outflows in nine weeks as investors piled into cash amid fears that the US economy could be headed for a recession.

- UK consumers are starting to crumple in the face of soaring prices, according a series of reports that paint a grim picture of the nation’s cost of living crisis.

- Germany’s economy minister said he can’t be sure that Russia will resume shipments through a key gas pipeline following planned maintenance next month, raising the prospect of a fresh surge in prices and rationing this winter.

A more detailed look at global markets from Newsquawk

Asia-Pac stocks ultimately followed suit to the gains on Wall St where a decline in yields and lower commodity prices helped the major indices claw back from the opening losses which were triggered by disappointing PMI data. ASX 200 was positive with tech stocks encouraged by US counterparts which benefitted from the lower yield environment although gains in the index were capped by weakness in the commodity-related sectors after the recent pressure in energy and metal prices. Nikkei 225 found early momentum alongside currency flows and held on to gains despite the JPY reversal. Hang Seng and Shanghai Comp. were positive after officials recently suggested ample policy space to sustain a steady economic performance and with the PBoC upping its liquidity efforts.

Top Asian News

- PBoC injected CNY 60bln via 7-day reverse repos with the rate at 2.10% for a CNY 50bln net daily injection, according to Reuters.

- Xi Trip to Hong Kong in Doubt After Top Officials Get Covid

- Hong Kong’s Jumbo Mystery Deepens as Restaurant May Be Afloat

- Gold Set for Weekly Drop on Powell’s Unconditional Inflation Vow

- Iron Ore Poised to End Wild Week Down as Steel Inventories Rise

- Hedge Funds Buy Dollar-Yen Downside Options on Recession Risks

European bourses have coat-tailed on the positivity seen on Wall Street yesterday and across APAC overnight, with European indices firmer to varying degrees. Sectors overall project a modest defensive bias as Healthcare, Media, Consumer Products, and Food & Beverages reside among the winners, although Tech is also buoyed by the pullback in bond yields. Europe’s largest online retailer Zalando (-12%) slumped following a profit warning, and in turn dragged the European Retail sector to the lowest level since March 2020. Stateside, US equity futures are firmer across the board – with the NQ narrowly leading the pack – participants also flagged the ES overcoming resistance at 3,800.

Top European News

- UK PM Johnson’s Conservatives lost the parliamentary seat in the Wakefield by-election to the Labour Party and lost the by-election in Tiverton and Honiton to the Liberal Democrats, according to Reuters. Subsequently, PM Johnson has been warned to “watch out for a coup”, according to reporting in The Telegraph. Furthermore, Conservative Party Chairman Dowden has resigned following the by-elections.

- 1922 Committee treasurer Sir Geoffrey Clifton-Brown hints that Tory leadership rules could be changed to allow rebels another shot at the PM, according to Mail’s Grove.

- Boris Johnson’s Party Chair Quits After Double Election Blow

- Zurich Insurance Sells Legacy German Life Portfolio to Viridium

- Ukraine Latest: Troops to Leave Key Eastern City as Russia Gains

- Airlines 2Q Seen Profitable for Most, Deterioration in 2023: DB

FX

- Kiwi elevated amidst favourable crosswinds on NZ market holiday – Nzd/Usd probes 0.6300 as Aud/Nzd retreats towards 1.0950.

- Euro encouraged by elements of German Ifo survey and Pound shrugs off mixed UK consumption data, all time low consumer sentiment and more pain for PM Johnson on risk factors and gravitating Greenback – Eur/Usd firm on 1.0500 handle, Cable tests 1.2300 and DXY close to base of 104.120-510 range.

- Aussie, Loonie and Franc all bounce within ranges as Buck backs off, but Yen continues to encounter resistance after decent retracement – Aud/Usd back over 0.6900, Usd/Cad fades from pop above 1.3000 and Usd/Chf reverses through 0.9600 pivot.

- Scandi Crowns claw back lost ground, Yuan underpinned by PBoC liquidity injection and Peso by hawkish Banxico guidance to supplement 75 bp hike – Eur/Sek sub-10.7000, Eur/Nok near 10.4500, Usd/Cnh under 6.7000 and Usd/Mxn beneath 20.0000.

Fixed Income

- Debt recoils after stretching recovery limits further – Bunds top out at 149.00, Gilts at 114.55 and 10 year T-note 118-00

- Trading volumes pick-up on the way back down towards or to intraday lows of 147.21, 113.54 and 117-10+, as risk appetite steadily improves and focus turns to pm agenda

Commodities

- WTI and Brent August futures are extending their modest gains in recent trade despite a lack of news flow.

- EIA said a status update on the weekly DOE oil inventories report will be provided on Monday.